INDIAN ECONOMY: A STABLE, LARGE BUT SLOW.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INDIAN ECONOMY: A STABLE, LARGE BUT SLOW.

MALAVIYA NATIONAL INSTITUTE OF TECHNOLOGY JAIPUR

IMPACT OF MONETARY & BANKING REFORMS POST LIBERALSIATION

2014-2015

Presented by

Aakash Bhatia 2011UCH4002

Gagan Gothwal 2011UCH1023

Kuldeep Singh Bhati 2011UCH1759

Mayank Mehta 2011UCH1590

OVERVIEW

MONETARY POLICY & ITS OBJECTIVE

TRADE OFF IN MONETARY GOALS

EVOLUTION OF MONETARY POLICY

INSTRUMENTS OF MONETARY POLICY IN INDIA

MONETARY REFORMS

BANKING REFORMS

OUTCOMES OF THESE REFORMS

DEMERITS

MONETARY POLICY & ITS OBJECTIVE

Monetary policy is defined as comprising of such measures which lead to

influencing the cost, volume and availability of money and credit so as to achieve

certain set objectives.

The main objectives or goals of monetary policy are:-

(1) Price stability

(2) Economic growth

(3) Full employment and

(4) Maintenance of balance of payments equilibrium

WHY THESE OBJECTIVES ?

Price Stability

Fluctuations in prices bring about uncertainty and instability in the

economy.

Price stability keeps the value of money stable, eliminates cyclical fluctuations,

brings economic stability, helps in reducing inequalities of income and wealth,

secures social justice and promotes economic welfare.

Innovations may reduce the cost of production but a policy of stable prices may

bring larger profits to producers at the cost of consumers and wage earners.

Economic Growth

Economic growth implies raising the standard of living of the people, and

reducing inequalities of income distribution.

Full Employment

Full employment is a situation in which everybody who wants to work gets work.

Full employment can be achieved in an economy by following an expansionary

monetary policy.

Balance of payment’s Equilibrium

A balance of payments deficit reflects excessive money supply in the economy. As

a result, people exchange their excess money holdings for foreign goods and

securities.

TRADE OFF IN MONETARY GOALS

Full Employment and Economic Growth

Economic growth and Price stability

Full employment and price stability

Full employment and Balance of payments

EVOLUTION OF MONETARY POLICY

The evolution of monetary policy framework in India can be seen in phases.

In the formative years during 1935–1950, the focus of monetary policy was to

regulate the supply of and demand for credit in the economy through the bank

rate, reserve requirements and open market operations (OMO).

In the development phase during 1951–1970, monetary policy was geared towards

supporting plan financing. This led to introduction of several quantitative control

measures to contain consequent inflationary pressures. While ensuring credit to

preferred sectors, the bank rate was often used as a monetary policy instrument.

During 1971–90, the focus of monetary policy was on credit planning. Both the

statutory liquidity ratio (SLR) and the cash reserve ratio (CRR) were used to

balance government financing and the attendant inflationary pressure.

INSTRUMENTS OF MONETARY POLICY IN

INDIA

QUANTITATIVE TOOLS

BANK RATE

The interest rate at which a nation's central bank lends money to domestic

banks.

Often these loans are very short in duration.

Bank Rate serves as a reference rate for other rates in the financial markets.

From 2004-10, it was kept constant at 6 per cent.

Bank Rate is 8.75% which is in effect from 15 January 2015.

CASH RESERVE RATIO (CRR)

Cash Reserve Ratio (CRR) is a specified minimum fraction of the total

deposits of customers, which commercial banks have to hold as reserves

either in cash or as deposits with the central bank.

CRR is set according to the guidelines of the central bank of a country.

The Narasimham Committee in its report submitted in November 1991, was

of the view that a high cash Reserve Ratio (CRR) adversely affects the bank

profitability.

Thus, government decided to reduce the CRR over a four year period to a

level below 10 per cent.

As per the policy announced on April 24, 2010, the CRR in India was 6.00 per

cent.

Currently it is at 4%.

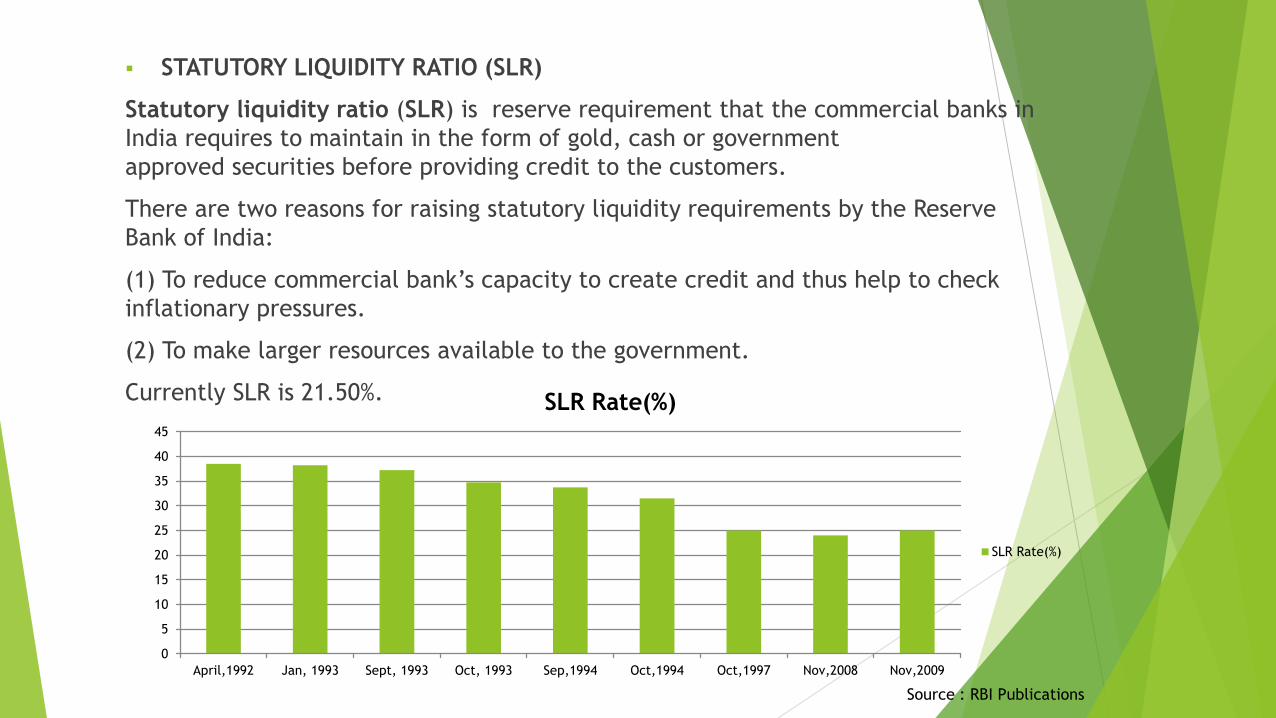

STATUTORY LIQUIDITY RATIO (SLR)

Statutory liquidity ratio (SLR) is reserve requirement that the commercial banks in

India requires to maintain in the form of gold, cash or government

approved securities before providing credit to the customers.

There are two reasons for raising statutory liquidity requirements by the Reserve

Bank of India:

(1) To reduce commercial bank’s capacity to create credit and thus help to check

inflationary pressures.

(2) To make larger resources available to the government.

Currently SLR is 21.50%.

0

5

10

15

20

25

30

35

40

45

April,1992 Jan, 1993 Sept, 1993 Oct, 1993 Sep,1994 Oct,1994 Oct,1997 Nov,2008 Nov,2009

SLR Rate(%)

SLR Rate(%)

Source : RBI Publications

OPEN MARKET OPERATIONS

The open market operation policy is that policy by which the central bank contracts

or expands the credit by sale or purchase of securities in the open market.

Open market operations is an effective instrument for liquidity management in

economy.

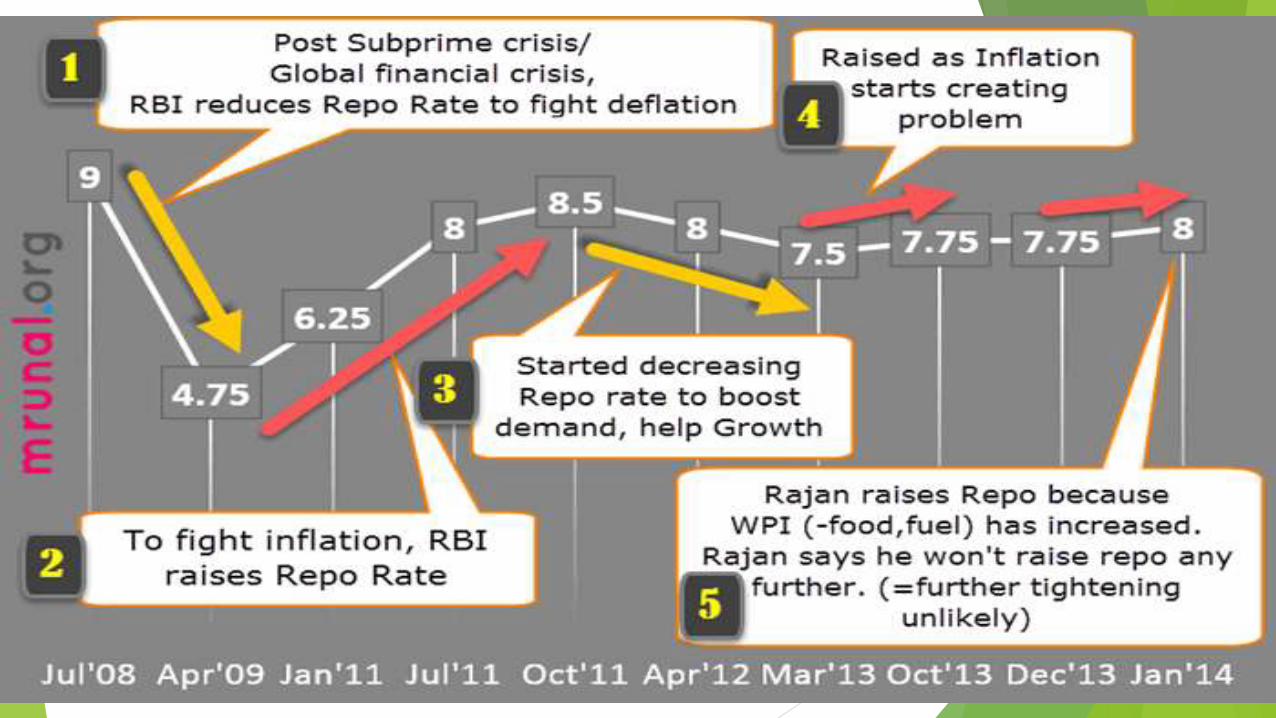

REPO RATE

Bank sells the security to RBI to raise money. When banks sell security , banks

promise to buy back the same security from RBI at a predetermined date with an

interest at the rate of REPO .

Currently Repo rate is 7.75%.

0

2

4

6

8

10

12

14

16

18

Repo Rate (%)

Repo Rate (%)

Source : RBI Publications

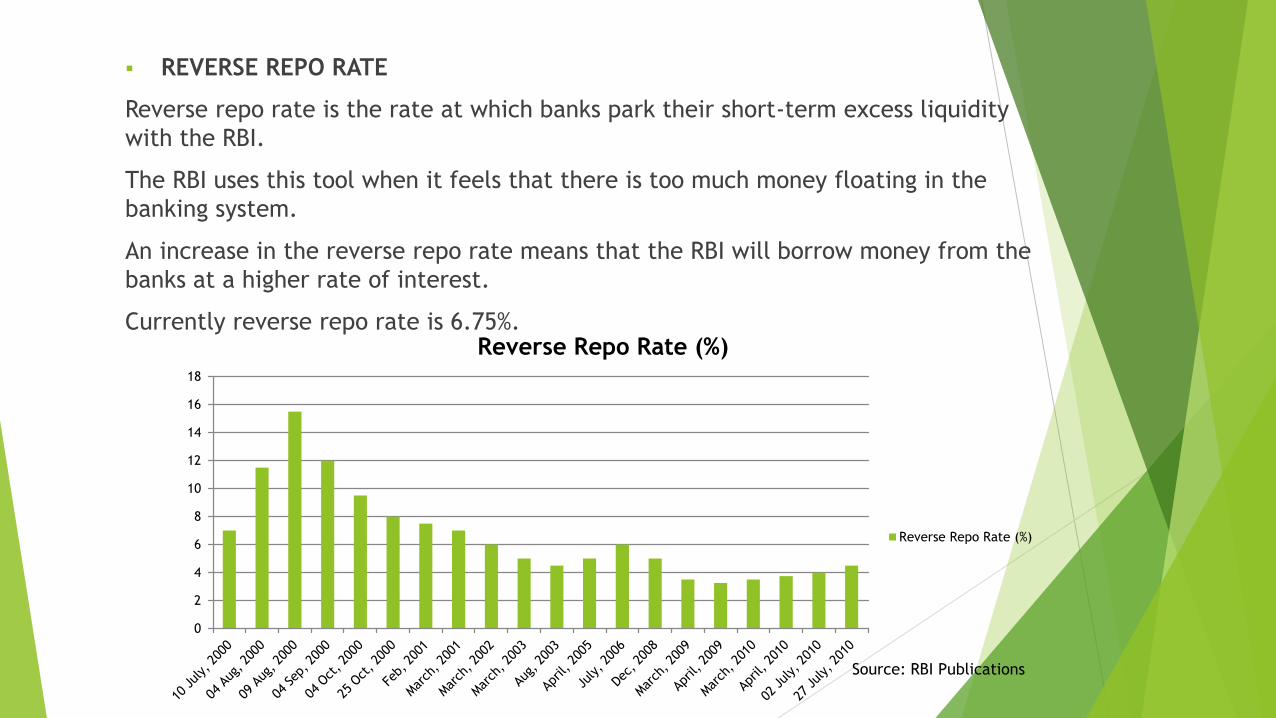

REVERSE REPO RATE

Reverse repo rate is the rate at which banks park their short-term excess liquidity

with the RBI.

The RBI uses this tool when it feels that there is too much money floating in the

banking system.

An increase in the reverse repo rate means that the RBI will borrow money from the

banks at a higher rate of interest.

Currently reverse repo rate is 6.75%.

0

2

4

6

8

10

12

14

16

18

Reverse Repo Rate (%)

Reverse Repo Rate (%)

Source: RBI Publications

QUALITATIVE TOOLS

While the quantitative tools controls relate to the total volume of credit (changing

High-powered money) and the cost of credit, qualitative tools operate on the

distribution of total credit.

Measures can be used to encourage greater channelling of credit into particular

sectors, as is being done in India in favour of designated priority sectors, is the

positive aspect.

Varying Margin Requirement

It is an important qualitative method of credit control. This method was initially

used in America in 1929. The banks keep a certain margin while lending money

against securities.

Banks do not advance money to the full value of the security pledged for the loan. .

Regulation of Consumer Credit

It helps to regulate the terms and conditions under which the credit repayable in

instalments could be extended to the consumers for purchasing the durable goods

The central bank can control the consumer credit

1. by changing the amount that can be borrowed for the purchase of the consumer

durables and

2. by changing the maximum period over which the instalments can be extended.

Rationing of Credit

The central bank can also adopt the rationing of credit as a selective measure.

Under this method, the central bank can fix a limit for the credit facilities available

to commercial bank.

This is to control and regulate the purpose for which the credit is granted by the

banks.

Direct Action

Direct action refers to direct dealings with the individual bank which adopt policies

against the policies of the central bank.

Under this system,

(1) the central bank may refuse to rediscount the bills of exchange of the

commercial banks .

(2) it may charge a penal rate of interest over and above the bank rate and

(3) the central bank may refuse to grant more credit to the particular banks.

Moral Persuasion

Moral suasion means advising, requesting and persuading the commercial banks to

co-operate with the central bank in implementing its general monetary policy.

MONETARY REFORMS

Reduced CRR and SLR

reduced from the earlier high level of 15% plus incremental CRR of 10.5% to current 4% level.

The SLR is also reduced from early 30.5% to current minimum of 23% level.

This has left more loanable funds with commercial banks.

Increased Micro Finance

The RBI has focused more on the SHG (self-help group) to strengthen the Rural Finance.

Micro Finance Institutions (MFIs) are kept under priority sector lending, for instance Urban Co-operative banks. It comprises small and marginal farmers, Agriculture and Non-Agriculture Labour, Artisans and Rural sections of the society.

Now, still only 30% of the target population has been benefited.

Fixing prudential norms

For professionalism in its operations, the RBI fixed prudential norms for commercial banks.

It includes recognition of income sources, classification of assets, provisions for bad-debts, maintaining international standards in accounting practices etc.

It helped banks in reducing and re-structuring non-performing assets (NPAS).

Introduction of CRAR

started in 1992.

Almost all the banks in India has reached the CAR above the statutory level of 9%.

Diversification of banking

banks have started new services and new products.

Some bank have established subsidiaries in Merchant Banking, mutual funds,

insurance, venture capital etc.

New generation banks

Bank such as ICICI Bank, UTI Bank have given a big challenge to the Public Sector

Banks leading to a greater degree of competition.

Operational autonomy

satisfies the CAR then freedom in opening new branches.

Improved profitability and efficiency

happened due to reduced, non-performing loans, use of technology, use of

computers and some other relevant measures adopted by the govt.

Changes in accordance to the external reforms

comprises various controls on imports, reduce tariffs, etc.

The Monetary Policy has shown the impact of liberal inflow of the foreign capital

and its implication on domestic money supply

BANKING REFORMS

Banking Reforms in India: Phase I

Lowering SLR And CRR

Prudential Norms

Capital Adequacy Norms (CAN): In April 1992 RBI fixed CAN at 8%.

Deregulation Of Interest Rates

Recovery Of Debts

Competition From New Private Sector Banks

Phasing Out Of Directed Credit

Access To Capital Market

Freedom Of Operation

Local Area banks (LABs)

Supervision Of Commercial Banks

Banking Reforms in India: Phase II in 1998

New areas for bank financing have been opened

New Instruments :- For greater flexibility and better risk management

Strengthening Technology

Increase Inflow Of Credit

Increase in FDI Limit: From 49% to 74%

Adoption Of Global Standards

Mergers And Amalgamation

Guidelines For Anti-Money Laundering

Base Rate System Of Interest Rates

Managerial Autonomy

OUTCOMES OF THESE REFORMS

Business per Employee (Rs. in Lakhs)

Profit per Employee (Rs. In Lakh)Source : New Century Publications, 2008

Source : New Century Publications, 2008

0

2

4

6

8

10

12

14

16

18

20

Lending Rate after 1991 (%)

Source: RBI Publications

0

2

4

6

8

10

12

14

Deposit Rate(%) after 1991

Source: RBI Publications

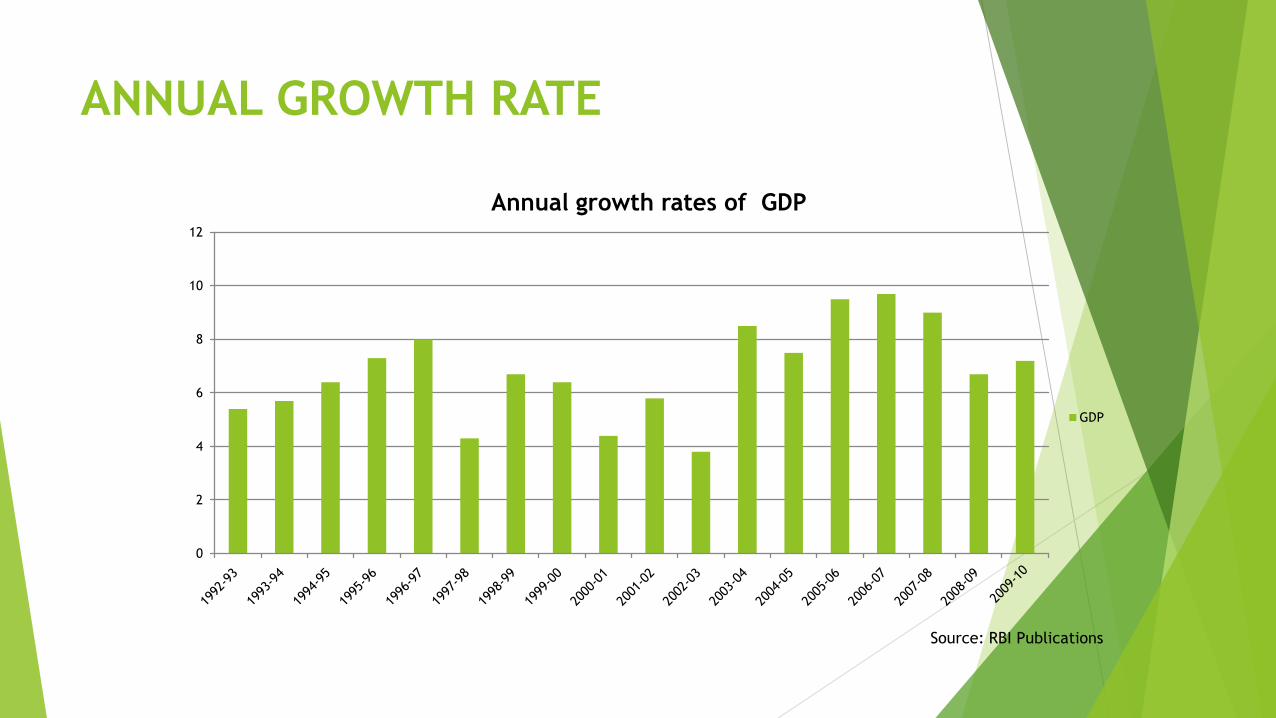

ANNUAL GROWTH RATE

0

2

4

6

8

10

12

Annual growth rates of GDP

GDP

Source: RBI Publications

SECTORIAL GDP

Agriculture, 31.4

Industry, 19.8

Service, 48.8

1990-01

Agriculture24%

Industry20%

Service56%

2000-01

Agriculture, 14.4

Industry, 27.9

Service, 57.7

2010-11

Agriculture, 12

Industry, 28.2Service,

59.8

2014-15forecast

Source: RBI Publications

FISCAL DEFICIT

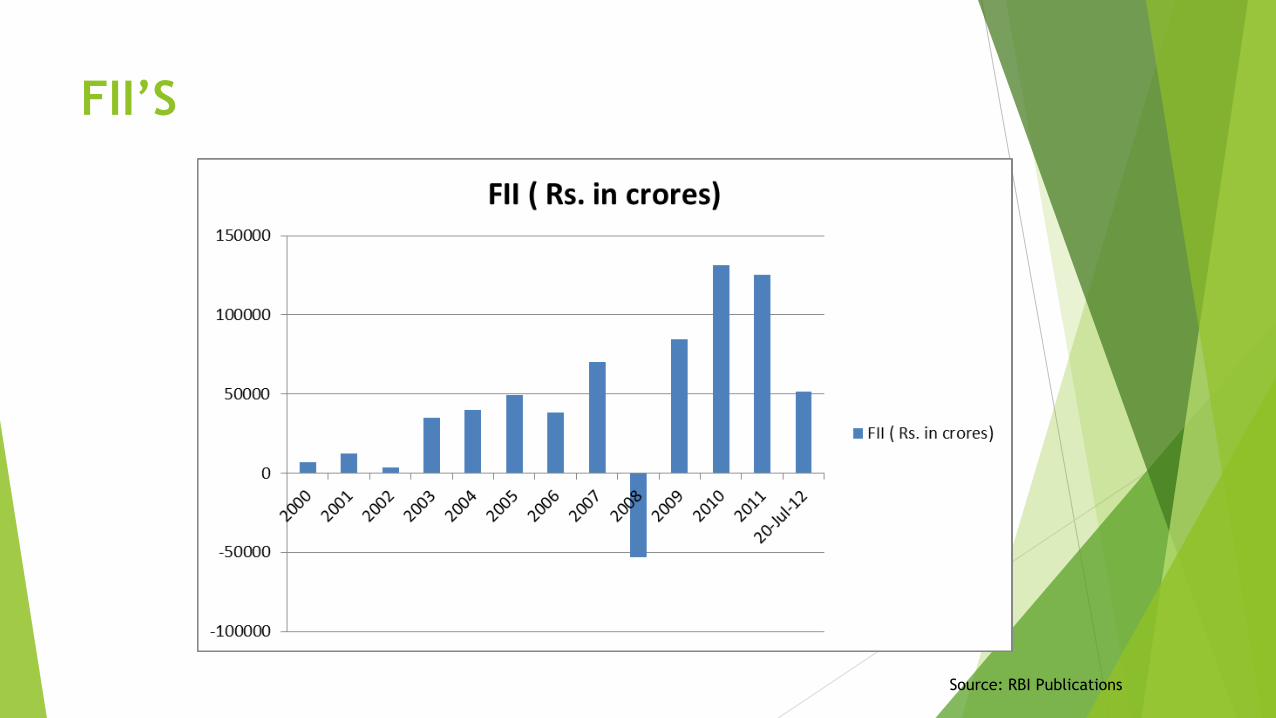

FII’S

Source: RBI Publications

DEMERITS

Monetary Policy fails to tackle Budgetary Deficit-The higher level of budget deficit has made Monetary Policy ineffective. The automatic monetization of deficit has let to high Monetary expansion.

The coverage area of Monetary Policy is limited-Monetary Policy covers only commercial banking sector. Other non-banking institutions remains untouched. It limits the effectiveness of the Monetary Policy in India.

Money market is not organized-There is a huge size of money market in our country. It does not come under the control of the RBI. Thus any tools of the Monetary Policy does not affect the unorganized money market making Monetary Policy less affective.

Predominance of cash transaction- In India still there is huge dominance of the cash in total money supply. It is one of the main obstacles in the effective implementation of the Monetary Policy. Because monetary policy operates on the bank credit rather on cash.

Increase volatility– As the Monetary has adopted changes in accordance to the changes in the external sector in India, It could lead to high amount of the volatility.

Related Documents