Major Deal Elements Venture Capital Term Sheets Analysis Daniel J. Piedra J.D., expected ‘16 University of San Diego School of Law

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Major Deal Elements Venture Capital Term Sheets Analysis

Daniel J. PiedraJ.D., expected ‘16University of San Diego School of Law

Major Deal Elements

1. A Preferred Return

2. Protection of Valuation and Position re: Future Money

3. Management of the Investment

4. Exit Strategies

Preferred Return❖ Perception of the VC Investor:

❖ When the Investor writes the check, he has done almost everything he promised

❖ The entrepreneur has done nothing yet

❖ Result: The VC wants its money to be paid back before the Entrepreneur gets his/her return.

❖ Instrument: CONVERTIBLE PREFERRED STOCK

Preferred Return❖ Dividends:

❖ Paid to Preferred First

❖ Cumulative or Accruing

❖ Liquidation Preference ❖ “Straight” Liquidation Preference: The Preferred receives its original

investment amount plus accrued dividends (if any) before Common receives anything.

❖ Participating (“Double Dip”) Preferred: The Preferred first gets its liquidation preference and then shares any remaining proceeds with Common. Increasingly subject to a cap of 3X or 4X (including preference).

Preferred Return: Liquidation Events

❖ Liquidation, dissolution, sale of assets

❖ Money comes into corporation

❖ Money paid out to stockholders to redeem stock

❖ “Deemed liquidation”— merger or other positive event

❖ Consideration may be stock or cash

❖ Consideration may go directly to stockholders

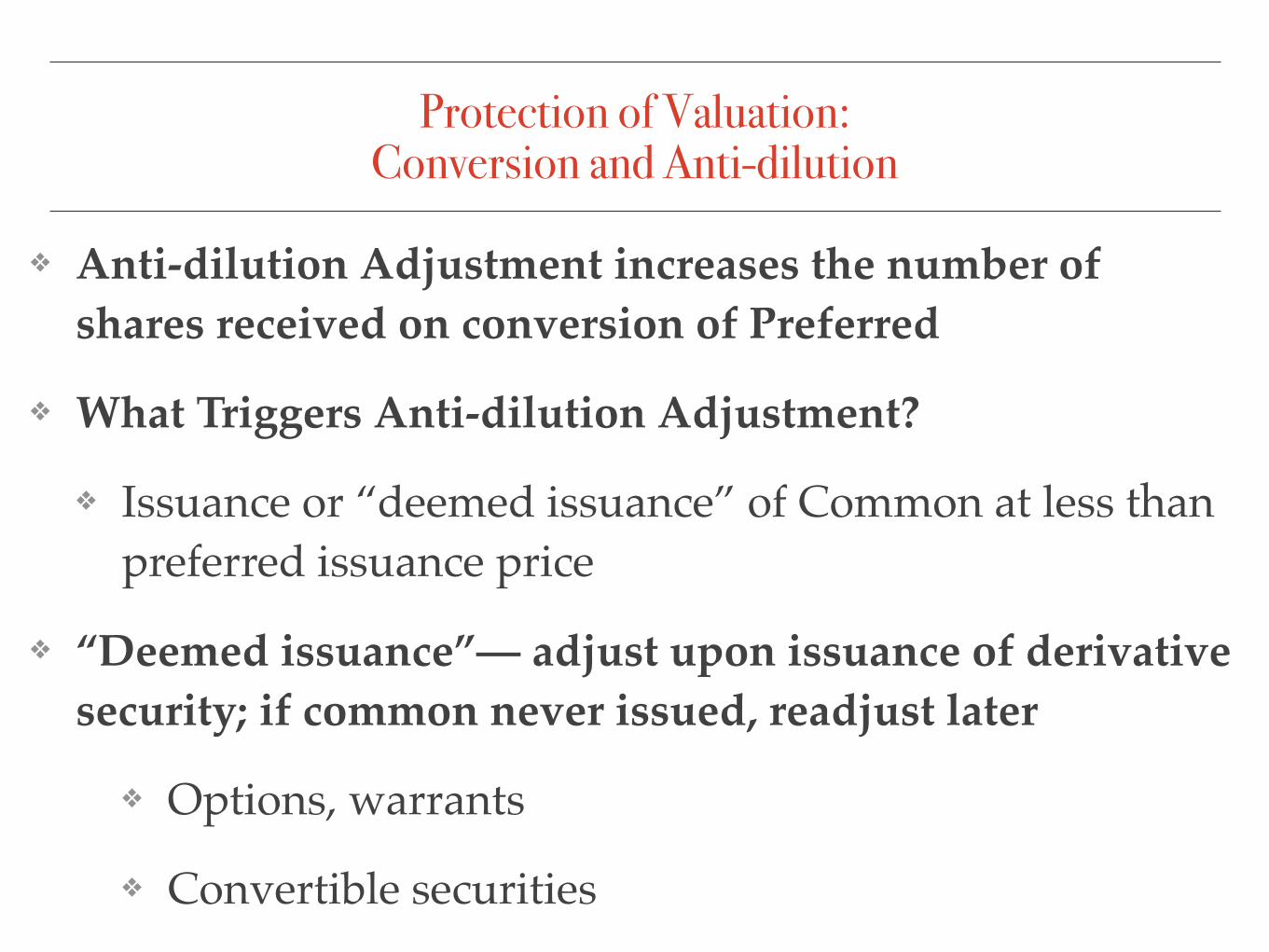

Protection of Valuation:Conversion and Anti-dilution

❖ Anti-dilution Adjustment increases the number of shares received on conversion of Preferred

❖ What Triggers Anti-dilution Adjustment?

❖ Issuance or “deemed issuance” of Common at less than preferred issuance price

❖ “Deemed issuance”— adjust upon issuance of derivative security; if common never issued, readjust later

❖ Options, warrants

❖ Convertible securities

Protection of Valuation:Conversion and Anti-dilution

❖ Conversion Events: When Does Preferred Convert Into Common?

❖ Voluntary

❖ Forced: often some % of Preferred can force conversion of all

❖ Automatic--upon “Qualified IPO”

❖ Minimum total offering; minimum share price (usually 3 to 5 times initial purchase price)

❖ Conversion Ratio--initially 1:1

❖ Adjustments--stock splits, etc; price anti-dilution

❖ Exceptions--option pool, conversion of preferred, outstanding warrants, other existing conditions, other special exceptions

Valuation❖ Conversion Ratio:

❖ Original Purchase Price (OPP)/ Conversion Price (CP)

❖ Initially OPP = CP, so Conversion Ratio = 1:1

❖ “Full ratchet”: CP reset to equal price at which diluting security is sold

❖ “Weighted average”: CP new = CP old x R

❖ Where R = (N + M/CP old)/(N+S)

❖ N = old shares outstanding (fully diluted)

❖ S = new shares to be issued

❖ M = new money ($)

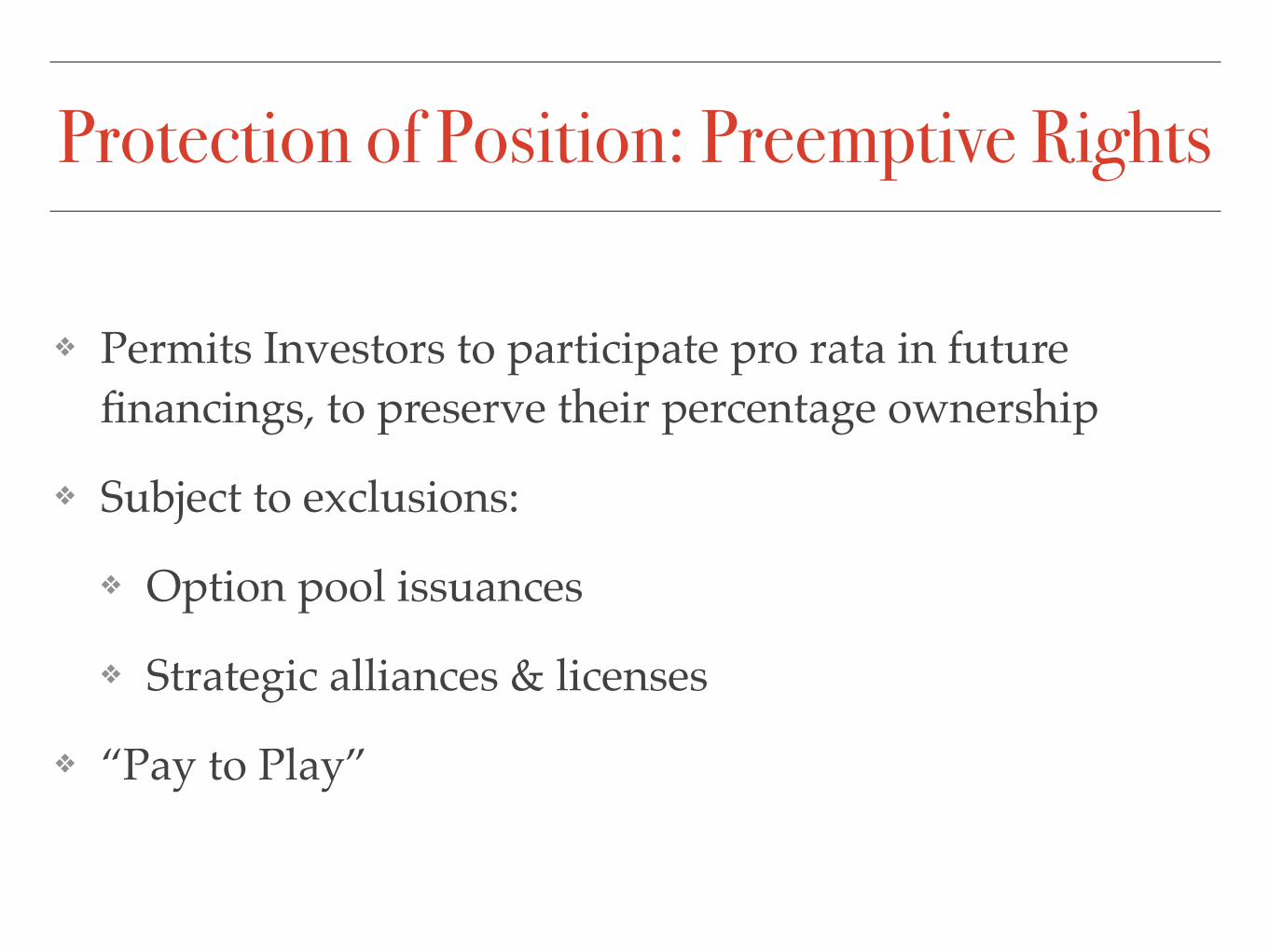

Protection of Position: Preemptive Rights

❖ Permits Investors to participate pro rata in future financings, to preserve their percentage ownership

❖ Subject to exclusions:

❖ Option pool issuances

❖ Strategic alliances & licenses

❖ “Pay to Play”

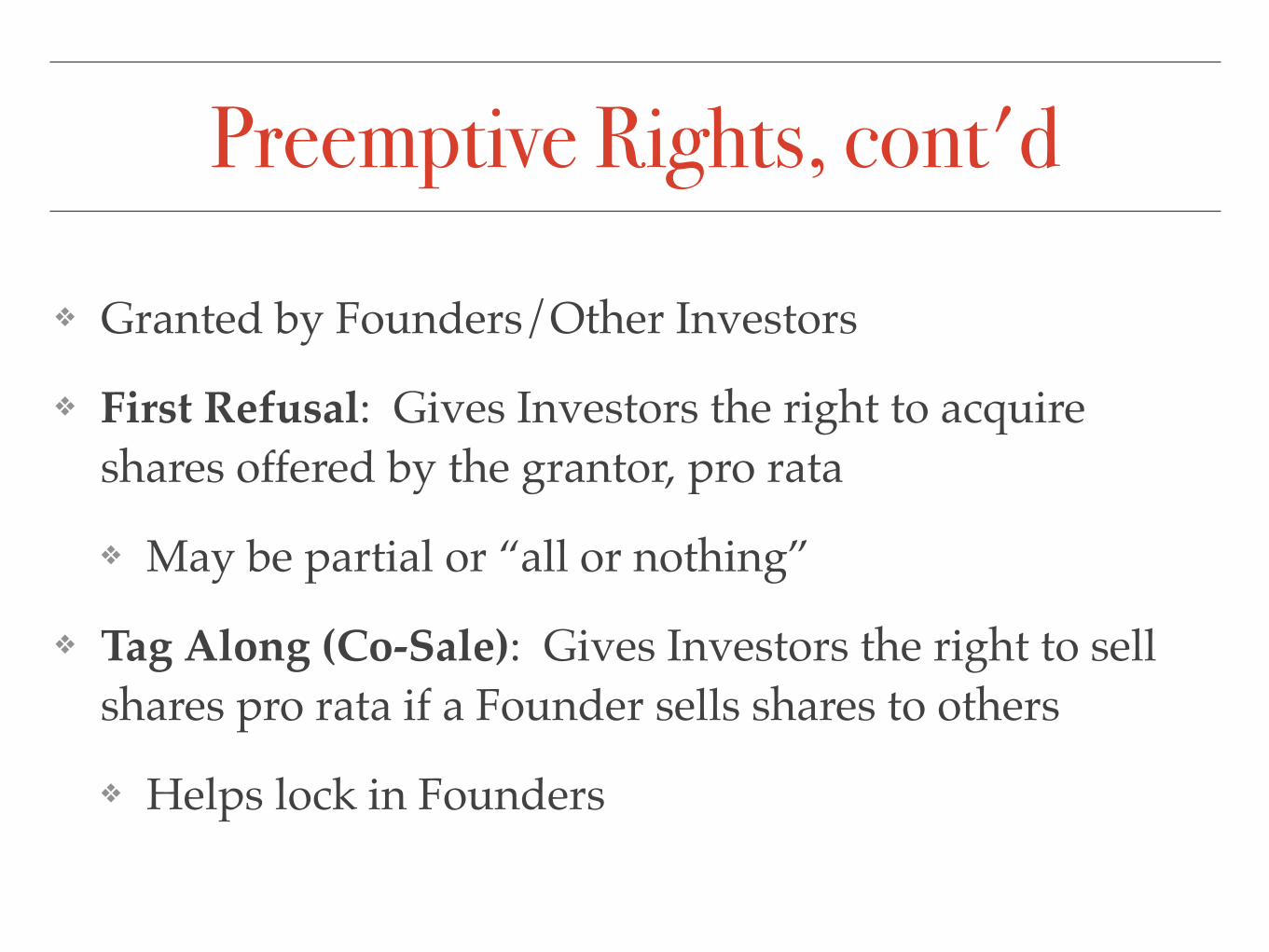

Preemptive Rights, cont'd

❖ Granted by Founders/Other Investors

❖ First Refusal: Gives Investors the right to acquire shares offered by the grantor, pro rata

❖ May be partial or “all or nothing”

❖ Tag Along (Co-Sale): Gives Investors the right to sell shares pro rata if a Founder sells shares to others

❖ Helps lock in Founders

Management of the Investment❖ Board Seat(s)

❖ Importance of the “Independent Director(s)”

❖ Business Approvals ❖ Capital Expenditures, etc.

❖ Approval of Annual Budget and Operating Plans

❖ Information Rights ❖ Reports, financial statements — NDA advised

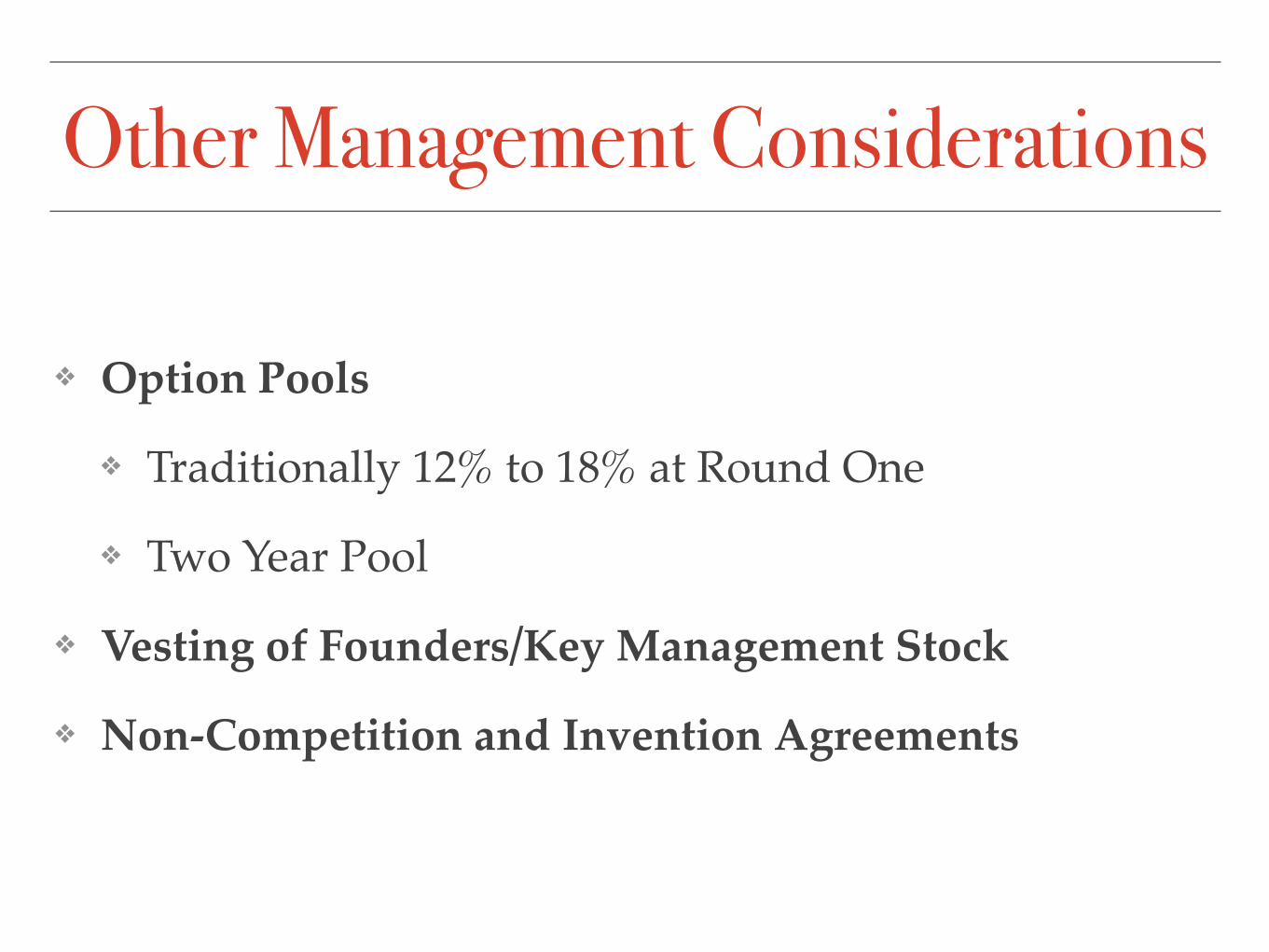

Other Management Considerations

❖ Option Pools

❖ Traditionally 12% to 18% at Round One

❖ Two Year Pool

❖ Vesting of Founders/Key Management Stock

❖ Non-Competition and Invention Agreements

Exit Strategies• IPOs and Registration Rights

• Sale/Acquisition

• Redemption of Stock

• Registration Rights

Registration Rights

❖ Shares cannot be freely sold without filing a Registration Statement with the SEC

❖ Only the Company can file

❖ So the Investors negotiate for certain Registration Rights to insure a contractual ability to exit into the public markets

Registration Rights, cont’d❖ Enables Investors to sell shares publicly by means

of a registered offering❖ Sales prior to end of 1-year holding period❖ Avoid compliance with volume limitations of

Rule 144❖ Registration paid for by the Company❖ Are Founders included?

Demand Registration Rights

❖ Exercisable after the IPO or within 3-7 years of investment

❖ Can be exercised 1 to 3 times;

❖ Can be exercised by holders of 20-50% of the registrable shares, with value of [$$$]

Piggyback Registration Rights❖ Investors “piggyback” on another registration

❖ Can they participate in other shareholders’ demand rights?

❖ Subject to underwriter “cutback”

❖ S-3 Registrations generally unlimited

❖ Acorn

❖ Beach

Redemption

❖ The Company’s repurchase of Preferred Stock at the demand of the Investors

❖ When Used: When the Company hasn’t gone public

❖ Because Founders Don’t Want To

❖ Because Business Doesn’t Develop Into an IPO Type

Redemption, cont’d❖When Does Redemption Kick In?

❖Typically after Five (5) years❖Often phased over Three (3) years

❖Trigger❖Automatic❖Upon vote of Preferred

❖Price❖Initial Purchase Price paid plus accrued dividends❖Sometimes additional return

❖Different classes of preferred — later classes won’t let earlier investors out first

Macon, Inc. Venture Capital Term Sheets Analysis

Daniel J. PiedraJ.D., expected ‘16University of San Diego School of Law

Differences & Similarities

Acorn Ventures

Beach Fund

Acorn Ventures

Capitalization Table: Acorn, with Escrow

Capitalization Table: Acorn, No-Escrow

Beach Fund

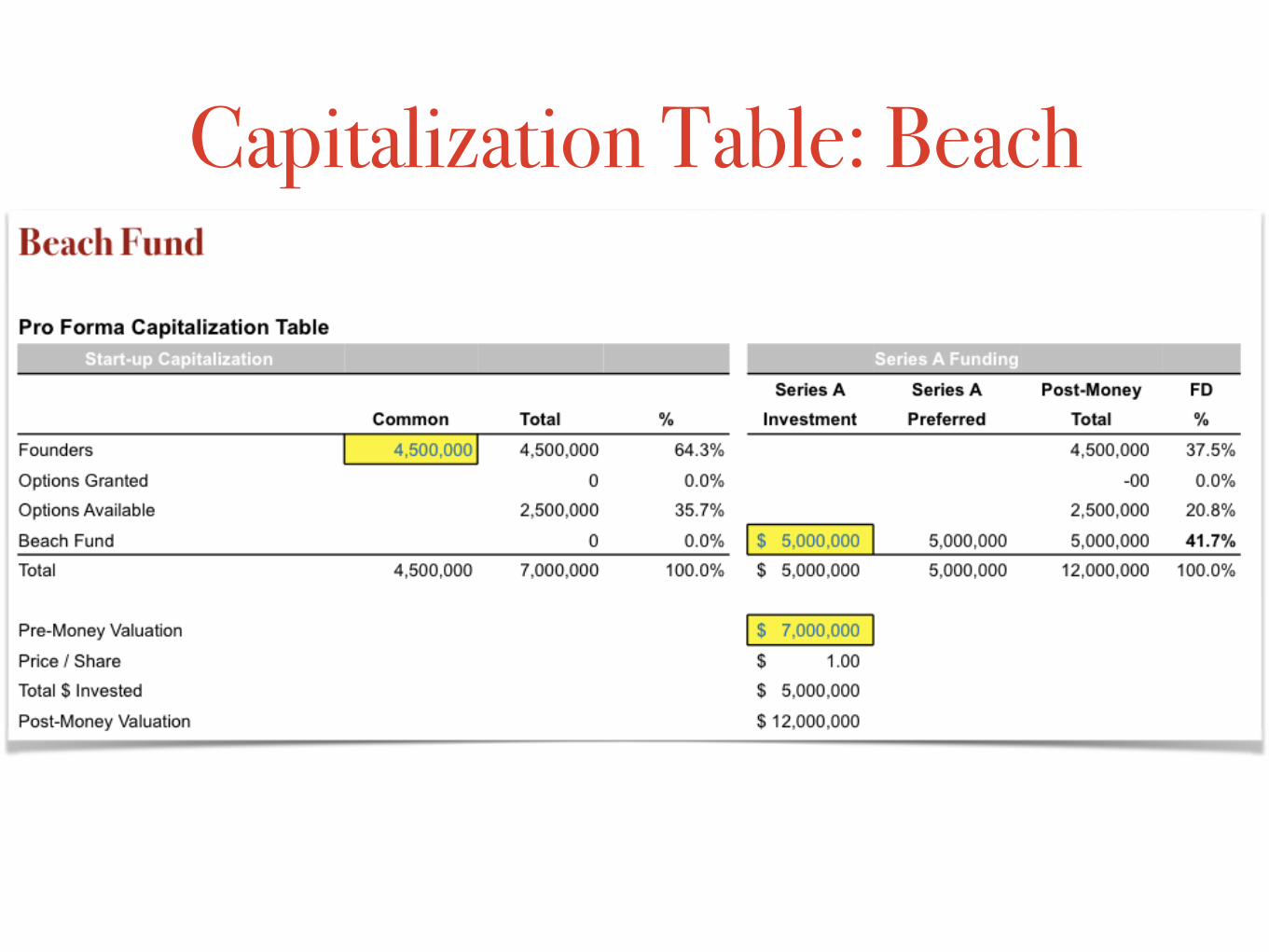

Capitalization Table: Beach

Similarities ❖ Investment Amount: $5 million

❖ Series A Convertible Preferred Stock

❖ Conversion Rate

❖ Registration Rights

❖ Information Rights

❖ No Termination Rights

❖ Closing Conditions: Acorn — “Securities Purchase Agreement”; Beach — “Conditions Precedent to Financing”

❖ No “No-shop” Provision

Differences

❖ Valuation ❖ Acorn: Pre-Calculated

❖ $7.53 million, with 3 million “performance shares”

❖ Performance Shares: “Shares held in escrow; non-issuable if Macon doesn’t reach performance milestone

❖ Beach: Standard, with employee option pool

Dividends (Differences)❖ Acorn:

❖ Non-cumulative — $0.08 (standard) on a Series A Preferred Outstanding, when and as declared by the Board of Directors

❖ Other dividends: Participates with Common Stock on an as-converted basis

❖ Most beneficial to company❖ Beach

❖ Cumulative — most beneficial to investors; bad for company❖ 10% (above standard) per year commencing on one year

anniversary of issuance of Series A Preferred❖ Ends when dividend accrual reaches 25% of Series A Purchase Price❖ Can also cease with consent of Board of Directors

Liquidation (Differences)❖ Acorn

❖ 3x multiple — A return of three times the initial pay issuance price

❖ Lower than standard 5x

❖ Beach ❖ 1 1/4 multiple — A return of 1.25 the initial purchase

price plus all declared but unpaid dividends

❖ Pro rata distribution

Automatic Conversion (Differences)❖ Acorn

❖ Majority of Preferred can consent to conversion

❖ No assurance that VC can control or at least veto and /or change number of holders

❖ Valuation: $25 million offering at $5 million/share

❖ Beach ❖ Valuation: $25 million offering at $20/share

❖ Consent of Preferred not required

❖ Automatic conversion at IPO

Liquidation Differences, cont’d

Acorn: ❖ Better option

❖ Investor payment is approx. $5,330,000 at a $0.08 dividend

❖ Preferred is capped at three times initial investment amount

❖ Lower than standard (5x)

❖ Better for a merger and IPO because Investors are capped at 3x their initial investment

Liquidation Differences, cont’d

Beach: ❖ Larger initial payback to the investors of roughly

$7,500,000 at a $0.25 unpaid dividend

❖ Allows for pro rata distribution of remaining proceeds to all shareholders

❖ No multiplier on distribution of remaining assets

❖ Excludes reference to subsequent financings

Anti-Dilution (Differences)❖ Acorn

❖ Broad-based weighted average❖ Carve out: No adjustment for issuance up to 3 million Common to

employees, directors, etc., pursuant to board-approved equity incentive plans❖ Helps to retain talent and incentivize employees

❖ Beach ❖ Weighted average❖ Share issuance of less than 50% of Series A Purchase Prices slips to

full ratchet ❖ Conditional: Only if Series A holder invests its pro rata share

Voting RightsAcorn

❖Standard list that requires 60% approval of Preferred, including:❖Creation / issuance of senior securities❖ Increase in number of authorized shares of Preferred❖Any changes in rights adverse to Preferred (typical)❖Change of control❖Dividend or distribution of capital stock❖Any transaction involving all or substantially all company assets

Beach ❖Friendlier terms❖Class vote with Common on as-converted basis on all matters presented to stockholders❖Exception: Preferred entitled to separate vote under Protective Provisions —

supermajority (does not state exact number) consent required for corporate actions to be agreed upon at a later date

Rights of First Refusal & Co-Sale❖ Acorn

❖Right of First Refusal❖Preferred has

❖ (1) pro rata right based on equity ownership to participate in subsequent equity financings; and

❖ (2) right to consider purchase of any potential sale of Common stock

❖Right of Co-Sale: Except through an IPO sale, Preferred have right to participate in Common transferring of shares

❖ Beach ❖Neither Right of First Refusal nor Co-Sale Rights

Anti-Dilution (Differences)

Beach ❖Down round after Series A financing❖No waiver ❖Reset of anti-dilution protection by existing investors required

Board Representation❖ Acorn

❖Favorable to investors❖ If Performance Shares released, then investors have option to replace the

outside director with a investor-chosen director❖Harmful to control

❖ Beach ❖More favorable to Founders❖Arrangements include:

❖One member elected by the Founder;❖Two Series A Investor-elected representatives;❖One outsider company nominated; and ❖One outsider company nominated and acceptable to all

#2: The No Frills Term Sheet

On-its-Face Selection of One Term

Sheet

Selection: Beach Fund❖ Acorn has three investors;

potential conflicts❖ Dividend term concerning but

negotiation — Board’s consent authority mitigating factor

❖ Simple Board structure❖ Acorn’s Registration Rights

potential to be expensive❖ Better liquidation preference

(except for merger)

#3: Term Alterations During Negotiations

1.Valuation

2.Liquidation Preference

1. Caps

3.Anti-Dilution Provisions

4.Dividends

5.Voting Rights

6.Redemption Rights

7.Founders Vesting Rights

8.Board Composition

9.Miscellaneous

Valuation

❖ Risk of "counting chickens before the eggs have hatched”

❖ Goal: Increase value placed on company to minimize cost of VC investment

❖ Develop financial projections for time of likely VC exit

Liquidation Preference

❖ Goal: Cap on Participating Preferred

❖ Non-Participating Preferred

❖ Cannot participate as common shareholders

❖ Aim for non-participating preferred shares, but odds are slim

❖ IPO inapplicable

Dilution❖ Focus on definition of “Outstanding Securities”

❖ Investors want full ratchet

❖ Conversion price of preferred is adjusted downward for a dilutive issuance on a dollar-for-dollar basis

❖ Least favorable to company

❖ Always try to get a “floor” on ratchet

❖ Company wants broad-based provision

❖ Calculating dilution based upon a “weighted average” more beneficial to the company

❖ Easily negotiable

Dividends❖ “When as declared by Board” – a non-cumulative dividend

❖ If Board does not declare then there is no dividend

❖ Standard for an early stage company

❖ Typical not to get a dividend every year – VC more interested in getting a bigger return at end, rather than a bit back every year

❖ For later-stage companies, it is more common to see cumulative dividend, generally paid out

❖ These companies have more money and investors may want to start seeing return

Voting Rights❖ Focus on limiting to events that directly impact preferred

rights or investments

❖ holder of Preferred will have the

❖ 1:1 votes / share ideal

❖ Avoid provisions that give investors too much management control

❖ Acorn: Substantial control requirements

❖ Beach: Certain corporate actions requires “supermajority” vote by Series A Preferred

❖ Indicated flexibility

Founders Vesting Rights

❖ Negotiate for acceleration in the event of change of control or termination

❖ Request shorter vesting period

❖ Acorn: 4 years for employees with 12-month cliff

❖ Founders: 25% instant vesting, the rest spread out for three years

❖ Beach: Same, except unvested portion subject to buyback provision

Board Composition❖ Heavily negotiated❖ All about control❖ Critical for exits❖ Common for VCs to want at least one seat on the board (and perhaps

more depending on the amount invested)❖ Focus on the final seat

❖ Will preferred and common vote together as a single class or separately?

❖ Additional control granted if Company fails to meet benchmarks?❖ Negotiations will focus on amount invested and level of control sought or

required

Rights of First Refusal & Co-Sale Acorn ❖ Right of First Refusal too broad — includes all Series

A Preferred❖ Recommended: Preferred may exercise such right

only at a price equal to the lower of: ❖ (i) the price offered by the proposed third party

purchaser; and ❖ (ii) the price most recently set by the Board of

Directors as the fair market value of the Common.

Miscellaneous

❖ Information Rights ❖ Seek appropriate restrictions such as a non-disclosure

agreement

❖ Protective Provisions ❖ Ensure that VCs do not have too much control

❖ Drag Along Rights ❖ Focus on appropriate thresholds

#4: Slow Growth or Fast Growth

Benefits & Drawbacks for

Company

• Instant growth mean results in higher valuation from subsequent investors

• If passion for company is high, then slow growth best option — but VC

investors wary

• Hobson’s Choice

• Key Determinant of Valuation: Risk

• Low valuation at start up

• Limit involvement with too many investors so as not to set unreachable

milestones

• Value of company grows and risks decrease as milestones are reached

• Result: Cost of company shares increase

• Ultimate Question: What is goal of company?

• Large Business

• Small Business

#5: Realization: IPO v. Merger

Benefits & Drawbacks for

Company

Acorn: •Automatic Conversion: Upon IPO, preferred shares are converted to

common, whereas the VC loses liquidation preference•Beneficial to Company

•Vesting Provision•One-year accelerated vesting following change of control transaction•Favorable to Founder

Beach: •Automatic conversion: For IPO, subject to share price limitation and

aggregate proceeds offering•70% preferred holders, acting as single voting class, can elect to not treat a

consolidation or merger as a dissolution or winding up•Favorable to preferred, because liquidation preference survives merger or

consolidation•Vesting Provision

•Restricts Founders’ access to shares with 48-month vesting period; early exit poses challenge

#6: Other Considerations

Important Factors Outside

of the Term Sheet

•Reputation

•Good chemistry with leaders

•Experience

•Track record

•Length of operation

•Successful investments

•Post-exit relationships with previous partners

•Successful management and operational structure

Personalities, Management & Track Record

VC Involvement: Normally involves a representation on boardOther factors:

Active •Value-added services (i.e., marketing, market knowledge, recruitment, etc.)

•An active partnership

Passive / Major Decisions •Involvement in major decisions

•Appointed board member as watchdog

•Information rights (periodic statements of financial and other information.

•Get-in and get-out

Viability Fund must have committed financiers who are “going for the gold”

Flexibility: • Founders should seek out flexible in adjusting to

unpredictable events and changes in Company• Many VCs have rigid rules

Geographic Proximity

Related Documents