Presentation to Parliamentary Portfolio Committee on Finance Bruce Cameron Editor: Personal Finance (Personal Finance is an Independent Newspapers publication published in the Saturday Star, Saturday Argus, Pretoria News Weekend and the Independent on Saturday. Personal Finance is also published as a quarterly magazine.)

Presentation to Parliamentary Portfolio Committee on Finance Bruce Cameron Editor: Personal Finance (Personal Finance is an Independent Newspapers publication.

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presentation to Parliamentary Portfolio Committee on Finance

Bruce Cameron

Editor: Personal Finance(Personal Finance is an Independent Newspapers publication

published in the Saturday Star, Saturday Argus, Pretoria News Weekend and the Independent on Saturday. Personal Finance is

also published as a quarterly magazine.)

Rusconi: Only the tip of the costs

• Simple facts of costs

• Brief historical cost perspective

• Costs: A feeding frenzy

• Disclosure

• The red herrings

• Possible solutions

Simple factsNo product can be cost freeWhat matters is:• The quantum

• Whether the costs are justified

• Whether the costs are negotiable

• Whether the costs are fully disclosed

• Whether the costs are understandable

• Whether the costs are comparable

• Whether the consumer is placed in the most cost-effective and appropriate product taking all factors into account

A Brief History

Once there were Defined Benefit Funds.

• Members contributed to the fund

• Members received a pension from the fund

• There were no additional costs to buy a pension

And then the cost feeding frenzy started...

The main driving factor in increased costs has been a consequence of the move from defined benefit pension funds to defined contribution pension and provident funds

Cost factor 1: Buying a Pension

Employer-sponsored retirement funds:

• Most funds now either outsource the provision of pensions to a life assurance company; or

• Members are permitted to purchase their own pensions (annuities).

(Note: Annuity costs are variable and depend on factors such as type of annuity, commissions)

Cost factor 1: Buying a pension

Retirement annuities

• When a retirement annuity matures (age 55 to 69) at least two thirds must be used to purchase a pension (annuity)

• Even where the same life assurance company is involved there will be a second round of costs

Cost factor 1 (Commission Eg):

Commission on an Investment of R100 000 Guaranteed Life Annuity Living Annuity

Initial: R3 000 R2 500

Over next 10 years (to age 70): R6 962

Over next 10 years (to age 80) R13 275

Over next 10 years (to age 90): R25 312

Total Commission: R3 000 R48 049Assumptions:• Guaranteed Annuity: Commission is the three percent maximum permissible.• Living Annuity: Based on:

• .Average inflation rate of five percent.• .Average annual investment growth rate of 12 percent.• .Initial commission of 2,5 percent.• .Annual commission of 0,5 percent.

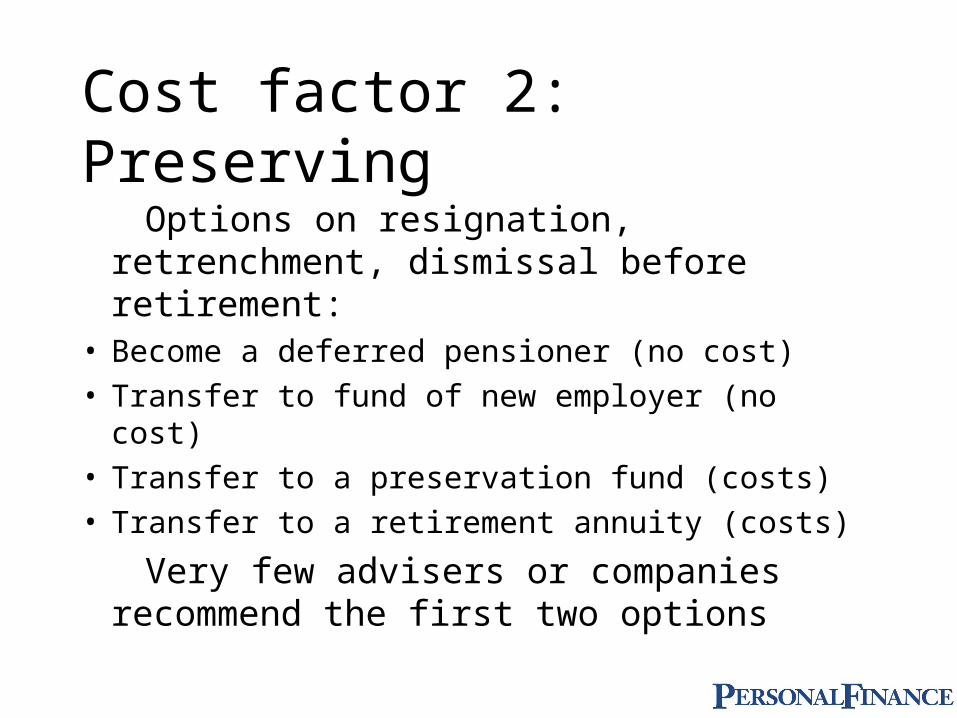

Cost factor 2: Preserving

Options on resignation, retrenchment, dismissal before retirement:

• Become a deferred pensioner (no cost)• Transfer to fund of new employer (no cost)• Transfer to a preservation fund (costs)• Transfer to a retirement annuity (costs)

Very few advisers or companies recommend the first two options

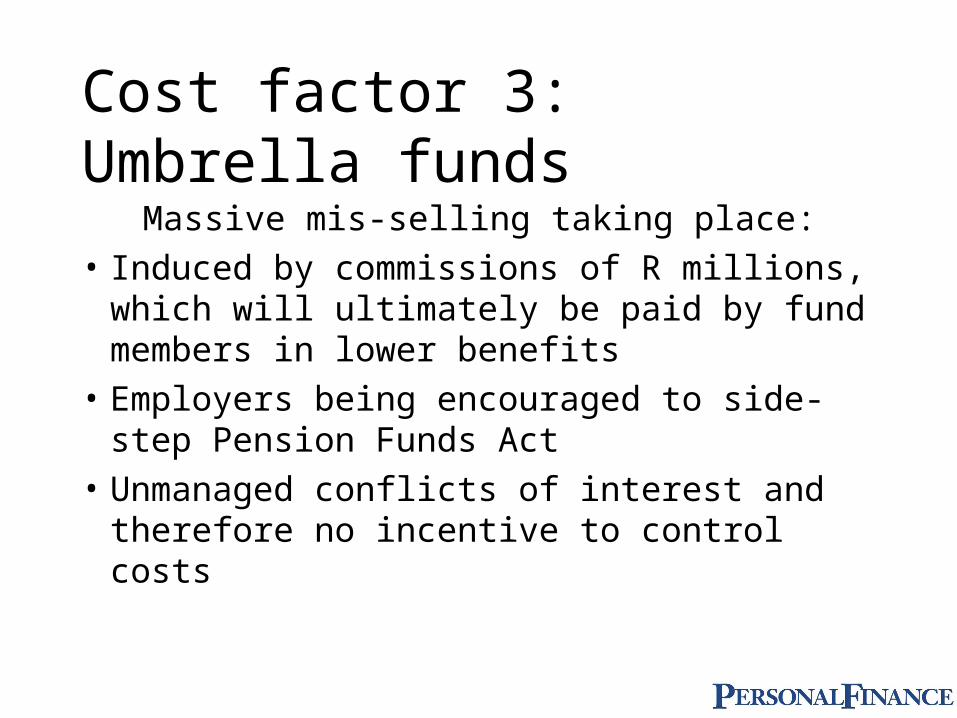

Cost factor 3: Umbrella funds

The intention of financial services industry sponsored umbrella retirement funds:

• To provide cost effective retirement vehicle for small employer.

Cost factor 3: Umbrella funds

Massive mis-selling taking place:

• Induced by commissions of R millions, which will ultimately be paid by fund members in lower benefits

• Employers being encouraged to side-step Pension Funds Act

• Unmanaged conflicts of interest and therefore no incentive to control costs

Cost factor 3: Umbrella fundsEmployer No. of Contribution Costs Liberty Momentum Old Mutual Sanlam TCS

Employees Monthly

Sales 11 R18491.00 Admin charges 1559.00 602.00 586.00 1800.00 751.00

Commissions/Fees 1230.00 1230.00 1230.00 1230.00 322.00

Total 2789.00 1832.00 1816.00 3030.00 1073.00

Percentage 15.08% 9.91% 9.82% 16.39% 5.80%

Roofing 12 R 3106.00 Admin charges 369.00 670.00 639.00 1800.00 788.00

Commissions/Fees 273.00 272.00 274.00 274.00 338.00

Total 642.00 942.00 913.00 2074.00 1126.00

Percentage 20.67% 30.33% 29.39% 66.77% 36.25%

Engineering 37 R 212282.00 Admin charges 2261.00 1851.00 2557.00 1840.00 1585.00

Commissions/Fees 6754.00 6754.00 5000.00 4953.00 679.00

Total 9015.00 8605.00 7557.00 6793.00 2264.00

Percentage 4.25% 4.05% 3.56% 3.20% 1.07%

Source:Total Care Strategy (TCS)

Note: These costs exclude asset management charges.

Costs of employee sponsored funds (two real examples):

Provident Fund 1172 employees 0.61% of every contribution

Pension fund 896 employees 0.57% of every contribution

Cost factor 3: Use of own service providers

Most umbrella funds, retirement annuity, preservation funds also insist that all their own services be used including:

• Asset management• Administration• Group life and and disability assurance• Actuarial consulting

IE. There is no attempt to find the most cost-effective service provider

Cost factor 4: Surrender penalties

Life assurance policies including retirement annuities are issued for contract periods

• If a policy lapses in the first two years commissions are clawed back from the adviser but not passed on to the policyholder

• If a retirement annuity is made paid up or the premium reduced the cost factor remains much the same ie far lower maturity values for the policyholder.

Cost factor 5: Investment choice

Major trend towards giving maximum choice in build up and in retirement: Consequences are:

• Higher costs (and higher profits) • Prudential investment guidelines (Regulation 28

being ignored.• Financial advisers becoming quasi asset managers

without the necessary skills. Huge loses being suffered by consumers.

Cost factor 6: Escalation clauses

Automatic increases in premiums on retirement annuities to keep up with inflation: Consequences are:

• Can be reduction in investment value if cancelled • Costs cannot be recovered in last two or three

years.• Policies will be made paid-up or have premiums

reduced with consequent penalties for policyholders

Understanding Costs

• Cost structures vary between companies.• Cost structures vary between different products of

companies.• Costs may be disclosed as Rands and/or in

percentages. • Costs can be: - Initial (as payment is made); and/or

- On-going (monthly/annually); and/or

- On exit (when an investment is made paid up or cashed in)

Disclosure

Companies are required in terms of the Policyholder Protection Rules (of the Long Term Assurance Act) and the Financial Advisory and Intermediary Services Act to disclose all costs.

But…....

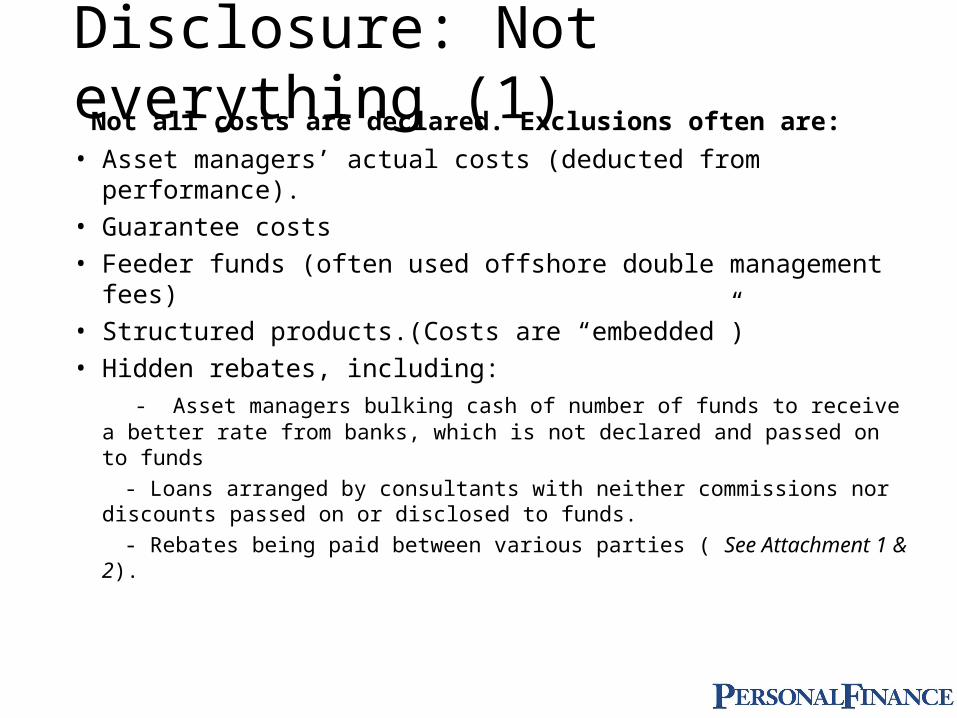

Disclosure: Not everything (1) Not all costs are declared. Exclusions often are:

• Asset managers’ actual costs (deducted from performance).

• Guarantee costs

• Feeder funds (often used offshore double management fees)

• Structured products.(Costs are “embedded”)

• Hidden rebates, including:

- Asset managers bulking cash of number of funds to receive a better rate from banks, which is not declared and passed on to funds

- Loans arranged by consultants with neither commissions nor discounts passed on or disclosed to funds.

- Rebates being paid between various parties ( See Attachment 1 & 2).

Disclosure: Not everything (2) Not all costs are declared. Exclusions often are:

• Underlying costs. For example many products are multi-tiered. Layers include:

- Linked investments services product

- Life assurance legal wrapper (e.g. Retirement annuity, preservation fund)

- A risk-adjusted investment portfolio

- A unit trust fund

- Asset manager/s

• Surrender penalties. There is no formula for how penalties are applied for making an R/A paid up or reducing premiums.

• Early withdrawal/switching: Penalties charged for changing living annuity provider (Lisp and life company)

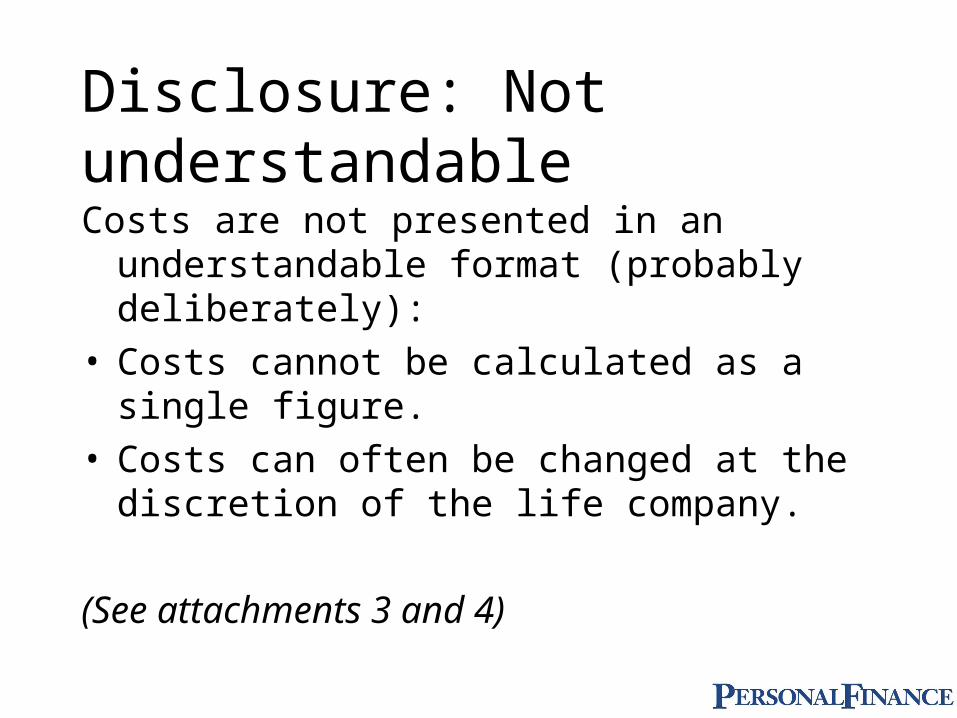

Disclosure: Not understandable

Costs are not presented in an understandable format (probably deliberately):

• Costs cannot be calculated as a single figure. • Costs can often be changed at the discretion of the

life company.

(See attachments 3 and 4)

Disclosure: Not comparableExample:• September 2003 Personal Finance published a report on

life assurance endowment (include retirement annuities) to which a life assurance company took exception.

• Personal Finance asked for comparable cost details.

• Personal Finance was “warned off” and threatened.

• Attempts made to mislead Personal Finance (eg comparing a unit trust foreign specialist (high costs) with a life assurance money market portfolio (low cost)

• Report published: July 2004.

(See Attachment 5)

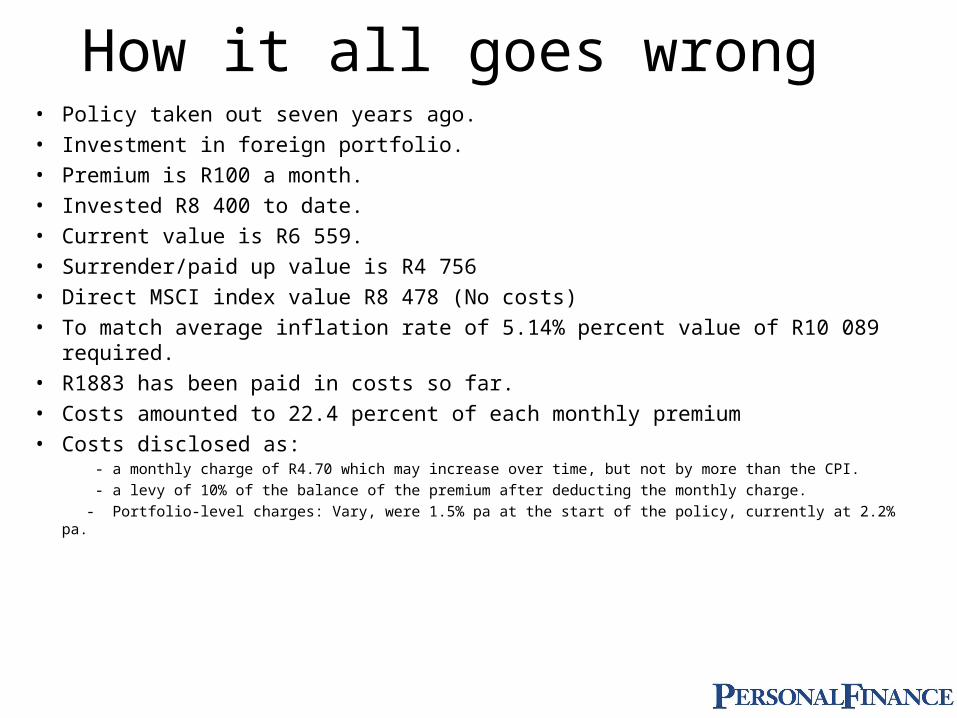

How it all goes wrong• Policy taken out seven years ago.

• Investment in foreign portfolio.

• Premium is R100 a month.

• Invested R8 400 to date.

• Current value is R6 559.

• Surrender/paid up value is R4 756

• Direct MSCI index value R8 478 (No costs)

• To match average inflation rate of 5.14% percent value of R10 089 required.

• R1883 has been paid in costs so far.

• Costs amounted to 22.4 percent of each monthly premium

• Costs disclosed as: - a monthly charge of R4.70 which may increase over time, but not by more than the CPI.

- a levy of 10% of the balance of the premium after deducting the monthly charge.

- Portfolio-level charges: Vary, were 1.5% pa at the start of the policy, currently at 2.2% pa.

The Red Herrings The industry often makes false or misleading claims or

denies what has not been said. Examples include:• Disciplined saving with life products….but look at the surrender and lapse

figures. R billions lost every year.

• Distinction between single premium and recurring premium….but people don’t save for retirement with single premiums.

• Benefit illustration agreement. Misleading, particularly on costs. Planned new option a big improvement (See Attachment 6)

• Distribution costs. Blame it on advisers when other costs are involved (See Attachment 7 - Note sent to a financial adviser from life company)

• Ombudsman for Long Term Assurance: Very limited as is precluded from dealing with performance which will include costs)

Possible solutions1. The entire financial services industry must adopt common standards and formats

for disclosing costs: This should include:• Full break down of all costs (initial, on-going and exit).• As a total in rands for the investment period• As a percentage of the investment for the investment period.• As a reduced yield This means that a Rand maturity figure must be provided on what benefit

would be received if no costs are involved; and what the figure is reduced when costs are involved.

2. Proper disclosure of commissions/fees so investor can ensure that commission is not the basis for advice. Should be disclosed as:

• Initial and on-going.• As a total in rands for the investment period• As a percentage of the investment for the investment period.• As a reduced yield : If no costs are involved; and when costs are involved.

(See attachment 8)

Possible solutions3. Ban upfront commissions on life products and change to as-and-

when as with the unit trust industry. This will:• Help reduce the high surrender and lapse figures as there will be no “new”

commission incentive every three years.

• Help reduce the high surrender, lapse, paid-up and reduced premiums penalties.

4. Ban all non-cash incentives to financial advisers. This includes:• Foreign trips (What is the difference between Mac Maharaj accepting a free trip to

Disneyland and a financial adviser accepting a trip)

5. Ban rebates (kickbacks), discounts, fees, commissions between service providers.

6. Create a standard formula for penalties on surrenders, paid up policies, reduced premiums etc.

Possible solutions7. Create low cost retirement saving options for low income workers

either through the unit trust industry or a national government-sponsored fund, using independent trustees and private sector service providers.

8. Ban all incentives from service providers to retirement fund trustees.

9. Urgently approve draft legislation on umbrella funds.

10. Allow the Government’s RSA retail bonds to be used as an underlying investment for living annuities. (Currently can only be owned by a natural person. By law the life office owns the assets invested in a living annuity.

11. Stop practice of forcing people into hands of advisers by charging a fee equal to maximum commission when going direct.

Related Documents