One-Stop-Shop for a Healthy Future © 2010-2011 Arseus. All rights reserved. Jan Peeters, CFO Arseus NV 10 November 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

One-Stop-Shop for a Healthy Future

© 2010-2011 Arseus. All rights reserved.

Jan Peeters, CFO Arseus NV

10 November 2011

Key Facts Arseus

Products, services and concepts for professionals in the healthcare sector

Strong focus on innovation, service and added value

Number 1 or 2 position in selected market segments

Present in 19 countries in Europe, the US, Brazil and Argentina

Listed on NYSE Euronext Brussels/Amsterdam

Included in the BEL-Mid index and in the AScX-index

Current market capitalization of € 350 million

2

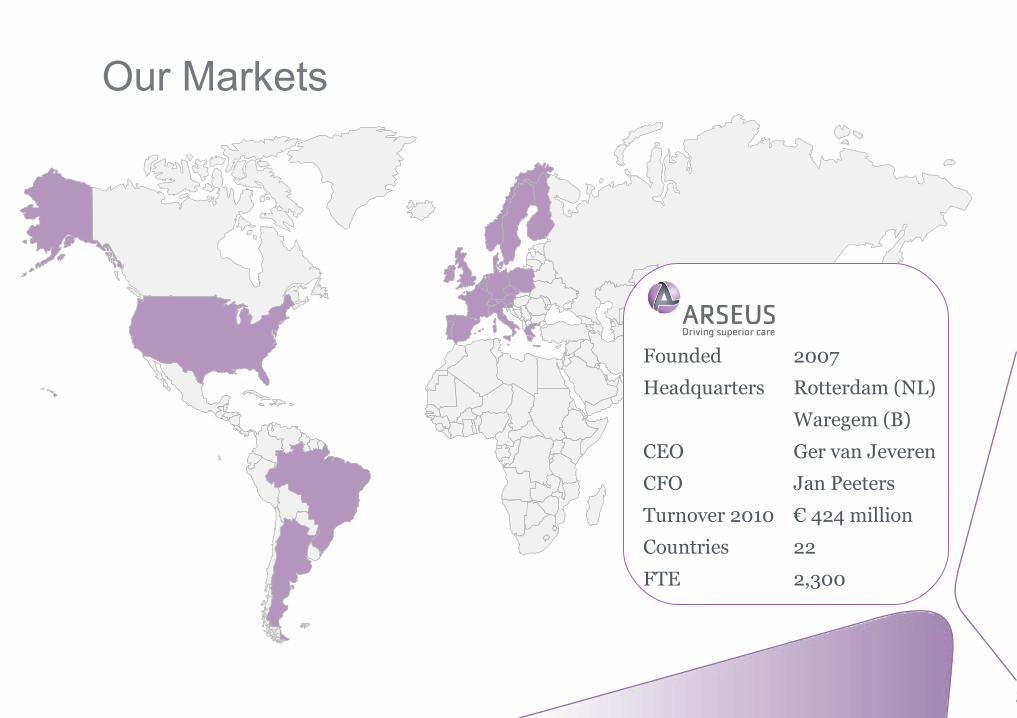

Our Markets

Founded 2007

Headquarters Rotterdam (NL)

Waregem (B)

CEO Ger van Jeveren

CFO Jan Peeters

Turnover 2010 € 424 million

Countries 22

FTE 2,300

3

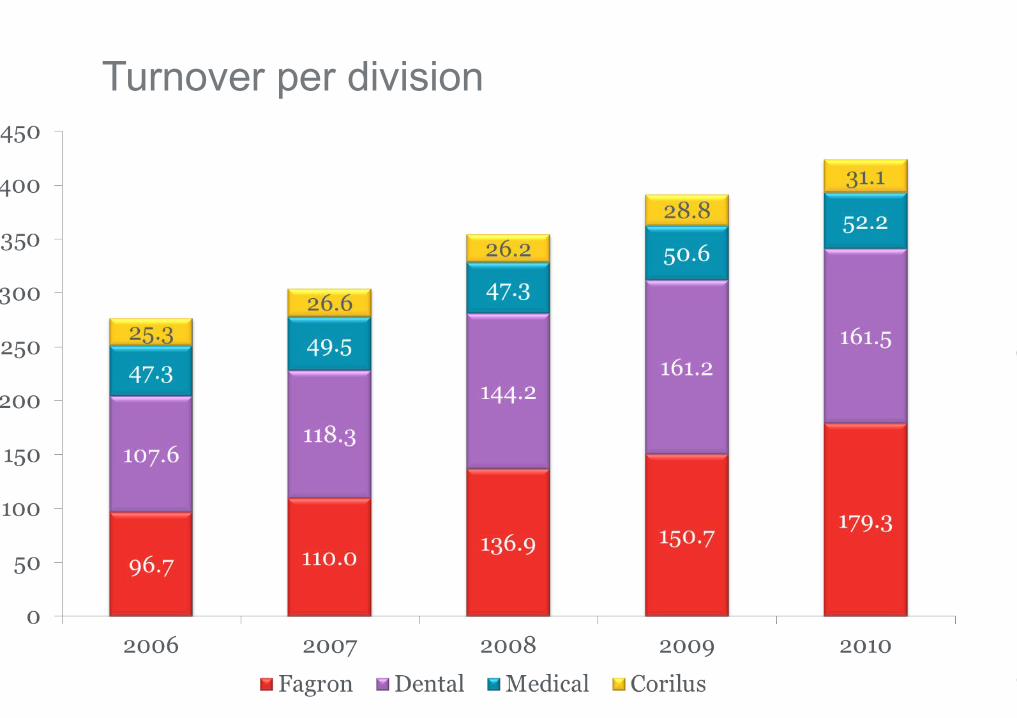

Turnover per division

Four Divisions

Arseus Dental

6

- Partner to all professionals in the dental market

- Focus on dental cabinets and dental labs

- Market leader in selected segments in Belgium, the Netherlands and

France (active in five European countries)

- 2010: Sales € 161.5 million, REBITDA € 10.0 million, 637 FTE

Arseus Medical

7

- Innovative solutions to support medical professionals to deliver

superior care to their patients

- Focus on doctors, hospitals and rest homes

- Market leader in selected segments in Belgium and the Netherlands

- 2010: Sales € 52.2 million, REBITDA € 5.2 million, 176 FTE

Corilus

8

- Total ICT-solutions for medical professionals

- Market leader in Belgium, also active in the Netherlands and France

- 2010: Sales € 31.1 million, REBITDA € 9.2 million, 210 FTE

Fagron

Global One-Stop-Shop for Pharmaceutical

Compounding

10

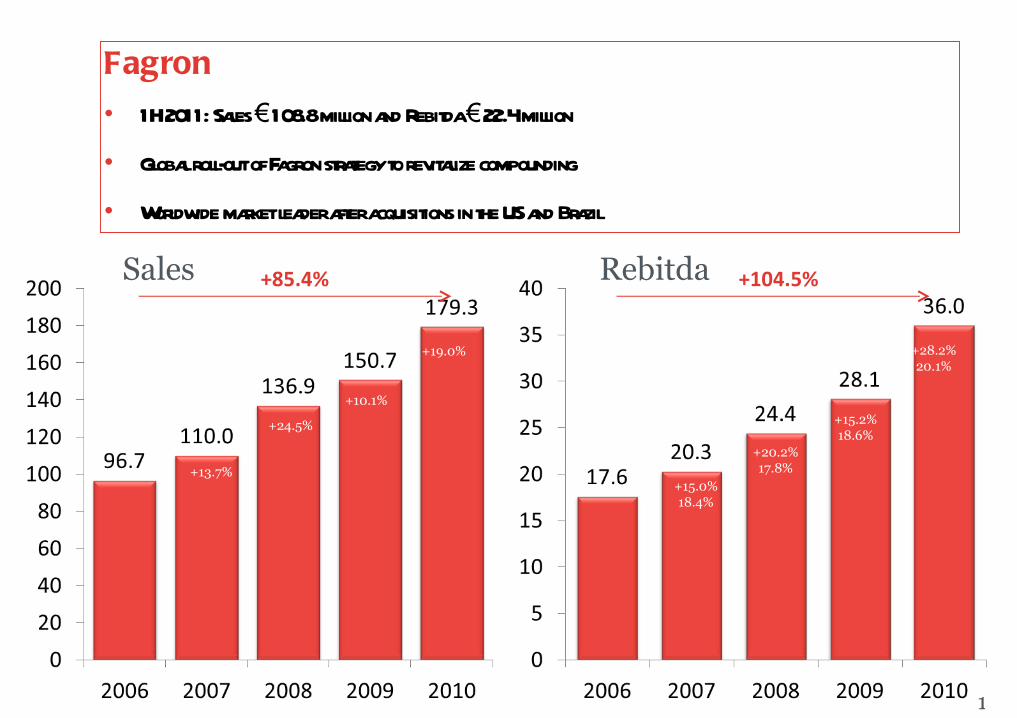

Fagron

• 1H 2011: Sales 108.8 million and Rebitda 22.4 million€ €

• Global roll-out of Fagron strategy to revitalize compounding

• Worldwide market leader after acquisitions in the US and Brazil

Sales Rebitda

+28.2%20.1%

+10.1%

+15.2%18.6%

+24.5%

+20.2%17.8%+13.7%

+15.0%18.4%

+19.0%

+85.4% +104.5%

Mission

• We revitalize compounding in order to widen the therapeutic scope of the

prescriber, to enable tailor-made pharmaceutical care for the patient

• By doing so, we are supporting the unique selling point of pharmacists:

Compounding

Acquisition Track-Record

2007

2008

2009

2010

2011

Acquisition

Acquisition

Acquisition

Acquisition

Greenfield

Partnerships

Greenfield

Greenfield

Acquisition

Acquisitions

Brazil is the Future!

Huge In All Aspects

Brazil Global Ranking

Compounding market US$ 4,000 million 1

Area 8,154,877 sq km. 5

Population 203.4 million 5

Labor force 103.6 million 6

Unemployment rate 6.7% 62

GDP (2011E)

Total US$2.517 trillion 6

Per capita US$ 12,916 54

Inflation (2010E) 5.o% 146

15

Testimonial Acquiring companies In Brazil

Acquisition Of DEG

www.deg.com.br

Location São Paulo

Founded 1974

Market position #2

Turnover 2010 € 25 mln

EBITDA-margin 16%

Employees 177

17

Acquisition Of Pharma Nostra

www.pharma-nostra.com.br

Location Rio de Janeiro

Anápolis

Campinas

Founded 2000

Market position #1

Turnover 2010 € 45 mln

EBITDA-margin 15%

Employees 316

18

Culture

• Very formal at first but after gaining confidence => very informal and relaxed (big “hug” culture)

• Entrepreneurial

• Latin temperament, sometimes emotional or theatrical

• Disciplined, proud and hard workers

• Only senior level speak good English or other foreign languages / analphabets are still not an exception

• Very cash-driven (because of high inflation “trauma”)

• Meetings often start late and end late

19

Business Environment• Governmental inefficiency

• Legal and bureaucratic complications

• Decreasing informal economy (f.i. bribery)

• High taxation

• Poor infrastructure: transport is extremely expensive

• Security related issues

• High (but decreasing) inflation => structural yearly wage increases (about 8% per annum last 3 years)

• Increasing lease and real estate prices (SP is becoming more expensive than NY)

• Skilled academic people are very expensive

20

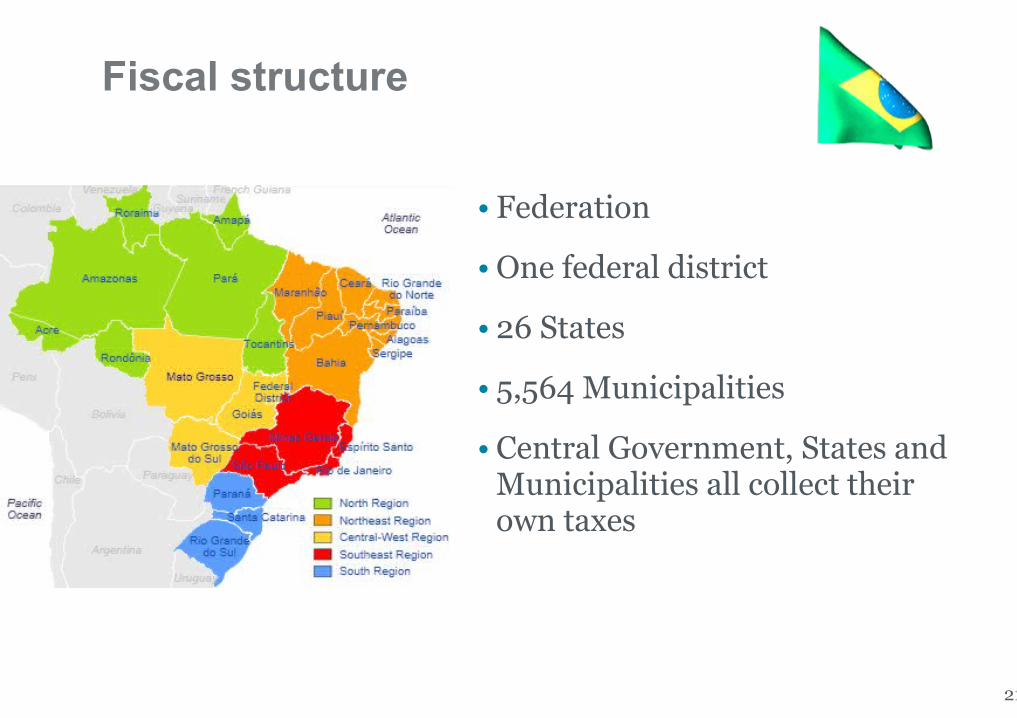

Fiscal structure

• Federation

• One federal district

• 26 States

• 5,564 Municipalities

• Central Government, States and Municipalities all collect their own taxes

21

Fiscal

• Very high import taxes

• ‘Tax wars’ between the 26 Brazilian states

⇒Huge amount of litigations

⇒Political problem

• Transfer pricing: not in line with OECD transfer pricing

guidelines

• Goodwill: can be fiscally amortized in some cases

22

Financing• Local financing is very expensive

• Taxes to be paid on the import of capital

• Major local banks: Banco do Brasil and Itau

• Major international banks: Banco Santander and HSBC

• Brazilian business people still think and breath « dollar »

23

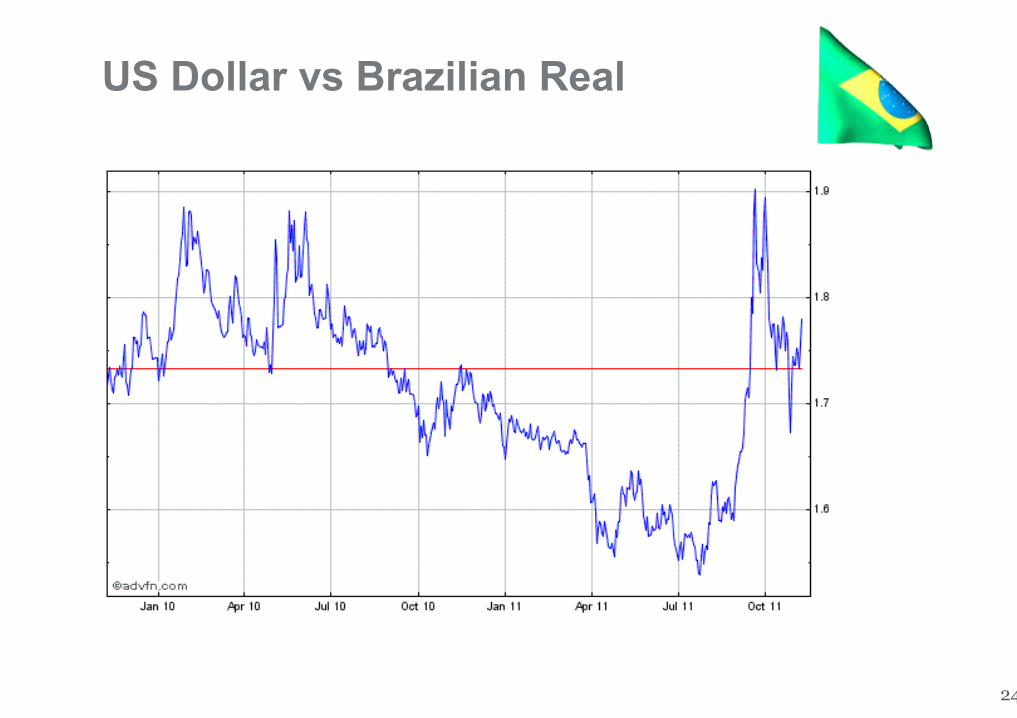

US Dollar vs Brazilian Real

24

Advisors

• Law firms : precific regime for international law firms

• Accounting firms

25

It’s important to work closely with local lawyers and accountants. This is extremely useful in overcoming many of the unfathomable local complexities.

Conclusion

• Brazil is a very promising economy with a lot of upside

potential

• Latin, entrepreneurial culture

• Social democratic environment

• Infrastructure and education: need to be improved

• Import and export of capital and foreign ownership is no

issue

• (Increasing) protectionist approach (high import taxes)

• Complex fiscal environment and high level of burocracy

26

Questions

Related Documents