Federal Income Taxation Chapter 2 Income In Kind? Professors Wells Presentation: August 22, 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Federal Income Taxation Chapter 2 Income In Kind? Professors Wells

Presentation:

August 22, 2017

2

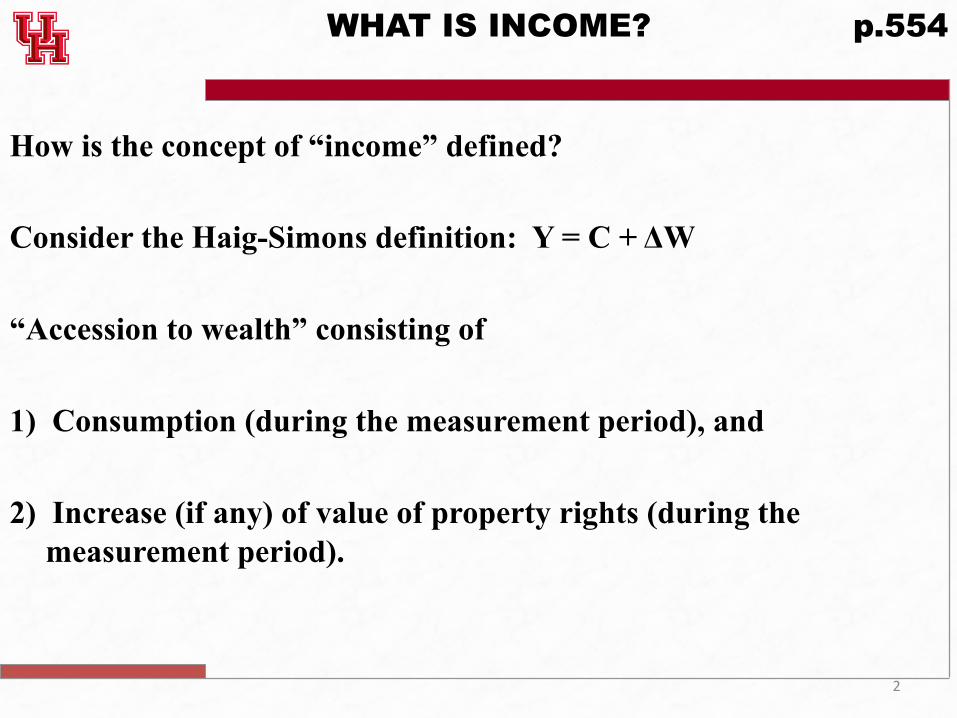

How is the concept of “income” defined? Consider the Haig-Simons definition: Y = C + ΔW “Accession to wealth” consisting of 1) Consumption (during the measurement period), and 2) Increase (if any) of value of property rights (during the

measurement period).

WHAT IS INCOME? p.554

3

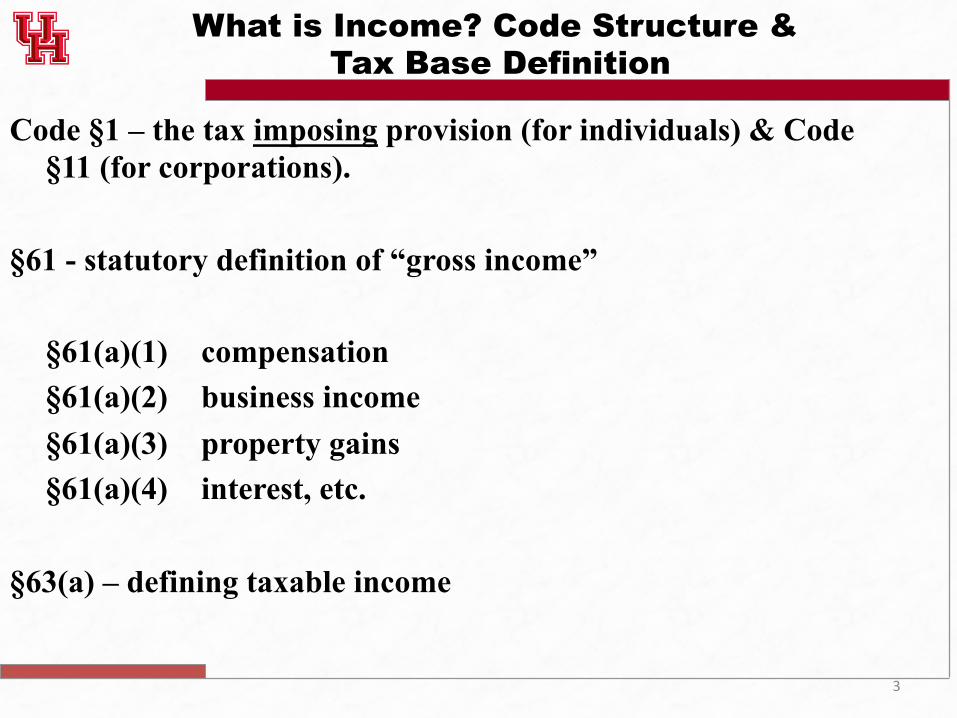

What is Income? Code Structure & Tax Base Definition

Code §1 – the tax imposing provision (for individuals) & Code §11 (for corporations).

§61 - statutory definition of “gross income”

§61(a)(1) compensation §61(a)(2) business income §61(a)(3) property gains §61(a)(4) interest, etc.

§63(a) – defining taxable income

4

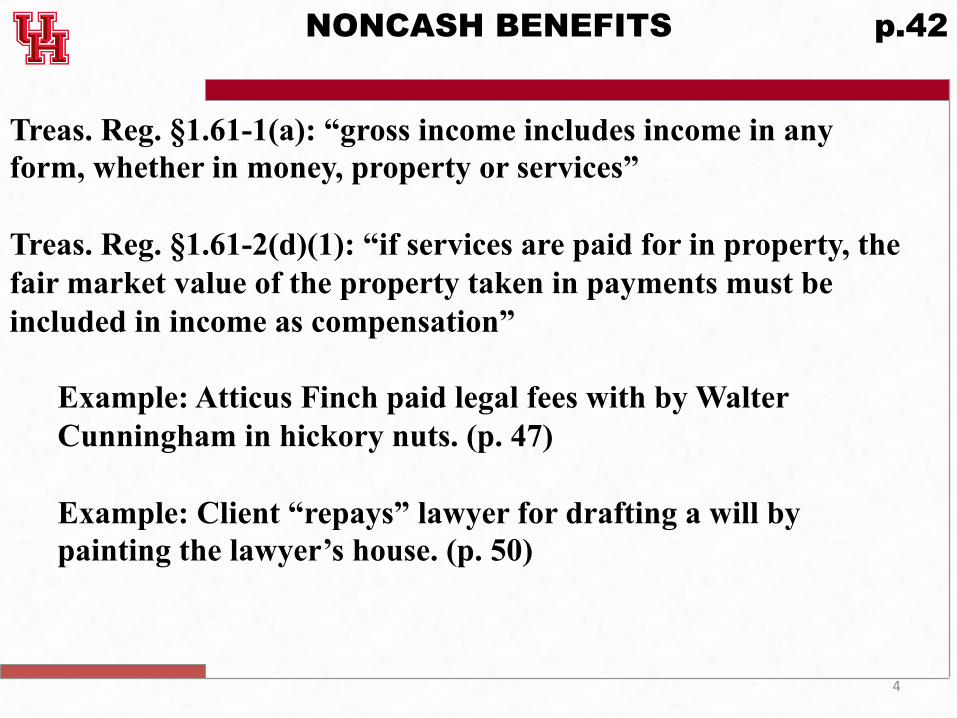

Treas. Reg. §1.61-1(a): “gross income includes income in any form, whether in money, property or services” Treas. Reg. §1.61-2(d)(1): “if services are paid for in property, the fair market value of the property taken in payments must be included in income as compensation”

Example: Atticus Finch paid legal fees with by Walter Cunningham in hickory nuts. (p. 47)

Example: Client “repays” lawyer for drafting a will by painting the lawyer’s house. (p. 50)

NONCASH BENEFITS p.42

5

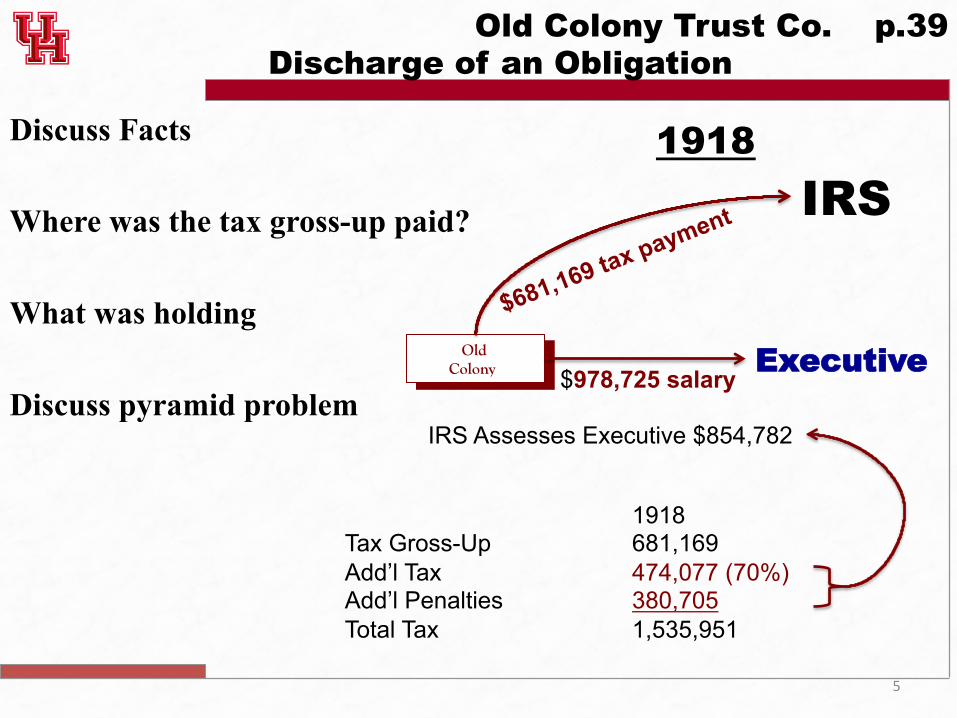

Old Colony Trust Co. p.39 Discharge of an Obligation

Discuss Facts Where was the tax gross-up paid? What was holding Discuss pyramid problem

Old Colony Executive

$978,725 salary

IRS 1918

1918 Tax Gross-Up 681,169 Add’l Tax 474,077 (70%) Add’l Penalties 380,705 Total Tax 1,535,951

IRS Assesses Executive $854,782

6

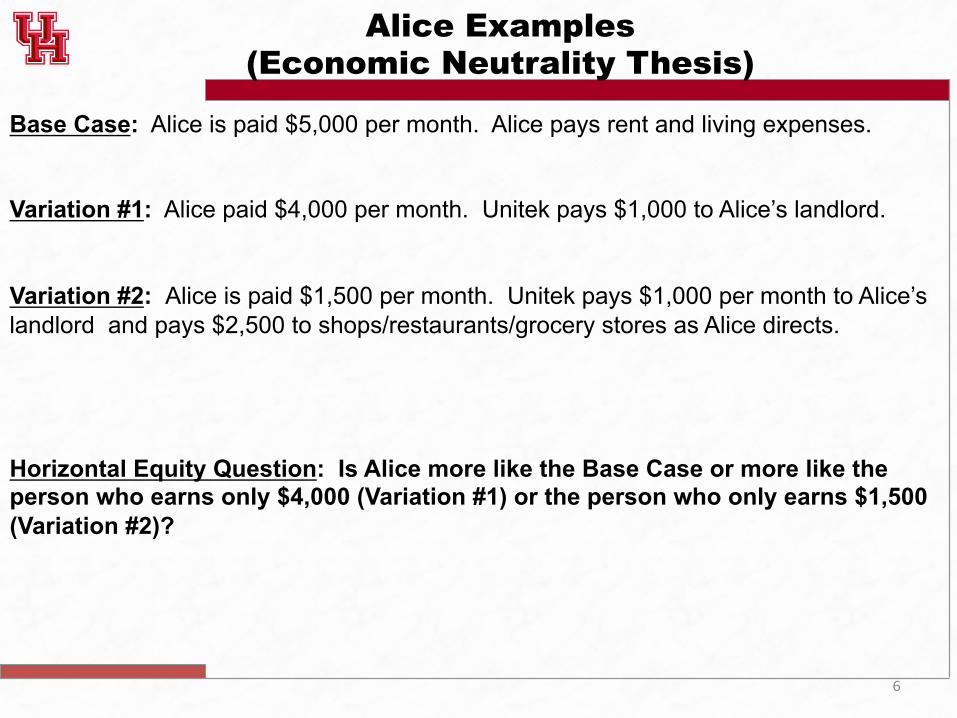

Alice Examples (Economic Neutrality Thesis)

Base Case: Alice is paid $5,000 per month. Alice pays rent and living expenses. Variation #1: Alice paid $4,000 per month. Unitek pays $1,000 to Alice’s landlord. Variation #2: Alice is paid $1,500 per month. Unitek pays $1,000 per month to Alice’s landlord and pays $2,500 to shops/restaurants/grocery stores as Alice directs. Horizontal Equity Question: Is Alice more like the Base Case or more like the person who earns only $4,000 (Variation #1) or the person who only earns $1,500 (Variation #2)?

7

Meals & Lodging Provided By Employer p.44 Benaglia v. Commissioner

Facts: Hotel manager receives cost meals and lodging at no cost.

8

Royal Hawaiian Hotel: A Starwood Five Star Hotel

9

Lodging in the King Kamehameha Suite www.royal-hawaiian.com

10

Lodging in the King Kamehameha Suite www.royal-hawaiian.com

11

Lodging in the King Kamehameha Suite www.royal-hawaiian.com

12

Dining at the Jewell-Toned Azur Restaurant www.royal-hawaiian.com

13

Work-related Fringe Benefits

Should consumption items provided by the employer be excluded from gross income when motivated by “the convenience of the employer”, e.g., meals onsite to keep the employee on location for the lunch period?

Consider horizontal equity issues if employers furnish many “in-kind” benefits to some employees.

Are working conditions not consumption substitutes? Enable partial exclusion only?

14

Turner v. Commissioner p.48

Discuss Facts 1. Retail first-class ticket price: $2,220 2. Exchange first-class ticket plus $12.50 for 4 round trip tourist

tickets to Rio de Janiero. What amount in income? Court Holding: $1,400

15

Notes to Turner p.50

1. Does this case provide a viable solution for the valuation problem in Benaglia?

2. Suppose Benaglia could show that living in a hotel was for him no boon but a burden. Would that justify excluding or assigning a low value to the lodging provided him?

3. Suppose it could be shown that Benaglia had a passion for hotels and that living in a hotel was worth much more to him (“consumer surplus”) than the price of a room. Would it then be justifiable to tax Benaglia on more than the established room rent?

4. Is difficulty of valuation a reason for omitting a noncash benefit from income entirely? Conversely, is ease of valuation a reason for taxation?

5. Does the fact that an item is supplied for the convenience of an employer, or other payor, bear significantly on the question of valuation or any other relevant question?

6. Does identity of payor impact the analysis?

16

Non-Employer Benefits; Gross Income Inclusion? Haverly p.51

Free textbook samples - Gross income? When samples received?

Why treat as income samples received only when deduction claimed for income tax?

Necessity for “symmetry” in the tax system?

Correct approach utilized here? Why not include in gross income when the books were received? A valuation dilemma?

Other possible argument?

17

§119 p.53

Requirements for §119 gross income exclusion eligibility:

1) Meal issue 2) Furnished issue 3) “Convenience of the employer” issue 4) “On the business premises”

How negotiate the manager’s employment contract (considering §119)?

18

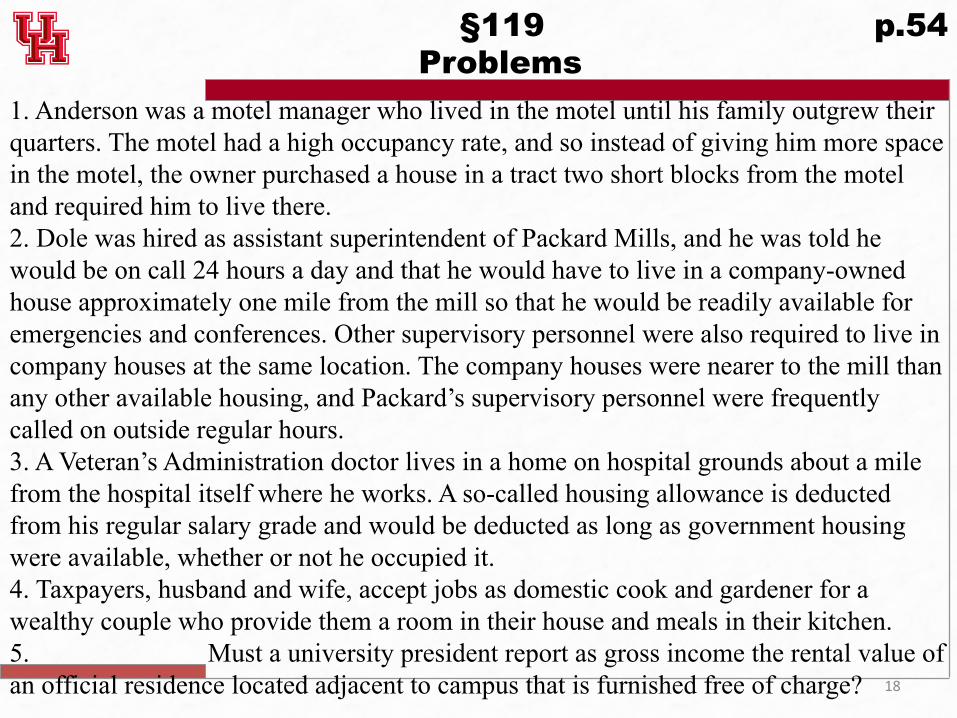

§119 p.54 Problems

1. Anderson was a motel manager who lived in the motel until his family outgrew their quarters. The motel had a high occupancy rate, and so instead of giving him more space in the motel, the owner purchased a house in a tract two short blocks from the motel and required him to live there. 2. Dole was hired as assistant superintendent of Packard Mills, and he was told he would be on call 24 hours a day and that he would have to live in a company-owned house approximately one mile from the mill so that he would be readily available for emergencies and conferences. Other supervisory personnel were also required to live in company houses at the same location. The company houses were nearer to the mill than any other available housing, and Packard’s supervisory personnel were frequently called on outside regular hours. 3. A Veteran’s Administration doctor lives in a home on hospital grounds about a mile from the hospital itself where he works. A so-called housing allowance is deducted from his regular salary grade and would be deducted as long as government housing were available, whether or not he occupied it. 4. Taxpayers, husband and wife, accept jobs as domestic cook and gardener for a wealthy couple who provide them a room in their house and meals in their kitchen. 5. Must a university president report as gross income the rental value of an official residence located adjacent to campus that is furnished free of charge?

19

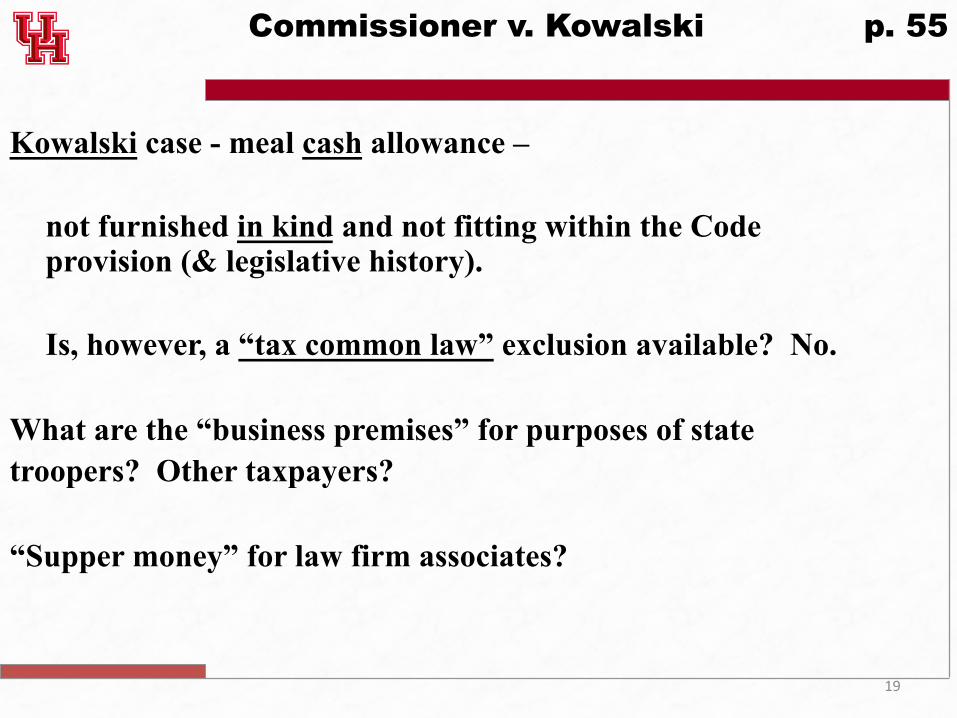

Commissioner v. Kowalski p. 55

Kowalski case - meal cash allowance –

not furnished in kind and not fitting within the Code provision (& legislative history).

Is, however, a “tax common law” exclusion available? No.

What are the “business premises” for purposes of state troopers? Other taxpayers? “Supper money” for law firm associates?

20

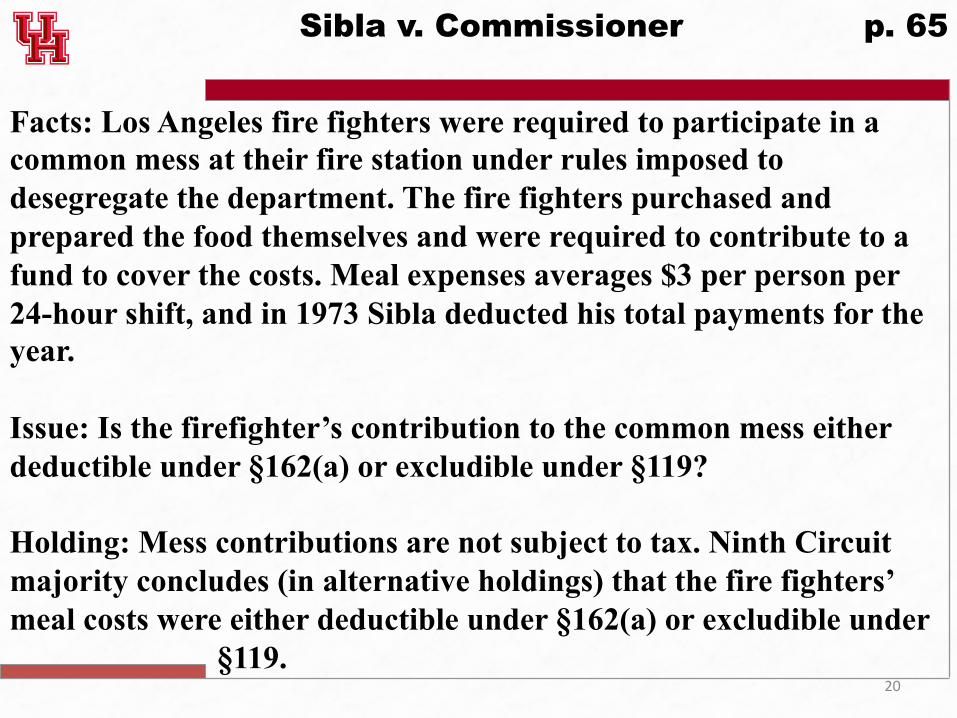

Sibla v. Commissioner p. 65

Facts: Los Angeles fire fighters were required to participate in a common mess at their fire station under rules imposed to desegregate the department. The fire fighters purchased and prepared the food themselves and were required to contribute to a fund to cover the costs. Meal expenses averages $3 per person per 24-hour shift, and in 1973 Sibla deducted his total payments for the year. Issue: Is the firefighter’s contribution to the common mess either deductible under §162(a) or excludible under §119? Holding: Mess contributions are not subject to tax. Ninth Circuit majority concludes (in alternative holdings) that the fire fighters’ meal costs were either deductible under §162(a) or excludible under

§119.

21

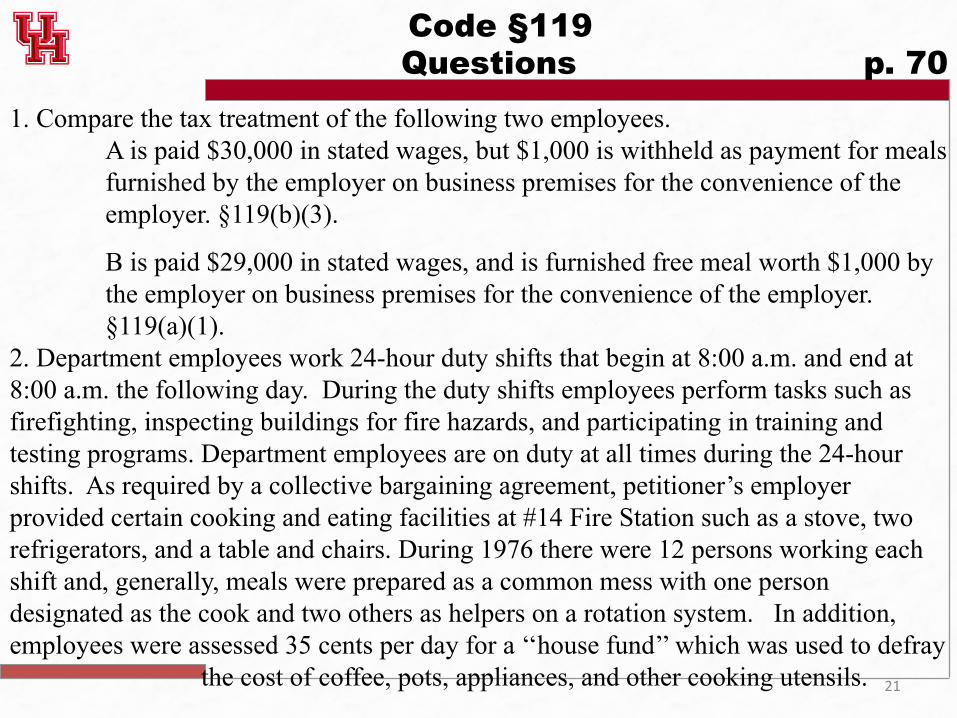

Code §119 Questions p. 70

1. Compare the tax treatment of the following two employees. A is paid $30,000 in stated wages, but $1,000 is withheld as payment for meals furnished by the employer on business premises for the convenience of the employer. §119(b)(3).

B is paid $29,000 in stated wages, and is furnished free meal worth $1,000 by the employer on business premises for the convenience of the employer. §119(a)(1).

2. Department employees work 24-hour duty shifts that begin at 8:00 a.m. and end at 8:00 a.m. the following day. During the duty shifts employees perform tasks such as firefighting, inspecting buildings for fire hazards, and participating in training and testing programs. Department employees are on duty at all times during the 24-hour shifts. As required by a collective bargaining agreement, petitioner’s employer provided certain cooking and eating facilities at #14 Fire Station such as a stove, two refrigerators, and a table and chairs. During 1976 there were 12 persons working each shift and, generally, meals were prepared as a common mess with one person designated as the cook and two others as helpers on a rotation system. In addition, employees were assessed 35 cents per day for a ‘‘house fund’’ which was used to defray

the cost of coffee, pots, appliances, and other cooking utensils.

22

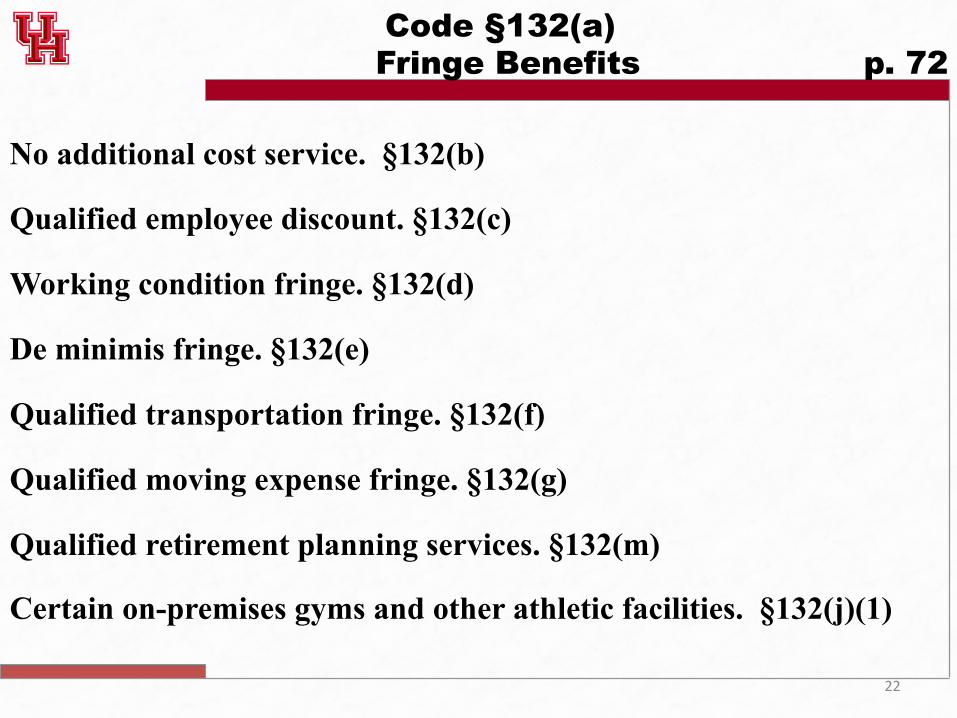

Code §132(a) Fringe Benefits p. 72

No additional cost service. §132(b)

Qualified employee discount. §132(c)

Working condition fringe. §132(d)

De minimis fringe. §132(e)

Qualified transportation fringe. §132(f)

Qualified moving expense fringe. §132(g)

Qualified retirement planning services. §132(m)

Certain on-premises gyms and other athletic facilities. §132(j)(1)

23

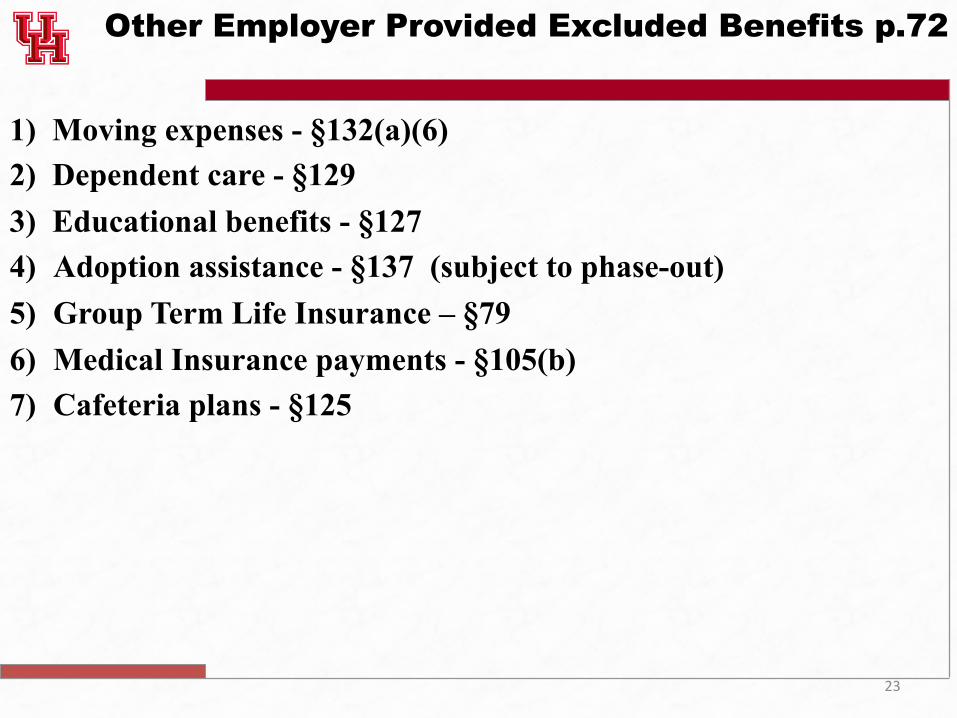

Other Employer Provided Excluded Benefits p.72

1) Moving expenses - §132(a)(6) 2) Dependent care - §129 3) Educational benefits - §127 4) Adoption assistance - §137 (subject to phase-out) 5) Group Term Life Insurance – §79 6) Medical Insurance payments - §105(b) 7) Cafeteria plans - §125

24

Questions p.76

1. Ford executive gets free car for both business and personal use. a) Is the personal use of the car income to employee? b) On audit, the revenue agent adds $6,000 to Derek’s gross income,

representing the value of the personal use of the Ford cars and asserts that only the exclusions from gross income set forth in the Code and regulations are allowable. Is this correct? See §61(a)(1).

c) If some amount is includible in Derek’s gross income, How is it determined?

2. Associate supper money. See §132(e)(1); §132(e)(2) & (f). 3. Employee Discounts 4. Employer provided cell phones and cell service so the employee can speak with

clients at times when the employee is away from the office, or if the employee’s job demands that she speak with clients located in other time zones at times outside of her normal work day. Employees are not prohibited from using employer-provided phones for personal purposes. Is any amount taxable? §132(d), (e); IRS Notice 2011-72, 2011-2 C.B. 407.

25

Treatment of Frequent Flyer Miles p.77 Problem 6

Inclusion in gross income? What if sale (or equivalent)? What if miles attributable to business travel and miles not credited to the employer? Why is the IRS not acting administratively on this issue? See Announcement 2002-18, 2002-1 C.B. 621.

26

Imputed Income p.77

1. Imputed Income from Self-Provided Services – imputed income from a self-created economic benefit?

2. Imputed Income from the Ownership of Consumer Assets – homes, vehicles & consumer durables? How value? Cost of consumer assets would not be deductible under a cash flow consumption tax.

3. General Psychic Benefits – the “happy life” as a gross income item. Value of leisure?

27

Imputed Income p.80 Rev. Rul. 79-24 (Supp. #29)

1. In return for legal services, housepainter paints the lawyer’s house.

2. Landlord receives work of art from painter in return for rent-free use of an apartment for six months.

3. Barter exchanges are required to be reported to the IRS. See §6045(c)(1)(B)

28

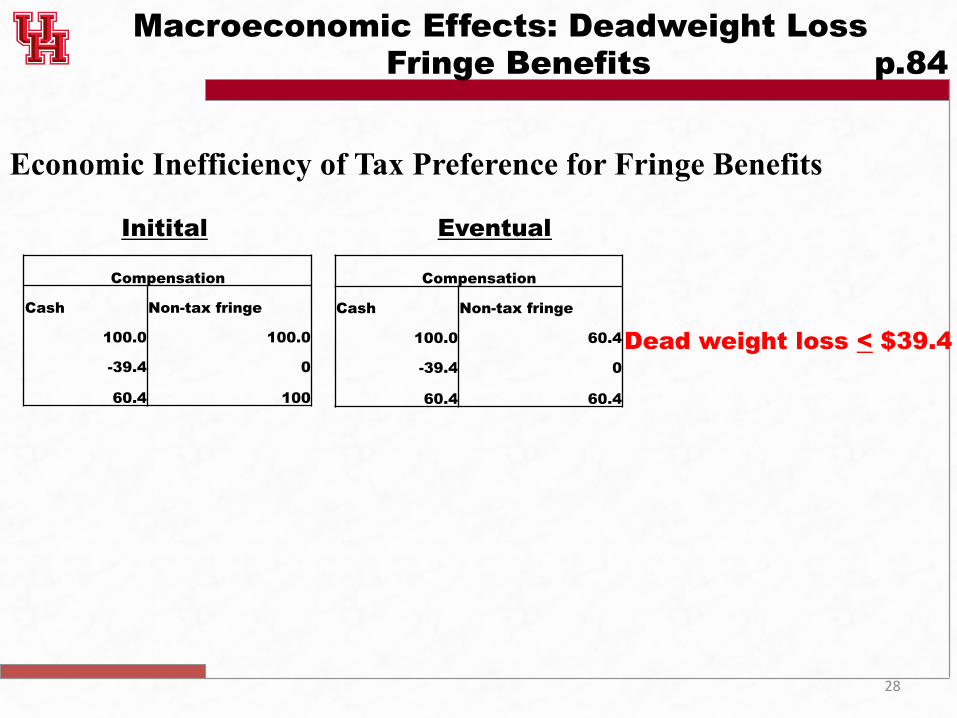

Macroeconomic Effects: Deadweight Loss Fringe Benefits p.84

Economic Inefficiency of Tax Preference for Fringe Benefits

Compensation

Cash Non-tax fringe

100.0 100.0

-39.4 0

60.4 100

Compensation

Cash Non-tax fringe

100.0 60.4

-39.4 0

60.4 60.4

Initital Eventual

Dead weight loss < $39.4

Related Documents