Presentation by R. S. (Shyam) Khemani Principal, MiCRA, Washington DC, USA and Consultant-Advisor, CUTS Jaipur/New Delhi, India Email contact: [email protected] IMPACT OF REGULATORY AND OTHER PUBLIC POLICIES ON COMPETITION IN THE ‘STAPLE FOOD’ SECTOR: EMERGING FINDINGS FROM THE CUTS-CREW PROJECT IN FOUR CONTRIES

Presentation by R. S. (Shyam) Khemani Principal, MiCRA, Washington DC, USA and Consultant-Advisor, CUTS Jaipur/New Delhi, India Email contact: [email protected].

Jan 01, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presentation by

R. S. (Shyam) KhemaniPrincipal, MiCRA, Washington DC, USA

andConsultant-Advisor, CUTS Jaipur/New Delhi,

IndiaEmail contact:

IMPACT OF REGULATORY AND OTHER PUBLIC POLICIES ON COMPETITION IN THE ‘STAPLE

FOOD’ SECTOR: EMERGING FINDINGS FROM THE CUTS-CREW PROJECT IN FOUR

CONTRIES

Topics To Be Covered

1. Role and Importance of Competition

2. Constraints to Competition: Public Policy & Private Business Restraints

3. Inter-face Between Economic Regulation & Competition Policies: Promoting Effective Competition

4. CREW Project: Sectors/Countries

5. Emerging Findings

6. Concluding Messages

Why Competition & Competition Policy Matter

• Why are we interested in competition? ‘Competition is absolutely essential at every stage of

economic development’ (Robert Solow, Commission on Growth and Development, May 2008)

• Role for Competition Policy ‘Strong competition policy is not just a luxury to be

enjoyed by rich countries, but a real necessity for those striving to create democratic market economies’ (Joseph Stiglitz, Nobel Prize Winner, August 2001)

COMPETITIVE PROCESS NOT AUTOMATIC NEEDS To Be: Safeguarded and Sustained

Competition can be distorted by public policies and restrictive business practices.

Public policy often manipulated by interest groups source of/entrench anticompetitive business practices and policies

Results in higher prices, lower/inefficient output, reduced choice and adversely affects consumer (and producer) welfare, investment……..

Adversely impacts especially on the common man/poorer segments of society…..

Major Source of Distortions

“The ‘really big’ distortions to competition are in poor countries”

Distortions to competition are not always obvious: “they have to

be dug out of each market”; “they are hard to find…(and)

significant forces gain from their existence”

(William Lewis, The Power of Productivity, 2004)

Why Sector Specific Competition Assessments?

Distinction between Systemic vs. Industry/Sector/Case Specific Impact

Regulatory reforms such as reducing/eliminating Tariffs & Non-Tariff Barriers to Trade; Restrictions on Ownership-Investment Generally Systemic Impact.

Enforcing Competition Law--case by case application Firm/Industry/Sector Impact.

Complementary Buttress each other Especially Competition Advocacy

Competition Law-Policy & Economic Regulation

Competition Law & Policy and Economic Regulation—Complementary or Antithetical?

Both deal with ‘Market Failures’ Effective ‘Competition Advocacy’ can foster

greater policy coherency and consistency Focus on measures-indicators that matter: Prices,

Output, Choice, Access to vital products/critical inputs, Consumer and Producer Welfare….

Focus on policies-regulations least interfere with markets

CREW: Competition Reforms in Key Markets for Enhancing Social-Economic

Welfare Project

Focus on Two ‘Key Sectors’ Across Four Countries

Sectors: (i)Passenger Bus Transportation and (ii) Staple Foods

Countries: Ghana (Maize), India (Wheat), Philippines (Rice) and Zambia (Maize)

Research Approach: Desk and Field Research (including interviews), ‘Perception’ Surveys……

KEY OBJECTIVES OF CREW-KEY SECTOR COMPETITION DIAGNOSTIC

COUNTRY REPORTS(DCR) Analyze & evaluate existing sector specific

regulatory & economic policies in terms of impact on competition, social and economic welfare

Identify gaps/distortions/areas where benefits of competition can be strengthened and improved

Build broad based support/informed discussion for increased competition benefits through regulatory-economic policy reforms

Recommend & chart appropriate course of action; monitor, evaluate and report outcomes

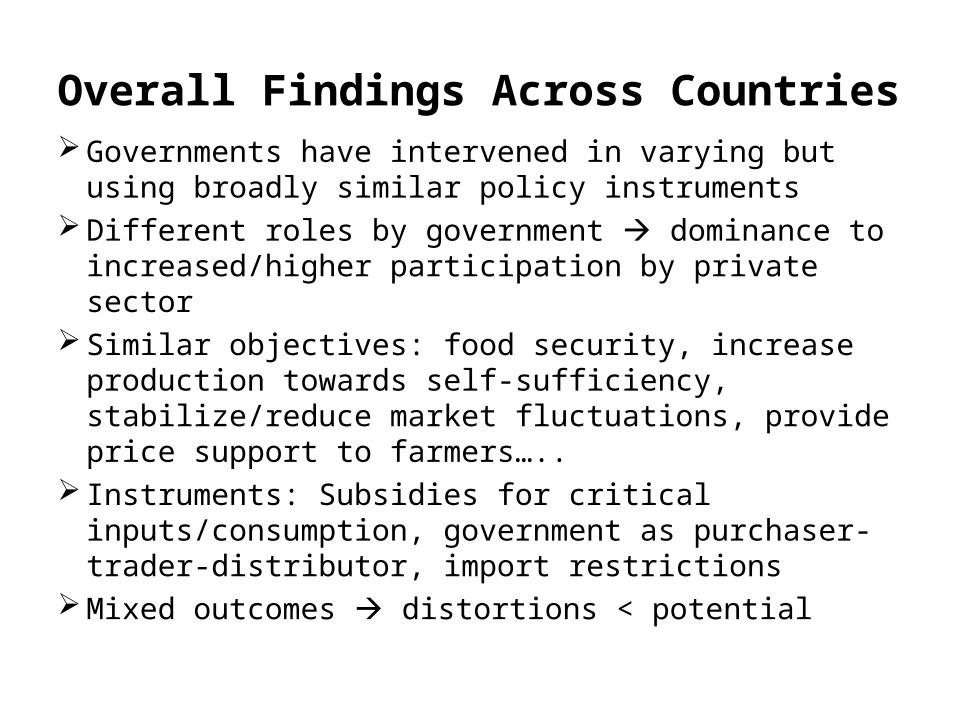

Overall Findings Across Countries Governments have intervened in varying but using

broadly similar policy instruments Different roles by government dominance to

increased/higher participation by private sector Similar objectives: food security, increase production

towards self-sufficiency, stabilize/reduce market fluctuations, provide price support to farmers…..

Instruments: Subsidies for critical inputs/consumption, government as purchaser-trader-distributor, import restrictions

Mixed outcomes distortions < potential

EMERGING FINDINGS--INDIA

Wheat: Farm Gate to Marketing: Bihar & Rajasthan. Average annual consumption 53Kg per capita

Supply chain analysis: India-Typically 9 Intermediaries; US 2-3 Intermediaries

Long supply chain Increased costs: Mark-ups India 135% vs. US 9% Wastage: India 8-10%

Critical inputs: Fertilizer & Seed Government dominance-subsidization in

Fertilizer: Distortionary effects

EMERGING FINDINGS—INDIA—Contd.

Fertilizer Subsidization Non-optimal usage; productivity stagnant; adverse impact on investment and production Import dependence

Seed: Liberalization; Entry Hybrid seeds (high profits); small farmers reliance on own crops

Between 1966-2005: 19 Laws/Amendments/Regulatory-Economic Policy changes…..re: seed uncertainty

While Barriers to Entry lowered, Low inter-firm competition : Benefits to skewed towards large farmers

EMERGING FINDINGS—INDIA—Contd.

Marketing-Procurement-Warehousing-Distribution: various policies & public sector Institutions

Objectives: Provide price support & Reduce Price Fluctuations & Increased Food Security

Agricultural Products Marketing Committee (APMC) Foster Investment….

Agricultural Pricing Policy (APP) Price Support Food Corporation of India (FCI) Warehousing Public Distribution System (PDS) Distribution

Outlets….

Emerging Recommendations--India Agricultural policies primarily State Government

level wide variation in outcomes point to need for policy harmonization, re-vamping, improved implementation.

Production: Fertilizer Concerted action to improve ‘enabling environment’ Removal of price controls over inputs (natural gas) & outputs (urea): low-prices low public & private investment….

Production: Seed liberalization private entry, vibrant competition BUT public sector focused on main seeds, private sector on hybrids higher profits

Emerging Recommendations—India—Contd.

PPP Bihar highly successful similar approach need to be disseminated/adopted in Rajasthan & beyond…

Marketing: APMC—Divergent experiences Rajasthan contract farming, direct marketing low private participation

Bihar repealed APMC no regulatory oversight no improved competition, low public and private investment…..point to need for multi-pronged, harmonized multi-level approach….

Emerging Recommendations—India—Contd.

Marketing: APP: Procurement extensively bu public sector agencies limited presence in rural areas MSP benefits larger farmers small farmers confront market access problems

Distortions: Stock piling-surplus > required quantity increase in wholesale & retail prices

Need to promote private participation, increased cross-agency competition, entry through ‘bidding’ for marketing rights….

Emerging Recommendations—India—Contd.

Warehousing: Overall private participation low 17% national capacity.

Unattractive: Require comprehensive reforms re: availability of land, credit and taxation….

Distribution: Targeted Public Distribution System (TDPS) performance-implementation issues leakages to wrong beneficiaries, pilferage, financial non-viability….

Fair price shops policy local monopolies

Emerging Recommendations—India—Contd.

India ‘staple food’ situation indicative of extensive distortions induced by plethora of cumulated ill-designed and poorly implemented policies and regulations coupled with heavily bureaucratic procedures and inept public sector participation that has failed to levarage competition and private sector participation.

Requires massive over-haul.

EMERGING FINDINGS—Philippines

Rice: Paddy field to retail marketing: Metro Manila & Central Luzon. Average annual per capita consumption 114 Kg

Supply chain analysis: Significant competition at each stage. Mark-ups low 2-5% at different levels

Entry easy, licensing, registration etc. do not pose major barriers

National Food Authority (NFA) interventionist regulator with wide-ranging powers

Monopoly over imports

EMERGING FINDINGS--Philippines-Contd.

Many marginal producers & tradersDomestic production & yields

increased<consumption rice importedAs trader NFA does not significantly,

directly influences prices BUTAs monopoly importer insufficient

competition at import levelDomestic prices>International prices

EMERGING FINDINGS--Philippines-Contd.

Import liberalization 10 fold increase in imports (Good or Bad? Food security, adverse impact on small farmers….)

WTO ascension trade liberalization measures adopted –rice sector: special treatment

Rice prices would decrease 6-7%; Aggregate consumer surplus would increase > reduction in producer surplus Net benefit to economy

Key Recommendation: Rice: Philippines

Government needs to reconsider its rice import policy re: quotas and tariffs.

Reduce/eliminate import quotas, increase private sector participation in imports

Move towards full WTO agreement/trade liberalization re: rice

Emerging Findings--Ghana

Maize: Per capita consumption 44 Kg per annum; Preferred food staple, however 4th largest crop (value terms)

Focus on Brong Ahafo and Ashanti Regions—among primary maize producers

Cultivation mainly by small resource poor rain-fed farmers (2 million)

85% supply consumption (white maize), 15% for poultry and other uses (yellow maize-mainly imports)

Gradual increase in production/yield < potential

Emerging Findings—Ghana—Contd.

Until 1990s lack of comprehensive policy framework Adoption of pro-market-private sector reforms including agriculture: Medium Term Agricultural Development Program (MTADP) pricing-supply liberalization of seed & fertilizer

Various other policies-institutions re: agricultural diversification, sector adjustment credits, price stabilization, supply of critical inputs, R&D-productivity programs, food security among others.

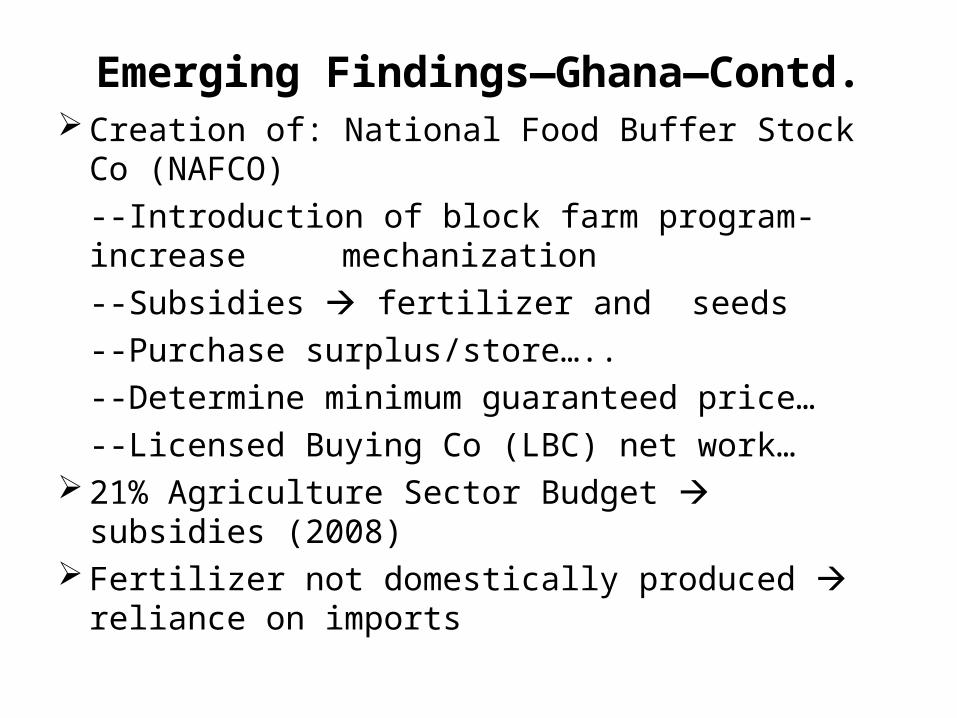

Emerging Findings—Ghana—Contd. Creation of: National Food Buffer Stock Co

(NAFCO)

--Introduction of block farm program-increase mechanization

--Subsidies fertilizer and seeds

--Purchase surplus/store…..

--Determine minimum guaranteed price…

--Licensed Buying Co (LBC) net work… 21% Agriculture Sector Budget subsidies (2008) Fertilizer not domestically produced reliance on

imports

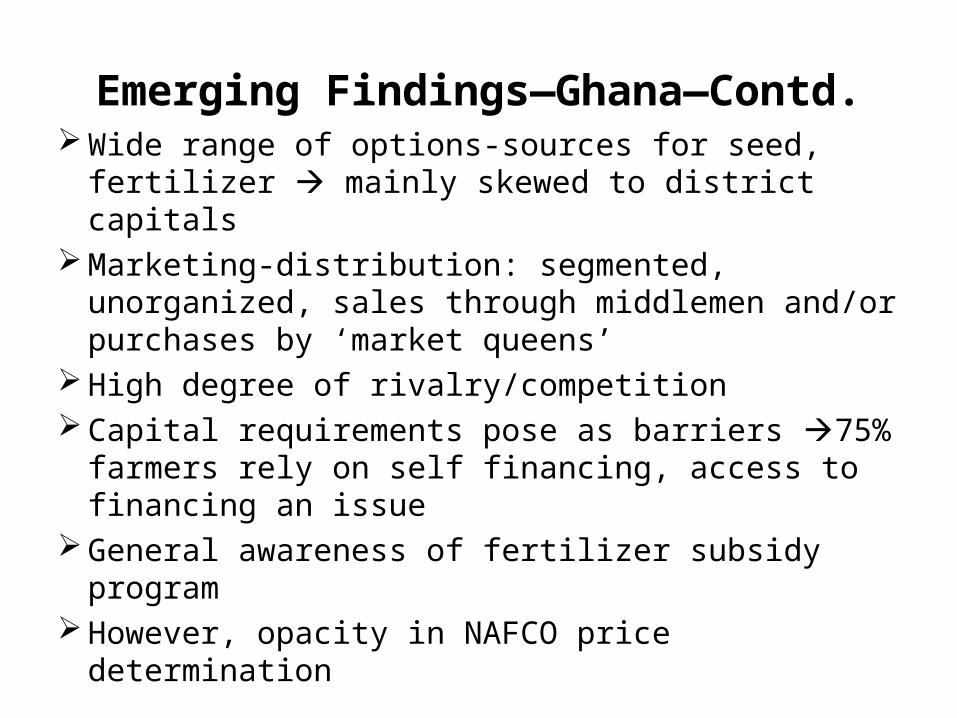

Emerging Findings—Ghana—Contd. Wide range of options-sources for seed, fertilizer

mainly skewed to district capitals Marketing-distribution: segmented, unorganized,

sales through middlemen and/or purchases by ‘market queens’

High degree of rivalry/competition Capital requirements pose as barriers 75%

farmers rely on self financing, access to financing an issue

General awareness of fertilizer subsidy program However, opacity in NAFCO price determination

Key Recommendations--Ghana

Government needs to facilitate distribution of subsidized fertilizer, expand low interest credit financing to farmers especially in rural areas

Improve infrastructure (transport-warehousing) to increase market access

70% farmers without access to warehouse storage, 50% farmers indicate problems re: availability of seed

Key Recommendations—Ghana--Contd

Increase communications/awareness of various support policies, especially determination of minimum guaranteed prices—84% unaware of government support price, 89% how its established

Engage with NGO’s, civil society, other public-private sector entities to achieve these goals

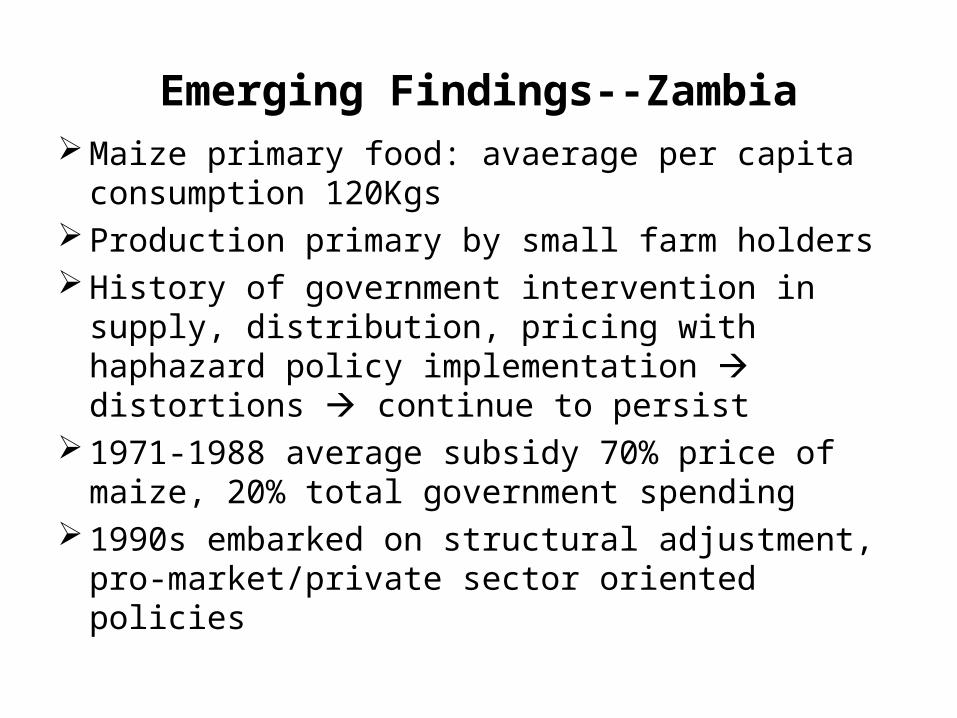

Emerging Findings--Zambia Maize primary food: avaerage per capita

consumption 120Kgs Production primary by small farm holders History of government intervention in supply,

distribution, pricing with haphazard policy implementation distortions continue to persist

1971-1988 average subsidy 70% price of maize, 20% total government spending

1990s embarked on structural adjustment, pro-market/private sector oriented policies

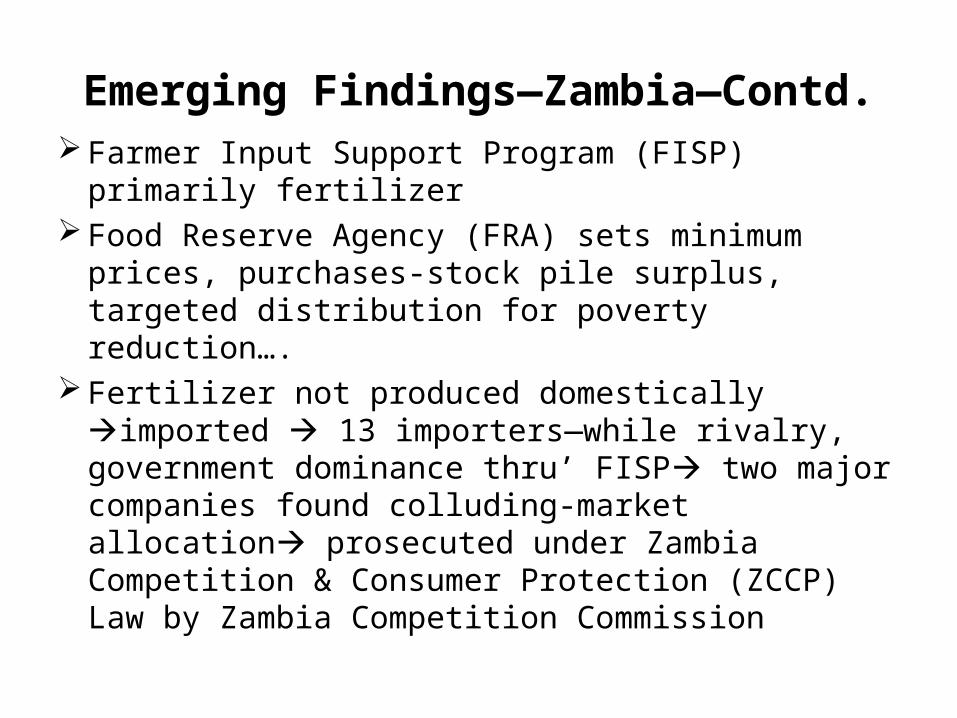

Emerging Findings—Zambia—Contd. Farmer Input Support Program (FISP) primarily

fertilizer Food Reserve Agency (FRA) sets minimum

prices, purchases-stock pile surplus, targeted distribution for poverty reduction….

Fertilizer not produced domestically imported 13 importers—while rivalry, government dominance thru’ FISP two major companies found colluding-market allocation prosecuted under Zambia Competition & Consumer Protection (ZCCP) Law by Zambia Competition Commission

Emerging Findings—Zambia—Contd.

Under FISP, government dominant importer of fertilizer (66-80%) sets prices, subsidy level, allocates supply thru’ bidding, allegations of irregularities dominated by two companies, found violating ZCCP law

Nitrogen Company of Zambia (NCZ), a SOE, inefficient, allocated imported fertilizer for blending crowding out private participation…

FRA dominant purchaser of maize (26-86%), with purchase price> free market equilibriumcrowds out private firms, stifling competition

Emerging Findings--Zambia 30-40 Millers significant competition tho’ new

entrants face BTEs in form of capital requirements, economies of scale, market fluctuations, excess capacity…..

Traders dominated by 4 major companies w/40%+ market shares, potential exercise of market power

Different views re: subsidies and impact on production (skewed towards larger farmers), prices (lead to higher costs, prices)…

Overall policies viewed to reduce competition, increased business uncertainty, adverse effects on investment…

Emerging Recommendations--Zambia

Emerging findings suggest unfinished agenda re: agricultural policy framework, especially for maize

Need to re-vise/re-vamp subsidy programs and role and functioning of government entities e.g. NCZ, FISP, FRA in markets

Address allegations re: irregularities in bidding processes, distribution of critical inputs to rural areas, determination of minimum support prices…..

Concluding Remarks

Draft DCRs represent ‘work-in-progress’ Different countries have adopted similar approaches

re: provision of critical inputs, minimum support prices, creating government agencies to purchase and stock-pile supplies, stabilize prices and other objectives such as security and availability of staple foods

Differences in policies/regulations also exist with different outcomes

History of past government interventions and some existing policies-regulations persist in distorting markets

Concluding Remarks—Contd.

In all 4 countries, role of private sector and pro-competition/pro-market measures have been ‘ham-strung’

Point to un-tapped opportunities for increasing affordability, competitive supply and access to staple foods and poverty alleviation

A course of formulating and advocating alternative policy approaches and possible actions is required The Next Step in the DCRs

Thank You

Related Documents