From Basel I to Basel III and beyond – state of the play DKF 2014 Dorothea Schäfer Munich, April 1, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

From Basel I to Basel III and beyond – state of the play

DKF 2014

Dorothea Schäfer

Munich, April 1, 2014

1 Basel I

2 Basel II and risk weighting

3 Basel III: state of the play and assessment

4 Beyond

Overview

Dorothea Schäfer From Basel I to Basel III

Basel I

1

3

Basel I

Initiation: Herstatt bankruptcy 1974

Publication of new rules 1988, Implementation: 1992,

Minimum capital requirement = amount of credit x 8 % x percentage

weight of risk class

Risk classes and percentage weights: no discredition for banks

• 0 % for sovereign bonds of OECD-countries (zero!)

• 20% for interbank credits (1 million) within OECD countries (16 000)

• 50% for collateralized real estate credits (40 000)

• 100% for other credit engagement including loans to corporations (80000)

Important elements

1

From Basel I to Basel III Dorothea Schäfer 4

Basel I

1. Common equity capital and retained earnings (core (Tier 1) capital)

2. Additional internal and external resources of the bank

(supplementary capital, long-term liabilities, specific provisions)

Tier 1 capital: core Tier 1 capital plus other instruments, e.g. non-

redeemable non-cumulative preferred stock

Loss taking: Common equity capital and retained earnings

Weird: other instruments than loss taking instruments qualify as bank

capital

Definition of capital within Basel I

1

From Basel I to Basel III Dorothea Schäfer 5

Basel I

• Only four risk categories

• Independency of risk weights of borrower‘s solvency

and liquidity

• Cross-subsidization of loans and credits (good

borrowers subsidize bad borrowers)

Main critique of Basel I

1

From Basel I to Basel III Dorothea Schäfer 6

Basel II

2

Dorothea Schäfer 7 From Basel I to Basel III

Basel II

2004: publication of Basel II framework

2007: implementation

Main elements

1. Basically no change in definition of capital

2. Introduction of individual risk weights

1. Ratings (ECAI External Credit Assessment Institution, e.g S&P, Moody’s,

Fitsch)[standard approach]

2. Own calculations (bank itself assesses risk)[IRB approach]

3. Calculation of a bank’s required capital

Basic Overview

2

From Basel I to Basel III Dorothea Schäfer 8

capital x 100 % ≥ 8 % (minimum capital ratio)

credit risk + 12.5 (market risk + operational risk)

Basel II

Calculation of Risk weights: standard approach

1

From Basel I to Basel III Dorothea Schäfer 9

Credit exposure to

Rating classes (coming from ECAI)

AAA A+ BBB+ BB+ B+ Below Without

to to to to to B- Rating

AA- A- BBB- BB- B-

Sovereign states/central banks (Lex EU)

0% 20% 50% 100% 150% 100%

Banks (option 1-3): according to the rating of the home state (option 1)

20% 50% 100% 150% 100%

Corporations/non-banks

20% 50% 100% 150% 100%

Asset Backed Securities

20% 50% 100% 350%

1.250 % (deductio

n from core

capital)

Basel II

“The European CRDs have introduced […] a risk weight of 0% for

“exposures to Member States’ central government […].

[…] instead of confining the zero risk weight to the standardised

approach, (the CRDs) permit a generalised zero risk weight through the

so-called “IRB permanent partial use” rules”

IRB permanent partial use: IRB in general except for sovereign debt. (Speech of Hervé Hannoun, Deputy General Manager Bank for International Settlements, at Financial

Stability Institute High-Level Meeting Abu Dhabi, UAE, 26 October 2011 )

EU CRDs: Exposure to sovereign EU member states

2

From Basel I to Basel III Dorothea Schäfer 10

Basel II

Amount of credit (in million Euro)

Risk weight (%)

Minimum capital ratio (%)

Mimimum capital

Leverage ratio

Leverage

2 5% 8% 8000 0,40% 250

50% 8% 80000 4,00% 25

Example for the calculation of minimum

capital

1

From Basel I to Basel III Dorothea Schäfer 11

Risk weight IRB approach: RW(LGD, PD, M)

Basel II

Incentives

2

Dorothea Schäfer 12

From Basel I to Basel III

1. Investing in the zero risk weight debt of EU member

states

2. Minimum risk assessment with own models

3. Investing in highly rated securities (e.g super senior

tranches of US subprime CDOs)

4. Installing off-balance sheet vehicles with no capital

requirements (continues from Basel I, no

counterbalancing regulation present)

Basel II

Consequence

2

Dorothea Schäfer 13

From Basel I to Basel III

1. Growing of total assets without additional capital

2. Bank got bigger and bigger

3. Excessive leverage and extremely low leverage

ratios

4. Expansion of off-balance sheet vehicles

Basel II

Basis for such incentives

Leverage effet in combination with bonuses which are linked to the return

on equity

2

From Basel I to Basel III Dorothea Schäfer 14

return return on equity

return on assets

interest rate

debt/equity

If equity capital is fixed more debt brings the bank managers in the desired direction

Basel II

Trends in banking after introduction of risk

weighting

Leverage (multiple of equity capital) and ratio of risk-

weighted and total assets of the four largest banks in UK

2

From Basel I to Basel III Dorothea Schäfer 15

30

35

40

45

50

55

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008

Hebel (100 Prozent/Leverage Ratioin Prozent) (linke Skala)

risikogewichteteAktiva/Bilanzsumme in Prozent(rechte Skala)

Leverage (left-hand axis)

Risk-weighted assets to total assets (right-hand axis) in %

Basel II

Acceleration of a ongoing trend? Leverage Ratio of

Deutsche Bank (1870-1914)

2

From Basel I to Basel III Dorothea Schäfer 16

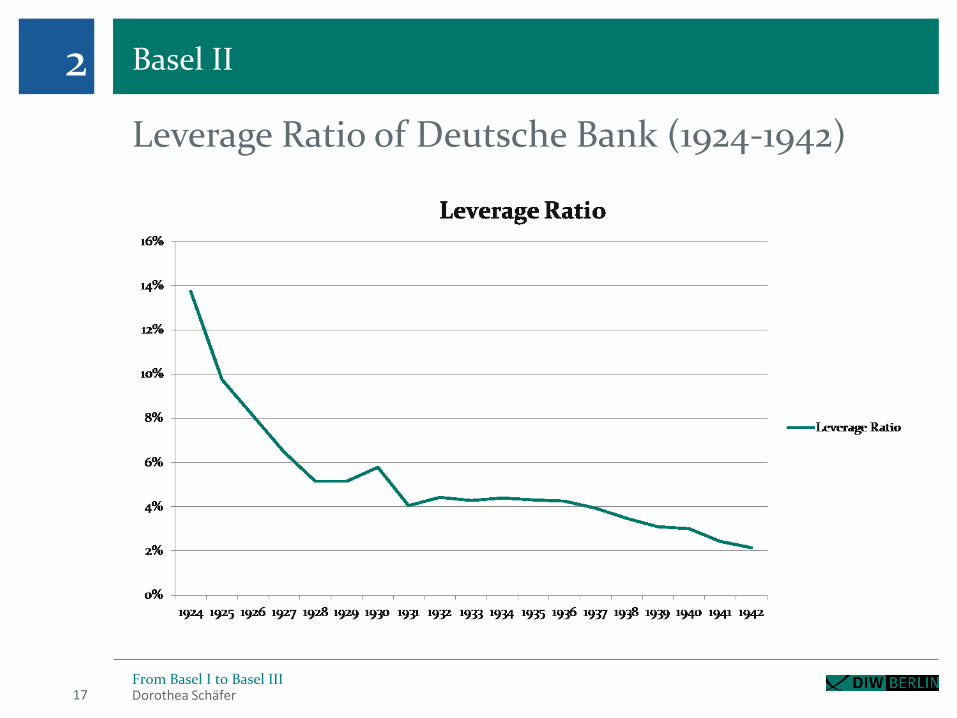

Basel II

Leverage Ratio of Deutsche Bank (1924-1942)

2

From Basel I to Basel III Dorothea Schäfer 17

Basel II

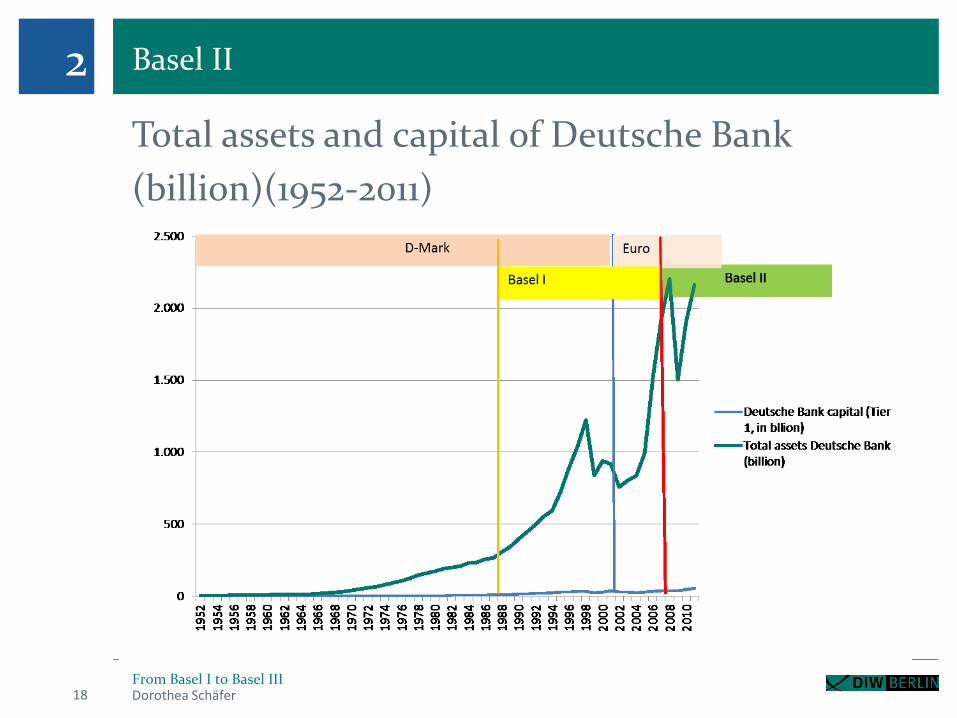

Total assets and capital of Deutsche Bank

(billion)(1952-2011)

2

From Basel I to Basel III Dorothea Schäfer 18

Basel II

Leverage Ratio of Deutsche Bank (1952-2011)

2

From Basel I to Basel III Dorothea Schäfer 19

Trend till 2019?

Basel II

More anectotic evidence: the Swedish real estate case

2

Dorothea Schäfer 20

When the Basel 2 accord came into effect in Sweden in 2007, Sweden’s

largest mortgage lenders were authorized by FI to use internal models to

calculate the risk weights in their credit exposures. The result of the

introduction of the models was that risk weights for Swedish mortgages

dropped sharply, and many of the largest players now have average risk

weights down at around 5 per cent for these exposures. This can be

compared to risk weights of 50 per cent in the regulations applicable until

2007 – the Basel 1.” (Finansinspektionen – Memorandum Nov 26, 2012)

From Basel I to Basel III

Basel II

More anectotic evidence: the Swedish real estate case

2

Dorothea Schäfer 21

When the Basel 2 accord came into effect in Sweden in 2007, Sweden’s

largest mortgage lenders were authorized by FI to use internal models to

calculate the risk weights in their credit exposures. The result of the

introduction of the models was that risk weights for Swedish mortgages

dropped sharply, and many of the largest players now have average risk

weights down at around 5 per cent for these exposures. This can be

compared to risk weights of 50 per cent in the regulations applicable until

2007 – the Basel 1.” (Finansinspektionen – Memorandum Nov 26, 2012)

From Basel I to Basel III

Basel II

Summer stress test of EBA in 2011

Starke Hebelung der Bankbilanzen großer Banken

2

From Basel I to Basel III Dorothea Schäfer 22

10 largest German banks (in million Euro)

Source: DIW Berlin, own calculations on the basis of published stress test data.

Leverage Ratio in %

If a leverage ratio of 5% is required Cap required(left)/additional cap needed right (million Euro)

Basel II

Ongoing: high leverage in banks‘ balance sheets

2

From Basel I to Basel III Dorothea Schäfer 23

IMF Financial Stability Report 2012

Basel II

The zero risk weight approach for EU member states fires

back

2

Dorothea Schäfer 24

From Basel I to Basel III

Dramatic loss of value of large proportion of EU-banks‘ assets because of downgrading Investors lost confidence in solvency of banks (and of states)

AAA

AA

A

BBB

BB

B

CCC

CC

C

SD

01.01.2009 16.05.2010 28.09.2011 09.02.2013

Rating steps 01.01.2009 - 01.09.2013

Greece Ireland Italy Portugal Spain

Source: Christopher F. Baum & Margarita Karpava & Dorothea Schäfer & Andreas Stephan, 2013. "Credit Rating Agency Downgrades and the Eurozone Sovereign Debt Crises," Boston College Working Papers in Economics 841,

From Basel I to Basel III Dorothea Schäfer 25

-500

0

500

1000

1500

2000

2500

3000

3500

4000Spreads Sovereign Bonds 2000 – 2014: losses in value until

summer 2012

Frankreich

Italien

Portugal

Irland

Griechenland

Spanien

Hans-Helmut Kotz und Dorothea Schäfer (2014), Rating-Agenturen: Fehlbar und überfordert. In: Schäfer D, Semmler W. and Young B. (Ed.), Nachhaltige Europäische Konsolidierungspolitik

Basel II

Conclusion for Basel II

2

From Basel I to Basel III Dorothea Schäfer 26

Risk weights in Basel II • have enabled banks to get larger and larger without increasing the amount of

loss-absorbing equity capital, • made banks more vulnerable, • have contributed to the European financial crisis

• because of the short distance of many large European banks to default and

• the therefore high probability that sovereign EU/Euro member states have to accumulate more debt in order to help their banks

In addition: lobby groups use risk weights to fight for lower ones (e.g. sme loans, real estate loans, energy investments). This may decrease credit costs on the micro level but decreases stability on the macro level (race to the bottom)

Basel III

Is it the answer to these problems?

3

Dorothea Schäfer 27 From Basel I to Basel III

Basel III

Important elements

3

From Basel I to Basel III Dorothea Schäfer 28

• Narrower definition of eligible capital (focus: loss absorption)

• Increase of capital requirements

• Banks in general

• Global systemically (Sifis), domestic systemically important

financial institutions

• Leverage ratio

Still dominant: risk weighting is basis for capital requirements

Struggle with US about role of rating agencies

Basel III

Important elements

3

From Basel I to Basel III Dorothea Schäfer 29

• Liquidity coverage ratio and net stable funding ratio

• Liquidity for 30 day of stress (recently postponed 2015 to

2019)

• NSFR: fighting of maturity mismatch (goal: liquid for one

year)

• Payment rules (bonus systems)

(CRD IV: EUP and EUC struggle)

Basel III

Capital requirements

3

From Basel I to Basel III Dorothea Schäfer 30

• Core capital (Common equity and retained earnings)

• Banks in general (7 %, including max. CCB: 9.5 %)

• from 2% to 4.5%

• capital conservation buffer: 2.5 % (supervisory authorities impose

constraints)

• Counter cylical buffer (CCB) from 0 to 2.5 %

• Sifis: on top between 1% and 2.5 % (depends on

importance) + 1% in addition for the highest class Sifis (in

discussion)

Reminder: Tier 1 capital ratio of German banks 11.9 % (IMF)

Basel III

Capital requirements

3

From Basel I to Basel III Dorothea Schäfer 31

CRD IV: EUP and EUC struggle about eligibility of additional

buffers (Sweden, UK)

EUP: fear of competitive advantage for buffer countries

Weird because for years lower capital requirements than the

“strong Basel II” rules were labelled as competitive advantage

(e.g. German banks complained a lot about US bank not

following the Basel II rules)

Basel III

Capital requirements

3

From Basel I to Basel III Dorothea Schäfer 32

Leverage ratio : 3 percent in 2019

• Too low for large banks

it implies a leverage of 33 x the required capital,

no constraint for the growth in size (no constraint for mh)

• Required capital is broader defined than the core capital,

therefore: required core leverage ratio is actually lower

• Too late

• Not exactly clear: mandatory or only ratio for observation

Basel III

Final remark

3

From Basel I to Basel III Dorothea Schäfer 33

Basel III is not the answer to the identified problems

• It does not effectively constrain the leveraged growth model

of banks

• It does not effectively constrain the banks’ discretion about

the risk weighting and the capital requirements

• It does not effectively remove the management’s incentive

to build on the leveraged growth model

• Limitation of the moral hazard (mh) problem of Sifis: highly

questionable

Vielen Dank für Ihre Aufmerksamkeit.

DIW Berlin — Deutsches Institut

für Wirtschaftsforschung e.V.

Mohrenstraße 58, 10117 Berlin

www.diw.de

Thanks for your attention

Related Documents