LFA Training Finance Clinic EFR & Budget efficiencies: The LFA role Geneva, Switzerland – February 2009 Program Finance

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LFA Training Finance Clinic EFR & Budget efficiencies: The LFA role

Geneva, Switzerland – February 2009Program Finance

Agenda

• What is it and Why do it?

• Some complications

• LFA role

• Examples

What is Enhanced Financial Reporting (EFR)?

• An additional annual financial reporting form (+ phase 2)

• A basic budget vs expenditure variance analysis

• Shows costs broken down by cost categories, SDA and implementing entities

Why is the Global Fund requesting Enhanced Financial Reporting?

• Improving Performance Based Funding and Grant Management

• Increased Transparency and Accountability

• Responding to Requests from Board, Donors and Stakeholders

• Improving Value For Money Analysis

• Leveraging Additional Financial Resources

Potential Challenges of EFR

• Can expenditure be tracked against budget in these categories, especially by service delivery area (SDA)?

• Ensuring Sub Recipients provide accurate and timely financial information

• Obtaining cumulative information for oIder grants

The Role of the LFA

Expected to perform a review NOT a verification

1. Has the template been fully completed?

2. Comment on the PRs approach to completing the template including reasonableness of the assumptions

3. Comment on the variance analysis provided by the PR.

Which expenditures?

Expenditure reported

=

PR direct expenditureDisbursements to SRs should not be

considered as expenditure

+

SRs expenditureDisbursements to S-SRs should not be

considered as expenditure

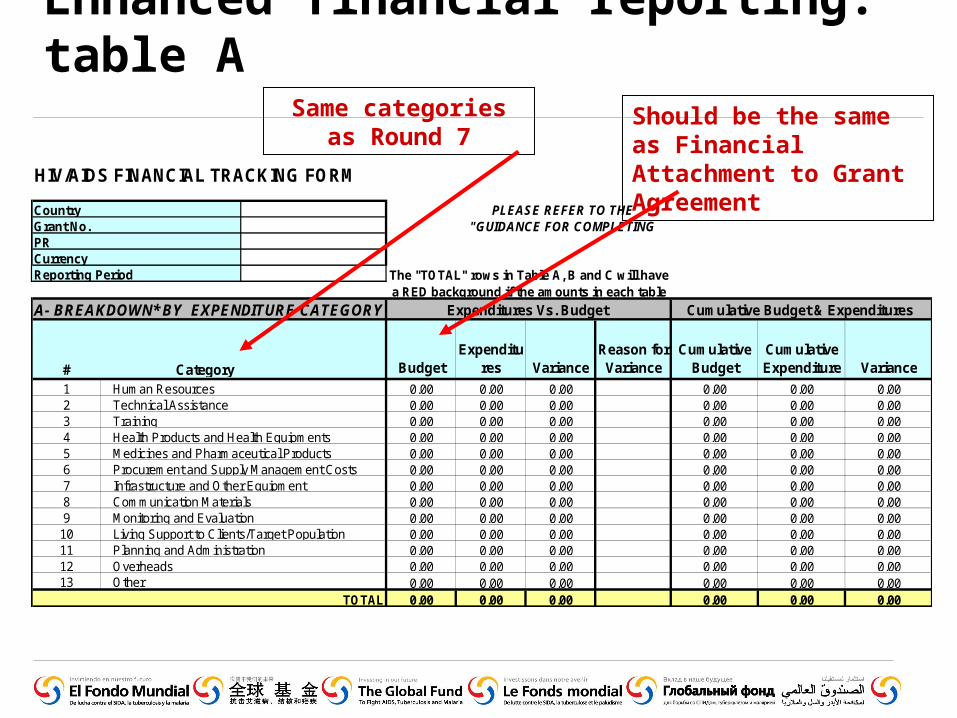

Enhanced financial reporting: table A

A- BREAKDOWN* BY EXPENDITURE CATEGORY

#

Budget

Expenditures Variance

Reason for Variance

Cumulative Budget

Cumulative Expenditure Variance

1 0.00 0.00 0.00 0.00 0.00 0.002 0.00 0.00 0.00 0.00 0.00 0.003 0.00 0.00 0.00 0.00 0.00 0.004 0.00 0.00 0.00 0.00 0.00 0.005 0.00 0.00 0.00 0.00 0.00 0.006 0.00 0.00 0.00 0.00 0.00 0.007 0.00 0.00 0.00 0.00 0.00 0.008 0.00 0.00 0.00 0.00 0.00 0.009 0.00 0.00 0.00 0.00 0.00 0.0010 0.00 0.00 0.00 0.00 0.00 0.0011 0.00 0.00 0.00 0.00 0.00 0.0012 0.00 0.00 0.00 0.00 0.00 0.0013 0.00 0.00 0.00 0.00 0.00 0.00

TOTAL 0.00 0.00 0.00 0.00 0.00 0.00

Category

Other

Grant No.

The "TOTAL" rows in Table A, B and C will have a RED background if the amounts in each table

Living Support to Clients/Target PopulationPlanning and AdministrationOverheads

HIV/AIDS FINANCIAL TRACKING FORM

Expenditures Vs. Budget

PRCurrency

Country PLEASE REFER TO THE "GUIDANCE FOR COMPLETING

Reporting Period

Human ResourcesTechnical AssistanceTrainingHealth Products and Health EquipmentsMedicines and Pharmaceutical ProductsProcurement and Supply Management CostsInfrastructure and Other EquipmentCommunication MaterialsMonitoring and Evaluation

Cumulative Budget & Expenditures

Same categories as Round 7

Should be the same as Financial Attachment to Grant Agreement

Enhanced financial reporting: table B

B- BREAKDOWN* BY PROGRAM ACTIVITY

# Macro-category Objectives

Service Delivery

Area

BudgetExpenditu

res VarianceReason for Variance

Cumulative Budget

Cumulative Expenditure Variance

1 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.002 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.003 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.004 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.005 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.006 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.00… Please Select…

Please Select… 0.00 0.00 0.00 0.00 0.00 0.00

TOTAL 0.00 0.00 0.00 0.00 0.00 0.00

C- BREAKDOWN* BY IMPLEMENTING ENTITY

# PR/SR Name

Type ofImplementing Entity

Budget

Expenditures Variance

Reason for Variance

Cumulative Budget

Cumulative Expenditure Variance

1 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.002 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.003 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.004 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.005 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.00… Please Select …

Please Select … 0.00 0.00 0.00 0.00 0.00 0.00

TOTAL 0.00 0.00 0.00 0.00 0.00 0.00

Expenditures Vs. Budget

Expenditures Vs. Budget

Cumulative Budget & Expenditures

Cumulative Budget & Expenditures

Totals should be same for all 3 tablesDrop down lists

Enhanced financial reporting: table C

B- BREAKDOWN* BY PROGRAM ACTIVITY

# Macro-category Objectives

Service Delivery

Area

BudgetExpenditu

res VarianceReason for Variance

Cumulative Budget

Cumulative Expenditure Variance

1 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.002 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.003 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.004 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.005 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.006 Please Select… Please 0.00 0.00 0.00 0.00 0.00 0.00… Please Select…

Please Select… 0.00 0.00 0.00 0.00 0.00 0.00

TOTAL 0.00 0.00 0.00 0.00 0.00 0.00

C- BREAKDOWN* BY IMPLEMENTING ENTITY

# PR/SR Name

Type ofImplementing Entity

Budget

Expenditures Variance

Reason for Variance

Cumulative Budget

Cumulative Expenditure Variance

1 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.002 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.003 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.004 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.005 Please Select … Please 0.00 0.00 0.00 0.00 0.00 0.00… Please Select …

Please Select … 0.00 0.00 0.00 0.00 0.00 0.00

TOTAL 0.00 0.00 0.00 0.00 0.00 0.00

Expenditures Vs. Budget

Expenditures Vs. Budget

Cumulative Budget & Expenditures

Cumulative Budget & Expenditures

Totals should be same for all 3 tablesDrop down lists

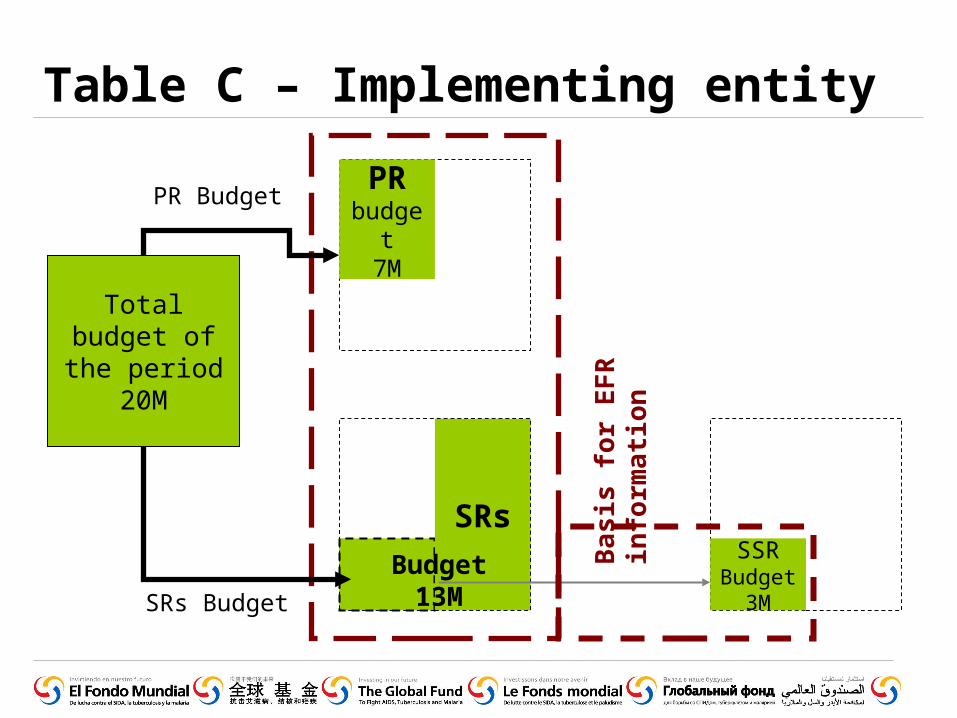

Total budget of the period

20M

Table C – Implementing entity

Ba

sis

fo

r E

FR

info

rma

tio

n

PR budget

7M

SRsSSR

Budget 3M

Budget 13M

PR Budget

SRs Budget

Budget efficiencies

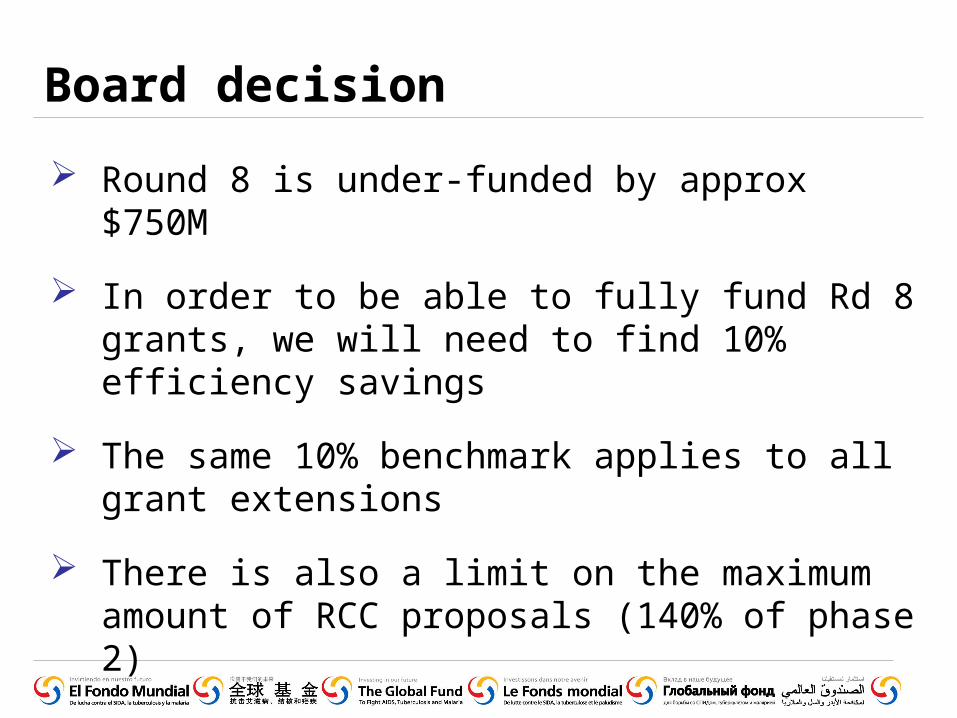

Board decision

Round 8 is under-funded by approx $750M

In order to be able to fully fund Rd 8 grants, we will need to find 10% efficiency savings

The same 10% benchmark applies to all grant extensions

There is also a limit on the maximum amount of RCC proposals (140% of phase 2)

What does it mean for LFAs?

More focus on TRP review comments

Increased importance and focus of LFA budget review (higher quality)

LFAs will be asked to strongly justify why a reduction is not possible

LFA level of budget reductions may be tracked and this used in assessment of performance

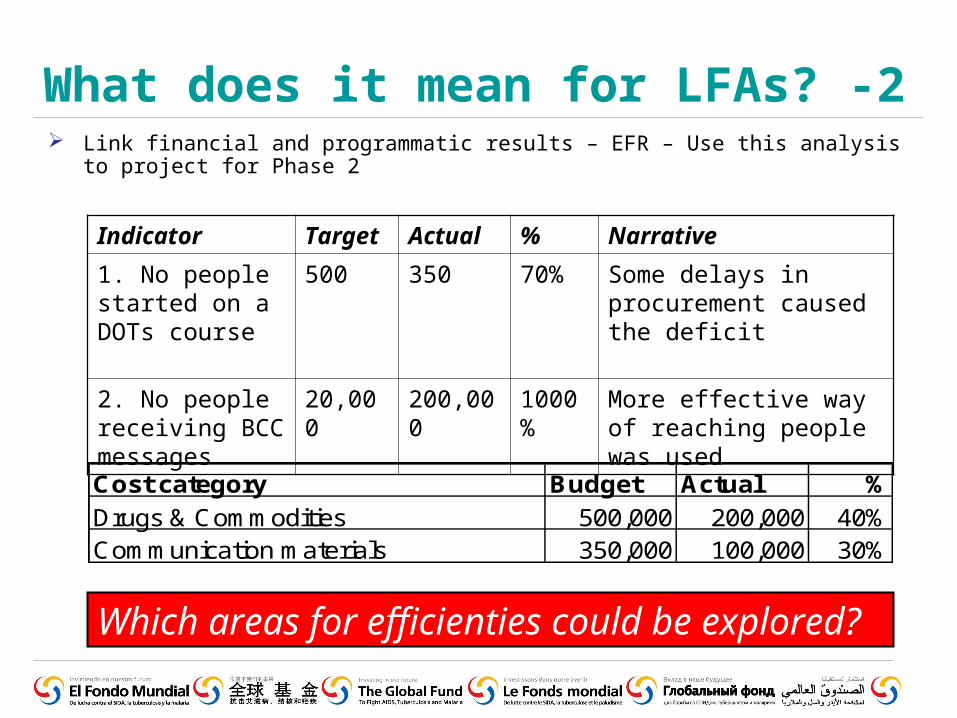

What does it mean for LFAs? -2 Link financial and programmatic results – EFR – Use this analysis to project for

Phase 2

Indicator Target Actual % Narrative

1. No people started on a DOTs course

500 350 70% Some delays in procurement caused the deficit

2. No people receiving BCC messages

20,000 200,000 1000%

More effective way of reaching people was used

Which areas for efficienties could be explored?

Cost category Budget Actual %

Drugs & Commodities 500,000 200,000 40%Communication materials 350,000 100,000 30%

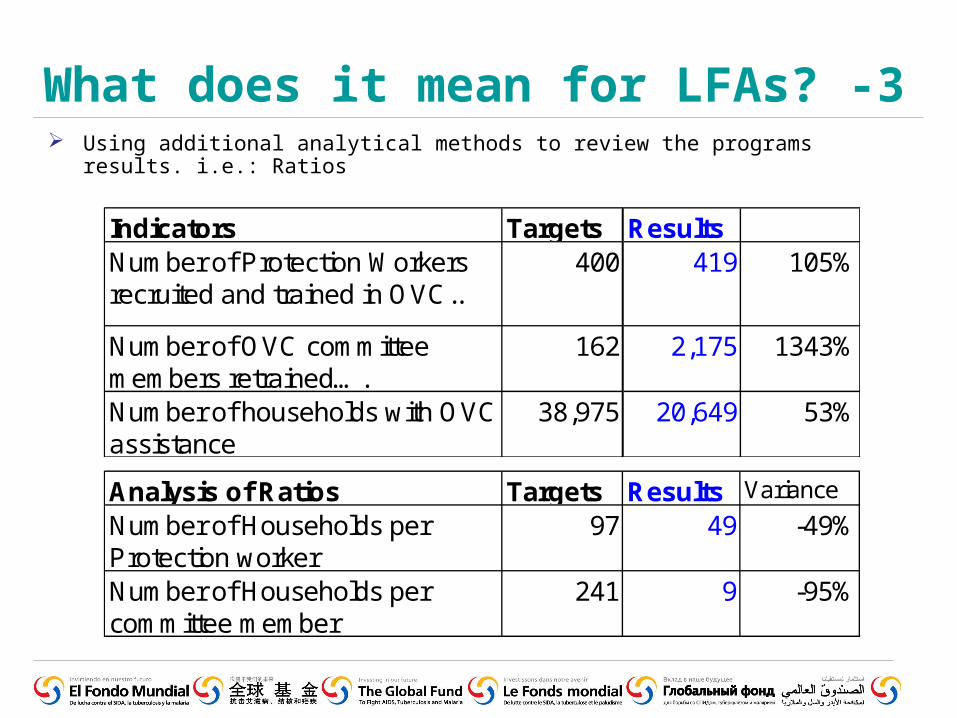

What does it mean for LFAs? -3 Using additional analytical methods to review the programs results. i.e.: Ratios

Analysis of Ratios Targets Results Variance

Number of Households per Protection worker

97 49 -49%

Number of Households per committee member

241 9 -95%

Indicators TargetsNumber of Protection Workers recruited and trained in OVC..

400

Number of OVC committee members retrained….

162

Number of households with OVC assistance

38,975

Results419 105%

2,175 1343%

20,649 53%

What does it mean for LFAs? -4 What are your references when reviewing budgets?

Activity Units U.C. TotalMotorcycles for health workers 100 1,200 120,000

Country Area Population

A 500,000 sq. km 8,000,000B 400 sq. km 150,000

Coverage per motorcycle Area Population

A 5,000 sq. km 80,000B 4 sq. km 1,500

P. 16: "1 motorcycle per health centre (100,000 people) spread over 3 years"World Health Organization, Global Malaria Programme, "Methodology for estimating the costs of global malaria control (2006–2015)"

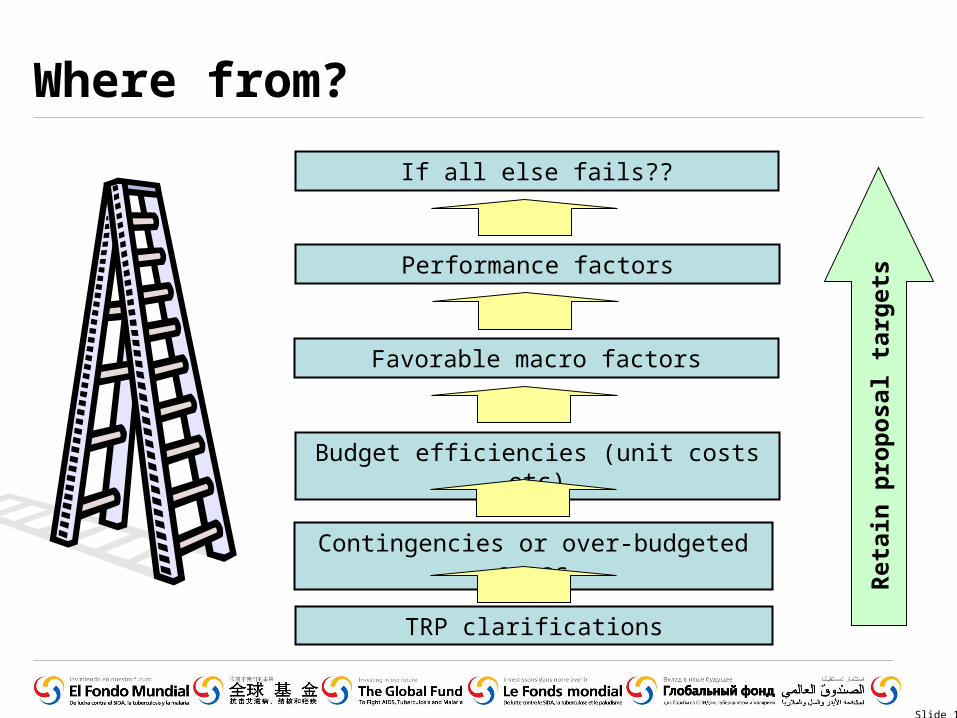

Where from?

Slide 18

Contingencies or over-budgeted areas

Budget efficiencies (unit costs etc)

Favorable macro factors

Performance factors

Ret

ain

pro

po

sal

targ

ets

If all else fails??

TRP clarifications

Where not from?

Reducing the scope and scale of successful programs

What could change?

Greater scrutiny of budgets in grant negotiation and phase 2 decisions

Annual clawback on poor spenders?

Reinvesment of Phase 1 undisbursed amount (at phase 2) – need for justification will increase

Track record of spending/over-budgeting considered (LFAs too!)

Ratings matter even more

Questions

Related Documents