Technical Assistance Consultant’s Report This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. (For project preparatory technical assistance: All the views expressed herein may not be incorporated into the proposed project’s design.) Project Number: TA 4988 CAM October 2008 Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects Final Report: October 2008 Prepared by Les Henning, Nihal Fernandopulle and Russell Leith Cambodia

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Technical Assistance Consultant’s Report

This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. (For project preparatory technical assistance: All the views expressed herein may not be incorporated into the proposed project’s design.)

Project Number: TA 4988 CAM

October 2008

Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

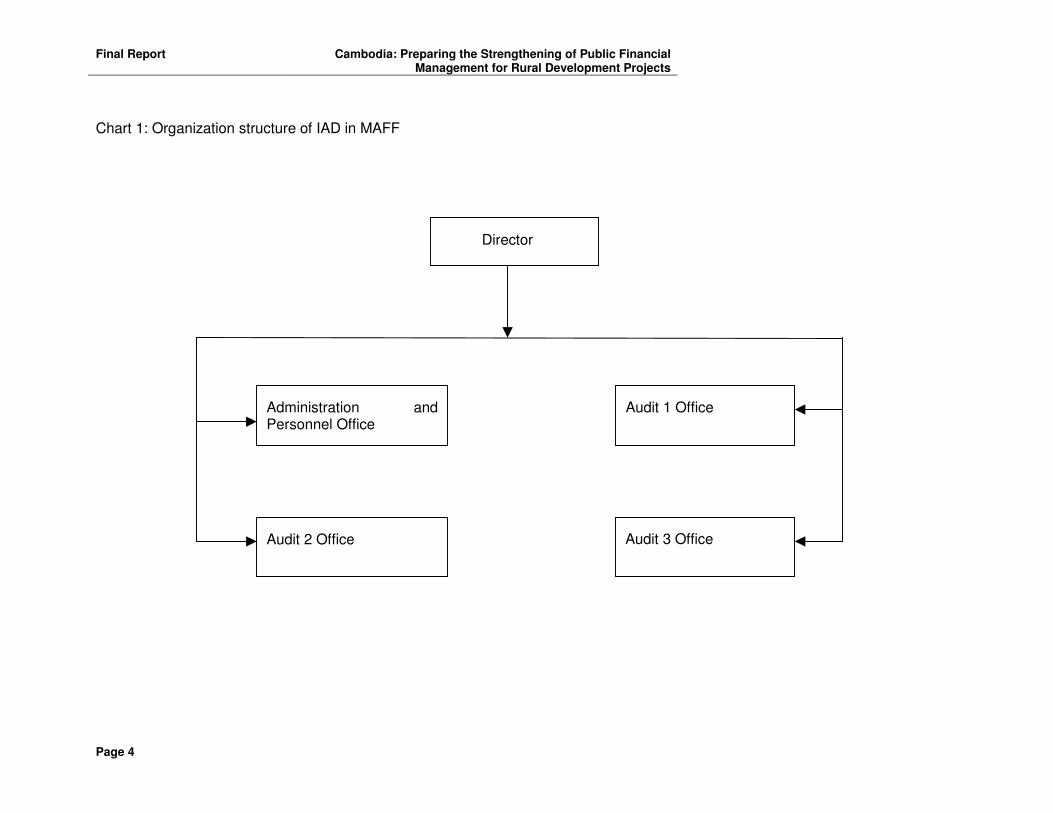

Final Report: October 2008

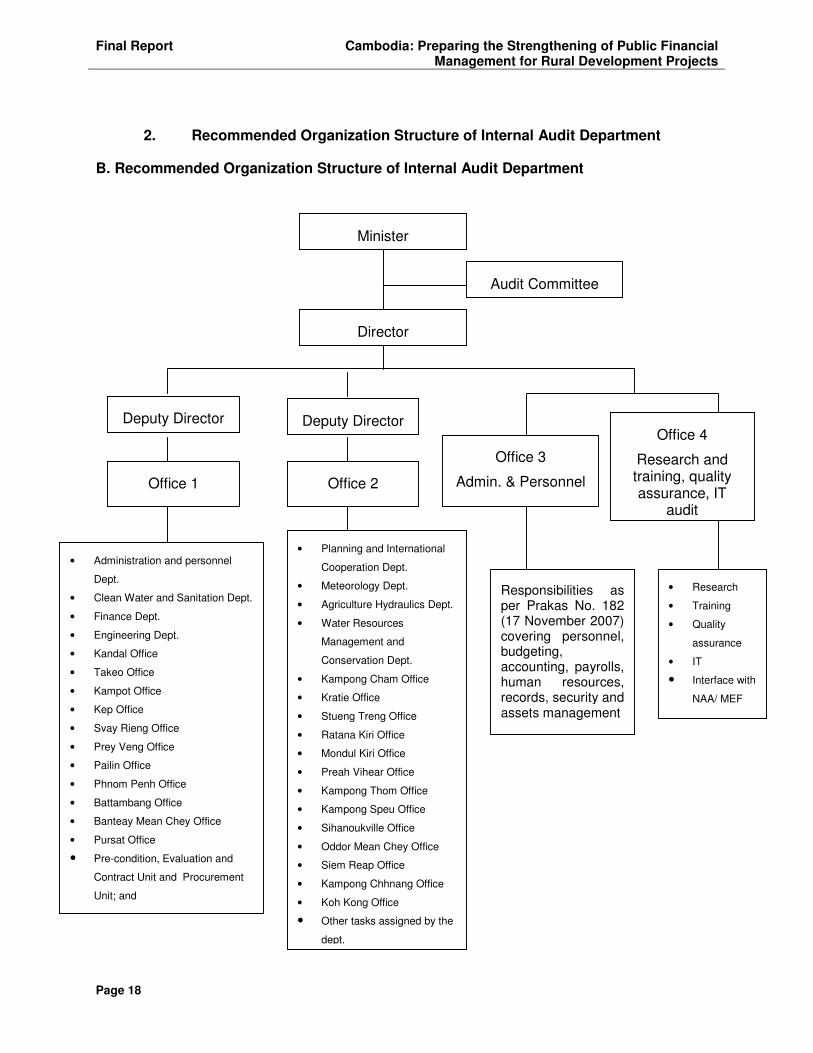

Prepared by Les Henning, Nihal Fernandopulle and Russell Leith

Cambodia

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page i

CONTENTS

I. BACKGROUND AND INTRODUCTION 1

A. Objectives of the Technical Assistance 1

B. Implementation of the Technical Assistance 1

C. Rural Sector Description and Objectives 2

D. ADB Involvement in the Rural Sector 3

II. PUBLIC FINANCIAL MANAGEMENT REFORM 4

A. The Public Financial Management Reform Program (PFMRP) 4

B. PFMPR in Rural Development Ministries 6

C. ADB’s Contribution to PFMRP 9

D. External Audit Function 9

E. Internal Audit Function 10

F. Inter-governmental Financial Relations 13

III. OTHER ACTIVITIES AND OUTPUTS 15

A. PFMRP Annual Retreat 15

B. Equipment Procurement 15

APPENDICES

APPENDIX 1 – LIST OF PERSONS MET 16

APPENDIX 2 22

Appendix 2A – Summary of PFM Reform Program 23

Appendix 2B – ADB Submission on Cambodia PFMRP, Stage 2 Framework 28

APPENDIX 3 – Reviews of the Financial Management and Planning Functions of

MAFF, MRD and MOWRAM, Final Report

32

APPENDIX 4 – MAFF PFM Capacity Development Plan 92

APPENDIX 5 – MOWRAM PFM Capacity Development Plan 133

APPENDIX 6 – MRD PFM Capacity Development Plan 173

APPENDIX 7 – NAA Draft Capacity Building and Training Plan for Loan Projects 213

APPENDIX 8 – Assessment of International Audit Function in MOWRAM 224

APPENDIX 9 – Assessment of International Audit Function in MAFF 264

APPENDIX 10 – Assessment of International Audit Sub-Decree 290

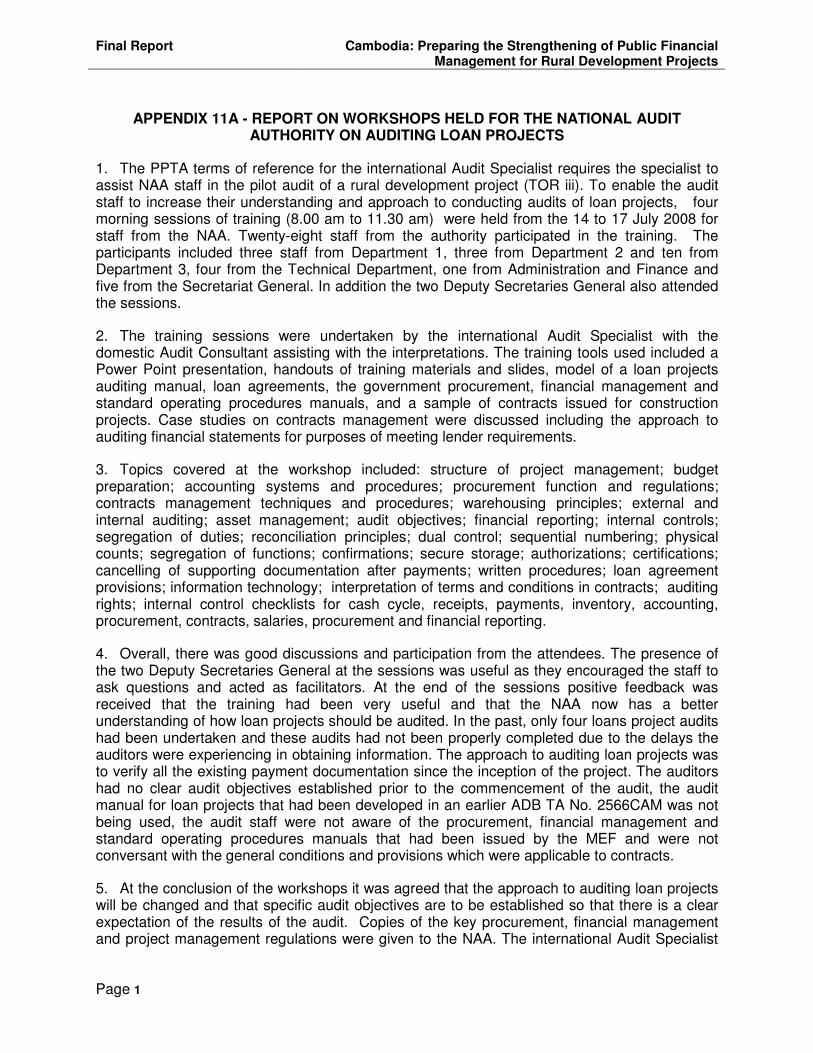

APPENDIX 11 322

Appendix 11A - Report on workshops held for the NAA on auditing loan projects 322

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page i

CONTENTS

I. BACKGROUND AND INTRODUCTION 1

A. Objectives of the Technical Assistance 1

B. Implementation of the Technical Assistance 1

C. Rural Sector Description and Objectives 2

D. ADB Involvement in the Rural Sector 3

II. PUBLIC FINANCIAL MANAGEMENT REFORM 4

A. The Public Financial Management Reform Program (PFMRP) 4

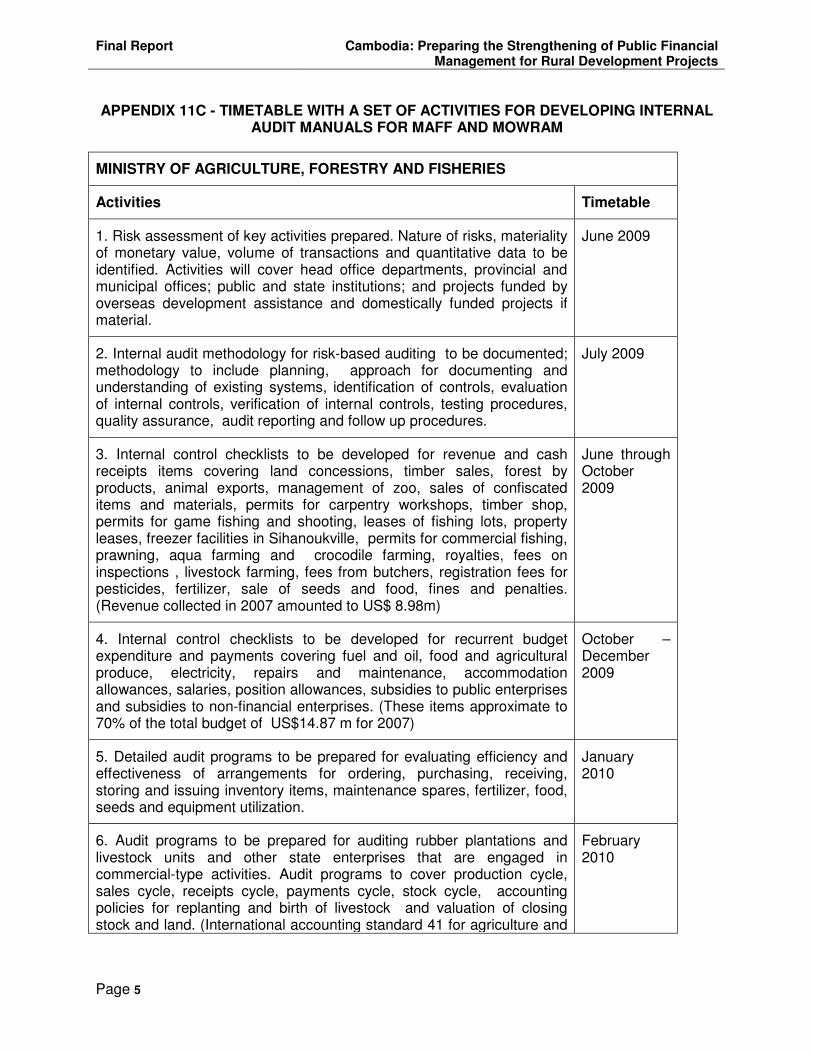

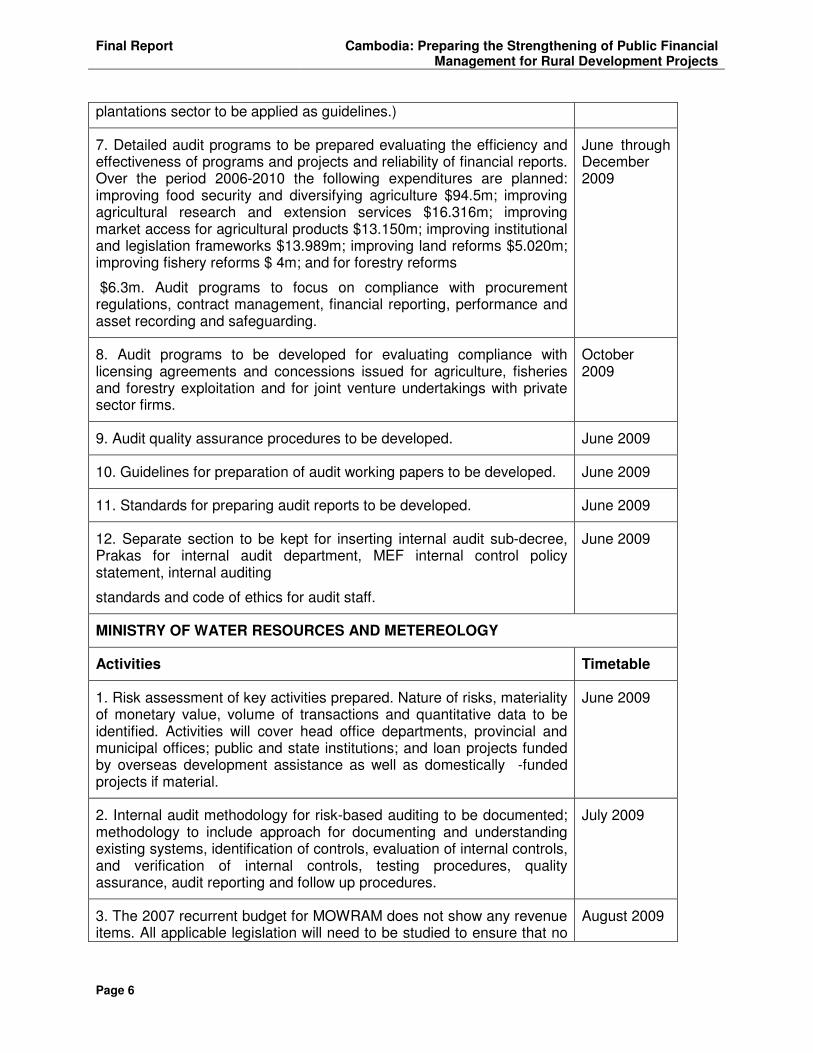

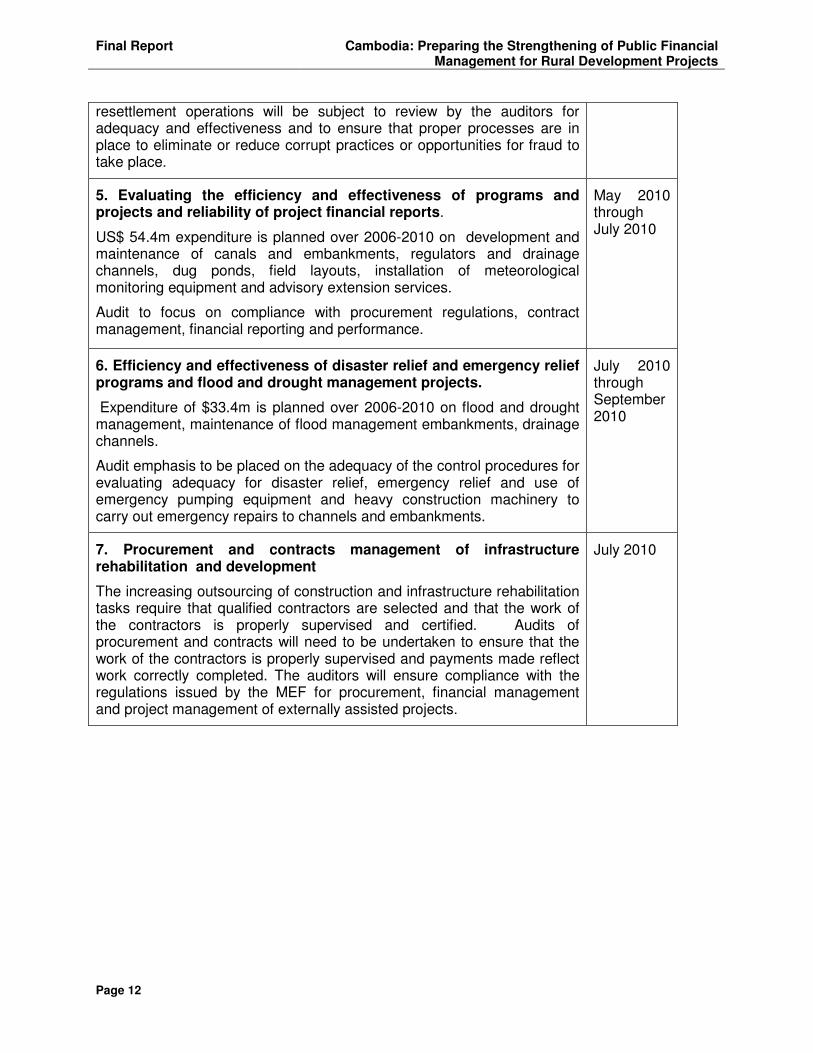

B. PFMPR in Rural Development Ministries 6

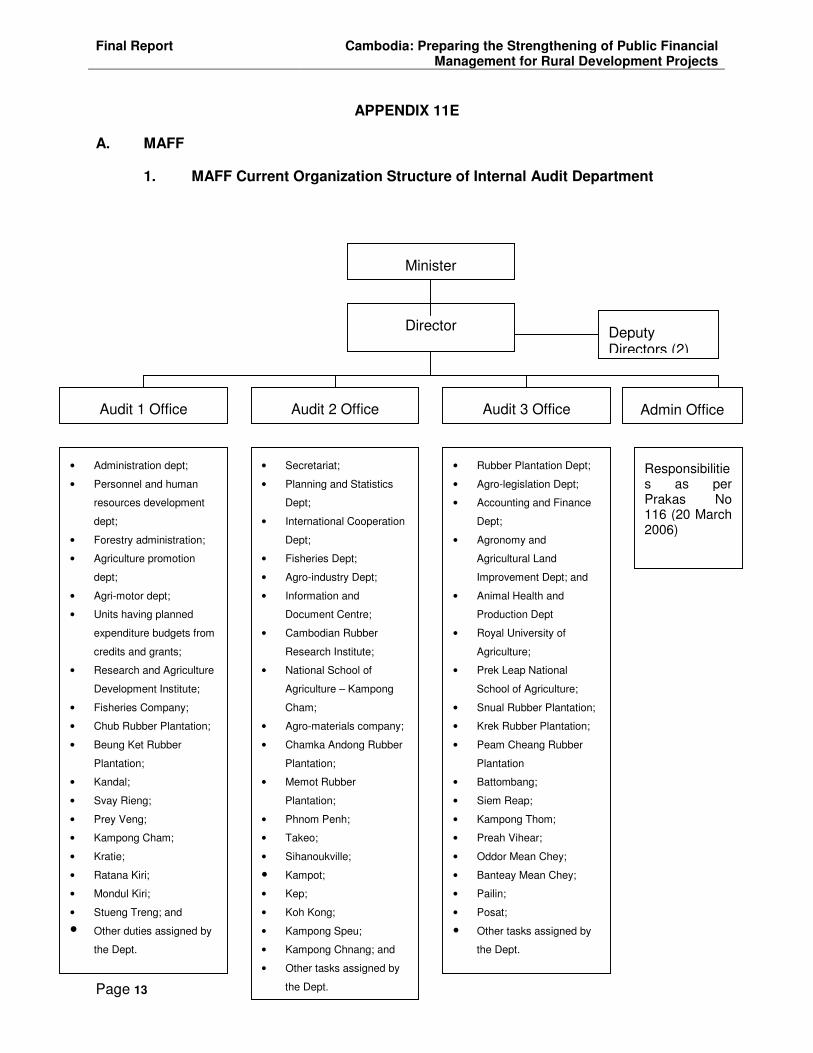

C. ADB’s Contribution to PFMRP 9

D. External Audit Function 9

E. Internal Audit Function 10

F. Inter-governmental Financial Relations 13

III. OTHER ACTIVITIES AND OUTPUTS 15

A. PFMRP Annual Retreat 15

B. Equipment Procurement 15

APPENDICES

APPENDIX 1 – LIST OF PERSONS MET 16

APPENDIX 2 22

Appendix 2A – Summary of PFM Reform Program 23

Appendix 2B – ADB Submission on Cambodia PFMRP, Stage 2 Framework 28

APPENDIX 3 – Reviews of the Financial Management and Planning Functions of

MAFF, MRD and MOWRAM, Final Report

32

APPENDIX 4 – MAFF PFM Capacity Development Plan 92

APPENDIX 5 – MOWRAM PFM Capacity Development Plan 133

APPENDIX 6 – MRD PFM Capacity Development Plan 173

APPENDIX 7 – NAA Draft Capacity Building and Training Plan for Loan Projects 213

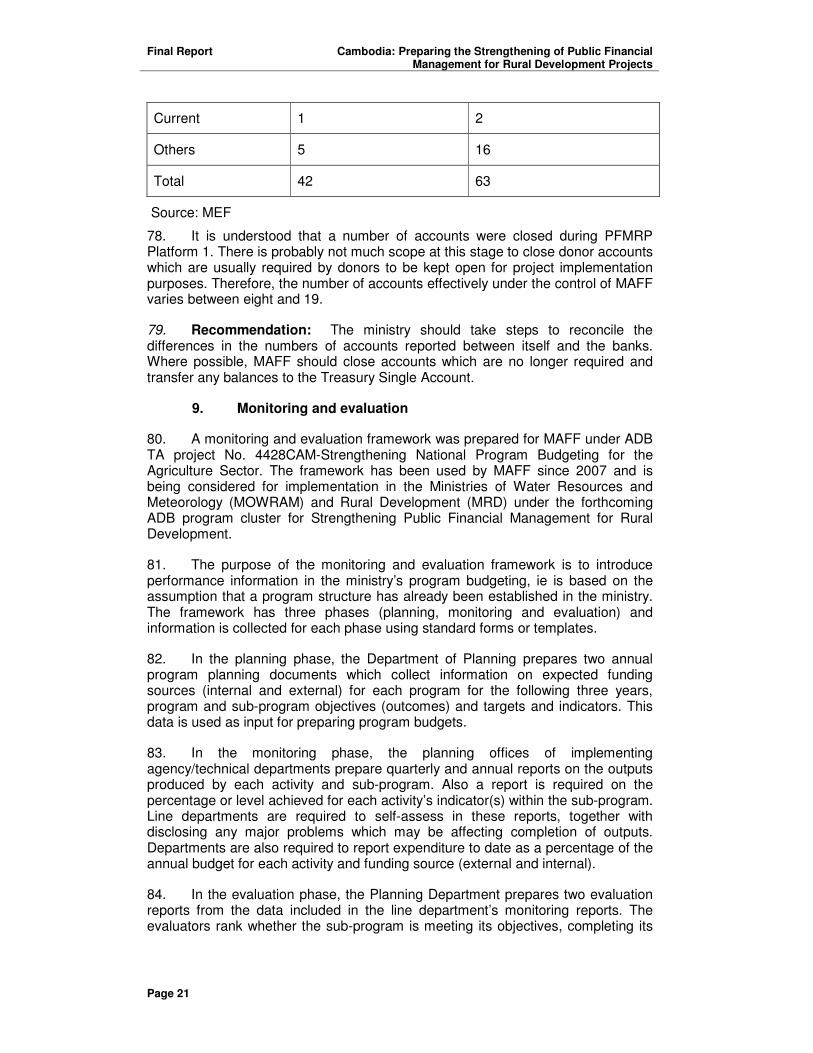

APPENDIX 8 – Assessment of International Audit Function in MOWRAM 224

APPENDIX 9 – Assessment of International Audit Function in MAFF 264

APPENDIX 10 – Assessment of International Audit Sub-Decree 290

APPENDIX 11 322

Appendix 11A - Report on workshops held for the NAA on auditing loan projects 322

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page ii

Appendix 11B – Report on workshops held for Internal Audit in MAFF and MOWARM 325

Appendix 11C – Timetable to develop internal audit manuals for MAFF and MOWARM 328

Appendix 11D – Elements of internal audit work plans for MAFF and MOWARM 333

Appendix 11E – MAFF and MOWRAM organizational structures 338

Appendix 11F – Networking Arrangements between NAA and Internal Audit: TOR and

cost estimates

352

APPENDIX 12 – Cambodia Draft Law on Administration Management of Capital,

Provinces, Municipalities, Districts and Khans

356

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page iii

ABBREVIATIONS

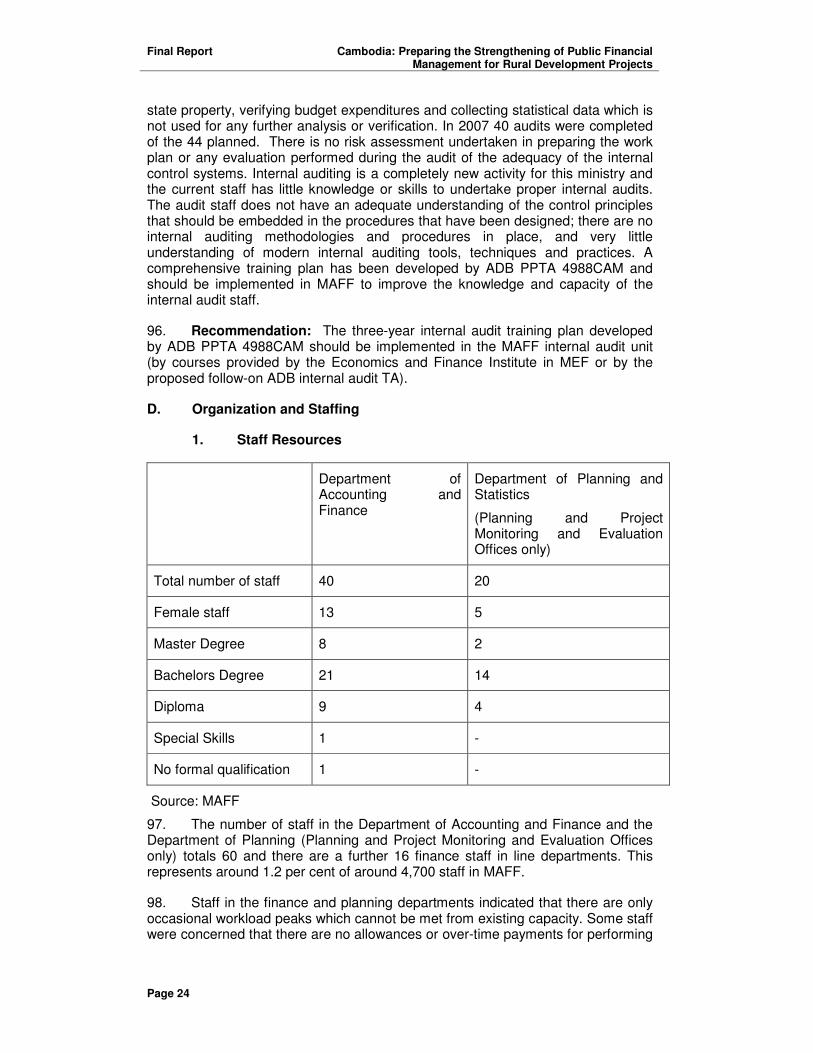

ADB Asian Development Bank

AusAID Australian Agency for International Development

CAP Consolidated Action Plan

CARM Cambodia Regional Mission (ADB country office)

D and D Devolution and deconcentration

DPC Development Partners Committee

EAP External Advisory Panel

FMIS Financial Management Information System

IFAPER Integrated Fiduciary Assessment and Public Expenditure Review

IMF International Monetary Fund

MAFF Ministry of Agriculture Forestry and Fisheries

MOEYS Ministry of Education Youth and Sport

MOI Ministry of Interior

MEF Ministry of Economy and Finance

MOWRAM Ministry of Water Resources and Meteorology

MRD Ministry of Rural Development

NAA National Audit Authority

NSDP National Strategic Development Plan

PFM Public financial management

PFMPCRD Public Financial Management Program Cluster for Rural Development

PFMRP Public Financial Management Reform Program

PPTA Project preparatory technical assistance

RGC Royal Government of Cambodia

RRP Report and Recommendation of the President (of the ADB)

TA Technical assistance

TORs Terms of reference

WB World Bank

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 1

I. BACKGROUND AND INTRODUCTION

A. Objectives of the Technical Assistance

1. The overall objective of the PPTA has been twofold: to assist RGC rural development ministries in planning to improve their public financial management (PFM) capacity particularly under PFMRP and, secondly, to assist ADB to design a program to aid those agencies in improving their PFM capacity. The activities of the PPTA have been directed at producing six main outputs: (i) an update on progress of the Public Financial Management Reform Program (PFMRP) during its Platform 1 implementation and during planning for Platform 2, (ii) review of progress in implementing PFM reforms in MAFF, MOWRAM and MRD, (iii) review of the implementation of the internal audit function in the three line ministries, (iv) review of the capacity of the NAA to carry out an effective external audit function, (v) training needs analyses of MAFF, MOWRAM, MRD and NAA to assess their need for PFM-related training and other skills development and (vi) preparation of capacity development plans for MAFF, MOWRAM, MRD to provide for PFM-related and other types of capacity development in those ministries.

B. Implementation of the Technical Assistance

2. The PPTA (4988CAM: Preparing the Strengthening of Public Financial Management for Rural Development Project) was intended to be implemented between December 2007 and August 2008. However, because of delays in recruitment of consultants, the implementation period has been from March to September 2008.

3. The executing agency for the project has been the MEF and the implementing agencies have been MAFF, MOWRAM, MRD and NAA.

4. The project commenced on 3 March 2008. Mr Les Henning, Public Financial Management Specialist/Team Leader, provided in-country inputs to the project from 3 March to 10 May and from 2 June to 30 August 2008. Mr Russell Leith, Institutional Development Specialist, provided inputs between 3 and 22 April, 14 May and 6 June, 17 June and 11 July and 24 July and 20 August 2008. Mr Nihal Fernandopulle, Audit Specialist, provided inputs between 6 and 20 April, 1 and 12 May, 11 June and 17 July and 28 July and 27 August 2008. National consultants Mr Ros Kheng, Budget Consultant, Mr Many Cheng, Capacity Development Consultant and Mr Nop Saravoan, Audit Consultant, have been employed continuously with the project since 10 February, 27 March and 5 May respectively.

5. A project inception report including work plan was submitted to the authorities and the ADB in early April 2008 and a mid-term report on progress to 30 June 2008 was submitted in early July. The PPTA team made a presentation of PPTA findings and recommendations to representatives of MEF, MAFF, MOWRAM, MRD and ADB in Phnom Penh on 26 August.

6. While accompanying ADB missions and during project interviews the project has met with a large number of officials from MEF, MAFF, MOWRAM, MRD and NAA and with other donor agencies. Team members have established good working relations with all of these officials and the project team is very grateful for the cooperation and assistance it has received. A list of persons met during the PPTA is included in Appendix 1 below.

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 2

C. Rural Sector Description and Objectives

7. High economic growth rates since the mid-1990s have contributed to significant poverty reduction in Cambodia (from 47 per cent of the population in 1993-94 to 34.7 per cent in 2004 (latest figures available)). However, the impacts of growth have not been evenly spread and rural poverty at 39.2 per cent remained significantly higher than the national average in 2004.

8. The RGC is committed to sustaining high rates of economic growth and in meeting its Millennium Development Goal (MDG) targets. As Cambodia’s poverty reduction strategy, the National Strategic Development Plan (NSDP) 2006-2010 builds on the MDG targets and outlines a strategy for reducing poverty through rural development. Of the NSDP’s Rectangular Strategy’s four key components there are two which directly affect rural development: (A) Enhancement of the Agricultural Sector by (i) improving productivity and diversifying the agricultural sector, (ii) land reform and mine clearance, (iii) fisheries reform and (iv) forestry reform and (B) Further Rehabilitation and Construction of Physical Infrastructure through (i) further construction of transport infrastructure and (ii) management of water resources and irrigation. Of the 43 high level development targets set in the NSDP 2006-2010, eight are directly in the rural development sector and are shown in the following table.

Table 1: NSDP 2006-2010 Targets

Target Actual 2005

Target 2010

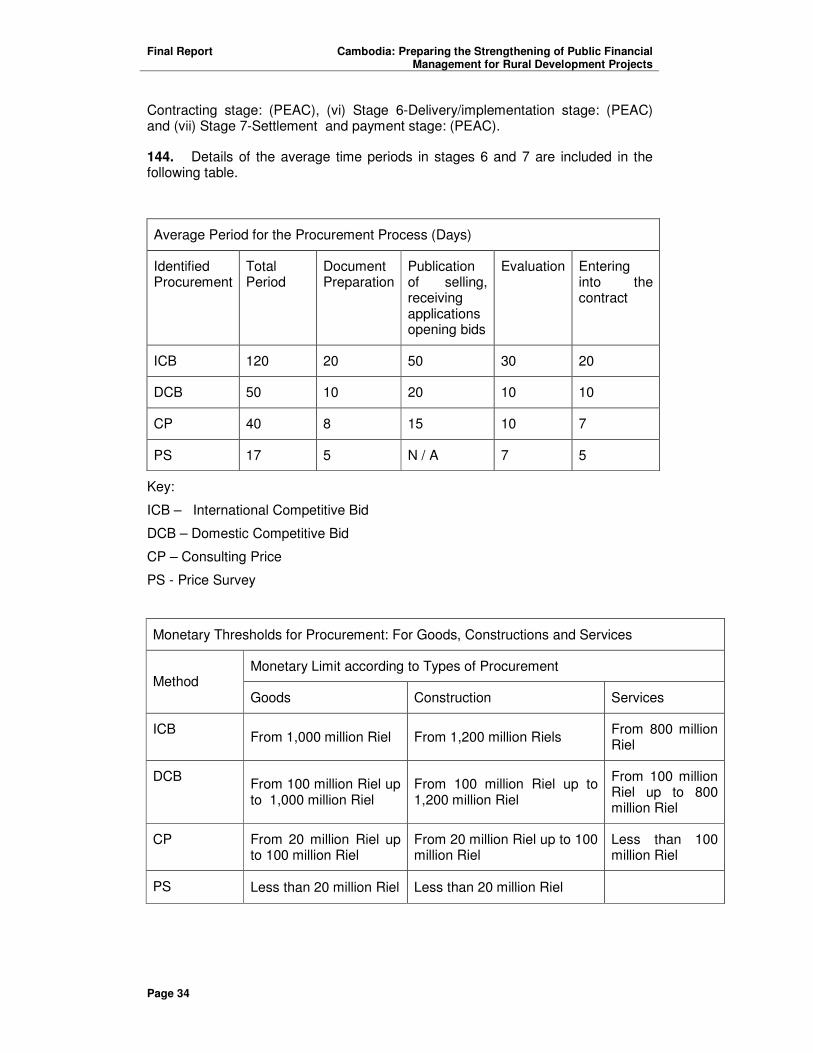

ENHANCE AGRICULTURAL PRODUCTION AND PRODUCTIVITY

Paddy yield per hectare (tons) 1.97 2.4

Irrigated land including supplemental irrigation (% of rice area)

20 25

Land reform: land titles to farmers (% of total agricultural land)

12 24

RURAL DEVELOPMENT

Rural roads rehabilitated (kms-out of 28,000) 22,700 25,000

Safe drinking water access (% of rural population) 41.6 45

Sanitation access (% of rural population) 16.4 25

ENVIRONMENTAL SUSTAINABILITY

Forest cover (% of total area) 60 58

Fuel wood dependency 83.9 61

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 3

9. The most challenging strategic goal for the rural sector, however, will be to reach the target of reducing poverty to below 25 percent of the total population by 2010, from 34.7 percent in 2004. Because, as indicated above, a higher proportion of the poor live in rural areas, meeting the NSDP poverty reduction goal by 2010 will require well-targeted and increasingly efficient public sector programs, as well as significant private investment.

10. A serious deficiency in Cambodia’s public financial management system has been the low budget execution rate by ministries, i.e. rural ministries’ actual expenditures have frequently fallen significantly short of their approved budgets. For example, Ministry of Agriculture, Forestry and Fisheries spent only 90 percent of its current budget in 2003, although it increased its disbursement rate to 96.9 percent by 2007. Ministry of Rural Development increased its rate of current spending from 80.5 percent to 93.3 percent of approved budget over the same period and Ministry of Water Resources spending rate declined from 95.9 percent to 93.5 percent of budget over the same period. Poor PFM systems in line ministries have serious impacts on the efficiency and effectiveness of service delivery of line ministries’ programs and thus the attainment of poverty reduction goals.

D. ADB Involvement in the Rural Sector.

11. From the resumption of ADB operations in1993 to the end of 2007, ADB had supported the agriculture and natural resources sectors with a total approved amount of $125.5 million (five loans, one grant project and 25 technical assistances (TAs)). This comprises approximately one quarter of the total assistance approved by ADB for Cambodia. At the end of 2007, continuing loans and grants (three project loans, one program loan and one project grant) for agriculture and natural resources totaled $83.59 million or 15.9 per cent of ADB’s active portfolio in Cambodia. Also, in late 2007, the active TA portfolio in the agriculture and natural resources sector totaled nine projects for a total value of $7.05 million.

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 4

II. PUBLIC FINANCIAL MANAGEMENT REFORM

A. The Public Financial Management Reform Program (PFMRP)

12. PFMRP was adopted in December 2004 in response to observed weaknesses1 (low budget execution rates, excessive payment arrears, fiduciary risks associated with cash-based transactions systems, low resource mobilization rates and poor control systems) in public financial management (PFM)2. PFMRP was established as a 10-year reform program, based on a sequenced platform approach:

• Platform 1: Making the budget more credible in terms of timely and predictable delivery of funds (including improving the comprehensiveness of the budget; strengthening macro-fiscal and revenue forecasting and streamlining spending processes);

• Platform 2: Implementing effective financial accountability;

• Platform 3: Achieving a fully affordable policy agenda through policy-budget linkage; and

• Platform 4: Achieving effective program performance accountability.

13. Stage 1 of the program covered the period 2005 to 2007, with 2007 also being designated as a transition year for planning the changes needed to move to Stage 2 of the program. The methodology in Stage 1 of the PFMRP was to design and implement a series of activities (and related actions) that would contribute directly to meeting the objectives of Platform 1 as well as a set of activities which were deemed to be prerequisites for commencement of Platforms 2, 3 and 4 in later years.

14. Major outputs of Platform 1 of the program included (i) establishment of a revenue mobilization strategy, together with improved macro-fiscal planning, (ii) improved resource flows from improved revenue collection techniques in National Treasury (also assisted by strong economic growth), improved cash management (including consolidating several hundred government bank accounts into the Treasury Single Account) and increased use of the banking system (rather than cash) for government transactions, (iii) incorporation of off-budget revenues into the budget, (iv) implementation of a debt management function in MEF, (v) streamlining the expenditure commitments and payments system to improve budget holders’ ability to spend in line with budget provision, (vi) reduction in the stock of payment arrears and measures to avoid re-accumulation of arrears and (vii) implementation of revised procurement procedures.

15. Activities undertaken in Stage 1 as prerequisites for later platforms included (i) redesign of the chart of accounts and budget classification and (ii) initial design of a government-wide Financial Management Information System, (iii) introduction of an internal audit function, (iv) redesign of the budget cycle, introduction of program budgeting on a pilot basis in selected ministries, (v) investigating options for fiscal decentralization and (vi) completion of a PFM capacity development plan.

16. The PFMRP was reviewed by an independent External Advisory Panel in early 2007. As a result of the review, it was recognized at the annual PFMRP retreat in Siem

1 World Bank/ADB, Integrated Fiduciary Assessment and Public Expenditure Review, 2004

2 MEF, Public Financial Management Reform Program: Strengthening Governance in Cambodia through

Enhanced Public Financial Management, 2004

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 5

Reap in April 2007 that, while not all activities proposed under Platform 1 had been fully completed, sufficient progress had been made for the overall objectives of Platform 1 to have been substantially achieved and for planning for Platform 2 to commence.

17. MEF prepared, in consultation with development partners, a framework for implementing Stage 2 of the PFMRP from 2008 to 2010 in the document Building on Improved Budget Credibility toward Achieving Better Financial Accountability (also known as the PFMRP Consolidated Action Plan Stage 2 (CAP2)), which outlines the proposed second stage and the second platform of the PFMRP.

18. The activities in Stage 2 are grouped in three main types; (i) continuing Platform 1 activities that need to be strengthened in Stage 2, (ii) Platform 2 activities that are to be implemented in Stage 2 and (iii) activities for later platforms (3 and 4) which need to be commenced in 2008.

19. The continuing Platform 1 activities are (i) to further improve revenue policy and administration, (ii) debt management and (iii) cash and bank account management. The activities planned for Platform 2 are: (i) improving lines of accountability by clarifying roles, functions and responsibilities between levels of government and within spending agencies, (ii) improved instruments for encouraging responsible financial management including an incentives and sanctions regime, (iii) further completing implementation of the chart of accounts and the budget classification, (iv) improved budget implementation and financial management by further streamlining of the commitments and payments system and commencing implementation of the FMIS, (v) improved accounting, financial reporting and transparency by adoption of international accounting standards, quarterly and annual budget execution reporting and an improved budget document, (vi) completing the coverage and strengthening internal audit in line ministries, (vii) developing fiscal decentralization policy and strategy and (viii) building institutional capacity and motivational measures. Activities planned for Stage 2 as prerequisites for later platforms include (i) further integration of the recurrent and capital budgets, (ii) further inclusion of off-budget revenues and expenditures in the budget and (iii) further implementation of program budgeting.

20. The PPTA prepared a summary and comments on the PFMRP Stage 1 outcomes and activities proposed for Stage 2, a summary table of which can be found in Appendix 2A (full details can be found in Appendix 1 of the Mid Term Review). Also, the PPTA prepared the ADB’s submission to the RGC on the CAP2 which is included as Appendix 2B. In the submission the ADB indicated that it strongly supported the proposed framework as a suitable basis for Stage 2 of the program, but suggested some options for strengthening the framework. These were (i) inclusion of specific internal audit training activities for line ministries, (ii) further clarification of line ministries’ intended involvement in internal audit, program budgeting and further reform of the commitments and payments system. Also, clarification was required on whether further action would be required in Stage 2 on certain Platform 1 activities which remained incomplete (further out-posting of financial controllers to line ministries, preparation of an IT strategy, additional public expenditure tracking surveys (PETS) and completion of government asset registers.

21. CAP2 was adopted as the framework for PFMRP Stage 2 at the annual program retreat in June 2008, with implementation to commence in late 2008.

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 7

greater transparency of bidding opportunities. (All ministries will be required to participate in the further procurement reforms.)

27. Other Stage 2 activities in which MAFF, MOWRAM and MRD will participate are (i) improving accountability by defining appropriate financial responsibilities between management levels in ministries (and between levels of government), (ii) implementing the new economic and administrative classifications in the chart of accounts and budget classification by 2009 and the new functional classification by 2010, (iii) improved and more frequent budget reporting, (iv) further deepening of internal auditing procedures introduced in Platform 1 including MEF quality control of internal audit reports and (v) implementation of new financial arrangements at sub-national level pursuant to the deconcentration and devolution organic law passed in 2008.

28. Further work will be undertaken in preparation for activities, which are to be fully implemented in Platforms 3 and 4 from 2011 to 2015. MRD and MAFF as pilot ministries for program budgeting will be required to review and amend their program structures and budgeting procedures in the light of lessons learned in Platform 1. All ministries will be required to bring donor-funded programs and projects into their budget preparation cycle to the greatest extent possible.

29. A major focus of Platform 2 will be capacity building in line ministries under the PFM capacity development plan prepared by the Economics and Finance Institute (EFI) of MEF in 2007 and approved by the Government as the blueprint for PFM capacity building until 2010. The plan provides for extensive (up to 8,000 participants across the public sector) training in 33 different PFM technical skills, (ii) broader skills development training (leadership, management), (iii) new human resources policies (accelerated advancement, job rotation, overseas scholarships and study tours). It is also proposed that the Merit Based Pay Initiative will become available to all line ministries to extend incentives to staff to improve their performance and to participate in the PFMRP. The proposed TAs to MAFF, MOWRAM, MRD and NAA under the proposed ADB program cluster should be designed to fit seamlessly with the PFM capacity development plan.

30. To assist the line ministries to prepare for PFMRP Stage 2 and for the ADB to design activities for its proposed rural development program cluster, the PPTA has carried out functional reviews of the finance and planning departments of MAFF, MOWRAM and MRD with the cooperation of the staffs of those ministries. The reviews, which are reported at Appendix 3, confirmed earlier findings such as those of the 2007 EAP that the take-up of PFM reforms in line ministries between 2005 and 2007 had been slight.

31. The main findings of the reviews were that (i) estimated receipts and expenditures of donor projects (which can comprise a large proportion of the resources available to the three ministries) were not being included in preparation of the ministries’ budgets, (ii) there was poor or non-existent coordination in including provincial departments’ budget estimates in the ministries’ budgets preparation, (iii) there was poor coordination between preparing the program and non-program budgets (MAFF and MRD), (iv) there was inadequate reporting of budget execution by provincial departments during the fiscal year, (v) accounting systems in the three ministries are rudimentary (although MAFF is introducing a commercial accounting package prior to its inclusion in the FMIS pilot in 2010), (vi) the internal audit function was not yet well developed in the two ministries (MAFF and MOWRAM) in which it had been introduced, (vii) although new procurement procedures had been introduced, fiduciary risks associated with public procurement by the ministries appeared to be still high and (viii) only a small, and probably inadequate, amount of PFM training had been provided to

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 8

line ministries (in MOWRAM only three staff had attended PFM training provided by MEF during Stage 1).

32. The results of the reviews indicated that significant effort would be required in MAFF, MOWRAM and MRD for institutional and staff capacity building during PFMRP Stage 2. The reviews showed that there is a need for significant strengthening of PFM activities which were commenced in Platform 1 such as improving budget comprehensiveness (i.e. inclusion of off-budget revenue and expenditure items in the budget), procurement procedures, internal audit and implementation of the new chart of accounts, as well as the activities scheduled for Platform 2 such as improved accounting and budget execution reporting. The reviews also suggest that further effort will be required to consolidate program budgeting in the two ministries (MAFF and MRD) in which it has been piloted. There is a need for MAFF to engage with MEF in planning for introduction of FMIS.

33. To assist line ministries and ADB further in implementing PFM reforms, the PPTA prepared PFM capacity development plans for MAFF, MOWRAM and MRD, based on training needs assessments carried out in cooperation with the staffs of those respective ministries.

34. The methodology of the training needs assessments comprised three parts: (i) identification of the PFM training and other capacity development needs specified or implied in the PFMRP Stage 2 framework (CAP2) which included the PFM capacity development plan, (ii) by using the PFM Working Group in each ministry as a focus group in which middle to senior managers in the finance, planning and internal audit departments were asked to identify the development needs of their staff and themselves and (iii) a survey of the staff in the finance, planning and internal audit departments of the ministries to ascertain their views on their organization, their prior experience, training and qualifications and their perceived needs for their own development. The focus groups and surveys sought views on general skills development as well as focusing specifically on PFM training needs. Seventy-four respondents in MAFF, 33 in MOWRAM and 50 in MRD completed the survey questionnaire.

35. The responses, which are summarized in attachments to the capacity development plans for MAFF, MOWRAM and MRD, are included in Appendices 4, 5 and 6 respectively. The respondents indicated needs for a wide range of training in PFM topics which are to be provided in the EFI’s proposed schedule of training as well as other activities not currently scheduled by EFI such as enhanced procurement and internal audit training.

36. The capacity development plans have matched the demand for training with the scheduled training program which EFI proposes to deliver between 2008 and 2010. The proposed plans allocate a proportion of training places to each ministry for all of the PFM and related courses which EFI proposes to offer. In addition, the plans propose training in other areas not presently covered by the EFI schedule. These additional courses include enhanced internal audit, enhanced procurement, program budgeting, commitments and payments system changes, preparing budget execution reports, monitoring and evaluation techniques and implementing devolution and deconcentration. The training plan for each ministry also includes proposed staff numbers to be trained, training modality and implementation period. Training of rural development ministry staff on these supplementary topics would be suitable for inclusion in the proposed ADB TA project.

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 6

B. PFMRP in Rural Development Ministries

22. While much of the focus of Stage 1 was on activities in MEF, line ministries also had a major role in its implementation. The involvement of line ministries including MAFF, MOWRAM and MRD in Stage 1 has included (i) streamlining the commitments and payments system (by removing commitments requirements for salaries and non-procurement purchasing and out-posting financial controllers to selected ministries), (ii) consolidation of ministries’ bank accounts to the Treasury Single Account in National Treasury to improve cash management and reduce fiduciary risks, (iii) reducing ministries’ payment arrears (which were paid out by MEF) to improve their ability to meet current year expenditures, (iv) deconcentration of procurement by introducing new purchasing procedures including raising the thresholds for line ministries to do their own procurement without prior MEF approval, (v) introduction of internal audit units in line ministries (units were set up in MAFF and MOWRAM but not MRD), (vi) introduction of program budgeting on a pilot basis in seven ministries (including MAFF and MRD, but not MOWRAM) and (vii) introduction of strategic budget plans in the budget preparation process as a first step to linking budget planning and policy priorities.

23. While there has been significant progress with the Platform 1 objective (improved budget credibility) (revenue out-turns are now within five per cent of budget estimates, MAFF’s expenditure execution rate has increased from 94 to 97 per cent between 2005 and 2007, MRD’s increased from 90 to 93 per cent and MOWRAM’s from 89 to 93 per cent), many of the reforms particularly at line ministry level have had limited impact and may not be sustainable in the longer term without further reinforcement.3 For example, while 23 of 35 budget-funded agencies have established internal audit units, it is unclear which, if any, are producing good quality audit reports, Further, despite efforts to rationalize the number of government bank accounts, ministries still hold a large number of accounts (about 1,800). (However, the rural development ministries hold only small numbers of accounts.)

24. In planning for PFMRP Stage 2, MEF has recognized the need for greater involvement of line ministries in the program in order to (i) meet the Platform 2 objective of ‘increased financial accountability’ and (ii) strengthen the reforms, which were introduced in Platform 1. There will also be a need to commence or strengthen activities, which are prerequisites for Platform 3 and 4. The assistance to be provided under the proposed ADB program cluster will be directed at meeting these objectives.

25. MAFF, MOWRAM and MRD will be brought into PFMRP implementation more closely in Platform 2 by including them (along with representatives of all other line ministries) on the PFM Reform Committee, the high level group that sets the policy direction and oversights implementation of the program. Also, all line ministries will be required to prepare their own PFM Ministry Action Plan and a PFM Capacity Building Plan.

26. Further enhancements of Platform 1 activities which will be implemented between 2008 and 2010 will include (i) further improvement of revenue policy and collection including implementation of an oil and gas revenue policy (It is expected that ministries such as MAFF which have significant non-tax revenues should review and periodically adjust the rates of their fees and charges) and (ii) further improvements in public procurement including implementation of procurement rules and regulations and standard bidding documents, MEF ex-post monitoring of ministries’ procurements and

3 External Advisory Panel report, 2007

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 9

37. Other general development topics included in the training plans were business English, report and project proposal writing skills, project management, supervisory skills and basic and advanced IT packages. Consideration should also be given to including these topics in the ADB TA project or funding them from the project’s resources.

38. The capacity development plans also identified other personal development measures which would be suitable for finance and planning staff of the three ministries. These include scholarship schemes offered by various development partners, study tours and in-country courses such as the Japan/ADB Public Policy Training Program. The capacity development plans also recommend that the members of the PFM Working Group in each ministry should be admitted to the Merit Based Pay Initiative (MBPI) as a first step in extending that scheme to line ministries. An option which should be considered in relation to MBPI is whether funding of the scheme in the three rural development ministries would be eligible expenditure in the ADB TA project.

39. The PPTA was requested by the PFM Working Group in MRD to assist it in preparing the PFM Ministry Action Plan (MAP), which is the mandatory strategic plan for PFM reform activity in the ministry from 2008 to 2010. Although this task was additional to the existing TORs and work plan of the PPTA, the Director SEGF agreed that the PPTA should remain flexible in meeting ministry requests for ad hoc assistance and, as this appeared to be a significant activity, ADB would be prepared to rearrange other less significant activities from the PPTAs TORs and work plan, if necessary, to accommodate it. In the event, a draft of MRD’s MAP was prepared within existing project resources and can be found in Appendix 5 of the Mid Term Review. The draft has been submitted to MEF for comment and has been developed further with MRD staff, including discussion of a work plan to implement its various components. As well as assisting the ministry develop its internal audit function (see section 2.5 below) and its PFM capacity development plan (as detailed above), the project has advised the PFM Working Group in MRD on options for joining the MBPI.

C. ADB’s Contribution to PFMRP

40. ADB has contributed significantly since 2005 to activities of the Public Financial Management Reform Program (PFMRP) Platform 1. ADB provided assistance to the RGC in TA No. 2566CAM-Developing Capacity in Audit and Inspectorate Functions to establish the National Audit Authority (NAA). In TA No. 3634CAM–Strengthening Public Financial Management, ADB assisted the Government in 2004 and 2005 to (i) set up an internal audit function, initially in MEF and (ii) strengthen the institutional structure of the NAA. Also, the project assisted MEF to establish a medium term expenditure framework and a macroeconomic forecasting capability. In TA No. 4441CAM-Support to Public Financial Management Program, ADB assisted MEF to establish a debt management function. This activity involved setting up a debt management office in the ministry, installation of a debt management database, preparation of debt management procedures and a manual and staff capacity building. PFM-related technical assistance (although not formally part of the PFMRP) was provided to MAFF in TA No. 4428CAM-Strengthening National Program Budgeting for the Agriculture Sector which prepared a program-based financial management system including a new chart of accounts, a monitoring and evaluation framework and manual and a financial training manual.

D. External Audit Function

41. The National Audit Authority which was established under the Audit Law of 2000 is the supreme audit institution of Cambodia which reports directly to the National

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 10

Assembly and Senate. In recognition of its independent status, the external audit function has not been formally included in the PFMRP. However, it has been acknowledged that external audit of the public accounts and performance and compliance auditing are essential to ensuring accountability over public resources (including donor-funded projects) and therefore effective service delivery to the rural development sector.

42. As indicated above, ADB has provided significant assistance for establishing and strengthening the external audit function in two TAs between 1999 and 2003. In recognition of its lack of experienced audit staff and its lack of capacity to undertake certain activities such as performance auditing, the NAA has requested the ADB to provide further assistance to strengthen its capacity. Accordingly, the outputs of this PPTA will be used in the preparation of the proposed TA to strengthen capacity in the NAA under the ADB program cluster.

43. A major output of this PPTA has been the preparation of an assessment of the capacity of the NAA (Appendix 2 in the Mid Term Review). The main findings of the assessment were review of (i) the audit law and sub-decree, (ii) NAA’s relationship with the legislature and legislative committees, (iii) NAA’s structure, staffing, processes and procedures and (iv) NAA’s relationship with the internal audit and inspectorate functions. The report also includes terms of reference for a proposed peer review of NAA by another national audit institution. RGC agreement in 2008 to such a peer review proceeding has been included as a policy action trigger for sub-program 1 of the proposed ADB program cluster. The report includes conclusions and recommendations for reform of the NAA and for improving its institutional and staff capacity.

44. Another significant output has been the completion of a capacity building plan for NAA which is included at Appendix 7. The plan is intended to fit under the NAA’s Strategic Development Plan 2007-2011 and focuses particularly on training and capacity building for loan project audits. It proposes training for NAA staff in (i) RGC and donor procurement procedures and auditing of procurements, (ii) donor project financial management requirements, (iii) donor standard operating procedures, (iv) audit planning, (v) review and evaluation of internal controls including IT controls, (vi) loan arrangements and English language training to allow auditors to understand manuals etc.

45. Initial training was provided to NAA staff (including the Deputy Secretaries General) by the PPTA in July 2008. The workshops delivered 14 hours of contact time to 28 staff of the authority on the procedures for auditing loan projects. Further detail on the content of the training and the outcomes are shown in Appendix 11A.

46. The PPTA is assisting the NAA to undertake a pilot performance audit of an ADB development project for school construction in MOEYS (Second Education Sector Development Project: ADB Loan No. 2122CAM). As part of the pilot audit the consultants have been training the staff of the audit department responsible for loan projects in audit planning, determining audit objectives, developing the audit program, preparing internal control checklists and carrying out the audit. Training was also provided on the key features of the procurement, financial management and project management regulations.

E. Internal Audit Function

47. An internal audit function was established in PFMRP Platform 1 as a prerequisite for achieving effective financial accountability which is the main thrust of

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 11

PFMRP Platform 2. With ADB technical assistance, the Internal Audit Department in MEF was formed in 2005 by transfer of 20 staff from the General Inspections Department. Internal audit standards and a code of conduct were prepared by MEF and disseminated to line ministries. Some training in audit procedures was provided to line ministries by MEF.

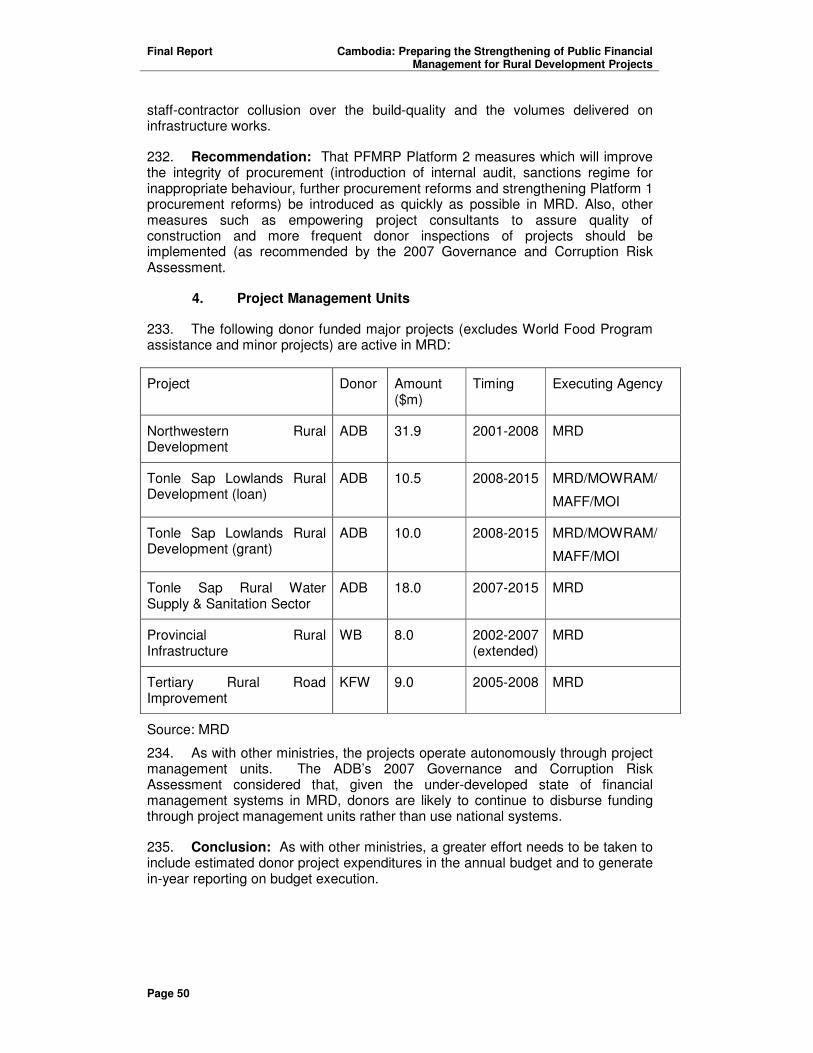

48. The Audit Law of 2000 requires each ministry to establish an internal audit function in accordance with the sub-decree on internal audit (No. 40/ANK/BK of 2005). Internal audit units have been established in MAFF and MOWRAM and a draft sub-decree to establish an internal audit function in MRD was approved by the Prime Minister in August 2008. The independent review by the External Advisory Panel (EAP) in early 2007 found that 19 ministries (subsequently increased to 24 of 35 budget-funded agencies) had established internal audit units but that only seven were found to be operational. The EAP found that the capacity of these units to carry out internal audits effectively was low. The report cited the findings of a WB appraisal which identified (i) internal audit skills development, (ii) guidance on internal audit methodologies and (ii) acquisition of sufficient resources as major requirements of line ministry internal audit departments.

49. An effective internal audit function is essential in line ministries to strengthen internal controls processes to reduce fiduciary risks and to provide assurances to development partners and other stakeholders. In PFMRP Platform 2 it is intended to complete the coverage of internal audit to all line ministries and to strengthen capacity in all ministries in support of the Platform’s main objective of increasing financial accountability. In continuation of its earlier assistance, the ADB program cluster will support a TA project to strengthen internal audit in MEF, MAFF, MRD and MOWRAM.

50. To support the preparation of that TA, the present PPTA has completed a number of outputs. Reviews of the internal audit capacity of MOWRAM and MAFF (shown at Appendices 8 and 9 respectively) have confirmed the view that capacity within the internal audit units is weak.

51. In the MOWRAM review it was found that, although the internal audit unit has a three year work plan and has produced five audit reports, its capacity to undertake audits at a professional standard remains low, due mainly to inexperience of the staff and lack of appropriate educational qualifications. Also there is no generally accepted auditing methodology in place and there are no internal audit procedures manuals. The report includes conclusions and recommendations for improving staff capacity and internal audit procedures, including a three year internal audit training plan which is at Annex E of the report.

52. The review of internal audit in MAFF reaches similar conclusions to the MOWRAM review. Generally, the capacity to undertake adequate internal audits is low and various measures to improve staff capacity and audit procedures will be required. The three year internal audit training plan outlined above is a generic plan and will be appropriate for MAFF and for MRD when its internal audit unit is established.

53. The PPTA assisted MAFF in undertaking a pilot audit of the payments cycle. The Agricultural Office of Steung Treng province was selected for the pilot audit. The internal audit department had scheduled to undertake this audit as part of its annual work plan for 2008 and the PPTA consultants assisted the audit team in executing this audit. The audit focused on evaluating the internal control systems relating to the payments system covering (i) repairs and maintenance of buildings and temples; (ii) accommodation expenses; and (iii) payments of subsidies to enterprises. These three

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 12

items of expenditure represent over 50% of the total expenditure of the 2007 budget allocation for this province.

54. Audit objectives, audit programs and Internal Control Questionnaires were developed together with a detailed planning document. Several training sessions were conducted with the audit teams before the commencement of each phase of the field audit.

55. The PPTA prepared an assessment of the existing internal audit sub-decree which is included as Appendix 10. The assessment concluded that the internal audit sub-decree is adequate to enable the functioning of an effective and professional internal auditing activity in the public sector, as it has been based on the practices recommended by international internal auditing standards. The sub-decree can be strengthened further by introducing provisions to require the establishment of audit committees, permitting external appointments to the more senior positions in the ministry audit departments, permitting the use of short-term experts and contractors for specialized areas of internal audit, requiring an external assessment of the internal audit function once every five years and by requiring that the ministries develop and maintain proper auditing procedures manuals.

56. A two-day workshop on internal audit concepts and procedures was delivered to 33 audit staff of MAFF and MOWRAM in July 2008. Details of the training topics and the outcomes are also shown in Appendix 11B.

57. The PPTA prepared a report advising on the content which should be included in proposed internal audit procedures manuals for MAFF and MOWRAM. The report is included as Appendix 11C. Similarly, an outline of the elements which MAFF and MOWRAM will have to consider in preparing their annual internal audit work plans is included as Appendix 11D. The factors to be considered include: (i) the annual revenue and expenditure cycles, (ii) auditing of procurement, inventories and fixed assets, (iii) auditing of trading and semi-commercial operations (MAFF), (iv) efficiency and effectiveness of projects, (v) resettlement schemes (MOWRAM) and adequacy of disaster and emergency relief programs (MOWRAM).

58. The shortcomings in the current organizational structures of MAFF and MOWRAM’s internal audit departments which were identified in the above reviews have been addressed in proposed new structures for the departments which are included in Appendix 11E. This appendix also includes proposed job descriptions for the various levels of audit staff in the two departments. Because of similarities in the functions of NAA and internal audit departments in line ministries there are risks of overlap and duplication occurring. For this reason, good coordination between these functions is essential and accordingly proposed arrangements for networking between the internal and external audit functions are outlined in Appendix 11F.

59. As indicated above, MRD proposes to establish a functional internal audit unit by the end of 2008. Sub-decree No 113 for establishing the internal audit department in MRD was approved by the Prime Minister on the 13 August 2008. A director and two deputy directors have since been appointed to IAD, although no other staff have yet been appointed. The department is not yet operational and the director has requested the assistance of the TA audit consultants to assist him during this initial stage of start up.

60. The project agreed with MRD’s PFM Working Group that the domestic audit consultant will work with the Director of IAD during September 2008 to assist him to:

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 13

• Draft a Prakas for the IAD based on the requirements of the internal audit sub-decree;

• Identify the key activities undertaken in the ministry;

• Draft a suitable organizational structure for the IA;

• Prepare an outline of the internal audit work plan; and

• Prepare position descriptions for each audit staff member

61. Advice was provided to the Director of IAD to increase awareness of the approach and purpose of internal audit and the techniques and methodologies that are used in modern internal auditing. The need to have a clear demarcation of responsibilities between the newly established internal audit function and the existing inspection function in MRD was also emphasized.

F. Inter-governmental Financial Relations (Devolution and Deconcentration-D and D)

62. As the majority of Cambodia’s poor live in rural areas, improving service delivery to rural communities is seen as an essential step for poverty alleviation. The 2003 IFAPER report noted that decentralization of service delivery responsibility is an essential part of public sector reform. Also, as noted by this project in the functional reviews of the three rural development ministries there is a lack of coordination between the central offices of the ministries and their provincial departments for budget planning and execution, thus detracting from the efficiency of service delivery in rural areas.

63. In PFMRP Platform 1 preparatory work on inter-governmental financial relations was commenced as a pre-requisite for reforms which were to be carried out in later platforms. In the 2007 EAP report progress was noted as (i) enactment in 2001 of a commune and sangkat organic law, (ii) setting up a Commune and Sangkat Fund (to receive central government funding equivalent to about 2.5 percent of recurrent expenditure each year) and (iii) establishment of a system of fiscal grants to communes and sangkats based on a simple fiscal equalisation formula.

64. However, the other levels of sub-national government (provinces, municipalities, districts, and khans) have lacked adequate legal mandates as to their institutional structures, roles and responsibilities (expenditure mandates) and revenue powers and sources. To this end, a devolution and deconcentration organic law was prepared and presented at a major conference in Sihanoukville. The PPTA consulted with the Development Partners D and D Working Group and the DPC on the draft law in March 2008 and prepared a summary and comments on the draft organic law (included at Appendix 12). As the law was introduced for passage to the National Assembly on 27 March 2008, there was no opportunity to engage the relevant ministries on the issues raised in the comments paper.

65. The organic law provides a clearly defined institutional basis for sub-national administrations. It legislates for expenditure responsibilities of the various levels of government to be determined and for a system of assigned revenue types (mostly non-tax revenues), shared taxes (with the central government) and conditional and unconditional transfers from the central government to sub-national administrations, which are to be included in a law on the financial regime and asset management of sub-national administrations. MEF has prepared drafts of the financial law, an early version of which was translated to English by the project team.

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 14

66. However, the implementation provisions of the organic law have been deferred for inclusion in 32 further laws, decrees and sub-decrees. The National Committee on Deconcentration and Devolution (within MOI) with the assistance of high level officials from other ministries is currently working on developing these implementation arrangements, although it is unclear when these tasks will be completed.

67. The PFMRP Stage 2 framework provides for a detailed plan to be prepared to support initial implementation of the fiscal and financial provisions of the D and D organic law (Objective 27). Also, Objective 21 of the framework proposes that the budget holders and lines of accountability at the various levels of government be clearly defined as a basis for improving accountability.

68. Because further policy development has been delegated to the National Committee (and which went into abeyance during the period of the 2008 national elections), the PPTA has been unable to engage further with the authorities on D and D issues. However, after the National Committee has completed the assignment of expenditure roles and of revenue types to sub-national levels, line ministries will require considerable assistance to implement the new arrangements. Therefore, it is recommended that the TA on strengthening PFM reforms in the three rural development ministries remain flexible in responding to assistance needs for the new arrangements.

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 15

III. OTHER ACTIVITIES AND OUTPUTS

A. PFMRP Annual Retreat

69. MEF conducted its annual review meeting for the PFMRP on 28 and 29 May 2008, at which the Prime Minister launched Platform 2 of the program. The ADB Country Director was requested to deliver a closing address on behalf of the development partner community. Mr Russell Leith attended the retreat as an observer.

B. Equipment Procurement

70. The project has completed procurement by competitive quotes of computers and other office equipment for the NAA, MAFF and MRD. This equipment is intended to contribute to increased productivity in these agencies.

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 16

APPENDIX 1 – LIST OF PERSONS MET

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 17

MINISTRY OF ECONOMY AND FINANCE ( MEF)

H.E. Aun Porn Moniroth Secretary of State

H.E. Hang Chuon Naron Secretary General, National Economic Council

Mr. Tep Vannda Assistant to H.E Hang Chuon Naron

H.E. Vongsey Vissoth Deputy Secretary General

Mr. Sunly Thearith Assistant to Deputy Secretary General

Mr You Channan Deputy Chief

Mr. Khuth Sakhan

Director of Administration and Financial Management

Department of Investment and Cooperation

H.E. Chan Sothy

Director of Department of Investment and Cooperation

Mr Pen Thirong

First Deputy Director of Department of Investment and Cooperation

Mr. Chhuon Samrith Chief, ADB Division

Mr. Hak Ponnarin Deputy Chief, ADB Division

Ms Sun Naly Deputy Director of Debt Management Unit

Reform Committee Secretariat (RCS)

Dr. Sok Saravuth Director of Department of Budget Management, PFM Reform Secretariat

Mr. Youk Bunna Deputy Head of Secretariat and Program Coordinator

Mr. Bou Vong Sokha Liaison Officer for PFM Reform Committee at RCS

Mr. Bun Roith Liaison Officer (CRS), Chief of Administrative Office (BD)

Mr. Nuon Vithya Liaison Officer ( PFMRC)

Mr. Ieng Auntouch Liaison Officer ( Revenue Group )

Internal Audit Department ( IAD )

Dr. Chea Vuthna Director of Internal Audit Department

Mr. Var Neov

Non-Tax Revenue Department

Mr. Aun Bunhak Director of Non-Tax Revenue Department

Mr. Thao Sokmuny Deputy Director of Non-Tax Revenue Department

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 18

Mr. Pen Vutha First Deputy Director of Department of Non-Tax Revenue

Department of Public Procurement

Mr. Chhim Sareth, Advisor to the Prime Minister & Director of Department of Public Procurement

Mr. Chhay Vuth Director of Department of Public Procurement

Mr. Vong Roda Vuth First Deputy Director of Department of Public Procurement

Mr. Ngan Phirum

Deputy Director of Department of Public Procurement

Mr. Huot Vathna Deputy Director of Department of Public Procurement

Department of Financial Affairs

Mr Ieng Sunly First Deputy Director of Department of Financial Affairs

National Treasury

Mr. Chhean Hieng, Deputy Director of National Treasury

Economics and Finance Institute ( EFI )

Mr. Seng Sreng Director of Economics and Finance Institute

Ms Soun Len

Training Coordinator of Economics and Finance Institute

ICT Unit

Dr Phan Phalla, Director of ICT Unit

FINANCE AND BANKING COMMISSION

H.E Phan Na

Secretary of Economic, Finance, Banking and Audit Commission

NATIONAL AUDIT AUTHORITY ( NAA)

H.E. Uth Chhorn Auditor General

H.E Chhay Kim Deputy Auditor General

H.E. Luk Nhep Secretary General

H.E Ung Silan Deputy Secretary General

Mr. Long Atichbora Director of Technical Department

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 19

Mr. Keo Chea Director of the 3rd Audit Department

Ms. Keo Sochenda Secretariat General Office

MINISTRY OF RURAL DEVELOPMENT ( MRD)

H.E. Lu Lay Sreng

Deputy Prime Minister and Minister of Rural Development

H.E. Mr. Yim Chhaily Secretary of State

H.E. Suos Kong Secretary of State

H.E. Sao Chivoan Under Secretary of State

H.E. Chuop Sam Ath Director General of Administration and Finance

H.E Hout Sarim Deputy Director General of Administration and Finance

H.E. Chan Darong

Director General of General Department of Technical Affairs

Mr. Sam Say Director of Supply & Finance Department

Dr. Mao Saray, Director of Rural Water Supply Department

Mr. Ma Sovanna

Director of Department of Planning and International Cooperation and member of PFM-WG.

Ek Sokheyna Deputy Director of Department of Supply and Finance

Mr. Hourt Sarim

Deputy Director General of Administration and Finance and member of PFM-WG

Mr. Toun Sophal

Deputy Director General of Administration and Finance and member of PFM-WG

Mr Ngoun Dara Deputy Director of Department of Rural Roads

MINISTRY OF WATER RESOURCES AND METEOROLOGY ( MOWRAM)

H.E Veng Sakhon Secretary of State

Mr. Chorng Seng Im Director of Finance Department

Mr. Muy Monin Deputy Director of Finance Department

Mr. Soeng Sophal Director of Internal Audit Department

Mr. Chhea Bunrith Director of Administration Department

Mr. Chea Chhun Keat Director of Department of Planning and International Coperation

Mr. Klok Sam Ang PMO Manager

Mr Chuon Bithol Program Manager

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 20

Mr Duong Sam Ang Chief of Finance Office

Mr Sam Rithy Technical staff of Finance Department

MINISTRY OF AGRICULTURE FORESTRY AND FISHERIES (MAFF)

H.E Chan Tong Yves Secretary of State

H. E Koum Saron Director General

Mr. Duong Bunny Director of Department of Accounting & Finance

Mr. Nhep Chanthet Director of Department of Internal Audit

Mr. Mong Leng Deputy Director of Department of Accounting and Finance

Mr. Kik Seng Director of Department of Planning and Statistics

Mr. Mouch Chantha Chief of Planning Office

Mr Che Savun, Chief of Office of Public Investment

Mr. Srey Vuthy Chief of Monitoring and Evaluation Office

Mr. Hong Ponnaka Chief of Finance Office

DEVELOPMENT PARTNERS

Mr. Peter Lindenmayer First Secretary Development Cooperation, AusAID

Mr. Jens Lauring Knudsen Agriculture & Rural Development Advisor, AusAID

Mr. Juergen Schilling Country Director, GTZ

Mr. Erik Illes First Secretary, Embassy of Sweden

Mr Sodeth Ly Economist, International Monetary Fund

Ms Jacinta Barrins Decentralization Advisor, UNDP

Ms Helga Wilkerling Audit Trainer, GTZ

Mr. Peter F. Murphy Senior Public Sector Management Specialist, World Bank

Mr Guillaume Prevost Economic Counsellor, Embassy of France

Dr Andrew Wardell Counsellor-Development, Royal Danish Embassy

Ms Louise Scura Lead Natural Resource Economist, World Bank

Ms Jolanda Jonkhart Programme Officer, European Union

Mr John Nelmes Resident Representative, International Monetary Fund

Ms Sandy Rost Audit Adviser, GTZ

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 21

ASIAN DEVELOPMENT BANK

Mr. Jaseem Ahmed Director, SEGF

Ms Rita O'Sullivan Senior Counsel

Mr. Kelly Bird Economist (Trade), SEGF

Mr. Arjun Goswami Country Director, CARM

Mr. Eric Sidgwick Senior Country Economist, CARM

Mr. Alain Goffeau Portfolio Management Specialist, CARM

Mr. Paulin Van Im Sr. Project Implementation Officer, CARM

Mr. Chamroen Ouch Programs Officer (Governance), CARM

Mr. Vanndy Hem Economics and Financial Sector Officer, CARM

Mr. Chantha Kim Economics and Financial Sector Officer, CARM

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 22

APPENDIX 2

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 23

APPENDIX 2A – Summary of the PFM Reform Program

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 24

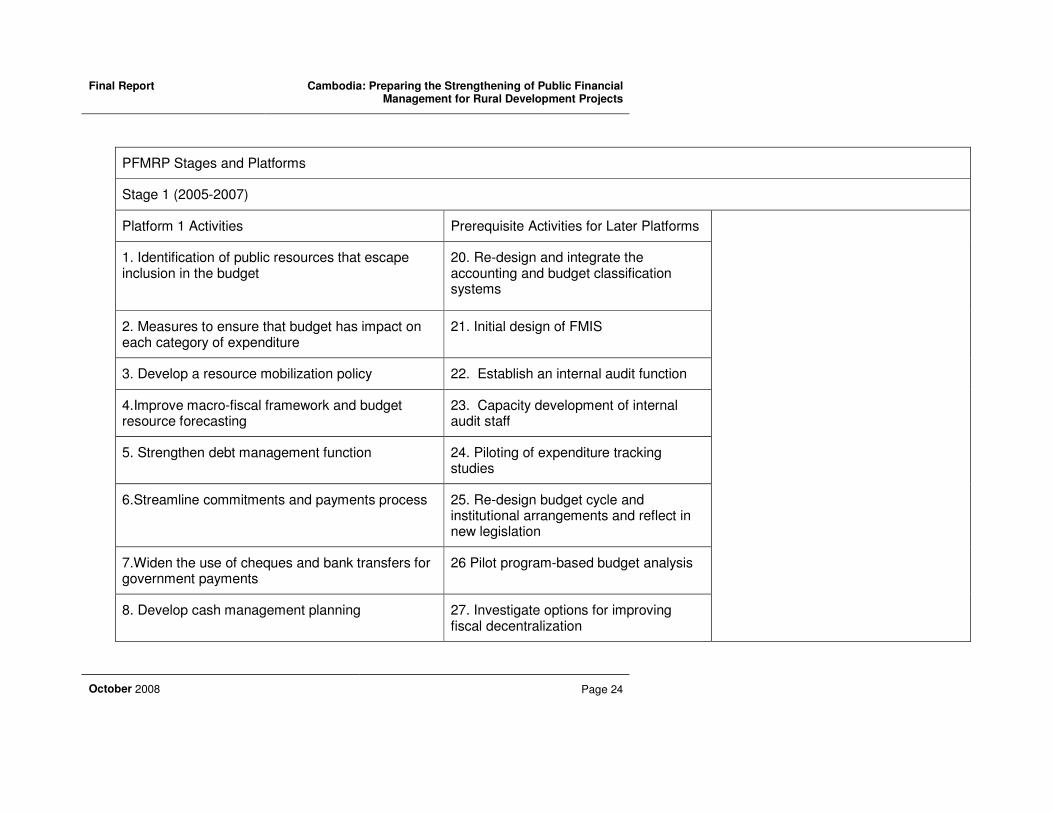

PFMRP Stages and Platforms

Stage 1 (2005-2007)

Platform 1 Activities Prerequisite Activities for Later Platforms

1. Identification of public resources that escape inclusion in the budget

20. Re-design and integrate the accounting and budget classification systems

2. Measures to ensure that budget has impact on each category of expenditure

21. Initial design of FMIS

3. Develop a resource mobilization policy 22. Establish an internal audit function

4.Improve macro-fiscal framework and budget resource forecasting

23. Capacity development of internal audit staff

5. Strengthen debt management function 24. Piloting of expenditure tracking studies

6.Streamline commitments and payments process 25. Re-design budget cycle and institutional arrangements and reflect in new legislation

7.Widen the use of cheques and bank transfers for government payments

26 Pilot program-based budget analysis

8. Develop cash management planning 27. Investigate options for improving fiscal decentralization

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 25

9. Consolidate government bank accounts into the Treasury Single Account

28. Develop an IT management strategy

10. Eliminate stock of payment arrears 29. Initial design of an asset register

11. Take steps to avoid re-accumulation of payment arrears

12. Improve process for post-budget supplementary expenditure approvals

13. Develop revised procurement procedures

30. Capacity development measures (various) to support Platform 1

31. Motivational measures within MEF (mainly MBPI)

32. Investigate freedoms and flexibilities to encourage line ministries to engage in PFM reforms

33. Initial integration of functions in MEF

Stage 2 (2008-2010)

Strengthening of Platform 1 Activities Platform 2 Activities Prerequisite Activities for Later Platforms

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 26

11. Further improve revenue policy and administration (continues activities 3 and 4 above)

21 Improved lines of accountability by clarifying roles and responsibilities between levels of government and within spending units (continues activity 32 above)

31. Improve and expend program budgeting (continues activity 26 above)

12. Further improve debt management (continues activity 5 above)

22. Establish incentives and sanctions to encourage responsible resource management

32. Further improve comprehensiveness and integration of the budget (integrate capital and recurrent budgets, include off-budget expenditures in budget )( continues activity 1 above)

13. Further improve cash and bank account management (continues activities 7,8 and 9 above)

23. Further improve the chart of accounts and budget classification (continues activity 20 above)

14. Further improve public procurement (continues activity 13 above)

24. Improve budget implementation and financial management systems (further streamlining of commitments/payments system, piloting of FMIS) (continues activities 6 and 21 above)

25 Improved accounting, financial reporting and transparency

26. Improved internal auditing (continues activity 22 and 23 above)

27 Strengthen and develop fiscal decentralization (continues activity 27 above)

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 27

28. Institutional capacity building and motivational measures (various)

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 28

APPENDIX 2B – ADB submission on Cambodia PFMRP, Stage 2 Framework

(Prepared by ADB PPTA No. 4988CAM-Preparing for Strengthening of Public Financial Management for Rural Development)

1. Following significant progress with Stage I of the Public Financial Management Reform Program (PFMRP) between 2005 and 2007, the Ministry of Economy and Finance (MEF) has prepared, in consultation with development partners (DPs), a framework for implementing Stage 2 of the PFMRP from 2008 to 2010. MEF has circulated a draft document Building on Improved Budget Credibility toward Achieving Better Financial Accountability, which outlines the proposed second stage and the second platform of the PFMRP. (The version provided was Final Draft dated 19 March 2008.)

2. The Asian Development Bank (ADB) strongly supports the commencement of Stage 2 of the PFMRP as soon as possible in 2008 and endorses the framework document as a suitable basis for Stage 2 implementation. However, ADB considers that the document could be strengthened in a number of places by drafting changes, prior to its consideration at the annual review in April-May 2008 and endorsement by Government. The following comments are provided to assist in making those drafting changes.

1. Continuing Platform 1 Activities

3. It has been recognized in various reviews of the PFM program, eg the 2007 External Advisory Panel (EAP) report, that there would be a need to continue to deepen most Platform 1 reform activities well beyond the nominal implementation period, ie 2005 to 2007. It appears that most Platform 1 activities are being carried forward into Stage 2 with the exception of activities 2-budget impact on expenditure categories and 12-post-budget supplementary approvals which seem to be regarded as completed. It should be confirmed that these activities are now completed.

2. Stage 1 Activities which were prerequisites for Platform 2

4. With regard to activities which commenced in Stage 1 as prerequisites for later platforms, most have been included in Stage 2 in some form but with a number of exceptions. These exceptions are:

In Stage 1 financial controllers were out-posted from MEF’s Financial Affairs Department to a number of line ministries to streamline the commitments and payments process. Activity 24 deals in part with further streamlining of the commitments and payments system; however there is no mention of further out-posting to line ministries which did not receive a financial controller in Stage 1.

MEF completed several pilot public expenditure tracking surveys (PETS) in 2007. There are no continuing PETS activities shown in the document and it is unclear whether it is proposed to carry out more surveys during Stage 2. If further surveys are intended, this should be clarified in the document;

PFM Stage 1 had an activity (Activity 28) to develop an MEF IT strategy (separate from the FMIS activity). The 2007 External Advisory Panel review noted that it was unclear whether the ICT Unit in MEF or the Economics and Finance Institute (EFI) had main responsibility for IT planning and that this issue should be resolved. It now appears that a broader IT planning activity has been replaced by a plan to implement an MEF LAN/WAN (Activity 28a). It should be confirmed that it is no longer intended to develop a broad IT strategy;

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 29

Stage 1 Activity 29 provided for completion of a government asset register by entering inventory data into the database which had been developed. This activity was incomplete in early 2007; however, there is no mention of it in the Stage 2 document and it is unclear whether the activity has been completed since 2007 or has been terminated. Terminating this activity, if incomplete, would not be consistent with the plans to develop accrual-based accounting in Platform 2;

3. Other comments on Stage 2 activities

5. More general comments with regard to Stage 2 activities include:

Capacity development of internal audit staff was a separate activity in Platform 1. In Platform 2 (Activity 26), preparation and implementation of internal audit training and a manual are stated as key targets. However, a specific training component has not been included in this activity. This issue is of particular interest to the ADB as one of the major outputs of ADB PPTA project no. 4988-Preparing the Strengthening of Public Financial Management for Rural Development Project will be to identify a set of measures necessary to establish an effective internal audit function in MAFF, MOWRAM and MRD;

For activity 27 on strengthening fiscal decentralization, it should be made clear that activities 27.6 and 27.7 are necessary prerequisites to completing other activities in the section. Specifically, it will be necessary for MEF to determine in consultation with the National Committee on D and D what resources will be transferred from the central government to lower levels and what continuing funding arrangements (shared revenue, fiscal grants etc) will apply, before activities 27.1 to 27.4 can be completed fully. Similarly, some knowledge of which expenditure functions are to be assigned or delegated to the various levels by the National Committee will be needed before these activities can be carried out properly. To put the proposed financial arrangements on a firm legal basis, it would be useful to identify enactment of the proposed Law on Financial Regime and Management of Assets of Sub-national Administrations as a specific activity in Stage 2;

Under Activity 23 relating to the new chart of accounts and budget classification, a key target is to have completed piloting of accrual accounting in pilot line ministries in 2009 and 2010. However, there are no actions for implementing accrual accounting or training staff in line ministries. It is also noted that in the joint review mission in late 2007 concern was raised that introducing accrual accounting in the short or medium term may be infeasible because of the lack of suitably qualified accountants in MEF;

The PFM Capacity Development Plan shown in Annexe 5 does not appear to be linked to any specific activity in Platform 2 (although there are numerous references to individual training or capacity building actions). It would seem to fit logically with Activity 28a.

4. Involvement of Line Ministries

6. Annex 3 of the PFM draft includes descriptions of PFM Platform 2 activities which will require active engagement by line ministries. These actions comprise a comprehensive range of activities by line ministries but have some major omissions:

While it is proposed to complete the coverage of internal audit in all line ministries in Stage 2, the document does not detail any concrete actions which line ministries will be required to undertake to implement/improve the internal audit function. As indicated in the previous section this is an issue of particular interest to ADB in its continuing PPTA No. 4988CAM-Preparing the Strengthening of Public Financial Management in Rural Development Project;

In Annex 3, it is proposed that line ministries should design their own policies, strategies and manuals for carrying out functional reviews and that they undertake their own reviews. ADB considers that ministries will require considerable guidance from MEF or TA support to carry out

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 30

functional reviews and the need for this support should be reflected in the document. ADB TA 4988CAM will undertake functional reviews of the finance and planning (as relates to budget planning and execution) departments in the Ministries of Agriculture, Forestry and Fisheries, Water Resources and Meteorology and Rural Development over the next few months and the experience gained from those reviews should provide guidance for MEF and other line ministries carrying out functional reviews;

Although line ministries are intended presumably to be involved in developing the MTEF (Objective 32.1) and program budgeting (Objective 31) there are no specific actions in Annex 3 which will require their involvement;

There are no activities to involve line ministries in further improvements in the payments and commitments system or in the development of FMIS beyond a small number of ministry pilots by 2010. (See also comments above about out posting financial controllers to line ministries.) Completion of these activities is essential if effective control of and accountability for government expenditure is to be achieved and consideration should be given to extending this activity to all ministries by 2010;

There is no activity to engage line ministries in the consolidation of bank accounts (Activity 13.1), even though ministries are known to hold large numbers of accounts, albeit that many of these are donor project accounts which cannot realistically be closed in the short-term. Concrete actions should be included to require line ministries to justify the retention of all bank accounts which they would wish to maintain;

It is unclear whether line ministries are holding any payment arrears (or whether arrears have been consolidated by MEF) and whether they should in consequence be engaged in the exercise to liquidate arrears (Activity 13.4);

In the Capacity Development Plan (Annex 5) consideration might be given to specifying what underlying professional skills development, MEF, line ministries and their staffs will require. Some possible areas are further formal training in economics, accounting finance and auditing, legal studies, English language (various levels), research skills and report writing skills. To the motivational development measures could be added annual performance evaluations of all staff, career planning for all staff (not just high flyers) and introduction of a civil service code of conduct.

7. The process for engagement of line ministries in Stage 2 is strongly supported. However, to keep line ministries on track to complete the objectives of Stage 2 consideration should be given to making their activities time bound (possibly in the high level performance measures in Annex 7).

5. Performance Indicators-Annex 7

8. Monitoring of performance under CAP2 will include continued preparation of five of the fifteen performance indicators from Platform 1 (revenue outturn, real annual revenue increases, no new arrears and expenditures in line with budgets).

9. Consideration should be given to retaining performance indicator 9-all significant areas of both revenue and expenditure captured in both the budget and accounts of the government. While significant progress has been made in improving budget comprehensiveness such as improved banking arrangements it is not clear that all significant revenues and expenditures which were previously off-budget have now been captured in the budget. It is noted that Activity 32.2 has a target of reducing off-budget government expenditure to less than one percent by 2010 and at least 75 percent of donor projects being included in budget estimates. Appropriate performance indicators should be developed to monitor these targets.

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 31

The ADB would appreciate consideration being given to the above comments during further revision of the draft document.

Asian Development Bank

1 April 2008

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

October 2008 Page 32

APPENDIX 3 - REVIEWS OF THE FINANCIAL MANAGEMENT AND PLANNING FUNCTIONS OF THE MAFF, MRD AND MWRM, FINAL REPORT

Final Report Cambodia: Preparing the Strengthening of Public Financial Management for Rural Development Projects

Reviews of the Financial Management and Planning Functions of the