Prepared by Diane Tanner University of North Florida Chapter 2 1 Normal Costing

Prepared by Diane Tanner University of North Florida Chapter 2 1 Normal Costing.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Prepared byDiane TannerUniversity of North Florida

Chapter 2

Normal Costing

Assigning Costs to Cost Objects

Actual

CostingNormal Costing

Standard Costing

Direct Materials Actual Actual Budgeted*

Direct Labor Actual Actual Budgeted*

Manufacturing Overhead Actual Budgeted Budgeted*

• Three methods– Actual costing – Normal costing– Standard costing

• Differ in how product costs are assigned to products or services

2

3

Normal Vs. Actual Costing• Normal costing

– Used effectively when there are multiple products– Allocates manufacturing overhead to individual

products based on a ‘predetermined’ rate calculation

–Based on estimates

• Actual costing– Allocates manufacturing overhead to individual

products based on an end of period rate calculation –Based on actual amounts

Estimated MOHEstimated Activity

Actual MOHActual Activity

4

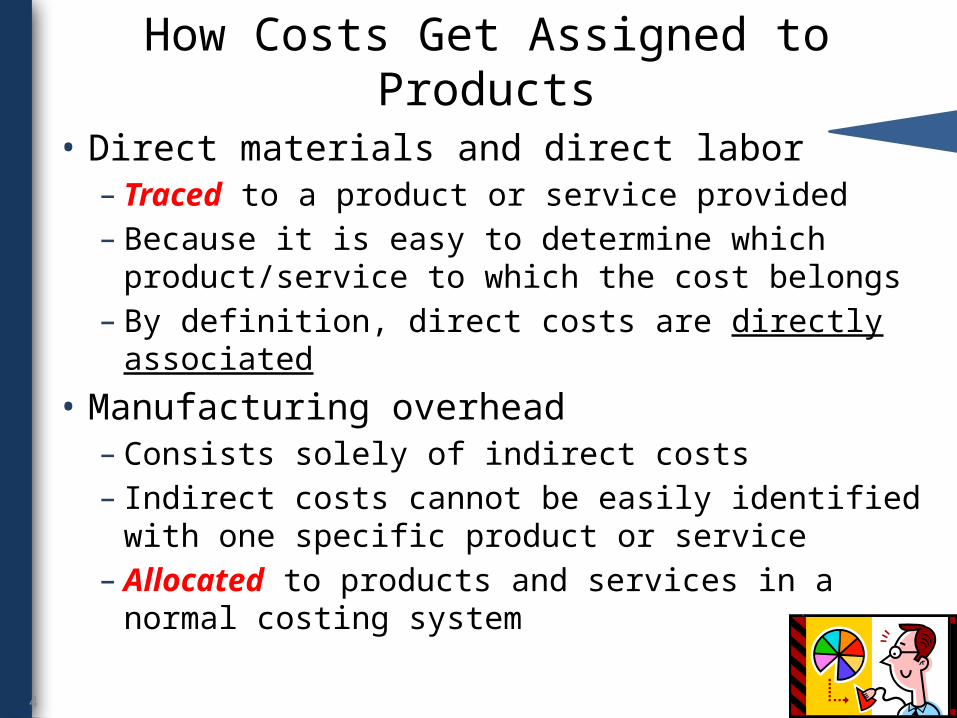

How Costs Get Assigned to Products

• Direct materials and direct labor– Traced to a product or service provided– Because it is easy to determine which

product/service to which the cost belongs – By definition, direct costs are directly associated

• Manufacturing overhead– Consists solely of indirect costs– Indirect costs cannot be easily identified with one

specific product or service– Allocated to products and services in a normal

costing system

5

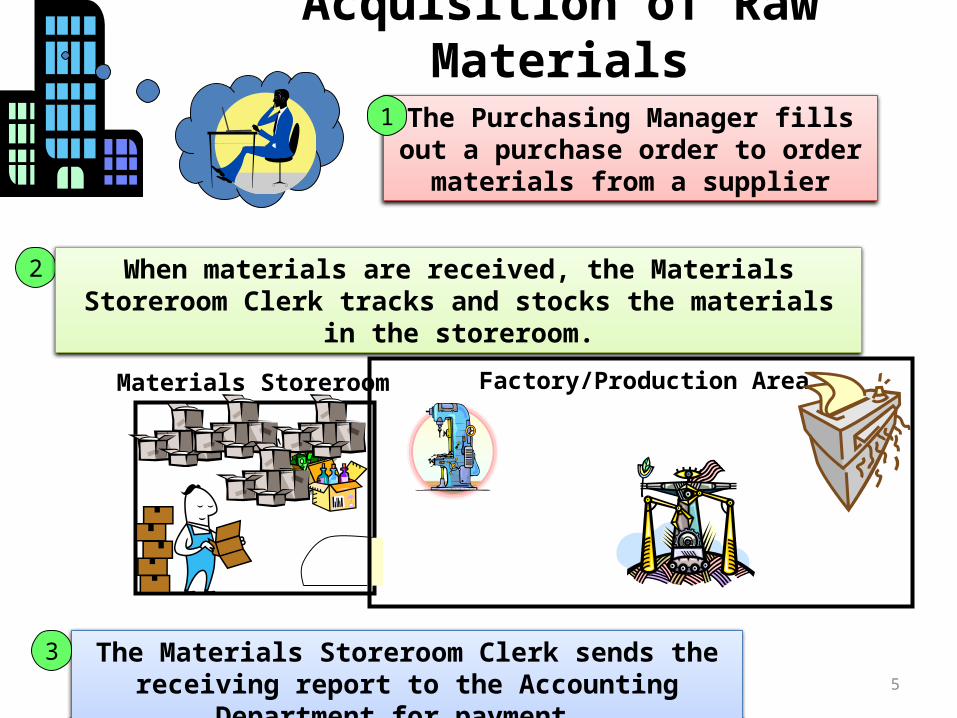

Acquisition of Raw Materials

Materials Storeroom Factory/Production Area

The Purchasing Manager fills out a purchase order to order materials

from a supplier

1

2 When materials are received, the Materials Storeroom Clerk tracks and stocks the materials in the storeroom.

The Materials Storeroom Clerk sends the receiving report to the Accounting Department for payment.

3

6

Transactions to Acquire Materials

Purchase Materials for Cash• Debit Raw Materials• Credit Cash Purchase Materials on Account• Debit Raw Materials• Credit Accounts Payable Pay for materials previously purchased on account• Debit Accounts Payable• Credit Cash• Credit Inventory for cash discount, if any

7

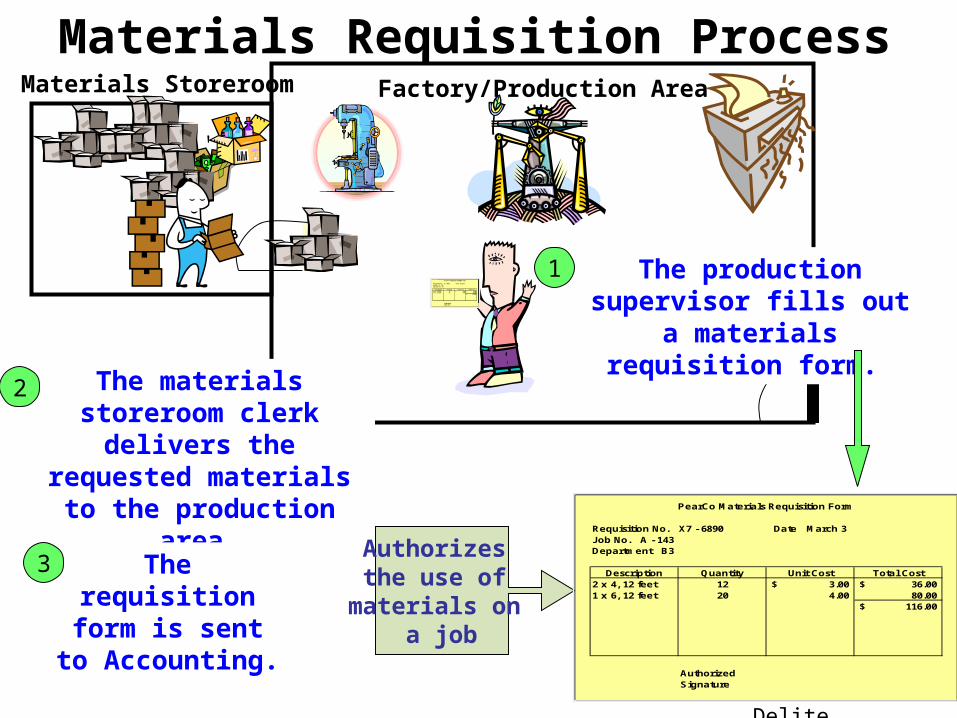

Materials Requisition ProcessMaterials Storeroom Factory/Production Area

The production supervisor fills out a materials requisition form.

PearCo Materials Requisition Form

Requisition No. X7 - 6890 Date March 3Job No. A - 143Department B3

Description Quantity Unit Cost Total Cost2 x 4, 12 feet 12 3.00$ 36.00$ 1 x 6, 12 feet 20 4.00 80.00

116.00$

Authorized Signature Will E.

Delite

1

The materials storeroom clerk delivers the

requested materials to the production area.

2

Authorizes the use of

materials on a job

The requisition form is sent to Accounting.

3

PearCo Materials Requisition Form

Requisition No. X7 - 6890 Date March 3Job No. A - 143Department B3

Description Quantity Unit Cost Total Cost2 x 4, 12 feet 12 3.00$ 36.00$ 1 x 6, 12 feet 20 4.00 80.00

116.00$

Authorized Signature

8

Accounting for Materials Used in Production

Requisition of Direct Materials to Production• Debit Work in Process • Credit Raw Materials Requisition Indirect Materials to Production• Debit Manufacturing Expense• Credit Raw Materials

9

Incurring Labor Costs

Materials Storeroom

Factory/Production Area

Employees use time tickets to record the time spent on each job

PearCo Employee Time Ticket

Time Ticket No. 36 Date March 4

Employee I. M. Skilled Station 42

Starting Ending Hours HourlyTime Time Completed Rate Amount Job No.0800 1600 8.00 11.00$ 88.00$ A-143

Totals 8.00 11.00$ 88.00$ A-143

Supervisor C. M. Workman

Measuring and Tracking Direct Labor

10

Direct labor cost = [Hourly rate] × [Number of hours worked]

Fringe benefits Normally included as part of the direct labor ‘rate’

Overtime premium (the extra ‘half’ time paid) If the result of production problems, treat as

manufacturing overhead If the result of accepting a rush order, treat as direct

labor Idle time

Treat as overhead Because it is not part of the cost to get inventory

ready to sell

11

Accounting for Labor Costs Used in Production

Direct Labor Costs Incurred• Debit Work in Process• Credit Cash, salaries payable, etc.Indirect Labor Costs incurred• Debit MOH expense• Credit Cash, salaries payable, etc.

‘Applying’ MOH under Normal Costing

• What is ‘applying overhead’? – The process of adding MOH cost to products

based on an allocation rate• Why is MOH applied using normal costing?

– It is an indirect cost, which is impossible or impractical to trace to a particular product

– Managers need to know job costs as production occurs, i.e., on a timely basis• For making decisions such as pricing, product

changes, etc. – Waiting until the end of the period when actual

costs are known makes information untimely

12

13

Accounting for MOH Using Normal Costing

Incur MOH Costs• Debit Manufacturing Overhead (control account) • Credit Cash, salaries payable, etcApply MOH to Products• Debit Work in Process• Credit Manufacturing Overhead

Using a predetermined rate

14

The End

Related Documents