PRACTICAL PLANNED GIVING IN CONGREGATIONS

PRACTICAL PLANNED GIVING IN CONGREGATIONS. Planned Giving – in General: What is it? ANNUAL GIVINGPLANNED GIVING.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PRACTICAL PLANNED GIVINGIN CONGREGATIONS

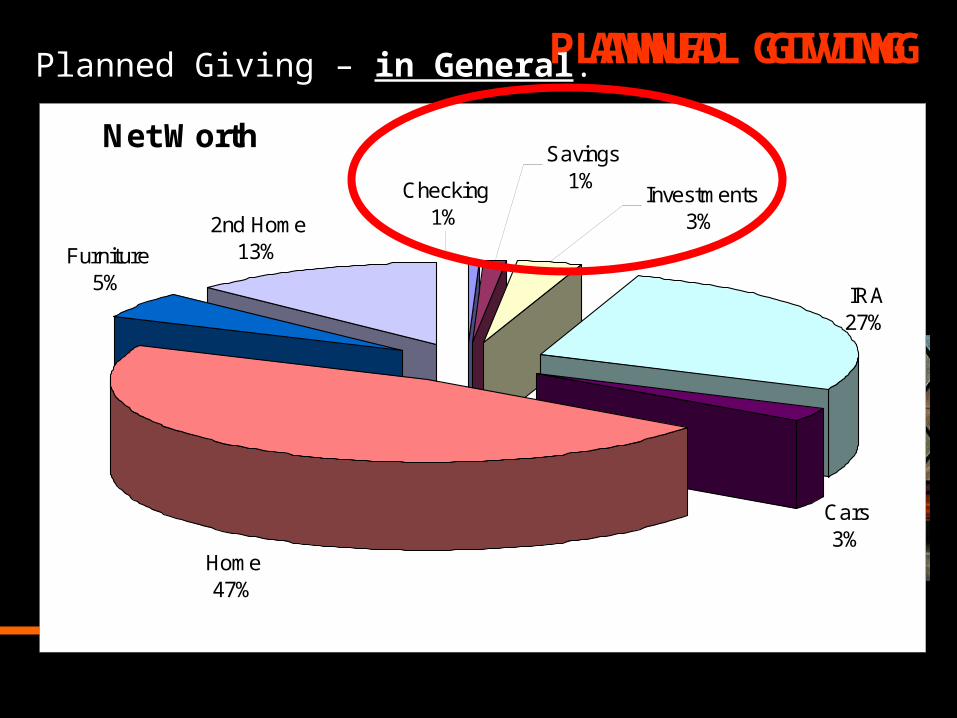

Planned Giving – in General:

What is it?Net Worth

IRA27%

Cars3%

Home47%

2nd Home13%

Checking1%

Investments3%

Savings1%

Furniture5%

ANNUAL GIVINGPLANNED GIVING

Planned Giving

In 2008 bequests to charities totaled $22,600,000,000.

This has caught the attention of major charities, and they have allocated significant resources to pursuing planned gifts.

Those charities are run like a business. They’ve hired staff, assigned goals, developed enormous marketing budgets and

brought in vast sums of money.

Planned Giving

Universities, hospitals, museums, arts, health societies, retirement communities, etc.

Think about: What are your top 5-10 organizations?

What are they doing?

Planned Giving

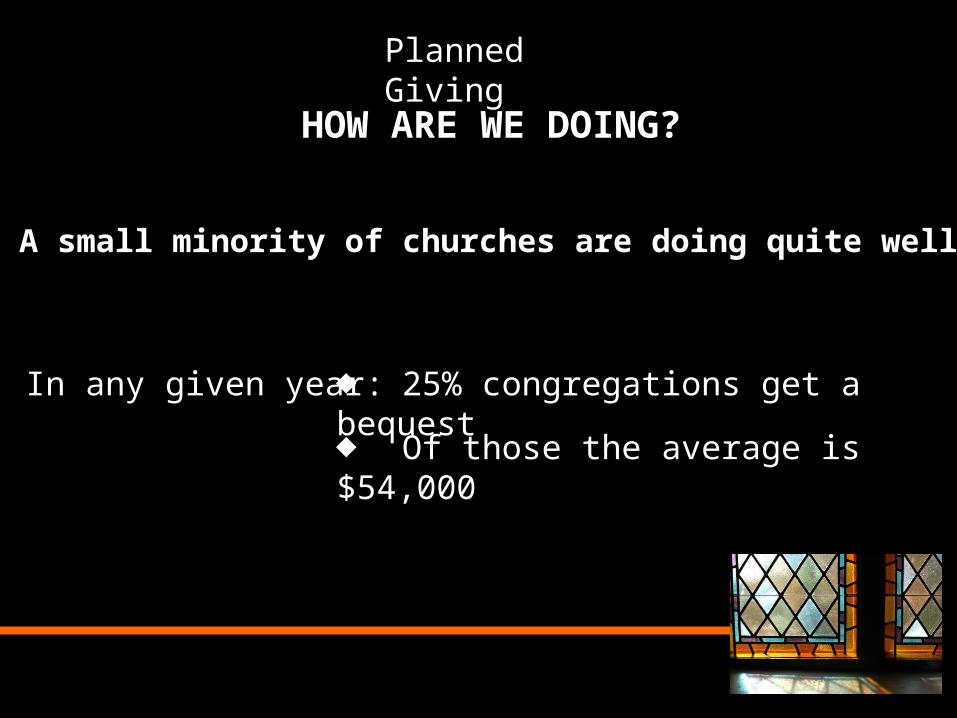

HOW ARE WE DOING?

In any given year: 25% congregations get a bequest

Of those the average is $54,000

A small minority of churches are doing quite well.

Planned Giving

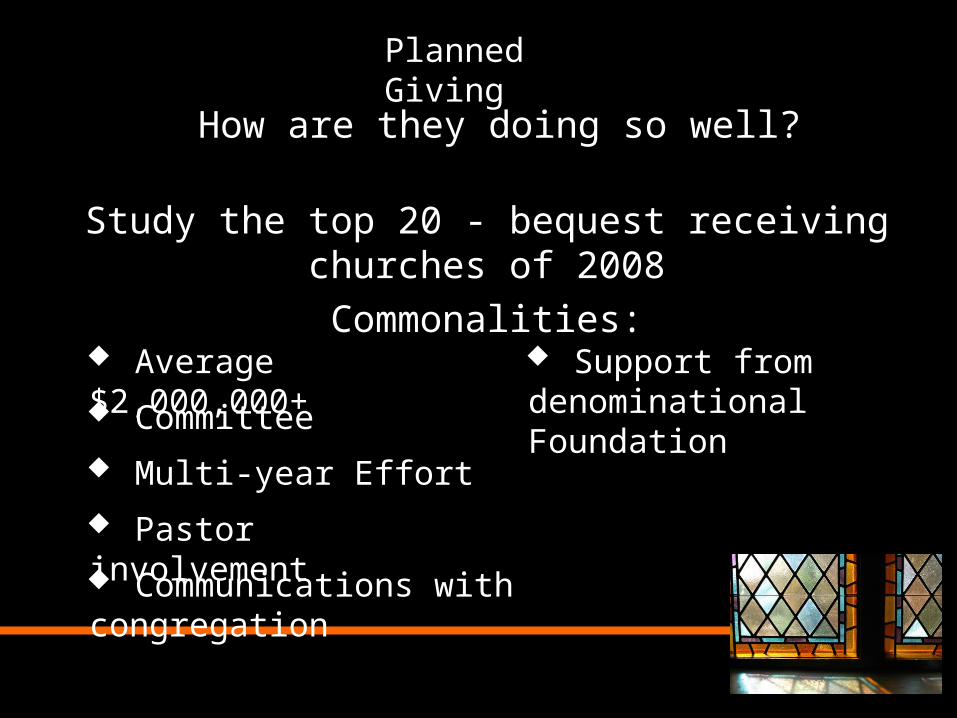

How are they doing so well?

Study the top 20 - bequest receiving churches of 2008

Commonalities:

Average $2,000,000+

Committee

Multi-year Effort

Pastor involvement

Communications with congregation

Support from denominational Foundation

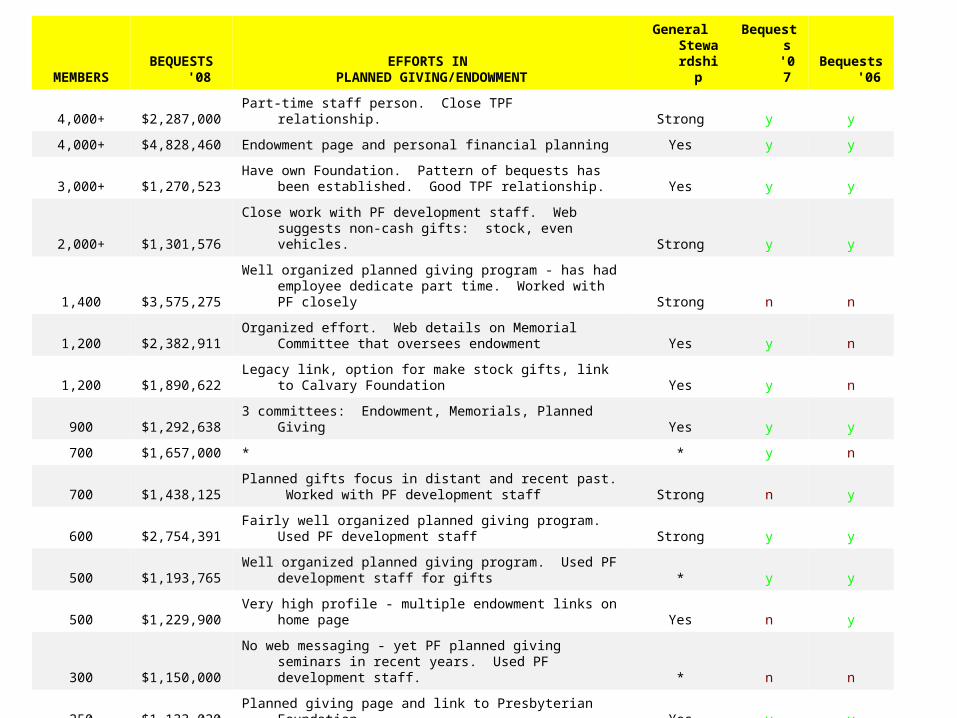

MEMBERS

BEQUESTS '08

EFFORTS IN PLANNED GIVING/ENDOWMENT

General Stewardshi

p

Bequests '07

Bequests

'06

4,000+ $2,287,000 Part-time staff person. Close TPF relationship. Strong y y

4,000+ $4,828,460 Endowment page and personal financial planning Yes y y

3,000+ $1,270,523Have own Foundation. Pattern of bequests has been

established. Good TPF relationship. Yes y y

2,000+ $1,301,576Close work with PF development staff. Web suggests

non-cash gifts: stock, even vehicles. Strong y y

1,400 $3,575,275

Well organized planned giving program - has had employee dedicate part time. Worked with PF closely Strong n n

1,200 $2,382,911Organized effort. Web details on Memorial Committee

that oversees endowment Yes y n

1,200 $1,890,622Legacy link, option for make stock gifts, link to Calvary

Foundation Yes y n

900 $1,292,638 3 committees: Endowment, Memorials, Planned Giving Yes y y

700 $1,657,000 * * y n

700 $1,438,125Planned gifts focus in distant and recent past. Worked

with PF development staff Strong n y

600 $2,754,391Fairly well organized planned giving program. Used PF

development staff Strong y y

500 $1,193,765Well organized planned giving program. Used PF

development staff for gifts * y y

500 $1,229,900Very high profile - multiple endowment links on home

page Yes n y

300 $1,150,000No web messaging - yet PF planned giving seminars in

recent years. Used PF development staff. * n n

250 $1,133,020Planned giving page and link to Presbyterian

Foundation Yes y y

125 $1,228,183 * (new church development)

Online pledg

e n n

100 $3,932,069 NF* * n y

100 $2,200,000 NF* * n n

75 $1,080,000 * Strong n n

60 $3,700,000 * Yes y n

Planned Giving

FUNDAMENTAL BEST PRACTICES

• Committee specifically on Planned Giving, diverse membership

• Policies and Guidelines

• Investment – often under auspices of separate committee • Committee Charter and Guidelines; roles, responsibilities, reporting

• Gift / Donation Acceptance Policy

• Annual Report – financial information and gift impact information

• Endowment Policy; distribution policy, spending policy

• Leadership education

• Leadership participation; gifts and support

• Case Statement

Planned Giving

FUNDAMENTAL BEST PRACTICES continued

• Pastor support and involvement

• Sermons• Basic knowledge of and comfort with planned giving

• Congregational Communications

• Regular communications; newsletter, bulletins, minute for mission• Recognize wills emphasis Sunday

• USE THE PRESBYTERIAN FOUNDATION• Highly skilled professionals employed to support you

• High quality print materials for churches

• Manage the gift tools for your Church

Understand the planned giving tools

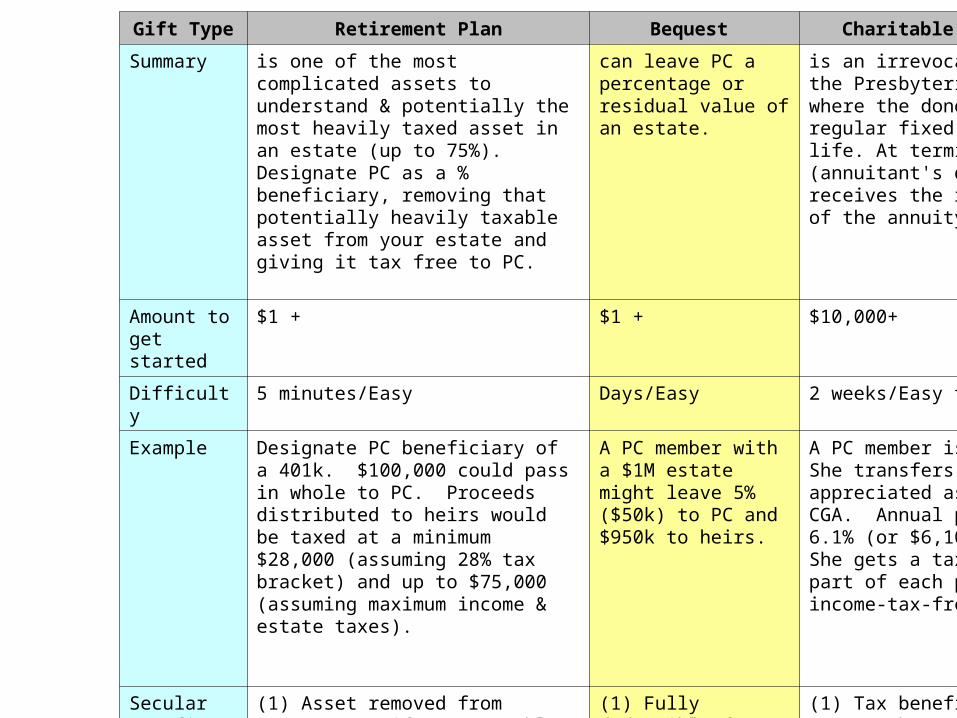

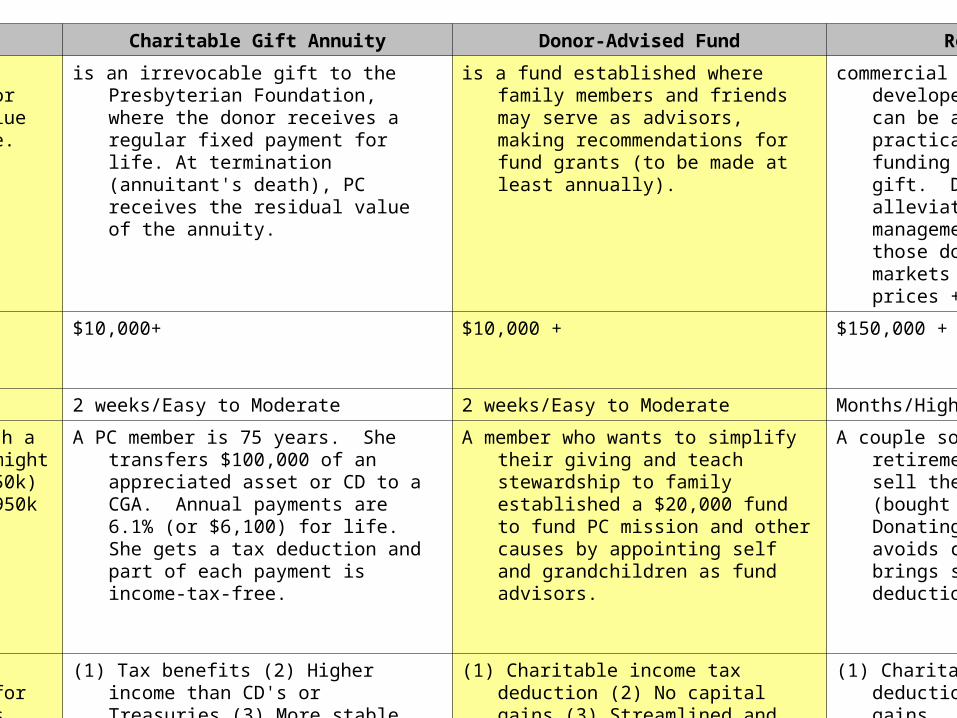

Gift Type Retirement Plan Bequest Charitable Gift Annuity Donor-Advised Fund Real Estate Charitable Remaindr Trst Life Insurance

Summary is one of the most complicated assets to understand & potentially the most heavily taxed asset in an estate (up to 75%). Designate PC as a % beneficiary, removing that potentially heavily taxable asset from your estate and giving it tax free to PC.

can leave PC a percentage or residual value of an estate.

is an irrevocable gift to the Presbyterian Foundation, where the donor receives a regular fixed payment for life. At termination (annuitant's death), PC receives the residual value of the annuity.

is a fund established where family members and friends may serve as advisors, making recommendations for fund grants (to be made at least annually).

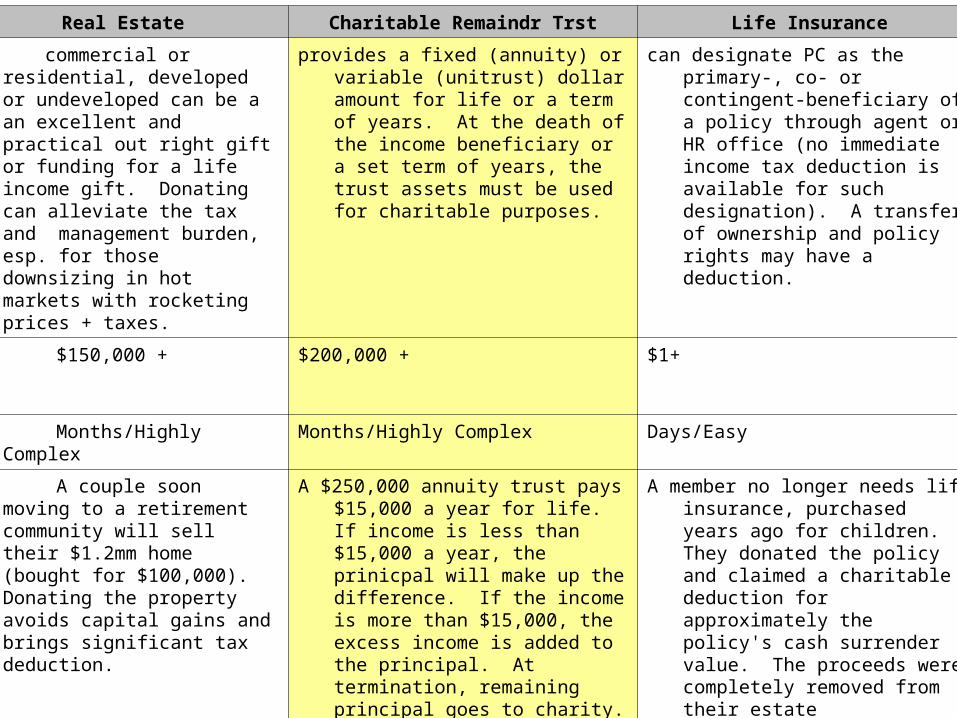

commercial or residential, developed or undeveloped can be a an excellent and practical out right gift or funding for a life income gift. Donating can alleviate the tax and management burden, esp. for those downsizing in hot markets with rocketing prices + taxes.

provides a fixed (annuity) or variable (unitrust) dollar amount for life or a term of years. At the death of the income beneficiary or a set term of years, the trust assets must be used for charitable purposes.

can designate PC as the primary-, co- or contingent-beneficiary of a policy through agent or HR office (no immediate income tax deduction is available for such designation). A transfer of ownership and policy rights may have a deduction.

Amount to get started

$1 + $1 + $10,000+ $10,000 + $150,000 + $200,000 + $1+

Difficulty 5 minutes/Easy Days/Easy 2 weeks/Easy to Moderate 2 weeks/Easy to Moderate Months/Highly Complex Months/Highly Complex Days/Easy

Example Designate PC beneficiary of a 401k. $100,000 could pass in whole to PC. Proceeds distributed to heirs would be taxed at a minimum $28,000 (assuming 28% tax bracket) and up to $75,000 (assuming maximum income & estate taxes).

A PC member with a $1M estate might leave 5% ($50k) to PC and $950k to heirs.

A PC member is 75 years. She transfers $100,000 of an appreciated asset or CD to a CGA. Annual payments are 6.1% (or $6,100) for life. She gets a tax deduction and part of each payment is income-tax-free.

A member who wants to simplify their giving and teach stewardship to family established a $20,000 fund to fund PC mission and other causes by appointing self and grandchildren as fund advisors.

A couple soon moving to a retirement community will sell their $1.2mm home (bought for $100,000). Donating the property avoids capital gains and brings significant tax deduction.

A $250,000 annuity trust pays $15,000 a year for life. If income is less than $15,000 a year, the prinicpal will make up the difference. If the income is more than $15,000, the excess income is added to the principal. At termination, remaining principal goes to charity.

A member no longer needs life insurance, purchased years ago for children. They donated the policy and claimed a charitable deduction for approximately the policy's cash surrender value. The proceeds were completely removed from their estate

Secular Benefits

(1) Asset removed from estate (2) Gift not taxable to PC, but would be to heirs (3) no immediate financial commitment

(1) Fully deductible for estate taxes

(1) Tax benefits (2) Higher income than CD's or Treasuries (3) More stable than equities (4) Significant support to PC

(1) Charitable income tax deduction (2) No capital gains (3) Streamlined and efficient gifting mechanism

(1) Charitable income tax deduction (2) No capital gains

(1) Reduce estate size & potential tax (2) capture long-term capital gain without immediate tax (3) Create charitable deduction (4) Funding asset protected

(1) Possible income, estate and gift tax relief (2) Remove asset from estate

Does this fit you?

(1) I love PC (2) My assets are locked up (3) I can not part with this today, becase I may need it in the future (4) My successors might redeem this at a great tax expense

(1) I love PC (2) I want to make major gift (3) Assets are locked up, and I may need them in the future.

(1) I love PC (2) I have financial resources, but they are working to earn my income (3) I could use a higher income and more stable source of income (4) I have capital gains on assets

(1) I love PC (2) I want a culture of giving in my family (3) I want to support PC and other charities (4) I wish to streamline my giving

(1) I love PC (2) I inherited estate/ property that can't afford/ manage (3) I am downsizing (4) I can't afford to stay, but can't afford to leave (retained life estate)

(1) I love PC (2) My heirs may be affect by estate tax (3) I may wish to protect heirs from visible high net worth (disqualify from special needs, target for litigation, spendthrift, etc.)

(1) I love PC (2) My beneficiaries no longer need my insurance (3) I am exploring other assets as gift opportunities

Gift Type Retirement Plan Bequest Charitable Gift Annuity Donor-Advised Fund Real Estate Charitable Remaindr Trst Life Insurance

Summary is one of the most complicated assets to understand & potentially the most heavily taxed asset in an estate (up to 75%). Designate PC as a % beneficiary, removing that potentially heavily taxable asset from your estate and giving it tax free to PC.

can leave PC a percentage or residual value of an estate.

is an irrevocable gift to the Presbyterian Foundation, where the donor receives a regular fixed payment for life. At termination (annuitant's death), PC receives the residual value of the annuity.

is a fund established where family members and friends may serve as advisors, making recommendations for fund grants (to be made at least annually).

commercial or residential, developed or undeveloped can be a an excellent and practical out right gift or funding for a life income gift. Donating can alleviate the tax and management burden, esp. for those downsizing in hot markets with rocketing prices + taxes.

provides a fixed (annuity) or variable (unitrust) dollar amount for life or a term of years. At the death of the income beneficiary or a set term of years, the trust assets must be used for charitable purposes.

can designate PC as the primary-, co- or contingent-beneficiary of a policy through agent or HR office (no immediate income tax deduction is available for such designation). A transfer of ownership and policy rights may have a deduction.

Amount to get started

$1 + $1 + $10,000+ $10,000 + $150,000 + $200,000 + $1+

Difficulty 5 minutes/Easy Days/Easy 2 weeks/Easy to Moderate 2 weeks/Easy to Moderate Months/Highly Complex Months/Highly Complex Days/Easy

Example Designate PC beneficiary of a 401k. $100,000 could pass in whole to PC. Proceeds distributed to heirs would be taxed at a minimum $28,000 (assuming 28% tax bracket) and up to $75,000 (assuming maximum income & estate taxes).

A PC member with a $1M estate might leave 5% ($50k) to PC and $950k to heirs.

A PC member is 75 years. She transfers $100,000 of an appreciated asset or CD to a CGA. Annual payments are 6.1% (or $6,100) for life. She gets a tax deduction and part of each payment is income-tax-free.

A member who wants to simplify their giving and teach stewardship to family established a $20,000 fund to fund PC mission and other causes by appointing self and grandchildren as fund advisors.

A couple soon moving to a retirement community will sell their $1.2mm home (bought for $100,000). Donating the property avoids capital gains and brings significant tax deduction.

A $250,000 annuity trust pays $15,000 a year for life. If income is less than $15,000 a year, the prinicpal will make up the difference. If the income is more than $15,000, the excess income is added to the principal. At termination, remaining principal goes to charity.

A member no longer needs life insurance, purchased years ago for children. They donated the policy and claimed a charitable deduction for approximately the policy's cash surrender value. The proceeds were completely removed from their estate

Secular Benefits (1) Asset removed from estate (2) Gift not taxable to PC, but would be to heirs (3) no immediate financial commitment

(1) Fully deductible for estate taxes

(1) Tax benefits (2) Higher income than CD's or Treasuries (3) More stable than equities (4) Significant support to PC

(1) Charitable income tax deduction (2) No capital gains (3) Streamlined and efficient gifting mechanism

(1) Charitable income tax deduction (2) No capital gains

(1) Reduce estate size & potential tax (2) capture long-term capital gain without immediate tax (3) Create charitable deduction (4) Funding asset protected

(1) Possible income, estate and gift tax relief (2) Remove asset from estate

Does this fit you?

(1) I love PC (2) My assets are locked up (3) I can not part with this today, becase I may need it in the future (4) My successors might redeem this at a great tax expense

(1) I love PC (2) I want to make major gift (3) Assets are locked up, and I may need them in the future.

(1) I love PC (2) I have financial resources, but they are working to earn my income (3) I could use a higher income and more stable source of income (4) I have capital gains on assets

(1) I love PC (2) I want a culture of giving in my family (3) I want to support PC and other charities (4) I wish to streamline my giving

(1) I love PC (2) I inherited estate/ property that can't afford/ manage (3) I am downsizing (4) I can't afford to stay, but can't afford to leave (retained life estate)

(1) I love PC (2) My heirs may be affect by estate tax (3) I may wish to protect heirs from visible high net worth (disqualify from special needs, target for litigation, spendthrift, etc.)

(1) I love PC (2) My beneficiaries no longer need my insurance (3) I am exploring other assets as gift opportunities

Gift Type Retirement Plan Bequest Charitable Gift Annuity Donor-Advised Fund Real Estate Charitable Remaindr Trst Life Insurance

Summary is one of the most complicated assets to understand & potentially the most heavily taxed asset in an estate (up to 75%). Designate PC as a % beneficiary, removing that potentially heavily taxable asset from your estate and giving it tax free to PC.

can leave PC a percentage or residual value of an estate.

is an irrevocable gift to the Presbyterian Foundation, where the donor receives a regular fixed payment for life. At termination (annuitant's death), PC receives the residual value of the annuity.

is a fund established where family members and friends may serve as advisors, making recommendations for fund grants (to be made at least annually).

commercial or residential, developed or undeveloped can be a an excellent and practical out right gift or funding for a life income gift. Donating can alleviate the tax and management burden, esp. for those downsizing in hot markets with rocketing prices + taxes.

provides a fixed (annuity) or variable (unitrust) dollar amount for life or a term of years. At the death of the income beneficiary or a set term of years, the trust assets must be used for charitable purposes.

can designate PC as the primary-, co- or contingent-beneficiary of a policy through agent or HR office (no immediate income tax deduction is available for such designation). A transfer of ownership and policy rights may have a deduction.

Amount to get started

$1 + $1 + $10,000+ $10,000 + $150,000 + $200,000 + $1+

Difficulty 5 minutes/Easy Days/Easy 2 weeks/Easy to Moderate 2 weeks/Easy to Moderate Months/Highly Complex Months/Highly Complex Days/Easy

Example Designate PC beneficiary of a 401k. $100,000 could pass in whole to PC. Proceeds distributed to heirs would be taxed at a minimum $28,000 (assuming 28% tax bracket) and up to $75,000 (assuming maximum income & estate taxes).

A PC member with a $1M estate might leave 5% ($50k) to PC and $950k to heirs.

A PC member is 75 years. She transfers $100,000 of an appreciated asset or CD to a CGA. Annual payments are 6.1% (or $6,100) for life. She gets a tax deduction and part of each payment is income-tax-free.

A member who wants to simplify their giving and teach stewardship to family established a $20,000 fund to fund PC mission and other causes by appointing self and grandchildren as fund advisors.

A couple soon moving to a retirement community will sell their $1.2mm home (bought for $100,000). Donating the property avoids capital gains and brings significant tax deduction.

A $250,000 annuity trust pays $15,000 a year for life. If income is less than $15,000 a year, the prinicpal will make up the difference. If the income is more than $15,000, the excess income is added to the principal. At termination, remaining principal goes to charity.

A member no longer needs life insurance, purchased years ago for children. They donated the policy and claimed a charitable deduction for approximately the policy's cash surrender value. The proceeds were completely removed from their estate

Secular Benefits

(1) Asset removed from estate (2) Gift not taxable to PC, but would be to heirs (3) no immediate financial commitment

(1) Fully deductible for estate taxes

(1) Tax benefits (2) Higher income than CD's or Treasuries (3) More stable than equities (4) Significant support to PC

(1) Charitable income tax deduction (2) No capital gains (3) Streamlined and efficient gifting mechanism

(1) Charitable income tax deduction (2) No capital gains

(1) Reduce estate size & potential tax (2) capture long-term capital gain without immediate tax (3) Create charitable deduction (4) Funding asset protected

(1) Possible income, estate and gift tax relief (2) Remove asset from estate

Does this fit you?

(1) I love PC (2) My assets are locked up (3) I can not part with this today, becase I may need it in the future (4) My successors might redeem this at a great tax expense

(1) I love PC (2) I want to make major gift (3) Assets are locked up, and I may need them in the future.

(1) I love PC (2) I have financial resources, but they are working to earn my income (3) I could use a higher income and more stable source of income (4) I have capital gains on assets

(1) I love PC (2) I want a culture of giving in my family (3) I want to support PC and other charities (4) I wish to streamline my giving

(1) I love PC (2) I inherited estate/ property that can't afford/ manage (3) I am downsizing (4) I can't afford to stay, but can't afford to leave (retained life estate)

(1) I love PC (2) My heirs may be affect by estate tax (3) I may wish to protect heirs from visible high net worth (disqualify from special needs, target for litigation, spendthrift, etc.)

(1) I love PC (2) My beneficiaries no longer need my insurance (3) I am exploring other assets as gift opportunities

Planned Giving RESOURCES

Planned Giving

RESOURCES

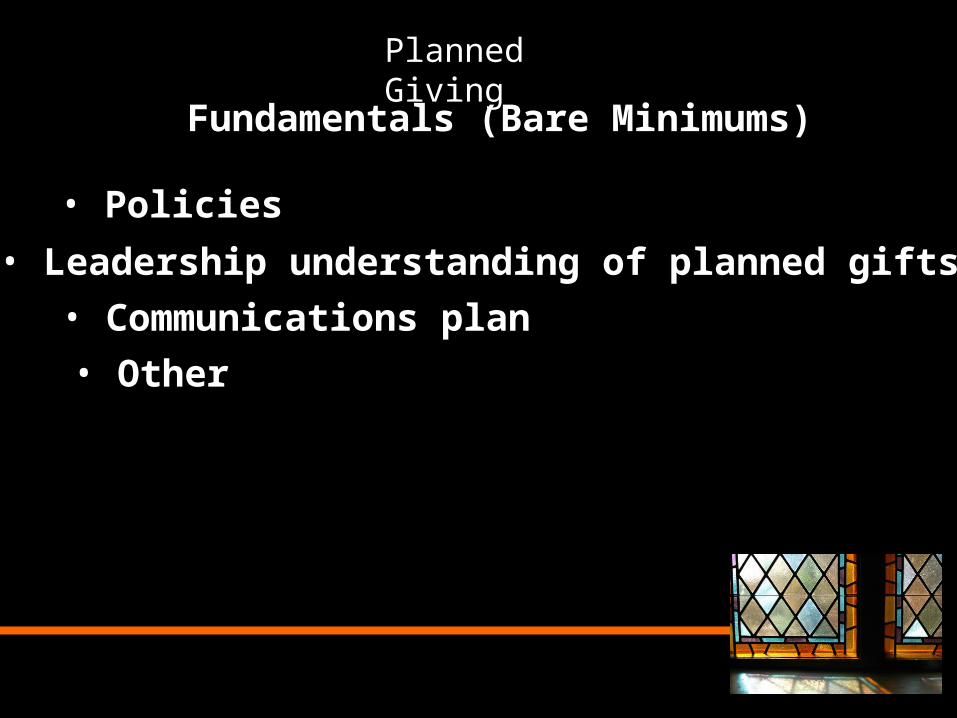

Planned Giving

Fundamentals (Bare Minimums)

• Policies

• Leadership understanding of planned gifts

• Communications plan

• Other

Related Documents