MODULE - A Indian Financial System – An Overview 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MODULE - AIndian Financial System – An Overview

1

A financial system means

Savings are transformed into investments

Through Financial Intermediaries

2

Reserve Bank of India (RBI)

• RBI was constituted under the RBI Act 1934 and started on 01.04.1935.

• Control of RBI vests with the Central Board of Directors, that comprises the

Governor, Four Deputy Governors and 12 Directors and 4 others- one each

from local board.

6

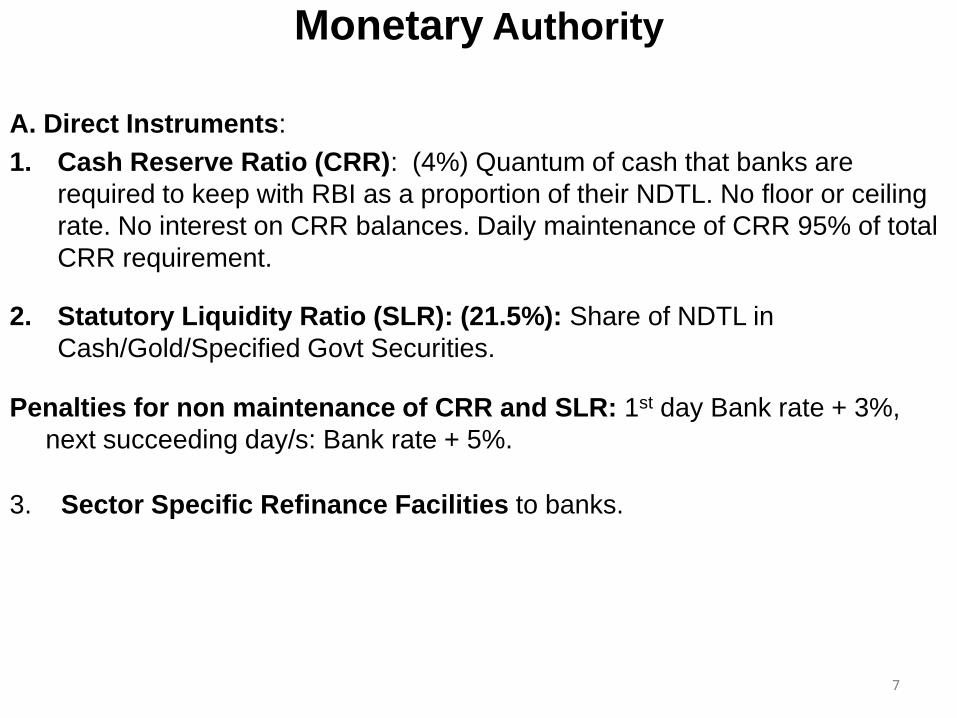

Monetary Authority

A. Direct Instruments:

1. Cash Reserve Ratio (CRR): (4%) Quantum of cash that banks are

required to keep with RBI as a proportion of their NDTL. No floor or ceiling

rate. No interest on CRR balances. Daily maintenance of CRR 95% of total

CRR requirement.

2. Statutory Liquidity Ratio (SLR): (21.5%): Share of NDTL in

Cash/Gold/Specified Govt Securities.

Penalties for non maintenance of CRR and SLR: 1st day Bank rate + 3%,

next succeeding day/s: Bank rate + 5%.

3. Sector Specific Refinance Facilities to banks.

7

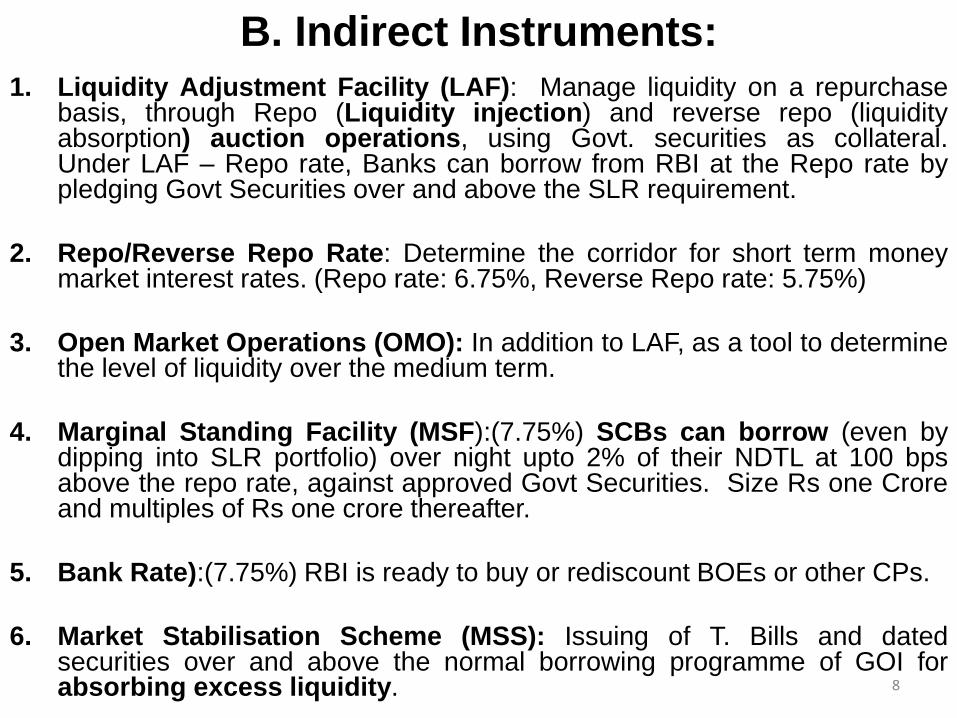

B. Indirect Instruments:1. Liquidity Adjustment Facility (LAF): Manage liquidity on a repurchase

basis, through Repo (Liquidity injection) and reverse repo (liquidityabsorption) auction operations, using Govt. securities as collateral.Under LAF – Repo rate, Banks can borrow from RBI at the Repo rate bypledging Govt Securities over and above the SLR requirement.

2. Repo/Reverse Repo Rate: Determine the corridor for short term moneymarket interest rates. (Repo rate: 6.75%, Reverse Repo rate: 5.75%)

3. Open Market Operations (OMO): In addition to LAF, as a tool to determinethe level of liquidity over the medium term.

4. Marginal Standing Facility (MSF):(7.75%) SCBs can borrow (even bydipping into SLR portfolio) over night upto 2% of their NDTL at 100 bpsabove the repo rate, against approved Govt Securities. Size Rs one Croreand multiples of Rs one crore thereafter.

5. Bank Rate):(7.75%) RBI is ready to buy or rediscount BOEs or other CPs.

6. Market Stabilisation Scheme (MSS): Issuing of T. Bills and datedsecurities over and above the normal borrowing programme of GOI forabsorbing excess liquidity. 8

Issuer of Currency

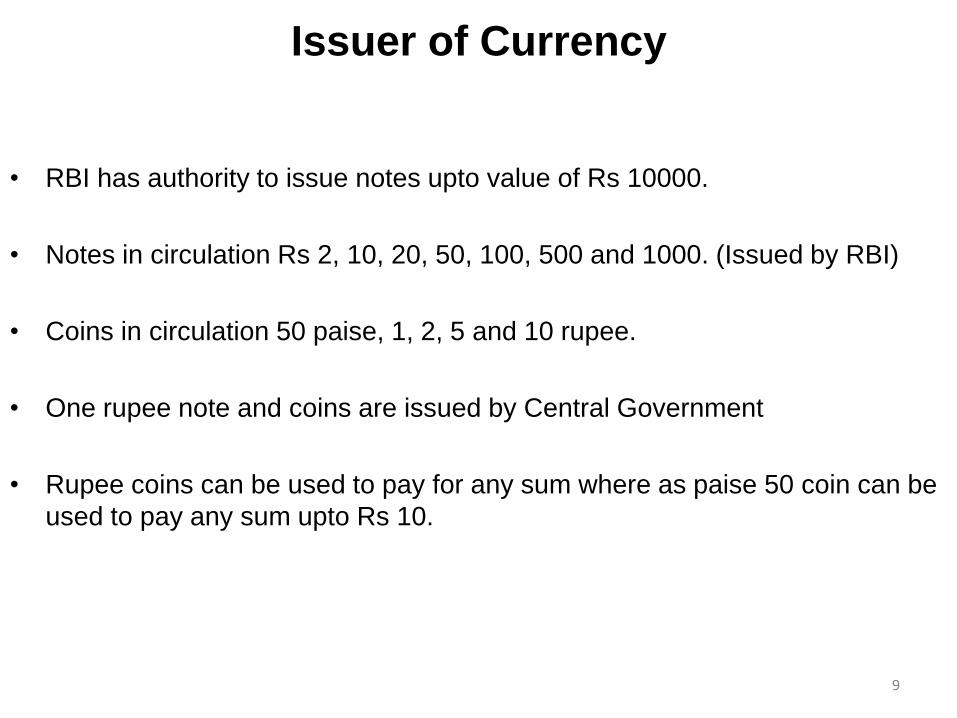

• RBI has authority to issue notes upto value of Rs 10000.

• Notes in circulation Rs 2, 10, 20, 50, 100, 500 and 1000. (Issued by RBI)

• Coins in circulation 50 paise, 1, 2, 5 and 10 rupee.

• One rupee note and coins are issued by Central Government

• Rupee coins can be used to pay for any sum where as paise 50 coin can be

used to pay any sum upto Rs 10.

9

Banker and Debt Manager to Govt

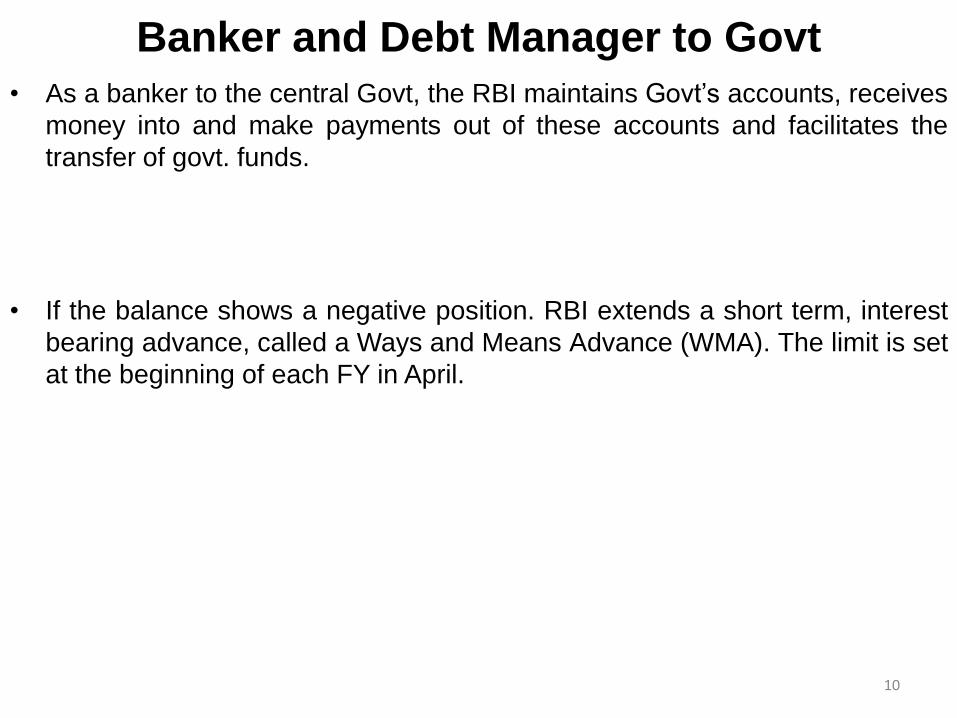

• As a banker to the central Govt, the RBI maintains Govt’s accounts, receives

money into and make payments out of these accounts and facilitates the

transfer of govt. funds.

• If the balance shows a negative position. RBI extends a short term, interest

bearing advance, called a Ways and Means Advance (WMA). The limit is set

at the beginning of each FY in April.

10

Bankers to Banks

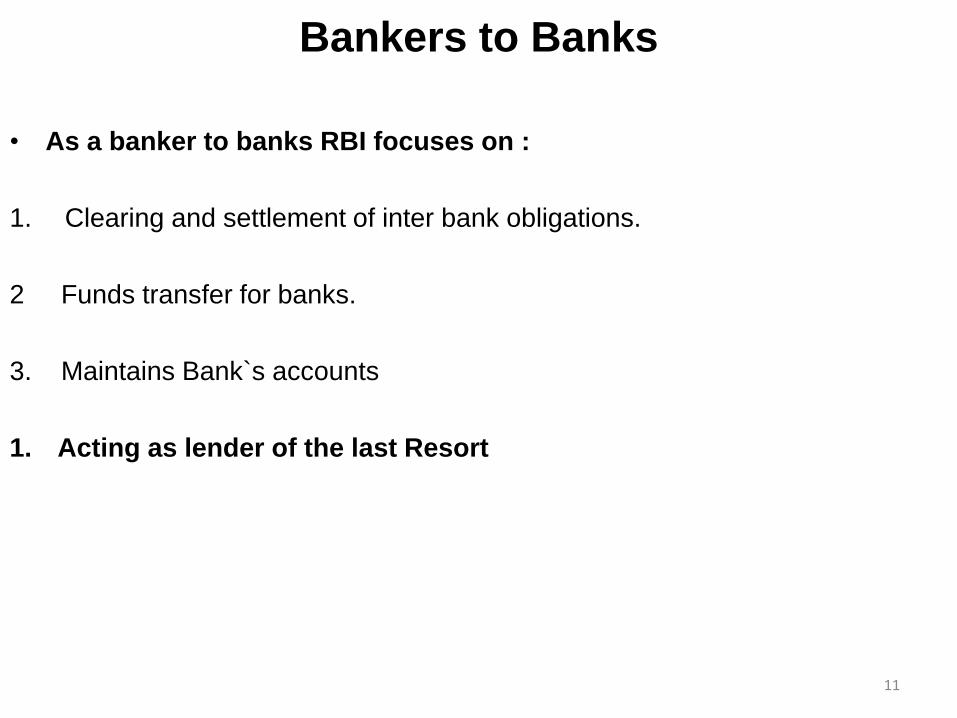

• As a banker to banks RBI focuses on :

1. Clearing and settlement of inter bank obligations.

2 Funds transfer for banks.

3. Maintains Bank`s accounts

1. Acting as lender of the last Resort

11

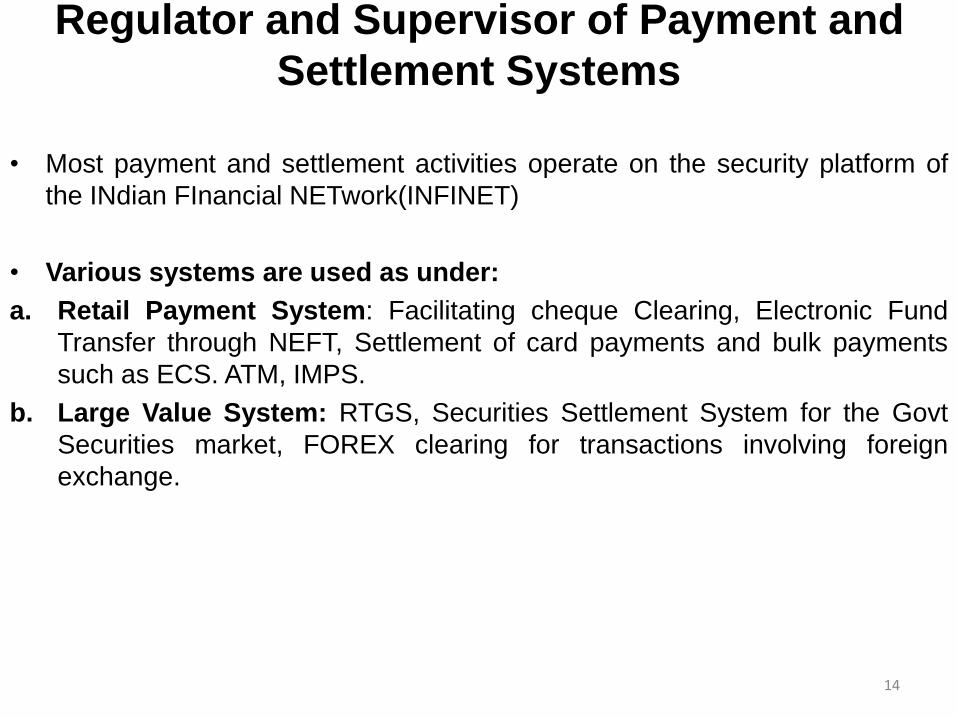

Regulator and Supervisor of Payment and

Settlement Systems

• Most payment and settlement activities operate on the security platform of

the INdian FInancial NETwork(INFINET)

• Various systems are used as under:

a. Retail Payment System: Facilitating cheque Clearing, Electronic Fund

Transfer through NEFT, Settlement of card payments and bulk payments

such as ECS. ATM, IMPS.

b. Large Value System: RTGS, Securities Settlement System for the Govt

Securities market, FOREX clearing for transactions involving foreign

exchange.

14

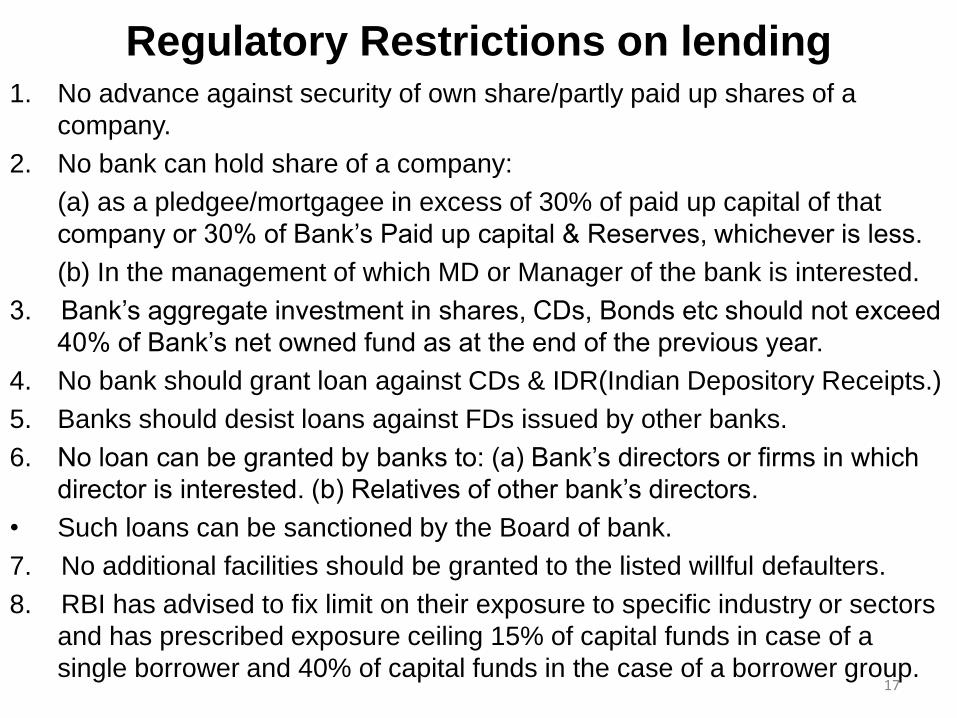

Regulatory Restrictions on lending1. No advance against security of own share/partly paid up shares of a

company.

2. No bank can hold share of a company:

(a) as a pledgee/mortgagee in excess of 30% of paid up capital of that

company or 30% of Bank’s Paid up capital & Reserves, whichever is less.

(b) In the management of which MD or Manager of the bank is interested.

3. Bank’s aggregate investment in shares, CDs, Bonds etc should not exceed

40% of Bank’s net owned fund as at the end of the previous year.

4. No bank should grant loan against CDs & IDR(Indian Depository Receipts.)

5. Banks should desist loans against FDs issued by other banks.

6. No loan can be granted by banks to: (a) Bank’s directors or firms in which

director is interested. (b) Relatives of other bank’s directors.

• Such loans can be sanctioned by the Board of bank.

7. No additional facilities should be granted to the listed willful defaulters.

8. RBI has advised to fix limit on their exposure to specific industry or sectors

and has prescribed exposure ceiling 15% of capital funds in case of a

single borrower and 40% of capital funds in the case of a borrower group.17

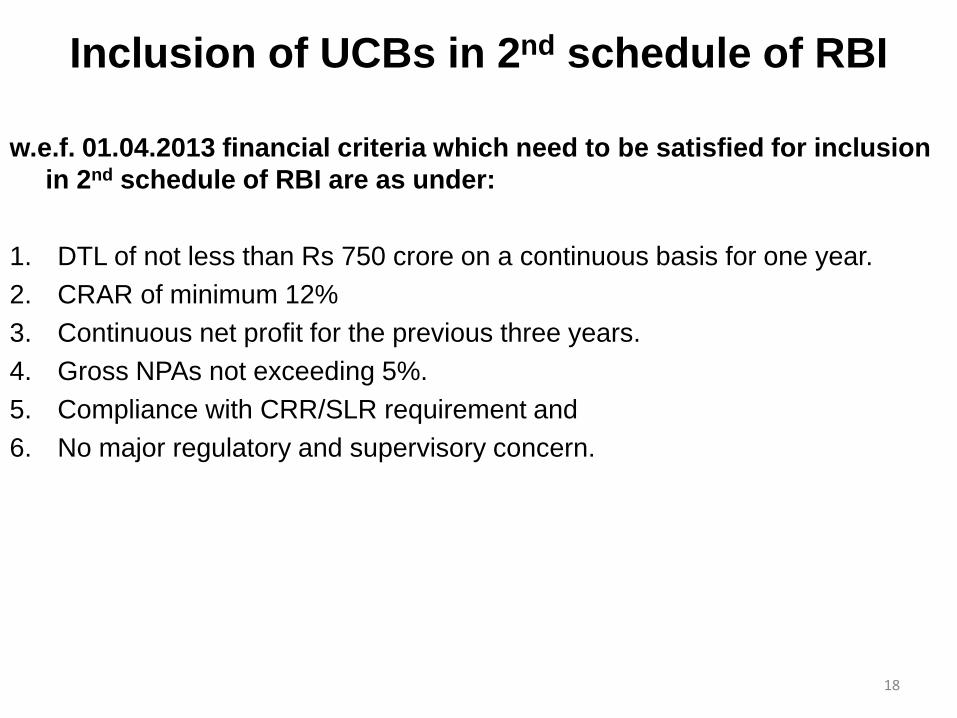

Inclusion of UCBs in 2nd schedule of RBI

w.e.f. 01.04.2013 financial criteria which need to be satisfied for inclusion

in 2nd schedule of RBI are as under:

1. DTL of not less than Rs 750 crore on a continuous basis for one year.

2. CRAR of minimum 12%

3. Continuous net profit for the previous three years.

4. Gross NPAs not exceeding 5%.

5. Compliance with CRR/SLR requirement and

6. No major regulatory and supervisory concern.

18

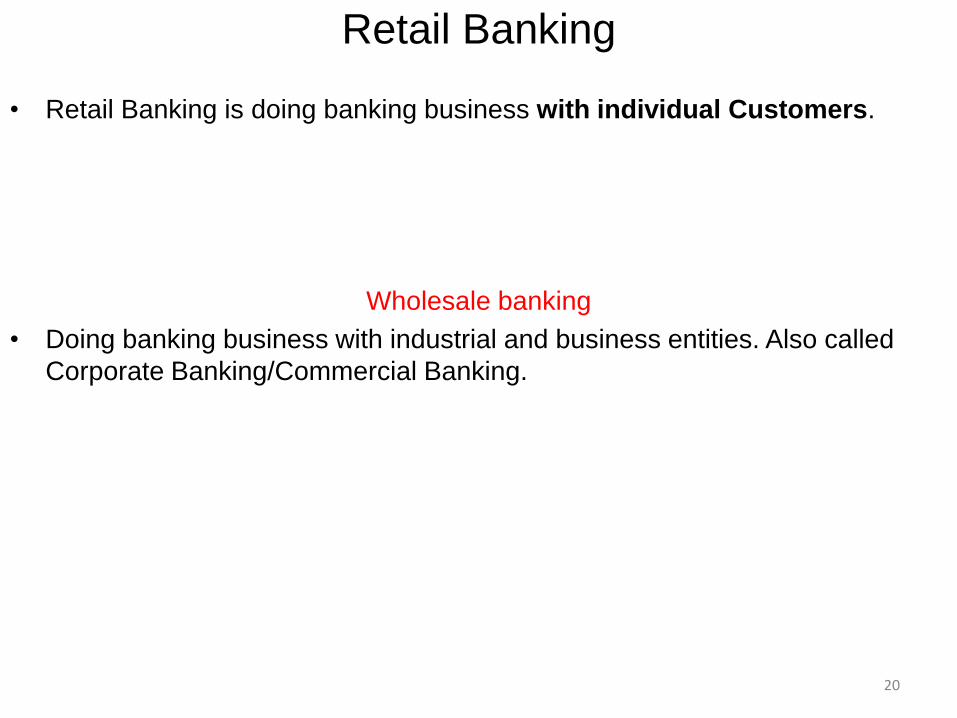

Retail Banking

• Retail Banking is doing banking business with individual Customers.

Wholesale banking

• Doing banking business with industrial and business entities. Also called

Corporate Banking/Commercial Banking.

20

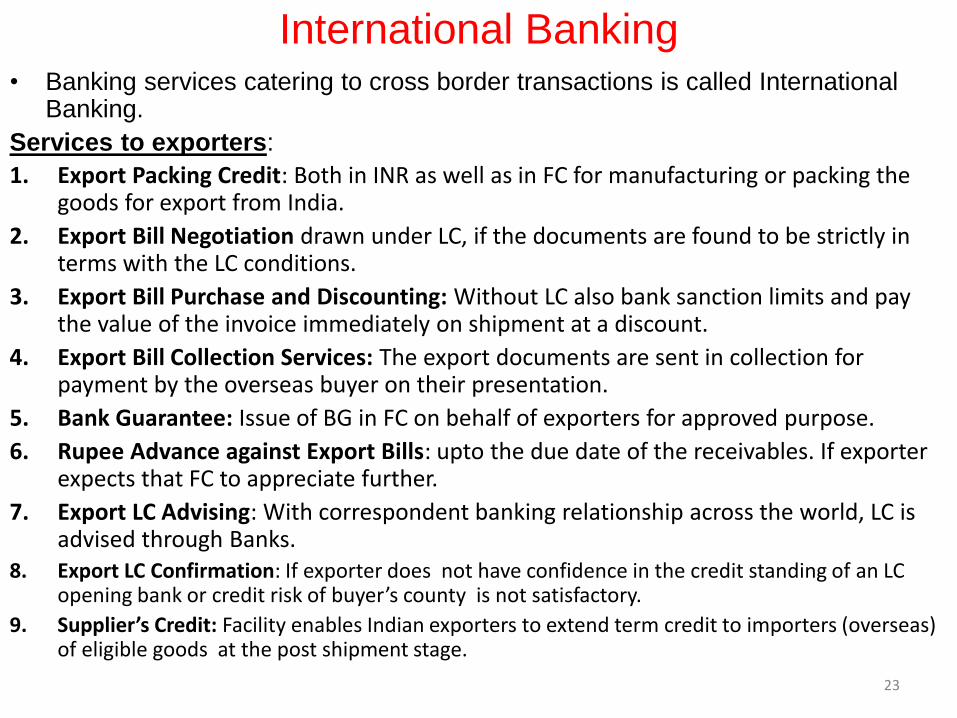

International Banking• Banking services catering to cross border transactions is called International

Banking.

Services to exporters:

1. Export Packing Credit: Both in INR as well as in FC for manufacturing or packing the goods for export from India.

2. Export Bill Negotiation drawn under LC, if the documents are found to be strictly in terms with the LC conditions.

3. Export Bill Purchase and Discounting: Without LC also bank sanction limits and pay the value of the invoice immediately on shipment at a discount.

4. Export Bill Collection Services: The export documents are sent in collection for payment by the overseas buyer on their presentation.

5. Bank Guarantee: Issue of BG in FC on behalf of exporters for approved purpose.

6. Rupee Advance against Export Bills: upto the due date of the receivables. If exporter expects that FC to appreciate further.

7. Export LC Advising: With correspondent banking relationship across the world, LC is advised through Banks.

8. Export LC Confirmation: If exporter does not have confidence in the credit standing of an LC opening bank or credit risk of buyer’s county is not satisfactory.

9. Supplier’s Credit: Facility enables Indian exporters to extend term credit to importers (overseas) of eligible goods at the post shipment stage.

23

B. Requirements of Importers

1. Import Collection Bill Services: Bank handle the Import Collection

documents meticulously and help the importers to remit the import value.

2. Direct Import Bills: Banks help importers to settle payments against the

direct imports.

3. Advance Payment towards Imports: Bank provide advisory services and

also assist in faster remittance to the suppliers.

4. Import Letter of Credit: Banks issue import LC on behalf of importers.

5. Arranging for Buyer’s and Supplier’s Credit: Banks also arrange for

financing import requirements of importers by way of Suppliers’ credit and

Buyers’ Credit.

6. Bank Guarantee: Banks issue BG in FC on behalf of importers.

C. Remittance Services:

1. EEFC (Exchange Earners Foreign Currency) Accounts Services in all

permitted purposes.

2. Receipt of Foreign Inward Remittance Services:

3. Payment Services to Abroad (Outward Remittances):

24

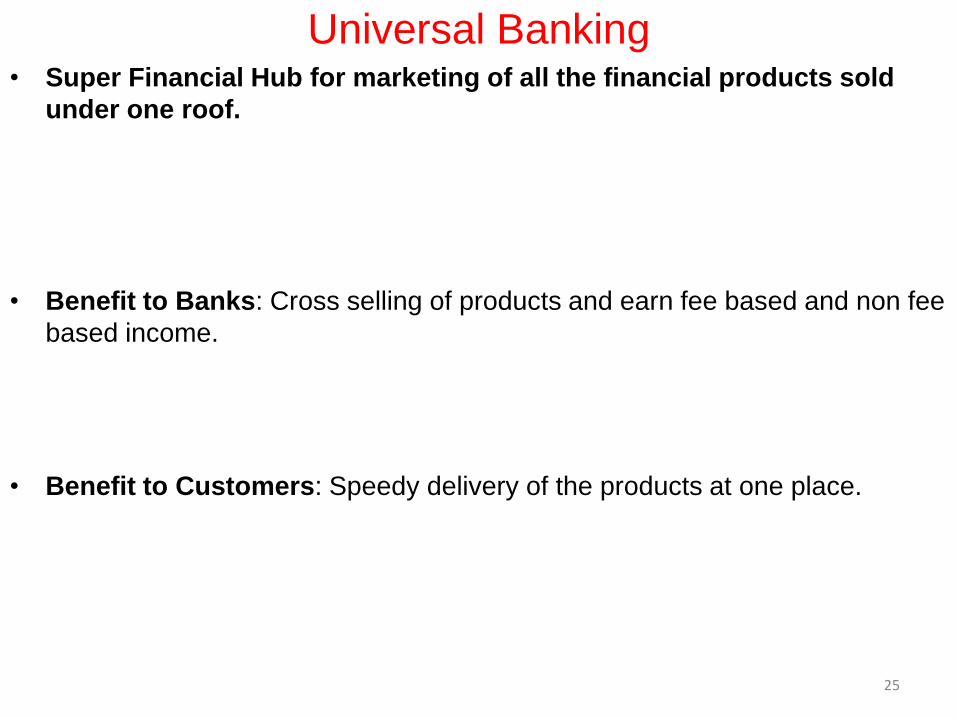

Universal Banking• Super Financial Hub for marketing of all the financial products sold

under one roof.

• Benefit to Banks: Cross selling of products and earn fee based and non fee

based income.

• Benefit to Customers: Speedy delivery of the products at one place.

25

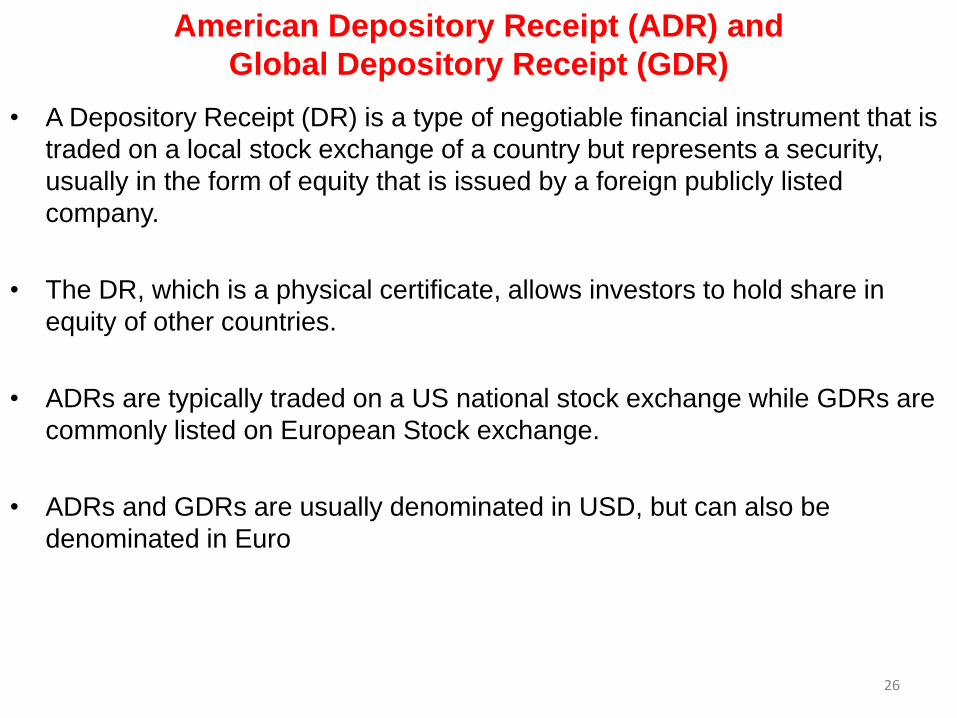

American Depository Receipt (ADR) and

Global Depository Receipt (GDR)

• A Depository Receipt (DR) is a type of negotiable financial instrument that is

traded on a local stock exchange of a country but represents a security,

usually in the form of equity that is issued by a foreign publicly listed

company.

• The DR, which is a physical certificate, allows investors to hold share in

equity of other countries.

• ADRs are typically traded on a US national stock exchange while GDRs are

commonly listed on European Stock exchange.

• ADRs and GDRs are usually denominated in USD, but can also be

denominated in Euro

26

Participatory Notes (PN)• Foreigners are not allowed to invest directly in the Indian Stock Market.

• PNs are issued by FIIs to entities that want to invest in the Indian stock

market but do not want to register themselves with the SEBI.

• FIIs registered with SEBI can issue, deal or hold PN.

• FIIs are not allowed to issue PNs to Indian nationals, persons of Indian

origin or overseas corporate bodies.

27

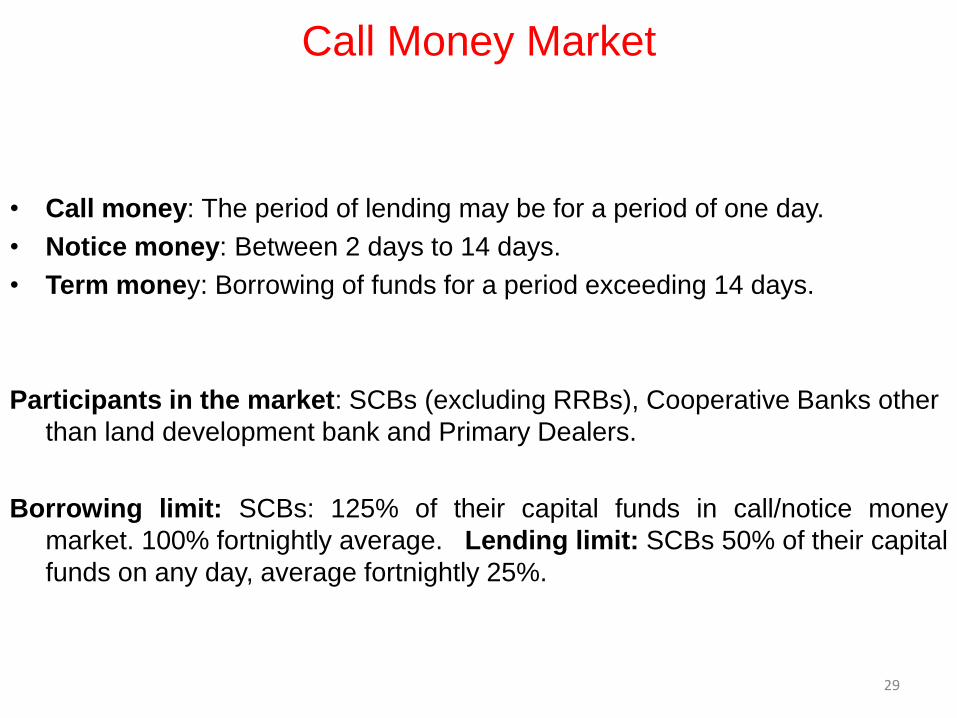

Call Money Market

• Call money: The period of lending may be for a period of one day.

• Notice money: Between 2 days to 14 days.

• Term money: Borrowing of funds for a period exceeding 14 days.

Participants in the market: SCBs (excluding RRBs), Cooperative Banks other

than land development bank and Primary Dealers.

Borrowing limit: SCBs: 125% of their capital funds in call/notice money

market. 100% fortnightly average. Lending limit: SCBs 50% of their capital

funds on any day, average fortnightly 25%.

29

Money Market instruments and operations1. Treasury Bills: To finance short term debt obligation of GOI. Three types of

T. Bills are issued 91 days, 182 days and 364 days through bidding.Quoted at a discount price. Min amount of Rs 25000

.

2 Certificate of Deposit (CD): CD is a negotiable instrument issued at

discount in demat form or as a usance promissory note issued by SCBs

(excluding RRBs)/LABs/all India FI. Tenor 7 days to 1 year. Min amount Rs

1 lakh or multiples thereof.

3 Commercial Paper (CP): Issued by a corporate at discount. Eligibility: TNW

is not less than Rs 4 cr and sanctioned WC limit by bank/FIs & A/c is in

standard asset category. Min credit rating P-2 of CRISIL or equivalent

rating. Maturities:7 days to 1 year. Denomination Rs 5L or multiples thereof.

4 Collateralized Borrowing and lending obligation (CLBO): Operated by

CCIL for its members to borrow or lend funds against the collateral of

eligible securities. Issued at discount, maturity one day to 90 days.

30

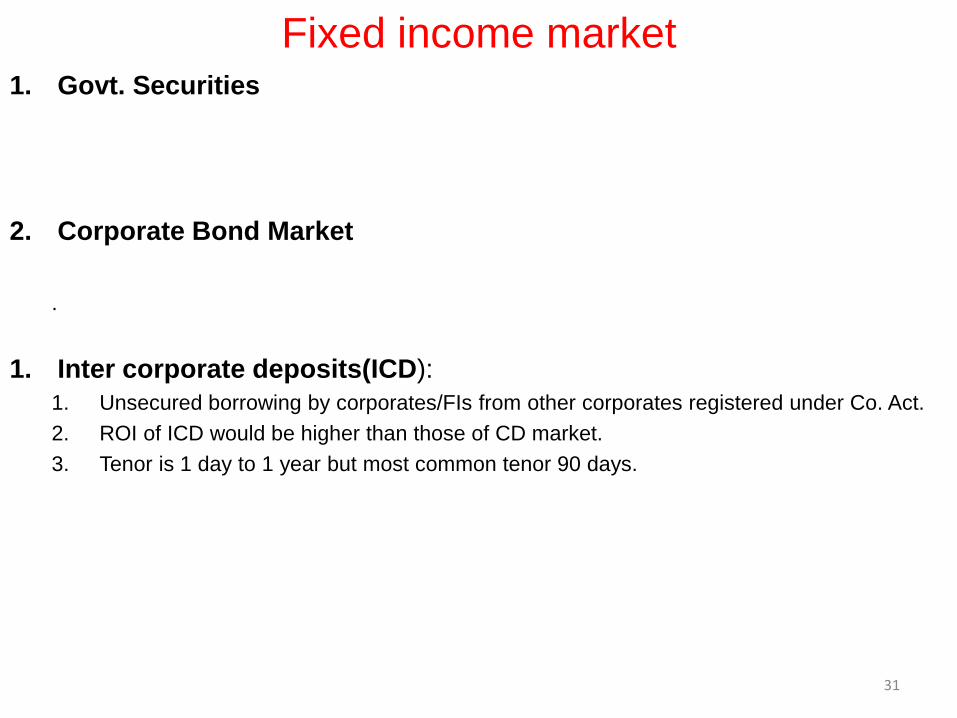

Fixed income market1. Govt. Securities

2. Corporate Bond Market

.

1. Inter corporate deposits(ICD):

1. Unsecured borrowing by corporates/FIs from other corporates registered under Co. Act.

2. ROI of ICD would be higher than those of CD market.

3. Tenor is 1 day to 1 year but most common tenor 90 days.

31

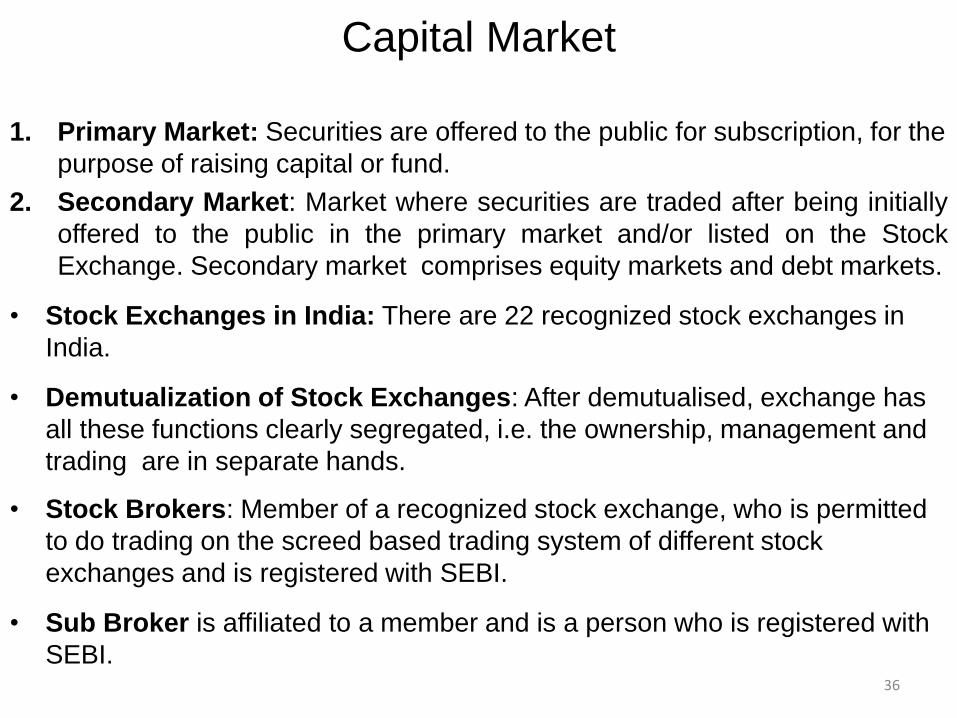

Capital Market

1. Primary Market: Securities are offered to the public for subscription, for the

purpose of raising capital or fund.

2. Secondary Market: Market where securities are traded after being initially

offered to the public in the primary market and/or listed on the Stock

Exchange. Secondary market comprises equity markets and debt markets.

• Stock Exchanges in India: There are 22 recognized stock exchanges in

India.

• Demutualization of Stock Exchanges: After demutualised, exchange has

all these functions clearly segregated, i.e. the ownership, management and

trading are in separate hands.

• Stock Brokers: Member of a recognized stock exchange, who is permitted

to do trading on the screed based trading system of different stock

exchanges and is registered with SEBI.

• Sub Broker is affiliated to a member and is a person who is registered with

SEBI.36

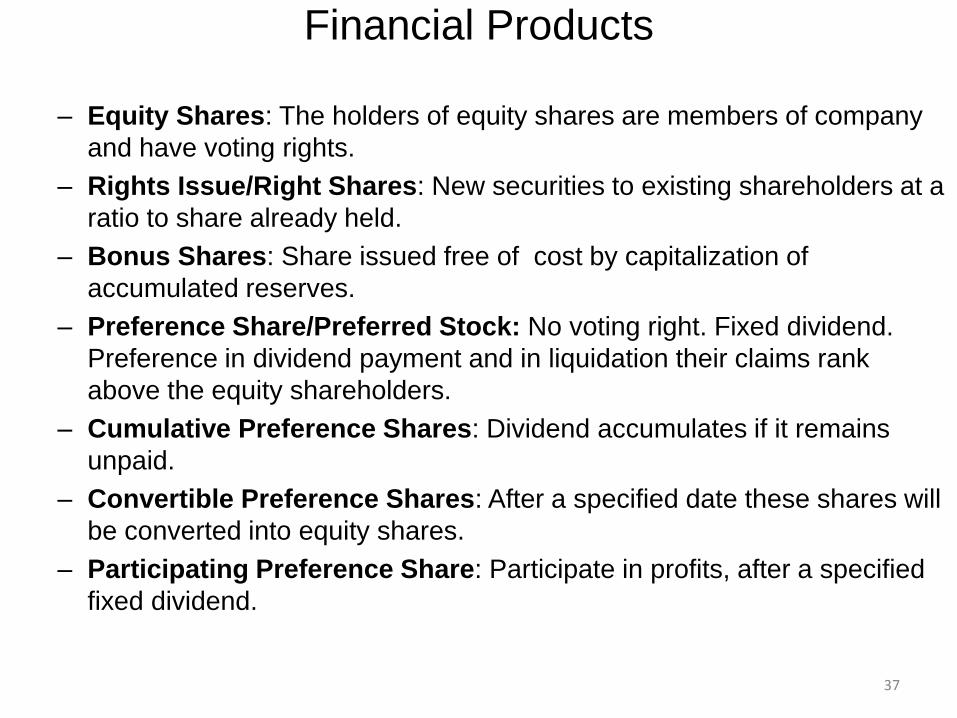

Financial Products

– Equity Shares: The holders of equity shares are members of company

and have voting rights.

– Rights Issue/Right Shares: New securities to existing shareholders at a

ratio to share already held.

– Bonus Shares: Share issued free of cost by capitalization of

accumulated reserves.

– Preference Share/Preferred Stock: No voting right. Fixed dividend.

Preference in dividend payment and in liquidation their claims rank

above the equity shareholders.

– Cumulative Preference Shares: Dividend accumulates if it remains

unpaid.

– Convertible Preference Shares: After a specified date these shares will

be converted into equity shares.

– Participating Preference Share: Participate in profits, after a specified

fixed dividend.

37

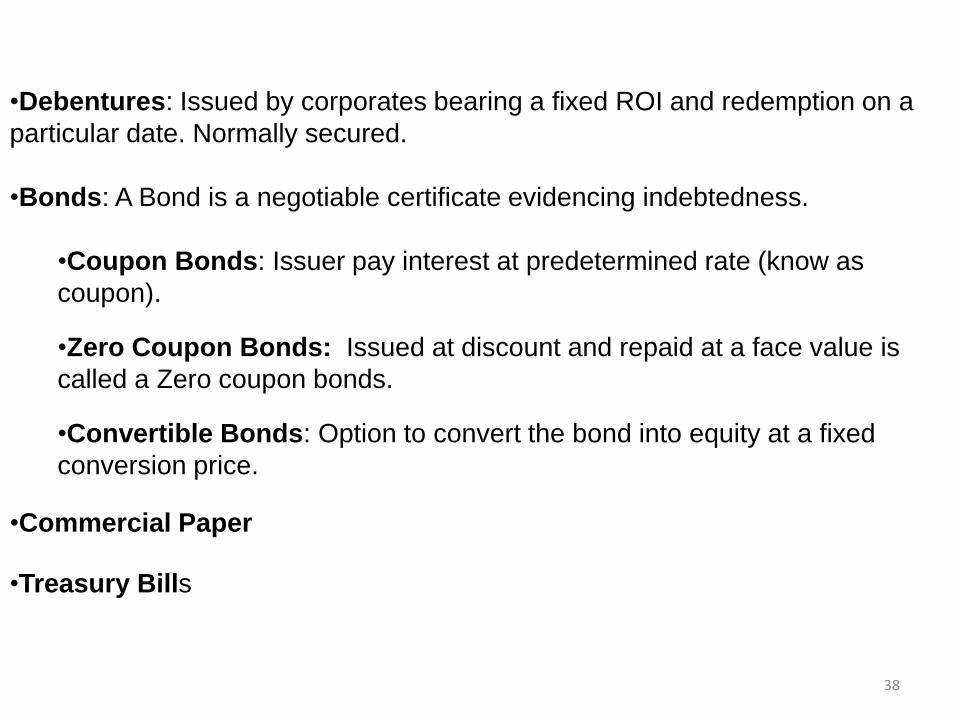

•Debentures: Issued by corporates bearing a fixed ROI and redemption on a

particular date. Normally secured.

•Bonds: A Bond is a negotiable certificate evidencing indebtedness.

•Coupon Bonds: Issuer pay interest at predetermined rate (know as

coupon).

•Zero Coupon Bonds: Issued at discount and repaid at a face value is

called a Zero coupon bonds.

•Convertible Bonds: Option to convert the bond into equity at a fixed

conversion price.

•Commercial Paper

•Treasury Bills

38

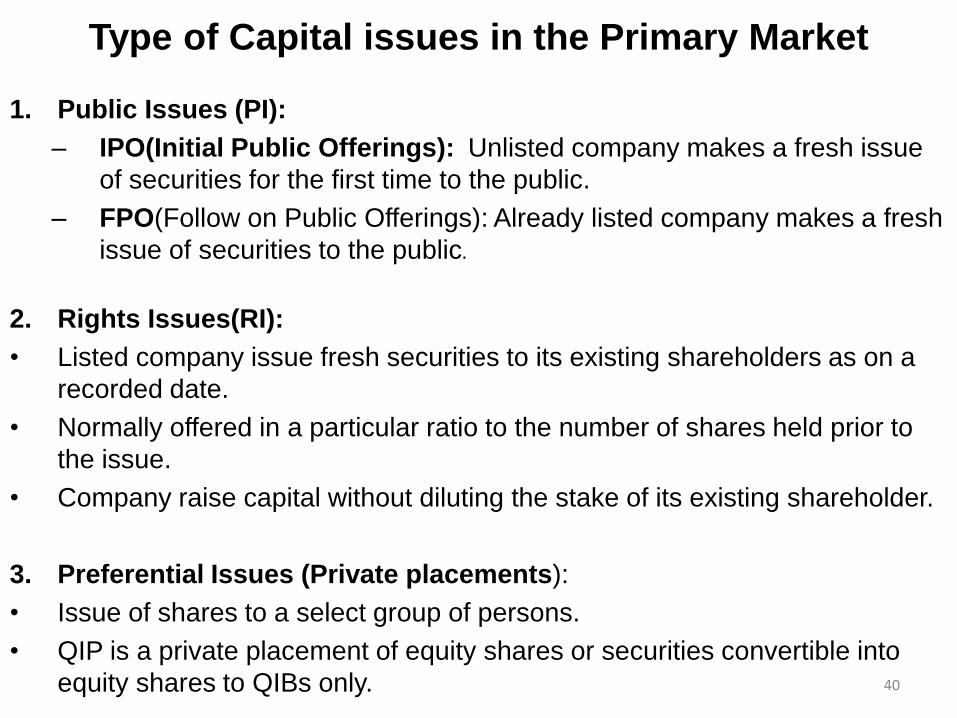

Type of Capital issues in the Primary Market

1. Public Issues (PI):

– IPO(Initial Public Offerings): Unlisted company makes a fresh issue

of securities for the first time to the public.

– FPO(Follow on Public Offerings): Already listed company makes a fresh

issue of securities to the public.

2. Rights Issues(RI):

• Listed company issue fresh securities to its existing shareholders as on a

recorded date.

• Normally offered in a particular ratio to the number of shares held prior to

the issue.

• Company raise capital without diluting the stake of its existing shareholder.

3. Preferential Issues (Private placements):

• Issue of shares to a select group of persons.

• QIP is a private placement of equity shares or securities convertible into

equity shares to QIBs only. 40

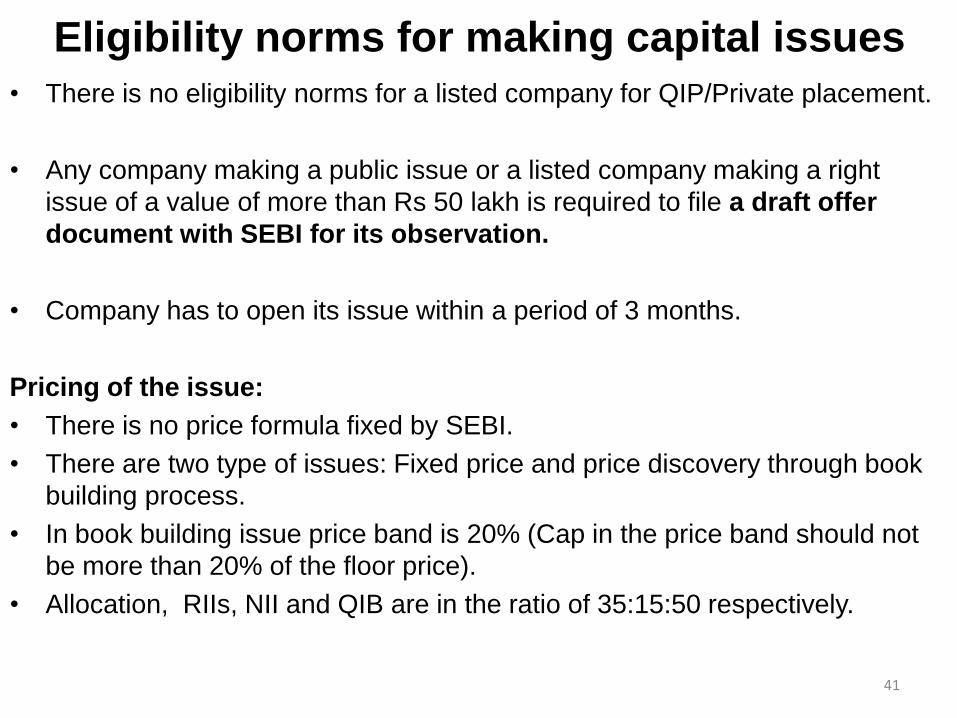

Eligibility norms for making capital issues

• There is no eligibility norms for a listed company for QIP/Private placement.

• Any company making a public issue or a listed company making a right

issue of a value of more than Rs 50 lakh is required to file a draft offer

document with SEBI for its observation.

• Company has to open its issue within a period of 3 months.

Pricing of the issue:

• There is no price formula fixed by SEBI.

• There are two type of issues: Fixed price and price discovery through book

building process.

• In book building issue price band is 20% (Cap in the price band should not

be more than 20% of the floor price).

• Allocation, RIIs, NII and QIB are in the ratio of 35:15:50 respectively.

41

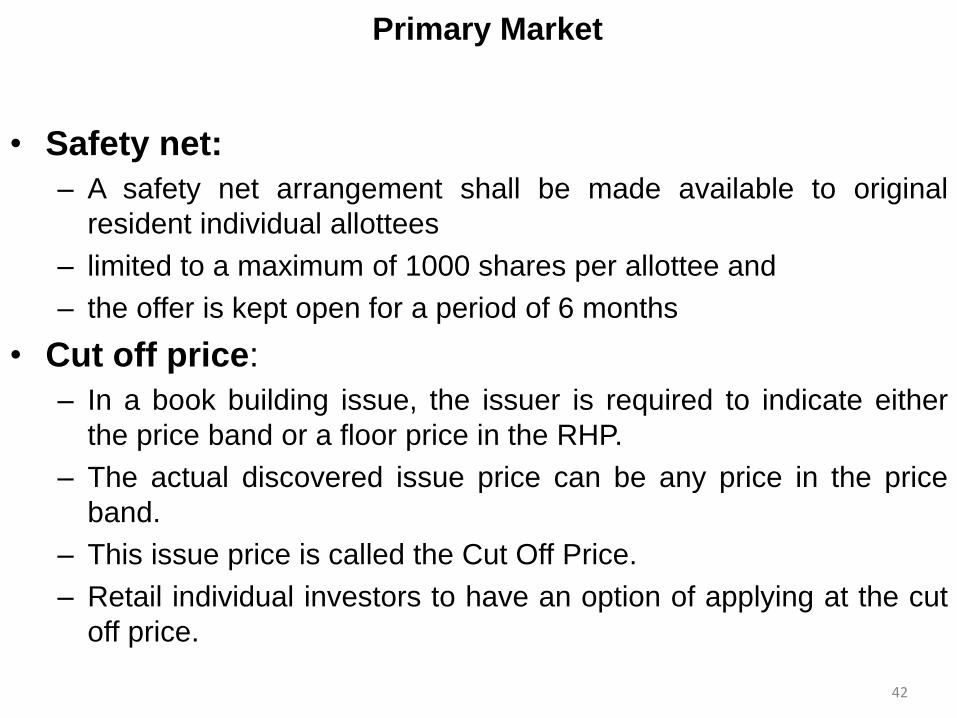

Primary Market

• Safety net:

– A safety net arrangement shall be made available to original

resident individual allottees

– limited to a maximum of 1000 shares per allottee and

– the offer is kept open for a period of 6 months

• Cut off price:

– In a book building issue, the issuer is required to indicate either

the price band or a floor price in the RHP.

– The actual discovered issue price can be any price in the price

band.

– This issue price is called the Cut Off Price.

– Retail individual investors to have an option of applying at the cut

off price.

42

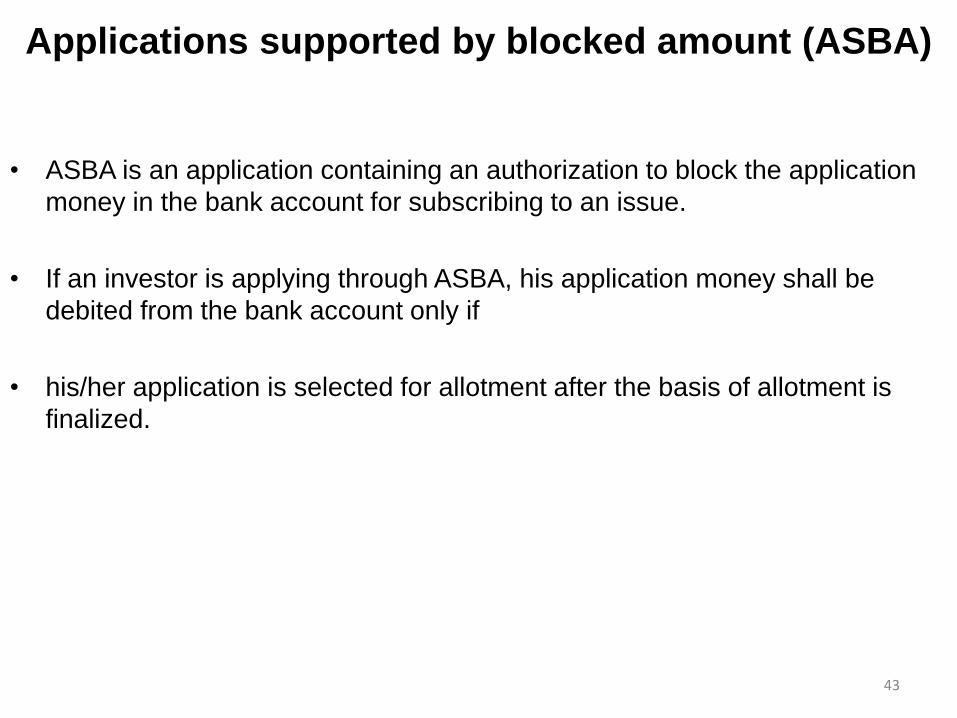

Applications supported by blocked amount (ASBA)

• ASBA is an application containing an authorization to block the application

money in the bank account for subscribing to an issue.

• If an investor is applying through ASBA, his application money shall be

debited from the bank account only if

• his/her application is selected for allotment after the basis of allotment is

finalized.

43

Securities Exchange Board of India (SEBI)

To protect the interests of investors in securities and to promote the

development of and to regulate the securities market

45

Mutual Fund (MF)

• A MF is required to be registered with SEBI.

• A MF is set up in the form of trust, which has sponsors,

trustees, Asset Management Companies(AMCs) and

custodians.

– Sponsors are promoter of a company.

– Trustees hold its property for the benefit of the unit holders.

– AMC, approved by SEBI manages the funds by making

investments.

– Custodian, registered with SEBI holds securities of the fund in its

custody.

• Net Asset Value (NAV): Performance of a scheme is denoted

by NAV. The NAV per unit is the market value of securities, less

expenses incurred on the scheme, divided by total number of

units of scheme on any particular date.

48

Different type of Mutual Funds• Open-ended Scheme/plan: One that is available for subscription and

repurchase on a continuous basis.

• Close ended Scheme/plan: Fund is open for subscription only during aspecified period at the time of launch. Exit routes: either repurchase facility orthrough listing on stock exchange.

• Growth Scheme/Equity Oriented Scheme: Invest major part in equity. Higherrisk. Different options like dividend option, capital appreciation etc.

• Income Scheme/Debt Oriented Scheme: Provide regular and steady income.Invest in fixed income securities. Less risky.

• Balance Plan/Scheme: Provide growth and regular income. Invest both inequities and fixed income securities in the proportion indicated in their offerdocument.

• Money Market or Liquid Fund: Provide easy liquidity, preservation of capitaland to ensure a moderate income.

• Gilt Fund: Invest exclusively in Govt Securities. No default risk.

• Index Fund: Invest in the securities in the same weight age comprising anindex, BSE sensitive index, Nifty etc.

• Sector Specific Fund: Invest only those sectors or industries as specified in theoffer documents.

• Tax Saving Scheme: ELSS (Equity linked saving Scheme) are growth orientedand invest predominantly in equities. Lock in period 3 years.

• Fund of Funds (FoFs): Invest primarily in other schemes of the same MF orother MF. Greater diversification through one scheme.

• Gold Exchange Traded Fund (GETF) scheme49

Rajiv Gandhi Equity Saving Scheme (RGESS)

• Section 80CCG - tax benefit :

– Investment upto Rs 50000 and

– whose gross total annual income is upto Rs 12.00 lakh.

50

Insurance

• Entry level Capital required for a new insurance company in India is

Rs 1 Cr.

• 1st insurance company was started in India in 1818 at Kolkata.

• Insurance Act, 1938 and IRDA Act 1999 are primary legislation that

deals with insurance sector in India.

54

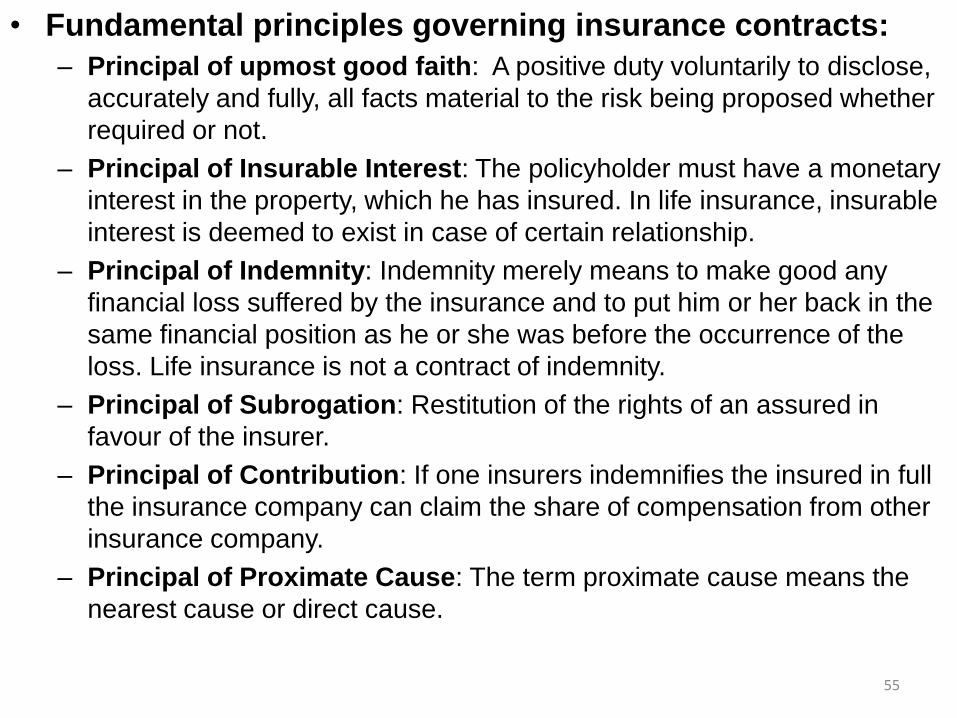

• Fundamental principles governing insurance contracts:

– Principal of upmost good faith: A positive duty voluntarily to disclose,

accurately and fully, all facts material to the risk being proposed whether

required or not.

– Principal of Insurable Interest: The policyholder must have a monetary

interest in the property, which he has insured. In life insurance, insurable

interest is deemed to exist in case of certain relationship.

– Principal of Indemnity: Indemnity merely means to make good any

financial loss suffered by the insurance and to put him or her back in the

same financial position as he or she was before the occurrence of the

loss. Life insurance is not a contract of indemnity.

– Principal of Subrogation: Restitution of the rights of an assured in

favour of the insurer.

– Principal of Contribution: If one insurers indemnifies the insured in full

the insurance company can claim the share of compensation from other

insurance company.

– Principal of Proximate Cause: The term proximate cause means the

nearest cause or direct cause.

55

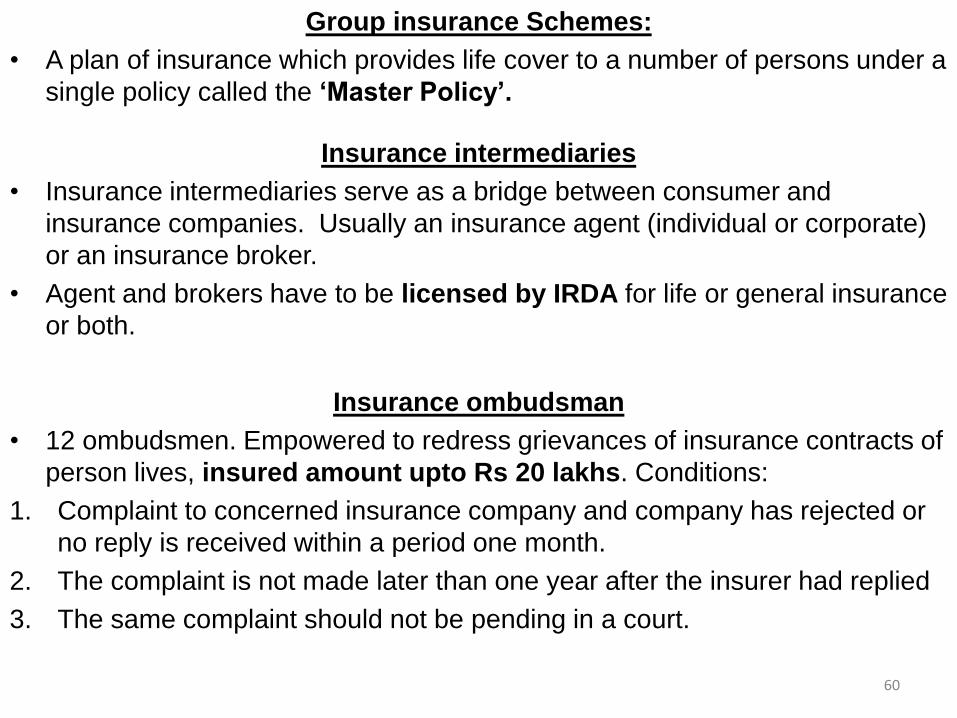

Group insurance Schemes:

• A plan of insurance which provides life cover to a number of persons under a

single policy called the ‘Master Policy’.

Insurance intermediaries

• Insurance intermediaries serve as a bridge between consumer and

insurance companies. Usually an insurance agent (individual or corporate)

or an insurance broker.

• Agent and brokers have to be licensed by IRDA for life or general insurance

or both.

Insurance ombudsman

• 12 ombudsmen. Empowered to redress grievances of insurance contracts of

person lives, insured amount upto Rs 20 lakhs. Conditions:

1. Complaint to concerned insurance company and company has rejected or

no reply is received within a period one month.

2. The complaint is not made later than one year after the insurer had replied

3. The same complaint should not be pending in a court.

60

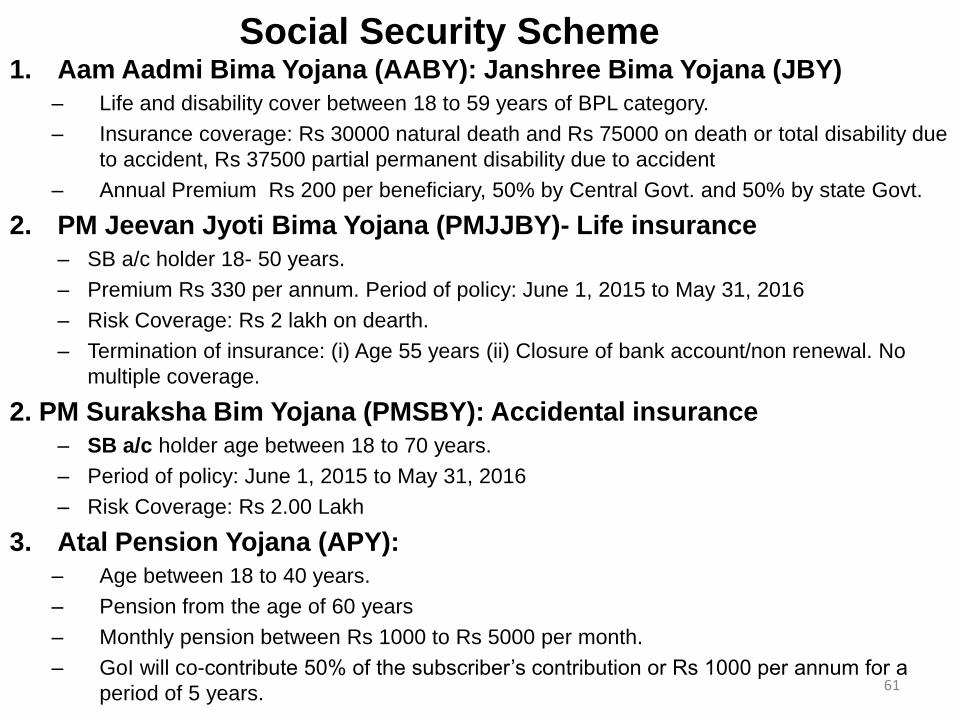

Social Security Scheme1. Aam Aadmi Bima Yojana (AABY): Janshree Bima Yojana (JBY)

– Life and disability cover between 18 to 59 years of BPL category.

– Insurance coverage: Rs 30000 natural death and Rs 75000 on death or total disability due

to accident, Rs 37500 partial permanent disability due to accident

– Annual Premium Rs 200 per beneficiary, 50% by Central Govt. and 50% by state Govt.

2. PM Jeevan Jyoti Bima Yojana (PMJJBY)- Life insurance

– SB a/c holder 18- 50 years.

– Premium Rs 330 per annum. Period of policy: June 1, 2015 to May 31, 2016

– Risk Coverage: Rs 2 lakh on dearth.

– Termination of insurance: (i) Age 55 years (ii) Closure of bank account/non renewal. No

multiple coverage.

2. PM Suraksha Bim Yojana (PMSBY): Accidental insurance

– SB a/c holder age between 18 to 70 years.

– Period of policy: June 1, 2015 to May 31, 2016

– Risk Coverage: Rs 2.00 Lakh

3. Atal Pension Yojana (APY):

– Age between 18 to 40 years.

– Pension from the age of 60 years

– Monthly pension between Rs 1000 to Rs 5000 per month.

– GoI will co-contribute 50% of the subscriber’s contribution or Rs 1000 per annum for a

period of 5 years.61

Bancassurance• Selling of insurance products through banks and

• exploiting the true synergies between the bank and insurer and

• optimally utilizing their respective strengths.

62

Factoring• Factoring - arrangement in which receivables created out of sale of goods

and services are sold to an agency know as “factor’.

• This will be with recourse or without recourse, but in India without recourse is not permitted.

• As soon as the invoice is submitted to the factor, the factor will pay say 85% of invoice to the seller.

• The balance payment will be paid to the seller on recovering from the purchaser.

• The Factor will recover finance charges for funds prepaid to the seller against the invoice.

Types of Factoring:

1. Recourse Factoring (with recourse)

2. Non – recourse Factoring (without recourse)

• Domestic Factoring

• International Factoring 65

Forfaiting Services

• Method of discounting of international trade receivables on a without

recourse basis.

• Exporter is fully protected against interest and/or currency rate moving

unfavorable during the credit period as the entire risk is passed on to the

forfaiter.

66

Off Balance sheet Items

OBS items are those items in the books of a bank, which are not

mentioned in the balance sheet of the bank. These contingent

liabilities have to be disclosed as ‘Notes to the Balance sheet’.

1. Guarantees: A contract to perform the promise or discharge the liability of

a third person in case of default. Three parties

• Performance Guarantees: Issued in respect of performance of a contract

or obligation.

• Financial Guarantees: In lieu of financial commitments. Guarantee in

favour of custom authorities, Tax Authorities, an respect of any disputed

liabilities.

• Deferred Payment Guarantees: DPGs normally arise in the case of

purchase of machinery or such other capital equipment by customers.

67

2. Letter of Credit:

LC is a definite undertaking by bank, on behalf of buyer to the seller to pay for

goods and/or service, provided that the seller presents documents comply

fully with the terms and conditions of the documentary credit.

Parties to LC:

1. Applicant: Importer or buyer.

2. Issuing Bank: Usually the applicant’s bank. Issuing bank is ultimately

responsible for payment under LC.

3. Advising Bank: A correspondent or a branch of the issuing bank is able to

authenticate the LC message before advising the same to the beneficiary.

4. Confirming Bank: Same role as advising bank except that the confirming

bank provides an undertaking to the beneficiary, that they will pay, accept &

negotiate documents presented as per terms & conditions of LC.

5. Beneficiary: Exporter or seller of the goods.68

Types of Credits1. Irrevocable LC: T&C cannot be amended without the agreement of all the

parties of Credit. If a credit is silent, the credit is deemed to be irrevocable.

2. Revocable LC: May be amended or cancelled by the applicant at any time

without reference to or consent of the beneficiary.

3. Unconfirmed LC: Advising bank has no responsibility for payment.

4. Confirmed LC: Undertaking of the confirming bank to effect payment upon

presentation at its counter of credit confirming documents.

5. Revolving LC: Either by time (a stated amount is available in a given

period) and amount( available upto a fixed amount for any one drawing).

6. Standby LC: Similar to BG but is issued in a format corresponding to that

of a documentary credit.

7. Transferable LC: When seller is acting as an agent in the export order.

The LC are transferred to the actual supplier of the goods.

8. Back to back LC: Open as another LC locally at his end in favour of

manufacturer for supply of goods to himself or the purpose of shipment under the

original Credit.

9. Red clause LC is the one which provides for advance payment to exporter

for the procuring shipment material and arranging for its actual shipment.

10. If LC provides for further advance to facilitate temporary storage of goods

at exporters end, the LC will be know as Green Clause LC69

Alliances

• Two or more organizations agree to cooperate in the operation of a business

activity, where each involved company brings different strengths and

capabilities to the arrangement.

Example: Three PSBs – Indian Bank, Corporation Bank and OBC entered

into strategic alliance in Oct. 2006 for formation of a joint appraisal cell to

undertake appraisal of large projects, participating in training programmes

and building up a common data centre, IT platform.

78

Mergers/Amalgamation

• Unification of two or more companies into a single company, whereone survives with its name and the other lose their corporateexistence.

• All the assets and liabilities of the merging company gets transferredto the surviving company.

Type of mergers:

• Horizontal Mergers: Merger of two or more companies which areproducing similar products or rendering the same type of services.

• Vertical Mergers: Merger of two companies, where one of them isan actual or potential supplier of goods or services to the other.

• Extension Mergers: The merged company provides an extension ofproduct line, market participants or technology to the survivingcompany.

• Conglomerate Mergers: “Merger that is not horizontal orvertical; in general, it is the combination of firms in differentindustries or firms operating in different geographic areas"79

Consolidation

• Combining of two existing companies into a new company.

• The existing companies lose their identities and a new entity is

created with the different or the same name.

80

Acquisition or take-over

• Acquisition or take over of a company refers to:

– the acquiring of a controlling stake in the ownership of a

company by another entity.

81

CICs operating in India

1. CIBIL (Credit Information Bureau (India) Limited): Incorporated in 2000,

owned by Trans Union International Inc. 3 NBFCs and 10 Commercial

Banks in India. Prepares CIR for individuals as well as corporate entities.

More than 500 members.

2. Experian Credit Information Company (India) Private Limited:

Incorporated in 2010. Helps in credit risk, prevent fraud. Recently launched

fraud prevention tool as ‘Hunter’.

3. Equifax Credit Information Services Private Limited

4. High Mark Credit Information Company Limited

Credit History and Credit Score:

• Loans and Credit Card facilities availed from banks/FIs, re-payment record,

current balance on each facility, new credit facilities obtained, number of

new enquiries from lenders, default in repayment of dues, suit filed

information etc is referred to as credit history of borrower.

• A Credit Score is a number statistically generated which indicates credit

worthiness of an individual. It indicates the probability that a person will be

able to repay or not a debt extended to him/her on credit.85

Banking Codes and Standards Board of India (BCSBI)

• BCSBI registered as a society on 18.02.2006. Autonomous body.

• Monitor and assess the compliance with codes and minimum standards of

services to individual customer to which the banks agreed to.

• Bank register with BCSBI as member and have the code adopted by their

respective board.

• Generate awareness in the common man about his rights as a consumer of

banking service.

.

88

Payment and Settlement System

• Initiatives taken by RBI

1. Paper based Payments:

- Cheques, drafts. MICR (Magnetic Ink Character Recognition) Technology, CTS

2010 (cheque truncation system).

2. Electronic Payments:

1. ECS Credit/Debit through national electronic clearing system.

2. NEFT: System provides for batch settlements at hourly intervals. No Min. and

Max. amount limitation, facilitating one way transfer to Nepal.

3. RTGS: Transfer of money take place from one bank to another on a real time

and on gross basis. Gross settlement means the transaction is settled on one to

one basis without netting with any other transaction.

4. CCIL (Clearing Corporation of India Ltd): Function as a industry service

organization for clearing and settlement for trade in money market, Govt.

securities and foreign exchange markets.

5. Prepaid payment system: Payment instruments that facilitate purchase of

goods and services against the value stored on these instruments. Max. value

Rs 50000.

6. Mobile Banking System

7. ATM/POS terminal/online transactions

8. National Payment Corporation of India (NPCI)90

The Depositor Education and Awareness Fund Scheme 2014

Amount to be credited to the Fund includes:

• Credit balances in any deposit account maintained with banks

• Which have not been operated upon for 10 years or more or

• Any amount remaining unclaimed for 10 years or more.

Utilization of fund:

• For promotion of depositors’ interest.

• Preservation of Records:

• Details of all accounts and transactions credited to the fund

permanently.

• Where refund has been claimed from the fund, for a period of at

least 5 years from the date of refund from trust.91

93

Related Documents