Information current as of March 15, 2016 PPG Architectural Coatings Vince Morales Vice President, Investor Relations and Treasurer Goldman Sachs Chemical Intensity Days Houston, TX March 15, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Information current as of March 15, 2016

PPG Architectural CoatingsVince Morales

Vice President, Investor Relations and Treasurer

Goldman Sachs Chemical Intensity Days

Houston, TX March 15, 2016

2

Forward Looking StatementThe Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements made by

or on behalf of the Company. This presentation contains forward-looking statements that reflect the Company’s

current views with respect to future events and financial performance. You can identify forward-looking statements

by the fact that they do not relate strictly to current or historic facts. Forward-looking statements are identified by the

use of the words “aim,” “believe,” “expect,” “anticipate,” “intend,” “estimate,” “project,” “outlook,” “forecast” and other

expressions that indicate future events and trends. Any forward-looking statement speaks only as of the date on

which such statement is made, and the Company undertakes no obligation to update any forward looking statement,

whether as a result of new information, future events or otherwise. You are advised, however, to consult any further

disclosures we make on related subjects in our reports to the Securities and Exchange Commission. Also, note the

following cautionary statements.

Many factors could cause actual results to differ materially from the Company’s forward-looking statements. Such

factors include global economic conditions, increasing price and product competition by foreign and domestic

competitors, fluctuations in cost and availability of raw materials, the ability to maintain favorable supplier

relationships and arrangements, the timing of and the realization of anticipated cost savings from restructuring

initiatives, difficulties in integrating acquired businesses and achieving expected synergies therefrom, economic and

political conditions in international markets, the ability to penetrate existing, developing and emerging foreign and

domestic markets, foreign exchange rates and fluctuations in such rates, fluctuations in tax rates, the impact of

future legislation, the impact of environmental regulations, unexpected business disruptions and the unpredictability

of existing and possible future litigation, including litigation that could result if the proposed asbestos settlement does

not become effective. However, it is not possible to predict or identify all such factors. Consequently, while the list of

factors presented here and under Item 1A of PPG’s 2015 Form 10-K is considered representative, no such list

should be considered to be a complete statement of all potential risks and uncertainties. Unlisted factors may

present significant additional obstacles to the realization of forward-looking statements. Consequences of material

differences in the results compared with those anticipated in the forward-looking statements could include, among

other things, lower sales or earnings, business disruption, operational problems, financial loss, legal liability to third

parties, other factors set forth in Item 1A of PPG’s 2015 Form 10-K and similar risks, any of which could have a

material adverse effect on the Company’s consolidated financial condition, results of operations or liquidity.

3

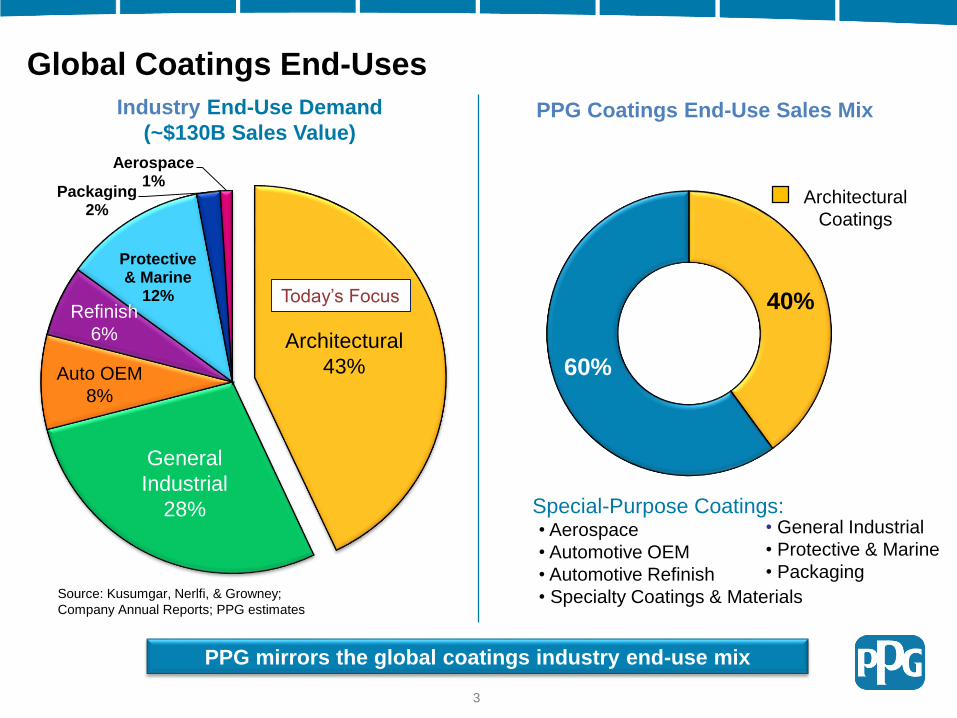

Global Coatings End-Uses

40%

60%

Special-Purpose Coatings:• Aerospace

• Automotive OEM

• Automotive Refinish

• Specialty Coatings & Materials

Protective & Marine

12%

Packaging2%

Aerospace1%

Architectural

43%

General

Industrial

28%

Refinish

6%

Auto OEM

8%

Industry End-Use Demand

(~$130B Sales Value)

Source: Kusumgar, Nerlfi, & Growney;

Company Annual Reports; PPG estimates

• General Industrial

• Protective & Marine

• Packaging

Architectural

Coatings

PPG Coatings End-Use Sales Mix

PPG mirrors the global coatings industry end-use mix

Today’s Focus

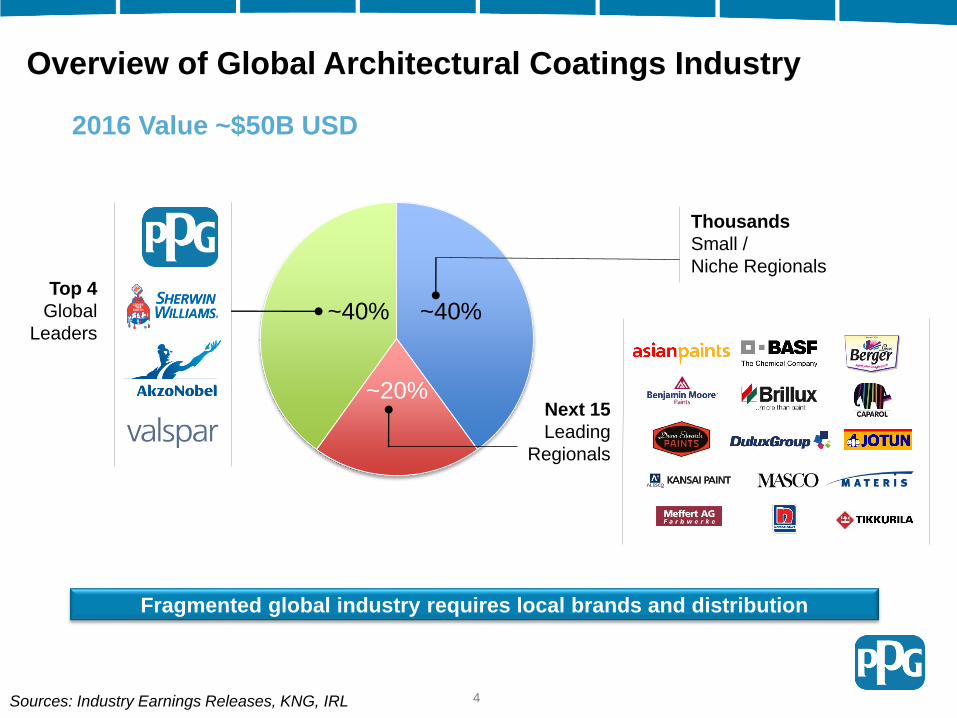

Overview of Global Architectural Coatings Industry

Top 4

Global

Leaders~40%

~20%Next 15

Leading

Regionals

~40%

Thousands

Small /

Niche Regionals

2016 Value ~$50B USD

Sources: Industry Earnings Releases, KNG, IRL

Fragmented global industry requires local brands and distribution

4

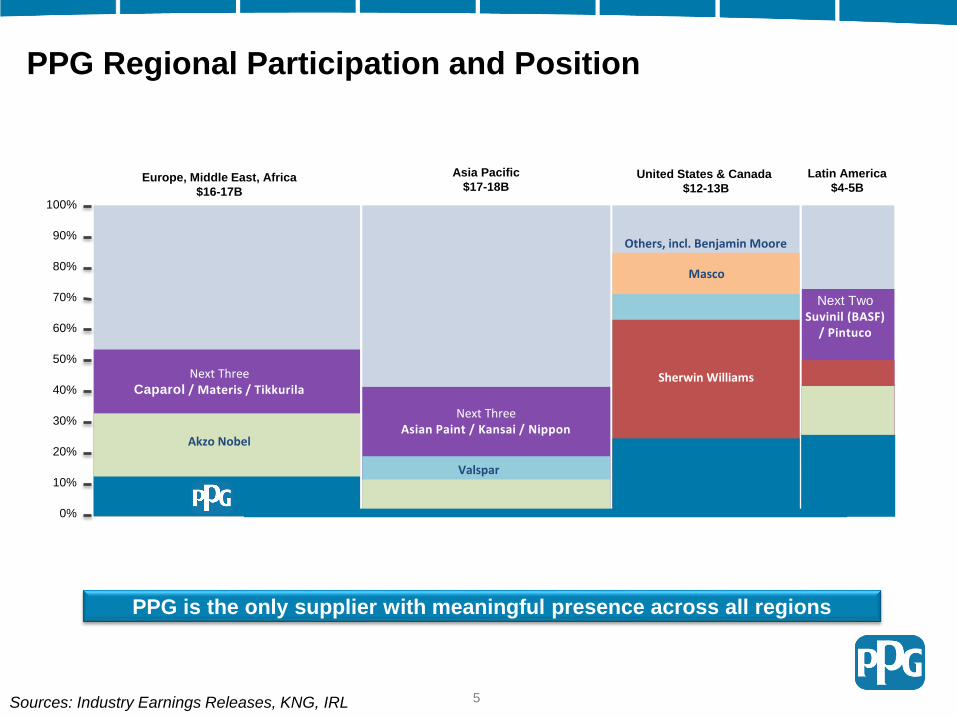

PPG Regional Participation and Position

Europe, Middle East, Africa

$16-17B

Asia Pacific

$17-18BUnited States & Canada

$12-13B

Latin America

$4-5B

Next ThreeCaparol / Materis / Tikkurila

Akzo Nobel

Next ThreeAsian Paint / Kansai / Nippon

Masco

Valspar

Sherwin Williams

Next Two

Suvinil (BASF) / Pintuco

100%

80%

70%

60%

50%

40%

30%

20%

10%

0%

90%Others, incl. Benjamin Moore

Sources: Industry Earnings Releases, KNG, IRL

PPG is the only supplier with meaningful presence across all regions

5

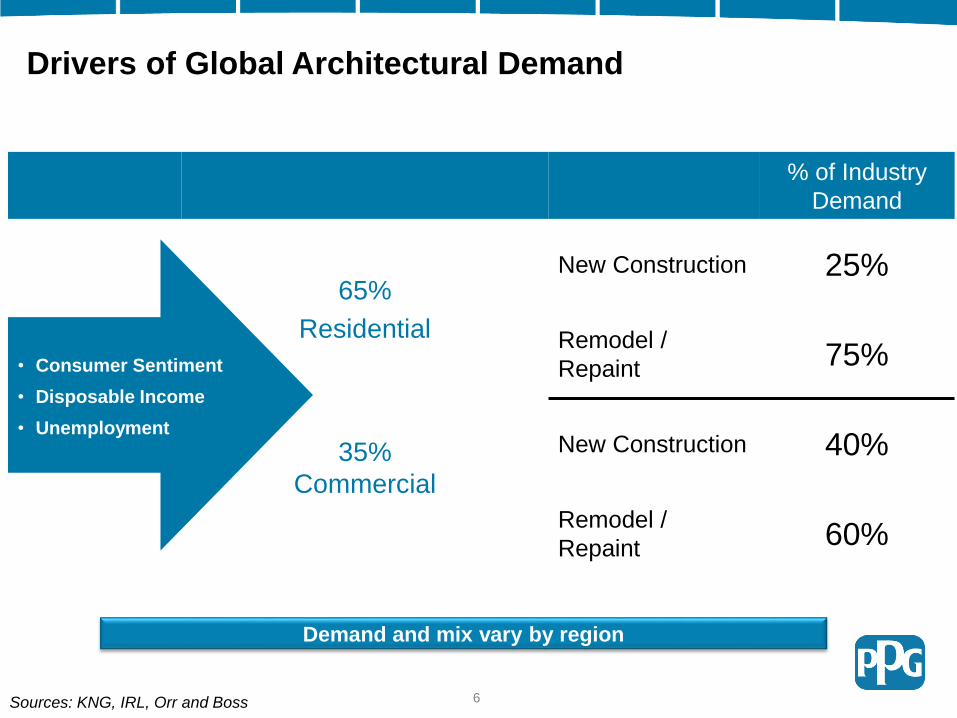

% of Industry

Demand

65%

Residential

New Construction 25%

Remodel /

Repaint75%

35%

Commercial

New Construction 40%

Remodel /

Repaint60%

Drivers of Global Architectural Demand

• Consumer Sentiment

• Disposable Income

• Unemployment

Demand and mix vary by region

Sources: KNG, IRL, Orr and Boss 6

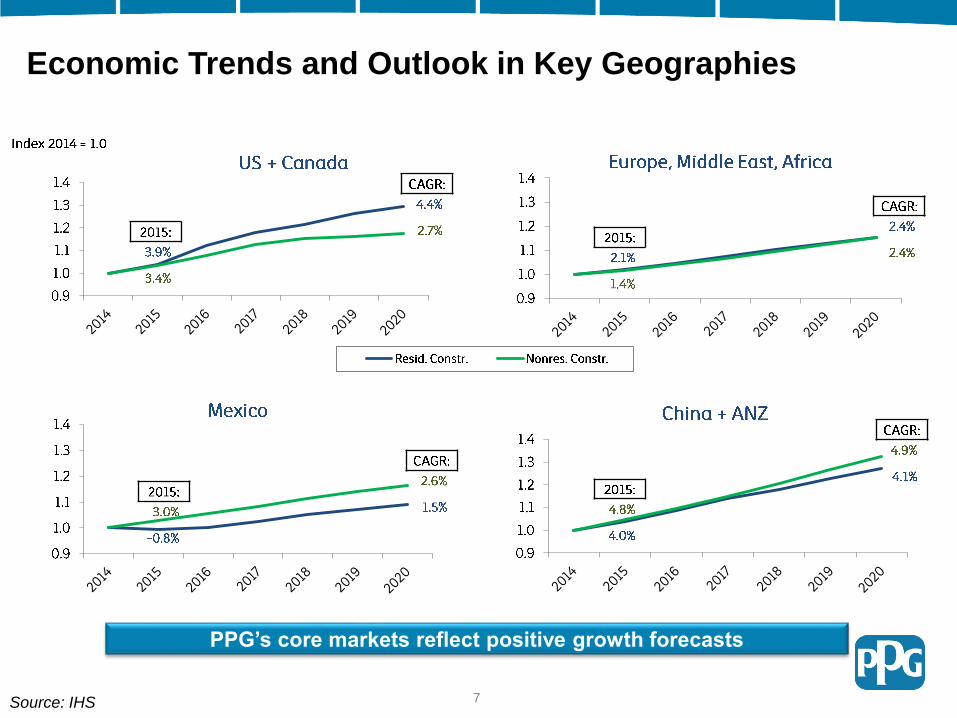

Economic Trends and Outlook in Key Geographies

PPG’s core markets reflect positive growth forecasts

Source: IHS 7

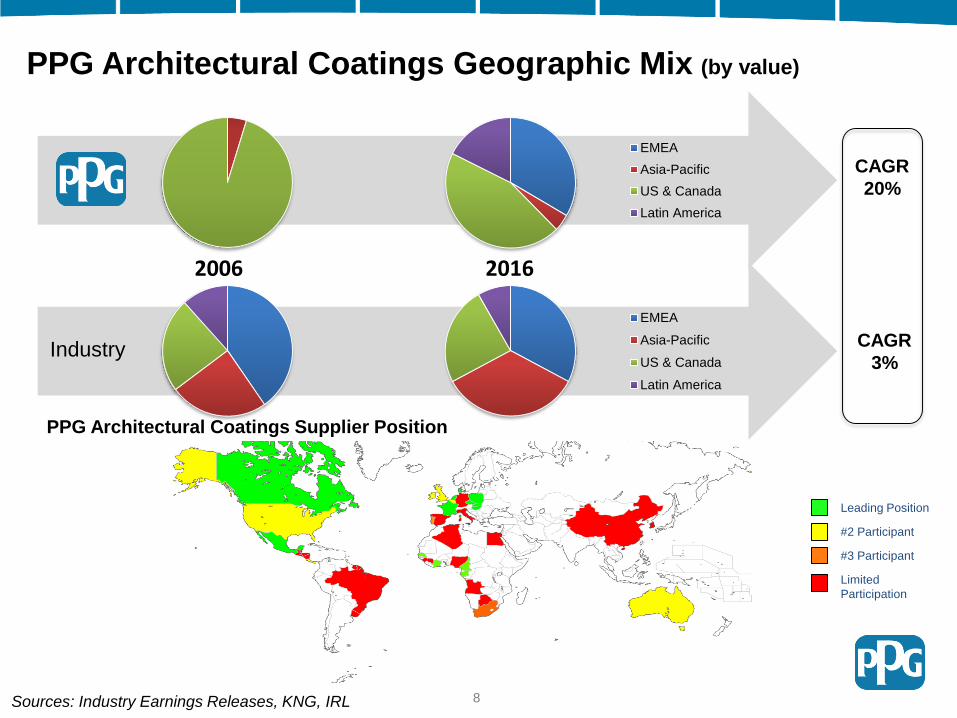

PPG Architectural Coatings Geographic Mix (by value)

Industry

EMEA

Asia-Pacific

US & Canada

Latin America

EMEA

Asia-Pacific

US & Canada

Latin America

CAGR

20%

CAGR

3%

2006 2016

Leading Position

#2 Participant

#3 Participant

Limited

Participation

Sources: Industry Earnings Releases, KNG, IRL

PPG Architectural Coatings Supplier Position

8

Distinct Channels and Brands Around the World

USCA

EMEA

LATAM

AP

PPG

Global

Industry

9

Home Centers Becoming Increasingly Global

* *

*Announced during the past 3 months

10

Industry Details – Latin America

• Oil is moderating Mexican GDP,

consumer spending is improving

• High single-digit (HSD) growth in

Central America is expected over

the next several years

• Brazilian paint demand declined

HSD in 2015; remains weak in 2016

• Paint season is strongest from

October through December

• Distribution through independents;

home centers still a small component

• Consumers are very brand centric

• Central America remains very

fragmented

50%

10%

25%

15%

Mexico Central America Brazil Other

Outlook

Regional Industry Characteristics

11Source: PPG Estimates

Industry Revenue by Country

0%

1%

2%

3%

4%

2015 2016 2017 2018 2019 2020

Mexican GDP Growth Forecast(PPG Comex historically grew at ~2x GDP)

Sources: World Bank, KNG, IRL 11

Mexican Architectural Coatings Landscape

Company DescriptionStore Count

Coatings industry leader,

Largest exclusive network 4,000+

~155Large manufacturer in north

region, Home Depot supplier

Large presence in the

metropolitan area with ~60

stores

~360

Strong presence in central

region with ~ 135 third party

stores

~300

~180 stores in southwest

region and Jalisco~350

~135 third party stores in the

central region~630

PPG Comex Store Location

Geographic expansion opportunities remain for PPG Comex

Density

Lower

Higher

12

Rapidly Growing Comex and Glidden in Central America

Stores

(Comex and Glidden)

PPG supplies all major distribution channels in PanamaChannel exclusivity through Glidden sub-brands

Belize

Costa Rica

Nicaragua

Panama

Honduras

El Salvador

Guatemala 39

19

11

9

9

6

4

2016 $400MM Industry

13

Industry Details – Asia-Pacific

• Regional growth rates remain above

developed regions

• China growth continues – but moderating

due to commercial construction

• Australian house price appreciation is

attracting homeowner investments; new

home builds continue to be solid

• China and Australia have very different paint dynamics:

Home centers growing and predominant in Australia; not relevant in China

Chinese competitive environment very fragmented

Professionals account for 90% of paint application in China

• Home center consolidation underway in Australia (PPG aligned with Bunnings)

45%

21%

7%

7%

20%

China India Japan Australia Other

Outlook

Regional Industry Characteristics

14Source: PPG Estimates

Industry Revenue by Country

0%

1%

2%

3%

4%

2015 2016 2017 2018 2019 2020

Australia Housing Renovation Forecast

Value of Investment

Sources: Housing Industry Association Limited, KNG, IRL

Avg. Growth +2.6%

14

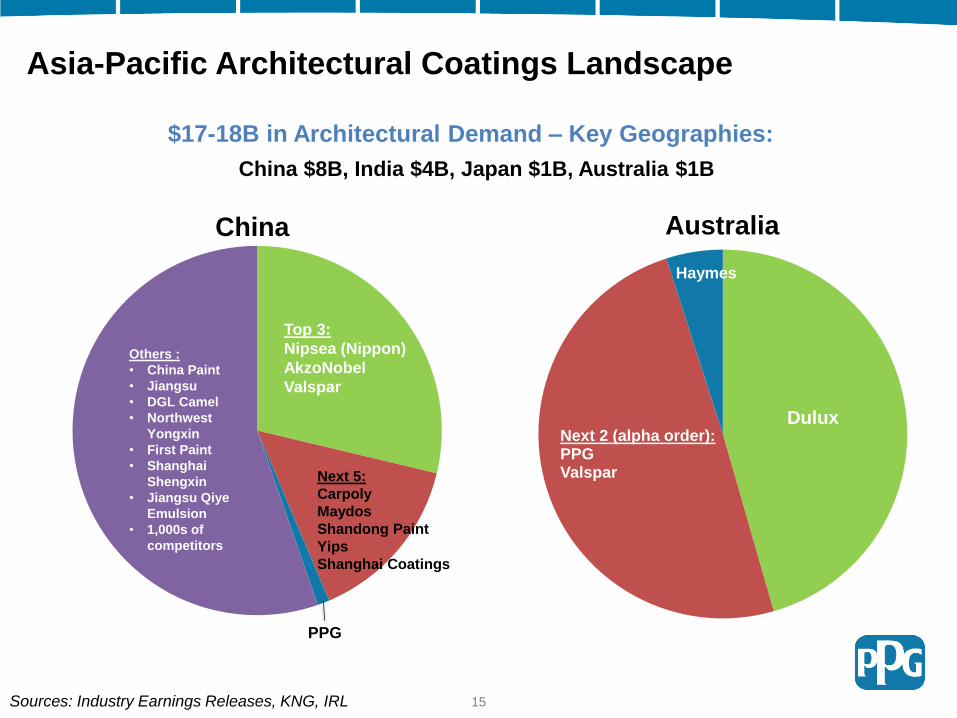

Asia-Pacific Architectural Coatings Landscape

Others :

• China Paint

• Jiangsu

• DGL Camel

• Northwest

Yongxin

• First Paint

• Shanghai

Shengxin

• Jiangsu Qiye

Emulsion

• 1,000s of

competitors

DuluxNext 2 (alpha order):PPGValspar

Haymes

China Australia

$17-18B in Architectural Demand – Key Geographies:

China $8B, India $4B, Japan $1B, Australia $1B

Top 3:

Nipsea (Nippon)

AkzoNobel

Valspar

Next 5:

Carpoly

Maydos

Shandong Paint

Yips

Shanghai Coatings

PPG

Sources: Industry Earnings Releases, KNG, IRL 15

PPG Asia-Pacific Architectural Coatings at a Glance

Australia PPG Brands

• PPG strongly aligned with Bunnings (leading ANZ home center)

• ~40 Taubmans company-owned stores; Bristol captive independents

China PPG Brands

• Master’s Mark® product competes favorably in premium range

• Seigneurie ® used for project segment

• PPG a very small participant in the Chinese architectural paint industry

Home Center

Company Stores

Independent Dealer

PPG Revenue Mix

Australia

China

1616

Industry Details – Europe, Middle East, and Africa (EMEA)

• UK & Ireland continue to demonstrate growth

above other developed countries

• Home center consolidation activities

• Eastern Europe growing but mixed

• France demand stabilizing

• Early 2016 industry demand growth

• Private label is prevalent in home centers

• Western Europe is much different than

Eastern Europe:

Western Europe: mature distribution models,

focus on product quality and service

Eastern Europe: lower consumption; wholesaler

distribution models

35%

25%

40%

Home Center Company Stores Independent

Outlook

Regional Industry Characteristics

17Source: PPG Estimates

Industry Revenue by Channel

Sources: Euroconstruct, KNG, PPG estimates

-4%

-2%

0%

2%

4%

2011 2012 2013 2014 2015 2016 2017 2018

France Construction

weighted index

17

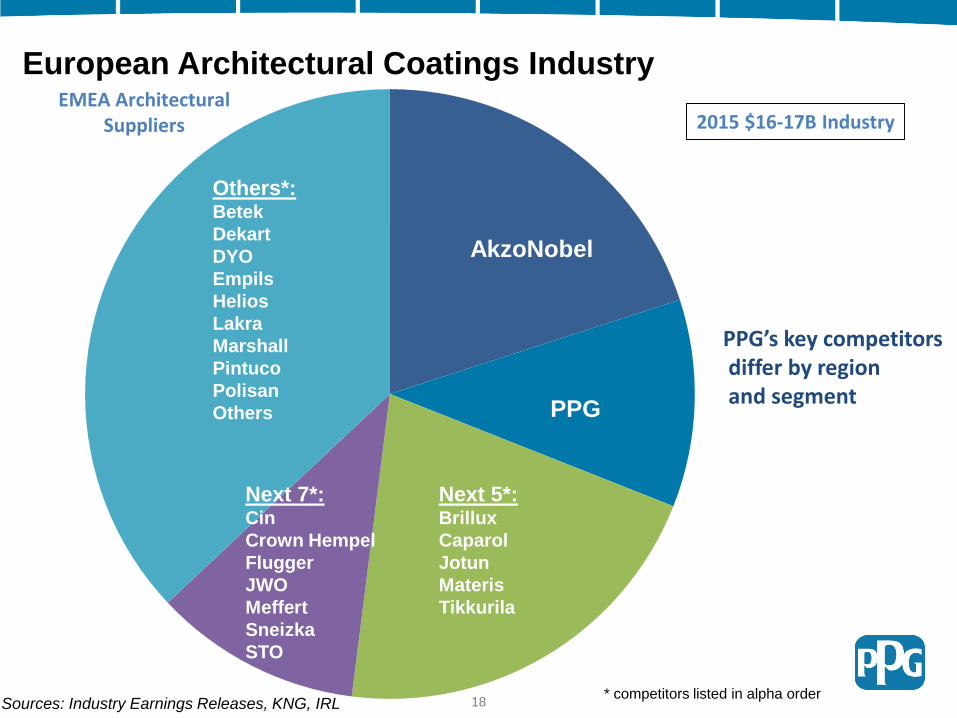

European Architectural Coatings Industry

PPG’s key competitorsdiffer by regionand segment

EMEA Architectural Suppliers

Others*:Betek

Dekart

DYO

Empils

Helios

Lakra

Marshall

Pintuco

Polisan

Others

2015 $16-17B Industry

Sources: Industry Earnings Releases, KNG, IRL 18

AkzoNobel

PPG

Next 5*:Brillux

Caparol

Jotun

Materis

Tikkurila

Next 7*:Cin

Crown Hempel

Flugger

JWO

Meffert

Sneizka

STO

* competitors listed in alpha order

Competitive Landscape Varies by Country

IBERIA

Cin

Materis

PPG

Titan

ITALY

>500 paint companies

FRANCE

AkzoNobel

Materis

PPG

V 33

UNITED KINGDOM

AkzoNobel

Hempel (Crown)

Ostendorf

PPG

POLAND

AkzoNobel

PPG

Sneizka

Tikkurila

GERMANY

Brillux

DAW

Ostendorf

Remmers

Sources: Industry Earnings Releases, KNG, IRL

European paint supply is fragmented by country and sub-region

note: competitors listed in alpha order

SCANDANVIA

AkzoNobel

Flugger

Jotun

Tikkirula

19

PPG Remains Positioned for Growth in Europe

$5B

$9B

PPG Participation:

top 1 or 2 position

PPG participation:small to none

#1 PPG Position

#2 PPG Position

#3 PPG Position

>#3 PPG Position

No PPG Participation

European* Coatings

DemandDemand in regions relative to

PPG Presence

*Does not include Middle East and Africa

Sources: IRL, KNG, PPG estimates 20

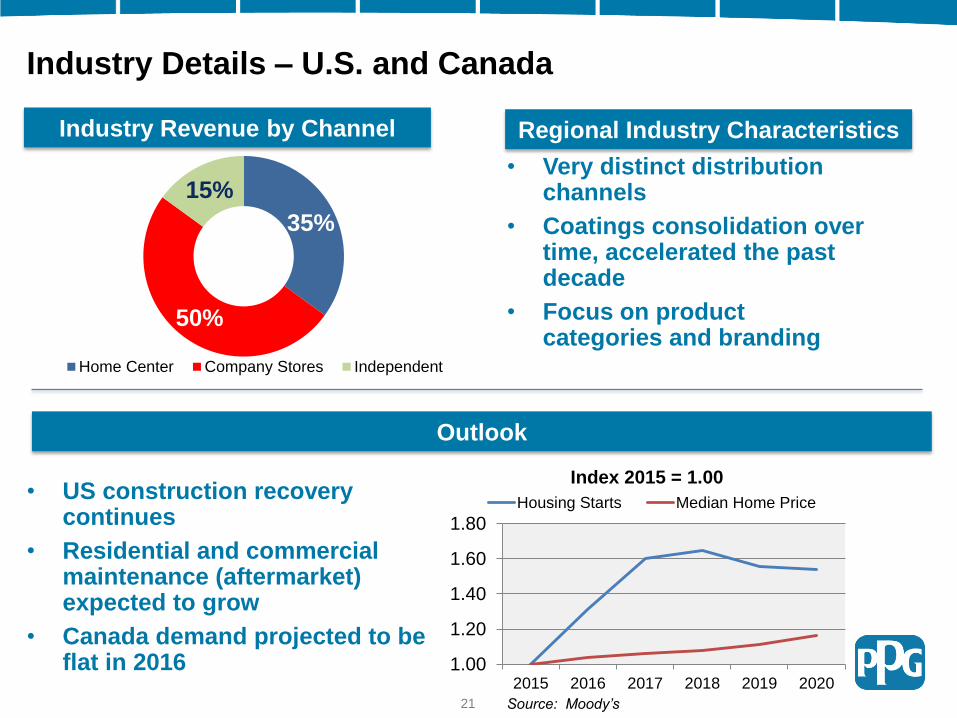

Industry Details – U.S. and Canada

35%

50%

15%

Home Center Company Stores Independent

Outlook

Regional Industry Characteristics

21Source: PPG Estimates

Industry Revenue by Channel

1.00

1.20

1.40

1.60

1.80

2015 2016 2017 2018 2019 2020

Index 2015 = 1.00

Housing Starts Median Home Price

Source: Moody’s

• Very distinct distribution channels

• Coatings consolidation over time, accelerated the past decade

• Focus on product categories and branding

• US construction recovery continues

• Residential and commercial maintenance (aftermarket) expected to grow

• Canada demand projected to be flat in 2016

21

U.S. and Canada Architectural Coatings Competitive Landscape

Source: Company Reports, PPG estimates 22Source: PPG Analysis

• Competitive set differs by

channel and country

• PPG is a major participant

in all 3 channels

• PPG is a clear leader in

Canada

22

Other

U.S. and Canada Architectural Coatings Industry Landscape

Source: Company Reports, PPG estimates 23

Company Owned Stores Home Centers Independent Dealer

0% 50% 100%

PPG

Industry

Ind. Dealers – End Use

0% 25% 50% 75% 100%

PPG

Industry

Company Stores – End Use

0% 50% 100%

PPG

Industry

Home Centers– End Use

Professional DIY

Source: PPG Analysis

PPG has significant participation in all channels

23

24

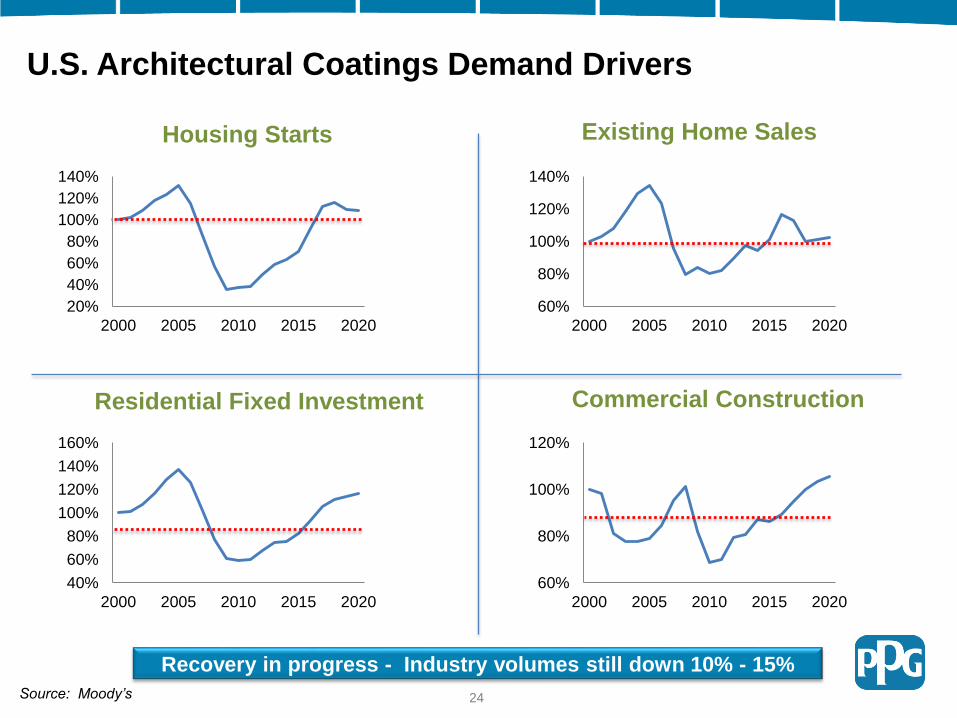

U.S. Architectural Coatings Demand Drivers

20%

40%

60%

80%

100%

120%

140%

2000 2005 2010 2015 2020

Housing Starts

60%

80%

100%

120%

140%

2000 2005 2010 2015 2020

40%

60%

80%

100%

120%

140%

160%

2000 2005 2010 2015 2020

60%

80%

100%

120%

2000 2005 2010 2015 2020

Existing Home Sales

Residential Fixed Investment Commercial Construction

Recovery in progress - Industry volumes still down 10% - 15%

Source: Moody’s

65%

35%

Residential Commercial

Customer Touch Points

Home Center Company Stores

Independent Dealer

Channel Points of

Sale (POS)

Home Centers ~8,000

Independent

Distributors~6,000

Company-

Owned Stores~900

Total ~15,000

PPG Architectural Coatings – U.S. and Canada

80%

20%

Channel Mix - Revenue End-Use Mix - Revenue

2525

PPG Company-Owned Stores – U.S. and Canada

26

Growth opportunities: increase density and expand presence

26

Company-Owned Stores: Supporting Professional Painters

Professional Painters – Value Drivers

Store Manager

Full Time Associate(s)

Part Time Associate(s)

Robust Support Network Surround Stores

Sales Support

Account Development

Regional Sales

Zone Sales

Operations

Store Group Manager

Director of Store Operations

Vice President of Stores

• Product specifications

• Product performance

• Delivery

• Credit

• Product availability

• Competitive pricing

Rebranding Initiative

• Consistent branding coast-to-coast

• Store upgrades

27

28

National Home Centers

Wide Offering of

Decorative Paint

PPG sales to home centers

Leader in

Stains

Leveraging

Adhesives and Sealants

PAINT REPRESENTS

7-9% OF HOME CENTER SALES

Coatings remains an important sales category for home centers

Source: Lowes/THD Annual Reports

Paint is critical for home centers; drives foot traffic and profits

29

2016 National Accounts Product LaunchesProviding value for key channel partners

Source: Lowes/THD Annual Reports

Launches supported by $15MM investment in Q1 2016

2016 Brand

Investment

• New premium

products

• New product

formulations

• New product

labeling

• Increased focus

on customer field

support, tools

New product delivers

extreme durabilityNew & improved formula

Best paint for value-

conscious consumer

First super premium

paint at MenardsWalmart premium offering

Clear product differentiation

30

Independent Dealer Channel

• 10,000 + locations in USCA

• Range from hardware stores to

dedicated paint stores

• Vary in size from single store to several

dozen locations

• Service

• Location

• Product

• Multiple supplier brands

• Range of decorative -to-

protective coatings

• Some offer interior design services

Benjamin Moore

PPG

Valspar (Ace Hardware)

Pratt and Lambert (Sherwin-Williams)

California Paints

Offering Coatings Suppliers

Dealer Attributes PPG Strategy

• “Partner of Choice”

• Differentiate through products, brands

and professional programs

• Acquirer of choice for owners exiting

the business

Key Comments on Architectural Coatings

• Global Industry

Growing across most geographies; emerging region growth outpacing mature

region growth

Local brands, distribution, and operational excellence drive commercial

success

• Competitive Dynamics

Fragmented competitive landscape with few global players

Industry consolidation likely to continue as key competitors build scale

Strong regional players will continue to exist and grow

• PPG Focus

Continue to develop and expand in existing regions

New stores, independent dealer acquisitions, enhanced brand strategy

Balance emerging region growth with mature market opportunities

Acquisitions and organic growth

Drive margin expansion via scale and operational excellence

31

32

PPG Video

Key Comments on Architectural Coatings

• Global Industry

Growing across most geographies; emerging region growth outpacing mature

region growth

Local brands, distribution, and operational excellence drive commercial

success

• Competitive Dynamics

Fragmented competitive landscape with few global players

Industry consolidation likely to continue as key competitors build scale

Strong regional players will continue to exist and grow

• PPG Focus

Continue to develop and expand in existing regions

New stores, independent dealer acquisitions, enhanced brand strategy

Balance emerging region growth with mature market opportunities

Acquisitions and organic growth

Drive margin expansion via scale and operational excellence

33

Related Documents