Property, Plant and Property, Plant and Equipment – Wasting Equipment – Wasting Assets Assets

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Property, Plant and Property, Plant and Equipment – Wasting AssetsEquipment – Wasting Assets

Property, Plant and Property, Plant and Equipment – Wasting AssetsEquipment – Wasting Assets

Relevant StandardsRelevant Standards Relevant StandardsRelevant Standards

• PAS 16 – Property, Plant and Equipment

• PAS 37 – Provisions, CL and CA• PFRS 6 – Exploration for and

Evaluation of Mineral Resources

Computation of DepletionComputation of Depletion Computation of DepletionComputation of Depletion Method - Should reflect pattern of

benefit consumption, usually output method

Output x Depletion rate = Depletion

Cost P xxResidual value ( xx)Amount subject to depletion xx/Estimated reserves xxDepletion rate xx

Costs of Wasting AssetsCosts of Wasting AssetsCosts of Wasting AssetsCosts of Wasting Assets

• Acquisition

• Exploration and evaluation

• Development

• Restoration

PFRS 6 – PFRS 6 – Exploration for and EvaluationExploration for and Evaluation of Mineral Resources of Mineral Resources

PFRS 6 – PFRS 6 – Exploration for and EvaluationExploration for and Evaluation of Mineral Resources of Mineral Resources• PFRS 6 permits an entity to develop

an accounting policy for exploration and evaluation assets without specifically considering the requirements of paragraphs 11 and 12 of PAS 8.

• Thus, an entity adopting PFRS 6 may continue to use the accounting policies applied immediately before adopting the PFRS.

Methods used before PFRS 6Methods used before PFRS 6Methods used before PFRS 6Methods used before PFRS 6

Successful efforts methodCost of successful exploration – Capitalized

Cost of unsuccessful exploration – Expensed

Successful – The technical feasibility and commercial viability of extracting a mineral resource are demonstrable

Full cost methodAll exploration and evaluation expenditures

are capitalized

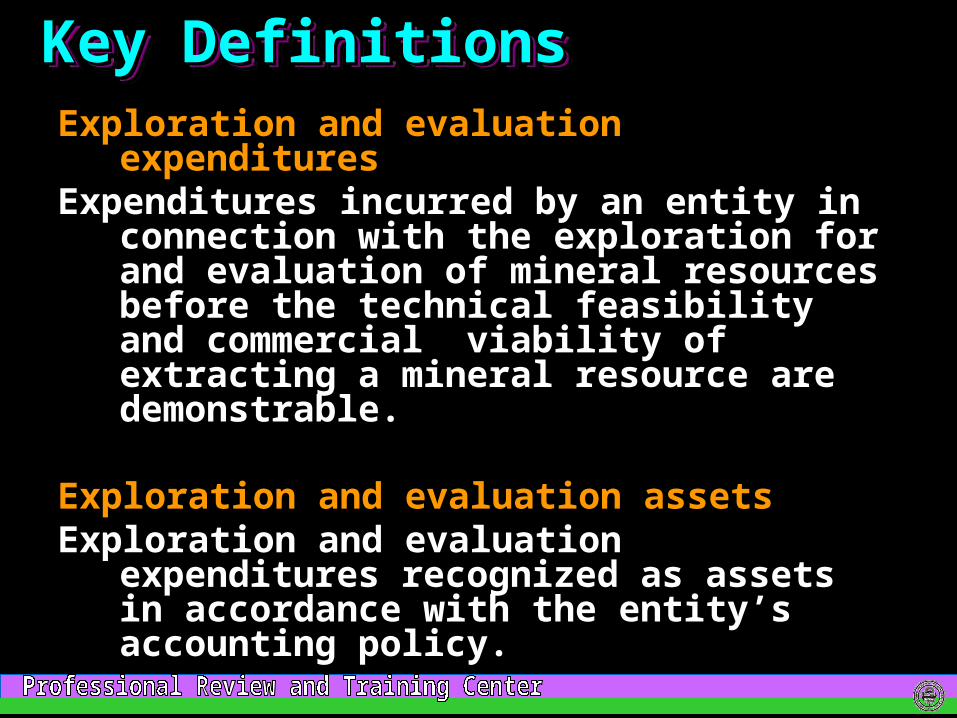

Key DefinitionsKey DefinitionsKey DefinitionsKey DefinitionsExploration for and evaluation of

mineral resources

The search for mineral resources, including minerals, oil, natural gas and similar non-regenerative resources after the entity has obtained legal rights to explore in a specific area, as well as the determination of the technical feasibility and commercial viability of extracting the mineral resource.

Examples of Exploration and Examples of Exploration and Evaluation ActivitiesEvaluation ActivitiesExamples of Exploration and Examples of Exploration and Evaluation ActivitiesEvaluation Activities

• acquisition of rights to explore• topographical, geological,

geochemical and geophysical studies

• exploratory drilling• trenching• sampling• activities in relation to evaluating

the technical feasibility and commercial viability of extracting a mineral resource

Key DefinitionsKey DefinitionsKey DefinitionsKey DefinitionsExploration and evaluation

expendituresExpenditures incurred by an entity in

connection with the exploration for and evaluation of mineral resources before the technical feasibility and commercial viability of extracting a mineral resource are demonstrable.

Exploration and evaluation assetsExploration and evaluation

expenditures recognized as assets in accordance with the entity’s accounting policy.

Reclassification of Exploration Reclassification of Exploration and Evaluation Assetand Evaluation AssetReclassification of Exploration Reclassification of Exploration and Evaluation Assetand Evaluation Asset

• An exploration and evaluation asset shall no longer be classified as such when the technical feasibility and commercial viability of extracting a mineral resource are demonstrable.

• Exploration and evaluation assets shall be assessed for impairment, and any impairment loss recognized, before reclassification.

Development CostDevelopment Cost Development CostDevelopment Cost Intangible e.g. Cost of drilling and construction of wells

Include in the cost of wasting asset

Tangiblee.g. Building and machinery and equipment

Recognize as separate asset

Depreciation method:Same method for other PPE

If the problem is silentUseful life > Life of WA – OutputUseful life < Life of WA – SL

Estimated Restoration CostEstimated Restoration Cost Estimated Restoration CostEstimated Restoration Cost

Included when recognized as provision. Therefore the restoration cost must

- Be a present obligation,- Represent a probable outflow of

economic resources, and- Be measurable reliably

Presentation of DepletionPresentation of Depletion Presentation of DepletionPresentation of Depletion

Unsold - Inventory

Sold – Cost of sales

- PROBLEMS -

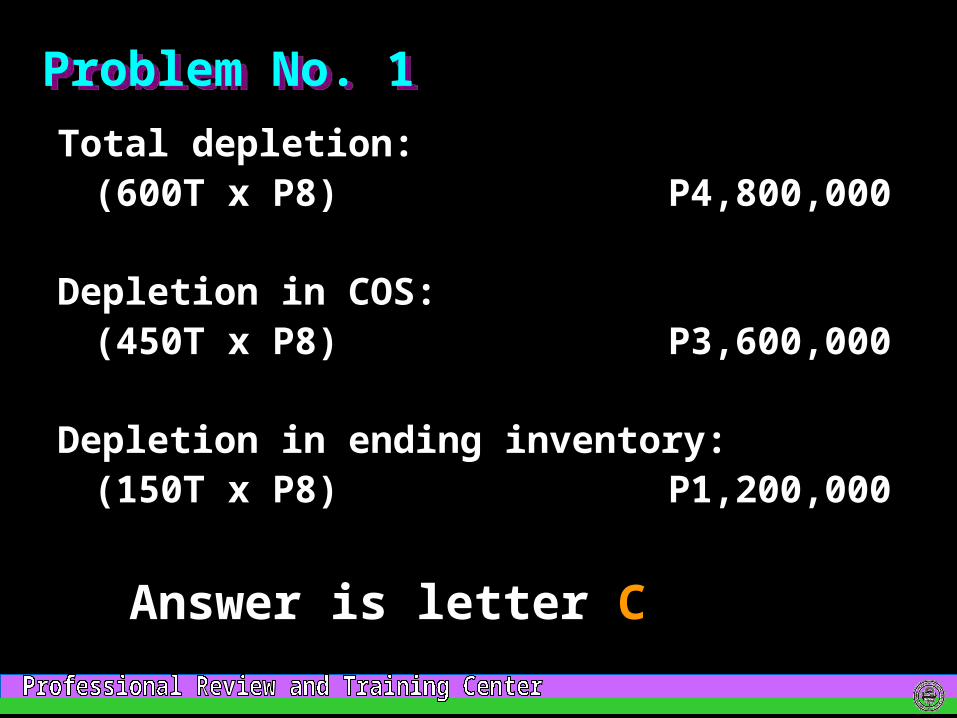

Acquisition cost P20,000,000Est. restoration cost 2,000,000Exploration cost 13,000,000Development cost – drilling 10,000,000Total cost 45,000,000Residual value ( 5,000,000)Depletable amount 40,000,000/Total est. reserves 5,000,000Depletion rate P8/ton

Problem No. 1Problem No. 1

Total depletion:(600T x P8) P4,800,000

Depletion in COS:(450T x P8) P3,600,000

Depletion in ending inventory:(150T x P8) P1,200,000

Problem No. 1Problem No. 1

Answer is letter C

Acquisition cost P 500,000Successful exploration cost

(P1.5M x 1/3) 500,000Total cost/DA 1,000,000/Total est. reserves 2,000,000Depletion rate P 0.5/ozx Output 500,000 ozDepletion for 2010 P 250,000

Problem No. 2Problem No. 2

Answer is letter C

Acquisition cost P 800,000

Est. restoration cost(P4.2M x PVF) ?

Problem No. 3Problem No. 3

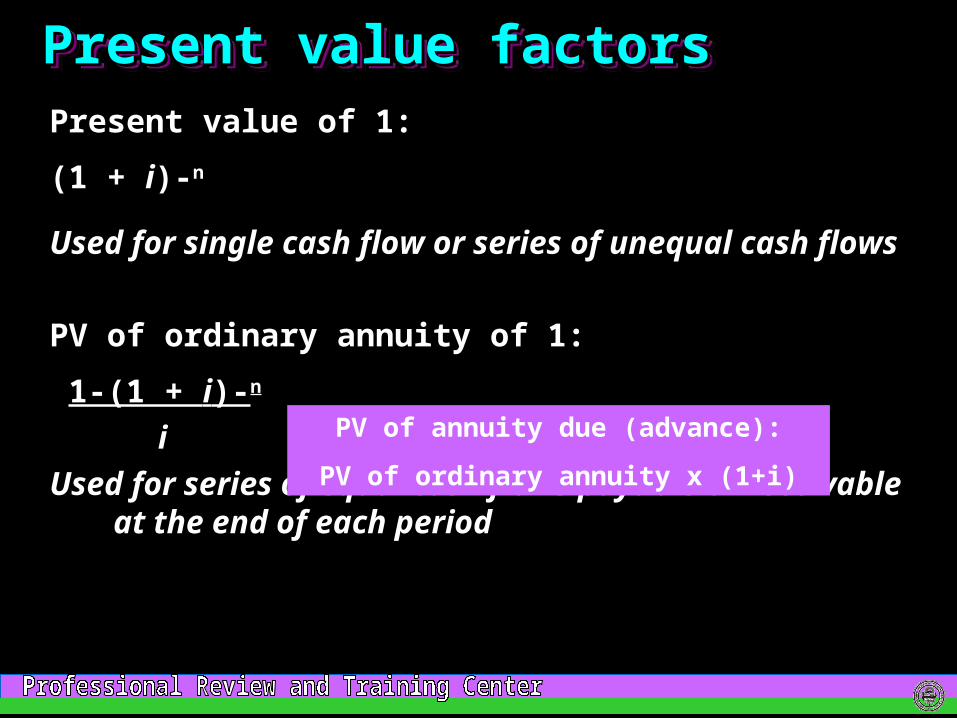

Present value factorsPresent value factorsPresent value factorsPresent value factorsPresent value of 1:

(1 + i)-n

Used for single cash flow or series of unequal cash flows

PV of ordinary annuity of 1:

1-(1 + i)-n

iUsed for series of equal cash flows payable or

receivable at the end of each period

PV of annuity due (advance):

PV of ordinary annuity x (1+i)

Acquisition cost P 800,000Est. restoration cost

(P4.2M x .3405) 1,430,100Total cost/DA 2,230,100/Total est. reserves 1,000Depletion rate P2,230/tonx Output 100 tonsDepletion for 2010 P 223,000

Problem No. 3Problem No. 3

Answer is letter C

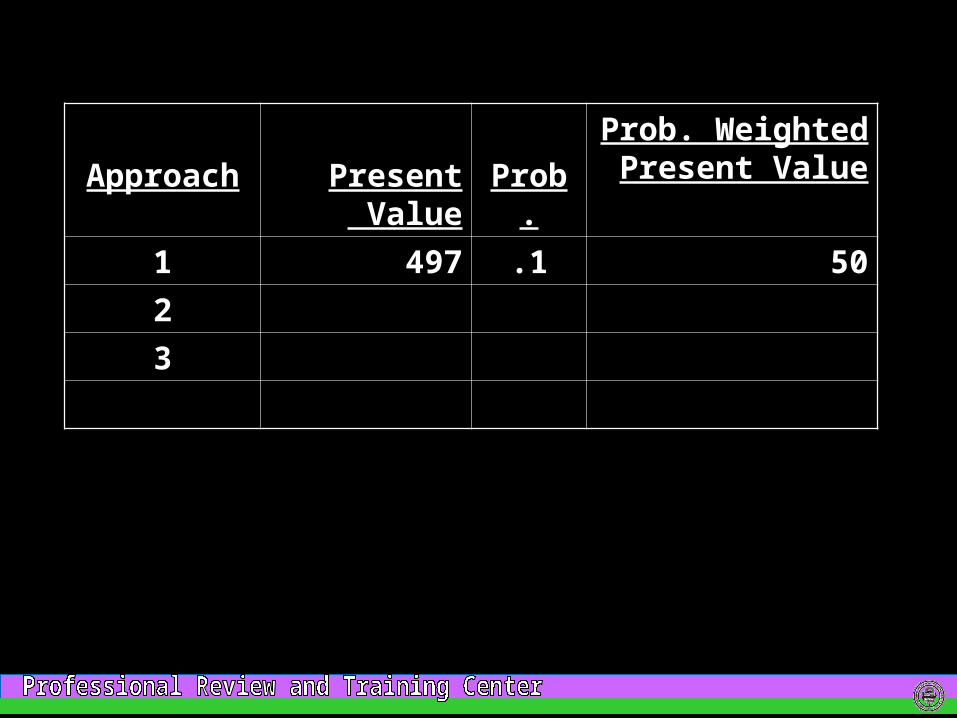

Problem No. 4Problem No. 4Problem No. 4Problem No. 4

Approach Present Value

Prob.

Prob. Weighted

Present Value

1

2

3

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497

2

3

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497 .1

2

3

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497 .1 50

2

3

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497 .1 50

2 9,938

3

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497 .1 50

2 9,938 .2

3

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497 .1 50

2 9,938 .2 1,988

3

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497 .1 50

2 9,938 .2 1,988

3 149,066

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497 .1 50

2 9,938 .2 1,988

3 149,066 .7

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497 .1 50

2 9,938 .2 1,988

3 149,066 .7 104,346

Approach Present Value

Prob.

Prob. Weighted

Present Value

1 497 .1 50

2 9,938 .2 1,988

3 149,066 .7 104,346

106,384

Cost of land P500,000Decontamination cost 106,384Total cost P606,384

Answer is letter A

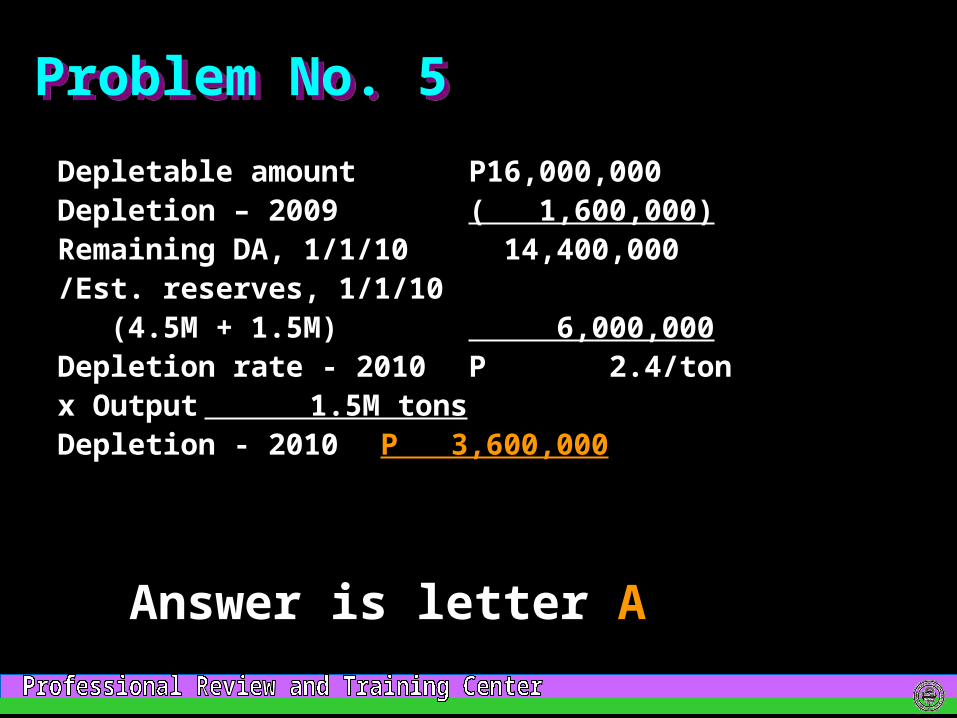

Acquisition cost P20,000,000Residual value ( 4,000,000)Depletable amount 16,000,000/Total est. reserves 5,000,000Depletion rate - 2009 P 3.2/tonx Output 500,000 tonsDepletion for 2009 P 1,600,000

Problem No. 5Problem No. 5

Problem No. 5Problem No. 5

Depletable amount P16,000,000Depletion – 2009 ( 1,600,000)Remaining DA, 1/1/10 14,400,000/Est. reserves, 1/1/10 (4.5M + 1.5M) 6,000,000Depletion rate - 2010 P 2.4/tonx Output 1.5M tonsDepletion - 2010 P 3,600,000

Answer is letter A

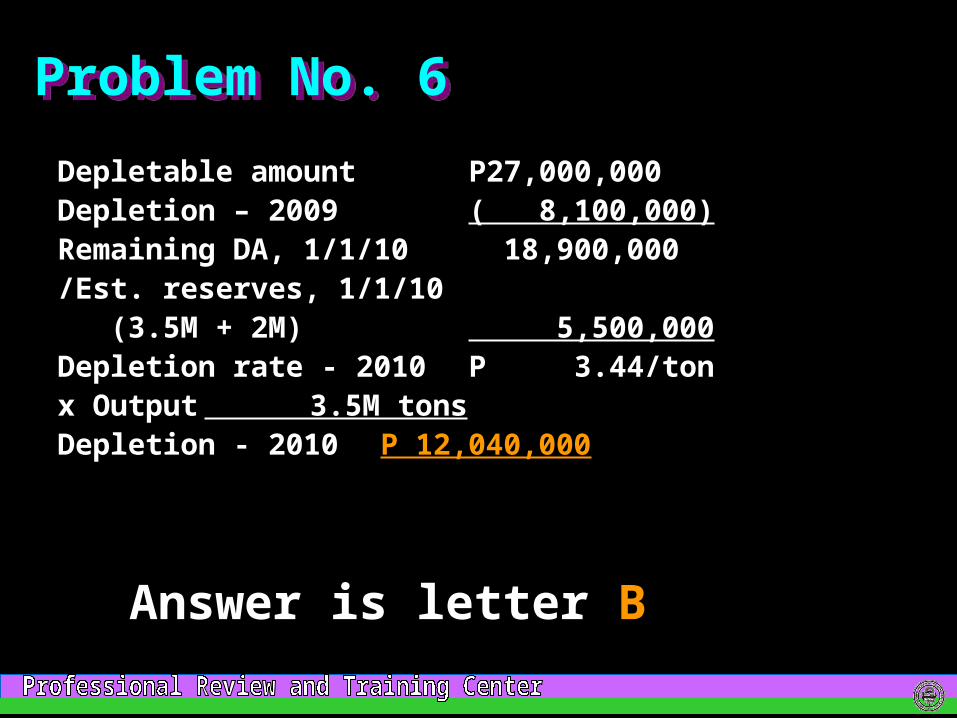

Problem No. 6Problem No. 6Acquisition cost P28MEst. restoration cost 2MDevelopment cost – 2008 1MDevelopment cost – 2009 1MTotal cost 32MResidual value ( 5M)Depletable amount 27M/Est. reserves 10MDepletion rate - 2009 2.7x Output – 2009 3MDepletion – 2009 P8.1M

Problem No. 6Problem No. 6

Depletable amount P27,000,000Depletion – 2009 ( 8,100,000)Remaining DA, 1/1/10 18,900,000/Est. reserves, 1/1/10 (3.5M + 2M) 5,500,000Depletion rate - 2010 P 3.44/tonx Output 3.5M tonsDepletion - 2010 P 12,040,000

Answer is letter B

Problem No. 7Problem No. 7Depreciation method:Useful life > Life of WA – OutputUseful life < Life of WA – SL

Life of WA (1.2M/240T) = 5 years

Fixed installations:Useful life – 8 years; method – Output

Equipment:Useful life – 4 years; method – SL

Problem No. 7Problem No. 7Fixed installations: DR = P9.6M/1.2M units DR = P8/unit (120,000 units x P8) P 960,000

Equipment (P12.4M/4) 3,100,000

Total P4,060,000

Answer is letter A

Depreciable amount P15,000,000Depreciation – 1st yr.

(200,000 x P15) ( 3,000,000)Remaining DA 12,000,000Depreciation – 2nd yr.

(P12M/5) ( 2,400,000)Remaining DA 9,600,000/Rem. est. reserves 800,000Depreciation rate–3rd yr.P 12/tonx Output 300,000 tonsDepreciation – 3rd yr. P 3,600,000

Problem No. 8Problem No. 8

Answer is letter C

Retained earnings P10,000,000Acc. Depletion 20,000,000Total 30,000,000Capital liquidated – PY (15,000,000)Depletion-E.I.

(20,000 x P50) ( 1,000,000)Maximum P14,000,000

Problem No. 9Problem No. 9

Answer is letter B

Journal entry Retained earnings P10MCapital liquidated 4M

Dividends payable P14M

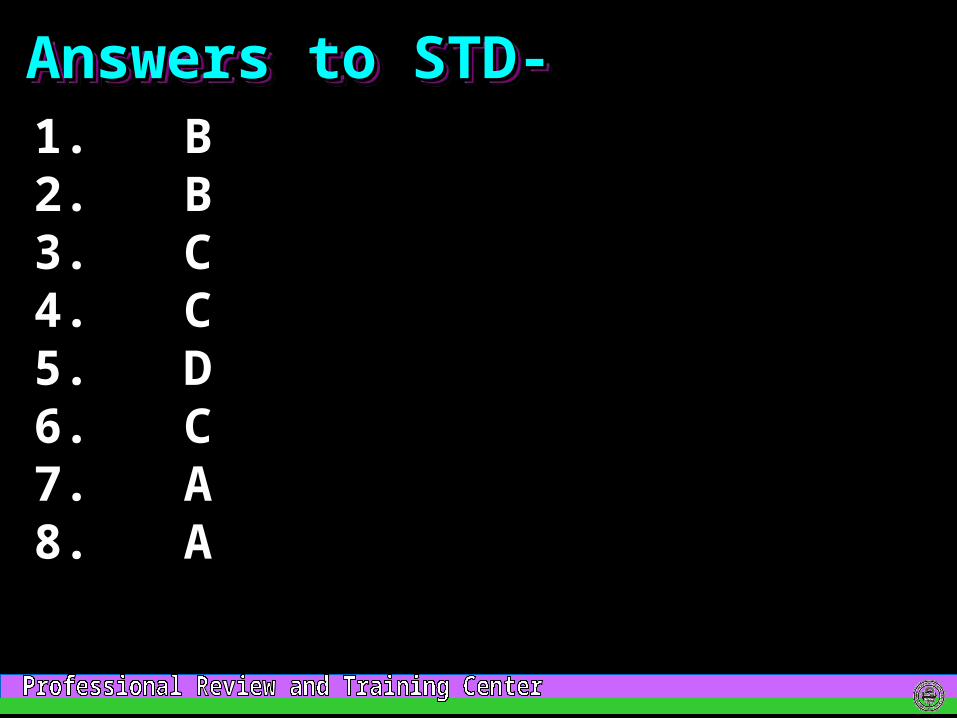

-now do your STD-

Answers to STD-Answers to STD-Answers to STD-Answers to STD-1. B2. B3. C4. C5. D6. C7. A8. A

Related Documents