Investor Presentation September 2015 happy moments

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Investor Presentation

September 2015

happy moments

2

1. Ülker: Ülker In Brief

2. Organic Growth Drivers

3. Inorganic Growth Opportunities & Godiva

4. Operational Performance

5. Financials

6. Appendix

3

8

13

18

24

29

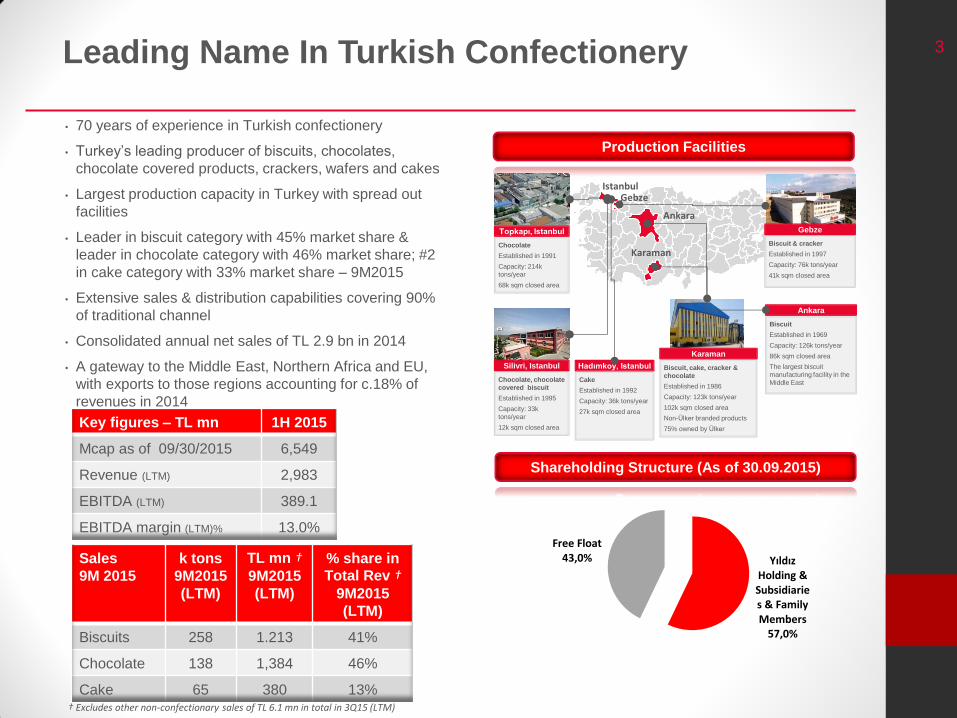

3 Leading Name In Turkish Confectionery

• 70 years of experience in Turkish confectionery

• Turkey’s leading producer of biscuits, chocolates,

chocolate covered products, crackers, wafers and cakes

• Largest production capacity in Turkey with spread out

facilities

• Leader in biscuit category with 45% market share &

leader in chocolate category with 46% market share; #2

in cake category with 33% market share – 9M2015

• Extensive sales & distribution capabilities covering 90%

of traditional channel

• Consolidated annual net sales of TL 2.9 bn in 2014

• A gateway to the Middle East, Northern Africa and EU,

with exports to those regions accounting for c.18% of

revenues in 2014

Key figures – TL mn 1H 2015

Mcap as of 09/30/2015 6,549

Revenue (LTM) 2,983

EBITDA (LTM) 389.1

EBITDA margin (LTM)% 13.0%

† Excludes other non-confectionary sales of TL 26 mn

Production Facilities

Chocolate

Established in 1991

Capacity: 214k

tons/year

68k sqm closed area

Topkapı, Istanbul

Istanbul

Chocolate, chocolate

covered biscuit

Established in 1995

Capacity: 33k

tons/year

12k sqm closed area

Silivri, Istanbul Biscuit, cake, cracker &

chocolate

Established in 1986

Capacity: 123k tons/year

102k sqm closed area

Non-Ülker branded products

75% owned by Ülker

Karaman

Cake

Established in 1992

Capacity: 36k tons/year

27k sqm closed area

Hadımkoy, Istanbul

Biscuit

Established in 1969

Capacity: 126k tons/year

86k sqm closed area

The largest biscuit

manufacturing facility in the

Middle East

Ankara

Biscuit & cracker

Established in 1997

Capacity: 76k tons/year

41k sqm closed area

Gebze

Gebze

Ankara

Karaman

Sales

9M 2015

k tons

9M2015

(LTM)

TL mn † 9M2015

(LTM)

% share in

Total Rev † 9M2015

(LTM)

Biscuits 258 1.213 41%

Chocolate 138 1,384 46%

Cake 65 380 13%

Shareholding Structure (As of 30.09.2015)

Yıldız Holding & Subsidiaries & Family Members

57,0%

Free Float 43,0%

† Excludes other non-confectionary sales of TL 6.1 mn in total in 3Q15 (LTM)

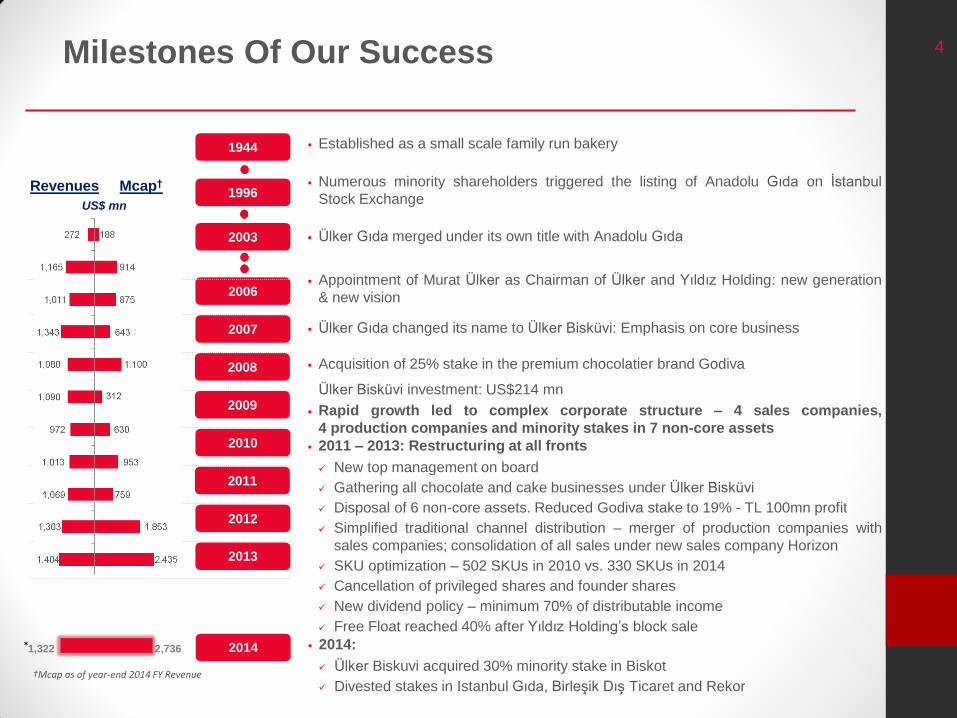

4

1996

Milestones Of Our Success

1944

2003

2006

2007

2008

2009

2010

2011

2012

2013

Established as a small scale family run bakery

Ülker Gıda merged under its own title with Anadolu Gıda

Ülker Gıda changed its name to Ülker Bisküvi: Emphasis on core business

Acquisition of 25% stake in the premium chocolatier brand Godiva

Ülker Bisküvi investment: US$214 mn

2011 – 2013: Restructuring at all fronts

New top management on board

Gathering all chocolate and cake businesses under Ülker Bisküvi

Disposal of 6 non-core assets. Reduced Godiva stake to 19% - TL 100mn profit

Simplified traditional channel distribution – merger of production companies with

sales companies; consolidation of all sales under new sales company Horizon

SKU optimization – 502 SKUs in 2010 vs. 330 SKUs in 2014

Cancellation of privileged shares and founder shares

New dividend policy – minimum 70% of distributable income

Free Float reached 40% after Yıldız Holding’s block sale

†Mcap as of year-end 2014 FY Revenue

Revenues Mcap†

US$ mn

Appointment of Murat Ülker as Chairman of Ülker and Yıldız Holding: new generation

& new vision

Numerous minority shareholders triggered the listing of Anadolu Gıda on İstanbul

Stock Exchange

Rapid growth led to complex corporate structure – 4 sales companies,

4 production companies and minority stakes in 7 non-core assets

2014 2014:

Ülker Biskuvi acquired 30% minority stake in Biskot

Divested stakes in Istanbul Gıda, Birleşik Dış Ticaret and Rekor

1,322 2,736 *

5

Advocacy

Familiarness

Recognition

Like

The “Best Recognized” FMCG Brand

Most Genuine

Company

(MediaCat & Ipsos,

2014)

The “Brand Award”

(International Brands

Conference, 2011)

# 1

# 2

# 3

# 4

# 5

Source: Ipsos

Ülker has always been the “most recognized” brand and

“closest to consumers

Best Recognized

Brands Brand One Feels

Closest To

Long lasting relationships with end users enhance brand

perception

Ülker Perception Study in 2014 Proves that Ülker is

positioned well above Turkey Benchmark in Trust, Like,

Recognition, Familiarness, and Advocacy

Strength of the brand is proven by national and

international awards

Trust

Source: ACNielsen

Ülker Turkey

Consensus

79% 45%

79% 47%

83% 56%

99% 91%

73% 42%

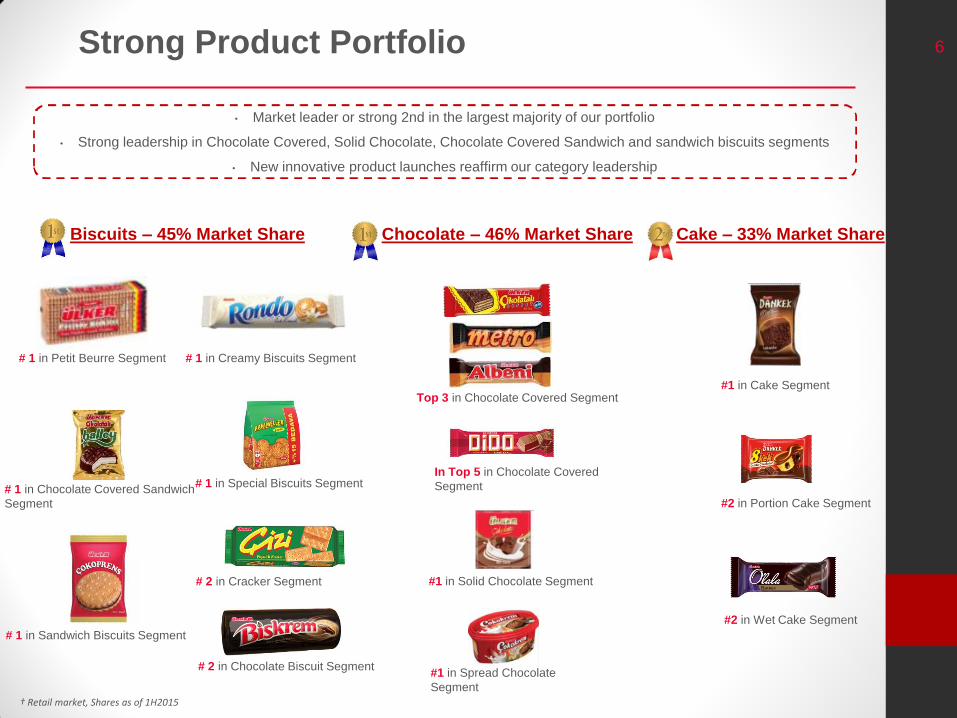

6 Strong Product Portfolio

Biscuits – 45% Market Share Chocolate – 46% Market Share

† Retail market, Shares as of 1H2015

# 1 in Petit Beurre Segment

Cake – 33% Market Share

# 1 in Sandwich Biscuits Segment

# 1 in Creamy Biscuits Segment

# 1 in Special Biscuits Segment # 1 in Chocolate Covered Sandwich

Segment

Top 3 in Chocolate Covered Segment

#1 in Solid Chocolate Segment

#1 in Spread Chocolate

Segment

#1 in Cake Segment

# 2 in Cracker Segment

# 2 in Chocolate Biscuit Segment

In Top 5 in Chocolate Covered

Segment

#2 in Portion Cake Segment

#2 in Wet Cake Segment

• Market leader or strong 2nd in the largest majority of our portfolio

• Strong leadership in Chocolate Covered, Solid Chocolate, Chocolate Covered Sandwich and sandwich biscuits segments

• New innovative product launches reaffirm our category leadership

7

1. Ülker: Ulker In Brief

2. Organic Growth Drivers

3. Inorganic Growth Opportunities & Godiva

4. Operational Performance

5. Financials

6. Appendix

3

8

13

18

24

29

8

16%

12%

14%

15%

14%

12%

17%

25%

17%

17%

14%

11%

8%

7%

0-14

15-24

25-34

35-44

45-54

55-64

65+

EU-27 Turkey

59%

41%59%

41%

1.7%

1.4%

1.3%

1.2%

0.9%

0.7%

0.5%

0.5%

0.5%

0.3%

0.2%

0.2%

0.2%

-0.1%

Malaysia

Turkey

Indonesia

S.Africa

Brazil

UK

France

Italy

Netherlands

Czech Rep.

Poland

Russia

Greece

Germany

Turkey has one

of the youngest

and fastest

growing

populations

Attractive target

consumer group

Source: World Bank, Turkstat

Sizeable market with a growing population Youngest population in Europe

Favorable Demographics & Young Target

Population

Total population in millions

63

29

78

247

51

199

66

61

17

11

39

144

11

82

European median

41 yrs

Turkey median

31 yrs

CAGR 2007-

2014

Population

Source: Turkstat, Eurostat

9

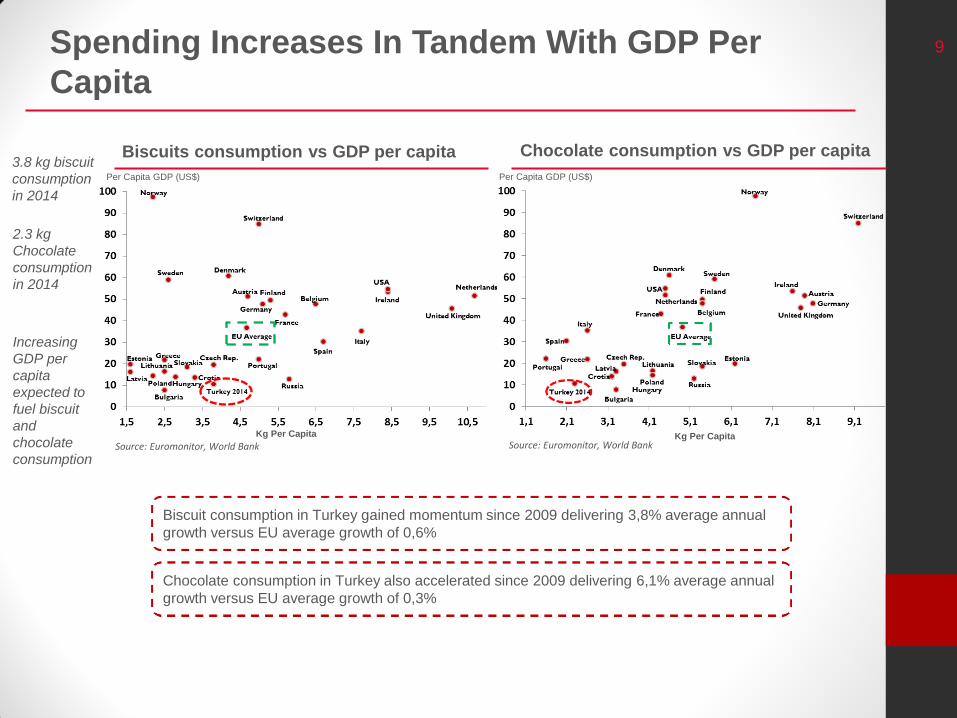

Kg Per Capita

Chocolate consumption in Turkey also accelerated since 2009 delivering 6,1% average annual

growth versus EU average growth of 0,3%

Biscuits consumption vs GDP per capita Chocolate consumption vs GDP per capita 3.8 kg biscuit

consumption

in 2014

Per Capita GDP (US$)

Biscuit consumption in Turkey gained momentum since 2009 delivering 3,8% average annual

growth versus EU average growth of 0,6%

Spending Increases In Tandem With GDP Per

Capita

Source: Euromonitor, World Bank Source: Euromonitor, World Bank

2.3 kg

Chocolate

consumption

in 2014

Increasing

GDP per

capita

expected to

fuel biscuit

and

chocolate

consumption

Kg Per Capita

Per Capita GDP (US$)

10

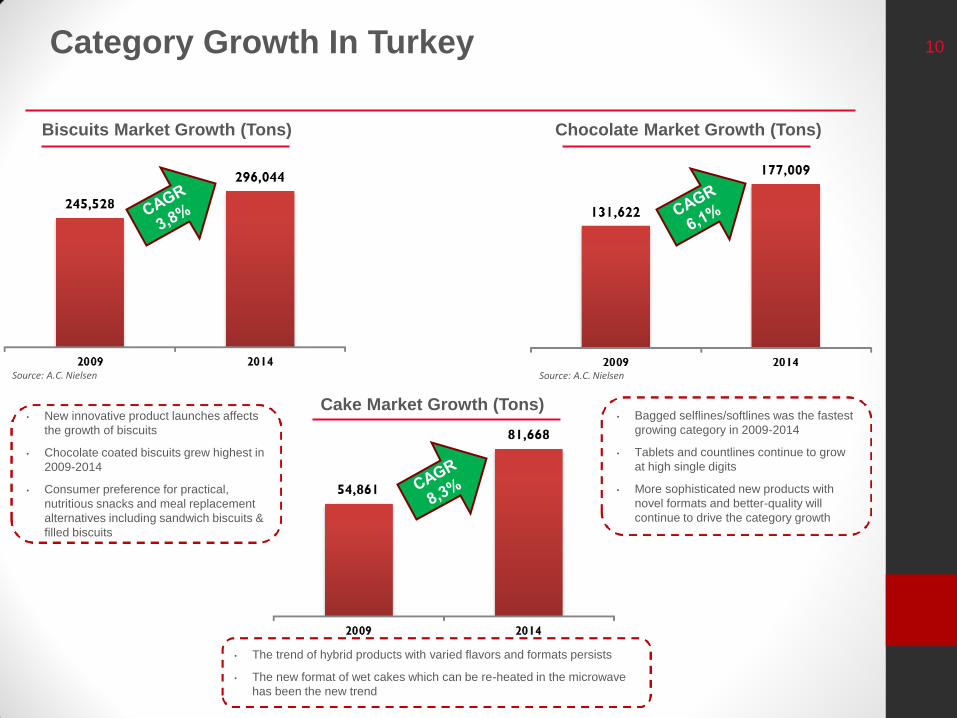

Biscuits Market Growth (Tons)

Category Growth In Turkey

• New innovative product launches affects

the growth of biscuits

• Chocolate coated biscuits grew highest in

2009-2014

• Consumer preference for practical,

nutritious snacks and meal replacement

alternatives including sandwich biscuits &

filled biscuits

Chocolate Market Growth (Tons)

Cake Market Growth (Tons)

Source: A.C. Nielsen Source: A.C. Nielsen

• Bagged selflines/softlines was the fastest

growing category in 2009-2014

• Tablets and countlines continue to grow

at high single digits

• More sophisticated new products with

novel formats and better-quality will

continue to drive the category growth

• The trend of hybrid products with varied flavors and formats persists

• The new format of wet cakes which can be re-heated in the microwave

has been the new trend

11

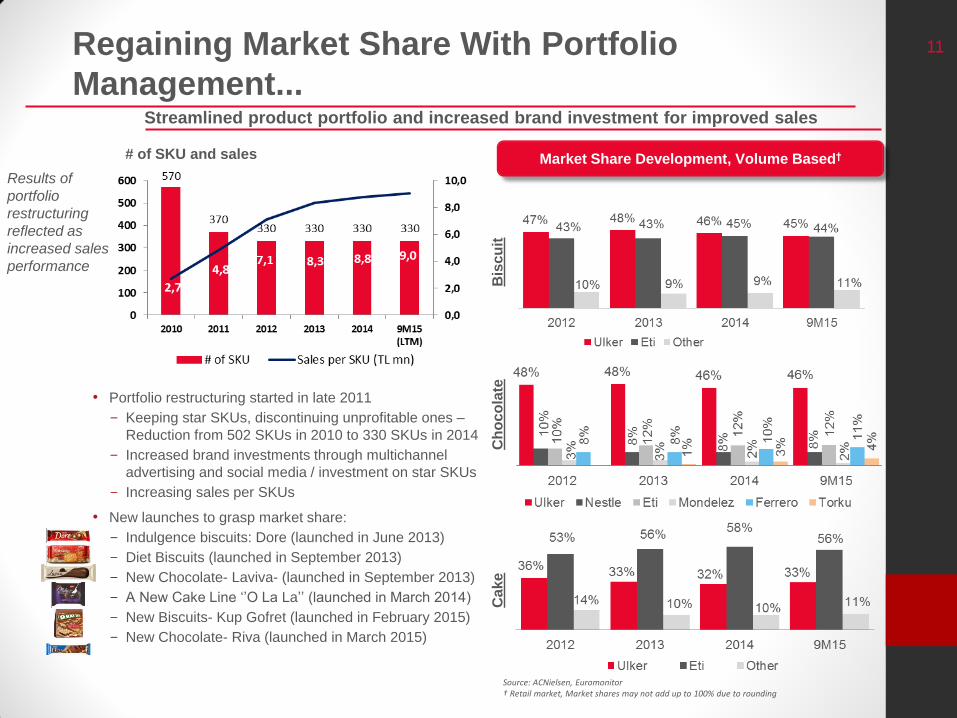

• Portfolio restructuring started in late 2011

- Keeping star SKUs, discontinuing unprofitable ones –

Reduction from 502 SKUs in 2010 to 330 SKUs in 2014

- Increased brand investments through multichannel

advertising and social media / investment on star SKUs

- Increasing sales per SKUs

• New launches to grasp market share:

- Indulgence biscuits: Dore (launched in June 2013)

- Diet Biscuits (launched in September 2013)

- New Chocolate- Laviva- (launched in September 2013)

- A New Cake Line ‘’O La La’’ (launched in March 2014)

- New Biscuits- Kup Gofret (launched in February 2015)

- New Chocolate- Riva (launched in March 2015)

Regaining Market Share With Portfolio

Management...

# of SKU and sales

Streamlined product portfolio and increased brand investment for improved sales

Market Share Development, Volume Based†

Bis

cu

it

Ch

oc

ola

te

Ca

ke

Results of

portfolio

restructuring

reflected as

increased sales

performance

Source: ACNielsen, Euromonitor † Retail market, Market shares may not add up to 100% due to rounding

12

1. Ülker: Ulker In Brief

2. Organic Growth Drivers

3. Inorganic Growth Opportunities & Godiva

4. Operational Performance

5. Financials

6. Appendix

3

8

13

18

24

29

13

Established in 2000

55% Yıldız Holding, 45% local partner

Biscuit, chocolate and cake production

Capacity: 43.000tons

c. 100 trucks reaching c. 10,000 sales

points

Saudi Arabia: A Market On The Move

Saudi Arabia Key Facts;

• Population of 30.8 mn on a 27.163.977 sq km land in 2014

• Average population growth of 2.9% in the last 5 years

• One of the world’s top 25 most competitive economies with a total GDP of US$ 745 bn

• Largest free market in the Middle East, having 38% of the total Arab GDP

• One of the world’s fastest growing countries- 5% average growth in the last 5 years

• One of the world’s most stable currency- Saudi Riyal

• c.US$ 2,5 bn confectionery market

2010 2011 2012 2013 2014

GDP Growth 1,8% 7,4% 8,6% 3,8% 3,5%

Inflation 5,8% 5,2% 3,9% 3,1% 2,5%

Population 27,6 28,4 29,2 30,0 30,8

Population

Growth 3,4% 2,9% 2,9% 2,7% 2,6%

Inorganic Growth Opportunities Lie Ahead

Source: Euromonitor, World Bank

Tons 2010 2011 2012 2013 2014

Chocolate

41.732

48.119 52.729

57.870

62.847

Biscuit

91.400

96.100 101.700

107.600

114.100

Cake

60.300

64.300 68.700

73.700

79.300

Value (US$ mn) 2010 2011 2012 2013 2014

Chocolate

600,8

738,7

852,4

993,0

1.115,6

Biscuit

485,4

541,3

606,0

680,9

751,5

Cake

417,7

459,8

516,8

583,6

649,3

FMC

(SAR x000) 2013 2014 2015E

Sales Volume

(Tons) 26,764

29,404

34,747

Net Sales

341,877

386,724 400.829

EBITDA 18,727 31,725 41,207

EBITDA

Margin 5.5% 8.2% 10.3%

Net Debt (17,279) 46,974 38,756

14

Established in 2007

46% Yıldız Holding, 54% - 2 Local

partners

Biscuit, production

Capacity: 30,000 tons

Egypt: Presenting Various Opportunities In A Sophisticated Market

Egypt Key Facts;

• Population of 83,4 mn on a 1,001,450 sq km land in 2014

• Average population growth of 1.7% in the last 5 years

• %50 of the population is under the age of 24

• Second largest economy in the Arab world with a GDP of US$

286,5 bn

• c.US$ 1,8 bn confectionery market

• Traditional channel is still dominant with c 80%

2010 2011 2012 2013 2014

GDP Growth 2,1% 1,9% 1,5% 2,0% 2,1%

Inflation 10,0% 12,0% 12,0% 9,0% 11,0%

Population 78,1 79,4 80,7 82,1 83,4

Population

Growth 1,7% 1,7% 1,7% 1,7% 1,6%

Inorganic Growth Opportunities (cont)

Source: Euromonitor, World Bank

Tons 2010 2011 2012 2013 2014

Chocolate

26.000

26.979 28.671

29.888

31.779

Biscuit

192.400

204.500 217.700

231.800

246.700

Cake

50.100

52.800 56.000

59.600

63.700

Value (US$ mn) 2010 2011 2012 2013 2014

Chocolate

266,8

289,1

324,3

327,4

362,7

Biscuit

804,9

865,4

956,8

961,1

1.022,1

Cake

286,8

317,8

346,5

343,3

374,9

Hi Food

(EGP x000) 2013 2014 2015E

Sales Volume

(Tons)

21,943

21,948 26,020

Net Sales

289,332 304,630 390,372

EBITDA 44,883 40,728 44,643

EBITDA

Margin 15,4% 13,4% 11.4%

Net Debt 42,053 81,548 73,911

15

Established in 1997

100% Yıldız Holding

Biscuit, chocolate and cake production

Capacity: 47.000 tons

Covering 14,000 sales points with 62

trucks

Kazakhstan: A Bridge From East To West

Kazakhstan Key Facts;

• Population of 17,3 mn on a 2,724,900 sq km land in 2014

• Average population growth of 1.4% in the last 5 years

• One of the largest economy in CIS with a GDP of US$ 216 bn

• Located right in the heart of Eurasia

• A gateway to Russia, China, India

• c.US$ 1,3 bn confectionery market

• Traditional channel is still dominant with c 84%

2010 2011 2012 2013 2014

GDP Growth 28,4% 27,0% 8,2% 13,9% -8,5%

Inflation 7,0% 8,0% 5,0% 6,0% 7,0%

Population 16,3 16,6 16,8 17,0 17,3

Population

Growth 1,4% 1,4% 1,4% 1,5% 1,5%

Inorganic Growth Opportunities (cont)

Source: Euromonitor, World Bank

Tons 2010 2011 2012 2013 2014

Chocolate

83,8

85,5 87,7

90,8

91,4

Biscuit

45,7

46,4 46,9

47,8

48,9

Cake

13,0

13,3 13,5

13,8

14,1

Value (US$ mn) 2010 2011 2012 2013 2014

Chocolate

755

816

878

978

1.000

Biscuit

175

186

200

214

197

Cake

78

84

90

97

89

Hamle

(KZT in bn) 2013 2014 2015E

Sales Volume

(Tons)

12,540

11,036 9,913

Net Sales

5,593 5,826 5,394

EBITDA 136.4 15.7 -149.3

EBITDA Margin 2,4% 0,3% -

Net Debt 3,816 3,515 6,183

16

• Leading premium chocolate producer with significant

brand equity worldwide

• Entry into China, S.Korea, Indonesia, S. Arabia and

Turkey since the acquisition

• Yet to reach its potential in terms of growth and margins

by

• restructuring the company,

• investing in store expansion, especially in the Far

East,

• closing down inefficient stores,

• reshuffling the product portfolio,

• Godiva plans to open 50 new stores per annum and

reach US$ 1bn in revenues and US$ 120mn EBITDA in

2017

Godiva – A Valuable Financial Asset

Key

figures

2008 2013 2014

# of stores 432 439 444

Revenues US$

470mn

US$

680mn

US$

732mn

EBITDA - US$ 42mn US$ 48mn

• Owns and operates 444 retail boutiques, with

presence in over 100 countries as of 2014 year-end

• Available via over 10,000 specialty retailers

Geographical presence of Godiva as of 2014 year end

209 stores in

the US

&Canada

16 stores in

Europe

345 stores

in Asia

Godiva store in Harrods, London

Godiva store in Denver, the US

Year U.S. Japan China Pac Rim Belgium Others

2008 262 99 - 32 8 21

2013 195 128 46 35 5 30

2014 191 136 47 36 5 29

Geographical store evolution

Acquired by

Yıldız Holding in

2008

Ülker stake in

Godiva - 19%

17

1. Ülker: Ulker In Brief

2. Organic Growth Drivers

3. Inorganic Growth Opportunities & Godiva

4. Operational Performance

5. Financials

6. Appendix

3

8

13

18

24

29

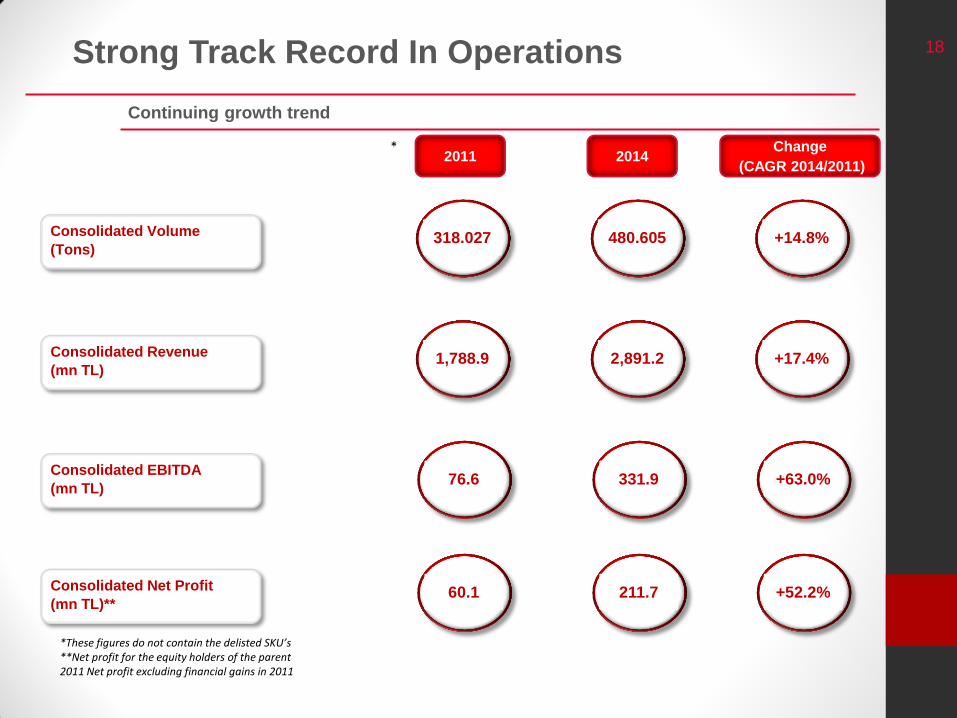

18 Strong Track Record In Operations

Continuing growth trend

Consolidated Volume

(Tons)

Consolidated Revenue

(mn TL)

Consolidated EBITDA

(mn TL)

Consolidated Net Profit

(mn TL)**

318.027 480.605 +14.8%

1,788.9 2,891.2 +17.4%

76.6 331.9 +63.0%

60.1 211.7 +52.2%

*These figures do not contain the delisted SKU’s **Net profit for the equity holders of the parent 2011 Net profit excluding financial gains in 2011

2011 2014 Change

(CAGR 2014/2011)

*

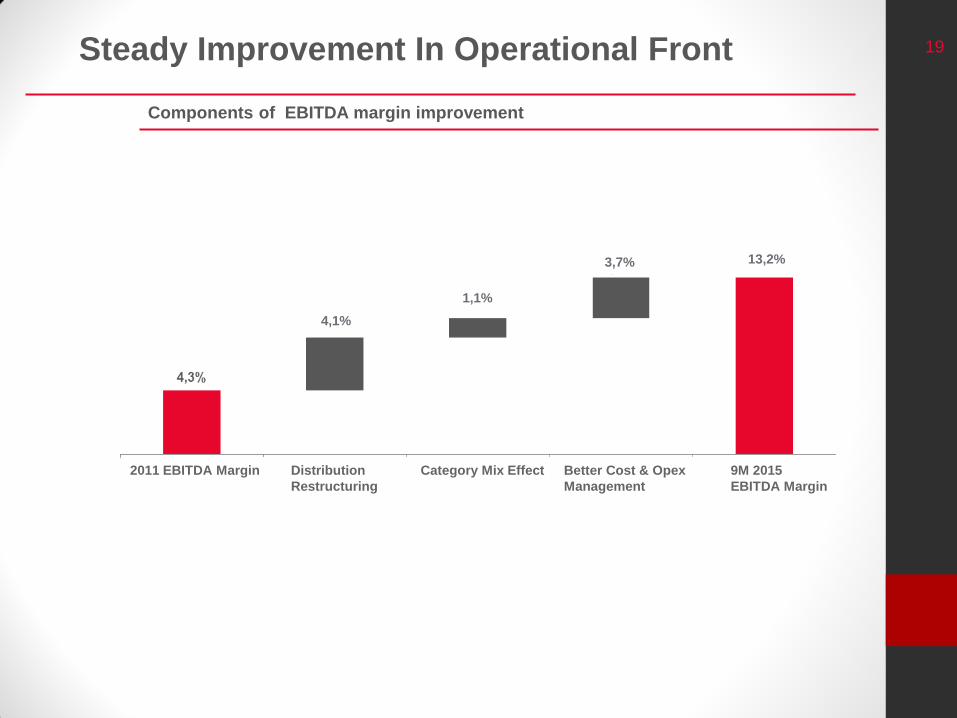

19 Steady Improvement In Operational Front

Components of EBITDA margin improvement

4,1%

1,1%

3,7% 13,2%

9M 2015

EBITDA Margin

Better Cost & Opex

Management

Category Mix Effect Distribution

Restructuring

2011 EBITDA Margin

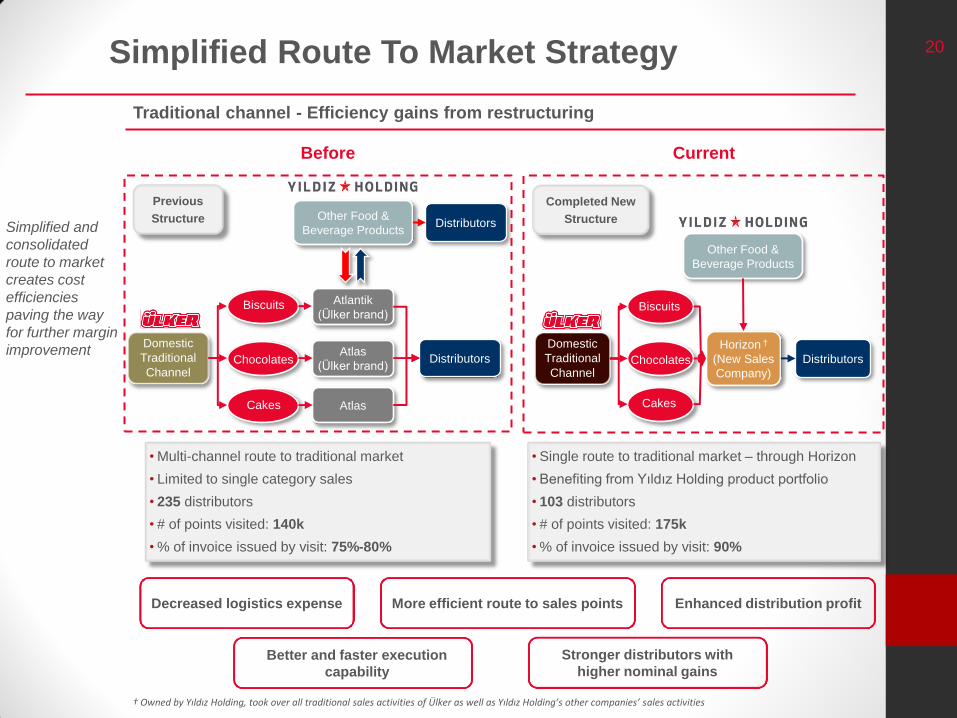

20 Simplified Route To Market Strategy

Simplified and

consolidated

route to market

creates cost

efficiencies

paving the way

for further margin

improvement

• Multi-channel route to traditional market

• Limited to single category sales

• 235 distributors

• # of points visited: 140k

• % of invoice issued by visit: 75%-80%

• Single route to traditional market – through Horizon

• Benefiting from Yıldız Holding product portfolio

• 103 distributors

• # of points visited: 175k

• % of invoice issued by visit: 90%

Other Food &

Beverage Products

Domestic

Traditional

Channel

Biscuits

Chocolates

Cakes

Horizon †

(New Sales

Company)

Distributors

Completed New

Structure

Before Current

Other Food &

Beverage Products Distributors

Domestic

Traditional

Channel

Biscuits

Chocolates

Cakes

Atlas

(Ülker brand) Distributors

Atlantik

(Ülker brand)

Atlas

Previous

Structure

† Owned by Yıldız Holding, took over all traditional sales activities of Ülker as well as Yıldız Holding’s other companies’ sales activities

Traditional channel - Efficiency gains from restructuring

Decreased logistics expense More efficient route to sales points Enhanced distribution profit

Stronger distributors with

higher nominal gains

Better and faster execution

capability

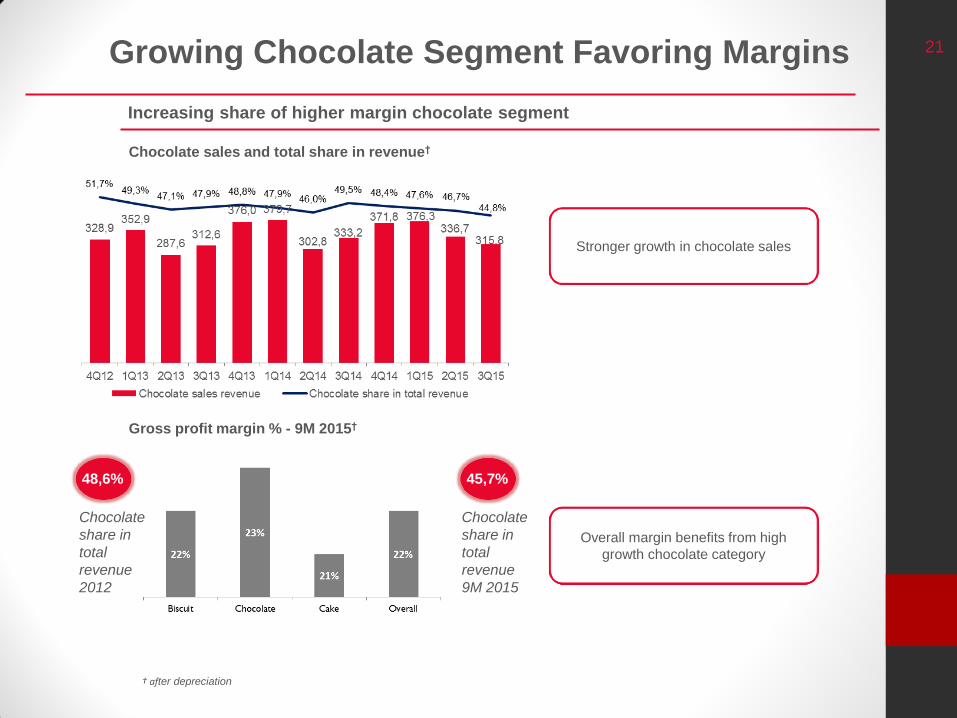

21 Growing Chocolate Segment Favoring Margins

Gross profit margin % - 9M 2015†

48,6% 45,7%

Chocolate

share in

total

revenue

2012

Chocolate

share in

total

revenue

9M 2015

Increasing share of higher margin chocolate segment

† after depreciation

Overall margin benefits from high

growth chocolate category

Chocolate sales and total share in revenue†

Stronger growth in chocolate sales

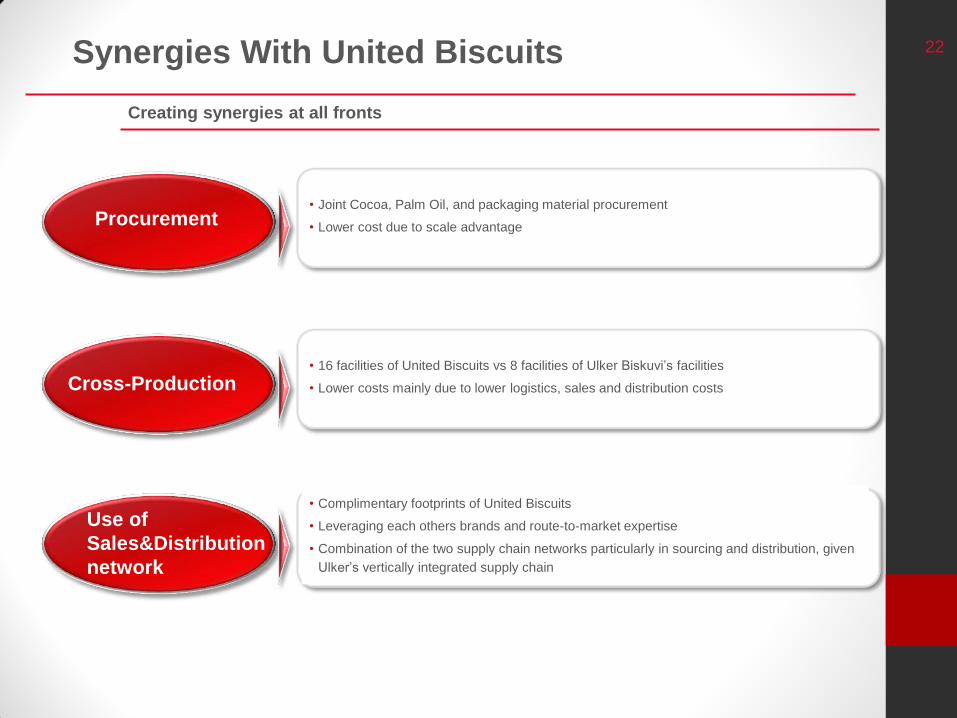

22 Synergies With United Biscuits

Creating synergies at all fronts

• Joint Cocoa, Palm Oil, and packaging material procurement

• Lower cost due to scale advantage Procurement

Cross-Production

Use of

Sales&Distribution

network

• 16 facilities of United Biscuits vs 8 facilities of Ulker Biskuvi’s facilities

• Lower costs mainly due to lower logistics, sales and distribution costs

• Complimentary footprints of United Biscuits

• Leveraging each others brands and route-to-market expertise

• Combination of the two supply chain networks particularly in sourcing and distribution, given

Ulker’s vertically integrated supply chain

23

1. Ülker: Ülker In Brief

2. Organic Growth Drivers

3. Inorganic Growth Opportunities & Godiva

4. Operational Performance

5. Financials

6. Appendix

3

8

13

18

24

29

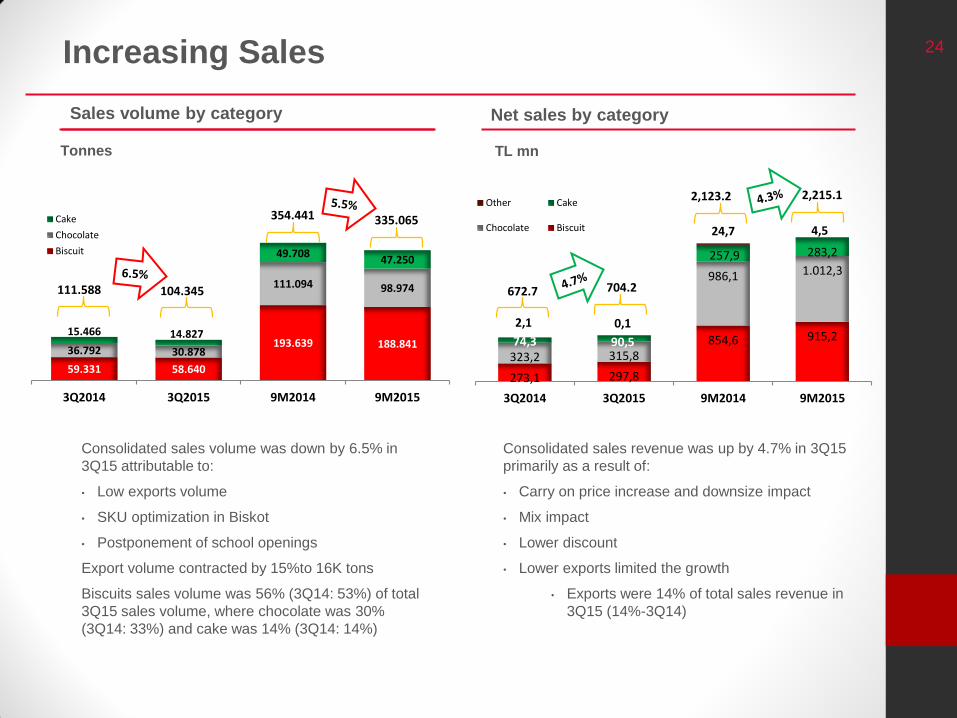

24

273,1 297,8

854,6 915,2

323,2 315,8

986,1 1.012,3

74,3 90,5

257,9 283,2

2,1 0,1

24,7 4,5

3Q2014 3Q2015 9M2014 9M2015

Other Cake

Chocolate Biscuit

Consolidated sales revenue was up by 4.7% in 3Q15

primarily as a result of:

• Carry on price increase and downsize impact

• Mix impact

• Lower discount

• Lower exports limited the growth

• Exports were 14% of total sales revenue in

3Q15 (14%-3Q14)

Increasing Sales

Sales volume by category Net sales by category

Consolidated sales volume was down by 6.5% in

3Q15 attributable to:

• Low exports volume

• SKU optimization in Biskot

• Postponement of school openings

Export volume contracted by 15%to 16K tons

Biscuits sales volume was 56% (3Q14: 53%) of total

3Q15 sales volume, where chocolate was 30%

(3Q14: 33%) and cake was 14% (3Q14: 14%)

Tonnes TL mn

59.331 58.640

193.639 188.841 36.792 30.878

111.094 98.974

15.466 14.827

49.708 47.250

3Q2014 3Q2015 9M2014 9M2015

Cake

Chocolate

Biscuit

111.588

354.441

104.345

335.065

672.7

2,123.2

704.2

2,215.1

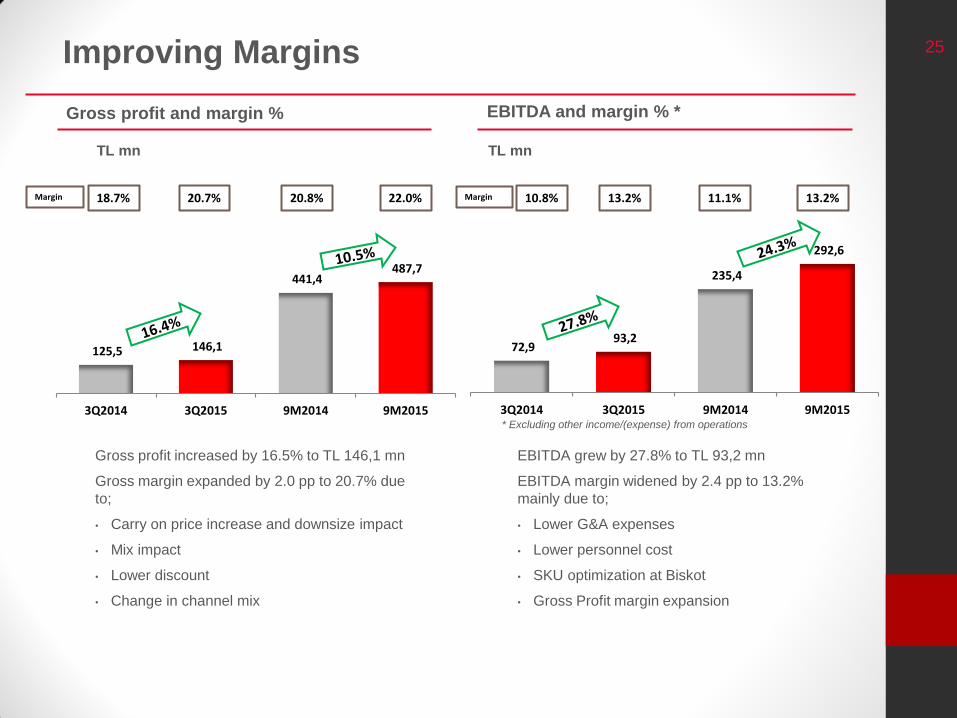

25

72,9 93,2

235,4

292,6

3Q2014 3Q2015 9M2014 9M2015

Improving Margins

Gross profit and margin % EBITDA and margin % *

TL mn TL mn

Gross profit increased by 16.5% to TL 146,1 mn

Gross margin expanded by 2.0 pp to 20.7% due

to;

• Carry on price increase and downsize impact

• Mix impact

• Lower discount

• Change in channel mix

* Excluding other income/(expense) from operations

EBITDA grew by 27.8% to TL 93,2 mn

EBITDA margin widened by 2.4 pp to 13.2%

mainly due to;

• Lower G&A expenses

• Lower personnel cost

• SKU optimization at Biskot

• Gross Profit margin expansion

18.7% 20.8% Margin 10.8% 11.1% Margin 20.7% 22.0% 13.2% 13.2%

125,5 146,1

441,4 487,7

3Q2014 3Q2015 9M2014 9M2015

26 Working Capital & Net Debt

Average working capital days Net debt

• Net debt as of Sept. 30, 2015: TL 395 mn (US$ 130 mn)

• Net debt to EBITDA (LTM) is 1.0x

• Financial debt

- US$ denominated due to company strategy

- Maturity breakdown as of Sept. 30, 2015:

- Short term 7.3%

- Long term 92.7%

Cash & cash equivalents breakdown based on currency

- TL: 13,7 mn

- US$: 1.383,2 mn†

- Euro: - mn†

• Net working capital was TL 466 mn as of 9M15

and TL 305 mn at the end of 2014

• Working capital requirement over sales ratio was

21.0% in 9M2015 vs 23.0% in 9M2014

• FX short position of

TL 377 mn (US$ 124 mn)

† Amounts expressed in Turkish Lira “TL”

Average WC days

2011 2012 2013 2014 9M14 9M15

Trade receivables

87 84 76 72 77 71

Inventory 38 34 33 32 36 35

Trade payables 79 81 77 74 68 67

WC - days 46 37 32 30 45 39

Net debt - TL mn 2012 2013 2014 9M15

Financial debt 1.501 1.260 1.335 1.796

Short term financial debt 614 1.250 91 131

Long term financial debt 887 10 1.244 1.665

Non-trade receivables from related parties

131 3 0 4

Cash and cash equivalents 1.268 1.164 1.034 1.397

Net debt 102 92 301 395

55 102 96

301

395

2011 2012 2013 2014 9M15

Net Debt (TL mn)

27 Financials

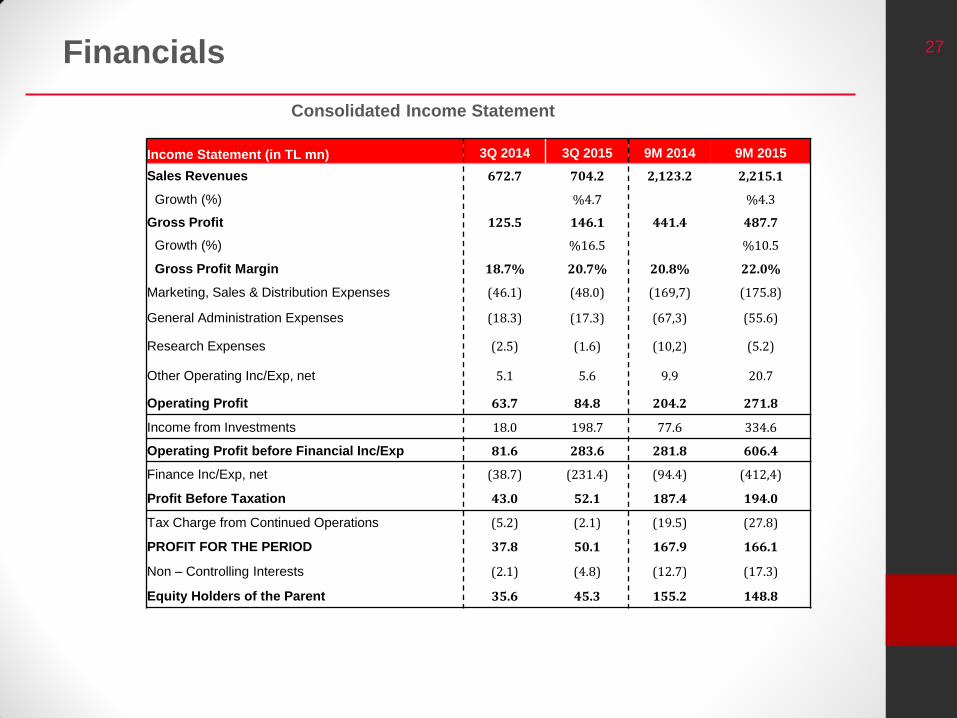

Consolidated Income Statement

Income Statement (in TL mn) 3Q 2014 3Q 2015 9M 2014 9M 2015

Sales Revenues 672.7 704.2 2,123.2 2,215.1

Growth (%) %4.7 %4.3

Gross Profit 125.5 146.1 441.4 487.7

Growth (%) %16.5 %10.5

Gross Profit Margin 18.7% 20.7% 20.8% 22.0%

Marketing, Sales & Distribution Expenses (46.1) (48.0) (169,7) (175.8)

General Administration Expenses (18.3) (17.3) (67,3) (55.6)

Research Expenses (2.5) (1.6) (10,2) (5.2)

Other Operating Inc/Exp, net 5.1 5.6 9.9 20.7

Operating Profit 63.7 84.8 204.2 271.8

Income from Investments 18.0 198.7 77.6 334.6

Operating Profit before Financial Inc/Exp 81.6 283.6 281.8 606.4

Finance Inc/Exp, net (38.7) (231.4) (94.4) (412,4)

Profit Before Taxation 43.0 52.1 187.4 194.0

Tax Charge from Continued Operations (5.2) (2.1) (19.5) (27.8)

PROFIT FOR THE PERIOD 37.8 50.1 167.9 166.1

Non – Controlling Interests (2.1) (4.8) (12.7) (17.3)

Equity Holders of the Parent 35.6 45.3 155.2 148.8

28

1. Ülker: Ülker In Brief

2. Organic Growth Drivers

3. Inorganic Growth Opportunities & Godiva

4. Operational Performance

5. Financials

6. Appendix

3

8

13

18

24

29

29

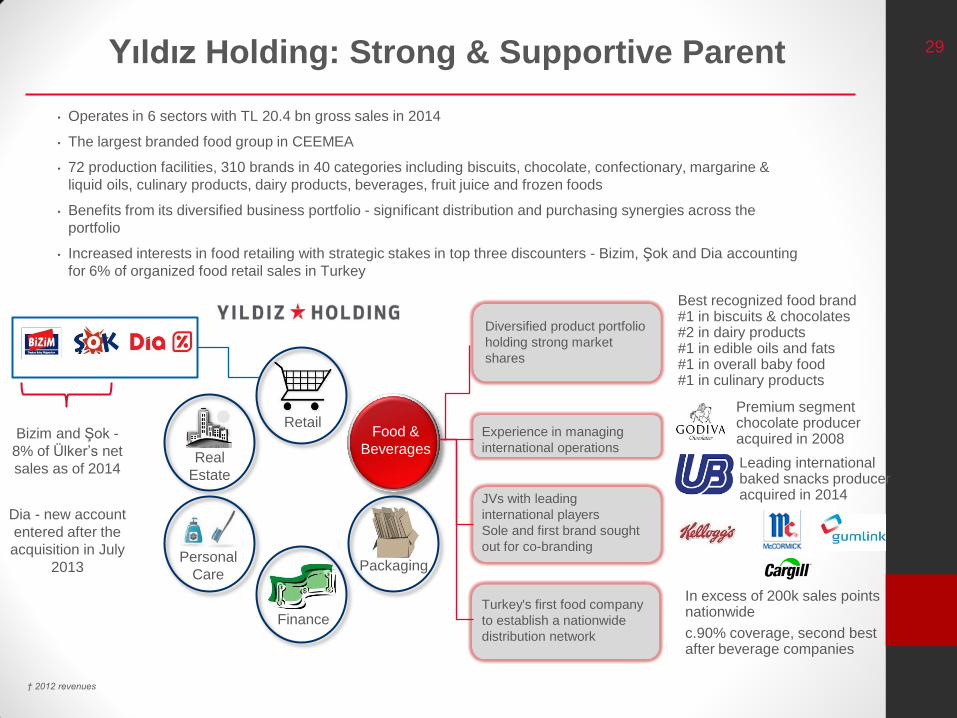

Experience in managing

international operations

• Operates in 6 sectors with TL 20.4 bn gross sales in 2014

• The largest branded food group in CEEMEA

• 72 production facilities, 310 brands in 40 categories including biscuits, chocolate, confectionary, margarine &

liquid oils, culinary products, dairy products, beverages, fruit juice and frozen foods

• Benefits from its diversified business portfolio - significant distribution and purchasing synergies across the

portfolio

• Increased interests in food retailing with strategic stakes in top three discounters - Bizim, Şok and Dia accounting

for 6% of organized food retail sales in Turkey

Yıldız Holding: Strong & Supportive Parent

Food &

Beverages

Packaging

Finance

Retail

Real

Estate

Personal

Care

Best recognized food brand #1 in biscuits & chocolates #2 in dairy products #1 in edible oils and fats #1 in overall baby food #1 in culinary products

Premium segment chocolate producer acquired in 2008

In excess of 200k sales points nationwide

c.90% coverage, second best after beverage companies

Diversified product portfolio

holding strong market

shares

JVs with leading

international players

Sole and first brand sought

out for co-branding

Turkey's first food company

to establish a nationwide

distribution network

Bizim and Şok -

8% of Ülker’s net

sales as of 2014

Dia - new account

entered after the

acquisition in July

2013

† 2012 revenues

Leading international baked snacks producer acquired in 2014

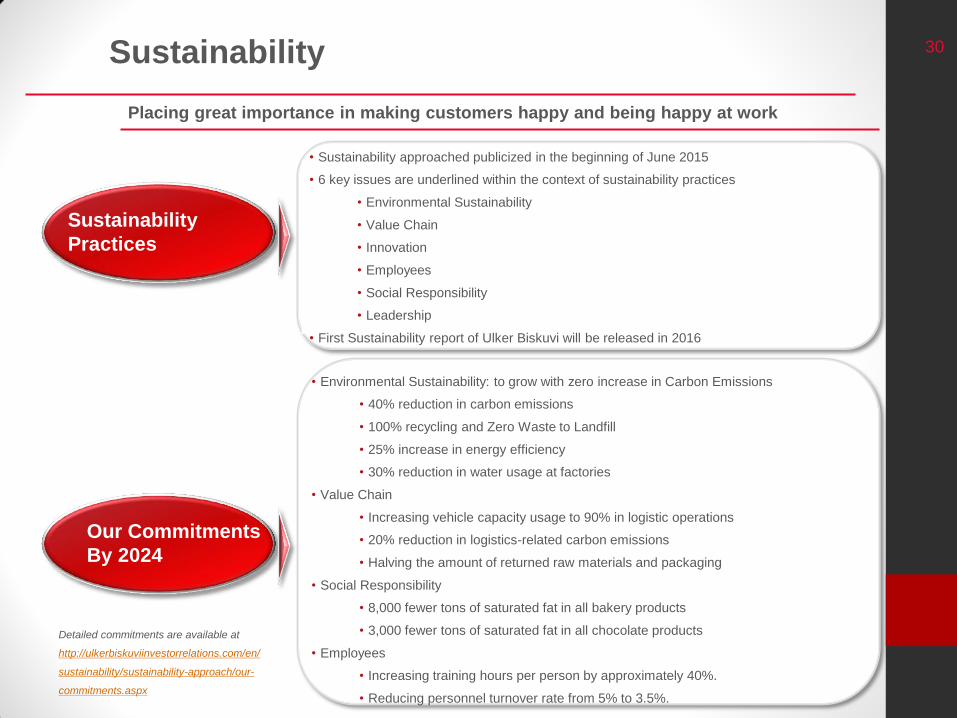

30 Sustainability

Placing great importance in making customers happy and being happy at work

Sustainability

Practices

Our Commitments

By 2024

• Sustainability approached publicized in the beginning of June 2015

• 6 key issues are underlined within the context of sustainability practices

• Environmental Sustainability

• Value Chain

• Innovation

• Employees

• Social Responsibility

• Leadership

• First Sustainability report of Ulker Biskuvi will be released in 2016

• Environmental Sustainability: to grow with zero increase in Carbon Emissions

• 40% reduction in carbon emissions

• 100% recycling and Zero Waste to Landfill

• 25% increase in energy efficiency

• 30% reduction in water usage at factories

• Value Chain

• Increasing vehicle capacity usage to 90% in logistic operations

• 20% reduction in logistics-related carbon emissions

• Halving the amount of returned raw materials and packaging

• Social Responsibility

• 8,000 fewer tons of saturated fat in all bakery products

• 3,000 fewer tons of saturated fat in all chocolate products

• Employees

• Increasing training hours per person by approximately 40%.

• Reducing personnel turnover rate from 5% to 3.5%.

Detailed commitments are available at

http://ulkerbiskuviinvestorrelations.com/en/

sustainability/sustainability-approach/our-

commitments.aspx

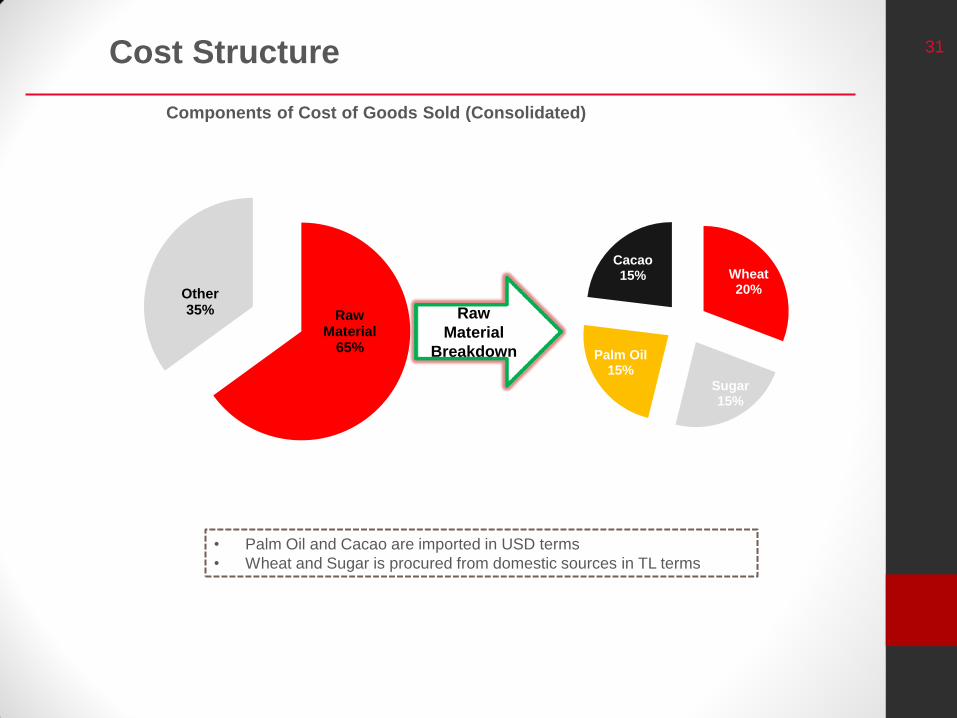

31 Cost Structure

Components of Cost of Goods Sold (Consolidated)

Raw Material

65%

Other 35% Raw

Material

Breakdown

Wheat 20%

Sugar 15%

Palm Oil 15%

Cacao 15%

• Palm Oil and Cacao are imported in USD terms

• Wheat and Sugar is procured from domestic sources in TL terms

32 Disclaimer

• This presentation contains information and analysis on financial statements and is prepared for the sole purpose

of providing information relating to Ülker Bisküvi Sanayi A.Ş. (“Ülker”)

• This presentation contains forward-looking statements which are based on certain expectations and

assumptions at the time of publication of this presentation and are subject to risks and uncertainties that could

cause actual results to differ materially from those expressed in these materials. Many of these risks and

uncertainties relate to factors that are beyond Ülker’s ability to control or estimate precisely, such as future

market and economic conditions, the behavior of other market participants, the ability to successfully integrate

acquired businesses and achieve anticipated cost savings and productivity gains as well as the actions of

government regulators

• Readers are cautioned not to place undue reliance on these forward-looking statements, which apply only as of

the date of this presentation. Ülker does not undertake any obligation to publicly release any revisions to these

forward-looking statements to reflect events or circumstances after the date of these materials

• This presentation merely serves the purpose of providing information. It neither represents an offer for sale nor

for subscription of securities in any country, including Turkey. This presentation does not include an official offer

of shares; an offering circular will not be published

• This presentation is not allowed to be reproduced, distributed or published without permission or agreement of

Ülker

• The figures in this presentation are rounded to provide a better overview. The calculation of deviations is based

on figures including fractions. Therefore rounding differences may occur

• Neither Ülker nor any of its managers or employees nor any other person shall have any liability whatsoever for

any loss arising from the use of this presentation

Related Documents