POWER SENERIO : BHUTAN AND NEPAL Presented By : Ashish Singh MBA – PM 500033217

Power Scenario of Bhutan and Nepal

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

POWER SENERIO : BHUTAN AND NEPAL

Presented By :

Ashish Singh

MBA – PM

500033217

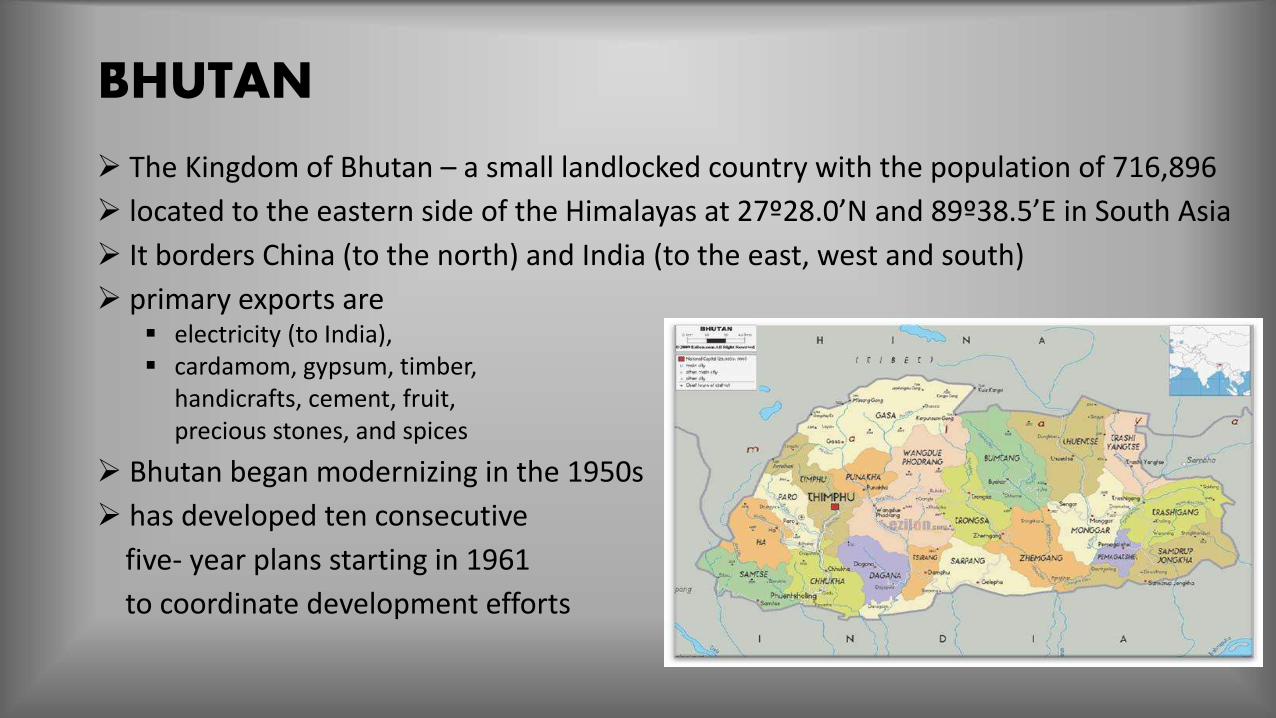

BHUTAN

BHUTAN

The Kingdom of Bhutan – a small landlocked country with the population of 716,896

located to the eastern side of the Himalayas at 27º28.0’N and 89º38.5’E in South Asia

It borders China (to the north) and India (to the east, west and south)

primary exports are electricity (to India), cardamom, gypsum, timber,

handicrafts, cement, fruit, precious stones, and spices

Bhutan began modernizing in the 1950s

has developed ten consecutive

five- year plans starting in 1961

to coordinate development efforts

Cont.

Previously, there were no paved roads, most homes were built from mud and grass, literacy was low

The country has made significant progress in extending access to safe drinking water and sanitation,

protecting and managing the country’s natural resources,

providing basic health care and

increasing access to primary education

The previous king, who came to the throne in 1974, invested the country’s meager finances in an airport, an east-west road, bridges, national education, health care, and select energy-producing technologies like hydropower, which provides almost all the country’s electricity

Bhutan’s economy is one of the world's smallest and least developed and is based on agriculture, forestry, and hydroelectricity

Cont.

Despite this constraint, hydroelectricity and construction continue to be the two major industries of growth for the country

Bhutan Government has undertaken a number of measures to ensure a diverse economy and prosperity for the rural dwellers in remote areas

One such measure is the Rural Electrification (RE) program which aims at achieving 100% rural electrification by end of 2013

In 2010 Bhutan was ranked by the Transparency International Corruption Perception as the least corrupt country in South Asia (The World Bank Group (WBG), 2010)

Cont.

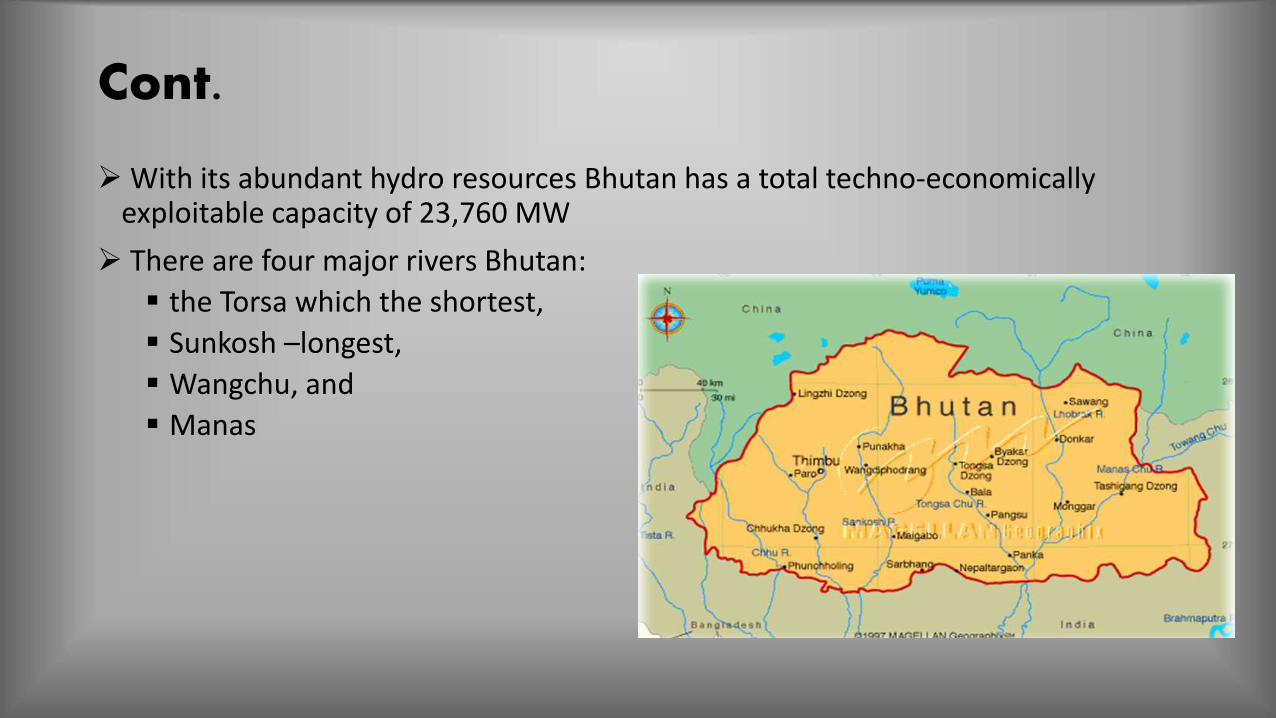

With its abundant hydro resources Bhutan has a total techno-economically exploitable capacity of 23,760 MW

There are four major rivers Bhutan:

the Torsa which the shortest,

Sunkosh –longest,

Wangchu, and

Manas

Brief of Bhutan Economy

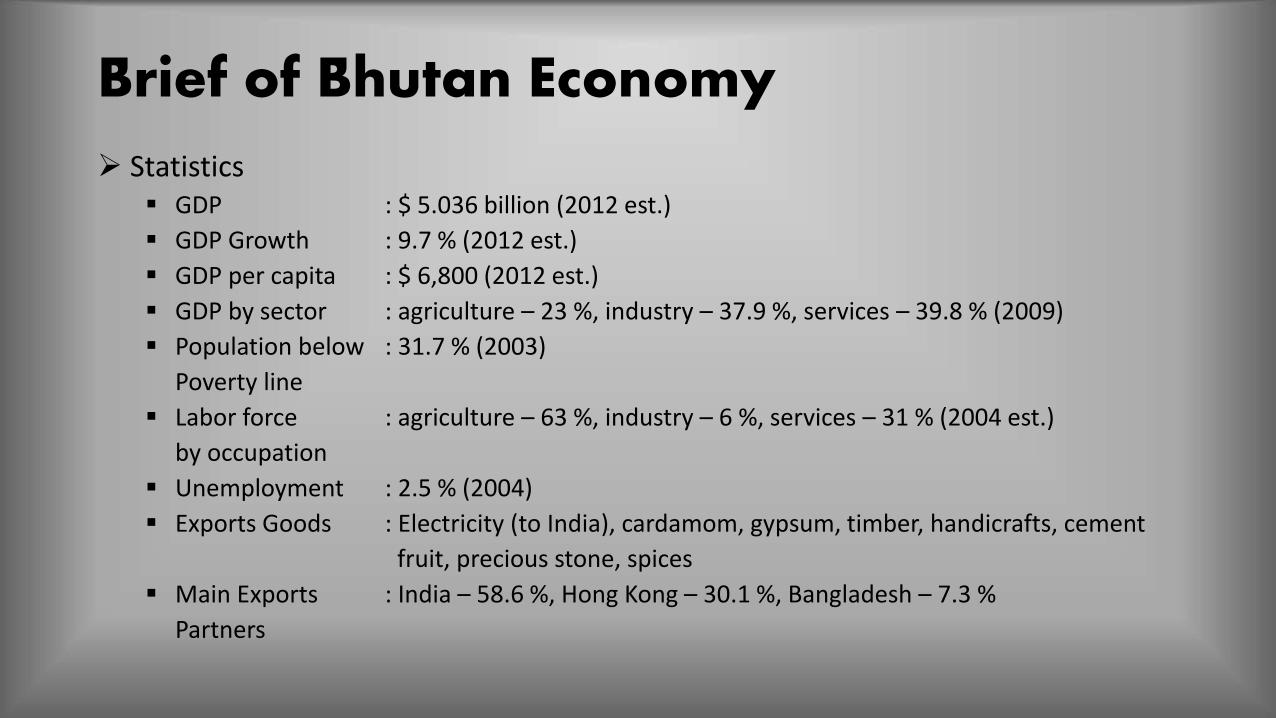

Statistics GDP : $ 5.036 billion (2012 est.)

GDP Growth : 9.7 % (2012 est.)

GDP per capita : $ 6,800 (2012 est.)

GDP by sector : agriculture – 23 %, industry – 37.9 %, services – 39.8 % (2009)

Population below : 31.7 % (2003)

Poverty line

Labor force : agriculture – 63 %, industry – 6 %, services – 31 % (2004 est.)

by occupation

Unemployment : 2.5 % (2004)

Exports Goods : Electricity (to India), cardamom, gypsum, timber, handicrafts, cement

fruit, precious stone, spices

Main Exports : India – 58.6 %, Hong Kong – 30.1 %, Bangladesh – 7.3 %

Partners

Objective And Scope

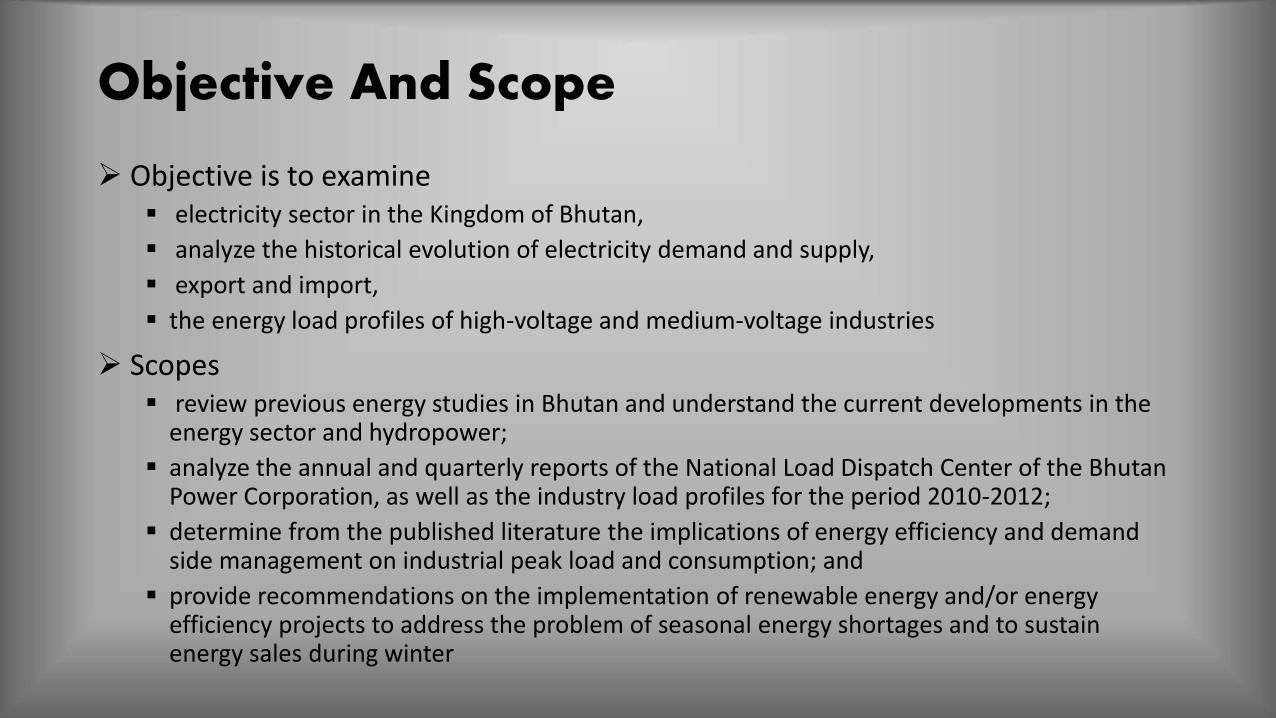

Objective is to examine electricity sector in the Kingdom of Bhutan,

analyze the historical evolution of electricity demand and supply,

export and import,

the energy load profiles of high-voltage and medium-voltage industries

Scopes review previous energy studies in Bhutan and understand the current developments in the

energy sector and hydropower;

analyze the annual and quarterly reports of the National Load Dispatch Center of the Bhutan Power Corporation, as well as the industry load profiles for the period 2010-2012;

determine from the published literature the implications of energy efficiency and demand side management on industrial peak load and consumption; and

provide recommendations on the implementation of renewable energy and/or energy efficiency projects to address the problem of seasonal energy shortages and to sustain energy sales during winter

Sector Development Context

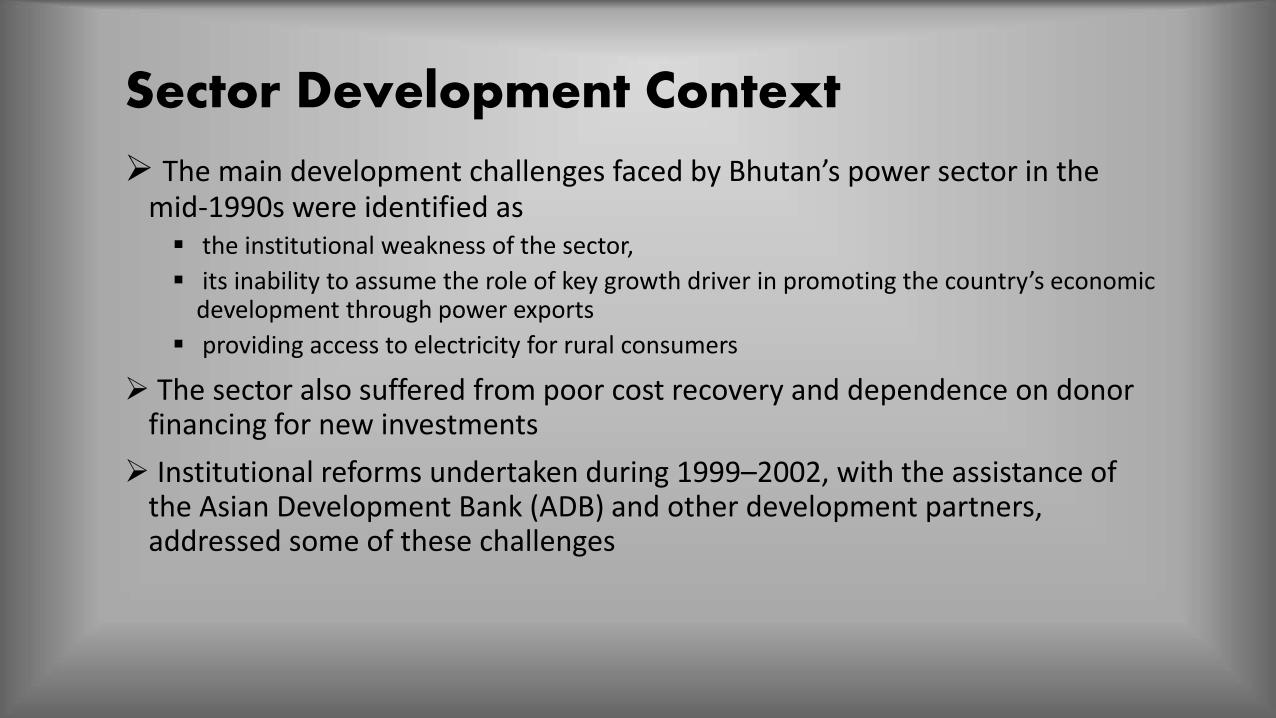

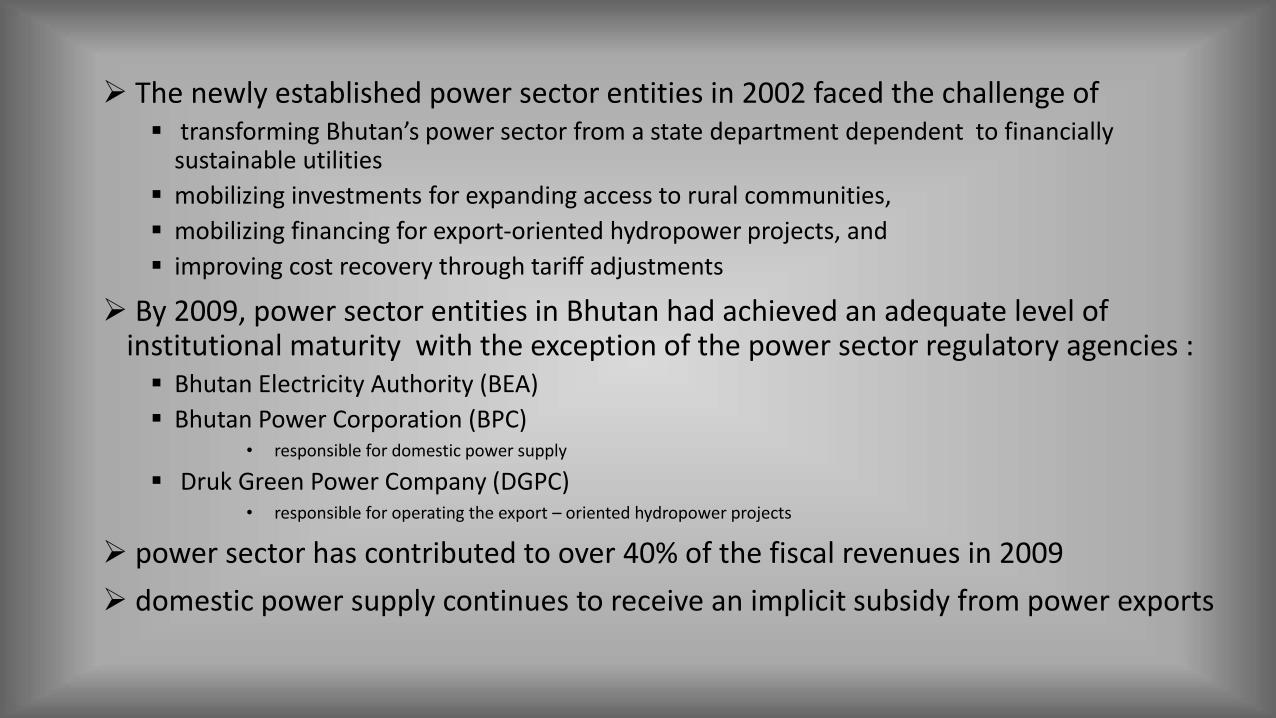

The main development challenges faced by Bhutan’s power sector in the mid-1990s were identified as the institutional weakness of the sector,

its inability to assume the role of key growth driver in promoting the country’s economic development through power exports

providing access to electricity for rural consumers

The sector also suffered from poor cost recovery and dependence on donor financing for new investments

Institutional reforms undertaken during 1999–2002, with the assistance of the Asian Development Bank (ADB) and other development partners, addressed some of these challenges

The newly established power sector entities in 2002 faced the challenge of transforming Bhutan’s power sector from a state department dependent to financially

sustainable utilities

mobilizing investments for expanding access to rural communities,

mobilizing financing for export-oriented hydropower projects, and

improving cost recovery through tariff adjustments

By 2009, power sector entities in Bhutan had achieved an adequate level of institutional maturity with the exception of the power sector regulatory agencies : Bhutan Electricity Authority (BEA)

Bhutan Power Corporation (BPC)• responsible for domestic power supply

Druk Green Power Company (DGPC)• responsible for operating the export – oriented hydropower projects

power sector has contributed to over 40% of the fiscal revenues in 2009

domestic power supply continues to receive an implicit subsidy from power exports

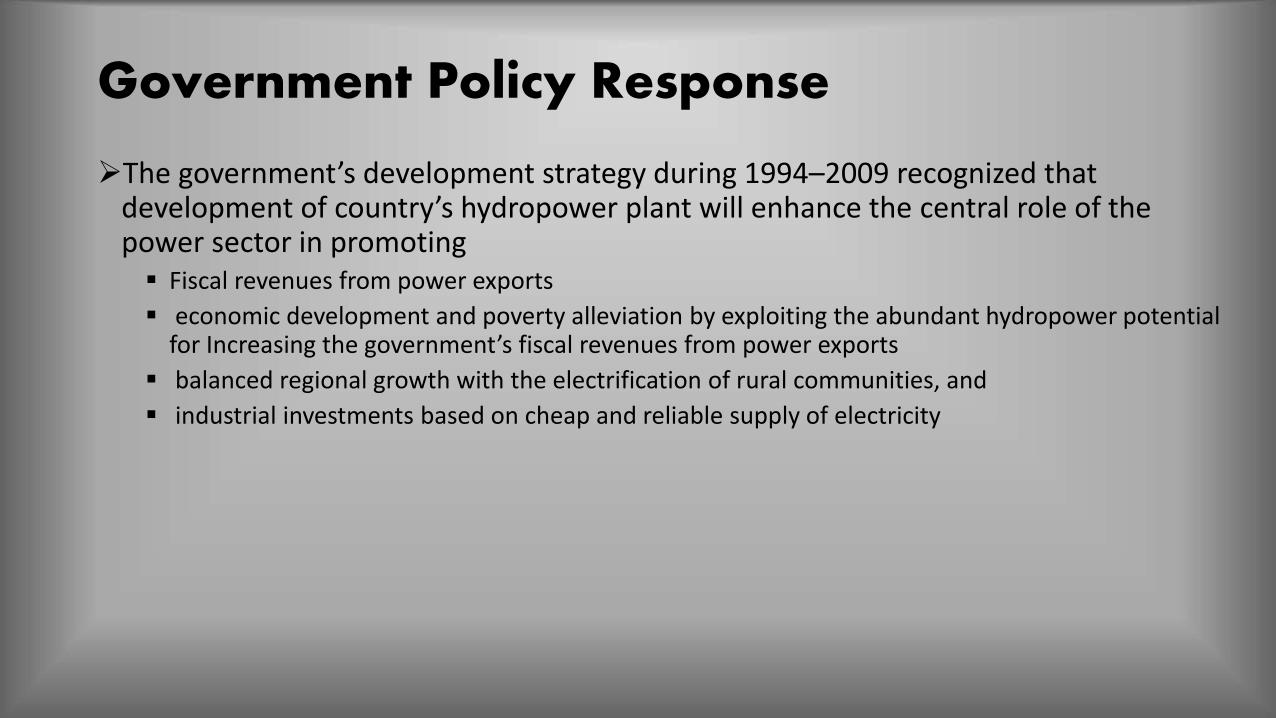

Government Policy Response

The government’s development strategy during 1994–2009 recognized that development of country’s hydropower plant will enhance the central role of the power sector in promoting Fiscal revenues from power exports

economic development and poverty alleviation by exploiting the abundant hydropower potential for Increasing the government’s fiscal revenues from power exports

balanced regional growth with the electrification of rural communities, and

industrial investments based on cheap and reliable supply of electricity

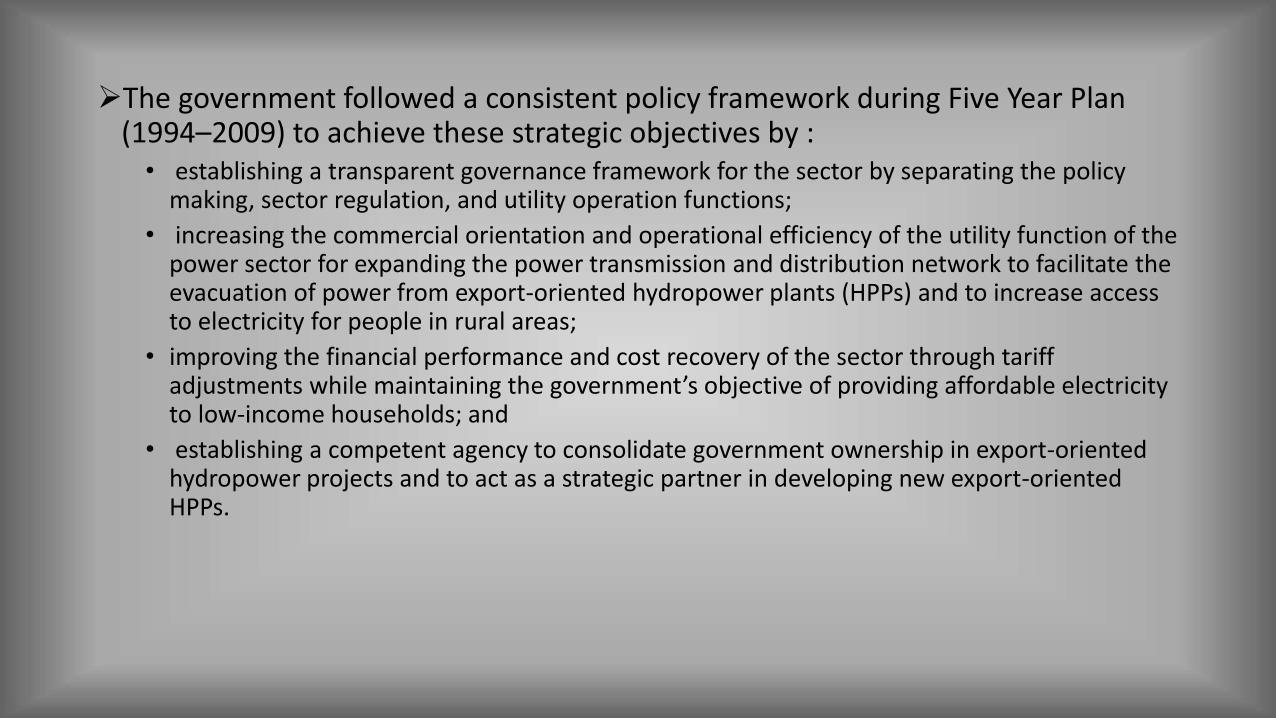

The government followed a consistent policy framework during Five Year Plan (1994–2009) to achieve these strategic objectives by :• establishing a transparent governance framework for the sector by separating the policy

making, sector regulation, and utility operation functions;

• increasing the commercial orientation and operational efficiency of the utility function of the power sector for expanding the power transmission and distribution network to facilitate the evacuation of power from export-oriented hydropower plants (HPPs) and to increase access to electricity for people in rural areas;

• improving the financial performance and cost recovery of the sector through tariff adjustments while maintaining the government’s objective of providing affordable electricity to low-income households; and

• establishing a competent agency to consolidate government ownership in export-oriented hydropower projects and to act as a strategic partner in developing new export-oriented HPPs.

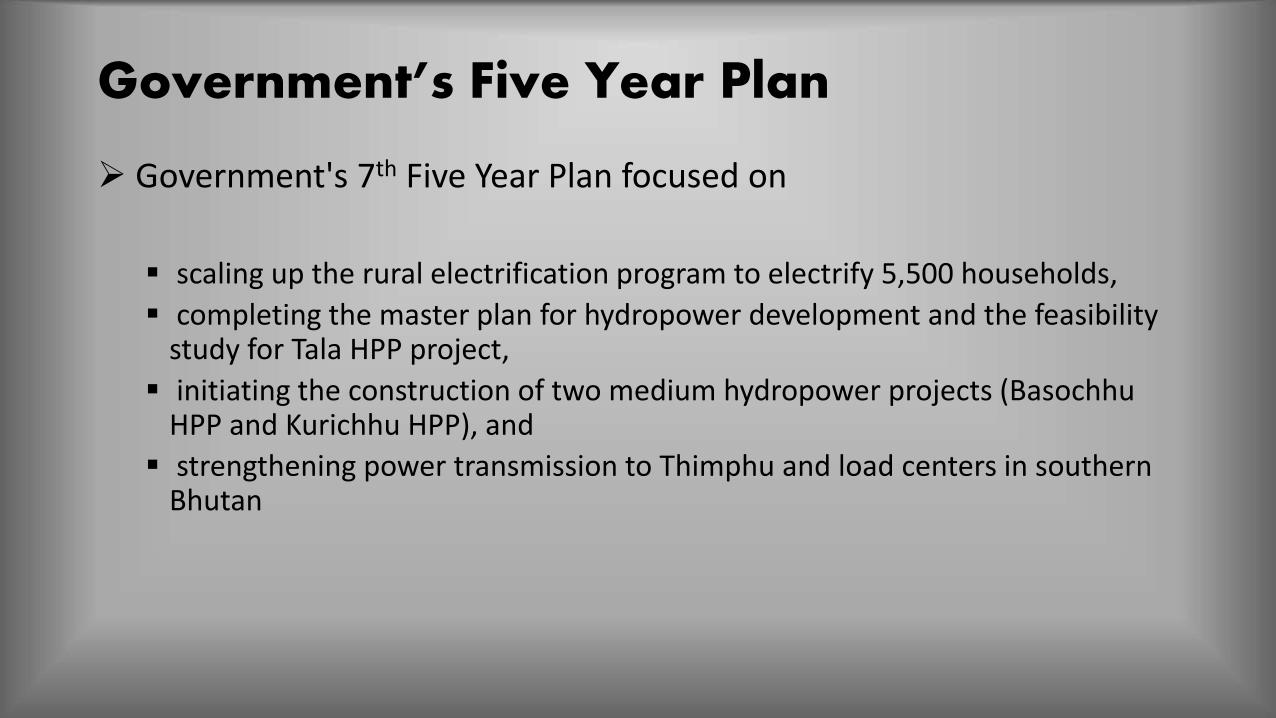

Government’s Five Year Plan

Government's 7th Five Year Plan focused on

scaling up the rural electrification program to electrify 5,500 households,

completing the master plan for hydropower development and the feasibility study for Tala HPP project,

initiating the construction of two medium hydropower projects (Basochhu HPP and Kurichhu HPP), and

strengthening power transmission to Thimphu and load centers in southern Bhutan

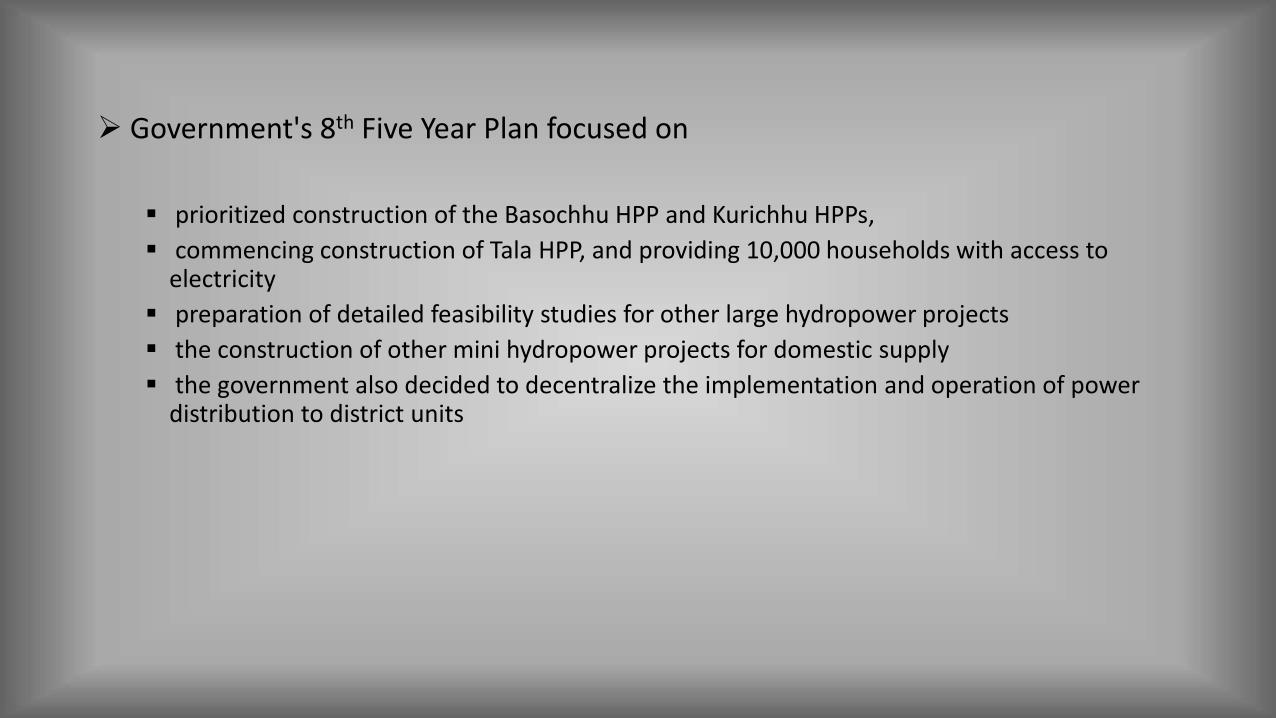

Government's 8th Five Year Plan focused on

prioritized construction of the Basochhu HPP and Kurichhu HPPs,

commencing construction of Tala HPP, and providing 10,000 households with access to electricity

preparation of detailed feasibility studies for other large hydropower projects

the construction of other mini hydropower projects for domestic supply

the government also decided to decentralize the implementation and operation of power distribution to district units

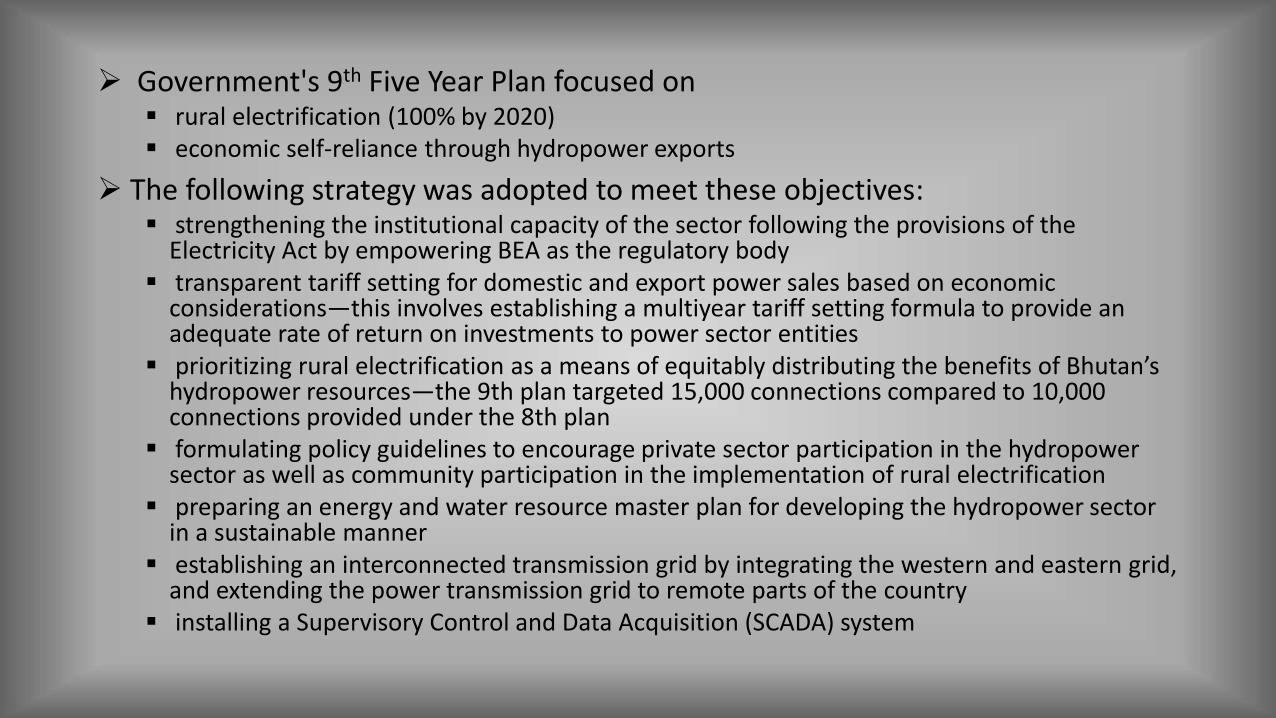

Government's 9th Five Year Plan focused on rural electrification (100% by 2020) economic self-reliance through hydropower exports

The following strategy was adopted to meet these objectives: strengthening the institutional capacity of the sector following the provisions of the

Electricity Act by empowering BEA as the regulatory body transparent tariff setting for domestic and export power sales based on economic

considerations—this involves establishing a multiyear tariff setting formula to provide an adequate rate of return on investments to power sector entities

prioritizing rural electrification as a means of equitably distributing the benefits of Bhutan’s hydropower resources—the 9th plan targeted 15,000 connections compared to 10,000 connections provided under the 8th plan

formulating policy guidelines to encourage private sector participation in the hydropower sector as well as community participation in the implementation of rural electrification

preparing an energy and water resource master plan for developing the hydropower sector in a sustainable manner

establishing an interconnected transmission grid by integrating the western and eastern grid, and extending the power transmission grid to remote parts of the country

installing a Supervisory Control and Data Acquisition (SCADA) system

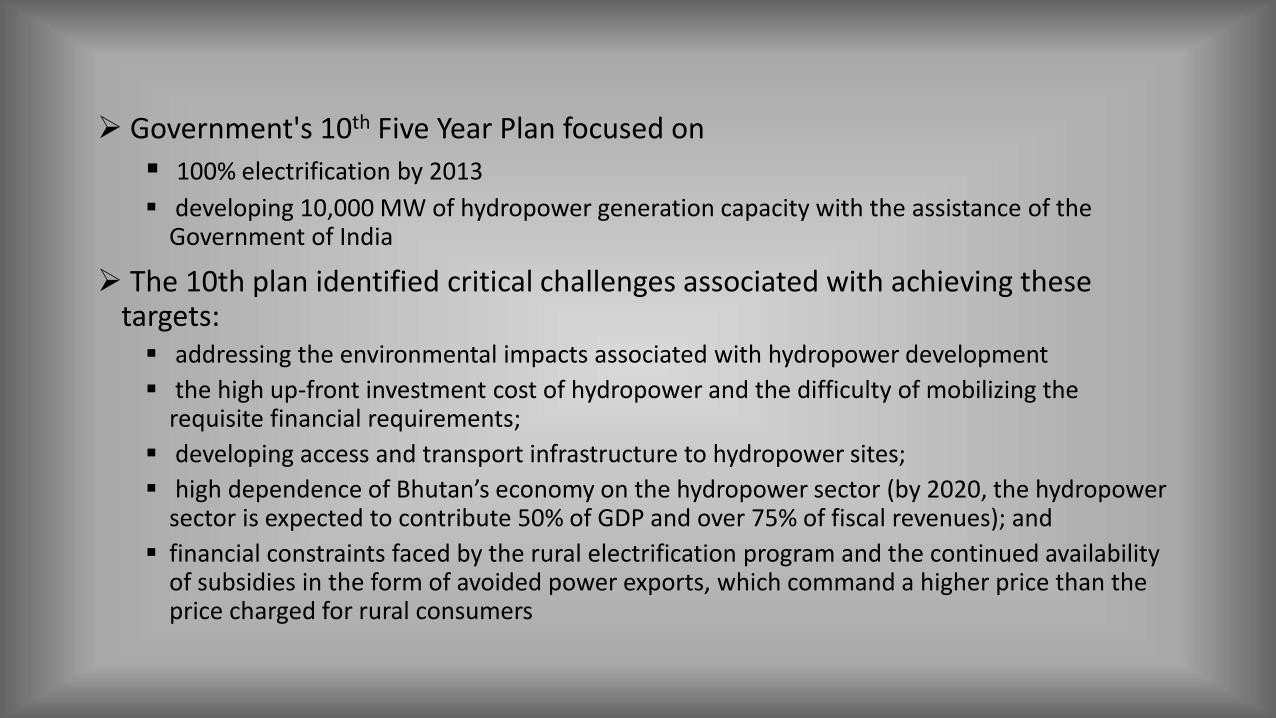

Government's 10th Five Year Plan focused on

100% electrification by 2013

developing 10,000 MW of hydropower generation capacity with the assistance of the Government of India

The 10th plan identified critical challenges associated with achieving these targets: addressing the environmental impacts associated with hydropower development

the high up-front investment cost of hydropower and the difficulty of mobilizing the requisite financial requirements;

developing access and transport infrastructure to hydropower sites;

high dependence of Bhutan’s economy on the hydropower sector (by 2020, the hydropower sector is expected to contribute 50% of GDP and over 75% of fiscal revenues); and

financial constraints faced by the rural electrification program and the continued availability of subsidies in the form of avoided power exports, which command a higher price than the price charged for rural consumers

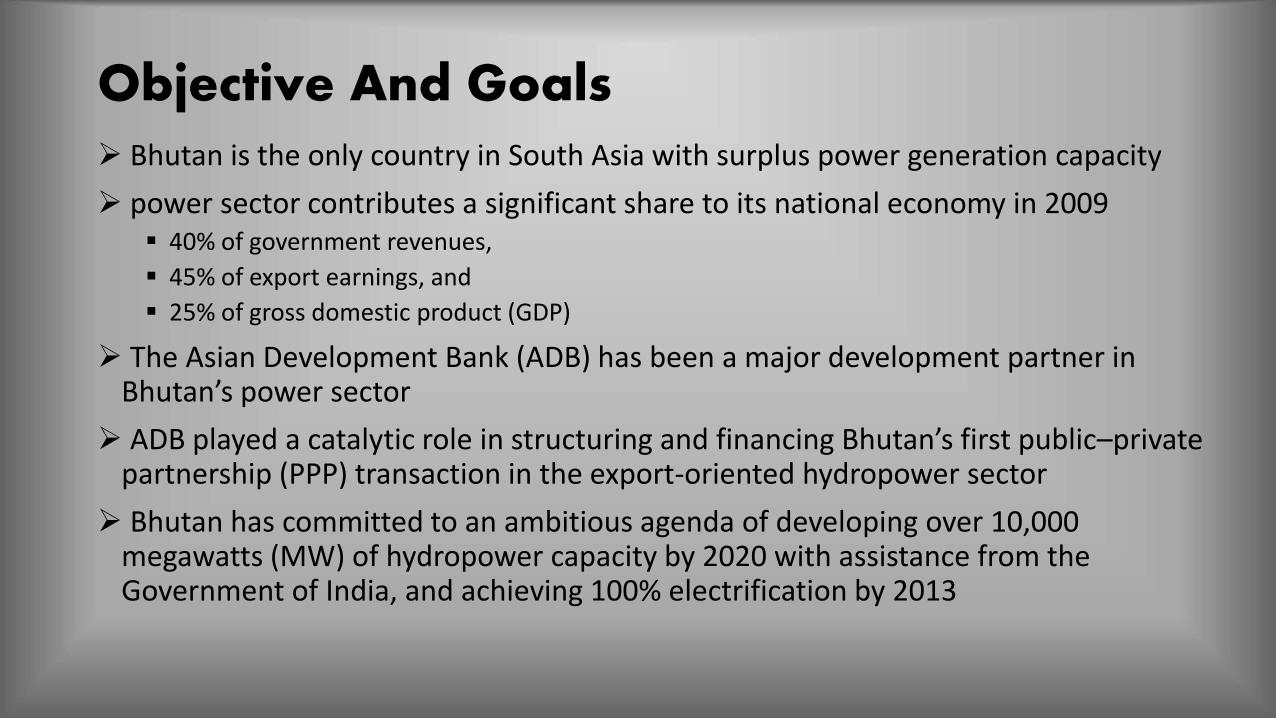

Objective And Goals Bhutan is the only country in South Asia with surplus power generation capacity

power sector contributes a significant share to its national economy in 2009 40% of government revenues,

45% of export earnings, and

25% of gross domestic product (GDP)

The Asian Development Bank (ADB) has been a major development partner in Bhutan’s power sector

ADB played a catalytic role in structuring and financing Bhutan’s first public–private partnership (PPP) transaction in the export-oriented hydropower sector

Bhutan has committed to an ambitious agenda of developing over 10,000 megawatts (MW) of hydropower capacity by 2020 with assistance from the Government of India, and achieving 100% electrification by 2013

Institutional Context

Electricity supply in Bhutan in the 1990s (including the operation of mini HPPs and diesel power plants) was the responsibility of the DOP, which was part of the Ministry of Trade and Investment

A major turning point in the overall development of the power sector was the commissioning of the 336 megawatt (MW) Chhukha Hydro Power Plant together with transmission links to connect the power station to both Bhutan’s domestic network and the Indian grid in 1988

The project was implemented as a joint venture between the Government of India and the Government of Bhutan, and then incorporated in July 1991 under the Companies Act, 1989 as Chhukha Hydro Power Company (CHPC), a government-owned company

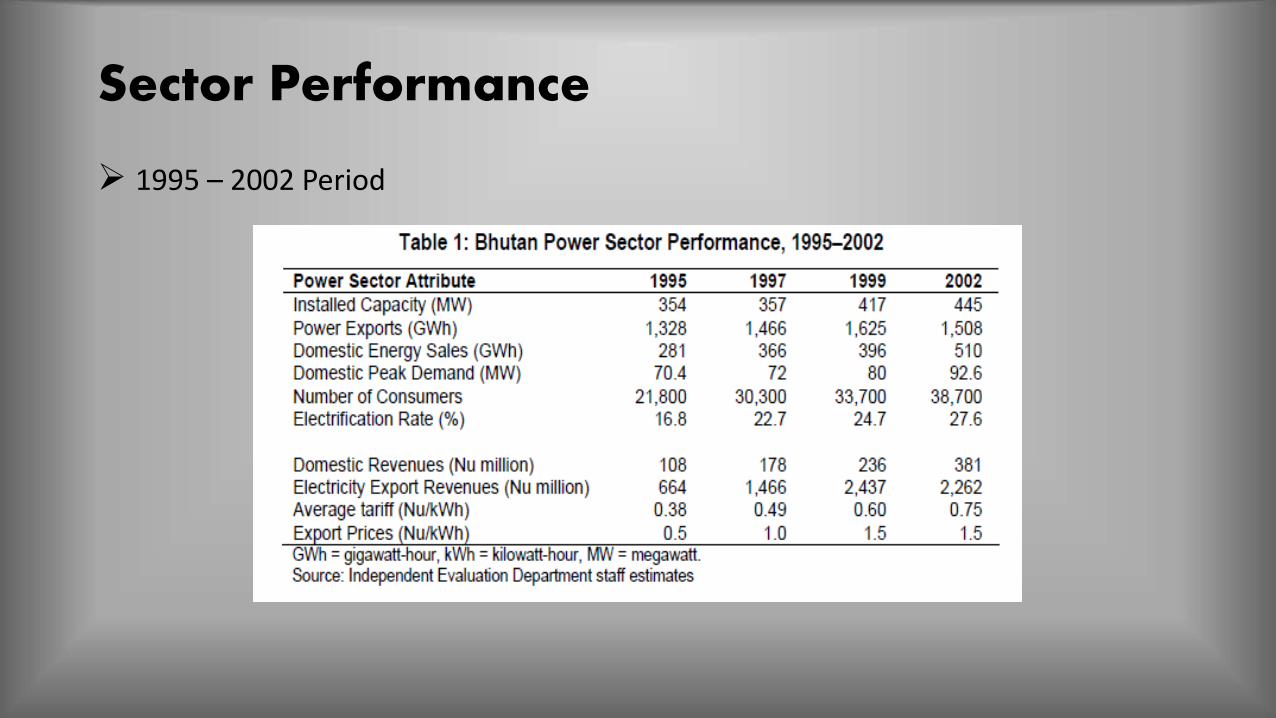

Sector Performance

1995 – 2002 Period

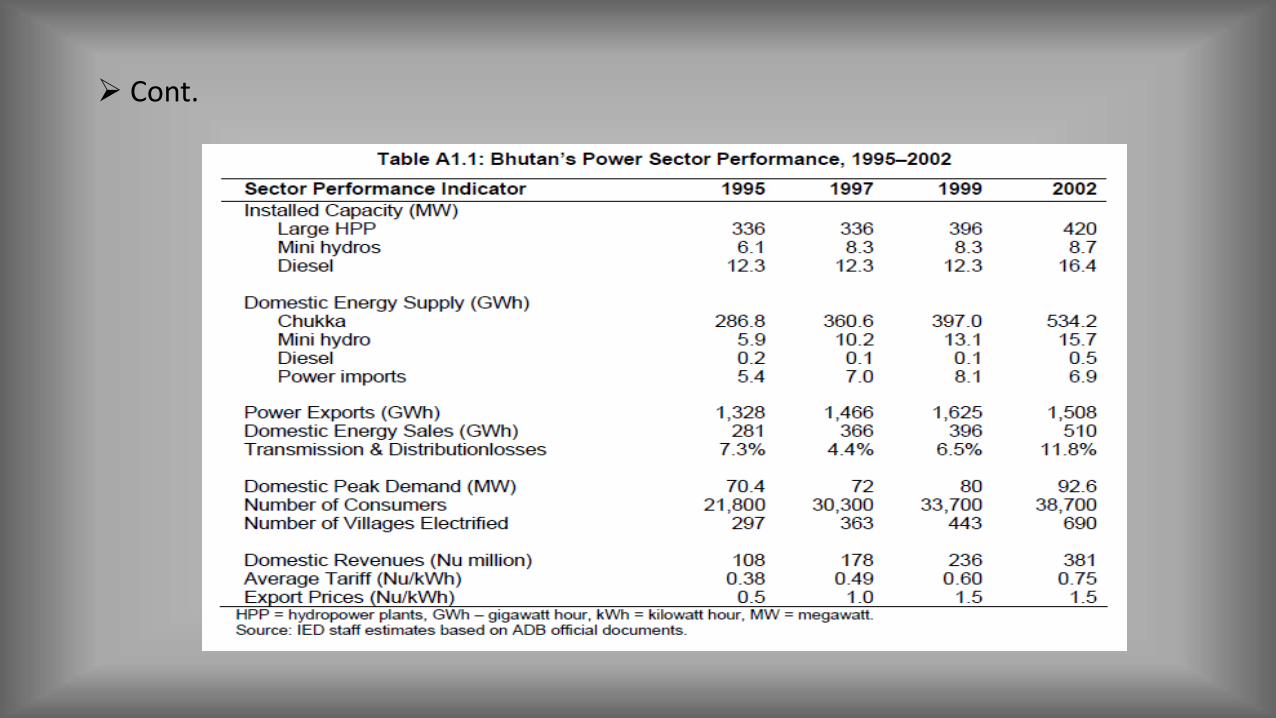

Cont.

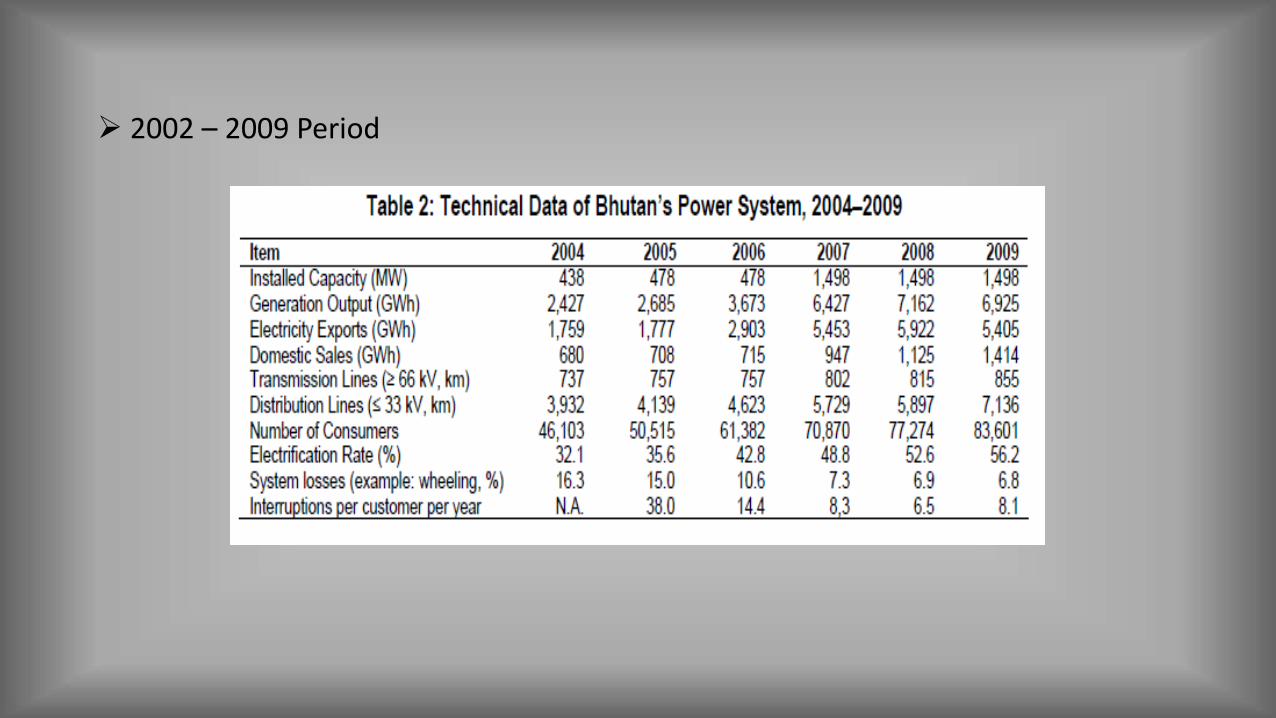

2002 – 2009 Period

Cont.

HYDROPOWER

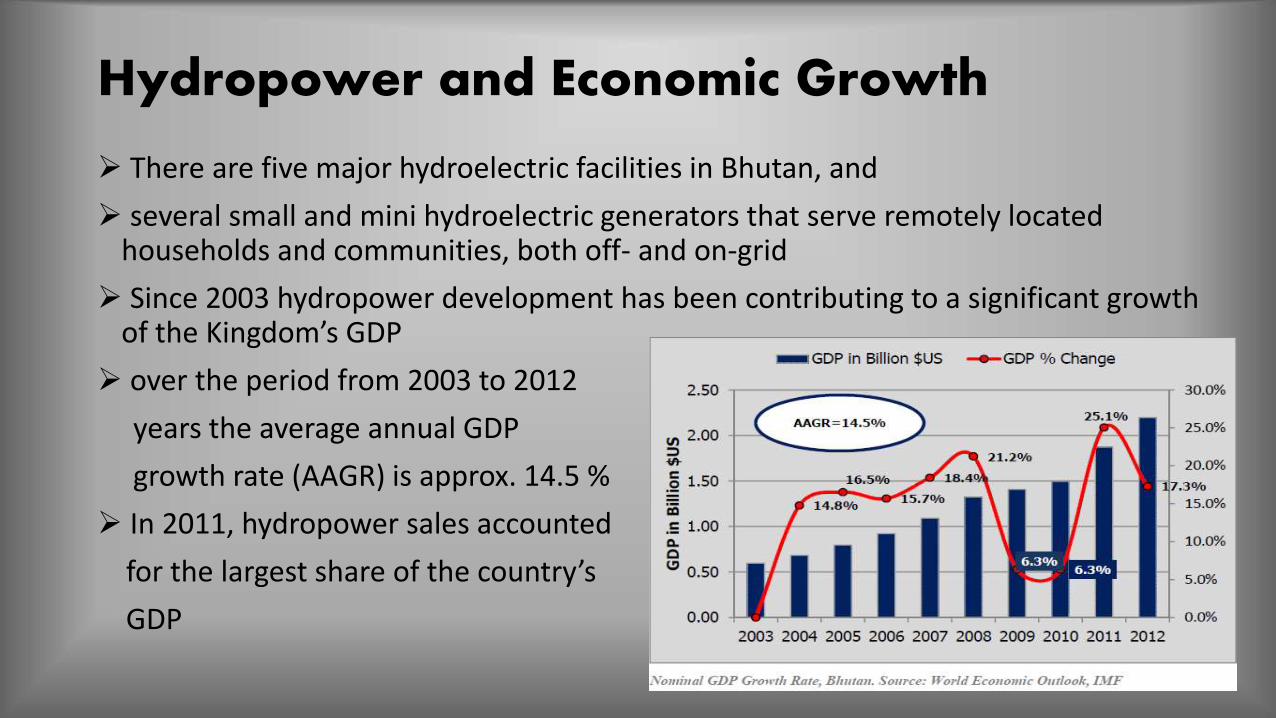

Hydropower and Economic Growth

There are five major hydroelectric facilities in Bhutan, and

several small and mini hydroelectric generators that serve remotely located households and communities, both off- and on-grid

Since 2003 hydropower development has been contributing to a significant growth of the Kingdom’s GDP

over the period from 2003 to 2012

years the average annual GDP

growth rate (AAGR) is approx. 14.5 %

In 2011, hydropower sales accounted

for the largest share of the country’s

GDP

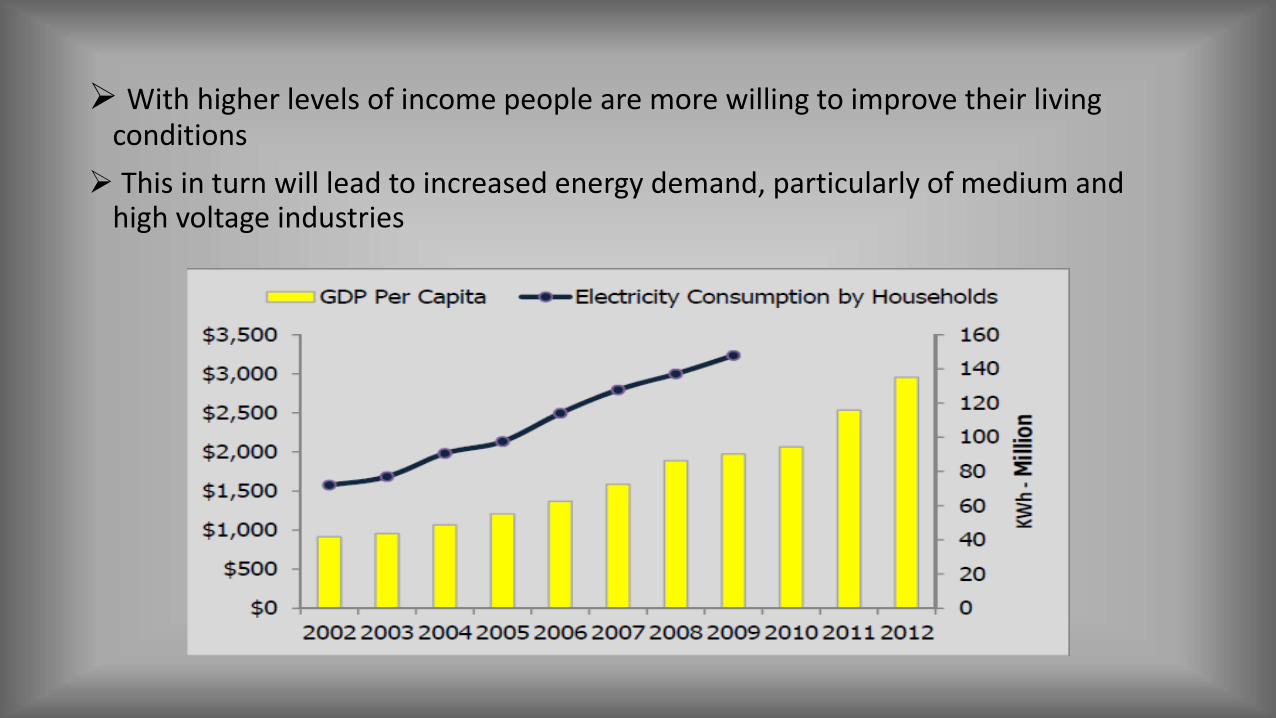

With higher levels of income people are more willing to improve their living conditions

This in turn will lead to increased energy demand, particularly of medium and high voltage industries

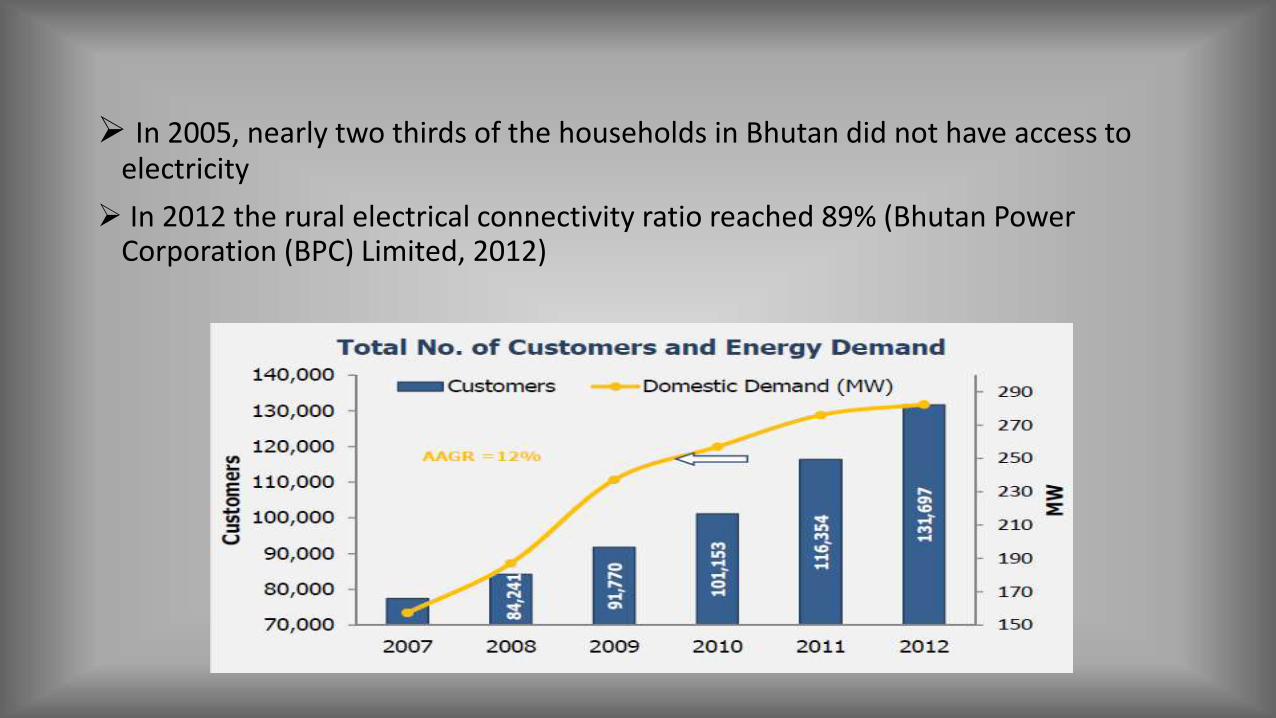

In 2005, nearly two thirds of the households in Bhutan did not have access to electricity

In 2012 the rural electrical connectivity ratio reached 89% (Bhutan Power Corporation (BPC) Limited, 2012)

Supply And Demand

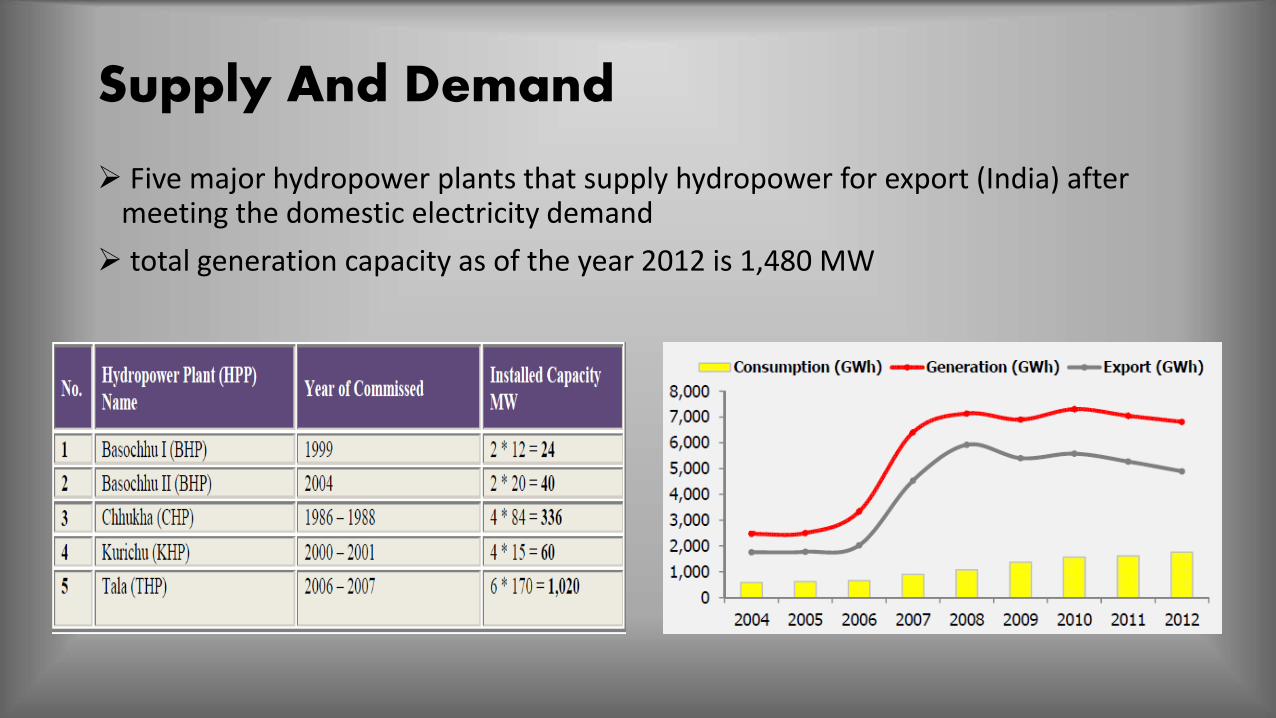

Five major hydropower plants that supply hydropower for export (India) after meeting the domestic electricity demand

total generation capacity as of the year 2012 is 1,480 MW

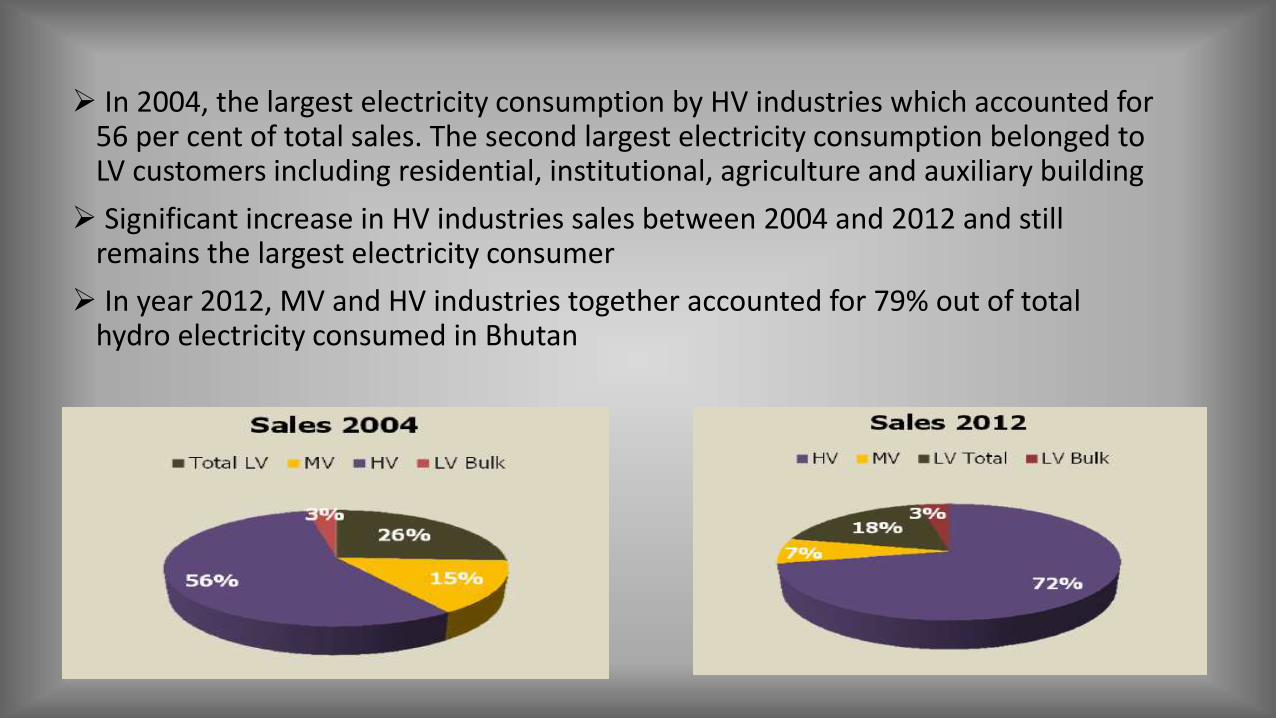

In 2004, the largest electricity consumption by HV industries which accounted for 56 per cent of total sales. The second largest electricity consumption belonged to LV customers including residential, institutional, agriculture and auxiliary building

Significant increase in HV industries sales between 2004 and 2012 and still remains the largest electricity consumer

In year 2012, MV and HV industries together accounted for 79% out of total hydro electricity consumed in Bhutan

Climate Change & Hydropower

Currently, hydropower accounts for nearly 16% of the world’s total power supply

World’s most dominant (86%) source of renewable electrical energy (2012)

Asia alone possesses a technically feasible potential of 6,800 TWh/y

Total capacity potential of 1,928,286 MW (2012)

A feasible potential for global hydropower is 2 to 3 times higher than the current generation

However, there is an uncertainty brought by global climate change which poses some risk for the hydropower generation sector

Climatic changes are causing changes in runoff and increasing retreat/melting of glaciers

The Himalayan region is in a very active seismic zone, thus it is possible that earthquakes may trigger outburst of glacial lakes

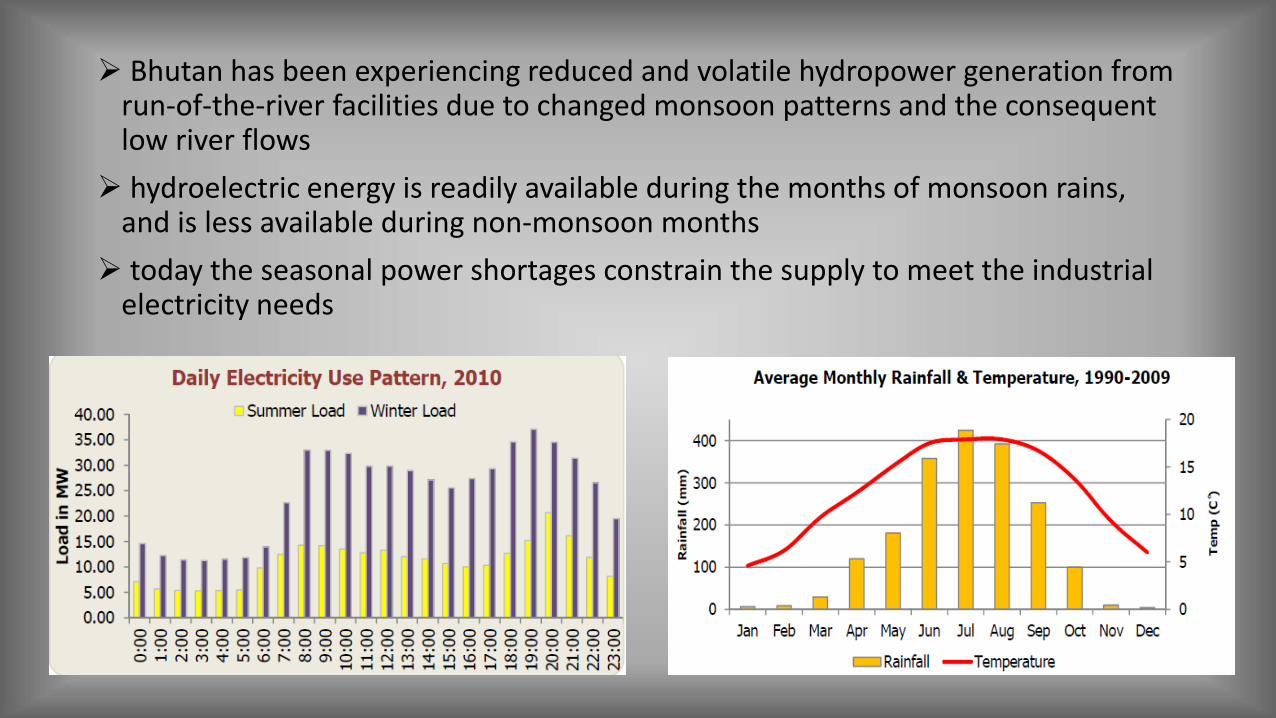

Bhutan has been experiencing reduced and volatile hydropower generation from run-of-the-river facilities due to changed monsoon patterns and the consequent low river flows

hydroelectric energy is readily available during the months of monsoon rains, and is less available during non-monsoon months

today the seasonal power shortages constrain the supply to meet the industrial electricity needs

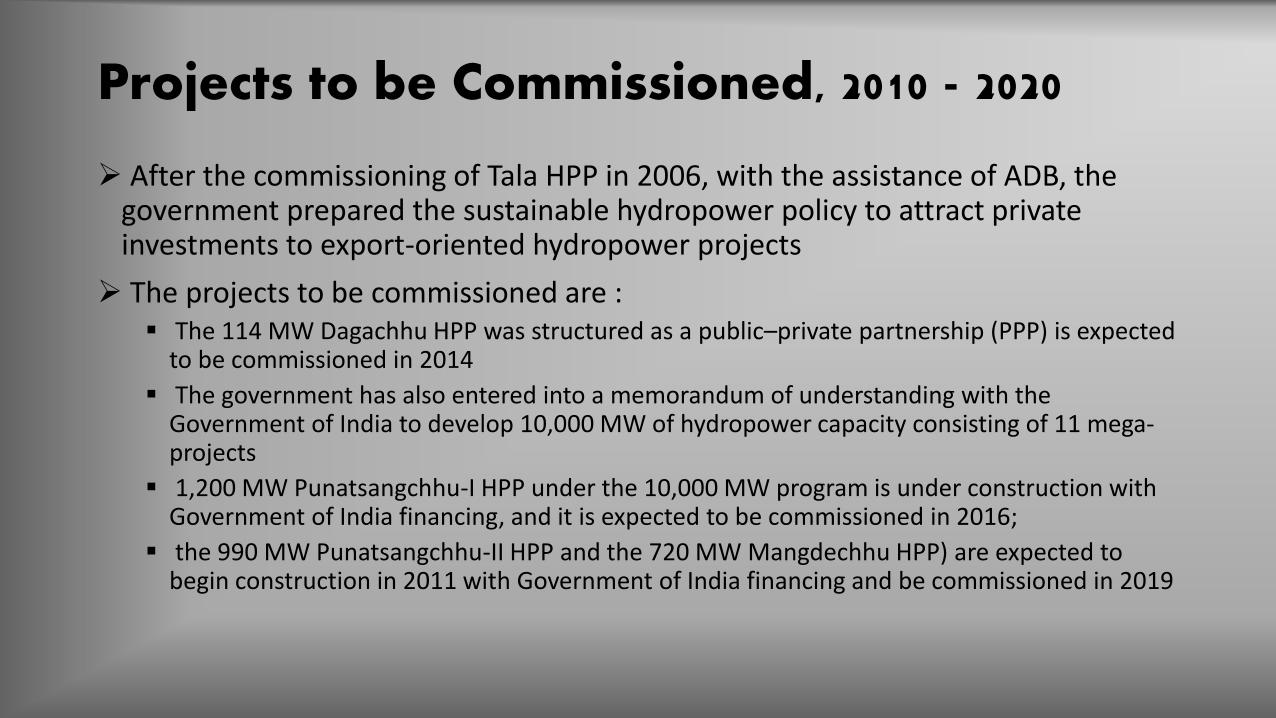

Projects to be Commissioned, 2010 - 2020

After the commissioning of Tala HPP in 2006, with the assistance of ADB, the government prepared the sustainable hydropower policy to attract private investments to export-oriented hydropower projects

The projects to be commissioned are : The 114 MW Dagachhu HPP was structured as a public–private partnership (PPP) is expected

to be commissioned in 2014

The government has also entered into a memorandum of understanding with the Government of India to develop 10,000 MW of hydropower capacity consisting of 11 mega-projects

1,200 MW Punatsangchhu-I HPP under the 10,000 MW program is under construction with Government of India financing, and it is expected to be commissioned in 2016;

the 990 MW Punatsangchhu-II HPP and the 720 MW Mangdechhu HPP) are expected to begin construction in 2011 with Government of India financing and be commissioned in 2019

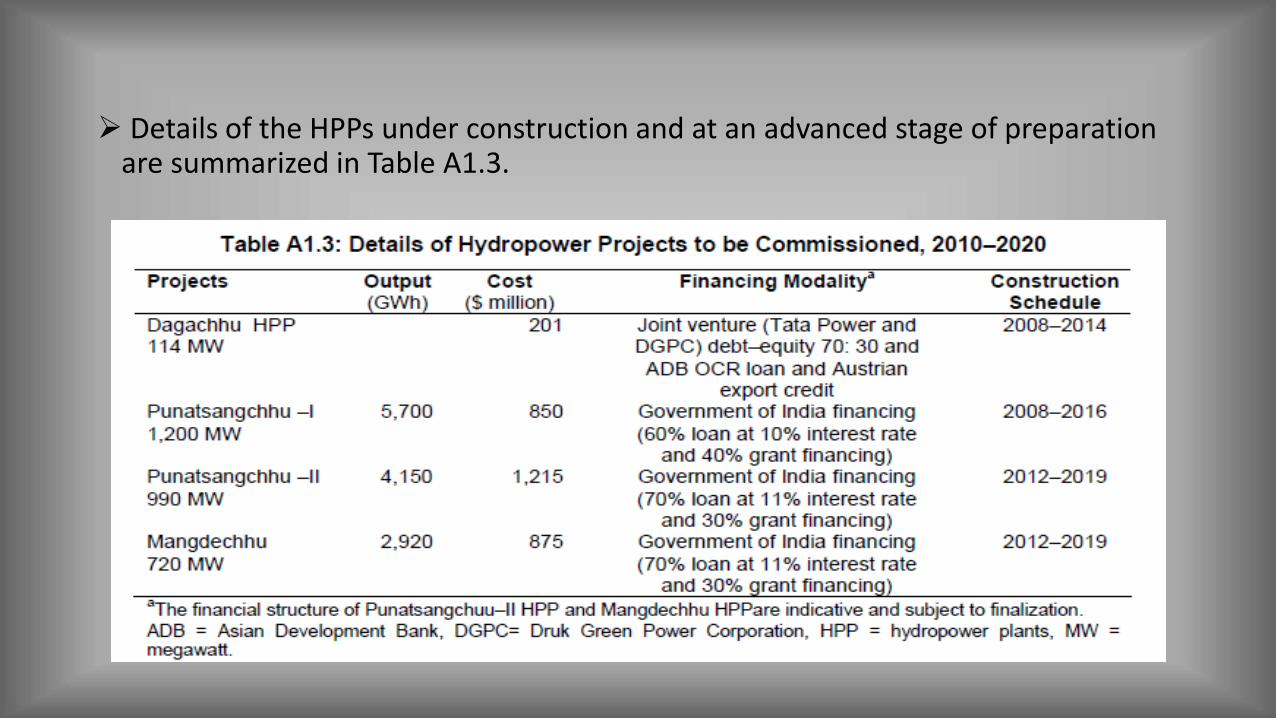

Details of the HPPs under construction and at an advanced stage of preparation are summarized in Table A1.3.

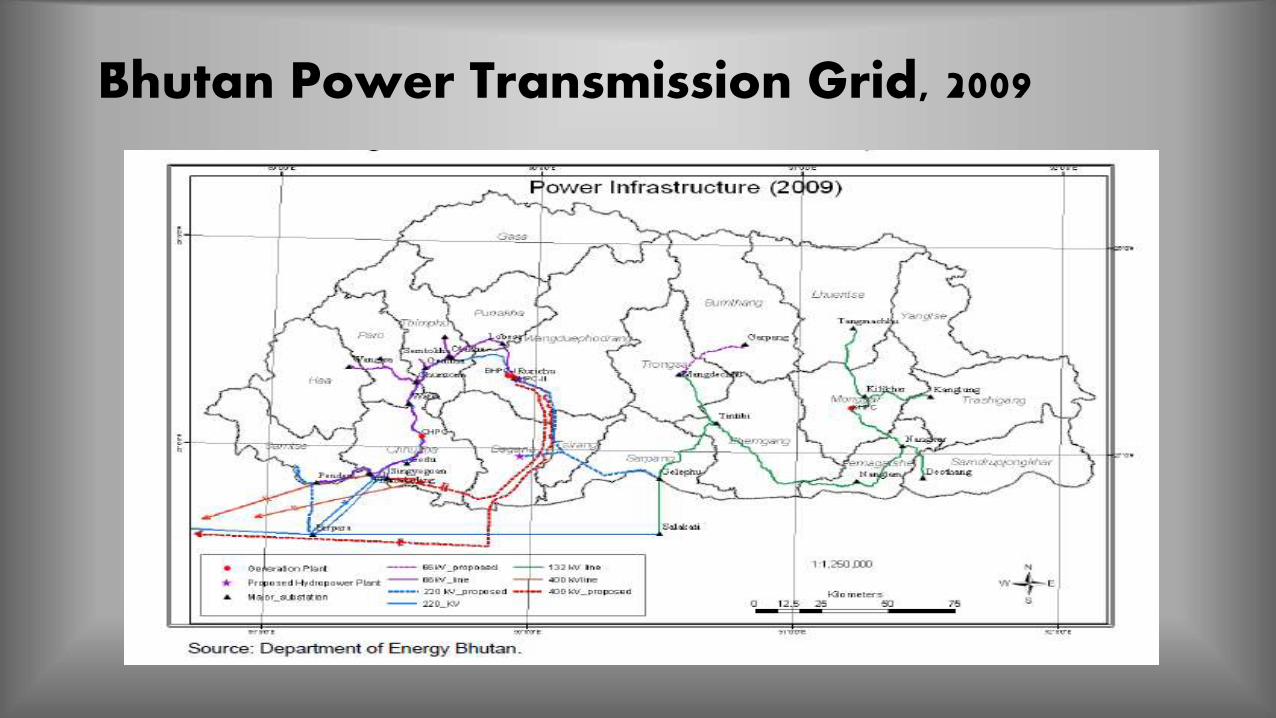

Bhutan Power Transmission Grid, 2009

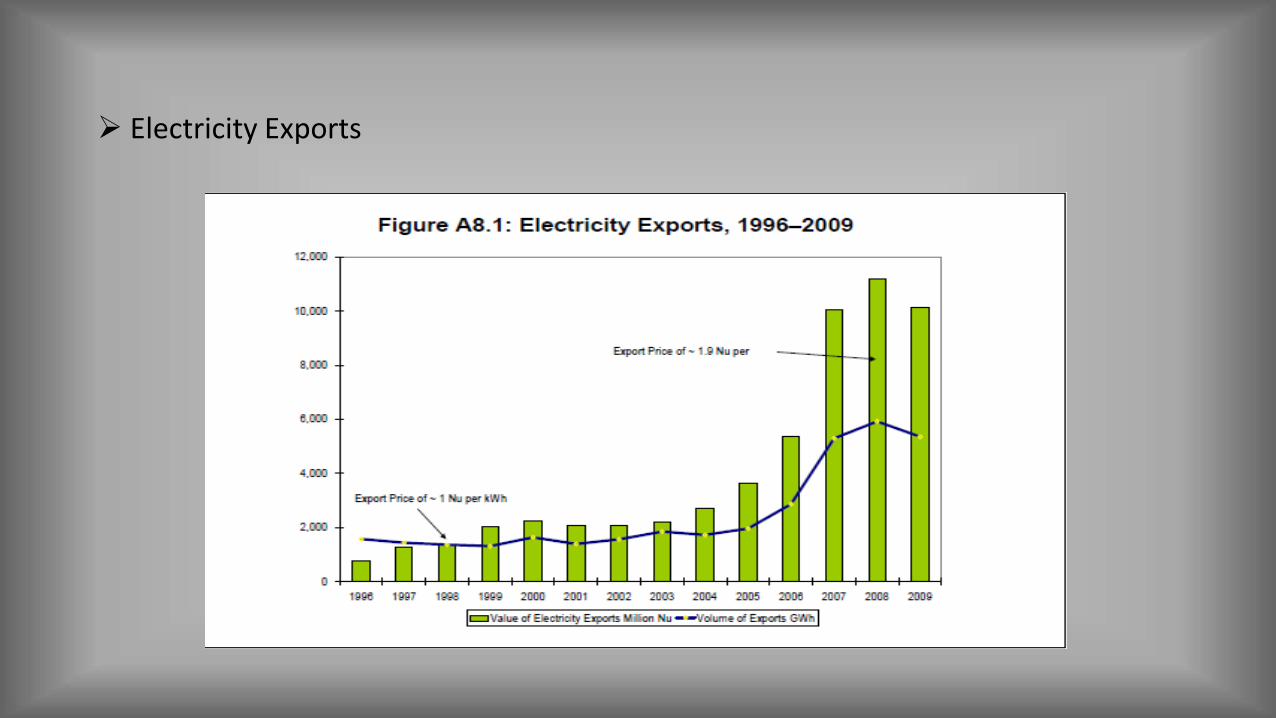

Macroeconomic Impacts of Export –Oriented Hydropower Development

Power exports, which accounted for about 21% of total exports in 1996, grew in value in 1997 as India agreed to lift the power purchase price in steps from an average Nu0.5 per kilowatt-hour (kWh) in 1996 to Nu1.5/kWh in 1999

Current export price averages Nu1.9/kWh

The commissioning of Tala hydropower plant (HPP) for 1,020 megawatts (MW) in 2007 had a major impact on both gross domestic product (GDP) and exports, with exports rising to over Nu10 billion

Power exports contributed a significant share to the overall GDP in 2009 as well as the government’s fiscal revenues

The export-oriented power generation plants provided an implicit subsidy amounting to Nu1,958 million to the domestic power supply in 2009

Electricity Exports

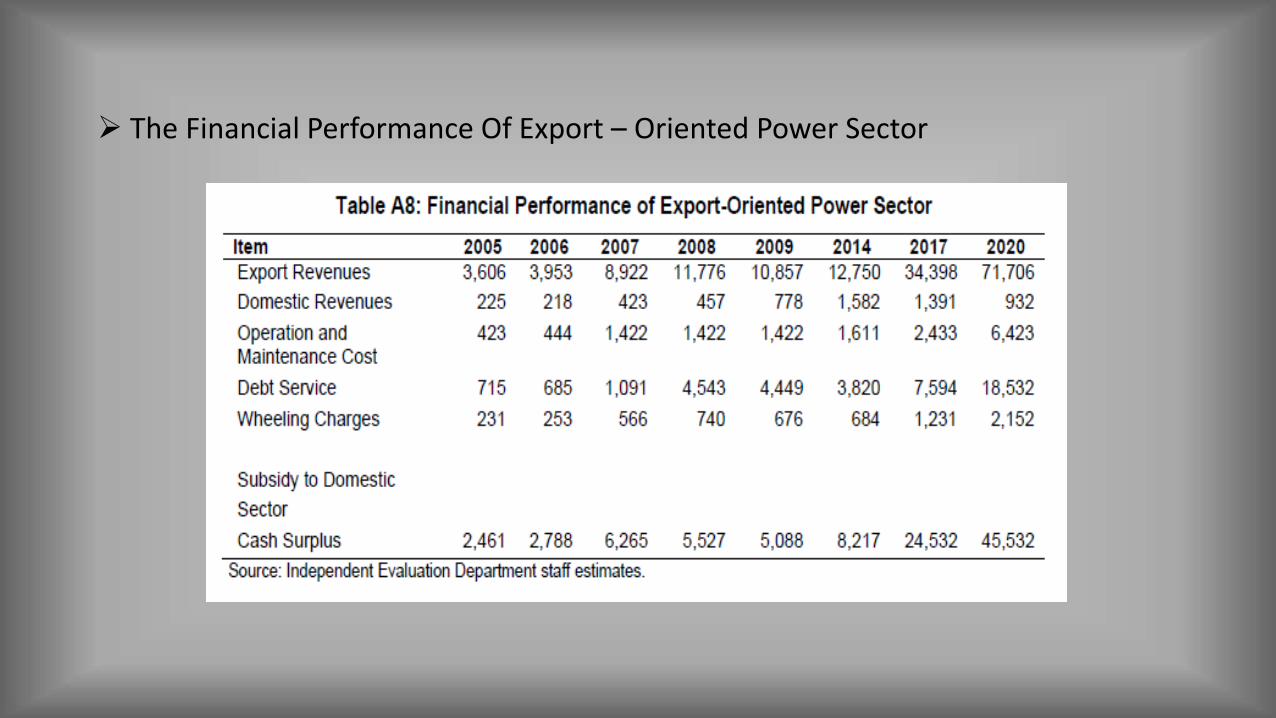

The Financial Performance Of Export – Oriented Power Sector

Bhutan Energy Sector Institutions and Current Energy Policies

Department of Energy (DOE): The DOE is responsible for policy formulation,

planning, and

coordination of activities for the energy sector

overall responsibility for implementing the government’s ambitious rural electrification program and

developing the new export-oriented HPPs

Bhutan Electricity Authority (BEA), a regulatory body under the DOE: Acts as an entrusted body for the economic

and technical regulation of power sector entities, including tariff setting and licensing

Druk Green Power Corporation harnessing and sustaining Bhutan’s renewable energy resources

It controls the four major hydropower projects including Chukha HPP, Basochhu HPP, Kurichhu HPP, and Tala HPP

Bhutan Power Corporation Limited (BPC) :established as a public utility on 1 July 2002 mandate of distributing electricity throughout the country and

also providing transmission access for generating stations for domestic supply as well as export

The Renewable Energy Division (RED) under DOE implementation of alternative renewable energy development projects,

construction of MV and LV lines and substations

current mandate of the RED is expansion of the distribution infrastructure to achieve the Royal Government’s goal of 'Electricity for All by the year 2013'

Smart Grid and DSM

Smart Grid is based on the application of digital technology in the electricity network in order to supply electricity consumers via two-way communication

monitor and analyze the energy use and help improve energy efficiency,

ensure transparency and reliability of the energy supply chain

Smart energy enabled by 'information and communication technologies' (ICTs) can allow consumers to closely monitor their consumption and energy suppliers to more efficiently meet the demand

Smart energy response and management technologies provide utilities with tools to streamline and target Demand Side Management (DSM) and potential reduction opportunities

Conclusion

The royal govt. of Bhutan is pursuing opportunities for the enlargement of Hydropower capacities

Several Hydropower projects are underway, which are expected to generate a total of 10,000 MW by 2020

Nevertheless, there are risk of dependency on the sales of a commodity to a single market – India

There are risk from natural disasters, such as earthquakes, as Bhutan is located between the Indian and Asian Tectonic plates

Climate change effects including glacial melts, landslides and monsoon may also pose a several risk to the infrastructure

NEPAL

Nepal

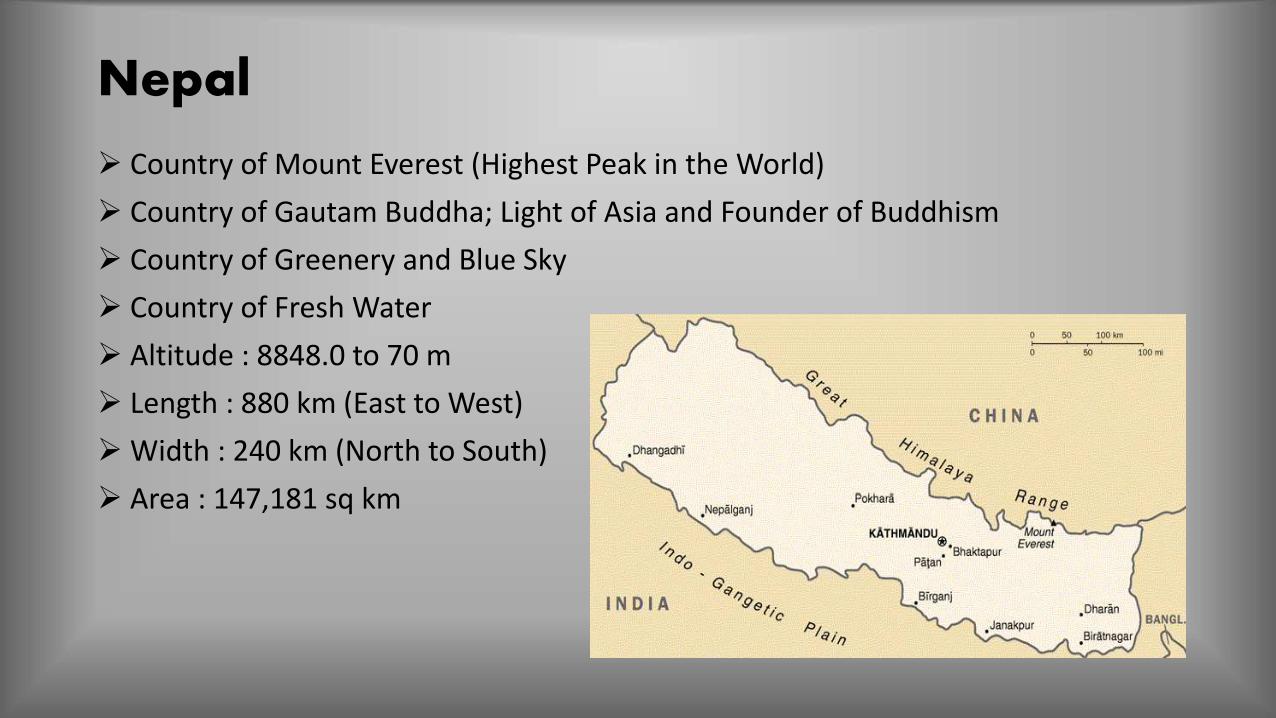

Country of Mount Everest (Highest Peak in the World)

Country of Gautam Buddha; Light of Asia and Founder of Buddhism

Country of Greenery and Blue Sky

Country of Fresh Water

Altitude : 8848.0 to 70 m

Length : 880 km (East to West)

Width : 240 km (North to South)

Area : 147,181 sq km

Brief History of Nepal

Nepal had many Small Kingdoms before 1768

The Modern State was formed with the Unification of Nepal. United by the King Prithvi Narayan Shah on December 21, 1768

Until 2006, Nepal was a kingdom ruled by Royal Family.

On December 28, 2007, the Interim Parliament passed a bill and declared Nepal to be a Federal Democratic Republic

The First Meeting of the Constituent Assembly on May 28, 2008

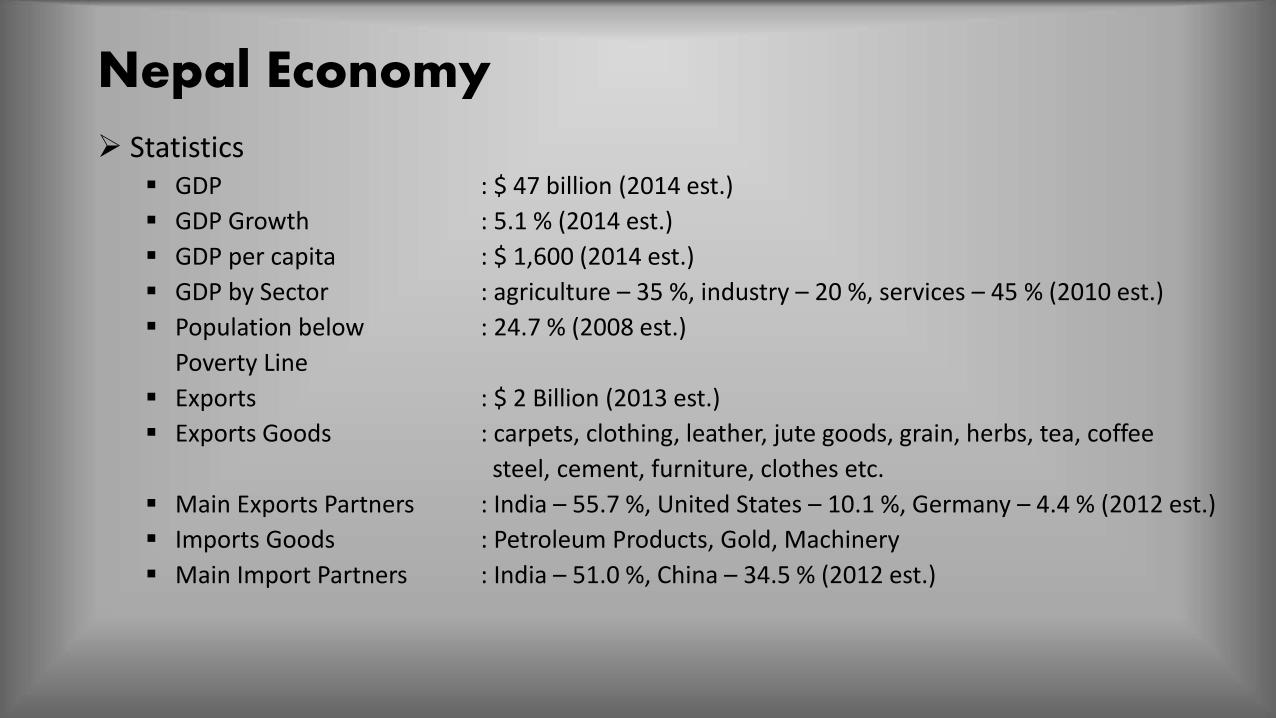

Nepal Economy

Statistics GDP : $ 47 billion (2014 est.)

GDP Growth : 5.1 % (2014 est.)

GDP per capita : $ 1,600 (2014 est.)

GDP by Sector : agriculture – 35 %, industry – 20 %, services – 45 % (2010 est.)

Population below : 24.7 % (2008 est.)

Poverty Line

Exports : $ 2 Billion (2013 est.)

Exports Goods : carpets, clothing, leather, jute goods, grain, herbs, tea, coffee

steel, cement, furniture, clothes etc.

Main Exports Partners : India – 55.7 %, United States – 10.1 %, Germany – 4.4 % (2012 est.)

Imports Goods : Petroleum Products, Gold, Machinery

Main Import Partners : India – 51.0 %, China – 34.5 % (2012 est.)

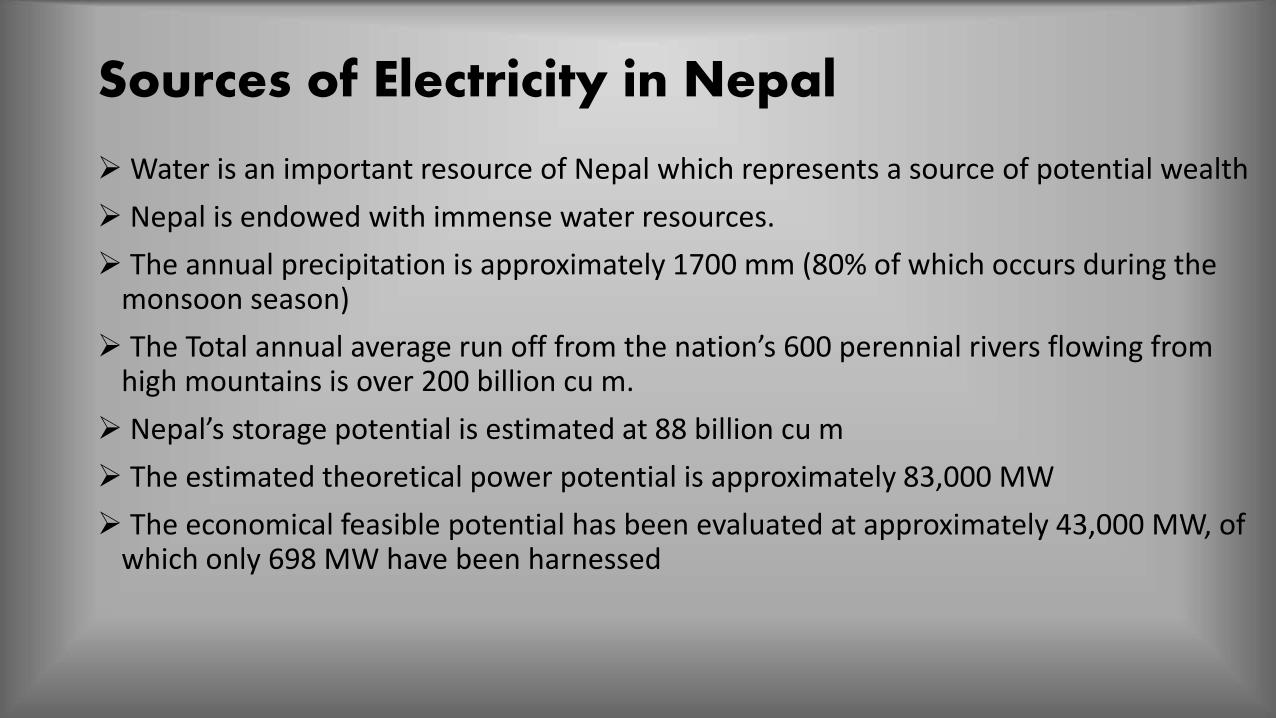

Sources of Electricity in Nepal

Water is an important resource of Nepal which represents a source of potential wealth

Nepal is endowed with immense water resources.

The annual precipitation is approximately 1700 mm (80% of which occurs during the monsoon season)

The Total annual average run off from the nation’s 600 perennial rivers flowing from high mountains is over 200 billion cu m.

Nepal’s storage potential is estimated at 88 billion cu m

The estimated theoretical power potential is approximately 83,000 MW

The economical feasible potential has been evaluated at approximately 43,000 MW, of which only 698 MW have been harnessed

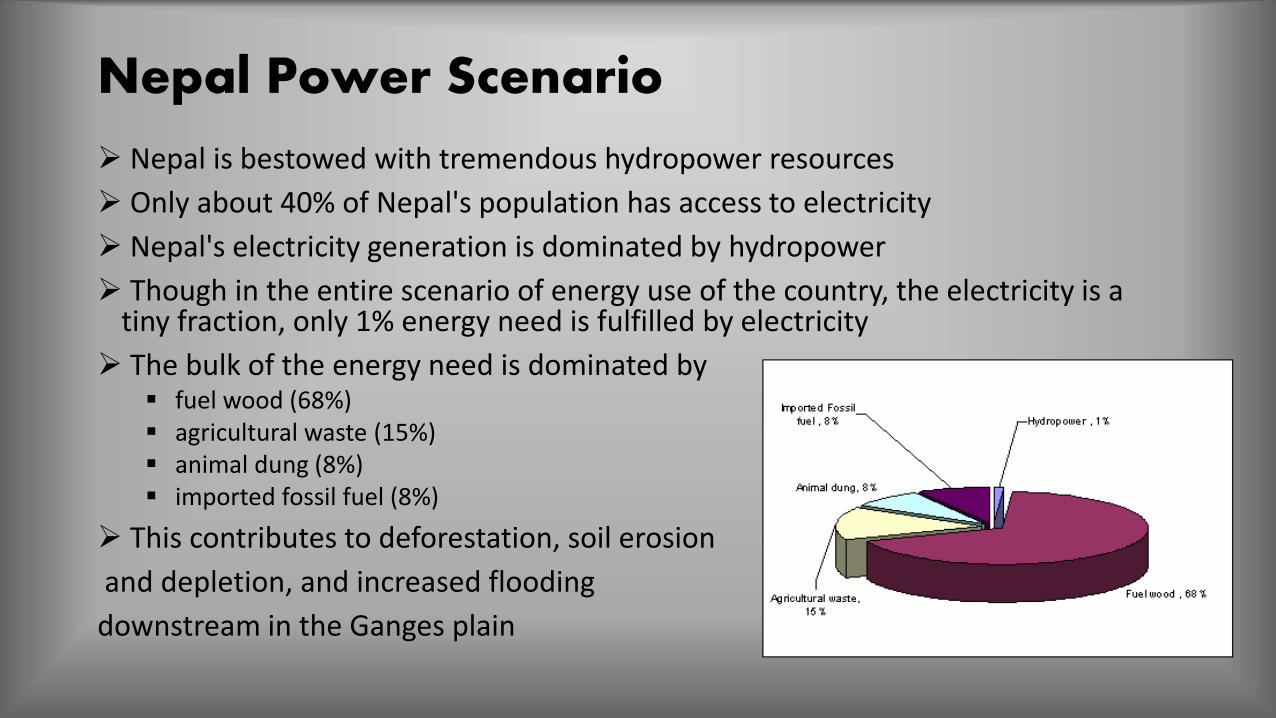

Nepal Power Scenario

Nepal is bestowed with tremendous hydropower resources

Only about 40% of Nepal's population has access to electricity

Nepal's electricity generation is dominated by hydropower

Though in the entire scenario of energy use of the country, the electricity is a tiny fraction, only 1% energy need is fulfilled by electricity

The bulk of the energy need is dominated by fuel wood (68%) agricultural waste (15%) animal dung (8%) imported fossil fuel (8%)

This contributes to deforestation, soil erosion

and depletion, and increased flooding

downstream in the Ganges plain

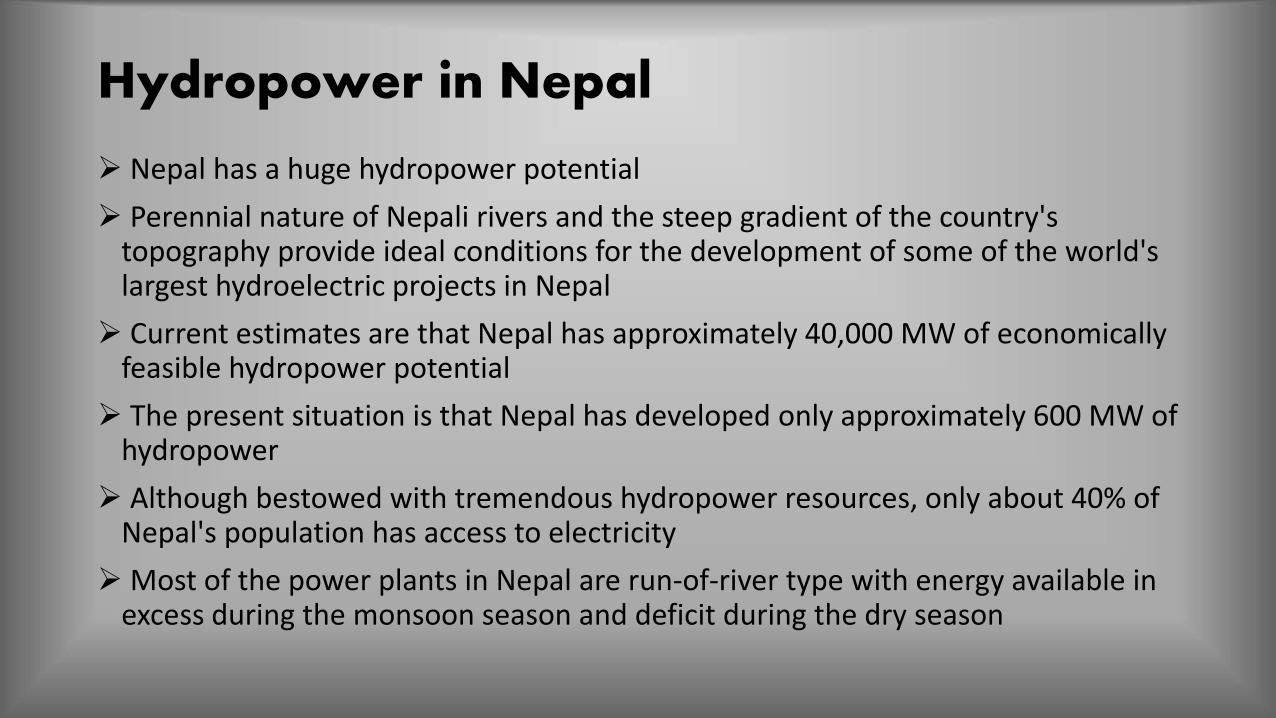

Hydropower in Nepal

Nepal has a huge hydropower potential

Perennial nature of Nepali rivers and the steep gradient of the country's topography provide ideal conditions for the development of some of the world's largest hydroelectric projects in Nepal

Current estimates are that Nepal has approximately 40,000 MW of economically feasible hydropower potential

The present situation is that Nepal has developed only approximately 600 MW of hydropower

Although bestowed with tremendous hydropower resources, only about 40% of Nepal's population has access to electricity

Most of the power plants in Nepal are run-of-river type with energy available in excess during the monsoon season and deficit during the dry season

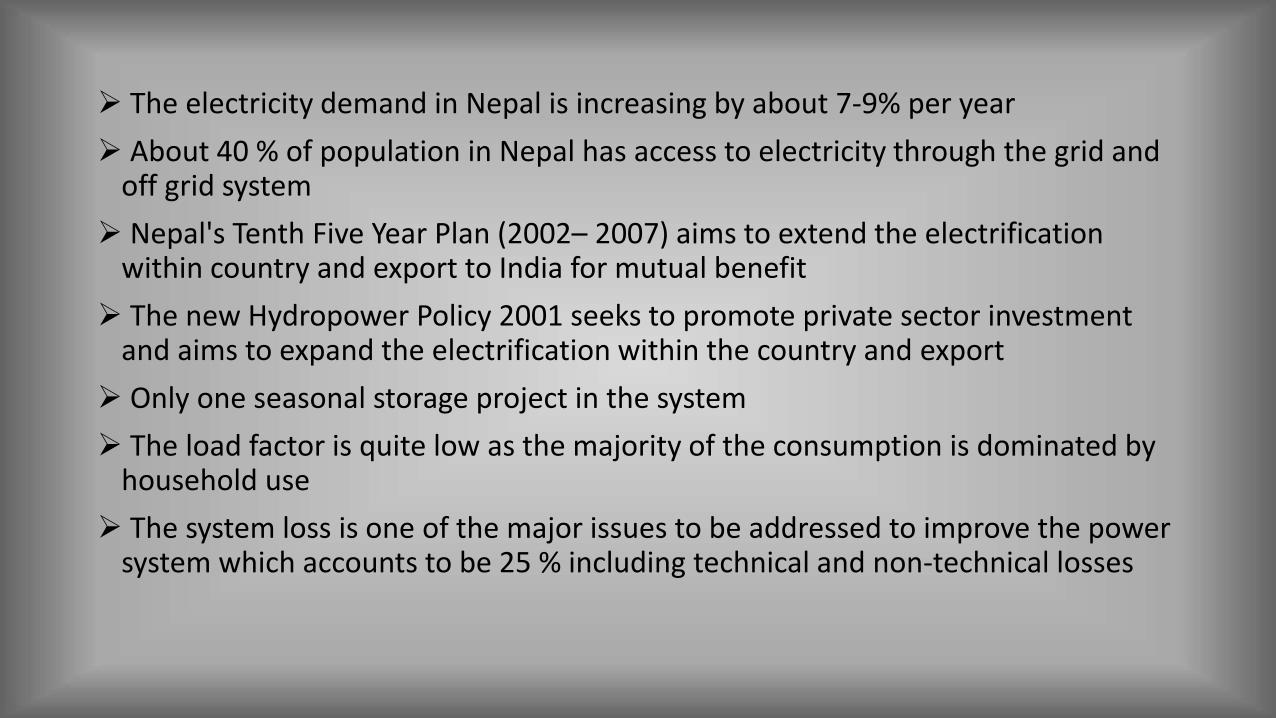

The electricity demand in Nepal is increasing by about 7-9% per year

About 40 % of population in Nepal has access to electricity through the grid and off grid system

Nepal's Tenth Five Year Plan (2002– 2007) aims to extend the electrification within country and export to India for mutual benefit

The new Hydropower Policy 2001 seeks to promote private sector investment and aims to expand the electrification within the country and export

Only one seasonal storage project in the system

The load factor is quite low as the majority of the consumption is dominated by household use

The system loss is one of the major issues to be addressed to improve the power system which accounts to be 25 % including technical and non-technical losses

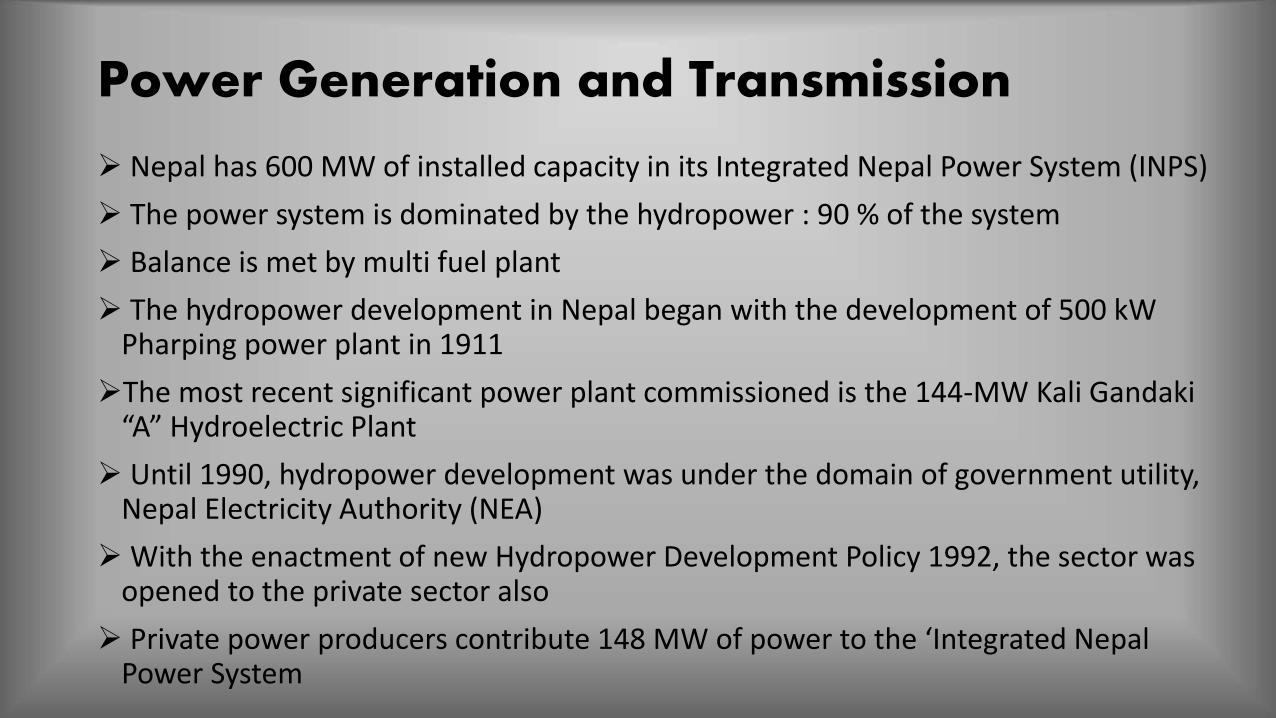

Power Generation and Transmission

Nepal has 600 MW of installed capacity in its Integrated Nepal Power System (INPS)

The power system is dominated by the hydropower : 90 % of the system

Balance is met by multi fuel plant

The hydropower development in Nepal began with the development of 500 kW Pharping power plant in 1911

The most recent significant power plant commissioned is the 144-MW Kali Gandaki “A” Hydroelectric Plant

Until 1990, hydropower development was under the domain of government utility, Nepal Electricity Authority (NEA)

With the enactment of new Hydropower Development Policy 1992, the sector was opened to the private sector also

Private power producers contribute 148 MW of power to the ‘Integrated Nepal Power System

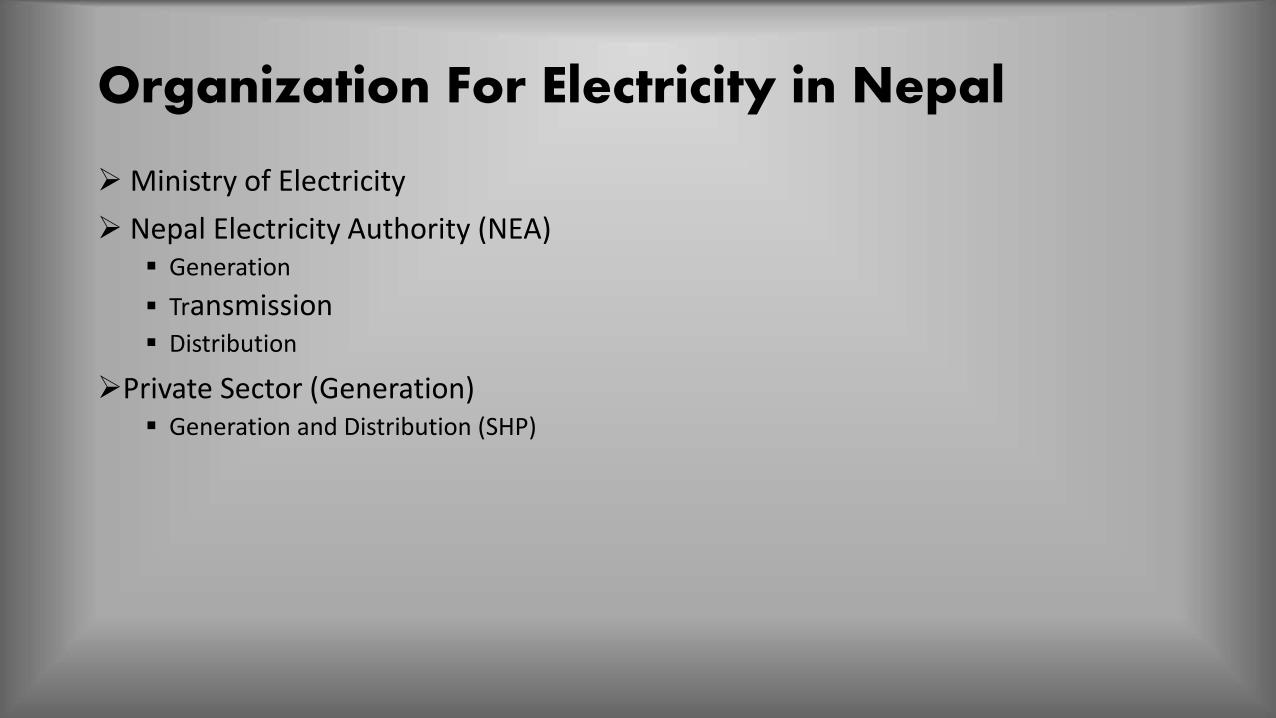

Organization For Electricity in Nepal

Ministry of Electricity

Nepal Electricity Authority (NEA) Generation

Transmission Distribution

Private Sector (Generation) Generation and Distribution (SHP)

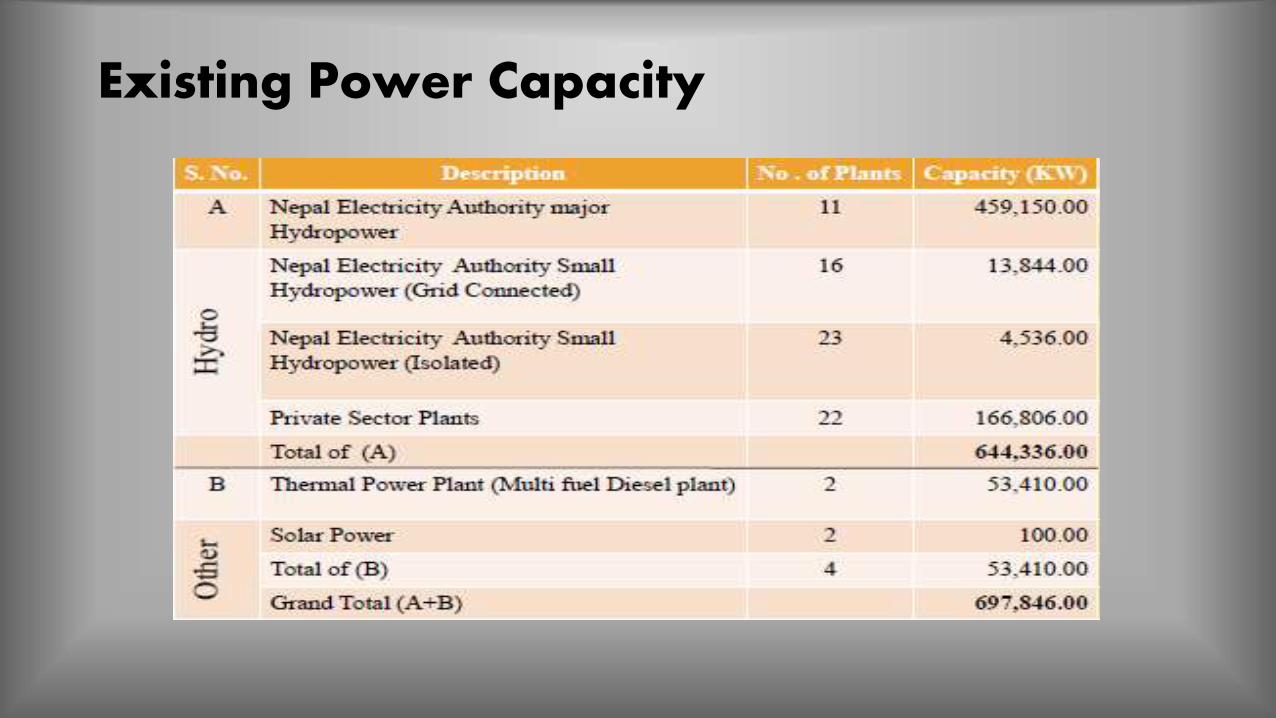

Existing Power Capacity

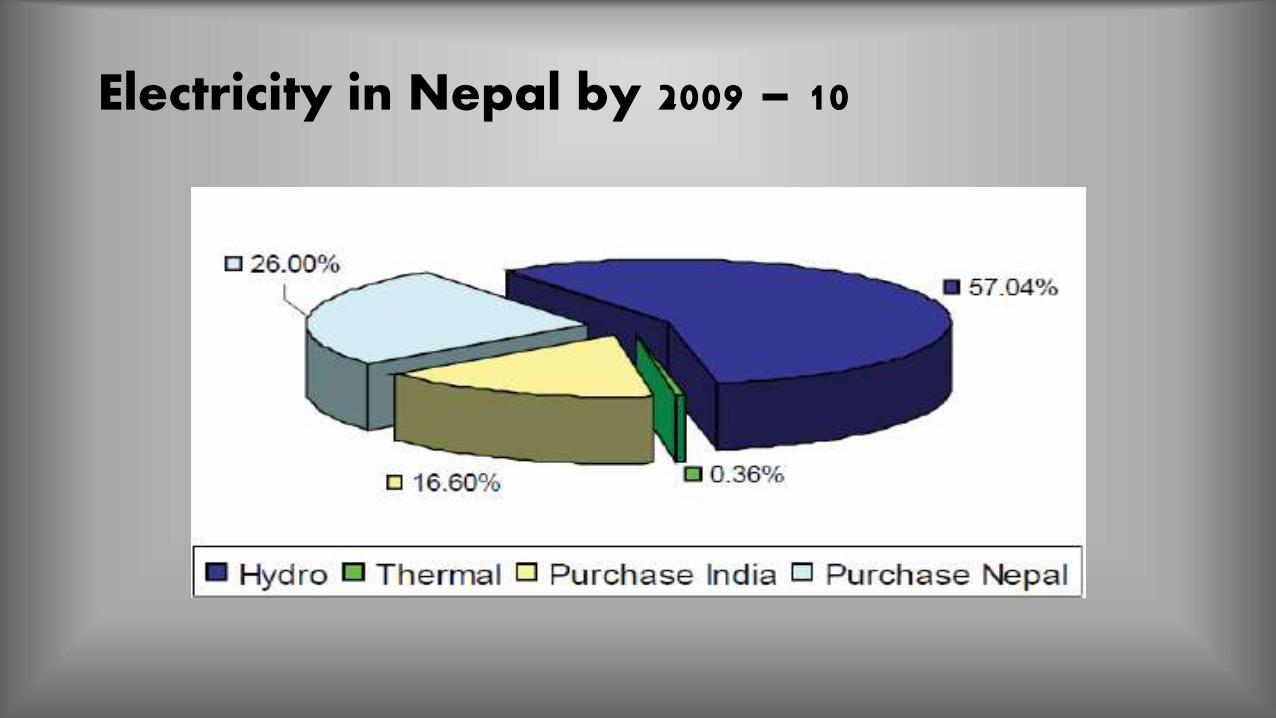

Electricity in Nepal by 2009 – 10

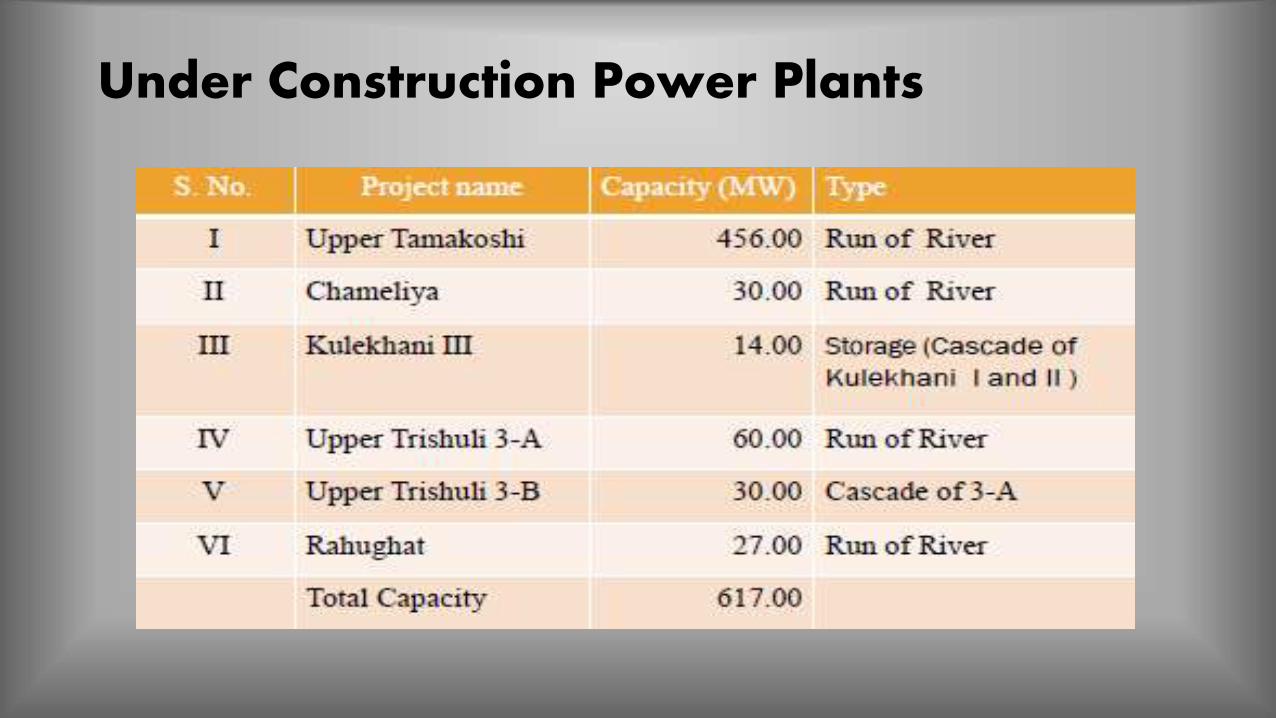

Under Construction Power Plants

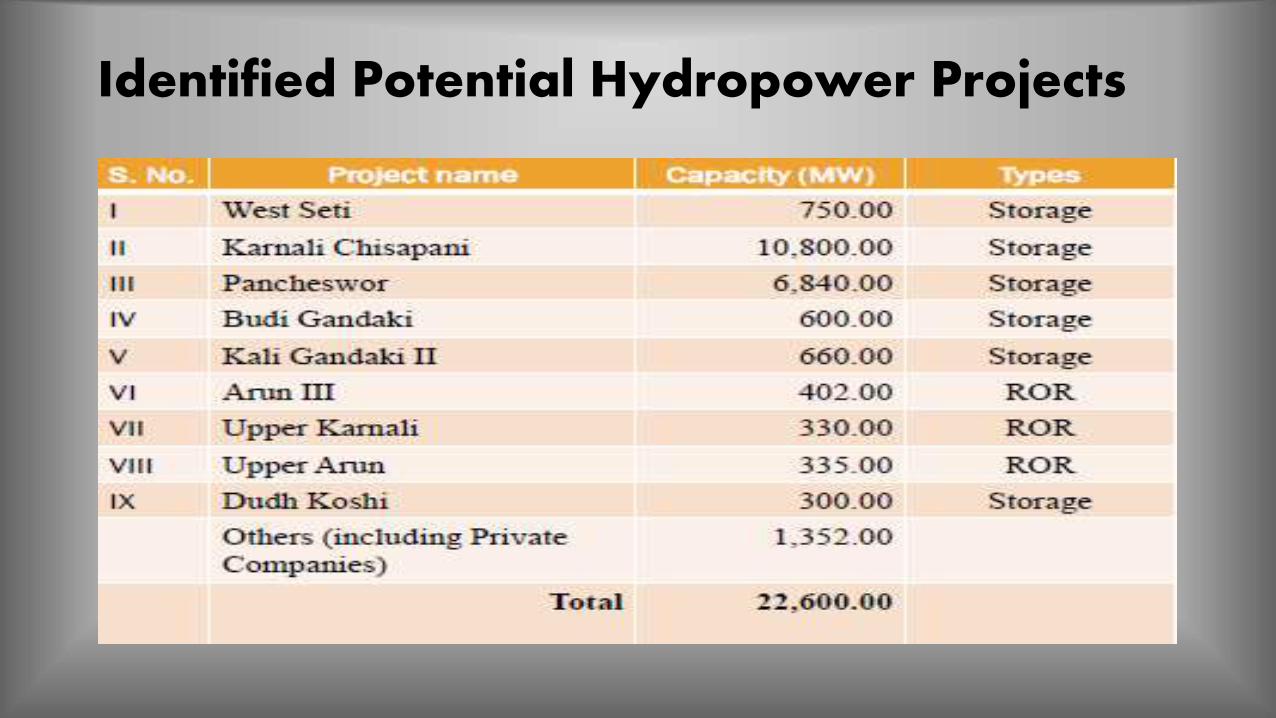

Identified Potential Hydropower Projects

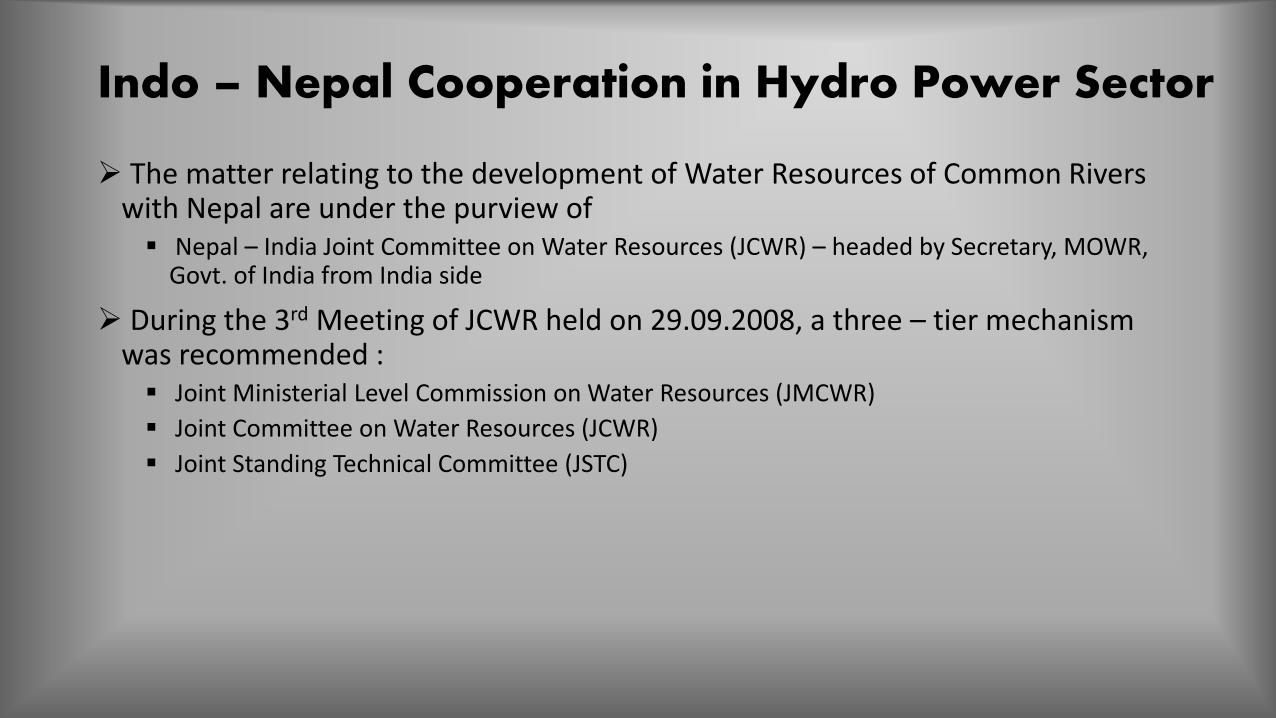

Indo – Nepal Cooperation in Hydro Power Sector

The matter relating to the development of Water Resources of Common Rivers with Nepal are under the purview of Nepal – India Joint Committee on Water Resources (JCWR) – headed by Secretary, MOWR,

Govt. of India from India side

During the 3rd Meeting of JCWR held on 29.09.2008, a three – tier mechanism was recommended : Joint Ministerial Level Commission on Water Resources (JMCWR)

Joint Committee on Water Resources (JCWR)

Joint Standing Technical Committee (JSTC)

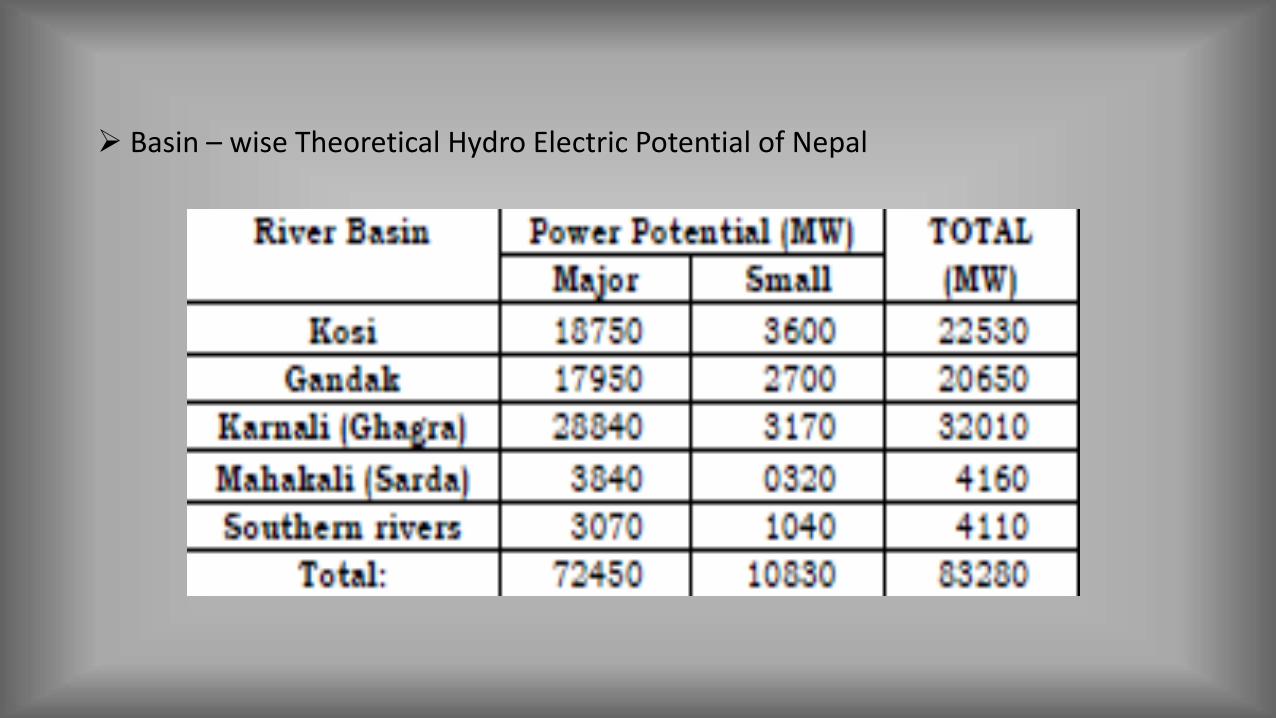

Basin – wise Theoretical Hydro Electric Potential of Nepal

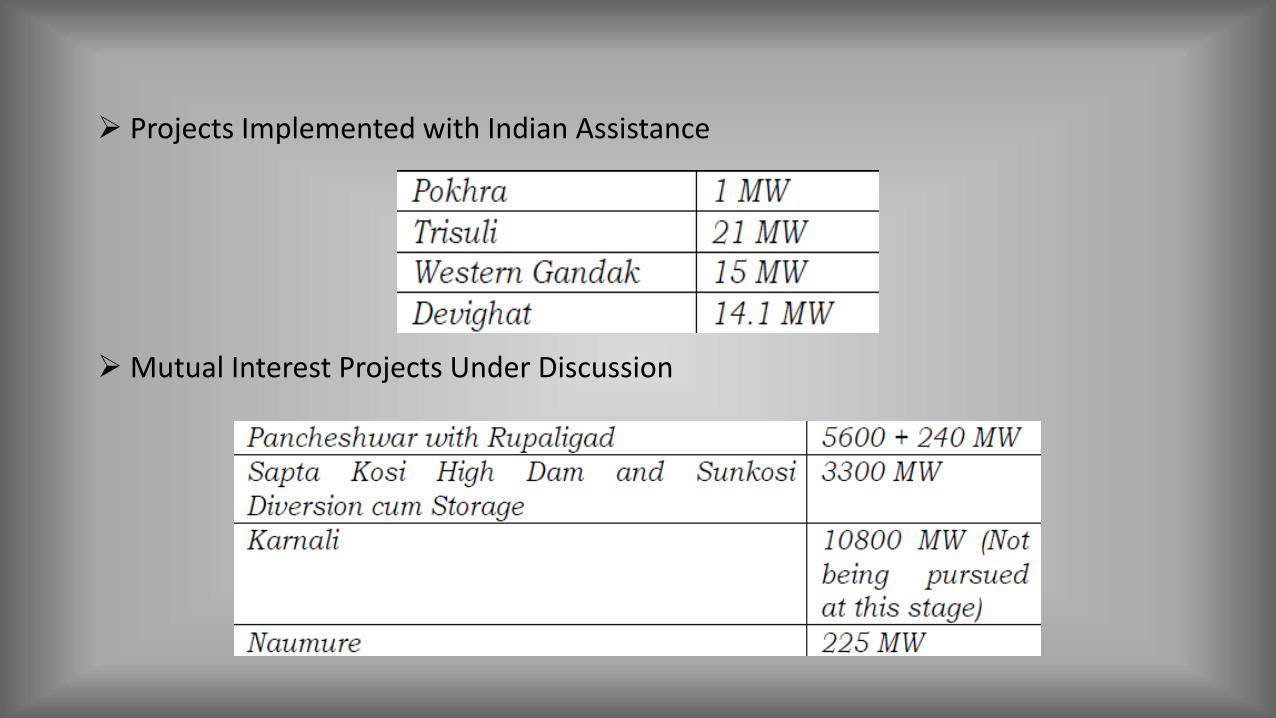

Projects Implemented with Indian Assistance

Mutual Interest Projects Under Discussion

Conclusion

Government has declared Energy crisis but yet to be approved by parliament

Reduction in custom duties for hydro – electrical equipments

Extended the taking over period

Reduction of Royalties

In coming years, Nepal’s Power Sector is expected to boom tremendously.

Hydropower Projects currently under construction, planned and proposed sholdboost the country’s total generating capacity up to 22,000 MW, half of the country’s economical hydropower potential

Meantime creation and search of market Power Export

THANK YOU

Related Documents