POWER ENGINEERING CONSULTING JSC 2 HSX: TV2 UPDATE REPORT June 4, 2021 TV2 - BUY Stock information (03/06/2021) Stock exchange HOSE Market price (VND) 50.800 Average volume (10 days) 117.980 Capitalization (VND billion) 1.830 Common share (million) 36 Target price 77.700 Upside +53,0% Equity Research Mr. Trinh Van Ha [email protected] +84-2838200796 ext 643 VCBS’s Report www.vcbs.com.vn/vn/Services/AnalysisResearch VCBS Bloomberg Page: <VCBS><go> Research Department Page | 0 TV2 – WIND POWER SUPPORT GROWTH, O&M MAKE A BREAKTHROUGH RECOMMENDATION Our expectations for the long-term growth of all three spearheads: Consulting, Construction and Investment. In addition, operations management is a new field with great potential . We recommend BUY for TV2 with a target price in 2021-2022 of VND 77,700/share, offering an upside of 53.0% compared to the closing price on June 3nd, 2021. Based on the significantly growth of O&M services along with the good performance of invested projects and consulting, electricity construction and installation are still stable in the short term and have many long-term potential contracts. FORECAST VCBS forecasts that TV2’s net revenue in 2021 will reach VND3,790 billion (+13.2% yoy, 2.9% higher than 2021’s plan) and NPAT is estimated to reach VND301 billion (+15% yoy, 11.5% higher than 2021’s plan), equivalent to 2021F EPS of VND8,355/share and a forward PE of 6.0. PROSPECTIVE (1) O&M is a new segment with nearly 5% revenue but bring significantly profit (~20%) due to high GPM. (2) Wind EPC help TV2 to offset high base of Solar PV EPC last year beside long term growth of Thermal power (coal – fired and LNG) (3) Profitable investing in power generation projects due to take advantage of planning, pre – FS, FS contract and other electricity consultant projects. (4) Although low contributed in revenue, Consulting still be a majority segment to support other segments. Major financial factors 2019 2020 2021F 2022F Revenue (VND billion) 3,322 3,346 3,790 4,084 +/- yoy (%) 80.5% 0.7% 13.2% 7.8% NPAT (VND billion) 255 262 301 375 +/- yoy (%) 3% 15% 25% Total Equity (VND billion) 931 1,167 1,453 1,810 D/A (%) 14% 14% 11% 11% GMP (%) 9.6% 12.8% 12.7% 13.1% ROE (%) 31% 25% 23% 23% Dividend/Share holder equity 83% 50% 35% 40% EPS (VND) 10,626 7,280 8,355 10,421 P/E 8 7 6.01 4.82 BVPS (VND) 38,781 32,411 40,348 50,248 P/B 2.5 1.9 1.24 1.00

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

POWER ENGINEERING CONSULTING JSC 2

HSX: TV2

UPDATE REPORT June 4, 2021

TV2 - BUY

Stock information

(03/06/2021)

Stock exchange HOSE

Market price (VND) 50.800

Average volume (10

days)

117.980

Capitalization (VND

billion)

1.830

Common share (million) 36

Target price 77.700

Upside +53,0%

Equity Research

Mr. Trinh Van Ha

+84-2838200796 ext 643

VCBS’s Report

www.vcbs.com.vn/vn/Services/AnalysisResearch

VCBS Bloomberg Page: <VCBS><go>

Research Department Page | 0

TV2 – WIND POWER SUPPORT GROWTH, O&M MAKE

A BREAKTHROUGH

RECOMMENDATION

Our expectations for the long-term growth of all three spearheads: Consulting, Construction

and Investment. In addition, operations management is a new field with great potential .

We recommend BUY for TV2 with a target price in 2021-2022 of VND 77,700/share,

offering an upside of 53.0% compared to the closing price on June 3nd, 2021. Based on

the significantly growth of O&M services along with the good performance of invested

projects and consulting, electricity construction and installation are still stable in the short

term and have many long-term potential contracts.

FORECAST

VCBS forecasts that TV2’s net revenue in 2021 will reach VND3,790 billion (+13.2% yoy,

2.9% higher than 2021’s plan) and NPAT is estimated to reach VND301 billion (+15% yoy,

11.5% higher than 2021’s plan), equivalent to 2021F EPS of VND8,355/share and a forward

PE of 6.0.

PROSPECTIVE

(1) O&M is a new segment with nearly 5% revenue but bring significantly profit (~20%) due

to high GPM.

(2) Wind EPC help TV2 to offset high base of Solar PV EPC last year beside long term growth

of Thermal power (coal – fired and LNG)

(3) Profitable investing in power generation projects due to take advantage of planning, pre –

FS, FS contract and other electricity consultant projects.

(4) Although low contributed in revenue, Consulting still be a majority segment to support

other segments.

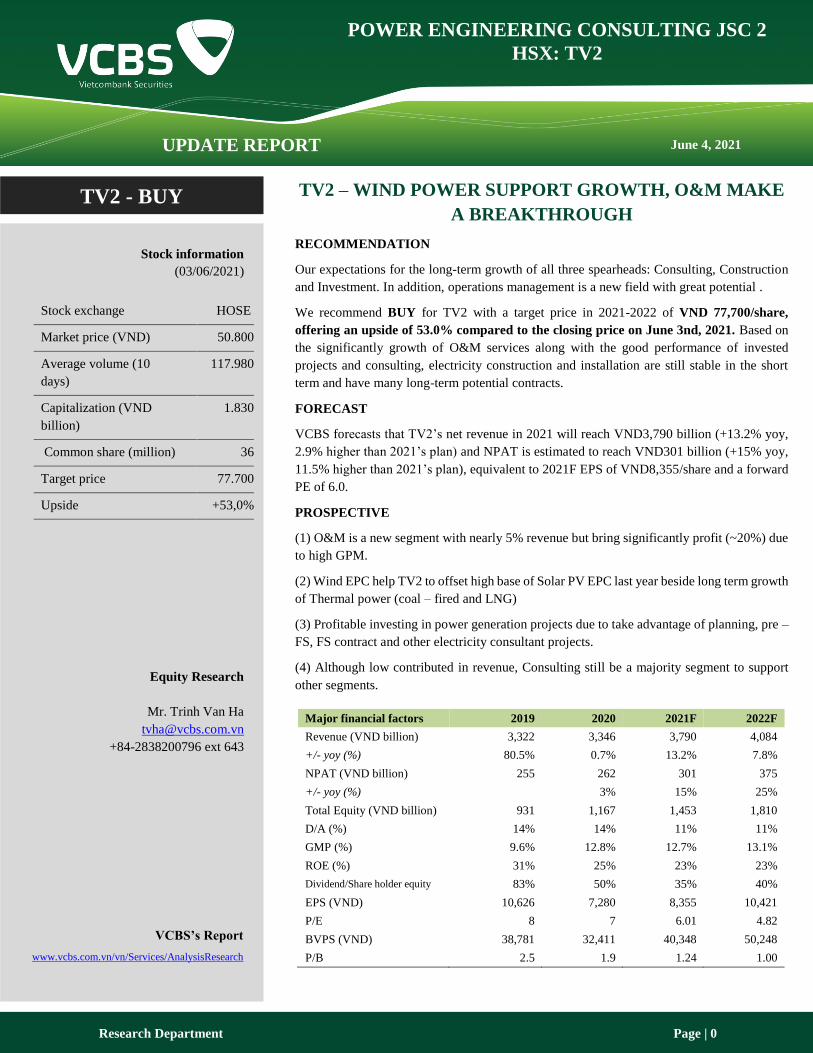

Major financial factors 2019 2020 2021F 2022F

Revenue (VND billion) 3,322 3,346 3,790 4,084

+/- yoy (%) 80.5% 0.7% 13.2% 7.8%

NPAT (VND billion) 255 262 301 375

+/- yoy (%) 3% 15% 25%

Total Equity (VND billion) 931 1,167 1,453 1,810

D/A (%) 14% 14% 11% 11%

GMP (%) 9.6% 12.8% 12.7% 13.1%

ROE (%) 31% 25% 23% 23%

Dividend/Share holder equity 83% 50% 35% 40%

EPS (VND) 10,626 7,280 8,355 10,421

P/E 8 7 6.01 4.82

BVPS (VND) 38,781 32,411 40,348 50,248

P/B 2.5 1.9 1.24 1.00

Research department - VCBS Page | 1

TV2 – UPDATE REPORT

PERFORMANCE

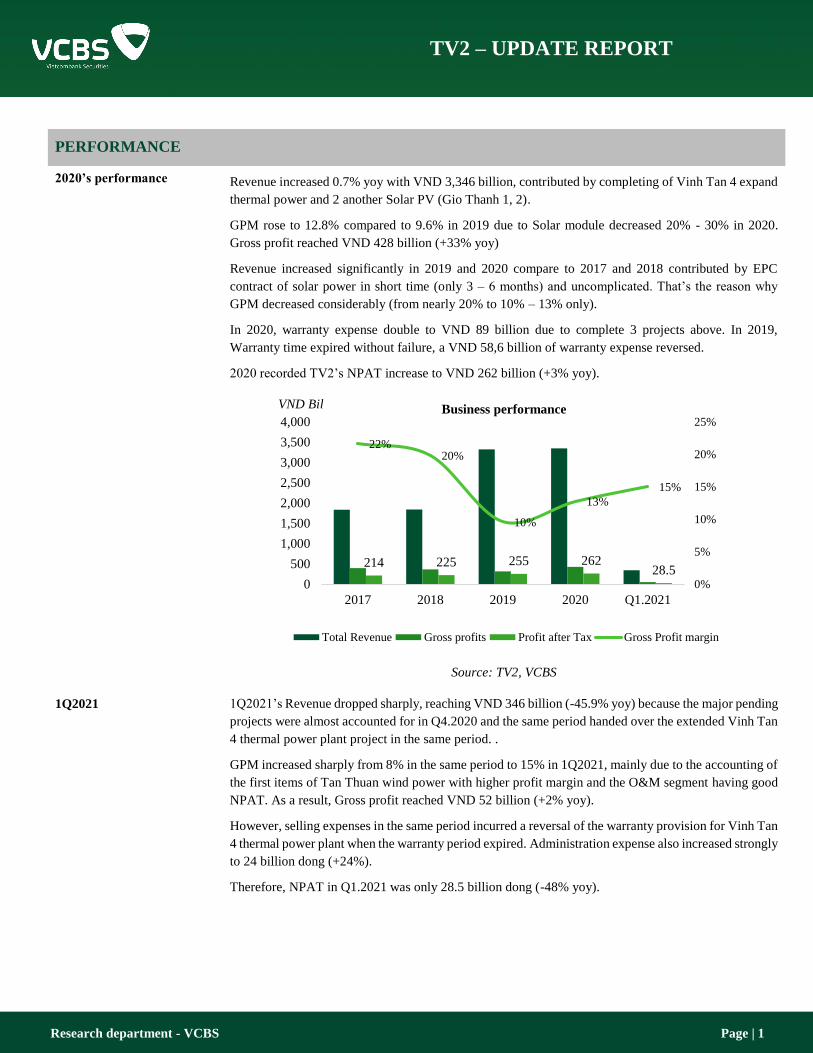

2020’s performance

Revenue increased 0.7% yoy with VND 3,346 billion, contributed by completing of Vinh Tan 4 expand

thermal power and 2 another Solar PV (Gio Thanh 1, 2).

GPM rose to 12.8% compared to 9.6% in 2019 due to Solar module decreased 20% - 30% in 2020.

Gross profit reached VND 428 billion (+33% yoy)

Revenue increased significantly in 2019 and 2020 compare to 2017 and 2018 contributed by EPC

contract of solar power in short time (only 3 – 6 months) and uncomplicated. That’s the reason why

GPM decreased considerably (from nearly 20% to 10% – 13% only).

In 2020, warranty expense double to VND 89 billion due to complete 3 projects above. In 2019,

Warranty time expired without failure, a VND 58,6 billion of warranty expense reversed.

2020 recorded TV2’s NPAT increase to VND 262 billion (+3% yoy).

Source: TV2, VCBS

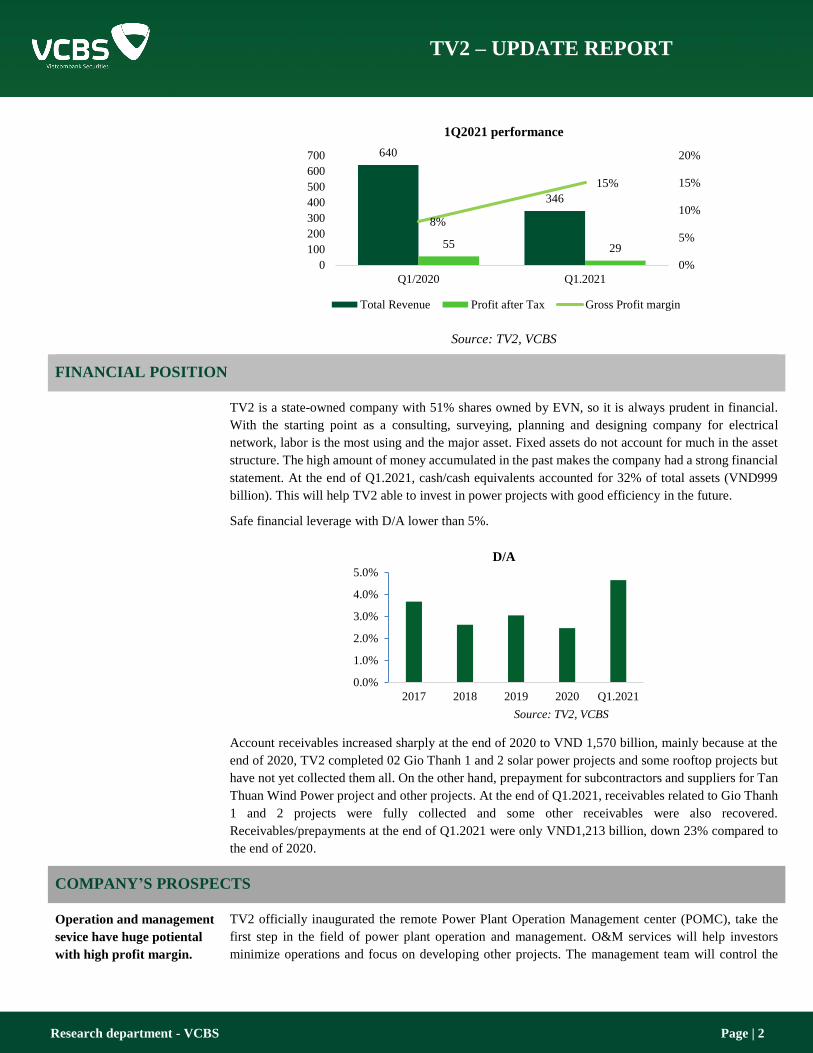

1Q2021 1Q2021’s Revenue dropped sharply, reaching VND 346 billion (-45.9% yoy) because the major pending

projects were almost accounted for in Q4.2020 and the same period handed over the extended Vinh Tan

4 thermal power plant project in the same period. .

GPM increased sharply from 8% in the same period to 15% in 1Q2021, mainly due to the accounting of

the first items of Tan Thuan wind power with higher profit margin and the O&M segment having good

NPAT. As a result, Gross profit reached VND 52 billion (+2% yoy).

However, selling expenses in the same period incurred a reversal of the warranty provision for Vinh Tan

4 thermal power plant when the warranty period expired. Administration expense also increased strongly

to 24 billion dong (+24%).

Therefore, NPAT in Q1.2021 was only 28.5 billion dong (-48% yoy).

214 225 255 262 28.5

22%20%

10%

13%

15%

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2017 2018 2019 2020 Q1.2021

Business performance

Total Revenue Gross profits Profit after Tax Gross Profit margin

VND Bil

Research department - VCBS Page | 2

TV2 – UPDATE REPORT

Source: TV2, VCBS

FINANCIAL POSITION

TV2 is a state-owned company with 51% shares owned by EVN, so it is always prudent in financial.

With the starting point as a consulting, surveying, planning and designing company for electrical

network, labor is the most using and the major asset. Fixed assets do not account for much in the asset

structure. The high amount of money accumulated in the past makes the company had a strong financial

statement. At the end of Q1.2021, cash/cash equivalents accounted for 32% of total assets (VND999

billion). This will help TV2 able to invest in power projects with good efficiency in the future.

Safe financial leverage with D/A lower than 5%.

Account receivables increased sharply at the end of 2020 to VND 1,570 billion, mainly because at the

end of 2020, TV2 completed 02 Gio Thanh 1 and 2 solar power projects and some rooftop projects but

have not yet collected them all. On the other hand, prepayment for subcontractors and suppliers for Tan

Thuan Wind Power project and other projects. At the end of Q1.2021, receivables related to Gio Thanh

1 and 2 projects were fully collected and some other receivables were also recovered.

Receivables/prepayments at the end of Q1.2021 were only VND1,213 billion, down 23% compared to

the end of 2020.

COMPANY’S PROSPECTS

Operation and management

sevice have huge potiental

with high profit margin.

TV2 officially inaugurated the remote Power Plant Operation Management center (POMC), take the

first step in the field of power plant operation and management. O&M services will help investors

minimize operations and focus on developing other projects. The management team will control the

640

346

55 29

8%

15%

0%

5%

10%

15%

20%

0

100

200

300

400

500

600

700

Q1/2020 Q1.2021

1Q2021 performance

Total Revenue Profit after Tax Gross Profit margin

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2017 2018 2019 2020 Q1.2021

D/A

Source: TV2, VCBS

Research department - VCBS Page | 3

TV2 – UPDATE REPORT

power plant 24/24 to maximize the power generation and can calculate in advance the possible problems,

the parts to be replaced through the management system. POMC will reduce human and material

resources for each plant to reduce operating costs and increase power generation efficiency for investors.

The main cost of this activity segment is the cost of labor and operating assets, so the

As out expect, TV2 charge 5% - 7% of Power generation revenue for O&M service with Solar power

plants (without replacement cost), 30% - 35% lower than average cost (7% - 10% of revenue).

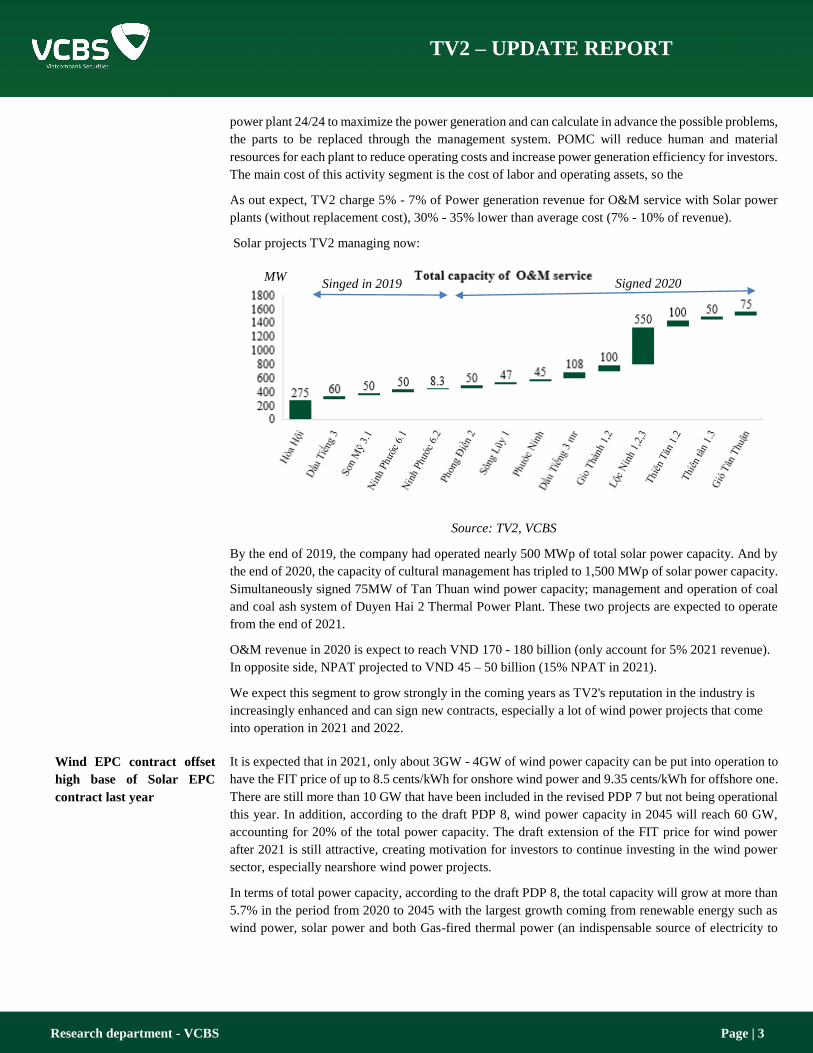

Solar projects TV2 managing now:

Source: TV2, VCBS

By the end of 2019, the company had operated nearly 500 MWp of total solar power capacity. And by

the end of 2020, the capacity of cultural management has tripled to 1,500 MWp of solar power capacity.

Simultaneously signed 75MW of Tan Thuan wind power capacity; management and operation of coal

and coal ash system of Duyen Hai 2 Thermal Power Plant. These two projects are expected to operate

from the end of 2021.

O&M revenue in 2020 is expect to reach VND 170 - 180 billion (only account for 5% 2021 revenue).

In opposite side, NPAT projected to VND 45 – 50 billion (15% NPAT in 2021).

We expect this segment to grow strongly in the coming years as TV2's reputation in the industry is

increasingly enhanced and can sign new contracts, especially a lot of wind power projects that come

into operation in 2021 and 2022.

Wind EPC contract offset

high base of Solar EPC

contract last year

It is expected that in 2021, only about 3GW - 4GW of wind power capacity can be put into operation to

have the FIT price of up to 8.5 cents/kWh for onshore wind power and 9.35 cents/kWh for offshore one.

There are still more than 10 GW that have been included in the revised PDP 7 but not being operational

this year. In addition, according to the draft PDP 8, wind power capacity in 2045 will reach 60 GW,

accounting for 20% of the total power capacity. The draft extension of the FIT price for wind power

after 2021 is still attractive, creating motivation for investors to continue investing in the wind power

sector, especially nearshore wind power projects.

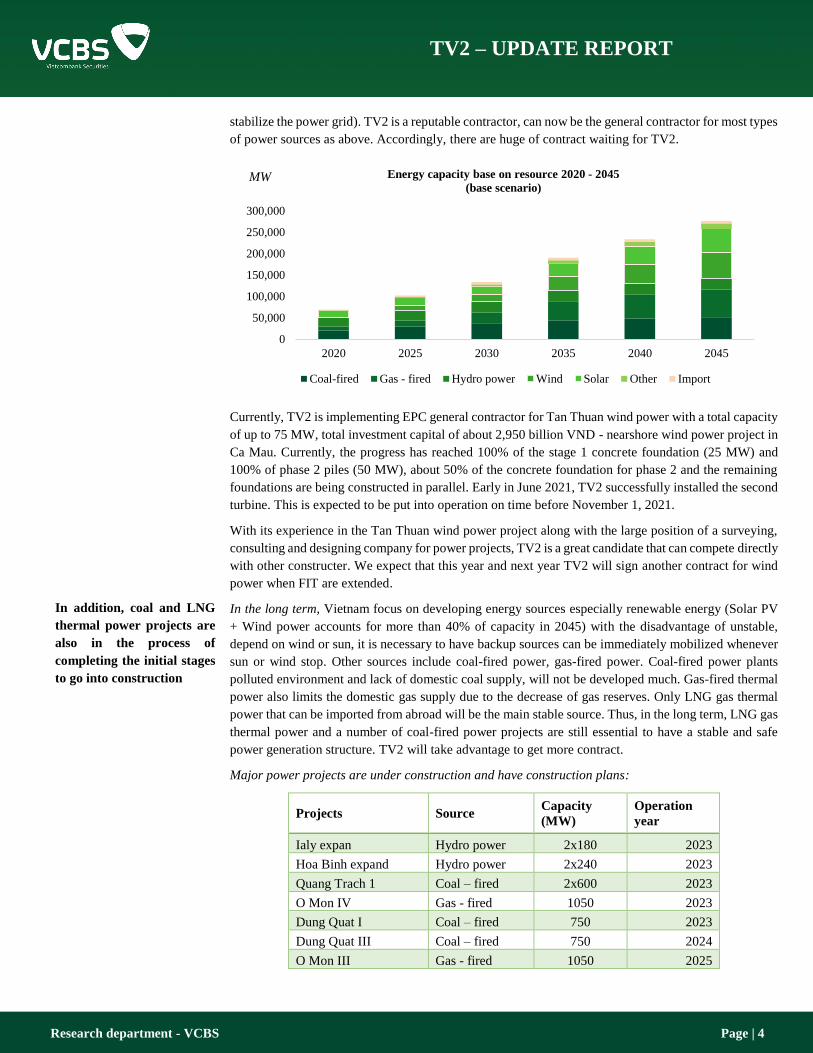

In terms of total power capacity, according to the draft PDP 8, the total capacity will grow at more than

5.7% in the period from 2020 to 2045 with the largest growth coming from renewable energy such as

wind power, solar power and both Gas-fired thermal power (an indispensable source of electricity to

Singed in 2019 Signed 2020 MW

Research department - VCBS Page | 4

TV2 – UPDATE REPORT

In addition, coal and LNG

thermal power projects are

also in the process of

completing the initial stages

to go into construction

stabilize the power grid). TV2 is a reputable contractor, can now be the general contractor for most types

of power sources as above. Accordingly, there are huge of contract waiting for TV2.

Currently, TV2 is implementing EPC general contractor for Tan Thuan wind power with a total capacity

of up to 75 MW, total investment capital of about 2,950 billion VND - nearshore wind power project in

Ca Mau. Currently, the progress has reached 100% of the stage 1 concrete foundation (25 MW) and

100% of phase 2 piles (50 MW), about 50% of the concrete foundation for phase 2 and the remaining

foundations are being constructed in parallel. Early in June 2021, TV2 successfully installed the second

turbine. This is expected to be put into operation on time before November 1, 2021.

With its experience in the Tan Thuan wind power project along with the large position of a surveying,

consulting and designing company for power projects, TV2 is a great candidate that can compete directly

with other constructer. We expect that this year and next year TV2 will sign another contract for wind

power when FIT are extended.

In the long term, Vietnam focus on developing energy sources especially renewable energy (Solar PV

+ Wind power accounts for more than 40% of capacity in 2045) with the disadvantage of unstable,

depend on wind or sun, it is necessary to have backup sources can be immediately mobilized whenever

sun or wind stop. Other sources include coal-fired power, gas-fired power. Coal-fired power plants

polluted environment and lack of domestic coal supply, will not be developed much. Gas-fired thermal

power also limits the domestic gas supply due to the decrease of gas reserves. Only LNG gas thermal

power that can be imported from abroad will be the main stable source. Thus, in the long term, LNG gas

thermal power and a number of coal-fired power projects are still essential to have a stable and safe

power generation structure. TV2 will take advantage to get more contract.

Major power projects are under construction and have construction plans:

Projects Source Capacity

(MW)

Operation

year

Ialy expan Hydro power 2x180 2023

Hoa Binh expand Hydro power 2x240 2023

Quang Trach 1 Coal – fired 2x600 2023

O Mon IV Gas - fired 1050 2023

Dung Quat I Coal – fired 750 2023

Dung Quat III Coal – fired 750 2024

O Mon III Gas - fired 1050 2025

0

50,000

100,000

150,000

200,000

250,000

300,000

2020 2025 2030 2035 2040 2045

Energy capacity base on resource 2020 - 2045

(base scenario)

Coal-fired Gas - fired Hydro power Wind Solar Other Import

MW

Research department - VCBS Page | 5

TV2 – UPDATE REPORT

Tri An expand Hydro power 200 2025

Quang Trach II Coal – fired 2x600 2025

Nhon Trach 3&4

Gas – fired

(LNG) 2x750 2023 – 2025

LNG Long Sơn

Gas – fired

(LNG) 3.600 2025 – 2026

Source: EVN, VCBS

TV2 is currently carrying out procedures to invest in Long Son LNG thermal power plant with other

partners and may have a component contract to construct this project. This project has a total capacity

of up to 3,600 MW and is in the process of completing investment procedures.

On the other hand, BOT Quang Tri I coal – fire thermal power which TV2 is one of main EPC contractor

have been pending because the BOT law has expired on December 31, 2020, but the investor (EGATi)

has not yet established a BOT company in Vietnam, so it cannot start construction in 2021. ..

In 2020, the FIT price for Solar PV has expired and face a significantly growth of Solar PV with nearly

18,000 MWp, accounting for nearly 25% of total power capacity. However, it wouldn’t extend, so in

2021 there is no contract for Solar PV. Meanwhile, in the same period, the company recorded nearly

VND 2,300 billion in revenue from Solar PV only within Q3 and Q4.2020. Thus, the possibility of

revenue growth this year faces a lot of pressure.

Consultin, surveying and

design is the traditional

segment and the backbone

of the whole system and

brings stable revenue.

TV2 is one of the most famous names in consulting, grid planning, surveying and designing power

project. Projects from the parent company (EVN with 51% stake) will be given priority over other units.

Survey activities, pre-feasibility and feasibility reports, dam safety assessment, environmental impact,

etc. will still bring stable revenue to TV2.

By being exposed to projects at the first stage, TV2 can access high potential project for investment.

Therefore, the importance of consulting, surveying and designing fields is very significant, creating an

abundant source of work/projects for other fields such as EPC general contractor, project investment.

Project completed in 2020: Thermal power plant: Dung Quat I, III, Son My 3.1 thermal power plant,

Pre-FS Long Son LNG thermal power plant 1, Long An thermal power plant I – II, Vung Ang 3 thermal

power plant, bidding documents for thermal power plant Nhon Trach 3 – 4. Currently implementing FS

for Long An Thermal Power Plant I – II. Executing PMC of Song Hau 2 thermal power project; Establish

FS of hydropower plants such as: Tri An Extension, Thac Mo Extension, Da Nhim Extension, Dak Mi

2, Bao Lam, Thac Ba 2 and 500 kV transmission lines.

Revenue reach VND 100 – 150 billion/year with high GPM up to 20%.

Investment in power

projects will be the main

driving force for the

company to increase its

scale.

This is one of the three spearheads the company is aiming for in the near future. With the advantages

from the above-mentioned consulting, surveying and designing fields, TV2 can easily access high-

efficiency projects for investment. From this investment, TV2 also has a large source of work for the

construction segment, and O&M also.

Research department - VCBS Page | 6

TV2 – UPDATE REPORT

Projects in timeline:

Projects Ownership Total investment

(VND bil)

Operation

year

Vinh Tan electricity center

Solar PV 100% 106.3 2019

Son My 3.1 Solar PV 25% 87.4 2019

Tan Thuan Wind power 25% 91.55 20211

Thac Ba hydro power expand 45% 5.4 20232

Biomass Hau Giang 25% N/a 2023

Gas – fired (LND) Long Son N/a N/a n/a

Source: TV2, VCBS

02 Solar PV project operated in 2019 with high efficiency of 9.35 cent/kWh within 20 years:

The Vinh Tan Power Center Solar PV, 100% owned by TV2 100% with a capacity of 6.2 MWp, is

considered quite successful with an estimated IRR of about 18% - 20%. Although the business results

are still low (EAT in 2020 is -1.33 billion VND, but because TV2 implements fast depreciation in 5 -

5.5 years compared to the project life of 20 years. Annual cash flow account for 18-21 billion dong,

expected to pay back without discount within 5.5 years. In 2020, although Binh Thuan is the place where

many projects are deflated, this project is almost not deflated due to its efficient operation.

Son My 3.1 Solar PV (25% stake of TV2). Annual revenue reach nearly 180 billion VND, equivalent

to 85 - 90 million kWh/year. 2020 is the first year this project pays dividends to TV2 with the amount

of VND 4.37 billion. This project is expected to bring a steady increase in income in the future while

reducing debt and financial expense. According to TV2, this project has 02 connecting lines to national

grid, so it is not affected by the overload. According to enterprises, the IRR of this project is over 20%.

About Tan Thuan wind power. According to our calculations, IRR can reach over 18% due to very

good selling price, up to 9.35 cents/kWh – applicable for offshore wind power projects. However, this

is only a nearshore project, so the installation cost will be much lower than offshore projects. According

to our calculation installation cost is equal to onshore wind power projects. The only difficulty of the

project is the water level and waves during construction. However, about simpler construction methods

such as: Pressing concrete piles then fill the foundation by concrete, without having to level or dig the

foundation like onshore wind power. The transportation is also simpler, it is not necessary to make the

access road to the wind tower, only need to put the material on the barge, pull it to the construction site,

install it, and do not have to dismantle the crane when moving to another wind power pylon.

We estimate that the capacity factor is up to more than 40%, bringing in annual revenue of about VND

500 - 550 billion/year and cash flow of more than VND 400 billion/year when the whole project comes

into operation. TV2 currently owns 25% of this project.

This project is expected to be profitable right after it is put into operation due to its good price and

location with a steady wind with an average speed of up to 7 m/s – 8 m/s.

The remaining projects are in the early stages, so they will not contribute revenue in the next 2 years.

1 Plan 2 Plan

Research department - VCBS Page | 7

TV2 – UPDATE REPORT

All projects invested are accounted by using the cost method, so profits will only be generated when

the joint venture/associate pays dividends, so the profits in the early stages of these projects will not

reflect reflect the true value of those investments.

EVN divest plan will help

TV2’s operation without

limited

According to sharing from enterprises and EVN, TV2 has proposed to reduce EVN's ownership from

51% to about 30%. It is expected that this will be included in the divestment plan for the period 2021 -

2025 so that TV2 can operate better, avoid barriers to bidding law and be more proactive in business. If

the divestment plan is successful, TV2 will have more autonomy in business matters, while still

benefiting from projects inside and outside EVN to ensure continuous work and create new

breakthroughs in the future. However, in our opinion, the divestment plan will take a long time, going

through many complicated processes, so in the short term it is not a catalist to help TV2 increase its

price.

VALUATION

We chose the method of some of the parts (SOTP) to valuate each segment of TV2 because of its different properties. O&M services

and consulting - survey - design - construction general contractor segment use P/E method, power source development investment

segment uses discounted cash flow (DCF) method.

O&M service Assumptions:

- O&M service revenue without replacement cost is about 7 USD/kW/year or 3.7% - 4.0% of power

generation revenue for solar pv.

- O&M service revenue for wind power reach nearl 11 USD/kW/year or 3.5% – 4.0% of power

generation revenue.

- O&M service revenue for Duyen Hai 2 thermal power account to VND 20 billion/year.

- After 2021, when more than 3 GW – 5GW of wind power is put into operation, TV2 can sign more

O&M contracts for wind power plants.

We estimate O&M service revenue reach VND 185,8 billion in 2021 and NPAT of VND 47.5 billion.

EPS achieve VND 1,320.

The service will bring steady growth in revenue with high efficiency depending on how to operate to

maximize the generating capacity. In addition, in our opinion, the revenue and profit of this segment in

the coming years will grow by about 20% - 30%/year. Therefore, we choose a P/E of about 10x for this

segment (PEG is only 0.3 – 0.5).

As a result, fair value for O&M service as below:

Fair value/share = 10 x 1,320 = VND 13,200 per share.

Consulting, surveying,

construction + mechanics

We use the P/E comparison method to evaluate the consulting, surveying, design and EPC general

contractors due to the volatility of the project progress and high dependence on the back log and new

sign contract value.

Research department - VCBS Page | 8

TV2 – UPDATE REPORT

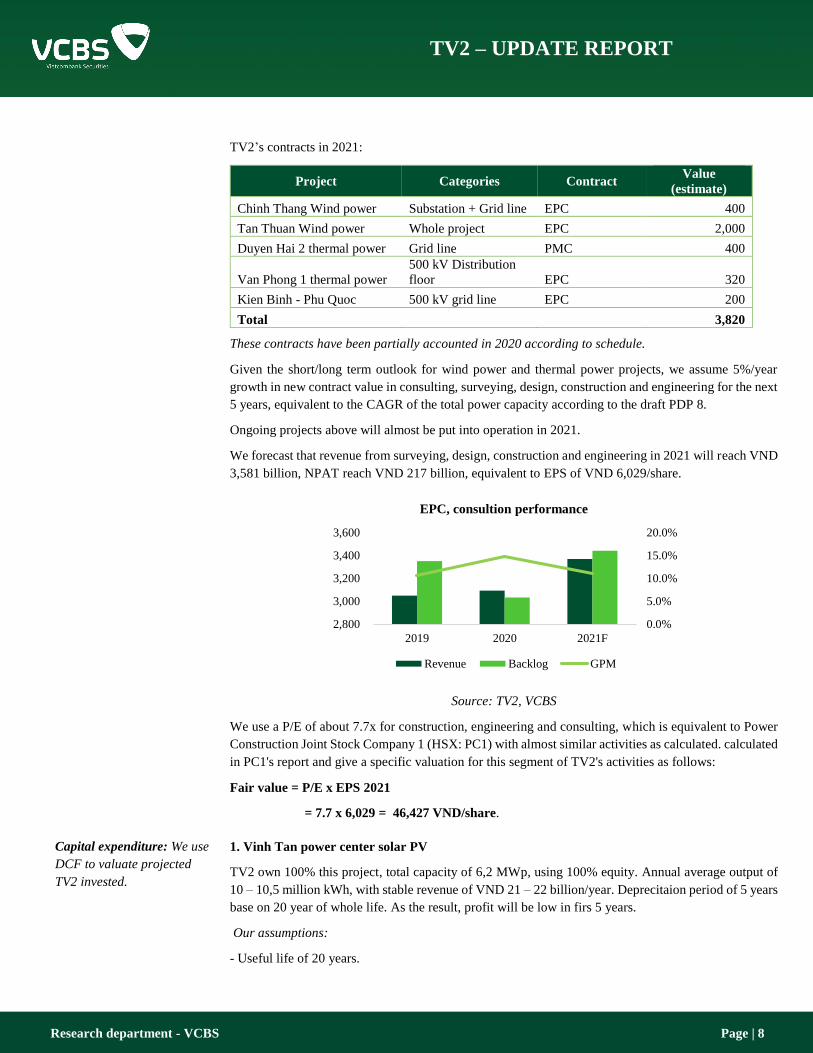

TV2’s contracts in 2021:

Project Categories Contract Value

(estimate)

Chinh Thang Wind power Substation + Grid line EPC 400

Tan Thuan Wind power Whole project EPC 2,000

Duyen Hai 2 thermal power Grid line PMC 400

Van Phong 1 thermal power

500 kV Distribution

floor EPC 320

Kien Binh - Phu Quoc 500 kV grid line EPC 200

Total 3,820

These contracts have been partially accounted in 2020 according to schedule.

Given the short/long term outlook for wind power and thermal power projects, we assume 5%/year

growth in new contract value in consulting, surveying, design, construction and engineering for the next

5 years, equivalent to the CAGR of the total power capacity according to the draft PDP 8.

Ongoing projects above will almost be put into operation in 2021.

We forecast that revenue from surveying, design, construction and engineering in 2021 will reach VND

3,581 billion, NPAT reach VND 217 billion, equivalent to EPS of VND 6,029/share.

Source: TV2, VCBS

We use a P/E of about 7.7x for construction, engineering and consulting, which is equivalent to Power

Construction Joint Stock Company 1 (HSX: PC1) with almost similar activities as calculated. calculated

in PC1's report and give a specific valuation for this segment of TV2's activities as follows:

Fair value = P/E x EPS 2021

= 7.7 x 6,029 = 46,427 VND/share.

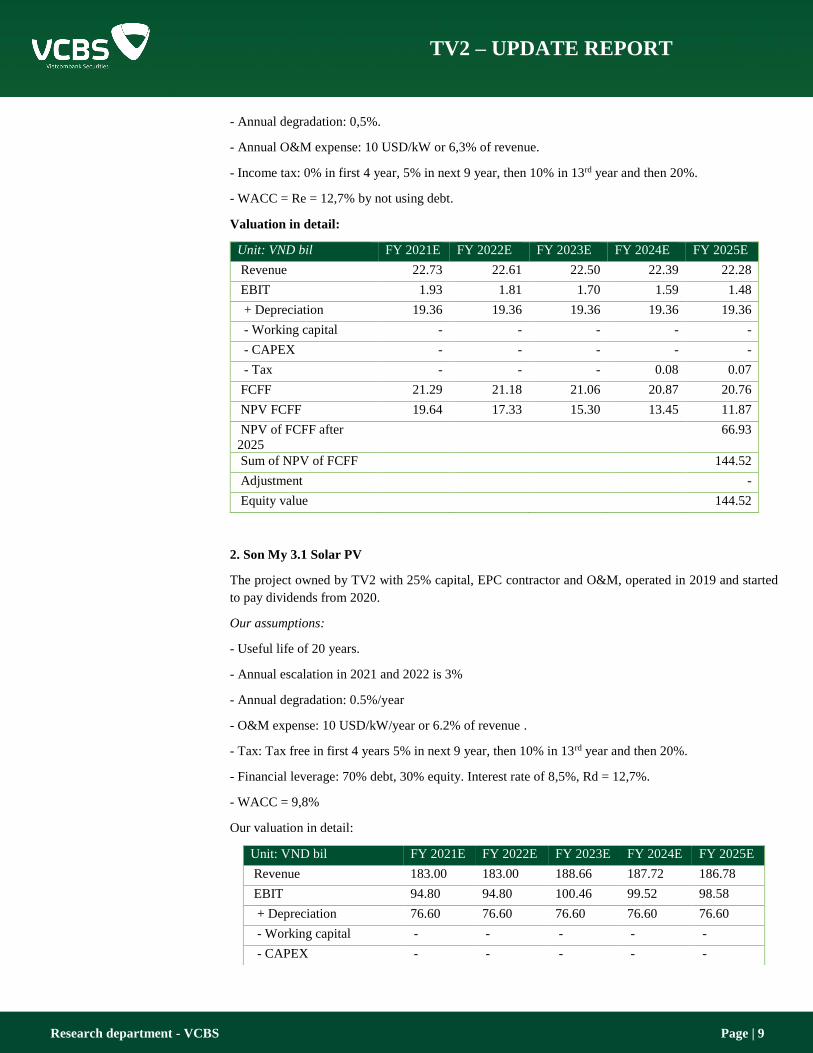

Capital expenditure: We use

DCF to valuate projected

TV2 invested.

1. Vinh Tan power center solar PV

TV2 own 100% this project, total capacity of 6,2 MWp, using 100% equity. Annual average output of

10 – 10,5 million kWh, with stable revenue of VND 21 – 22 billion/year. Deprecitaion period of 5 years

base on 20 year of whole life. As the result, profit will be low in firs 5 years.

Our assumptions:

- Useful life of 20 years.

0.0%

5.0%

10.0%

15.0%

20.0%

2,800

3,000

3,200

3,400

3,600

2019 2020 2021F

EPC, consultion performance

Revenue Backlog GPM

Research department - VCBS Page | 9

TV2 – UPDATE REPORT

- Annual degradation: 0,5%.

- Annual O&M expense: 10 USD/kW or 6,3% of revenue.

- Income tax: 0% in first 4 year, 5% in next 9 year, then 10% in 13rd year and then 20%.

- WACC = Re = 12,7% by not using debt.

Valuation in detail:

Unit: VND bil FY 2021E FY 2022E FY 2023E FY 2024E FY 2025E

Revenue 22.73 22.61 22.50 22.39 22.28

EBIT 1.93 1.81 1.70 1.59 1.48

+ Depreciation 19.36 19.36 19.36 19.36 19.36

- Working capital - - - - -

- CAPEX - - - - -

- Tax - - - 0.08 0.07

FCFF 21.29 21.18 21.06 20.87 20.76

NPV FCFF 19.64 17.33 15.30 13.45 11.87

NPV of FCFF after

2025

66.93

Sum of NPV of FCFF 144.52

Adjustment -

Equity value 144.52

2. Son My 3.1 Solar PV

The project owned by TV2 with 25% capital, EPC contractor and O&M, operated in 2019 and started

to pay dividends from 2020.

Our assumptions:

- Useful life of 20 years.

- Annual escalation in 2021 and 2022 is 3%

- Annual degradation: 0.5%/year

- O&M expense: 10 USD/kW/year or 6.2% of revenue .

- Tax: Tax free in first 4 years 5% in next 9 year, then 10% in 13rd year and then 20%.

- Financial leverage: 70% debt, 30% equity. Interest rate of 8,5%, Rd = 12,7%.

- WACC = 9,8%

Our valuation in detail:

Unit: VND bil FY 2021E FY 2022E FY 2023E FY 2024E FY 2025E

Revenue 183.00 183.00 188.66 187.72 186.78

EBIT 94.80 94.80 100.46 99.52 98.58

+ Depreciation 76.60 76.60 76.60 76.60 76.60

- Working capital - - - - -

- CAPEX - - - - -

Research department - VCBS Page | 10

TV2 – UPDATE REPORT

- Tax - - - 2.486 2.665

FCFF 171.40 171.40 177.06 173.64 172.52

NPV FCFF 160.94 146.63 138.00 121.52 110.14

NPV of FCFF after 2025 759.57

Sum of NPV of FCFF 1436.80

Adjustment (745.73)

Equity value 691.07

TV2 ownership 25%

Value for TV2 172.77

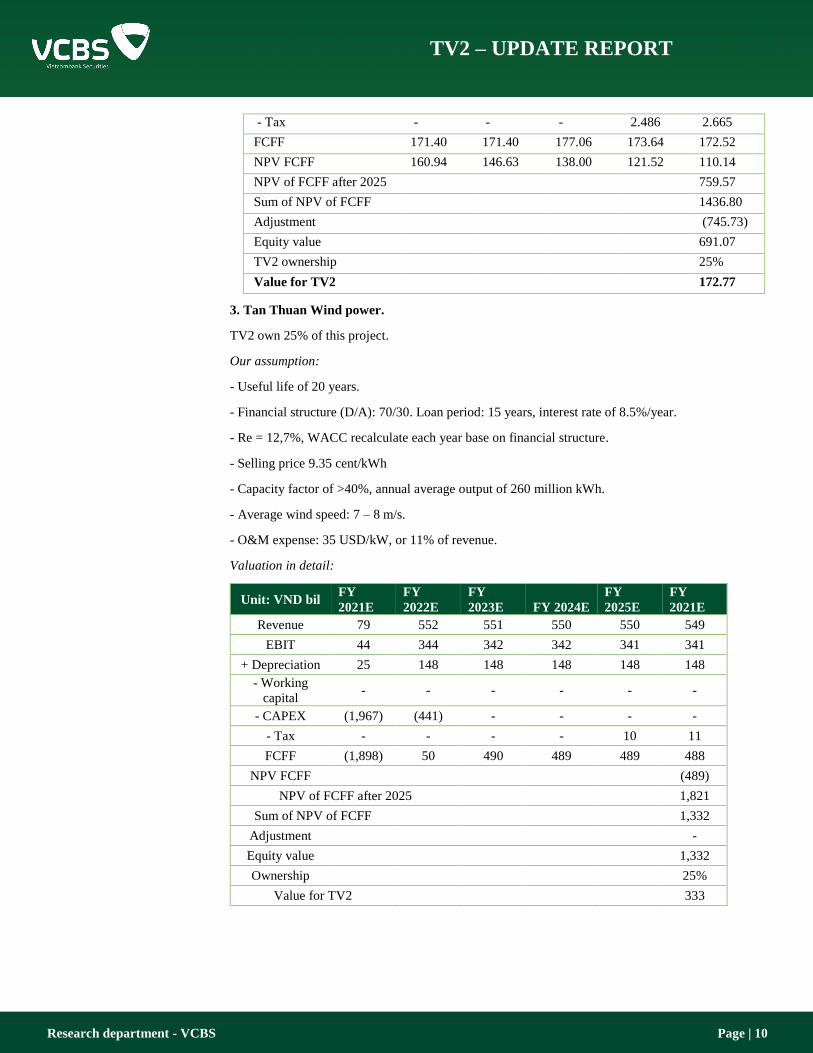

3. Tan Thuan Wind power.

TV2 own 25% of this project.

Our assumption:

- Useful life of 20 years.

- Financial structure (D/A): 70/30. Loan period: 15 years, interest rate of 8.5%/year.

- Re = 12,7%, WACC recalculate each year base on financial structure.

- Selling price 9.35 cent/kWh

- Capacity factor of >40%, annual average output of 260 million kWh.

- Average wind speed: 7 – 8 m/s.

- O&M expense: 35 USD/kW, or 11% of revenue.

Valuation in detail:

Unit: VND bil FY

2021E

FY

2022E

FY

2023E FY 2024E

FY

2025E

FY

2021E

Revenue 79 552 551 550 550 549

EBIT 44 344 342 342 341 341

+ Depreciation 25 148 148 148 148 148

- Working

capital - - - - - -

- CAPEX (1,967) (441) - - - -

- Tax - - - - 10 11

FCFF (1,898) 50 490 489 489 488

NPV FCFF (489)

NPV of FCFF after 2025 1,821

Sum of NPV of FCFF 1,332

Adjustment -

Equity value 1,332

Ownership 25%

Value for TV2 333

Research department - VCBS Page | 11

TV2 – UPDATE REPORT

Sum of valuation:

Project

Value (VND

billion)

Value per share

(VND)

Vinh Tan PC Solar PV 145 4,013

Son My 3.1 Solar PV 173 4,797

Tan Thuan Wind power 333 9,249

Total 650 18,059

In addition, TV2 also invests in projects such as: Owning 45% of Thac Ba hydropower plant expansion

(capacity of 18.9 MW) and 25% of biomass power (20 MW) in Hau Giang. These 2 projects are expected

to ground breaking this year and are expected to operate in 2023. However, these projects are in legal

procedures completing stage, so we have not included these projects in their valuation.

Sum of valuation Segments Valuation

method

Value

(VND bil)

Value/share

(VND)

EPC,

Mechanism,

Consulting

P/E

1.672

46,427

Capital

expenditure FCFF

650

18,059

O&M service P/E

476

13,212

Total 2.798

77.697

Upside 53,0%

We recommend BUY for TV2 with a target price in 2021-2022 of VND 77,700/share, offering an upside

of 53.0% compared to the closing price on June 3nd, 2021.

INVESTMENT RISKS

(1) Bad weather will slow down the project progress. In 2021, the project that contributes the most

revenue is the Tan Thuan wind power in nearshore area in Ca Mau. This area will enter the

monsoon season from October every year onwards. Strong winds will make the sea surface very

rough, making it impossible for continuous construction. If the project is behind schedule up to

this point, there is impossible of COD in time, reducing the project's efficiency. Thus, both

construction revenue and profit shared from this project will not meet our plan and our estimate.

(2) Steel prices have increased sharply in recent times, affecting the GPM of construction

companies. However, whenever signing the contract, TV2 has signed with the supplier as well.

EPC general contractor activities also often re-sign prices with subcontractors, so they are not

affected much.

Research department - VCBS Page | 12

TV2 – UPDATE REPORT

Unit: VND billion

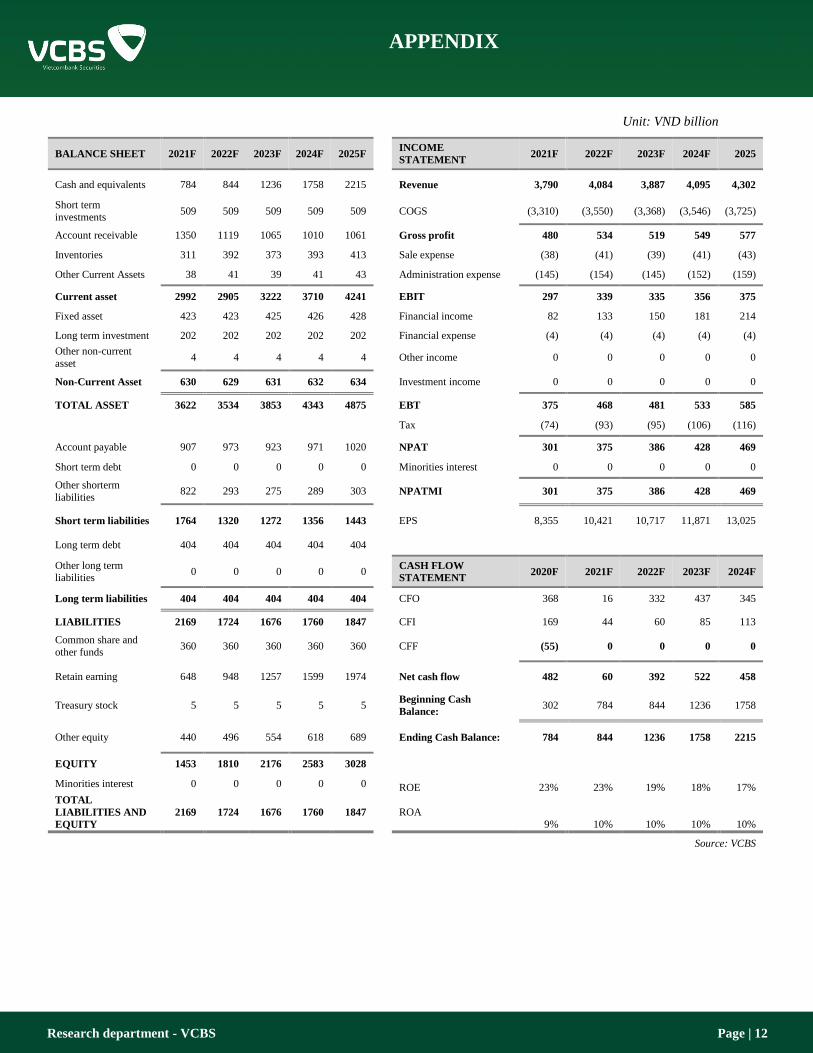

BALANCE SHEET 2021F 2022F 2023F 2024F 2025F

INCOME

STATEMENT 2021F 2022F 2023F 2024F 2025

Cash and equivalents 784 844 1236 1758 2215

Revenue 3,790 4,084 3,887 4,095 4,302

Short term

investments 509 509 509 509 509

COGS (3,310) (3,550) (3,368) (3,546) (3,725)

Account receivable 1350 1119 1065 1010 1061 Gross profit 480 534 519 549 577

Inventories 311 392 373 393 413 Sale expense (38) (41) (39) (41) (43)

Other Current Assets 38 41 39 41 43 Administration expense (145) (154) (145) (152) (159)

Current asset 2992 2905 3222 3710 4241 EBIT 297 339 335 356 375

Fixed asset 423 423 425 426 428 Financial income 82 133 150 181 214

Long term investment 202 202 202 202 202 Financial expense (4) (4) (4) (4) (4)

Other non-current

asset 4 4 4 4 4

Other income 0 0 0 0 0

Non-Current Asset 630 629 631 632 634 Investment income 0 0 0 0 0

TOTAL ASSET 3622 3534 3853 4343 4875 EBT 375 468 481 533 585

Tax (74) (93) (95) (106) (116)

Account payable 907 973 923 971 1020 NPAT 301 375 386 428 469

Short term debt 0 0 0 0 0 Minorities interest 0 0 0 0 0

Other shorterm

liabilities 822 293 275 289 303

NPATMI 301 375 386 428 469

Short term liabilities 1764 1320 1272 1356 1443

EPS 8,355 10,421 10,717 11,871 13,025

Long term debt 404 404 404 404 404

Other long term liabilities

0 0 0 0 0

CASH FLOW

STATEMENT 2020F 2021F 2022F 2023F 2024F

Long term liabilities 404 404 404 404 404 CFO 368 16 332 437 345

LIABILITIES 2169 1724 1676 1760 1847 CFI 169 44 60 85 113

Common share and

other funds 360 360 360 360 360

CFF (55) 0 0 0 0

Retain earning 648 948 1257 1599 1974

Net cash flow 482 60 392 522 458

Treasury stock 5 5 5 5 5

Beginning Cash

Balance: 302 784 844 1236 1758

Other equity 440 496 554 618 689

Ending Cash Balance: 784 844 1236 1758 2215

EQUITY 1453 1810 2176 2583 3028

Minorities interest 0 0 0 0 0 ROE 23% 23% 19% 18% 17%

TOTAL

LIABILITIES AND

EQUITY

2169 1724 1676 1760 1847

ROA 9% 10% 10% 10% 10%

Source: VCBS

APPENDIX

Research department - VCBS Page | 13

TV2 – UPDATE REPORT

DISCLAIMER

This report is designed to provide updated information on the fixed-income, including bonds, interest rates, some other related. The VCBS analysts

exert their best efforts to obtain the most accurate and timely information available from various sources, including information pertaining to market

prices, yields and rates. All information stated in the report has been collected and assessed as carefully as possible.

It must be stressed that all opinions, judgments, estimations and projections in this report represent independent views of the analyst at the date of

publication. Therefore, this report should be best considered a reference and indicative only. It is not an offer or advice to buy or sell or any actions

related to any assets. VCBS and/or Departments of VCBS as well as any affiliate of VCBS or affiliate that VCBS belongs to or is related to

(thereafter, VCBS), provide no warranty or undertaking of any kind in respect to the information and materials found on, or linked to the repor t and

no obligation to update the information after the report was released. VCBS does not bear any responsibility for the accuracy of the material posted

or the information contained therein, or for any consequences arising from its use, and does not invite or accept reliance being placed on any

materials or information so provided.

This report may not be copied, reproduced, published or redistributed for any purpose without the written permission of an authorized representative

of VCBS. Please cite sources when quoting. Copyright 2012 Vietcombank Securities Company.

CONTACT INFORMATION

Any further information, please contact as below:

Tran Minh Hoang Ly Hoang Anh Thi Trinh Van Ha

Head of research

Deputy head of research

Equity research

VIETCOMBANK SECURITIES CORPORATION

http://www.vcbs.com.vn

Headquarters Hanoi 12rd & 17th Floor, Vietcombank Building, No. 198 Tran Quang Khai, Hoan Kiem District, Hanoi,

Tel: (84-24) -393675- Ext: 18/19/20

Ho Chi Minh branch 1st & 7th Floor, Green Star Building, No. 70 Pham Ngoc Thach, Ward 6, District 3, City. Ho Chi Minh

Tel: (84-28)-3820799 - Ext: 104/106

Da Nang branch 12th floor, 135 Nguyen Van Linh, Vinh Trung Ward, Thanh Khe District, Da Nang

Tel: (84-236) -33888991 - Ext: 12/13

Can Tho Branch 1st floor, Vietcombank Can Tho Building, 7 Hoa Binh, Ninh Kieu District, Can Tho

Tel: (84-710) -3750888

Phu My Hung Transaction Office Lawrence Sting Building, No. 801 Nguyen Luong Bang, Phu My Hung Urban Area, District 7, City. Ho Chi Minh

Tel: (84-28)-54136573

Giang Vo Transaction Office 1st floor, C4 Giang Vo Building, Giang Vo Ward, Ba Dinh District, Hanoi.

Tel: (+84-24) 3726 5551

An Giang Representative Office 6th floor, Nguyen Hue Building, 9/9 Tran Hung Dao, My Xuyen Ward, Long Xuyen, An Giang

Tel: (84-76) -3949841

Representative Office of Dong Nai F240-F241 Vo Thi Sau Street, Quarter 7, Thong Nhat Ward, City. Bien Hoa, Dong Nai

Tel: (84-61)-3918812

Representative office of Vung Tau Ground floor, 27 Le Loi Street, City. Vung Tau, Ba Ria - Vung Tau

Tel: (84-64)-3513974/75/76/77/78

Hai Phong Representative Office 2nd floor, 11 Hoang Dieu Street, Minh Khai Ward, Hong Bang District, Hai Phong

Tel: (+84-31) 382 1630

DISCLAIMER

Related Documents