Potential Nordic Issuers 2018 15 December 2017 Investment Research www.danskebank.com/CI This document is intended for institutional investors and is not subject to all the independence and disclosure standards applicable to debt research reports prepared for retail investors. Senior Analyst Mads Rosendal +45 40 44 67 56 [email protected] Important disclosures and certifications are contained from page 20 of this report.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Potential Nordic Issuers 2018

15 December 2017

Investment Researchwww.danskebank.com/CI

This document is intended for institutional investors and is not subject to all the independence and disclosure standards applicable to debt research

reports prepared for retail investors.

Senior Analyst

Mads Rosendal

+45 40 44 67 56

Important disclosures and certifications are contained from page 20 of this report.

2

Methodology and assumptions

We aim to provide an overview of potential Nordic corporate issuers in 2018.

For the sake of simplicity, we limit ourselves to the Danske Bank DCM Research coverage universe and we

exclude Financials and distressed issuers.

We use a two-tiered approach based on funding surplus (deficit) and upcoming redemptions.

The funding surplus (deficit) is defined as:

– cash and equivalents (including marketable securities) + CFO (E) – capex (E) – ST debt – dividends.

We disregard short-term debt composition and acknowledge that, in many cases, ST debt will be rolled without

issuing bonds (e.g. CPs or deposit funding).

For listed companies, we use Bloomberg consensus estimates for CFO and capex, for unlisted companies we

use Danske Bank DCM Research estimates and company guidance.

Our list of upcoming redemptions is pulled from Bloomberg using <SRCH>GO and picking Nordic corporate

bonds maturing between 15 January 2018 and 30 June 2019. (We have extended the maturity period relative to

previous versions of this research piece due to expectations of high pre-funding levels in 2018.)

To assess the likelihood of replacement, we measure the redemption size (in LCY) relative to total debt.

Disclaimer: due to time constraints, data provided by Bloomberg has not been cross-checked and conclusions

from this analysis are based on the premise that the data provided is correct.

3

Theoretical funding surplus (deficit)*

*Estimated using Bloomberg consensus, and company data. Funding surplus (deficit) defined as: Cash and equivalents + CFO (E) – capital expenditures (E) – dividends – short-term debt

Source: Bloomberg, company data, Danske Bank DCM Research estimates

100%

100%

100%

100%

100%

100%

100%

100%

100%

91%

71%

57%55%

52% 50%

42%39%

37%

31% 30%26%

23%19%

15% 14%

8% 6% 6% 4% 2% 1%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

-2,000

-1,000

0

1,000

2,000

3,000

4,000

EU

Rm

Estimated Funding surplus (deficit) incl. Credit facilities (EURm) Estimated Funding surplus (deficit) ex. Credit facilities (EURm) Theoretical RCF usage (%)

Nordic bond maturities by currency (15/01/2018 - 30/06/2019)*

*Excluding Financials and distressed issuers and limited to names under coverage by Danske Bank DCM Research. Source: Bloomberg SRCH<GO>

5

EUR redemptions

6.3%

2.7%0.8%

18.6%16.5%

4.3%3.7%5.3%

2.7%4.7%

1.5%

12.3%

4.4%4.5%4.3%3.1%

8.4%

44.6%

3.5%

7.7%8.3%

5.1%

17.6%

3.9%

21.7%

5.7%

1.8%1.8%

10.8%

5.8%

2.5%2.3%2.3%

6.2%

10.5%

19.7%

3.8%

15.9%

26.3%

10.7%

2.3%

8.8%11.1%

5.3%

8.8%

11.5%

58.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

0

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

700,000,000

800,000,000

Te

len

or

AS

A (1

5/0

1/2

018)

Volv

o T

reasu

ry A

B (1

9/0

2/2

01

8)

Sto

ra E

nso O

YJ (2

2/0

2/2

018)

TD

C A

/S (2

3/0

2/2

018)

Securita

s A

B (1

4/0

3/2

018)

Sta

tkra

ft A

S (1

5/0

3/2

01

8)

Sto

ra E

nso O

YJ (1

9/0

3/2

018)

SA

TO

Oyj (

20/0

3/2

018)

Volv

o T

reasu

ry A

B (0

3/0

5/2

01

8)

Mets

o O

YJ (1

3/0

5/2

01

8)

Sto

ra E

nso O

YJ (2

3/0

5/2

018)

SK

F A

B (2

5/0

5/2

018)

Vatte

nfa

ll A

B (1

8/0

6/2

018)

Volv

o T

reasu

ry A

B (2

0/0

6/2

01

8)

Neste

Oyj (

29/0

6/2

018

)

Volv

o T

reasu

ry A

B (0

3/0

8/2

01

8)

Fin

na

ir O

YJ (2

9/0

8/2

018)

Kesko

OY

J (1

1/0

9/2

018)

Investo

r A

B

(17/0

9/2

018)

Spon

da O

YJ (0

9/1

0/2

018)

Scania

CV

AB

(2

4/1

0/2

018)

Essity A

B (2

7/1

1/2

018

)

G4S

In

tern

ational F

inan

ce P

LC

…

Volv

o T

reasu

ry A

B (1

2/1

2/2

01

8)

SR

V G

roup O

YJ (1

8/1

2/2

018)

Vatte

nfa

ll A

B (3

1/0

1/2

019)

Ste

na

AB

(0

1/0

2/2

019

)

Ste

na

AB

(0

1/0

2/2

019

)

Te

olli

suu

den V

oim

a O

yj…

Nokia

OY

J (0

4/0

2/2

019)

Scania

CV

AB

(1

3/0

2/2

019)

Volv

o T

reasu

ry A

B (1

3/0

2/2

01

9)

Te

lia C

o A

B

(18/0

2/2

019)

Sto

ra E

nso O

YJ (0

7/0

3/2

019)

Mets

a B

oa

rd O

YJ (1

3/0

3/2

019

)

Atlas C

opco A

B (1

5/0

3/2

019)

AP

Molle

r -

Maers

k A

/S…

Fo

rtum

OY

J (2

0/0

3/2

019)

Ram

irent O

YJ

(21/0

3/2

019)

Sta

tkra

ft A

S (0

2/0

4/2

01

9)

Volv

o T

reasu

ry A

B (0

3/0

4/2

01

9)

Sw

ed

ish M

atc

h A

B (0

3/0

4/2

019)

SS

AB

AB

(1

0/0

4/2

01

9)

SA

TO

Oyj (

16/0

4/2

019)

Ors

ted A

/S (0

7/0

5/2

019)

Kem

ira O

YJ (2

7/0

5/2

019)

St1

Nord

ic O

y (0

4/0

6/2

019)

Red

em

pti

on

am

ou

nt

rela

tive t

o t

ota

l d

eb

t

EU

R

Source: Bloomberg <SRCH>GO

6

SEK redemptions (1 of 3)

1%1%

3%

1%

4%

2%

0%

7%

1%1%0%

5%

3%

2%

0%

9%

1%0%

6%

2%

5%

3%

6%

4%

1%

21%

11%

10%

1%

3%

0%0%0%

1%1%

10%

3%3%

7%

2%

1%

0%1%

3%

1%1%

9%

0%

5%

10%

15%

20%

25%

0

5,000,000,000

10,000,000,000

15,000,000,000

20,000,000,000

25,000,000,000

30,000,000,000

35,000,000,000

Vasakro

na

n A

B (1

7/0

1/2

01

8)

Vasakro

na

n A

B (2

2/0

1/2

01

8)

Sw

ed

ish M

atc

h A

B (0

1/0

2/2

018)

Sw

ed

ish M

atc

h A

B (0

1/0

2/2

018)

Sw

ed

avia

AB

(0

5/0

2/2

018)

Vasakro

na

n A

B (1

4/0

2/2

01

8)

Vasakro

na

n A

B (2

0/0

2/2

01

8)

AP

Molle

r -

Maers

k A

/S (2

6/0

2/2

01

8)

AP

Molle

r -

Maers

k A

/S (2

6/0

2/2

01

8)

Volv

o T

reasu

ry A

B (2

6/0

2/2

01

8)

Volv

o T

reasu

ry A

B (2

6/0

2/2

01

8)

Klo

ve

rn A

B

(04/0

3/2

018)

Akeliu

s R

esid

ential P

ropert

y A

B…

Volv

o T

reasu

ry A

B (0

9/0

3/2

01

8)

Volv

o T

reasu

ry A

B (0

9/0

3/2

01

8)

Skanska F

inancia

l S

erv

ices A

B…

Hem

so F

astig

hets

AB

(1

2/0

3/2

018

)

Vasakro

na

n A

B (1

6/0

3/2

01

8)

Fo

rtum

OY

J (2

0/0

3/2

018)

Fo

rtum

OY

J (2

0/0

3/2

018)

Fa

stP

art

ner

AB

(2

1/0

3/2

01

8)

Sta

tne

tt S

F (2

3/0

3/2

018)

Ele

ctr

olu

x A

B

(26/0

3/2

018)

Ele

ctr

olu

x A

B

(26/0

3/2

018)

Caste

llum

AB

(2

6/0

3/2

01

8)

Bill

eru

dK

ors

nas A

B (2

7/0

3/2

01

8)

Bill

eru

dK

ors

nas A

B (2

7/0

3/2

01

8)

Core

m P

ropert

y G

roup A

B…

SS

AB

AB

(0

3/0

4/2

01

8)

Klo

ve

rn A

B

(04/0

4/2

018)

Vasakro

na

n A

B (0

4/0

4/2

01

8)

Meda

AB

(0

5/0

4/2

018

)

Volv

o T

reasu

ry A

B (1

3/0

4/2

01

8)

Hem

so F

astig

hets

AB

(1

7/0

4/2

018

)

Hem

so F

astig

hets

AB

(1

7/0

4/2

018

)

Jern

huse

n A

B (2

3/0

4/2

01

8)

Wih

lbo

rgs F

astighete

r A

B…

Jern

huse

n A

B (2

3/0

4/2

01

8)

Getinge A

B (2

1/0

5/2

018)

Getinge A

B (2

1/0

5/2

018)

Fa

stighets

AB

Bald

er

(21

/05/2

01

8)

Vasakro

na

n A

B (2

1/0

5/2

01

8)

Sand

vik

AB

(2

3/0

5/2

018)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Vasakro

na

n A

B (2

8/0

5/2

01

8)

Volv

o T

reasu

ry A

B (3

0/0

5/2

01

8)

Sw

ed

avia

AB

(0

4/0

6/2

018)

Rela

tive t

o t

ota

l d

eb

t

SE

K

Source: Bloomberg <SRCH>GO

7

SEK redemptions (2 of 3)

6%5%

3%1%1%1%1%

2%1%

19%

1%1%2%1%0%

21%

0%

2%2%4%3%2%

7%

1%2%

4%3%

1%1%1%0%

10%

2%0%

6%

2%1%

17%

7%

2%0%

50%

1%3%

1%2%4%

0%

10%

20%

30%

40%

50%

60%

0

5,000,000,000

10,000,000,000

15,000,000,000

20,000,000,000

25,000,000,000

Husqvarn

a A

B (0

4/0

6/2

018)

Arl

a F

oods F

inance A

/S…

Arl

a F

oods F

inance A

/S…

Caste

llum

AB

(0

4/0

6/2

01

8)

Vasakro

na

n A

B (0

7/0

6/2

01

8)

Volv

o T

reasu

ry A

B (1

3/0

6/2

01

8)

Volv

o T

reasu

ry A

B (1

3/0

6/2

01

8)

Hem

so F

astig

hets

AB

(1

4/0

6/2

018

)

Hem

so F

astig

hets

AB

(1

5/0

6/2

018

)

Nynas A

B (2

6/0

6/2

018)

Sand

vik

AB

(2

2/0

8/2

018)

Vasakro

na

n A

B (2

3/0

8/2

01

8)

Volv

o T

reasu

ry A

B (2

4/0

8/2

01

8)

Volv

o T

reasu

ry A

B (2

4/0

8/2

01

8)

Vasakro

na

n A

B (2

4/0

8/2

01

8)

NC

C T

reasury

AB

(3

0/0

8/2

018)

Vasakro

na

n A

B (1

0/0

9/2

01

8)

Te

olli

suu

den V

oim

a O

yj…

Te

olli

suu

den V

oim

a O

yj…

Hexago

n A

B (1

7/0

9/2

01

8)

Hexago

n A

B (1

7/0

9/2

01

8)

Fo

rtum

Va

rme H

old

ing s

am

agt…

Sw

ed

ish M

atc

h A

B (1

9/0

9/2

018)

Caste

llum

AB

(2

6/0

9/2

01

8)

Caste

llum

AB

(1

0/1

0/2

01

8)

Skanska F

inancia

l S

erv

ices A

B…

Hem

so F

astig

hets

AB

(2

4/1

0/2

018

)

Hem

so F

astig

hets

AB

(2

4/1

0/2

018

)

Vasakro

na

n A

B (2

4/1

0/2

01

8)

Vasakro

na

n A

B (0

2/1

1/2

01

8)

Vasakro

na

n A

B (0

5/1

1/2

01

8)

Fin

gri

d O

YJ (1

9/1

1/2

018)

Jern

huse

n A

B (2

1/1

1/2

01

8)

Scania

CV

AB

(3

0/1

1/2

018)

Vic

toria

Park

AB

(0

3/1

2/2

018)

Scania

CV

AB

(0

3/1

2/2

018)

Scania

CV

AB

(0

3/1

2/2

018)

Saab

AB

(1

0/1

2/2

018)

Saab

AB

(1

0/1

2/2

018)

Vasakro

na

n A

B (1

2/1

2/2

01

8)

Vasakro

na

n A

B (1

8/1

2/2

01

8)

Jefa

st H

old

ing A

B (2

4/0

1/2

019)

Vasakro

na

n A

B (2

4/0

1/2

01

9)

Hem

so F

astig

hets

AB

(2

5/0

1/2

019

)

Hem

so F

astig

hets

AB

(0

4/0

2/2

019

)

Sw

ed

ish M

atc

h A

B (1

5/0

2/2

019)

Wih

lbo

rgs F

astighete

r A

B…

Red

em

pti

on

am

ou

nt

rela

tive t

o t

ota

l d

eb

t

SE

K

Source: Bloomberg <SRCH>GO

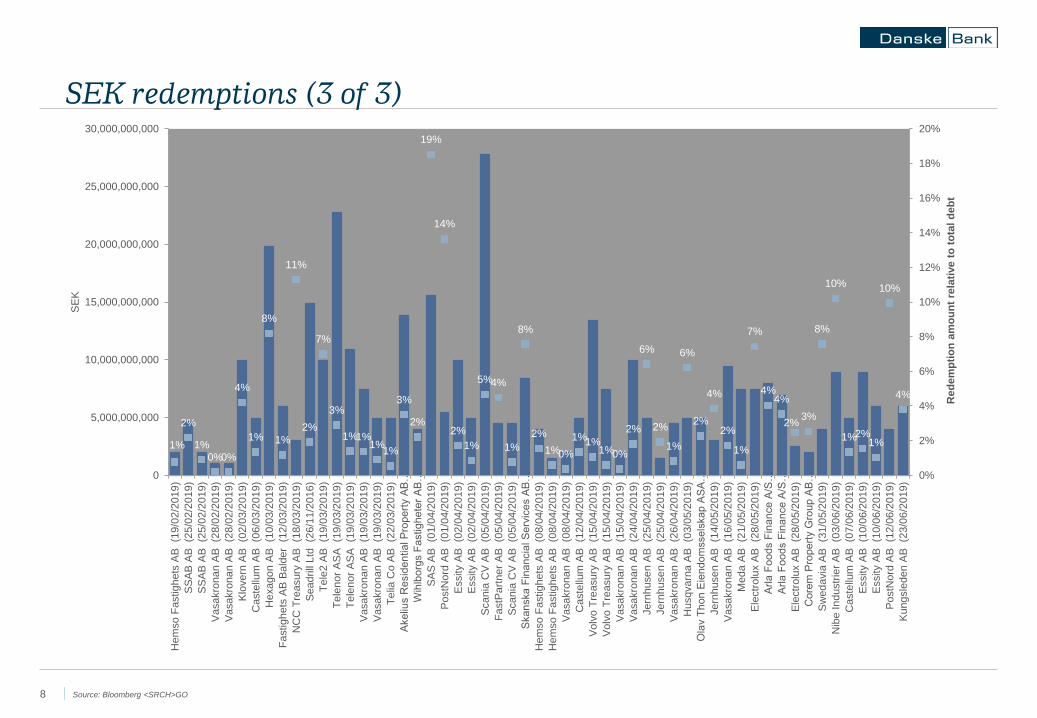

8

SEK redemptions (3 of 3)

1%

2%

1%0%0%

4%

1%

8%

1%

11%

2%

7%

3%

1%1%1%

1%

3%

2%

19%

14%

2%

1%

5%4%

1%

8%

2%

1%0%

1%1%1%0%

2%

6%

2%

1%

6%

2%

4%

2%

1%

7%

4%4%

2%3%

8%

10%

1%2%1%

10%

4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

5,000,000,000

10,000,000,000

15,000,000,000

20,000,000,000

25,000,000,000

30,000,000,000

Hem

so F

astig

hets

AB

(1

9/0

2/2

019

)

SS

AB

AB

(2

5/0

2/2

01

9)

SS

AB

AB

(2

5/0

2/2

01

9)

Vasakro

na

n A

B (2

8/0

2/2

01

9)

Vasakro

na

n A

B (2

8/0

2/2

01

9)

Klo

ve

rn A

B

(02/0

3/2

019)

Caste

llum

AB

(0

6/0

3/2

01

9)

Hexago

n A

B (1

0/0

3/2

01

9)

Fa

stighets

AB

Bald

er

(12

/03/2

01

9)

NC

C T

reasury

AB

(1

8/0

3/2

019)

Sead

rill

Ltd

(2

6/1

1/2

016)

Te

le2

AB

(1

9/0

3/2

019

)

Te

len

or

AS

A (1

9/0

3/2

019)

Te

len

or

AS

A (1

9/0

3/2

019)

Vasakro

na

n A

B (1

9/0

3/2

01

9)

Vasakro

na

n A

B (1

9/0

3/2

01

9)

Te

lia C

o A

B

(22/0

3/2

019)

Akeliu

s R

esid

ential P

ropert

y A

B…

Wih

lbo

rgs F

astighete

r A

B…

SA

S A

B (0

1/0

4/2

01

9)

PostN

ord

AB

(0

1/0

4/2

019)

Essity A

B (0

2/0

4/2

019

)

Essity A

B (0

2/0

4/2

019

)

Scania

CV

AB

(0

5/0

4/2

019)

Fa

stP

art

ner

AB

(0

5/0

4/2

01

9)

Scania

CV

AB

(0

5/0

4/2

019)

Skanska F

inancia

l S

erv

ices A

B…

Hem

so F

astig

hets

AB

(0

8/0

4/2

019

)

Hem

so F

astig

hets

AB

(0

8/0

4/2

019

)

Vasakro

na

n A

B (0

8/0

4/2

01

9)

Caste

llum

AB

(1

2/0

4/2

01

9)

Volv

o T

reasu

ry A

B (1

5/0

4/2

01

9)

Volv

o T

reasu

ry A

B (1

5/0

4/2

01

9)

Vasakro

na

n A

B (1

5/0

4/2

01

9)

Vasakro

na

n A

B (2

4/0

4/2

01

9)

Jern

huse

n A

B (2

5/0

4/2

01

9)

Jern

huse

n A

B (2

5/0

4/2

01

9)

Vasakro

na

n A

B (2

6/0

4/2

01

9)

Husqvarn

a A

B (0

3/0

5/2

019)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Jern

huse

n A

B (1

4/0

5/2

01

9)

Vasakro

na

n A

B (1

6/0

5/2

01

9)

Meda

AB

(2

1/0

5/2

019

)

Ele

ctr

olu

x A

B

(28/0

5/2

019)

Arl

a F

oods F

inance A

/S…

Arl

a F

oods F

inance A

/S…

Ele

ctr

olu

x A

B

(28/0

5/2

019)

Core

m P

ropert

y G

roup A

B…

Sw

ed

avia

AB

(3

1/0

5/2

019)

Nib

e In

dustr

ier

AB

(0

3/0

6/2

019)

Caste

llum

AB

(0

7/0

6/2

01

9)

Essity A

B (1

0/0

6/2

019

)

Essity A

B (1

0/0

6/2

019

)

PostN

ord

AB

(1

2/0

6/2

019)

Kung

sle

den A

B (2

3/0

6/2

019)

Red

em

pti

on

am

ou

nt

rela

tive t

o t

ota

l d

eb

t

SE

K

Source: Bloomberg <SRCH>GO

9

NOK redemptions

1%

4%

2%

13%13%

2%

1%1%

2%2%

4%

2%

4%

14%

2%1%

2%

5%

2%1%

1%

2%2%1%

11%

2%1%

3%3%

1%1%0%

11%

1%

12%

1%

8%

3%3%

9%

2%2%2%

14%

5%

6%8%

2%2%1%1%

6%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

-

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1,800,000,000

2,000,000,000

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Th

on H

old

ing A

S (0

2/0

2/2

018)

Ste

en

& S

trom

AS

(0

8/0

2/2

018)

Poste

n N

org

e A

S

(09/0

2/2

018)

Fe

lleskjo

pet

Ag

ri S

A (1

3/0

2/2

018

)

Ste

en

& S

trom

AS

(2

1/0

2/2

018)

Ste

en

& S

trom

AS

(2

3/0

2/2

018)

Ste

en

& S

trom

AS

(0

8/0

3/2

018)

Sead

rill

Ltd

(1

2/0

3/2

018)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Sto

lt-N

iels

en L

td

(19/0

3/2

018)

Citycon

Tre

asury

BV

(1

9/0

3/2

01

8)

Dfd

s A

/S (2

1/0

3/2

018)

TIN

E S

A (0

4/0

4/2

01

8)

Th

on H

old

ing A

S (2

0/0

4/2

018)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Ste

en

& S

trom

AS

(0

2/0

5/2

018)

Norw

egia

n A

ir S

huttle

AS

A…

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Ste

en

& S

trom

AS

(0

6/0

6/2

018)

Ste

en

& S

trom

AS

(1

2/0

6/2

018)

Walle

niu

s W

ilhelm

sen L

og

istics…

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Norg

esG

rupp

en A

SA

(1

5/0

6/2

01

8)

Th

on H

old

ing A

S (2

7/0

6/2

018)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Th

on H

old

ing A

S (0

3/0

8/2

018)

Ste

en

& S

trom

AS

(0

8/0

8/2

018)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Ste

en

& S

trom

AS

(0

7/0

9/2

018)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Poste

n N

org

e A

S

(21/0

9/2

018)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Ta

llin

k G

rupp A

S (1

8/1

0/2

018)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Nort

h A

tlantic D

rilli

ng L

td…

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Odfjell

SE

(0

3/1

2/2

018)

Bonh

eur

AS

A (1

1/0

2/2

019)

Sta

tkra

ft A

S (1

1/0

2/2

01

9)

Ste

en

& S

trom

AS

(2

1/0

2/2

019)

Fre

d O

lsen

Ene

rgy A

SA

…

Schib

ste

d A

SA

(0

1/0

3/2

019

)

Ship

Fin

an

ce In

tern

ation

al L

td…

Oce

an Y

ield

AS

A (2

6/0

3/2

019)

Walle

niu

s W

ilhelm

sen L

og

istics…

Sta

tne

tt S

F (2

2/0

5/2

019)

Sta

tne

tt S

F (2

2/0

5/2

019)

Vasakro

na

n A

B (1

8/0

6/2

01

9)

Ola

v T

hon E

iendom

ssels

kap A

SA

…

Red

em

pti

on

am

ou

nt

rela

tive t

o t

ota

l d

eb

t

NO

K

Source: Bloomberg <SRCH>GO

10

Other currency redemptions (USD, JPY, GBP)

12%

2% 2%

28%

4%5%

2%

22%

28%

2%

11% 11%

22%

1%

13%

4%

1%1% 0% 0%

1%0%

14%

-20%

-10%

0%

10%

20%

30%

40%

-

2,000,000,000

4,000,000,000

6,000,000,000

8,000,000,000

10,000,000,000

12,000,000,000

Rela

tive t

o t

ota

l d

eb

t

Am

ou

nt

in

US

D,

JP

Y o

r G

BP

Source: Bloomberg <SRCH>GO

11

Number of redemptions by issuer*

0

2

4

6

8

10

12

14

16

18

20

# of redemptions by issuer

Source: Bloomberg <SRCH>GO.*Number of redemptions between 15/01/2018 and 30/06/2019

12

0

5,000,000,000

10,000,000,000

15,000,000,000

20,000,000,000

25,000,000,000

30,000,000,000

35,000,000,000

40,000,000,000

45,000,000,000

Redemption volume by issuer in local currency

Redemption volumes by issuer*

Source: Bloomberg <SRCH>GO.*Total redemption volumes by issuer in local currency between 15/01/2018 and 30/06/2019

13

Redemption statistics by issuer

0%

10%

20%

30%

40%

50%

60%

70%S

t1 N

ord

ic O

y

Ke

sko O

YJ

G4S

PL

C

NC

C A

B

Bill

eru

dK

ors

na

s A

B

Vo

lvo A

B

Ram

irent O

YJ

Fo

rtum

OY

J

Sa

ab A

B

UP

M-K

ym

mene O

YJ

SR

V G

roup O

YJ

Sw

edis

h M

atc

h A

B

Sw

edavia

AB

Skanska A

B

Sta

tkra

ft S

F

Ele

ctr

olu

x A

B

Atla

s C

opco A

B

Nyn

as G

roup

TD

C A

/S

SA

S A

B

Nokia

OY

J

Se

curita

s A

B

Te

lenor

AS

A

SS

AB

AB

Te

olli

suuden V

oim

a O

yj

Arla

Fo

ods a

mb

a

Hexagon A

B

Ta

llin

k G

rupp A

S

Husqvarn

a A

B

SK

F A

B

Sto

ra E

nso O

YJ

AP

Mo

ller

- M

aers

k A

/S

Ke

mira O

YJ

Norg

esG

ruppen A

SA

Me

tsa B

oard

OY

J

Va

ttenfa

ll A

B

Sh

ip F

inance Inte

rnatio

nal Ltd

Nib

e Industr

ier

AB

Essity A

B

Getinge

AB

Fin

grid

OY

J

Sta

toil

AS

A

Ors

ted A

/S

Fin

nair O

YJ

Te

le2 A

B

Sta

tnett S

F

Norw

egia

n A

ir S

huttle

AS

A

Schib

ste

d A

SA

Mets

o O

YJ

Walle

niu

s W

ilhelm

sen L

ogis

tics

Neste

Oyj

Dfd

s A

/S

ES

B Ire

land H

old

ings L

td

Te

lia C

o A

B

Ste

na A

B

Fo

rtum

Varm

e H

old

ing s

am

agt m

e

Bo

nheur

AS

A

Sa

ndvik

AB

Redemptions relative to total debt by issuer (%)

Source: Bloomberg <SRCH>GO

14

Issuers with redemptions between 15/01/2018 and 30/06/2019 (higher issuance likelihood)

Company name Corp ticker# of bond

maturitiesTotal volume (LCYm)

Deficit inc.

Facilities

Deficit ex.

FacilitiesRCF use (%)

Total volume to

total debt

Volvo AB VLVY 19 39,765,532,500 NO YES 39% 30%

Swedish Match AB SWEMAT 5 2,440,830,000 NO NO 0% 22%

Vattenfall AB VATFAL 5 11,734,590,250 NO NO 0% 10%

Essity AB SCHHYG 5 5,972,490,000 NO NO 0% 10%

Statoil ASA STLNO 5 2,850,000,000 NO NO 0% 9%

Electrolux AB ELTLX 4 2,000,000,000 NO NO 0% 20%

Telenor ASA TELNO 4 12,395,840,000 NO YES 55% 16%

SSAB AB SSABAS 4 3,388,060,808 NO NO 0% 16%

Arla Foods amba ARLA 4 302,760,000 YES YES 100% 15%

Stora Enso OYJ STERV 4 399,095,000 NO NO 0% 12%

Statnett SF STATNE 4 2,276,180,000 NO YES 91% 7%

Fortum OYJ FUMVFH 3 1,168,818,000 NO NO 0% 25%

Swedavia AB SWEDAV 3 1,130,100,000 YES YES 100% 21%

Skanska AB SKABSS 3 2,350,000,000 NO NO 0% 21%

Statkraft SF STATK 3 7,876,800,000 NO NO 0% 20%

Teollisuuden Voima Oyj TVOYFH 3 701,840,000 NO YES 14% 15%

Hexagon AB HEXAG 3 363,312,000 NO NO 0% 15%

AP Moller - Maersk A/S MAERSK 3 1,854,080,400 NO NO 0% 12%

Telia Co AB TELIAS 3 3,372,754,747 NO NO 0% 4%

G4S PLC GFSLN 2 790,160,000 NO NO 0% 32%

NCC AB NCCAB 2 850,000,000 NO NO 0% 32%

BillerudKorsnas AB BILL 2 1,500,000,000 YES YES 100% 32%

Saab AB SAABAB 2 1,350,000,000 NO NO 0% 24%

Source: Bloomberg <SRCH>GO

15

Company name Corp ticker# of bond

maturitiesTotal volume (LCYm)

Deficit inc.

Facilities

Deficit ex.

FacilitiesRCF use (%)

Total volume to

total debt

UPM-Kymmene OYJ UPMFH 2 423,800,000 NO NO 0% 22%

Nokia OYJ NOKIA 2 723,910,594 NO NO 0% 18%

Husqvarna AB HUSQB 2 1,000,000,000 NO NO 0% 12%

Ship Finance International Ltd SFL 2 170,752,000 YES YES 100% 10%

Getinge AB GETAB 2 2,000,000,000 NO YES 24% 10%

Wallenius Wilhelmsen Logistics WWLNO 2 179,250,000 NO NO 0% 5%

Stena AB STENA 2 2,021,293,200 NO NO 0% 4%

Sandvik AB SANDSS 2 625,000,000 NO NO 0% 2%

St1 Nordic Oy STNORD 1 100,000,000 NO NO 0% 59%

Kesko OYJ KESBV 1 250,000,000 NO NO 0% 45%

Ramirent OYJ RMRVFH 1 100,000,000 YES YES 100% 26%

SRV Group OYJ SRVYHT 1 75,000,000 NO YES 42% 22%

Atlas Copco AB ATCOA 1 4,954,150,000 NO NO 0% 20%

Nynas Group NYNAAB 1 1,100,000,000 NO NO 0% 20%

TDC A/S TDCDC 1 4,465,680,000 NO YES 26% 19%

SAS AB SASSS 1 1,574,000,000 NO NO 0% 18%

Securitas AB SECUSS 1 2,972,490,000 NO YES 15% 16%

Tallink Grupp AS TALLNK 1 91,620,000 NO YES 71% 12%

SKF AB SKFBSS 1 2,314,677,963 NO NO 0% 12%

Kemira OYJ KEMIRA 1 100,001,000 NO NO 0% 11%

NorgesGruppen ASA NORGRU 1 800,000,000 NO NO 0% 11%

Issuers with redemptions between 15/01/2018 and 30/06/2019 (higher issuance likelihood)

Source: Bloomberg <SRCH>GO

16

Company name Corp ticker# of bond

maturitiesTotal volume (LCYm)

Deficit inc.

Facilities

Deficit ex.

FacilitiesRCF use (%)

Total volume to

total debt

Metsa Board OYJ METSA 1 67,269,000 NO NO 0% 11%

Nibe Industrier AB NIBEBS 1 900,000,000 NO YES 4% 10%

Fingrid OYJ FINPOW 1 100,920,000 NO YES 2% 9%

Orsted A/S DONGAS 1 2,085,480,003 NO NO 0% 9%

Finnair OYJ FOY 1 64,918,000 NO NO 0% 8%

Tele2 AB TELBSS 1 1,000,000,000 NO YES 19% 7%

Norwegian Air Shuttle ASA NASNO 1 1,250,000,000 YES YES 100% 5%

Schibsted ASA SCHNO 1 300,000,000 NO NO 0% 5%

Metso OYJ METSO 1 40,000,000 NO NO 0% 5%

Neste Oyj NESVFH 1 50,000,000 NO NO 0% 4%

Dfds A/S DFDSDC 1 125,004,000 NO NO 0% 4%

ESB Ireland Holdings Ltd ESBIRE 1 191,557,600 NO NO 0% 4%

Fortum Varme Holding samagt me FVHSAM 1 252,000,000 NO NO 0% 2%

Bonheur ASA BONNO 1 300,000,000 NO NO 0% 2%

Issuers with redemptions between 15/01/2018 and 30/06/2019 (higher issuance likelihood)

Source: Bloomberg <SRCH>GO

17

Company name Corp ticker# of bond

maturitiesTotal volume (LCYm)

Deficit inc.

Facilities

Deficit ex.

FacilitiesRCF use (%)

Total volume to

total debt

Caruna Oy CARUNA 0 0 YES YES 100% 0%

Teekay Offshore Partners LP TOO 0 0 YES YES 100% 0%

YIT OYJ YITYH 0 0 YES YES 100% 0%

Avinor AS AVINOR 0 0 NO YES 57% 0%

Lantmannen ek for LATMEK 0 0 NO YES 52% 0%

Danfoss A/S DNFSDC 0 0 NO YES 50% 0%

Elisa OYJ ELIAV 0 0 NO YES 37% 0%

Svenska Cellulosa AB SCA SCABSS 0 0 NO YES 31% 0%

Faroe Petroleum PLC FPMLN 0 0 NO YES 34% 0%

ICA Gruppen AB ICASS 0 0 NO YES 8% 0%

HKScan OYJ HKSAV 0 0 NO YES 6% 0%

Color Group AS COLLIN 0 0 NO YES 6% 0%

DNA Oyj DNAFH 0 0 NO YES 1% 0%

Stockmann OYJ Abp STCBV 0 0 NO NO 0% 0%

Ambu A/S AMBUDC 0 0 NO NO 0% 0%

Beerenberg Holdco II AS BERHLD 0 0 NO NO 0% 0%

AX IV EG Holding III ApS EGASDK 0 0 NO NO 0% 0%

BW Offshore Ltd BWONO 0 0 NO NO 0% 0%

Ixat Intressenter AB CABONL 0 0 NO NO 0% 0%

Carlsberg A/S CARLB 0 0 NO NO 0% 0%

Com Hem Holding AB COMHSS 0 0 NO NO 0% 0%

Crayon Group Holding ASA CRAYON 0 0 NO NO 0% 0%

DSV A/S DSVDC 0 0 NO NO 0% 0%

Elekta AB EKTAB 0 0 NO NO 0% 0%

Issuers without redemptions between 15/01/2018 and 30/06/2019 (lower issuance likelihood)

Source: Bloomberg <SRCH>GO

18

Corp ticker# of bond

maturitiesTotal volume (LCYm)

Deficit inc.

Facilities

Deficit ex.

FacilitiesRCF use (%)

Total volume to

total debt

Elenia Oy ELENFH 0 0 NO NO 0% 0%

Ellevio AB ELLEVI 0 0 NO NO 0% 0%

GAS Networks Ireland BOGAEI 0 0 NO NO 0% 0%

ISS A/S ISSDC 0 0 NO NO 0% 0%

Link Mobility Group ASA LINKNO 0 0 NO NO 0% 0%

Luossavaara-Kiirunavaara AB LKAB 0 0 NO NO 0% 0%

Loomis AB LOOMBS 0 0 NO NO 0% 0%

Orkla ASA ORKBNO 0 0 NO NO 0% 0%

Outokumpu OYJ OUTOK 0 0 NO YES 0% 0%

Teekay Shuttle Tankers LLC TKSHTN 0 0 NO NO 0% 0%

Telefonaktiebolaget LM Ericsso ERICB 0 0 NO NO 0% 0%

Vestas Wind Systems A/S VWSDC 0 0 NO NO 0% 0%

GLX Holding AS GLXHLD 0 0 NO NO 0% 0%

Issuers without redemptions between 15/01/2018 and 30/06/2019 (lower issuance likelihood)

Source: Bloomberg <SRCH>GO

19

Danske Bank DCM credit research team

Find the latest Credit Research: :

Danske Bank DCM Research: http://www.danskebank.com/danskemarketsresearch Bloomberg: DNSK<GO>

Thomas Hovard

Head of Credit Research

+45 45 12 85 05

Gabriel Bergin

Strategy, Financials

+46 8 568 80602

Jakob Magnussen

Utilities, Energy

+45 45 12 85 03

Henrik René Andresen

Credit Portfolios

+45 45 13 33 27

Bendik Engebretsen

Industrials & Norwegian HY

+47 85 40 69 14

Brian Børsting

Industrials

+45 45 12 85 19

David Boyle

Industrials & Norwegian HY

+47 85 40 54 17

Niklas Ripa

Credit Portfolios

+45 45 12 80 47

Louis Landeman

Industrials, Real Estate

+46 8 568 80524

Mads Rosendal

Industrials, TMT

+45 45 14 88 79

August Moberg

Industrials & Construction

+46 8 568 80593

Jesper Damkjær

Financials

+45 45 12 80 41

Haseeb Syed

Industrials & Norwegian HY

+47 85 40 54 19

Katrine Jensen

Financials

+45 45 12 80 56

Christopher Hellesnes

General Industrials

+46 8 568 80547

20

DisclosuresThis research report has been prepared by Danske Bank DCM Research, a division of Danske Bank A/S (‘Danske Bank’). The author of this research report is Mads Rosendal, Senior Analyst.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the research report accurately reflect the research analyst’s personal view about the financial

instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly,

related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it

conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial

Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

Danske Bank’s research reports are prepared in accordance with the recommendations of the Danish Securities Dealers Association.

Danske Bank is not registered as a Credit Rating Agency pursuant to the CRA Regulation (Regulation (EC) no. 1060/2009). Hence, Danske Bank does not comply with nor seek to comply with the

requirements applicable to Credit Rating Agencies.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are

documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of

research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas

within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to

specific corporate finance or debt capital transactions.

Danske Bank, its affiliates and subsidiaries are engaged in commercial banking, securities underwriting, dealing, trading, brokerage, investment management, investment banking, custody and other

financial services activities, may be a lender to the companies mentioned in this publication and have whatever rights are available to a creditor under applicable law and the applicable loan and credit

agreements. At any time, Danske Bank, its affiliates and subsidiaries may have credit or other information regarding the companies mentioned in this publication that is not available to or may not be

used by the personnel responsible for the preparation of this report, which might affect the analysis and opinions expressed in this research report.

Completion and first dissemination

The completion date and time in this research report mean the date and time when the author hands over the final version of the research report to Danske Bank’s editing function for legal review and

editing.

The date and time of first dissemination mean the date and estimated time of the first dissemination of this research report. The estimated time may deviate up to 15 minutes from the effective

dissemination time due to technical limitations.

See the final page of this research report for the date and time of first dissemination.

Validity time period

This communication as well as the communications in the list referred to below are valid until the earlier of (a) dissemination of a superseding communication by the author, or (b) significant changes in

circumstances following its dissemination, including events relating to the market or the issuer, which can influence the price of the issuer or financial instrument.

21

Investment recommendations disseminated in the preceding 12-month period

A list of previous investment recommendations disseminated by the lead analyst(s) of this research report in the preceding 12-month period can be found at www-

2.danskebank.com/Link/researchdisclaimer. Select DCM Research recommendation history – Recommendation history.

Other previous investment recommendations disseminated by Danske Bank DCM Research, Debt Capital Markets Research are also available in the database.

General disclaimerThis research has been prepared by Danske Bank DCM Research (a division of Danske Bank A/S). It is provided for informational purposes only. It does not constitute or form part of, and shall under no

circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial instruments mentioned herein or other financial instruments

of any issuer mentioned herein and/or options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable. While reasonable care has been taken to

ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any

direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date hereof. These opinions are subject to change, and

Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is not intended for, and may not be redistributed to, retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without

Danske Bank’s prior written consent.

Disclaimer related to distribution in the United StatesThis research report was created by Danske Bank A/S and is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank A/S, pursuant to

SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The research report is intended for distribution in the United States solely to ‘U.S. institutional

investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the research analysts of Danske Bank who have

prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that

investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be

subject to the reporting and auditing standards of the U.S. Securities and Exchange Commission.

Report completed: 15 December 2017 at 09:54 CET

Report disseminated: 15 December 2017 at 10:55 CET

Related Documents