Potential Impacts of the Solid Bio-fuel Industry in Westmeath Research into Regional Opportunities for the Biomass Industry This research dissertation is submitted in partial fulfilment of the Degree of Masters in Business Administration at the Athlone Institute of Technology

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Potential Impacts of the

Solid Bio-fuel Industry in

Westmeath

Research into Regional Opportunities for the BiomassIndustry

This research dissertation is submitted in partial fulfilment

of the Degree of Masters in Business Administration at the

Athlone Institute of Technology

Submitted to: Athlone Institute of Technology

Submitted by: Michael Ward

Research Supervisor: Edward Whyte

Date Submitted: 3rd September, 2007

Statement Of Declaration

I have read the institutes code of practice on plagiarism. I

herby certify this material, which I now submit for

assessment on the programme of study leading to the award of

Masters of Business Administration, is entirely my own work

and has not been taken from the work of others, save and to

the extent that such work is cited within the text of my

work.

Student ID Number: A00118826

Name of Candidate: Michael Ward

Signature of Candidate:

Date: 3rd September, 2007

Table Of Contents

SECTION 1 - EXECUTIVE SUMMARY..............................5

SECTION 2 - INTRODUCTION...................................9

2.1 CHAPTER OVERVIEW.......................................92.2 BACKGROUND TO THE SECTOR.................................92.3 DRIVERS OF THE INDUSTRY – PEAK OIL......................102.4 DRIVERS OF THE INDUSTRY – CLIMATE CHANGE..................122.5 CURRENT SITUATION......................................132.6 BARRIERS TO THE INDUSTRY................................142.7 COMMENTARY & CONCLUSIONS................................14

SECTION 3 - METHODOLOGY...................................16

3.1 INTRODUCTION..........................................163.2 THE RESEARCH QUESTION..................................163.3 THE RESEARCH OBJECTIVES................................163.3.1 Policy Analysis......................................173.3.2 Resource Assessment..................................173.3.3 Market Analysis......................................173.3.4 Operations and Supply Chain Development..............183.3.5 Economic Impact......................................18

3.4 ACCESS AND LIMITATIONS.................................193.5 SECONDARY DATA........................................193.6 THE INTERVIEW PROCESS..................................203.7 QUESTIONNAIRES........................................233.7.1 Selecting the sample size............................24

SECTION 4 - POLICY ANALYSIS...............................25

4.1 INTRODUCTION..........................................254.2 POLICY OVERVIEW.......................................254.3 BIO-ENERGY STRATEGY....................................274.4 EXPANDING THE RENEWABLE HEAT SECTOR......................294.4.1 Incentives on the Supply Side........................304.4.1.1 Bio-energy Scheme for Willow and Miscanthus 2007

304.4.1.2......Relief for Investment in Renewable Energy Generation...........................................31

4.4.1.3. .Wood Biomass Harvesting Machinery Grant Scheme31

4.4.1.4.......................Afforestation Grant Rates32

4.4.2 Incentives on the Demand Side........................344.4.2.1............................Greener Homes Scheme

344.4.2.2.............................Warmer Homes Scheme

354.4.2.3...............................House of Tomorrow

354.4.2.4................................Reheat Programme

354.4.2.5......Combined Heat and Power (CHP) Grant Scheme

364.5 OUTCOMES TO DATE......................................364.6 INTERVIEW COMMENTS.....................................374.7 COMMENTARY & CONCLUSIONS................................38

SECTION 5 - RESOURCE ASSESSMENT...........................40

5.1 INTRODUCTION..........................................405.2 FORESTRY CO-PRODUCTS...................................405.3 POST CONSUMER WOOD WASTE...............................435.3.1 Recycled Timber......................................435.3.2 Sawmill Co-Products..................................445.3.3 Arboricultural Arisings..............................45

5.4 DEDICATED ENERGY CROPS.................................455.5 INTERVIEW COMMENTS.....................................475.6 COMMENTARY & CONCLUSIONS................................48

SECTION 6 - MARKET ANALYSIS...............................50

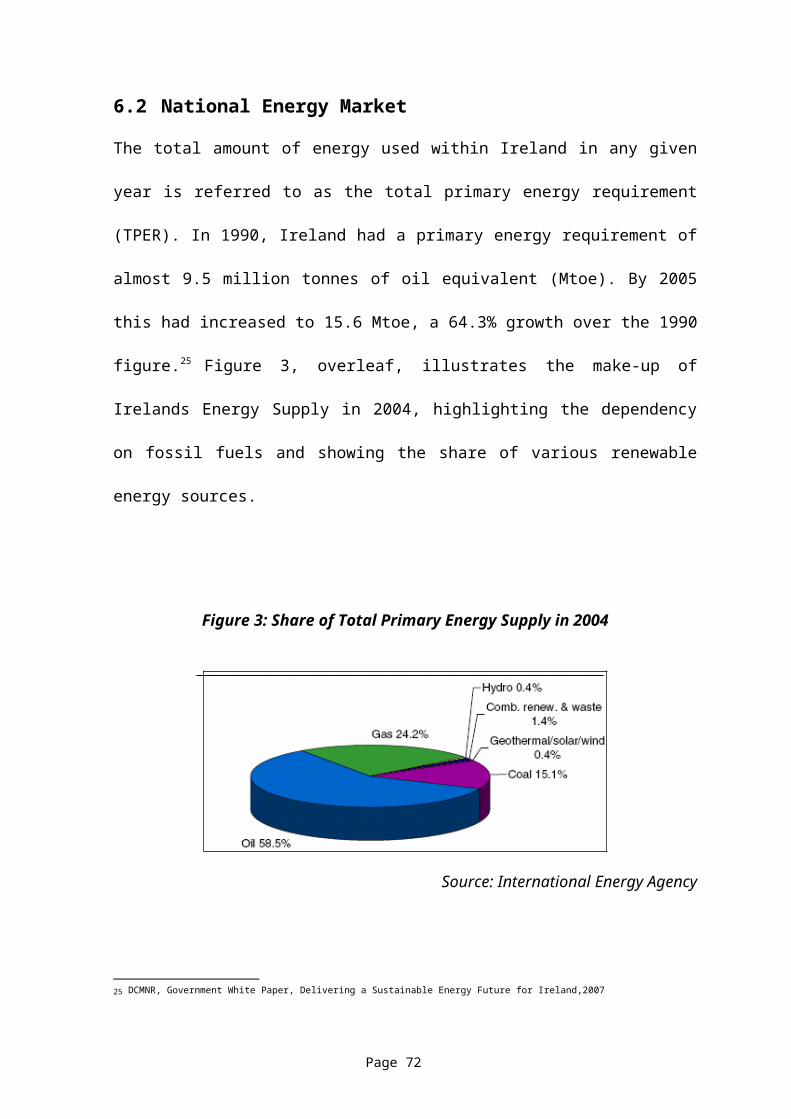

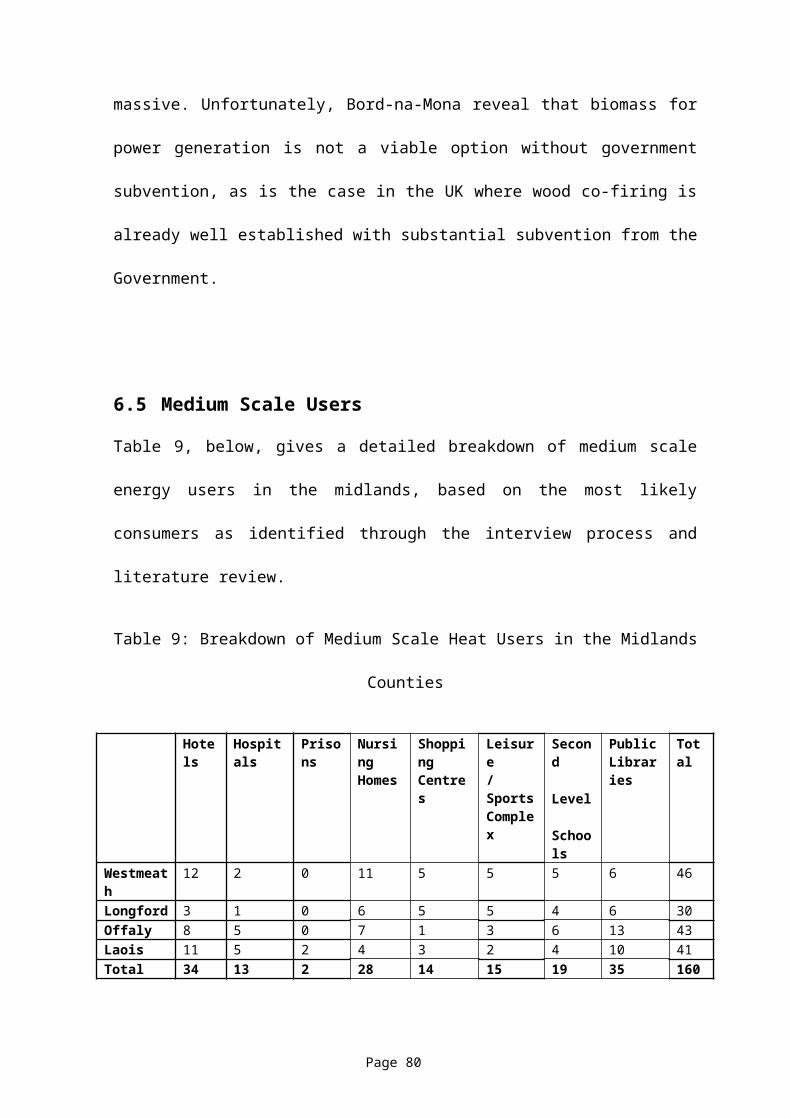

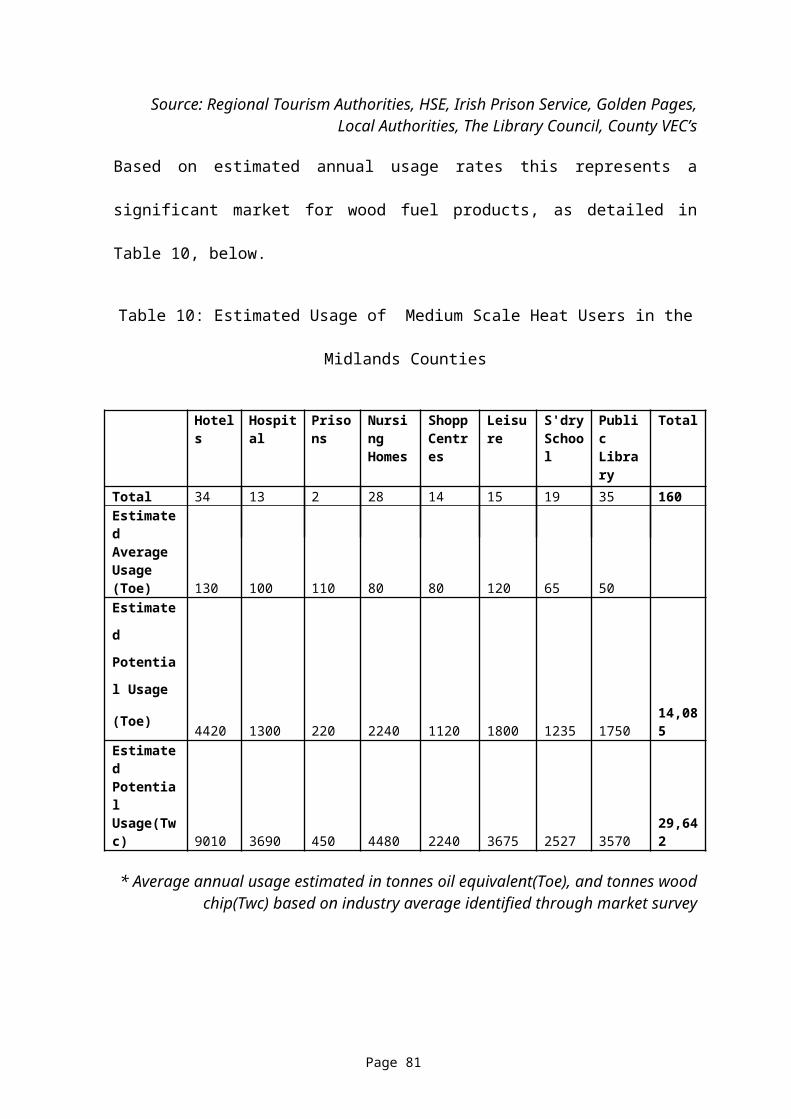

6.1 INTRODUCTION..........................................506.2 NATIONAL ENERGY MARKET.................................506.3 IDENTIFYING MARKET SEGMENTS.............................546.4 LARGE SCALE USERS.....................................556.5 MEDIUM SCALE USERS....................................566.5.1 Medium Scale Market Survey...........................57

6.6 SMALL SCALE USERS.....................................596.6.1 Assessment of Future Potential.......................61

6.7 INTERVIEW COMMENTS.....................................626.8 COMMENTARY & CONCLUSIONS................................63

SECTION 7 - OPERATIONS & SUPPLY CHAIN.....................65

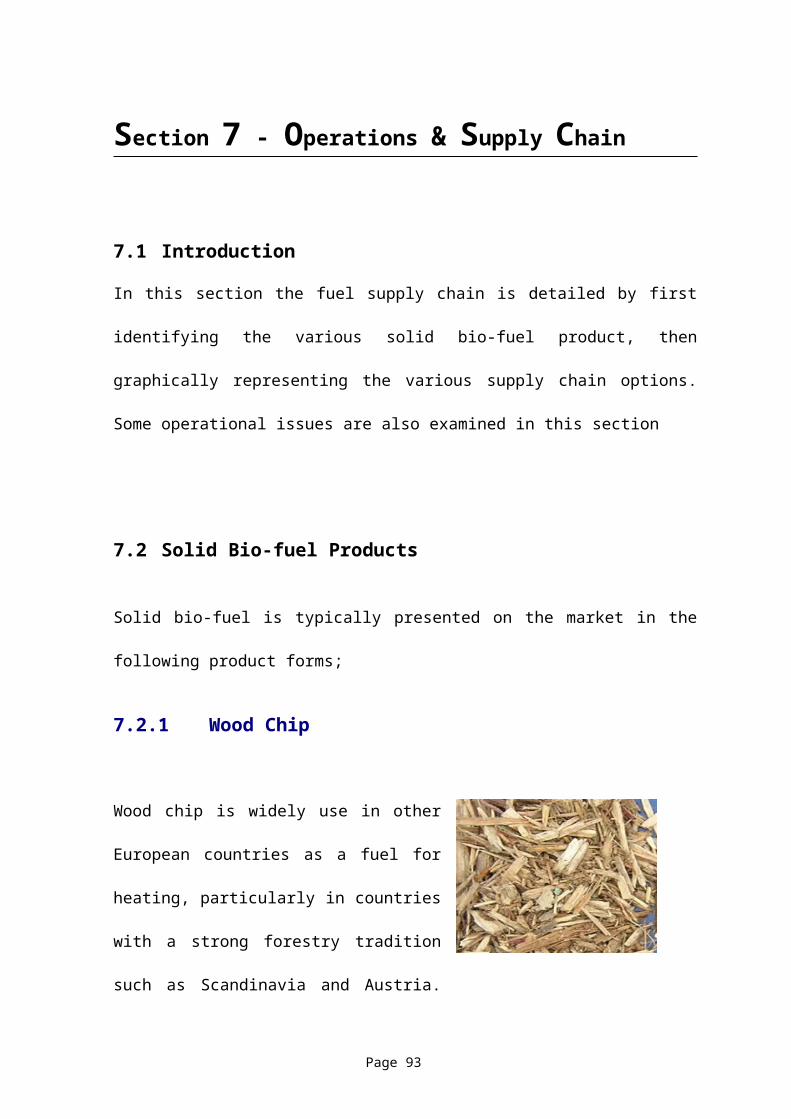

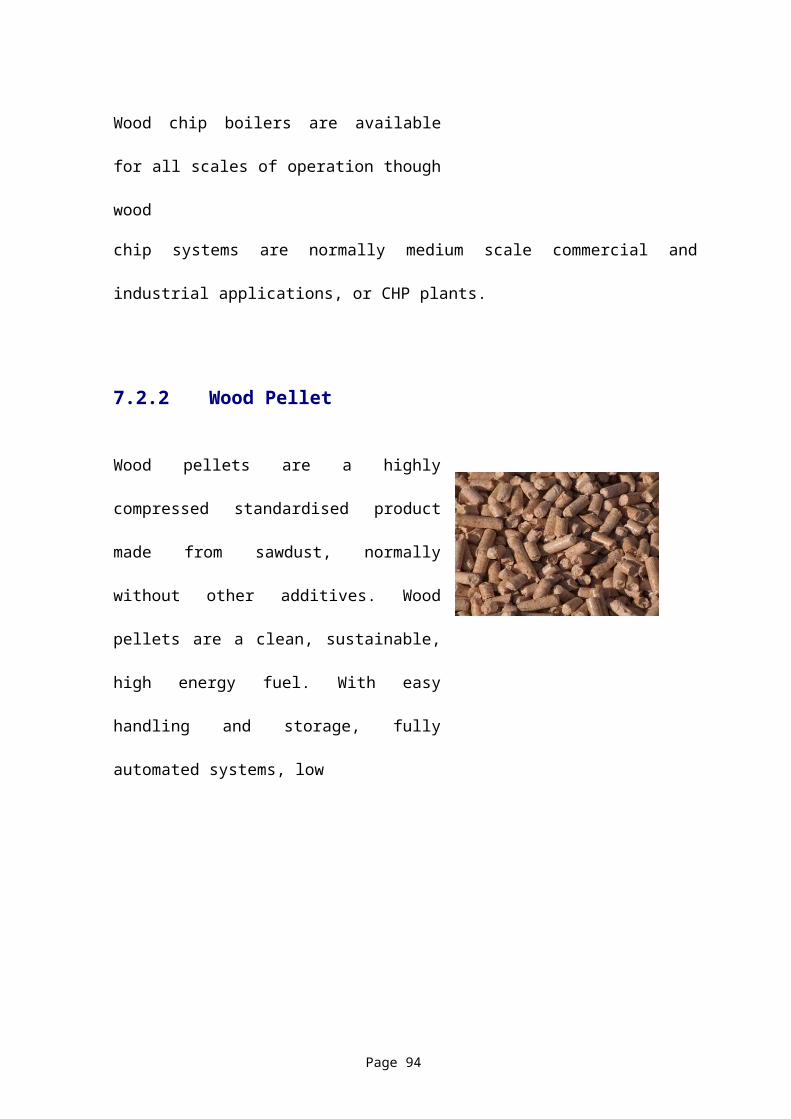

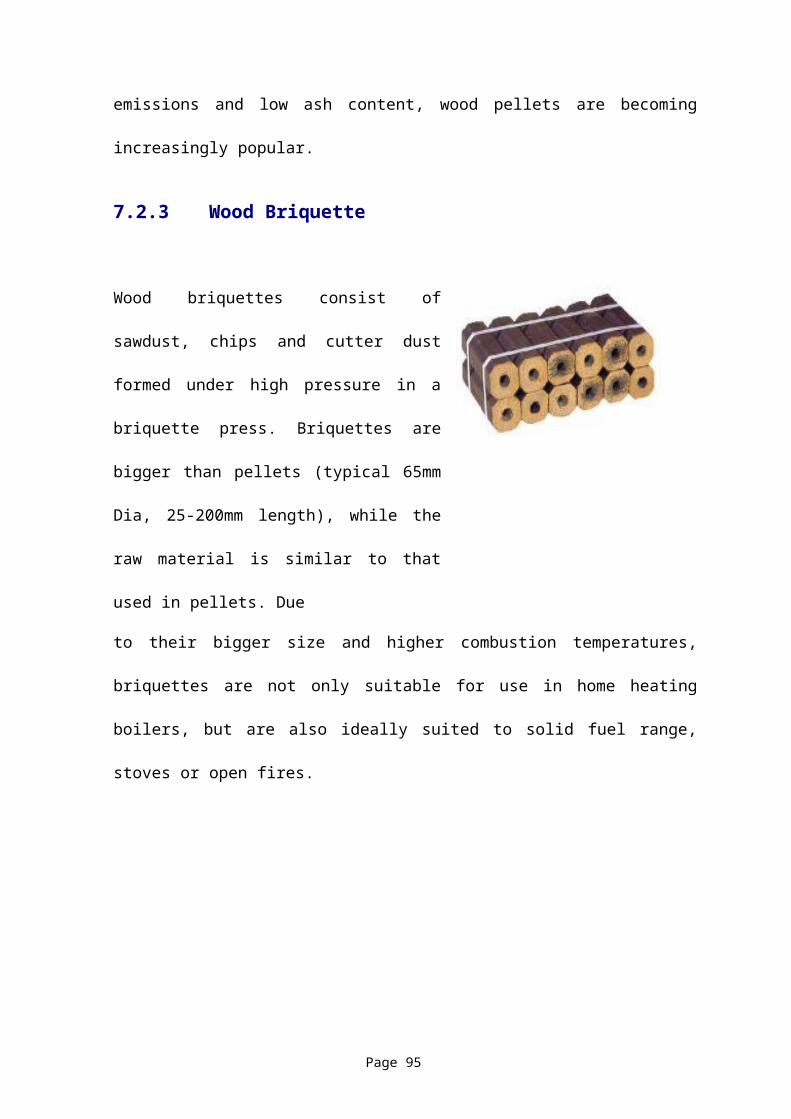

7.1 INTRODUCTION..........................................657.2 SOLID BIO-FUEL PRODUCTS................................657.2.1 Wood Chip............................................657.2.2 Wood Pellet..........................................667.2.3 Wood Briquette.......................................667.2.4 Cereals/Grain........................................66

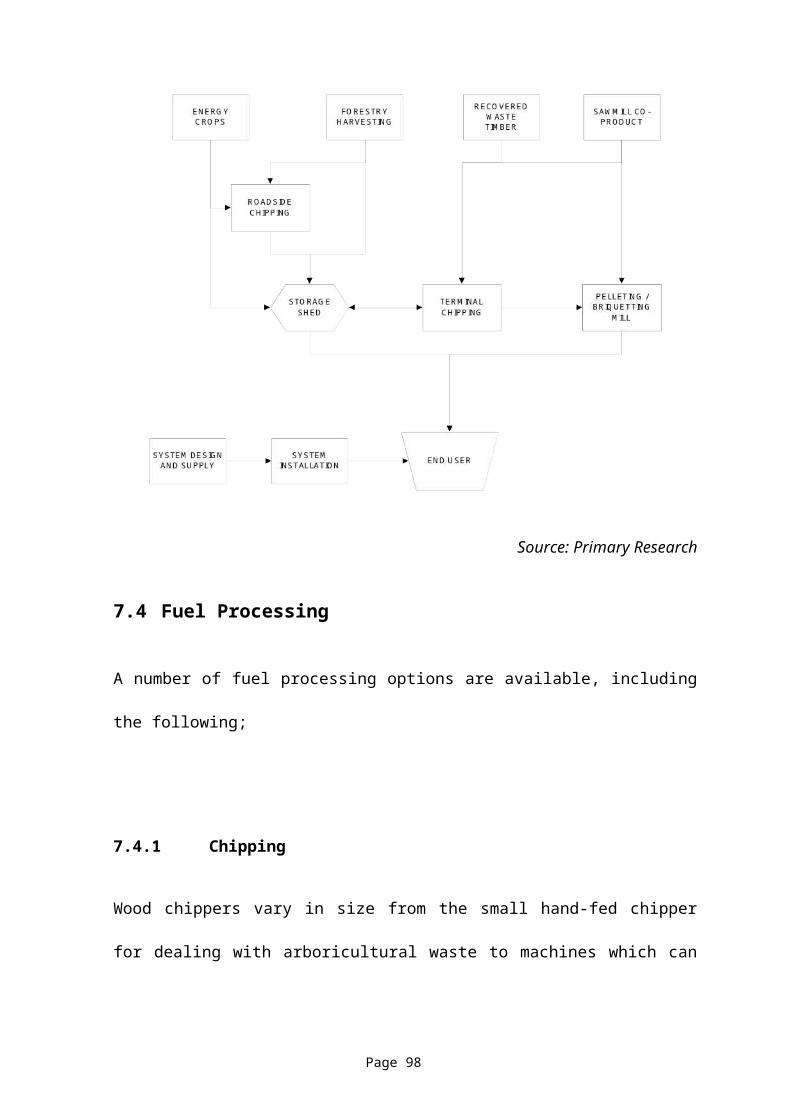

7.3 THE FUEL SUPPLY CHAIN..................................677.4 FUEL PROCESSING.......................................687.4.1 Chipping.............................................687.4.2 Pelletising/Briqueting...............................697.4.3 Drying and storage...................................707.4.4 Internal Transport & Delivery to End-Customers.......70

7.5 QUALITY CONTROL FOR SOLID BIO-FUELS......................717.6 SUPPLY CONTRACTS......................................717.7 INTERVIEW COMMENTS.....................................727.8 COMMENTARY & CONCLUSIONS................................73

SECTION 8 - ECONOMIC IMPACT & CONCLUSIONS...............75

8.1 INTRODUCTION..........................................758.2 ADVANTAGES OF SOLID BIO-FUELS...........................758.3 JOB CREATION..........................................768.4 IMPACTS OF REACHING NATIONAL TARGETS.....................788.4.1 Residential Heating Target...........................788.4.2 Electricity Co-Firing Target.........................798.4.3 National Impacts.....................................80

8.5 COMMENTARY & CONCLUSIONS................................80

SECTION 9 - OPPORTUNITIES FOR FURTHER RESEARCH..........84

REFERENCES & BIBLIOGRAPHY.................................86

APPENDIX..................................................90

APPENDIX 1A - HOUSEHOLD SURVEY QUESTIONNAIRE...................90APPENDIX 1B - COMMERCIAL USERS SURVEY QUESTIONNAIRE.............92APPENDIX 2 - TOTAL FOREST COVER BY COUNTY (HA)................94APPENDIX 3 – SAWMILLS IN THE MIDLANDS.........................95APPENDIX 4 - TECHNICAL STANDARDS.............................96Appendix 5 - Existing Solid Bio-fuel Enterprise in Westmeath 98

Glossary

BES Bio-energy Scheme run by the Department of

Agriculture, Fisheries & Food to support the

production of energy crops

Bio-energy Renewable energy produced from biomass

Bio-fuel Liquid, solid or gaseous fuel produced by

conversion of biomass

Biomass Renewable organic matter such as agricultural

crops and residue, wood and wood waste, animal

waste, aquatic plants and organic components

of municipal and industrial wastes

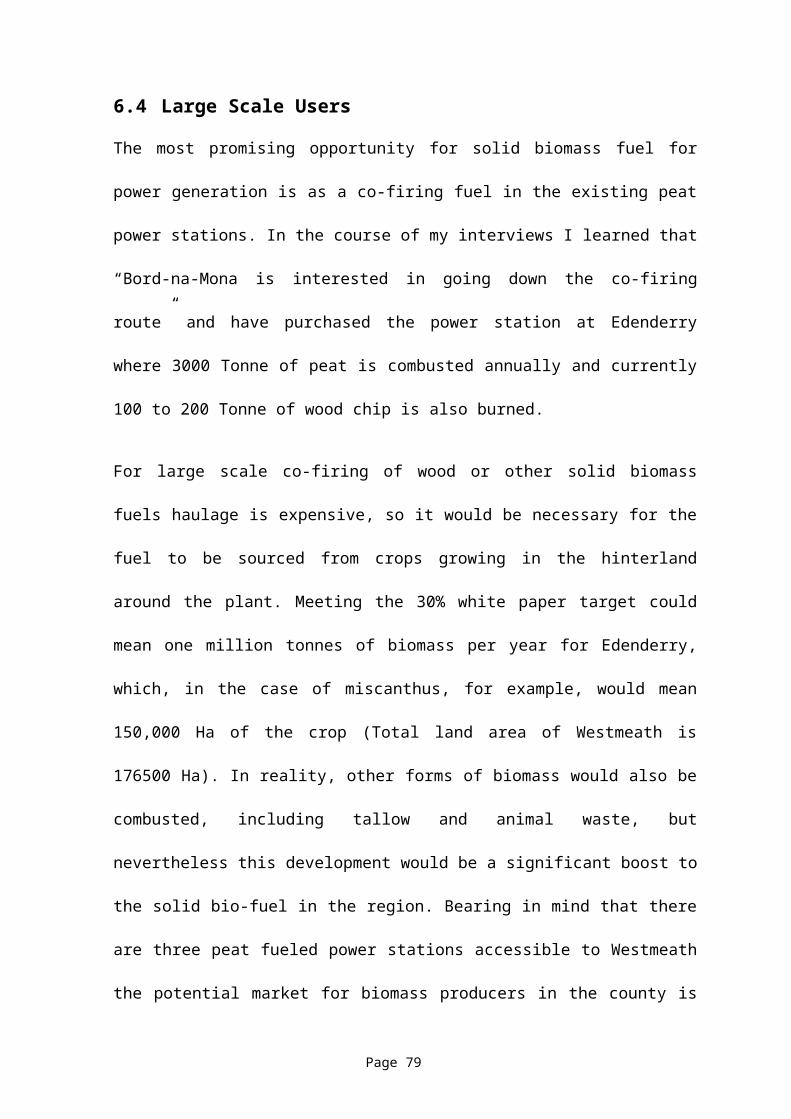

Bord-na-Mona

One of Ireland‘s leading energy providers, BNM

owns significant peat resources

Carbon Neutral

The practice of balancing carbon dioxide

released into the atmosphere with practices

that remove or sequester carbon from the

atmosphere i.e. growing biomass crops absorbs

carbon from the atmosphere which is then

released when the biomass is converted to

energy, so that the net carbon emissions are

zero

CHP Combined Heat & Power. The sequential

production of electricity and useful thermal

energy from a common fuel source

CO2 Carbon Dioxide. A product of combustion. The

most common greenhouse gas

COFORD National Council for Forest Research and

Development

Conventional Oil

Readily accessible (by conventional means)

crude oil

ECAS Energy Crops in the Atlantic Space. An EU

funded research project of the Mid-South

Roscommon Leader Company

Energy Crops

Crops grown specifically for their fuel value

EPA Environmental Protection Agency

ESCo Energy Supply Company

ESRI The Economic and Social Research Institute,

founded in 1960 to produce high quality

research, with a core focus on Ireland’s

economic and social development, in order to

inform policy-making and societal

understanding

EUBIONET European Bio-energy Network

Forfas Ireland’s national policy and advisory board

for trade, science, technology and innovation

(of the Department of Enterprise, Trade and

Employment

GHG Greenhouse Gas. Gases that trap the heat of

the sun in the Earth’s atmosphere producing

the greenhouse effect. The two major

greenhouse gases are water vapour and carbon

dioxide. Other greenhouse gases include

methane, ozone, chlorofluorocarbons, and

nitrous oxide

GJ Giga Joule. A measure of energy equivalent to

278KWh

Green Tonne 1,000 kilogram’s of un-dried biomass material.

Moisture content must be specified if green

tons are used as a measure of fuel energy

Ha Hectare - Unit for measurement of area - 1Ha =

2.49 Acres

IEA International Energy Agency

Ktoe Kilo Tonnes Oil Equivalent (1000 toe)

KW A measure of electrical power equal to 1,000

Watts. 1 kW = 3,413 Btu/hr = 1.341 horsepower.

KWh A measure of energy equivalent to the

expenditure of one kilowatt for one hour

Kyoto The Kyoto Protocol was adopted at the Third

Session of the Conference of the Parties (COP)

to the UN Framework Convention on Climate

Change (UNFCCC) in 1997 in Kyoto, Japan. It

contains legally binding commitments by

countries included in Annex B of the Protocol

(most OECD countries and EITs) who agreed to

reduce their anthropogenic emissions of

greenhouse gases to agreed upon targets

Midlands Counties Westmeath, Longford, Laois and Offaly

Miscanthus A woody perennial tufted or rhizomatous grass

grown as an energy crop (sometimes called

Elephant Grass)

Mtoe Million Tonnes Oil Equivalent

MW Megawatt. Unit of power that equals one

million Watts (1,000 kW).

MWe Megawatt Electricity

NDP National Development Plan

NFI National Forestry Inventory

Peak Oil Peak Oil is the point or timeframe at which

the maximum global petroleum production rate

is reached. After this timeframe, the rate of

production will by definition enter terminal

decline. According to the Hubbert model,

production will follow a roughly symmetrical

bell-shaped curve

RCG Reed Canary Grass. A robust perennial grass

sometimes grown as an energy crop

REFIT Renewable Energy Feed In Tariff - A Government

support mechanism for renewable electricity

projects operated by the Department of

Communications Marine and Natural resources

REIO Renewable Energy Information Office (of the

SEI)

Renewable Energy

An energy source that is replenished

continuously in nature or that is replaced

after use through natural means. Renewable

energy sources include the sun, the winds,

flowing water, biomass and geothermal energy.

REPS Rural Environment Protection Scheme - a five

year scheme where a farmer enters into a

contract with the Department of Agriculture to

farm in accordance with an agri-environmental

plan drawn up by an approved planning agency

RES-H Renewable Energy Supply, Heat

SEI Sustainable Energy Ireland

Solid Bio-fuel

Solid fuel produced by conversion of biomass,

examples include wood chip, wood pellet, fuel

grain

SRC Short Rotation Coppice. Plantings established

and managed under short-rotation intensive

culture practices, for example Willow

SustainableEnergy

An energy source that is replenished

continuously in nature or that is replaced

after use through natural means. Sustainable

energy sources include the sun, the winds,

flowing water, biomass and geothermal energy

Teagasc The Irish agriculture and food development

authority

TFC Total Final Consumption

TFC–H Total Final Consumption, Heat

Toe Tonnes Oil Equivalent

TPER Total Primary Energy Resource

TPES Total Primary Energy Supply

VAT Value Added Tax

WDC Western Development Commission

Willow Rapidly growing deciduous species that coppice

freely, i.e. produce numerous new stems from

the cut stump (popular energy crop)

Section 1 - Executive Summary

Based on various crosschecks, annual ‘solid bio-fuels’

consumption in Europe can be estimated at about 50 million

Tonne Oil Equivalent (Toe). By a systematic salvage of

forestry by-products, industrial wood-waste and scrap wood,

it is estimated that this contribution could probably be

doubled in the next 10 to 15 years. Factoring in the

potential for dedicated energy crops, including willow short

rotation coppice (SRC), Miscanthus and grain, this figure can

be increased even further.

France, Austria, Finland, Sweden, and Germany are among the

countries in the European Union where wood energy consumption

is largest. The southern countries such as Spain, Portugal,

and Italy come next. Among the eastern European countries,

Turkey is the largest wood energy consumer, followed by the

Czech Republic, Poland and Romania.

When produced and managed in a sustainable manner, solid bio-

fuel provides a multitude of advantages. It does not only

serve as an energy provider, but also as an environmentally

favourable and economically beneficial resource. Ireland is

clearly behind in terms of solid bio-fuel usage when compared

to the rest of Europe, but can exploit the "latecomer’s

advantage" through benefiting from technical advances and

industry experience/successes within Europe. Many significant

insights and lessons can be generated from the various

experiences among European countries in relation to the

evolution of this fledgling industry.

Solid bio-fuel is a local and diffuse renewable resource

which, unlike conventional energy, is not distributed by

large industrial groups, but by a network of various small to

medium sized companies or organisations including farmers and

foresters, fuel producers, distributors etc. However, some

companies of an international dimension are starting to show

an interest in the sector.

This document examines the solid bio-fuel industry in

Ireland, with a particular focus on the potential to develop

related value-added enterprise in Co. Westmeath. In

particular this study is designed to evaluate the;

Page 6

Government policy driving the sector

Raw material resource available

Specific markets which are relevant to this product

Operations and supply chain development within the

sector

Potential economic impact on the industry for County

Westmeath

A mix of primary and secondary research was undertaken in the

delivery of this report including the following aspects;

Detailed research into relevant literature and current

policy framework as is relevant to the research topic

Evaluation of current and potential future raw material

resources. This aspect of the study is derived from

secondary sources including;

Forest Service

Department of Agriculture, Fisheries and Food

Environmental Protection Agency

Teagasc

Page 7

Evaluation of current and potential future markets. This

aspect of the study is derived from a combination of

secondary research in evaluating the scale of the

particular market segments, and primary research in the

form of market survey to determine the potential within

each market sector for solid bio-fuel product

Determination of best fit operational and supply chain

options for the region. This part of the study is

informed by an examination of national and international

best practice, and through a series of in-depth

interview’s and discussion’s with a number of leading

industry experts

Based on the information gleaned from this research, an

evaluation of the potential economic impact for Co.

Westmeath is produced

The findings of this study are briefly summarised as follows;

Government policy is committed to driving the industry

forward, although, in the hierarchy of renewables, bio-

energy is given a lower priority than wind

Page 8

There is substantial raw material supply available to

sustain the industry going forward and market growth in

the sector will not be constrained by a shortage of

material. However, the future of dedicated energy crop

farming is not so clear as the uptake on the bio-energy

not likely to change

The main markets are the commercial, and residential

heat markets, both of which show significant potential

if the fuel supply chains are established

In the commercial sector awareness and information is

needed to drive the market

In the residential market, concerns around reliability

and quality of fuel supply must be addressed

Solid bio-fuel will play a part in power generation at

the midlands peat power stations, but as a co-fired

fuel. The extent of this market is not yet known as

other bio-fuels including tallow and animal waste will

also be co-fired to meet government 33% co-firing target

Westmeath, with its central location ideal for clustered

approach to serve greater midlands and Irish market.

Page 9

There is a significant number of companies already

operating in this sector, although few are exclusive to

bio-fuel

Page 10

Section 2 - Introduction

2.1 Chapter Overview

This section of the report will examine the background to the

solid bio-fuel industry in Ireland and identify some of the

key drivers of that industry. The current position of the

industry in Ireland will also be assessed.

2.2 Background to the Sector

The bulk of solid bio-fuel in Ireland is used in the form of

heat energy in the wood processing industry, and to provide

heat in domestic dwellings. More recently solid bio-fuel is

gaining popularity in the commercial sector, being

particularly suited to hotels, leisure centres and schools.

However, current usage rates represents only a very small

fraction of the potential contribution wood energy can make

to the national energy requirement.

Page 11

In recent years the subject of ‘sustainable’ or ‘renewable’

energy has been the focus of much discussion. While the

advantages and opportunities regarding this technology have

been well documented, the industry has not taken off in

Ireland as it has in other European countries. This would

seem to be due to a number of factors, including:

Government failure to commit to the use of ‘biomass’ for

electricity generation by converting peat burning power

generation plants, or building new biomass burning

plants

Issues around the creation of the ‘supply chain’

necessary to take the crop from the field to the fire.

In this regard we have a chicken and egg situation

whereby growers are nervous as the market has not yet

developed for the product, and the market is non-

committal as there is not a steady supply of the raw

material

On the other hand, fluctuating oil prices and the threat of

future shortages has seen an increase in interest in

Page 12

renewable energy and many commentators believe this is a

technology whose time has come.

This report will investigate these and other factors

influencing the development of this industry in Ireland in

order to make a reasoned prediction on the future potential

impacts of the industry for Westmeath.

2.3 Drivers of the Industry – Peak Oil

Life is today’s world is critically dependant on the ready

availability of a secure supply of energy in a convenient

form, so the threat of depleting oil resources has the

potential to change the world as we know it. In his article

in the OPEC review (1999), Mamdouh G. Salameh argued that

‘conventional oil’ would reach the last phase of its cycle by

2040, and that “rising global demand and declining reserve

discovery rates could lead to a radical increase in the price

of oil in the near future and that chronic shortages could be

predicted to develop from 2010 onwards”1. John Wilson,

however, in 2007 countered that many “misinformed assumptions

1 Salameh, M.G., Technology, Oil Reserve Depletion and the Myth of the Reserves-to-Production Ratio, 1999

Page 13

and misplaced beliefs” are being used as a basis for energy

policy, and that fossil fuels should remain our “primary

energy source for many years to come”. On biomass based fuels

Wilson predicts that they can “at best, be only a minor

contributor to meeting the worlds future energy needs”2.

In the Irish context the Economic and Social Research

Institute, (ESRI), concluded that “the rapidly rising demand

for energy due to the growth of the world economy is eroding

the potential spare world oil and gas capacity with limited

prospects of new finds of fossil fuels over the coming

decades it seems quite likely that real oil and gas prices

will rise dramatically in the longer term. In addition, the

need to tackle the problem of global warming will also lead

to increasing real prices for consumers of fossil fuels.

Preparing for a world of much higher energy prices will

require significant policy changes” 3. They also recognise

that there is a need for major investment in new electricity

generating capacity over the coming decade in Ireland. With

regard to renewables, Irish policy makers are placing a

2 Wilson, J., Energising our Future, How Disinformation and Ignorance are Misdirecting Our Efforts, 2007

3 Fitzgerald, J., et al., (ESRI), Aspects of Irish Energy Policy (Policy Research Series Number 57),

2005

Page 14

strong emphasis on wind as the answer, but the ESRI recommend

hedging the risk by developing a “diverse portfolio of

generating technologies and fuels”. Biomass is one of those

fuels that should be included in that portfolio. With this in

mind the ESRI recommend “peat plant should either be closed

or gradually converted to biomass”, and investment in new

power generation plants should include biomass options.

In their 2006 baseline assessment of Ireland’s oil dependence

Ireland’s national policy and advisory board for trade,

science, technology and innovation, (Forfas), agree that the

supply of conventional oil will peak sometime in the first

half of the 21st century and that Ireland is in a very

vulnerable position due to our heavy dependence on oil4.

Forfas conclude that “viable mitigation options exist both on

the supply and demand sides to address this situation”. The

report puts forward options such as “expanding domestic oil

storage capabilities” and developing more “East-West

electricity interconnection with the UK” as policy options to

mitigate against Irelands sensitivity to high oil prices, and

also endorses the possibility of developing nuclear energy as

4 Forfas, A Baseline Assessment of Ireland’s Oil Dependance, April 2006

Page 15

a long term solution for power generation in Ireland.

However, the report fails to recognise that the nuclear

resource is also finite, and renewables such as bio-fuel are

not given a great deal of consideration in the report which

limits itself by taking a narrow focus and viewing the

potential threat as a “liquid fuel crises” rather than a more

wide reaching energy crises.

2.4 Drivers of the Industry – Climate Change

There is also a growing concern for the harm that burning of

fossil fuels is doing to our global environment. Under the

Kyoto Protocol Ireland agreed to a target of limiting its

greenhouse gas emissions to 13% above 1990 levels by the

first commitment period 2008-2012 as part of its contribution

to the overall EU target. Ireland ratified the Kyoto Protocol

on the 31 May 2002, along with the EU and all other Member

States and is internationally legally bound to meet the

challenging greenhouse gas emissions reduction target. To

ensure Ireland reaches its target under the Kyoto Protocol

and building on measures put in place following the

Page 16

publication of the first National Climate Change Strategy in

2000, the Government has published a new National Climate

Change Strategy in 20075. The Strategy provides a framework

for action to reduce Ireland's greenhouse gas emissions. In

this document the Government recognise that “There is now a

scientific consensus that global warming is happening, that

it is directly related to man-made greenhouse gas emissions

and that we have little time remaining to stabilise and

reduce these emissions if we are to avoid devastating impacts

on our planet”. They also concede that “There is also an

economic consensus that the costs of inaction will greatly

outweigh the costs of action and that progressive climate

change policies, based on innovation and investment in low-

carbon technology, are consistent with global economic

growth”. Later on in Section 4 the initiatives introduced by

the government to kick start this drive towards a “low-carbon

economy” as are relevant to the solid bio-fuel sector will be

reviewed.

5 Department of the Environment, National Climate Change Strategy 2007 – 2012

Page 17

2.5 Current Situation

The effects of these driving forces can bee seen on the

ground in the form of wood chip and pellet boilers becoming

increasingly popular, encouraged by the financial incentives

introduced through SEI (Sustainable Energy Ireland) in the

form of grants to assist in installation costs. In a 2006

publication Teagasc predicted that “Demand for wood pellets

and chips is set to rise rapidly in Ireland, catching up with

the rest of Europe, as more and more wood chip and pellet

heating systems are installed” 6. The same report suggests

that “Irish farmers growing energy as a crop isn’t as mad as

it sounds. Many farmers are already doing this throughout

Europe. And we only need to go back a few decades when 20% of

the agricultural land in Ireland was devoted to growing fuel:

oats to ‘fuel’ horses pulling the plough before tractors (and

fossil fuel) took over. If the same trend takes place in

Ireland as in other European countries, then energy crops may

well displace food crops on Irish farms". This report

however, does not consider the influence that large scale re-

deployment of land for non-food crops will have on grain

6 Teagasc, Wood Energy from Farm Forests, 2006

Page 18

prices or the propensity for Irish farmers to change,

particularly in the event of grain price increases due to a

reduced supply globally.

2.6 Barriers to the Industry

Sustainable Energy Ireland, (SEI), identify the barriers to

bio-energy “On the supply side, fuel resources of sufficient

quality and quantity need to be collected, transported and

stored, all at low cost. On the demand side, selling

electricity in the new market raises access and pricing

issues, and selling heat depends on local demand of

sufficient size and dependability and on appropriate

infrastructure” 7. They suggest these obstacles can be

overcome through “scale and experience, and some specific

interventions”. SEI also suggests that most bio-energy

pathways are currently “not fully competitive.” Although many

are “close to being so”, and that “supports are required to

kick-start the bio-energy market”. The National Council for

Forest Research and Development, (COFORD), point out that

“there is an increasing interest among growers of the

7 SEI, Renewable Energy Development, 2006

Page 19

prospects of trading the carbon stored in their forests”

8,and this is also true of farmers in relation to biomass

crops, but we have yet to see landowners embrace this new

alternative land use in any significant numbers.

2.7 Commentary & Conclusions

Currently Ireland imports more than 90% of its energy, with

energy demand increasing by approx. 5% per year 9. Despite

the many opposing opinions on peak oil, the real question is

not ‘if’, but ‘when’, and Ireland is in a very vulnerable

position when this happens. This and a combination of other

factors including the threat of further increases in oil

prices (analysts predict oil will soon hit $100 a barrel),

changes in the farming industry including the demise of the

sugar industry and the increasing trend towards part time

farming, may make the relatively low labour intensive

alternative of growing wood crops for energy an increasingly

attractive proposition for farmers. Naturally though, the

uptake will ultimately depend on the required returns being8 COFORD, Factors influencing farmer participation in forestry, 2002

9 SEI, Renewable Energy Development 2006

Page 20

achievable for the participants and many people are yet to be

convinced that the infrastructure, or climate, in Ireland is

suitable to allow this to happen.

The main points emerging from this section are;

The solid bio-fuel industry has been slow to take off in

Ireland in comparison to many other EU countries

The bulk of solid bio-fuel in Ireland is processed from

wood processing industry waste and used ‘in house’

Heat for domestic dwellings is a growing market for

solid bio-fuel, as is heat in the commercial sector

Current usage rates offer significant scope for increase

The main drivers of the industry at the moment are the

peak oil threat and climate change

The main focus of the government with regard to

renewable energy is on wind and tidal technologies, with

biomass considered to have less valuable potential

Many solid bio-fuel pathways are not currently

financially viable

Page 21

Section 3 - Methodology

3.1 Introduction

COFORD identifies two categories of value for the biomass

industry, i.e. the value to society and the planetary

community and value to the individual producer10. This report

will focus on the value, or opportunity, for the local

community of Westmeath through the development of the solid

bio-fuel industry in the region. In this section of the

report the methodology used to research the topic is

detailed.

3.2 The Research Question

The research question that this report seeks to address is

“What, if any, is the likely impact of the solid bio-fuel

industry on County Westmeath?”

The desired project outcome is a research report into the

development of a solid bio-fuel industry with a particular10 COFORD, Carbon credits in Ireland: issues and potentials, 2001

Page 22

focus on the potential in Co. Westmeath for value-added

enterprise. Solid bio-fuel in this case is defined as

timber, forestry or agriculture crops which can be burned to

produce renewable energy.

3.3 The Research Objectives

In answering the above question, this research document

particularly addresses the specific study objectives detailed

as follows.

3.3.1 Policy Analysis

The study will review the current framework within which bio-

energy policy is formulated with particular attention to the

Ministerial Task Force national ‘Bio-energy Action Plan’

published on March 4th, 2007, and the ‘White Paper on Energy’

published on March 12th, 2007.

Page 23

3.3.2 Resource Assessment

In order to understand the potential opportunities for this

industry it is essential to quantify how much of the resource

is produced and what amount is actually available for energy

use. It is essential to understand how this is likely to

change in the future. It is also necessary to determine the

form in which the raw material will be made available in

order to determine the level of processing which will be

required and for logistical planning purposes. In this regard

the resource available to Westmeath is assumed to include

that of the other Midland Counties as this material is easily

accessible for operators in Westmeath.

3.3.3 Market Analysis

There are a number of factors pushing the development of

biomass as a renewable energy source that suggests a great

potential for wood energy development in the region. It is

important, however, to establish the potential scale of the

Page 24

market and what is required to initiate and facilitate new

developments.

The aim of this part of the study is to define relevant

market sectors and to evaluate these. This process will

include;

Identifying current and potential future end users

Determining current and potential future

requirements

*The market analysis is extended beyond the borders of Westmeath to include the

other Midland Counties as these are readily accessible markets for Westmeath

Product.

3.3.4 Operations and Supply Chain Development

During the course of this research, different business models

are evaluated in terms of transferability and suitability to

supporting sectoral development in Westmeath. Specific

logistical issues will be identified and investigated as to

Page 25

how they interact with each other and impact on the viability

industry as a whole.

3.3.5 Economic Impact

Based on the above analysis, the study will conclude with an

examination of the potential impact that the development of

the industry will have on Westmeath. In summary this report

proposes to examine the overall potential economic impact

that the development of this industry will have on the

region.

3.4 Access and Limitations

To advance this research a strategy was developed which

utilised a range of techniques incorporating both primary and

secondary research, and employing both quantative and

qualitive research methods. My research began with an in

depth review of the literature, with a view to understanding

current position of the sector and likely future government

Page 26

and EU policy on energy and agriculture and what impact this

will have on the sector.

My ability to collect primary data was highly dependant on

gaining access to appropriate sources. Fortunately, I have

worked on the EU funded ‘Energy Crops in the Atlantic Space’

(ECAS) project which offered me the opportunity for

networking within the sector, and helped me to build up a

network of contacts within the industry who I could interview

during the course of my research.

3.5 Secondary Data

My secondary research addressed the following areas;

Analysis of national and international energy and

agriculture policy

Analysis of raw material statistics

Comparison of yields and returns with alternative land

use

Analysis and evaluation of existing and future market

Commentary on international best practice

Page 27

Relevant data gleaned from other research projects in

this area

3.6 The Interview Process

In researching this subject a number of exploratory

interviews were conducted with key industry experts as

follows:

Date: 10th November 2006

Location: Roscommon

Interview Type: Face to face, one to one, semi-

structured interview

Present: The Author, Senior executive of Bord-na-Mona

Date: 12th December 2006

Location: Roscommon

Interview Type: Face to face, group,

unstructured/informant interview

Page 28

Present: The Author, Chairman of Mid-South Roscommon

Leader Company, Past President of Agricultural Scientist

Institute, Willow Farmer, Miscanthus Farmer,

Owner/manager of a wood fuel company, Representative

from Bord-na-Mona.

Date: 18th January 2007

Location: Company Premises

Interview Type: Face to face, one to one,

unstructured/informant interview

Present: The Author, Owner/manager of a renewable energy

systems installation company operating nationally

Date: 28th Feb 2007

Location: Athlone

Interview Type: Face to face, group,

unstructured/informant interview

Page 29

Present: The Author, A leading wood consultant,

Environmental campaigner/T.V presenter and award winning

architect, Representative from Mid-South Leader Company.

Date: 24th March 2007

Venue: On site a wood product manufacturing plant

Interview Type: Face to face, group,

unstructured/informant interview

Present: The Author, A leading wood consultant, MD of a

major wood product industry and producer of wood pellet

Date: 24th March 2007

Location: Telephone

Interview Type: Telephone, one to one, semi-structured

interview

Present: The Author, Senior Teagasc wood fuel researcher

Date: 21st August 2007

Location: Business Innovation Centre

Page 30

Interview Type: Face to face, one to one, semi-

structured interview

Present: The Author, Regional Manager Business

Innovation Centre

Recognising that the selected interviewees are all experts in

their own fields it was decided to utilise unstructured or

informant interview techniques. This means that the

interviews themselves were loosely structured and conducted

in an informal way allowing the interviewer to explore the

relevant themes without a predetermined set of questions. In

essence allowing the interview to be guided by the

perceptions of the interviewee, who was permitted to talk

freely about events, experiences and express opinions on the

topic, thereby allowing the interviewer the flexibility to

react to, and further develop, points of particular interest.

In a number of cases the researcher elected to conduct these

interviews in a group setting, allowing for more free flowing

discussion. In this situation the topics were comprehensively

discussed and debated, with a variety of points emerging,

Page 31

offering the interviewer the opportunity to probe more deeply

in the exploration of concepts.

Two of the interviews which were particularly focussed on a

specific topic were conducted in a one-to-one, semi-

structured way with the interviewer having a set list of

themes and some particular questions to be covered.

The use of qualitive research interviews facilitated the

collection of a rich and detailed set of data and offered and

excellent insight into the industry. Much of the thinking in

this report is influenced by the themes raised in these

interviews that were thought provoking and relevant across

all of the research objective topics.

Some of the key themes to emerge from these interviews were

further developed and evaluated in the marketing

questionnaires, while others were very relevant to the

operations and supply chain, and economic impact sections.

Page 32

3.7 Questionnaires

In evaluating the particular market segments a survey

strategy was adopted which would allow for a large amount of

data to be collected from a large population in an economical

way and allowing for easy compilation and comparison. In this

regard a questionnaire was developed to evaluate the

residential heat market and the medium scale commercial

market. As mentioned previously, the survey questionnaire was

developed with knowledge input from prior literature based

research and from the interview process.

Based on a number of factors, a self-administered, postal

questionnaire was chosen for both groups. Due to the size of

the population in both cases the probability sample approach

was deemed appropriate. The sampling process used is outlined

below;

3.7.1 Selecting the sample size

In the case of the residential market, the sampling frame was

identified from the 2006 Census report published by the

Page 33

Central Statistics Office. This revealed the total number of

households in Westmeath and the Midlands which were used for

the basis of the survey considering that any product produced

in Westmeath would be readily accessible for the midlands

market. For the purpose of this research a 95% level of

certainty was required, and a 3% margin of error. A total of

150 questionnaires were returned.

Similarly, with the commercial, medium-scale energy user, the

sampling frame concentrated on Westmeath and the Midland

counties, and the most appropriate population was developed

based on knowledge acquired from literature and from the

interview process. Again, a 95% level of certainty and a 3%

margin of error was used as a basis for calculating the

sample size. A total of 70 questionnaires were returned.

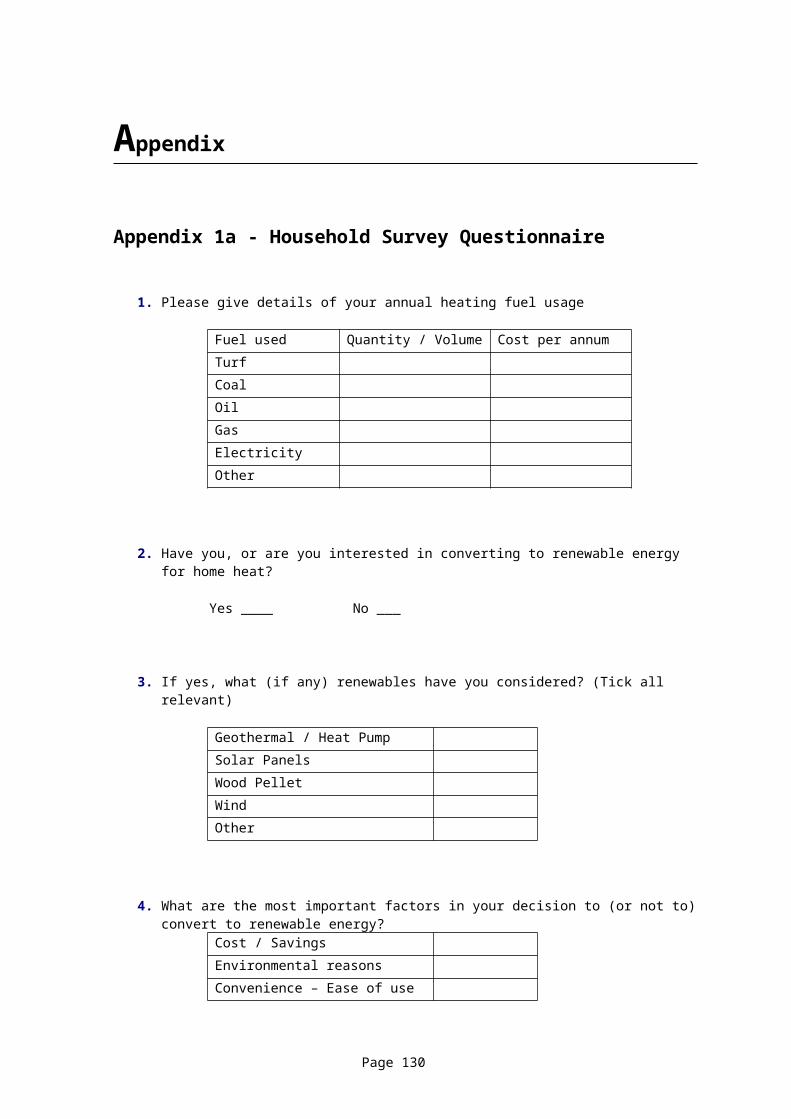

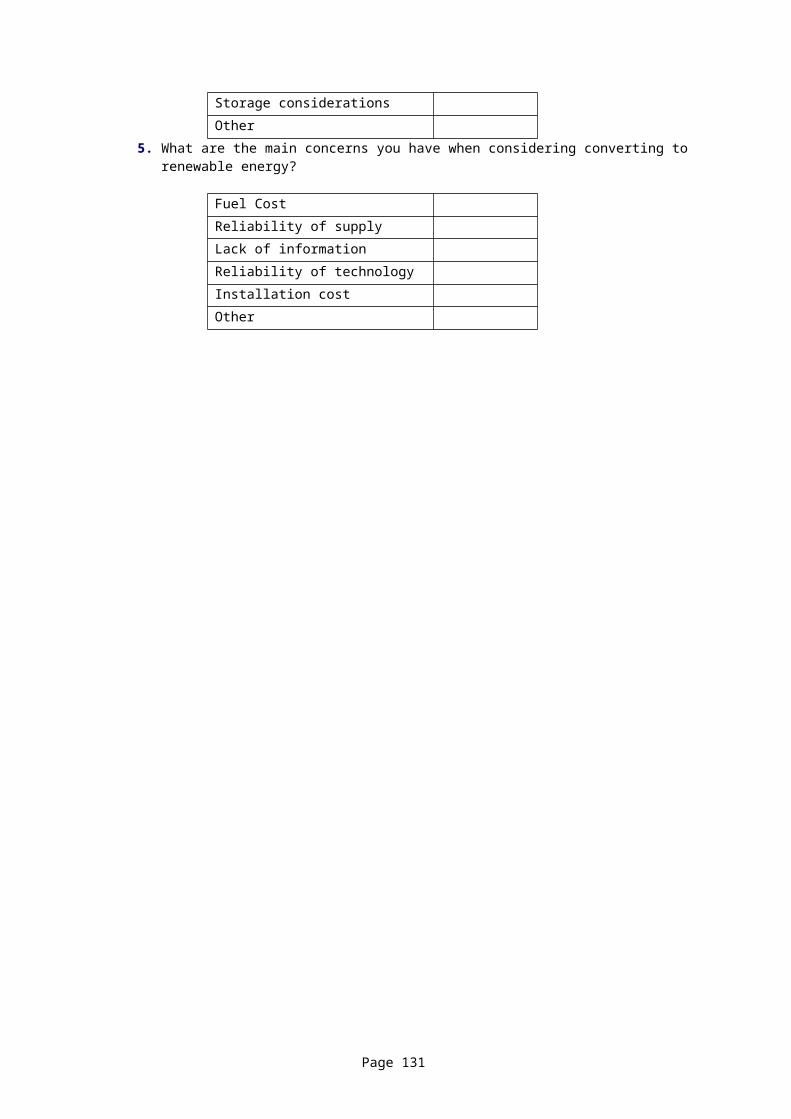

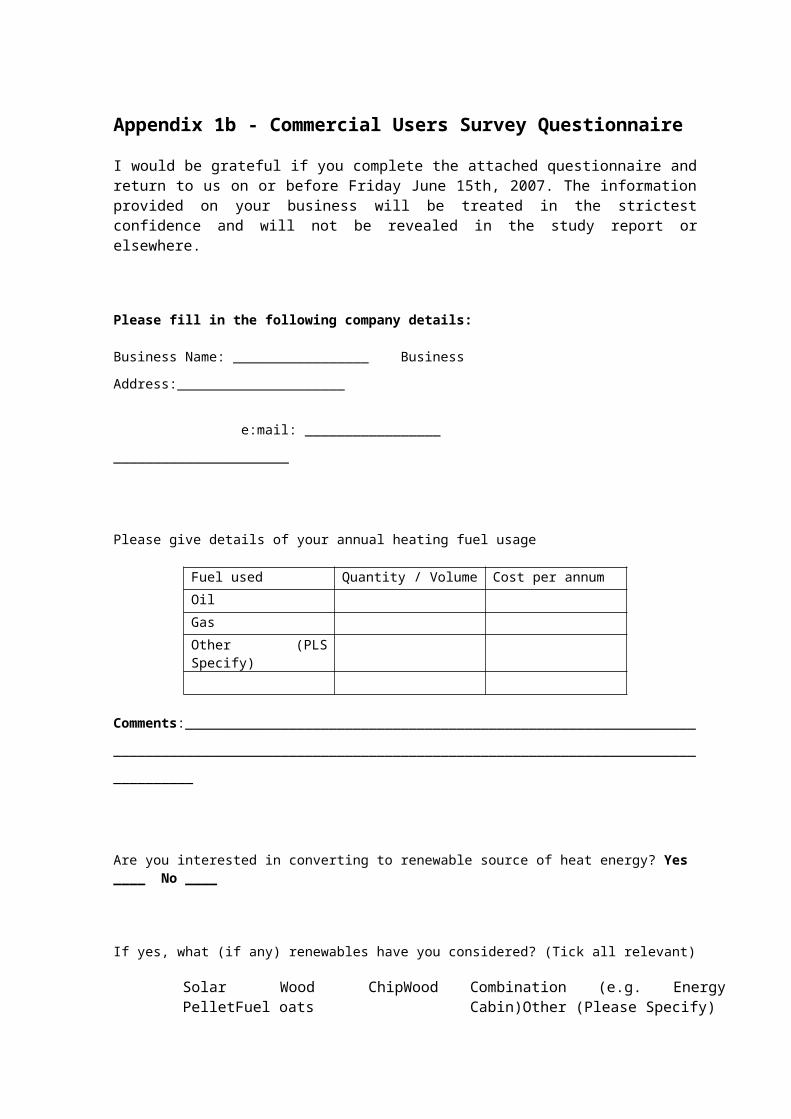

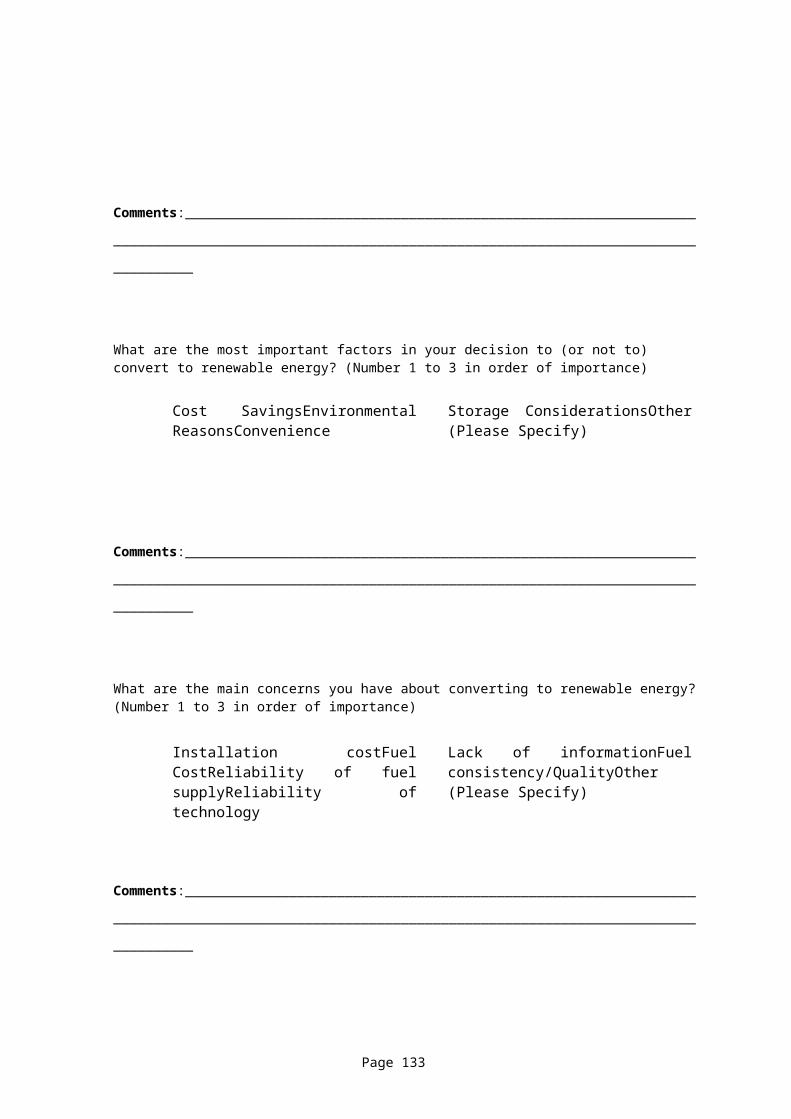

*Both Questionnaires are included in Appendix 1.

Page 34

Section 4 - Policy Analysis

4.1 Introduction

In this section Government Policy with regard to solid bio-

fuel is examined, identifying the relevant EU and Irish

targets and the various initiatives introduced to help

achieve these.

4.2 Policy Overview

Throughout Europe renewable energy is now receiving the

political and economic emphasis that will enable it to make a

meaningful contribution to reducing dangerous carbon

emissions. In parallel there is now real concern that global

fossil fuel reserves are diminishing rapidly and are held in

increasingly unstable areas of the world. In response to the

impact of this on energy prices and security of supply, the

EU is prepared to take action to secure alternative energy

supplies.

Page 35

In particular the following actions are taking place:

The EU is committed under the Kyoto Protocol to reducing

greenhouse gas emissions to 8% below 1990 levels by the

period 2008-2012

The EU has also committed to cut CO2 emissions by 20%

from 1990 levels by 2020

Overall, the EU have targeted a contribution from

renewable sources to total energy consumption of 12% by

2010

EU has further targeted a 20% overall renewable fuel use

by 202011

Within this context, Ireland is now placing considerable

emphasis on its renewable energy strategy, offering long-term

purchase contracts for renewable power and committing

significant additional funds through the national development

plan (NDP) and Sustainable Energy Ireland (SEI) to encourage

the development of this industry as a whole. In summary,

Ireland’s current position is as follows:

11 Commission of European Communities, Biomass Action Plan, 2005

Page 36

Ireland’s Kyoto target is to limit CO2 emissions growth

to 13% above 1990 levels by 2012. Ireland has already

exceeded this level and the National Development Plan

provides some €270 million to fund the purchase carbon

allowances as part of our strategy to meet the Kyoto

targets

The NDP also provides for €276 million which will fund

the large scale development of wind energy capacity and

the development of alternative sources of energy

including biomass and bio-fuels

Ireland currently imports more than 90% of its primary

fuel needs. This is amongst the highest in the EU and

means that Ireland has, potentially, the lowest security

of supply within Europe

Renewable energy in Ireland currently accounts for only

2% of usage and approximately 5 – 6% of capacity12

With a Green Party influence in Government it is expected

that Ireland will shortly be implementing new carbon taxes on

fossil fuels that will follow the “polluter pays” principle.

12 SEI, Renewable Energy Development, 2006

Page 37

Biomass fuel will be exempt from such a tax. While the

implementation of this tax may be phased and/or certain large

businesses may have allowances, the cumulative impact is

predicted to be a 15% price hike on fossil fuels in the

medium term.

In order to underpin the growth of the renewable heat sector,

the Government also introduced a capital programme in 2006 of

€65m over 5 years to promote the wood energy market from the

bottom up. Following a high level of demand in the schemes, a

further €24m was allocated for these schemes in Budget 2007

and the total funding package over the five year period now

stands at €89m. This includes grant schemes for growing

biomass crops, harvesting and processing machinery and

schemes administered through Sustainable Energy Ireland to

promote the adoption of biomass fuel technology by private,

industrial and commercial consumers.

Importantly, many of the renewable energy conversion

technologies have also reduced in price and improved in

reliability and performance making renewable energy projects

Page 38

a lower risk and better return prospect for potential

investors. As a result, there is increasing interest in this

area from a business and profitability perspective.

4.3 Bio-energy Strategy

In December 2005 the EU published a ‘Biomass Action Plan’

that focuses on ‘soft’ market support measures such as

training, standards, certification and awareness raising.

This also includes proposals for a renewable heat directive

and builds upon the Sustainable Energy Europe (2005-2008)

Campaign.13

At National Level, the Irish Government sets out its policy

for developing the renewable energy industry in the ‘National

Development Plan’14 and subsequently in the ‘Bio-energy

Action Plan’15 and ‘Energy White Paper’16 both of which were

published in 2007. The following targets relating to the

‘Heat Sector’ were outlined;

13 Commission of European Communities, Biomass Action Plan, 2005

14 National Development Plan 2007-2013 "Transforming Ireland, A Better Quality of Life for All"

15 Department of Communications, Marine and Natural Resources, Bio-energy Action Plan for Ireland, 20007

16 DCMNR, Government White Paper, Delivering a Sustainable Energy Future for Ireland,2007

Page 39

5% renewable share in the heating sector by 2010

12% renewable share in the heating sector by 2020

(taking into account the target of 30% co-firing in the

Peat Stations by 2015)

Expand the Greener Homes Scheme to provide support for

residential consumers to adopt renewable technologies

for heating. This is being delivered through an

additional €20m provided in Budget 2007

Expand the commercial Reheat Scheme to include a

combination of renewable technologies e.g. solar and

wood chip. This is being delivered through an additional

€4m provided in Budget 2007

Expand the eligibility of the commercial Reheat Scheme

to include the voluntary and community sectors.

Through these targets and support the importance of bio-

energy is set to increase in this country. However, unlike

almost all other EU countries Ireland currently has no system

of carbon taxes and this puts wood energy at a disadvantage.

The introduction of a carbon tax would go a long way towards

making many solid bio-fuel processes commercially viable.

Page 40

In relation to the large scale power generation sector, the

following targets have been set out by the government;

Expand the REFIT feed-in-tariff support scheme to

facilitate delivery of co-firing in peat stations of 30%

by 2015

33% target for renewable electricity by 2020

Expand the REFIT feed-in-tariff support scheme to

encourage waste-to-energy projects by supporting hybrid

projects.

If biomass is to play a role in meeting these targets,

particularly in the case of the existing peat fired power

stations, it will seriously impact on the availability and

cost of solid bio-fuel to other market sectors.

4.4 Expanding the Renewable Heat Sector

One of the issues identified as inhibiting the development of

the solid bio-fuel industry in Ireland is the slow pace of

progress in developing a reliable supply chain from the

private sector forest and energy crop resource. As a result

Page 41

of these supply challenges, potential users of wood biomass

have traditionally been reluctant to invest in biomass boiler

technology. To address this issue a number of grant schemes

have been developed to encourage the development of supply

chains and to directly address the high start up costs for

individuals and small businesses that opt for greener fuels.

These are discussed here in relation to incentives on both

the supply and demand side in this sector.

4.4.1 Incentives on the Supply Side

The following initiatives are directed towards the production

of biomass, and processing of solid bio-fuel.

4.4.1.1 Bio-energy Scheme for Willow and Miscanthus 2007

To increase the production of energy crops in Ireland and to

encourage alternative land use options, the Bio-energy Scheme

(BES) provides establishment grants to encourage the growing

Page 42

of willow and miscanthus for the production of biomass

suitable for use as a renewable source of energy. 17

Aid is payable on 50% of the approved costs associated with

establishing miscanthus and willow crops for biomass. The

cost of establishment is estimated at €2,900 per hectare,

giving a maximum payment rate of up to €1,450 per hectare,

with the balance to be invested by the applicant.

On the REPS area, farmers growing willow or miscanthus can

receive the bio-energy establishment grant of €1,450 per

hectare, the EU Energy Premium of €45 per hectare, a national

payment of €80 per hectare and an adjusted REPS 3 payment of

EUR155 per hectare. Under REPS 4 this payment will increase

to €189 per hectare.

The minimum allowable area per applicant eligible for the

establishment grant is 4 Ha and the maximum allowable area is

20 Ha.

17 Department of Agriculture, Terms And Conditions Bioenergy Scheme For Willow And Miscanthus, 2007

Page 43

4.4.1.2 Relief for Investment in Renewable Energy

Generation

In the Finance Act 200718, The Minister for Finance has

extended relief for investment in renewable energy generation

from 31st December 2006 to 31st December 2011.

This incentive came into force on 18th of March, 1999. The

main provisions allow a company to get a deduction of the

amount of a relevant investment made by it in a qualifying

company i.e. a company carrying out a renewable energy

project. A renewable energy project means a renewable energy

project as certified by the Minister for Communications,

Marine & Natural Resources which includes Biomass projects.

The amount that can be invested in any one project cannot

exceed 50 per cent of the relevant cost of the project, or

€9,525,000, whichever is the lesser. A company can, however,

invest up to €12.7m in various projects in a twelve month

period.

18 Finance Act, 2007, Number 11 of 2007

Page 44

4.4.1.3 Wood Biomass Harvesting Machinery Grant Scheme

In 2007 the Department of Agriculture, Fisheries and Food

took steps to stimulate the production of wood chip as a fuel

through the introduction of a limited capital grant scheme to

support the acquisition of suitable machinery. The purchase

of the following types of harvesting equipment is considered

for support under the scheme.19

Mobile Wood Chipping Units: Grant support of up to

€46,000 or an amount equivalent to 40% of the actual

cost (ex VAT) of the completed investment, whichever is

the lesser

Self-Contained Chippers: Grant support of up to €150,000

or an amount equivalent to 40% of the actual cost (ex

VAT) of the completed investment, whichever is the

lesser

For self-propelled chippers: Grant support of up to

€200,000 or an amount equivalent to 40% of the actual

cost (ex VAT) of the completed investment, whichever is

the lesser

19 Department of Agriculture, Biomass Harvesting Machinery Grant Terms And Conditions, 2007

Page 45

4.4.1.4 Afforestation Grant Rates

Afforestation Grants are paid for the creation of woodland on

an area of land. Grants are cost based and are designed to

cover all of the costs of establishing a plantation. The

Grant is paid in two installments. The first installment (75

% of the total grant) is paid after the initial work is

completed. The remaining 25% is paid after four years,

provided that the plantation is fully established. 20

There are six different rates of payment depending on the

trees planted and the land quality. The current levels of

grant payments are shown in Table 1 and 2, overleaf.

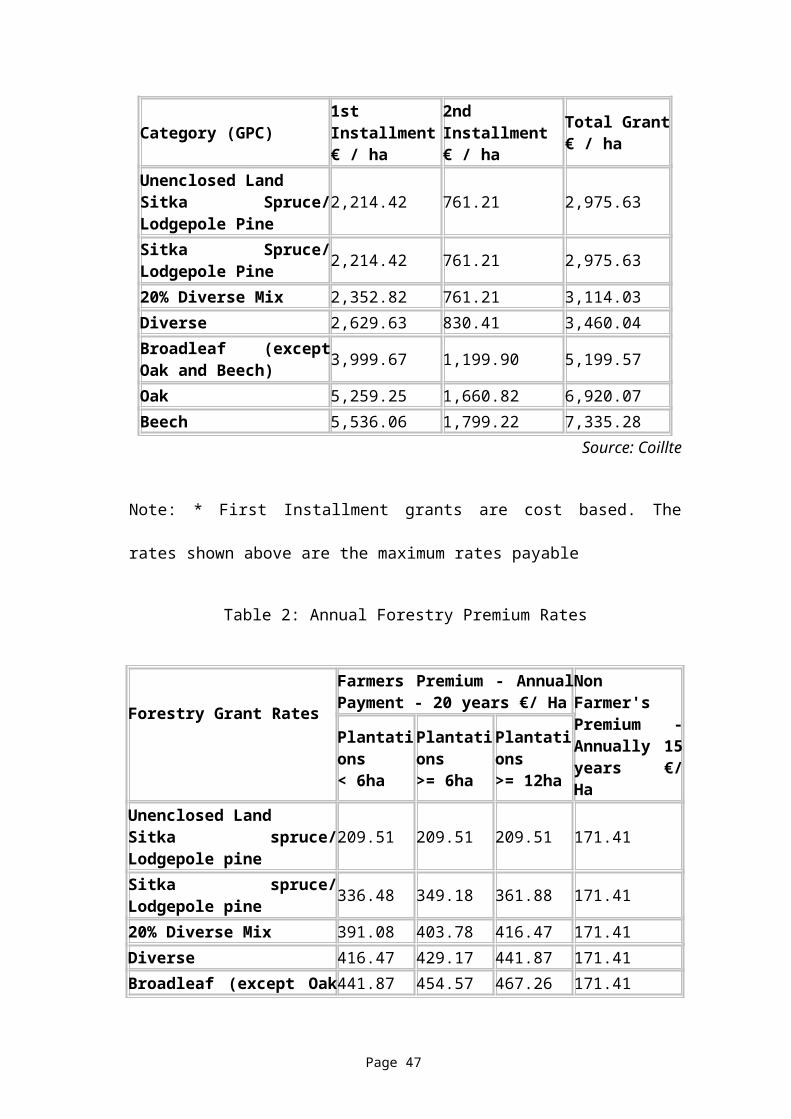

Table 1: Forestry Grant Rates

20 Coillte, 2007

Page 46

Category (GPC)1stInstallment€ / ha

2ndInstallment€ / ha

Total Grant€ / ha

Unenclosed LandSitka Spruce/Lodgepole Pine

2,214.42 761.21 2,975.63

Sitka Spruce/Lodgepole Pine 2,214.42 761.21 2,975.63

20% Diverse Mix 2,352.82 761.21 3,114.03Diverse 2,629.63 830.41 3,460.04Broadleaf (exceptOak and Beech) 3,999.67 1,199.90 5,199.57

Oak 5,259.25 1,660.82 6,920.07Beech 5,536.06 1,799.22 7,335.28

Source: Coillte

Note: * First Installment grants are cost based. The

rates shown above are the maximum rates payable

Table 2: Annual Forestry Premium Rates

Forestry Grant Rates

Farmers Premium - AnnualPayment - 20 years €/ Ha

NonFarmer'sPremium -Annually 15years €/Ha

Plantations< 6ha

Plantations>= 6ha

Plantations>= 12ha

Unenclosed LandSitka spruce/Lodgepole pine

209.51 209.51 209.51 171.41

Sitka spruce/Lodgepole pine 336.48 349.18 361.88 171.41

20% Diverse Mix 391.08 403.78 416.47 171.41Diverse 416.47 429.17 441.87 171.41Broadleaf (except Oak441.87 454.57 467.26 171.41

Page 47

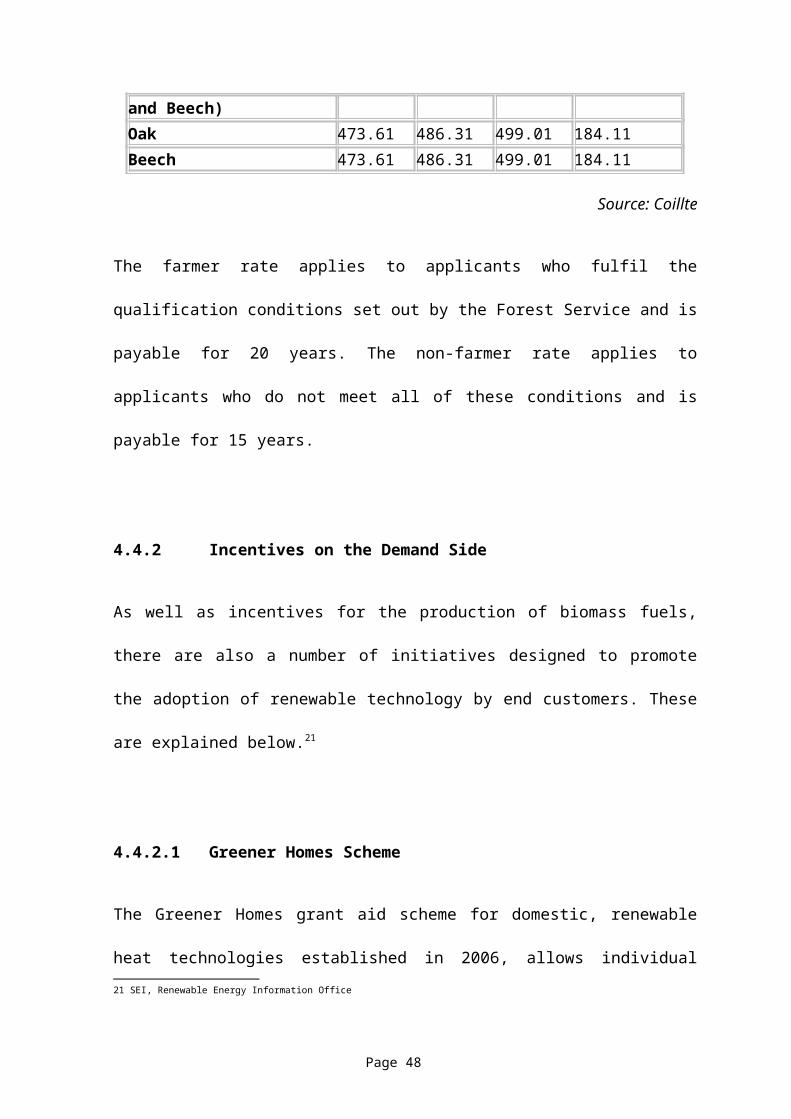

and Beech)Oak 473.61 486.31 499.01 184.11Beech 473.61 486.31 499.01 184.11

Source: Coillte

The farmer rate applies to applicants who fulfil the

qualification conditions set out by the Forest Service and is

payable for 20 years. The non-farmer rate applies to

applicants who do not meet all of these conditions and is

payable for 15 years.

4.4.2 Incentives on the Demand Side

As well as incentives for the production of biomass fuels,

there are also a number of initiatives designed to promote

the adoption of renewable technology by end customers. These

are explained below.21

4.4.2.1 Greener Homes Scheme

The Greener Homes grant aid scheme for domestic, renewable

heat technologies established in 2006, allows individual21 SEI, Renewable Energy Information Office

Page 48

householders to obtain grants for the installation of

renewable heat technologies including wood pellet stoves and

boilers, solar panels and geothermal heat pumps. Grant aid of

€1,100 to €6,500 is provided depending on the individual

technology used. The grant is intended to cover approximately

30% to 40% of the installed cost of the renewable technology.

The scheme is being rolled out over a five-year period and

was further resourced in Budget 2007 in light of substantial

demand.

Greener Homes Grant Levels include the following relevant to

the solid bio-fuel sector;

Wood chip/pellet boilers €4,200

Wood chip/pellet stoves €1,100

Wood chip/pellet stoves with back boiler €1,800

4.4.2.2 Warmer Homes Scheme

This programme provides funding to community based

organisations for the installation of energy efficiency

measures in low income dwellings in their respective

geographic areas. The homes to receive the services are

specifically identified by the community based organisations.

Page 49

4.4.2.3 House of Tomorrow

This element of the programme provides funding to developers

for the design and construction of clusters (minimum 10) of

superior energy performing housing units. Projects will be

considered where the energy performance is at least 40%

better than that required by the current building regulations

TGDL 2002 (new build). Preference is given to projects

incorporating renewable energy features including wood

fuelled heating systems.

4.4.2.4 Reheat Programme

This grant support scheme for commercial renewable heat

technologies enables companies and small businesses to obtain

grants for the installation of wood chip and wood pellet

boilers in large buildings and commercial premises. Grant aid

is available up to 30% of overall cost depending on the

overall size of the project. For example, an industrial scale

1 MW boiler, costing in the region of €250,000, could receive

Page 50

a grant of €75,000 under the scheme. The scheme is being

rolled-out over a five-year period and will support the

conversion of renewable energy in up to 600 installations

depending on overall project sizes. In Budget 2007, an

additional €4m was allocated to this scheme and it is now

being extended to enable community and voluntary groups to

apply for funding and to include other renewable

technologies.

4.4.2.5 Combined Heat and Power (CHP) Grant Scheme

The Combined Heat and Power (CHP) programme provides grants

for the installation of CHP units. These units generate

electricity at the site where the electricity is used, and

can simultaneously use the heat from the electricity

generating process. The scheme is aimed at small-scale units

(up to 1 MW), which can be deployed in hotels, leisure

centres, small hospitals, offices or commercial buildings

with a substantial heat requirement. Such units can be

fuelled by fossil fuels such as gas, as well as biomass (wood

and waste) products. The programme is running over a five-

Page 51

year period. The CHP programme aims to deliver 10 to 15 MWe

Biomass CHP, and up to 200 small-scale fossil fuel CHP

installations generating 10 to 20MWe of high efficiency CHP.

4.5 Outcomes to Date

Through the Bio-energy Scheme for Willow and Miscanthus,

applications have been approved in 2007 for 859.155 Ha of

Miscanthus and 107.56 Ha Willow. This represents a total of

112 different applications. A significant number of other

applications were submitted late or withdrawn and the

expectation is that these will be resubmitted in 2008.

(Source Department of Agriculture and Food)

The SEI schemes have also been heavily subscribed, in

particular the Greener Homes programme, which has attracted

over 14,000 applications to date. Biomass boilers and stoves

are proving to be the preferred technology with applications

in this category at 45% of overall demand, i.e. circa 6,000

applications with approximately 1,750 systems installed since

the launch of the programme. Under the new Reheat programme

aimed at commercial ‘medium scale’ users, SEI have received

Page 52

around 90 applications, the Reheat programme replaced the

Pilot Bioheat Programme, under which SEI received around 20

applications with 10 boilers installed. Prior to the launch

of these two programmes the best estimate for installations

is around 200 stoves and less than 50 boilers.

In heating terms alone, the Biomass element of these

programmes is expected to displace the equivalent of 36

million litres of heating oil per annum. The CHP programme,

together with the Bioheat programme, when fully deployed,

will displace almost 100 million litres of heating oil per

annum, which represents 13% of the heating oil consumed in

the commercial sector in 2004. This level of market growth

also represents a very significant development opportunity

for renewable technology suppliers, renewable technology

installers and renewable fuel supply companies.

4.6 Interview comments

“There is not enough awareness in the mainstream, people need

to be convinced that solid bio-fuel is the best option going

forward if they are to make the investment necessary. A

Page 53

culture change is needed if the industry is to succeed, this

will take a major financial incentive which does not

currently exist. If this is to be rectified it will most

likely be through taxation.”

“Real leadership is needed but our government is afraid to

rock the boat and there are too many vested interests. Our

energy costs are currently too cheap for the solid bio-fuel

industry to make any real impact, fossil fuels are expected

to increase dramatically but prices are unstable which

introduces uncertainty into the equation, the next ten years

is going to be critical and I believe that a carbon tax needs

to be introduced on a phased basis over this period, fixing

the cost of oil so that consumers know exactly what oil will

cost into the future, taking the uncertainty away and

allowing people to make a balanced decision. The income from

the carbon tax must be ring fenced for re-investment in

renewable energy solutions.”

“People are becoming more conscious of the environment and

becoming more aware that there is a problem, that climate

Page 54

change is happening, and the need to put in place policies

that are necessary for the environment and the economy”

4.7 Commentary & Conclusions

Ultimately, oil availability and cost will determine the

success or failure of the solid bio-fuel industry. Taking

Sweden as a case study, political decisions have set the

rules of the energy fuel market in that country through the

implementation of energy and environmental taxes. Considering

only fuel cost, wood pellet is more expensive than oil and

coal since pellet heating requires extra equipment for fuel

handling, more work effort, etc. The introduction of emission

taxes on carbon dioxide and sulphur dioxide bridged this

price gap by making it more expensive to fire fossil fuels

and hence the demand grew for the ‘less expensive’ biomass

fuels. If a carbon tax is introduced in Ireland in the near

future many solid bio-fuel pathways will become more

financially viable and solid bio-fuel will become a

significantly more attractive option for many people and

businesses.

Page 55

The main points emerging from this section are;

In Ireland and the EU renewable energy policy is geared

towards Kyoto targets

Irish policy relevant to the solid bio-fuel sector is

set out in the ‘National Development Plan’, ‘The Bio-

energy Action Plan’ and ‘The Energy White Paper’

A range of financial incentives have been introduced to

help develop this industry but many people involved in

the sector don’t believe that enough is being done

Page 56

Section 5 - Resource Assessment

5.1 Introduction

Solid bio-fuel is derived from recently grown organic matter

such as wood (e.g. sawdust, forest thinning), energy crops

(fast growing trees like poplar or willow, and grasses like

elephant grass and reed canary grass), and grain (including

oats and barley). The following biomass resources have been

identified which should be readily accessible to the solid

bio-fuel industry;

Forestry co-products including;

o First thinning of plantations

o Forest residues left on-site following final

felling

Post consumer wood waste including;

o Sawdust, bark and off-cuts arising from sawmilling

and board manufacture

o Untreated recycled wood

Page 57

Dedicated energy crops such as Willow (Short Rotation

Coppice), Reed Canary Grass, Miscanthus and Grain / Oats

In this section the raw material resources available in

Westmeath for the solid fuel production is evaluated.

5.2 Forestry Co-products

Wood is by far the largest biomass resource and it is in

plentiful supply both globally and in Ireland. National

afforestation policies across Western Europe over the past 50

years have resulted in an abundant and increasing supply of

wood with the following implications:

In the growing/harvesting of forest and the production

of finished timber much wood volume is produced as low

value by-products. Increasingly, there is an oversupply

of low value and waste product within the industry

These low value products are a good fuel. The

technologies to process and convert wood fuel into heat

and power are well proven, with consistently greater

than 90% energy conversion efficiency now possible for

Page 58

heating applications and 30% conversion efficiency for

electricity production22

60% of our overall energy requirement is in the form of

heat, not electricity, making wood an ideal renewable

fuel source to fulfil this requirement. Using biomass

for energy is carbon neutral, i.e. the organic matter

absorbs CO2 from the atmosphere as it grows and releases

it when it is converted to energy, with a net zero

effect

The main source of wood biomass in Ireland comes from the

national forest estate, currently 710,000 Ha. A potential 0.5

million tonnes of wood residues is available from this source

annually for energy recovery. Currently, there are sufficient

supplies of raw materials to supply the wood energy and wood

processing sectors.

The National Forestry Inventory (NFI) undertaken by the

Forest of the Department of Agriculture, Fisheries and Food

confirm that the total forest area in Ireland now stands at

22 Sorensen, B., Renewable Energy, Its Physics, Engineering, Environmental Impacts, Economics &

Planting.2004

Page 59

10% of the total land area of which 57% is in public

ownership and 43% in private ownership. Almost two thirds of

national forest estate is less than twenty years old.

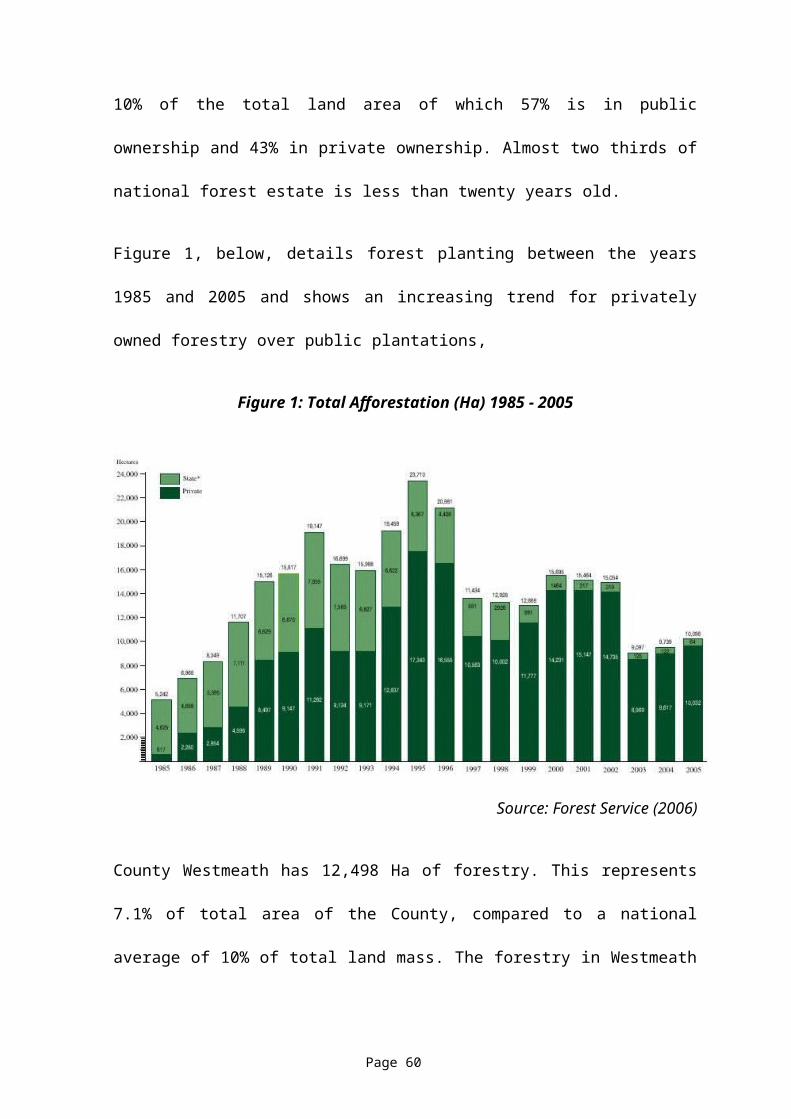

Figure 1, below, details forest planting between the years

1985 and 2005 and shows an increasing trend for privately

owned forestry over public plantations,

Figure 1: Total Afforestation (Ha) 1985 - 2005

Source: Forest Service (2006)

County Westmeath has 12,498 Ha of forestry. This represents

7.1% of total area of the County, compared to a national

average of 10% of total land mass. The forestry in Westmeath

Page 60

is a mix of private and public plantations, with 7,787 Ha in

private ownership and only 4,711 Ha of public forestry.

Private plantations in Westmeath are divided between 34

owners. 28 holdings by full-time farmers, 3 by part time

farmers and 3 by non-farmers.

The Midlands Counties of Longford, Westmeath, Offaly, Laois

have a total combined forestry resource of 83,683 Ha

representing 9.3% of total land mass. This resource is evenly

shared between public and private plantations. In private

ownership there are 121 holdings, 91 by full time farmers, 17

by part time farmers and 13 by non-farmers.

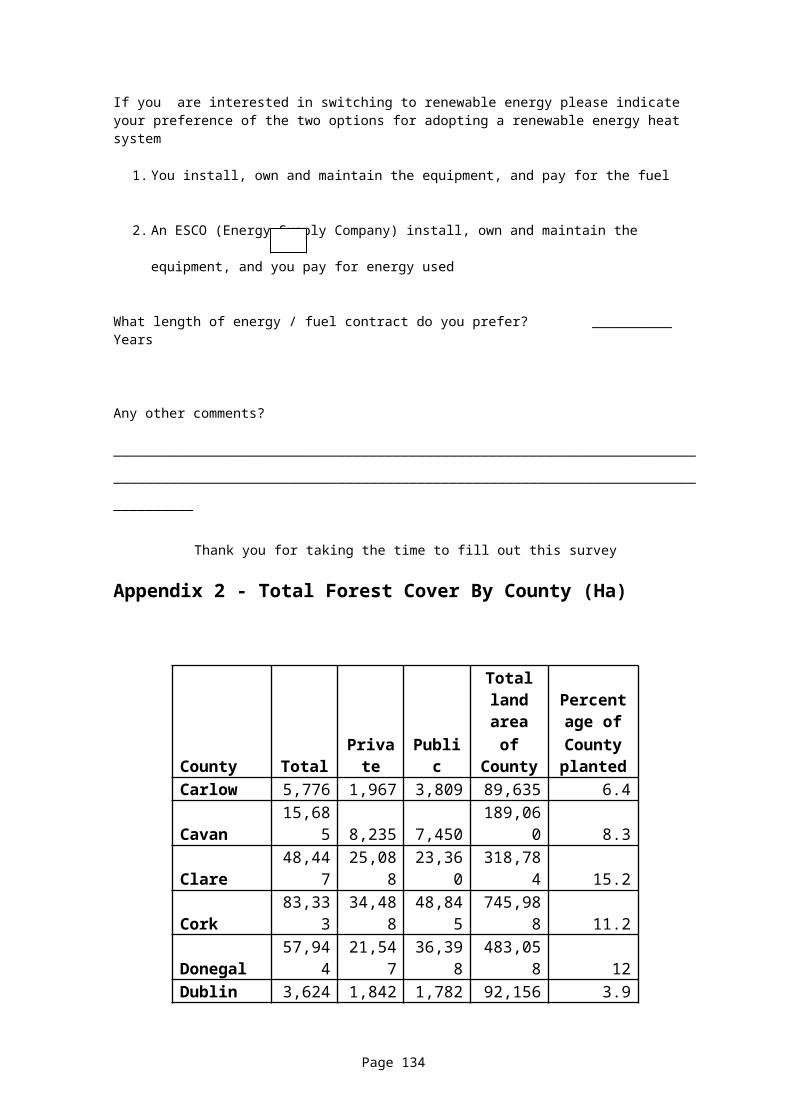

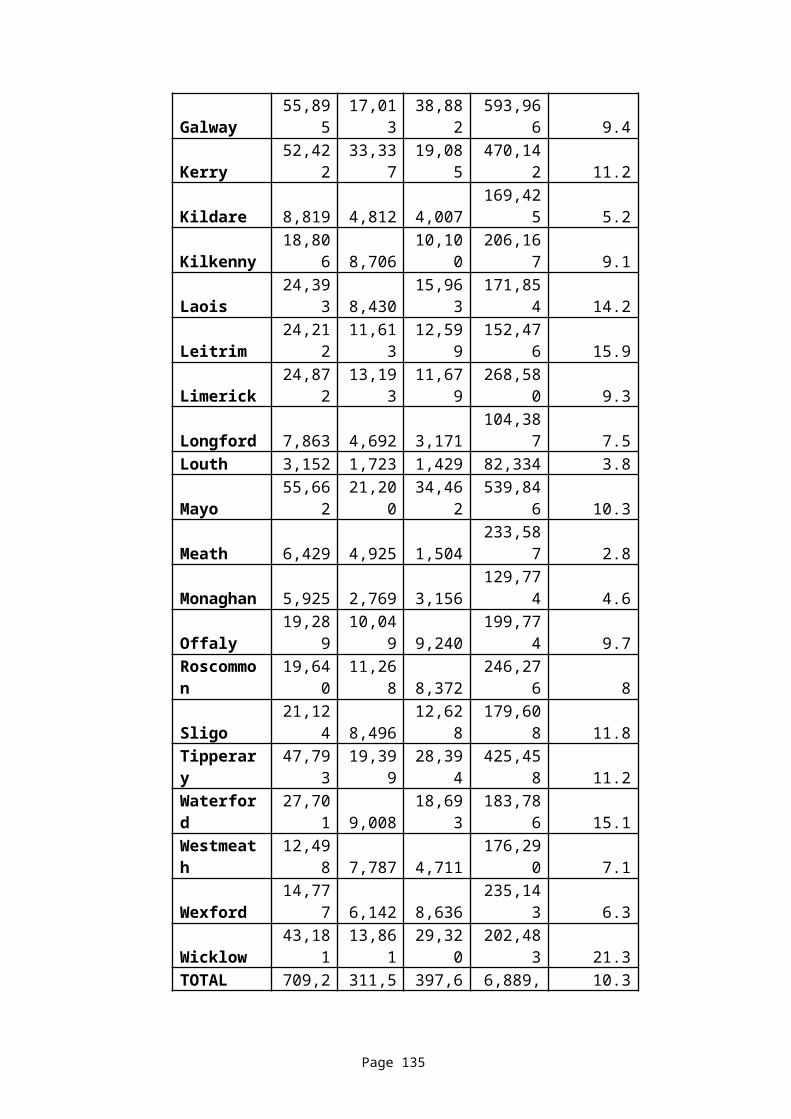

Appendix 2, presents comparative data on current forestry

cover for all Counties in Ireland. To sustain the supply of

pulpwood and thinning, the levels of forestry need to be

maintained and we can see from the information presented that

levels of forestry in the country is increasing annually,

albeit at a slowing pace. We also see evidence of a growing

trend towards private plantations.

It must be noted though that not all forestry product is

suitable for use as bio-fuel as good quality timber is much

Page 61

more valuable in other industry sectors. That which is

suitable for wood energy includes pulpwood (harvested from

the top section of trees) and forest thinning (removal of

smaller, poorly formed trees from the plantation).

5.3 Post Consumer Wood Waste

This includes recycled timber, sawmill co-products and

arboricultural arisings, each of which is discussed in more

detail below

5.3.1 Recycled Timber

A further potential source of wood fuel is recycled timber

that can be processed into woodchips or pellets. Timber can

be recovered from a variety of sources including used

pallets, construction waste and packaging. Most recent data

published by the EPA on the disposal and recovery of

municipal waste reveals that 213,926 Tonnes of wood waste was

generated in 200523. Of this 13,939 Tonnes was sent to land

23 EPA, National waste Report

Page 62

fill and a further 17,492 Tonnes was exported to the UK. This

wood was generated from the following waste streams;

Household Waste – 19,010Tonnes

Commercial waste (Including construction) – 74,036

Packaging waste (from commercial sector) – 120,880

The EPA estimated that nationwide, in 2005, about 125,000

Tonnes of mixed wood was recycled. Of this 52% was untreated

and therefore suitable for use as fuel.

The following are some of the important things to consider

when deciding whether recycled material is suitable for fuel

include:

Contamination: the material should not be contaminated

with paint or other chemical products

Metal content: all metal must be removed from the

material during the processing as this can damage auger

feed mechanisms and boiler grates

Page 63

5.3.2 Sawmill Co-Products

When round timber is processed through a sawmill it is only

possible to convert a proportion of the log, typically

between 40% and 60%, into a sawn timber product. The rest

forms a co-product of the sawmilling process such as

woodchips or shavings, sawdust, slab wood and other off-cut

material. There may be existing markets for these co-

products, such as the use of sawdust for agricultural

bedding, but they can also be turned into wood fuel by

further processing. Dry sawdust can be processed into wood

pellets, while off-cuts and slab wood can be processed into

woodchips.

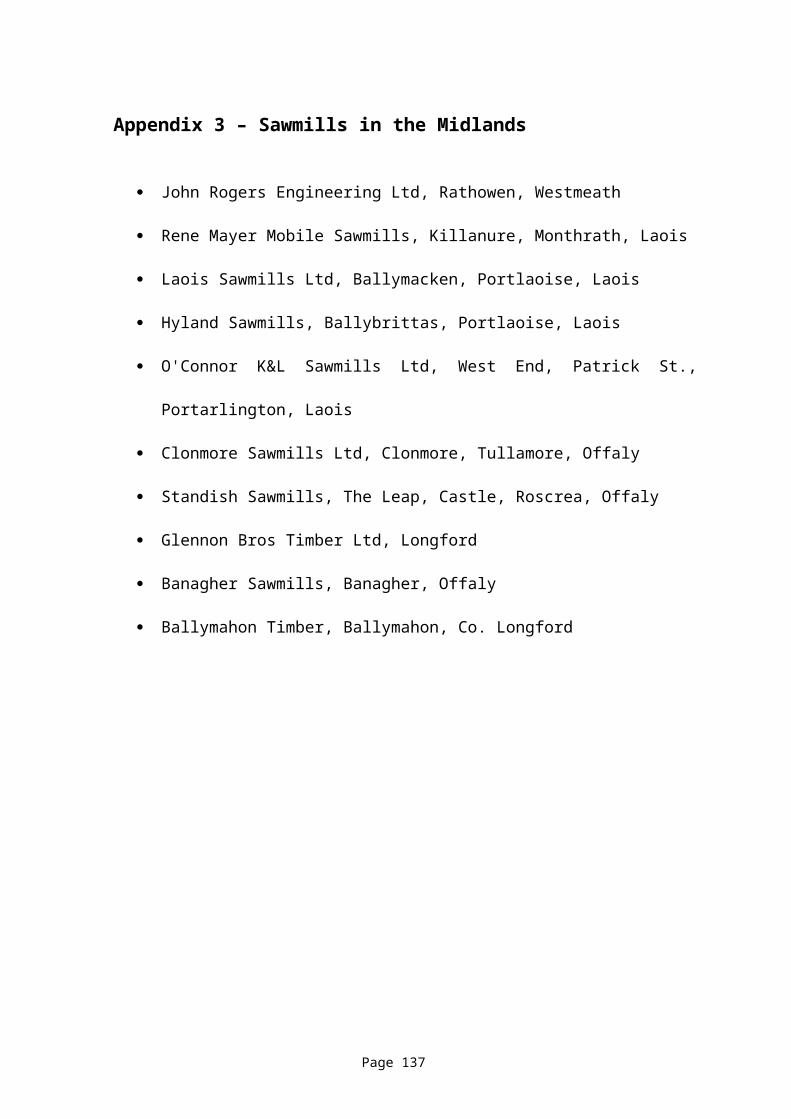

There are a number of sawmills in the midlands counties which

will have a supply of potential wood fuel raw material. These

are listed in Appendix 3.

5.3.3 Arboricultural Arisings

The term arboricultural arisings encompasses all the material

produced during arboricultural, or tree surgery, operations

and can include stems, branches and leaf material. Often the

Page 64

arisings are chipped on site or taken to land-fill sites.

However, some of this material may be suitable for processing

into wood fuel, most commonly woodchips, potentially turning

a costly waste material into a valuable product. The key

consideration here is in the logistics involved in the

collection and drying of the available material and in the

delivery to the end user. Typically the raw material is

sourced in many disparate locations, often in small

quantities, and the ability to efficiently collect and

transport the material to a central location for processing

is essential in making this source part of a viable supply

chain.

5.4 Dedicated Energy Crops

Energy crops are plants that are cultivated for the purpose

of producing energy. Energy crops can be classified into

those providing;

Solid fuels for direct combustion, thermal processing

(to yield solid, liquid and gaseous fuels) and

electricity generation, and

Page 65

Liquid fuels, notably bio-ethanol and bio-diesel.

Solid fuel crops include Willow SRC, Miscanthus, Reed Canary

Grass and whole-crop cereals. At present there is a limited

resource of dedicated energy crops in Westmeath and the

Midlands. Westmeath has only 4 Ha of Miscanthus planted in

April 2006 and no Willow. Through the Bio-energy Scheme of

the Department of Agriculture, Fisheries and Food,

applications for establishment grants have been approved for

24 Ha of Miscanthus and 6.5 Ha of Willow in County Westmeath.

In the Midlands applications were approved for a combined

total of 61.71 Ha Miscanthus and 6.5 Ha Willow.

Substantial potential exists for increasing this acreage as

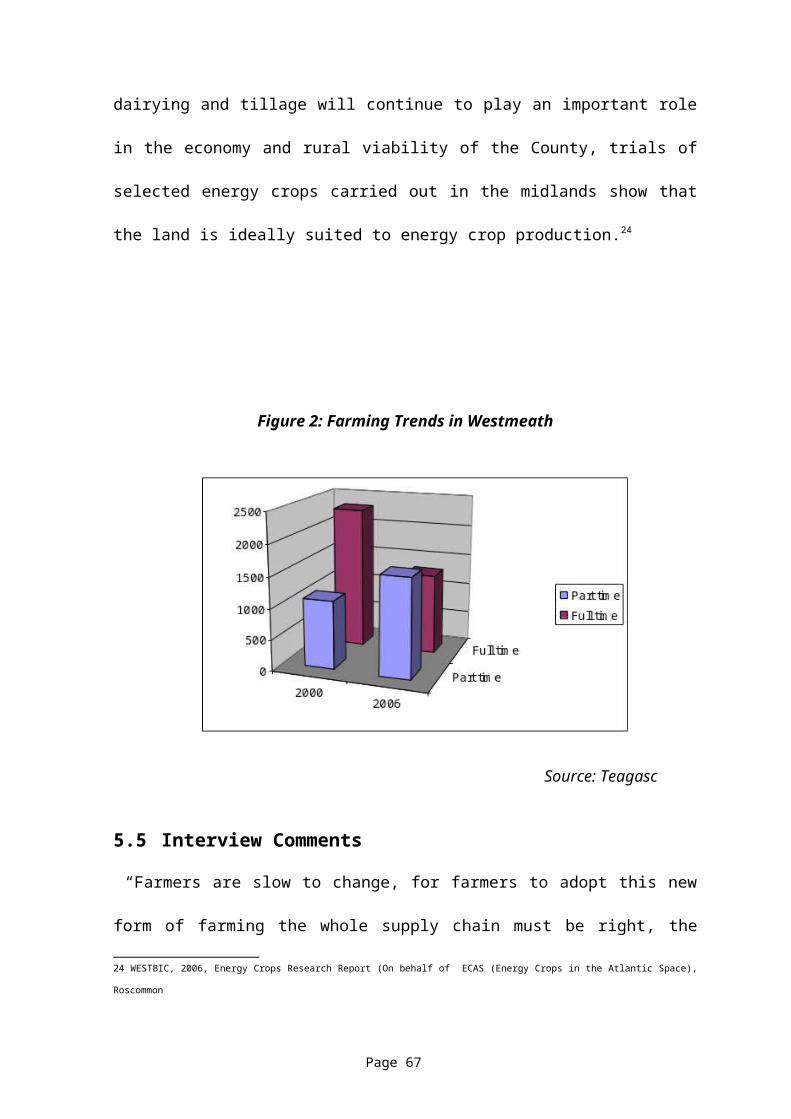

energy crop cultivation is a low maintenance form of farming

that can be very suitable for part time farmers. The trend in

Westmeath is towards part time farming as more and more

farmers are finding the need to supplement their farm income

with jobs off the farm. We can see from Figure 2, overleaf,

that the current situation is that there are now more part-

time farmers (1,600) in the County than full time farmers

(1,300). While the importance of dry-stock cattle/sheep,

Page 66

dairying and tillage will continue to play an important role

in the economy and rural viability of the County, trials of

selected energy crops carried out in the midlands show that

the land is ideally suited to energy crop production.24

Figure 2: Farming Trends in Westmeath

Source: Teagasc

5.5 Interview Comments

“Farmers are slow to change, for farmers to adopt this new

form of farming the whole supply chain must be right, the

24 WESTBIC, 2006, Energy Crops Research Report (On behalf of ECAS (Energy Crops in the Atlantic Space),

Roscommon

Page 67

farmers will need to be 150% sure before they will change in

any significant numbers”

“I have a hundred acres of good grass land. If I do a very

good job working it I can make a living off it. If I do a

very good job working somewhere else I can make a living too

and if I can have a supplementary income from energy crops

without investing too much time or effort then I am better

off.”

“Regarding the food versus fuel issue, in Europe and Ireland

there is a great deal of set aside land which will come back

into farming. We need to become more self sufficient in terms

of food and fuel. It’s about getting the balance right.”

“The main concern for the wood pellet industry in this

country is suitable raw material resource in the form of

sawdust. ‘Medite’ and other companies in that industry take

most of this suitable material so there is competition for

the material. I can foresee a situation where these companies

will lock up all the saw mills in contracts for this

material”

Page 68

“If using waste or recycled timber for fuel it is extremely

important to separate out any pressure treated, or painted

material. Pallets and crates could be sprayed with

insecticide, there are numerous things that need to be

screened for.”

5.6 Commentary & Conclusions