Highfield Resources Ltd Potash Market Fundamentals Hayden Locke – Head of Corporate Development November 2015 ASX Code: HFR

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Highfield Resources LtdPotash Market Fundamentals

Hayden Locke – Head of Corporate Development

November 2015

ASX Code: HFR

Highfield Resources Ltd.

POTASH MARKET FUNDAMENTALS

2

CONTENTS

1. Introduction

2. Potash is not iron ore

3. Types of potash

4. Supply and Demand Fundamentals

5. Where is the marginal unit of supply?

6. Why is there current price weakness?

7. What is Highfield´s strategic position?

8. Summary

9. Questions

1. Introduction

3

• Potash is not iron ore

• The marginal unit of production is controlled by some of the largest producers

• The marginal unit of production has no incentive to increase supply as it cannot displace any production of significance

• The potash market overcapacity is generally overstated

• The decline of the Canadian dollar over the past 12 months, and the associated cost implications for PotashCorp and

Mosaic cannot be overstated in terms of its impact on short term potash prices

• Highfield is in an outstanding strategic position with its high margin potash projects in Spain

2. Potash is not iron ore

Although both bulks and logistics is key, the market structure is fundamentally different

70% of demand is seaborne to

China

85% of demand if you include

Japan, Korea and Taiwan

Cost curve is much easier to

define

Pilbara is both lowest cost and

closes to centre of demand

The cost curve is much easier to define in iron ore

4

2. Potash is not iron ore

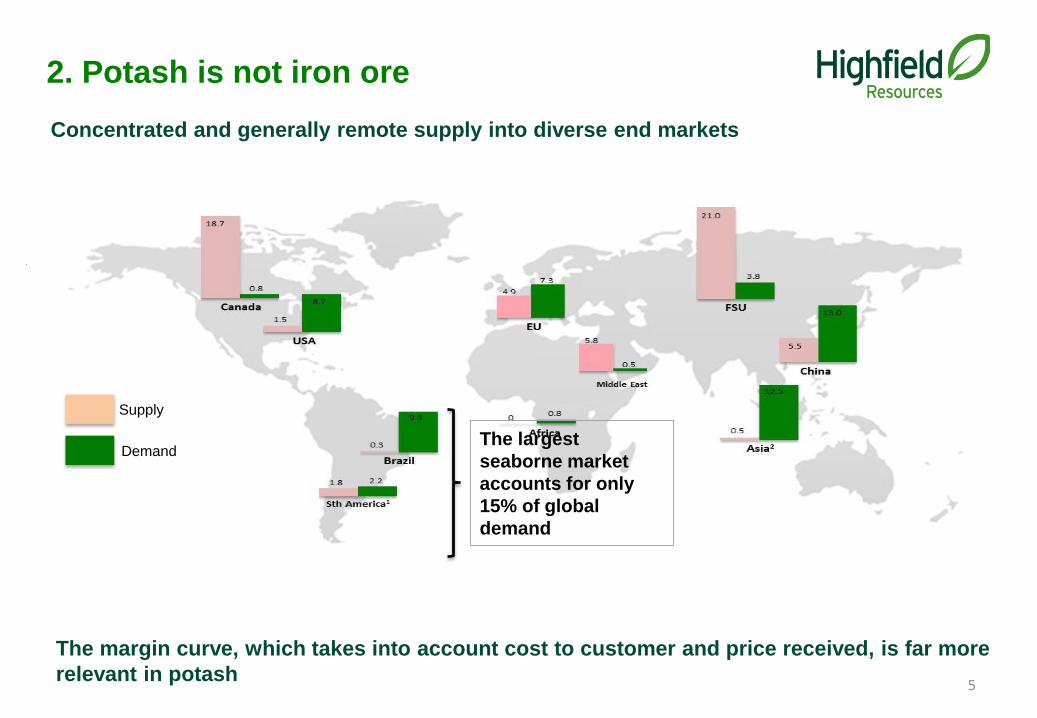

Concentrated and generally remote supply into diverse end markets

The margin curve, which takes into account cost to customer and price received, is far more

relevant in potash

Supply

DemandThe largest

seaborne market

accounts for only

15% of global

demand

5

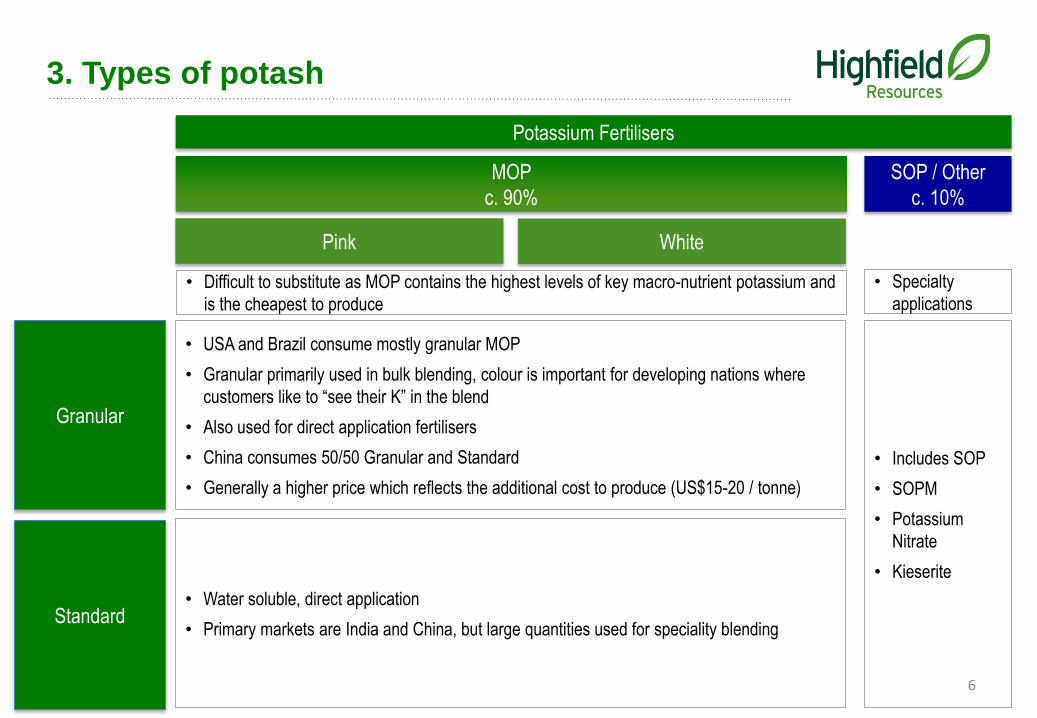

3. Types of potash

MOP

c. 90%

Pink White

SOP / Other

c. 10%

Granular

Standard

• USA and Brazil consume mostly granular MOP

• Granular primarily used in bulk blending, colour is important for developing nations where

customers like to “see their K” in the blend

• Also used for direct application fertilisers

• China consumes 50/50 Granular and Standard

• Generally a higher price which reflects the additional cost to produce (US$15-20 / tonne)

• Water soluble, direct application

• Primary markets are India and China, but large quantities used for speciality blending

Potassium Fertilisers

• Includes SOP

• SOPM

• Potassium

Nitrate

• Kieserite

• Difficult to substitute as MOP contains the highest levels of key macro-nutrient potassium and

is the cheapest to produce

• Specialty

applications

6

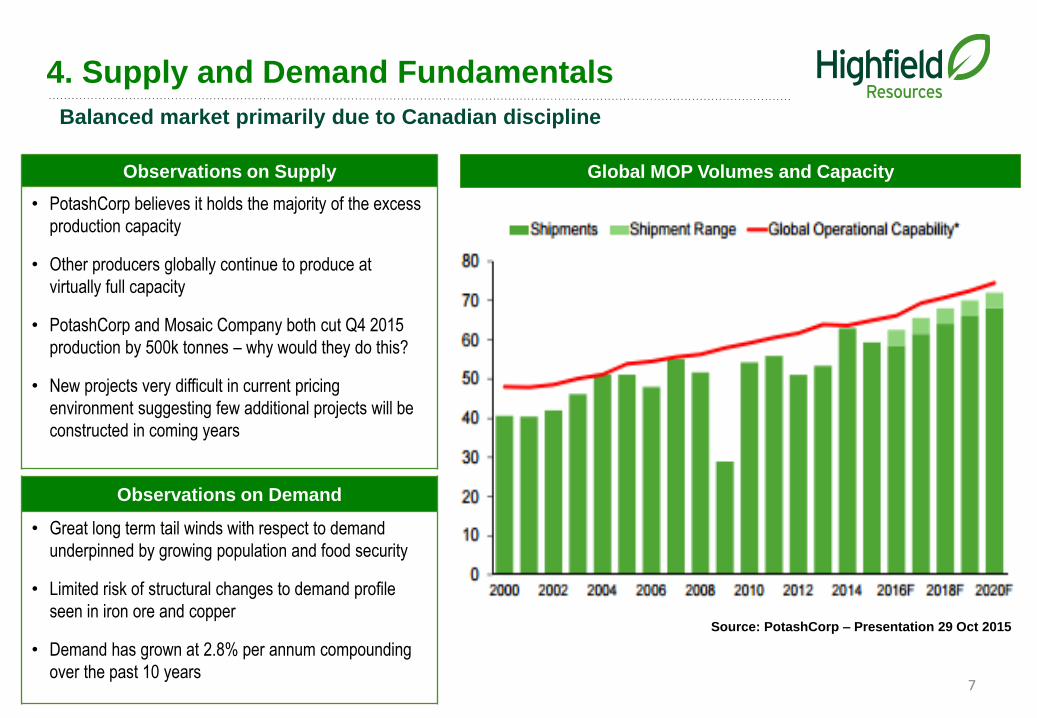

4. Supply and Demand Fundamentals

7

Global MOP Volumes and Capacity

Source: PotashCorp – Presentation 29 Oct 2015

Observations on Supply

• PotashCorp believes it holds the majority of the excess

production capacity

• Other producers globally continue to produce at

virtually full capacity

• PotashCorp and Mosaic Company both cut Q4 2015

production by 500k tonnes – why would they do this?

• New projects very difficult in current pricing

environment suggesting few additional projects will be

constructed in coming years

Balanced market primarily due to Canadian discipline

Observations on Demand

• Great long term tail winds with respect to demand

underpinned by growing population and food security

• Limited risk of structural changes to demand profile

seen in iron ore and copper

• Demand has grown at 2.8% per annum compounding

over the past 10 years

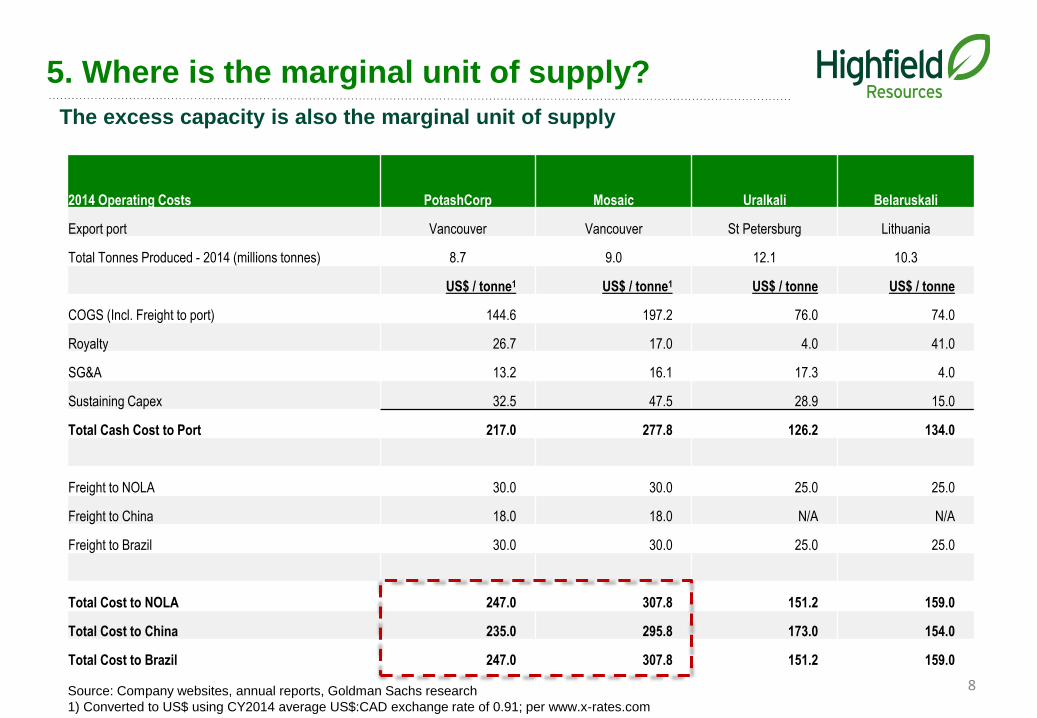

5. Where is the marginal unit of supply?

The excess capacity is also the marginal unit of supply

2014 Operating Costs PotashCorp Mosaic Uralkali Belaruskali

Export port Vancouver Vancouver St Petersburg Lithuania

Total Tonnes Produced - 2014 (millions tonnes) 8.7 9.0 12.1 10.3

US$ / tonne1 US$ / tonne1 US$ / tonne US$ / tonne

COGS (Incl. Freight to port) 144.6 197.2 76.0 74.0

Royalty 26.7 17.0 4.0 41.0

SG&A 13.2 16.1 17.3 4.0

Sustaining Capex 32.5 47.5 28.9 15.0

Total Cash Cost to Port 217.0 277.8 126.2 134.0

Freight to NOLA 30.0 30.0 25.0 25.0

Freight to China 18.0 18.0 N/A N/A

Freight to Brazil 30.0 30.0 25.0 25.0

Total Cost to NOLA 247.0 307.8 151.2 159.0

Total Cost to China 235.0 295.8 173.0 154.0

Total Cost to Brazil 247.0 307.8 151.2 159.0

Source: Company websites, annual reports, Goldman Sachs research

1) Converted to US$ using CY2014 average US$:CAD exchange rate of 0.91; per www.x-rates.com

8

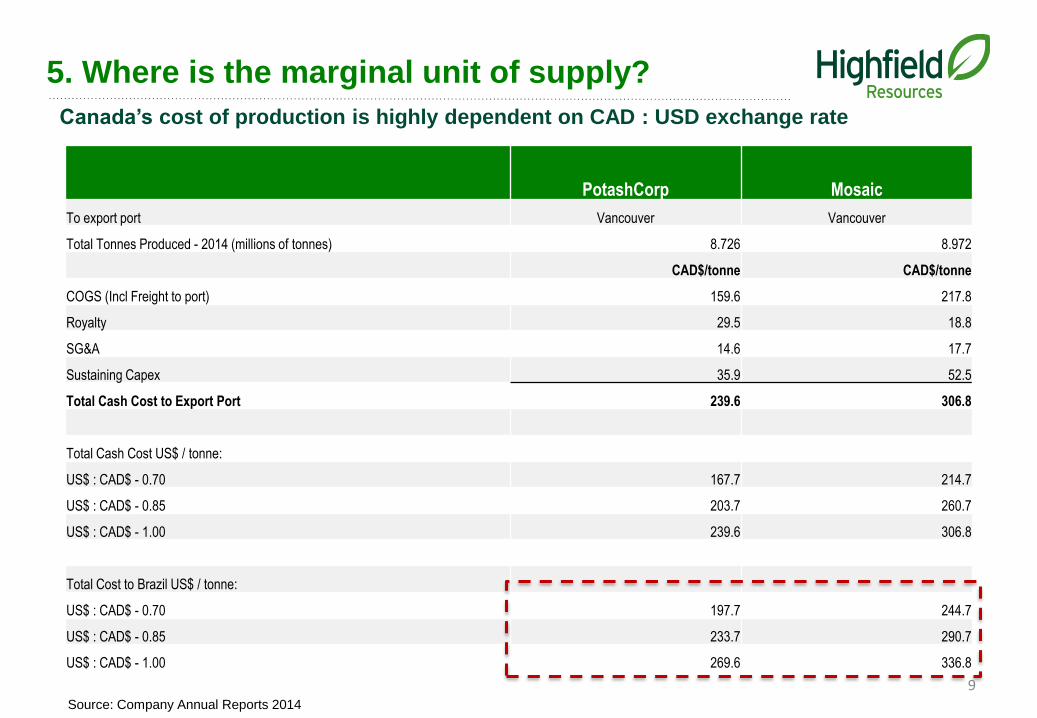

5. Where is the marginal unit of supply?

Canada’s cost of production is highly dependent on CAD : USD exchange rate

PotashCorp Mosaic

To export port Vancouver Vancouver

Total Tonnes Produced - 2014 (millions of tonnes) 8.726 8.972

CAD$/tonne CAD$/tonne

COGS (Incl Freight to port) 159.6 217.8

Royalty 29.5 18.8

SG&A 14.6 17.7

Sustaining Capex 35.9 52.5

Total Cash Cost to Export Port 239.6 306.8

Total Cash Cost US$ / tonne:

US$ : CAD$ - 0.70 167.7 214.7

US$ : CAD$ - 0.85 203.7 260.7

US$ : CAD$ - 1.00 239.6 306.8

Total Cost to Brazil US$ / tonne:

US$ : CAD$ - 0.70 197.7 244.7

US$ : CAD$ - 0.85 233.7 290.7

US$ : CAD$ - 1.00 269.6 336.8

Source: Company Annual Reports 2014

9

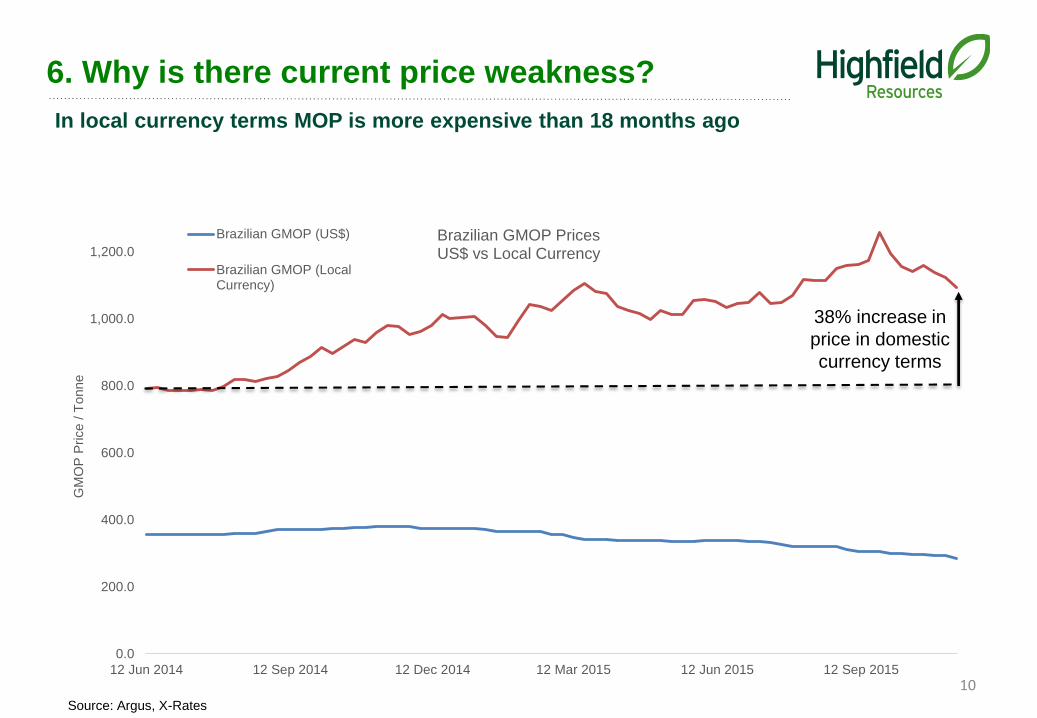

6. Why is there current price weakness?

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

12 Jun 2014 12 Sep 2014 12 Dec 2014 12 Mar 2015 12 Jun 2015 12 Sep 2015

GM

OP

Price /

Tonne

Brazilian GMOP PricesUS$ vs Local Currency

Brazilian GMOP (US$)

Brazilian GMOP (LocalCurrency)

38% increase in

price in domestic

currency terms

In local currency terms MOP is more expensive than 18 months ago

Source: Argus, X-Rates

10

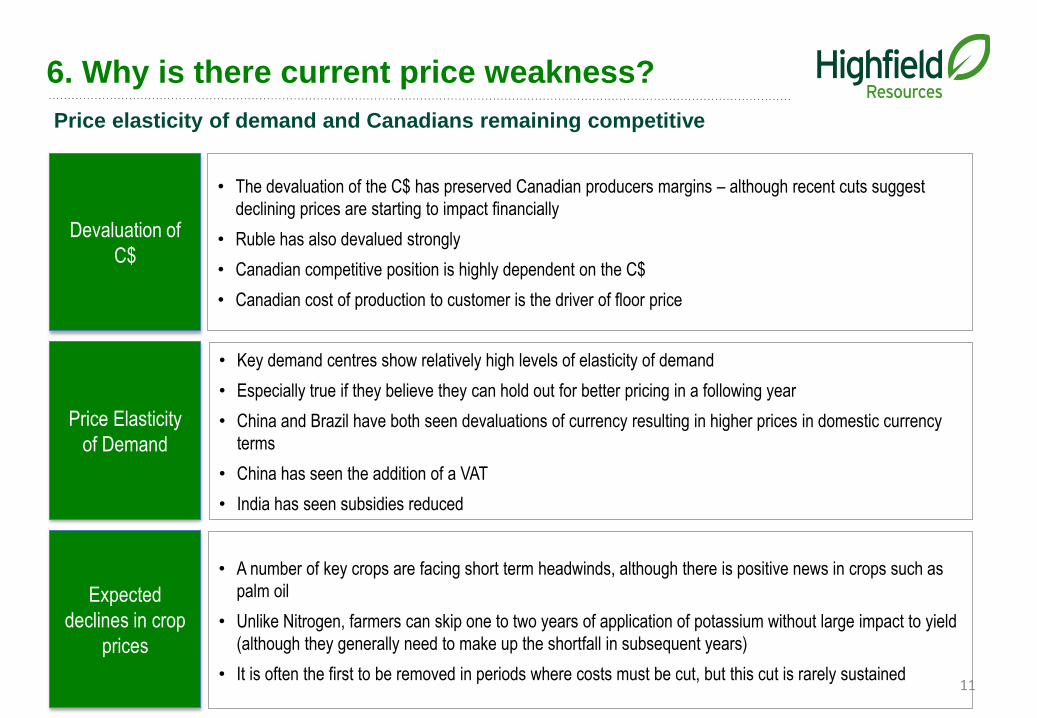

6. Why is there current price weakness?

Price elasticity of demand and Canadians remaining competitive

Price Elasticity

of Demand

Expected

declines in crop

prices

Devaluation of

C$

• The devaluation of the C$ has preserved Canadian producers margins – although recent cuts suggest

declining prices are starting to impact financially

• Ruble has also devalued strongly

• Canadian competitive position is highly dependent on the C$

• Canadian cost of production to customer is the driver of floor price

• Key demand centres show relatively high levels of elasticity of demand

• Especially true if they believe they can hold out for better pricing in a following year

• China and Brazil have both seen devaluations of currency resulting in higher prices in domestic currency

terms

• China has seen the addition of a VAT

• India has seen subsidies reduced

• A number of key crops are facing short term headwinds, although there is positive news in crops such as

palm oil

• Unlike Nitrogen, farmers can skip one to two years of application of potassium without large impact to yield

(although they generally need to make up the shortfall in subsequent years)

• It is often the first to be removed in periods where costs must be cut, but this cut is rarely sustained11

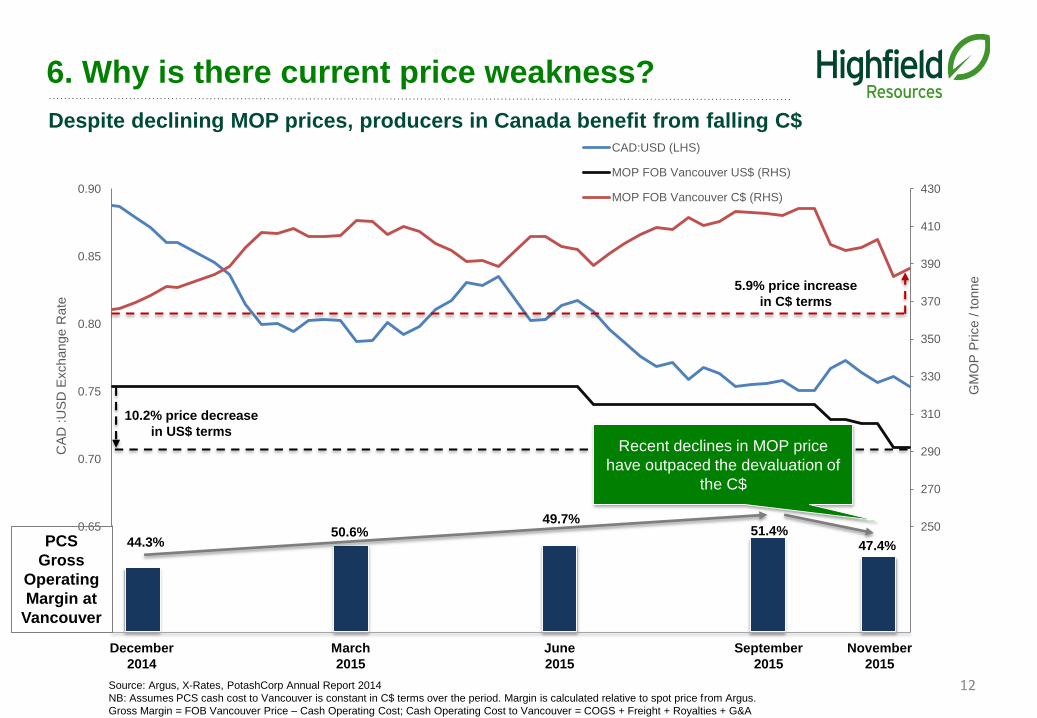

6. Why is there current price weakness?

Despite declining MOP prices, producers in Canada benefit from falling C$

250

270

290

310

330

350

370

390

410

430

0.65

0.70

0.75

0.80

0.85

0.90

GM

OP

Price /

tonne

CA

D :

US

D E

xchange R

ate

CAD:USD (LHS)

MOP FOB Vancouver US$ (RHS)

MOP FOB Vancouver C$ (RHS)

5.9% price increase

in C$ terms

10.2% price decrease

in US$ terms

December

2014

March

2015

June

2015

September

2015

44.3%50.6%

49.7%51.4%

PCS

Gross

Operating

Margin at

Vancouver

47.4%

November

2015

Recent declines in MOP price

have outpaced the devaluation of

the C$

Source: Argus, X-Rates, PotashCorp Annual Report 2014

NB: Assumes PCS cash cost to Vancouver is constant in C$ terms over the period. Margin is calculated relative to spot price from Argus.

Gross Margin = FOB Vancouver Price – Cash Operating Cost; Cash Operating Cost to Vancouver = COGS + Freight + Royalties + G&A

12

7. What is Highfield’s strategic position?

Unrivalled

Freight and

Logistics

Advantage

Domestic Market

Position

• Highfield’s potash travels 40% less distance than Canadian potash to Brazil, NOLA and East Coast USA

• Highfield is among the lowest cost producers delivered to these markets – on par with the Russians and

Belarussians

• Highfield can confidently target any customer in any market offering both price and contract incentives

• Customers are very happy to see new production outside the three major producing countries

• Highfield is within trucking distance of 1.3Mtpa of MOP demand

• Third party logistics charges and freight costs means Highfield is the lowest cost producer to these regions

by a significant margin

• Highfield can compete both on price and flexibility, which is likely to have a positive margin impact

Total cash costs to high priced customers likely to drive outstanding margins

13

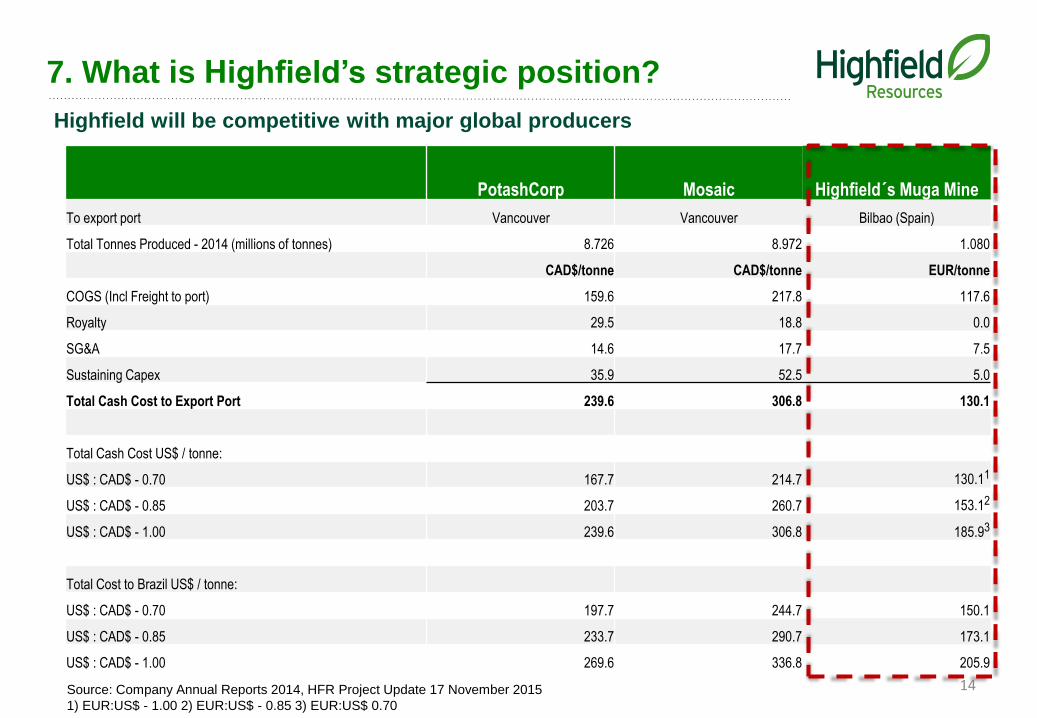

7. What is Highfield’s strategic position?

Highfield will be competitive with major global producers

PotashCorp Mosaic Highfield´s Muga Mine

To export port Vancouver Vancouver Bilbao (Spain)

Total Tonnes Produced - 2014 (millions of tonnes) 8.726 8.972 1.080

CAD$/tonne CAD$/tonne EUR/tonne

COGS (Incl Freight to port) 159.6 217.8 117.6

Royalty 29.5 18.8 0.0

SG&A 14.6 17.7 7.5

Sustaining Capex 35.9 52.5 5.0

Total Cash Cost to Export Port 239.6 306.8 130.1

Total Cash Cost US$ / tonne:

US$ : CAD$ - 0.70 167.7 214.7 130.11

US$ : CAD$ - 0.85 203.7 260.7 153.12

US$ : CAD$ - 1.00 239.6 306.8 185.93

Total Cost to Brazil US$ / tonne:

US$ : CAD$ - 0.70 197.7 244.7 150.1

US$ : CAD$ - 0.85 233.7 290.7 173.1

US$ : CAD$ - 1.00 269.6 336.8 205.9

Source: Company Annual Reports 2014, HFR Project Update 17 November 2015

1) EUR:US$ - 1.00 2) EUR:US$ - 0.85 3) EUR:US$ 0.70

14

8. Summary

15

• Potash supply and demand is well balanced

• Marginal unit of production, acting rationally, will meet demand as it is unable to displace most alternate production given

cost to customer structures

• Current price weakness is USD driven

• Similar to Australian gold producers, if your costs are in a currency that is depreciating faster than commodity price

declines your margins are maintained

• Highfield´s Muga Mine will be competitive with major global producers given royalty and logistics advantages

• Highfield has multiple high priced market options for the sale of its product

9. Questions

16

www.highfieldresources.com.au

REGISTERED OFFICE

169 Fullarton Road

Dulwich SA 5065

Australia

HEAD OFFICE

Avenida Carlos III, 13-15, 1B, 31002 Pamplona, Spain

T +34 948 050 577 | F +34 948 050 578

FURTHER INFORMATION

Anthony Hall - Managing Director T +34 617 872 100

John Claverley - General Manager T +34 607 748 435

Hayden Locke - Corporate Development T +34 609 811 257

17

Highfield Resources LtdPotash Project Fundamentals

Michael X. Schlumpberger – EGM Operations

November 2015

ASX Code: HFR

Highfield Resources Ltd.

POTASH PROJECT FUNDAMENTALS

2

CONTENTS

1. Introduction

2. How is potash mined?

3. How is potash processed?

4. What to look for in a potash project

5. Why is capex generally so high in potash?

6. How does Highfield’s Muga compare on capex?

7. How does Highfield’s Muga compare on opex?

8. Case Study – Lanigan Mine

9. Summary

1. Introduction

3

• Potash is currently produced by one of:

Three Mining Methods: Underground Conventional, Solution, or Brines,

and one of:

Two Processing Methods: Flotation Circuit, or Crystallisation

• The election of these methods heavily influences capex and site opex and is, primarily, driven by geological factors

• The location of a project is another significant factor in both capex and opex

• These two major factors (geology and location), and a number of less integral factors, will ultimately determine the margin

achieved by any potash project

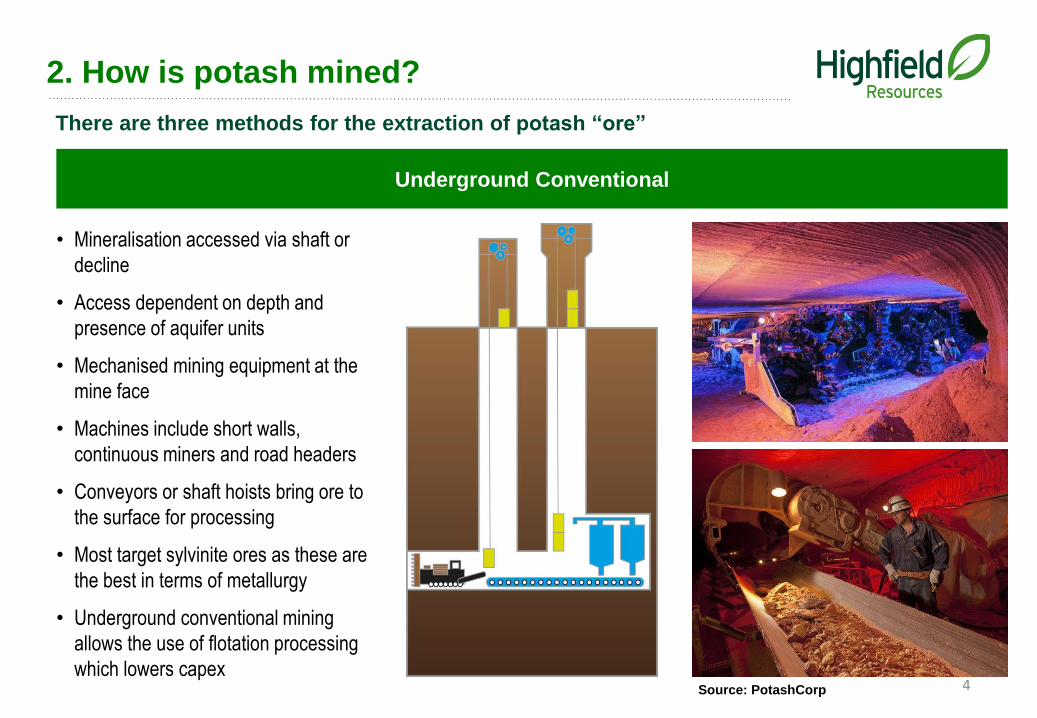

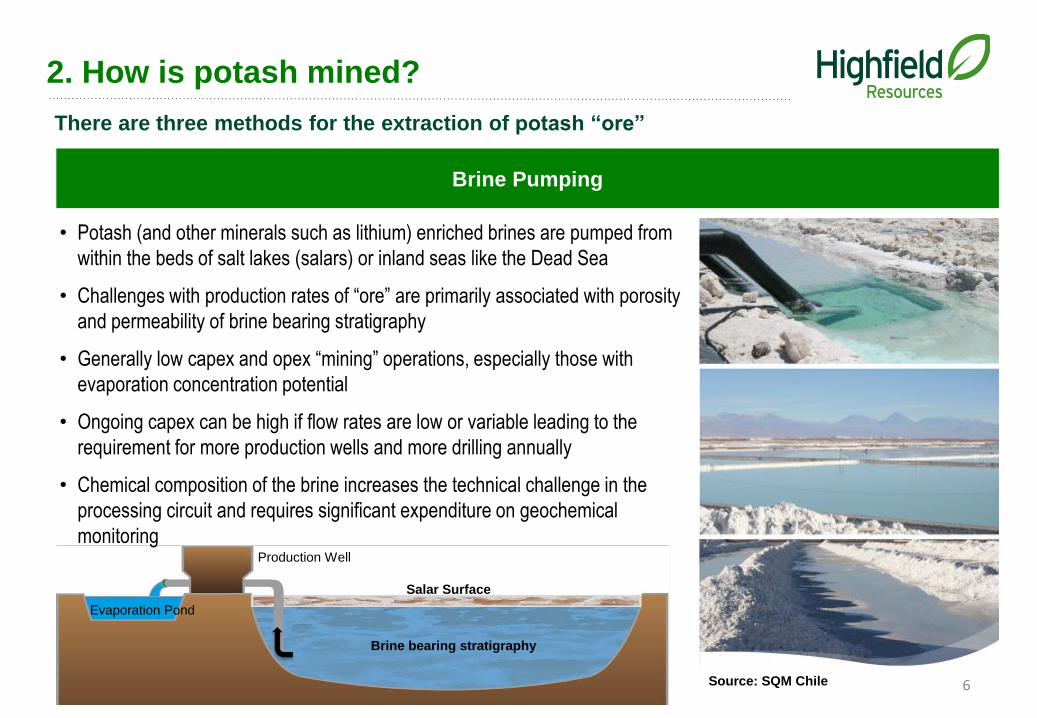

2. How is potash mined?

4

There are three methods for the extraction of potash “ore”

• Mineralisation accessed via shaft or

decline

• Access dependent on depth and

presence of aquifer units

• Mechanised mining equipment at the

mine face

• Machines include short walls,

continuous miners and road headers

• Conveyors or shaft hoists bring ore to

the surface for processing

• Most target sylvinite ores as these are

the best in terms of metallurgy

• Underground conventional mining

allows the use of flotation processing

which lowers capex

Underground Conventional

Source: PotashCorp

2. How is potash mined?

5

There are three methods for the extraction of potash “ore”

• Drilling both injection and production wells

to the targeted sylvinite horizon

• In some cases, directional (horizontal)

drilling is used to increase exposure of

injected liquid to potash seams with

technical challenges present at any depth

for different reasons

• Heated brines (generally) injected into

producing caverns

• The liquid preferentially dissolves the

potash layer

• Potash enriched brine is pumped back to

the surface for processing via hot

crystallisation or evaporation

Solution

Potash solution mining

Source: Paradox Potash Corp

Typical direction drilling schematic

Source: Agapito Associates, Inc.

Evaporation Pond

Production Well

Salar Surface

Brine bearing stratigraphy

2. How is potash mined?

6

There are three methods for the extraction of potash “ore”

• Potash (and other minerals such as lithium) enriched brines are pumped from

within the beds of salt lakes (salars) or inland seas like the Dead Sea

• Challenges with production rates of “ore” are primarily associated with porosity

and permeability of brine bearing stratigraphy

• Generally low capex and opex “mining” operations, especially those with

evaporation concentration potential

• Ongoing capex can be high if flow rates are low or variable leading to the

requirement for more production wells and more drilling annually

• Chemical composition of the brine increases the technical challenge in the

processing circuit and requires significant expenditure on geochemical

monitoring

Brine Pumping

Source: SQM Chile

2. How is potash mined?

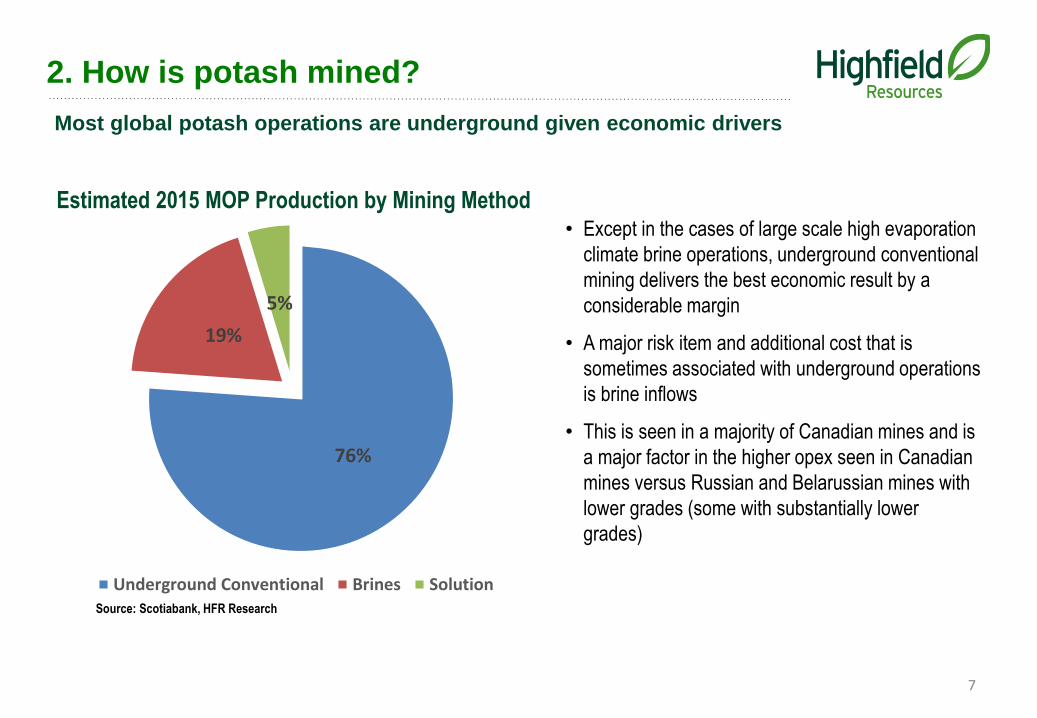

7

76%

19%

5%

Underground Conventional Brines SolutionSource: Scotiabank, HFR Research

Estimated 2015 MOP Production by Mining Method

Most global potash operations are underground given economic drivers

• Except in the cases of large scale high evaporation

climate brine operations, underground conventional

mining delivers the best economic result by a

considerable margin

• A major risk item and additional cost that is

sometimes associated with underground operations

is brine inflows

• This is seen in a majority of Canadian mines and is

a major factor in the higher opex seen in Canadian

mines versus Russian and Belarussian mines with

lower grades (some with substantially lower

grades)

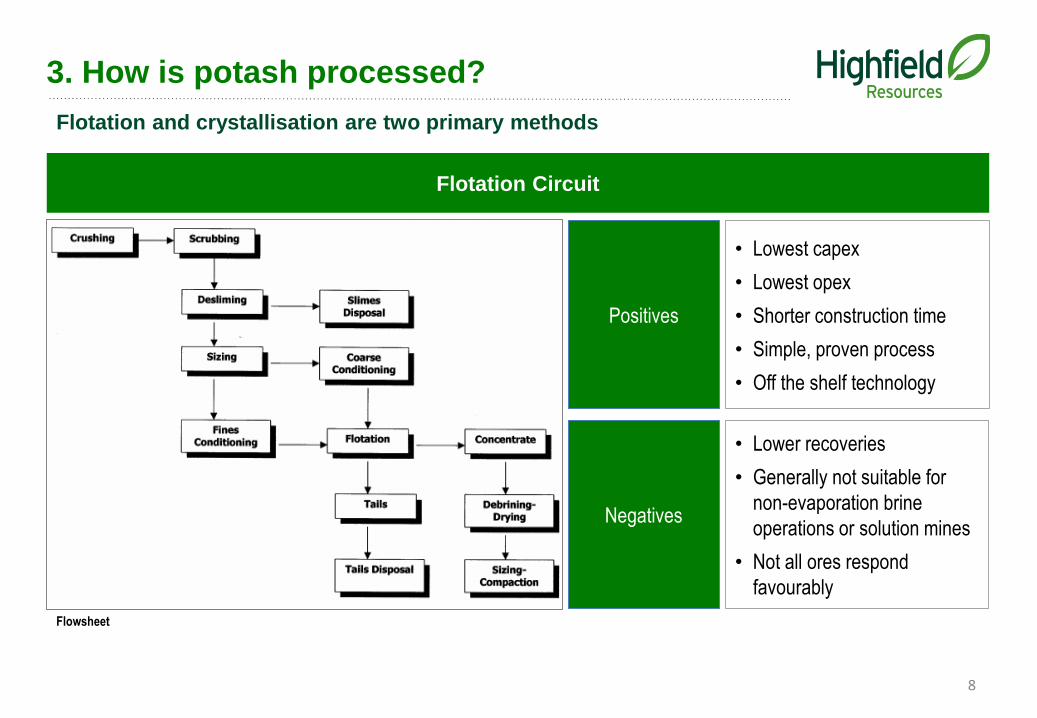

3. How is potash processed?

8

Flotation and crystallisation are two primary methods

Positives

• Lowest capex

• Lowest opex

• Shorter construction time

• Simple, proven process

• Off the shelf technology

Negatives

• Lower recoveries

• Generally not suitable for

non-evaporation brine

operations or solution mines

• Not all ores respond

favourably

Flotation Circuit

Flowsheet

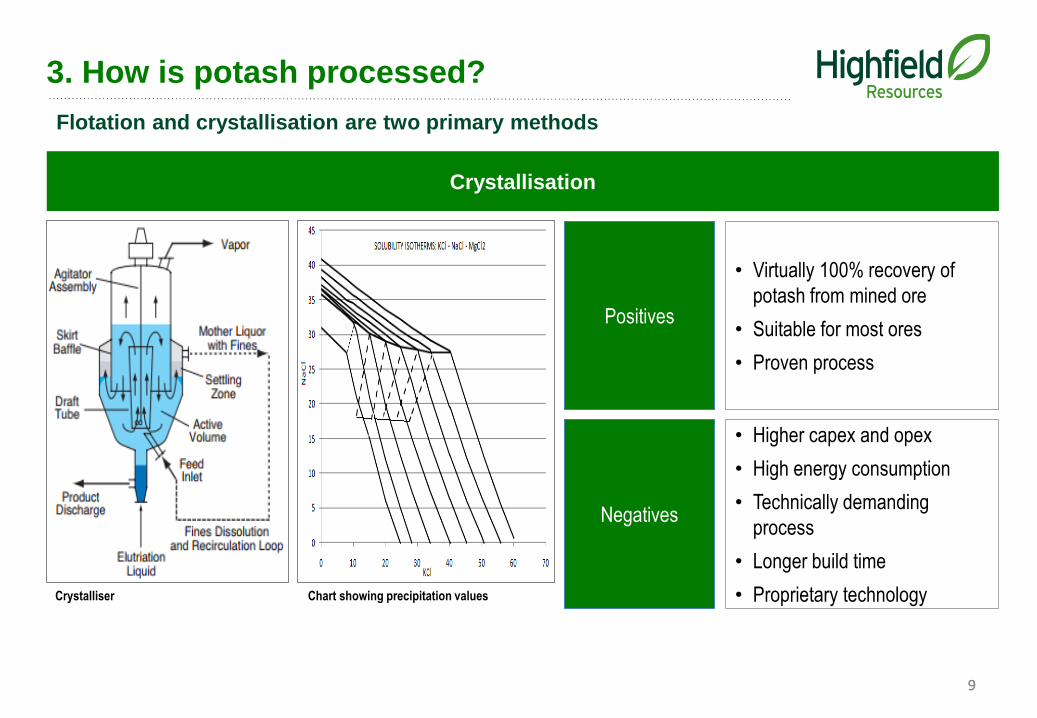

3. How is potash processed?

9

Flotation and crystallisation are two primary methods

Positives

• Virtually 100% recovery of

potash from mined ore

• Suitable for most ores

• Proven process

Negatives

• Higher capex and opex

• High energy consumption

• Technically demanding

process

• Longer build time

• Proprietary technology

Crystallisation

9

Chart showing precipitation valuesCrystalliser

10

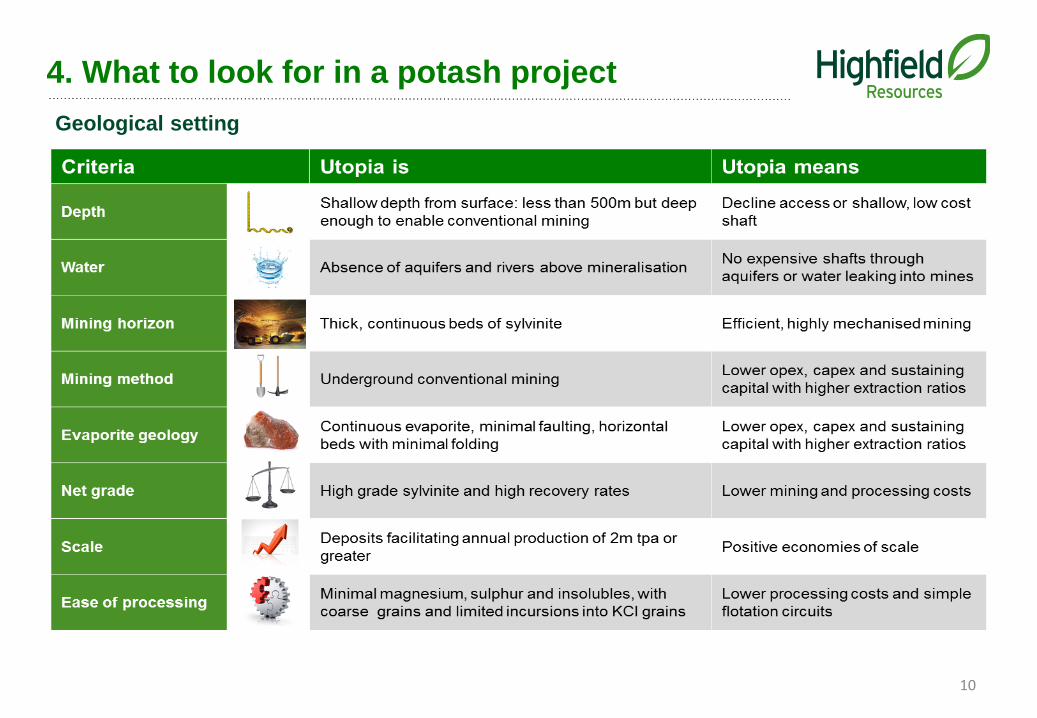

4. What to look for in a potash project

Geological setting

11

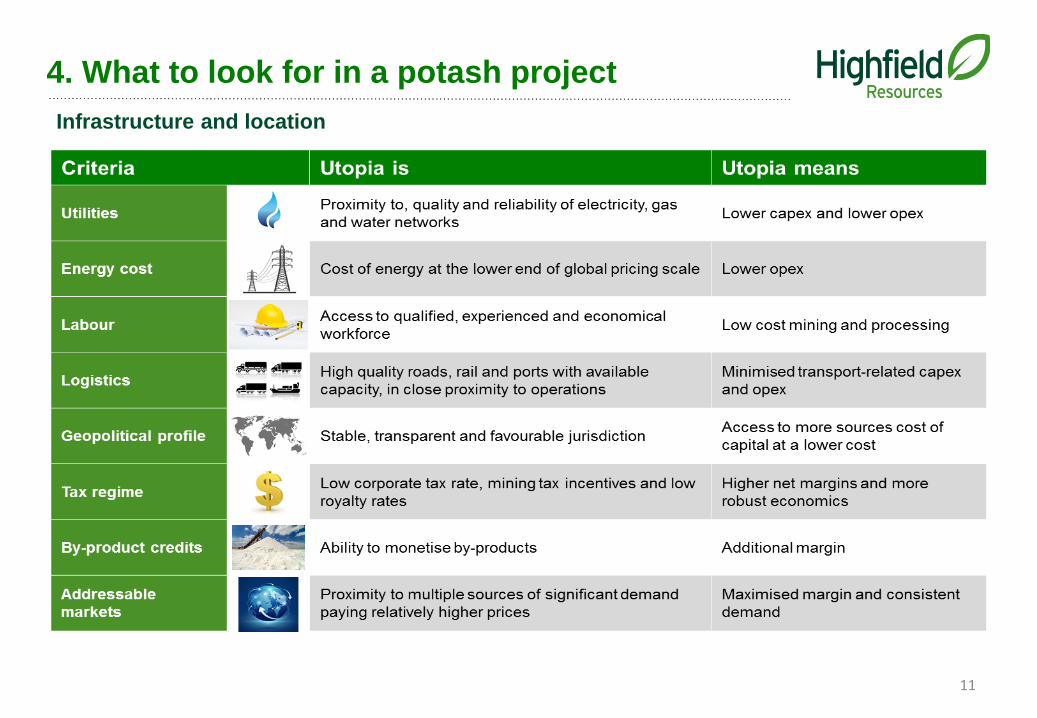

4. What to look for in a potash project

Infrastructure and location

Table based on Highfield assessment

1) Company information

12

4. What to look for in a potash project

Location is as important as mineralisation in potash production

13

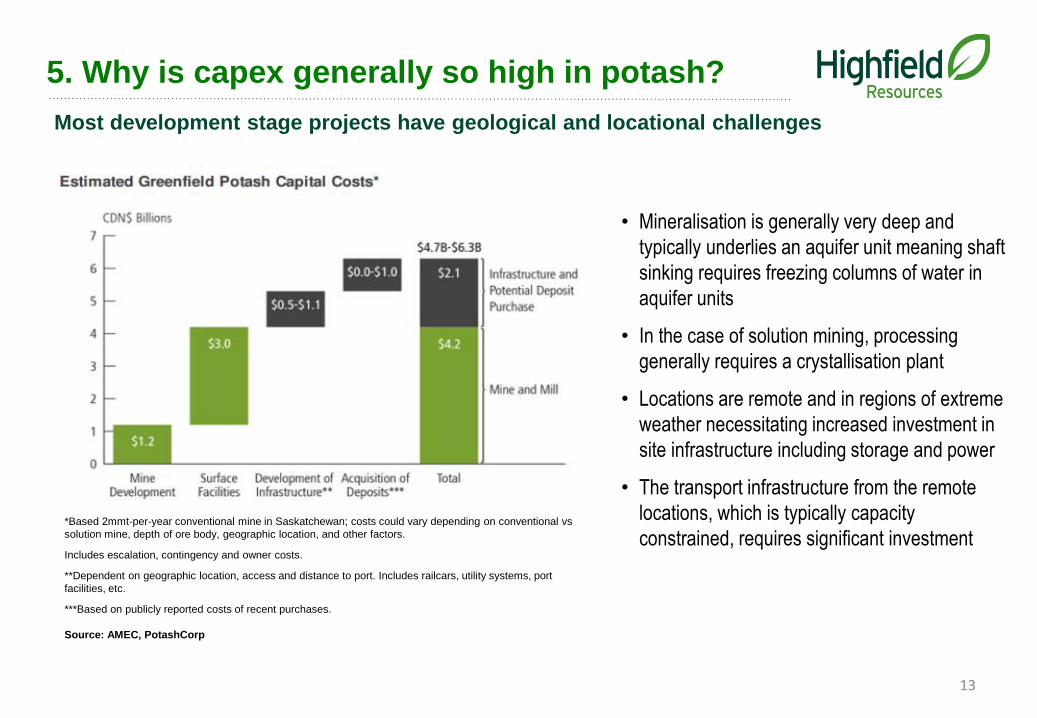

• Mineralisation is generally very deep and

typically underlies an aquifer unit meaning shaft

sinking requires freezing columns of water in

aquifer units

• In the case of solution mining, processing

generally requires a crystallisation plant

• Locations are remote and in regions of extreme

weather necessitating increased investment in

site infrastructure including storage and power

• The transport infrastructure from the remote

locations, which is typically capacity

constrained, requires significant investment

Most development stage projects have geological and locational challenges

5. Why is capex generally so high in potash?

*Based 2mmt-per-year conventional mine in Saskatchewan; costs could vary depending on conventional vs

solution mine, depth of ore body, geographic location, and other factors.

Includes escalation, contingency and owner costs.

**Dependent on geographic location, access and distance to port. Includes railcars, utility systems, port

facilities, etc.

***Based on publicly reported costs of recent purchases.

Source: AMEC, PotashCorp

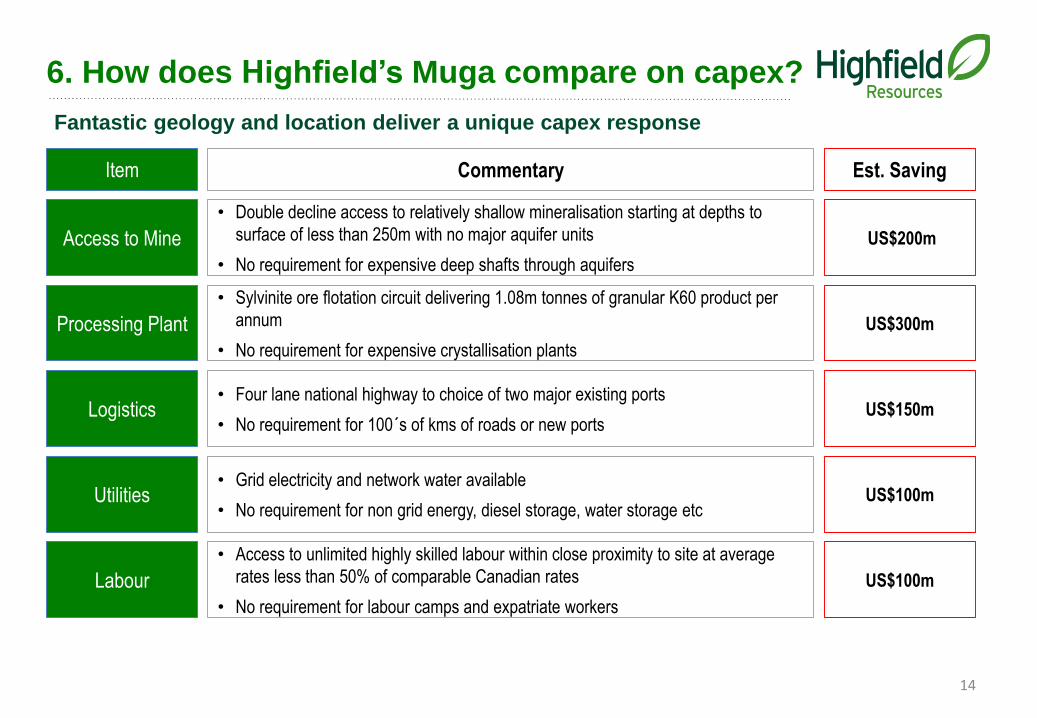

Fantastic geology and location deliver a unique capex response

6. How does Highfield’s Muga compare on capex?

Access to Mine

• Double decline access to relatively shallow mineralisation starting at depths to

surface of less than 250m with no major aquifer units

• No requirement for expensive deep shafts through aquifers

Item Commentary

US$200m

Est. Saving

Processing Plant

• Sylvinite ore flotation circuit delivering 1.08m tonnes of granular K60 product per

annum

• No requirement for expensive crystallisation plants

US$300m

Logistics• Four lane national highway to choice of two major existing ports

• No requirement for 100´s of kms of roads or new portsUS$150m

Utilities• Grid electricity and network water available

• No requirement for non grid energy, diesel storage, water storage etcUS$100m

Labour

• Access to unlimited highly skilled labour within close proximity to site at average

rates less than 50% of comparable Canadian rates

• No requirement for labour camps and expatriate workers

US$100m

14

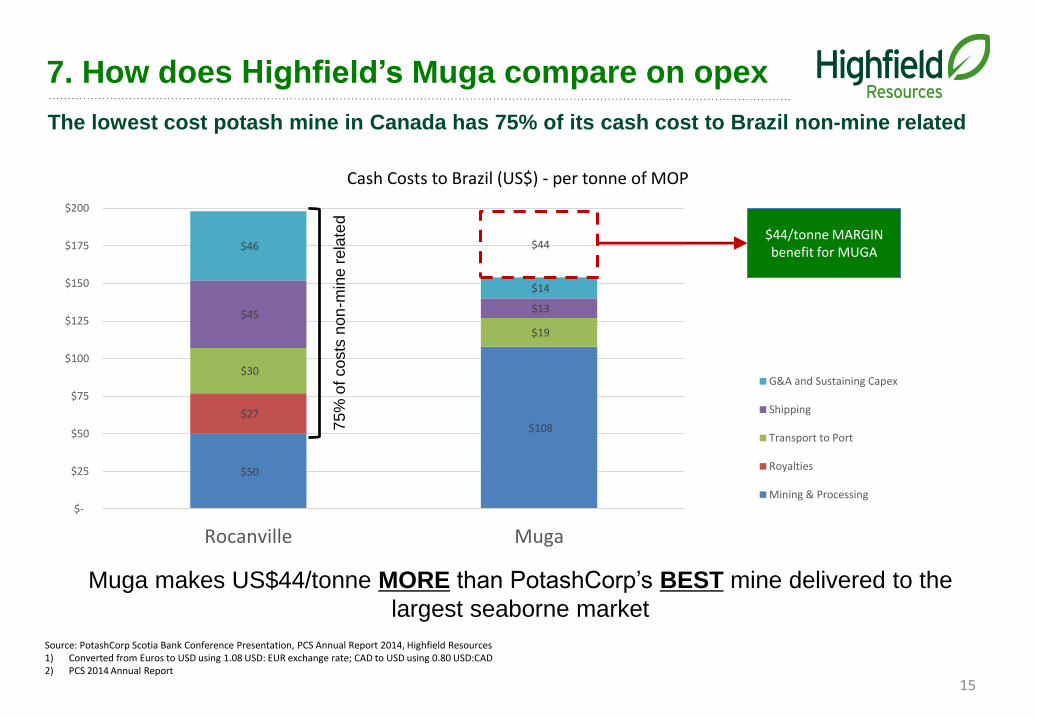

$50

$108 $27

$30

$19

$45 $13

$46

$14

$44

$-

$25

$50

$75

$100

$125

$150

$175

$200

Rocanville Muga

Cash Costs to Brazil (US$) - per tonne of MOP

G&A and Sustaining Capex

Shipping

Transport to Port

Royalties

Mining & Processing

7. How does Highfield’s Muga compare on opex

15

The lowest cost potash mine in Canada has 75% of its cash cost to Brazil non-mine related

Muga makes US$44/tonne MORE than PotashCorp’s BEST mine delivered to the

largest seaborne market

Source: PotashCorp Scotia Bank Conference Presentation, PCS Annual Report 2014, Highfield Resources1) Converted from Euros to USD using 1.08 USD: EUR exchange rate; CAD to USD using 0.80 USD:CAD2) PCS 2014 Annual Report

$44/tonne MARGIN benefit for MUGA

75

% o

f co

sts

no

n-m

ine

rela

ted

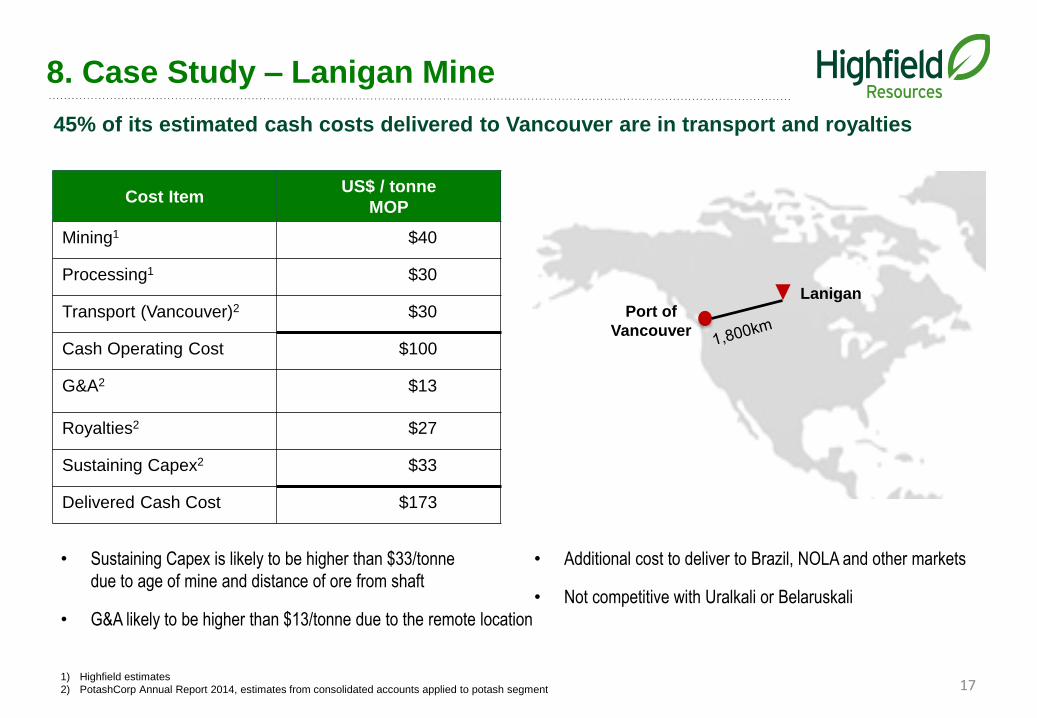

8. Case Study – Lanigan Mine

Geologically, Lanigan is a world class potash mine and is one of the best in Canada

Project Metric Data

Theoretical Capacity

(MOP)3.8Mtpa

Operating Capability

(MOP)2.2Mtpa

Depth 1,000 metres

K20 Grade to Mill 20.2%

Average Seam Thickness 5 metres

Recovery Rate

80%-90%

Combination flotation and

crystallisation

16

45% of its estimated cash costs delivered to Vancouver are in transport and royalties

1) Highfield estimates

2) PotashCorp Annual Report 2014, estimates from consolidated accounts applied to potash segment

Cost ItemUS$ / tonne

MOP

Mining1 $40

Processing1 $30

Transport (Vancouver)2 $30

Cash Operating Cost $100

G&A2 $13

Royalties2 $27

Sustaining Capex2 $33

Delivered Cash Cost $173

• Sustaining Capex is likely to be higher than $33/tonne

due to age of mine and distance of ore from shaft

• G&A likely to be higher than $13/tonne due to the remote location

• Additional cost to deliver to Brazil, NOLA and other markets

• Not competitive with Uralkali or Belaruskali

17

8. Case Study – Lanigan Mine

Port of

Vancouver

Lanigan

9. Summary

18

• Potash is currently produced by one of:

Three Mining Methods: Underground Conventional, Solution, or Brines,

and one of:

Two Processing Methods: Flotation Circuit, or Crystallisation

• The election of these methods heavily influences capex and site opex and is, primarily, driven by geological factors

• The location of a project is another significant factor in both capex and opex

• These two major factors (geology and location), and a number of less integral factors, will ultimately determine the margin

achieved by any potash project

10. Questions

19

www.highfieldresources.com.au

REGISTERED OFFICE

169 Fullarton Road

Dulwich SA 5065

Australia

HEAD OFFICE

Avenida Carlos III, 13-15, 1B, 31002 Pamplona, Spain

T +34 948 050 577 | F +34 948 050 578

FURTHER INFORMATION

Anthony Hall - Managing Director T +34 617 872 100

John Claverley - General Manager T +34 607 748 435

Hayden Locke - Corporate Development T +34 609 811 257

Highfield Resources LtdDeveloping the Muga Mine

John Claverley – General Manager

November 2015

ASX Code: HFR1

Highfield Resources Ltd.

DEVELOPING THE MUGA MINE

2

CONTENTS

1. Introduction

2. What is the approvals process in Spain?

3. Highfield approvals update

4. Why will Highfield get approved?

5. Summary

1. Introduction

3

• Permitting a mining project is a time consuming and highly intensive process no matter where you

operate

• Spain has an undeserved reputation as being a more difficult jurisdiction in which to permit mining

projects

• Spain has a long mining history, is pro-mining and very pro-investment

• The Spanish regulatory and permitting system:

• Is a transparent and well documented process

• Is protected by a strong regulatory framework

• Has idiosyncrasies which require local understanding

• Issues encountered often relate to a lack of commitment to the community or a lack of local experience

of those running the process

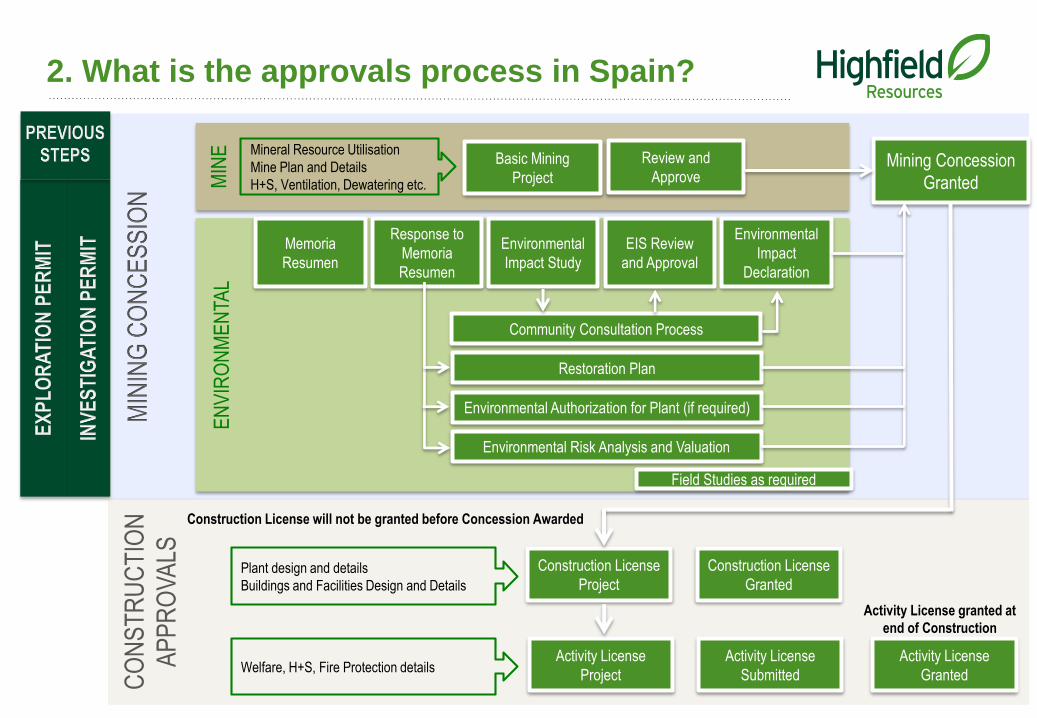

2. What is the approvals process in Spain?

EXPLORATION PERMIT INVESTIGATION PERMIT MINING CONCESSION

4

2. What is the approvals process in Spain?

CO

NS

TR

UC

TIO

N

AP

PR

OV

ALS

MIN

EE

NV

IRO

NM

EN

TAL

Memoria

Resumen

Response to

Memoria

Resumen

Environmental

Impact Study

EIS Review

and Approval

Environmental

Impact

Declaration

Restoration Plan

Environmental Risk Analysis and Valuation

Field Studies as required

Basic Mining

Project

Review and

ApproveMining Concession

Granted

Construction License

Project

Construction License

Granted

Activity License

Project

Activity License

Submitted

Activity License

Granted

Mineral Resource Utilisation

Mine Plan and Details

H+S, Ventilation, Dewatering etc.

Plant design and details

Buildings and Facilities Design and Details

Welfare, H+S, Fire Protection details

Activity License granted at

end of Construction

Construction License will not be granted before Concession Awarded

Environmental Authorization for Plant (if required)

Community Consultation Process

3. Where is Highfield in the process?

MIN

EE

NV

IRO

NM

EN

TAL

Memoria

Resumen

Response to

Memoria

Resumen

Environmental

Impact Study

EIS Review

and Approval

Environmental

Impact

Declaration

Restoration Plan

Environmental Risk Analysis and Valuation

Field Studies as required

Basic Mining

Project

Review and

ApproveMining Concession

Granted

Mineral Resource Utilisation

Mine Plan and Details

H+S, Ventilation, Dewatering etc.

Environmental Authorization for Plant (if required)

Community Consultation Process

February 2016

April 2016

- Strong local community support for the Muga Potash Mine

- Highfield responses to submissions from community consultation process completed 15 October 2015

- Letters of support to the Central Government received from local councils of all towns impacted by Muga

- Submissions with Central Government Environmental Authority for review

- Positive Environmental Declaration (“DIA”) expected by February 2016, mining concession by April 20166

4. Why will Highfield get approved?

An underground mine with decline access

Mine design studies and backfilling

Sylvinite ore

Comprehensive rehabilitation plan

MINIMAL VISUAL IMPACT

SUBSIDENCE UNLIKELY

NO TOXIC CHEMICALS OR WASTE

MINIMAL LEGACY

A Quality Project

7

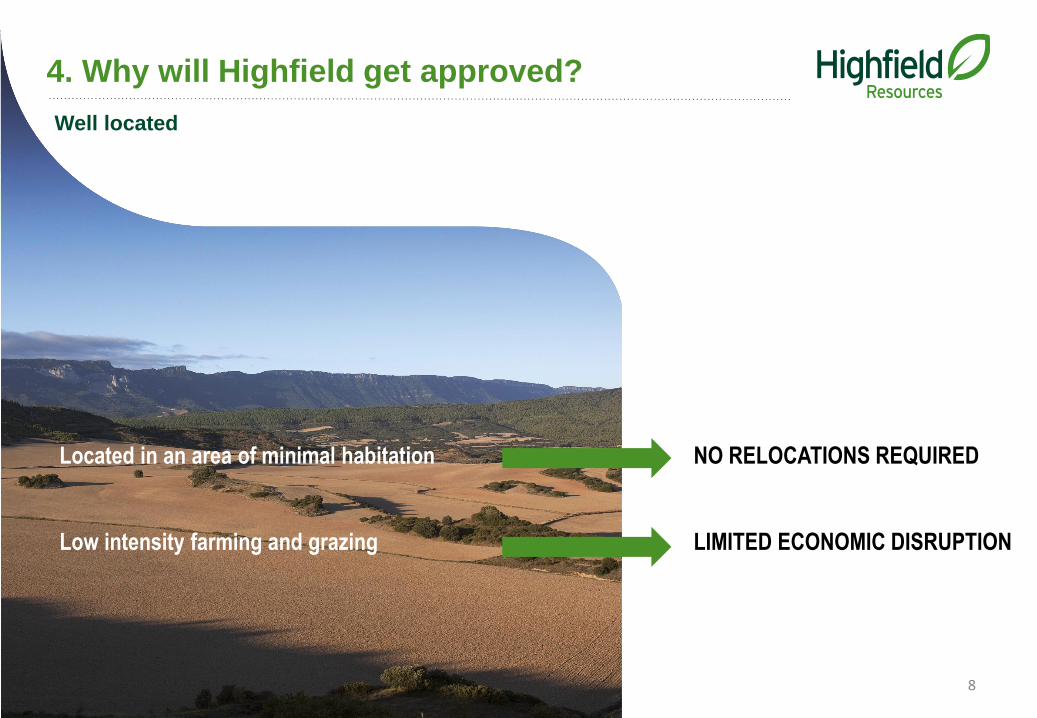

NO RELOCATIONS REQUIRED

LIMITED ECONOMIC DISRUPTION

4. Why will Highfield get approved?

Located in an area of minimal habitation

Low intensity farming and grazing

Well located

8

4. Why will Highfield get approved?

Pedro Rodriguez

Development Director

Michael Schlumpberger

EGM - Operations

• Geologist with over 30 years experience in

Spain, including for senior management roles

for multi-nationals including Billiton, Navan-

Almagrera and Newmont

• Direct responsibility for permitting and delivery

of the Aguas Teñidas, Los Santos and

Mazzarón mines

• Mining Engineer with extensive underground

mining experience including over 21 years at

PotashCorp

• Operational responsibility for the expansion and

ongoing operations at PotashCorp’s Lanigan

underground mine

Lanigan potash mine

Source: PotashCorp

Aguas Teñidas mine in Huelva, Spain. Opened 2009

With an experienced development and operations team

9

4. Why will Highfield get approved?

Spanish Team, based in Spain

• Pamplona office with 50+ professionals

• All Senior Management based in Pamplona

Buy Local policy

• Local contractors and suppliers given priority

Extensive Community Responsibility

program

• Dedicated Foundation developed

• Over 15 community programs in operation

Committed to Spain

10

4. Why will Highfield get approved?

Committed to our four operational pillars

11

Safety first Delivering positive

social benefits

Spreading the

economic opportunities

to all stakeholders

Ensuring best

practice

environmental

outcomes

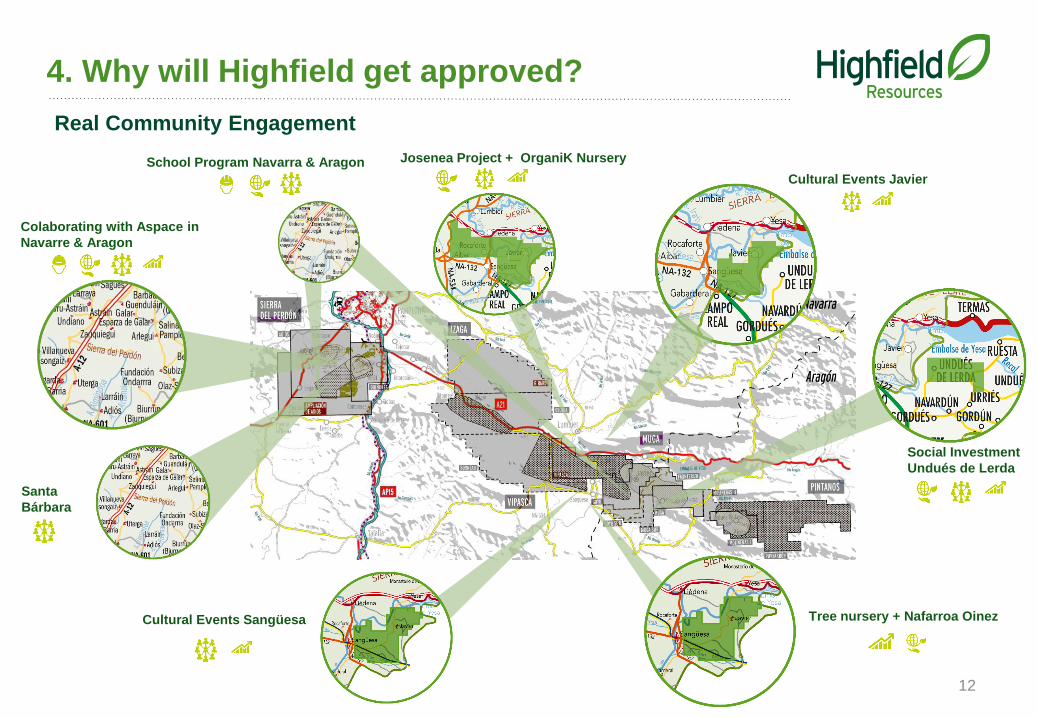

Josenea Project + OrganiK Nursery

Colaborating with Aspace in

Navarre & Aragon

Cultural Events Javier

Social Investment

Undués de Lerda

Tree nursery + Nafarroa OinezCultural Events Sangüesa

12

Santa

Bárbara

4. Why will Highfield get approved?

School Program Navarra & Aragon

Real Community Engagement

13

4. Why will Highfield get approved?

Foundation in operation since September 2014

14

4. Why will Highfield get approved?

Progressively becoming more visible with well visited website in operation

15

4. Why will Highfield get approved?

We are serious about demonstrating our commitment to the community

• Established communication channels with stakeholders (Community engagement and reporting)

• Branding all initiatives

• Completed Sustainability Report in September 2015

Sustainability ReportSchool Kit: Crecer Juntos + Sanos The importance of Potash

OrganiK sign

The Foundation Mascot

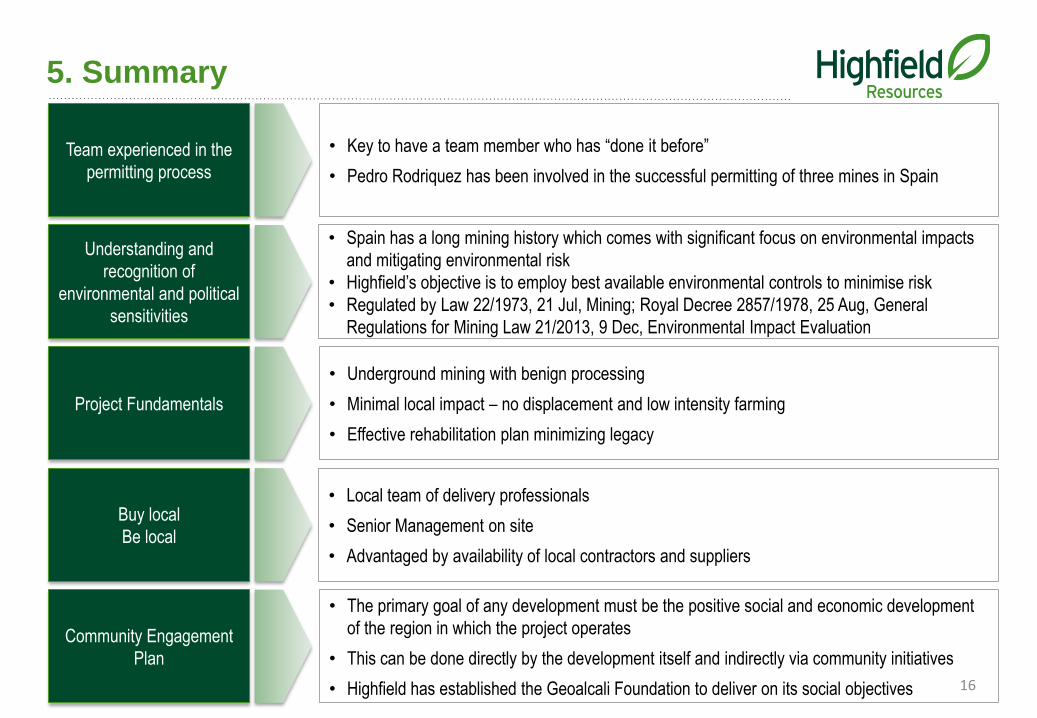

5. Summary

16

Team experienced in the

permitting process

Understanding and

recognition of

environmental and political

sensitivities

Project Fundamentals

Buy local

Be local

• Key to have a team member who has “done it before”

• Pedro Rodriquez has been involved in the successful permitting of three mines in Spain

• Spain has a long mining history which comes with significant focus on environmental impacts

and mitigating environmental risk

• Highfield’s objective is to employ best available environmental controls to minimise risk

• Regulated by Law 22/1973, 21 Jul, Mining; Royal Decree 2857/1978, 25 Aug, General

Regulations for Mining Law 21/2013, 9 Dec, Environmental Impact Evaluation

• Underground mining with benign processing

• Minimal local impact – no displacement and low intensity farming

• Effective rehabilitation plan minimizing legacy

• Local team of delivery professionals

• Senior Management on site

• Advantaged by availability of local contractors and suppliers

Community Engagement

Plan

• The primary goal of any development must be the positive social and economic development

of the region in which the project operates

• This can be done directly by the development itself and indirectly via community initiatives

• Highfield has established the Geoalcali Foundation to deliver on its social objectives

www.highfieldresources.com.au

REGISTERED OFFICE

169 Fullarton Road

Dulwich SA 5065

Australia

HEAD OFFICE

Avenida Carlos III, 13-15, 1B, 31002 Pamplona, Spain

T +34 948 050 577 | F +34 948 050 578

FURTHER INFORMATION

Anthony Hall - Managing Director T +34 617 872 100

John Claverley - General Manager T +34 607 748 435

Hayden Locke - Corporate Development T +34 609 811 257

Highfield Resources LtdThe Projects

Anthony Hall – Managing Director

November 2015

ASX Code: HFR

COMPETENT PERSON STATEMENT – RESOURCES

Information relating to resources was prepared by Mr Leo Gilbride, P.Eng and Ms Vanessa Santos, P.Geo, of Agapito Associates. The Competent Person for Resources

under JORC Code standards is Mr Leo Gilbride, P.Eng and Ms Vanessa Santos, P.Geo. of Agapito Associates of Colorado, USA. Mr Gilbride is a licensed professional

engineer in the State of Colorado, USA and is a registered member of the Society of Mining, Metallurgy and Exploration Inc. Ms Santos is a licensed professional geologist in

South Carolina and Georgia, USA, and is a registered member of the Society of Mining, Metallurgy and Exploration Inc.

The Society of Mining, Metallurgy and Exploration Inc is a JORC Code ‘Recognised Professional Organisation’ (RPO). An RPO is an accredited organisation of which the

Competent Person under JORC Code Reporting Standards must belong in order to report Exploration Results, Mineral Resources, or Ore Reserves through the ASX. Mr

Gilbride is the Vice President of Engineering and Field Services and Ms Santos is the Chief Geologist with Agapito Associates and both have sufficient experience to qualify

as a Competent Person for the relevant style and type of mineralisation and deposit under consideration of this release. Mr Gilbride and Ms Santos consent to the inclusion in

the report of the matters based on this information in the form and context in which it appears.

COMPETENT PERSON STATEMENT – RESERVES

Information relating to reserves was prepared by Mr. José Antonio Zuazo Osinaga, Technical Director of CRN, S.A.; Mr. Jesús Fernández Carrasco, Managing Director of

CRN, S.A. and Mr Manuel Jesus Gonzalez Roldan, Geologist of CRN, S.A. Mr. José Antonio Zuazo and Mr. Jesús Fernández, are licensed professional geologists in Spain,

and are registered members of the EUROPEAN FEDERATION OF GEOLOGISTS, an accredited organisation to which the Competent Person (CP) under JORC Code

Reporting Standards must belong in order to report Exploration Results, Mineral Resources, or Ore Reserves through the ASX.

Mr. José Antonio Zuazo is the Technical Director of CRN and he has sufficient experience which is relevant to the style of mineralisation and type of deposit under

consideration and to the activity which they are undertaking to qualify as a CP as defined in the 2012 Edition of the JORC Australasian Code for Reporting of Exploration

Results, Mineral Resources and Ore Reserves.

Mr. José Antonio Zuazo and Mr. Jesús Fernández consent to the inclusion in the release of the matters based on their information in the form and context in which it appears.

FORWARD LOOKING STATEMENTS

This presentation includes certain ‘forward looking statements’. All statements, other than statements of historical fact, are forward looking statements that involve various

risks and uncertainties. There can be no assurances that such statements will prove accurate, and actual results and future events could differ materially from those

anticipated in such statements.

Such information contained herein represents management’s best judgment as of the date hereof based on information currently available. The company does not assume

any obligation to update any forward looking statement.

Highfield Resources Ltd.

THE PROJECTS

3

CONTENTS

1. Introduction

2. Location – A key differentiating factor

3. The Projects

4. Highfield Value Proposition

5. Corporate Objective

6. What does success look like?

7. Summary

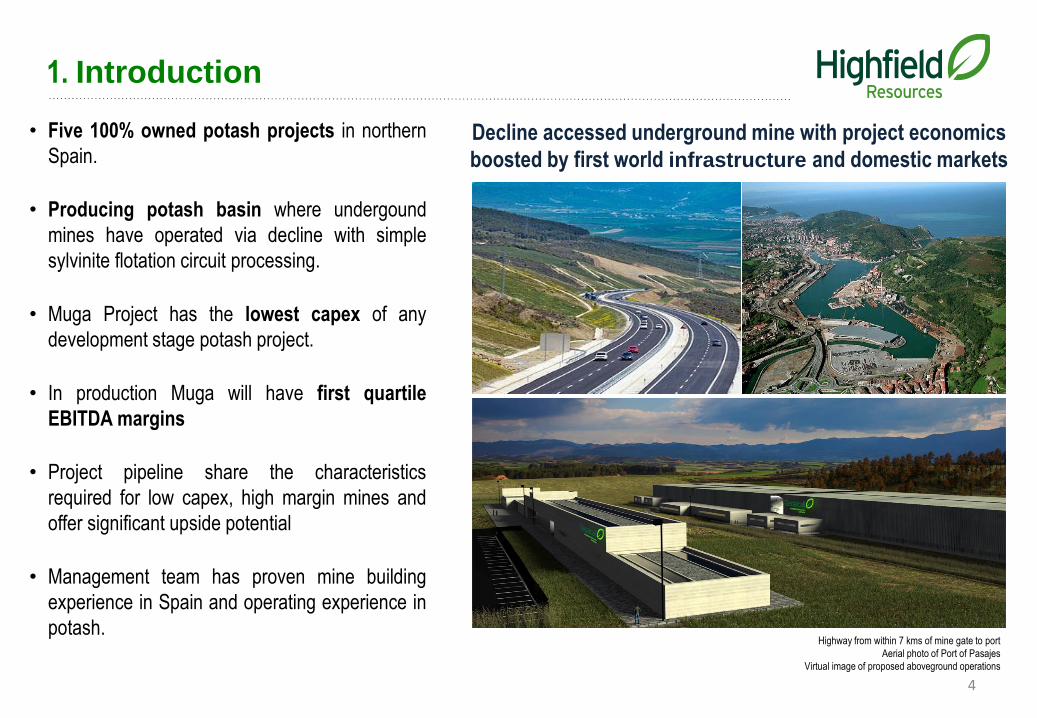

1. Introduction

4

Highway from within 7 kms of mine gate to port

Aerial photo of Port of Pasajes

Virtual image of proposed aboveground operations

Decline accessed underground mine with project economics

boosted by first world infrastructure and domestic markets

• Five 100% owned potash projects in northern

Spain.

• Producing potash basin where undergound

mines have operated via decline with simple

sylvinite flotation circuit processing.

• Muga Project has the lowest capex of any

development stage potash project.

• In production Muga will have first quartile

EBITDA margins

• Project pipeline share the characteristics

required for low capex, high margin mines and

offer significant upside potential

• Management team has proven mine building

experience in Spain and operating experience in

potash.

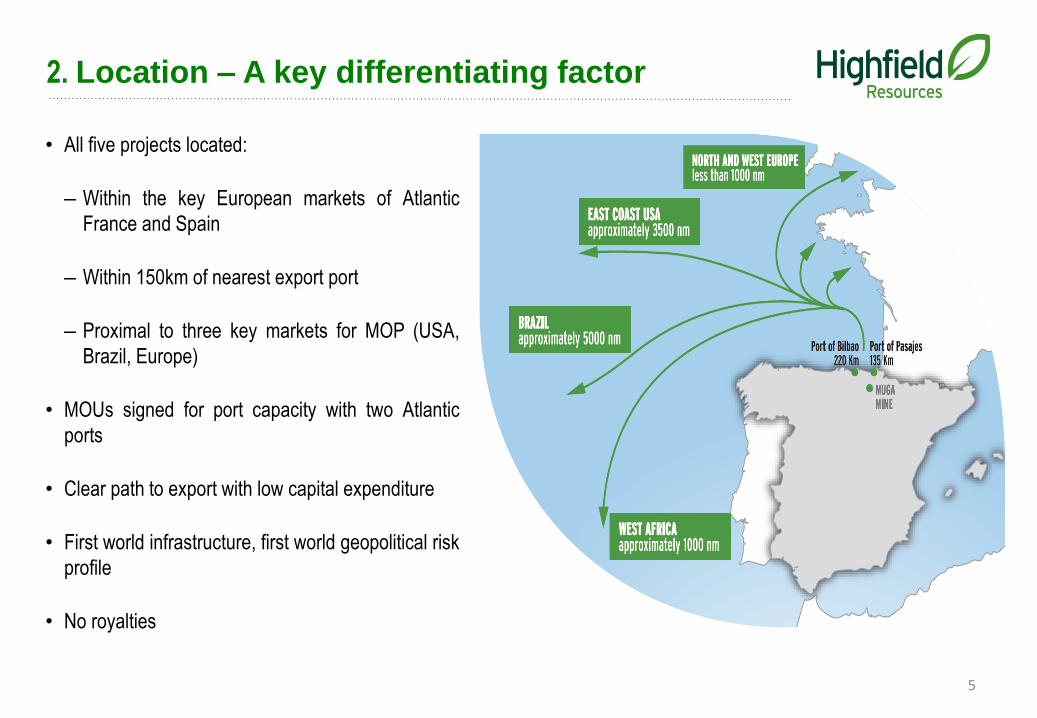

2. Location – A key differentiating factor

5

• All five projects located:

– Within the key European markets of Atlantic

France and Spain

– Within 150km of nearest export port

– Proximal to three key markets for MOP (USA,

Brazil, Europe)

• MOUs signed for port capacity with two Atlantic

ports

• Clear path to export with low capital expenditure

• First world infrastructure, first world geopolitical risk

profile

• No royalties

2. Location – A key differentiating factor

6

Highfield’s location is worth between c. $60 and c. $90 per tonne over Canadian producers

Royalties

Freight to Export

Port

G&A

Freight from Port

(Brazil)

Canada1 Russia2 Belarus3 Muga

$30 - 40

$30 - 50

$10 - 20

$30

Total $100 - 140

$5 - 10

$29 - 39

$15 - 20

$25

$73 - 94

$40 - 45

$15 - 20

$4 - 8

$25

$83 - 98

$0

$15 - 20

$5 -10

$20

$40 - 50

Non-Mine

Costs

Muga Mine

Advantage $60 - 90 $33 - 44 $43 - 48

1) Mosaic and PotashCorp Annual Reports 2013 and 2014, Highfield estimate on range

2) Uralkali 2014 Annual Report; Highfield estimate range

3) Goldman Sachs Research

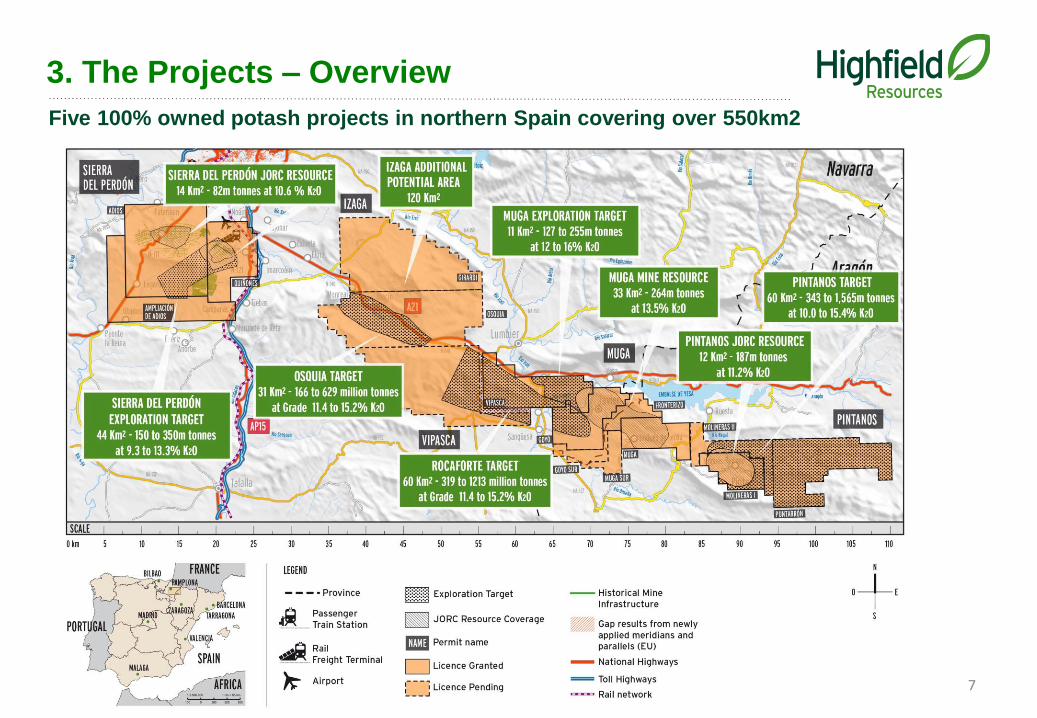

3. The Projects – Overview

Five 100% owned potash projects in northern Spain covering over 550km2

7

Muga - Highfield’s most advanced, low capex, high margin potash development project

Source: ASX Announcement dated 17 Nov. 20158

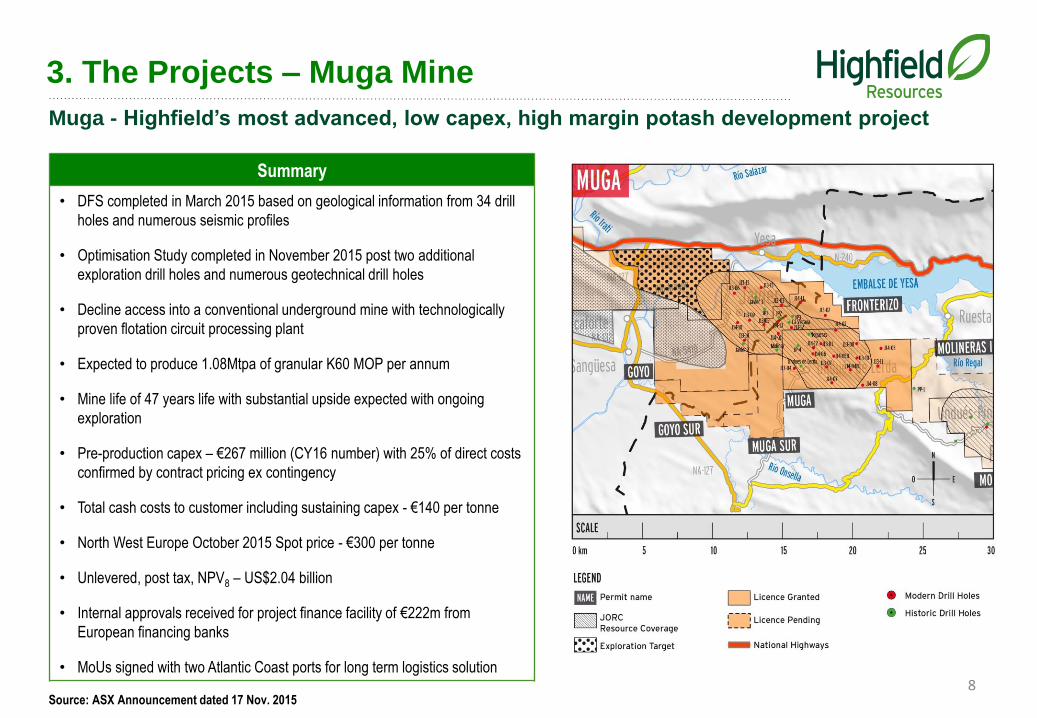

3. The Projects – Muga Mine

Summary

• DFS completed in March 2015 based on geological information from 34 drill

holes and numerous seismic profiles

• Optimisation Study completed in November 2015 post two additional

exploration drill holes and numerous geotechnical drill holes

• Decline access into a conventional underground mine with technologically

proven flotation circuit processing plant

• Expected to produce 1.08Mtpa of granular K60 MOP per annum

• Mine life of 47 years life with substantial upside expected with ongoing

exploration

• Pre-production capex – €267 million (CY16 number) with 25% of direct costs

confirmed by contract pricing ex contingency

• Total cash costs to customer including sustaining capex - €140 per tonne

• North West Europe October 2015 Spot price - €300 per tonne

• Unlevered, post tax, NPV8 – US$2.04 billion

• Internal approvals received for project finance facility of €222m from

European financing banks

• MoUs signed with two Atlantic Coast ports for long term logistics solution

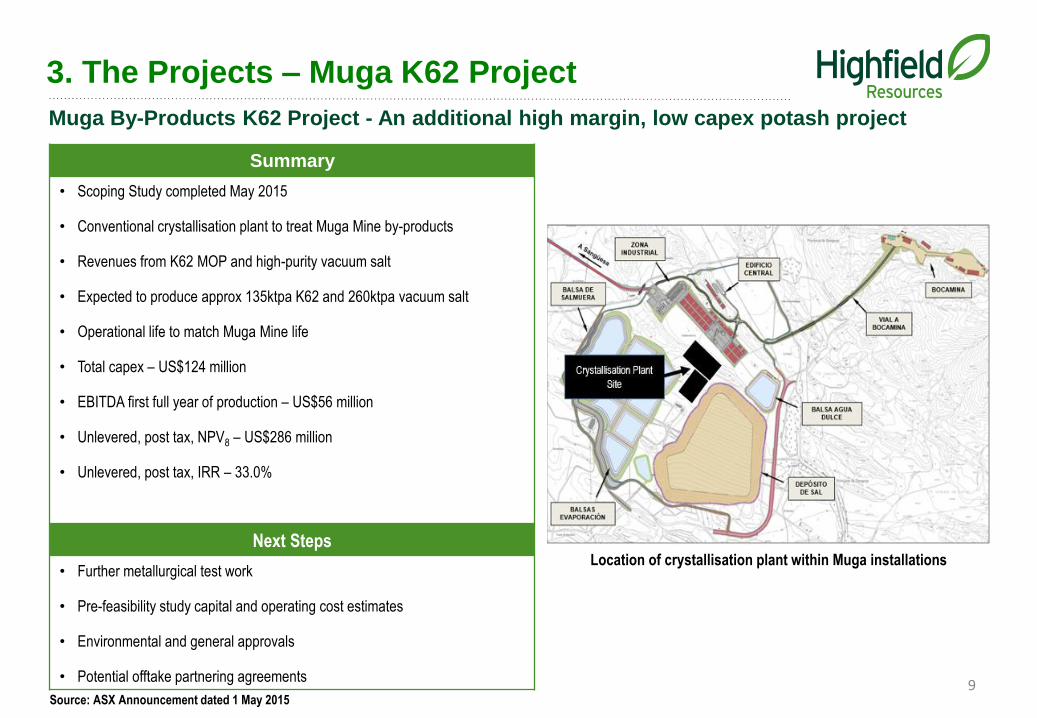

Muga By-Products K62 Project - An additional high margin, low capex potash project

Summary

• Scoping Study completed May 2015

• Conventional crystallisation plant to treat Muga Mine by-products

• Revenues from K62 MOP and high-purity vacuum salt

• Expected to produce approx 135ktpa K62 and 260ktpa vacuum salt

• Operational life to match Muga Mine life

• Total capex – US$124 million

• EBITDA first full year of production – US$56 million

• Unlevered, post tax, NPV8 – US$286 million

• Unlevered, post tax, IRR – 33.0%

Next Steps

• Further metallurgical test work

• Pre-feasibility study capital and operating cost estimates

• Environmental and general approvals

• Potential offtake partnering agreements

Location of crystallisation plant within Muga installations

Source: ASX Announcement dated 1 May 20159

3. The Projects – Muga K62 Project

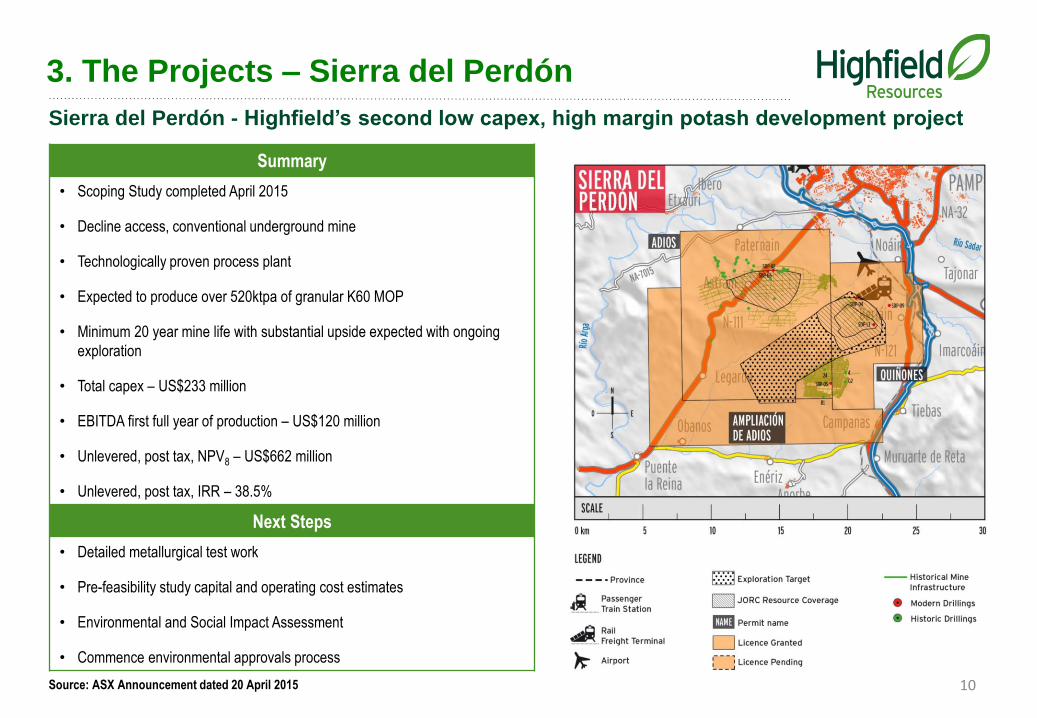

Sierra del Perdón - Highfield’s second low capex, high margin potash development project

Summary

• Scoping Study completed April 2015

• Decline access, conventional underground mine

• Technologically proven process plant

• Expected to produce over 520ktpa of granular K60 MOP

• Minimum 20 year mine life with substantial upside expected with ongoing

exploration

• Total capex – US$233 million

• EBITDA first full year of production – US$120 million

• Unlevered, post tax, NPV8 – US$662 million

• Unlevered, post tax, IRR – 38.5%

Next Steps

• Detailed metallurgical test work

• Pre-feasibility study capital and operating cost estimates

• Environmental and Social Impact Assessment

• Commence environmental approvals process

Source: ASX Announcement dated 20 April 2015 10

3. The Projects – Sierra del Perdón

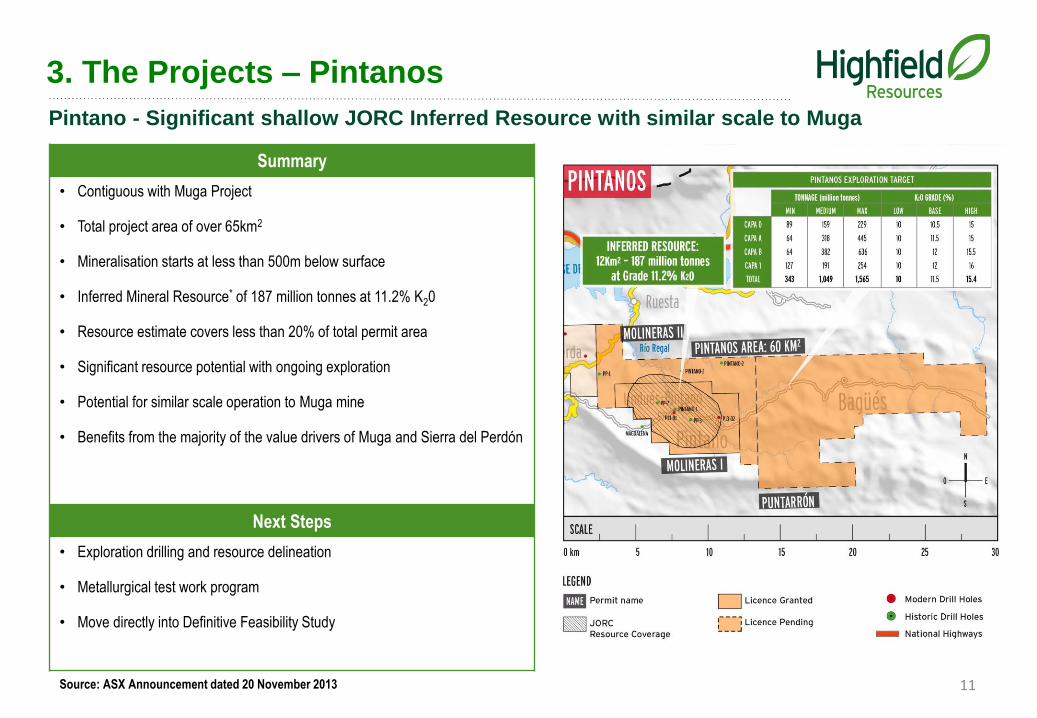

Pintano - Significant shallow JORC Inferred Resource with similar scale to Muga

Summary

• Contiguous with Muga Project

• Total project area of over 65km2

• Mineralisation starts at less than 500m below surface

• Inferred Mineral Resource* of 187 million tonnes at 11.2% K20

• Resource estimate covers less than 20% of total permit area

• Significant resource potential with ongoing exploration

• Potential for similar scale operation to Muga mine

• Benefits from the majority of the value drivers of Muga and Sierra del Perdón

Next Steps

• Exploration drilling and resource delineation

• Metallurgical test work program

• Move directly into Definitive Feasibility Study

Source: ASX Announcement dated 20 November 2013 11

3. The Projects – Pintanos

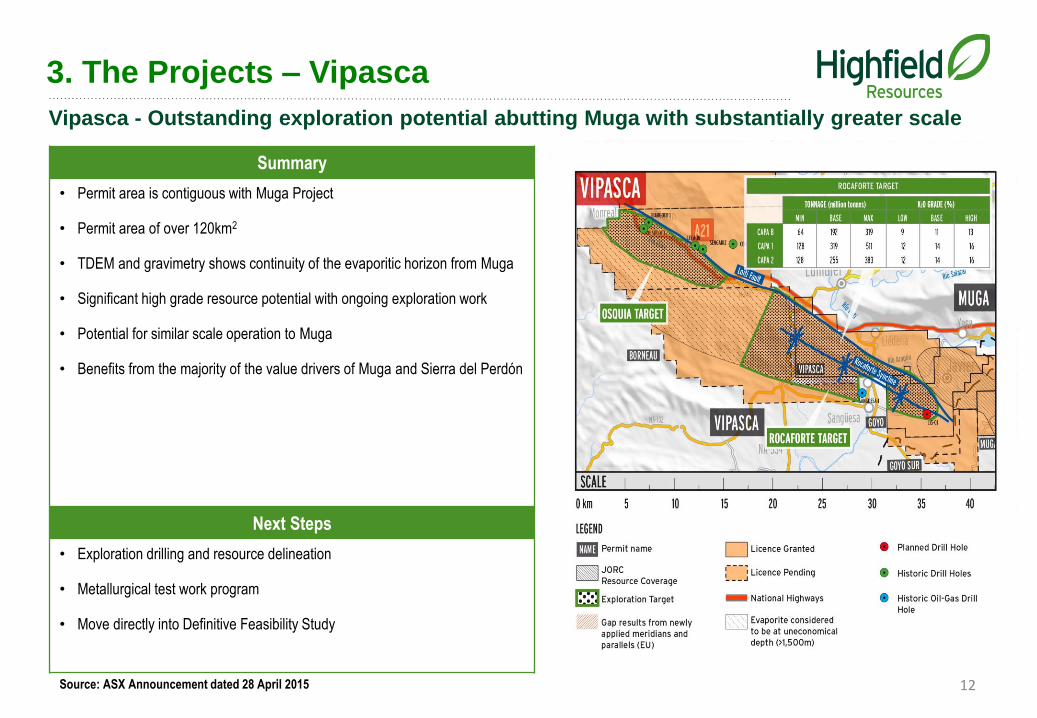

Vipasca - Outstanding exploration potential abutting Muga with substantially greater scale

Summary

• Permit area is contiguous with Muga Project

• Permit area of over 120km2

• TDEM and gravimetry shows continuity of the evaporitic horizon from Muga

• Significant high grade resource potential with ongoing exploration work

• Potential for similar scale operation to Muga

• Benefits from the majority of the value drivers of Muga and Sierra del Perdón

Next Steps

• Exploration drilling and resource delineation

• Metallurgical test work program

• Move directly into Definitive Feasibility Study

12Source: ASX Announcement dated 28 April 2015

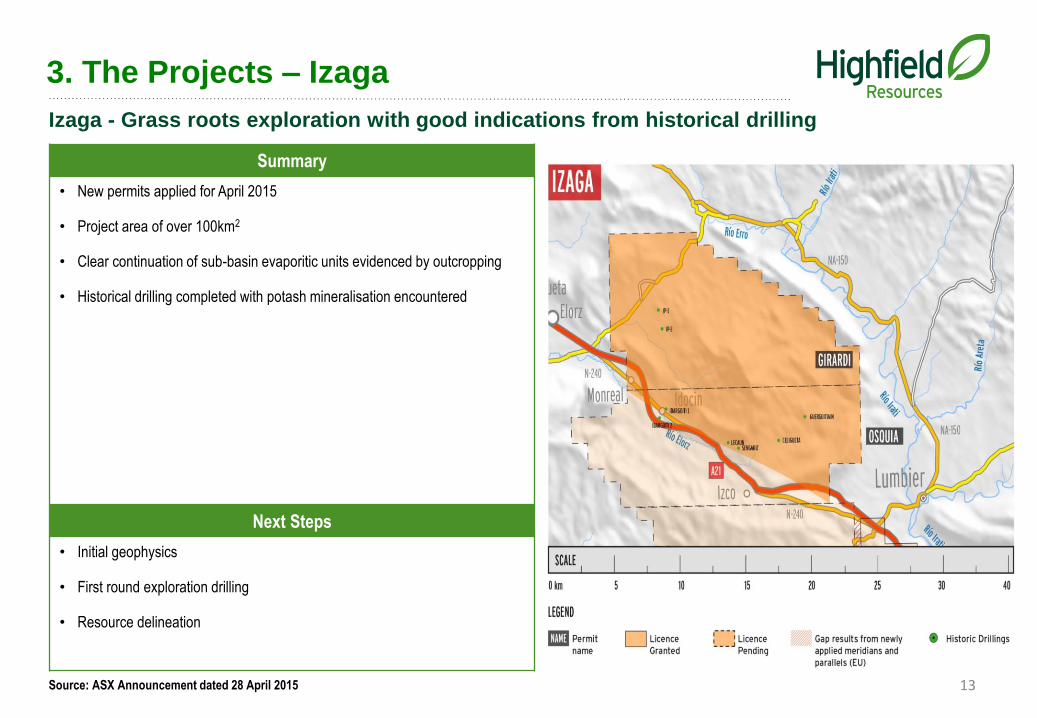

3. The Projects – Vipasca

Izaga - Grass roots exploration with good indications from historical drilling

Summary

• New permits applied for April 2015

• Project area of over 100km2

• Clear continuation of sub-basin evaporitic units evidenced by outcropping

• Historical drilling completed with potash mineralisation encountered

Next Steps

• Initial geophysics

• First round exploration drilling

• Resource delineation

Source: ASX Announcement dated 28 April 2015 13

3. The Projects – Izaga

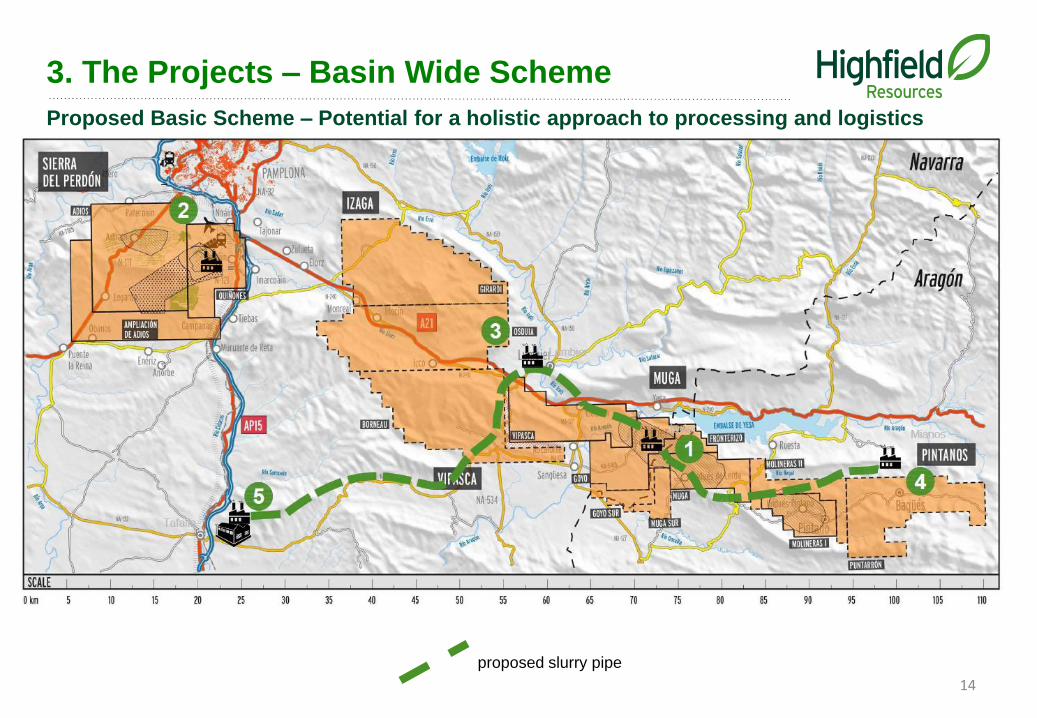

14

proposed slurry pipe

3. The Projects – Basin Wide Scheme

Proposed Basic Scheme – Potential for a holistic approach to processing and logistics

Capex

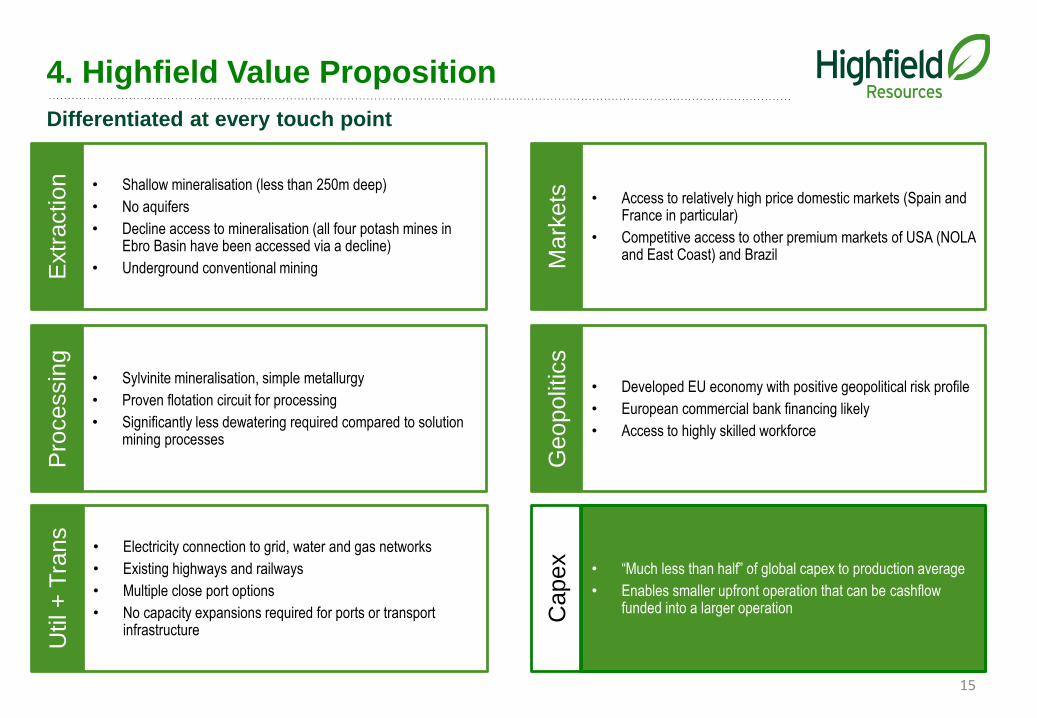

4. Highfield Value Proposition

15

Extr

action • Shallow mineralisation (less than 250m deep)

• No aquifers

• Decline access to mineralisation (all four potash mines in Ebro Basin have been accessed via a decline)

• Underground conventional mining

Pro

cessin

g

• Sylvinite mineralisation, simple metallurgy

• Proven flotation circuit for processing

• Significantly less dewatering required compared to solutionmining processes

Util+

Tra

ns

• Electricity connection to grid, water and gas networks

• Existing highways and railways

• Multiple close port options

• No capacity expansions required for ports or transportinfrastructure

Mark

ets • Access to relatively high price domestic markets (Spain and

France in particular)

• Competitive access to other premium markets of USA (NOLA and East Coast) and Brazil

Geopolit

ics

• Developed EU economy with positive geopolitical risk profile

• European commercial bank financing likely

• Access to highly skilled workforce

• “Much less than half” of global capex to production average

• Enables smaller upfront operation that can be cashflowfunded into a larger operation

Differentiated at every touch point

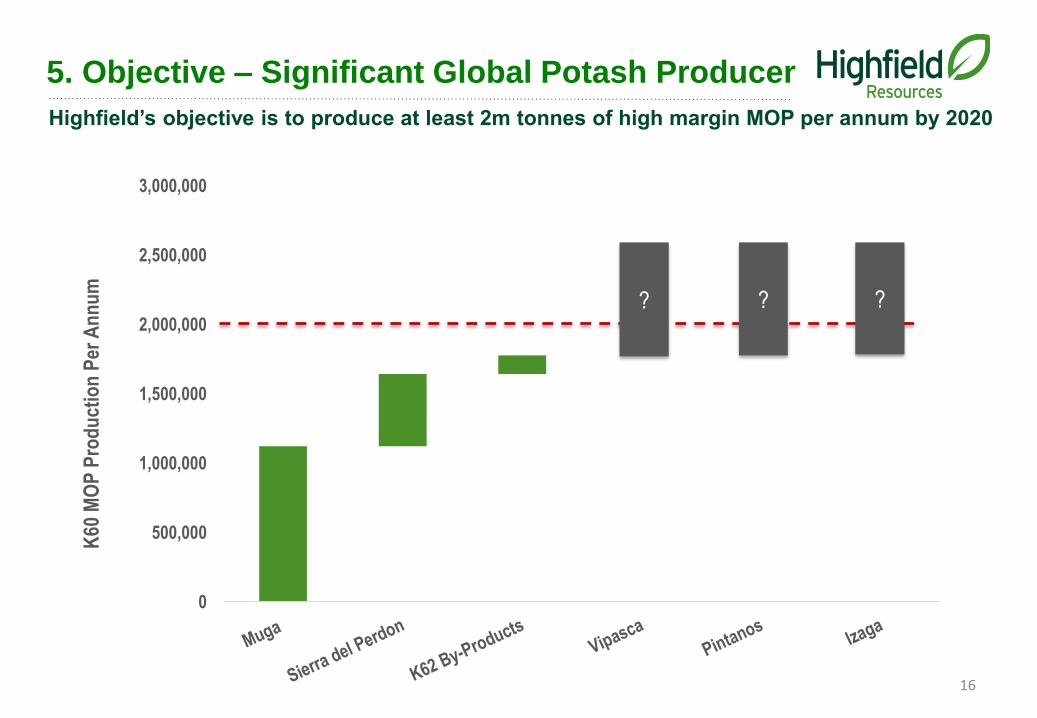

5. Objective – Significant Global Potash Producer

Highfield’s objective is to produce at least 2m tonnes of high margin MOP per annum by 2020

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

K60

MO

P P

rod

uct

ion

Per

An

nu

m

? ? ?

16

17

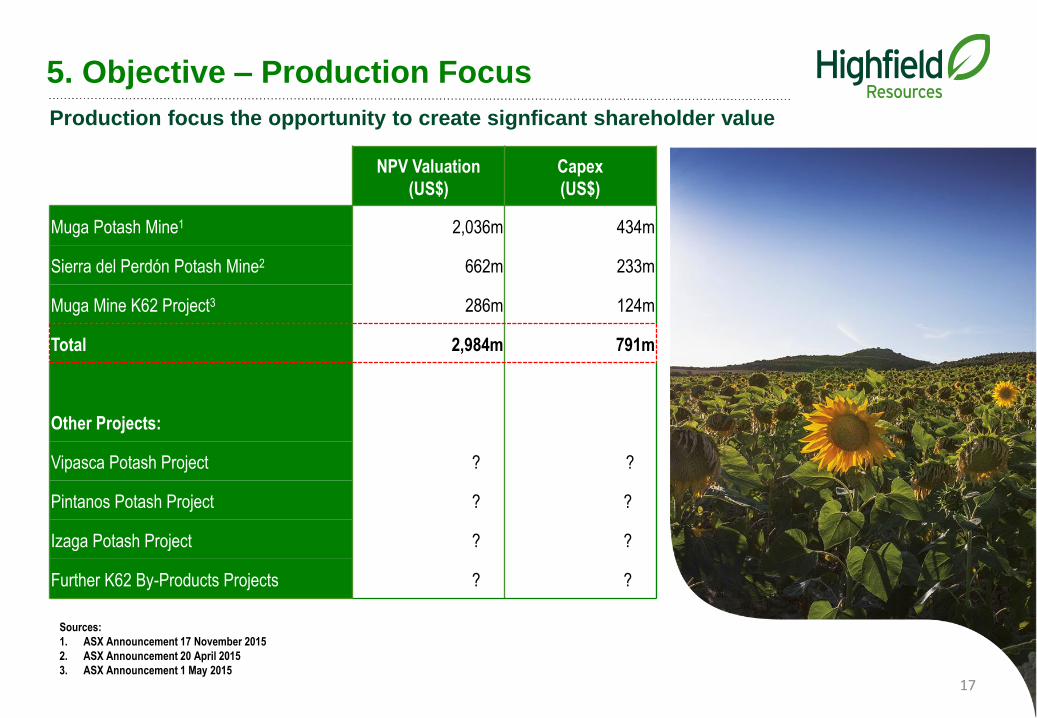

Production focus the opportunity to create signficant shareholder value

5. Objective – Production Focus

NPV Valuation

(US$)

Capex

(US$)

Muga Potash Mine1 2,036m 434m

Sierra del Perdón Potash Mine2 662m 233m

Muga Mine K62 Project3 286m 124m

Total 2,984m 791m

Other Projects:

Vipasca Potash Project ? ?

Pintanos Potash Project ? ?

Izaga Potash Project ? ?

Further K62 By-Products Projects ? ?

Sources:

1. ASX Announcement 17 November 2015

2. ASX Announcement 20 April 2015

3. ASX Announcement 1 May 2015

18

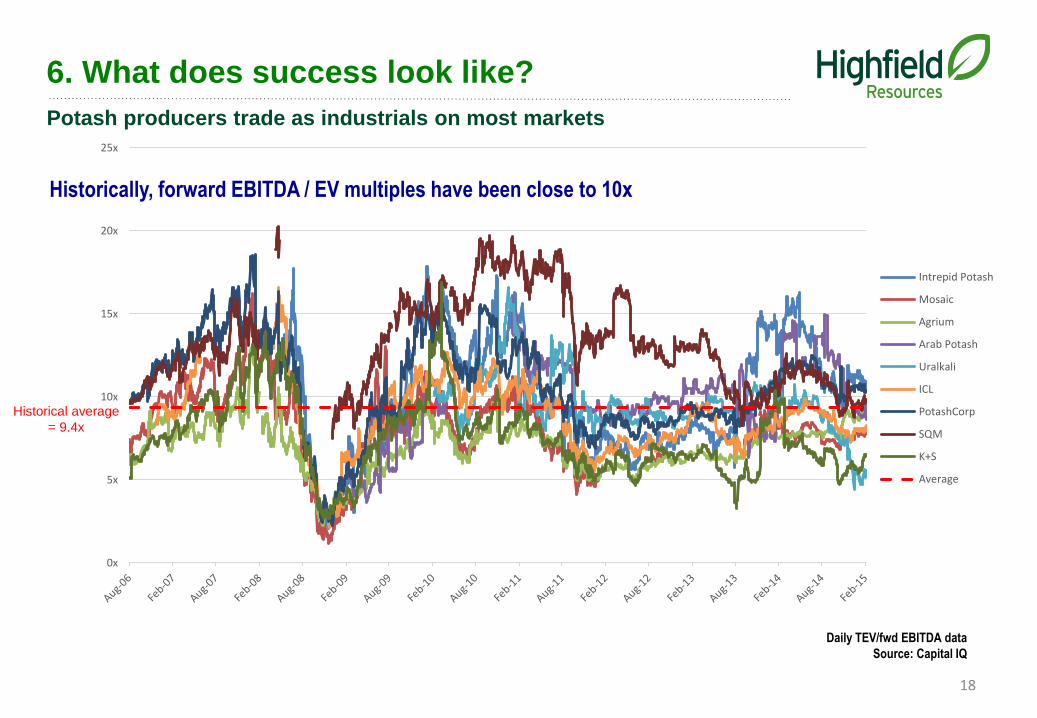

6. What does success look like?

Historically, forward EBITDA / EV multiples have been close to 10x

0x

5x

10x

15x

20x

25x

Intrepid Potash

Mosaic

Agrium

Arab Potash

Uralkali

ICL

PotashCorp

SQM

K+S

Average

Daily TEV/fwd EBITDA data

Source: Capital IQ

Historical average

= 9.4x

Potash producers trade as industrials on most markets

19

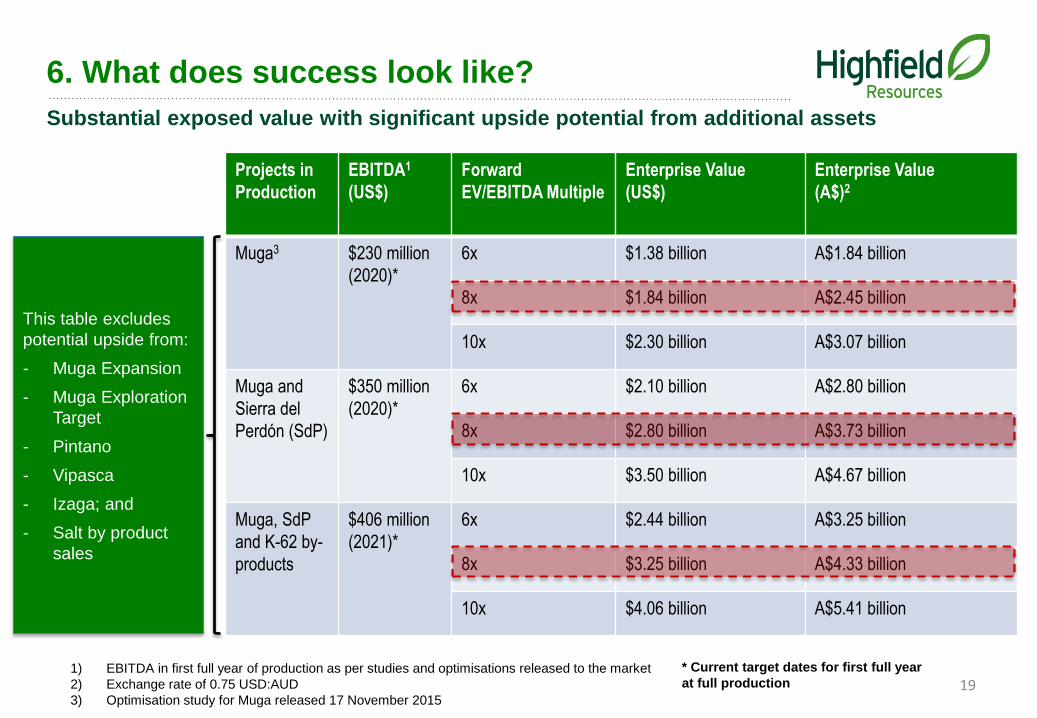

6. What does success look like?

Substantial exposed value with significant upside potential from additional assets

Projects in

Production

EBITDA1

(US$)

Forward

EV/EBITDA Multiple

Enterprise Value

(US$)

Enterprise Value

(A$)2

Muga3 $230 million

(2020)*

6x $1.38 billion A$1.84 billion

8x $1.84 billion A$2.45 billion

10x $2.30 billion A$3.07 billion

Muga and

Sierra del

Perdón (SdP)

$350 million

(2020)*

6x $2.10 billion A$2.80 billion

8x $2.80 billion A$3.73 billion

10x $3.50 billion A$4.67 billion

Muga, SdP

and K-62 by-

products

$406 million

(2021)*

6x $2.44 billion A$3.25 billion

8x $3.25 billion A$4.33 billion

10x $4.06 billion A$5.41 billion

1) EBITDA in first full year of production as per studies and optimisations released to the market

2) Exchange rate of 0.75 USD:AUD

3) Optimisation study for Muga released 17 November 2015

This table excludes

potential upside from:

- Muga Expansion

- Muga Exploration

Target

- Pintano

- Vipasca

- Izaga; and

- Salt by product

sales

* Current target dates for first full year

at full production

7. Summary

20

Logo of the Company’s Spanish Foundation that is currently delivering

several projects with local communities

• Highfield Resources is developing the Muga Potash Project, one of its five

100% owned potash projects in Northern Spain.

• The projects are in a producing potash basin

• The flagship Muga Mine Project has the lowest capex of any

development stage potash project.

• In production it will have first quartile EBITDA margins driven by

combination of high price end markets and low total cash costs to

customer.

• The projects share many characteristics required to be low capex,

high margin potash mines.

• A management team has been assembled with proven mine building

experience in Spain and in potash operations.

• There are few projects in any commodity that are as compelling as the

Muga Project.

www.highfieldresources.com.au

REGISTERED OFFICE

169 Fullarton Road

Dulwich SA 5065

Australia

HEAD OFFICE

Avenida Carlos III, 13-15, 1B, 31002 Pamplona, Spain

T +34 948 050 577 | F +34 948 050 578

FURTHER INFORMATION

Anthony Hall - Managing Director T +34 617 872 100

John Claverley - General Manager T +34 607 748 435

Hayden Locke - Corporate Development T +34 609 811 257

Related Documents