A Report On THE CORPORATE CREDIT MONITORING AND FOLLOW-UP PRACTICES OF INDIAN BANK By Chiranjit Basu INDIAN BANK, G .C. AVENUE BRANCH KOLKATA 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A Report

On

THE CORPORATE CREDIT MONITORING AND FOLLOW-UP PRACTICES OF INDIAN BANK

By

Chiranjit Basu

INDIAN BANK, G .C. AVENUE BRANCH

KOLKATA

1

A Report

On

THE CORPORATE CREDIT MONITORING AND FOLLOW-UP PRACTICES OF INDIAN BANK

By

Chiranjit Basu

Enrollment No. 09BSHYD0234

INDIAN BANK, G .C. AVENUE BRANCH

KOLKATA

A report Submitted in partial fulfillment of

The requirements of

MBA Program of

IBS Hyderabad

SUBMITTED TO: Company Guide: Faculty Guide: Mr. P. K. Misra Prof. L. Sridharan Senior Manager ICFAI Business School Indian Bank, Ganesh Chandra Avenue Branch Hyderabad Kolkata

Date of submission: 21st May, 2010

2

AUTHORIZATION

This is to certify that Mr. Chiranjit Basu, Enrollment No. 09BSHYD0234 has done his summer internship in Indian Bank, 1, Ganesh Chandra Avenue, Kolkata and has submitted this project report entitled “The Corporate Credit Monitoring and Follow-Up Practices of Indian Bank” towards partial fulfillment of the requirements for the award of the Post Graduate in Management 2009-2011. This Report is the result of his own work and to the best of my knowledge no part of it has earlier been comprised in any other report, monograph, dissertation or book. This project is carried out under my overall supervision.

Mr. P. K. Misra KOLKATA Senior Manager May 21, 2010 Indian Bank, G. C. Avenue

3

ACKNOWLEDGEMENT

A journey is easier when we travel together. Interdependence is certainly more important than independence. It will always be my pleasures to thank those who have helped me in making this project a lifetime experience for me.

I would like to express my heartiest gratitude to Indian Bank, Ganesh Chandra Avenue Branch, Kolkata for giving me an opportunity to work with its Department of Loans and Advances, my Institute and important persons associated with this project as without their guidance and hard work I would have never ever got a chance to have real life experience of working with a Public Sector Bank of such a great repute and learn practically about the Credit Appraisal and monitoring practices of Indian Bank.

I would also like to extend my gratitude to Mrs. Sikha Majumdar (Chief Manager, G. C. Avenue Branch) for giving me an opportunity to join her to know and learn various aspects of the Loans and Advances in the organization.

It is my privilege to thank Mr. P. K. Misra (Industry Guide & Chief Mentor) whose guidance has made me learn and understand the finer and complicated aspects of banking, in general and of Credit Monitoring of Indian Bank, in particular. The help and guidance which he has extended to me has made me feel as being an integral part of the organization.

I would like to pay my heartiest regards to Mr. K. P. Bose, the Concurrent Auditor to the branch. His meticulous technical expertise and above all kindness to share it with others need special mention. Without his inspiration and advices throughout the project period, this thesis would not have been possible.

Throughout the time I have gained wonderful guidance and tremendous support from my internal guide, Mr. L. Sridharan, a tireless champion. It has been a great pleasure to be associated with him and I feel almost lucky to have him as my mentor. I forward my heartfelt thanks to him.

I would like to thank all the staff members of Indian Bank, G. C. Avenue Branch for providing me with necessary information and for their affectionate care, valuable time and their patience for making this project a worth. I would especially thank Mrs. Shyamali, Mr. Partho, Mr. Deben, Mr. Samitabha, Mr. Rajesh Prasad, Mr. Keshab, Mr. Pradyut, Mr. Bidhan and Mr. Sridam for their constant help.

The greatest credit goes to the blessings bestowed upon me by Almighty Lord Krishna without whose causeless mercy, I could not have even moved a step forward and to my parents who are always a constant source of inspiration in all my endeavors. Chiranjit Basu

4

TABLE OF CONTENTS:

AUTHORIOZATION……………………………………………………………………………………………….3

ACKNOWLEDGEMENT………………………………………………………………………………………….4

ABSTRACT…………………………………………………………………………………………………………....8

1. INTRODUCTION……………………………………………………………………………………………….9

1.1 STATEMENT OF THE PROBLEM…………………………………………………………………10

1.2 OBJECTIVE OF THE STUDY…………………………………………………………………………11

1.3 LAYOUT OF THE STUDY…………………………………………………………………………….11

2. PROFILE OF THE COMPANY……………………………………………………………………………12

3. REVIEW OF LITERATURE………………………………………………………………………………..13

4. GENERAL METHODOLOGY…………………………………………………………………………….17

4.1 METHODS OF CREDIT APPRAISAL……………………………………………………………..17

4.2 MONITORING OF IMPLEMENTATION OF PROJECT……………………………………20

4.3 CREDIT FACILITIES FOR WORKING CAPITAL………………………………………………21

4.4 SANCTION & DISBURSEMENT OF CREDIT………………………………………………….28

4.5 POST-SANCTION MONITORING OF ADVANCES…………………………………………30

4.6 MONITORING OPERATIONS IN THE ACCOUNT………………………………………….37

4.7 IDENTIFICATION OF WILLFUL DEFAULTERS’ ACCOUNTS……………………………40

5. CREDIT RISK ASSESSMENT………………………………………………………………….………….42

5.1CATEGORIZATION OF RISK & ITS EVALUATION………………………………………….43

5

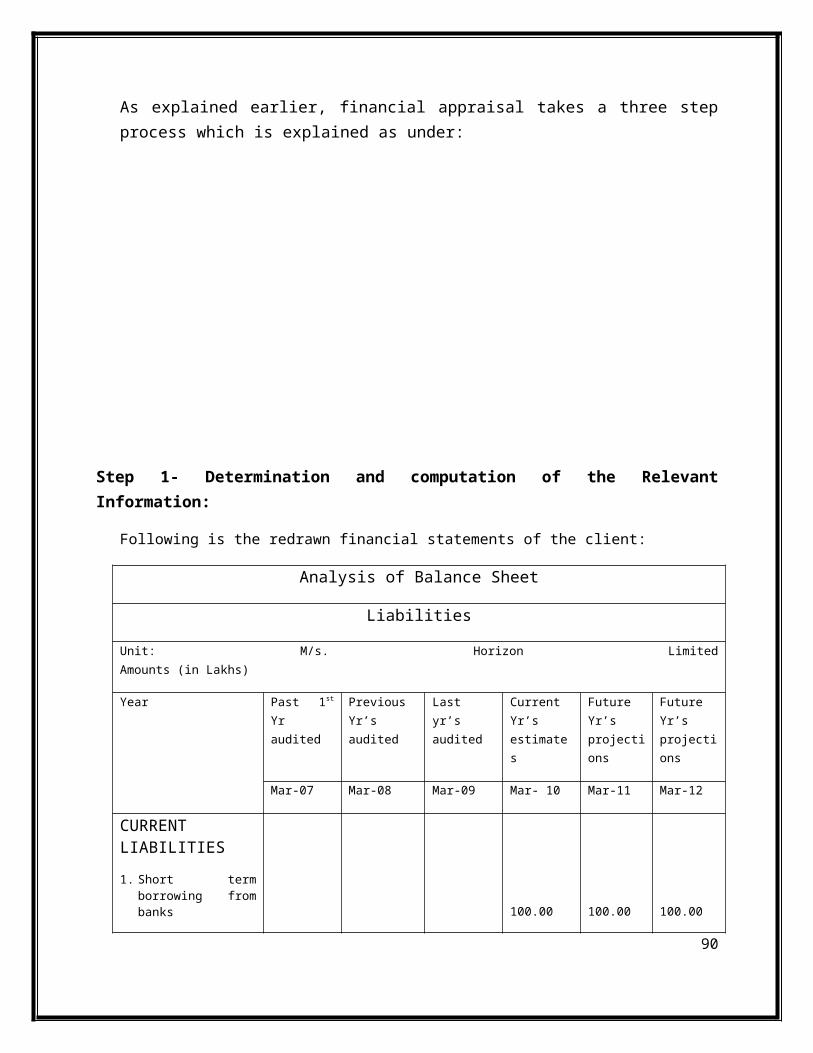

5.2FINANCIAL APPRAISAL………………………………………………………………………………46

5.2.1 BROAD STEPS FOR FINANCIAL APPRAISAL……………………………………………………..……47

5.2.2 RATIO ANALYSIS……………………………………………………………………………..………………..…49

5.2.3 SENSITIVITY ANALYSIS……………………………………………………………….…………………………52

5.2.4 BREAK EVEN ANALYSIS……………………………………………………..………………………………….53

5.2.5 OPERATING CYCLE……………………………………………………………………………………………….53

5.2.6 MAXIMUM PERMISSIBLE BANK FINANCE…..............................................................54

6. PRACTICAL CASE STUDY…………………………………………………………………………………56

6.1 ASSESSING THE PROMOTERS’ BACKGROUND…………………….…………………….56

6.2 ANALYSIS OF ASSET & LIABILITY STATEMENT……………………………………………58

6.3 ACTIVITIES PROPOSED IN THE CREDIT PROPOSAL…………………………………….61

6.4 ECONOMIC FEASIBILITY…………………………………………………………………………...61

6.5 INDUSTRY ANALYSIS…………………………………………………………………………………62

6.6 INDUSTRY GROWTH…………………………………………………………………………………62

6.7 SMEs IN AUTO COMPONENTS INDUSTRY…………………………………………………62

6.8 TECHNICAL FEASIBILITY…………………………………………………………………………...63

6.9 FINANCIAL APPRAISAL………………………………………………………………………………63

6.10SENSITIVITY ANALYSIS……………………………………………………………………………..70

6.11BREAK EVEN ANALYSIS…………………………………………………………………………….72

6.12MAXIMUM PERMISSIBLE BANK FINANCE…………………………………………………73

6.13CREDIT RISK ASSESSMENT……………………………………………………………………….74

7. STUDY ON THE NPA ACCOUNTS OF THE BANK………………………………………………80

6

7.1 OUT OF ORDER STATUS……………………………………………………………………………80

7.2 INCOME RECOGNITION……………………………………………………………………………81

7.3 NORMS FOR ASSET CLASSIFICATION………………………………………………………..81

7.4 SPECIAL MENTION ACCOUNTS (SMA)………………………………………………........82

7.5 NPA LOANS- A THEORETICAL PERSPECTIVE………………………………………………85

8. CONCLUSION………………………………………………………………………………………………..94

9. LIMITATIONS OF THE STUDY………………………………………………………………………….95

10.RECOMMENDATIONS…………………………………………………………………………………….96

11.REFERENCES………………………………………………………………………………………………..114

LIST OF ANNEXURES

ANNEXURE 1………………………………………………………………………………………………….99

ANNEXURE 2……………………………………………………………………………………………….102

ANNEXURE 3……………………………………………………………………………………………….103

ANNEXURE 4……………………………………………………………………………………………….106

ANNEXURE 5……………………………………………………………………………………………….107

ANNEXURE 6……………………………………………………………………………………………….110

ANNEXURE 7……………………………………………………………………………………………….113

7

Abstract

The project mainly concerns itself with the study of corporate credit monitoring practices of Indian bank, G. C. avenue branch, Kolkata with regards to large borrowal accounts with sanctioned credit limit of Rs. 1 Crore and above. As the first step, the project involves in depth analysis of the important returns /statements in the monitoring of working capital advances such as, MSODs, inspection of stocks, CMO monthly report, operations in the account, Quarterly information system (QIS) statements, annual audited accounts, review/renewal of advance, asset classification under IRAC and other norms, credit rating under RAM model, stock audit, concurrent auditor’s report and unit inspection report. The pre sanction appraisal involves the preparation of Credit Reports and careful study of the borrower’s character, capacity and capital (the 3 C’s). The internal and external credit ratings accorded to the company are studied. Track records of repayment / cash flow projections for capacity to repay are checked. The Key Ratios are studied to understand and evaluate Key Risk Indicators of the relevant industry. The compliance of terms and conditions by the borrower is studied and any deviation thereto is reported. Pre-release Audit is done in this regard. Legal audit reports are studied to understand the nature of the securities (stocks, equitable mortgages, land, residences etc.) entrusted with the bank. As the next step of follow-up, documentation of necessary formats and documents which are to be issued to the borrower on sanction of a renewal/ enhancement is done to create a charge on the security. Drawing Limits of various borrowal accounts are calculated on a monthly basis. As post sanction monitoring, stock and book debt audit are done to check adequate availability of primary security, its nature and quantity. Regular monitoring of the operations in the borrowal account is done to keep a tab on the fluctuations in the account. Few review/ renewal proposals are taken up to study the nature of an ongoing borrower and performances (financial, production, credit rating etc.) of the company are checked. Apart from the above steps, few activities are concurrent as the project advances, such as the unit inspection with the bank officials to cross verify the stock statement. The year end balance sheets and P & L statements submitted by the borrowers (FY 2009-2010) are studied and comparisons made on the projections with actuals especially on sales and profit. To understand the working capital assessment better, various structured products (such as, IND SME secure) of the bank are studied. Finally, a study on the bank’s NPA accounts is carried out to understand the nature of the non-remunerative borrowers and suggest possible remedial measures to prevent slippage of an account into substandard category.

8

Section One: INTRODUCTION

Banking is both an art and science, which cannot be guided by merely a set of rules. It is to be guided by general principles only. Even then there is no rigidity in the application of the set of principles in banking. As a consequence of post liberalization of the economy and on account of reforms in financial sector, the Banking Industry has witnessed phenomenal changes during the last decade. In view of such liberalization, the Credit Administration also needs to be re-looked, taking into account the variety of credit products unveiled in the industry and the competition faced from the new generation banks in luring the potential customers to strengthen their asset portfolio. There has been thrust for lending under structured retail banking products which are built on the basic platform of the Conventional Advances category (O&M Division, Head Office, 2006, manual of Instructions on Conventional Advances. Chennai: Indian Bank).

Adequately managing credit risk in financial institutions (FIs) is critical for the survival and growth of the FIs. In the case of banks, the issue of credit risk is even of greater concern because of the higher levels of perceived risks resulting from some of the characteristics of clients and business conditions that they find themselves in. Banks are in the business of safeguarding money and other valuables for their clients. They also provide loans, credit and payment services such as checking accounts, money orders and cashier’s checks. Banks also may offer investment and insurance products and a wide whole range of other financial services (Takang Felix Achou, Ntui Claudine Tenguh, 2008, Bank Performance And Credit Risk Management, University of Skovde).

Credit creation is the main income generating activity for the banks. But this activity involves huge risks to both the lender and the borrower. The risk of a trading partner not fulfilling his or her obligation as per the contract on due date or anytime thereafter can greatly jeopardize the smooth functioning of a bank’s business. On the other hand, a bank with high credit risk has high bankruptcy risk that puts the depositors in jeopardy. Among the risk that face banks, credit risk is one of great concern to most bank authorities and banking regulators. This is because credit risk is that risk that can easily and most likely prompts bank failure.

Credit management is a structured approach to managing uncertainties through risk assessment, developing strategies to manage it, and mitigation of risk using managerial

9

resources. The strategies include transferring to another party, avoiding the risk, reducing the negative effects of the risk, and accepting some or all of the consequences of a particular risk. (Available from: http://www.hsbc.com/ tips on credit management [accessed 15th April, 2010].

This thesis takes a fast look on Banking and Credit management and further probes into bank risk exposure, borrower’s assessment, effective post-sanction management and control. An attempt will be made to unfold the use of some credit management, evaluation and assessment tools, models, and techniques.

1.1 STATEMENT OF THE PROBLEM:

The very nature of the banking business is so sensitive because more than 85% of their liability is deposits from depositors (Saunders, Cornett, 2005). Banks use these deposits to generate credit for their borrowers, which in fact is a revenue generating activity for most banks. This credit creation process exposes the banks to high default risk which might lead to financial distress including bankruptcy. All the same, beside other services, banks must create credit for their clients to make some money, grow and survive stiff competition at the market place.

Banks forward credit to various types of business entities with a view to help them in carrying out various activities related to their business. Creating such borrowal accounts does not only involve assessment of the operations of the account, but also timely following up with the borrower to ensure the health of the credit and the proper end use of the fund.

The principal concern of this thesis is to ascertain to what extent banks can manage their large corporate credits, what tools or techniques are at their disposal to appraise, disburse and follow up with the borrowers and to what extent their performance can be augmented by analyzing and suggesting possible remedial measures to identify early warning signals in the quality of the asset.

10

1.2 OBJECTIVE OF THE STUDY:

To study the corporate credit monitoring practices of the bank extending credits to several manufacturing and trading firms having large borrowal accounts.

To suggest possible measures (if any) to identify early warning signals to prevent slippage of accounts in NPA category.

To appreciate the essential features of a legally binding contract.

To understand the issues involved in pursuing slow payers and debtor recovery.

To understand the Legal Processes in the Collection of Debts.

1.3 LAYOUT OF THE STUDY:

This study is divided into ten sections; the first section cuts across a general introduction, statement of problem, objective of the study, and layout of the study.Section two is on a brief introduction on the profile of Indian bank in which organization the thesis work is done.Section three elucidates the review of literature related to the work done in this project.Section four is on the methodology adopted to carry out the thesis work.Section five describes the Credit Risk Assessment in the Bank.Section six describes a comprehensive practical case study on the credit appraisal process of a borrower seeking term loan and working capital finance from the bank. Section seven is on a detailed study that is made in relation to the non-performing assets (bad debts) of the Bank.Section eight relates to the conclusions reached after the careful study of the findings of the research.Section nine describes the inherent limitations of the studySection ten elucidates few recommendations related to various issues involved in credit monitoring and NPA control.Section eleven is on the references used for the present work.

11

Section Two: PROFILE OF THE COMPANY

Indian bank is a premier bank owned by government of India. It was established on 15 th august, 1907 as part of the Swadeshi Movement and has been serving the nation since then with a current team of over 22000 dedicated staff. Total Business crossed Rs.1, 24,413 Crores as on 31.03.2009. Its Operating Profit increased to Rs. 2228.83 Crores as on 31.03.2009 and the net profit stands at Rs. 1245.32 Crores. Indian Bank follows the Core Banking Solution (CBS) in all 1750 branches making its efficiency commendable. It has international presence in Singapore and Colombo including a Foreign Currency Banking Unit at Colombo. It is a fully diversified banking firm with three subsidiary companies, Indbank Merchant Banking services Ltd., Indbank Housing Ltd., IndFund management Ltd. Indian bank is also a frontrunner in specialized banking services. It has 90 Forex Authorized branches inclusive of 1 Specialized Overseas Branch at Chennai exclusively for handling forex transactions arising out of Export, Import, Remittances and Non Resident Indian business. The bank has played several leadership roles in rural development. It pioneered in introducing Self Help Groups and Financial Inclusion Project in the country. It has won many accolades for its achievements. It is an Award winner for Excellence in Agricultural Lending from Honorable Union Minister for Finance. It is the winner of Best Performer Award for Micro-Finance activities in Tamil Nadu and Union Territory of Pondicherry from NABARD.

IMAGE which is the acronym for Indian bank Management Academy for Growth and Excellence is the prestigious Training Academy of Indian Bank. The academy stands at a quiet and peaceful locality of Chennai, India in a sprawling complex, with modern amenities like air-conditioned Class Rooms, Seminar Halls, indoor recreational facilities and a state-of-the-art Auditorium.

The Academy caters to the training needs of Indian Bank, its Subsidiaries and other members of the banking fraternity. The Academy also undertakes Training of Middle and Senior Management Personnel of Government, Public Sector and Corporate companies. The Infrastructure facilities are also available on payment of stipulated fees to select group of corporate companies and other bodies (Available from: http//www.indianbank.co.in [accessed 15th April].

12

Section Three: REVIEW OF LITERARTURE

How can bank managers, investors, bank regulators and other stakeholders know whether a bank is a good monitor? This question has gained in importance since the onset of the recent financial crisis, during which a large number of banks around the world have shown to be insufficiently attentive to risks within their portfolios. In this paper we study various methods for analyzing the ability of a bank to monitor its commercial loans.

The credit appraisal practices (both individual and corporate) of the bank, and in turn its effect on the overall profitability and loss assets of the bank has remained an active topic of banking finance research. Although there has been extensive study done on the banks’ ability to forecast the client’s repaying capability and its own risk taking ability through pre-sanction appraisal, there is not much research done on Post-sanction follow up on similar topic.

Although non-financial corporate debt (bond issues and privately issued debt) has become more common in the past 10-20 years, bank loans are still the prime source of business finance, especially for small and medium size enterprises (SME’s). As a consequence, banks’ ex-ante assessment of the riskiness of loan applicants, the resulting decision to grant credit or not at some risk-adjusted interest rate, and the way in which monitoring of granted loans takes place, are of great importance for most businesses.

Bank regulators also depend increasingly on the risk assessments made by banks. In the new Basel II Accord (Basel Committee on Banking Supervision, (2004), International Convergence of Capital Measurement and Capital Standards: a Revised Framework, June 2004, Basel, Switzerland), internal risk ratings produced by banks have been given a prominent role and the size of the required buffer capital will be made contingent on banks’ appraisal of ex-ante individual borrower risk. It will be up to the banks to characterize the riskiness of the borrowers and loans in their portfolios by means of a limited number of risk categories or ’rating classes’(Basel Committee on Banking Supervision, (2003), Quantitative Impact Study 3: Overview of Global Results, May 2003, Basel, Switzerland, available from: http:// www.bis.org/ [accessed 18th May, 2010]

Assessing borrower risk is generally considered one of the banking industry´s core activities. Banks’ role as an intermediary is commonly explained by their supposedly superior ability to collect and assess information with respect to borrower risk. Research has been extensive in this area, since Diamond formalized the concept of a delegated monitor (Diamond, Douglas,

13

(1984), Financial Intermediation and Delegated Monitoring, Review of Financial Studies, no. 51, pp.393-414).

When a borrower suffers unexpected losses its probability of bankruptcy rises and by a familiar moral hazard mechanism its incentives to invest optimally falls. A lender who monitors the borrower’s account and is able to detect such losses may be able to create incentives for the borrower to take actions that improve expected return. In particular, the lender may strive to ensure that the operating loan extended by the bank finances operations and not unexpected equity losses. It is thus an important advantage to a lender to be able to detect changes in normal seasonal borrowing needs, that is, flows of inventory and accounts receivable.

Although much of the literature cites a bank’s ability to monitor borrowers as one of its special talents, the literature rarely describes what gives the bank its monitoring advantage over other types of lenders. A bank loan officer has access to fine-grained information about a borrower’s activities through its operating account, as he or she can observe checks on an item-by-item basis and compare them to the borrower’s pro forma business plan (Loretta J. Mester, Leonard I. Nakamura, Micheline Renault, 2001, Checking Accounts and Bank Monitoring, Federal Reserve Bank of Philadelphia and The Wharton School, University of Pennsylvania (online). Available from: http://www.ssrn.com/ [accessed 20 May, 2010).

If banks collect private information about the borrowers they monitor, as economic theory tells us, in addition to the public information that a credit bureau possesses, and if credit ratings summarize the information included in them, then bank credit ratings should be able to forecast future changes in credit bureau ratings. On the other hand, credit bureau ratings should not be able to predict changes bank ratings (Treacy, William and Mark Carey, (2000), Credit risk rating systems at large U.S. banks, Journal of Banking and Finance, No. 24, pp. 167-201).

Banks’ internal credit ratings summarize the risk properties of the bank loan portfolio and are used by banks to manage their risk. One usually thinks of these ratings as monotonic transforms of the probability of default, although Loffler and Altman and Rijken have argued that credit ratings may have more complex functions (Loffler, Gunter, (2004), Ratings versus Market-based Measures of Default Risk in Portfolio Governance, Journal of Banking and Finance 28, pp. 2715-2746).

Internal ratings can also be considered to contain evidence of the private information that banks possess, and distinguishes them from ratings produced by credit bureaus (Loretta J.

14

Mester, Leonard I. Nakamura , Micheline Renault,2001, Checking Accounts and Bank Monitoring, Federal Reserve Bank of Philadelphia and The Wharton School, University of Pennsylvania (online). Available from: http://www.ssrn.com/ [accessed 20 May, 2010).

Another strand of literature has studied what conditions may weaken banks’ or other investors’ monitoring efforts. Recent work has also shown that screening and monitoring quality by financial intermediaries dropped substantially in the wake of the current financial crisis (Keys, Benjamin J., Tanmoy Mukherjee, Amit Seru, Vikrant Vig, 2009, Financial Regulation and Securitization: Evidence From Subprime Loans, Journal of Monetary Economics, 56 (5) (July, 2009), pp700-720). However, the general notion that financial intermediaries are superior monitors relative to, for example, public alternatives and other investors, remains empirically unchallenged. In particular, the informational superiority of bank credit ratings over public alternatives has not been demonstrated empirically.

The ability of a bank to collect private information and thereby produce a superior judgment of borrowers’ expected performance is of relevance not only for regulators and banks, but potentially also for the industrial organization of borrowers and for business cycle theory. Dell’Ariccia and Marquez (2004), for example, have pointed out that informational asymmetries among lenders affect banks’ ability to extract monopolistic rents by charging high interest rates. As a result, banks finance borrowers of relatively lower quality in markets characterized by greater information asymmetries (Dell’Ariccia, Giovanni, and Robert Marquez, 2004, "Information and bank credit allocation", Journal of Financial Economics 72, pp185—214).

When forced to curtail lending, they reallocate their loan portfolio towards more creditworthy, more captured borrowers. Povel, Singh and Winton (2007) investigate the relation between the cost of monitoring, and reporting fraud incentives for companies across the business cycle. Their work has implications for how carefully financial institutions should scrutinize firms in which they invest and for the gains from increased informativeness of publicly available information (Povel, Paul, Rajdeep Singh and Andrew Winton, 2007, "Booms, Busts, and Fraud", Review of Financial Studies 20 (4), pp. 1219-1254).

Profitability and Viability of Development Financial Institutions are directly affected by quality and performance of advances. The basic element of Sound NPA Management System is quick identification of Non- Performing advances, their containment at minimum levels and ensuring that their impingement on the financials is minimum. Excessive Reliance on Collaterals has led Institutions to long drawn litigations and hence it should not be sole criteria for sanction. Banks should manage their exposure limit to few borrower(s) and linkage should be placed with net

15

owned funds for developing control over high leverages of borrower level. Exchange of credit information among banks would be immense help to them to avoid possible NPAs. Management Information system and Market intelligence should be utilized to their full potential (Joshi, Dr. Amitabh, Analysis of Non-Performing Assets of IFCI Ltd (2003).

16

Section Four: GENERAL METHODOLOGY

The methodology followed in this project is in accordance with the guidelines for post sanction follow up and monitoring by Indian Bank. The HO is quite specific about the steps that are to be taken to follow up with the borrowal accounts and reporting the same. The whole project is studied with the help of few large borrowal accounts of different trading and manufacturing companies in and around Kolkata. The project is divided into three main parts:

1. Pre sanction appraisal

2. Disbursement

3. Post-sanction Monitoring and Analysis

4.1 METHODS OF CREDIT APPRAISAL:

The main methods of credit appraisal are done according to the Indian bank’s Loan Policy (2009-2010) as per RBI’s Guidelines. This is framed by the Head Office’s Credit Division. The methods by which a credit proposal is appraised are as follows:

4.1.1 Assessment of the profile of the borrower:

Purpose or need for credit: The banker should be very clear as to why the credit is required by the borrower and the sources wherefrom the borrower is expected to replay back the loan. If the advance is for hoarding stocks or for speculation, it should be discouraged. Again, if the money required is for liquidation of prior borrowings or to make good the loss incurred or for unproductive expenditure, then the banker should cautiously appraise the proposal.

The borrower may require stop-gap finance till the money from other sources flows in (for example, issuing of share capital/debentures likely to be subscribed to by the public). Such proposals may be favorably considered for good parties depending upon merits of each case and subject to RBI guidelines from time to time.

17

Also, with emphasis by government on export growth, the banks have been instructed to allocate at least 12% of their total credit to export sector. The bank has to finance new classes of people namely professionals, self employed persons, retail traders, agriculturists and transport operators for productive purposes and generation of employment.

Types of facilities required: while appraising a credit proposal, the bank has to evaluate and decide different types of credit that the borrower requires.

Integrity and reputation of borrower: the next step in appraisal process is to check the market reputation and the integrity of the prospective borrower. This is to ensure the proper end use of funds and timely service of the installment and interest.

Borrower’s business expertise, status of his economic activity: the bank has to ensure the efficiency with which the prospective borrower runs his business, his experience and expertise in the business concerned and the short and long term economic viability of the business.

Current risk profile and its sensitivity to changes: the bank has to enumerate the risk profile of the prospective borrower, check whether it fits for the advance and also evaluate the future chances of the borrower’s account being sensitive in terms of risk.

Internal and external credit rating: a very important next step is to accord suitable credit rating to the prospective borrower. A credit rating estimates the credit worthiness of an individual or corporation. It is an evaluation made by credit bureaus of a borrower’s overall credit history. Typically, a credit rating tells a lender or investor the probability of the subject being able to pay back a loan. Internal credit rating is done by the bank itself whereas the external ratings are given by professional credit rating agencies.

Adequacy and enforceability of the tangible securities/ guarantees under various scenarios : the securities charged to the bank should be free from all encumbrances and they should be legally enforceable at all times under all circumstances.

4.1.2 Standards for financial norms:

The next step is to check the Key Ratios of the business of the borrower, such as, Current ratio, Debt equity ratio, TOL/TNW, Interest Coverage ratio, Security Coverage ratio etc. The standard financial norms for considering credit proposals are given below:

18

S. no Key Ratios Bench Mark (Minimum)

1. Current Ratio i. 1.33(without inclusion of annual maturing term liabilities as current liability)

ii. 1.17(with inclusion of annual maturing term liabilities as current liability)

iii. 1.00(including annual maturing term liabilities in exceptional cases like sugar industry)

2 Debt Equity Ratio*

i. 2:1 for medium and large scale industriesii. 4:1 for infrastructure projects

3 TOL/TNW 3:1 for all borrowers with exception to the following sectors5:1 for infrastructure project9:1 for contractors (including guarantees-NFB) otherwise 3:1

4 DSCR 1.5 to 2- average; any year shall not be lower than 1.25 during the repayment period

5 Interest coverage ratio

1.5 times

6 Security Coverage Ratio

i. 1.25 times of advance value for WC limitsii. 1.20 for term loans

7 FACR 1.20

*Debt Equity ratio- normally promoter’s contribution should be brought front end. However, in big projects involving a construction period of more than a year or where a part of such funds are expected to be funded through internal generation or proposed public/ private offering of equity, bringing the promoters’ contribution up-front may not be feasible. In such circumstances it should be ensured that at the minimum ‘the pro rata level’ of promoters’ contribution is infused before releasing the loan.

4.1.3 Exposure to Defaulters/ Willful defaulters:

While evaluating the proposal for credit, it has to be kept in view whether the names of the borrower entity/ guarantors/ directors/ partners/ trustees of the borrowing entity are listed in

19

the caution list/ defaulter’s list circulated by RBI/ CIBIL/ECGC. As per RBI directives, no additional facilities shall be granted to the willful defaulters whose names appear in the RBI willful defaulters’’ list.

4.1.4 Preparation of IDO Report:

Techno economic viability forms an integral part of credit appraisal for manufacturing companies and other projects. All the credit proposals for the manufacturing sector for limits of more than Rs. 1 Crore shall be accompanied by Industrial Development Officer’s (IDO) report on the Technical viability of the proposal.

4.2 Monitoring of implementation of project:

In project financing, one of the major risks is the implementation risk which leads to revision in estimation of outlays, time limits and consequent deterioration in credit quality.

The implementation period is arrived at, taking into account, the various implementation risks perceived. As per the RBI guidelines, the asset is downgraded in case the commercial operation date (COD) extends beyond a period of six months from the original date of COD as documented at the time of financial closure.

Monitoring of the project acquires importance to ensure proper/ timely implementation of the project. Hence, progress report on implementation of the project duly counter signed by the lender’s Engineer/ Chartered Accountant shall be obtained and forwarded to the sanctioning authority on quarterly basis. An example of Project Implementation Progress Report is given as per Annexure 1.

Generally, the borrowers require credit facilities either for meeting their working capital purposes or for purchase of fixed assets, construction of factory buildings or office buildings etc.

4.3 Credit facilities for Working Capital:

A borrower may require finance for pre-sale transactions i.e. for the purpose of production. During the process of production he may have to hold raw materials, work-in process and finished goods at different levels. The actual holding of such inventory depends on factors like

20

nature of industry, size of the unit, volume of production and sales, availability of raw material, capacity utilization, etc. Banks are extending OCC/KCC/LC limits for financing against stocks and inventories. The borrower may require finance for meeting post-sales transactions i.e. credit sales through bills. Banks extend credit facilities for post-sales transactions by way of Bill Finance (Bill purchase and discount limits, Bills Negotiated under LC).

4.3.1 Application for Credit facility: The pre-sanction includes obtention of application form from the prospective borrower, analysis of the financial statements, projections, etc., compilation of a Credit Report and determination of the eligible quantum of advance, type of advance, securities to be obtained etc. At the time of receiving the credit proposal, branches should obtain a declaration from the borrowers about their relatives, if any, employed in the Bank or in any other bank / financial institution. Besides, facilities availed in other banks/branches should also be furnished by them separately. The details of legal heirs of the borrower/guarantor (Name, Age, Relationship, Address etc.,) should be obtained in the loan application. These details should be obtained for the borrower and guarantor separately. The information should be updated on an ongoing basis, even after filing suit against the borrower. A separate Credit Proposal Received Register is maintained in the branch to record information relating to all applications received for sanction of advances.

4.3.2-Analysis of collected information: a critical and careful analysis of the information collected from the applicant and from other sources is undertaken in this project. After analyzing the data, the Credit report/s of the borrower / guarantors is prepared and the applicant's request is presented in the form of a credit proposal to the sanctioning authority. If the applicant is already a customer of the bank (which is the case in this project) a scrutiny of the operations in the account will reveal the trends, connections, nature of business dealings etc. As far as possible, before sanctioning a credit facility, the borrower's place of business should be visited.

4.3.3-Preparation of Credit reports: Credit Report is the basic document on the basis of which assessment of the borrower's character, capital and capacity (normally referred to as three C's) is made by a banker. In preparing credit reports, the branch should be careful about the following:

i. Inclusion of assets not standing in the applicant's nameii. Inclusion of other's share of propertyiii. Suppression of encumbrances on the propertyiv. Overvaluation of assetsv. Suppression of liabilities.

21

Credit reports are compiled only after individual verification by a Chartered accountant of the information relating to the assets and liabilities furnished by them.

4.3.4-Calculation of Tangible Net Worth in Credit Reports:

The tangible net worth shall be arrived at as under:

i. For individuals/ Proprietorship concerns

Add a. Movable assets such as Bank deposits, gold ornaments/ jewellery, etc. b. Personal immovable properties (self acquired properties of an individual and also any share in the ancestral properties acquired on the division of the Joint Hindu Family) Less Loans taken against any of the above assets in individual name or offered as third party security

ii. For partnership / Joint Hindu Family firms Add a. Capital invested in the business b. Undivided profits/ deduct accumulated losses, if any c. Total worth of individual partners

iii Limited companies Add Paid up capital and Free Reserves Less Accumulated balance of loss, balance of deferred revenue expenditure and also intangible assets in all the above cases.

The renewal proposal should invariably be accompanied by the Credit Report. Reasons for increase or decrease in net worth should be indicated in the report. Reduction in net worth due to disposal of fixed assets or incurring of loss is a danger signal. If there is any increase in fixed

22

assets, source of acquiring them should be ascertained or it should be verified whether it is due to any revaluation of the assets.

When the borrower's/ guarantor's declared Net worth exceeds Rs.50 lakhs, the following documents should be obtained

i. Certificate from a Chartered Accountantii. Photocopy of the title deeds in case of immovable propertiesiii. A declaration that any disposal of properties will be intimated to the Bankiv. A declaration that additional liability assumed will be intimated to the Bank

In the event of the prospective borrower enjoying credit facilities with other banks, confidential report should be obtained from such banks and a certified true copy of the same should be sent to the appropriate sanctioning authority along with the proposal

4.3.5-Assessment of quantum of credit required: The next process involved in the pre-sanction stage is assessment of the credit requirements of the applicant. While carrying out this process, branches have to keep in view the purpose, the period for which the advance is required, type of facility, security offered, additional benefits that may accrue to the Bank etc. The assessment of Working Capital shall be made, taking into account reasonable projected level of activity, so as to avoid frequent sanction of adhoc limits and excess drawings. There are three main aspects that are to be considered here:

i. Assessment of the level of current assets required to be held for a given level of production,

ii. Determination of credit other than bank finance available to the borroweriii.Calculation of bank finance required

The following methods are adopted for assessment purposes:

A. Turnover method

B. Short Term Bank Credit(STBC) method

A. Turnover Method: the limit will be arrived at on the following basis-

i. 20% of the projected annual turnover

23

ii. The actual working capital needs as assessed by STBC method, whichever is higher

iii. The Bank Finance is intended only to support the need based requirements of the borrower. In order to ascertain the extent of assistance, the marginal contribution by way of Net long surplus viz., Networking Capital (NWC) should be reckoned. If it is more than 5% of the turnover, the limit (being 20% of the turnover) shall accordingly be reduced. For instance, if NWC is 8% (3% in excess of the prescribed 5%), then the limit will be computed as 17% (20% minus 3%) of the turnover. Thus, the aggregate of the limits plus NWC shall not exceed 25% of the turnover.

iv. While applying the above simple formula of 20%, it has to be ensured that the borrower’s financial health is satisfactory as revealed by the following:

1. Borrower’s operations result in net profit every year.2. Borrower’s Current Ratio as per the latest Audited Balance Sheet is not less than 1.20. (Current Assets around 33.33% of sales and Net Working Capital around 5 to 6 % of sales).3. Borrower’s Total Outside Liabilities (TOL) do not exceed 3 times of the equity (equity would include quasi-equity represented by subordinate debt, owed to owners of the business).

B. Short Term Bank Credit (STBC) Method: The Short Term Bank Credit Methodology of working capital assessment should be made applicable to all industrial advances in excess of Rs. 2 Crores. The computation of working capital under this method is primarily concerned about the level of Current Assets and the Net Working Capital.

i. Level of Current Assets: The level of Current Assets is expressed as a percentage of Gross Sales projected. However, it is necessary to ensure that no individual item of Current Assets is held for unduly longer periods. Banker has to use his judgment and experience in appraising inventory. There should not be any excessive inventory with speculative interest to make profits. If excessive raw material is due to poor working capital management and inefficient distribution channel, Bank should not encourage this.

24

ii. Net working capital: The minimum level of Net working Capital (NWC) will be the highest of the following:

25% of the assessed level of current assets less Annual maturing term liabilities

16.66% of assessed level of current assets Actual projection as per Balance Sheet

An example of Assessment of bank credit through STBC method for a borrower having limits of 1 Crore and above is shown in the Practical Case Study Section.

4.3.6-Compilation of Credit Proposal: a fresh/renewal proposal should contain the following essential particulars:

i. Name, address of the borrower/guarantor along with Asset Classification assigned to the borrower.

ii. Net Worth of the borrower/guarantor along with the Assets and liabilities statements and credit reports.

iii. Quantum of credit requirements of the borroweriv. Margin proposed, sources from which the borrower would bring in such

margins.v. Nature and value of security offered, its title, the mode of charging such

securityvi. The renewal proposals should also carry the particulars such as

a. Date of inspectionb. Name and designation of the officer who inspected the godown/unit c. Brief remarks with observation made during the inspection by the branch regarding value of stocks and other securities including adverse features, if any.

vii. While assessing the credit requirements of a party, the party's financial requirements for the next 12 months should be taken into consideration. This will avoid referring to the sanctioning authority very often for additional/adhoc facilities. However, for reasons unexpected, if temporary increase in limits or additional facilities are required and recommended, the reason for such increase or additional facility and the period for which they are required must be clearly stated.

25

For appraising a credit proposal, lot of information are supposed to be meticulously checked to ensure safety of the funds. The ways through which the banker would get these necessary informations are as follows:

i. Application for advance: the application tendered by the prospective borrower is a primary source of information available to the banker.

ii. Market reports through friends or competitors of similar trade or business: All such reports sometimes though contradictory to each other have to be weighed independently and a balanced opinion has to be formed about the 'three Cs' of the borrower.

iii. Mode of living: While preparing a credit report, the applicant's mode/style/status of living has to be ascertained to assess whether he is normal/moderate/lavish in his lifestyle.

iv. Borrower's bank accounts: the bank accounts of the borrower lying with other banks are studied side by side. Income-tax assessment order/returns are studied to ascertain the various sources of income and the investments declared.

v. Analysis of Assets and Liabilities statements.

4.3.7-Analysis of Assets and Liabilities Statement: these are very crucial sources of informations as it gives a clear picture about the net worth of the borrower. The Assets and Liabilities Statements should be obtained separately for each applicant and guarantor. They should bear the latest date as far as possible and should be obtained within a reasonable time, say, not more than 3 months from the date of such statements. The statement shall contain complete details regarding the assets and liabilities of the borrowers and guarantors. It must be accurate by collecting documentary evidences regarding all movable and immovable assets of the firm/person to whom the statement is related to. Similarly, all liabilities must also be recorded to arrive at the actual worth. If the property of a guarantor has already been offered as a security to the assessing Bank or other Bank/Financial Institution, the value of the same has to be excluded while arriving at the net worth of that guarantor. It is necessary to obtain contingent liabilities of a borrower/guarantor along with the Assets and Liabilities

26

Statement. Even though the contingent liabilities need not be taken into account for the purpose of arriving at the net worth, a footnote should be given in the Credit Report.

For Sole Proprietorship Concerns, the assets and liabilities of the firm and that of the proprietor should be merged to have a clear picture of the net worth. Alternatively, in the personal assets and liabilities statement, the capital employed in the sole proprietorship concern should be shown as Investment in Business.

For Partnership Firms, for compiling the individual net worth of the partners, Assets and Liabilities statements from individual partners showing all their private assets and liabilities should be obtained and credit report prepared. The capital employed by a partner in the firm should be ignored in the individual credit reports of the partners, as these investments form part of the firm’s Net Worth.

In case of Limited companies, their audited Balance Sheets and Profit & Loss accounts for three years should be obtained and an analysis and interpretation of the financial statements shall be done.

List of documents to be verified and valued while analyzing A & L statement:

i. In case of immovable properties(land and building)

Verification of charges in the register of charges maintained by the company

Registration of charges with Registrar of Companies in case of Limited companies

Search report on the searches made in the office of the Registrar of Assurances

Municipal tax receipt, ground rent receipt Wealth tax assessment order Sale deed and other title deeds, patta, etc Non encumbrance certificate.

ii. In case of machinery:

Original sale invoices of plant and machinery should be verified.iii. In case of Cash and Bank Balances:

27

Pass Book or Statement of account Balance sheet

iv. Realizable Book Debts: Making enquiries as to the long pending Search at the office of the Registrar of Companies (in case of limited

companies) Test check of prospective borrower's account books Bazaar reports

An example of A & L statement is given in the Practical Case Study section for the partners of a partnership firm with limits of Rs. 1 Crore and above.

4.4 SANCTION AND DISBURSEMENT OF CREDIT:

It is necessary that the terms and conditions contemplated are discussed with the borrower beforehand to judge the feasibility of including them in the sanction ticket. After such discussion and firming up, these terms and conditions should be mentioned in the final recommendations made to the sanctioning authority along with the reasons for instituting them.

Special conditions applicable to the respective loan/product depending on various factors like the type of facility, type of security, period of repayment, method of charging interest, percentage of margin, etc., could also be specified in the sanctions in addition to these general terms and conditions.

The sanction should be informed to the borrower in writing mentioning therein the terms and conditions to be complied with. The sanction communication should clearly divide the terms and conditions into Pre-disbursement conditions and Post-disbursement conditions. The advance will be released only upon completion of documentation in all respects as per Bank's rules. Processing fee and other charges like equitable Mortgage charges are collected before disbursement of credit. All fund based/non-fund based /fee based transactions shall be routed only through the account with the Bank. For working capital facilities against stock etc, monthly stock statement with break up of stocks as required by the Bank is to be submitted.

28

4.4.1 Documentation:

Documentation is done before disbursement of credit. This step is a must because the bank may not be able to enforce its rights in a court of law for recovery of the money due unless the documents executed by the borrowers and guarantors are complete in all respects and are in order (and kept alive). The documents are useful in:

i. Identification of the borrower,ii. Identification of the security,iii.Creation of a charge on the security,iv.Settlement of the terms and conditions of a contract/arrangement,v. Proving the transaction (like interest to be paid and repayment terms),vi. Prevention of fresh charge on the security,vii. Deciding the period of limitation,viii. Settlement of the rights and remedies of the lending banker against

the borrower andix. Filing suits and enforcing the claim.

The documents should be current and legally enforceable. It should have the description of securities, the amount of loan/facility, interest and overdue interest, the date of execution, should give terms of repayment, major and important terms and conditions mutually agreed upon, the place of execution etc.

The sanction is scrutinized, documents appropriate to the advance with reference to the terms and conditions are listed out, procured, the blanks are filled in correctly without overwriting, cutting, erasing, etc. Advances should not be released except when all the relevant documents are obtained from the parties concerned duly executed by them. The documents should be duly filled in and properly stamped before obtaining the signature of the borrowers.

4.4.1.1 Formats of documents: The Bank has printed standard forms of documents to be executed for various products/services normally handled by the branches. These forms have been drafted by the Bank's Legal Advisers in the (technical) language commonly adopted and judiciously interpreted by the Courts with preamble and consideration clauses, obligations, privileges and reservations and thus provide necessary legal safeguards to protect the Bank's interests.

In this context, a live case of documentation is given in Annexure 2 for a trading company.

29

4.4.2 Pre-release Audit:

On being satisfied that complete documentation / security creation/ compliance of terms and conditions are completed, pre-release audit is to be conducted for applicable advances.

Pre release Audit is stipulated in respect of advances with limits of Rs.10 lakhs and above in order to bring in discipline with regard to compliance of terms and conditions of credit sanctions, zero error documentation and conduct of accounts.

Pre-release Audit shall cover only pre-disbursement conditions and completeness in documentation.

A live case showing the Pre Release Audit report is given in Annexure 3.

4.5 POST SANCTION MONITORING OF ADVANCES:

While a qualitative credit appraisal indicates the viability and bankability of a credit proposal, post sanction measures such as timely disbursement, proper documentation, monitoring and follow-up play a crucial role in ensuring that the account continues to be a performing asset.

This plays the most crucial role as it ensures that the account continues to be a performing asset and the project continues to run in terms of the projections made. Monitoring also includes anticipation of problems in advance and taking suitable corrective measure in consultation with the borrower.

No industry becomes sick overnight and a careful watch over the working of the unit would help in tracking and averting sickness in the incipient stage itself. Close monitoring is of paramount importance particularly in the light of the fact that once a unit slips into sickness, it becomes difficult for the Bank to recover its advance in full or even part of it, at times.

The post sanction appraisal depends largely on the pre sanction appraisal. The requirements of post sanction follow up are:

4.5.1 Security Monitoring:

30

Banks borrowings must be adequately secured by core current assets. To ensure this, margins are prescribed on each of core current assets. Irregularity in the cash credit account arises when bank borrowings exceed the Drawing Power and the security position is adversely affected. If assets, existing or to be created out of bank borrowings, are taken as security, following things should be ensured:

The security conforms to the terms of sanction, is adequate, in good condition and readily enforceable.

All the legal formalities have been complied with and a valid charge on the security in the bank’s favor has been created.

While arriving at drawing limits on stocks/book debts, sundry creditors for goods (including those under supplier’s credit, co-acceptance liability under DA/LC) should be deducted from the values of such stocks/book debts.

A Practical example of calculation of adequacy of drawing power is given in Annexure 7.

4.5.2 Collection and analysis of data:

Various statements and returns need to be studied carefully for proper monitoring of the borrowal accounts. These are:

i. Monthly stock statement and monthly data on production and sales (Monthly Select operational data/MSODs),

ii. Inspection of stocks,

iii. CMO monthly report,

iv. Operations in the account,

v. Quarterly information system (QIS) statements,

vi. Annual audited accounts,

vii. Review/renewal of advance,

viii. Asset classification under IRAC and other norms,

ix. Credit rating under RAM model, 31

x. stock audit and concurrent auditor’s report

xi. Unit inspection report.

4.5.3 Stock statements:

Borrowers should submit a stock statement showing the quantity and value of stocks hypothecated to the bank. The stock statement should clearly show the value of unpaid stock, stocks under DA/LC etc.

Regular submission of stock statements from the OCC borrowers should be ensured. The stock statement received should be properly made use of by entering the advance value, insurance in force, verification of declaration in the statement, entering the relevant details in the appropriate registers, cross verification of particulars with borrower's books and physical verification of stocks during inspection etc.

Stocks - quantity and value should be reconciled from month to month showing opening stock, receipts, issues and closing stock. Wherever book debts are financed, the book debts upto the tenor accepted in the CMA only should be recognized. In case no specific tenor is fixed by the sanctioning authority, only book debts up to 180 days are to be taken cognizance for arrival of Drawing Power.

A review of stock statements (at least once in 6 months) shall reveal the degree of movement of inventory, raw material, finished goods, etc., and indicate the non-moving items and the degree of obsolescence of inventory. For this purpose, borrower should give break up of large value items under raw materials, stock in progress and finished goods. Such observations shall be confined only to high value items constituting substantial monetary value of inventory. (Stock-in-process, for instance, would remain the same if production is more or uniform every month).

4.5.4 Inspection of stocks:

32

4.5.4.1 Stock inspection is usually done on a monthly basis with an element of surprise maintained at the time of inspection. Such inspections are besides Stock Audit exercise for fund based and non-fund based working Capital limit of Rs.1 Crore and above.

4.5.4.2 Where there are large volumes of stocks, thorough stock inspection should be taken up on a small portion in quantity but significant in value. 4.5.4.3 All the establishments of the borrower in the same city like factory, go-down and office should be inspected on each inspection.

4.5.4.4 Stocks shown in the stock statement shall be cross verified with those in the books of accounts and the records maintained for the purpose of excise and other statutory authorities.

4.5.4.5 Valuation rates adopted for stocks with market rates/cost shall be verified to ascertain whether the company follows the same basis of valuation as disclosed in the audited Balance Sheet.

4.5.4.6 The supplementary data on consumption, production, sales etc., shall also be verified with the books of accounts of the borrower.

4.5.4.7 Insurance on stocks shall be examined for its adequacy and coverage and to ensure that all the policies are in force.

4.5.5-Other factors of relevance at the time of inspection

4.5.5.1 General working and tempo of activity

4.5.5.2 Power supply, alternate of power supply if any. Utilization of power shall be verified from meter reading. If through alternate supply the fuel consumption etc., shall be cross checked.

4.5.5.3 No. of shifts worked and labor statements

4.5.5.4 Purchase/sales returns, quality control, scrap/wastage management

4.5.5.5 Maintenance of Account Books and Records

33

4.5.5.6 Slow-moving/old stocks and book debts

4.5.5.7 Statutory liability/pressing creditors

4.5.5.8 Difficulties, if any, experienced in carrying out inspections.

4.5.5.9 Wherever shortfall in stocks/book debts is noticed, the matter should be reported to controlling office. While the borrower would be asked to regularize the accounts, the financial position of the company has to be examined in detail.

4.5.5.10 For Book Debts, books of accounts and records of the borrower must be verified and it should be ensured that periodical confirmation from debtors has been obtained by the company.

4.5.5.11 Internal Reports of the company as to age and quality of book debts, sales returns of finished goods may also be scrutinized.

4.5.5.12 Consignment stocks in and out to be supported by proper records.

4.5.5.13 Wherever any additional construction/other capital expenditure is noticed/incurred during unit inspection, it should be cross checked for source of funds to finance such activities.

4.5.6-Scope of periodical inspection:

Over a period of time, the system of physical verification/ inspection of stocks within the unit are not given the importance it deserves. It does not merely involve assessing the quality, quantity and valuation of stocks but also involves,

1. A look at the tempo of activity

2. A look at the books held at the unit, other relevant records including copies of returns/ statements submitted by them to the bank and to the statutory authorities.

3. Meeting and holding discussions with the borrower and key personnel and also the auditors of the unit.

34

4. Inspection officials satisfying themselves that the borrower is agile and committed to his responsibilities.

5. Supplementing and constantly updating bank’s knowledge about the operations of the borrower in particular and the industry in general.

4.5.7-Benefits:

1. It helps in ascertaining the extent to which the operations of the unit are conforming to the various norms/ assumptions, on the basis of which the advance is sanctioned.

2. It reveals several aspects which the financial data generally do not reveal.

An example of a Stock inspection for a trading company is shown in Annexure 4.

4.5.8 Stock Audit:

Stock Audit is an effective credit-monitoring tool, which offers an opportunity for making a qualitative assessment of the advances. The scope of stock audit is to go in for a detailed study on the adequate availability of primary security, its nature and quantity.

Stock Audit is a supplement to the system of inspection. It helps in identifying irregularities, thereby prompting for initiation of suitable and timely remedial measure which is crucial in improving the quality of loan assets of the Bank

The stock audit shall be carried out by an agency appointed by the Bank, the charges of which are to be borne by the borrower. Stock Audit has to be conducted once in a year for accounts with fund based and non-fund based working capital limit of Rs.1.00 crore and above.

For accounts identified by the Monitoring Committee for slippage/showing signs of slippage and for accounts specifically directed by the Sanctioning Authority, Stock Audit has to be conducted at Quarterly / Half yearly intervals as directed.

Coverage of stock audit: Stock audit should cover Book Debts, Pledge stocks, fixed assets (charged to Bank either as primary or as collateral security) and goods covered under LCs.

35

The stock audit report should cover the following:

i. Physical verification of the quantity of stock declared in the stock statement by visiting the places of storage;

ii. Reconciliation with the stock statement lodged with the bank;iii. Correctness of valuation of stock by scrutinizing invoices, valuation of raw material, stock-in-

process, finished goods, age, quality etc.;iv. Valuation of obsolete / slow moving stock;v. Recovery of obsolete / non-moving stock;vi. Major customers of the borrower;vii.System for maintenance of stock and stock records, movement of stock from stores, policy

of procurement, management of stocks;viii.Age-wise break-up of receivables and their realizability in normal course;

An example of the analysis of Stock and Book Debt audit is given in Annexure 5.

4.5.9 Periodical inspection of units and verification of securities:

Periodical inspection of goods secured under KCC/OCC should be done. Periodical inspection and verification may also be undertaken of machineries and immovable properties taken as security for term loans. It is to be noted that the purpose of inspection is not only to ensure the availability of sufficient security cover for the advance but also to have a first hand knowledge about the borrower's current business position, his problems, bottle necks faced etc. so that necessary corrective measures can be taken immediately.

Inspection of the units financed / securities charged on a regular basis constitutes a vital tool in effective credit administration. Besides, the signals forewarning the onset of any problems could also be detected during such inspection.

The inspection of units should be done on a monthly basis unless or otherwise the periodicity of the same is specified quarterly / half-yearly etc., in the sanction.

The order of priority for inspecting the Units is as follows:

i. Accounts which do not show healthy signs of operation and wherein the submission of stock statements and other financial data is irregular

36

ii. Accounts with healthy operationsiii.Consortium advances

4.6 Monitoring the operations in the account:

The operations in the cash credit accounts should be verified to check the health of the account, that is, if there are healthy fluctuations in the account depending on the sales etc. It should also be checked if there are any drawings for the purposes other than that for which the advance has been taken.

Following aspects should be meticulously checked in terms of an account

1. Unusual debit/ credit entry

2. Return of Bills Receivables/ Cheques unpaid

3. Repeated requests for additional funds which may indicate decline in sales, low realization of debtors or payment to pressing creditors, diversion of funds, cash loss etc.

4. Decline in level of operations in the account.

5. Large return of inward bills

6. Default in payment of Term Loan installments/interest

7. Devolvement of LCs, invocation of guarantees or excessive extension.8. Notice of demand from PF/Tax assessment, law suits or other legal action against the

borrowers.

4.6.1 Quarterly Information system (QIS):

For borrowal accounts having aggregate working capital limit of Rs.1 Crore and above, statements under Quarterly Information System (QIS) should be obtained as per time schedule prescribed and scrutinized. QIS can be used as a tool for checking the purpose of the drawals. The projections made in the QIS will enable the banker to know whether the drawal is to meet the working capital requirements or not.

37

QIS- I

Compare the information with projections for the whole year. Any variation over 10% should be scrutinized.

QIS- II

1. Production and Sales shall be compared with earlier projections; so also current assets and current liabilities. Any variation over 10% on either side should be enquired to initiate corrective steps.

2. Variation in NWC compared with the actuals of previous quarters shall be analyzed for possible diversion.

3. Actual sale and inventories of two quarters shall be compared with figures given in half-yearly statement. Cumulative sales for four quarters shall be compared with the audited accounts of the corresponding year.

QIS III

1. Sales, cost of goods sold and other expenses and operating profit shall be studied to understand the trend. Any negative trend should be noted down.

2. Variation over 10% between estimates and actuals shall be studied and analyzed.3. Relationship between insured value of stock/security and value declared shall be

studied. Any inadequacy has to be corrected.

A practical example of QIS-I and QIS-II for a trading company is given in Annexure 6.

4.6.2 Funds flow statement:

1. Variation in excess of 10% between estimates and actuals shall be analyzed to know how deficit was covered or excess was utilized.

2. Increase in bank borrowing without corresponding increase in inventory and receivables shall indicate that such borrowings were used for other purposes. Borrower should be advised to take steps to repay the amount so diverted.

38

4.6.3 Review/Renewal of advances:

4.6.3.1-Scope:

Review/renewal of advances is an important post sanction exercise. Review helps to identify the state of health of an advance and is an opportunity to evaluate the performance of borrowers and to adopt remedial measures to safeguard our Bank's interest.

Review/ renewal is also one of the many parameters on which the RBI evaluates a bank’s performance. So, all the borrowal accounts are subject to periodical review or renewal.

Review/renewal of advances involves collection and analysis of individual account data likei. Account behaviorii. Financial performanceiii. Market reports of the borrowersiv. Production performancev. Overall change in credit rating

The review exercise pays more attention to future performance of the company, apart from detailing account operations, profitability and security. The review covers the market risks and management risks (for example, there may be change in the management or in the quality of management).

The financial performance analysis has to give importance to the underlying reasons for the variance in actual performance vis-a-vis projections and management action required to correct the situation.

Proposals for increased working capital assistance shall be based on increase in sales projection. Any increase in demand for Working Capital without considerable improvement in sales calls for deeper study of the circumstances. Such a trend shall indicate that the company is using current surplus towards liquidation of term loan dues or acquisition of capital asset.

This process gives the banker an opportunity to evaluate the borrower's operational performance both quantitatively and qualitatively, to reassess his credit requirements, to check up afresh the continuity or otherwise of his financial solvency, to review the rating of his credit worthiness etc. These aspects help him decide his recommendations as to whether the limits should be renewed or reduced or cancelled.

39

While considering the application of renewal/enhancement/ additional/ fresh limits, it should be checked as to whether the names of the proprietor/partners/Directors find a place in the list of defaulters under various categories like RBI, CIBIL etc. All renewal proposals should be accompanied by a Credit report of the borrower as a review form.

Irregular features that have been detected during the course of operational/security/financial follow up, should be specifically mentioned in review proposal.

While submitting the review proposal, any steep fall in the security value, fall in Net Worth of the borrower/guarantor, fall in production/sales etc should be brought into notice.

Renewal proposals should also contain following additional particulars: Interest income derived Commission earned from non-fund based facilities Share of export business passed on to the bank Other financial benefits accrued/accruing to the Bank.

4.6.3.2-Study of Balance Sheets and other financial statements:

The balance sheet and other financial documents submitted by the borrower are extra sources of informations to the bank. These documents should be properly studied and commented upon on the liquidity, solvency, profitability and turnover of assets. Symptoms such as over-trading, decline in profits, decline in sales (in terms of quantity and/or price) decline in net worth/negative net worth, deterioration of current ratio, decline in gross profit and/or operating profit margin, mounting external debt, poor inventory turnover, diversion of funds outside the business, diversion of short term funds for long term uses etc. should be checked.

4.7 Identification of willful defaulters’ accounts:

Banks and FIs will report all cases of willful defaults which occurred or detected after 31st March, 1999 on a quarterly basis - (then and there without any delay) to RBI. A willful default would be deemed to have occurred, if any of the following events is noticed

The unit has defaulted in meeting its payment / repayment obligations to the lender even when it has the capacity to honor the said obligations.

40

The unit has defaulted in meeting its payment / repayment obligations to the lender and has not utilized the finance from the lender for the specific purposes for which the finance was availed of but has diverted the funds for other purposes.

The unit has defaulted in meeting its payment / repayment obligations to the lender and has siphoned off the funds so that the funds have not been utilized for the specific purpose for which the finance was availed of nor are the funds available with the unit in the form of other assets.

For accomplishing this, the willful defaulters’ list in the website www.cibil.com should be checked to identify names of the borrowers, directors, promoters or proprietors. In case, a similar name happens to occur in the list, the concerned party should be asked to give justification.

41

Section Five: CREDIT RISK ASSESSMENT

In today’s deregulated financial regime, risk perception in respect of a borrowing unit is considerably influenced by internal as well as external factors. If these factors are not favorable, a performing unit may suffer with adverse risk situations. Each Bank has to develop its own Internal Rating System to rate its Borrowers. All exposures have to be brought under Credit Rating Framework (CRF). For the purpose of internal rating, the Bank has developed the Risk Assessment Model (RAM).

A credit rating estimates the credit worthiness of an individual, corporation or even a country. It is an evaluation made by credit bureaus of a borrower’s overall credit history. Credit ratings are calculated from financial history and current asset and liabilities. Typically, a credit rating tells a lender or investor the probability of the subject being able to pay back a loan. However, in recent years, credit ratings have also been used to adjust insurance premiums, determine employment eligibility and establish the amount of a utility or leasing deposit.

A poor credit rating indicates a high risk of defaulting on a loan and leads to high interest rate, or the refusal of a loan by the creditor.

An individual’s credit score, along with his or her credit report, affects his or her ability to borrow money through financial institutions such as banks.

The factors which may influence a person’s credit rating are:

i. Ability to pay a loan

ii. Interest

iii. Amount of credit used

iv. Saving pattern

v. Spending patterns

vi. Debt

Thus, credit rating enables the investors to draw up the credit-risk profile and assess the adequacy or otherwise of the risk premium offered by the market. It saves the investor’s time and enables him to take quick decision and provides him better choices among available investment opportunities. Issues have a wider access to capital along with better pricing. Issuers

42

with a high credit rating can raise funds at a cheaper rate thereby lowering their cost of capital. It acts a s a marketing tool for the instrument, enhances the company’s reputation and recognition and enables even lesser known companies to raise funds from the capital market.

This way, credit rating is a tool in the hands of financial intermediaries, such as banks and financial institutions that can be effectively employed for taking decision relating to lending and investments.

5.1 Categorization of Risk and Its Evaluation:

In the Credit Risk Assessment System, all possible factors that go into appraising the risk associated with a loan proposal have been taken into account. These factors have been broadly classified as under-

1. Financial Risk

2. Industrial Risk

3. Management Risk

4. Country Risk

In order to arrive at the overall risk rating, the factors duly weighted are aggregated and calibrated to arrive at a single point indicator of the risk associated with the credit decision

1. Financial Risk:

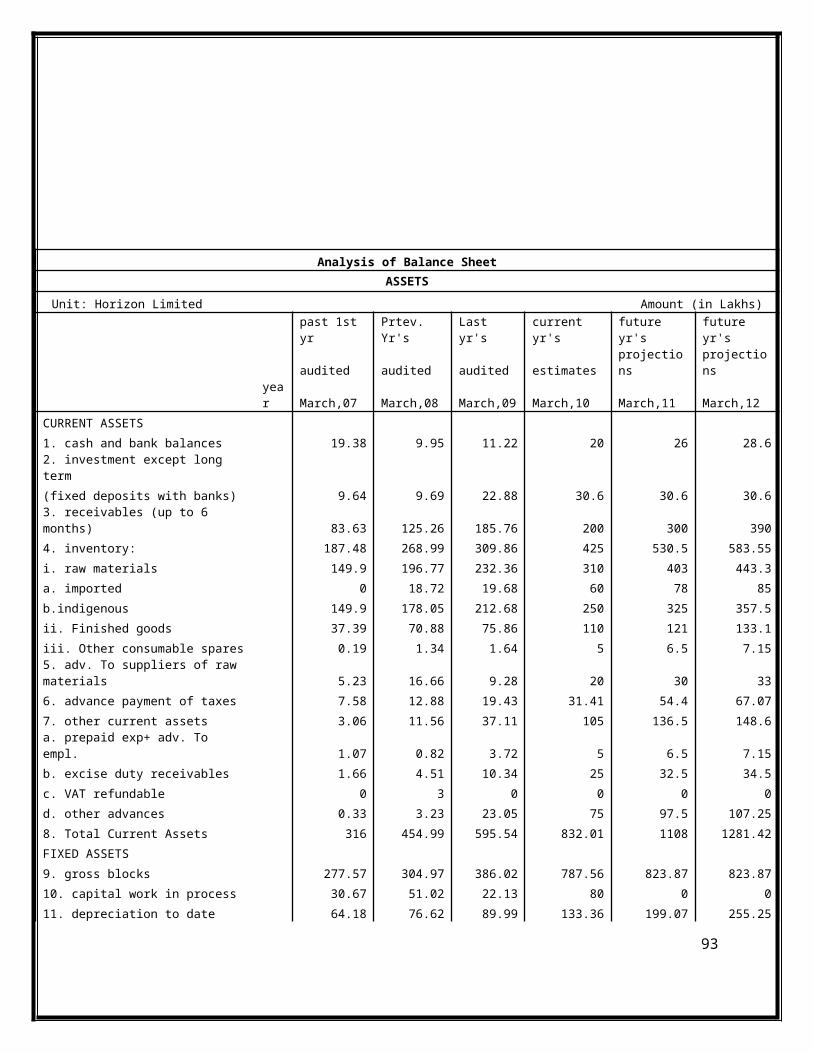

The financial risk of the project is ascertained on the basis of the financial data and related documents provided by the client. The credit analyst generally redraws the financial statements of the client incorporating the changes which he deems fit. The financial risk aspect of a credit proposal is indicated by the following parameters:

i. Latest financials of the unit (financial ratios)- there are a few selected number of ratios (actual for the existing companies and projected for the new companies) considered by Bank which throw light on the operational and financial risk aspect of the borrowing company. These ratios are also referred as ‘Quantitative (Static)’ parameters of the company. Six ratios have been considered for the purpose of risk assessment in Working Capital credit proposals and five ratios in case of Term Loan assessment proposals.

43

Ratios considered for financial risk assessment:

Working Capital Term Loans

1. Current ratio Project debt/ equity

2. TOL/TNW TOL/ TNW

3. PBDIT/ Interest Gross average DSCR of the Project

4. PAT/ Net Sales (%) Gross average DSCR for all loans

5. ROCE or ROA (%) Terms of payment (Years)

6. (Inventory+ receivables)/ Net Sales (In Days)