Flexible - Elegant - Convenient & Self-Managed Study CENTRE OF ISLAMIC BANKING & ECONOMICS Simply the best Automated Learning Solution ISLAMIC BANKING AND FINANCIAL PRODUCTS IB&F: 404: PARTNERSHIP BASED MODES OF ISLAMIC BANKING AND FINANCE POST GRADUATE DIPLOMA IN ISLAMIC BANKING & FINANCE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.alhudacibe.com/dlp

Flexible - Elegant - Convenient & Self-Managed Study

CENTRE OF ISLAMICBANKING & ECONOMICS

Simply the best Automated Learning Solution

ISLAMIC BANKING AND FINANCIAL PRODUCTS

IB&F: 404: PARTNERSHIP BASED MODES OF ISLAMIC BANKING AND FINANCE

POST GRADUATE DIPLOMA IN ISLAMIC BANKING & FINANCE

AlHuda CIBE

“The creation of liquidity instruments is not simply an aid to banks being able to manage their own liquidity but also an enormous aid to the development of the whole market itself because it will improve significantly our ability to rationally price credit.”

Brandon Davies, Board Director, Gatehouse Bank

IB&F: 404

PARTNERSHIP BASED MODESOF ISLAMIC BANKING AND FINANCE

C O N T E N T S

· Musharaka

· Mudarabah

· Diminishing Musharaka

www.alhudacibe.com/dlp

01

09

14

· Discussion Questions

· Summary

· Supplement Material

26

27

27

PARTICIPATORY MODES OF FINANCING

In this course, we will discuss the partnership modes of finance which involve generating the real economic activity and/or liability. The most preferable category of modes belonging to participatory or profit/loss-sharing (PLS) techniques is described as hereunder.

MUSHARKAH (SHIRKAH)

In the early books of Fiqh, the partnership business has been discussed mainly under the caption of Shirkah. Musharaka is a term used by contemporary scholars both for broad and limited connotations. Technically, Musharaka means a relationship established under a contract by the mutual consent of the parties for sharing of profits and losses arising from a joint enterprise or venture. Broadly, it is referred to as a traditional Shirkah contract while in specific sense, a combination of Shirkah and Mudarabah is sometime termed as Musharaka wherein a Mudarib, in addition to the capital provided by the Rabbul Mal, employs his own capital as well. This arrangement is also permissible according to the jurists.

There are mainly two kinds of Shirkah:

n Shirkat-ul-Milkn Shirkat-ul-Aqd

Shirkat-ul-Milk

Shirkat-ul-Milk is the mixing of ownership mandatory or by choice; basically, it is not for sharing of profit. The distribution of the revenue of Shirkat-ul-milk is always subject to the proportion of ownership; Co-owners are not agents of each other; Co-owner can sell his shares

01

Glossary:

Fiqh: Islamic substantive law. It is the science of the Shari'ah. It is an important source of Islamic economics.

Shares: A joint stock company divides its capital into units of equal denomination. Each unit is called a share. These units are offered for sale to raise capital.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

without other co-owner's consent and can guarantee the shares of other co-owner.

Shirkat-ul-Aqd

Shirkat-ul-Aqd is created through a contract with the basic purpose of Seeking profit; Partners are agents of each other; A partner cannot sell his share without other partners' consent; Partners cannot guarantee shares, or any profit, of other partners.

02

Keep In Mind

The difference between Shirkat-ul-Milk and Shirkat-ul-Aqd is that Shirkat-ul-

Milk is not for sharing profit whereas Shirkat-ul-Aqd is for seeking profit. In

Shirkat-ul-Milk, co -owner can sell his shares without other co-owner’s

consent and can guarantee the shares of other co-owner whereas in

Shirkat-ul-Aqd, a partner cannot sell his share without other partners’

consent and partners cannot guarantee shares, or any profit, of other

partners.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

Forms of Shirkat-ul-Aqd

There are three forms of Shirkat-ul-Aqd:

n Shirkat-ul-Amwal: Where all the partners invest some capital

into commercial enterprises.

n Shirkat-ul-A'mal: Where partners jointly undertake to render

some services to their customers and share the fee charged by

them according to agreed ratio.

n Shirkat-ul-Wujooh: (Partnership in Goodwill) Where all the

partners will avail credit from market using their credibility and

sell the commodity to share the profit so earned at an agreed

ratio.

Musharaka rules discussed hereunder relates to Shirkat-ul-Aqd:

n The partners may contribute funds, not necessarily equally the arrangement covered under caption of 'Inan as discussed in Fiqh books. Partnership business can also be conducted by contributing labor, management, skill and goodwill.

n Capital to be invested by the partners can be unequal and should preferably be in the nature of currency. If it were in the shape of commodities, the market value would be determined with mutual consent to determine the share of each partner. It may also be in the form of equal units representing currency called shares and the intended partners may buy these shares disproportionately. Cash/Receivables are to be taken at face value and the conversion rate of the day of transaction in case of currencies. In case of running finance facility on Musharaka basis the average utilized amount will be considered as Musharaka capital.

n Capital of Musharaka has to be merged; merger can be actual as also constructive.

n All assets of Musharakah are jointly owned in proportion to the contribution of each partner.

03

All assets of

TIP

Glossary:

Inan: It is a form of partnership in which each partner contributes capital and has a right to work for the business, not necessarily equally.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

n A person can become a partner of a running business having fixed assets by investing capital in cash/kind; merger of various partnership firms is also allowed.

n Each partner has a right to take part in Musharaka management, but some of the partners may decide not to work for the Musharaka and work as a sleeping partner and they may appoint a managing partner by mutual consent. If all the partners agree to work for the joint venture, each one of them shall be treated as the agent of the other in all the matters of the business and any work done by one of them in the normal course of business shall be deemed to be authorized by all the partners.

n Power of appropriation in the property and participation in the affairs of the Musharaka may be un-proportionate to the capital invested by the partners.

n In Musharaka (as also in Mudarabah), ratio of profit distribution may differ from ratio of investment in the total capital, but the loss must be divided exactly in accordance with the ratio of capital invested by each of the partners.

n Profit can be divisible unequally and un-proportionate to the capital invested on the basis of work to be conducted for Musharaka. It is not allowed to fix a lump sum amount for any of the partners, or any rate of profit tied up with his investment. The profit ratio must relate to the actual profit accrued to the business and not to the capital invested by any partner. For example, it can

04

Profit can be

divisible unequally

and un-

proportionate to the

capital invested on

the basis of work to

be conducted for

Musharaka.

TIP

Keep In Mind

Each partner has a right to take part in Musharaka management, but

some of the partners may decide not to work for the Musharaka and work

as a sleeping partner and they may appoint a man aging partner by

mutual consent. In Musharaka (as also in Mudarabah), ratio of profit

distribution may differ from ratio of investment in the total capital, but the

loss must be divided exactly in accordance with the ratio of capital

invested by each of the partners.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

be agreed that profit earned would be distributed between two parties on fifty: fifty, sixty: forty, or thirty: seventy, basis. It can also be agreed that partners A, B and C, for example, would get 30%, 40%, and 30% respectively of the net profit earned by the joint business.

05

In Musharaka, it is

not allowed to fix a

lump sum amount

for any of the

partners, or any rate

of profit tied up with

his investment.

TIP

n Profit, in excess of the ratio of capital contribution can be on the basis of work done for the Musharaka. It means that if one or more partners choose to become non-working or sleeping partners, the ratio of their profit cannot exceed the ratio which their capital investment bears to the total capital investment in Musharaka.

n The partners may at the later stage agree to change the profit sharing ratio, and on the date of distribution, a partner may surrender a part of his profit to another partner. Similarly, one partner can cap his share of profit. It is also permissible for partners to decide not to distribute a portion of profit and create reserve(s).

n Profit ratio can either be fixed or variable according to the tiers. For example, one partner can say to the managing partner that his share in profit will be 50 % if earnings are up to 30 per cent and 40 percent if profit of the business exceeds 30 per cent.

n Traditionally, the liability of the partners in Musharaka is unlimited. Therefore, if the liabilities of the business exceed its assets and the business goes in liquidation, all the exceeding liabilities shall be borne pro rata by all the partners. However, if all the partners have agreed that no partner shall incur any debt

Glossary:

Liability: Liability is the responsibility for a loan or credit account. When applying for

credit, a borrower agrees to be liable for any charges to his or her account, including

interest, fees and finance charges.

Unlimited liability: A type of business where owners share joint and several responsibilities for the entire amount of debt and other liabilities amassed by the business.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

during the course of business, then the exceeding liabilities shall be borne by that partner alone who has incurred a debt on the business in violation of the aforesaid condition. Thus, liability of the partners in a partnership firm is unlimited since a partnership is not a legal person like a limited liability company. In case of business failure, and if Musharaka goes under loss, all liabilities in excess of remaining assets are to be shared proportionally by the partners.

06

Liquidation of a

venture

If one of the

partners withdraws

his shares without

closing the business,

the venture will be

liquidated

constructively.

TIP

Keep In Mind

Traditionally, the liability of the partners in Musharaka is unlimited. Therefore, if the liabilities of the business exceed its assets and the business goes in

liquidation, all the exceeding liabilities shall be borne pro rata by all the

partners. However, if all the partners have agreed that no partner shall

incur any debt then the exceeding liabilities shall be borne by that partner

alone who has incurred a debt on the business in violation of the aforesaid

condition.

n In case when the whole Shirkah business comes to an end at the maturity or termination before the expiry, the business shall be liquidated actually and the settlement between the partners will take place. In case when one of the partners withdraws his shares without closing the business, the venture will be liquidated constructively.

n Firms desiring to raise funds for investment can use this arrangement and offer to sell Musharaka Certificates in the market. After the project is started by acquiring non-liquid assets, these certificates can be traded in the secondary market.

n Musharaka can be based on a written agreement between the bank and the client for a specific transaction or for a fixed period of time that can be renewed. Profit projections can play an important role in the Musharaka operations. The client would be required to provide periodically the results of operations of the business to the bank. The disputes can be resolved through a

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

Review Committee comprising persons to be named in the Musharaka agreement with mutual understanding of the parties.

07

Practical Use of Musharaka

Musharaka can be used for the following purposes:

n Project financing

n Working capital & Running finance

n Import & Export Financing

n Saving/Deposit account

n Certificates of Investments

n Term finance certificates

n Inter bank financing

Keep In Mind

If Qasim and Sohail enter into a partnership and it is agreed between them that Qasim shall be given Rs. 50,000/- per month as his share in the profit, and the rest will go to Sohail, the partnership is invalid. Similarly, if it is agreed between them that Qasim will get 15% of his investment, the contract is not valid. The correct basis for distribution would be an agreed percentages of the actual profit accrued to the business.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

08

Summary

In short, we can say that Musharaka is a contract in which all parties share in

capital. All parties of Musharaka share profits and losses as well. Profits are

distributed as per agreed ratio whereas loss is borne by the parties as per

capital ratio. Under Musharaka, every partner is an agent of other partner.

Graphical Representation of Musharaka

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

MUDARABAH

In typical Mudarabah, one party provides the necessary capital and the other provides human capital needed for the economic activity to be undertaken. The contract of Mudarabah (also known as Qirad/Muqaradah) is traditionally applied to commerce alone, but it provides the basis of the relationship between banks, depositors and the entrepreneurs, and according to majority of the contemporary scholars, can be applied in all sectors of the economy like trade, industry, agriculture, etc. According to majority of jurists, Mudarabah is also a type of Shirkah when used as a broad term.Some considerations under Mudarabah contract are as follows:

n A Mudarib who runs the business can be a natural person, a group of persons, or a legal entity and a corporate body. Mudarabah shall include banks, unit trusts, mutual funds or any other institutions or persons by whatever name called.

n Different Capacities of Mudarib are:

m Ameen (Trustee): The money given by Rabb-ul-maal and the assets required therewith are held by him as a trust.

m Wakeel (Agent): In purchasing goods for trade, he is an agent of Rabb-ul-maal.

m Shareek (Partner): In case the enterprise earns a profit, he is a partner of Rabb-ul-maal who shares the profit in agreed ratio

m Zamin (Liable): If the business suffers a loss due to his negligence or misconduct, he is liable to compensate the loss

m Ajeer (Employee): If the Mudaraba becomes void due to any reason the Mudarib is entitled to get a fee for his services

09

According to

majority of jurists,

Mudarabah is also a

type of Shirkah

when used as a

broad term

TIP

Glossary:

Mudarib: Mudarib is the one, who manages the enterprise or investment and has the right to take all executive decisions under a Mudarabah Contract.

Rabb-ul-maal: Rabb-ul-maal is the one, who provides investment and funds to start a venture under Mudarabah contract.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

n Mudarabah may be of various types, which may be multi purpose or specific purpose, perpetual, or for a fixed period, restricted or unrestricted and close or open-ended in accordance with the conditions respective to each of them.

n The capital in Mudaraba may be either in cash or kind. If the capital is in kind, its valuation is necessary, without which Mudaraba becomes void. Rabbul Mal shall provide his investment in money or goods, other than receivables, at a mutually agreed valuation which shall be placed at the disposal of the Mudarib.

n It is necessary for the validity of Mudaraba that the parties agree, right at the beginning, on a definite proportion of the actual profit to which each one of them is entitled. They can share the profit at any ratio they agree upon. However, in case the parties have entered into Mudaraba without mentioning the exact proportions of the profit, it will be presumed that they will share the profit in equal ratios. Some incentives can be given to the Mudarib as bonus for “good business”.

n The profit shall be divided according to the proportion agreed at the time of contract and no party shall be entitled to a predetermined amount of return or remuneration.

n Apart from the agreed proportion of the profit, the Mudarib cannot claim any periodical salary or a fee or remuneration for the work done by him for the Venture.

n Rabbul Mal will suffer the operational loss unless it is proved that the Mudarib has been guilty of fraud, negligence or misconduct,

10

Sharing of Profit:

Partners in

Mudarbah can share

the profit at any

ratio, they agree

TIP

Keep In Mind

The capital in Mudaraba may be either in cash or kind. If the capital is in

kind, its valuation is necessary, without which Mudaraba becomes void.

Rabbul Mal shall provide his investment in money or goods, other than

receivables, at a mutually agreed valuation which shall be placed at the

disposal of the Mudarib.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

11

Most of the saving

accounts of

financial

institutions work

according to

Mudarabah and

Musharaka.

TIP

or has acted in contravention of the mandate. For the Mudarib, the loss is in terms of his un-rewarded labor or entrepreneurship.

Keep In Mind

Profit of a Mudarabah project can also be reinvested in the business and

the jurists have discussed this aspect in detail. It also refers to the

arrangement of com bination of Musharaka and Mudarabah. The Mudarib

in that case would be entitled to get profit on his own capital in the

proportion that his capital bears to the total capital of the Mudarabah. In

addition to such share in the profit, the Mudarib shall also be entitled to

share the remaining profit in agreed proportion.

n The liability of Rabbul Mal is limited to his investment, unless otherwise specified in the Mudarabah contract.

n In the case of deposits mobilized by banks on the basis of Mudaraba the profit from the banking business is shared between the Mudarib) and the Bank (as investment account holder (as Rabb-ul-maal) in a pre-agreed ratio.

n The Mudarib can invest his funds in the business of the Mudarabah with the permission of Rabbul Mal. Profit of a Mudarabah project can also be reinvested in the business and the jurists have discussed this aspect in detail. It also refers to the arrangement of combination of Musharaka and Mudarabah. The Mudarib in that case would be entitled to get profit on his own capital in the proportion that his capital bears to the total capital of the Mudarabah. In addition to such share in the profit, the Mudarib shall also be entitled to share the remaining profit in agreed proportion.

Calculation Method of Mudarabah

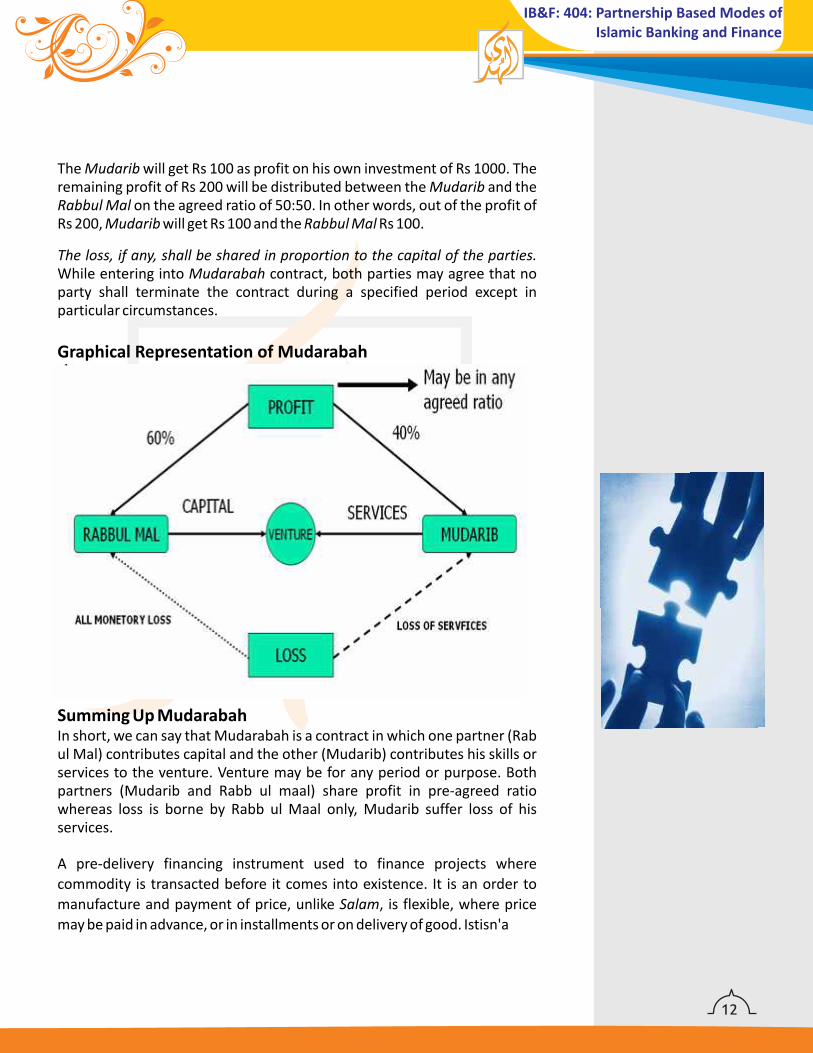

A Rabbul Mal provides Rs 2000 for Mudarabah, the Mudarib contributes Rs 1000 to the same with the permission of Rabbul Mal, and the parties have agreed to share the profit in the ratio of 50:50. Let us assume the profit earned by the Mudarib is Rs 300.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

The Mudarib will get Rs 100 as profit on his own investment of Rs 1000. The remaining profit of Rs 200 will be distributed between the Mudarib and the Rabbul Mal on the agreed ratio of 50:50. In other words, out of the profit of Rs 200, Mudarib will get Rs 100 and the Rabbul Mal Rs 100.

The loss, if any, shall be shared in proportion to the capital of the parties. While entering into Mudarabah contract, both parties may agree that no party shall terminate the contract during a specified period except in particular circumstances.

Graphical Representation of Mudarabah

Summing Up MudarabahIn short, we can say that Mudarabah is a contract in which one partner (Rab ul Mal) contributes capital and the other (Mudarib) contributes his skills or services to the venture. Venture may be for any period or purpose. Both partners (Mudarib and Rabb ul maal) share profit in pre-agreed ratio whereas loss is borne by Rabb ul Maal only, Mudarib suffer loss of his services.

A pre-delivery financing instrument used to finance projects where

commodity is transacted before it comes into existence. It is an order to

manufacture and payment of price, unlike Salam, is flexible, where price

may be paid in advance, or in installments or on delivery of good. Istisn'a

12

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

13

CASE STUDY ON MUDARABAH:

Regulation on the Parameterized Of Mudharabah Contract:A Critical Analysis

Abstract

Mudharabah is cooperation between an investor who gives fund or capital to a party who will manage the fund or capital for trading. The profit will be shared between two parties, investor and the care taker. Bank Negara Malaysia (BNM), the central bank, has already published the draft of its latest Shari'ah parameter on Mudharabah contract. The rationale of this Shari'ah parameter is to provide reference on the nature and features of the mudharabah contract to Islamic financial services industry, who is to promote the harmonization of Islamic finance market practices.

These are identified and proposed as secondary features mentioned in this parameter. This paper is focusing critically analyzes on practical constraint faced by Islamic banking in the implementation of Mudharabah financing facilities focus on under three categories: Demand Deposit, Mutual Investment Deposits and Special Investment Deposits. What do we expect from this paper may identify if a special rules apply to a types of contract mudharabah especially in restricted and unrestricted because their implication on conflict of interest.

The rationale of this

Shari’ah parameter

is to provide

reference on the

nature and features

of the mudharabah

contract to Islamic

financial services

industry

TIP

Case Study Reference:

The article mentioned for the case study is written by “Noraziah Che Arshad, College

of Business University Utara Malaysia”.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

DIMINISHING MUSHARAKAHAnother form of Musharaka, developed in the near past, is 'Diminishing Musharaka'. According to this concept, a financier and his client participate either in the joint ownership of a property or an equipment, or in a joint commercial enterprise. The share of the financier is further divided into a number of units and it is understood that the client will purchase the units of the share of the financier one by one periodically, thus increasing his own share till all the units of the financier are purchased by him so as to make him the sole owner of the property, or the commercial enterprise, as the case may be.

The Diminishing Musharaka based on the above concept has taken different shapes in different transactions.

Illustrations

n It has been used mostly in house financing. The client wants to purchase a house for which he does not have adequate funds. He approaches the financier who agrees to participate with him in purchasing the required house. 20% of the price is paid by the client and 80% of the price by the financier. Thus the financier owns 80% of the house while the client owns 20%. After purchasing the property jointly, the client uses the house for his residential requirement and pays rent to the financier for using his share in the property. At the same time the share of financier is further divided in eight equal units, each unit representing 10% ownership of the house. The client promises to the financier that

14

Diminishing

Musharaka is an

ideal product for

housing Finance but

can be utilized for

assets and

machinery

financing.

TIP

Keep In Mind

Diminishing Musharaka means a form of partnership which creates an

avenue for the capital provider to reduce or be free of the joint ownership

after the initial investment period has been satisfied. A normal Musharaka

contract allows for fluctuating levels of investme nt, but a Diminishing

Musharaka contract specifically relates to a reducing investment.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

he will purchase one unit after three months. Accordingly, after the first term of three months he purchases one unit of the share of the financier by paying 1/10th of the price of the house. It reduces the share of the financier from 80% to 70%. Hence, the rent payable to the financier is also reduced to that extent. At the end of the second term, he purchases another unit increasing his share in the property to 40% and reducing the share of the financier to 60% and consequentially reducing the rent to that proportion. This process goes on in the same fashion until after the end of two years, the client purchases the whole share of the financier reducing the share of the financier to 'zero' and increasing his own share to 100%. This arrangement allows the financier to claim rent according to his proportion of ownership in the property and at the same time allows him periodical return of a part of his principal through purchases of the units of his share.

15

n ’A' wants to purchase a taxi to use it for offering transport services to passengers and to earn income through fares recovered from them, but he is short of funds. 'B' agrees to participate in the purchase of the taxi; therefore, both of them purchase a taxi jointly. 80% of the price is paid by 'B' and 20% is paid by 'A'. After the taxi is purchased, it is employed to provide transport to the passengers whereby the net income of Rs. 1000/- is earned on daily basis. Since 'B' has 80% share in the taxi it is agreed that 80% of the fare will be given to him and the rest of 20% will be retained by 'A' who has a 20% share in the taxi. It means that Rs. 800/- is earned by 'B' and Rs. 200/- by 'A' on daily basis. At the same time the share of 'B' is further divided into eight units. After three months 'A' purchases one unit from the share of 'B'. Consequently the share of 'B' is reduced to 70% and share of 'A' is increased to 30% meaning thereby that as from that date 'A' will be entitled to Rs. 300/- from the daily income of the taxi and 'B' will earn Rs. 700/-. This process will go on until after the expiry of two years, the whole taxi will be owned by 'A' and 'B' will take back his original investment along with income distributed to him as aforesaid.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

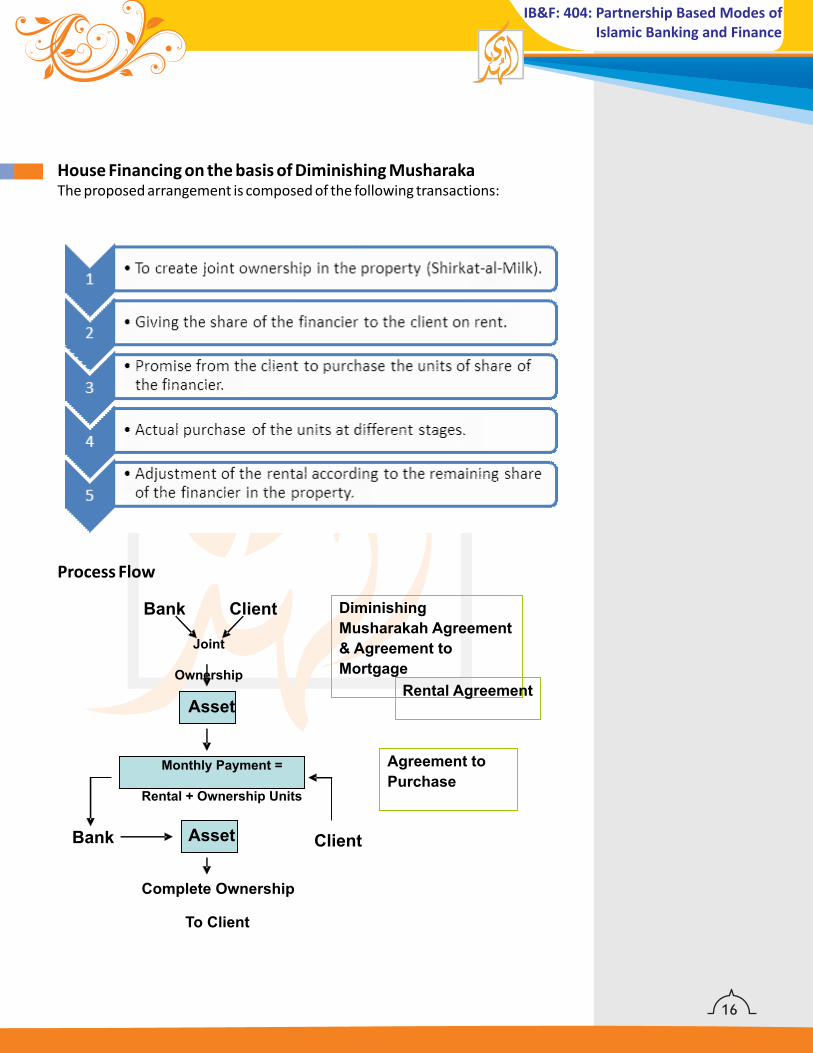

House Financing on the basis of Diminishing MusharakaThe proposed arrangement is composed of the following transactions:

Process Flow

16

Bank Client

Joint

Ownership

Asset

Monthly Payment =

Rental + Ownership Units

Asset Client Bank

Complete Ownership

To Client

Diminishing

Musharakah Agreement

& Agreement to

Mortgage

Rental Agreement

Agreement to

Purchase

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

Let us discuss each ingredient of the arrangement in a greater detail.

n The first step in the above arrangement is to create a joint ownership

in the property. It has already been explained in the beginning of this

chapter that 'Shirkat-al-Milk' (joint ownership) can come into

existence in different ways including joint purchase by the parties.

This has been expressly allowed by all schools of Islamic

jurisprudence. Therefore no objection can be raised against creating

this joint ownership.

n The second part of the arrangement is that the financier leases his

share in the house to his client and charges rent from him. This

arrangement is also above board because there is no difference of

opinion among the Muslim jurists in the permissibility of leasing

one's undivided share in a property to his partner. If the undivided

share is leased out to a third party its permissibility is a point of

difference between the Muslim jurists. Imam Abu Hanifah and Imam

Zufar are of the view that the undivided share cannot be leased out

to a third party, while Imam Malik and Imam Shafi'i, Abu Yusuf and

Muhammad Ibn Hasan hold that the undivided share can be leased

out to any person. But so far as the property is leased to the partner

himself, all of them are unanimous on the validity of 'Ijarah'.

n The third step in the aforesaid arrangement is that the client

purchases different units of the undivided share of the financier. This

transaction is also allowed. If the undivided share relates to both

land and building, the sale of both is allowed according to all the

Islamic schools. Similarly if the undivided share of the building is

intended to be sold to the partner, it is also allowed unanimously by

all the Muslim jurists. However, there is a difference of opinion if it is

sold to the third party.

17

Shirkat-al-Milk

(joint ownership)

can come into

existence in

different ways

including joint

purchase by the

parties.

TIP

Glossary:

Lease: In a lease contract, the party (the lessee) is granted the right to use the property of the lessor for a specified period of time at an agreed rental

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

It is clear from the foregoing three points that each one of the transactions mentioned hereinabove is allowed per se, but the question is whether this transaction may be combined in a single arrangement. The answer is that if all these transactions have been combined by making each one of them a condition to the other, then this is not allowed in Shari'ah, because it is a well settled rule in the Islamic legal system that one transaction cannot be made a pre-condition for another. However, the proposed scheme suggests that instead of making two transactions conditional to each other, there should be one sided promise from the client, firstly, to take share of the financier on lease and pay the agreed rent, and secondly, to purchase different units of the share of the financier of the house at different stages. This leads us to the fourth issue, which is, the enforceability of such a promise.

It is generally believed that a promise to do something creates only a moral obligation on the promisor which cannot be enforced through courts of law. However, there are a number of Muslim jurists who opine that promises are enforceable, and the court of law can compel the promisor to fulfil his promise, especially, in the context of commercial activities. Some Maliki and Hanafi jurists can be cited, in particular, who have declared that the promises can be enforced through courts of law in cases of need.

18

In Islamic legal

system, one

transaction cannot

be made a pre-

condition for

another.

TIP

Keep In Mind

If the undivided share is leased out to a third party its permissibility is a

point of difference between the Muslim jurists. Imam Abu Hanifah and

Imam Zufar are of the view that the undivided share cannot be leased out

to a third party, while Imam Malik and Imam Shafi‘i, Abu Yusuf and

Muhammad Ibn Hasan hold that the undivided share can be leased out to

any person. But so far as the property is leased to the partner himself, all of

them are unanimous on the validity of 'Ijarah'.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

19

The Hanafi jurists have adopted this view with regard to a particular sale called 'bai-bilwafa'. This bai-bilwafa is a special arrangement of sale of a house whereby the buyer promises to the seller that whenever the latter gives him back the price of the house, he will resell the house to him. This arrangement was in vogue in countries of central Asia, and the Hanafi jurists have opined that if the resale of the house to the original seller is made a condition for the initial sale, it is not allowed. However, if the first sale is affected without any condition, but after affecting the sale, the buyer promises to resell the house whenever the seller offers to him the same price, this promise is acceptable and it creates not only a moral obligation, but also an enforceable right of the original seller. The Muslim jurists allowing this arrangement have based their view on the principle that "‚

(The promise can be made enforceable at the time of need).

Even if the promise has been made before affecting the first sale, after which the sale has been affected without a condition, it is also allowed by certain Hanafi jurists. One may raise an objection that if the promise of resale has been taken before entering into an actual sale, it practically amounts to putting a condition on the sale itself, because the promise is understood to have been entered into between the parties at the time of sale, and therefore, even if the sale is without an express condition, it should be taken as conditional because a promise in an express term has preceded it.

This objection can be answered by saying that there is a big difference between putting a condition in the sale and making a separate promise without making it a condition. If the condition is expressly mentioned at the time of sale, it means that the sale will be valid only if the condition is fulfilled; meaning thereby that if the condition is not fulfilled in future,

Glossary:

Bai-bilwafa: bai-bilwafa is a special arrangement of sale of a house whereby the

buyer promises to the seller that whenever the latter gives him back the price of the

house, he will resell the house to him.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

the present sale will become void. This makes the transaction of sale contingent on a future event which may or may not occur. It leads to uncertainty (Gharar) in the transaction which is totally prohibited in Shari'ah.

Conversely, if the sale is without any condition, but one of the two parties

has promised to do something separately, then the sale cannot be held to be

contingent or conditional with fulfilling of the promise made. It will take

effect irrespective of whether or not the promisor fulfils his promise. Even if

the promisor backs out of his promise, the sale will remain effective. The

most the promise can do is to compel the promisor through court of law to

fulfill his promise and if the promisor is unable to fulfill the promise, the

promise can claim actual damages he has suffered because of the default.

This makes it clear that a separate and independent promise to purchase does not render the original contract conditional or contingent. Therefore, it can be enforced.

20

A separate and

independent

promise to

purchase does not

render the original

contract conditional

or contingent.

TIP

Keep In Mind

There is a big difference between putting a condition in the sale and making

a separate promise without making it a condition. If the condition is

expressly mentioned at the time of sale, it means that the sale will be valid

only if the condition is fulfilled; m eaning thereby that if the condition is not

fulfilled in future, the present sale will become void. This makes the

transaction of sale contingent on a future event which may or may not

occur. It leads to uncertainty (Gharar) in the transaction which is totally

prohibited in Shari‘ah.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

Calculation Method of Diminishing Musharaka in the case of Housing Finance

The calculation method of Diminishing Musharaka used by ABN AMRO for Housing Finance is as follows:

21

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

Conditions to use Diminishing Musharaka for House Financing

On the basis of the above mentioned analysis, diminishing Musharaka may be used for House Financing with following conditions:

n The agreement of joint purchase, leasing and selling different units of the share of the financier should not be tied-up together in one single contract. However, the joint purchase and the contract of lease may be joined in one document whereby the financier agrees to lease his share, after joint purchase, to the client. This is allowed because, as explained in the relevant chapter, Ijarah can be affected for a future date. At the same time the client may sign one-sided promise to purchase different units of the share of the financier periodically and the financier may undertake that when the client will purchase a unit of his share, the rent of the remaining units will be reduced accordingly.

n At the time of the purchase of each unit, sale must be affected by the exchange of offer and acceptance at that particular date

n It will be preferable that the purchase of different units by the client is affected on the basis of the market value of the house as prevalent on the date of purchase of that unit, but it is also permissible that a particular price is agreed in the promise of purchase signed by the client.

22

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

n M u s h a r a ka i s a t e r m u s e d b y contemporary scholars both for broad and limited connotations. Technically, Musharaka means a relationship established under a contract by the mutual consent of the parties for sharing of profits and losses arising from a joint enterprise or venture

n There are mainly two kinds of Shirkah: Shirkat-ul-Milk and Shirkat-ul-Aqd. The difference between Shirkat-ul-Milk and Shirkat-ul-Aqd is that Shirkat-ul-Milk is not for sharing profit whereas Shirkat-ul-Aqd is for seeking profit. In Shirkat-ul-Milk, co-owner can sell his shares without other co-owner's consent and can guarantee the shares of other co-owner whereas in Shirkat-ul-Aqd, a partner cannot sell his share without other partners' consent and partners cannot guarantee shares, or any profit, of other partners.

n Each partner has a right to take part in Musharaka management, but some of the partners may decide not to work for the Musharaka and work as a sleeping partner and they may appoint a managing partner by mutual consent. In Musharaka (as also in Mudarabah), ratio of profit distribution may differ from ratio of investment in the total capital, but the loss must be divided exactly in accordance with the ratio of capital invested by each of the partners.

23

Summary n Profit of a Mudarabah project can also be

reinvested in the business and the jurists have discussed this aspect in detail. It also refers to the arrangement of combination of Musharaka and Mudarabah. The Mudarib in that case would be entitled to get profit on his own capital in the proportion that his capital bears to the total capital of the Mudarabah. In addition to such share in the profit, the Mudarib shall also be entitled to share the remaining profit in agreed proportion.

n Diminishing Musharaka means a form of partnership which creates an avenue for the capital provider to reduce or be free of the joint ownership after the initial investment period has been satisfied. A normal Musharaka contract allows for fluctuating levels of investment, but a Diminish ing Musharaka contract specifically relates to a reducing investment.

n The capital in Mudaraba may be either in cash or kind. If the capital is in kind, its valuation is necessary, without which Mudaraba becomes void. Rabbul Mal shall provide his investment in money or goods, other than receivables, at a mutually agreed valuation which shall be placed at the disposal of the Mudarib.

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

n What is Musharaka? What are the types of Musharaka?n Explain some basic rules regarding Musharaka?n Show Musharaka and Mudarabah in graphical diagram?n What is Mudarabah? What are the rules regarding Mudarabah?n How diminishing Musharaka cab be used for house financing?n What are the conditions to use Musharaka for house financing?

For further study, you can consult our CD or e-library by getting log-in to your account. You

would get number of books, presentations, literature and reports on the following topics:

n Islamic financial services

n Contracts in Islamic commercial finance

n Islamic banking modes for house building finance by Mahm

n Islamic modes of business and fiancé

n Musharaka and Mudarabah as modes of finance by Taqi Usmani

n Practice of Mudarabah and Musharaka in Islamic banking by Mehmood Ahmed

n Regulation on The Parameterized of Mudharabah Contract: A Critical Analysis by

Noraziah Che Arshad, College of Business University

E-Library:

n Booksn Articlesn presentationsn Reports

24

Discussion Questions

Reference Material

IB&F: 404: Partnership Based Modes of Islamic Banking and Finance

Related Documents