Post-Depression Economics Neal Solomon† The essay presents the argument that the U.S. experienced a shallow economic depression in 2007-9 reminiscent of pre-war economic contractions. The economic data are analyzed to show that the downturn was more severe than any previous post-war downturn. Though technically over, the severity of the depression has led to extremely slow growth and a protracted period of high unemployment. The policies of the 2000s and the concentrated industrial structure they spawned are shown to have contributed to the severity of the downturn and to the slow recovery. The Keynesian and libertarian schools of economic thought are discussed in the context of their roles in offering prescriptions for improving economic growth. The essay critiques the academic economics profession for not predicting the downturn or providing useful prescriptions for solving economic problems. It is shown that China’s policies created a monetary and trade environment in the 2000s for the depression and that they are constraining economic growth as the U.S. exits the depression. A number of policy prescriptions are provided to improve economic growth. These best practices include constraining federal government spending, adjusting and balancing tax, competition, trade and intellectual property policies, promoting investment, education and innovation policies, and modulating Fed monetary policy. Index Introduction: What Happened to America? 2 Economic Analysis of the Downturn 5 Was the Downturn a Recession or a Depression? 13 This Time IS Different 25 Causes and Consequences of the Depression 36 The Rise of China 45 Policy Factors in the Economic Bubble and Aftermath 49 Redefining Conservatism 57 Failed Economics 62 Policy Prescriptions 66 List of Figures 78 List of Charts 78 Bibliography 79 † B.A., Reed College, 1981; A. M., University of Chicago, 1982; CEO, Advanced System Technologies, Inc. © 2010 by N eal Solomon. All rights reserv ed.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 1/82

Post-Depression Economics

Neal Solomon†

The essay presents the argument that the U.S. experienced a shallow economic depression in2007-9 reminiscent of pre-war economic contractions. The economic data are analyzed to showthat the downturn was more severe than any previous post-war downturn. Though technicallyover, the severity of the depression has led to extremely slow growth and a protracted period of high unemployment.

The policies of the 2000s and the concentrated industrial structure they spawned are shown tohave contributed to the severity of the downturn and to the slow recovery. The Keynesian andlibertarian schools of economic thought are discussed in the context of their roles in offeringprescriptions for improving economic growth. The essay critiques the academic economicsprofession for not predicting the downturn or providing useful prescriptions for solving

economic problems.

It is shown that China’s policies created a monetary and trade environment in the 2000s for thedepression and that they are constraining economic growth as the U.S. exits the depression.

A number of policy prescriptions are provided to improve economic growth. These bestpractices include constraining federal government spending, adjusting and balancing tax,competition, trade and intellectual property policies, promoting investment, education andinnovation policies, and modulating Fed monetary policy.

Index

Introduction: What Happened to America? 2Economic Analysis of the Downturn 5Was the Downturn a Recession or a Depression? 13This Time IS Different 25Causes and Consequences of the Depression 36The Rise of China 45Policy Factors in the Economic Bubble and Aftermath 49Redefining Conservatism 57Failed Economics 62Policy Prescriptions 66

List of Figures 78List of Charts 78Bibliography 79____________

† B.A., Reed College, 1981; A.M., University of Chicago, 1982; CEO, Advanced System Technologies, Inc.

© 2010 by Neal Solomon. All rights reserved.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 2/82

Post-Depression Economics

- 2 -

Introduction: What Happened to America?

“After the most severe recession since the 1930s, the U.S. economy appears to berecovering. Real (inflation-adjusted) gross domestic product (GDP) grew during thethird quarter of 2009, after having fallen 3.7 percent since the recession began in thefourth quarter of 2007. However, the economy’s output is still about 7 percent belowthe Congressional Budget Office’s (CBO’s) estimate of potential GDP—the outputthe economy would produce if its resources were fully employed. From December2007 to December 2009, the unemployment rate jumped from 4.9 percent to 10.0percent, and payrolls fell by about 7.2 million jobs. Moreover, if employment hadgrowth during this period at the same rate at which it had growth from 1990 to 2007,millions of additional jobs would have been added to the economy during that period;all told, the recession has lowered employment by about 11 million relative to what itwould otherwise be. Nearly all professional forecasters believe that the economy haspassed the trough of the recession, but many also predict that the pace of the recoverywill be slow.” [CBO, Policies for Increased Economic Growth and Employment

in 2010 and 2011, p. 1, 2010]

In 2000, the U.S. government experienced record federal budget surpluses and the federal

debt was being paid down. Middle class wages were growing and economic growth was strong.

Industrial corporations experienced a productivity revolution with robust profits and high

competition. Unemployment and poverty rates were at historic lows.

In 2010, the U.S. government experienced record federal budget deficits while adding to

an extraordinary federal debt. The unemployment rate peaked at 10.6% and industrial capacity

was at a record post-war low. With a poverty rate of 14.3%, 44.3 million people were in

poverty. Industry concentration was at a peak and income structures were more stratified than at

any time since 1928. High commodity prices from a commodity bubble in 2008 squeezed an

already strained middle class. Remarkably, real median income of $49,777 in 2009 was lower

than in 2000. The U.S. education system did not make the top 10 list among industrial countries.

And, two significant wars were being wound down.

What happened in such a short time? America obviously witnessed the consequences of

the application of a “conservative” economic and social experiment. To identify the solutions to

the economic problems, it is essential to understand the anatomy and sources of the problems.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 3/82

Post-Depression Economics

- 3 -

There is no debate about the fact that the United States experienced a significant

economic downturn. There is considerable controversy, however, about the technical

classification of the downturn. Was it a recession or a depression? Are we still in the downturn?

What policy programs got us into the problems and what policy programs are most likely to

improve economic conditions? These questions require historical and analytical insight to

answer.

A thesis of this essay is that the U.S. was in, and is recovering from, a shallow economic

depression. While there are numerous technical factors that require analysis to understand the

scale and scope of the economic contraction and aftermath, the present analysis seeks to clarify

the economic events of 2007-9 and its recovery. The evidence reveals that the U.S. is in a major

historical economic structural transformation. In addition to the empirical evidence about the

U.S. economy in the last few years, evidence about the international economy shows several

factors that influence the U.S. economic picture.

The main argument is that the U.S. adopted policies in the 2000’s that led to a sharp

economic contraction with a “long tail” that is caused by the process of continued deleveraging

of debt from a substantial financial bubble. This process of GDP decline and deleveraging was

complicated, and aggravated, by a financial industry crisis, which was apt to prolong economic

growth prospects. During this long recovery period, unemployment and debt levels are likely to

remain high while housing prices and industrial capacity are likely to have downward pressure

from a protracted period of constrained demand. Further, the evidence suggests that the U.S. is

in a pre-war type of shallow economic depression that, even after heroic policy actions, now

constrains government policy makers to engineer near-term economic solutions and thereby

protracts the downturn. In the environment of the long tail, federal government political

paralysis and Federal Reserve policy constraints will likely limit significant economic growth.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 4/82

Post-Depression Economics

- 4 -

While there is little controversy about the economic depression in the housing sector, the

long-term effects of the housing bubble are detrimental to consumers and economic growth.

Furthermore, while the housing bubble and economic contraction are indisputable, perhaps more

problematic are the facts about the erosion of the middle class during the 2000’s. Economic

pressures have resulted in a fundamental restructuring of the composition of the middle class.

The effect of these changes is to increase the stratification of American society, with the top 1%

responsible for 23%, and the top tenth of 1% responsible for 11%, of income in 2007. However,

it is argued that stratification is the effect, not the cause, of economic challenges and that a

consequence of increased stratification is increased economic instability.

The parallels between the economic policies of the 1920’s and the 2000’s are very

similar.1 It should be no surprise, then, that the consequences of these policies lead to financial

crises and economic instability.

While the U.S. experienced a housing bubble, a middle class decline and an economic

depression, China experienced an economic Renaissance in the 2000s. It is argued that China’s

rise had adverse effects on the U.S. economy during this period.

Though the economics profession largely failed to predict the downturn, whether because

of increased specialization, an overemphasis on math, a lack of policy or historical experience, or

1 Income inequality is similar when comparing the 1920s and 2000s. “Income disparities before [the1929] crisis and before the recent one were the greatest in approximately the last 100 years. In 1928, thetop 10 percent of earners received 49.29 percent of total income. In 2007, the top 10 percent earned a

strikingly similar percentage: 49.74%. In 1928, the top 1 percent received 23.94 percent of income. In2007, those earners received 23.5 percent.” Story, L., “Income Inequality and Financial Crises,” NYT,2010 [drawing parallels between economic conditions of the Depression and the recent downturn]. Realmedian household income was $21.7K in 1947, $28K in 1977 and $50.2K in 2007, according to U.S.Census Bureau data. In 1977, the top 1 percent of the top 1 percent earned $2M and by 2009, the top.01% earned $11.5M, showing far faster growth at the top. See Atkinson, T. and T. Piketty, Top Incomes

Over the Twentieth Century: A Contrast Between Continental European and English-speaking Countries,2007 [showing 20th century income patterns between several countries] and; Saez, E. and T. Piketty,“Income Inequality in the United States, 1913-1998,” Quarterly J. of Economics, 2003 [showing 20th

century U.S. income inequality patterns].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 5/82

Post-Depression Economics

- 5 -

ideological biases, it is crucial to analyze empirical economic data and economic policy in order

to develop cogent, pragmatic and bipartisan policy prescriptions.

Economic Analysis of the Downturn

Chart 1 shows GDP changes from the third quarter of 2007 to the third quarter of 2010.

Chart 1

U.S. Gross Domestic Product (Trillions of dollars)

2007III

2007

IV

2008

I

2008

II

2008

III

2008

IV

2009

I

2009

II

2009III

2009IV

2010I

2010II

2010III

13.95 14.03 14.37 14.49 14.54 14.34 14.05 14.03 14.11 14.28 14.45 14.57 14.68*

Source: Federal Reserve Flow of Funds Report [F.6 “Distribution of Gross Domestic Product: 9/18/08,9/17/09 and 9/17/10] * Projected

The economy grew very slowly from the fourth quarter of 2007 to the third quarter of

2008. The financial crisis that was triggered by the failure of Lehman Brothers in September of

2008 shows a decline of 4.2%2 in the fourth quarter of 2008, a decline of 8% in the first quarter

of 2009 and a decline of .7% in the second quarter of 2009. The economy then grew 1.6% in the

third quarter of 2009 and 5% in the fourth quarter of 2009. 2007 had a growth rate of about

2.5%, 2008 experienced a decline of 2.7% and 2009 had a growth rate of .2%. From the third

quarter of 2008 to the second quarter of 2009, however, the economy declined at a 4.1%

annualized rate, the largest and most protracted post-war economic decline.3

2 The economic growth and decline data are annualized.3 If the U.S. economy had grown at 5% a year from 2007 to 2011, GDP would be $17T at the end of 2010, rather than its actual $15T. Therefore, the U.S. economy lost about thirteen percent of its potentialgrowth in the downturn in a three year period.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 6/82

Post-Depression Economics

- 6 -

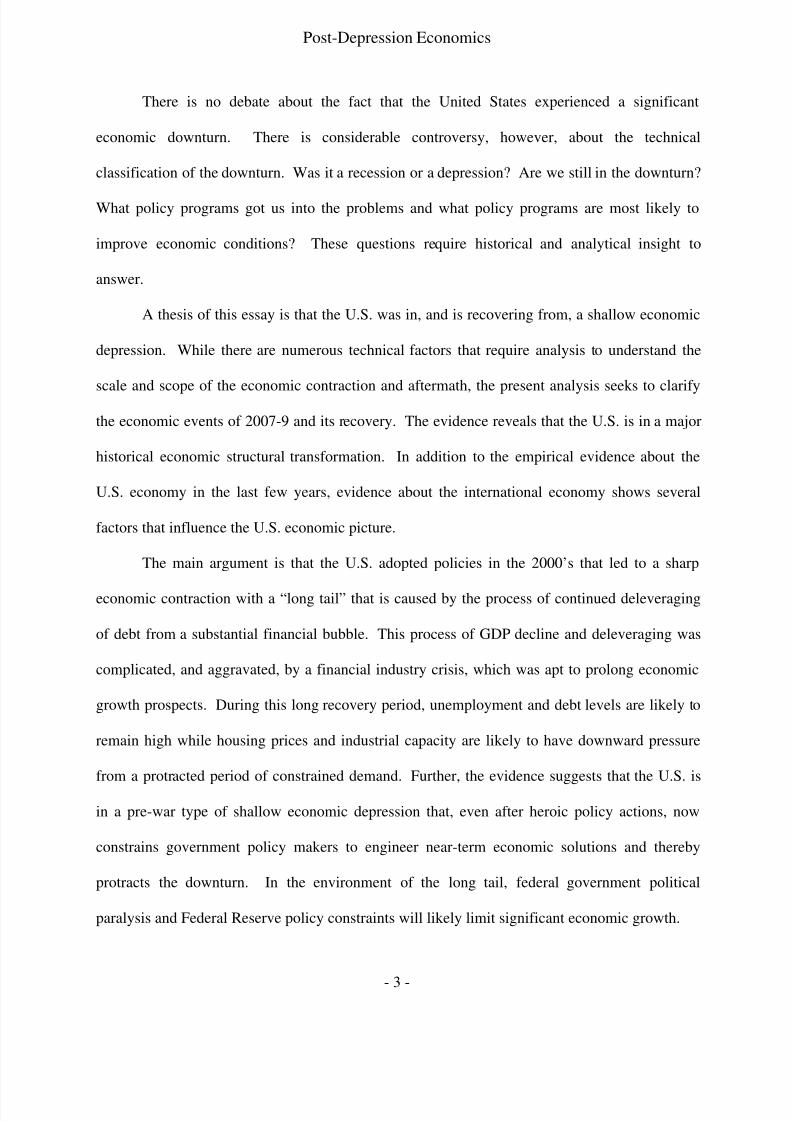

Figure 1

Relative GDP Decline of 2007-9 Downturn

Figure 1 shows the 2007-9 downturn GDP decline relative to post-war recessions. The chart

illustrates the relative severity of the downturn in technical terms. Both the length (18 months)

and depth (negative 4.1% GDP) show a severe contraction.

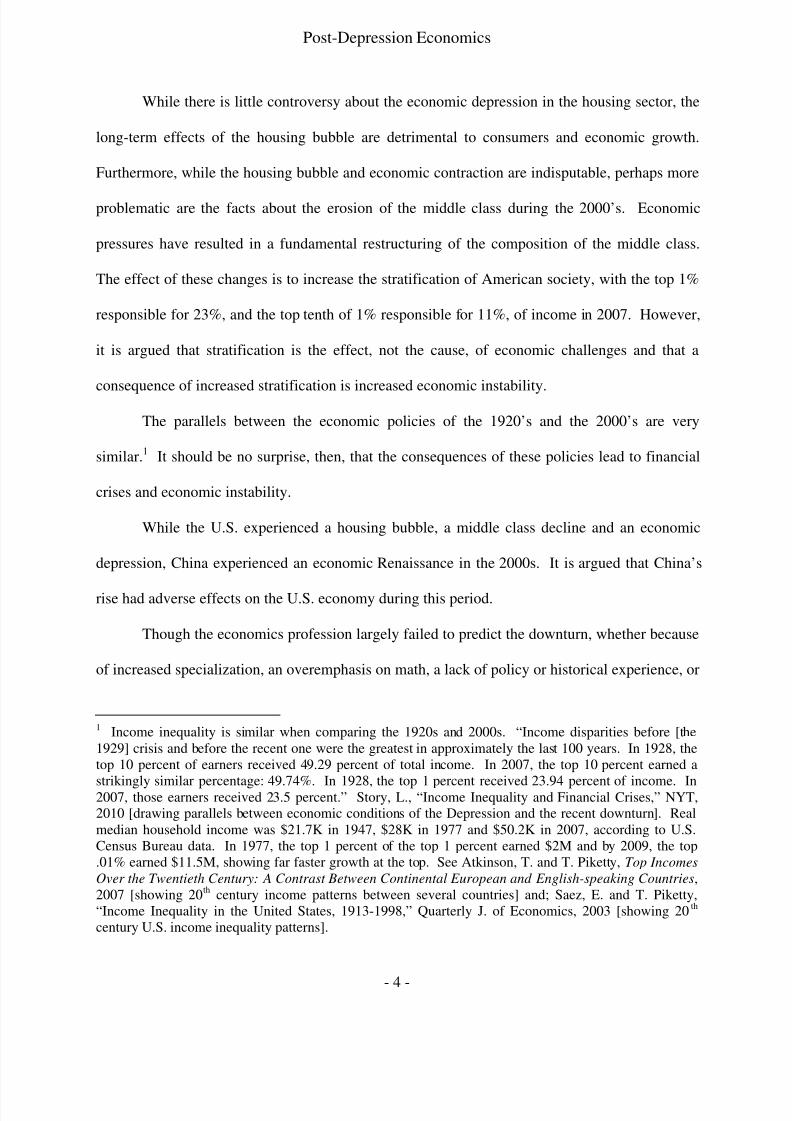

Chart 2

Total Net Worth 2007-2010

2007I

2007II

2007III

2007

IV

2008

I

2008

II

2008

III

2008

IV

2009

I

2009II

2009III

2009IV

2010I

2010

II

56.8 58 58.7 58.1 61.4 60.6 57.8 52.9 48.8 50.5 53 53.6 55 53.5

Source: Federal Reserve Flow of Funds Report [B.100 “Balance Sheet of Households and NonprofitOrganizations” 9/18/08, 9/17/09 and 9/17/10]

Chart 2 shows the total net worth data. These data reveal a much more substantial 19%

decline in the one year period from the second quarter of 2008 to the first quarter of 2009. The

8.4% decline from the third quarter of 2008 to the fourth quarter was the largest quarterly drop

since record keeping in 1951, reflecting the financial crisis in the immediate aftermath of the

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 7/82

Post-Depression Economics

- 7 -

failure of Lehman Brothers. This was followed by a 7.7% decline in the first quarter of 2009.

While the GDP data reflect public and private spending and show federal government spending

comprising a disproportionately larger share, the net worth data show a very severe downturn

that affected the private sector.4 The contraction in net worth from the fourth quarter of 2007 to

the third quarter of 2009 more clearly maps the extent of the downturn. According to this data, it

will take three and a half more years (early 2014) at a five percent annual growth rate to return to

the peak level of net worth shown in the first quarter of 2008.

Figure 2

Total Household Net Worth

Figure 2 graphically shows the relative decline in net worth since 1952. This illustrates

several post-war recessions, but the extraordinary decline of 2008-9 is illustrated at the right side.

The 2000s are shown as the “V” immediately prior to the precipitous decline.

4 The decline in net worth in the fourth quarter of 2008 and first quarter of 2009 reflected the drop invalue in the prices of both real estate and equities.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 8/82

Post-Depression Economics

- 8 -

The U.S. equity markets declined significantly in the downturn, with the Dow dropping

from about $14,000 in 2007 to about $6,500 in March, 2009, for a total decline of 53%,

comparable to the peak post-war decline in 1973-4.

Figure 3

S&P 500 [September 2007 to September 2010]

Source: S&P 500

Figure 3 shows S&P 500 data from September, 2007 to September, 2010. The equity

markets have been in a relatively narrow trading range during much of late 2009 and 2010,

reflecting the realities of slow expected economic growth. Note that it took the Dow Jones

Industrials twenty three years to return to its October, 1929, levels.5

The unemployment rate, however, rose rapidly beginning in the third quarter of 2008.

According to the U.S. Bureau of Labor Statistics, the unemployment rate moved from 4.6% in

2007, to 5.8% in 2008, 9.3% in 2009 and 9.9% in 2010. The unemployment rate peaked at

10.6% in March of 2010. This shows that while the economy grew nominally in the third quarter

5 The NASDAQ peaked at 5050 in March, 2000 and was about half of this level in 2010, suggesting thepotential for several more years to return to its peak level. The NASDAQ may be tracking the Dow’s1930s and 1940s performance.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 9/82

Post-Depression Economics

- 9 -

of 2009, unemployment was increasing to a peak level before declining in April of 2010.6 The

aftereffects of the downturn show a long tail in which unemployment continues to be unusually

high after the technical end of the downturn.7

Figure 4

Job Losses in Recent Recessions, as a Share of Employment

6 To show the relative severity of the depression, the total number of unemployed in 2008-10 was greaterthan in the downturns of 1981-2, 1990-1 and 2001 combined. While these data show the generalunemployment rate, the actual rate may be higher since those who are underemployed or who stoppedlooking are not counted. The Bureau of Labor Statistics indicated that the real unemployment rate peakedin 2010 at 16.6% (26M people) including underemployed and discouraged workers. An average of five

individuals applied for each job opening in 2010, the worst percentage since the 1930s.7 Poverty in the U.S. increased to its highest level – over 14% – since records were kept in the 1960s.An estimated twenty percent of children were in poverty. An eighth of Americans were on food stamps.The reason that our cities do not have Hoover town encampments of homeless and soup lines is that NewDeal and Great Society federal programs of unemployment insurance, food stamps, Welfare and socialsecurity provide a crucial social safety net. The idea of unraveling the safety net as a way to increaseeconomic efficiency and to save money is to shift risk onto individuals’ at their most vulnerable time,leading to nasty, brutish and short lives in a disintegrated post-industrial modern society. In the absenceof economic growth, the U.S. government maintains the burden of responsibility for surplus labor, whichpresents an economic conundrum in the long-run.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 10/82

Post-Depression Economics

- 10 -

Source: U.S. Department of Labor

Figure 4 shows the extraordinary unemployment decline in the 2007-9 downturn

compared to several prior recessions. The aggregate unemployment decline show the worst

downturn since the Great Depression.

Figure 5

Case Shiller Index

Source: S&P/Case Shiller Home Price Index

Housing price data show a substantial market decline as well. In the U.S., California,

Arizona, Florida, Nevada, Michigan and Ohio were particularly affected by the housing

contraction. In the aggregate, the U.S. experienced a dramatic housing price decline of over

30%, shown in figure 5, mainly driven by the oversupply of homes from record foreclosures.

The depression was not isolated to the U.S. World trade data – with declines of 12.2%

from 2008 to 2009 – also reflect a severe contraction akin to an economic depression. These

data are mirrored in commodity price declines from 2008 to 2010 and in industrial capacity data.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 11/82

Post-Depression Economics

- 11 -

Figure 6

Volume of World Merchandise Exports, 1965-2009

Source: WTO Secretariat

Figure 6 shows a 12.2% contraction in the volume of global trade from 2008 to 2010, the

worst post-war trade contraction.

Figure 7

Real GDP and Trade Growth of OECD Countries, 2008-9

Source: OECD Quarterly National Accounts

Figure 7 shows an even larger trade decline among Organisation of Economic Co-

operation and Development (OECD) countries, with corresponding GDP declines. Note that,

though global trade declined 12.2%, trade in the OECD countries – in both imports and exports –

declined at a sharper 15% from Q3 2008 to Q2 2009.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 12/82

Post-Depression Economics

- 12 -

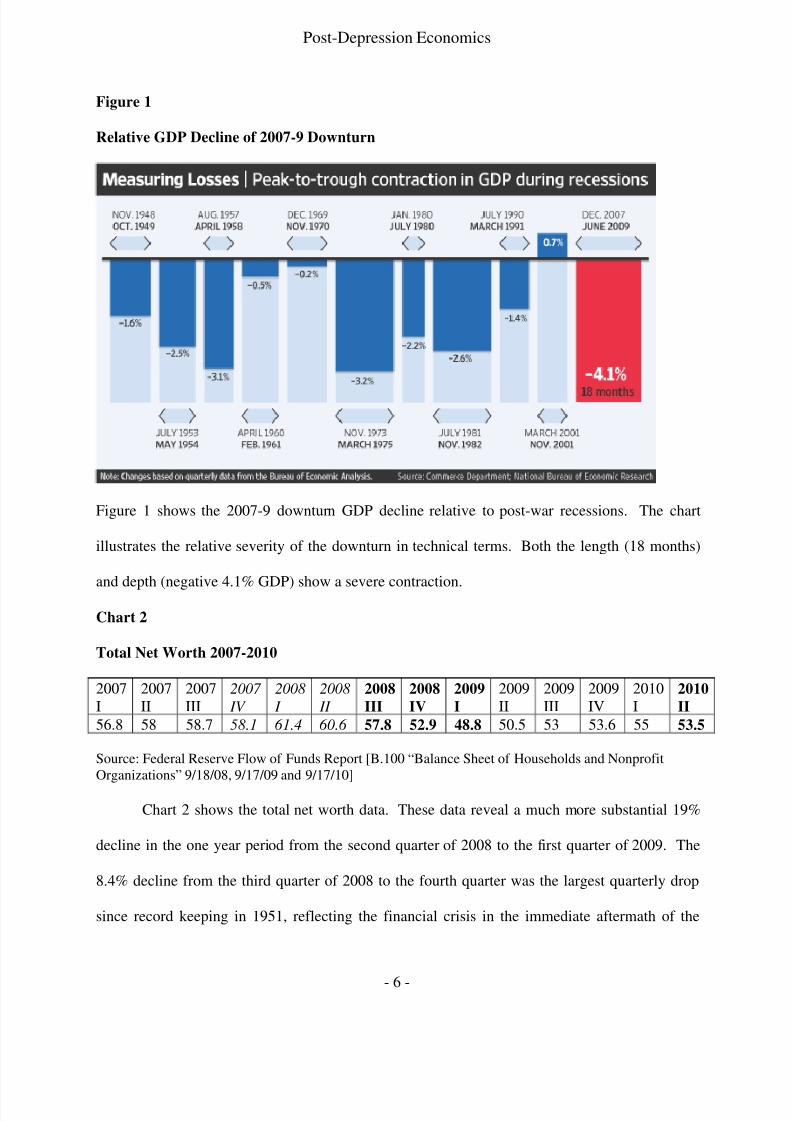

Figure 8

Growth in World Merchandise Exports Trade by Region

Source: IMF

The merchandise trade data from 2007 to 2009, shown in Figure 8, reflects the

commodity bubble in 2007 to 2008 that burst in 2008 to 2009. This suggests that the commodity

bubble may be a cause of or a factor in the economic destabilization period from 2007 to 2009.

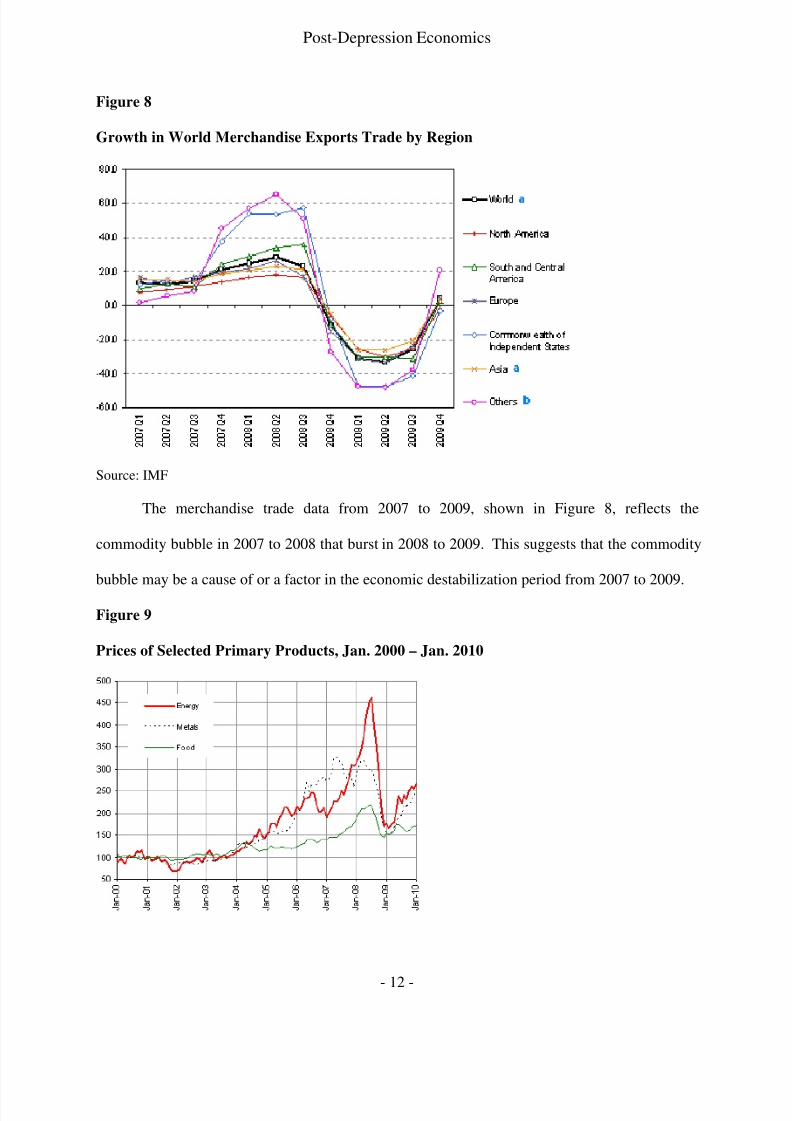

Figure 9

Prices of Selected Primary Products, Jan. 2000 – Jan. 2010

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 13/82

Post-Depression Economics

- 13 -

Source: IMF Primary Commodity Prices

The commodity price data, shown in Figure 9, also show a dramatic decline from mid-

2008 to mid-2009. Oil prices, for example, dropped from about $140 a barrel in August of 2008

to about $35 a barrel in July of 2009, reflecting both cartel market manipulation and a

precipitous drop in demand.

By all metrics, then, the global trade data indicate a greater correction than a typical

recession.

Finally, Ireland, Spain, Portugal, Greece, Hungary and the Czech Republic experienced

dramatic economic contractions that, in some cases, precipitated sovereign debt crises. Spain’s

Q2 2010 unemployment rate was over 20%. England experienced its worst GDP decline – at

5.9% – since 1921. Japan’s severe export-driven downturn precipitated significant political

instability. These economic events were not immediately responsive to coordinated heroic

international stimulus actions, indicating the intensity of the economic downturn. Collectively,

these cases illustrate the severity of the decline beyond a typical recession as well as the global

character of the economic downturn.

Multiple data sets, then, show that this was the worst downturn since the 1930s.

Was the Downturn a Recession or a Depression?

An economic recession is defined as a GDP downturn of two or more consecutive

quarters, while an economic depression is defined as a GDP downturn of three or more

consecutive quarters. In addition, a depression is characterized as a GDP decline of at least ten

percent from peak to trough; a great depression is characterized as a decline of at least twenty-

five percent. Since the 2007-9 downturn occurred over several quarters but GDP declined only

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 14/82

Post-Depression Economics

- 14 -

4.1%, it is generally seen as a severe recession, the so-called “Great Recession.”8 I have

suggested using the word “repression” to show an intermediary position between a recession and

a depression. However, the net worth, housing, trade, and industrial capacity declines of 12-30%

and the extraordinary unemployment data suggest that the contraction was more severe than a

recession. For example, the present downturn experienced an aggregate unemployment (viz.,

over 15M people) of greater than those in all of the last three recessions combined, including the

severe recessions of 1981-2 and 1990-1. The extraordinary unemployment data simply point to

the extreme depth and intensity of the fall-off of industrial production.9

There is some controversy about precisely when the contraction occurred. According to

Federal Reserve data, the contraction in GDP occurred from Q3 of 2008 (Lehman Brothers

collapse) to Q2 of 2009. This would provide a term of ten months. On the other hand, the

National Bureau of Economic Research (NBER) places the contraction period beginning in

December of 2007 and running to June of 2009 for a total of 18 months. If, however, the U.S.

economy did not come out of the contraction, based on NBER data, until Q1 of 2010 when

unemployment peaked at 10.6% in March, 2010.10 The period from December, 2007, to March,

2010, would constitute a 28 month contraction period if one includes the phase of the downturn

that accommodates the peak of unemployment. However, whether using the NBER 18 month

8 In 1931, Herbert Hoover used the term “Great Depression” to distinguish the severity of the economiccontraction to other events in recent historical memory. In 1981, the Reagan administration used the term“Great Recession” to describe the relative severity of the economic downturn at that time. The economiccontraction from 2007 to 2009 could be characterized as neither a “recession” nor as a “Great

Depression,” thus suggesting that the terms “depression” or “shallow depression” are more accuratedescriptions.9 See Barro, R. and J. Ursua, “Stock-Market Crashes and Depressions,” NBER Working Paper W14760,2009 [showing links between financial crises and economic contractions] and; Barro, R. and J. Ursua,“Macroeconomic Crises since 1870,” NBER Working Paper W13940, 2008 [analyzing post-Civil Wareconomic cycles].10 If the economy contracts from Q2 of 2010 to Q2 of 2011, following a trend of weak housing data andhigh unemployment, then the contraction period may be interpreted as qualifying as a “double diprecession” or as a continuous depression of up to 42 months. The evidence shows a net worth decline inthe third quarter of 2010 providing the prospect of a continuation of the contraction.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 15/82

Post-Depression Economics

- 15 -

mark or the 28 month mark that factors in a period to the peak phase of unemployment, the

downturn was empirically the worst continuous period of economic contraction since 1929-32.

In retrospect, there appears to have been three phases of the contraction. First, the initial

phase from Q4 2007 to Q3 2008 shows a period of disinflation and GDP atrophy. The second

phase, comprising the financial crisis and its immediate aftermath, consisted of a period of GDP

contraction from Q3 2008 to Q2 2009. The final phase, comprised of a period from Q2 2009 to

Q2 2010, witnessed an unemployment spike as industrial capacity dropped to a new equilibrium.

Though unemployment is a lagging indicator, and is expected to remain stubbornly high with a

gradual decline over several years, this later phase is a key characteristic of a severe economic

contraction. The multi-phasal view of the anatomy of the downturn suggests that the 2007-9

downturn was a protracted shallow depression much more reminiscent of pre-war downturns

than post-war downturns. However, even the minimalist view of the three-quarter technical

GDP contraction (i.e., phase II alone) qualifies as a shallow depression by historical standards.11

It is instructive to compare the 2007-9 downturn to the U.S. downturns since the Civil

War in order to assess its relative impact.

Chart 3 shows the history of U.S. post-Civil-war downturns.

11 A case can be made that a fourth, atrophy, phase may occur in 2010-12 from a further housing pricecontraction; this period has begun to experience disinflation as measured by price data and by net worthdeclines in the third quarter of 2010 from the second quarter of 2010.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 16/82

Post-Depression Economics

- 16 -

Chart 3

Business Contractions: Business Cycle Dates

Peak (Quarter) Trough (Quarter) Contraction

(months)

Prior Expansion

(months) June 1869 (II) December 1870 (IV) 18 18

October 1873 (III) * March 1879 (I) 65 18

March 1882 (I) May 1885 (II) 38 36

March 1887 (II) April 1888 (I) 13 22

July 1890 (III) May 1891 (II) 10 27

January 1893 (I) * June 1894 (II) 17 20

December 1895 (IV) June 1897 (II) 18 18

June 1899 (III) December 1900 (IV) 18 24

September 1902 (IV) August 1904 (III) 23 21

May 1907 (II) * June 1908 (II) 13 33

January 1910 (I) (dd) January 1912 (IV) 24 19January 1913 (I) (dd) December 1914 (IV) 23 12

August 1918 (III) ** (dd) March 1919 (I) 7 44

January 1920 (I) (dd) July 1921 (III) 18 10

May 1923 (II) July 1924 (III) 14 22

October 1926 (III) November 1927 (IV) 13 27

August 1929 (III) * March 1933 (I) 43 21

May 1937 (II) June 1938 (II) 13 50

February 1945 (I) ** October 1945 (IV) 8 80

November 1948 (IV) October 1949 (IV) 11 37

July 1953 (II) ** May 1954 (II) 10 45

August 1957 (III) April 1958 (II) 8 39

April 1960 (II) February 1961 (I) 10 24

December 1969 (IV) ** November 1970 (IV) 11 106

November 1973 (IV) March 1975 (I) 16 36

January 1980 (I) (dd) July 1980 (III) 6 58

July 1981 (III) (dd) November 1982 (IV) 16 12

July 1990 (III) March 1991 (I) 8 92

March 2001 (I) November 2001 (IV) 8 120

December 2007 (IV)* [June 2009 (III)] 18 73

Source: National Bureau of Economic Research

* Financial crisis ** War dd: Double dip

It is significant to note – and it is a key thesis of this essay to show – that the average

economic contraction from the Civil War to the Great Depression was 20.5 months, or about

exactly the average period – 18 months – of the 2007-9 downturn. On the other hand, the post-

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 17/82

Post-Depression Economics

- 17 -

War recessions were generally far more moderate at only 10.8 months each. The only anomaly

was the “double dip” recessions from 1980 to 1982 that could be described as a continuous

recession promulgated by activist Fed policy to correct exogenous inflationary pressures. The

depth of the downturn, in terms of industrial production, international trade, housing price

deflation and unemployment data is consistent with a prolonged and substantial pre-war slump.

As Chart 3 shows, excluding the Great Depression, in the 42 years between 1887 and

1929, there were thirteen downturns, for an average of one downturn roughly every three years.

The average downturn duration was 16.2 months and the average recovery period was 22.8

months. This Progressive era appears to have been an extremely volatile period of

entrepreneurship, financial crisis and urbanization. The intensely stratified configuration of the

economy was likely a key reason for explaining the unusually destabilized macroeconomic

system in this period of rapid industrial growth. With an average recession and expansion period

of about 39 months over this forty year period, this era is not a good harbinger for the near-term

future of the U.S. economy as it trends to an extremely stratified configuration. One key

implication of this observation is that before the Great Depression endogenous instability

generated from a stratified economic configuration. For instance, in contrast to the extreme

stratification from 1890 to 1930, the U.S. middle class thrived after WWII and the U.S.

witnessed a remarkable growth period to about the mid-70s. But projecting the model forward, it

is suggested that the U.S. may experience either a difficult period of slow growth or a worse

period of instability and a succession of crises.12

12 Using the analogy of the Progressive era, a period in which there was a recession after the trough of aprevious downturn every 22.8 months, there may be another recession in the U.S. shortly after mid-2011assuming the 2007-9 contraction ended at the end of the second quarter of 2009. Further, in the long-run,if the macroeconomic system is tracking this volatile period – with the absence of government policyinfluences – the U.S. may be in a generational period of extreme volatility in which significant recessionsoccur every three or four years, rather than every ten years like in the past generation. If we recall theperiod in the 1970s – the instability of which was largely caused by exogenous factors – we obtain a

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 18/82

Post-Depression Economics

- 18 -

The financial crisis of 1907 created an unstable period, with recessions in 1907, 1910 and

1913, to which the central bank was a response. The Federal Reserve Bank was created by

President Wilson in 1913 as a monetarist mechanism to moderate the extremes of market

speculation. But even with the genesis of the modern Fed, the frequency of recessions were not

moderated until after WWII.

One major theory used to describe the reduction in severity of post-War recessions to pre-

Great Depression contractions was the Fed’s active use of monetary policy to modulate

economic activity.13 It is interesting to note the protracted periods of growth between each

recession before 2007, at 92, 120 and 73 months, respectively, signifying the effectiveness of

Fed policy in a period of general growth.14 This evidence would support the view that

monetarist policy has been generally stimulative and effective to modulate growth and constrain

unemployment. However, even with supererogatory action, the Fed’s power is severely

closer picture of the potential for macroeconomic disequilibrium created from endogenous factors causedby extreme stratification. The massive build-up of debt (public, consumer and business), the difficulty of deleveraging, the limits of Fed and international central bank policy, the political paralysis, a massivewave of retiring baby boomers, sovereign debt crises and enormous trade imbalances all point to thepotential of a destabilizing period of continuous recessions and shallow recoveries for at least a

generation. It is possible, then, that the U.S. may witness a new equilibrium period of slowgrowth, increasingly frequent recessions and a new range of unemployment between 8% and12%. On the other hand, it is possible that the rate of growth will pick up in 2011 and 2012,much as the economy experienced a rapid growth phase in late 1993 after the 1990-1 recessionand long tail from a deleveraging process.13 See Bernanke, B., Essays on the Great Depression, 1994 [discussing Depression era monetary policy];

Bernanke, B., “The Macroeconomics of the Great Depression,” NBER Working Paper No. 4814, 1994[identifying economic policy conditions and prescriptions in the Depression]; Bernanke, B.,“Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression,” The American

Economic Review, Vol. 73 (June), pp. 257-276, 1983 [showing the role of the banking crisis in theDepression] and; Bernanke, B. and H. James, “The Gold Standard, Deflation, and Financial Crisis in theGreat Depression: An International Comparison,” NBER Working Paper No. W3488, 1990 [showing therole of the gold standard on monetary conditions in the Depression].14 In the twelve post-war recessions, though the average contraction duration was 10.8 months, theaverage recovery period was 60 months, for an average cycle period of 71 months or about double theduration of business cycles before the Great Depression.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 19/82

Post-Depression Economics

- 19 -

constrained at the present time, suggesting that we are in a new equilibrium period. In fact,

monetarism may be worthless in a disinflationary economy in which interest rates are near zero.

The duration of the recent downturn has been unusually protracted. While the decline in

GDP stopped in mid-2009,15 according to technical factors, the recovery period has been

particularly slow, with annual growth below 2%. With growth at a steady state level, total

employment will not change beyond the population growth rate, thereby maintaining a high

unemployment rate. Clearly, this relatively slow growth period is consistent with a downturn

that is accompanied by a financial crisis.16 When identifying those periods of economic

downturns accompanied by financial crises, such as 1873, 1907 and 1929, the present period

qualifies as a longer downturn than a typical recession.

The financial industry crisis had as the root cause the housing bubble. 17 The housing

industry has clearly been in a protracted economic depression that began in 2006 and persisted

through 2010.18 Since most people use their house as a source of economic value, the housing

price declines have affected the debt and credit components of a large portion of the economy.

Until excessive debt is liquidated, the housing sector will continue to languish. In addition, when

15 In some ways, the 2008 financial crisis was a perfect storm of events, particularly with the politicaluncertainty of a major presidential election and transition. While the early stimulus legislation likelyaverted a more severe downturn, the Obama administration clearly inherited the legacy of previous policyefforts to limit damage from the financial crisis. The severity of the crisis left few good options.16 See Reinhart, C. and K. Rogoff, “The Aftermath of the Financial Crises,” NBER Working Paper, No.W14656, 2009 [showing the macroeconomic effects of financial crises, indicating a pattern of protracteddownturns after crises].17

The sub-prime lending sector was not the only problem of the financial industry in the 2000s. Inretrospect, offering creative, adjustable, loans with no credit or down payment, securitizing the loans,mis-rating the securities (often with conflicts of interest), offering “credit default swap” insurance on thesecurities by the London-based AIG Financial Products group and paying absurdly high transaction-feesand bonuses to bankers to perform these financial services was probably not a good idea. One U.S.securities industry regulator responsible for policing the industry never heard of the credit default swapsused to insure mortgage backed securities, which seems a little puzzling.18 Fannie and Freddie offer home loans on median sized mortgages at 3% to 4% in 2009-2010, far belowthe 6% to 8% private market interest rates. Despite these subsidized loan prices the market still remainssoft in 2010.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 20/82

Post-Depression Economics

- 20 -

unemployment is high, further pressure is put on housing prices, deepening the cycle of debt

deleveraging. Since the bursting of the housing bubble was at the core of the recession, it is

critical to get control of this debt deleveraging process. Continuing housing price declines,

which are expected with a high backlog of foreclosures in the pipeline, will likely be a drag on

economic growth for the next few years.19

International trade, a measure of industrial production, experienced a 12.2% decline in

2008-2009, consistent with a significant economic depression. The trade data reflect the sharp

manufacturing contractions in the U.S., Japan, Europe and China as consumer demand dropped

precipitously. Furthermore, commodity prices dropped dramatically from 2008 to 2009,

reflecting a global economic depression caused by a sharp drop in demand.

The global character of the downturn is particularly indicative of an economic

depression. All economic data sets point to the greatest declines in GDP, employment, industrial

capacity, trade and housing prices since the Great Depression of the 1930s, suggesting that there

was a more severe economic downturn than a recession. In fact, the similarity of the downturn

to the early 1930s is instructive since there are parallels with the housing crises and the financial

crises between the periods.20

Going further, one can argue that the world economy experienced a

depression in 2007-10 that originated in the U.S.

If the U.S. experienced a shallow depression from 2007-9, an analysis of history shows

that the period from 2010 to 2015 is likely to witness protracted unemployment and a long tail of

19

There appears to be about five million homes in the foreclosure pipeline in 2010. At a rate of 95K amonth, this excess housing inventory is likely to have deflationary consequences. See the argumentbelow on the causes and consequences of the economic downturn. Finding ways to control the continuingsoft demand in the housing sector is critical to arresting the slow economic growth rate. On the otherhand, some argue that letting the housing market bottom is the best way to realize eventual healthyeconomic growth.20 See Stiglitz., J., Freefall: America, Free Markets, and the Sinking of the World Economy , 2010[arguing that the U.S. is in a structural economic decline] and; Day, V., The Return of the Great

Depression, 2009 [arguing that the economic conditions in 2008-9 are similar to the conditions in theearly 1930s].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 21/82

Post-Depression Economics

- 21 -

slow economic growth from reduced demand and continued debt deleveraging.21 This period of

relative stagnation may be reminiscent of the Japanese “lost decade” of the 1990s. The two

periods are likely to share similar economic and policy causes of a slow deleveraging process as

banks are unwilling to write off bad loans and as protracted high unemployment diminish

consumer demand. This period of relative stagnation may be part of a longer process associated

with a shallow economic depression, but is also a period highly susceptible to exogenous

economic shocks, such as commodity bubbles that lead to corresponding inflation. One way to

transmit this inflation is with a weakening dollar that is likely to occur, based on historical

experience, because of the large federal debt, projected federal deficits, U.S. trade imbalances

and expansionary Fed monetary policy. The effects of the stagnation and bubbles will lead to

further pressures on, and perhaps a recomposition of, the middle class. The possibility exists,

then, that the U.S. is only in the early phases of a protracted economic depression with a period

of tepid recovery, but then a period of declining demand, possibly a deflationary period and then

rapid inflation akin to the experience of the 1970s. These economic conditions will make the

Fed’s policy decisions particularly challenging.

For much of the 19th

century there was no central bank to moderate economic downturns

by supplying and regulating money to banks, companies and consumers. The markets were at

the mercy of the industrial and financial institutions – and their entrepreneurial leaders – which

tended to experience booms and busts. The post-Civil War depression of 1873 lasted five years,

with nearly half of the population unemployed at some point during the period. The depression

of 1893 was also substantial and protracted. These depressions were protracted because of the

21 See Reinhart, C. and K. Rogoff, This Time is Different: Eight Centuries of Financial Folly, Princeton,2009 [arguing that economic bubbles share a common pattern] and; Reinhart, C. and V. Reinhart, “Afterthe Fall,” op. cit. [arguing that economic crises that stem from financial crises require several years of debt deleveraging from which to recover].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 22/82

Post-Depression Economics

- 22 -

limited ability of the federal government to provide an antidote, particularly in the absence of a

central bank. The private economy was forced to repair itself without any assistance and these

self-organizing mechanisms were relatively slow to act. Similarly, the downturns of 190722 and

1929 witnessed a limited ability of the federal government to respond. In the 1930s, the Fed

made substantial policy mistakes that had the adverse effects of protracting the Depression in

1931 and 1937.

It should be obvious in hindsight that the present situation is reminiscent of these periods

that limits the extent to which government or the Fed can intervene.23 For example, with interest

rates at record lows, there is little more ammunition the Fed possesses to stimulate the economy

with monetary policy. Similarly, the federal government’s ideological polarization has led to

severe political constraints that limit the ability to stimulate the economy by adding to deficits.

In terms of economic policy, the period of the 2000s was very similar to the 1920s.24 The

1920s industrial and financial deregulation policy resulted in a housing bubble and industrial

concentration that led to a financial crisis that stimulated the protracted economic downturn of

the 1930s. In the 2000s, similar industrial and financial deregulation policy resulted in a similar

housing bubble and industrial concentration that led to a financial crisis that stimulated a

protracted downturn in its aftermath. These similarities suggest that there are clear policy

considerations that led to both economic downturns. While the 1931 bank crisis contributed to

making the 1929 recession a protracted – 43 month – depression, which resulted in a 96%

22 See Bruner and Carr, The Panic of 1907: Lessons Learned from the Market’s Perfect Storm , 2007[describing multiple conditions for the 1907 financial crisis].23 In September of 2008, the Fed held $480B of treasuries. By Q2 of 2010, the Fed held $2T of securities, including $1.2T in mortgage securities. In the first three quarters of 2010, Americans bought$200B of all debt securities and foreign holders bought $375B in treasuries. These actions have driveninterest rates to near zero.24 See Leuchtenburg, The Perils of Prosperity, 1914-32, 1993 [arguing that the conditions for the GreatDepression were sewn by adhering to laissez faire policies].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 23/82

Post-Depression Economics

- 23 -

decline in the value of the Dow from 1929 to 1932, the 2008 banking crisis25 may be shown to

have made the 2007 recession a depression that led to a 53% decline in the value of the Dow

from 2007 to 2009, rivaling the worst post-war equity price decline in 1973-4.26

Although the composition of industry in 1930s America is not completely analogical to

the present situation, mainly because the country now enjoys a much larger27 and more

diversified economy, comparing the 2007-9 downturn to the recession of 1991 to 1992 is more

instructive. The real estate bubble of the 1980s led to a financial industry crisis that required

several years to deleverage debt and was accompanied by slow growth and a period of high

protracted unemployment. The economy did not substantially rebound until the fourth quarter of

1993, while real estate prices declined an average of five percent a year from 1990 to 1998 in

many cities. However, the financial and real estate bubbles of the 2000s were larger and more

pervasive than those in the 1980s – fed by both deregulation and Fed easing – suggesting a far

more substantial downturn from 2007-9 than in 1990-1.

While viewing GDP data alone provides an ambiguous interpretation, viewing strategic

industries such as real estate, automobile and manufacturing as well as trade data, which

collectively experienced thirty percent declines from 2007 to 2009, shows that the recent

economic contraction was particularly onerous. Similarly, when viewing the net worth data

declines, it appears that the downturn was much more severe than the GDP data show, indicating

25 See Murphy, “An Analysis of the Financial Crisis of 2008: Causes and Solutions,” SSRN, 2008[revealing the anatomy of the financial crisis]; Reinhart, C. and K. Rogoff, “Banking Crises: An Equal

Opportunity Menace,” NBER Working Paper W14656, 2009 [arguing that banking crises typically showsimilar patterns] and; Reinhart, C. and K. Rogoff, “Is the 2007 U.S. Sub-Prime Financial Crisis soDifferent? An International Historical Comparison,” NBER Working Paper W13761, 2008 [usinghistorical and international evidence to show common patterns of banking crises].26 Without aggressive Fed policy and U.S. government stimulus and TARP policy actions, the declinewould likely have been more severe.27 The U.S. income tax receipts in 1929 were $1.1B and in 1935 were about $500M. Even after factoringin inflation, when considering that the sources of federal government income were personal income taxes,corporate taxes and excise taxes, the size of the federal government in the 1930s was significantly smallerthan the present time.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 24/82

Post-Depression Economics

- 24 -

that the private sector was particularly hard hit and that public spending from government stimuli

was crucial to mitigate even further declines. The implications of a more severe contraction than

traditional measurements of GDP data alone show are that these past metrics may be inadequate

to capture the depth of the downturn. If the data were much more straightforward to interpret,

the NBER would not have waited fifteen months after the technical indicators showed an end to

the downturn to define its parameters.

Although the aggregate data regarding the typology of the economic downturn is

controversial, the effects of the downturn on specific classes of individuals are less controversial.

The manufacturing sector experienced a structural decline responsible for a reduction from 30%

of GDP in 1970 to only 12% of GDP in 2009.28 Similarly, the middle class experienced an after-

inflation net decline of wages from 2001 to 2010 even while energy, education and health costs

increased at rates higher than the core rate of inflation. For the middle class, the average worker

and the poor, then, this downturn was, and is, structural and persistent.

Given these economic data points, it is appropriate to consider that the U.S. experienced a

significant, but relatively shallow, economic depression from late 2007 to at least mid-2009. The

depth, intensity, speed, prolonged duration and global character of the downturn suggest that the

U.S. experienced significantly more than a recession. For these reasons, the case can be made

that the U.S. was in, and is gradually recovering from, a shallow economic depression.

28 Much of U.S. manufacturing is concentrated in a few industries dominated by incumbents such asBoeing, Caterpillar, Intel, Ford and GM.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 25/82

Post-Depression Economics

- 25 -

This Time IS Different29

How was this time different? The magnitude and duration of the downturn, the

international aspect of the downturn and the inclusion of the financial (bank and sovereign debt)

crises suggest that 2007-9 was substantially worse than any economic downturn since 1929-32.

The case for an economic depression from 2007-9 is reinforced by looking at both

empirical and policy data from 2001 to 2010 and by comparing the data to historical economic

downturns. The depth of the decline is registered in unemployment data, industrial utilization

data, trade data and real estate price data from 2007 to 2010. According to these data, the

economic decline was unequivocally greater than any post-war recession. The argument for

viewing the economic contraction as a shallow depression suggests that we are in a new

destabilizing period with a long tail of recovery.30

In the aftermath of the contraction phase, the long tail that characterizes the slow

recovery is notable because of a new post-contraction equilibrium phase characterized by

29

See Reinhart, C. and K. Rogoff, This Time is Different: Eight Centuries of Financial Folly, 2009[arguing that similar patterns of boom and bust are seen at different times and places].30 The argument for a continuous shallow depression sees the increase in factory production of the lasthalf of 2009 and the first half of 2010 as a period of inventory restoration that, once complete, will thenlead to a period of protracted demand decline that mirrors the experience of the early 1930s. Further, theGDP gains in the last half of 2009 are likely caused by the federal government stimulus and by arelatively weak dollar that artificially stimulated exports. However, this modest temporary increase ismore typically part of a period of protracted decline characteristic of a continuous deflationary (ordisinflationary) period.

The notion that the U.S. may witness a “double dip” recession of a second phase of GDPcontraction is consistent with the view of one single continuous event. The U.S. experienced one post-war “double dip” recession in 1980 and in 1981-1982. However, this period could also be characterized

as a single continuous event, with two stimulative components. The first cause was the Iranian oilembargo that raised oil prices by two to three times, thereby causing both contraction and inflation.Because of the high inflation, the Fed, in keeping with its inflation targeting strategy, raised interest ratesin 1981-2 so high as to stimulate the second phase of the recession. It is argued that these phases of aprocess were causal and continuous and thus a single event, not a double dip. Nevertheless, parts of Europe appear to be experiencing either a double dip recession in 2010 or one continuous depression. SeeBernanke, B. and M. Woodford, eds., The Inflation-Targeting Debate, 2006 [discussing the Fed’sinflation targeting strategies] and; Bernanke, B., T. Laubach, F. Mishkin and A. Posen, Inflation

Targeting: Lessons from the International Experience, 2001 [articulating the use of inflation targeting bycentral banks in the international context].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 26/82

Post-Depression Economics

- 26 -

consistently slow growth. The industrial utilization and employment data are at post-war lows in

the aftermath of the initial downturn period largely because of persistent constrained demand. It

is this long tail that one can argue characterizes a “repression” or a protracted stagnation phase of

a prolonged period of severe recession. While the near-zero growth stagnation period is not a

depression, it is not characteristic of post-war growth either. Using a medical analogy, it appears

as though, after the original sickness, the patient has lost a considerable amount of weight and

cannot gain the weight back to return to a normal healthy state. We appear to be in a completely

new equilibrium going forward.

However, most post-war recessions have ended with a period of 5-6% annual growth.

With anticipated 1.5-2.5% annual growth in 2010-2011 and with unemployment at or near

double digits for the foreseeable future, the present long tail is not characteristic of past

termination periods of recessions. With only 80K jobs created monthly in 2010, this tepid

employment growth, experienced with 2.5% or less annual GDP growth, will not keep up with

population growth. It will take four years of 5% GDP growth to reduce the unemployment rate

from about 10% to a pre-downturn unemployment rate of about 4.6%. At an economic growth

rate substantially less than 5%, the U.S. may experience a structural employment slump over five

years.

Most U.S. recessions in the twentieth century had common profiles. For instance, 1907

and 1931 had financial crises. 191831 and 1945 were characterized by the end of WWI and

WWII. Each of the recessions from 1973 to 2001 was characterized by economic bubbles. In

1973 and 1979, the recessions resulted from commodity (i.e., exogenous oil) bubbles, 1990-1

from the 1980s real estate bubble and 2001 by the Internet and telecommunications bubble.

31 The influenza epidemic probably did not help the economic conditions in 1918.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 27/82

Post-Depression Economics

- 27 -

Each recession experienced a prolonged period of asset price deflation. In effect, each recession

was a solution to a period of abnormal price inflation.32

The 2000s real estate bubble was caused in part by an unusually protracted period of low

interest rates promulgated by the Fed to control the 2001 recession and by deregulation of

financial institutions in the aftermath of Glass-Steagall. However, the middle class from 2000-

2007 experienced slow employment growth (about two million, generally low quality service,

net jobs created mainly from 2003 to 2007) and a net after-inflation decline in real wages while

manufacturing was substantially off-shored. The considerable stress on the middle class in the

2000s set up a high-debt period that would lead to the intensity of the depth of the downturn,

much like the 1920s set up the conditions for the 1930s protracted contraction.

It is the extraordinary debt picture, and its deleveraging process, that set up the downturn

and slow recovery. The following figures show the debt data.

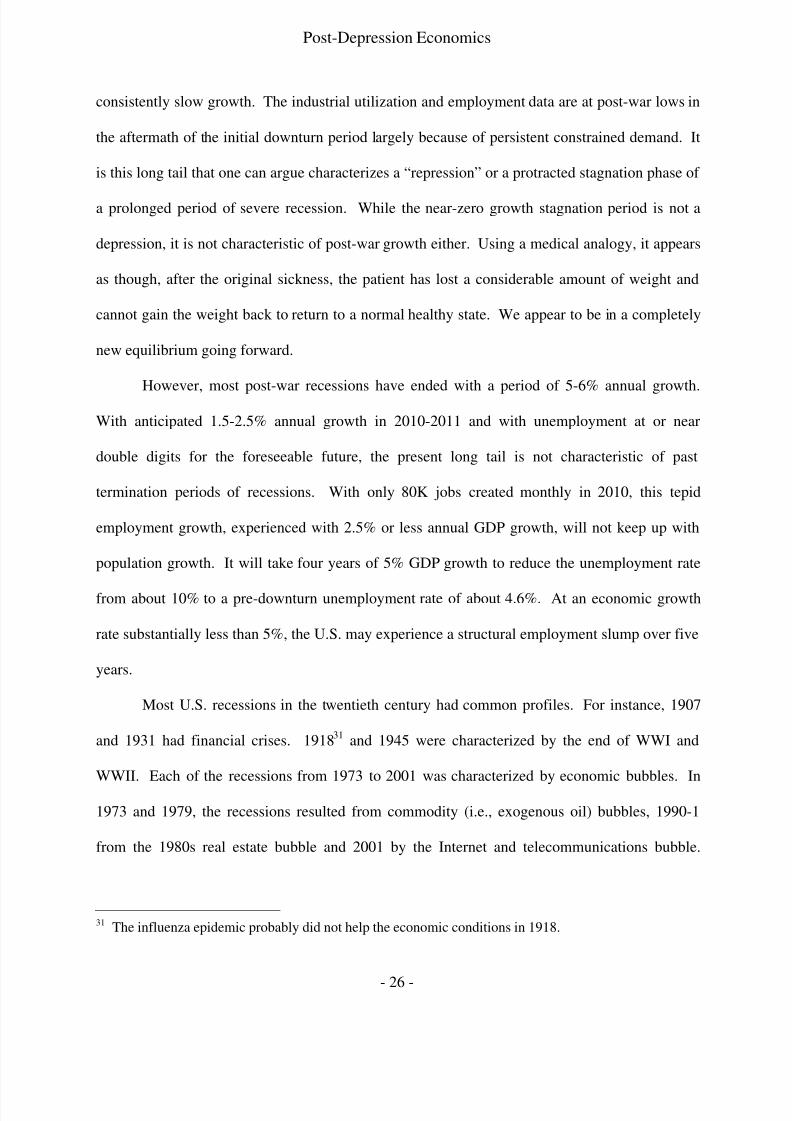

Figure 10

U.S. Debt by Sector

32 See Jagannathan, R., M. Kapoor and E. Schaumburg, “Why are We in a Recession? The FinancialCrisis is the Symptom Not the Disease,” NBER Working Paper No. W15404, 2009 [arguing that the coreproblems of the banking crisis are excess leverage that requires the deleveraging process manifest in arecession].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 28/82

Post-Depression Economics

- 28 -

Source: Fed Flow of Funds 2010

Fig. 10 shows the dramatic buildup of debt since 1990 in business, household, finance

and government sectors.

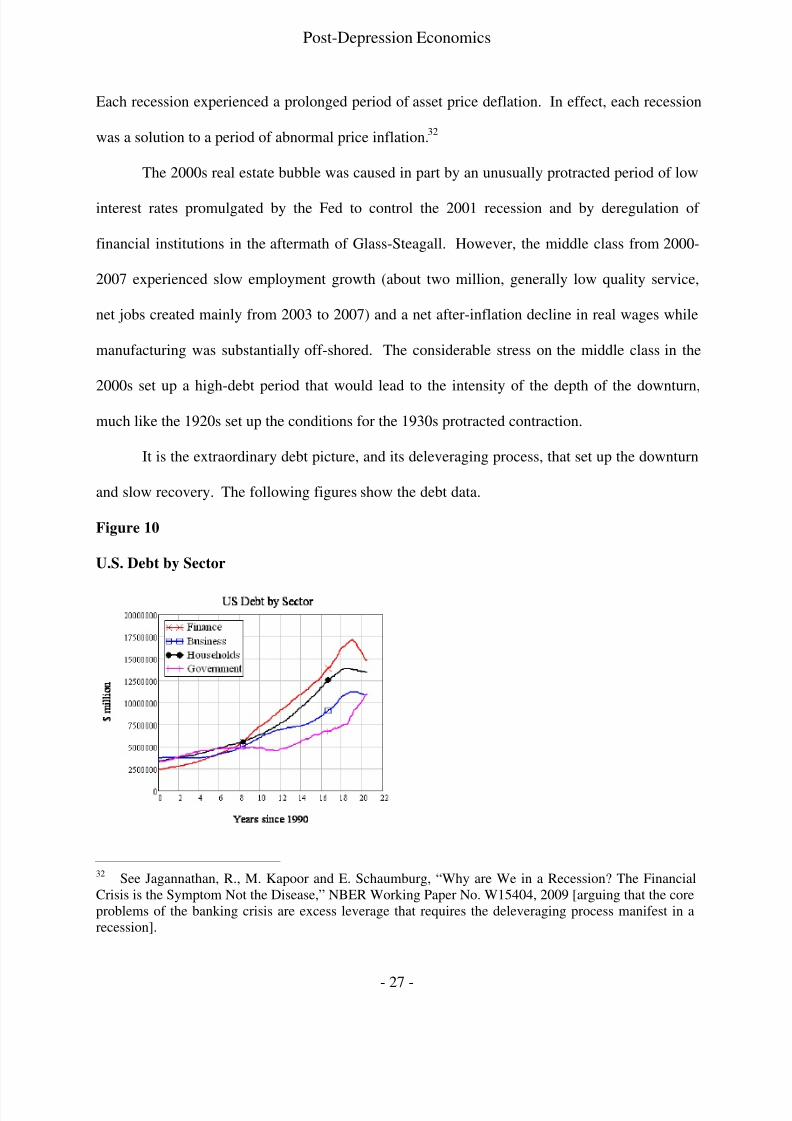

Figure 11

U.S. Gross Federal Debt as a Percentage of GDP

Figure 11 shows federal debt since WWII. The growth in federal debt is clear from 1981

to the present. The build-up of debt in the 1980s led to the deleveraging process in the 1990s.

The federal debt accumulated in the last few years is also non-trivial.

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 29/82

Post-Depression Economics

- 29 -

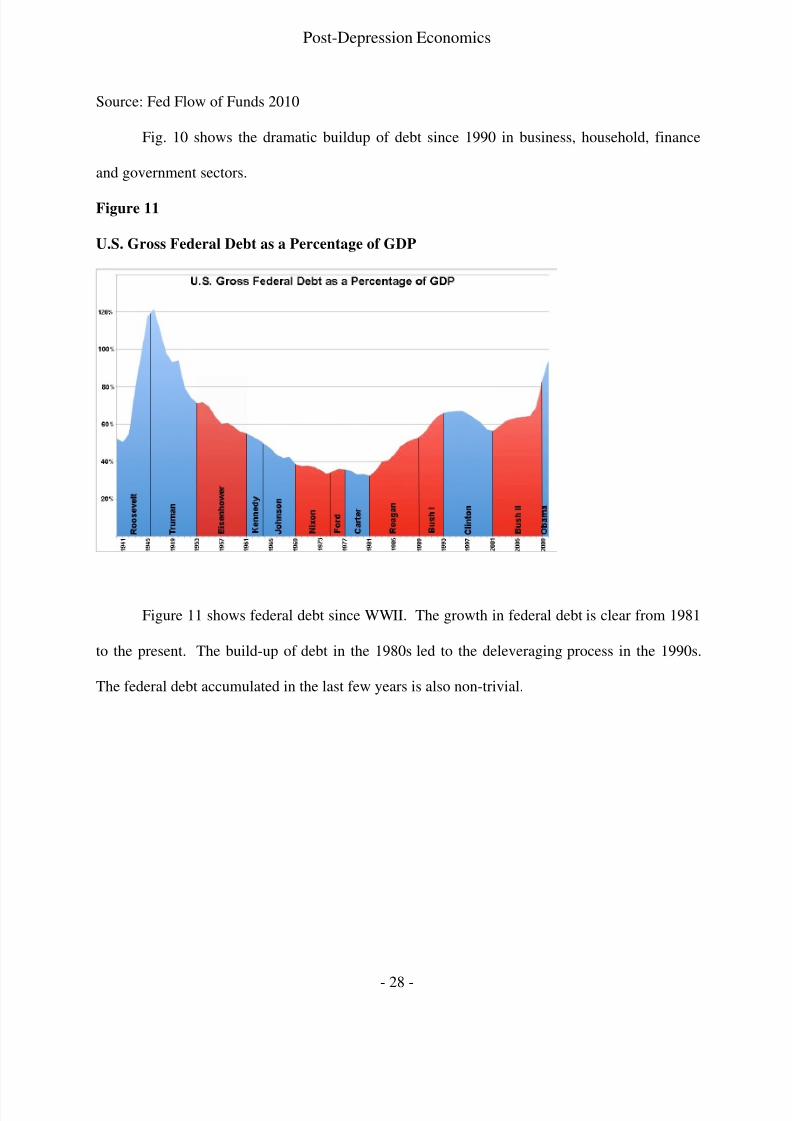

Figure 12

U.S. Debt and GDP 1990-2010

Source: Fed Flow of Funds 2010

Figures 12 shows private and public debt from 1990 to the present relative to GDP.

While the public debt is significant, the relative size of the private debt is alarming.

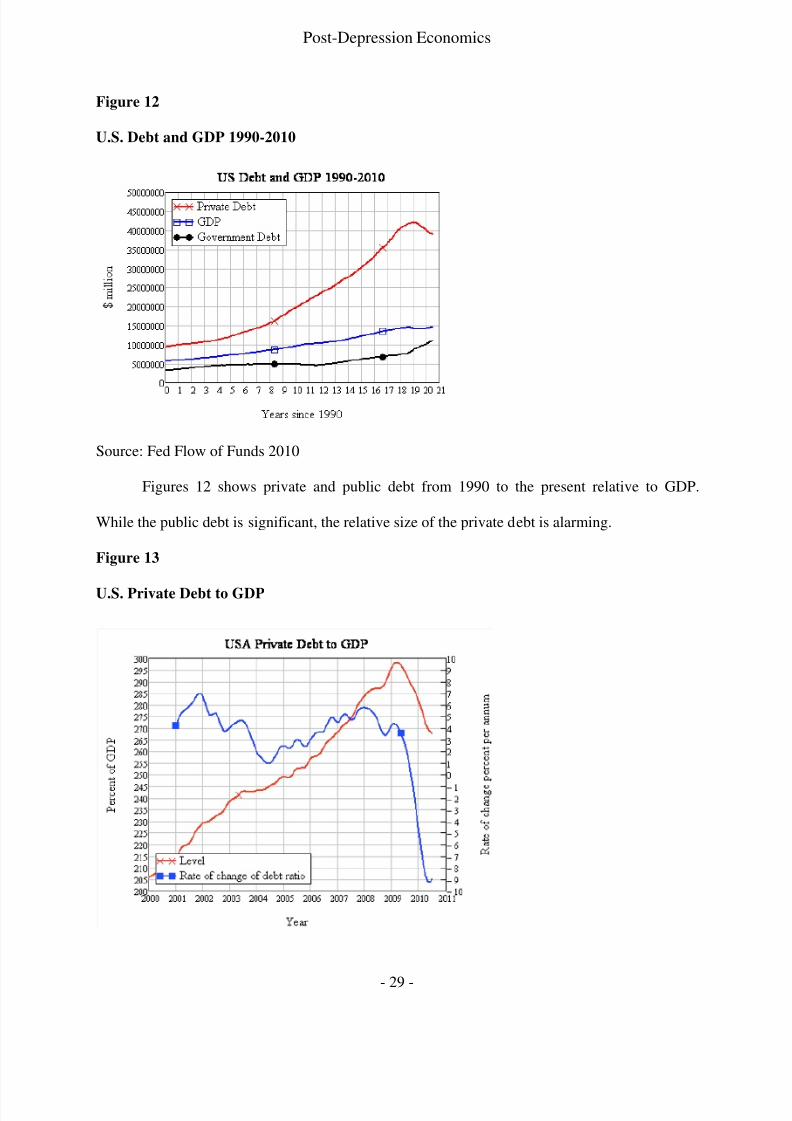

Figure 13

U.S. Private Debt to GDP

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 30/82

Post-Depression Economics

- 30 -

Source: Fed Flow of Funds 2010

Figure 13 shows the level of private debt relative to the change in debt. The drop in the

rate of change of debt ratio in the downturn is dramatic.

Figure 14

Correlation of Change in Debt and Unemployment

Source: Fed

The change of debt ratio, shown in figure 14, is correlated to the unemployment rate

change, showing the drop in demand that led to the dramatic increase of unemployment in the

downturn. It can be inferred from this correlation that the demand for goods was driven by debt.

This imbalance is also manifest in the U.S. trade deficits.33

33 Does the correlation of debt and employment imply that debt supports overconsumption and highemployment?

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 31/82

Post-Depression Economics

- 31 -

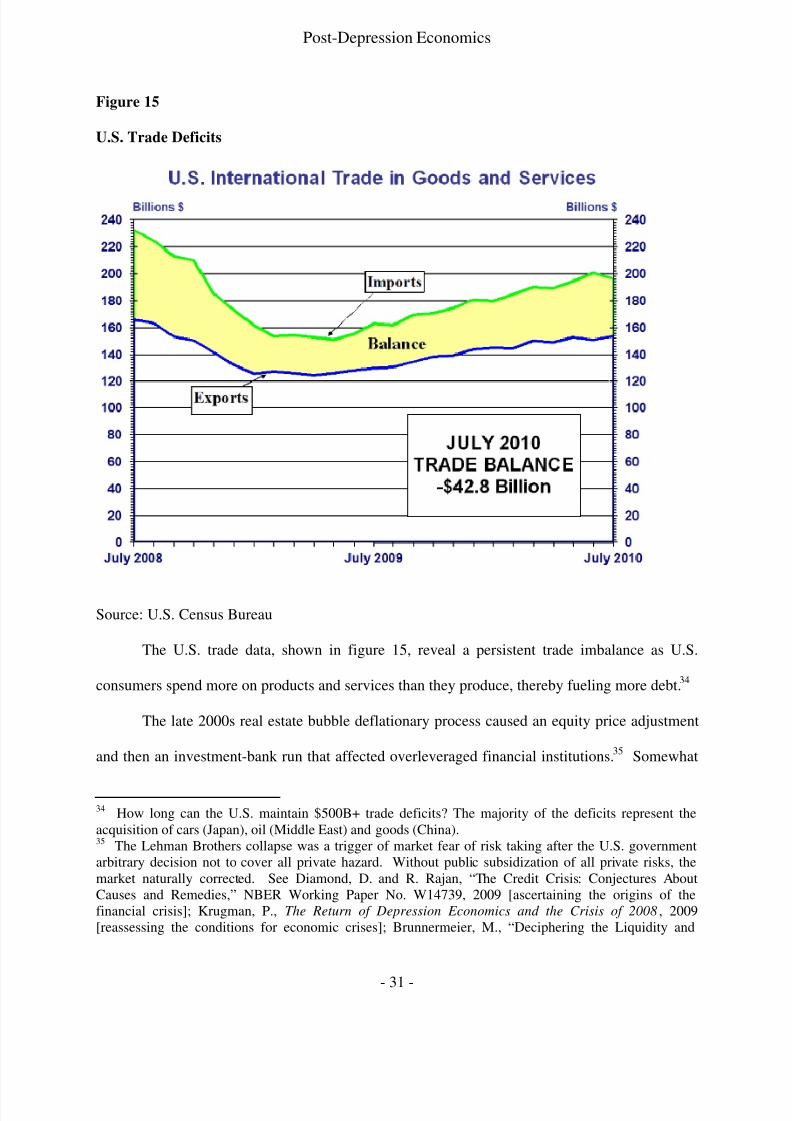

Figure 15

U.S. Trade Deficits

Source: U.S. Census Bureau

The U.S. trade data, shown in figure 15, reveal a persistent trade imbalance as U.S.

consumers spend more on products and services than they produce, thereby fueling more debt.34

The late 2000s real estate bubble deflationary process caused an equity price adjustment

and then an investment-bank run that affected overleveraged financial institutions.35 Somewhat

34 How long can the U.S. maintain $500B+ trade deficits? The majority of the deficits represent theacquisition of cars (Japan), oil (Middle East) and goods (China).35 The Lehman Brothers collapse was a trigger of market fear of risk taking after the U.S. governmentarbitrary decision not to cover all private hazard. Without public subsidization of all private risks, themarket naturally corrected. See Diamond, D. and R. Rajan, “The Credit Crisis: Conjectures AboutCauses and Remedies,” NBER Working Paper No. W14739, 2009 [ascertaining the origins of thefinancial crisis]; Krugman, P., The Return of Depression Economics and the Crisis of 2008, 2009[reassessing the conditions for economic crises]; Brunnermeier, M., “Deciphering the Liquidity and

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 32/82

Post-Depression Economics

- 32 -

reminiscent of the 1930s, the restructuring of the financial industry that began to occur in 2008

was a key factor in setting up the slow deleveraging process of the depression. For example, if

the banks were allowed to write off more of their real estate debts, the system would have likely

deleveraged debt far more quickly than it has. However, with a substantial amount of debt on

the books of businesses and consumers, and with a persistent deflationary real estate

environment in which millions of houses and commercial buildings were foreclosed, the

deleveraging process is more protracted than it would have been if the bank debts were

substantially written off in 2008.36

The Troubled Asset Relief Program (TARP) represented a political compromise in which

it was intolerable to rapidly write off public debt. The choice to slowly write off mortgage

related debt produced the present protracted deleveraging process. This political decision has

had, and will continue to have, significant ramifications akin to the Japanese lost decade in

Credit Crunch 2007-08,” NBER Working Paper No. W14612, 2008 [describing the credit crisis as aliquidity crisis]; Calomiris, C., “Banking Crises and the Rules of the Game,” NBER Working Paper No.W15403, 2009 [showing how banking policies change during banking crises]; Cassidy, J., How Markets

Fail: The Logic of Economic Calamities, 2009 [describing patterns of economic crises]; Rothbard, M., America’s Great Depression, 2005 [describing the economic policies responding to the conditions of theDepression]; Krugman, P., The Great Unraveling: Losing Our Way in the New Century, 2004 [arguingthat libertarian economic policies promote too much debt that eventually is deleveraged in an economicdownturn]; Cole, H. and L. Ohanian, “The U.S. and U.K. Great Depressions Through the Lens of Neoclassical Growth Theory,” American Economic Rev., 2002 [study of two nations’ remedies to theDepression]; Chancellor, E., Devil Take the Hindmost: A History of Financial Speculation, 2000 [historyof economic bubbles and recessions showing common patterns of financial speculation]; Garber, P.,

Famous First Bubbles: The Fundamentals of Early Manias, 2000 [history of economic crises from theSouth Sea bubble to the 21st century]; Romer, C., “The Great Crash and the Onset of the Depression,” The

Quarterly J. of Economics, 1990 [showing the 1929 stock market crash as a destabilizing event thatprecipitated the Depression] and; McElvaine, R., The Great Depression: America, 1929-1941, 1983[economic history of the Depression].36 See Krugman, P., “Financing Vs. Forgiving a Debt Overhang,” NBER Working paper No. W2486,1989 [presenting different arguments for policies to accelerate debt losses to promote rapid economicrecovery] and; Kessler, A., “TARP and the Continuing Problem of Toxic Assets,” WSJ, 2010 [describingthe monetary causes of the financial crisis and showing that the deleveraging process originated in TARPpolicy decisions].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 33/82

Post-Depression Economics

- 33 -

which banks refused to write down real estate debt and suffered average annual real estate price

declines of 5% from 1990 to 2005.37

If we are in a protracted economic depression, we may not have definitive information

for another several years about persistent price declines. In other words, we may not have

enough data to determine whether we are in a more substantial depression or stagnation period at

the present time, akin to only seeing the first two to three years of the Great Depression. But if

we are in a protracted depression, the federal government and Fed stimulus policy are limited to

modulate the economy going forward, thereby complicating economic development.38

The argument that a steep downturn leads to a strong recovery – which has been the

general rule in post-war recessions – has not been actualized in the present period. For the most

part, the rate of debt liquidation appears to determine the rate of recovery. In effect, a sharp

contraction is the cure for the mania of the 2000s, wherein a deleveraging period is required to

re-equilibrate the economy.39

But the 2007-9 contraction period, like the periods of 1929-32 and the early 1990s, also

witnessed financial industry crises. In the current period, the financial industry is constraining

credit and thereby perpetuating the duration of the deleveraging process.40

This financial

37 See Schularick, M. and A. Taylor, “Credit Booms Gone Bust: Monetary Policy, Leverage Cycles, andFinancial Crises, 1870-2008,” NBER Working Paper No. 15512, 2010 [describing the history of post-Civil War economic cycles from a perspective of monetary policy]; Taylor, J., “The Financial Crisis andthe Policy Responses: An Empirical Analysis of What Went Wrong,” NBER Working Paper No.W14631, 2009 [an anatomy of policy options to solve the financial crisis]; Taylor, J. and J. Williams, “A

Black Swan In the Money Market,” NBER Working Paper No. W13943, 2008 [arguing that the smallprobability of catastrophe was not adequately measured in monetary risk analyses] and; Whalen, R., “TheSubprime Crisis: Cause, Effect and Consequences,” Networks Financial Institute Policy Brief No. 2008-PB-04, 2008 [analysis of the sub-prime mortgage market as a key cause of the financial crisis].38 See Mishkin, F., “Is Monetary Policy Effective During Financial Crises?,” NBER Working Paper No.W14678, 2009 [arguing the limits of monetarism particularly when it is needed most].39 See Minsky, H., Stabilizing an Unstable Economy, 1986 [showing the policy choices in economiccrises with a particular focus on monetary institutions].40 See Ivanshina, V. and D. Scharfstein, “Bank Lending During the Financial Crisis of 2008,” EFA 2009Bergen Meetings Paper, 2009 [showing the transformation of bank lending as the crisis evolved].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 34/82

Post-Depression Economics

- 34 -

industry crisis was exacerbated by the extreme and rapid concentration of the industry in 2008.

In other words, while housing is a drag on the economy, the financial industry has limited credit

at the precise time that consumers need credit to sustain economic growth. Substantial evidence

shows that limited consumer and business lending created by the banking sector is stifling the

recovery.

Furthermore, the correlation between high unemployment data and a very soft housing

market suggests a negative feedback loop that will be particularly slow to change in the next few

years. The unemployment rate needs to come down substantially before consumers buy homes,

consumers need to buy homes before prices stabilize and prices need to stabilize before

economic growth will continue so as to bring the U.S. out of a protracted downturn.

While the technical factors show a severe contraction from 2007-9 from which the U.S. is

slowly recovering, some positive data reflect the successful performance of industrial

corporations. After a decline of corporate profits in 2008-9 of about thirteen percent, the profits

of large corporations have been robust in 2009-10. Unique factors that pertain to the increased

industrial globalization and concentration of American corporations in the 2000s have allowed

them to maintain robust profits in the aftermath of the downturn. Many industries, including

energy, finance, technology, communications and pharmaceutical, are oligopolously configured,

and consequently enjoy substantial monopoly profits. Therefore, while much of the U.S. is

experiencing a substantial downturn, including record post-war aggregate unemployment,

corporate profits in several industries have been excellent. Rarely in history have these

industries seen more highly valued corporations combined with record profits. Although the

extreme concentration of industrial organization is a result of decades of lax antitrust regulation,

the success of large corporations is contrasted to the performance of small and mid-sized

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 35/82

Post-Depression Economics

- 35 -

businesses. This extreme industrial stratification41 in the 2000s has similarities to the period of

the 1890s to 1920s of U.S. industrial development.42

It is this lack of government regulation that provides a similarity of the 2000s to the

1920s and suggests there is little the government can do to mitigate the depth of the downturn at

the present time. The theory that we are in a shallow depression similar to those in the 19th

century follows the view that the U.S. government did little to prevent 19 th century recessions

because of industry structure constraints and limited potential government stimuli.43

The prevailing logic is that Keynesian44 economic stimulus would add to the already

absorbitant deficits and restrict further stimulus actions. In other words, there is a perception

that, politically, there is little that the government can do to deal with the depth of the economic

downturn. Both the federal government and the Fed simply have no ammunition left in their

economic arsenal to stimulate the economy. This is particularly problematic if an exogenous

event occurs that plunges the economy into a new stage of decline, such as another Middle-

Eastern crisis.

According to the prevailing economic theory, then, the contraction occurred from 2007 to

2009 and could be mapped by “catastrophe” mathematical theory, while the technical “recovery”

began in mid-2009 and continues at a relatively slow pace. However, the data also seem to show

that a more substantial depression may be occurring in which the shallow depression of 2007-9

41 See Williamson, O., The Economic Institutions of Capitalism, 1998 [showing the market hierarchy of

industrial organizations] and; Williamson, O., Markets and Hierarchies: Analysis and Antitrust Implications, 1983 [showing how markets organize and evolve].42 See Porter, G., The Rise of Big Business, 1860-1920, 2006 [mapping the growth of corporations fromthe Civil War to the Progressive period] and; Prechel, H., Big Business and the State: Historical

Transitions and Corporate Transformation, 1880s to 1990s, 2000 [showing the complex relations of government and big business over the 20th century].43 This extreme industrial stratification is related to the increased, even symbiotic, relations of bigbusiness and the federal government in the 2000s.44 See Keynes, J., The General Theory of Employment, Interest and Money, 1936 [the classic economicwork arguing for activist government policy during economic crisis periods].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 36/82

Post-Depression Economics

- 36 -

was merely the first component of a longer process, particularly when factoring in the period of

unusually high unemployment rates or the duration of a return to the point of peak net worth or

potential economic growth.

While post-war recessions have shown similar patterns, the recent depression and

aftermath are substantially different in depth and duration. This time it was different.

Causes and Consequences of the Depression

There are several causes of the depression. In general, the core of the problem is

diminished demand from consumers. The source of diminished consumer demand is the housing

contraction caused by the bursting of the housing bubble in 2007. The economic downturn was

complicated by the financial crisis in 2008, which was promulgated by over-leverage, poor risk

management, short-term incentives and limited oversight. The financial crisis was a debt crisis

that moved from a U.S. consumer housing crisis to a European sovereign debt crisis. With

substantially diminished consumer demand, industrial capacity dropped and, with it,

employment. In general, consumers stopped buying goods financed by borrowing from the

inflating value of their homes.45

There are several causes of the prolonged downturn after the initial debt crisis. These

include (a) a liquidity crisis, (b) a deleveraging process and (c) a savings paradox. Many

businesses require capital flows that were interrupted by the financial crisis in 2008. With

diminished access to capital, many businesses were adversely affected by the downturn, which

was protracted as banks moved from an overt liberal strategy to an overt conservative strategy

during the downturn. Since capital flows were constrained, high debt worked through the

45 See Phelps, E., Structural Slumps: The Modern Equilibrium Theory of Unemployment, Interest, and

Assets, 1998 [dialectically discussing advantages and limits of various macroeconomic schools].

8/2/2019 Post Depression Economics

http://slidepdf.com/reader/full/post-depression-economics 37/82

Post-Depression Economics

- 37 -

system. Because about 75% of jobs are created by small business, the challenges of business

entrants are especially prominent in a downturn. Particularly with constrained access to capital

and relatively higher energy and health care costs, small businesses are disincentivized to grow

and hire workers. High relative debt requires a period of time to deleverage, which is

detrimental to stable business and consumer activity. While consumers had too much debt prior

to the downturn – in fact, a record negative savings rate – they are now saving relatively too

much. With too much savings, consumers are not spending as much on goods, which further

prolongs the recovery.46 The sum of these factors suggests that the downturn’s contraction

period was complicated by debt deleveraging aspects more typical in economic depressions.

47

While some have argued that increased class stratification has caused the crisis,48 I argue

that class stratification is a consequence of a set of economic events rather than its cause. One

can argue that when 1% of the population has 23% of income (and .1% with 11%) the economy