JULY 2018 This publication was produced for review by the United States Agency for International Development/Ghana mission by The Palladium Group. POSITIONING GHANA AS A FINANCIAL SERVICES HUB JULY 2018 FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

JULY 2018

This publication was produced for review by the United States Agency for International

Development/Ghana mission by The Palladium Group.

POSITIONING GHANA AS A FINANCIAL

SERVICES HUB

JULY 2018

FINANCING GHANAIAN AGRICULTURE PROJECT

(USAID FinGAP)

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

POSITIONING GHANA AS A FINANCIAL

SERVICES HUB

JULY 2018

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

i | P a g e

CONTENTS ACRONYMS & ABBREVIATIONS ii

EXECUTIVE SUMMARY 1

1 REPORT ON PROJECT MANAGEMENT 2

1.1 Project Duration 2

1.2 Project Team 2

1.3 Objective and Deliverables 3

2 REPORT ON RESEARCH 4

2.1 Key Benchmarks Used 4

2.2 International Benchmarks in the Development of an International Financial

Services Sector 4

2.3 Business Environment 4

2.4 Human Capital 10

2.5 Infrastructure 11

2.6 The Regional Environment 13

3 DRAFTING A FRAMEWORK FOR AN ACCRA INTERNATIONAL FINANCIAL

SERVICES CENTER: RECOMMENDATIONS 14

3.1 The Case for an “Enclave” Approach 14

3.2 Critical Enabling Factors in an Enclave 14

3.3 Strategic Partnerships with Other IFCS Crucial 15

3.4 Key Activities to Consider 15

4 CONCLUSIONS 16

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

ii | P a g e

ACRONYMS & ABBREVIATIONS

AIFMD Alternative Investment Fund Managers Directive

AU African Union

BoG Bank of Ghana

BOP Balance of Payments

CFC Casablanca Finance City

EU European Union

ECOWAS Economic Community of West African States

FDI Foreign Direct Investment

GDP Gross Domestic Product

ICT Information and communication technology

IFSC International Finance Services Center

IHQ International Headquarters

MOF Ministry of Finance

RHQ Regional Headquarters

SFZ Special Financial Zone

UCITS Undertakings for Collective Investment in Transferable Securities

USAID United States Agency for International Development

USAID FinGAP USAID Financing Ghanaian Agriculture Project

XDFDPC Xicheng District Financial Development Promotion Center

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

1 | P a g e

EXECUTIVE SUMMARY The USAID Financing Ghanaian Agriculture Project (USAID FinGAP) addresses a key constraint restricting

the development of commercial agriculture and food security in Ghana – access to finance necessary to

enable investment in agricultural value chains. USAID FinGAP has in the past four years used a

comprehensive approach to facilitate agriculture financing, including but not limited to engaging a broad

range of Ghanaian financial institutions (FIs) (e.g., banks, private equity firms, and investment funds) as well

as Business Advisory Service (BAS) providers, in partnership with strategic investors and buyers of maize,

rice, and soy in the north of Ghana. USAID FinGAP facilitates investment in the agriculture sector in

Ghana that complements Government of Ghana (GOG) and other donor programs aimed at expanding

commercial agriculture.

The President and Vice President of the Republic of Ghana have both expressed their vision of Ghana as

an African hub for financial services. The Ministry of Finance (MOF) has been tasked with coordinating

efforts to realize this vision and has established a taskforce to lead the endeavor.

In 2005, Ghana commenced an agenda to develop an International Finance Services Center (IFSC). This

was inspired by the government’s agenda to strengthen its financial sector, explore the growing

opportunities of cheaper private sector based investments, and strategically entrench Ghana’s role as the

gateway to Africa, especially the West African Sub region.

Initial implementation was focused on banking, which led to a passage of an Act of Parliament and licensing

of Barclays Bank of Ghana Limited to commence the maiden offshore banking service.

However, progress on the IFSC agenda stalled over time. In 2017, the government renewed its

commitment to establish a full fledge IFSC built on a “whole of Government” approach, as practiced in

Singapore, by 2019.

The Ministry has assembled a formidable taskforce of subject matter experts in various sectors of the

financial industry to provide input, insight and advisory on how best to achieve this goal per their points

of expertise. These industry leaders have generously offered their time to lead the running of a situation

analysis of the Financial Services sector in Ghana. This analysis will begin in context of other international

financial centers around the world such as Singapore, Hong Kong, Mauritius, London, New York and

Dubai. Their work will continue in a deep dive into the situation in Ghana and deliver operational and

policy framework recommendations to deliver real results.

To support, chaperone, and curate the findings of this body, the Ministry additionally engaged the services

of two USAID FinGAP consultants (a lead and a junior) to guide and coordinate the research conducted

by the subject matter experts, as well as conduct specific research to support these experts in the task

force, and finally guide the specific market and communication themes under which the research is collated

and presented. The consultants’ curation of the findings will be used as input for the preparation of a

strategic document with the goal of establishing a regional financial hub in Ghana. This hub will be a

preferred regional destination for operations within the banking, asset management, capital markets,

insurance, and financial technology spaces.

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

2 | P a g e

1 REPORT ON PROJECT MANAGEMENT 1.1 PROJECT DURATION

The duration of the research and consultation activities was 7 weeks (approximately 30 working days),

commencing in April 2018 and ending in July 2018.

1.2 PROJECT TEAM

The project team consisted of 2 consultants, assisted by an integrated task force from the Ministry of

Finance and related industry experts.

1.2.1 USAID FINGAP TEAM

Lead Consultant

Junior/Research Consultant

1.2.2 TASK FORCE MEMBERS

1. Joyce Awuku Darko Osei - Technical Advisor - Ministry of Finance

2. Dr. Sam Mensah - Advisor

3. Patience Akyianu - Lead expert on Banking

4. Keli Gadzepko - Lead expert on Insurance

5. Rev. Daniel Ogbarmey Tetteh - Lead expert on capital markets

6. Mr. Albert Essien - Advisor

7. Solomon - Ministry of Finance

1.2.3 TASK FORCE AND PROJECT RESEARCH STRUCTURE

Meghan.Gillis

Text Box

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

3 | P a g e

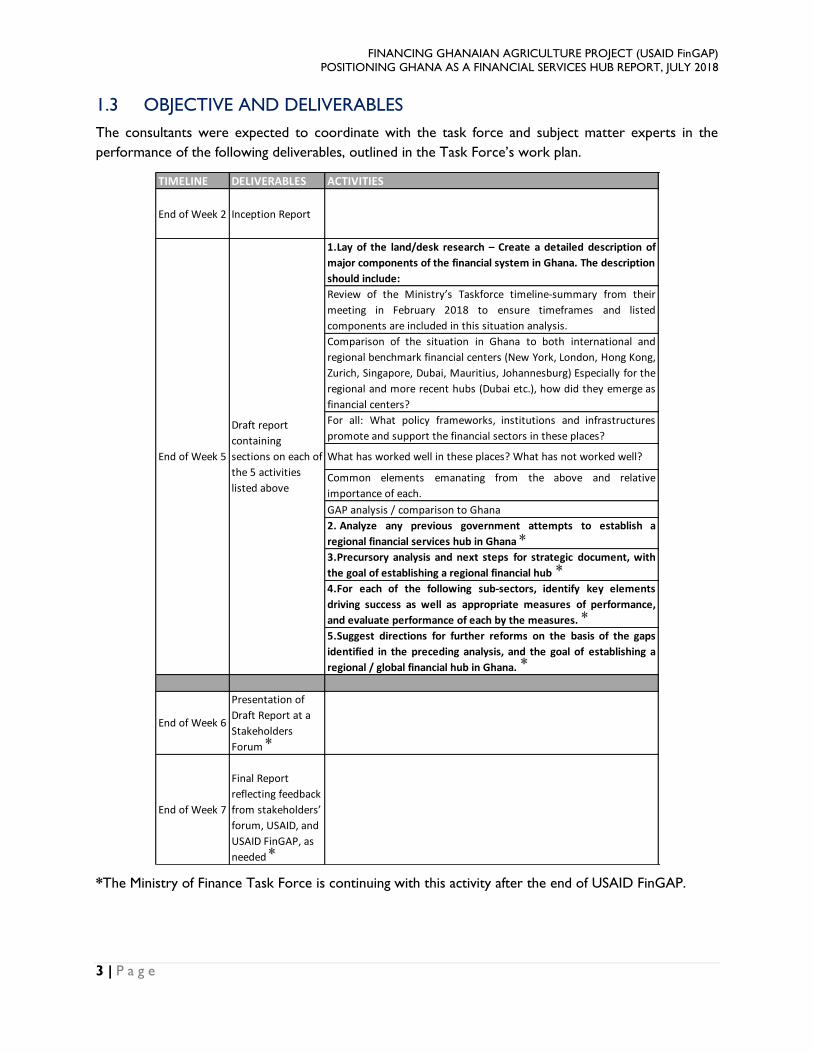

1.3 OBJECTIVE AND DELIVERABLES

The consultants were expected to coordinate with the task force and subject matter experts in the

performance of the following deliverables, outlined in the Task Force’s work plan.

*The Ministry of Finance Task Force is continuing with this activity after the end of USAID FinGAP.

TIMELINE DELIVERABLES ACTIVITIES COMMENT

End of Week 2 Inception Report Done prior to MoU with

FINGAP. Hence activity

was not repeated.

1.Lay of the land/desk research – Create a detailed description of

major components of the financial system in Ghana. The description

should include:

Review of the Ministry’s Taskforce timeline-summary from their

meeting in February 2018 to ensure timeframes and listed

components are included in this situation analysis.

Done

Comparison of the situation in Ghana to both international and

regional benchmark financial centers (New York, London, Hong Kong,

Zurich, Singapore, Dubai, Mauritius, Johannesburg) Especially for the

regional and more recent hubs (Dubai etc.), how did they emerge as

financial centers?

Done

For all: What policy frameworks, institutions and infrastructures

promote and support the financial sectors in these places?Done

What has worked well in these places? What has not worked well? Done

Common elements emanating from the above and relative

importance of each.Done

GAP analysis / comparison to Ghana Done

2. Analyze any previous government attempts to establish a

regional financial services hub in Ghana Not done

3.Precursory analysis and next steps for strategic document, with

the goal of establishing a regional financial hub Not done

4.For each of the following sub-sectors, identify key elements

driving success as well as appropriate measures of performance,

and evaluate performance of each by the measures.

On going

5.Suggest directions for further reforms on the basis of the gaps

identified in the preceding analysis, and the goal of establishing a

regional / global financial hub in Ghana.

On going - not

completed for all sub

sections

End of Week 6

Presentation of

Draft Report at a

Stakeholders

Forum

Not done

End of Week 7

Final Report

reflecting feedback

from stakeholders’

forum, USAID, and

USAID FinGAP, as

needed

Not done

End of Week 5

Draft report

containing

sections on each of

the 5 activities

listed above

*

*

*

*

*

*

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

4 | P a g e

2 REPORT ON RESEARCH 2.1 KEY BENCHMARKS USED

The consultants examined other IFSCs during their analysis of Ghana’s potential, which include:

Luxembourg

Singapore

Casablanca

Dubai

Qatar

Busan

Kuala Lumpur

Hong Kong

Mauritius

2.2 INTERNATIONAL BENCHMARKS IN THE DEVELOPMENT OF AN

INTERNATIONAL FINANCIAL SERVICES SECTOR

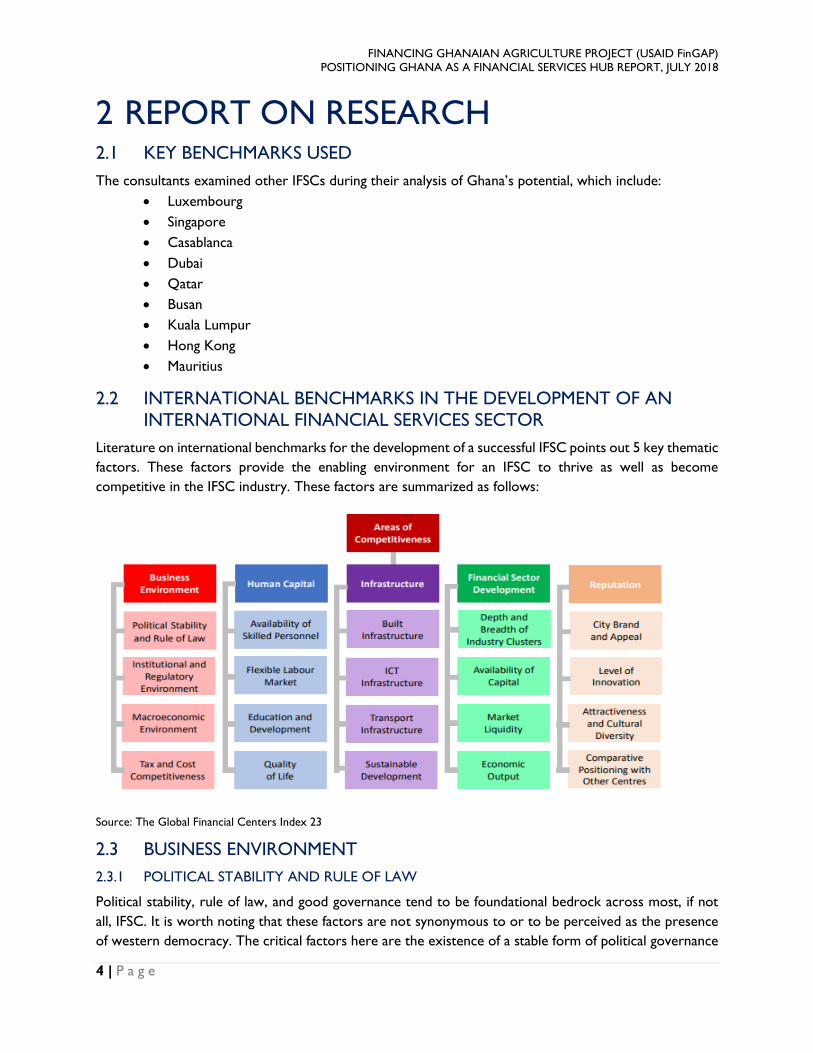

Literature on international benchmarks for the development of a successful IFSC points out 5 key thematic

factors. These factors provide the enabling environment for an IFSC to thrive as well as become

competitive in the IFSC industry. These factors are summarized as follows:

Source: The Global Financial Centers Index 23

2.3 BUSINESS ENVIRONMENT

2.3.1 POLITICAL STABILITY AND RULE OF LAW

Political stability, rule of law, and good governance tend to be foundational bedrock across most, if not

all, IFSC. It is worth noting that these factors are not synonymous to or to be perceived as the presence

of western democracy. The critical factors here are the existence of a stable form of political governance

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

5 | P a g e

which safeguards the existence and continuity of other factors needed for the development of an IFSC.

Hence a cursory overview of successful IFSC will indicate different political systems - including democratic

governments, authoritarian, and monarchies.

The common denominator is political stability, which does not interfere with or disrupt the functioning

of the IFSC. Successive governments in Mauritius have committed to safeguarding pro-business policies

and projects which supports international business. Hence they have been rated number one on the Mo

Ibrahim African Index of good governance for several years.

Secondly, political stability is not limited to domestic stability but stability in relations between the host

country and other key markets in the host region and the global political landscape. A cornerstone factor

for Luxemburg’s success as an IFSC has been its success at building its strategic geographical location, with

active engagement in and collaboration through European Union (EU) politics. On the other hand, the

recent Brexit vote presents a major challenge to the London IFSC. Also, the recent interest of Morocco

to join the Economic Community of West African States (ECOWAS) and rejoin the African Union (AU)

underpins the importance of political stability between the host country and relevant markets.

Rule of law refers to the assurance of justice and security in the domestic financial service markets that

are transparent and effective to both local and international investors. In particular, financial laws that

safeguard the financial interests of investors in relations to their invested financial assets are important. A

common practice across a number of IFSCs is to create a separate judiciary system, independent of the

domestic system. One example is the Dubai International Financial Services Center. Nonetheless, the

presence of an appreciable perception of the rule of law in the domestic environment cannot be

underestimated.

CURRENT STATUS

Ghana’s political environment is the most stable in West Africa and among the leading stable environments

in the African region with demonstrated commitment to pro-business initiatives by successive

governments. Also the country has enjoyed stability in geo political relations within the West African sub

region and Africa in general. Key highlights include:

Approximately 26 years of uninterrupted democratic rule, one of the longest in sub-Saharan

Africa;

5 democratically elected presidents since 1992;

3 successful presidential transitions between political parties in the 4th republic;

Ranked number 1 on rule of law in Africa1 in the Global Rule of Law Ranking;

Ranked number 2 in West Africa on Global peace index, which measures level of safety, the

extent of conflicts and the degree of militarization;

An independent and well-structured Judiciary system with Commercial and Human Rights

Courts;

Legal system based on the English law, which is highly regarded globally.

1 World Justice Report 2017; Global Rule of Law Ranking

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

6 | P a g e

However, a major gap in Ghana’s political stability in relation to an IFSC is the partisan approach on

national development. This has led to inconsistencies in the continuation of policies and programs with

changes in government. This challenge was reflected in the discontinuity of the previous project with the

change in government in 2008. Hence a renewed commitment to the IFSC should safeguard the continuity

of the agenda either through a bipartisan approach or an Act of Parliament.

2.3.2 INSTITUTIONAL, LEGAL AND REGULATORY ENVIRONMENT

There are two main models for the institutional, legal, and regulatory frameworks of IFSC:

The first model includes first generation legacy hubs which were developed as a by-product of a

city’s preeminence and inherent advantage in the global economy. They are anchored by significant

international home-based financial firms and have a natural gravitational pull in global finance and

commerce. Examples include the New York and London financial hubs. This type of system usually

does not have a deliberate IFSC policy, nor separate legal or regulatory frameworks.

The second model includes second generation IFSCs which make a deliberate effort to replicate

the first generation hubs. They may not have comparable inherent advantages, per se, including

the endowment of a critical mass of large home-based global players; hence, they create deliberate

policy incentives through institutional, legal, and regulatory frameworks to attract foreign firms

and investors. As a result, they make very conscious efforts in regulation or incentives to attract

foreign investors. Examples include Dubai, Luxembourg, and Mauritius, which have all influenced

their institutional, legal, and regulatory frameworks.

The hubs described by the first model are usually characterized by a single domestic legal and regulatory

environment, with regulation usually undertaken by multi-tiered and highly complex Self-Regulatory

Organizations. The latter model, on the other hand, are characterized by distinct institutional, legal, and

regulatory frameworks which are designed to increase the hub’s competitiveness on the global market.

Since these usually tend to be replicated centers, devoid of a default creation as a by-product of a city’s

inherent advantage, they are usually created through an Act of law, defining its legal entity, operating

structures and regulatory framework. The execution of the Act is undertaken by a legal entity, either a

private company limited by guarantee or a Public Private Partnership model. This entity is usually an

Authority with the objective to oversee the day-to-day administrative management of the IFSC, developing

its competitiveness and marketing it globally. This is followed by a regulatory structure that manages the

regulatory requirements of the IFSC.

Some advanced second generation IFSCs such as Dubai and Astana have added a layer of a distinct conflict

resolution framework made up of separate court and arbitration systems. This independent framework is

based on the English Common Law, which is a preferred global standard. There are also some second

generation IFSCs such as Casablanca whose IFSC is regulated by the domestic regulatory framework.

Nonetheless, it is worth noting that the recent global financial crises, coupled with increased competition

from emerging IFSCs, is driving reforms within the first generation hubs. An emerging trend, especially

with markets aligned with the British jurisdiction is adopting and adapting the “twin peaks” model in

financial sector regulation. Examples include London and cities in Australia, Canada, and South Africa. This

presents a shift from self-regulatory organizations to a coherent single regulator which will minimize if not

remove duplications, gaps, and inconsistencies characteristic of the old system. Regulation is shared among

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

7 | P a g e

two regulatory authorities focused on ensuring consumer protection and market stability, to combat

money laundering and promote open and transparent markets.

The twin peaks consist of a Prudential Regulation Authority, which falls under the Central Bank and

a Financial Conduct Authority. The former focuses on promoting transparency and viability of the

firms to ensure market stability, whilst the latter regulates the conduct of the firms with a focus on

consumer protection. These reforms made to the domestic sector also cover the operations of their

embedded IFSC.

Beside these is a recent industry-driven regulatory set of standards developed either from best practices

or preemptive strategies. Notable among these are the Basel III protocol in banking, Alternative

Investment Fund Managers Directive (AIFMD), and UCITS (Undertakings for Collective Investment in

Transferable Securities). AIFMD regulates the alternative investment funds market to safeguard investor

protections, increase transparency for investors and regulators, and provide enhanced management of

systemic risks. UCITS has become a global standard for distributed investment fund products. AIFM and

UCITS are Luxembourg-inspired best practices.

CURRENT STATUS

The institutional, legal, and regulatory framework for an IFSC is presently underdeveloped. The regulatory

framework of the financial sector is largely via self-regulatory organizations such as Bank of Ghana,

Securities and Exchange Commission (SEC), National Insurance Commission (NIC), and the National

Pension Regulatory Authority (NPRA). Recent instability in the domestic banking sector casts a shadow

on regulatory efficiency in the financial sector.

The IFSC relevant regulation covers the offshore banking regulation developed as part of the initial attempt

at the development of the Accra International Finance Center in 2007, as well as the ongoing efforts of

the Central Bank transition towards Basel II and III. The recent directive by the Central Bank on new

Capital Requirements promises to consolidate and strengthen the domestic banking system in line with

the capital accord requirements of Basel II. Likewise, the recent regulation on deposit-taking presents a

framework to strengthen regulation.

2.3.3 MACRO-ECONOMIC ENVIRONMENT

A strong domestic macroeconomic environment is important for the growth of an IFSC. Essential variables

include low and stable inflation, stable and predictable foreign exchange regime, low interest rate, fiscal

discipline, stable economic growth, and a sustainable financial stability.

A robust and extensive domestic financial sector has also been pivotal in the development of first

generation and some emerging market hubs. The depth and capacity to serve as an anchor for the hub

and facilitate interactions with the rest of the global financial system is critical. This also leads to the

development of ancillary financial services which is an organic growth pattern for the IFSC.

On the other hand, developing countries which do not have well-developed financial sectors typically

create Special Financial Zones/Financial Free Zones that replicate the institutional infrastructure and

regulatory incentives of a strong advanced financial system.

Free capital mobility and full control over foreign currency assets by investors is critical to the

attractiveness of an IFSC. Capital controls are very limited and rare within advanced industrial economies

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

8 | P a g e

which normally host first generation hubs. However, developing economies which usually host second

generation hubs tend to have capital controls which are a challenge to the competitiveness of IFSCs. Hence

they incorporate free capital mobility and foreign currency assets within their Special Financial Zones

(SFZ). A major challenge is the need to manage interactions between the SFZ and the domestic economy.

CURRENT STATUS

Ghana’s lower middle income economy remains promising, albeit with some challenges. Its key

macroeconomic variables such as fiscal management, inflation, GDP, interest rates, foreign exchange rates

and balance of payments (BOP) have witnessed frequent fluctuations over the past decade, thus posing a

challenge on the stability of macroeconomic fundamentals, both in the short- and long-run. This makes it

difficult to forecast on the direction of the economy and or the likely actions the policy makers would

take.

Nonetheless, significant improvements in macro-economic management in recent years have positioned

Ghana among the fastest growing economies in the world in 2017. The World Bank credits the significant

improvement made in the macroeconomic environment in 2017 in comparison to preceding fiscal year.

Ghana’s fiscal deficit reduced to 6% of gross domestic product (GDP) in 2017 from 9.3% in 2016.2 The

economy expanded by 8.5% in 2017 compared to 3.6% the previous year, driven by the mining and oil

sectors.3 Adding to the list, the government has introduced interventions such as the digital address

system, paperless system at the port, compulsory tax identification number registration, and National

Identification system—all aimed at improving domestic revenue collection.

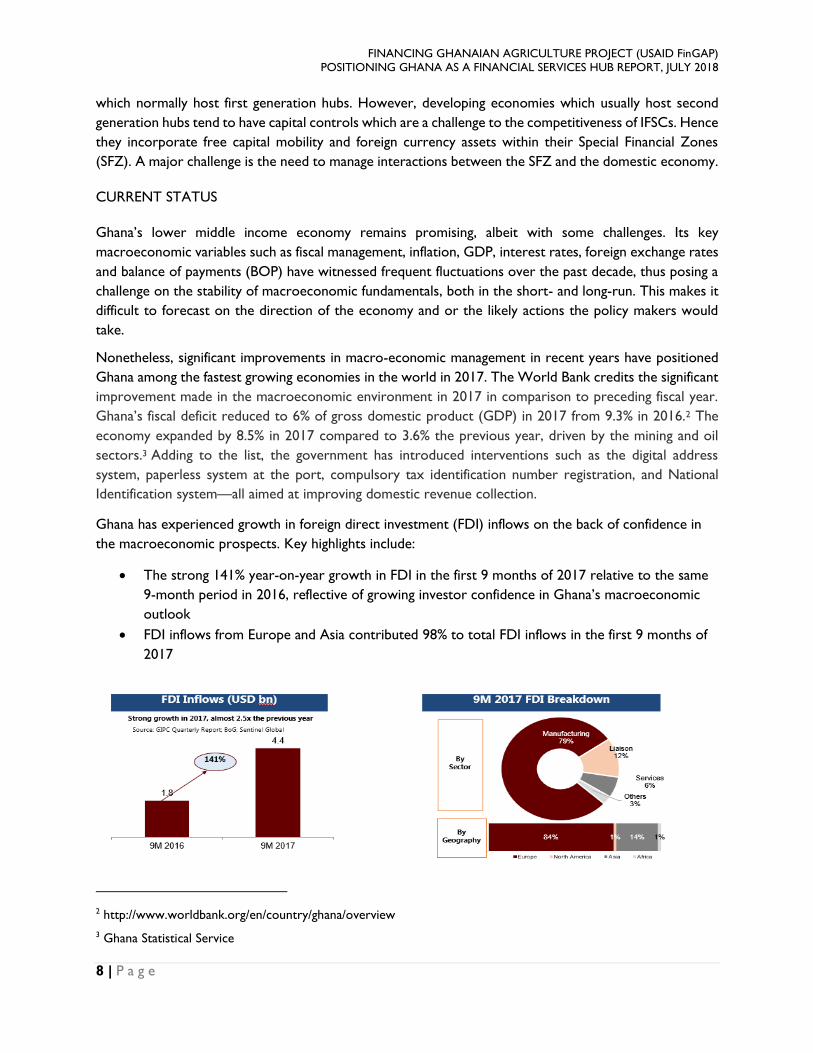

Ghana has experienced growth in foreign direct investment (FDI) inflows on the back of confidence in

the macroeconomic prospects. Key highlights include:

The strong 141% year-on-year growth in FDI in the first 9 months of 2017 relative to the same

9-month period in 2016, reflective of growing investor confidence in Ghana’s macroeconomic

outlook

FDI inflows from Europe and Asia contributed 98% to total FDI inflows in the first 9 months of

2017

2 http://www.worldbank.org/en/country/ghana/overview

3 Ghana Statistical Service

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

9 | P a g e

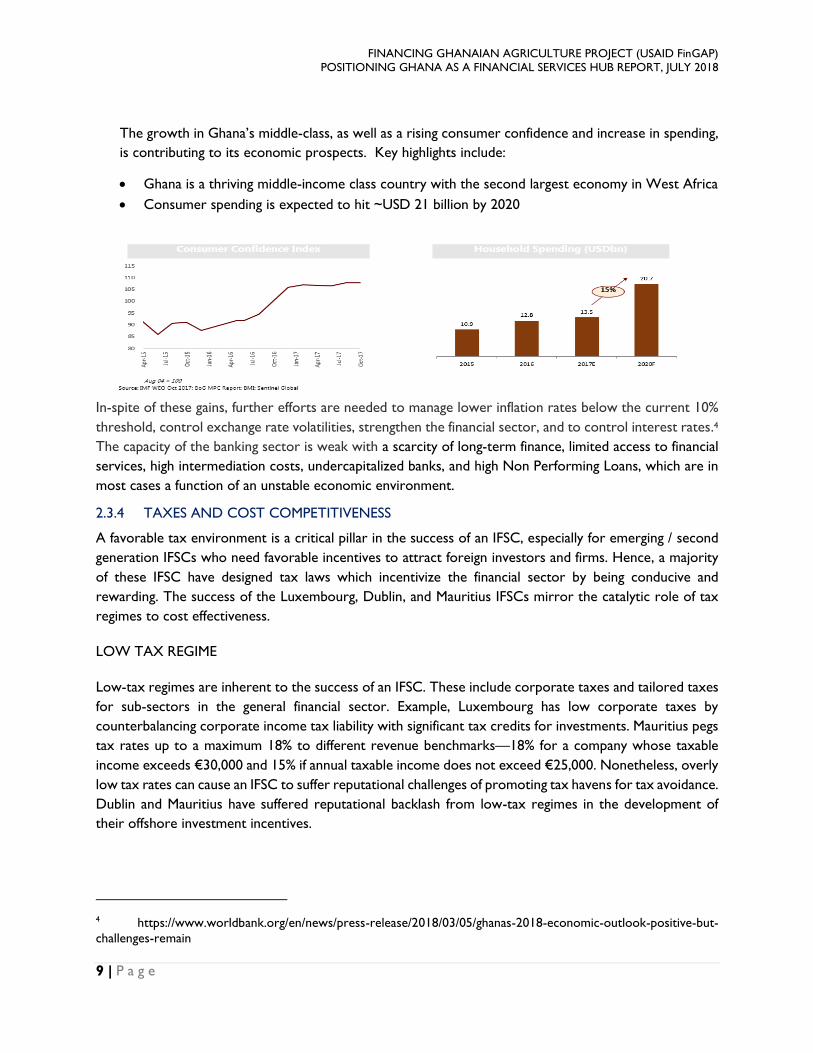

The growth in Ghana’s middle-class, as well as a rising consumer confidence and increase in spending,

is contributing to its economic prospects. Key highlights include:

Ghana is a thriving middle-income class country with the second largest economy in West Africa

Consumer spending is expected to hit ~USD 21 billion by 2020

In-spite of these gains, further efforts are needed to manage lower inflation rates below the current 10%

threshold, control exchange rate volatilities, strengthen the financial sector, and to control interest rates.4

The capacity of the banking sector is weak with a scarcity of long-term finance, limited access to financial

services, high intermediation costs, undercapitalized banks, and high Non Performing Loans, which are in

most cases a function of an unstable economic environment.

2.3.4 TAXES AND COST COMPETITIVENESS

A favorable tax environment is a critical pillar in the success of an IFSC, especially for emerging / second

generation IFSCs who need favorable incentives to attract foreign investors and firms. Hence, a majority

of these IFSC have designed tax laws which incentivize the financial sector by being conducive and

rewarding. The success of the Luxembourg, Dublin, and Mauritius IFSCs mirror the catalytic role of tax

regimes to cost effectiveness.

LOW TAX REGIME

Low-tax regimes are inherent to the success of an IFSC. These include corporate taxes and tailored taxes

for sub-sectors in the general financial sector. Example, Luxembourg has low corporate taxes by

counterbalancing corporate income tax liability with significant tax credits for investments. Mauritius pegs

tax rates up to a maximum 18% to different revenue benchmarks—18% for a company whose taxable

income exceeds €30,000 and 15% if annual taxable income does not exceed €25,000. Nonetheless, overly

low tax rates can cause an IFSC to suffer reputational challenges of promoting tax havens for tax avoidance.

Dublin and Mauritius have suffered reputational backlash from low-tax regimes in the development of

their offshore investment incentives.

4 https://www.worldbank.org/en/news/press-release/2018/03/05/ghanas-2018-economic-outlook-positive-but-

challenges-remain

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

10 | P a g e

DOUBLE TAXATION AVOIDANCE TREATIES

A double taxation treaty is a catalytic factor in driving foreign investments into emerging and second

generation hubs. The investor attraction strategy lies in the extensive double taxation avoidance treaties

it has with countries in different regions of the world. The number of agreements informs the growth and

direction of spread of the IFSC’s footprint across the globe. Luxembourg has over 60 double taxation

agreements, Singapore has 76, and Mauritius has over 30 agreements, hence attracting clients from all

these markets.

TAX CREDITS

Some IFSCs innovate with tax credits to drive foreign investments and new businesses. Luxembourg offers

tax credit as high as 13% of the increase in investment in depreciable assets gained in a year of assessment.

Also new businesses can enjoy tax exemptions of over 25% on corporate tax, and municipal business taxes

for profits made for a period of 8 to 10 years.

2.3.5 SPECIAL INCENTIVES FOR SPECIFIC FINANCIAL SERVICES

Some hubs also develop special incentives, relative to their product objectives to attract specific kinds of

clients. Singapore has special incentives to attract Regional Headquarters (RHQ) and International

Headquarters (IHQ). Companies with an RHQ in Singapore enjoy a 15% concessionary tax rate, while

companies with IHQ status enjoy lower rates between 0 to 10%.

Luxembourg has specific incentives for investment funds, financial participation companies, private wealth

management companies, securitization companies, venture capital vehicles, and financial services

companies. Investment funds are free from corporate income tax, municipal business tax, and withholding

tax on dividends. Private wealth management firms are exempt from taxation on income and net worth

tax reserve but pay a yearly subscription of 0.25% based on paid-up capital, share premium and excessive

debts. They also enjoy zero withholding tax on distributed dividends paid by non-resident private wealth

management companies on capital gains on shares. There are also specific regulations for banks, securities

depositories, insurance and reinsurance companies, and other financial service providers in establishing

taxable basis for corporate income tax. This includes neutralization of unrealized exchange gains, general

banking risk provision, provision for guarantee of deposits, mathematical reserves, and/or catastrophe

reserves.

CURRENT STATUS

Ghana’s tax regime does have some incentives aimed at attracting FDI, such as those imbedded in the

Free Zone Act. Also it has double taxation agreements with at least 11 countries. Lessons and best

practices here could serve as a guide in designing specific tax incentives for the Accra International

Financial Center.

2.4 HUMAN CAPITAL

Top-level skilled talent in economics, finance, banking, insurance (or actuarial), law, financial engineering,

information and communication technology (ICT), and relevant international languages is essential to the

success of an IFSC. This skilled workforce is normally generated by an ecosystem of top universities and

a vibrant domestic and regional financial sector providing both classroom and on-the-job training. In

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

11 | P a g e

countries with less vibrant ecosystems to generate such talent, flexible immigration policies targeted at

the IFSC have been a channel to attracting such talent.

This is a characteristic of emerging hubs which have to compete with the matured ecosystem of first

generation hubs for such talent. Example, the Casablanca Finance City has an immigration and residency

policy which allows visas within 73hrs, work permits in 3 days, and residency permits within 2 weeks.

Hubs within regional economic zones with free movement of people protocols enjoy high-skilled talent

from more advanced markets within the region. An example is Luxembourg which is benefiting from high-

level talent from advanced financial markets within the Eurozone without direct investment in training a

talent pool. There is also conscious effort by some centers to develop and attract such talent through

partnerships with universities to run IFSC relevant courses. This attracts students who move on to work

at the IFSC.

Closely related to this, is the quality of life of the city. This relates to cost of living and access to

international quality social amenities, including health services.

CURRENT STATUS

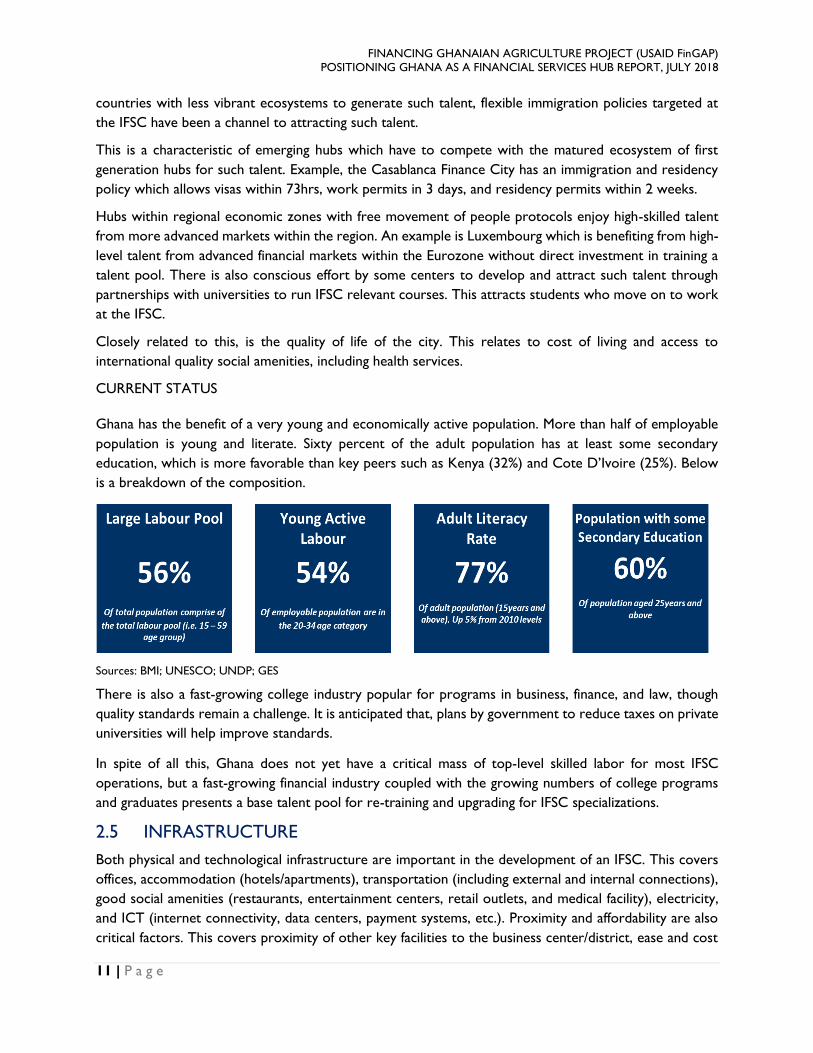

Ghana has the benefit of a very young and economically active population. More than half of employable

population is young and literate. Sixty percent of the adult population has at least some secondary

education, which is more favorable than key peers such as Kenya (32%) and Cote D’Ivoire (25%). Below

is a breakdown of the composition.

Sources: BMI; UNESCO; UNDP; GES

There is also a fast-growing college industry popular for programs in business, finance, and law, though

quality standards remain a challenge. It is anticipated that, plans by government to reduce taxes on private

universities will help improve standards.

In spite of all this, Ghana does not yet have a critical mass of top-level skilled labor for most IFSC

operations, but a fast-growing financial industry coupled with the growing numbers of college programs

and graduates presents a base talent pool for re-training and upgrading for IFSC specializations.

2.5 INFRASTRUCTURE

Both physical and technological infrastructure are important in the development of an IFSC. This covers

offices, accommodation (hotels/apartments), transportation (including external and internal connections),

good social amenities (restaurants, entertainment centers, retail outlets, and medical facility), electricity,

and ICT (internet connectivity, data centers, payment systems, etc.). Proximity and affordability are also

critical factors. This covers proximity of other key facilities to the business center/district, ease and cost

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

12 | P a g e

of connectivity to other regional/global hubs, efficient public transport, and the competitiveness of pricing

to other markets.

Emerging IFSC’s which may not have existing adequate level of infrastructure, opt for a dedicated enclave

facility with the entire needed infrastructure at international standards. This is usually a one-stop shop

financial city or space with facilities such as business centers, offices, data centers, restaurants,

hotels/apartments, entertainment centers, parks retail outlets/shopping centers, schools and medical

facilities. This can range from a few buildings to large tracts of land.

CURRENT STATUS

Currently Accra has one of the fastest growing business infrastructure developments in West Africa,

second to Lagos. There is substantial growth in private sector investments, in real estate and the hospitality

industry, leading to high-end housing and the presence of international hotel brands such as Kempinski,

Movenpick, Holiday Inn, Golden Tulip, Marriot, IBIS, and Best Western. But both hotels and prime housing

costs are too high by international standards. This presents a cost competitiveness challenge.

Ghana’s open skies policy has made Accra one of the most connected cities in the region with daily

flights/connecting flights to Europe, North America, Middle East, Asia, North Africa, Nigeria, Kenya, South

Africa, Cote D'Ivoire among others. The international airport is one of 5 US Federal Aviation Authority

Category One airports in Africa. The recently expanded airport terminals promise to enhance connectivity

in the near future.

The city has witnessed progressive improvements in internal transportation, which includes upgrading of

roads and modern taxi services, including Uber and Taxify. Traffic within the city remains a challenge to

ease of movement.

2.5.1 INVESTMENT IN ICT

Global financial transactions are predominately digital; hence, ICT and financial technology have become

critical enablers for IFSC. Thus in enhancing their competitiveness, IFSCs are investing in cutting-edge ICT

infrastructure and technology, including the development of robust Fintech industries.

Singapore is investing in the development of a ‘smart financial center’ initiative with an objective to improve

financial regulations, e-commerce, e-payment, cloud computing and digital content through digital

technologies. This will see developments in state-of-the-art data center infrastructure, high-speed internet

connectivity and the creation of ICT research centers in universities.

Likewise, Luxembourg launched digital ‘Letzebuerg’ in 2014—an agenda to develop telecom infrastructure

and support innovation and access to financing for Fintech start-ups. In 2017, it launched a house of

financial technology, to connect domestic and international Fintechs to consolidate it as a global leader in

financial technology.

CURRENT STATUS

Ghana’s ICT terrain is promising. Currently, there are three sub-marine cables providing relatively good

internet connectivity. The Accra Digital Center is being developed to host and incubate business

processing and outsourcing centers and Fintechs. The Fintech industry is developing, although it remains

quite under developed compared to peers, such as Nigeria and Kenya.

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

13 | P a g e

2.6 THE REGIONAL ENVIRONMENT

2018 GLOBAL FINANCIAL CENTERS INDEX RANKINGS

• Africa Leaders

– Casablanca – 32nd (international specialist)

– Johannesburg – 52nd (international diversified)

– Mauritius – 56th (local specialist)

• Associate IFSC

– Cape Town

– Nairobi

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

14 | P a g e

3 DRAFTING A FRAMEWORK FOR AN

ACCRA INTERNATIONAL FINANCIAL

SERVICES CENTER:

RECOMMENDATIONS 3.1 THE CASE FOR AN “ENCLAVE” APPROACH

All things being equal, Ghana should attain high marks in all 5 key indicators to be a competitive IFSC.

Currently, Ghana has a low competitiveness rating in most of these indicators. It will take substantial time

and resources for the country as a whole to improve its competitiveness across the board.

However, an enclave strategy allows Ghana a fast-track solution, by creating a special financial zone where

operating standards are at par with international competition, and that by-passes systemic problems in the

rest of the economy.

3.2 CRITICAL ENABLING FACTORS IN AN ENCLAVE

The emphasis is to focus on things that can be directly controlled. The following are the key factors for

Ghana:

BROADER COUNTRY-LEVEL:

– Political stability and rule of law

– Macroeconomic environment

ENCLAVE-SPECIFIC:

– Institutional and regulatory framework

– Infrastructure

– Human capital

SPECIALIZATION IS KEY

“IT SEEMS TO ME THAT MORE OF THE SMALLER CENTERS WOULD DO

BETTER BY SPECIALIZING IN ONE SECTOR. NOT EVERYONE CAN BE A

LONDON OR A NEW YORK.”

—ASSET MANAGER BASED IN MONTREAL, 2018 GFC INDEX

Emerging trends in the sector tend to avoid replicating or competing with established global IFSCs to

carve a niche with competitive advantage. Examples include Busan’s focus on marine finance and Kuala

Lumpur’s specialization in Islamic Finance.

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

15 | P a g e

It will be important for Ghana to identify a niche with competitive advantage that it can exploit for an

IFSC.

3.3 STRATEGIC PARTNERSHIPS WITH OTHER IFCS CRUCIAL

The market entry strategy should consider a marketing strategy where Ghana collaborates with other

global and regional IFSCs, feeding into and off their value chains. An example is the Casablanca Finance

City (CFC) which has entered into strategic partnerships with Luxembourg, Busan International Financial

City, Xicheng District Financial Development Promotion Center, among others.

It will be apt for Ghana to identify strategic relationships with Casablanca and Mauritius. Casablanca has

an objective to become a Regional Hub for North and West Africa. Its competitive positioning between

Europe and North America, coupled with other key factors, gives it a higher advantage in the sub region.

A strategic partnership with CFC could be considered for a less aggressive market entry.

3.4 KEY ACTIVITIES TO CONSIDER

1. Set up an institutional and regulatory action group with multi-ministerial representation,

supported with international experts, to develop a concise institutional and regulatory framework.

2. Secure an Act of Parliament to safeguard the project and designate an authority to oversee

implementation.

3. There is no need to fully develop the physical enclave before launching the IFSC. While a facility

is being developed, IFSC status firms can locate in any number of designated locations in

country/Accra.

4. Enact an interim law allowing firms to operate anywhere in country in the first few years while

the center is under construction (Dubai case, United Arab Emirates Financial Free Zones Law,

2004/Dubai International Finance Center Law 9).

5. Set up an estate management entity to facilitate the identification, negotiation and signing on of a

pool of business centers, hotels, apartments, offices and other related real estate and

infrastructure needs on behalf of clients. This could include tax breaks/incentives to real estate

providers for competitive pricing. This will ensure that, in the absence of a designated physical

enclave, clients would still have a single platform to access international standard facilities at

negotiated competitive rates. This could be done as a PPP vehicle, possibly with reputable global

IFSC estate developers or local real estate management company.

6. Leverage top rank position of “Doing Business Index” in West Africa for sub regional hub.

7. Though an improvement in Ghana’s rating will be good for broader country reputation, an enclave

model provides opportunity to directly provide these as part of offerings of the enclave,

independent from the domestic situation.

8. In the short-term, it will be necessary to import talent. This could begin with Ghanaian and African

Diaspora. Leverage Ghana's large expatriate community to attract international standard talent.

Develop an IFSC talent program in partnership with local universities/resident firms and other

partner IFSCs to train locals. Initiate a talent program in advance of launching the IFSC.

9. Build on the ongoing recapitalization of banks to support selected local banks to consolidate, build

capacity and spread across border within the sub region. This will help build a home grown

financial sector with regional spread.

FINANCING GHANAIAN AGRICULTURE PROJECT (USAID FinGAP)

POSITIONING GHANA AS A FINANCIAL SERVICES HUB REPORT, JULY 2018

16 | P a g e

4 CONCLUSIONS

The Ministry of Finance has taken steps towards achieving the vision of Ghana as an African hub for

financial services, or an International Finance Services Center (IFSC), through a taskforce comprised of

subject matter experts in various sectors of the financial industry to provide input, insight and advisory on

how best to achieve this goal per their points of expertise. The taskforce was supported by two USAID

FinGAP consultants.

To commence the assignment, the taskforce conducted a literature review on international benchmarks

for the development of a successful IFSC points out 5 key thematic factors. These factors provide the

enabling environment for an IFSC to thrive as well as become competitive in the IFSC industry. While

comparing Ghana with international financial centers around the world such as Singapore, Hong Kong,

Mauritius, London, New York and Dubai, the taskforce analysis concluded that currently, Ghana has a low

competitiveness rating in most of these indicators. It will take substantial time and resources for the

country as a whole to improve its competitiveness across the board.

However, they recommend an enclave strategy which would allow Ghana a fast-track solution by creating

a special financial zone where operating standards are at par with international competition, and that by-

passes systemic problems in the rest of the economy. The specific recommendations include establishing

strategic partnerships with other IFSCs and identifying a niche with competitive advantage that Ghana can

exploit for an IFSC.

These activities will strengthen Ghana’s financial sector, explore the growing opportunities of cheaper

private sector based investments, and strategically entrench Ghana’s role as the gateway to Africa,

especially the West African sub region.

Related Documents