1 A Portfolio of Pricing Options for Public Sector Cadastral Organisations Samwel Alananga-Sanga; School of Real Estate Studies; Ardhi University; Department of Land Management and Valuation; P.O.Box 35176,Dar es salaam, Tanzania. Fax:+255-22-2775448, 2775391 Mobile: +255 757 965150 Email: [email protected]; [email protected] Walter de Vries , ITC faculty of Geoinformation Science and Earth Observation;University of Twente: Department of Urban and Regional Planning and Geo-information Management; Phone : +31 (0)53 4874475; Fax: +31 (0)53 4874575; Email: [email protected] Abstract The relationship between pricing options for cadastral products and cost recovery is often portrayed to be two way, mandatory and automatic. However it is also evident that most cadastral organisations lack the capability to ascertain costs per product hence unable to directly match pricing options with cost recovery. Then a question arises as to whether the pricing options being implemented are in any way related to the imposed levels of cost recovery. This st udy takes a qualitative approach to understanding this question. First by using literature review pricing options and cost recovery regimes are defined and the link between them is established. E-survey was used to coll ect empirical data from 35 cadastral organisations across the globe using key-infor mant technique. The collected data were analysed using SPSS tools to establish the strength of the relationship between investigated variables. The result revealed a signif icantly strong relationship between cost recovery regimes and pricing options. However consistency in responses was poor though statistically significant. This means even if the imposition of a particular cost recovery regime necessitate the adoption of a certain pricing option or a set of pricing options, that or those pricing options ar e not exclusive for that r egime only. Therefore it is possible to infer possible pricing options for each cost recovery regime but not the other way round. Cadastral organisations under partial cost recovery regimes are likely to exhibit a wider range of pricing option because it is naturally designed to accommodate many policy goals where as a full cost recovery regime have limited option depending on the attached level of autonomy. Key Words: Pricing options, Cost recovery regimes, cadastral products; cadastral organisations; 1. Introduction Charging for the provision of cadastral information by public sector cadastral organizations has been challenged by both intellectuals and the general public ( Clark M., 2007). One argument against charging is that as long as cadastral organisations are government entities, charging for their products and services is unjustifiable since those products are produced through tax payer’s money ( Gompel, R. V. and J. Steyaert, 2002) . In this context charging seem to be unfair as those individuals who paid for the provision of cadastral products and services through taxes pay again for the same product or/and service. Despite this criticism, most public cadastral organisations whether independently or in corroboration with the

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 1/17

1

A Portfolio of Pricing Options for Public Sector Cadastral

OrganisationsSamwel Alananga-Sanga;

School of Real Estate Studies; Ardhi University;

Department of Land Management and Valuation; P.O.Box 35176,Dar es salaam, Tanzania.

Fax:+255-22-2775448, 2775391Mobile: +255 757 965150

Email: [email protected];

Walter de Vries, ITC faculty of Geoinformation Science and Earth

Observation;University of Twente: Department of Urban and Regional Planning and Geo-information

Management; Phone : +31 (0)53 4874475;

Fax: +31 (0)53 4874575;

Email: [email protected]

Abstract

The relationship between pricing options for cadastral products and cost recovery is often

portrayed to be two way, mandatory and automatic. However it is also evident that most

cadastral organisations lack the capability to ascertain costs per product hence unable todirectly match pricing options with cost recovery. Then a question arises as to whether the pricing options being implemented are in any way related to the imposed levels of cost

recovery. This study takes a qualitative approach to understanding this question. First by

using literature review pricing options and cost recovery regimes are defined and the link between them is established. E-survey was used to collect empirical data from 35 cadastral

organisations across the globe using key-informant technique. The collected data were

analysed using SPSS tools to establish the strength of the relationship between investigatedvariables. The result revealed a significantly strong relationship between cost recovery

regimes and pricing options. However consistency in responses was poor though statistically

significant. This means even if the imposition of a particular cost recovery regime

necessitate the adoption of a certain pricing option or a set of pricing options, that or those pricing options are not exclusive for that regime only. Therefore it is possible to infer

possible pricing options for each cost recovery regime but not the other way round.

Cadastral organisations under partial cost recovery regimes are likely to exhibit a wider range of pricing option because it is naturally designed to accommodate many policy goals

where as a full cost recovery regime have limited option depending on the attached level of

autonomy.

Key Words: Pricing options, Cost recovery regimes, cadastral products; cadastral

organisations;

1. Introduction

Charging for the provision of cadastral information by public sector cadastral organizationshas been challenged by both intellectuals and the general public (Clark M., 2007). Oneargument against charging is that as long as cadastral organisations are government entities,

charging for their products and services is unjustifiable since those products are produced

through tax payer’s money (Gompel, R. V. and J. Steyaert, 2002). In this context chargingseem to be unfair as those individuals who paid for the provision of cadastral products and

services through taxes pay again for the same product or/and service. Despite this criticism,

most public cadastral organisations whether independently or in corroboration with the

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 2/17

2

private sector, implements some form of charging by applying the user pay principle (Dale,

P. F. 2003). The principle provide that if public sector organisation are not making profit,they may charge a cost recovery price. However many researchers coincides that the whole

process of establishing costs for information products is hardly demonstrable (Gompel, R. V.

and J. Steyaert, 2002). This raises a question whether the prices charged are actually cost

recovery or not. This study provide a qualitative approach to address that question. Insection 2-3 literature review is used to define two concepts i.e. pricing options and cost

recovery regimes and establish a theoretical relationship between them. The concept were

necessary because it is almost impossible to establish the actual costs for each unit of a finalinformation product, due to team nature of the output (see Alchian A.A. and H. Demsetz,

1972). Section three explains the approach of the study specifically for test statistics. Data

collected through e-surveys and results of analysis are presented in section four wherediscussions and reccommendations are also provided.

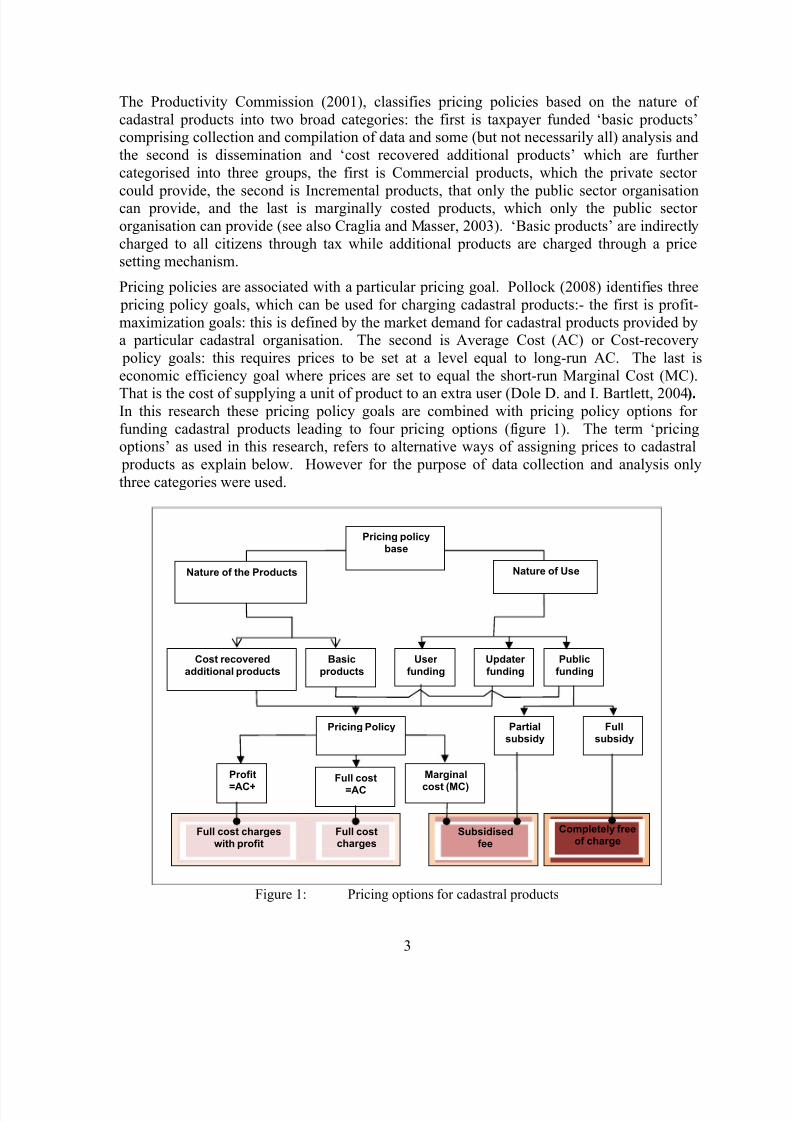

2. Pricing options for cadastral products

Cadastral products are a subcategory of Public Sector Information (PSI) which by it nature

may be considered public good. Eaton J.J. and D. Bawden (1991) provide five characteristics of information products pertinent for cadastral products which are; one, non-

rivalriness i.e. the consumption by one may not reduce its availability to others: two, non-

excludability in consumption three, its value is not readily quantifiable, four, It is not a staticresource to be stored and five, it is unique for each end user. These characteristics makes

charging most PSI a controversial issues since it is not physically and economically feasible

to identify and charge consumers and to exclude non-purchasers or it may be costly and, inthe extreme virtually impossible (see Feeny D. et al. 1990). Likewise, charging for the

provision of cadastral products is highly controlled by rules and regulations which impede

price setting autonomy and incentives to reduce costs (Pollock, 2008). Despite theseconstraints, a number of pricing options are being implemented by cadastral organisations

across the globe. This means under certain circumstances it is possible to have a system of dissemination which may include a mechanisms to monitor the use of cadastral products, or exclude consumption; such as through access controls or licenses in on-line systems (Walsh

and Woods, 2001). Likewise the current global trend suggests that cadastral services have

been restructured and the private sector has been included in the provision of cadastral

products in many countries (Demir H. and A. Yavuz, 2009). Thus cadastral products arenot pure public product rather can be regarded as semi public products since they exhibit

both characteristics of public products and private products i.e. double edged instruments

(Poe, Bishop et al., 1992; see also Morris S. and Hyun Song Shin, 2002).

Pricing Options for cadastral products can be understood within the wider context of PublicSector information (PSI) (see Craglia and Masser, 2003). These policies are either based on

the nature of use for which a cadastral product is demanded or on the nature of the cadastral product (Gompel and Steyaert, 2002; Craglia and Masser, 2003). Pollock (2008) identifiesthree types of pricing policies, based on the nature of use for which products are demanded.

The first are policies based on the availability of public funding, which involve seeking

either full or partial subsidy from general government revenues, the second are those relatingto the possibility of updater funding where a charge applies only to those who make changes

to those products and the last are those policies based on the possibility of user funding

where a charge applies to anyone using cadastral products (see figure 1).

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 3/17

3

The Productivity Commission (2001), classifies pricing policies based on the nature of

cadastral products into two broad categories: the first is taxpayer funded ‘basic products’comprising collection and compilation of data and some (but not necessarily all) analysis and

the second is dissemination and ‘cost recovered additional products’ which are further

categorised into three groups, the first is Commercial products, which the private sector

could provide, the second is Incremental products, that only the public sector organisationcan provide, and the last is marginally costed products, which only the public sector

organisation can provide (see also Craglia and Masser, 2003). ‘Basic products’ are indirectly

charged to all citizens through tax while additional products are charged through a pricesetting mechanism.

Pricing policies are associated with a particular pricing goal. Pollock (2008) identifies three

pricing policy goals, which can be used for charging cadastral products:- the first is profit-

maximization goals: this is defined by the market demand for cadastral products provided bya particular cadastral organisation. The second is Average Cost (AC) or Cost-recovery

policy goals: this requires prices to be set at a level equal to long-run AC. The last is

economic efficiency goal where prices are set to equal the short-run Marginal Cost (MC).

That is the cost of supplying a unit of product to an extra user (Dole D. and I. Bartlett, 2004). In this research these pricing policy goals are combined with pricing policy options for

funding cadastral products leading to four pricing options (figure 1). The term ‘pricingoptions’ as used in this research, refers to alternative ways of assigning prices to cadastral

products as explain below. However for the purpose of data collection and analysis only

three categories were used.

Figure 1: Pricing options for cadastral products

Full cost chargeswith profit

Full costcharges

Subsidisedfee

Cost recovered

additional products

Pricing policybase

User

funding Basic

products

Pricing Policy

Updater

funding Public

funding

Profit

=AC+ Full cost

=AC

Partialsubsidy

Fullsubsidy

Marginal

cost (MC)

Nature of the Products Nature of Use

Completely freeof charge

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 4/17

4

The first pricing option is “completely free of charge” where the final consumers get the

product without paying anything. This option is favoured on the ground that it offer accessto all hence democratic (Longhorn and Blakemore, 2008), it avoid double taxation since

taxpayers have already paid for the collection of data (Van der Molen, 2001; Longhorn and

Blakemore, 2008). Also it has a higher possibility to stimulate economic growth due to

increased businesses which may employ more people and ultimately generate more taxeswhich can further enhance the provision of cadastral products (see Longhorn and Blakemore,

2008; Wagner R. P., 2003). However it can impede the development of new products and

operate against the financial interests of the governments since even if lower prices increasesthe use of cadastral products that does not automatically mean either increased tax revenue or

decreased societal cost (Clark M., 2007). This is because if information products are offered

at ‘completely free of charge’ pricing option, users are likely to demand more than theywould otherwise (Productivity Commission, 2001).

The second option for pricing cadastral products is ‘subsidised fee’ pricing option where

marginal charges or a fees that is in no way related to the true costs or Subsidy costing-flat

rate payment are applicable (see Cheng, Dogan et al., 2006). In practice some cadastral

organisations do not have a clear link between spending and sources of revenues and oftensome revenues generated are submitted to a pool of common government revenues (Barnes

G., 2000). Although some scholars advocates the ‘subsidised fee’ pricing optionsspecifically a MC approach where full costs for information products including shipping,

promotion, personnel and IT costs are charged (see Craglia and Masser, 2003; Clark M.,

2007), the provision of information products at a highly subsidised fees is so problematic

which has forced many governments to move away from direct taxation to indirect taxationand full cost user charges (see Longhorn and Blakemore, 2008).

The third pricing option is “full Cost charges” where there is no subsidy and the organisation

charges either either MC or AC. However the use of either approach may lead to someshortcomings. The MC pricing is often seen as inappropriate when an organisation is

required to recover all the costs. Holland (1995) states that, providing information for

commercial purposes at MC unfairly subsidizes private profit at taxpayer’s expenses. In atwo sided market (where the buying and selling takes place at a platform i.e. internet), Bolt

and Tieman (2005), proves that setting prices equal to MC (without a fixed costs

component), will induce losses for the monopoly platform. Rossi and James (1975) arguethat, Setting price equal to MC will be consistent with full cost-recovery only if, MC is

greater or equal to AC. If MC is less than AC, subsidisation will be necessary.

The last pricing option that may be adapted for charging cadastral products is ‘full cost

charges with profit’ where prices are set not only to reflect the full costs of producing a product but also includes a profit for reinvestment or for meeting some other future

obligations (Absorption Costing-all cost or AC plus mark-up) (Cheng, Dogan et al., 2006).Given the monopoly nature of most cadastral organisations different pricing strategies may be adopted such as differentiation of access to cadastral products by time, place and duration,

differentiation of actuality, completeness or extent of details of a product. Differentiation

could also be in terms of speed of delivery, user friendliness and support. Bundling of information products may also be implemented for profit making purposes (see Cheng, W.

and S. Yuan, 2008). However making profit is seen as unfair for government agencies like

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 5/17

5

cadastral organisations (Gompel and Steyaert, 2002), therefore most of these pricing

strategies are not well advocated in land administration literature.

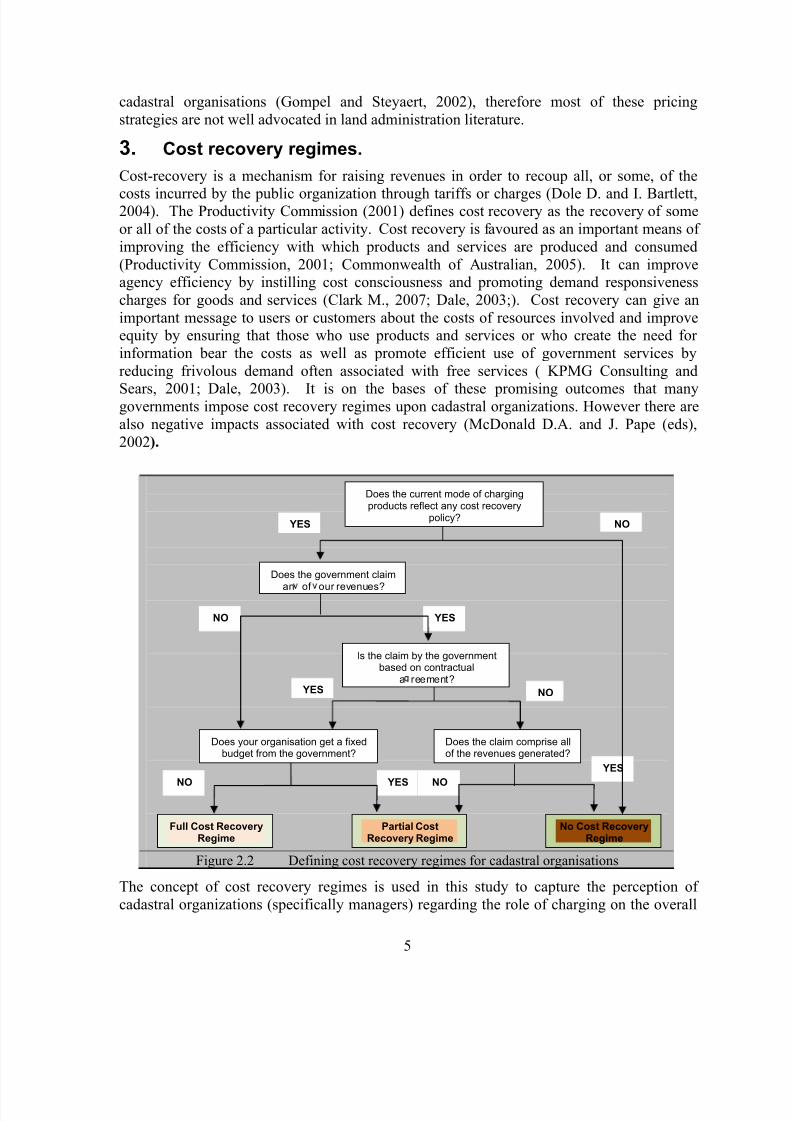

3. Cost recovery regimes.

Cost-recovery is a mechanism for raising revenues in order to recoup all, or some, of the

costs incurred by the public organization through tariffs or charges (Dole D. and I. Bartlett,2004). The Productivity Commission (2001) defines cost recovery as the recovery of some

or all of the costs of a particular activity. Cost recovery is favoured as an important means of

improving the efficiency with which products and services are produced and consumed

(Productivity Commission, 2001; Commonwealth of Australian, 2005). It can improveagency efficiency by instilling cost consciousness and promoting demand responsiveness

charges for goods and services (Clark M., 2007; Dale, 2003;). Cost recovery can give an

important message to users or customers about the costs of resources involved and improveequity by ensuring that those who use products and services or who create the need for

information bear the costs as well as promote efficient use of government services by

reducing frivolous demand often associated with free services ( KPMG Consulting and

Sears, 2001; Dale, 2003). It is on the bases of these promising outcomes that manygovernments impose cost recovery regimes upon cadastral organizations. However there are

also negative impacts associated with cost recovery (McDonald D.A. and J. Pape (eds),

2002).

Figure 2.2 Defining cost recovery regimes for cadastral organisations

The concept of cost recovery regimes is used in this study to capture the perception of

cadastral organizations (specifically managers) regarding the role of charging on the overall

YESNO

YES

Does your organisation get a fixedbudget from the government?

YES

NO YES

Does the current mode of chargingproducts reflect any cost recovery

policy?

Does the government claim

an of our revenues?

Is the claim by the governmentbased on contractual

a reement?

Does the claim comprise allof the revenues generated?

No Cost RecoveryRegime

Partial CostRecovery Regime

Full Cost RecoveryRegime

NO

YES NO

NO

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 6/17

6

financial performance of the organization given the central role of the government in the

provision of cadastral products. It is a constrained clustering mechanism which categorisescadastral organizations based on their ability to recoup costs and to use the proceeds for

further provision of cadastral products. Thus three categories of “cost recovery regimes”

(CRR) were defined as shown in figure 2.5.1. These are ‘no cost recovery’ regime, ‘partial

cost recovery’ regime and ‘full cost recovery’ regimes.Under ‘no cost recovery’ regimes (NCR) the generation or collection of cadastral products is

done by the governments which rely on statutory powers to create the products (Clark M.,

2007). If under certain legal obligations a cadastral organisation is to charge for its products,

the revenues generated by the organisation are submitted to the pool of general governmentrevenues such as taxes, fines and other user fee (Barnes G., 2000). Under these

circumstances the cadastral organisation may lack incentives to match products with demand

(Heeks, 2002). Pricing options that may be adopted depend on the overall government policies (Longhorn and Blakemore, 2008; Pollock, 2008). Under “Partial Cost Recovery”

regime (PCR) the funding for running the organisation are contributed by both the

organisation the government through service level agreement (Dale, 2003). The last regime

is ‘ Full cost recovery’ regime (FCR) where the charges applied for cadastral products areoften equal (full cost charges) or higher than the AC (full cost charges with profit) of a

product (Van der Molen, 2001).

The literature review so far provides definitions and establishes the theoretical relationship between cost recovery regimes and pricing options for cadastral products. Figure 3

summarises that relationship and forms the basis upon which data were collected. It can be

seen that cost recovery regimes are associated with certain pricing option or a set of pricingoptions for cadastral products offered under each of those regimes. However at product level

there are limited empirical researches with findings that suggest the adoption of specific

pricing option for a particular cadastral products or a set of cadastral products when a pre-specified cost recovery regimes is imposed to the provider (cadastral organizations). This is

because cost recovery regimes are imposed based on the legal and political requirements

(holistic in nature) while pricing options are influenced by the level of autonomy a cadastralorganization may have in setting prices and other market condition for each cadastral

products (specific in nature). To understand the pricing options that may be available to a

cadastral organisation in pricing cadastral products, empirical data from 35 cadastralorganisations were collected and analyzed as explained using the approach described in the

following section.

4. Research Methodology

Since there is no specific number of cadastral products, it was important first to definesample products for inclusion into the study. Seven cadastral products were purposely

selected based on the presumed fact that most cadastral organization provide them and may

be in a position to understand what comprises those products (see Appendix A). A survey

questionnaire was designed and distributed online using the surveymonkey facility(www.surveymonkey.com) to a number of cadastral organizations across the globe, of which

35 responded. The cadastral organisations as well as respective respondent from those

organisations were purposely selected based on their ability to respond to the questions posed following a prearranged communication with the respective organisation. Other

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 7/17

7

selection criteria included ease of obtaining responses, political stability of a country and the

possibility of getting online resources such as documents.

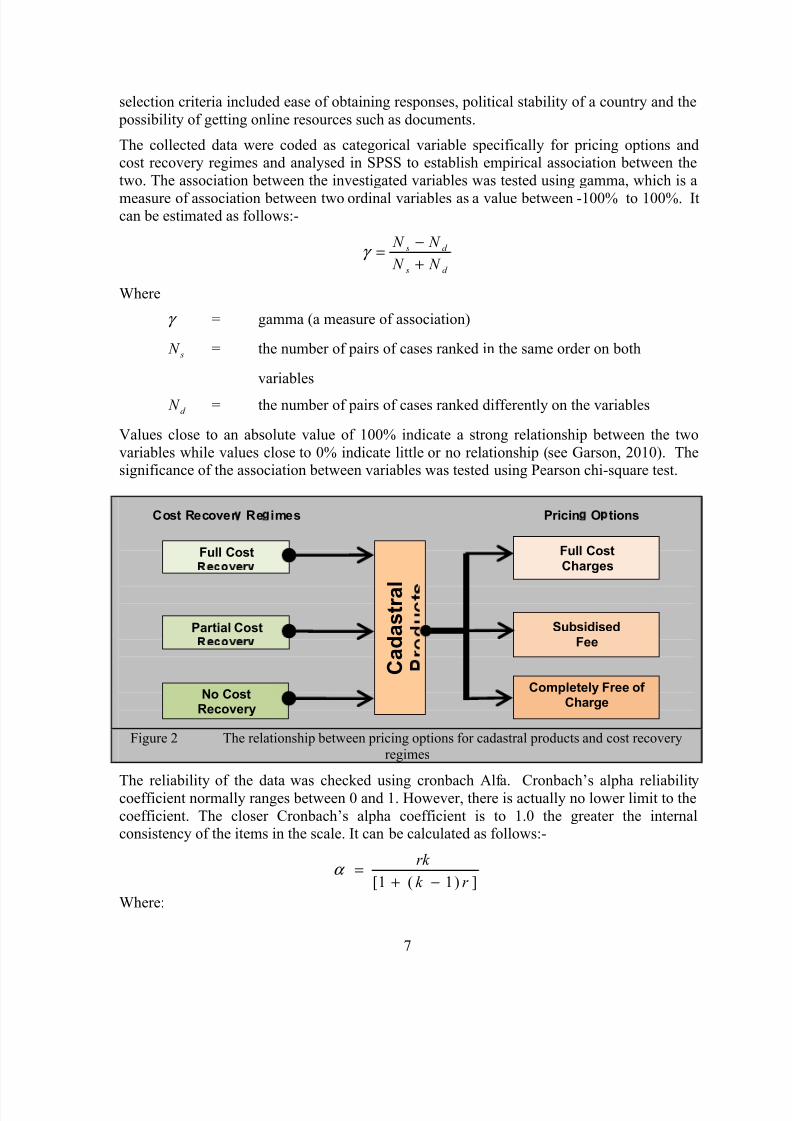

The collected data were coded as categorical variable specifically for pricing options andcost recovery regimes and analysed in SPSS to establish empirical association between the

two. The association between the investigated variables was tested using gamma, which is a

measure of association between two ordinal variables as a value between -100% to 100%. Itcan be estimated as follows:-

d s

d s

N N

N N

+

−=γ

Where

γ = gamma (a measure of association)

s N = the number of pairs of cases ranked in the same order on both

variables

d N = the number of pairs of cases ranked differently on the variables

Values close to an absolute value of 100% indicate a strong relationship between the two

variables while values close to 0% indicate little or no relationship (see Garson, 2010). Thesignificance of the association between variables was tested using Pearson chi-square test.

Figure 2 The relationship between pricing options for cadastral products and cost recovery

regimes

The reliability of the data was checked using cronbach Alfa. Cronbach’s alpha reliabilitycoefficient normally ranges between 0 and 1. However, there is actually no lower limit to the

coefficient. The closer Cronbach’s alpha coefficient is to 1.0 the greater the internalconsistency of the items in the scale. It can be calculated as follows:-

])1(1[ r k

rk

−+=α

Where:

No CostRecovery

Cost Recover Re imes

Full CostCharges

Completely Free of Charge

SubsidisedFee

Full Cost

Partial Cost

C a d a s t r a l

Pricin O tions

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 8/17

8

α = Cronbach Alfa

k = the number of items considered and

r = the mean of the inter-item correlations

The size of α is determined by both the number of items in the scale and the mean inter-

item correlations. The rules of thumb for the consistency in responses is that if α ≥ 0.9 – itis excellent, if α > 0.8 – it is good, if α > 0.7 it is acceptable, if α > 0.6 it is

questionable, if α > 0.5 it is poor, and if α ≤ 0.5 it is unacceptable” (Griem, et al., 2003).

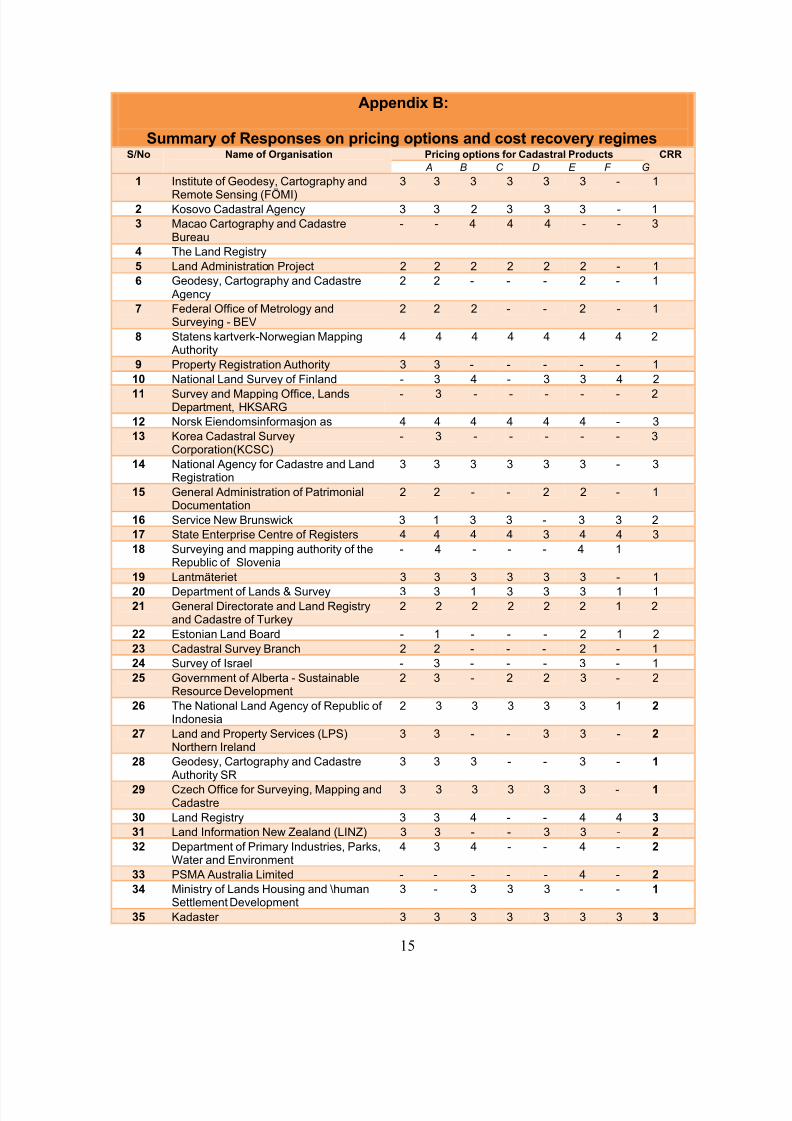

The data collected and analysed in the study are summarised in Appendix B.

5. Findings and Discussion

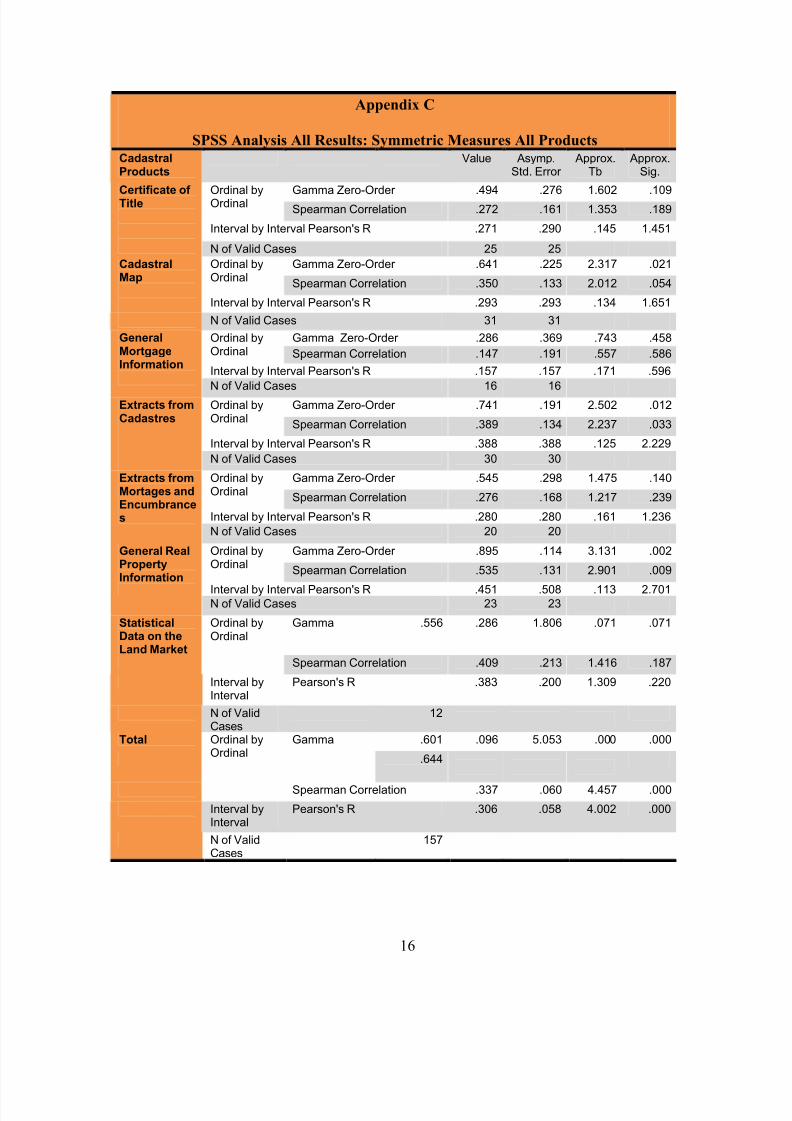

Table 1, shows the results of cross tabulation in SPSS in terms of the relationship between pricing option and cost recovery regimes. If all the seven products are considered in the

analysis, it was observed that there was a significant association between the two as shown in

table 2. That is the imposition of a certain cost recovery regime requires the adoption of certain pricing option specific for certain products. However the association between cost

recovery regimes and pricing option was not significant for all products. The imposition of cost recovery regimes seem to influence the adoption of specific pricing options for

Cadastral maps, General real property information and extracts from cadastres (see Appendix

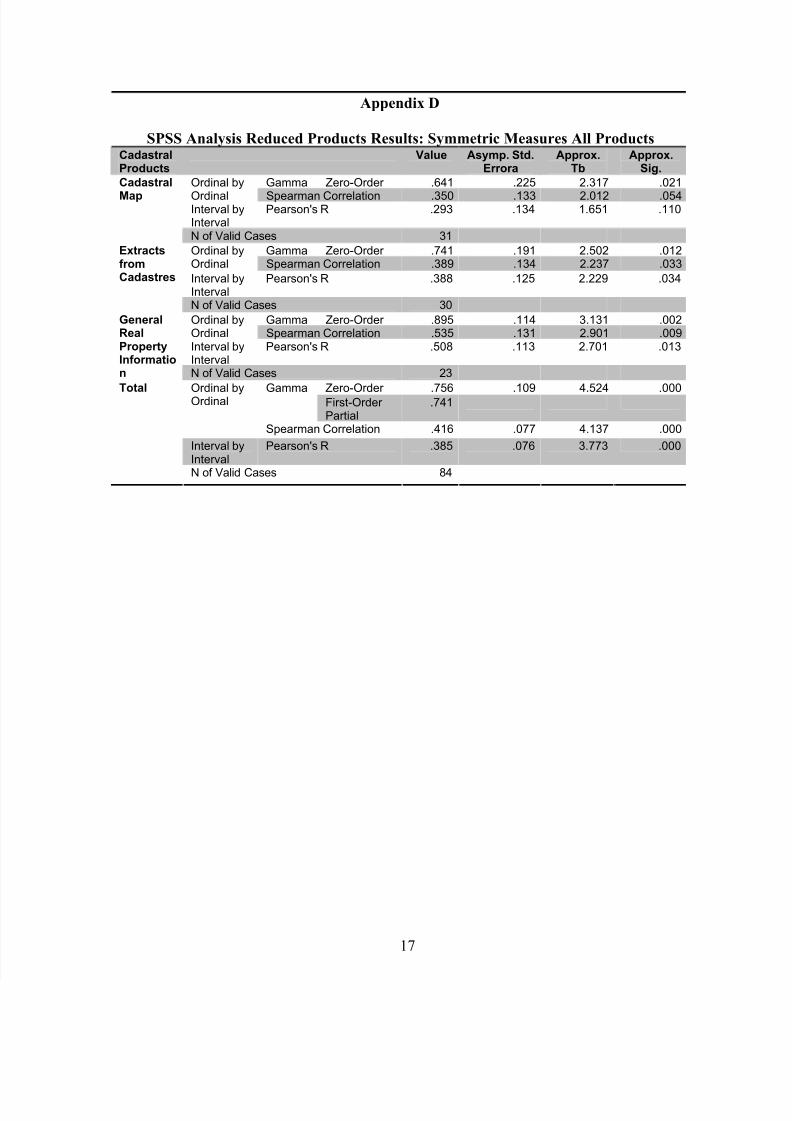

C and D). When the remaining products with insignificant association are removed from the

analysis the association between cost recovery regime significantly improves from λ = 0.60

to λ =0.76 (see table 3).

Mode of Cost Recovery Total

No CostRecoveryRegime

Partial CostRecoveryRegime

Full CostRecoveryRegime

Completely

Free of Charge

count 2 4 0 6

% of responses within a mode of cost recovery

3% 7% 0% 4%

Subsidised fee count 21 12 0 33

% of responses within a mode of cost recovery

35% 21% 0% 21%

Full CostCharges

count 37 41 40 118

P r i c i n g O p t i o n s

% of responses within a mode of cost recovery

62% 72% 100% 75%

Total count 60 60 57 40% of responses within a mode of cost recovery

100% 100% 100% 100%

Consistency of responses (all

Products-)

α = 0.44

Consistency of responses (Productswith significant association)

α = 0.51

Strength of Association (all products λ = 0.60 Strength of Association (Productswith significant association)

λ = 0.76

Table1: The relationship between pricing options for cadastral products and cost

recovery regimes

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 9/17

9

The analysis provides substantial evidence that cadastral organizations converge towards

certain pricing options when cost recovery regimes are imposed and implemented. However

the level of consistency in responses as given by Cronbach Alfa (α ), was too small to be

acceptable (α = 0.44 i.e. unacceptable, and improves to 0.51,

i.e. poor, with only products that are significantly associated i.e. poor). That means there islimited evidence to suggest that higher levels of cost recovery regimes were directly linked

to higher levels of pricing option. This was true even when the products were only those

with a high degree of association i.e. λ =0.76 (see Appendix D). From the test statistic

results it can be observed that there is a significant consistency among responses but using

the rule of thumb set above, such consistency is too small to conclude that the imposition of

cost recovery regimes necessitate the adoption of certain levels of pricing option. Thismeans that if cost recovery is defined to mean both charging and ultimate use of financial

resources for further provision of cadastral products, the adoption of any cost recovery

requirement does not dictate a specific pricing option. Table 1 shows that FCR requires theadoption of full cost or full cost with profit charges but, such pricing option are not exclusive

for that regime only. They are highly implemented under other cost recovery regimes as

well. The reason for this is that pricing goes beyond cost recovery; it is a tool of public policy that can be used for a variety of social, economic, and financial purposes (Dole D. and

I. Bartlett, 2004).

Therefore while on one hand cost recovery regimes seem to be more specific towards pricing

options, pricing options are not. There are for example a substantial number of responsesfrom organizations under NCR charging at either full cost or full cost charges with profit.

This can be interpreted to mean that, though cadastral organisations across the globe coincide

that the provision of cadastral products should be paid for by beneficiaries that does notautomatically translate to mean the revenues generated thereof are used for further provision

of cadastral products. This may be a good explanation for inadequate provision of cadastral

products for cadastral organisations in transition (Heeks, 2002).Cost recovery for cadastral information need to be understood as an attempt to charge for the

provision of cadastral product and at the same time using the proceeds for further provision

of cadastral products. Traditionally the interest on cost recovery has been on the financialaspects only where the performance of an organisation is measured in terms of revenue

generated regardless of whether such revenue are directly appropriated in the organisation or

not. This study provides a qualitative tool to cluster cadastral organisation based on their

ability to meet financial obligation as well as provide further cadastral products. It has beenobserved that cadastral organisations may well meet financial obligation but fail to provide

cadastral products in the long run as financial resources are managed elsewhere. Charging

high level prices for cadastral products may not necessarily lead to operational sustainability

of the cadastral organisation. The government may for example use charges derived fromthe sale of cadastral product for general provision of social services.

In assessing the performance of cadastral organizations, this study proposes a clusteredwithin-category comparison of cadastral organization in terms of the ability to meet financial

cost recovery. Cross comparison of cadastral organization based on the ability to meet

operational or even the total cost of production is inadequate as cadastral organization differ substantially in terms of their pricing policy goals. Therefore charging and revenue

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 10/17

10

generation do not give a clear indication of the performance of cadastral organizations across

CRR. However it could be a good performance measure within a particular CRR as thefinancial conditions underlying pricing policy are the same within a CRR. Also it should be

noted that pricing options or a set of pricing options adopted within a CRR displays stepwise

continuum without breaks in the ordinal scale. Therefore mixing divergent prices for

cadastral products is not recommended rather organizations should seek appropriate mixwithin the ordinal spectrum of pricing options to meet its intended goals.

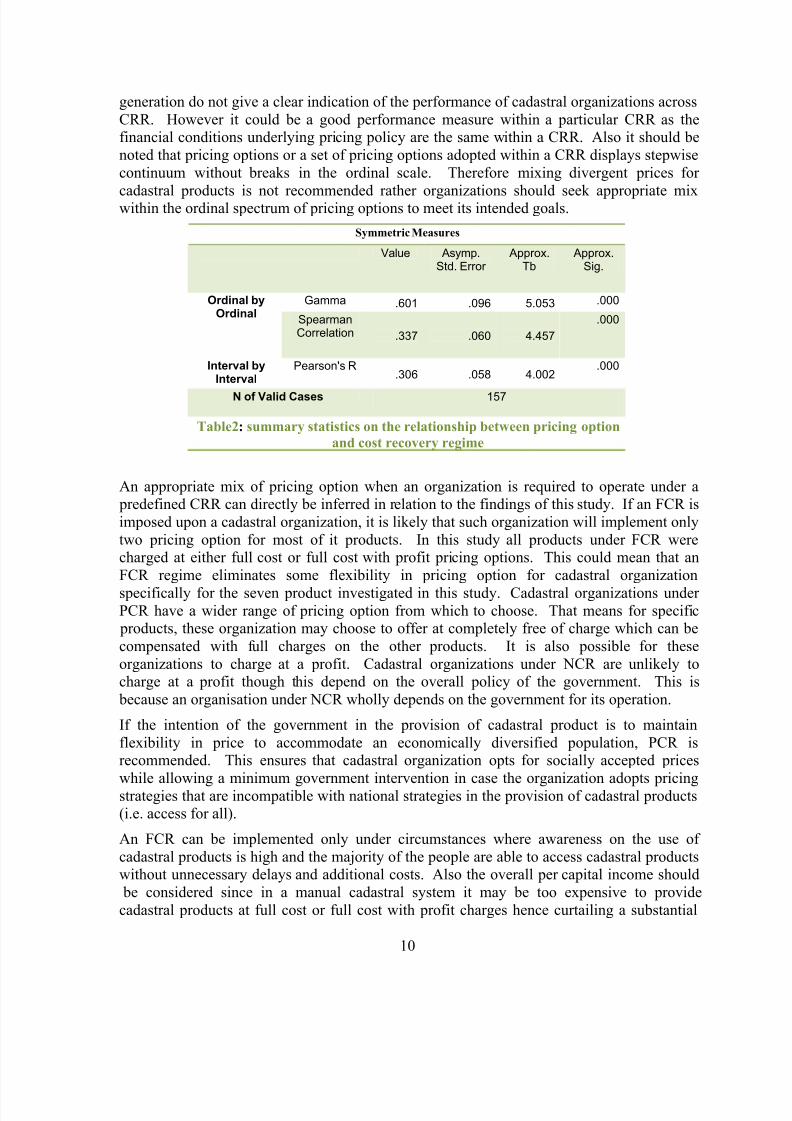

Symmetric Measures

Value Asymp.Std. Error

Approx.Tb

Approx.Sig.

Gamma .601 .096 5.053 .000Ordinal byOrdinal Spearman

Correlation .337 .060 4.457

.000

Interval byInterval

Pearson's R.306 .058 4.002

.000

N of Valid Cases 157

Table2: summary statistics on the relationship between pricing option

and cost recovery regime

An appropriate mix of pricing option when an organization is required to operate under a predefined CRR can directly be inferred in relation to the findings of this study. If an FCR is

imposed upon a cadastral organization, it is likely that such organization will implement only

two pricing option for most of it products. In this study all products under FCR werecharged at either full cost or full cost with profit pricing options. This could mean that an

FCR regime eliminates some flexibility in pricing option for cadastral organization

specifically for the seven product investigated in this study. Cadastral organizations under PCR have a wider range of pricing option from which to choose. That means for specific products, these organization may choose to offer at completely free of charge which can be

compensated with full charges on the other products. It is also possible for these

organizations to charge at a profit. Cadastral organizations under NCR are unlikely tocharge at a profit though this depend on the overall policy of the government. This is

because an organisation under NCR wholly depends on the government for its operation.

If the intention of the government in the provision of cadastral product is to maintain

flexibility in price to accommodate an economically diversified population, PCR isrecommended. This ensures that cadastral organization opts for socially accepted prices

while allowing a minimum government intervention in case the organization adopts pricingstrategies that are incompatible with national strategies in the provision of cadastral products(i.e. access for all).

An FCR can be implemented only under circumstances where awareness on the use of

cadastral products is high and the majority of the people are able to access cadastral productswithout unnecessary delays and additional costs. Also the overall per capital income should

be considered since in a manual cadastral system it may be too expensive to provide

cadastral products at full cost or full cost with profit charges hence curtailing a substantial

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 11/17

11

component of the population from access to these products. That means FCR is highly

recommended for automated cadastral systems and in developed countries in order to avoidthe design-actuality gap resulting from incompatibilities between cadastral systems and the

user (Heeks, 2002). With automated cadastral systems, the provision of cadastral products at

MC may be possible and in some cases such MC is closer to zero hence even if all the costs

are paid for by the consumer, it can still be affordable. However when per capita income islow, the necessary awareness necessary for mass consumption of cadastral products to

sustain the overall cost of running the cadastral organization may be difficult to meet. Hence

both income and the nature of the information system need to be considered when FCR issought.

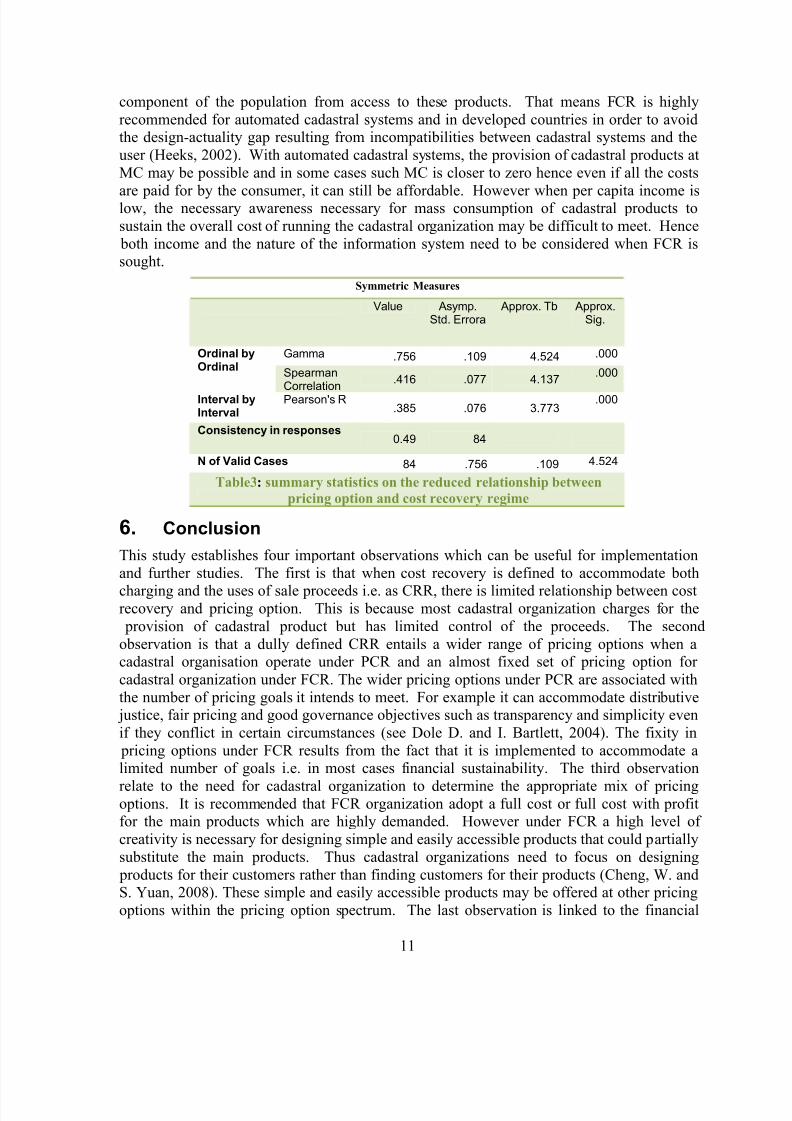

Symmetric Measures

Value Asymp.Std. Errora

Approx. Tb Approx.Sig.

Gamma .756 .109 4.524 .000Ordinal byOrdinal Spearman

Correlation.416 .077 4.137

.000

Interval byInterval

Pearson's R.385 .076 3.773

.000

Consistency in responses0.49 84

N of Valid Cases 84 .756 .109 4.524

Table3: summary statistics on the reduced relationship between

pricing option and cost recovery regime

6. Conclusion

This study establishes four important observations which can be useful for implementation

and further studies. The first is that when cost recovery is defined to accommodate both

charging and the uses of sale proceeds i.e. as CRR, there is limited relationship between costrecovery and pricing option. This is because most cadastral organization charges for the

provision of cadastral product but has limited control of the proceeds. The second

observation is that a dully defined CRR entails a wider range of pricing options when acadastral organisation operate under PCR and an almost fixed set of pricing option for

cadastral organization under FCR. The wider pricing options under PCR are associated with

the number of pricing goals it intends to meet. For example it can accommodate distributive justice, fair pricing and good governance objectives such as transparency and simplicity even

if they conflict in certain circumstances (see Dole D. and I. Bartlett, 2004). The fixity in

pricing options under FCR results from the fact that it is implemented to accommodate alimited number of goals i.e. in most cases financial sustainability. The third observation

relate to the need for cadastral organization to determine the appropriate mix of pricingoptions. It is recommended that FCR organization adopt a full cost or full cost with profitfor the main products which are highly demanded. However under FCR a high level of

creativity is necessary for designing simple and easily accessible products that could partially

substitute the main products. Thus cadastral organizations need to focus on designing

products for their customers rather than finding customers for their products (Cheng, W. andS. Yuan, 2008). These simple and easily accessible products may be offered at other pricing

options within the pricing option spectrum. The last observation is linked to the financial

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 12/17

12

performance of cadastral organization whereby this study suggests the use of CRR as defined

in this study to cluster cadastral organizations before any financial comparison is sought.

Acknowledgements

Special thanks to Prof. Van der Molen of the faculty of Geoinformation Science and Earth

Observation of the University of Twente, The Netherlands for the reference materials and detailedcontact lists he provided us, which were useful in reaching out specific individuals within the targeted

cadastral organisations. We also extend our sincere gratitude to all cadastral organisations that

participated in this study by providing us with specialised professionals whose responses were highly

valuable. Finally we extend our appreciation to the respondents themselves for their clear, detailed

and self-explanatory survey responses as well as for being tolerant to our often-disturbing remainder

emails.

ReferencesAlchian A.A. and H. Demsetz (1972). Production, Information Costs, and Economic Organization,

The American Economic Review, 62( 5), 777-795.Barnes G. (2000). Land Registration Modernization in Developing Economies: A Discussion of the

Main Problems in Central/Eastern Europe, Latin America, and the Caribbean. URISA

Journal,12(4), 33-42.

Bolt, W. and A. F. Tieman (2005). "Social Welfare and Cost Recovery in Two-Sided Markets."

SSRN eLibrary.

Chang, Wei-Lun and Soe-Tsyr Yuan, (2008). Collaborative pricing model for bundling information

goods. Journal of Information Science 34(2008), 635 - 650.

Cheng, H., K. Dogan, et al. (2006). "Pricing and Capacity Decisions for Non-Profit Internet Service

Providers." Information Technology and Management 7(2): 91-107.

Clark M. (2007). Fee or free? The hidden costs of free public sector information. Business

Information Review, 24(1): 49–59.

Commonwealth of Australian (2005). Australian Government Cost Recovery Guidelines. Financeand Administration. Canberra, Australia Government,: 77.

Craglia, M. and I. Masser (2003). "Access to Geographic Information: A European Perspective."

URISA Journal, 15(2003): 51-59.

Dale, P. F. (2003). Sustainable Land Administration: Taking a Business Approach. UConsortium of

Blom ASA,U. Ljubljana, Kadaster, Registers of Scotland,: 8.

Demir H. and A. Yavuz, (2009). Cadastral services in Turkey within the framework of new public

management. African Journal of Business Management, 3 (10), 582-590.

De Vries, W. T. and S. Beerens (2002). Economics and Capacity Implications of geo-ICT.

GIS@Development.

Dole D. and I. Bartlett, (2004). Beyond Cost Recovery:Setting User Charges for Financial,

Economic, and Social Goals. Pgs 46.

Eaton J.J. and D. Bawden ( 1991). What Kind of Resource is Information? The International Journalof information Management, 17(1991), 156-l 65.

Feeny D. et al. (1990). The Tragedy of the Commons: Twenty-Two Years Later. Human Ecology,

18(1 ), 1-19.

Gompel, R. V. and J. Steyaert (2002). Going Beyond Access: Accessibility of Government

Information in the Electronic Media Age. Intercultural Communication 23 Conference and

General Assembly IAMCR. Barcelona, Catholic University of Leuven: 30.

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 13/17

13

Griem, J. A., and Griem, R. R. (2003). Calculating, Interpreting, and Reporting Cronbach’s Alpha

Reliability Coefficient for Likert-Type Scales. Midwest Research to Practice Conference in

Continuing and community education, 2003, p. 7. Midwest.

Heeks, R. ( 2002). Information Systems and Developing Countries:Failure, Success, and Local

Improvisations. The Information Society , 18, 101–112,.

Holland, W. S., Esq. (1995). "Copyright, Licensing and Cost Recovery for Geographic and Land

Information Systems Data: A Legal, Economic and Policy Analysis." Retrieved 15/10/2009,2009, from http://www.spatial.maine.edu/~onsrud/tempe/holland.html.

KPMG Consulting and G. Sears (2001). Canadian Geospatial Data Policy Study (executivesummary): Report Prepared for GeoConnections,. Policy Advisory Node of GeoConnections.

Ottawa, KPMG Consulting: 32.

McDonald D.A. and J. Pape (eds) (2002). Cost Recovery and the Crisis of Service Delivery in South

Africa, Human Sciences Research Council Publishers, Pgs 208.

Morris S. and Hyun Song Shin (2002). Social Value of Public Information. The AmericanEconomic Review 92(5), 1521 - 1537.

Longhorn, R. A. and M. Blakemore (2008). Geographic Information : Value, Pricing, Production,

and Consumption. Boca Raton, CRC.

Poe, G. L., R. C. Bishop, et al. (1992). Benefit - Cost Principles for Land Information Systems.

URISA Journal, 4(2): 20-31.Pollock, R. (2008). The Economics of Public Sector Information. Cambridge, University of

Cambridge: 50.

Productivity Commission (2001). Cost Recovery by Government Agencies. Report No. 15. Ausinfo.

Canberra: 640.

Rossi, D. and A. James (1975). Cost Recovery in Pricing and Capacity Decision for Automated

Information Systems Washington DC, U.S. Dept. of Commerce, National Bureau of

Standards 61.

Van der Molen, P. (2001). "Cost Recovery for Land Administration." Survey Review, 36(282): 241-

248.

Walsh, S. and R. Woods (2001). Pricing Electronic Goods in the Public Sector. Government

Information Systems Forum. Wellington, New Zealand, Land Information New Zealand.

Wagner R. P., (2003). Information Wants to Be Free: Intellectual Property and the Mythologies of Control. Columbia Law Review, 103(4), 995-1034.

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 14/17

14

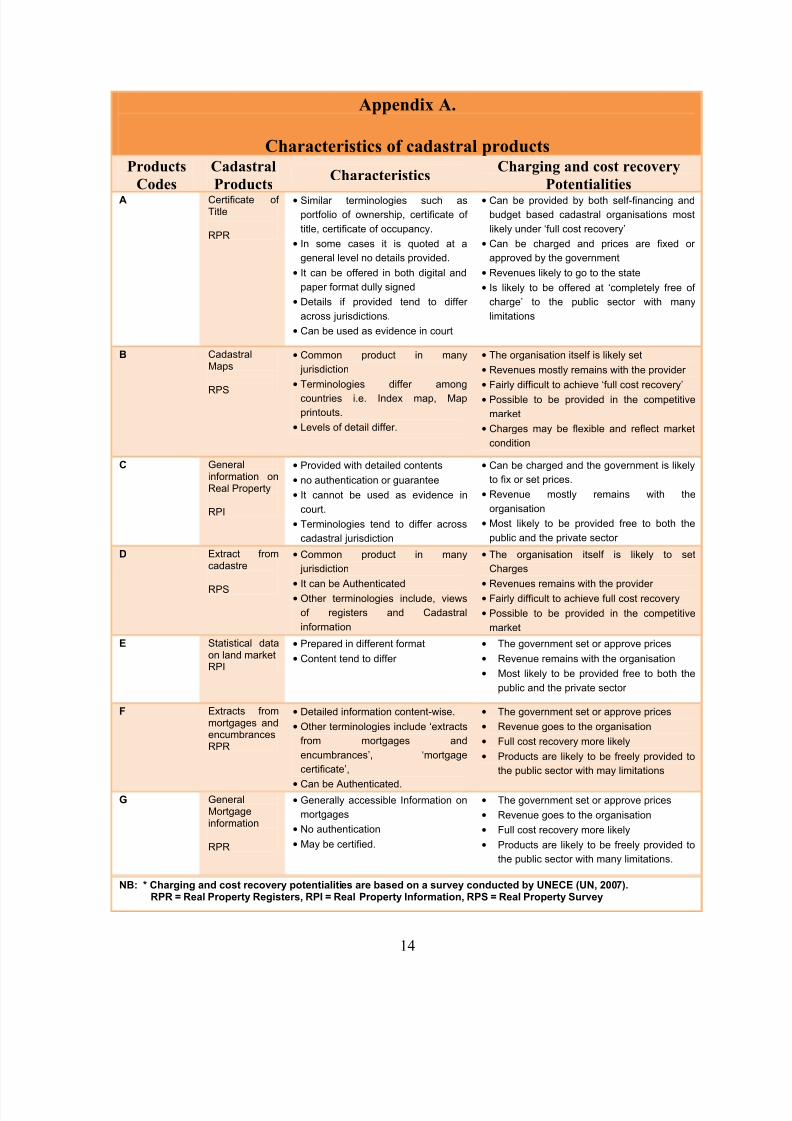

Appendix A.

Characteristics of cadastral productsProducts

Codes

Cadastral

ProductsCharacteristics

Charging and cost recovery

PotentialitiesA Certificate of

Title

RPR

• Similar terminologies such asportfolio of ownership, certificate of

title, certificate of occupancy.

• In some cases it is quoted at a

general level no details provided.

• It can be offered in both digital and

paper format dully signed

• Details if provided tend to differ

across jurisdictions.

• Can be used as evidence in court

• Can be provided by both self-financing andbudget based cadastral organisations most

likely under ‘full cost recovery’

• Can be charged and prices are fixed or

approved by the government

• Revenues likely to go to the state

• Is likely to be offered at ‘completely free of

charge’ to the public sector with many

limitations

B CadastralMaps

RPS

• Common product in many

jurisdiction

• Terminologies differ among

countries i.e. Index map, Map

printouts.

• Levels of detail differ.

• The organisation itself is likely set

• Revenues mostly remains with the provider

• Fairly difficult to achieve ‘full cost recovery’

• Possible to be provided in the competitive

market

• Charges may be flexible and reflect market

condition

C Generalinformation onReal Property

RPI

• Provided with detailed contents

• no authentication or guarantee

• It cannot be used as evidence in

court.

• Terminologies tend to differ across

cadastral jurisdiction

• Can be charged and the government is likely

to fix or set prices.

• Revenue mostly remains with the

organisation

• Most likely to be provided free to both the

public and the private sector

D Extract fromcadastre

RPS

• Common product in many

jurisdiction

• It can be Authenticated

• Other terminologies include, views

of registers and Cadastral

information

• The organisation itself is likely to set

Charges

• Revenues remains with the provider

• Fairly difficult to achieve full cost recovery

• Possible to be provided in the competitive

market

E Statistical dataon land marketRPI

• Prepared in different format

• Content tend to differ

• The government set or approve prices

• Revenue remains with the organisation

• Most likely to be provided free to both the

public and the private sector

F Extracts frommortgages andencumbrancesRPR

• Detailed information content-wise.

• Other terminologies include ‘extracts

from mortgages and

encumbrances’, ‘mortgage

certificate’,

• Can be Authenticated.

• The government set or approve prices

• Revenue goes to the organisation

• Full cost recovery more likely

• Products are likely to be freely provided to

the public sector with may limitations

G GeneralMortgageinformation

RPR

• Generally accessible Information on

mortgages

• No authentication

• May be certified.

• The government set or approve prices

• Revenue goes to the organisation

• Full cost recovery more likely

• Products are likely to be freely provided to

the public sector with many limitations.

NB: * Charging and cost recovery potentialities are based on a survey conducted by UNECE (UN, 2007).RPR = Real Property Registers, RPI = Real Property Information, RPS = Real Property Survey

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 15/17

15

Appendix B:

Summary of Responses on pricing options and cost recovery regimes

Pricing options for Cadastral ProductsS/No Name of Organisation

A B C D E F G

CRR

1 Institute of Geodesy, Cartography and

Remote Sensing (FÖMI)

3 3 3 3 3 3 - 1

2 Kosovo Cadastral Agency 3 3 2 3 3 3 - 13 Macao Cartography and Cadastre

Bureau- - 4 4 4 - - 3

4 The Land Registry5 Land Administration Project 2 2 2 2 2 2 - 16 Geodesy, Cartography and Cadastre

Agency2 2 - - - 2 - 1

7 Federal Office of Metrology andSurveying - BEV

2 2 2 - - 2 - 1

8 Statens kartverk-Norwegian MappingAuthority

4 4 4 4 4 4 4 2

9 Property Registration Authority 3 3 - - - - - 110 National Land Survey of Finland - 3 4 - 3 3 4 2

11 Survey and Mapping Office, LandsDepartment, HKSARG

- 3 - - - - - 2

12 Norsk Eiendomsinformasjon as 4 4 4 4 4 4 - 313 Korea Cadastral Survey

Corporation(KCSC)- 3 - - - - - 3

14 National Agency for Cadastre and LandRegistration

3 3 3 3 3 3 - 3

15 General Administration of PatrimonialDocumentation

2 2 - - 2 2 - 1

16 Service New Brunswick 3 1 3 3 - 3 3 217 State Enterprise Centre of Registers 4 4 4 4 3 4 4 318 Surveying and mapping authority of the

Republic of Slovenia- 4 - - - 4 1

19 Lantmäteriet 3 3 3 3 3 3 - 1

20 Department of Lands & Survey 3 3 1 3 3 3 1 121 General Directorate and Land Registry

and Cadastre of Turkey2 2 2 2 2 2 1 2

22 Estonian Land Board - 1 - - - 2 1 223 Cadastral Survey Branch 2 2 - - - 2 - 124 Survey of Israel - 3 - - - 3 - 125 Government of Alberta - Sustainable

Resource Development2 3 - 2 2 3 - 2

26 The National Land Agency of Republic of Indonesia

2 3 3 3 3 3 1 2

27 Land and Property Services (LPS)Northern Ireland

3 3 - - 3 3 - 2

28 Geodesy, Cartography and CadastreAuthority SR

3 3 3 - - 3 - 1

29 Czech Office for Surveying, Mapping andCadastre

3 3 3 3 3 3 - 1

30 Land Registry 3 3 4 - - 4 4 3

31 Land Information New Zealand (LINZ) 3 3 - - 3 3 - 2

32 Department of Primary Industries, Parks,Water and Environment

4 3 4 - - 4 - 2

33 PSMA Australia Limited - - - - - 4 - 2

34 Ministry of Lands Housing and \humanSettlement Development

3 - 3 3 3 - - 1

35 Kadaster 3 3 3 3 3 3 3 3

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 16/17

16

Appendix C

SPSS Analysis All Results: Symmetric Measures All Products

CadastralProducts

Value Asymp.Std. Error

Approx.Tb

Approx.Sig.

Gamma Zero-Order .494 .276 1.602 .109Ordinal byOrdinal Spearman Correlation .272 .161 1.353 .189

Interval by Interval Pearson's R .271 .290 .145 1.451

Certificate of Title

N of Valid Cases 25 25Gamma Zero-Order .641 .225 2.317 .021Ordinal by

Ordinal Spearman Correlation .350 .133 2.012 .054

CadastralMap

Interval by Interval Pearson's R .293 .293 .134 1.651

N of Valid Cases 31 31

Gamma Zero-Order .286 .369 .743 .458Ordinal byOrdinal Spearman Correlation .147 .191 .557 .586

Interval by Interval Pearson's R .157 .157 .171 .596

GeneralMortgageInformation

N of Valid Cases 16 16

Gamma Zero-Order .741 .191 2.502 .012Ordinal byOrdinal Spearman Correlation .389 .134 2.237 .033

Interval by Interval Pearson's R .388 .388 .125 2.229

Extracts fromCadastres

N of Valid Cases 30 30

Gamma Zero-Order .545 .298 1.475 .140Ordinal byOrdinal Spearman Correlation .276 .168 1.217 .239

Interval by Interval Pearson's R .280 .280 .161 1.236

Extracts fromMortages andEncumbrances

N of Valid Cases 20 20

Gamma Zero-Order .895 .114 3.131 .002Ordinal byOrdinal Spearman Correlation .535 .131 2.901 .009

Interval by Interval Pearson's R .451 .508 .113 2.701

General RealPropertyInformation

N of Valid Cases 23 23

StatisticalData on theLand Market

Gamma .556 .286 1.806 .071 .071Ordinal byOrdinal

Spearman Correlation .409 .213 1.416 .187

Interval byInterval

Pearson's R .383 .200 1.309 .220

N of ValidCases

12

Total .601 .096 5.053 .000 .000Gamma

.644

Ordinal byOrdinal

Spearman Correlation .337 .060 4.457 .000

Interval byInterval

Pearson's R .306 .058 4.002 .000

N of ValidCases

157

8/8/2019 Portfolio of Pricing Options Draft 1

http://slidepdf.com/reader/full/portfolio-of-pricing-options-draft-1 17/17

17

Appendix D

SPSS Analysis Reduced Products Results: Symmetric Measures All Products

CadastralProducts

Value Asymp. Std.Errora

Approx.Tb

Approx.Sig.

Gamma Zero-Order .641 .225 2.317 .021Ordinal by

Ordinal Spearman Correlation .350 .133 2.012 .054Interval byInterval

Pearson's R .293 .134 1.651 .110

Cadastral

Map

N of Valid Cases 31Gamma Zero-Order .741 .191 2.502 .012Ordinal by

Ordinal Spearman Correlation .389 .134 2.237 .033Interval byInterval

Pearson's R .388 .125 2.229 .034

ExtractsfromCadastres

N of Valid Cases 30Gamma Zero-Order .895 .114 3.131 .002Ordinal by

Ordinal Spearman Correlation .535 .131 2.901 .009Interval byInterval

Pearson's R .508 .113 2.701 .013

GeneralRealPropertyInformation N of Valid Cases 23

Zero-Order .756 .109 4.524 .000Gamma First-Order Partial

.741Ordinal byOrdinal

Spearman Correlation .416 .077 4.137 .000

Interval byInterval

Pearson's R .385 .076 3.773 .000

Total

N of Valid Cases 84

Related Documents