Business Plan, May 2016 Institute for Manufacturing Charles Babbage Road, Cambridge Table of Contents 1. Executive Summary 2. Business Overview 3. Products and Services 4. Markets and Competition 5. Sales and Marketing Strategy 6. Management 7. Operations 8. Financial Projections 9. Financial Requirements 10. Assessment of Risk 11. Appendices

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Business Plan, May 2016

Institute for Manufacturing Charles Babbage Road, Cambridge

Table of Contents

1. Executive Summary 2. Business Overview 3. Products and Services 4. Markets and Competition 5. Sales and Marketing Strategy 6. Management 7. Operations 8. Financial Projections 9. Financial Requirements 10. Assessment of Risk

11. Appendices

Business Plan PolyPack May 2016

Executive Summary

PolyPack is our innovative solution to creating beautiful, sturdy and environmentally sustainable packaging. Made from waste plastic bottles, PolyPack packaging consists of a soft fibrous interior connected to a hard plastic shell that provides twofold protection for highvalue items. Instead of selling this packaging to consumer goods manufacturers, PolyPack will lease the machines that allow manufacturers to create the packaging themselves from waste material. We’ll additionally offer the ability to manufacture bespoke packaging to promote brand values including (but not limited to) environmental awareness. The combination of our leasing business model and disruptive, net environmental benefitproviding technology will set PolyPack apart from all current packaging solutions: allowing us to claim a significant portion of consumable goods packaging (especially considering the expected demise of some of the most conventional packaging solutions). PolyPack will focus particularly on selling to consumable goods manufacturers that create small, highvalue goods and to online retailers that distribute such goods with emphasis on those firms who care most about the environment. This focus leaves £200m of the UK (and £10.7bn of the worldwide) packaging market applicable for us to access.

Our management team consists of Laura Tuck, Cam Hardman and James Veale all currently pursuing a Masters in Manufacturing Engineering from the University of Cambridge’s Institute for Manufacturing. To date, we have made rapid and successful progress in the development of prototypes at a proof of concept level and above.

Initial conservative estimates show PolyPack as profitable in Year 3, holding £1m in retained earnings in Year 5 and growing rapidly after that point. We are looking for a total of £400,000 in investments (half in Year 0 and half in Year 1 when our progress will make us even more attractive as an investment) in order to grow the business while remaining cash positive. Shareholders will be paid dividends of 10% of annual profits, with investors expecting to be paid a total of around £60,000 in the years up to Year 5.

Business Overview

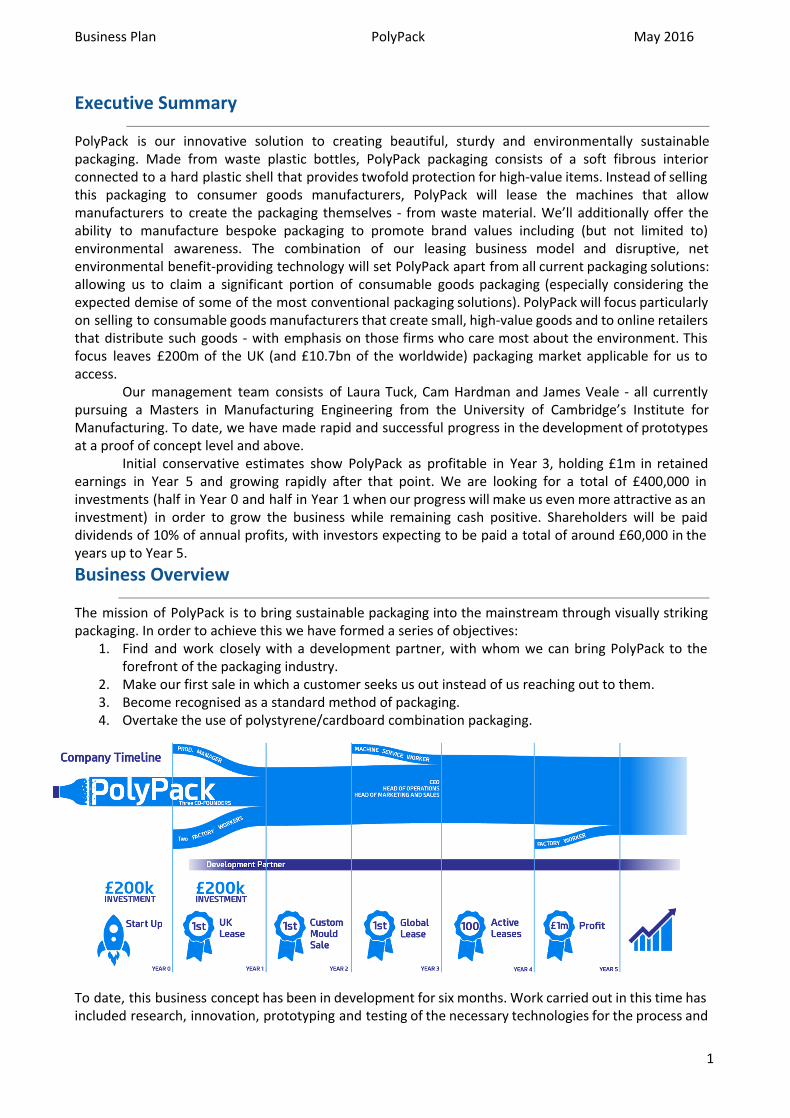

The mission of PolyPack is to bring sustainable packaging into the mainstream through visually striking packaging. In order to achieve this we have formed a series of objectives:

1. Find and work closely with a development partner, with whom we can bring PolyPack to the forefront of the packaging industry.

2. Make our first sale in which a customer seeks us out instead of us reaching out to them. 3. Become recognised as a standard method of packaging. 4. Overtake the use of polystyrene/cardboard combination packaging.

To date, this business concept has been in development for six months. Work carried out in this time has included research, innovation, prototyping and testing of the necessary technologies for the process and

1

Business Plan PolyPack May 2016

the creation of preliminary financials for the proposed business. The management team (formed of three CoFounders) has related experience in manufacturing,

prototyping, assembly and factory work, and an education in financial and business strategy. PolyPack will be a Limited Liability Company, signalling our commitment to the company and

allowing a flexible management structure. Ownership of the company will be retained by the three CoFounders, who will each hold 20% of equity: leaving 40% of equity to be held by relevant investors.

Products and Services

We will lease PolyPack machines (consisting of a PolyProducer and a PolyPacker), with a Business to Business model similar to Rolls Royce’s “Power By The Hour”. PolyPack will be responsible for servicing the machines, which our customers will use in line with their own manufacturing/assembly processes. PolyPack will also offer a custom mould design service allowing customers to order more complicated custom moulds with which to create iconic packaging.

PolyPack stands out from other packaging products with its new and unique aesthetic, its cradle to cradle nature and its inherent ability to offer customised packaging without a reliance on ink. Additionally, it stands out from other PET recycling methods in its lower energy use per kilogram of plastic and its potential to be used for many plastics or a mix of polymers.

PolyPack will offer value to our customers as it allows them to project a green brand image through their packaging, enhanced by Polypack’s distinctive style. Value is also obtained through decreased cost of packaging recovery notes (within the EU).

As our customers’ needs may develop in the long term, PolyPack is ready to adapt. For example, if PET stops being used for disposable drinks bottles, PolyPack machines can be altered to use any polymer, allowing our business to continue despite changes in our environment. As such, PolyPack is a solution not only for today, but for the future. Other polymers may also be used to deliver different mechanical or thermal properties for changing industry needs. This may also allow companies to use their own waste material as the input for PolyPack production, or encourage industrial symbiosis.

Key features of the packaging industry to note, due to their potential to affect our business, include UK, EU and other regulations regarding the use of ‘waste materials’. In the EU, once a material has been classified as waste, only suitably certified firms may handle the material. This may cause complications in allowing firms to run the PolyPack process within their own production lines and as such special attention will be paid to this issue. Another aspect of the industry that must be considered is the development and entry of other new packaging technologies such as Myco Foam Mushroom® Packaging.

Markets and Competition

We can define our initial market as UK firms that manufacture and sell their own products, as they are the firms most likely to benefit from inline packaging solutions. We may segment this market between customers that produce small, highvalue products and those with larger or lower value products. We can also distinguish between manufacturers that have a strong environmental consciousness and those that don’t. The segment that suits our product best would be those UK manufacturers that produce small, highvalue goods and also have a strong environmental awareness.

As a disruptive technology with no known near substitutes, it is hard to find a reliable figure for the UK and world markets applicable to PolyPack. Making some conservative assumptions (found in the Appendices), our market segment can be valued at around £200mwithin the UK and £10.7bn worldwide. While our initial focus will be on these segments, we may market to the broader segments within consumer goods manufacturers. Furthermore, as PolyPack grows we will branch out and market towards online retailers. As with our original target market segments, they will be customers who would be willing to invest in order to improve environmental efficiency or brand impact.

2

Business Plan PolyPack May 2016

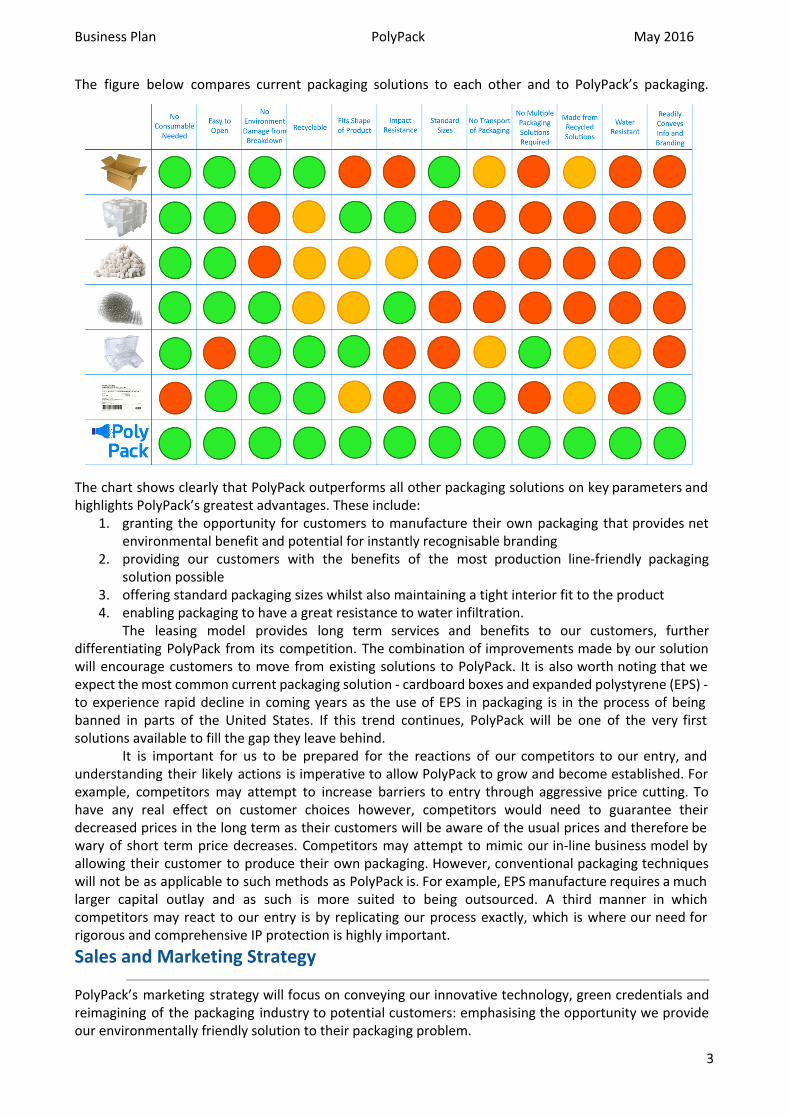

The figure below compares current packaging solutions to each other and to PolyPack’s packaging.

The chart shows clearly that PolyPack outperforms all other packaging solutions on key parameters and highlights PolyPack’s greatest advantages. These include:

1. granting the opportunity for customers to manufacture their own packaging that provides net environmental benefit and potential for instantly recognisable branding

2. providing our customers with the benefits of the most production linefriendly packaging solution possible

3. offering standard packaging sizes whilst also maintaining a tight interior fit to the product 4. enabling packaging to have a great resistance to water infiltration.

The leasing model provides long term services and benefits to our customers, further differentiating PolyPack from its competition. The combination of improvements made by our solution will encourage customers to move from existing solutions to PolyPack. It is also worth noting that we expect the most common current packaging solution cardboard boxes and expanded polystyrene (EPS) to experience rapid decline in coming years as the use of EPS in packaging is in the process of being banned in parts of the United States. If this trend continues, PolyPack will be one of the very first solutions available to fill the gap they leave behind.

It is important for us to be prepared for the reactions of our competitors to our entry, and understanding their likely actions is imperative to allow PolyPack to grow and become established. For example, competitors may attempt to increase barriers to entry through aggressive price cutting. To have any real effect on customer choices however, competitors would need to guarantee their decreased prices in the long term as their customers will be aware of the usual prices and therefore be wary of short term price decreases. Competitors may attempt to mimic our inline business model by allowing their customer to produce their own packaging. However, conventional packaging techniques will not be as applicable to such methods as PolyPack is. For example, EPS manufacture requires a much larger capital outlay and as such is more suited to being outsourced. A third manner in which competitors may react to our entry is by replicating our process exactly, which is where our need for rigorous and comprehensive IP protection is highly important.

Sales and Marketing Strategy

PolyPack’s marketing strategy will focus on conveying our innovative technology, green credentials and reimagining of the packaging industry to potential customers: emphasising the opportunity we provide our environmentally friendly solution to their packaging problem.

3

Business Plan PolyPack May 2016

PolyPack will focus on relationship based marketing techniques in order to maintain customers (in addition to gaining new ones), allowing a predictable revenue stream to be established and reducing uncertainty. As we are selling business to business, our promotion policy and sales process will avoid advertising and instead will involve sending CoFounders (with knowledge and experience) as salespeople to factories. This allows them to communicate closely with potential customers and show them the benefits of leasing our product. We will use a professional website as a landing platform that will provide comprehensive information on PolyPack. This will work particularly well when dealing with online retailers as potential customers. We will also hold ‘single company trade shows’ in which we will invite a number of firms to a demonstration of our technology and business in order to gain contacts and customers, perhaps making the most of sitting in the periphery of large trade shows without the costs of being within a trade show itself.

In our first year, our sales and marketing strategy will have a specific focus on finding a suitable development partner and building a limited customer base by offering discounts in return for feedback. Working closely with these early customers and development partners will demonstrate our determination to improve the PolyPack machines and will aid the development of our technology and business. Under our leasing model, repeat sales are made by customers renewing their lease and by increasing the number of machines they lease when upgrading their capacity.

Profit will be made on the sale of leases and custom moulds. Leased machines will comprise the majority contribution due to the larger volume of this core aspect. The design and sale of custommoulds will provide a significantly larger margin due to its nonstandard nature, but a smaller contribution to profit due to its lower volume. The margins for both will increase after Year 1 as we rise to full prices once established.

Expected sales, costs and gross profit for the first five years after development, for both of the revenue streams, are listed in the Financial Projections section (with full details in the Appendices).

Management

Initially the three CoFounders will be flexible in fulfilling various management tasks, but once PolyPack is more established as a business they will be allocated the roles of CEO, Head of Marketing and Sales and Head of Operations. Finance and administration tasks will be conducted under operations management until such a point that the company is large enough for the Penrose Constraint to take effect and additional management staff are employed. All CoFounders will be taking up PolyPack as a fulltime job due to their belief in the product and company. The CoFounders all have established strengths in time management skills and working with others and have individual skills and interests highlighted to the left. One of the first HR tasks will be the employment of a production manager with a background in quality engineering. This experienced member of the team will avoid expensive mistakes on the factory floor as none of the three founders are sufficiently experienced for such a role. All of the CoFounders of PolyPack have technical backgrounds coming from an engineering degree and are therefore technically competent. This will be reflected in the manner in which the company is managed. For example, from an operations management perspective MRP will initially be used, transitioning through MRP II to ERP as the company grows. The CoFounders are in the strongest position to pitch PolyPack to potential customers as we understand and have the most experience with our technology and have a strong vision of how PolyPack will operate. We will also benefit from the sales/pitching process in early years as we can choose our first customers for best fit and find the most suitable development partner. In order to allow us to make the most of sales opportunities and develop an understanding of the sales process beyond that given by university modules,

the CoFounders will all take part in a sales and marketing course towards the end of Year 0.

4

Business Plan PolyPack May 2016

PolyPack has access to many mentors from its origins in the Institute for Manufacturing as well as expert input from advisors at Barclays. Additionally we hope that our investors will give helpful insights and suggestions into the running of PolyPack, contributing knowledge as well as capital.

All three CoFounders will earn a living wage for the foreseeable future (taking no wage in Year 0) in order to support them enough to be able to put in 100% for PolyPack without spending large proportions of investment of wages. As a new startup, PolyPack isn’t expected to pay high wages early on, but will pay all employees at least the living wage. A full outline of wages and a personnel plan is found in the Appendices. All employees will be entitled to the UK standard 28 days paid leave per annum.

Operations

Our current location in Cambridge holds many benefits including access to mentors, equipment and a large community of startups and tech firms and as such we will remain in Cambridge for at least Year 0 and potentially Year 1. We expect to later move northward, allowing production to be nearer to the UK’s industrial hubs. Such a move will allow us to also make the most of other benefits, including lower land prices, wages and cost of living.

The cost of transporting our finished product is likely to be higher than the cost of transporting raw material, due to its increased volume. As such, being close to customers (or perhaps to centralised distribution points) will be a priority in choosing a location for manufacturing operations. Once potential sites have been found heuristics such as the North West Corner Methods will be used to assess their suitability. The availability of labour and land prices in the chosen area will also be considered.

An initial capital outlay will be required to purchase machinery (including rollers, welding equipment, a guillotine, CNC mill and lathe) and production rates will be limited by order numbers. As the company grows and demand increases the bottleneck in our process will likely be the milling machine as it is used a number of times in the production of each machine. As such, an additional mill may be purchased to increase capacity when required.

PolyPack machines will be made to order (as their manufacturing lead time is relatively short) so there will not be a finished good inventory, which avoids large warehouse costs. Rawmaterials inventory will be calculated based upon an Economic Order Quantity calculation.

Throughout Years 14 our predicted demand indicates that two Factory Workers would be sufficient, with the 3 CoFounders and Production Manager covering all other roles. In Year 3 a Machine Service Worker will be hired, travelling to provide machine servicing and in Year 5 the increase in sales justifies the recruitment of a third Factory Worker. We do not currently anticipate sufficient custom mould orders to justify the recruitment of a specialised designer, but this may be required depending on popularity of bespoke designs. Assuming the company has reached a sufficient level of maturity, the CoFounders will move into the three roles of CEO, Head of Operations and Head of Marketing and Sales in Year 3.

Suppliers will be chosen based upon standard measures of cost, location, flexibility and delivery speed but also on their level of sustainability and environmental impact. Such impacts are important to both PolyPack and our target customers. Along these lines, PolyPack will seek to achieve ISO 14001 accreditation and may require it from our suppliers.

Financial Projections

Sales Forecast PolyPack Machine Year 0 1 2 3 4 5

New UK 0 10 20 40 80 160

New Rest of World 0 0 0 10 20 40

Total UK 0 10 30 69 147 302

Total Rest of World 0 0 0 10 30 69

Total 0 10 30 79 177 371

In Year 1, we will limit ourselves to 10 leases in order to be able to work closely with our customers and continue to develop our product. In order to achieve this we have budgeted time to allow us to make two new sales attempts each week. With a conservative success rate of 10% on the hundred

5

Business Plan PolyPack May 2016

or so attempts this gives us we should be able to match our expectations. In subsequent years, we aim to double our sales of new leases each year until at least Year 5. This will be possible due to increased effort in sales and an increased success rate as our product gains popularity. The figures above for our total number of active leases assume that our customers lease on a two year contract with a (conservative) retention rate of 90% at the end of each contract. We are confident that our retention rate will be higher than this due to how closely we plan to work with our initial customers in order to ensure the superiority of our product and service . From Year 3 onwards we will expand our reach to access the much larger global market. Sales Forecast Custom Moulds

Year 0 1 2 3 4 5

UK 0 0 3 10 23 49

Rest of World 0 0 0 0 3 10

Total 0 0 3 10 26 59

We envisage large increases in custom mould orders with time as PolyPack becomes more established and as our total clientele increases. Cash Flow Summary

Year 0 1 2 3 4 5

Total Cash In 103,435 (10,295) (57,395) 90,636 369,316 872,095

Cash at Start 0 103,435 93,140 35,745 126,381 495,696

Cash at End 103,435 93,140 35,745 126,381 495,696 1,367,791

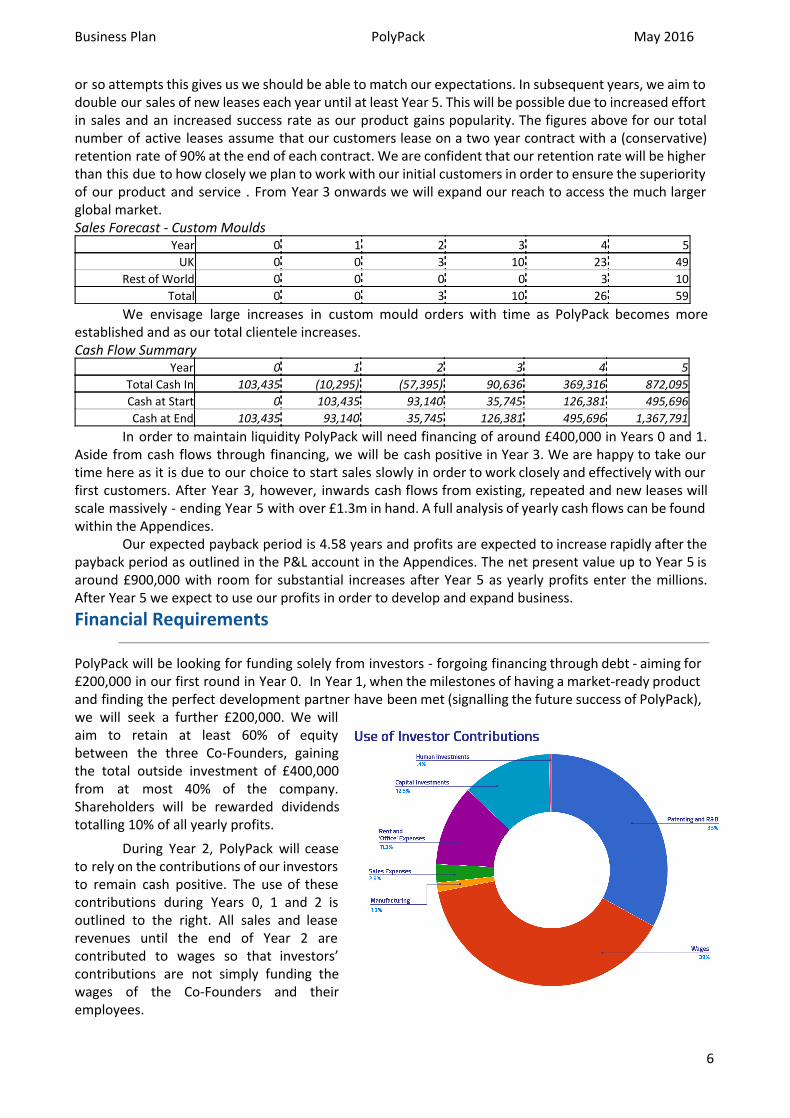

In order to maintain liquidity PolyPack will need financing of around £400,000 in Years 0 and 1. Aside from cash flows through financing, we will be cash positive in Year 3. We are happy to take our time here as it is due to our choice to start sales slowly in order to work closely and effectively with our first customers. After Year 3, however, inwards cash flows from existing, repeated and new leases will scale massively ending Year 5 with over £1.3m in hand. A full analysis of yearly cash flows can be found within the Appendices.

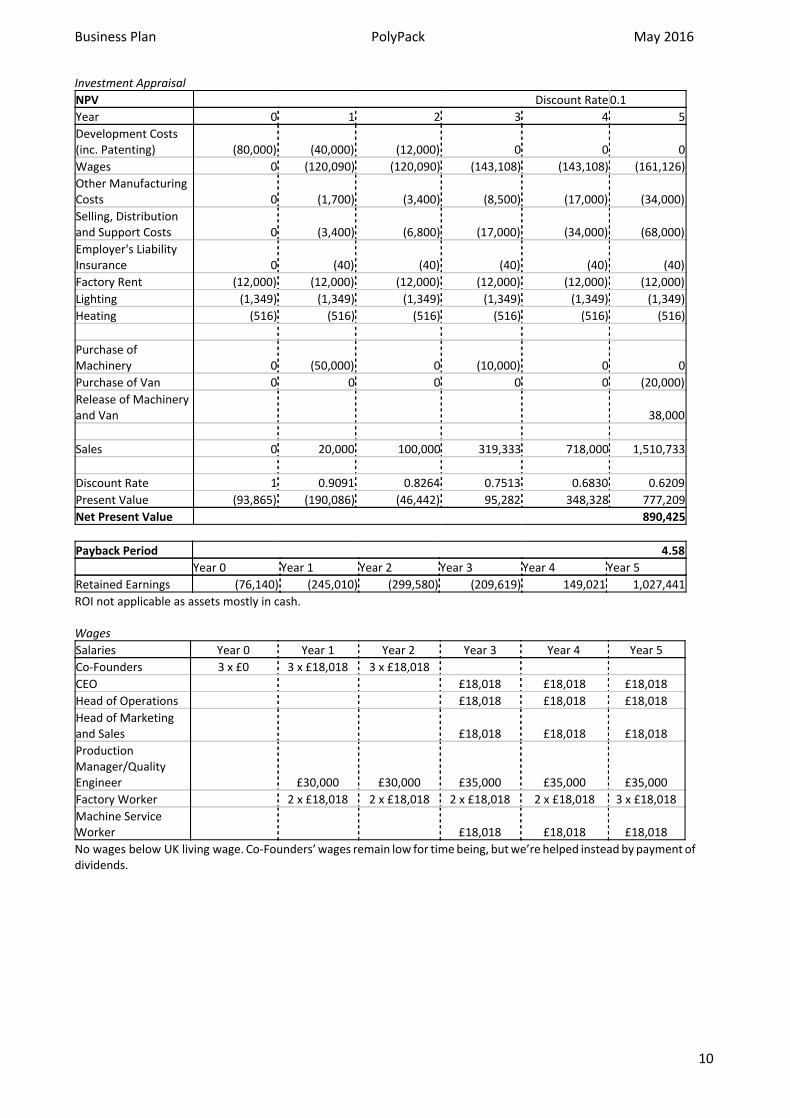

Our expected payback period is 4.58 years and profits are expected to increase rapidly after the payback period as outlined in the P&L account in the Appendices. The net present value up to Year 5 is around £900,000 with room for substantial increases after Year 5 as yearly profits enter the millions. After Year 5 we expect to use our profits in order to develop and expand business.

Financial Requirements

PolyPack will be looking for funding solely from investors forgoing financing through debt aiming for £200,000 in our first round in Year 0. In Year 1, when the milestones of having a marketready product and finding the perfect development partner have been met (signalling the future success of PolyPack), we will seek a further £200,000. We will aim to retain at least 60% of equity between the three CoFounders, gaining the total outside investment of £400,000 from at most 40% of the company. Shareholders will be rewarded dividends totalling 10% of all yearly profits.

During Year 2, PolyPack will cease to rely on the contributions of our investors to remain cash positive. The use of these contributions during Years 0, 1 and 2 is outlined to the right. All sales and lease revenues until the end of Year 2 are contributed to wages so that investors’ contributions are not simply funding the wages of the CoFounders and their employees.

6

Business Plan PolyPack May 2016

Assessment of Risk

PolyPack’s CoFounders are aware that much of what is outlined in this business plan may change radically due to unforeseen circumstances. In order to prepare as fully as possible, areas where these deviations may arise have been identified and scenario planning used to plan our potential reactions. Some examples of these scenarios are shown below.

Scenario A Interest in PolyPack exceeds expectations and demand exceeds capacity in Years 1 or 2

Excess orders will be taken with an agreed delivery date for the PolyPack machine. These orders will require customers to place a deposit and with this extra cash we will act to increase capacity to the required level. If additional cash is needed to meet this requirement we will take out short term loans. Our options to increase capacity include:

1. Overtime work as a short term solution 2. Employing more Factory Workers permanently (if we are confident that this level of demand will

remain) 3. Using Factory Workers from agencies 4. Purchasing more machinery, specifically targeting the bottlenecks 5. Outsourcing some manufacturing if cheaper or if increased capacity can be achieved more

quickly this way

Scenario B After development with partners in Year 1, it becomes clear that the intended market requires an extended period of education in order to appreciate the benefits of PolyPack

We will cease development work on PolyPack but marketing efforts will continue. However, we will attempt to shift our target market to a different segment. An example could be offering PolyPack as an alternative choice of Amazon packaging for their environmentally conscious customers. We may move to a different country (for example Denmark) where cultures and markets are more aware of and active on environmental issues. Further, we could begin research into alternative uses for the fibres made by the PolyProducer: including thermal and acoustic insulation of walls and the production of yarn.

Scenario C World shift from mass consumption to servicisation leading to a decreased market for all packaging solutions

Similarly to the last action listed above, if the decrease in demand for packaging becomes too low for us to feasibly grow our business within our target market we may attempt to expand to cover a larger portion of the overall packaging market or we may work on researching other uses for our fibres and technology as covered above.

Appendices

Market Appraisal

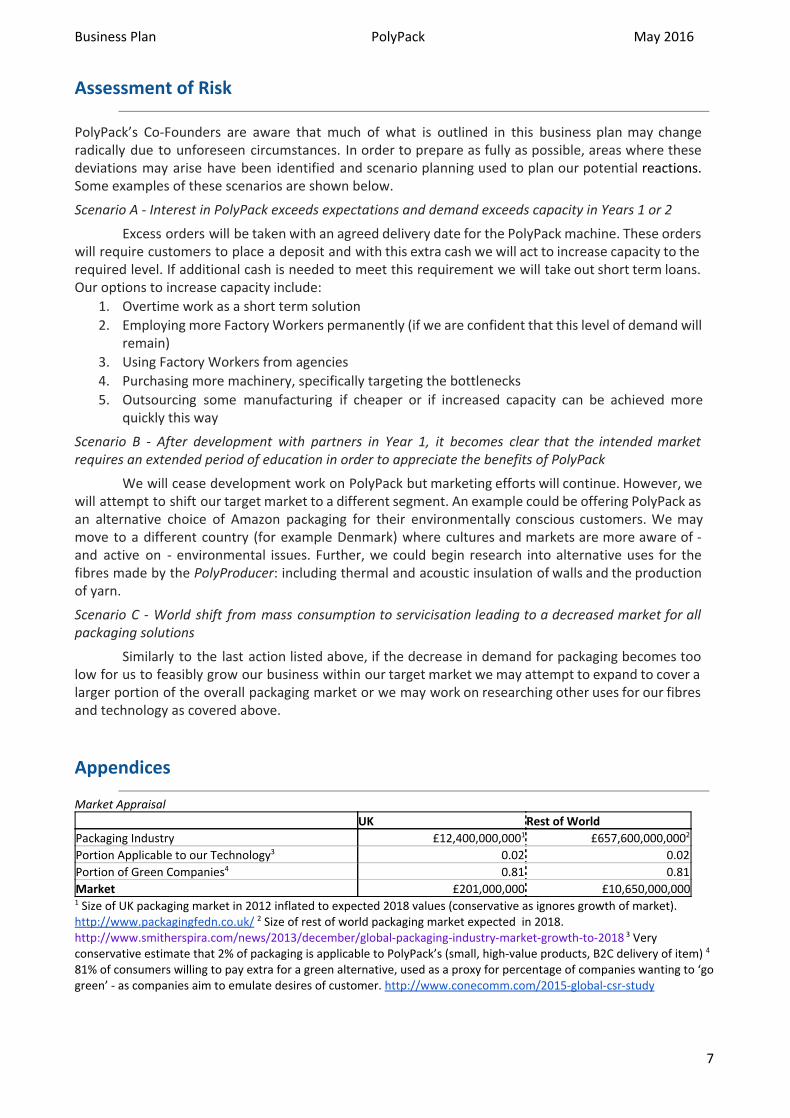

UK Rest of World Packaging Industry £12,400,000,0001 £657,600,000,0002 Portion Applicable to our Technology3 0.02 0.02

Portion of Green Companies4 0.81 0.81

Market £201,000,000 £10,650,000,0001 Size of UK packaging market in 2012 inflated to expected 2018 values (conservative as ignores growth of market). http://www.packagingfedn.co.uk/ 2 Size of rest of world packaging market expected in 2018. http://www.smitherspira.com/news/2013/december/globalpackagingindustrymarketgrowthto2018 3 Very conservative estimate that 2% of packaging is applicable to PolyPack’s (small, highvalue products, B2C delivery of item) 4 81% of consumers willing to pay extra for a green alternative, used as a proxy for percentage of companies wanting to ‘go green’ as companies aim to emulate desires of customer. http://www.conecomm.com/2015globalcsrstudy

7

Business Plan PolyPack May 2016

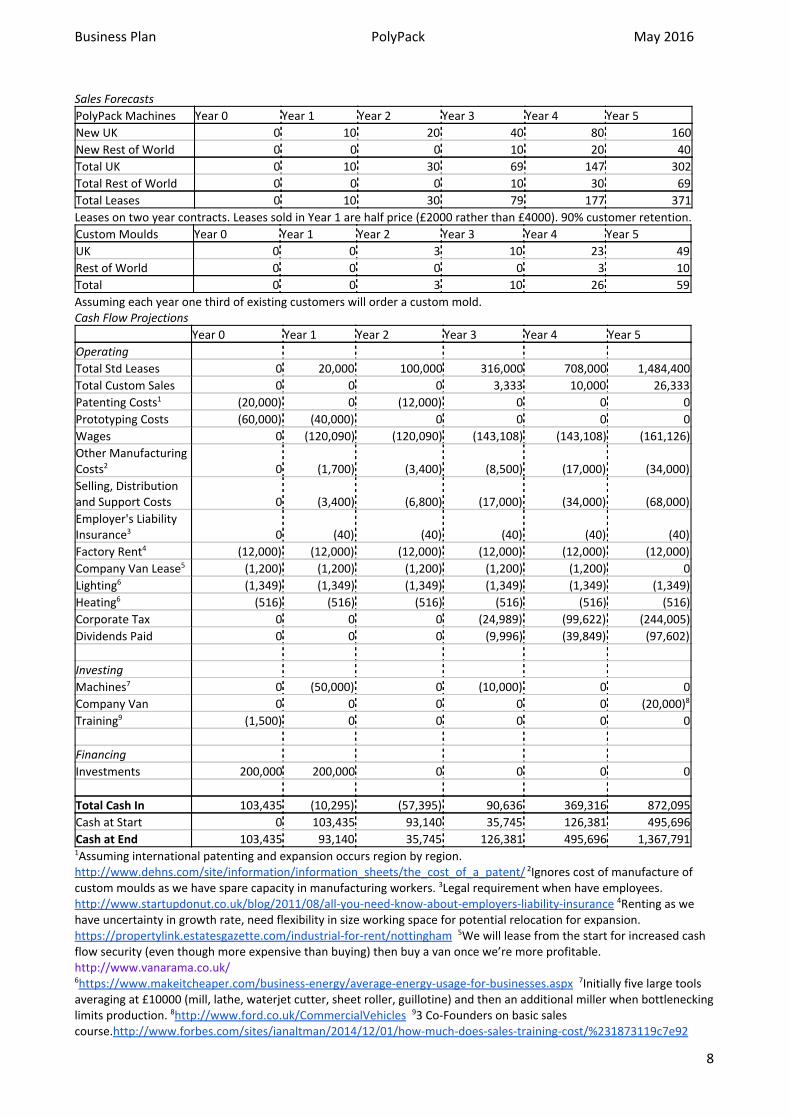

Sales Forecasts

PolyPack Machines Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

New UK 0 10 20 40 80 160

New Rest of World 0 0 0 10 20 40

Total UK 0 10 30 69 147 302

Total Rest of World 0 0 0 10 30 69

Total Leases 0 10 30 79 177 371

Leases on two year contracts. Leases sold in Year 1 are half price (£2000 rather than £4000). 90% customer retention.

Custom Moulds Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

UK 0 0 3 10 23 49

Rest of World 0 0 0 0 3 10

Total 0 0 3 10 26 59

Assuming each year one third of existing customers will order a custom mold. Cash Flow Projections

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Operating

Total Std Leases 0 20,000 100,000 316,000 708,000 1,484,400

Total Custom Sales 0 0 0 3,333 10,000 26,333

Patenting Costs1 (20,000) 0 (12,000) 0 0 0

Prototyping Costs (60,000) (40,000) 0 0 0 0

Wages 0 (120,090) (120,090) (143,108) (143,108) (161,126)

Other Manufacturing Costs2 0 (1,700) (3,400) (8,500) (17,000) (34,000)

Selling, Distribution and Support Costs 0 (3,400) (6,800) (17,000) (34,000) (68,000)

Employer's Liability Insurance3 0 (40) (40) (40) (40) (40)

Factory Rent4 (12,000) (12,000) (12,000) (12,000) (12,000) (12,000)

Company Van Lease5 (1,200) (1,200) (1,200) (1,200) (1,200) 0

Lighting6 (1,349) (1,349) (1,349) (1,349) (1,349) (1,349)

Heating6 (516) (516) (516) (516) (516) (516)

Corporate Tax 0 0 0 (24,989) (99,622) (244,005)

Dividends Paid 0 0 0 (9,996) (39,849) (97,602)

Investing

Machines7 0 (50,000) 0 (10,000) 0 0

Company Van 0 0 0 0 0 (20,000)8 Training9 (1,500) 0 0 0 0 0

Financing

Investments 200,000 200,000 0 0 0 0

Total Cash In 103,435 (10,295) (57,395) 90,636 369,316 872,095

Cash at Start 0 103,435 93,140 35,745 126,381 495,696

Cash at End 103,435 93,140 35,745 126,381 495,696 1,367,7911Assuming international patenting and expansion occurs region by region. http://www.dehns.com/site/information/information_sheets/the_cost_of_a_patent/ 2Ignores cost of manufacture of custom moulds as we have spare capacity in manufacturing workers. 3Legal requirement when have employees. http://www.startupdonut.co.uk/blog/2011/08/allyouneedknowaboutemployersliabilityinsurance 4Renting as we have uncertainty in growth rate, need flexibility in size working space for potential relocation for expansion. https://propertylink.estatesgazette.com/industrialforrent/nottingham 5We will lease from the start for increased cash flow security (even though more expensive than buying) then buy a van once we’re more profitable. http://www.vanarama.co.uk/ 6https://www.makeitcheaper.com/businessenergy/averageenergyusageforbusinesses.aspx 7Initially five large tools averaging at £10000 (mill, lathe, waterjet cutter, sheet roller, guillotine) and then an additional miller when bottlenecking limits production. 8http://www.ford.co.uk/CommercialVehicles 93 CoFounders on basic sales course.http://www.forbes.com/sites/ianaltman/2014/12/01/howmuchdoessalestrainingcost/%231873119c7e92

8

Business Plan PolyPack May 2016

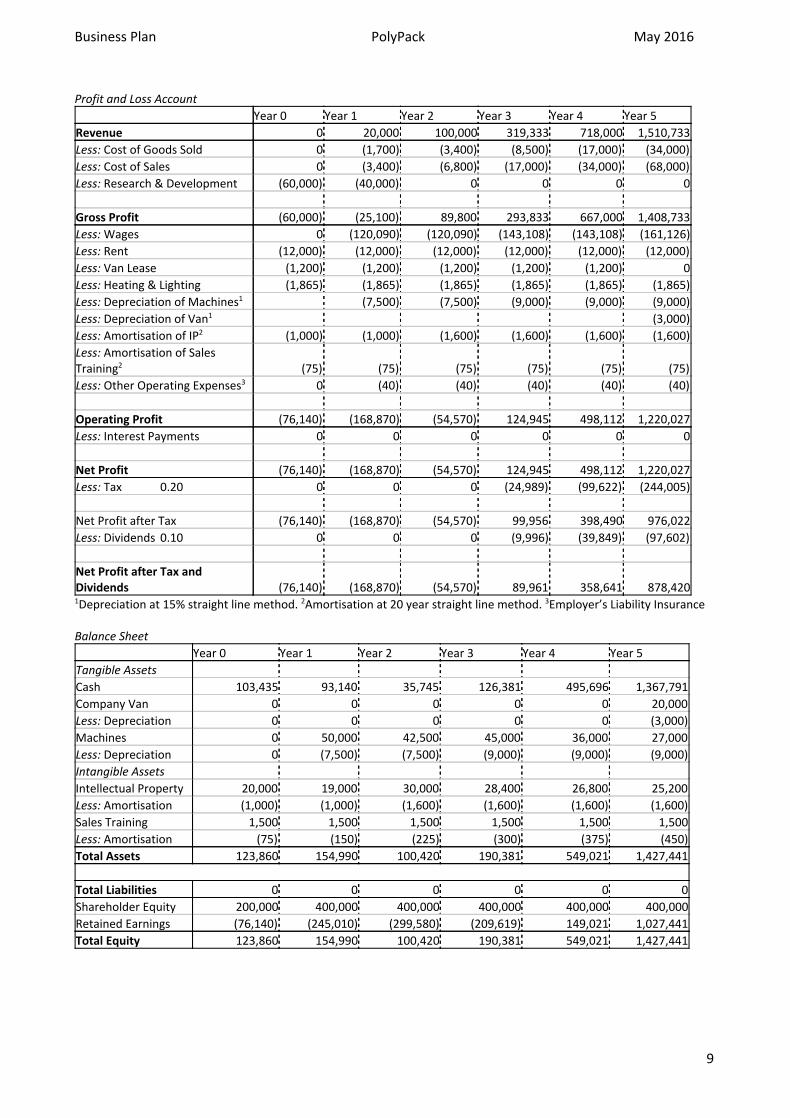

Profit and Loss Account

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Revenue 0 20,000 100,000 319,333 718,000 1,510,733

Less: Cost of Goods Sold 0 (1,700) (3,400) (8,500) (17,000) (34,000)

Less: Cost of Sales 0 (3,400) (6,800) (17,000) (34,000) (68,000)

Less: Research & Development (60,000) (40,000) 0 0 0 0

Gross Profit (60,000) (25,100) 89,800 293,833 667,000 1,408,733

Less: Wages 0 (120,090) (120,090) (143,108) (143,108) (161,126)

Less: Rent (12,000) (12,000) (12,000) (12,000) (12,000) (12,000)

Less: Van Lease (1,200) (1,200) (1,200) (1,200) (1,200) 0

Less: Heating & Lighting (1,865) (1,865) (1,865) (1,865) (1,865) (1,865)

Less: Depreciation of Machines1 (7,500) (7,500) (9,000) (9,000) (9,000)

Less: Depreciation of Van1 (3,000)

Less: Amortisation of IP2 (1,000) (1,000) (1,600) (1,600) (1,600) (1,600)

Less: Amortisation of Sales Training2 (75) (75) (75) (75) (75) (75)

Less: Other Operating Expenses3 0 (40) (40) (40) (40) (40)

Operating Profit (76,140) (168,870) (54,570) 124,945 498,112 1,220,027

Less: Interest Payments 0 0 0 0 0 0

Net Profit (76,140) (168,870) (54,570) 124,945 498,112 1,220,027

Less: Tax 0.20 0 0 0 (24,989) (99,622) (244,005)

Net Profit after Tax (76,140) (168,870) (54,570) 99,956 398,490 976,022

Less: Dividends 0.10 0 0 0 (9,996) (39,849) (97,602)

Net Profit after Tax and Dividends (76,140) (168,870) (54,570) 89,961 358,641 878,4201Depreciation at 15% straight line method. 2Amortisation at 20 year straight line method. 3Employer’s Liability Insurance Balance Sheet

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Tangible Assets

Cash 103,435 93,140 35,745 126,381 495,696 1,367,791

Company Van 0 0 0 0 0 20,000

Less: Depreciation 0 0 0 0 0 (3,000)

Machines 0 50,000 42,500 45,000 36,000 27,000

Less: Depreciation 0 (7,500) (7,500) (9,000) (9,000) (9,000)

Intangible Assets

Intellectual Property 20,000 19,000 30,000 28,400 26,800 25,200

Less: Amortisation (1,000) (1,000) (1,600) (1,600) (1,600) (1,600)

Sales Training 1,500 1,500 1,500 1,500 1,500 1,500

Less: Amortisation (75) (150) (225) (300) (375) (450)

Total Assets 123,860 154,990 100,420 190,381 549,021 1,427,441

Total Liabilities 0 0 0 0 0 0

Shareholder Equity 200,000 400,000 400,000 400,000 400,000 400,000

Retained Earnings (76,140) (245,010) (299,580) (209,619) 149,021 1,027,441

Total Equity 123,860 154,990 100,420 190,381 549,021 1,427,441

9

Business Plan PolyPack May 2016

Investment Appraisal

NPV Discount Rate 0.1

Year 0 1 2 3 4 5

Development Costs (inc. Patenting) (80,000) (40,000) (12,000) 0 0 0

Wages 0 (120,090) (120,090) (143,108) (143,108) (161,126)

Other Manufacturing Costs 0 (1,700) (3,400) (8,500) (17,000) (34,000)

Selling, Distribution and Support Costs 0 (3,400) (6,800) (17,000) (34,000) (68,000)

Employer's Liability Insurance 0 (40) (40) (40) (40) (40)

Factory Rent (12,000) (12,000) (12,000) (12,000) (12,000) (12,000)

Lighting (1,349) (1,349) (1,349) (1,349) (1,349) (1,349)

Heating (516) (516) (516) (516) (516) (516)

Purchase of Machinery 0 (50,000) 0 (10,000) 0 0

Purchase of Van 0 0 0 0 0 (20,000)

Release of Machinery and Van 38,000

Sales 0 20,000 100,000 319,333 718,000 1,510,733

Discount Rate 1 0.9091 0.8264 0.7513 0.6830 0.6209

Present Value (93,865) (190,086) (46,442) 95,282 348,328 777,209

Net Present Value 890,425

Payback Period 4.58 Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Retained Earnings (76,140) (245,010) (299,580) (209,619) 149,021 1,027,441

ROI not applicable as assets mostly in cash. Wages

Salaries Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

CoFounders 3 x £0 3 x £18,018 3 x £18,018

CEO £18,018 £18,018 £18,018

Head of Operations £18,018 £18,018 £18,018

Head of Marketing and Sales £18,018 £18,018 £18,018

Production Manager/Quality Engineer £30,000 £30,000 £35,000 £35,000 £35,000

Factory Worker 2 x £18,018 2 x £18,018 2 x £18,018 2 x £18,018 3 x £18,018

Machine Service Worker £18,018 £18,018 £18,018

No wages below UK living wage. CoFounders’wages remain low for timebeing, butwe’re helped instead by payment of dividends.

10

Related Documents