Political economy of banking (financial sector) regulation – fighting the past wars Topic 1 – is it fair to blame banks for the past crisis? Chronology of events, factors … Topic 2 – moral hazard and the issue of size Topic 3 – the global regulatory tsunami – facts and impacts Topic 4 – irresponsible consumers? Are we coming close (or past) the limits of reasonable consumer protection? Consumer protection and free market. Moral hazard. Topic 5 – the specific Czech case – are we really so different? Topic 6 – is Banking Union (in the EU) THE answer?

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Political economy of banking (financial sector) regulation – fighting the past wars

Topic 1 – is it fair to blame banks for the past crisis? Chronology of events, factors …

Topic 2 – moral hazard and the issue of size

Topic 3 – the global regulatory tsunami – facts and impacts

Topic 4 – irresponsible consumers? Are we coming close (or past) the limits of reasonable consumer protection? Consumer protection and free market. Moral hazard.

Topic 5 – the specific Czech case – are we really so different?

Topic 6 – is Banking Union (in the EU) THE answer?

Topic 7 – the raid of non bank financial entities into – what was until recently – banking business: new opportunities for regulatory arbitrage?

Hopes and reality• „Spain is not Greece“ Elena Salgado, Spanish minister of finance 2/2010• „Portugal is not Greece“ The Economist 4/2010• „Greece is not Ireland“ George Papaconstantinos, Greek minister of

finance, 11/2010• „Ireland is not Greece„ Brian Lenihan, Irish minister of finance, 11/2010• “Ireland is not Spain or Portugal” - Angel Gurria, general secretary OECD,

11/2010• “Spain is not Ireland or Portugal” - Elena Salgado, Spanish minister of

finance, 11/2010• „Italy is not Spain” - Ed Parker, Fitch, 6/2012• “Spain is not Uganda” – Mariano Rajoy, Spanish prime minister, 6/2012• “Uganda does not intend to be like Spain” - Sam Kutesa, Ugandian

minister of foreign affairs, 6/2012

Let us not forget, the financial crisis had its roots in the decision by Congress to embark on a course of social justice to get everyone that wanted a home into one, regardless of whether or not they could afford it. (Ed Royce,US politician)

Derivatives are financial weapons of mass destruction. (Warren Buffett)

Topic 1 (crisis and banks)Prologue

• A crisis is a more or less drastic correction of imbalances, created in previous times …

• In most cases, a crisis is generated by an overheating of the economy, apparent through „bubbles“ on various markets

• Unsustainable deviations are misinterpreted as trends• But, at the end of the day, the disciplining role (power) of the market can

hardly be avoided …• Although crises may be of a diverse nature (monetary, banking, debt),

they have all one thing in common: risks are being underestimated, old truth is being (intentionally) overlooked, prudential behaviour weakened

The roots of crisis are always found in „good times“, when the world looks pretty and sweet

It has been no different last time and banks should rightly be allocated part of the responsibility for it (but not all of the

responsibility)

1.1. But let's take it from the beginning – the recent episode … macroeconomic developments and policies

• A prolonged period of low inflation, implying low profit returns on investment

↓- Mistakes of central bankers, overlooking the bubbles (and the message

these bubbles were sending to policy makers), a misinterpretation of the long period of low inflation …

↓

- Investors in search for higher risk- Creativity in new and complex investment products, offering higher

returns (and distributing – hiding – (excessive) risks- In an environment of unshakable trust in an ever growing global economy,

driven by new global players (mostly the BRICs) showing an unlimited hunger for growth

- The psychology of investors „if they can make it, we have to make it as well, if they succeeded, we will as well“

- Expectation of small investors, depositors, shareholders: all of them willing to „be there, get their own part of the cake“ – lesson of human psychology: would anyone resist to become rich, if risks seem to have evaporated from the landscape?

1.2. The financial (banking) causes:

• Enormous diversification of financial intermediary, an extremely robust surge of the non-banking intermediary (partially in response to ever increasing limitation imposed by regulators

• Development of a „shadow“ (or parallel) banking, various special purpose vehicles (SPVs), investment banks (detached from primary deposits and with huge leverage ratios), investment funds, hedge funds

• A failure to properly manage risk in the credit process: the mortgage provider would, for instance, sell, within the six months, the instrument to a third party: thus, his motives to assess the creditworthiness of clients went severely weakened

• Expectations and instructions of bank shareholders to managements – pressure on profits, shortening of investment horizons

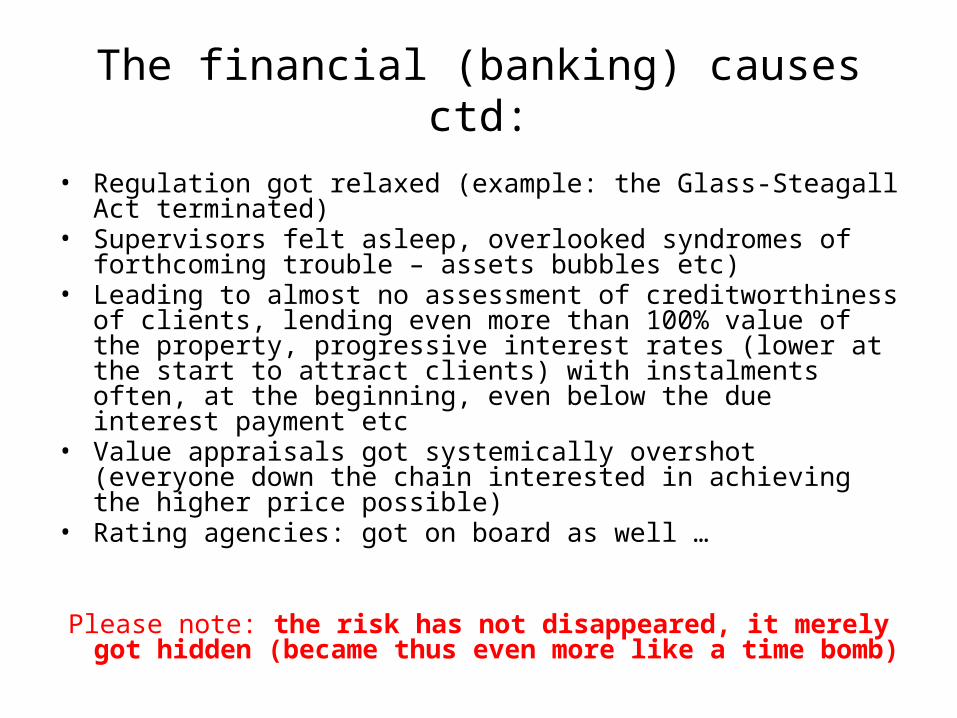

The financial (banking) causes ctd:

• Regulation got relaxed (example: the Glass-Steagall Act terminated)• Supervisors felt asleep, overlooked syndromes of forthcoming trouble –

assets bubbles etc)• Leading to almost no assessment of creditworthiness of clients, lending

even more than 100% value of the property, progressive interest rates (lower at the start to attract clients) with instalments often, at the beginning, even below the due interest payment etc

• Value appraisals got systemically overshot (everyone down the chain interested in achieving the higher price possible)

• Rating agencies: got on board as well …

Please note: the risk has not disappeared, it merely got hidden (became thus even more like a time bomb)

1.3. Role of institutions (governments, regulators, supervisors): far from being innocent

• Community Reinvestment Act (1977, J. Carter): support access to housing

• Fannie Mae and Freddie Mac (government sponsored enterprises, purpose: access to housing for low income people)

• Commodity Futures Modernisation Act (2000): derivates exempted from regulatory requirements and supervision and minimum reserve requirements

• 2002: FED terminates supervision of mortgage companies• 2004: Securities and Exchange Commission grants an

exemption from the required debt-to-net capital ratio to Goldman Sachs, Merrill Lynch, Lehman Brothers, Bear Sterns, Morgan Stanley (the allowed leverage ratio increased from 12 to 40)

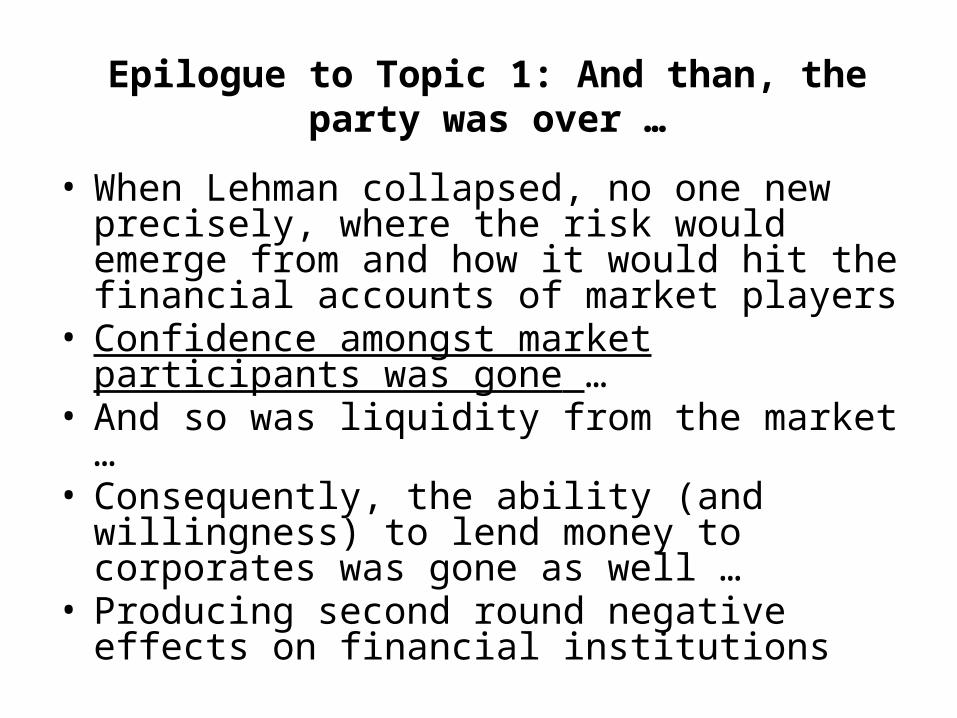

Epilogue to Topic 1: And than, the party was over …

• When Lehman collapsed, no one new precisely, where the risk would emerge from and how it would hit the financial accounts of market players

• Confidence amongst market participants was gone …• And so was liquidity from the market …• Consequently, the ability (and willingness) to lend

money to corporates was gone as well …• Producing second round negative effects on financial

institutions

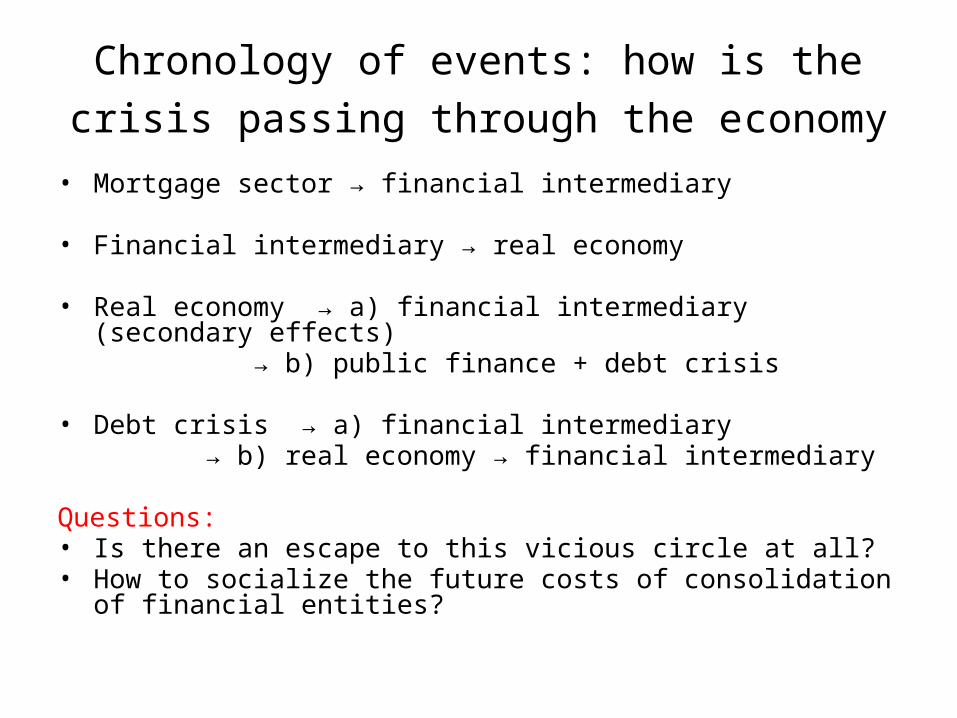

Chronology of events: how is the crisis passing through the economy

• Mortgage sector → financial intermediary

• Financial intermediary → real economy

• Real economy → a) financial intermediary (secondary effects) → b) public finance + debt crisis

• Debt crisis → a) financial intermediary → b) real economy → financial intermediary

Questions:• Is there an escape to this vicious circle at all?• How to socialize the future costs of consolidation of financial entities?

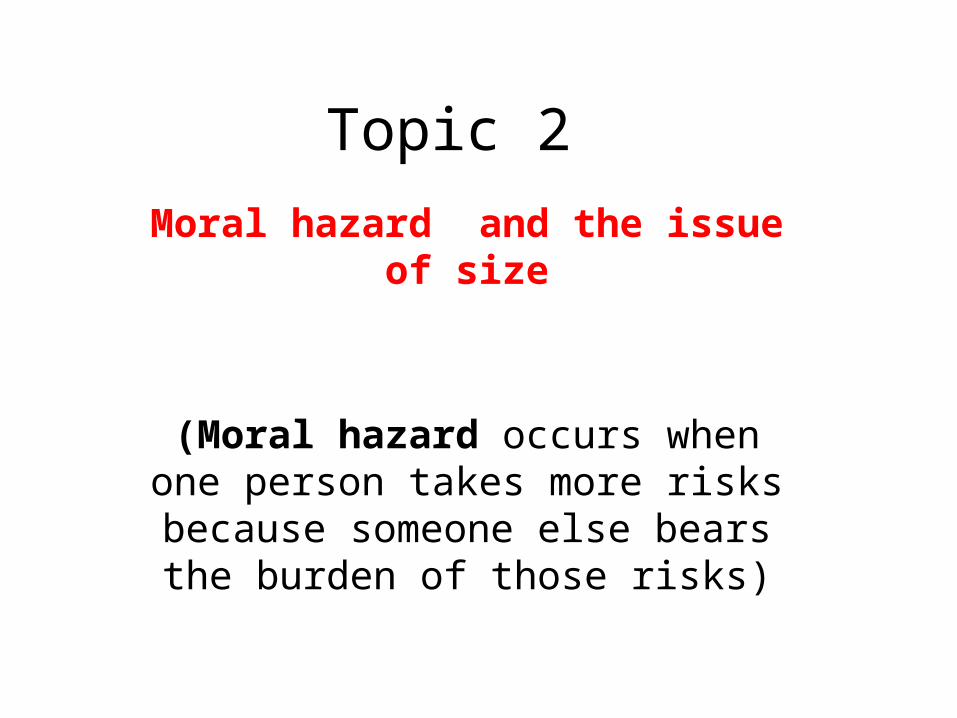

Topic 2

Moral hazard and the issue of size

(Moral hazard occurs when one person takes more risks because

someone else bears the burden of those risks)

Banking assets to GDP represent 150% in the USA

Assets of commercial banks in EU and in USA

(thousands of billions USD)

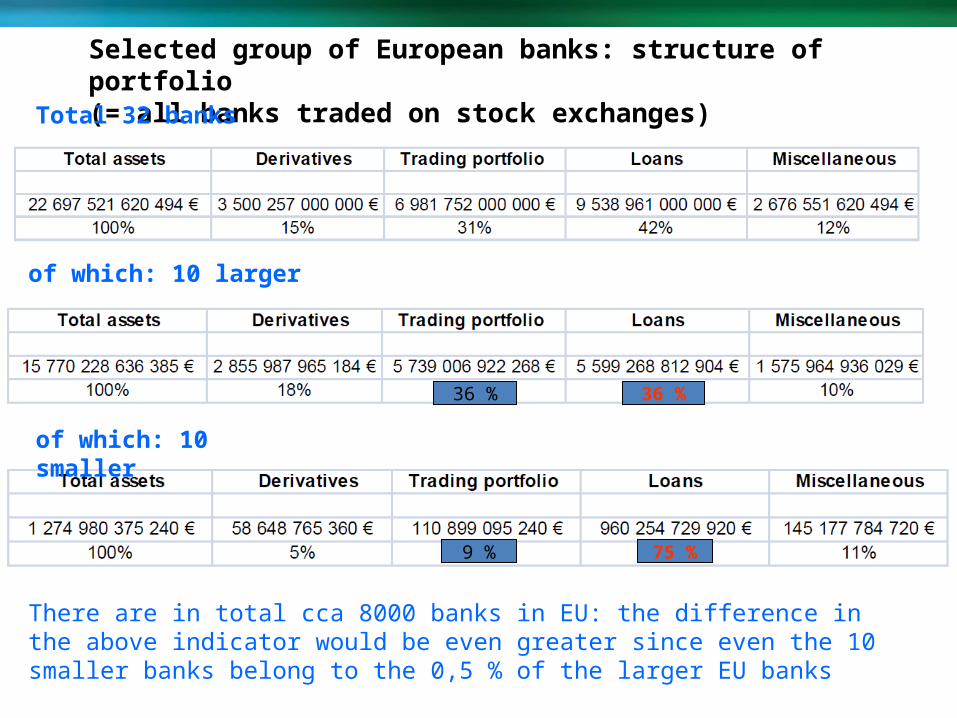

Selected group of European banks: structure of portfolio (= all banks traded on stock exchanges)

Total 32 banks

of which: 10 larger

of which: 10 smaller

36 %

9 %

36 %

75 %

There are in total cca 8000 banks in EU: the difference in the above indicator would be even greater since even the 10 smaller banks belong to the 0,5 % of the larger EU banks

Remember the term Moral Hazard – we will use it again in a moment

Topic 3

The global regulatory tsunami – facts and impacts

19

Key regulatory initiatives

CRD IV/Basel III

Corporate Governance

and Remuneration

Policies

Revision of MiFID and

Market Abuse Directive

SIFI

Bank Recovery and

Resolution

Deposit Guarantee and

Investor Compensation

Schemes

Consumer Protection

Financial Transaction /Activity Tax

The European Banking Federation (of which we are members) is currently following 150 different regulatory initiatives

Examples• CRDIV

– Capital adequacy– Liquidity requirements– Leverage ratio– corporate governance– Compensation schemes

• Own funds, liauidity risk management, large exposures, pillar 2, financial conglomerates, macro-prudentail supervision, securitisation,

• SIFI• DGS• MiFID (financial instruments)• FTT• Sectoral taxes• CDS (credit default swaps)• Derivatives regulation• Crisis resolution and recovery• Mortgage directive• Consumer credit directive• EMIR (market infrstructure)• Payment services• Accounting standards

– IFRS• Reporting standards• Audit rules• Consumer protection

– Financial inclusion– Switching– Tying

• AML• PRIPS (packaged retail investment products)• SEPA• Interest rate benchmarks

New institutions

• EBA• ESMA• EIOPA• ECB• European resolution authority• ESM• EC• ESBR European board for systemic risk)

Background Response to the crisis AIM - strengthen the resilience of the banking sector → reduce

the probability and severity of future financial crises and remove current regulation shortcomings

RISKS: Adoption of measures that would not be taken in a more stable

period. Adoption under time pressure raises doubts about the proper

calibration, timing and globally consistent implementation. Limiting the banks ability to grant credits to individuals and/or

companies and/or governments → negative impact on real economy.

23

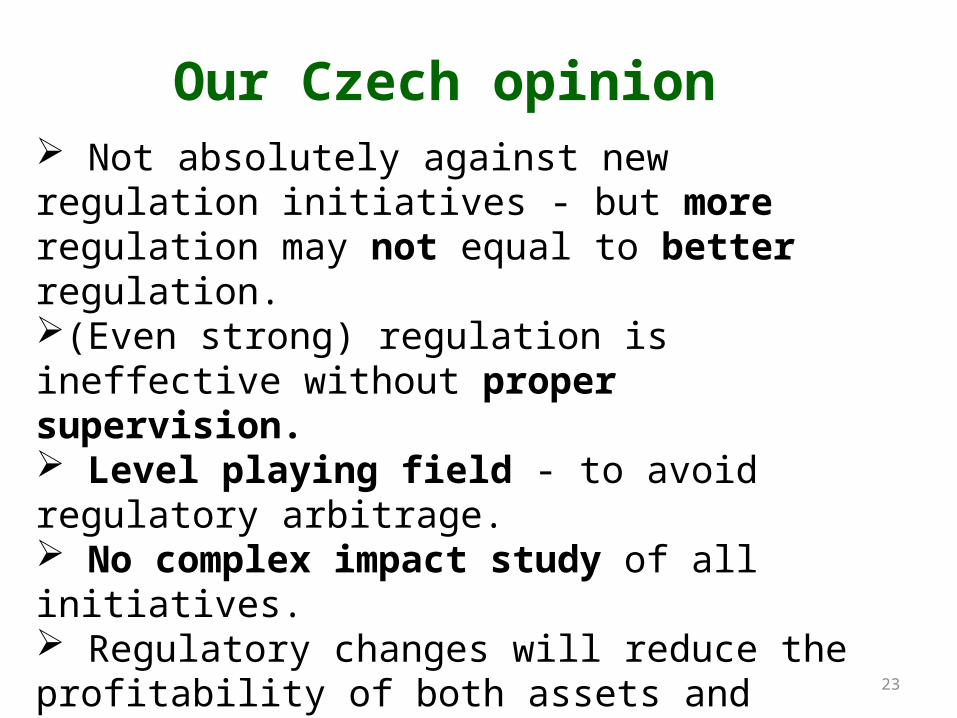

Our Czech opinion

Not absolutely against new regulation initiatives - but more regulation may not equal to better regulation.(Even strong) regulation is ineffective without proper supervision. Level playing field - to avoid regulatory arbitrage. No complex impact study of all initiatives. Regulatory changes will reduce the profitability of both assets and capital; the consequences thereof will fall upon not only shareholders but also clients, and thus, in the broader context, upon the entire economy.

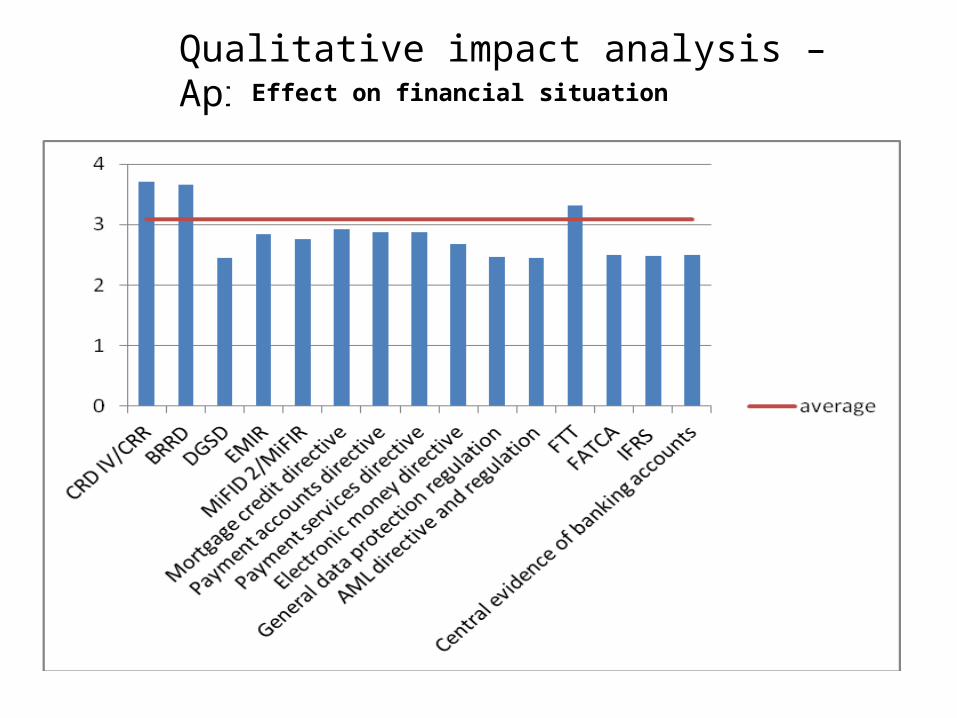

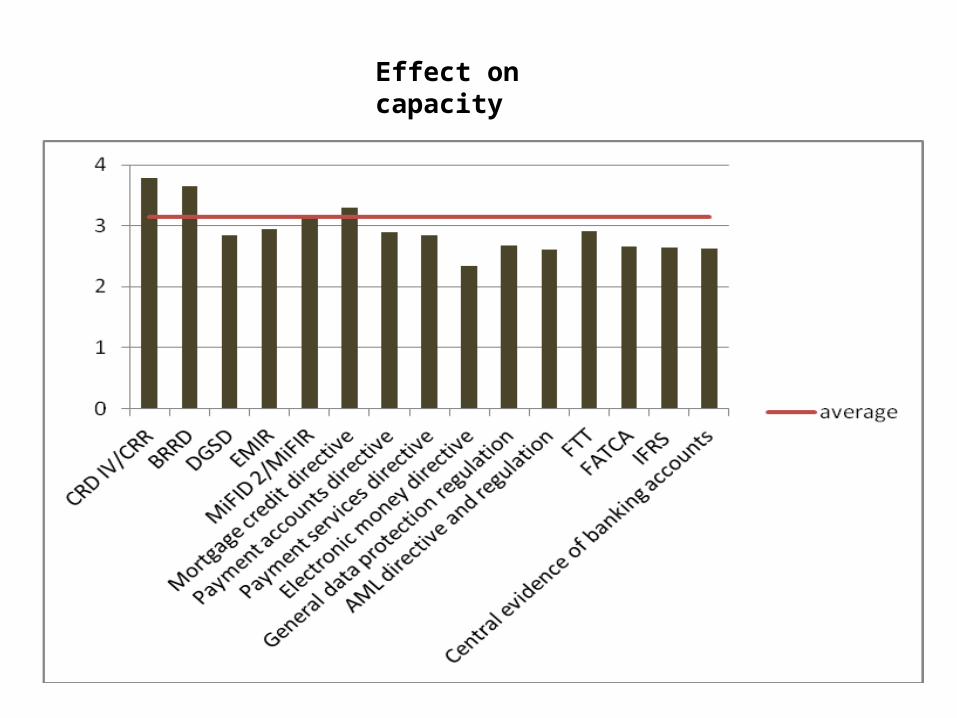

Qualitative impact analysis – April 2015Effect on financial situation

Effect on capacity

Topic 4 – irresponsible consumers?

Are we coming close (or past) the limits of reasonable consumer protection?

Consumer protection and free market. Moral hazard.

Examples• Deposit insurance• Haircuts of consumer debt• Creating funds to help repay debt• Consumer insolvency

Items for discussion:• Administrative controls of interest rates?

Topic 5 – the specific Czech case

Are we really so different?

Deposit/Loan ratio

Total private debt/GDP

Conclusion to Topic 5

• Indeed, we ARE different: better• In our case, the regulatory tsunami is a cure of a very healthy patient• One size does not fit all (even by far not)• Compliance costs vs global competitive position of the Czech banking industry

Single EU supervisor

Single EU deposit

guarantee scheme

Common resolution authority and fund

Single rule book

Banking Union

Topic 6 – is Banking Union (in the EU) THE answer?

120 banks are directly supervised by the ECB

Benefits and risks• less regulatory arbitrage• less compliance costs• single set of rules – better competitive environment• simplified management of activities at group level• supervision immune to political pressure • potential risk to local (remote, small) market, especially where entity is a DiSIF• distant supervision may not be sensitive to local specifics• local authorities short of one key instrument to protect stablity of local market

Topic 7

The raid of non bank financial entities into – what was until recently – banking business: new opportunities for regulatory arbitrage?

Related Documents