STRICTLY PRIVATE AND CONFIDENTIAL Katy Hedlund, J.P. Morgan High Yield and Leveraged Loan Capital Markets PLI Leveraged Finance Market Update Pages May 2020

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L

Katy Hedlund, J.P. Morgan High Yield and Leveraged Loan Capital Markets

PLI Leveraged Finance Market Update Pages May 2020

C O N F I D E N T I A L

This presentation was prepared exclusively for the benefit and internal use of the J.P. Morgan client to whom it is directly addressed and delivered (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating, on a preliminary basis, the feasibility of a possible transaction or transactions and does not carry any right of publication or disclosure, in whole or in part, to any other party. This presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by J.P. Morgan. Neither this presentation nor any of its contents may be disclosed or used for any other purpose without the prior written consent of J.P. Morgan. The information in this presentation is based upon any management forecasts supplied to us and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. J.P. Morgan’s opinions and estimates constitute J.P. Morgan’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Company or which was otherwise reviewed by us. In addition, our analyses are not and do not purport to be appraisals of the assets, stock, or business of the Company or any other entity. J.P. Morgan makes no representations as to the actual value which may be received in connection with a transaction nor the legal, tax or accounting effects of consummating a transaction. Unless expressly contemplated hereby, the information in this presentation does not take into account the effects of a possible transaction or transactions involving an actual or potential change of control, which may have significant valuation and other effects. Notwithstanding anything herein to the contrary, the Company and each of its employees, representatives or other agents may disclose to any and all persons, without limitation of any kind, the U.S. federal and state income tax treatment and the U.S. federal and state income tax structure of the transactions contemplated hereby and all materials of any kind (including opinions or other tax analyses) that are provided to the Company relating to such tax treatment and tax structure insofar as such treatment and/or structure relates to a U.S. federal or state income tax strategy provided to the Company by J.P. Morgan. J.P. Morgan's policies on data privacy can be found at http://www.jpmorgan.com/pages/privacy. J.P. Morgan is a party to the SEC Research Settlement and as such, is generally not permitted to utilize the firm's research capabilities in pitching for investment banking business. All views contained in this presentation are the views of J.P. Morgan’s Investment Bank, not the Research Department. J.P. Morgan’s policies prohibit employees from offering, directly or indirectly, a favorable research rating or specific price target, or offering to change a rating or price target, to a subject company as consideration or inducement for the receipt of business or for compensation. J.P. Morgan also prohibits its research analysts from being compensated for involvement in investment banking transactions except to the extent that such participation is intended to benefit investors. Changes to Interbank Offered Rates (IBORs) and other benchmark rates: Certain interest rate benchmarks are, or may in the future become, subject to ongoing international, national and other regulatory guidance, reform and proposals for reform. For more information, please consult: https://www.jpmorgan.com/global/disclosures/interbank_offered_rates JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters included herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone not affiliated with JPMorgan Chase & Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties. J.P. Morgan is a marketing name for investment businesses of JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Securities, syndicated loan arranging, financial advisory, lending, derivatives and other investment banking and commercial banking activities are performed by a combination of J.P. Morgan Securities LLC, J.P. Morgan Securities plc, J.P. Morgan AG, JPMorgan Chase Bank, N.A. and the appropriately licensed subsidiaries and affiliates of JPMorgan Chase & Co. worldwide. J.P. Morgan deal team members may be employees of any of the foregoing entities. J.P. Morgan Securities plc is authorized by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. J.P. Morgan AG is authorized by the German Federal Financial Supervisory Authority (BaFin) and regulated by BaFin and the German Central Bank (Deutsche Bundesbank). For information on any J.P. Morgan German legal entity see: https://www.jpmorgan.com/country/US/en/disclosures/legal-entity-information#germany. For information on any other J.P. Morgan legal entity see: https://www.jpmorgan.com/country/GB/EN/disclosures/investment-bank-legal-entity-disclosures. This presentation does not constitute a commitment by any J.P. Morgan entity to underwrite, subscribe for or place any securities or to extend or arrange credit or to provide any other services. Copyright 2020 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability.

C O N F I D E N T I A L

nCoV Globally Confirmed Cases

3,226

2,912 1.52%

0.64%

0.5%

0.7%

0.9%

1.1%

1.3%

1.5%

1.7%

2,200

2,400

2,600

2,800

3,000

3,200

3,400

1/31 2/7 2/14 2/21 2/28 3/6 3/13 3/20 3/27 4/3 4/10 4/17 4/24

S&P 500 UST 10yr. 3.2m cases

12k cases

COVID-19 introduced significant volatility in leveraged finance markets

Mac

ro

Since Friday 2/21 LL Avg Price ($10.43)

% at or above

par (38.71%)

Fund Flows ($13.4bn)

CLO issuance $14.3bn

$97.45

$87.04 44.52%

0.10% 0%

10%

20%

30%

40%

50%

$74.00

$79.00

$84.00

$89.00

$94.00

$99.00

1/31 2/7 2/14 2/21 2/28 3/6 3/13 3/20 3/27 4/3 4/10 4/17 4/24

JPM LL Avg. Price % Trading at or Above Par

6.09%

9.25%

472bps

875bps

420bps

520bps

620bps

720bps

820bps

920bps

1020bps

1120bps

1220bps

5.8%

6.8%

7.8%

8.8%

9.8%

10.8%

11.8%

12.8%

1/31 2/7 2/14 2/21 2/28 3/6 3/13 3/20 3/27 4/3 4/10 4/17 4/24

JPM HY YTW JPM HY STW

Hig

h yi

eld

bond

s Le

vera

ged

loan

s

Source: J.P. Morgan, Bloomberg, LevFin Insights, Informa Global Markets Note: All market and issuance data as of 4/30/2020 closing levels; CLO issuance as of 4/27/2020

Since Friday 2/21

SPX (12.74%)

10yr UST (83)bps

VIX 99.94%

WTI (64.71%)

3M LIBOR (112)bps

Since Friday 2/21

HY YTW 339bps

BB YTW 215bps

B YTW 359bps CCC YTW 515bps

HY STW 429bps

Fund Flows $3.4bn

1

C O N F I D E N T I A L

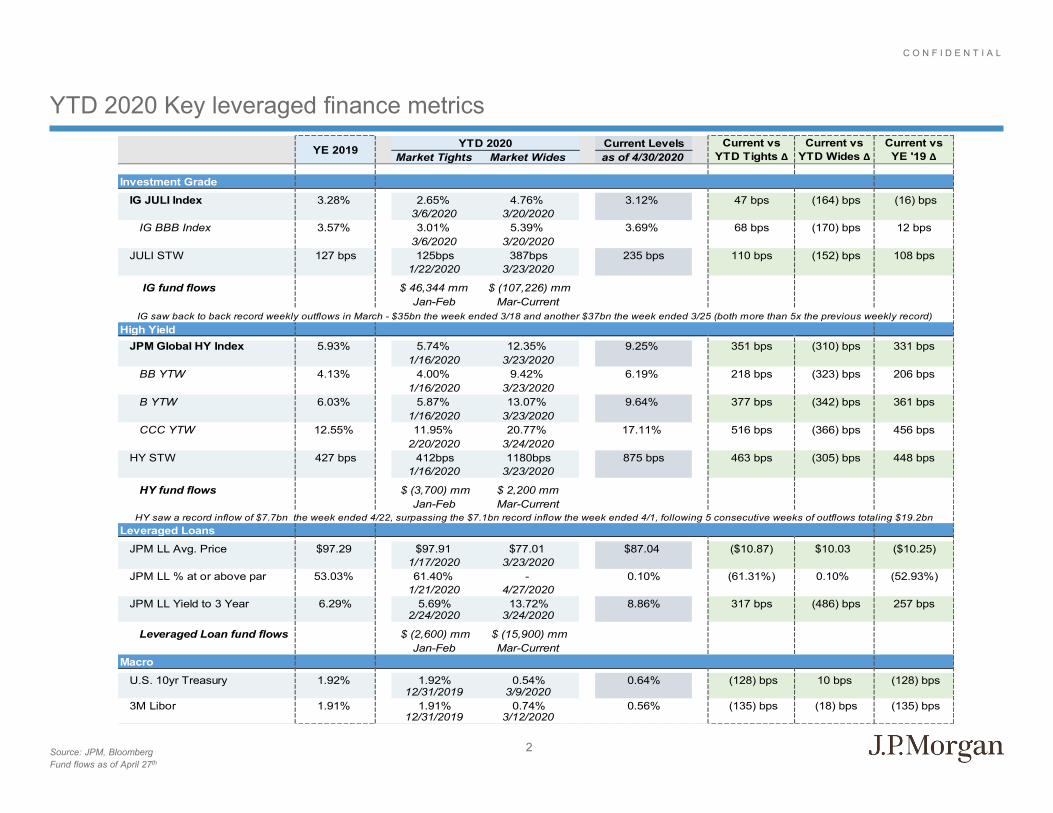

YTD 2020 Key leveraged finance metrics

Source: JPM, Bloomberg Fund flows as of April 27th

YTD 2020 Current LevelsMarket Tights Market Wides as of 4/30/2020

Investment GradeIG JULI Index 3.28% 2.65% 4.76% 3.12% 47 bps (164) bps (16) bps

3/6/2020 3/20/2020IG BBB Index 3.57% 3.01% 5.39% 3.69% 68 bps (170) bps 12 bps

3/6/2020 3/20/2020JULI STW 127 bps 125bps 387bps 235 bps 110 bps (152) bps 108 bps

1/22/2020 3/23/2020

IG fund flows $ 46,344 mm $ (107,226) mmJan-Feb Mar-Current

IG saw back to back record weekly outflows in March - $35bn the week ended 3/18 and another $37bn the week ended 3/25 (both more than 5x the previous weekly record)High Yield

JPM Global HY Index 5.93% 5.74% 12.35% 9.25% 351 bps (310) bps 331 bps1/16/2020 3/23/2020

BB YTW 4.13% 4.00% 9.42% 6.19% 218 bps (323) bps 206 bps1/16/2020 3/23/2020

B YTW 6.03% 5.87% 13.07% 9.64% 377 bps (342) bps 361 bps1/16/2020 3/23/2020

CCC YTW 12.55% 11.95% 20.77% 17.11% 516 bps (366) bps 456 bps2/20/2020 3/24/2020

HY STW 427 bps 412bps 1180bps 875 bps 463 bps (305) bps 448 bps1/16/2020 3/23/2020

HY fund flows $ (3,700) mm $ 2,200 mmJan-Feb Mar-Current

Leveraged LoansJPM LL Avg. Price $97.29 $97.91 $77.01 $87.04 ($10.87) $10.03 ($10.25)

1/17/2020 3/23/2020JPM LL % at or above par 53.03% 61.40% - 0.10% (61.31%) 0.10% (52.93%)

1/21/2020 4/27/2020JPM LL Yield to 3 Year 6.29% 5.69% 13.72% 8.86% 317 bps (486) bps 257 bps

2/24/2020 3/24/2020

Leveraged Loan fund flows $ (2,600) mm $ (15,900) mmJan-Feb Mar-Current

MacroU.S. 10yr Treasury 1.92% 1.92% 0.54% 0.64% (128) bps 10 bps (128) bps

12/31/2019 3/9/20203M Libor 1.91% 1.91% 0.74% 0.56% (135) bps (18) bps (135) bps

12/31/2019 3/12/2020

HY saw a record inflow of $7.7bn the week ended 4/22, surpassing the $7.1bn record inflow the week ended 4/1, following 5 consecutive weeks of outflows totaling $19.2bn

Current vs YTD Tights ΔYE 2019 Current vs

YTD Wides ΔCurrent vs YE '19 Δ

2

C O N F I D E N T I A L

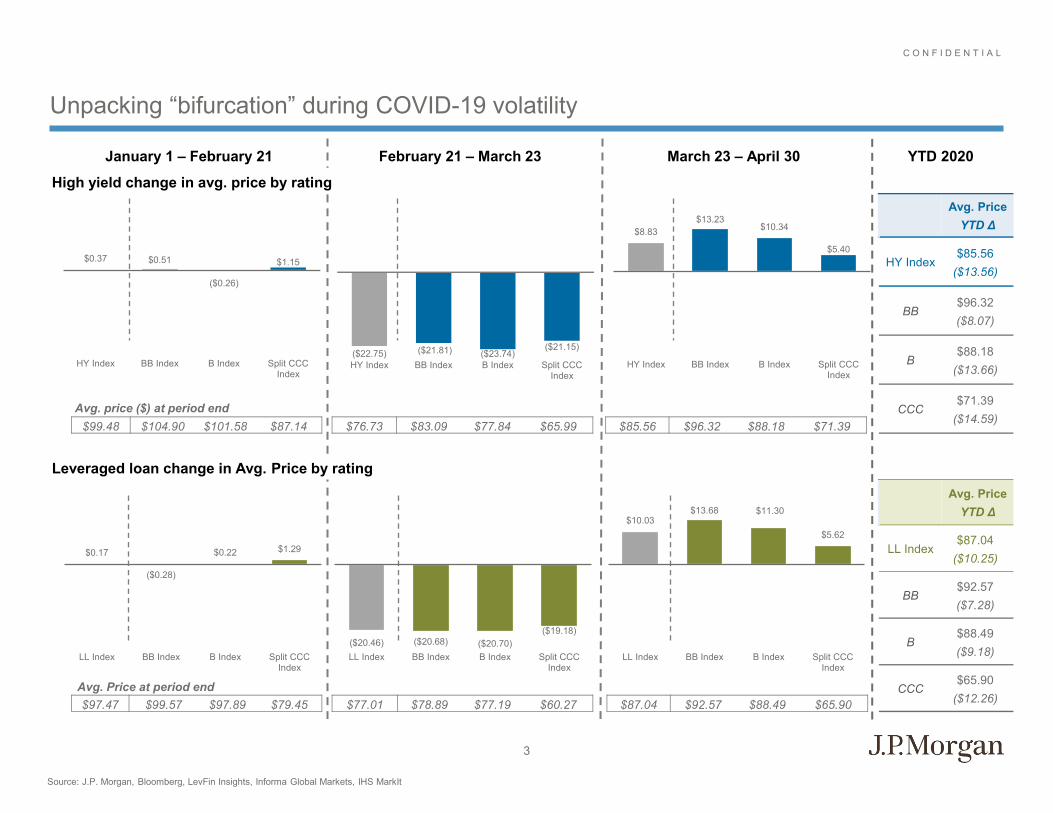

Unpacking “bifurcation” during COVID-19 volatility

Source: J.P. Morgan, Bloomberg, LevFin Insights, Informa Global Markets, IHS MarkIt

$0.37 $0.51

($0.26)

$1.15

HY Index BB Index B Index Split CCCIndex

$0.17

($0.28)

$0.22 $1.29

LL Index BB Index B Index Split CCCIndex

($20.46) ($20.68) ($20.70) ($19.18)

LL Index BB Index B Index Split CCCIndex

$10.03 $13.68 $11.30

$5.62

LL Index BB Index B Index Split CCCIndex

January 1 – February 21 February 21 – March 23 March 23 – April 30

$99.48 $104.90 $101.58 $87.14 $76.73 $83.09 $77.84 $65.99 $85.56 $96.32 $88.18 $71.39

$97.47 $99.57 $97.89 $79.45 $77.01 $78.89 $77.19 $60.27 $87.04 $92.57 $88.49 $65.90

High yield change in avg. price by rating YTD 2020

Avg. Price

YTD Δ

HY Index $85.56

($13.56)

BB $96.32 ($8.07)

B $88.18

($13.66)

CCC $71.39

($14.59)

Avg. Price

YTD Δ

LL Index $87.04

($10.25)

BB $92.57 ($7.28)

B $88.49 ($9.18)

CCC $65.90

($12.26)

Avg. price ($) at period end

Avg. Price at period end

Leveraged loan change in Avg. Price by rating

3

($22.75) ($21.81) ($23.74) ($21.15)

HY Index BB Index B Index Split CCCIndex

$8.83 $13.23

$10.34

$5.40

HY Index BB Index B Index Split CCCIndex

C O N F I D E N T I A L

37%

8%

84%

9% 21%

82%

63%

39%

16%

91% 78%

18% [VALUE]

53%

0% 0% 1% 0%

30-Apr31-DecCOVID-194Q18O&G &China '16

FinancialCrisis

<90 (distressed) 90-100 100+

0.56% 1.91% 1.23% 2.81% 0.62% 1.87%

8.30%

4.38%

12.49% 5.41% 7.19%

20.85% [VALUE]

6.29%

13.72%

8.22% 7.81%

30-Apr31-DecCOVID-194Q18O&G &China '16

FinancialCrisis

LIBOR Implied Spread

875

427

1,180

583

924

1,925

30-Apr31-DecCOVID-194Q18O&G &China '16

FinancialCrisis

5.24%

9.25%

5.93%

12.35% 8.32% 10.49%

20.92%

30-Apr31-DecCOVID-194Q18O&G &China '16

FinancialCrisis

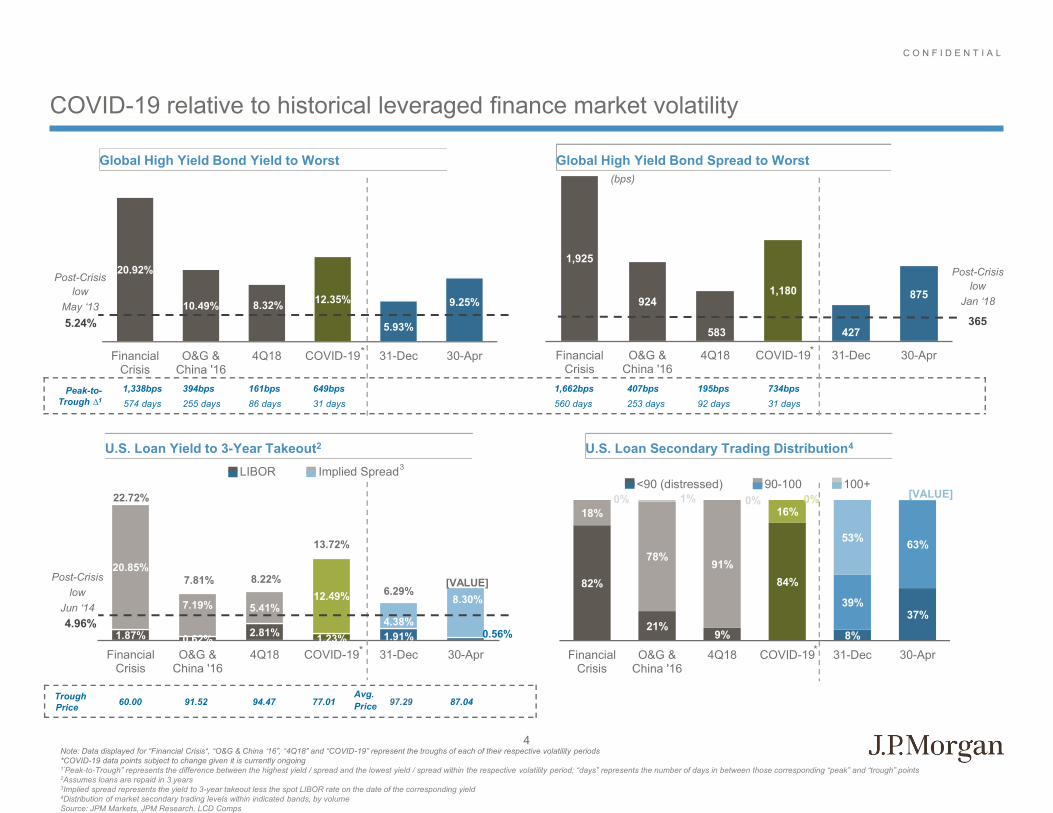

COVID-19 relative to historical leveraged finance market volatility

Global High Yield Bond Spread to Worst

U.S. Loan Yield to 3-Year Takeout2 U.S. Loan Secondary Trading Distribution4

Note: Data displayed for “Financial Crisis“, “O&G & China ‘16”, “4Q18” and “COVID-19” represent the troughs of each of their respective volatility periods *COVID-19 data points subject to change given it is currently ongoing 1”Peak-to-Trough” represents the difference between the highest yield / spread and the lowest yield / spread within the respective volatility period; “days” represents the number of days in between those corresponding “peak” and “trough” points 2Assumes loans are repaid in 3 years 3Implied spread represents the yield to 3-year takeout less the spot LIBOR rate on the date of the corresponding yield

4Distribution of market secondary trading levels within indicated bands, by volume Source: JPM Markets, JPM Research, LCD Comps

Global High Yield Bond Yield to Worst

Peak-to-Trough ∆1

1,338bps 574 days

394bps 255 days

161bps 86 days

649bps 31 days

1,662bps 560 days

407bps 253 days

195bps 92 days

734bps 31 days

Trough Price 60.00 91.52 94.47 77.01 97.29 87.04

(bps)

4.96%

Post-Crisis low

May ‘13

Post-Crisis low

Jun ‘14

365

Post-Crisis low

Jan ‘18

Avg. Price

3

22.72%

* *

* *

4

C O N F I D E N T I A L

The leveraged loan market has been slow to recover, but is picking up momentum

(0.0) (2.6)

(13.4)

(2.5)

January February March April

Outflows Inflows

Prim

ary

mar

ket

Seco

ndar

ies

Fund

Flo

ws

The leverage loan market has been much more sluggish since the COVID-19 outbreak in the U.S. with only $12.3bn pricing in March and April combined

Why has leveraged loan issuance lagged while high yield has reached near-record levels? Loan secondary prices remain in the

high 80s Lack of call protection / prepayability

of leveraged loans caps the amount of upside available to lenders

MFN protection in existing loans

Importantly, the composition of the leveraged loan buyer base has evolved in recent years, with retail funds now representing ~5% of the buyer base and CLOs representing ~60% of all loan buyers Widespread ratings downgrades have

put pressure on CLO funds, who have Weighted-Average-Rating-Factor (“WARF”) tests that limit the amount of CCC paper that can be held in the vehicle

In recent weeks, leveraged loans have started to see signs of the return toward normalcy, with Delta, T-Mobile and Samsonite the most notable new issues since the market re-opened

Average price on the JPM LL Index has recovered significantly from YTD lows

Primary issuance has been slow to return…

Loan outflows have moderated in recent weeks ($bn)

Note: Represents JPM LL index

Source: JPM, Bloomberg, Lipper Note: Market data as of 4/30/20 closing levels

5

120.1

71.0

4.5 7.7

99.5

45.9

20.6

25.1

January February March April

Refi Ex-RefiPost-crisis monthly record

[CATEGORY NAME] [VALUE]

[CATEGORY NAME] [VALUE]

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%

$70.00$75.00$80.00$85.00$90.00$95.00

$100.00

12/31 1/14 1/28 2/11 2/25 3/10 3/24 4/7 4/21

Average Price % of Loans Trading At Or Above Par

C O N F I D E N T I A L

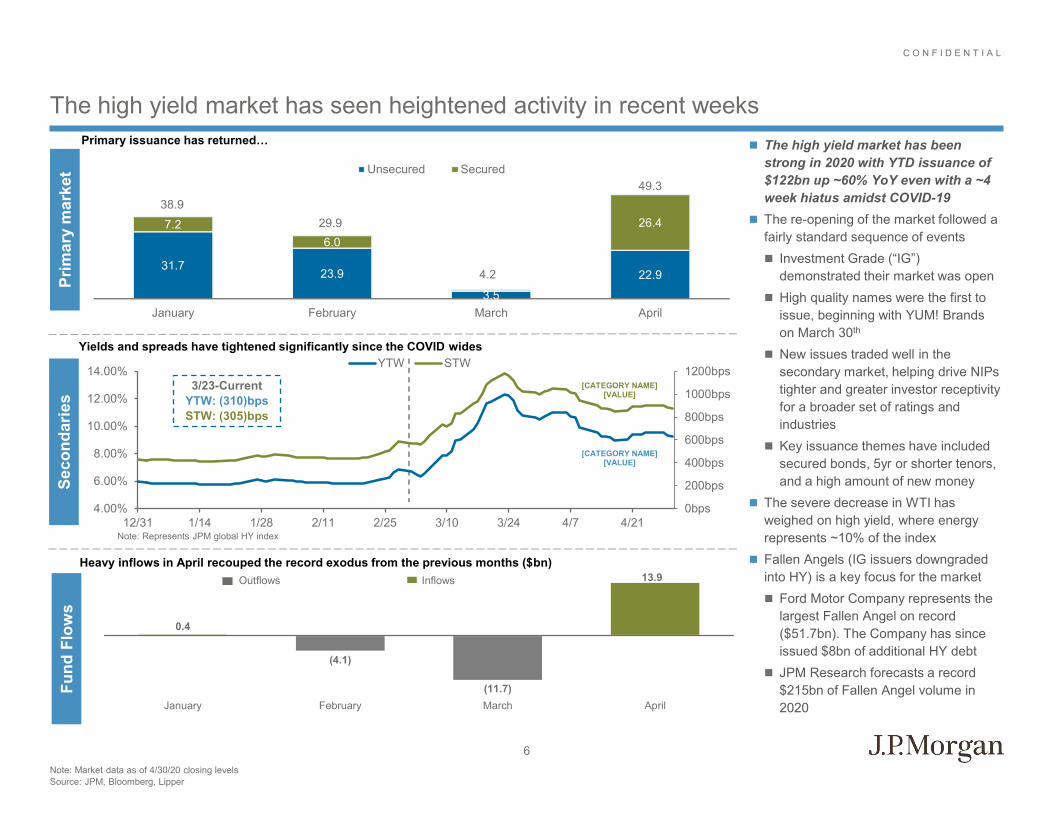

The high yield market has seen heightened activity in recent weeks

0.4

(4.1)

(11.7)

13.9

January February March April

Outflows Inflows

Prim

ary

mar

ket

Seco

ndar

ies

Fund

Flo

ws

The high yield market has been strong in 2020 with YTD issuance of $122bn up ~60% YoY even with a ~4 week hiatus amidst COVID-19

The re-opening of the market followed a fairly standard sequence of events Investment Grade (“IG”)

demonstrated their market was open High quality names were the first to

issue, beginning with YUM! Brands on March 30th

New issues traded well in the secondary market, helping drive NIPs tighter and greater investor receptivity for a broader set of ratings and industries

Key issuance themes have included secured bonds, 5yr or shorter tenors, and a high amount of new money

The severe decrease in WTI has weighed on high yield, where energy represents ~10% of the index

Fallen Angels (IG issuers downgraded into HY) is a key focus for the market Ford Motor Company represents the

largest Fallen Angel on record ($51.7bn). The Company has since issued $8bn of additional HY debt

JPM Research forecasts a record $215bn of Fallen Angel volume in 2020

Yields and spreads have tightened significantly since the COVID wides

Primary issuance has returned…

Heavy inflows in April recouped the record exodus from the previous months ($bn)

Note: Represents JPM global HY index

Source: JPM, Bloomberg, Lipper Note: Market data as of 4/30/20 closing levels

6

38.9 29.9

4.2

49.3

31.7 23.9

3.5

22.9

7.2 6.0

26.4

January February March April

Unsecured Secured

[CATEGORY NAME] [VALUE]

[CATEGORY NAME] [VALUE]

0bps

200bps

400bps

600bps

800bps

1000bps

1200bps

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

12/31 1/14 1/28 2/11 2/25 3/10 3/24 4/7 4/21

YTW STW

3/23-Current YTW: (310)bps STW: (305)bps

C O N F I D E N T I A L

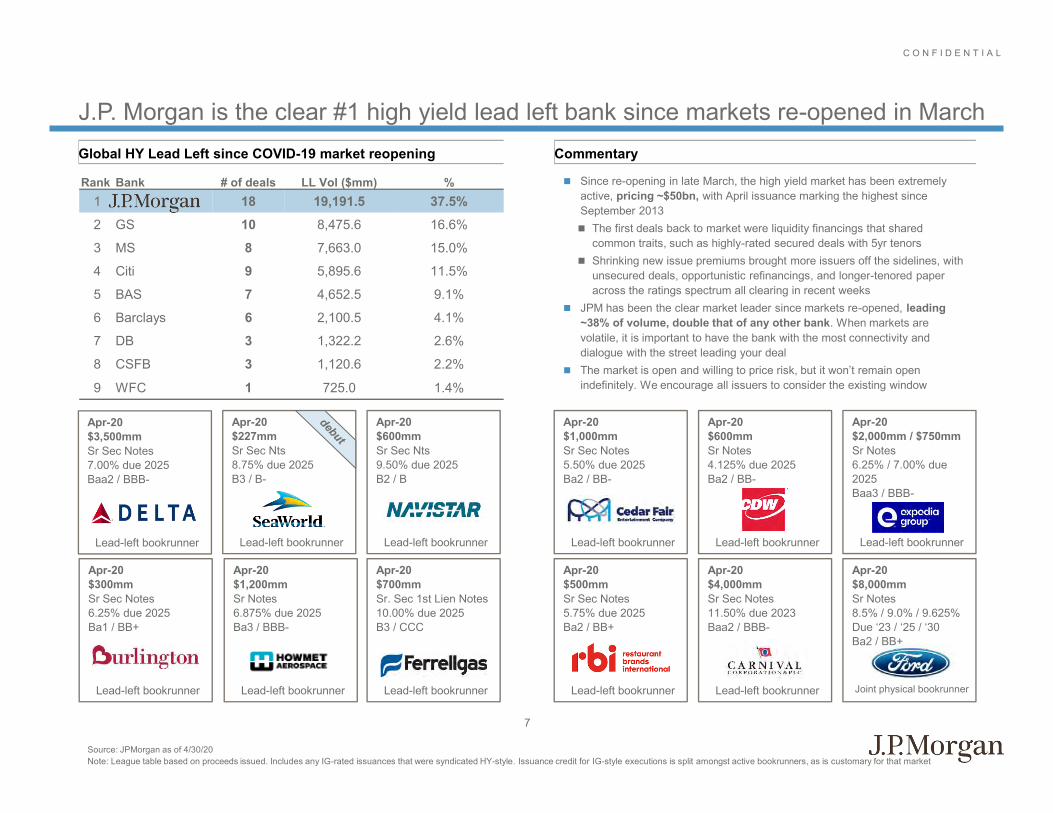

Rank Bank # of deals LL Vol ($mm) % 1 18 19,191.5 37.5% 2 GS 10 8,475.6 16.6%

3 MS 8 7,663.0 15.0%

4 Citi 9 5,895.6 11.5%

5 BAS 7 4,652.5 9.1%

6 Barclays 6 2,100.5 4.1%

7 DB 3 1,322.2 2.6%

8 CSFB 3 1,120.6 2.2%

9 WFC 1 725.0 1.4%

Apr-20 $8,000mm Sr Notes 8.5% / 9.0% / 9.625% Due ‘23 / ‘25 / ‘30 Ba2 / BB+

Joint physical bookrunner

J.P. Morgan is the clear #1 high yield lead left bank since markets re-opened in March Global HY Lead Left since COVID-19 market reopening Commentary

Apr-20 $227mm Sr Sec Nts 8.75% due 2025 B3 / B-

Lead-left bookrunner

Apr-20 $600mm Sr Sec Nts 9.50% due 2025 B2 / B

Lead-left bookrunner

Apr-20 $1,000mm Sr Sec Notes 5.50% due 2025 Ba2 / BB-

Lead-left bookrunner

Apr-20 $600mm Sr Notes 4.125% due 2025 Ba2 / BB-

Lead-left bookrunner

Apr-20 $300mm Sr Sec Notes 6.25% due 2025 Ba1 / BB+

Lead-left bookrunner

Apr-20 $700mm Sr. Sec 1st Lien Notes 10.00% due 2025 B3 / CCC

Lead-left bookrunner

Apr-20 $500mm Sr Sec Notes 5.75% due 2025 Ba2 / BB+

Lead-left bookrunner

Apr-20 $4,000mm Sr Sec Notes 11.50% due 2023 Baa2 / BBB-

Lead-left bookrunner

Source: JPMorgan as of 4/30/20 Note: League table based on proceeds issued. Includes any IG-rated issuances that were syndicated HY-style. Issuance credit for IG-style executions is split amongst active bookrunners, as is customary for that market

Apr-20 $1,200mm Sr Notes 6.875% due 2025 Ba3 / BBB-

Lead-left bookrunner

Since re-opening in late March, the high yield market has been extremely active, pricing ~$50bn, with April issuance marking the highest since September 2013 The first deals back to market were liquidity financings that shared

common traits, such as highly-rated secured deals with 5yr tenors Shrinking new issue premiums brought more issuers off the sidelines, with

unsecured deals, opportunistic refinancings, and longer-tenored paper across the ratings spectrum all clearing in recent weeks

JPM has been the clear market leader since markets re-opened, leading ~38% of volume, double that of any other bank. When markets are volatile, it is important to have the bank with the most connectivity and dialogue with the street leading your deal

The market is open and willing to price risk, but it won’t remain open indefinitely. We encourage all issuers to consider the existing window

Apr-20 $2,000mm / $750mm Sr Notes 6.25% / 7.00% due 2025 Baa3 / BBB-

Lead-left bookrunner

7

Apr-20 $3,500mm Sr Sec Notes 7.00% due 2025 Baa2 / BBB-

Lead-left bookrunner

Government Programs in Response to COVID-19 Pandemic

May 5, 2020

Overview

11

• Since March 15, the government has taken unprecedented and wide-ranging steps to address the economic impact of COVID-19: − Discount Window / Fed and Interagency Regulatory Actions designed to ease capital restrictions and

encourage banks to use liquidity and capital buffers to respond to crisis − Monetary Policy actions designed to increase liquidity including reduction in the federal funds rate,

quantitative easing and expansion of repo operations − Pre-CARES Act Fed Reserve Liquidity facilities:

• Commercial Paper Funding Facility • Term Asset-Backed Securities Loan Facility • Primary and Secondary Market Commercial Credit Facility • Other programs such as primary dealer, money market and municipal liquidity facilities

− CARES Act programs: • Air carriers / air ticketing / national security programs • Paycheck Protection Program • Main Street New Loan Facility • Main Street Expanded Loan Facility • Main Street Priority Loan Facility

• The details of these programs are summarized in Annex I. Focus of this presentation will be on the CARES Act and in particular the PPP and Main Street programs

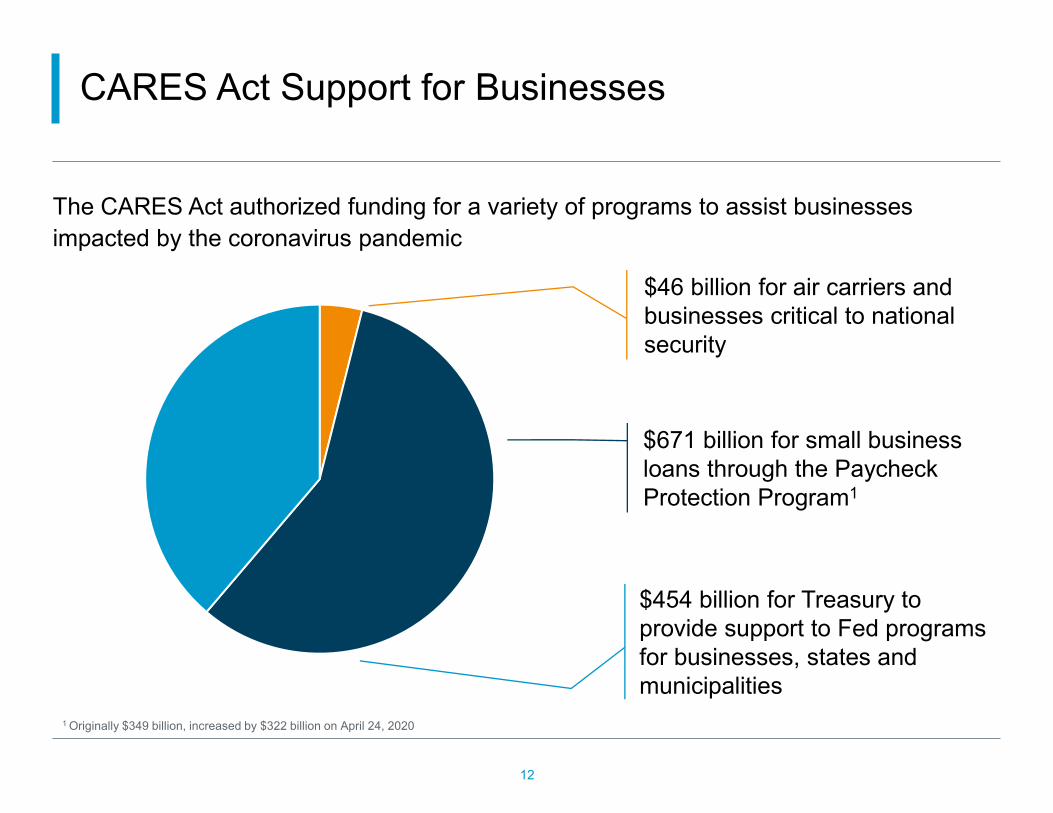

CARES Act Support for Businesses

12

The CARES Act authorized funding for a variety of programs to assist businesses impacted by the coronavirus pandemic

$46 billion for air carriers and businesses critical to national security

$671 billion for small business loans through the Paycheck Protection Program1

$454 billion for Treasury to provide support to Fed programs for businesses, states and municipalities

1 Originally $349 billion, increased by $322 billion on April 24, 2020

Relevant Laws and Regulations

13

• Key regulatory authority: − Section 13(3) of the Federal Reserve Act − Regulation A of the Board of Governors of the Federal Reserve − Title IV of the CARES Act

• And in this presentation we will reference in particular the April 30, 2020 iterations of: − Main Street New Loan Facility Term Sheet − Main Street Expanded Loan Facility Term Sheet − Main Street Priority Loan Facility Term Sheet

14

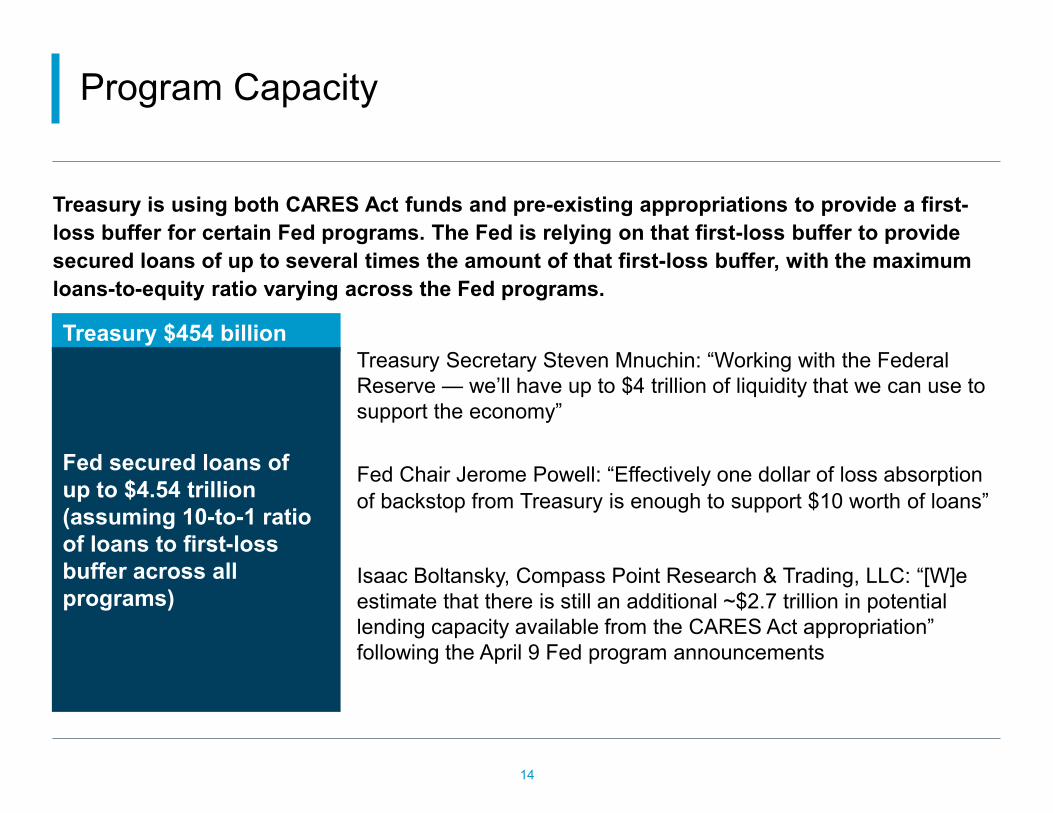

Treasury is using both CARES Act funds and pre-existing appropriations to provide a first-loss buffer for certain Fed programs. The Fed is relying on that first-loss buffer to provide secured loans of up to several times the amount of that first-loss buffer, with the maximum loans-to-equity ratio varying across the Fed programs.

Program Capacity

Treasury $454 billion

Fed secured loans of up to $4.54 trillion (assuming 10-to-1 ratio of loans to first-loss buffer across all programs)

Treasury Secretary Steven Mnuchin: “Working with the Federal Reserve — we’ll have up to $4 trillion of liquidity that we can use to support the economy”

Fed Chair Jerome Powell: “Effectively one dollar of loss absorption of backstop from Treasury is enough to support $10 worth of loans”

Isaac Boltansky, Compass Point Research & Trading, LLC: “[W]e estimate that there is still an additional ~$2.7 trillion in potential lending capacity available from the CARES Act appropriation” following the April 9 Fed program announcements

13(3) Conditions

15

• Any Fed program deployed must meet the requirements of Section 13(3) of the Federal Reserve Act. These include: − The Fed cannot lend to an insolvent company − The Fed must be fully secured

• The Fed can meet this requirement by lending to the relevant SPV or eligible corporate and having the SPV or eligible corporate pledge or repledge eligible assets

• It does not mean that loans to corporates under all programs will be required by the program to be collateralized (e.g., loans made under the Main Street lending facilities may be on an unsecured basis)

− The Fed must charge an interest rate higher than the applicable market interest rate in “normal times”

− Any program or facility must be broad based — i.e., must have at least five participants; cannot be aimed at one company

“America First” Provisions

16

• The CARES Act also requires that certain “America First” provisions must be met by any Treasury-supported Fed program. The ultimate borrower must meet all three criteria: − Be created or organized under U.S. law − Have significant operations in the United States − Have a majority of its employees in the United States

• Treatment of U.S. subsidiaries of foreign companies under Main Street programs not yet known

Payout Restrictions Required Under a Direct Loan

17

• Where a “direct loan” is made under the CARES Act to an eligible business as borrower, certain requirements apply to the ultimate borrower (as opposed to a bank or other financial intermediary) for the life of the loan plus 12 months: − No stock buybacks − No dividends or other capital distributions on common stock − No raises for an employee who made more than $425,000 in 2019; pay cuts for employees

who made more than $3M in 2019

• A direct loan is: − a bilateral loan entered into directly with an eligible business as borrower, and − does not include syndicated credit, loans originated by financial institutions in the ordinary

course, or securities or capital markets transactions.

• The Fed has stated that these restrictions apply to Eligible Borrowers under the Main Street programs; the restrictions do not apply to the beneficiaries of the PMCCF, SMCCF, CPFF or TALF

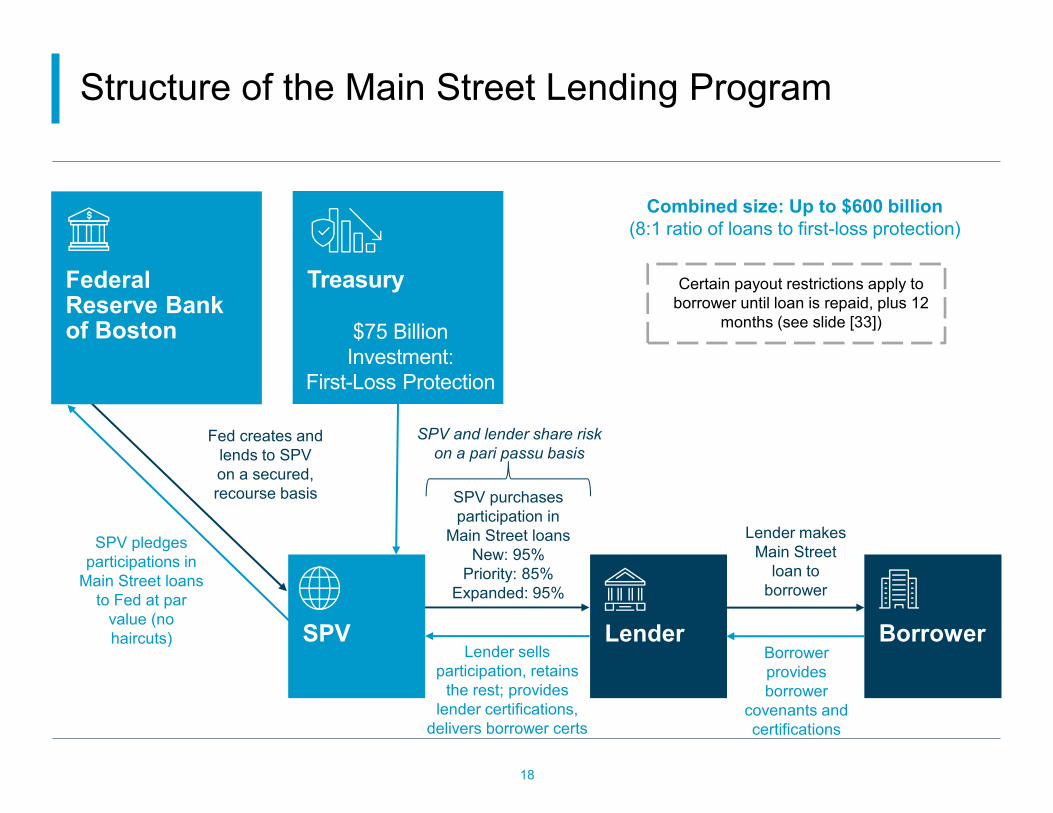

Structure of the Main Street Lending Program

18

SPV Lender Borrower

Treasury

$75 Billion Investment:

First-Loss Protection

SPV pledges participations in

Main Street loans to Fed at par

value (no haircuts)

Borrower provides borrower

covenants and certifications

Federal Reserve Bank of Boston

Lender makes Main Street

loan to borrower

Fed creates and lends to SPV on a secured, recourse basis

Combined size: Up to $600 billion (8:1 ratio of loans to first-loss protection)

Lender sells participation, retains

the rest; provides lender certifications,

delivers borrower certs

SPV purchases participation in

Main Street loans New: 95%

Priority: 85% Expanded: 95%

SPV and lender share risk on a pari passu basis

Certain payout restrictions apply to borrower until loan is repaid, plus 12

months (see slide [33])

Architecture of the Program Documents and Contractual Arrangements

19

Participation Agreement

Borrower

The Fed has not yet announced when any forms might be published or if they will be subject to comment.

Loan Agreement

Borrower Certifications collected by Lender

Lender Certifications + delivery of Borrower Certs

Securitization or Sale

Sale/Assignment Agreement

Main Street SPV

Lender

• Each of these agreements must address the requirements of Section 13(3) of the Federal Reserve Act, its implementing regulations, the CARES Act and the term sheets). − MSELF loans have pre-existing agreements, so no standard form can be imposed, but it is possible that the

Fed will issue a set of principles for that facility. • The Participation Agreement between lenders and the SPV will be important in setting out the obligations and

risks of each party (e.g., put-back risk, remedies for violations of representations and warranties, and voting rights of the SPV, among others).

• The FAQs state that the Main Street SPV may sell its participation, which we believe implies a securitization. Whether lenders could also sell into the securitization is unknown.

?

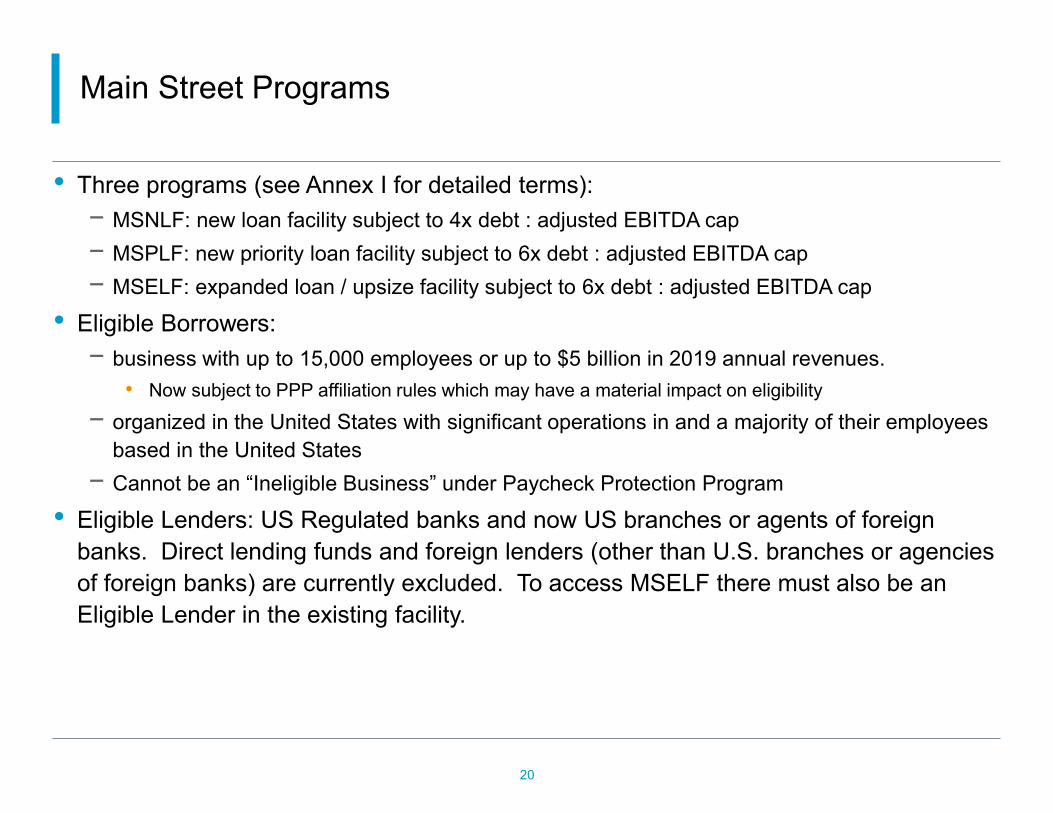

Main Street Programs

20

• Three programs (see Annex I for detailed terms): − MSNLF: new loan facility subject to 4x debt : adjusted EBITDA cap − MSPLF: new priority loan facility subject to 6x debt : adjusted EBITDA cap − MSELF: expanded loan / upsize facility subject to 6x debt : adjusted EBITDA cap

• Eligible Borrowers: − business with up to 15,000 employees or up to $5 billion in 2019 annual revenues.

• Now subject to PPP affiliation rules which may have a material impact on eligibility

− organized in the United States with significant operations in and a majority of their employees based in the United States

− Cannot be an “Ineligible Business” under Paycheck Protection Program

• Eligible Lenders: US Regulated banks and now US branches or agents of foreign banks. Direct lending funds and foreign lenders (other than U.S. branches or agencies of foreign banks) are currently excluded. To access MSELF there must also be an Eligible Lender in the existing facility.

Main Street Programs (cont.)

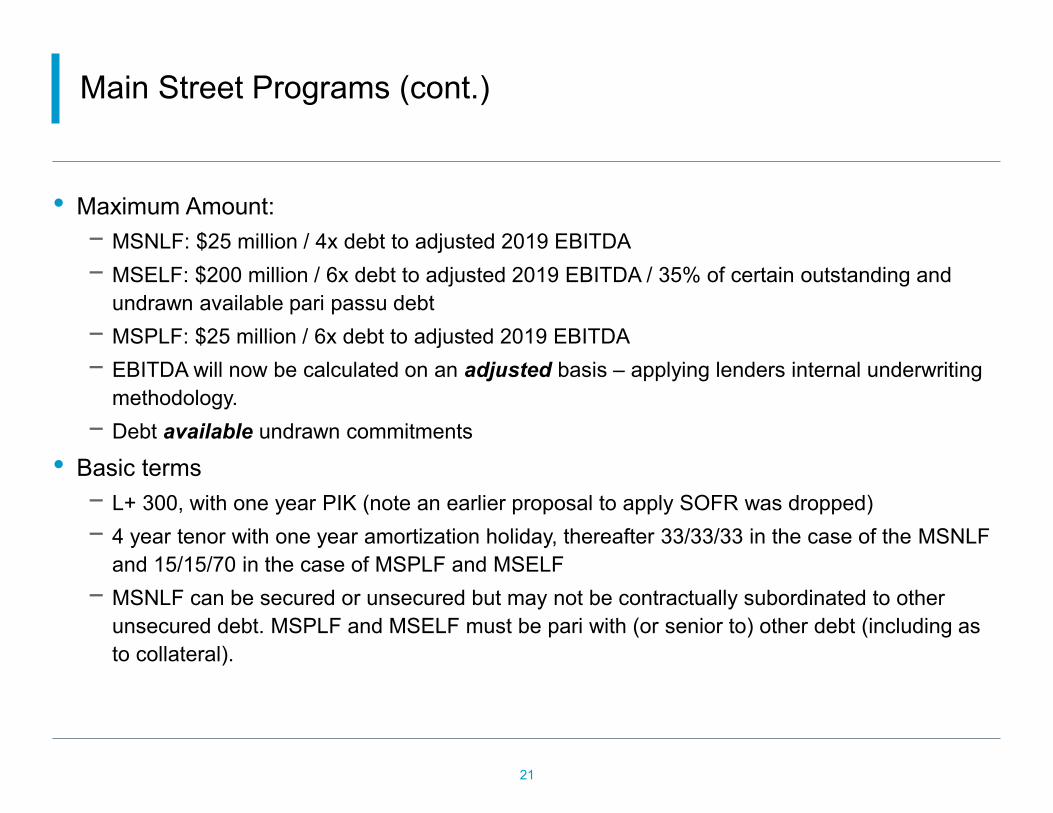

21

• Maximum Amount: − MSNLF: $25 million / 4x debt to adjusted 2019 EBITDA − MSELF: $200 million / 6x debt to adjusted 2019 EBITDA / 35% of certain outstanding and

undrawn available pari passu debt − MSPLF: $25 million / 6x debt to adjusted 2019 EBITDA − EBITDA will now be calculated on an adjusted basis – applying lenders internal underwriting

methodology. − Debt available undrawn commitments

• Basic terms − L+ 300, with one year PIK (note an earlier proposal to apply SOFR was dropped) − 4 year tenor with one year amortization holiday, thereafter 33/33/33 in the case of the MSNLF

and 15/15/70 in the case of MSPLF and MSELF − MSNLF can be secured or unsecured but may not be contractually subordinated to other

unsecured debt. MSPLF and MSELF must be pari with (or senior to) other debt (including as to collateral).

Main Street Programs (cont.)

22

• Limits on prepayments: − MSPLF permits loan proceeds at issuance to be used to refinance existing debt owed by the

Eligible Borrower to a lender that is not the Eligible Lender − All facilities otherwise preclude repayment of any other debt while Main Street loan remains

outstanding (other than certain mandatory payments).

• Other requirements: − Borrower will be subject to the CARES Act payment restrictions noted above for the life of the

loan plus 12 months (exception added for tax pass-through) − Borrower must certify that it has a reasonable basis to believe that, after giving effect to the

loan, it has ability to meet its financial obligations, and not expected to file for bankruptcy, for 90 days

− Borrowers are required to use reasonable efforts to maintain their payroll and retain their employees during the term of the loan

− Existing loans of a borrower must have a risk rating equivalent to a “pass” in the Federal Financial Institutions Examination Council’s supervisory rating system as of December 31, 2019

Main Street Programs (cont.)

23

• Key characteristic of the program is that the SPV will “expeditiously” acquire − 95% participation interest in MSNLF and MSELF Eligible Loans − 85% participation interest in the MSPLF Eligible Loans

• Eligible Lenders are prohibited from divesting their retained interest until the maturity of the loan (or the SPV’s earlier disposition of all of its participation interest).

• Eligible Lenders in MSELF also prohibited from disposing of their interest in the underlying loans subject to expansion.

• Details of participation (e.g. voting rights) will be forth coming, though FAQs clarify it will be a “true sale”.

Main Street Programs (cont.)

24

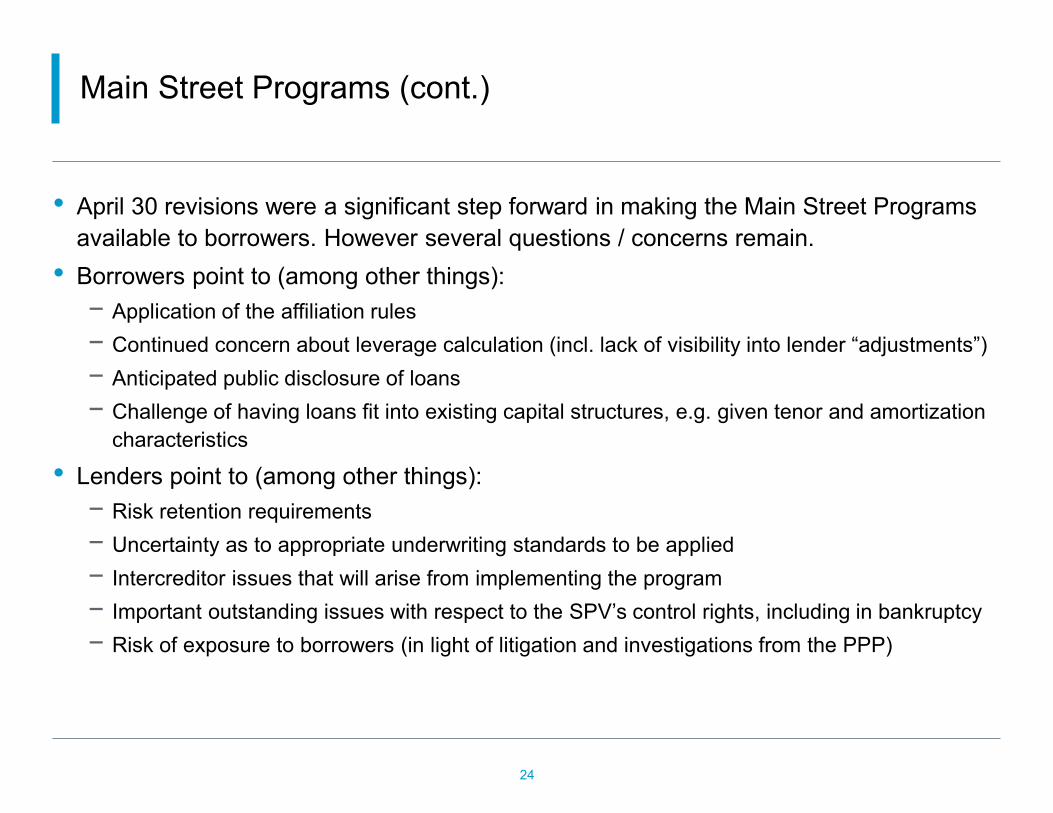

• April 30 revisions were a significant step forward in making the Main Street Programs available to borrowers. However several questions / concerns remain.

• Borrowers point to (among other things): − Application of the affiliation rules − Continued concern about leverage calculation (incl. lack of visibility into lender “adjustments”) − Anticipated public disclosure of loans − Challenge of having loans fit into existing capital structures, e.g. given tenor and amortization

characteristics

• Lenders point to (among other things): − Risk retention requirements − Uncertainty as to appropriate underwriting standards to be applied − Intercreditor issues that will arise from implementing the program − Important outstanding issues with respect to the SPV’s control rights, including in bankruptcy − Risk of exposure to borrowers (in light of litigation and investigations from the PPP)

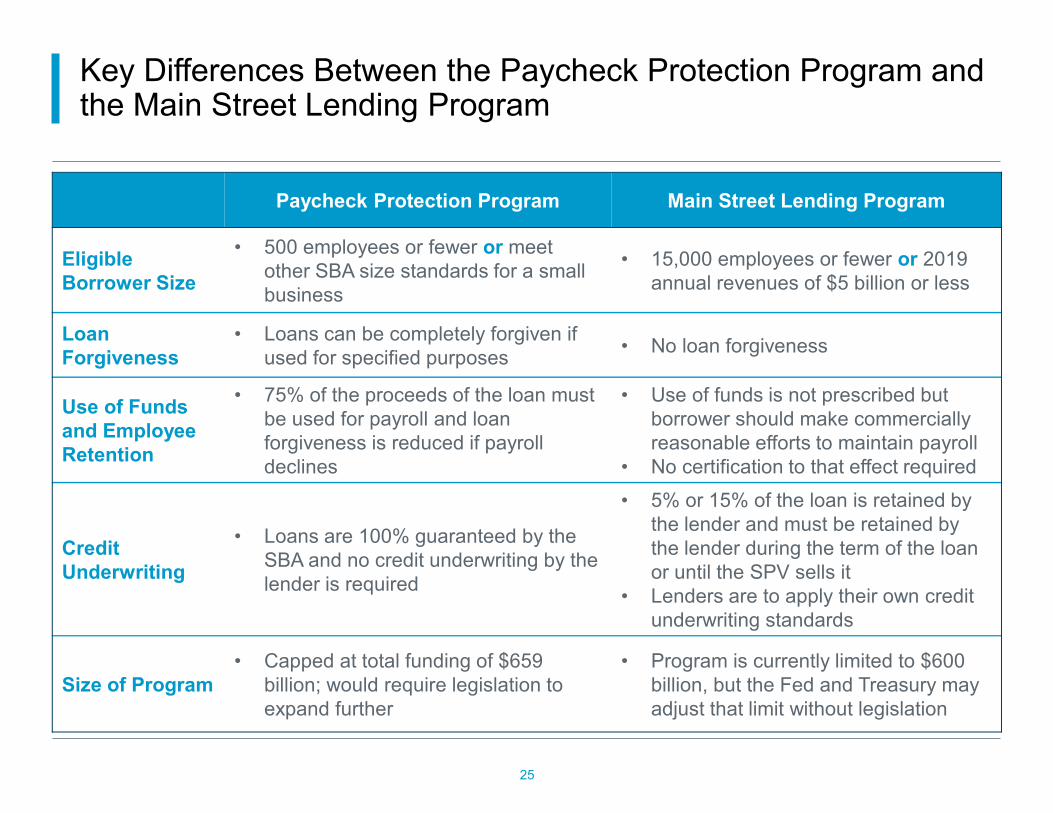

Key Differences Between the Paycheck Protection Program and the Main Street Lending Program

Paycheck Protection Program Main Street Lending Program

Eligible Borrower Size

• 500 employees or fewer or meet other SBA size standards for a small business

• 15,000 employees or fewer or 2019 annual revenues of $5 billion or less

Loan Forgiveness

• Loans can be completely forgiven if used for specified purposes • No loan forgiveness

Use of Funds and Employee Retention

• 75% of the proceeds of the loan must be used for payroll and loan forgiveness is reduced if payroll declines

• Use of funds is not prescribed but borrower should make commercially reasonable efforts to maintain payroll

• No certification to that effect required

Credit Underwriting

• Loans are 100% guaranteed by the SBA and no credit underwriting by the lender is required

• 5% or 15% of the loan is retained by the lender and must be retained by the lender during the term of the loan or until the SPV sells it

• Lenders are to apply their own credit underwriting standards

Size of Program • Capped at total funding of $659

billion; would require legislation to expand further

• Program is currently limited to $600 billion, but the Fed and Treasury may adjust that limit without legislation

25

I

Annex I

Discount Window and Regulatory Actions

27

Action Discount Window Reserve Requirement Buffers Released SLR Modification

Fed Release March 15 March 15 March 15 April 1

Description

Primary credit rate reduced to 25 bps, term extended to up to

90 days.

Fed, FDIC, OCC issued statements encouraging

discount window borrowing.1

Reserve requirement cut to 0%.

The reserve requirement is the amount of money that a

depository institution must have in its account at a Federal

Reserve Bank, as a percentage of its deposit liabilities.

Reducing the requirement to 0 frees these funds to support

more lending.

Fed, FDIC, OCC issued statements encouraging firms to use their buffers to respond

to the crisis.

Interim final rule provides a more gradual phase-in of automatic restrictions on

distributions as firms dip into their capital and liquidity buffers

and approach minimum requirements.

Fed interim final rule temporarily excludes on-balance sheet U.S.

Treasury securities and FRB reserves from the denominator of the supplementary leverage

ratio (SLR) for all regulated holding companies for which the

SLR applies.

This allows banking organizations to more easily

expand their balance sheets to facilitate Fed actions and

continue financial intermediation.

Eligible Borrowers Depository institutions.

Eligible Collateral

List of eligible collateral, subject to haircuts, set forth in

the “Margins and Collateral Guidelines”

Rate

Primary credit: 25 bps.

Secondary credit: 75 bps.

Seasonal credit: 120 bps.

Not applicable. Not applicable. Not applicable.

Term Up to 90 days. Not applicable. Not applicable. Exclusions are in effect through March 31, 2021.

1 At the same time, the Fed also encouraged banks to use its intraday credit facilities. On March 19, the Fed stated that it “is encouraged by the notable increase in discount window borrowing this week with banks demonstrating a willingness to use the discount window.”

Monetary Policy Actions

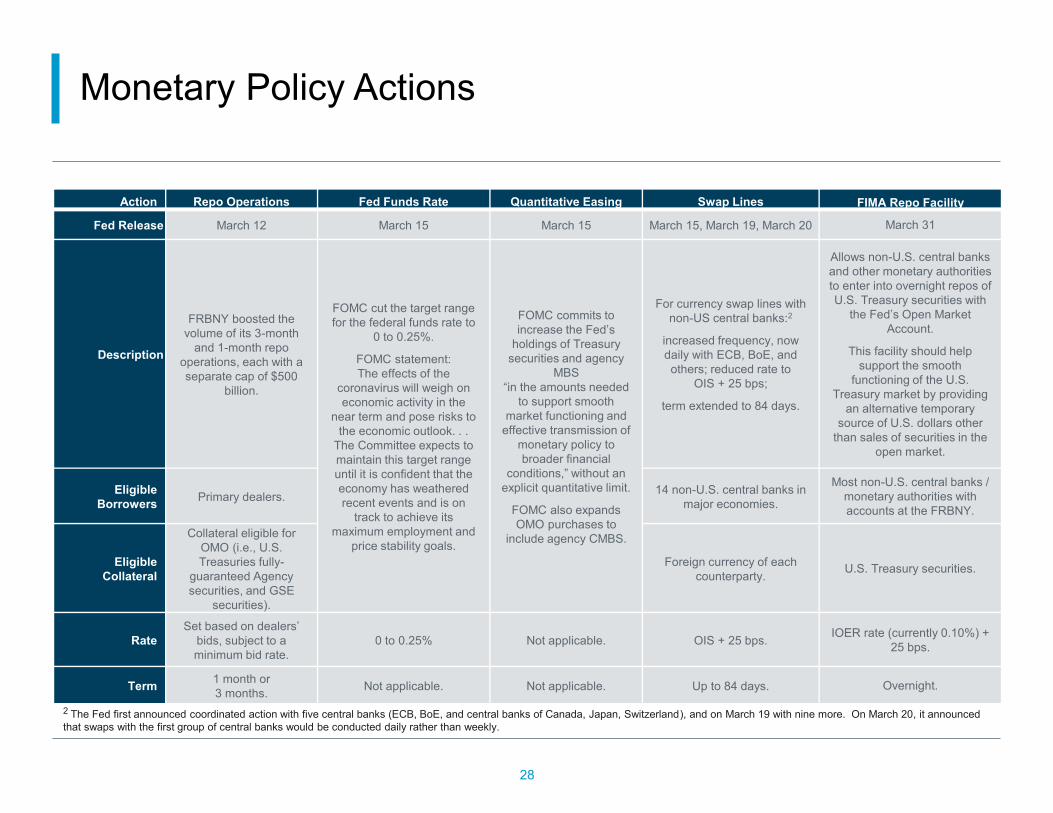

28

Action Repo Operations Fed Funds Rate Quantitative Easing Swap Lines FIMA Repo Facility

Fed Release March 12 March 15 March 15 March 15, March 19, March 20 March 31

Description

FRBNY boosted the volume of its 3-month

and 1-month repo operations, each with a separate cap of $500

billion.

FOMC cut the target range for the federal funds rate to

0 to 0.25%.

FOMC statement: The effects of the

coronavirus will weigh on economic activity in the

near term and pose risks to the economic outlook. . .

The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on

track to achieve its maximum employment and

price stability goals.

FOMC commits to increase the Fed’s

holdings of Treasury securities and agency

MBS “in the amounts needed

to support smooth market functioning and

effective transmission of monetary policy to broader financial

conditions,” without an explicit quantitative limit.

FOMC also expands OMO purchases to

include agency CMBS.

For currency swap lines with non-US central banks:2

increased frequency, now daily with ECB, BoE, and others; reduced rate to

OIS + 25 bps;

term extended to 84 days.

Allows non-U.S. central banks and other monetary authorities to enter into overnight repos of U.S. Treasury securities with

the Fed’s Open Market Account.

This facility should help support the smooth

functioning of the U.S. Treasury market by providing

an alternative temporary source of U.S. dollars other

than sales of securities in the open market.

Eligible Borrowers Primary dealers. 14 non-U.S. central banks in

major economies.

Most non-U.S. central banks / monetary authorities with accounts at the FRBNY.

Eligible Collateral

Collateral eligible for OMO (i.e., U.S. Treasuries fully-

guaranteed Agency securities, and GSE

securities).

Foreign currency of each counterparty. U.S. Treasury securities.

Rate Set based on dealers’

bids, subject to a minimum bid rate.

0 to 0.25% Not applicable. OIS + 25 bps. IOER rate (currently 0.10%) + 25 bps.

Term 1 month or 3 months. Not applicable. Not applicable. Up to 84 days. Overnight.

2 The Fed first announced coordinated action with five central banks (ECB, BoE, and central banks of Canada, Japan, Switzerland), and on March 19 with nine more. On March 20, it announced that swaps with the first group of central banks would be conducted daily rather than weekly.

Federal Reserve Liquidity Facilities

29

Action Primary Dealer Credit Facility (PDCF)

Commercial Paper Funding Facility

(CPFF)

Money Market Mutual Fund Liquidity Facility

(MMLF)

Term Asset-Backed Securities Loan Facility (TALF)

Fed Release March 17 March 17, March 23 March 18, March 20, March 23 March 23, April 9

Description

Loans from the FRBNY to primary dealers, with full recourse, secured

by eligible collateral.

Size: Not stated.

SPV buys commercial paper from U.S. issuers, including financial and commercial companies and munis.

FRBNY lends to the SPV, with recourse, secured by all assets of the SPV including purchased CP,

without haircuts.

Size: Not stated. $10 billion of first-loss support from Treasury.

Nonrecourse loans from FRB Boston to eligible borrowers, secured by

eligible collateral that was purchased by eligible borrowers from eligible MMFs and pledged to FRB Boston

at market value at time of purchase, without further haircuts.

Interim final rule neutralizes the regulatory capital impact on eligible

borrowers of holding eligible collateral.

Size: Not stated. $10 billion of first-loss support from Treasury.

Nonrecourse loans from an SPV to eligible borrowers secured by eligible

ABS collateral and pledged to the SPV, subject to haircuts.3

FRBNY lends to the SPV with recourse, secured by all assets of

SPV including eligible ABS collateral.

Size: Up to $100 billion, with $10 billion of first-loss support from

Treasury.

Eligible Borrowers /

Issuers Eligible Borrowers: Primary dealers.

Eligible Issuers: U.S. CP issuers (including U.S. subsidiaries of

foreign parents).

Eligible Borrowers: U.S. banks/thrifts, U.S. BHCs,4 U.S.

branches and agencies of FBOs. Eligible MMFs: Prime and municipal

MMFs.

Eligible Borrowers: U.S. companies that own eligible ABS collateral and

maintain a relationship with a primary dealer.5

3 Haircuts range from 5% (for, e.g., ABS of SBA loans with up to 5 years weighted average life) to 22% (for CLOs of leveraged loans with 6 to 7 years weighted average life) and largely mirror the schedule used for the TALF established for the 2008 global financial crisis. 4 Although SLHCs were not expressly listed, it appears that they may also be eligible borrowers because they are covered by the associated regulatory capital relief in the interim final rule. 5 For purposes of TALF, PMCCF, SMCCF, MSNLF and MSELF, a “U.S. company” means a business that is created or organized in the United States, or under the laws of the United States, with significant operations in and a majority of its employees based in the United States.

Federal Reserve Liquidity Facilities (cont.)

30

Action Primary Dealer Credit Facility (PDCF) Commercial Paper

Funding Facility (CPFF)

Money Market Mutual Fund Liquidity Facility

(MMLF)

Term Asset-Backed Securities Loan Facility (TALF)

Eligible Collateral / Assets to

Purchase

Eligible Collateral: Wide range, many types of investment-

grade debt and equities.

Eligible Assets to Purchase: 3-month CP (incl. tax-exempt CP) rated

A1 / P1 / F1 by an NRSRO. A one-time sale of collateral rated A2 / P2 / F2 is permitted in the event of a

ratings downgrade.

Eligible Collateral: U.S. Treasuries and fully guaranteed agency securities; GSE-guaranteed securities; ABCP, unsecured

CP; CDs issued by U.S. issuers and rated at least A1 / F1 / P1; U.S. muni

short-term debt (excluding VRDNs) rated in top two categories; VRDNs puttable at

option of holder and rated in top two categories; potentially certain repo

receivables.

Eligible Collateral: USD cash ABS issued by a U.S. company and rated

AAA by an eligible NRSRO; no synthetic ABS or ABS of ABS; CMBS must be issued before March 23; Non-CMBS must be issued on or after March 23.

Eligible Underlying Exposures: Specified exposure types;6 for non-CMBS, all or

substantially all exposures on which any eligible ABS collateral is based must be newly originated by a U.S. company; for

CMBS, all commercial mortgage exposures on which the CMBS are

based must be to real property located in the United States.

Pricing, Rates and Fees Primary credit rate.

Purchase price of CP based on 3-month OIS + 110 bps for A1/P1/F1-rated

collateral; 3-month OIS + 200 bps for A2/P2/F2

rated collateral.

Primary rate for U.S. Treasuries and Agencies and GSE-guaranteed

securities collateral; Primary + 25 bps for muni collateral;

Primary + 100 bps for other collateral.

Eligible CLOs: 30-day SOFR + 150 bps; SBA 7(a) Loans: Fed Funds target rate

+ 75 bps; SBA 504 Loans: 3Y OIS rate + 75 bps; Other ABS w/out gov. guarantee: 2Y/3Y

OIS rate + 125 bps. All ABS: SPV will charge a 10 bps

administrative fee.

Term7 Up to 90 days. Same as CP purchased by SPV. Equal to maturity of collateral pledged, must be ≤12 mos. 3 years.

6 Eligible underlying exposures are auto loans and leases, student loans, credit card receivables, equipment loans and leases, floorplan loans, insurance premium finance loans, certain small business loans guaranteed by the SBA, leveraged loans and commercial mortgages. For CLOs, only static non-CRE CLOs will be eligible collateral. CRE CLOs and single-asset single-borrower CMBS are not eligible collateral. 7 Term of secured loan from Federal Reserve Bank to SPV or eligible borrower, as applicable.

Federal Reserve Liquidity Facilities (cont.)

31

Action Primary Market Commercial Credit Facility (PMCCF)

Secondary Market Commercial Credit Facility (SMCCF)

Municipal Liquidity Facility (MLF)

Fed Release March 23, April 9 March 23, April 9 April 9

Description

SPV buys at issuance eligible corporate bonds as sole investor or portions (no more than 25%) of syndicated

corporate loans or bonds.

SPV buys on secondary market from eligible sellers eligible corporate bonds issued by eligible issuers and

eligible ETFs.

SPV buys newly issued short-term notes issued by and directly from eligible issuers.

A Federal Reserve Bank lends with recourse to the SPV.

Proceeds may be used to manage cash flow impact associated with (a) income tax deferrals, (b) potential

reductions in tax revenues or increases in expenses due to COVID-19 pandemic and (c) principal and interest

payments on obligations of the eligible issuers (or, if the eligible issuer is an instrumentality, that issuer’s

corresponding state, city or county). Size: Up to $500 billion, with $35 billion in first-loss

support from Treasury.

FRBNY lends to single, common SPV for both PMCCF and SMCCF with recourse, secured by all assets of SPV including eligible bond and ETF collateral, without haircuts.

Combined size of PMCCF and SMCCF: Up to $750 billion, with $75 billion of first-loss support from Treasury, with $50 billion earmarked for PMCCF and $25 billion earmarked for SMCCF.

Eligible Issuers / Sellers

Eligible Issuers: U.S. companies, other than IDIs or depository institution holding companies, that were investment grade as of March 22, 2020. If the issuer was investment grade as of March 22, 2020 but is no longer investment

grade (a fallen angel), the issuer must be rated at least BB-/Ba3 at the time the Facility makes a purchase. Must not have received specific support pursuant to the CARES Act or any subsequent federal legislation and that

satisfy the conflict of interest requirements in CARES Act section 4019, which apply to businesses owned or controlled by a covered U.S. government official.

Eligible Issuers: U.S. states (defined to include D.C.), U.S. cities with > 1 million residents,

U.S. counties with > 2 million residents; and instrumentalities issuing on behalf of such states, cities

and counties. Issuer cannot participate in MSELF or MSNLF.

Eligible Sellers to the Facility: U.S. companies. Businesses must also satisfy the conflicts-of-interest

requirements of section 4019 of the CARES Act.

Eligible Assets to Purchase

Corporate bonds or syndicated corporate loans or bonds issued by an eligible issuer with a maturity of 4 years or

less.

Corporate bonds issued by an eligible issuer with a remaining maturity of 5 years or less. Not applicable to

syndicated loans. ETFs with investment objectives to provide broad exposure to the market for U.S. corporate bonds.

Preponderance of the SMCCF’s ETF holdings will be ETFs whose primary investment objective is exposure to U.S. IG corporate bonds; remainder will be ETFs whose

primary investment objective is exposure to U.S. HY corporate bonds.

Tax anticipation notes (TANs), tax and revenue anticipation notes (TRANs),

bond anticipation notes (BANs) and other similar short-term notes issued by an eligible issuer, in all cases with a maturity of not more than 24

months, plus callable at par by the issuer.

Pricing, Rates and Fees

Corporate bonds: Issuer-specific pricing “informed by market conditions,” plus a 100 bps facility fee

Syndicated loans and bonds: Same pricing as other syndicate members, plus a 100 bps facility fee on the

PMCCF’s share of the syndication

Purchase price = fair market value on secondary market. Facility will avoid purchasing ETFs trading at prices that

materially exceed estimated NAV.

Pricing based on eligible issuer’s rating at time of purchase.

10 bps origination fee. More details to come.

Term Same as assets purchased by SPV.

[1] See note 5 for definition of U.S. company. [2] See note 7.

Federal Reserve Liquidity Facilities (cont.)

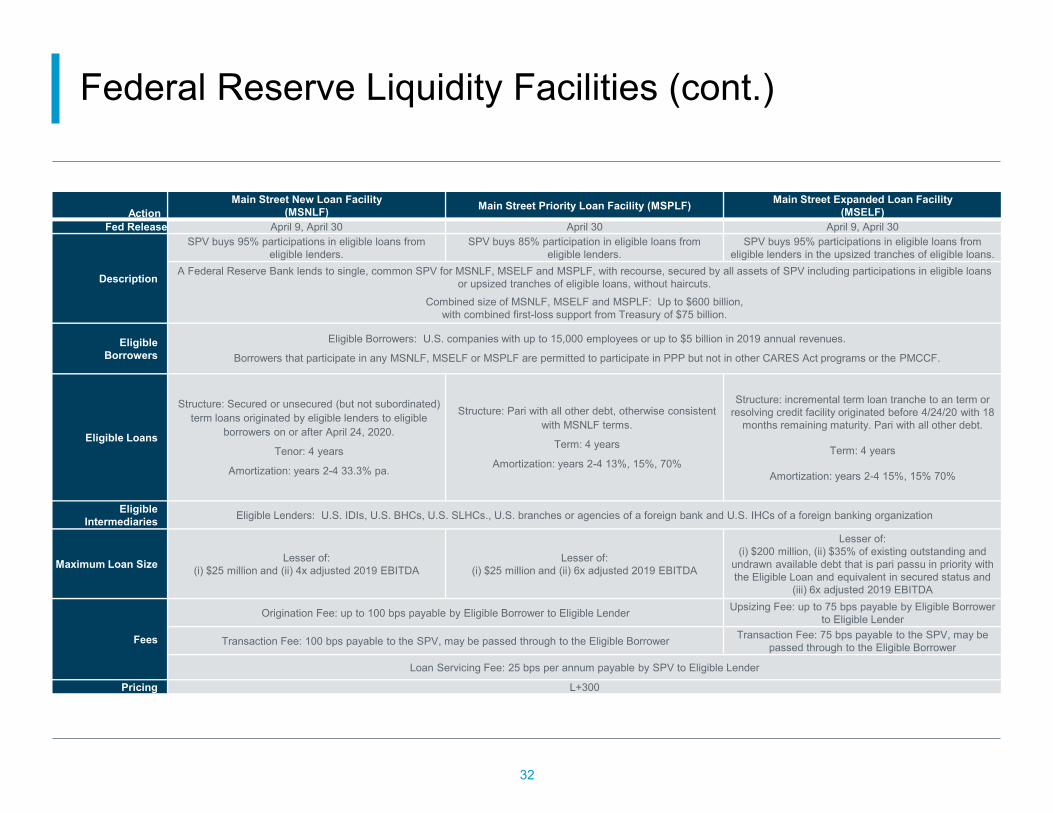

32

Action Main Street New Loan Facility

(MSNLF) Main Street Priority Loan Facility (MSPLF) Main Street Expanded Loan Facility (MSELF)

Fed Release April 9, April 30 April 30 April 9, April 30

Description

SPV buys 95% participations in eligible loans from eligible lenders.

SPV buys 85% participation in eligible loans from eligible lenders.

SPV buys 95% participations in eligible loans from eligible lenders in the upsized tranches of eligible loans.

A Federal Reserve Bank lends to single, common SPV for MSNLF, MSELF and MSPLF, with recourse, secured by all assets of SPV including participations in eligible loans or upsized tranches of eligible loans, without haircuts.

Combined size of MSNLF, MSELF and MSPLF: Up to $600 billion, with combined first-loss support from Treasury of $75 billion.

Eligible Borrowers

Eligible Borrowers: U.S. companies with up to 15,000 employees or up to $5 billion in 2019 annual revenues.

Borrowers that participate in any MSNLF, MSELF or MSPLF are permitted to participate in PPP but not in other CARES Act programs or the PMCCF.

Eligible Loans

Structure: Secured or unsecured (but not subordinated) term loans originated by eligible lenders to eligible

borrowers on or after April 24, 2020.

Tenor: 4 years

Amortization: years 2-4 33.3% pa.

Structure: Pari with all other debt, otherwise consistent with MSNLF terms.

Term: 4 years

Amortization: years 2-4 13%, 15%, 70%

Structure: incremental term loan tranche to an term or resolving credit facility originated before 4/24/20 with 18

months remaining maturity. Pari with all other debt.

Term: 4 years

Amortization: years 2-4 15%, 15% 70%

Eligible Intermediaries Eligible Lenders: U.S. IDIs, U.S. BHCs, U.S. SLHCs., U.S. branches or agencies of a foreign bank and U.S. IHCs of a foreign banking organization

Maximum Loan Size Lesser of: (i) $25 million and (ii) 4x adjusted 2019 EBITDA

Lesser of: (i) $25 million and (ii) 6x adjusted 2019 EBITDA

Lesser of: (i) $200 million, (ii) $35% of existing outstanding and

undrawn available debt that is pari passu in priority with the Eligible Loan and equivalent in secured status and

(iii) 6x adjusted 2019 EBITDA

Fees

Origination Fee: up to 100 bps payable by Eligible Borrower to Eligible Lender Upsizing Fee: up to 75 bps payable by Eligible Borrower to Eligible Lender

Transaction Fee: 100 bps payable to the SPV, may be passed through to the Eligible Borrower Transaction Fee: 75 bps payable to the SPV, may be passed through to the Eligible Borrower

Loan Servicing Fee: 25 bps per annum payable by SPV to Eligible Lender

Pricing L+300

Federal Reserve Liquidity Facilities (cont.)

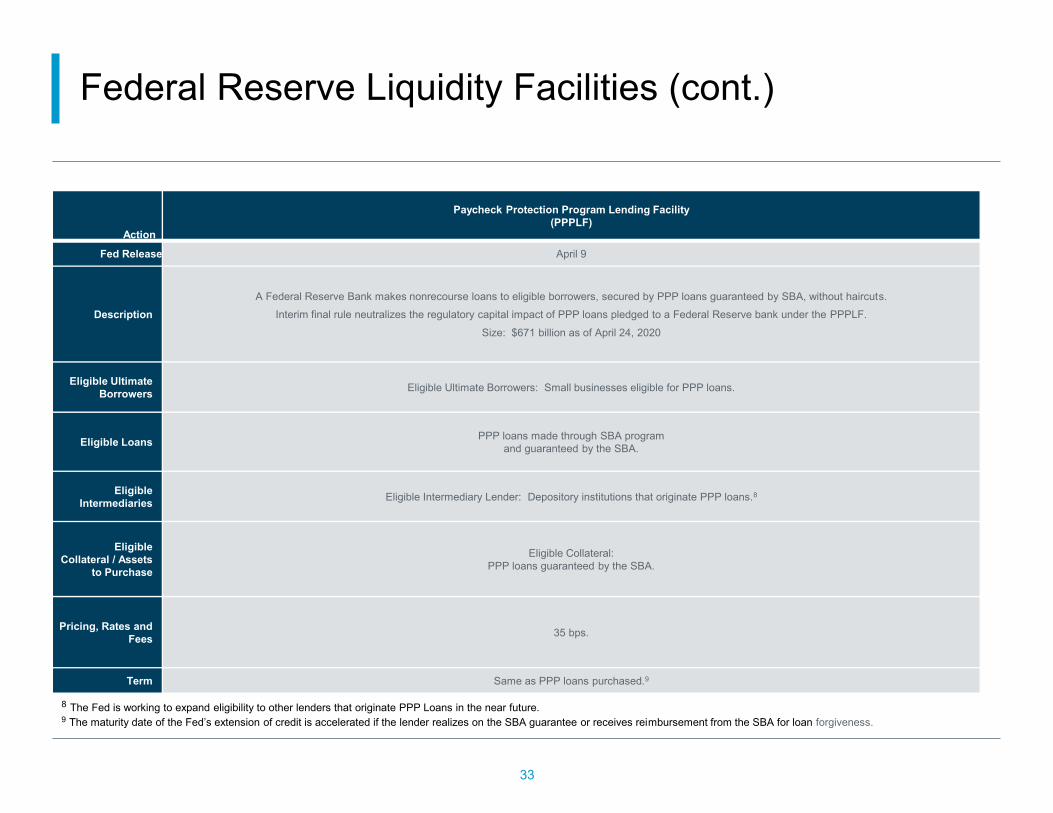

33

Action

Paycheck Protection Program Lending Facility (PPPLF)

Fed Release April 9

Description A Federal Reserve Bank makes nonrecourse loans to eligible borrowers, secured by PPP loans guaranteed by SBA, without haircuts.

Interim final rule neutralizes the regulatory capital impact of PPP loans pledged to a Federal Reserve bank under the PPPLF. Size: $671 billion as of April 24, 2020

Eligible Ultimate Borrowers Eligible Ultimate Borrowers: Small businesses eligible for PPP loans.

Eligible Loans PPP loans made through SBA program and guaranteed by the SBA.

Eligible Intermediaries Eligible Intermediary Lender: Depository institutions that originate PPP loans.8

Eligible Collateral / Assets

to Purchase

Eligible Collateral: PPP loans guaranteed by the SBA.

Pricing, Rates and Fees 35 bps.

Term Same as PPP loans purchased.9

8 The Fed is working to expand eligibility to other lenders that originate PPP Loans in the near future. 9 The maturity date of the Fed’s extension of credit is accelerated if the lender realizes on the SBA guarantee or receives reimbursement from the SBA for loan forgiveness.

As the world returns to “normalcy”,

LIBOR work rolls on

Meredith Coffey [email protected] 212-880-3019

35

What We’re Talking About…

• Do we still assume LIBOR ends on 12/31/21 (Spoiler: Yes!)

• What we have done in the past year… …and how does that gets us to a successful 1/1/22?

• Increased familiarity with rates – their behavior, strengths & weakness, appropriateness

• Action items – Conventions, Operations, Fallbacks, New SOFR loan documentation

36

FCA/BoE/Sterling WG Statement (April 2020): It remains the central assumption that firms cannot rely on LIBOR being published after the end of 2021. The FCA and the Bank of England have worked with members of the Working Group on Sterling Risk-Free Reference Rates (RFRWG) and its sub-groups and task forces to consider how all firms’ LIBOR transition plans may be impacted by Coronavirus. ARRC FAQs (April 2020): The ARRC recognizes that near-term, interim steps may be delayed given the current economic environment with the global pandemic, but given the latest announcements from the official sector reiterating the overall expected timeline (see here and here), it remains clear that the financial system should continue to move to transition by the end of 2021.

Do we still have to assume LIBOR ends 12/31/21? Yes…

37

Reduce operational risk to avoid market freezing up/interest disputes/market disruption Increase ability to execute “fallbacks” en masse to avoid market disruption Reduce, then eliminate, reliance on LIBOR before end of 2021 Have operationalization clarity by 3Q2020: Vendors and banks are working hard to get SOFR operationalized. Simple SOFR is nearly operationalized already and may be first step. New loans go to hardwired fallbacks by 3Q2020: We will have refined fallback language, economic and operationalization clarity. New loans stop offering LIBOR in 2021: CAs start only using SOFR options in 2021

What We Are Trying to Do…And How?

Wh

at?

Ho

w?

38

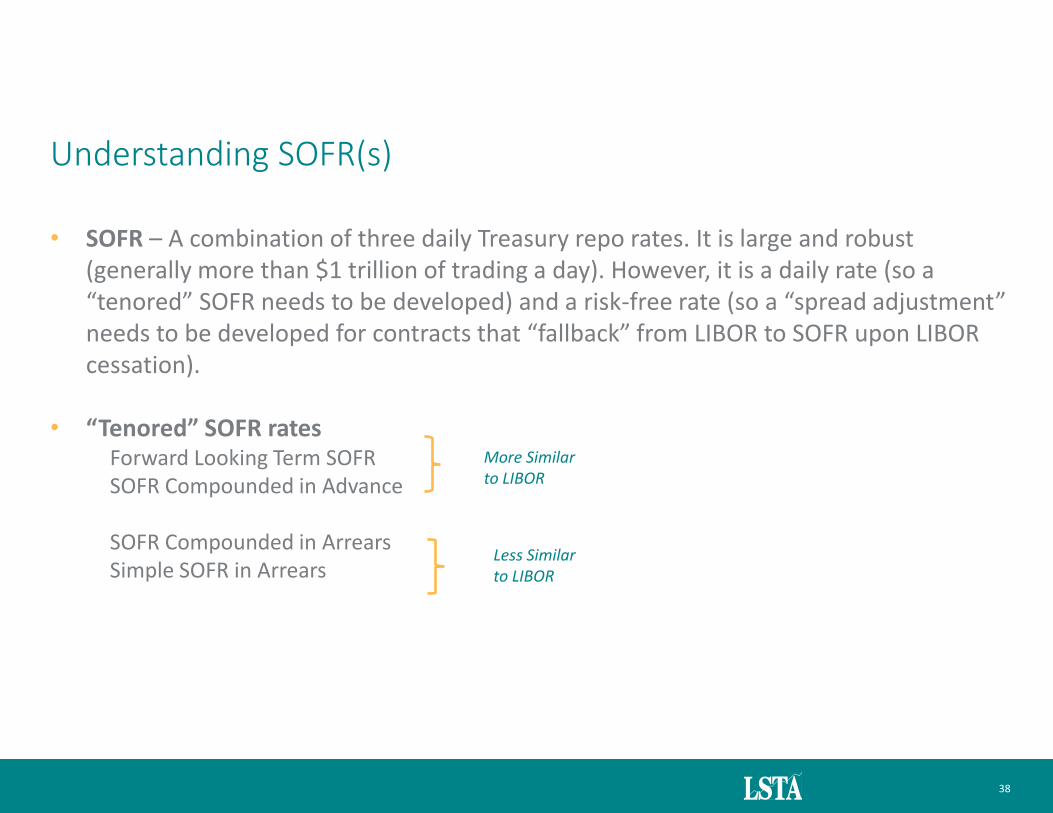

• SOFR – A combination of three daily Treasury repo rates. It is large and robust (generally more than $1 trillion of trading a day). However, it is a daily rate (so a “tenored” SOFR needs to be developed) and a risk-free rate (so a “spread adjustment” needs to be developed for contracts that “fallback” from LIBOR to SOFR upon LIBOR cessation).

• “Tenored” SOFR rates

Forward Looking Term SOFR SOFR Compounded in Advance

SOFR Compounded in Arrears Simple SOFR in Arrears

Understanding SOFR(s)

More Similar to LIBOR

Less Similar to LIBOR

39

Daily SOFR Volatility Exists, but Has Limited Impact on “Tenored” SOFRs

Source: ARRC, FRBNY

• LIBOR is relatively stable, but this is partly because it’s mostly derived from “expert judgement” • Overnight SOFR is volatile at quarter-end and year-end, but compounded or term SOFR is not volatile

1

1.5

2

2.5

3

3.5

4

4.5

5

5.5

Rat

e (

%)

O/N SOFR Can Be Volatile; "Tenored" SOFR More Stable

Compounded 1M SOFR Compounded 3M SOFR

Overnight SOFR

40

Economics of Simple and Compounded SOFR are Nearly Identical

Source: FRBNY, St Louis Fed

• Simple & Compounded SOFR levels are very similar (because you are compounding (SOFR/360, a very small rate) • Charts demonstrate little difference between Simple & Compounded SOFR – through multiple interest rate environments

0%

1%

2%

3%

4%

5%

6%

7%

Feb

-98

Feb

-00

Feb

-02

Feb

-04

Feb

-06

Feb

-08

Feb

-10

Feb

-12

Feb

-14

Feb

-16

Feb

-18

Rat

e (

%)

Quarterly Compound vs Simple SOFR Rates (1998-2019)

Monthly Compound SOFR

Monthly Simple SOFR

-

1

2

3

4

5

6

Feb

-98

Feb

-00

Feb

-02

Feb

-04

Feb

-06

Feb

-08

Feb

-10

Feb

-12

Feb

-14

Feb

-16

Feb

-18

Bas

is (

bp

s)

Simple/Compound SOFR Basis (1998-2019)

1M Simple/Compound SOFR Basis

3M Simple/Compound SOFR Basis

41

• While Simple and Compounded SOFR are economically similar, Compounded SOFR is operationally far more complex

• SOFR Compounded in Arrears: • Definition: a SOFR rate that is compounded during the interest period. For example, for a

30-day SOFR beginning on April 1, SOFR would be compounded every day beginning April 1 • Strengths: What other markets are doing; aligns with derivatives and easily hedgeable;

includes (small) “time value of money”. • Weaknesses: Will make loan trading more cumbersome than it is today; will be complex to

operationalize even for untraded loans; may increase operational risk; may be difficult to explain to less sophisticated counterparties

• Simple SOFR • Definition: SOFR rate that is pulled daily and accrued, but not compounded, during the

interest period. For example, for a 30-day SOFR beginning on April 1, SOFR would be pulled and accrued every day beginning April 1.

• Strengths: Easier to explain to less sophisticated counterparties; easier to trade and operationalize than Compound SOFR because concepts already exists in systems and market as daily LIBOR or daily Prime; lower operational risk; rate is very close to Compound SOFR;

• Weaknesses: Different than what other markets are doing; could add (modest) basis risk to CLO equity; does not include (small) “time value of money”.

Compounded vs Simple SOFR: Strengths & Weaknesses

42

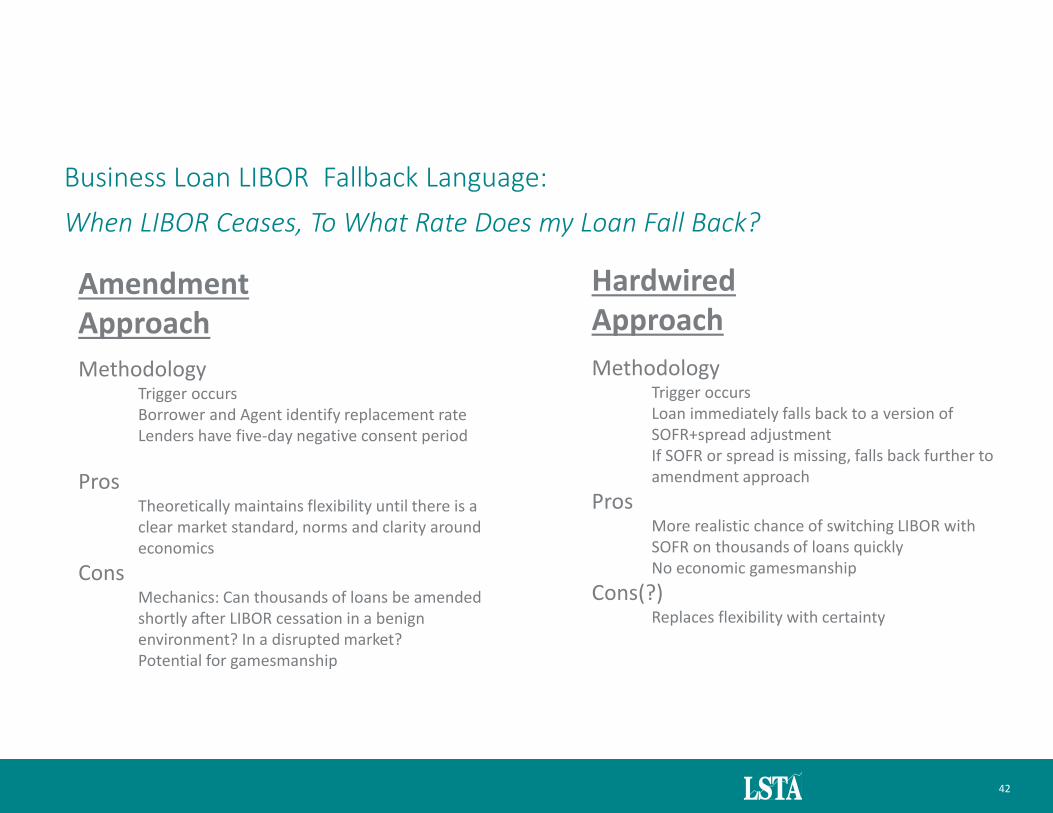

Methodology Trigger occurs Borrower and Agent identify replacement rate Lenders have five-day negative consent period

Pros Theoretically maintains flexibility until there is a clear market standard, norms and clarity around economics

Cons Mechanics: Can thousands of loans be amended shortly after LIBOR cessation in a benign environment? In a disrupted market? Potential for gamesmanship

Business Loan LIBOR Fallback Language:

When LIBOR Ceases, To What Rate Does my Loan Fall Back?

Methodology Trigger occurs Loan immediately falls back to a version of SOFR+spread adjustment If SOFR or spread is missing, falls back further to amendment approach

Pros More realistic chance of switching LIBOR with SOFR on thousands of loans quickly No economic gamesmanship

Cons(?) Replaces flexibility with certainty

Amendment Approach

Hardwired Approach

43

Could borrowers get their LIBOR fallback amendments done?

90 has been a typical cut off point between “par” and “distressed” loans We assumed companies rated B-/B3 or better AND priced 90 or better are more likely to get fallback amendments done Companies rated below B-/B3 or priced below 90 might struggle to get fallback amendments done and would be stuck in Prime based pricing In March, nearly all Index loans were below 90; By late April, this was only half of outstanding loans Unless all companies are performing well and no one expects volatility around LIBOR cessation(!), borrowers may be well-advised to go with hardwired fallbacks

0%

20%

40%

60%

80%

100%

2/13 2/20 2/27 3/5 3/12 3/19 3/26 4/2 4/9 4/16 4/23

Share of performing loans in the S&P/LSTA LL Index

Below 90

Below 80

Below 70

Source: S&P/LCD

44

• Hardwired fallbacks – ARRC BLWG is refining the business loan hardwired fallback language to incorporate what we’ve learned in the past year; ARRC recommending market being using hardwired fallbacks by 3Q20

• New SOFR Loans - The LSTA is developing concept credit agreements for compounded SOFR in arrears (and not LIBOR) and simple SOFR in arrears.

Documentation next steps

45

APPENDIX – SUPPORTING SLIDES

46

The SOFRs “Known in Advance”

SOFR Compounded in Advance Description: The SOFR rate calculated by compounding daily rate for previous 1/3/6-month periods. For a 30-day SOFR loan beginning April 1st, SOFR would be compounded Mar 1-30th, and the compounded SOFR would be locked in on April 1st.

• Strengths: Rate known in advance; looks and feels like LIBOR; easy to operationalize

• Weaknesses: Backwards looking and may be perceived to be stale; some banks uncomfortable with asset-liability management issues

Forward Looking Term SOFR RR Description: The forward-looking 1/3-month rate; most analogous to LIBOR. Because SOFR is a daily rate, any forward looking term rate must be developed through SOFR futures trading.

• Strengths: Rate known in advance; looks and feels like LIBOR; easy to operationalize

• Weaknesses: Does not exist today; Will not exist for years; Not guaranteed to exist as an IOSCO compliant rate at LIBOR cessation or for syndicated loans; fallbacks may not be perfectly hedgeable

47

The SOFRs Not “Known in Advance”

SOFR Compounded in Arrears Description: Daily rate compounded over the life of the interest contract. For a 30-day SOFR loan beginning April 1st, SOFR would be pulled and compounded every day from April 1-30th.

• Strengths: What ISDA is doing; perfectly hedgeable; is the actual interest rate over the interest period; includes (slight) time value of money

• Weaknesses: Rate not known in advance; looks and feels very different from LIBOR; challenging to operationalize; significant conventions changes

Daily Simple SOFR in Arrears Description: Daily SIMPLE rate over the life of the interest period. For a 30-day SOFR loan beginning April 1st, SOFR would be pulled and accrued (but not compounded) every day from April 1-30th.

• Strengths: Understandable; rate is close to compounded in arrears; much easier than compounded in arrears to operationalize

• Weaknesses: Rate not known in advance; however, systems can take a daily uncompounded rate; will require conventions changes

48

• Issue: SOFR Compounded in Arrears loans may be complicated to trade. • On a daily compounded rate loan, both the principal and interest are compounded daily. This is reasonably

easy to calculate if there is no trading. However, if a loan is sold intraperiod, the seller will 1) earn interest on the loan for the period it owned it and 2) may earn “interest on interest” that it earned when it owned the loan even though it no longer owns the loans. This is not necessarily a material economic issue, but the operational aspect gets very complex with a lot of trading. There were roughly 80,000 loan trades in October 2019, according to LSTA trade study.

• It will be necessary to track whether the seller or the buyer is owed Compounded “Interest on Interest” on

every single trade. Options are below; 2 & 3 are demonstrated on following page: 1. Simple SOFR: This is not an issue with Simple SOFR because there is no compounding. 2. Seller keeps the Compounded “Interest on Interest” of any sale. This may be operationally cumbersome and may slow systems significantly. (“Independent Calc” Methodology, Column 8) 3. Buyer “buys” Compounded “Interest on Interest” of any purchase. This more complex than today, but is operationally simpler than seller retaining interest on interest; it will require the market to understand and price the (very small) stub of interest on interest. (“Pro Rata” Methodology, Column 9) 4. (Theoretically) Trade with Accrued Interest: Because only the owner of record receives interest, there is no need to track “interest on interest” for instruments that trade with accrued. Thus, this issue is not a problem for FRNs.

Simple vs Compound SOFR: Trading Issues

Related Documents