The plastic money in the economy and its impact on the speed in economic activities Presented By: Nirbhik Jangid

Plastic money in the Economy and Its Impact on the Speed in Economic Activities

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The plastic money in the

economy and its impact on

the speed in economic

activities

Presented By:

Nirbhik Jangid

What is plastic money?

Plastic money is a term that is used predominantly in reference to the hard plastic cards we use everyday in place of actual bank notes. They can come in many different forms such as cash cards, credit cards, debit cards, pre-paid cash cards and store cards.

Types of Plastic Money

Debit Cards

Credit Cards

Cash Cards

Prepaid Cash Cards

Cash cards:

• Allows you to withdraw money directly from your bank via ATM.

• But it will not allow the holder to purchase anything directly with it.

Credit cards:

• It permits the card holder to withdraw cash from an ATM and allows the user to purchase goods and services directly.

• But, unlike a cash card the money is basically a high interest loan to the card holder.

Debit cards:

• This type of card will directly debit money from your bank account and can be used to purchase goods and services.

• If an overdraft facility is available then the limit will be to the extent of the overdraft.

Prepaid cash cards:

• As the name suggest, the user will add credit to the card themselves and will not exceed that amount.

Economy

The state of a country or region

in terms of the production and

consumption of goods and

services and the supply of

money .

Careful management of

available resources.

Economic Cycle

Impact of electronic payment

on economic growthRising card payments drive economic

growth

Value derived from the migration to electronic payment

Card penetration

The macroeconomic impact of card usage

The value of card payment

Rising card payments drive

economic growth

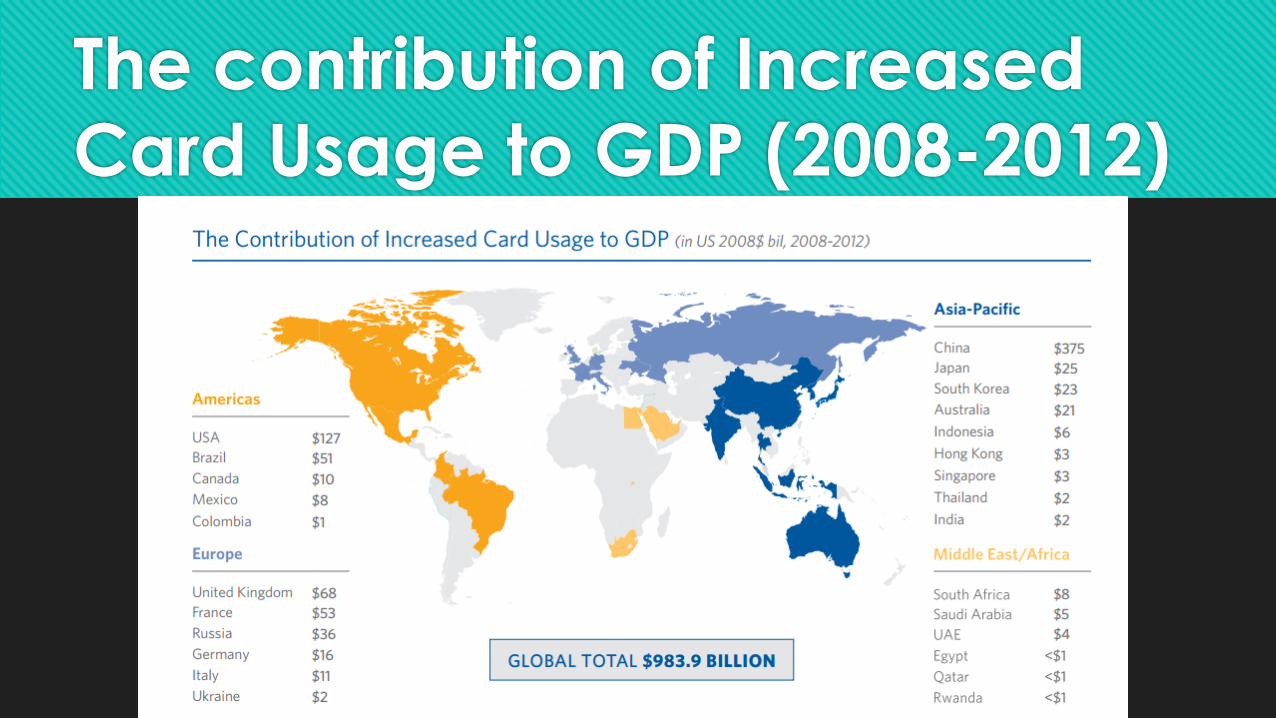

Global economic growth - $983B (2008–2012)

Electronic payment contributed to

Emerging markets - 0.8% increase in GDP

Developed markets - 0.3% increase in GDP

Card growth boosts recovery - Global real GDP was only 1.8% per annum (2008–2012); without increased card usage, that growth would have been 1.6%

Value derived from the migration

to electronic payment

Higher potential tax revenue.

Lower cash handling cost.

Guaranteed payment for merchants.

A reduction in the gray economy due to lower

unreported cash transaction.

Greater financial inclusion.

Card penetration

The macroeconomic impact

of card usage

The card usage in 2008 was 27.4% which has

drastically increased to 32.8% in 2012.

Private consumption.

Card penetration as a percent of total PCE.

The growth of card usage.

GDP growth due to card usage.

Global Total Non-Cash Transaction Volumes

2008, 2011 and 2015 (Millions)

The contribution of Increased

Card Usage to GDP (2008-2012)

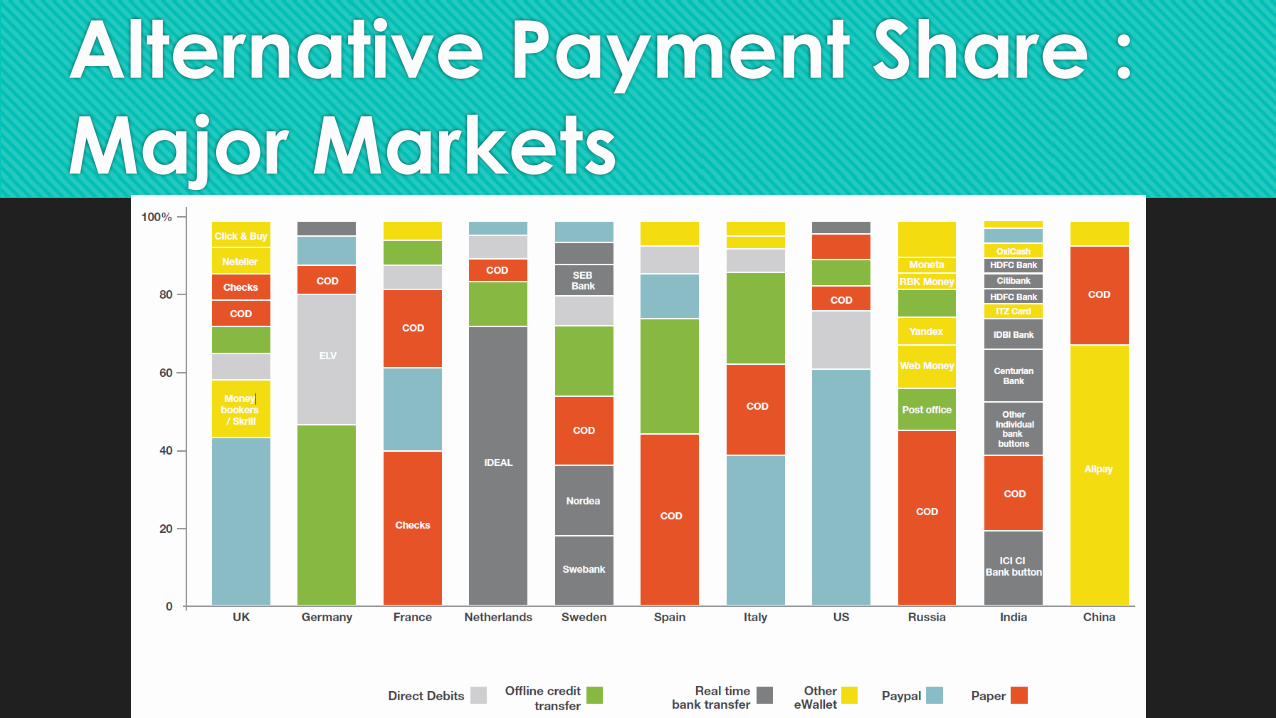

Alternative Payment Share :

Major Markets

Smaller Markets

The value of card payment

Less friction more efficiency.

Card benefits all parties (consumer, merchant, bank ).

Security.

Convenience.

Transparency.

Reference

Facts are collected from

Moody’s Analytics report covering 2008-2012

RBI, Mint Research

Nielsen - IS THE SWIPE REPLACING THE CHA-CHING AT THE CASH REGISTER?

ROI Payments

You would love this.

• Internet usage

Worldwide, 2015

Next Slide

Nirbhik JangidConnect with me just by one click

Related Documents