Plant Assets, Natural Resources, and Intangibles Chapter 9 Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-1

Plant Assets, Natural Resources, and Intangibles Chapter 9 Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall9-1.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Plant Assets, Natural Resources,

and Intangibles

Chapter 9

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-1

Learning Objectives

1. Measure the cost of a plant asset

2. Account for depreciation using the straight-line, units-of-production, and double-declining-balance methods

3. Journalize entries for the disposal of plant assets

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-2

Learning Objectives

4. Account for natural resources

5. Account for intangible assets

6. Use the asset turnover ratio to evaluate business performance

7. Journalize entries for the exchange of plant assets (Appendix 9A)

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-3

Learning Objective 1

Measure the cost of a plant asset

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-4

What Are Plant Assets?

Long-lived, tangible assets used in the operation of the business.

• Land• Buildings• Equipment• Furniture• Automobiles

Cost PrincipleThe actual cost of a plant

asset is its purchase price plus all the costs

necessary to get the asset ready for its

intended use.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-5

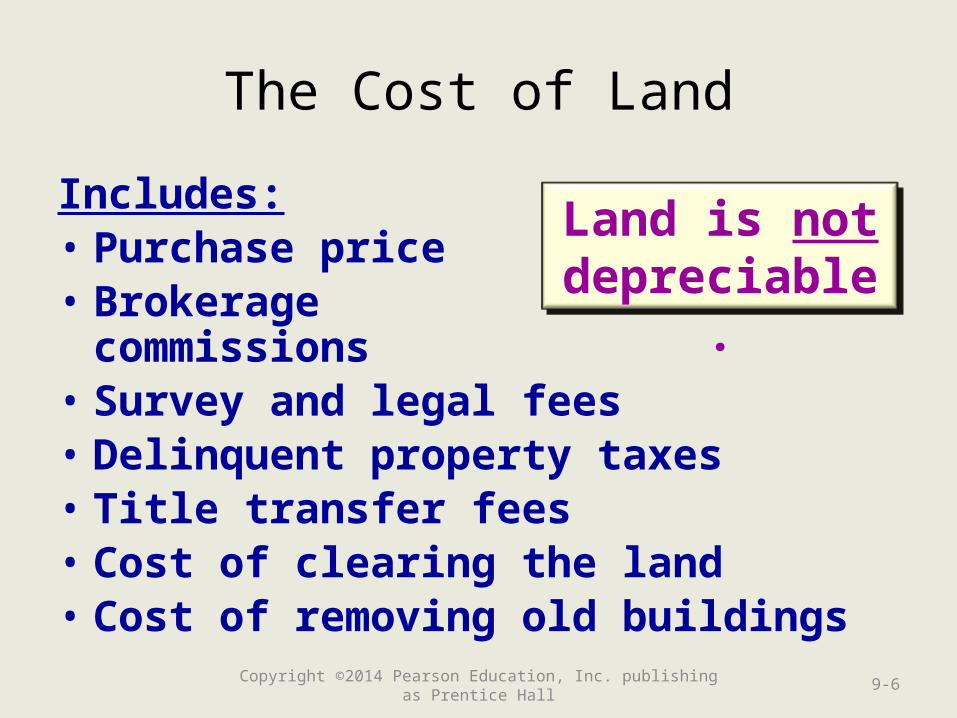

The Cost of Land

Land is not depreciable.

Includes:• Purchase price• Brokerage

commissions• Survey and legal fees• Delinquent property taxes• Title transfer fees• Cost of clearing the land• Cost of removing old buildings

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-6

The Cost of Land

These costs are referred to as

Land Improvements.

Land Improvements ARE depreciated.

Does Not Include:• Fencing• Paving• Sprinkler systems• Lighting• Signs

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-7

The Cost of Land

Smart Touch Learning purchases land on August 1, 2015, for $50,000 with a note payable. Other

costs related to this transaction include $4,000 in delinquent property taxes, $2,000 in transfer

taxes, $5,000 to remove an old building, and a $1,000 survey fee. The additional costs are paid

in cash.

What is the cost of the land on Smart Touch Learning’s books?

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-8

The Cost of Land

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-9

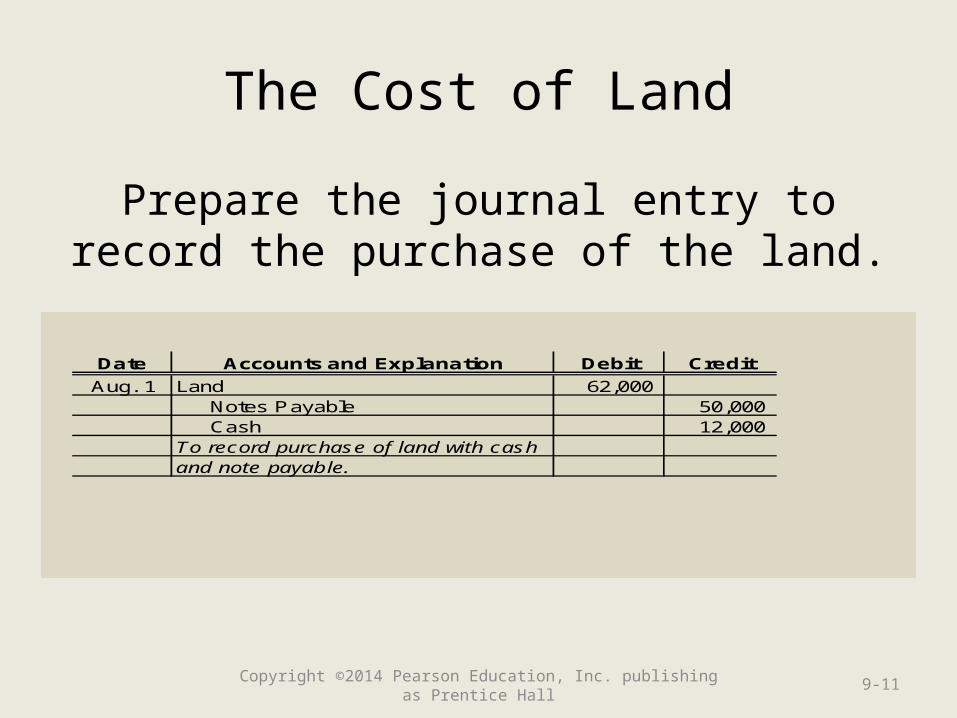

The Cost of Land

Prepare the journal entry to record the purchase of the land.

Date Accounts and Explanation Debit Credit

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-10

The Cost of Land

Prepare the journal entry to record the purchase of the land.

Date Accounts and Explanation Debit Credit

Aug. 1 Land 62,000 Notes Payable 50,000 Cash 12,000 To record purchase of land with cashand note payable.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-11

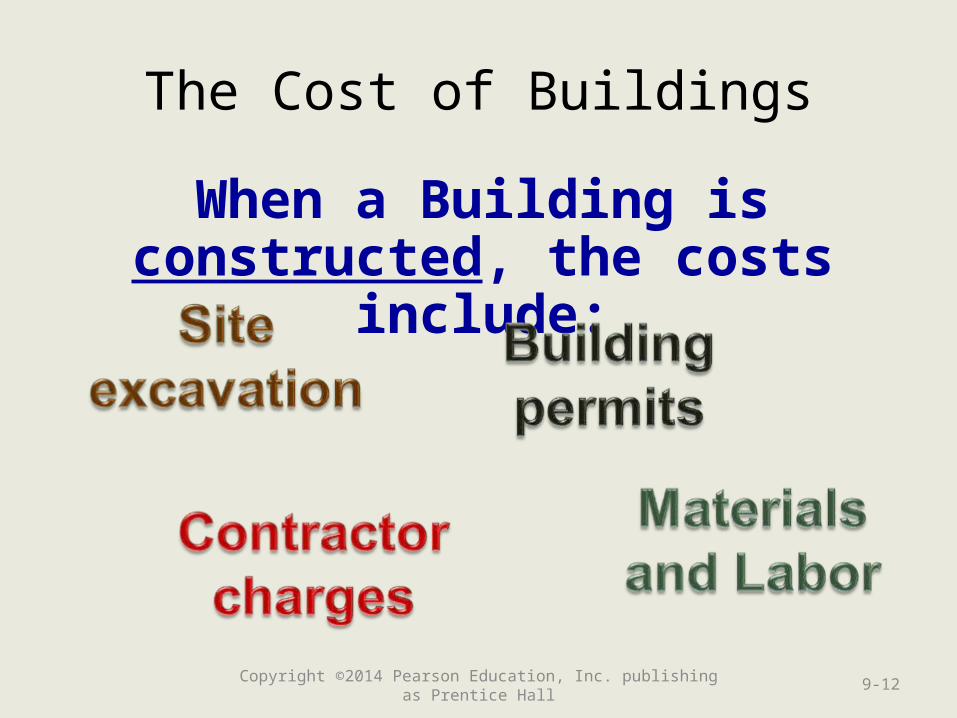

The Cost of Buildings

When a Building is constructed, the costs include:

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-12

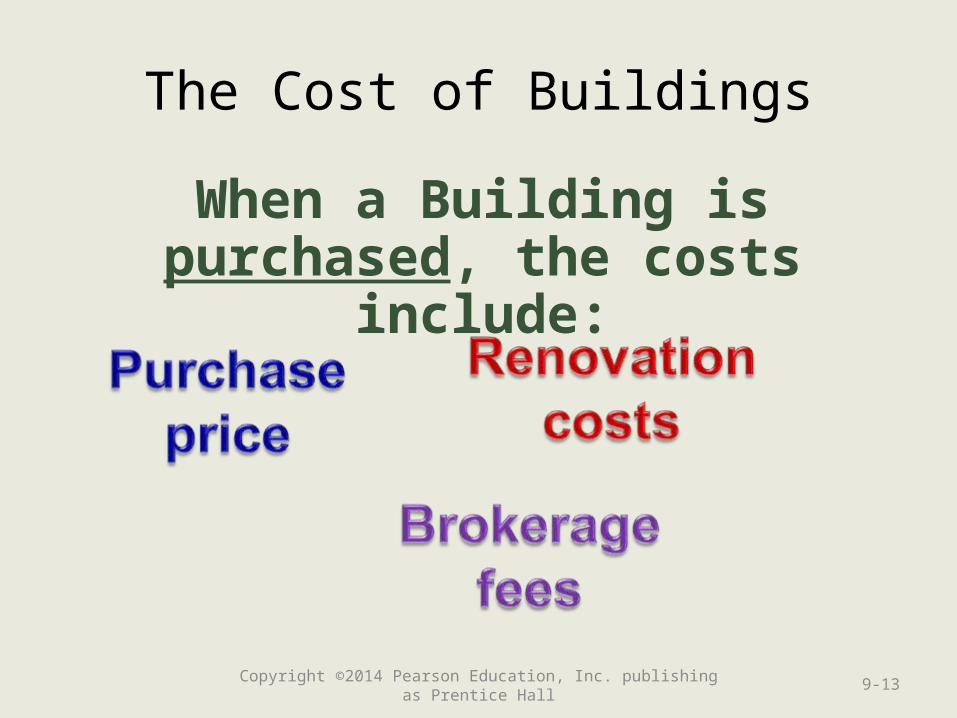

The Cost of Buildings

When a Building is purchased, the costs include:

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-13

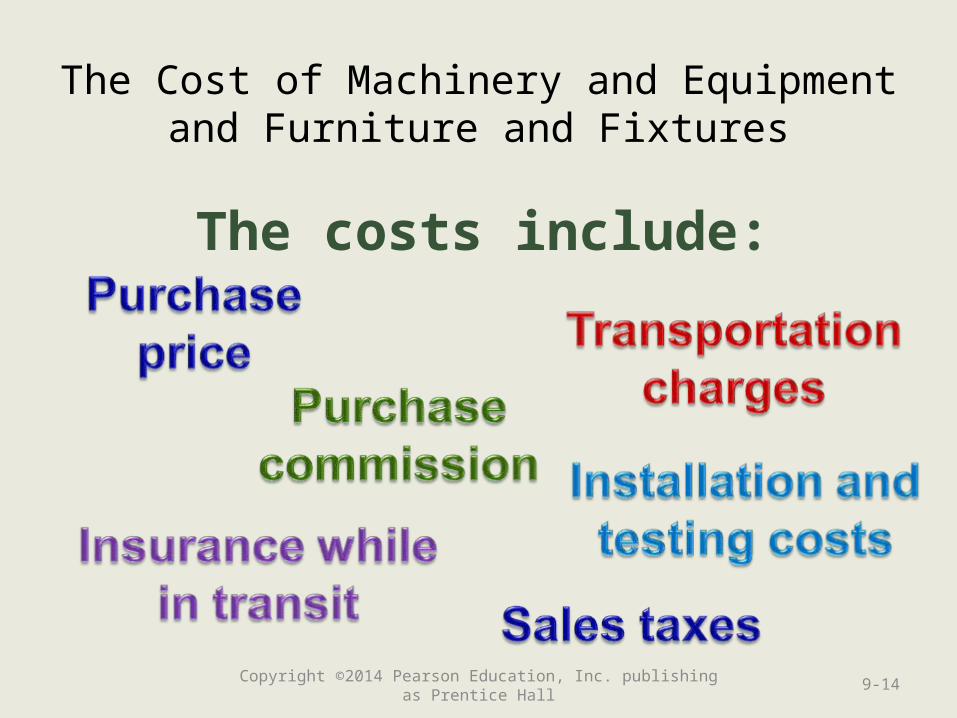

The Cost of Machinery and Equipment and Furniture and Fixtures

The costs include:

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-14

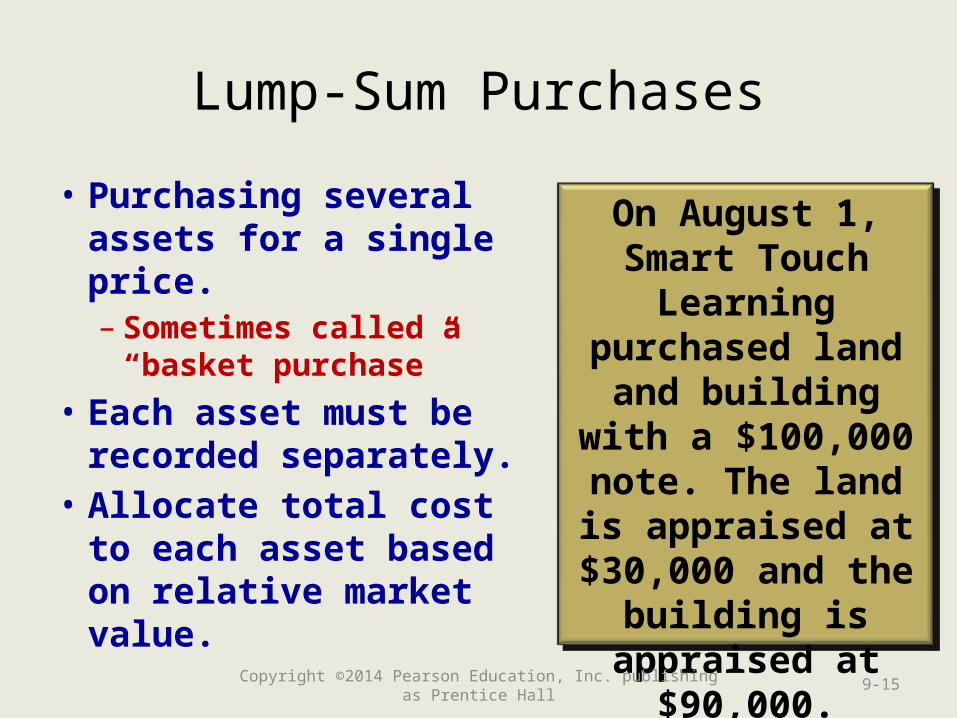

Lump-Sum Purchases

• Purchasing several assets for a single price.– Sometimes called a

“basket purchase”

• Each asset must be recorded separately.

• Allocate total cost to each asset based on relative market value.

On August 1, Smart Touch Learning

purchased land and building with a

$100,000 note. The land is appraised at

$30,000 and the building is

appraised at $90,000.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-15

Lump-Sum Purchases

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-16

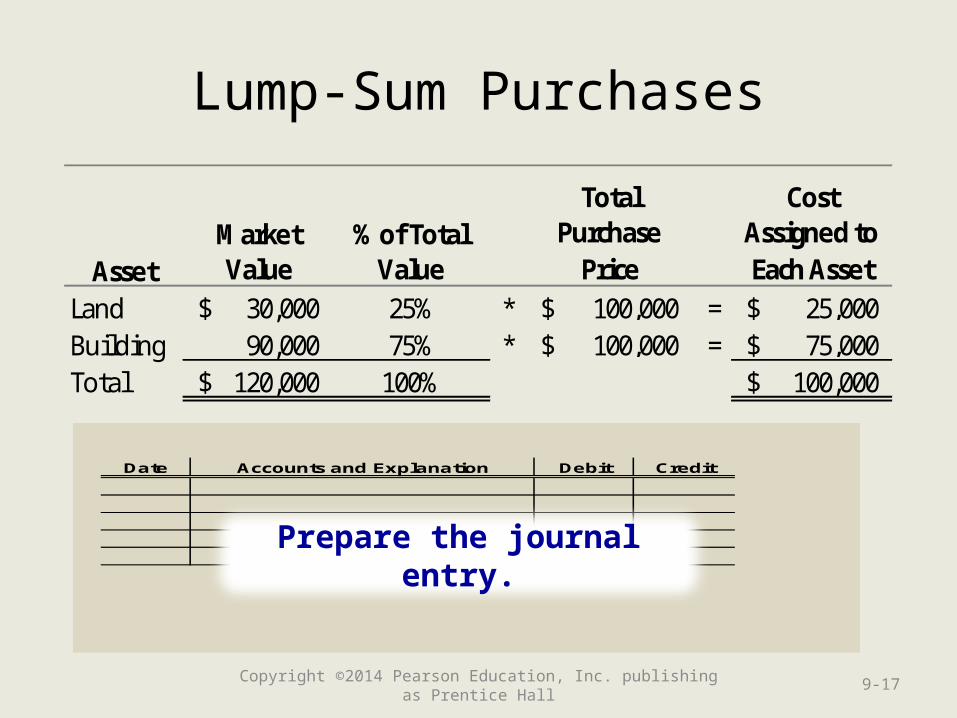

Lump-Sum Purchases

AssetMarket Value

% of Total Value

Total Purchase

Price

Cost Assigned to Each Asset

Land 30,000$ 25% * 100,000$ = 25,000$ Building 90,000 75% * 100,000$ = 75,000$ Total 120,000$ 100% 100,000$

Date Accounts and Explanation Debit Credit

Prepare the journal entry.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-17

Lump-Sum Purchases

AssetMarket Value

% of Total Value

Total Purchase

Price

Cost Assigned to Each Asset

Land 30,000$ 25% * 100,000$ = 25,000$ Building 90,000 75% * 100,000$ = 75,000$ Total 120,000$ 100% 100,000$

Aug. 1 Land 25,000 Building 75,000 Notes Payable 100,000 To record purchase of land and building.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-18

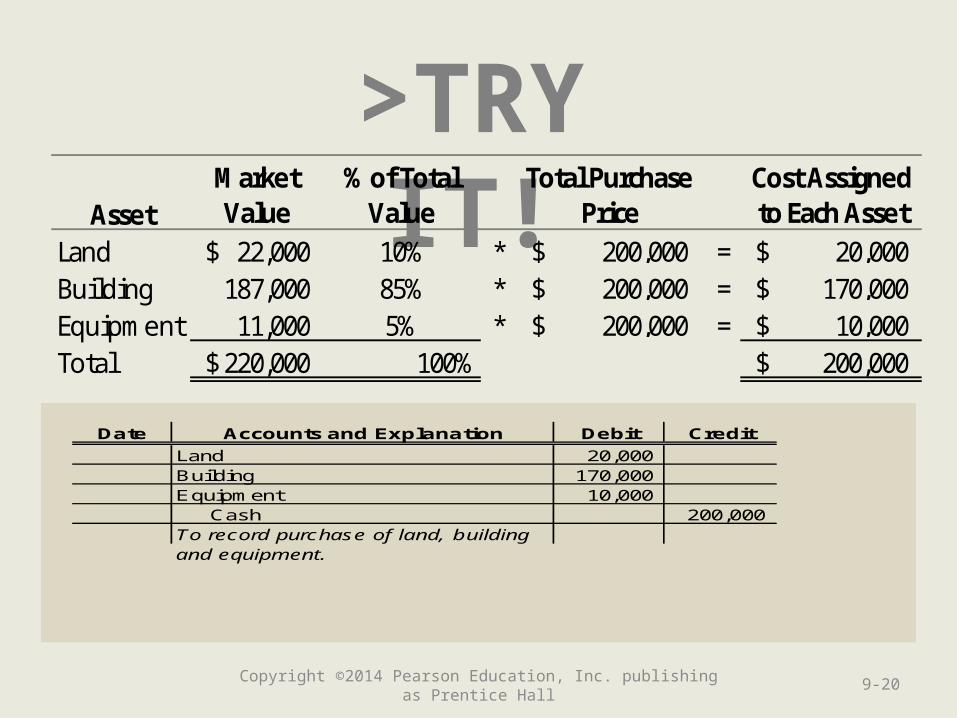

>TRY IT!

Date Accounts and Explanation Debit Credit

Budget Banners pays $200,000 for a bulk purchase of land, building, and equipment. The land had a market value of $22,000, the building had a market value of $187,000, and the equipment had a market

value of $11,000.

Prepare the journal entry.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-19

>TRY IT!

Date Accounts and Explanation Debit Credit

Land 20,000 Building 170,000 Equipment 10,000 Cash 200,000 To record purchase of land, buildingand equipment.

AssetMarket Value

% of Total Value

Total Purchase Price

Cost Assigned to Each Asset

Land 22,000$ 10% * 200,000$ = 20,000$ Building 187,000 85% * 200,000$ = 170,000$ Equipment 11,000 5% * 200,000$ = 10,000$ Total 220,000$ 100% 200,000$

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-20

Learning Objective 2

Account for depreciation using the straight-line,

units-of-production, and double-

declining-balance methods

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-21

What Is Depreciation?

• Plant assets are recorded as assets when purchased.

• Depreciation is the process of allocating an asset’s cost to expense over its useful life.

Remember, to record depreciation, we debit Depreciation Expense

and credit Accumulated

Depreciation (a contra-asset).

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-22

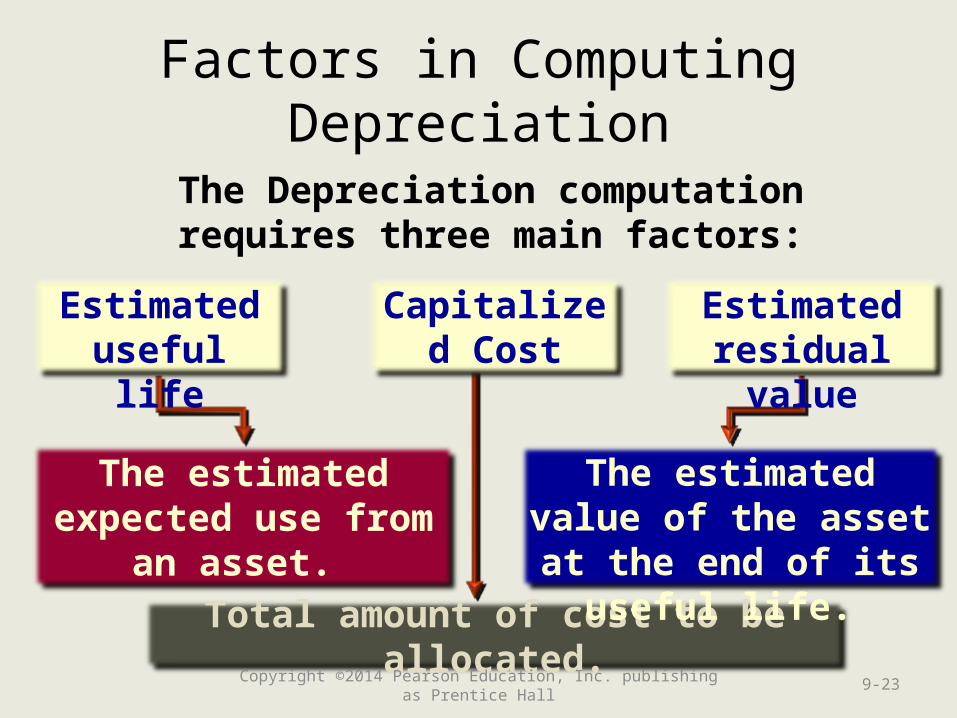

The Depreciation computation requires three main factors:

The estimated expected use from an

asset.

Total amount of cost to be allocated.

The estimated value of the asset at the end of

its useful life.

Capitalized Cost

Estimated useful life

Estimated residual value

Factors in Computing Depreciation

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-23

Smart Touch Learning purchases a truck on

January 1, 2014

Smart Touch Learning purchases a truck on

January 1, 2014

Depreciation Methods

There are three common

depreciation methods:

• Straight-Line• Units-of-

Production• Declining-

Balance

There are three common

depreciation methods:

• Straight-Line• Units-of-

Production• Declining-

Balance

Data Item AmountCost of Truck 41,000$ Est. Residual Value 1,000 Depreciable Cost 40,000$ Est. Useful Life - Years 5 yearsEst. Useful Life - Units 100,000 miles

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-24

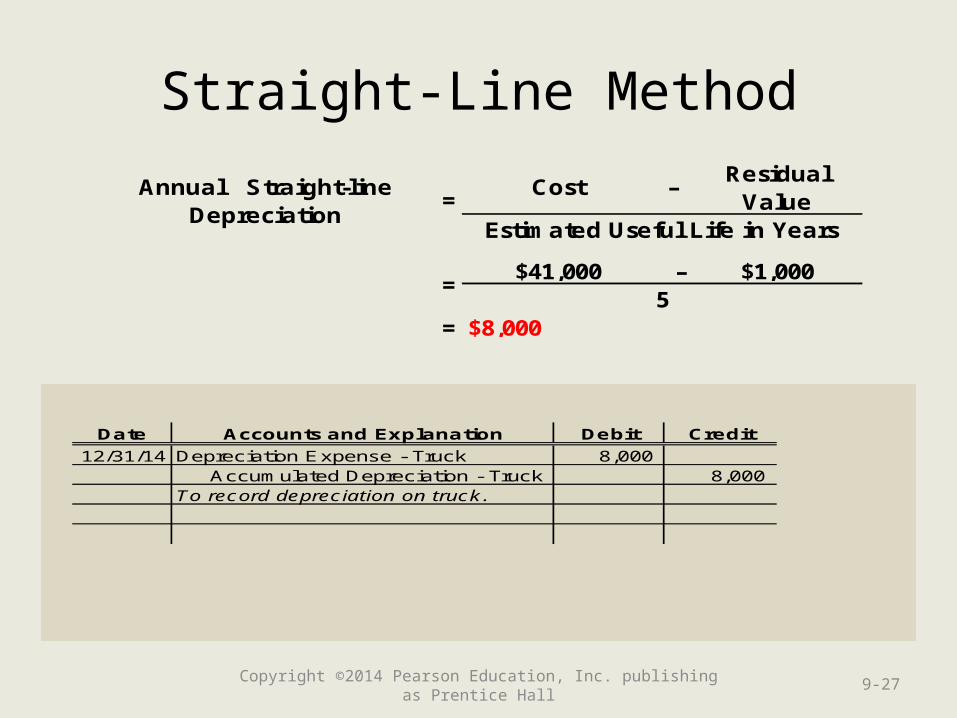

Straight-Line Method

The most widely used and most

easily understood method.

Results in the same amount of depreciation in each year of the asset’s

service life.

Cost –Residual

ValueEstimated Useful Life in

Years

Annual Straight-line Depreciation

=

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-25

Cost –Residual

Value

$41,000 – $1,000

= $8,000

=

Estimated Useful Life in Years

Annual Straight-line Depreciation

=

5

Straight-Line Method

Date Accounts and Explanation Debit Credit

Prepare the journal entry at December 31, 2014.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-26

Cost –Residual

Value

$41,000 – $1,000

= $8,000

=

Estimated Useful Life in Years

Annual Straight-line Depreciation

=

5

Straight-Line Method

Date Accounts and Explanation Debit Credit

12/31/14 Depreciation Expense - Truck 8,000 Accumulated Depreciation - Truck 8,000 To record depreciation on truck .

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-27

Units-of-Production Method

• Depreciation is a function of how much an asset is USED, rather than its age.

• Less predictable than other methods.

Smart Touch Learning purchases a truck on

January 1, 2014

Smart Touch Learning purchases a truck on

January 1, 2014

Data Item AmountCost of Truck 41,000$ Est. Residual Value 1,000 Depreciable Cost 40,000$ Est. Useful Life - Years 5 yearsEst. Useful Life - Units 100,000 miles

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-28

Units-of-Production Method

Assuming Smart Touch Learning drives the truck 20,000 miles in the first year, how much

depreciation should be recorded?

Step 1: Compute Depreciation per Unit

Depreciation per Unit

= ( Cost -Residual

Value ) ÷ Useful Life in Units

= ( $41,000 - $1,000 ) ÷ 100,000 miles = $0.40 per mile

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-29

Units-of-Production Method

Assuming Smart Touch Learning drives the truck 20,000 miles in the first year, how much

depreciation should be recorded?

Step 2: Compute Depreciation for the Period

Depreciation =Depreciation

per Unit *Current Year

Usage = $0.40 * 20,000 miles = $8,000 Depr. Exp. - Year 1

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-30

Double-Declining Balance Method

• An accelerated method.

• More depreciation early in an asset’s life.

• Total depreciation the same over the asset’s full life.

Smart Touch Learning purchases a truck on

January 1, 2014

Smart Touch Learning purchases a truck on

January 1, 2014

Data Item AmountCost of Truck 41,000$ Est. Residual Value 1,000 Depreciable Cost 40,000$ Est. Useful Life - Years 5 yearsEst. Useful Life - Units 100,000 miles

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-31

Double-Declining Balance Method

Multiply an asset’s declining book value by twice the straight-line depreciation

rate.Double-

Declining-Balance

Depreciation

= ( Cost -Accumulated Depreciation ) * ( 2 ÷

Useful Life )

= ( 41,000$ - $0 ) * ( 2 ÷ 5 years ) = 16,400$ Depreciation in Year 1

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-32

Double-Declining Balance Method

Multiply an asset’s declining book value by twice the straight-line depreciation

rate.Double-

Declining-Balance

Depreciation

= ( Cost -Accumulated Depreciation ) * ( 2 ÷

Useful Life )

= ( 41,000$ - $0 ) * ( 2 ÷ 5 years ) = 16,400$ Depreciation in Year 1

= ( 41,000$ - $16,400 ) * ( 2 ÷ 5 years ) = 9,840$ Depreciation in Year 2

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-33

Learning Objective 3

Journalize entries for the disposal of plant

assets

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-34

Discarding Plant Assets

• When an asset is disposed, sold, or retired, it must be removed from the books.

• All related Accumulated Depreciation must also be removed from the books.

• Gains/Losses on disposal are recorded.

STEPS• Bring depreciation up to

date.• Remove original cost of

asset and accumulated depreciation from the books.

• Record any cash received.

• Record the difference between book value and the cash received as a gain or loss.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-35

Discarding Plant AssetsExample #1

On July 1, Smart Touch Learning discards equipment that cost $10,000. The accumulated depreciation on the

asset is $10,000.

Date Accounts and Explanation Debit Credit

Prepare the journal entry at July 1, 2013.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-36

Discarding Plant AssetsExample #1

On July 1, Smart Touch Learning discards equipment that cost $10,000. The accumulated depreciation on the

asset is $10,000.

Date Accounts and Explanation Debit Credit

7/1/13 Accumulated Depreciation--Equip. 10,000 Equipment 10,000 Discarded fully depreciated equip.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-37

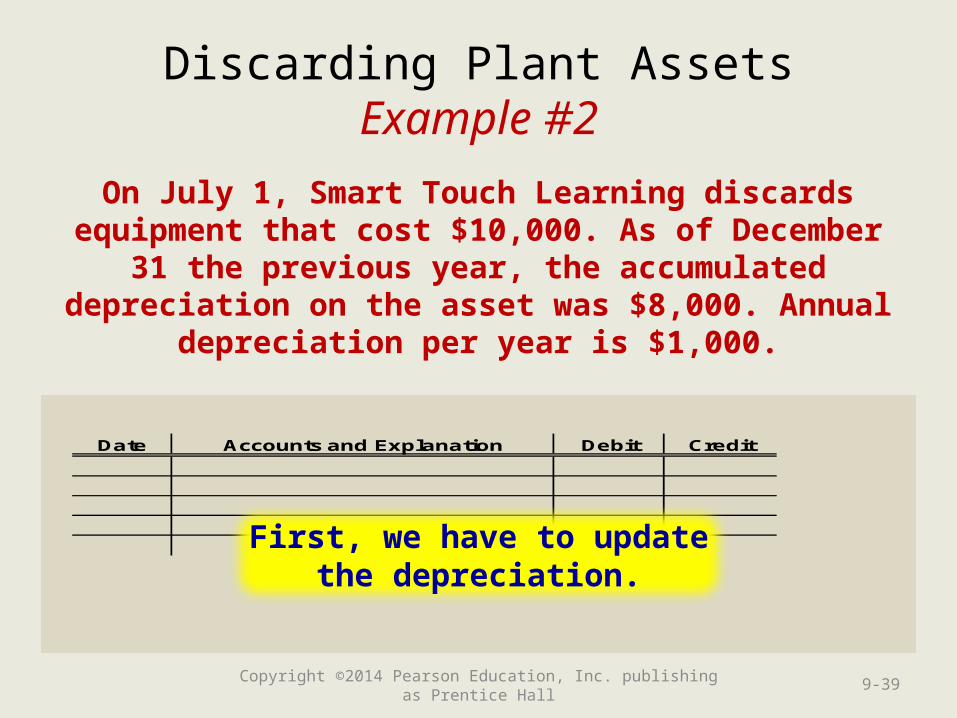

Discarding Plant AssetsExample #2

On July 1, Smart Touch Learning discards equipment that cost $10,000. As of December 31 the previous year, the accumulated depreciation

on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

Prepare the journal entry at July 1, 2013.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-38

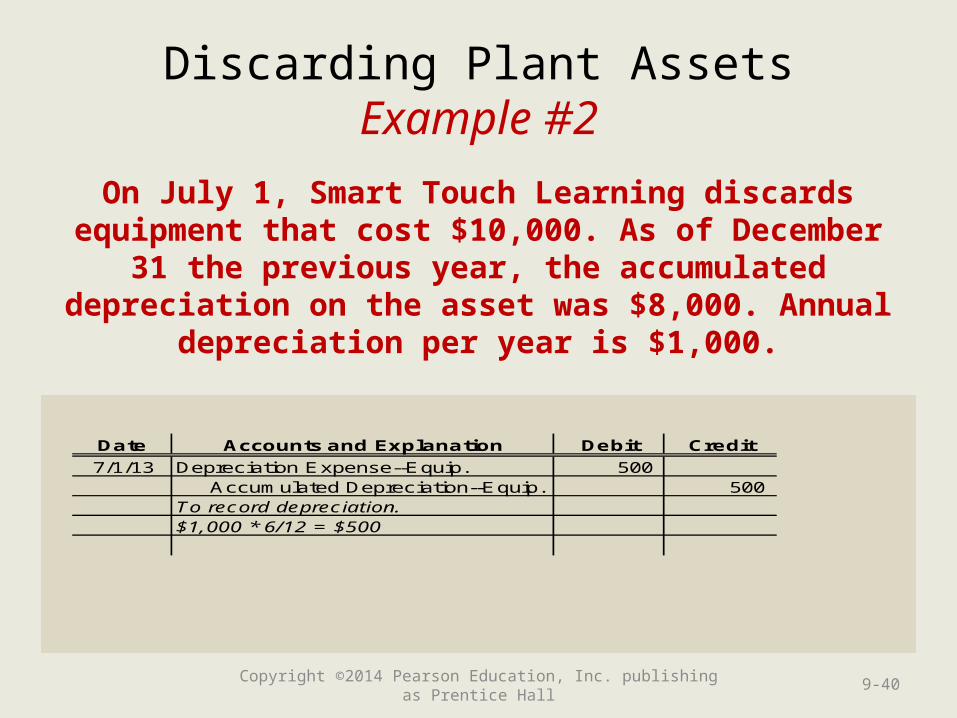

Discarding Plant AssetsExample #2

On July 1, Smart Touch Learning discards equipment that cost $10,000. As of December 31 the previous year, the accumulated depreciation

on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

First, we have to update the depreciation.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-39

Discarding Plant AssetsExample #2

On July 1, Smart Touch Learning discards equipment that cost $10,000. As of December 31 the previous year, the accumulated depreciation

on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

7/1/13 Depreciation Expense--Equip. 500 Accumulated Depreciation--Equip. 500 To record depreciation.$1,000 * 6/12 = $500

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-40

Discarding Plant AssetsExample #2

On July 1, Smart Touch Learning discards equipment that cost $10,000. As of December 31 the previous year, the accumulated depreciation

on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

Second, record the disposal.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-41

Discarding Plant AssetsExample #2

On July 1, Smart Touch Learning discards equipment that cost $10,000. As of December 31 the previous year, the accumulated depreciation

on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

7/1/13 Accumulated Depreciation--Equip. 8,500 Loss on Disposal 1,500 Equipment 10,000 To record disposal of equipment.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-42

Discarding Plant AssetsExample #3

On July 1, Smart Touch Learning sells equipment for $4,000. The equipment cost

$10,000. As of December 31 the previous year, the accumulated depreciation on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

Prepare the journal entries at July 1, 2013.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-43

Discarding Plant AssetsExample #3

On July 1, Smart Touch Learning sells equipment for $4,000. The equipment cost

$10,000. As of December 31 the previous year, the accumulated depreciation on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

First, update depreciation.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-44

Discarding Plant AssetsExample #3

On July 1, Smart Touch Learning sells equipment for $4,000. The equipment cost

$10,000. As of December 31 the previous year, the accumulated depreciation on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

7/1/13 Depreciation Expense--Equip. 500 Accumulated Depreciation--Equip. 500 To record depreciation.$1,000 * 6/12 = $500

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-45

Discarding Plant AssetsExample #3

On July 1, Smart Touch Learning sells equipment for $4,000. The equipment cost

$10,000. As of December 31 the previous year, the accumulated depreciation on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

Second, record the sale.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-46

Discarding Plant AssetsExample #3

On July 1, Smart Touch Learning sells equipment for $4,000. The equipment cost

$10,000. As of December 31 the previous year, the accumulated depreciation on the asset was $8,000. Annual depreciation per year is $1,000.

Date Accounts and Explanation Debit Credit

7/1/13 Cash 4,000 Accumulated Depreciation--Equip. 8,500 Gain on Sale of Equipment 2,500 Equipment 10,000 To record sale of equipment.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-47

Learning Objective 4

Account for natural resources

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-48

Natural Resources

• Assets that come from the earth and are consumed.

• The value of the “reserves” that a company owns/controls is a long-term asset.

Includes:• Iron ore• Oil• Natural Gas• Coal• Timber• Diamonds• Gold and silver

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-49

Natural Resources

• As the resources are extracted, Depletion Expense is recorded.

• A contra-asset Accumulated Depletion is also recorded.

• Steps (similar to Units-of-Production)1. Compute Depletion per Unit (based on

estimated reserves)

2. Compute Depletion for the period (based on actual extraction)

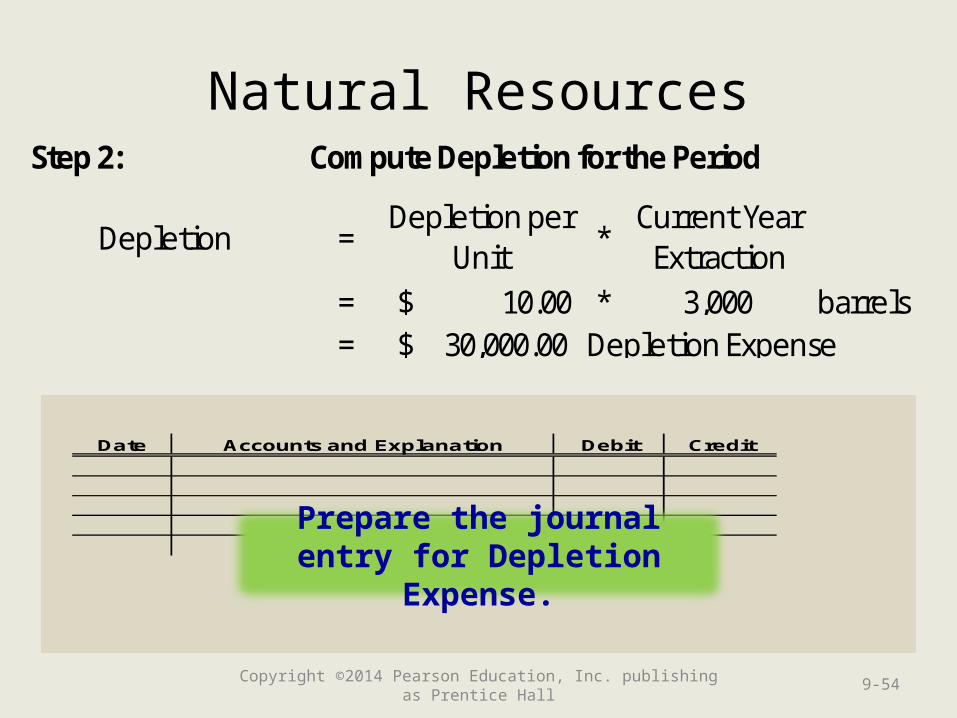

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-50

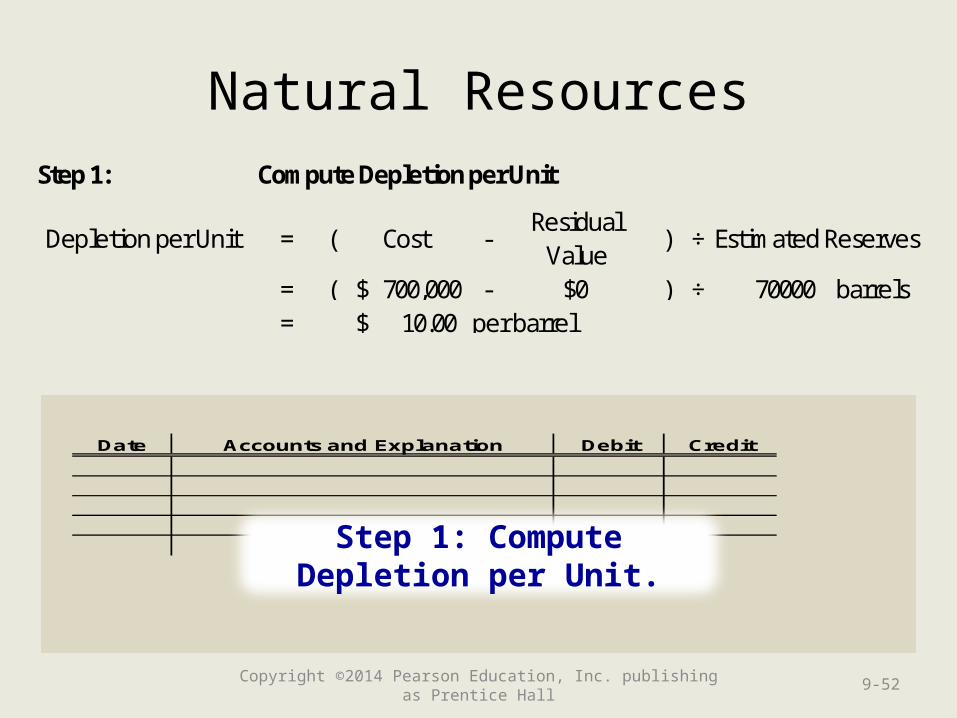

Natural Resources

A company owns oil reserves that cost $700,000 and is estimated to contain 70,000

barrels of oil. During the year, 3,000 barrels of oil are extracted.

Date Accounts and Explanation Debit Credit

Prepare the journal entry for Depletion Expense.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-51

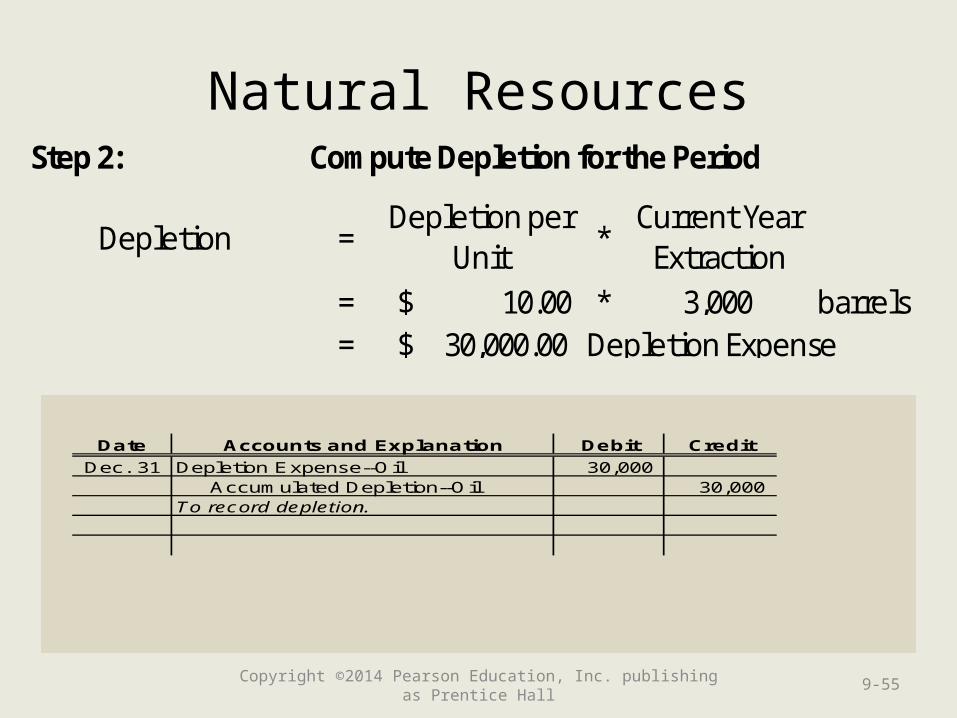

Natural Resources

Date Accounts and Explanation Debit Credit

Step 1: Compute Depletion per Unit.

Step 1: Compute Depletion per Unit

Depletion per Unit = ( Cost -Residual

Value ) ÷ Estimated Reserves

= ( $ 700,000 - $0 ) ÷ 70000 barrels = 10.00$ per barrel

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-52

Natural Resources

Date Accounts and Explanation Debit Credit

Step 2: Compute Depletion for the Period.

Step 2: Compute Depletion for the Period

Depletion =Depletion per

Unit *Current Year

Extraction = $ 10.00 * 3,000 barrels = 30,000.00$ Depletion Expense

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-53

Natural Resources

Date Accounts and Explanation Debit Credit

Prepare the journal entry for Depletion Expense.

Step 2: Compute Depletion for the Period

Depletion =Depletion per

Unit *Current Year

Extraction = $ 10.00 * 3,000 barrels = 30,000.00$ Depletion Expense

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-54

Natural Resources

Date Accounts and Explanation Debit Credit

Dec. 31 Depletion Expense--Oil 30,000 Accumulated Depletion--Oil 30,000 To record depletion.

Step 2: Compute Depletion for the Period

Depletion =Depletion per

Unit *Current Year

Extraction = $ 10.00 * 3,000 barrels = 30,000.00$ Depletion Expense

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-55

Date Accounts and Explanation Debit Credit

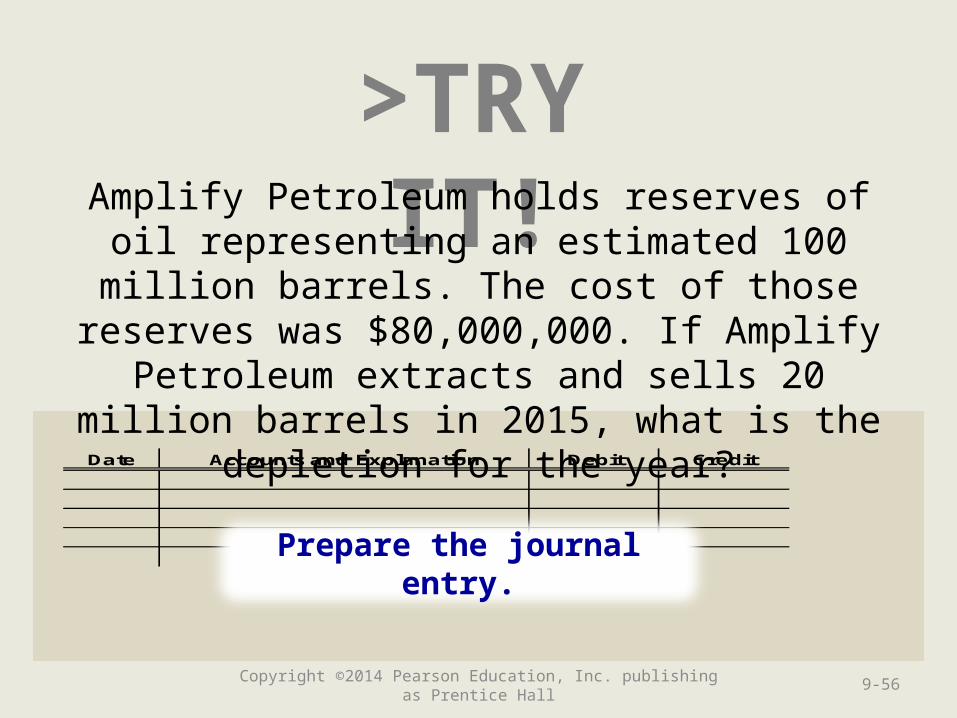

>TRY IT!

Prepare the journal entry.

Amplify Petroleum holds reserves of oil representing an estimated 100 million barrels. The cost of those reserves was $80,000,000. If Amplify Petroleum extracts and sells 20 million barrels in

2015, what is the depletion for the year?

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-56

>TRY IT!

Date Accounts and Explanation Debit Credit

Dec. 31 Depletion Expense--Oil 16,000,000 Accumulated Depletion--Oil 16,000,000 To record depletion for the year.20,000,000 barrels x $.80 per barrel

Amplify Petroleum holds reserves of oil representing an estimated 100 million barrels. The cost of those reserves was $80,000,000. If Amplify Petroleum extracts and sells 20 million barrels in

2015, what is the depletion for the year?

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-57

Learning Objective 5

Account for Intangible Assets

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-58

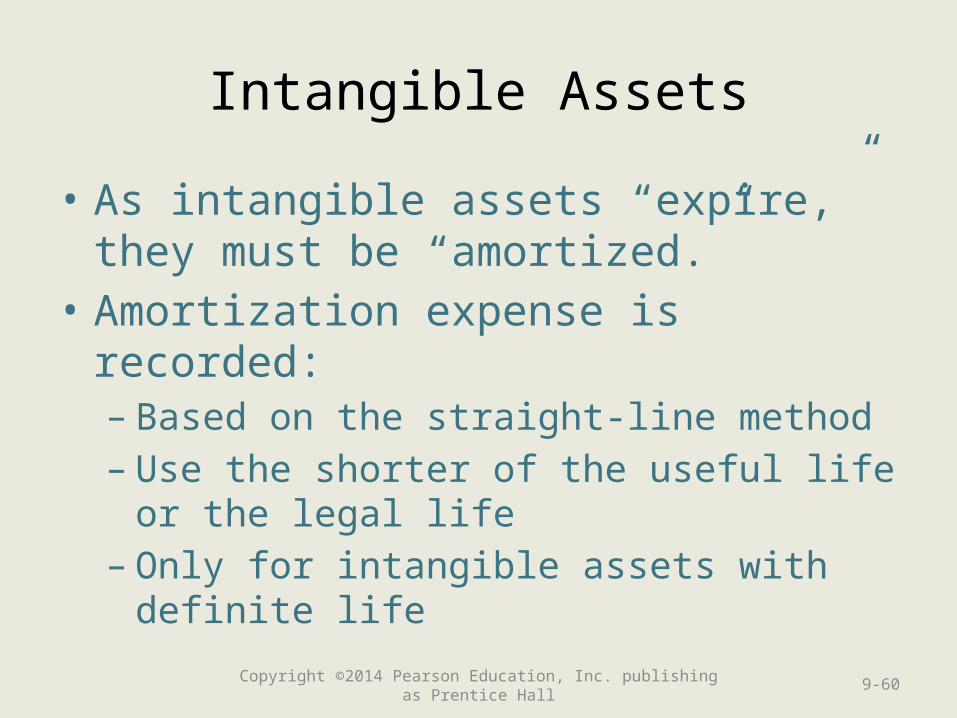

Intangible Assets

• Assets that have no physical substance.

• Usual convey rights to the owner.

• Recorded at cost.• Research and

development costs are NOT included.

Includes• Patents• Copyrights• Trademarks• Franchise

Agreements• Licenses• Goodwill

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-59

Intangible Assets

• As intangible assets “expire,” they must be “amortized.”

• Amortization expense is recorded:– Based on the straight-line method– Use the shorter of the useful life or the legal

life– Only for intangible assets with definite life

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-60

Intangible Assets

• There is no contra-asset account used with the amortization process.– The intangible asset is credited directly.– Each year the asset’s book value will

decrease by the amount of the amortization.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-61

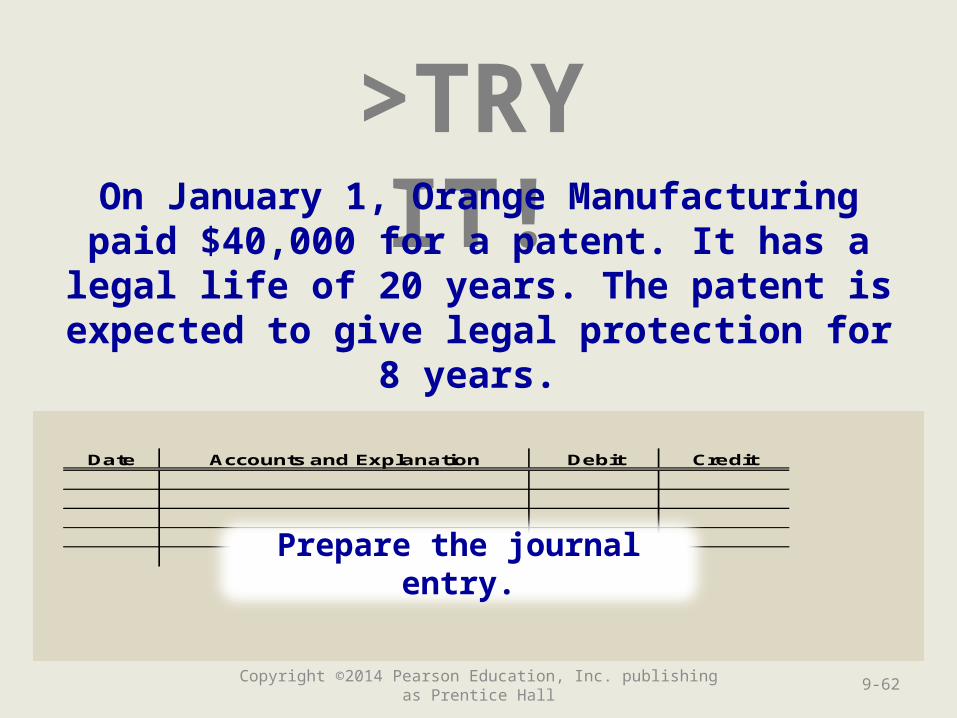

Date Accounts and Explanation Debit Credit

>TRY IT!

Prepare the journal entry.

On January 1, Orange Manufacturing paid $40,000 for a patent. It has a legal life of 20 years. The patent is expected to give legal

protection for 8 years.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-62

Date Accounts and Explanation Debit Credit

Dec. 31 Amortization Expense--Patent 5,000 Patent 5,000 To record amortization of patent.

>TRY IT!On January 1, Orange Manufacturing paid $40,000 for a patent. It has a legal life of 20 years. The patent is expected to give legal

protection for 8 years.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-63

Learning Objective 6

Use the asset turnover ratio to

evaluate business performance

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-64

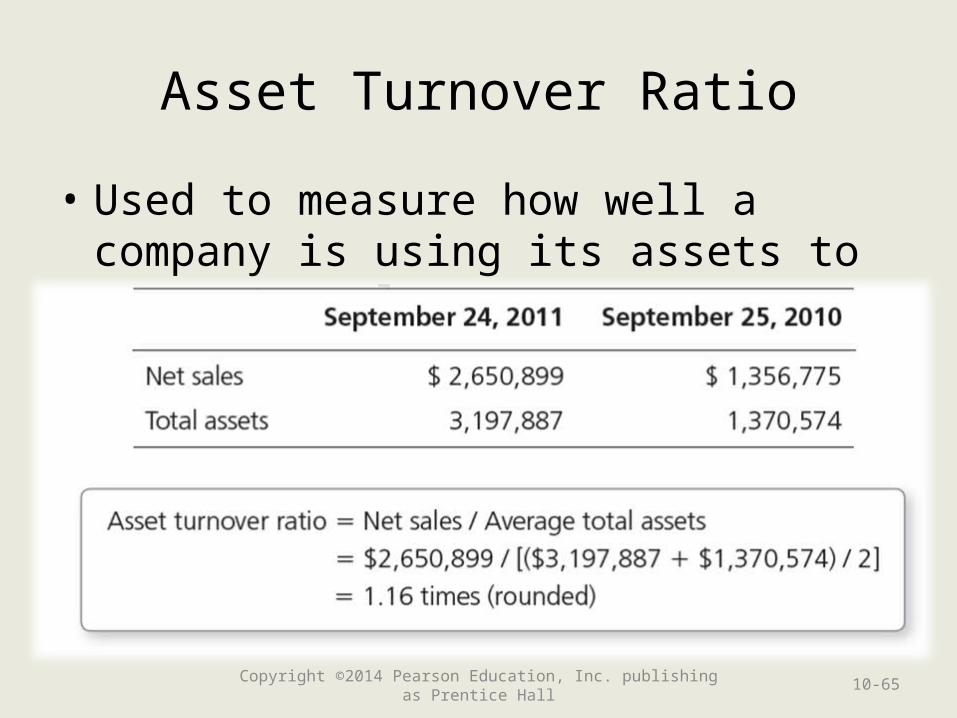

Asset Turnover Ratio

• Used to measure how well a company is using its assets to generate sales revenue.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 10-65

Learning Objective 7

Journalize entries for the exchange of

plant assets (Appendix 9A)

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-66

Exchange Plant Assets

• An exchange includes aspects of a sale and a disposal.

• Special accounting is required if the exchange transaction has commercial substance.– i.e.; the future cash flows will change as a

result of the exchange.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-67

Exchange Plant AssetsIf an exchange lacks

commercial substance, the new asset is recorded at the book value of the

asset that is given up, plus/minus any cash exchanged as

part of the transaction.

An auto dealer trades a blue sedan to another

auto dealer for a similar sedan in black to satisfy a customer’s preference.

There is no commercial substance related to this transaction. The future

cash flows do not change.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-68

Exchange Plant Assets

If an exchange has commercial

substance, the new asset is recorded at its market value on

the date of the exchange.

Gains or losses may have to be recorded.

On December 31, Smart Touch Learning exchanges used equipment and $2,000

cash for new equipment.

The old equipment has a cost of $10,000 and accumulated

depreciation of $9,000.

The new equipment has a market value of $8,000.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-69

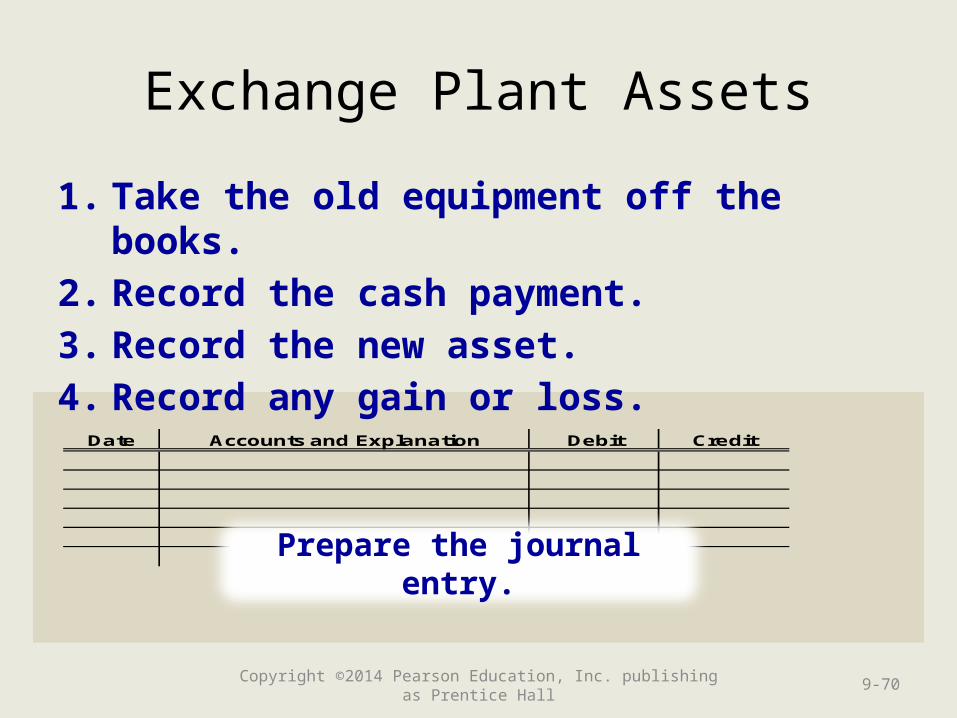

Date Accounts and Explanation Debit Credit

Exchange Plant Assets

1. Take the old equipment off the books.

2. Record the cash payment.

3. Record the new asset.

4. Record any gain or loss.

Prepare the journal entry.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-70

Exchange Plant Assets

1. Take the old equipment off the books.

2. Record the cash payment.

3. Record the new asset.

4. Record any gain or loss.

Date Accounts and Explanation Debit Credit

Dec. 31 Equipment (new) 8,000 Accumulated Depreciation--Equip. 9,000 Equipment (old) 10,000 Cash 2,000 Gain on Exchange 5,000 Exchanged old equipment for new.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-71

>TRY IT!Area Salvage Company purchased equipment

for $10,000. Over the asset’s life, they recorded accumulated depreciation of $8,000. They

exchange the old equipment and $4,000 for new equipment with a market value of $5,000.

Date Accounts and Explanation Debit Credit

Prepare the journal entry.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-72

>TRY IT!Area Salvage Company purchased equipment

for $10,000. Over the asset’s life, they recorded accumulated depreciation of $8,000. They

exchange the old equipment and $4,000 for new equipment with a market value of $5,000.

Date Accounts and Explanation Debit Credit

Equipment (new) 5,000 Accumulated Depreciation--Equip. 8,000 Loss on Exchange 1,000 Equipment (old) 10,000 Cash 4,000 To exchange old equipment for new.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 10-73

End of Chapter 9

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 9-74

Related Documents