placing substandard DI insurance cases DI 1325 7- 13 For Producer use only. Not for use with clients.

Placing substandard DI insurance cases DI 1325 7-13For Producer use only. Not for use with clients.

Jan 03, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

placing substandard DI insurance cases

DI 1325 7-13 For Producer use only. Not for use with clients.

disclosures

• In approved states, Disability Income insurance (forms 4501NC, 4502GR and 4503BOE) is issued by Ameritas Life Insurance Corp. located at 5900 O Street, Lincoln, NE 68510. In New York, Disability Income insurance (forms 5501-NC, 5502-GR and 5503-BOE) is issued by Ameritas Life Insurance Corp. of New York located at 1350 Broadway, Suite 2201, New York, NY 10018. Policy and riders may vary and may not be available in all states.

• This information is provided by Ameritas®, which is a marketing name for subsidiaries of Ameritas Mutual Holding Company, including, but not limited to, Ameritas Life Insurance Corp., Ameritas Life Insurance Corp. of New York and Ameritas Investment Corp., member FINRA/SIPC. Ameritas Life Insurance Corp. is not licensed in New York. Each company is solely responsible for its own financial condition and contractual obligations. For more information about Ameritas®, visit ameritas.com.

Ameritas® and the bison design are registered service marks of Ameritas Life Insurance Corp. Fulfilling life® is a registered service mark of Ameritas Holding Company. © 2013 Ameritas Mutual Holding Company

DI 1325 7-13 For Producer use only. Not for use with clients.

purpose of this presentation

• Help you understand the underwriting process

• Help you understand why some policies are issued “other than applied for”

• Help you better prepare your clients for a potential substandard policy

• Help you explain to your clients why they should strongly consider accepting a substandard policy

DI 1325 7-13 For Producer use only. Not for use with clients.

why are some policies issued on a substandard basis?

• Underwriting is an art…not a science

• The underwriter looks at the application, reports, etc., and attempts to make a judgment about your clients and their potential for disability

• He/She looks at current information, past history and attempts to look into the future

• He/She attempts to make an offer even when there is medical history which can be mitigated through the judicious use of ratings or exclusions

DI 1325 7-13 For Producer use only. Not for use with clients.

things to know about underwriting

• In 2012, we had a total submitted premium of $23 million

• 73% Approved

• 8% Declined

• 19% Withdrawn before Approval

DI 1325 7-13 For Producer use only. Not for use with clients.

more underwriting facts

• Over the last several years, underwriting has approved policies as follows:

• 59% on a standard basis

• 29% with exclusions

• 5% with ratings

• 7% with a combination of exclusions/ratings

DI 1325 7-13 For Producer use only. Not for use with clients.

more underwriting facts (cont.)

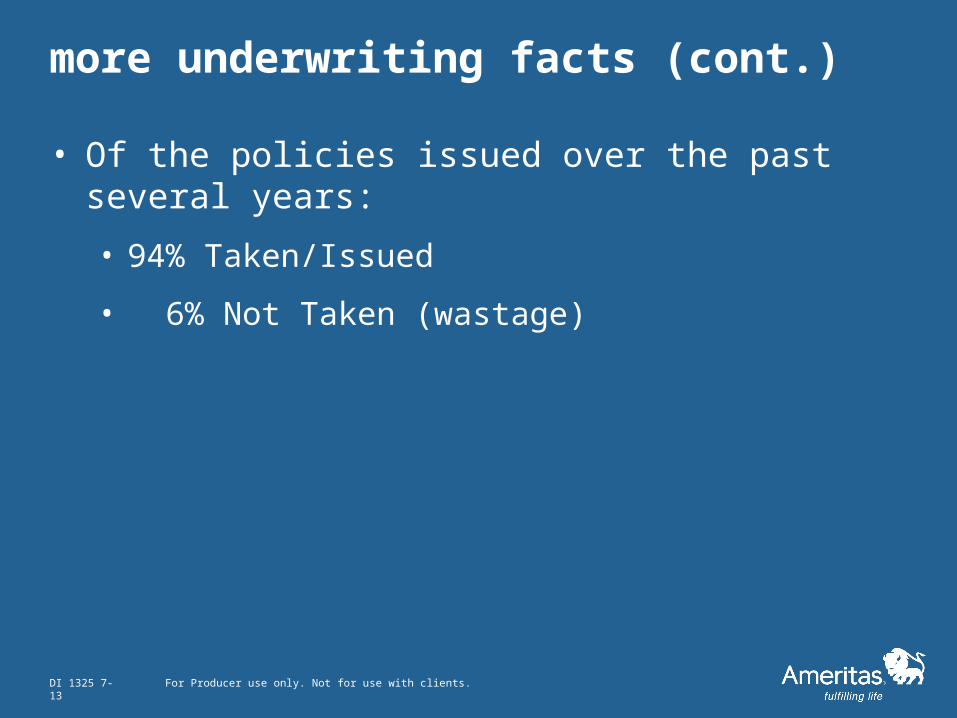

• Of the policies issued over the past several years:

• 94% Taken/Issued

• 6% Not Taken (wastage)

DI 1325 7-13 For Producer use only. Not for use with clients.

cover letter

• Allows you a chance to demonstrate your knowledge of your clients and your history with them

• Can be used to explain additional knowledge of your clients and circumstances that may not be evident from the application, interview, inspection or other reports

• Your knowledge and history with the client can be a significant determinate to the underwriter and his/her final decisions

DI 1325 7-13 For Producer use only. Not for use with clients.

what are the choices for issued policies?

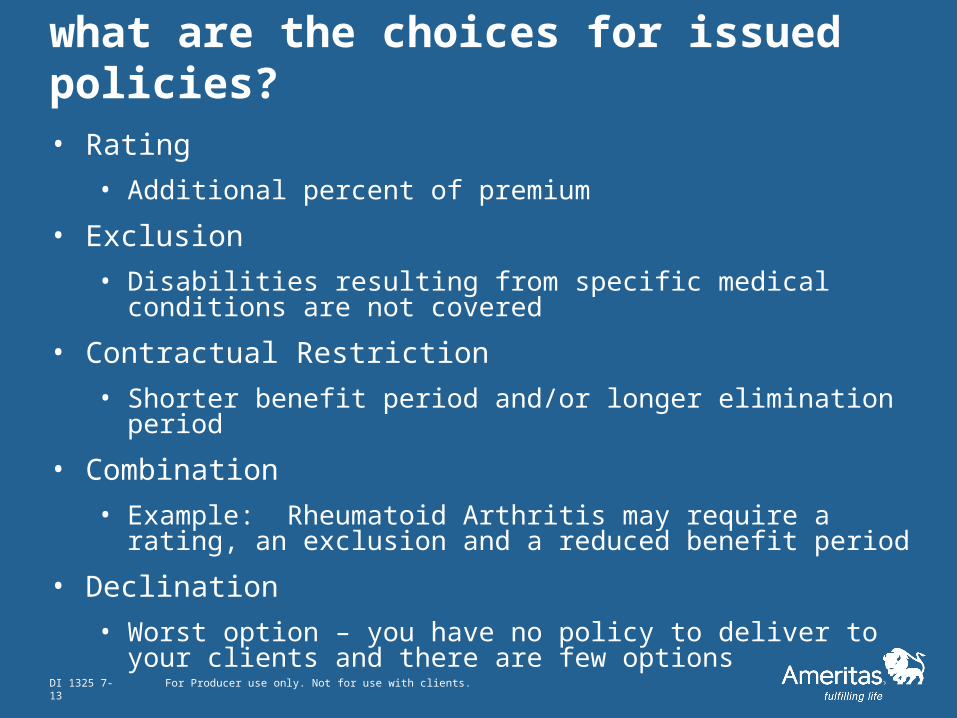

• Rating

• Additional percent of premium

• Exclusion

• Disabilities resulting from specific medical conditions are not covered

• Contractual Restriction

• Shorter benefit period and/or longer elimination period

• Combination

• Example: Rheumatoid Arthritis may require a rating, an exclusion and a reduced benefit period

• Declination

• Worst option – you have no policy to deliver to your clients and there are few options

DI 1325 7-13 For Producer use only. Not for use with clients.

prior to delivery

• Ensure you understand the rating and/or exclusion

• Review the file to see if a “reconsideration” on the exclusion is justified

• Talk to your underwriter – within reason and regulations, he/she can work with you to ensure you are able to provide some specifics to your clients

• Understand that there may be conditions or issues that preclude the release of information – examples might include HIV, mental/nervous conditions or substance abuse

• There could be times that the underwriter may only be able to tell you that there is “confidential information from an authorized source.”

• Understand, and truly believe, that most clients are much better off with a substandard policy versus going without one

DI 1325 7-13 For Producer use only. Not for use with clients.

understanding and empathy

• It is understandable and predictable that your clients will be unhappy or angry about a policy issued with an exclusion and/or rating or issued other than as applied for:

• Forces them to acknowledge their medical issue;

• Clients may focus all their attention on a medical condition they thought was less important than it really is;

• They may not realize how the underwriter is looking at the condition and trying to determine the odds of that or other conditions resulting in a disability; and

• Clients may have the attitude that “if they won’t cover me for that, then I won’t take the coverage.”

DI 1325 7-13 For Producer use only. Not for use with clients.

delivery techniques

• Specific Exclusions

• Remind your clients that you had discussed with them the possible outcomes based on their known health history and that being offered a policy, with only specific medical condition exclusions, allows them to be covered for thousands of other potential disabilities

• Discuss with the underwriter the idea of a reconsideration after 12 or 24 months, if the condition has improved and the client is symptom free for that period of time

DI 1325 7-13 For Producer use only. Not for use with clients.

delivery techniques

• Ratings

• You need to focus on the very positive news that the underwriter, while aware of the medical history, was able to issue the policy by charging additional premium, versus the use of an exclusion

• For certain ratings, i.e., height/weight, the rating may be removed following 12 months of improved readings

DI 1325 7-13 For Producer use only. Not for use with clients.

delivery techniques

• Changes in Policy Specifications

• If the change does not require additional premium, focus on this with your clients

• Longer elimination period and/or shorter benefit periods allow the underwriter to issue a policy that may have required either an exclusion, a rating, or even a declination

DI 1325 7-13 For Producer use only. Not for use with clients.

your attitude

• The greatest impediment to delivery of the rated and/or excluded policy is often your attitude:

• You must feel the underwriting decision is valid;

• You need to understand the underlying reasons for the underwriting action;

• You should focus on what the policy still covers – not on the additional premium charge; and

• We cannot overemphasize the need for field underwriting and setting expectations with your clients

DI 1325 7-13 For Producer use only. Not for use with clients.

key contacts

• Your agency or brokerage manager

• Your Ameritas® sales development team

• Your GSI regional director

• The DI product management team

DI 1325 7-13 For Producer use only. Not for use with clients.

Related Documents