© IPA 2010 LAMA Autumn Seminar LAMA Autumn Seminar 8 8 th th & 9 & 9 th th October , 2010 October , 2010 Listowel Arms Hotel Listowel Arms Hotel The evolving governance challenges for the The evolving governance challenges for the Irish Local Government Sector Irish Local Government Sector Dr Philip Byrne Senior Local Government Specialist INSTITUTE OF PUBLIC ADMINISTRATION www.ipa.ie

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© IPA 2010LAMA Autumn SeminarLAMA Autumn Seminar

88thth & 9 & 9thth October , 2010 October , 2010Listowel Arms HotelListowel Arms Hotel

The evolving governance challenges for the Irish Local The evolving governance challenges for the Irish Local Government SectorGovernment Sector

Dr Philip ByrneSenior Local Government Specialist

INSTITUTE OF PUBLIC ADMINISTRATION

www.ipa.ie

© IPA 2010

•Good Governance leads to:

• good management and performance, • good stewardship of funds, • good public ( stakeholder) engagement

and ultimately

• good outcomes

Key message

© IPA 2010

12

3

Issues to discussIssues to discuss

Governance Context and

PrinciplesGovernance obligations

On sector

Evolving Governance Challenges

© IPA 2010

DefinitionDefinition

Governance comprises the systems and Governance comprises the systems and procedures by which enterprises are procedures by which enterprises are

directed and manageddirected and managedGood governance should be seen as an aid Good governance should be seen as an aid

to performance and effectiveness. to performance and effectiveness. It is not there to inhibit enterprise or It is not there to inhibit enterprise or

innovation.innovation.

© IPA 2010

Governance controversies influence expectations and obligations

1. Poor leadership and decision making processes

2. Inadequate systems and controls, including regulatory oversight

3. Poor standards of conduct4. Ineffective risk management5. Poor Accountability arrangements6. Culture and Behaviour

© IPA 2010

What’s new in Governance?What’s new in Governance?

Codes, Guidelines, hard law, soft law Codes, Guidelines, hard law, soft law

Expectations on local authorities, state and Expectations on local authorities, state and publicly funded bodiespublicly funded bodies

Current Hot Topics Current Hot Topics

Rules and Regulations or Rules and Regulations or Principles and ValuesPrinciples and Values

© IPA 2010

2001 Local Government Act2001 Local Government Act

© IPA 2010

S 130: Policy role of elected S 130: Policy role of elected councilcouncil

It is a function of the elected council of a It is a function of the elected council of a local authority to determine by resolution local authority to determine by resolution the policy of the localthe policy of the local authority. authority.

© IPA 2010

S 131:Reserved functions S 131:Reserved functions

““function” does not include a function function” does not include a function relating relating to the employees of a localto the employees of a local authority or the direction, supervision, authority or the direction, supervision, service, remuneration or discipline of such service, remuneration or discipline of such employees employees

© IPA 2010

S139: Direction that works not S139: Direction that works not proceed. proceed.

Where the elected council or joint body is Where the elected council or joint body is informed of informed of any worksany works (not being any (not being any works which the local authority are works which the local authority are required by or under statute or by order of required by or under statute or by order of a court to undertake), the a court to undertake), the elected councilelected council, , as the case may be, may by resolution, as the case may be, may by resolution, direct that those works shall not direct that those works shall not proceed proceed

© IPA 2010

S 140: Requirement that a S 140: Requirement that a particular thing be done. particular thing be done.

an elected council may by resolution an elected council may by resolution require any particular actrequire any particular act, matter or thing , matter or thing specifically mentioned in the resolution specifically mentioned in the resolution and which the local authority or the and which the local authority or the manager concerned can lawfully do or manager concerned can lawfully do or effect, to be done or effected in the effect, to be done or effected in the performance of the executive functions of performance of the executive functions of the local authority. the local authority.

© IPA 2010

S 146:Suspension and removal S 146:Suspension and removal of manager of manager

the elected council of a county council or city the elected council of a county council or city council council may by resolution suspendmay by resolution suspend or or remove remove from employmentfrom employment the manager for such county the manager for such county council or city council, as the case may be, council or city council, as the case may be,

for for stated misbehaviourstated misbehaviour or if his or her or if his or her suspension or removal appears to them to be suspension or removal appears to them to be necessary for the effective performance by the necessary for the effective performance by the county council or city council, as the case may county council or city council, as the case may be, of its functions. be, of its functions.

© IPA 2010

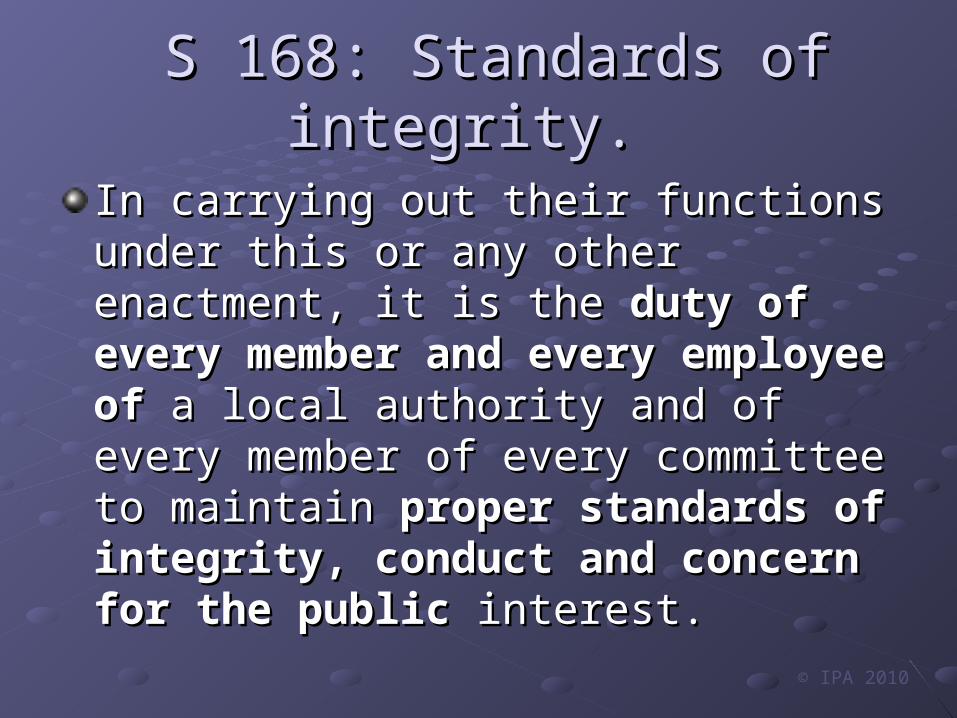

S 168: Standards of integrity. S 168: Standards of integrity.

In carrying out their functions under this or In carrying out their functions under this or any other enactment, it is the any other enactment, it is the duty of duty of every member and every employee ofevery member and every employee of a a local authority and of every member of local authority and of every member of every committee to maintain every committee to maintain proper proper standards of integrity, conduct and standards of integrity, conduct and concern for the publicconcern for the public interest. interest.

© IPA 2010

S 175: Declarable interests S 175: Declarable interests ((aa) ) any professionany profession, , business or occupationbusiness or occupation in which in which the person concerned is engaged or employed, whether the person concerned is engaged or employed, whether on his or her own behalf or otherwise, and which relates on his or her own behalf or otherwise, and which relates to to dealing in or developing land during the dealing in or developing land during the appropriateappropriate period; period;

((bb) any other ) any other remunerated traderemunerated trade, , profession, profession, employment, vocation, or other occupation of the employment, vocation, or other occupation of the personperson concerned held by that person during the concerned held by that person during the appropriate periodappropriate period

© IPA 2010

S 175: Declarable interestsS 175: Declarable interests

((cc) any ) any estate or interest the person estate or interest the person concerned in landconcerned in land including the case including the case where the person concerned, or any where the person concerned, or any nominee of his or her, is a member of a nominee of his or her, is a member of a company or other body which has an company or other body which has an estate or interest in landestate or interest in land

© IPA 2010

As organisations, Local Authorities have particular features 1 Public benefit, public interest body

• Legal and other obligations• Local presence / high visibility• Key local service provider• Public interface

2 Statutory responsibilities

3 Links to central government

4 Other stakeholder relationships

© IPA 2010

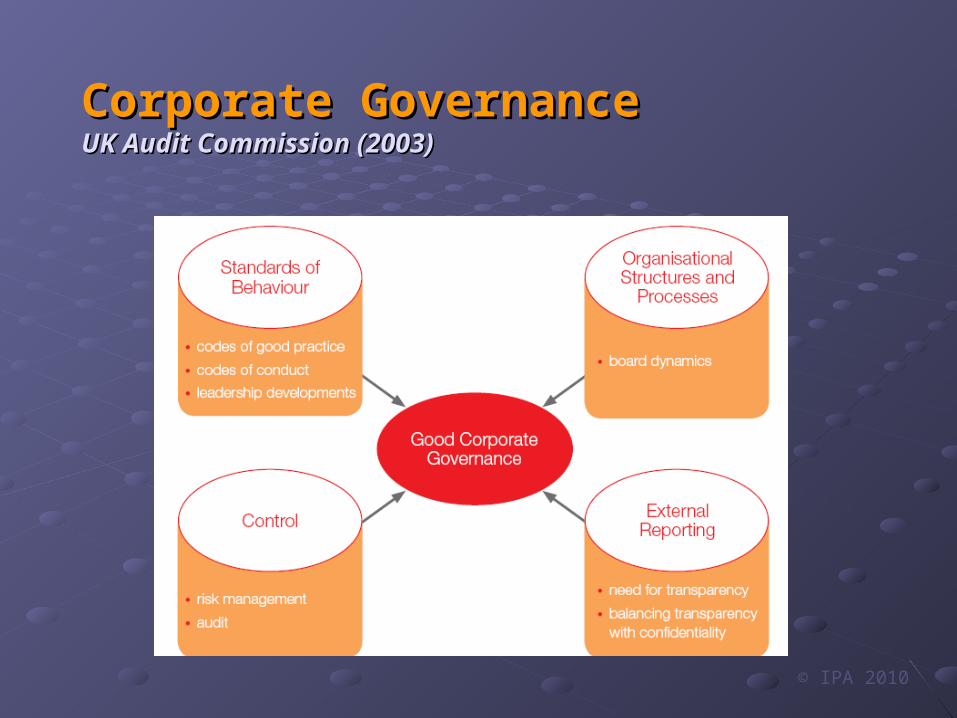

Corporate GovernanceCorporate GovernanceUK Audit Commission (2003)UK Audit Commission (2003)

© IPA 2010

International Federation of Accountants International Federation of Accountants (2009) (2009) Evaluating and improving governance in Evaluating and improving governance in organisationsorganisations

© IPA 2010

Code of Practice for the Governance of State Bodies

Board ProcessBoard Process AccountabilityAccountability

A The Board & A The Board & DirectorsDirectors

B RemunerationB Remuneration

C Risk Management,C Risk Management, Accountability, AuditAccountability, Audit

D Relations with the D Relations with the Oireachtas and the Oireachtas and the MinisterMinister

EE Specific Procedures Specific Procedures

© IPA 2010

Key areas of emphasis in Key areas of emphasis in 2009 Code2009 Code

Compliance StatementCompliance Statement (Board to formally confirm (Board to formally confirm compliance with up to date requirement of 2009 Code)compliance with up to date requirement of 2009 Code)Legislative ComplianceLegislative Compliance ( Board to ensure all statutory ( Board to ensure all statutory requirements are made known to it) requirements are made known to it) Confidential disclosuresConfidential disclosures (procedures to facilitate “good (procedures to facilitate “good faith reporting” – Whistle blowingfaith reporting” – Whistle blowingBoard EvaluationBoard Evaluation - to review its effectiveness and to - to review its effectiveness and to advise Minister on gaps in competencies advise Minister on gaps in competencies

© IPA 2010

Key areas of emphasis in Key areas of emphasis in 2009 Code Cont’d2009 Code Cont’d

Internal Control Effectiveness- Internal Control Effectiveness- Annual determination Annual determination of internal controls (financial; operational; compliance of internal controls (financial; operational; compliance and risk mgt)and risk mgt)Risk ManagementRisk Management: Risk mgt policy and framework : Risk mgt policy and framework approved by boardapproved by boardPerformance Frameworks – Performance Frameworks – Output statements Output statements including performance indicators to be produced (part of including performance indicators to be produced (part of TPS)TPS)Travel Policy: Travel Policy: (Need to achieve VFM – compliance with (Need to achieve VFM – compliance with DOF circulars)DOF circulars)

© IPA 2010

Key areas of emphasis in Key areas of emphasis in 2009 Code Cont’d2009 Code Cont’d

ProcurementProcurement : Board approval of a Corporate : Board approval of a Corporate Procurement Policy Plan to adhere to National and EU Procurement Policy Plan to adhere to National and EU rulesrulesReports and AccountsReports and Accounts: Significant list of Annual Report : Significant list of Annual Report disclosures and furnished to Ministerdisclosures and furnished to MinisterLegal DisputesLegal Disputes: Where legal disputes with other public : Where legal disputes with other public agencies, emphasis on mediation and arbitration and agencies, emphasis on mediation and arbitration and also to inform D o Financealso to inform D o FinanceBoard Member AttendancesBoard Member Attendances: Annual report to include : Annual report to include info on attendances at Boardinfo on attendances at Board

© IPA 2010

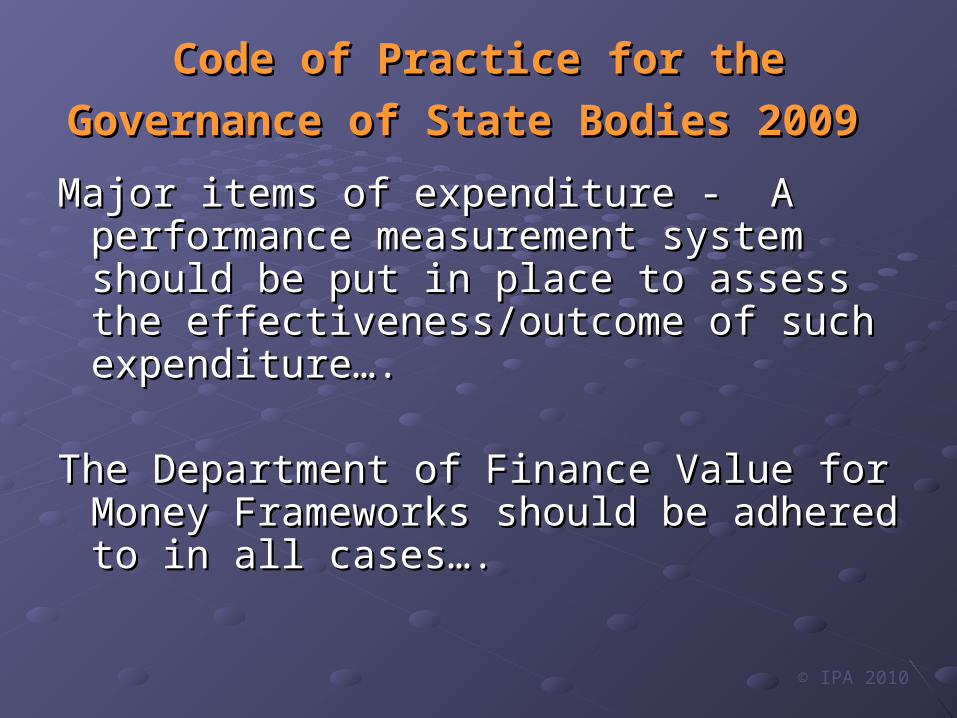

Code of Practice for the Code of Practice for the Governance of State Bodies 2009Governance of State Bodies 2009

Major items of expenditure - A performance Major items of expenditure - A performance measurement system should be put in measurement system should be put in place to assess the effectiveness/outcome place to assess the effectiveness/outcome of such expenditure….of such expenditure….

The Department of Finance Value for Money The Department of Finance Value for Money Frameworks should be adhered to in all Frameworks should be adhered to in all cases….cases….

© IPA 2010

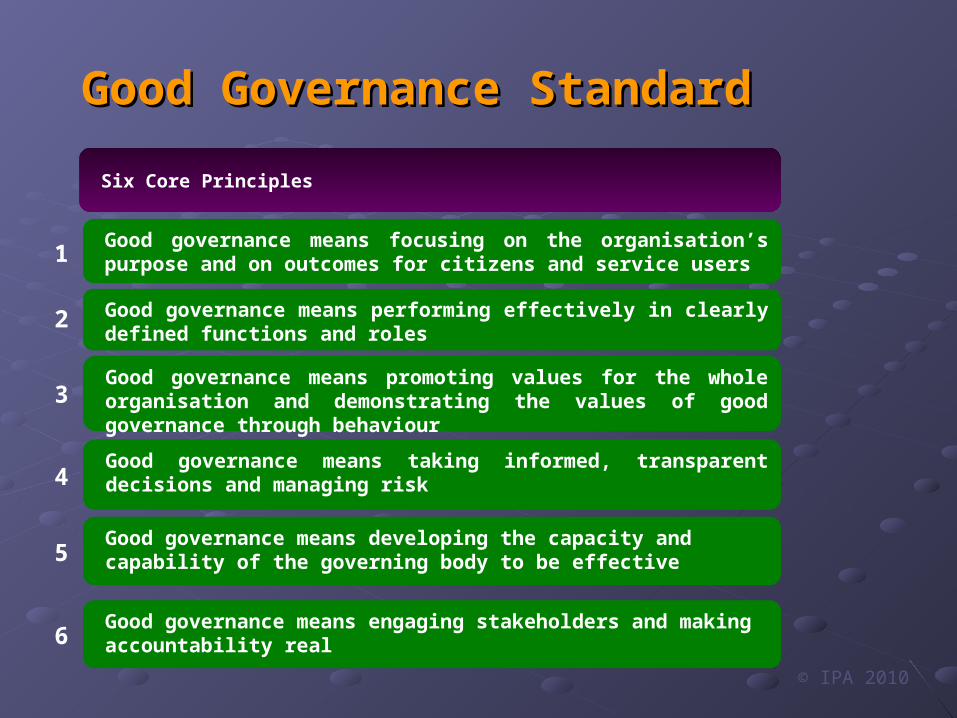

Good Governance StandardGood Governance Standard

Good governance means taking informed, transparent decisions and managing risk

Good governance means focusing on the organisation’s purpose and on outcomes for citizens and service users

Good governance means performing effectively in clearly defined functions and roles

Good governance means promoting values for the whole organisation and demonstrating the values of good governance through behaviour

Good governance means developing the capacity and capability of the governing body to be effective

Six Core Principles

Good governance means engaging stakeholders and making accountability real

1

2

3

4

5

6

© IPA 2010

1. Accountability and transparency2. Control and compliance3. Risk management4. Consistency in delivery5. Ensuring value for money6. Stakeholder engagement.

Governance Themes

© IPA 2010

The effective memberThe effective member

A commitment to the achievement of shared objectivesEnsuring compliance with legal and regulatory requirementsAccountability - supportive and challengingContribution- bringing knowledge, skills, experience and networks Values – demonstrating good governance through behaviour

© IPA 2010

Risk appetite is defined as the amount of risk the local authority is prepared to accept or retain in the pursuit of its core priority objectives.

What is the Risk appetite within your Local Authority and does this have implications for Governance

© IPA 2010

Manage the reputational risk with increasingly challenging public and media

Values and behaviours adopted by those in leadership and influential positions

Strong accountability, responsibility, control and compliance systems in place

Communicate and demonstrate the performance achievements

Appropriate stakeholder engagement to inform the decision-making process

Evolving Governance Challenges Evolving Governance Challenges

Efficiency Review and implications

1

2

3

4

5

6

© IPA 2010

Good Governance

Legislation and Codes A guide on many issues

Good Governance depends on People and the values they adopt An understanding of roles Focussing on the organisation’s

purpose

© IPA 2010

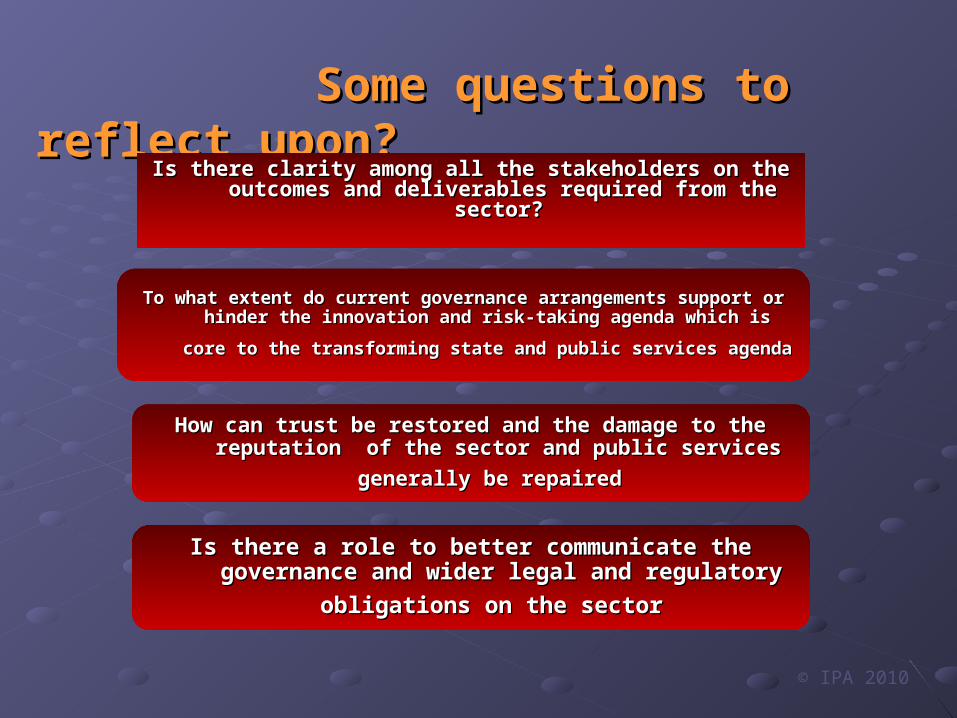

Some questions to reflect Some questions to reflect upon?upon?

Is there clarity among all the stakeholders on the Is there clarity among all the stakeholders on the outcomes and deliverables required from the outcomes and deliverables required from the

sector?sector?

To what extent do current governance arrangements support or To what extent do current governance arrangements support or hinder the innovation and risk-taking agenda which is core hinder the innovation and risk-taking agenda which is core

to the transforming state and public services agendato the transforming state and public services agenda

How can trust be restored and the damage to the How can trust be restored and the damage to the reputation of the sector and public services reputation of the sector and public services

generally be repairedgenerally be repaired

Is there a role to better communicate the Is there a role to better communicate the governance and wider legal and regulatory governance and wider legal and regulatory

obligations on the sectorobligations on the sector

© IPA 2010

LAMA Autumn SeminarLAMA Autumn Seminar

88thth & 9 & 9thth October , 2010 October , 2010Listowel Arms HotelListowel Arms Hotel

The evolving governance challenges for the Irish Local Government The evolving governance challenges for the Irish Local Government SectorSector

Thank youThank you

Dr Philip ByrneSenior Local Government Specialist

INSTITUTE OF PUBLIC ADMINISTRATION

www.ipa.ie

Related Documents