GLOBAL EMPLOYER GUIDE PHILIPPINES

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GLOBALEMPLOYERGUIDE

PHILIPPINES

Summary

Republic of the Philippines

Manila

FilipinoEnglish

Full name

Capital

Main Languages

106.7 million

Philippine Peso

.ph

+63

Philippine Peso

Population

Monetary unit

Internet domain

International dialing code

Currency

Basic Country Facts

P A G E 0 2G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

P A G E 0 3

Under Article 281 of the Labor Code ofthe Philippines, probationaryemployment shall not exceed six (6)months from the date the employeestarted working, unless it is covered byan apprenticeship agreement stipulatinga longer period.

Philippine employees are legally entitledto 5 days of paid 'service incentive leave',which can be used for vacation or sickleave. However, employers sometimes offer 15days of paid vacation and 15 days of paidsick leave for most professional levelpositions in the Philippines.

STATUTORY LABORREQUIREMENTS Probation Period

Annual Leave

New Year's Day (1st January)Chinese New Year (25th January)Bataan Day (9th April)Maundy Thursday (9th April)Good Friday (10th April)Labor Day (1st May)Eid al-FitrPhilippines Independence Day (12thJune)Eid al-AdhaNational Heroes' Day (in Philippines)(31st August)Bonifacio Day (30th November)Feast of the Immaculate Conception(8th December)Christmas Day (25th December)Rizal Day (30th December)

Public Holidays

All working mothers — including thoseemployed in the informal sector — cantake up to 105 days of paid maternityleave (up from 60 days for normalchildbirth or 78 days for a cesareandelivery) for each pregnancy, providedthey’ve made at least three monthlycontributions to the Social SecuritySystem (SSS) in the 12 months precedingthe semester of the birth and havenotified their employer.

Maternity Leave

Notwithstanding any law, rules andregulations to the contrary, everymarried male employee in the privateand public sectors shall be entitled to apaternity leave of seven (7) days with fullpay for the first four (4) deliveries of thelegitimate spouse

Paternity Leave

Philippine employees are legally entitledto 5 days of paid 'service incentiveleave', which can be used for vacation orsick leave.

Sick Leave

The normal hours work of an employeeshall not exceed 8 hours a day. However, Health Personnel shall have amaximum of 40 hours a week.

Work Hours

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

P A G E 0 4

Overtime pay is an additional pay of 25%of a covered employee's hourly rate forwork performed beyond eight (8) hoursa day or for overtime work.If health personnel are made to work inexcess of 40 hours, they are entitled to30% additional pay.

Overtime

As per Philippine laws, particularly theLabor Code, employees resigning ontheir own volition need to give theircompanies a notice of 30 days.

Notice Period

In case of termination due to theinstallation of labor saving devices orredundancy, the employee affected isentitled to a separation pay equivalentto at least his one (1) month pay or to atleast one (1) month pay for every year ofservice, whichever is higher.

Severance

Under Presidential Decree No. 851,employers from the private sector in thePhilippines are required to pay theirrank-and-file employees a Thirteenth13th Month Pay not later than December24 every year. The 13th month pay is equivalent to onetwelfth (1/12) of an employee's basicannual salary.

13th Month

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

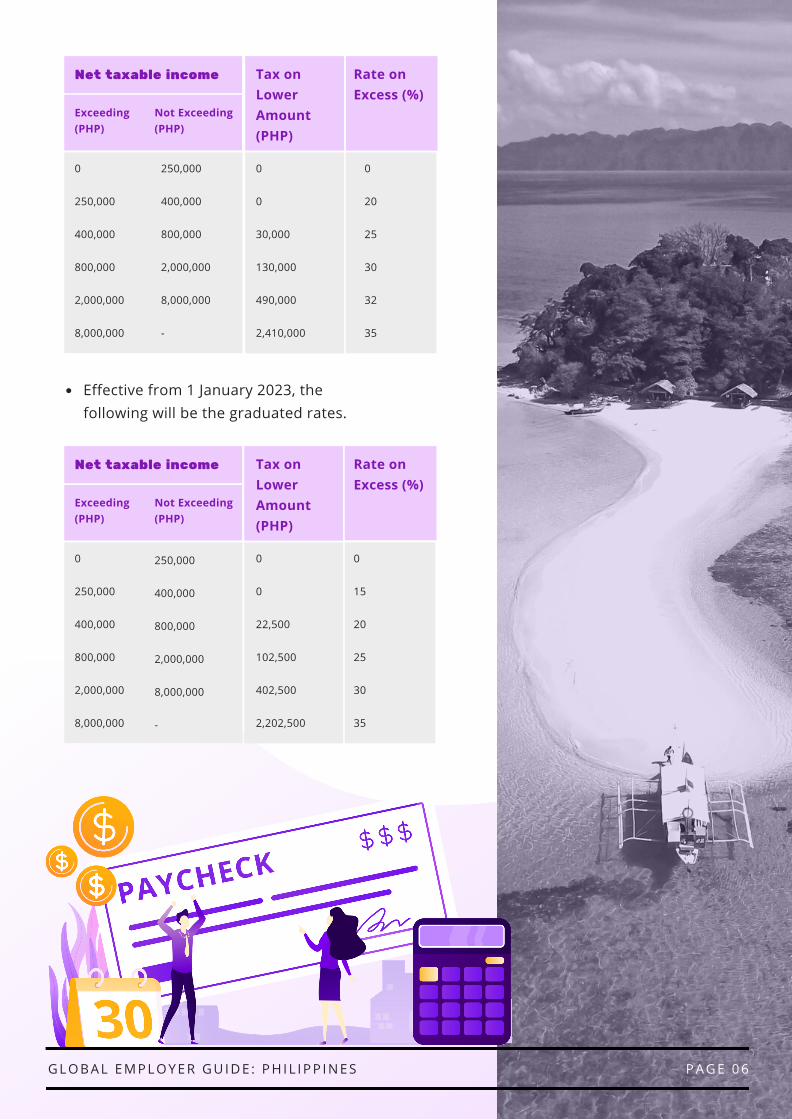

Resident citizens are subject to tax onworldwide income. Nonresident citizens, resident aliens andnonresident aliens are subject to tax onincome from Philippine sources. Bureau of Internal Revenue (BIR) Ruling517-2011 declared that employees of aPhilippine entity who are working abroadfor most of the tax year but remain onthe local payroll are not nonresidentcitizens. Accordingly, payments to them aresubject to withholding tax in thePhilippines.Employment income received for servicesprovided in the Philippines is subject totax in the Philippines regardless of wherethe compensation is paid. Remuneration for services remainsclassified as compensation even if paidafter the employer-employee relationshipis endedGross income includes compensation,income from the conduct of a trade,business or profession, and otherincome, including gains from dealings inproperty, interest, rent, dividends,annuities, prizes, pensions and partners’distributive shares.Net taxable compensation and businessincome of resident and nonresidentcitizens, resident aliens, and nonresidentaliens engaged in a trade or business areconsolidated and taxed at the followinggraduated rates.

P A G E 0 5

Income Tax

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

Tax onLowerAmount(PHP)

P A G E 0 6G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

0 250,000 400,000 800,000 2,000,000 8,000,000

Net taxable income Tax onLowerAmount(PHP)

Exceeding (PHP)

Not Exceeding (PHP)

Rate onExcess (%)

250,000 400,000 800,000 2,000,000 8,000,000 -

0 0 30,000 130,000 490,000 2,410,000

0 20 25 30 32 35

Effective from 1 January 2023, thefollowing will be the graduated rates.

0 250,000 400,000 800,000 2,000,000 8,000,000

Net taxable income

Exceeding (PHP)

Not Exceeding (PHP)

Rate onExcess (%)

250,000 400,000 800,000 2,000,000 8,000,000 -

0 0 22,500 102,500 402,500 2,202,500

0 15 20 25 30 35

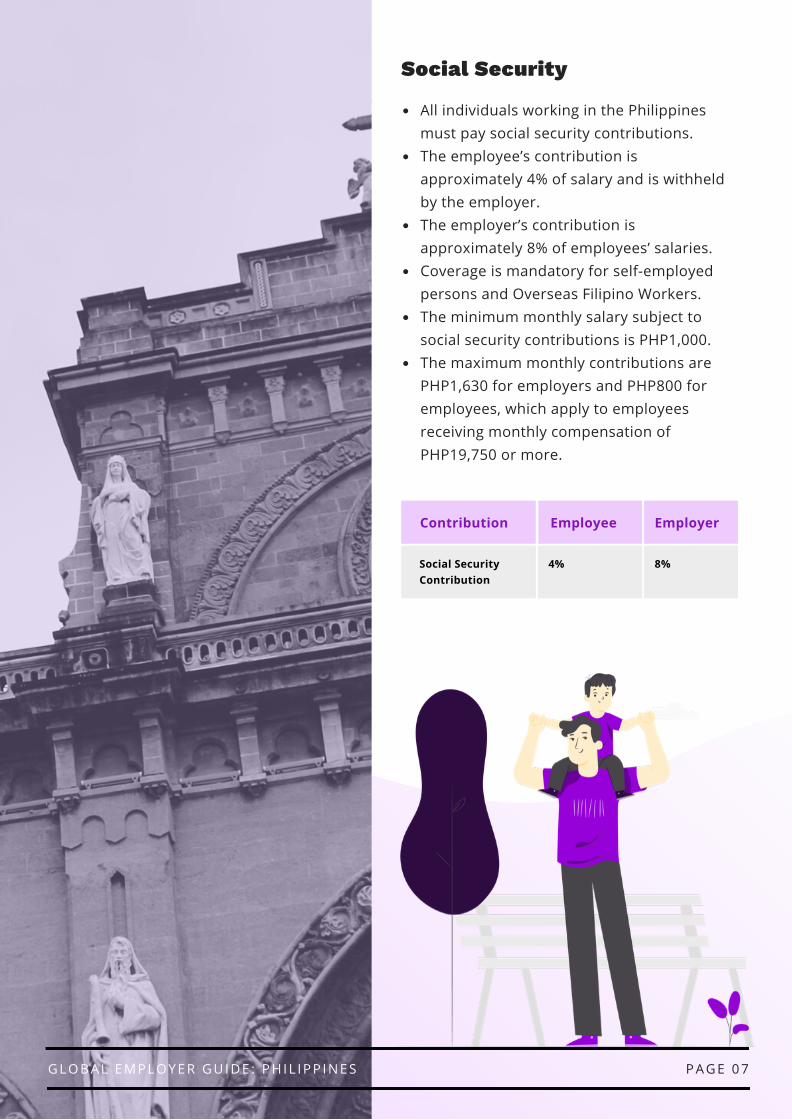

All individuals working in the Philippinesmust pay social security contributions. The employee’s contribution isapproximately 4% of salary and is withheldby the employer. The employer’s contribution isapproximately 8% of employees’ salaries. Coverage is mandatory for self-employedpersons and Overseas Filipino Workers. The minimum monthly salary subject tosocial security contributions is PHP1,000. The maximum monthly contributions arePHP1,630 for employers and PHP800 foremployees, which apply to employeesreceiving monthly compensation ofPHP19,750 or more.

P A G E 0 7

Social Security

Contribution

4%Social SecurityContribution

Employee Employer

8%

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

Aliens, whether residents or not, who arereceiving only salary or compensationincome are not allowed any deductionagainst such income.

Home mortgage interest, medicalexpenses, contributions, and otherpersonal expenses cannot be claimed asdeductions for income tax purposes. However, social security contributions, upto the prescribed amount of maximummandatory contributions, are excludedfrom gross income.

Employment Expenses

Personal Deductions

P A G E 0 8

Deductible Expenses

In the case of individuals engaged inbusiness or the practice of a profession,and who opted to be taxed at the regulargraduated income tax rates, the followingexpenses are allowed as deductions fromgross income:

All ordinary and necessary expensespaid or incurred during the taxableyear in connection with the trade,business, or profession, including rawmaterials, supplies, and direct labor.Wages and other forms ofcompensation for personal servicesactually rendered, including thegrossed-up monetary value of fringebenefits and travel expenses incurredin the pursuit of the trade orprofession.Business rentals.

Business Deductions

Interest paid or incurred within ataxable year in connection with theconduct of a taxpayer’s profession,trade, or business, less an amountequal to a certain percentage of theinterest income subject to final tax.Entertainment, amusement, andrecreation expensesTaxes.Losses.Bad debts.Depreciation.Charitable and other contributions,subject to certain limitations.Research and development (R&D)expenditures.

In lieu of these allowable deductions, anindividual, other than a non-residentalien, may elect an optional standarddeduction (OSD) not exceeding 40% ofgross business or professional income.

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

P A G E 0 9

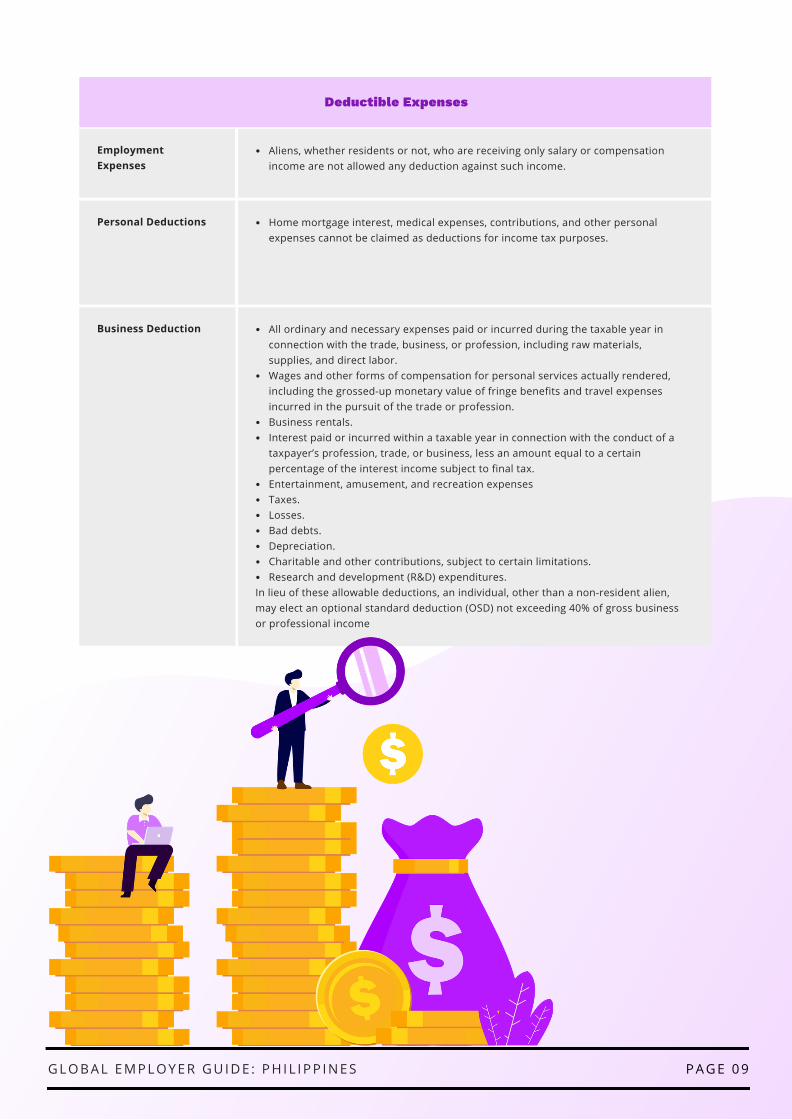

EmploymentExpenses

Aliens, whether residents or not, who are receiving only salary or compensationincome are not allowed any deduction against such income.

Personal Deductions Home mortgage interest, medical expenses, contributions, and other personalexpenses cannot be claimed as deductions for income tax purposes.

Business Deduction All ordinary and necessary expenses paid or incurred during the taxable year inconnection with the trade, business, or profession, including raw materials,supplies, and direct labor.Wages and other forms of compensation for personal services actually rendered,including the grossed-up monetary value of fringe benefits and travel expensesincurred in the pursuit of the trade or profession.Business rentals.Interest paid or incurred within a taxable year in connection with the conduct of ataxpayer’s profession, trade, or business, less an amount equal to a certainpercentage of the interest income subject to final tax.Entertainment, amusement, and recreation expensesTaxes.Losses.Bad debts.Depreciation.Charitable and other contributions, subject to certain limitations.Research and development (R&D) expenditures.

In lieu of these allowable deductions, an individual, other than a non-resident alien,may elect an optional standard deduction (OSD) not exceeding 40% of gross businessor professional income

Deductible Expenses

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

Unless specifically exempted or excluded,all foreign nationals desiring to work in thePhilippines must obtain an AEP from theDOLE. AEPs are normally valid for one year, butmay be extended annually to cover theforeign national’s length of employment, upto a maximum of five years.Local employers who desire to employ aforeign national must apply for the AEP onthe foreign national’s behalf with theregional office of the DOLE havingjurisdiction over the employee’s place ofwork. The petitioning company must prove thatthe foreign national possesses the requiredskills for the position. Educational background, work experienceand other relevant factors are consideredin evaluating the application. The petitioning company must prove thatno Filipino is available who is competent,able and willing to do the specific job andthat the employment of the foreignnational is in the best interest of the public. The AEP is not an exclusive authority for aforeign national to work in the Philippines. It is just one of the requirements in theissuance of a work visa to legally engage ingainful employment in the country. Companies that are listed in the “TenthRegular Foreign Investment Negative List”must comply with the Understudy TrainingProgram and Anti-Dummy conditions of theauthorities, which require them to obtainan “Authority to Employ Alien” from theDepartment of Justice (DOJ) based on theDOJ Ministry Order No. 210, series of 1980.

Alien Employment Permit

P A G E 1 0

Immigration

The Subic Bay Metropolitan Authority(SBMA) may issue a temporary work permit(TWP) to foreign expatriates in order toimmediately legalize a foreign national’sstatus as an investor or worker in the SubicBay Freeport Zone. The permit is issued while the foreignnational’s investor or work visa application isstill in process. It is valid for three months and may beextended every three months, subject to amaximum total extension of one year.

Temporary work permit

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

P A G E 1 1

Type of Visa Documentation Validity Eligibility

AlienEmploymentPermit

Duly notarized application form;Letter of request sent to DOLE;Secretary’s Certificate electingforeign national to position (fornon-resident foreign nationalswith elective positions);Authenticated passport withcurrent visa;Photocopy of Mayor’s Permit; andPhotocopy of Business Permit.

1 year (may beextended up toa maximum of5 years)

Unless specifically exemptedor excluded, all foreignnationals desiring to work inthe Philippines must obtainan AEP from the DOLE. Educational background,work experience and otherrelevant factors areconsidered in evaluating theapplication.

TemporaryWork Permit

Completed application formValid PassportPassport photos

3 months The Subic Bay MetropolitanAuthority (SBMA) may issuea temporary work permit(TWP) to foreign expatriatesin order to immediatelylegalize a foreign national’sstatus as an investor orworker in the Subic BayFreeport Zone.

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

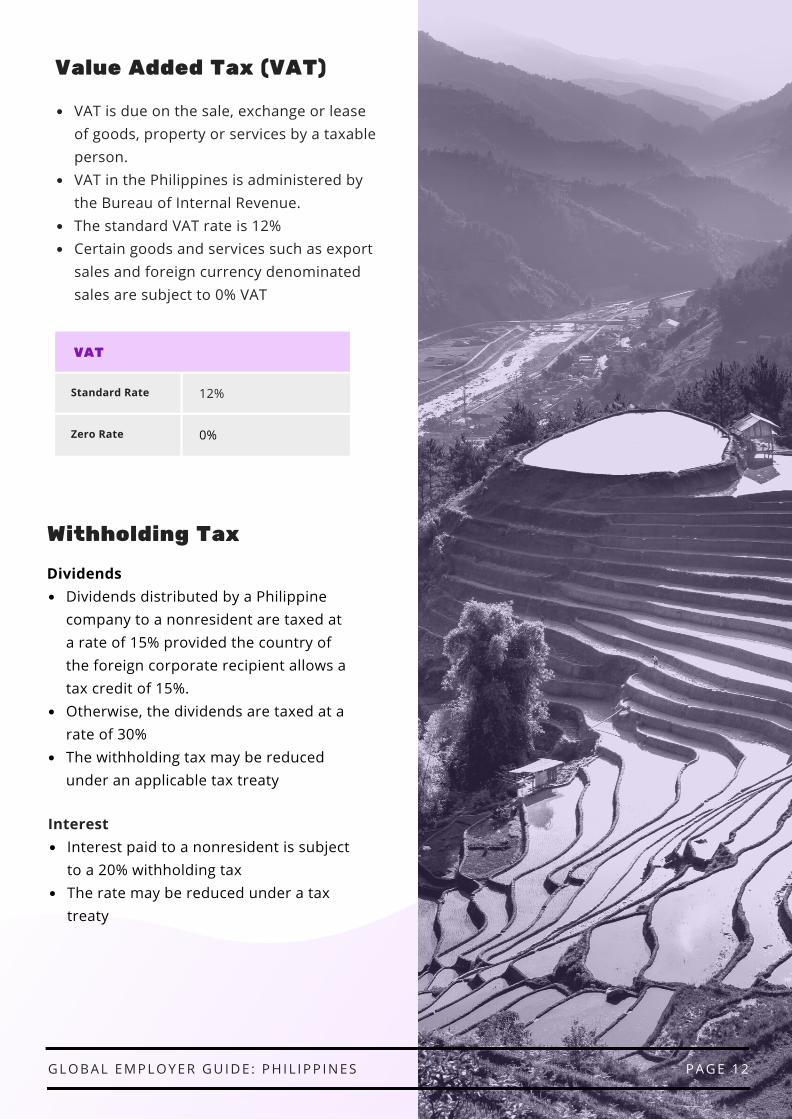

VAT is due on the sale, exchange or leaseof goods, property or services by a taxableperson.VAT in the Philippines is administered bythe Bureau of Internal Revenue.The standard VAT rate is 12%Certain goods and services such as exportsales and foreign currency denominatedsales are subject to 0% VAT

P A G E 1 2

Value Added Tax (VAT)

Standard Rate 12%

Zero Rate 0%

VAT

Withholding Tax

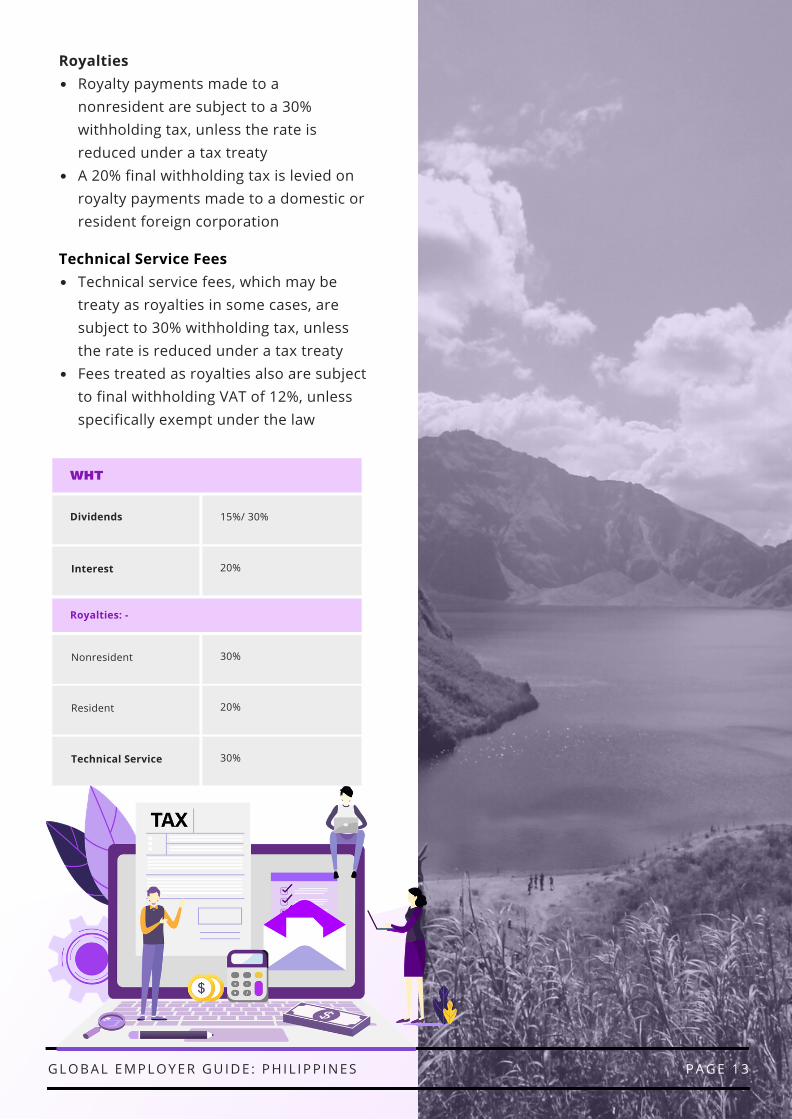

Dividends distributed by a Philippinecompany to a nonresident are taxed ata rate of 15% provided the country ofthe foreign corporate recipient allows atax credit of 15%.Otherwise, the dividends are taxed at arate of 30%The withholding tax may be reducedunder an applicable tax treaty

Dividends

Interest paid to a nonresident is subjectto a 20% withholding taxThe rate may be reduced under a taxtreaty

Interest

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

Dividends

P A G E 1 3

Royalty payments made to anonresident are subject to a 30%withholding tax, unless the rate isreduced under a tax treatyA 20% final withholding tax is levied onroyalty payments made to a domestic orresident foreign corporation

Royalties

Technical service fees, which may betreaty as royalties in some cases, aresubject to 30% withholding tax, unlessthe rate is reduced under a tax treatyFees treated as royalties also are subjectto final withholding VAT of 12%, unlessspecifically exempt under the law

Technical Service Fees

WHT

15%/ 30%

20%Interest

30%

Royalties: -

Nonresident

30%Technical Service

20%Resident

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

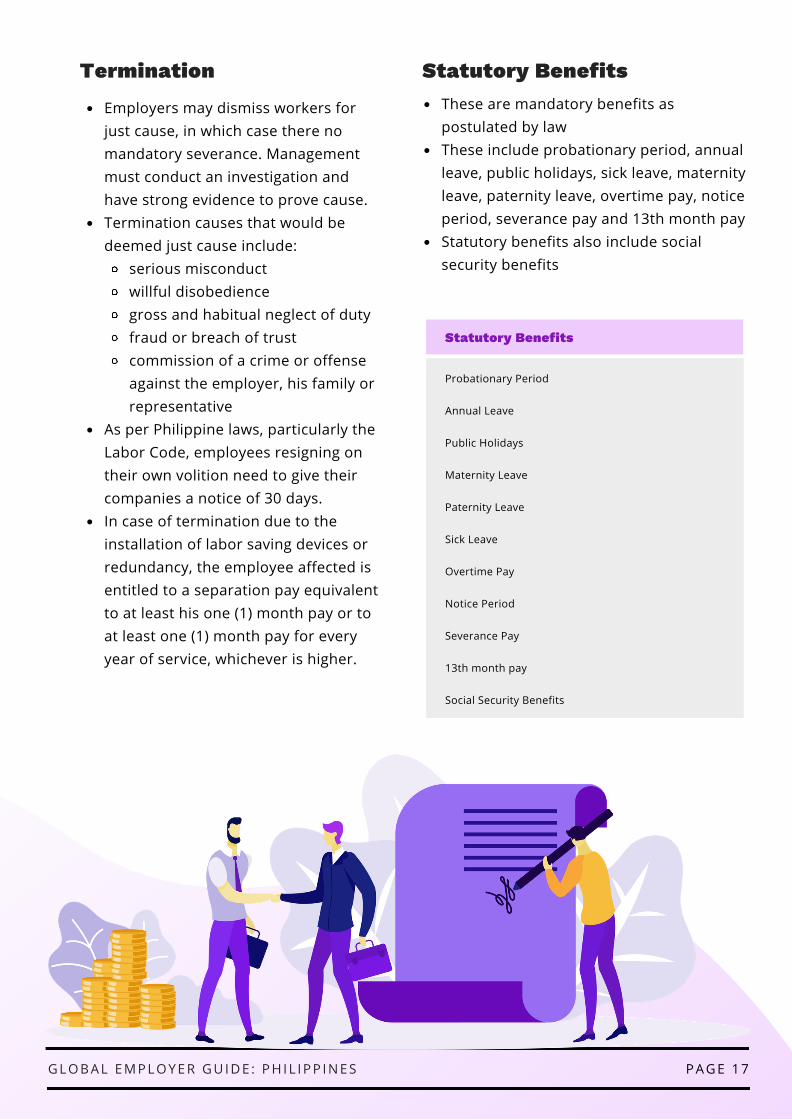

Employers may dismiss workers forjust cause, in which case there nomandatory severance. Managementmust conduct an investigation andhave strong evidence to prove cause.Termination causes that would bedeemed just cause include:

serious misconductwillful disobediencegross and habitual neglect of dutyfraud or breach of trustcommission of a crime or offenseagainst the employer, his family orrepresentative

As per Philippine laws, particularly theLabor Code, employees resigning ontheir own volition need to give theircompanies a notice of 30 days.In case of termination due to theinstallation of labor saving devices orredundancy, the employee affected isentitled to a separation pay equivalentto at least his one (1) month pay or toat least one (1) month pay for everyyear of service, whichever is higher.

P A G E 1 7

TerminationThese are mandatory benefits aspostulated by lawThese include probationary period, annualleave, public holidays, sick leave, maternityleave, paternity leave, overtime pay, noticeperiod, severance pay and 13th month payStatutory benefits also include socialsecurity benefits

Statutory Benefits

Statutory Benefits

Probationary Period Annual Leave Public Holidays Maternity Leave Paternity Leave Sick Leave Overtime Pay Notice Period Severance Pay 13th month pay Social Security Benefits

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

The tax year runs from 1 January to 31December.Unless impracticable, a husband and wife mustfile one consolidated income tax return, butthe tax is computed separately. Income thatcannot be definitely attributed or identified asexclusive income of either spouse is dividedequally between them. Generally, this results in lower combined taxliability than when the tax is jointly computed.Substituted filing is available for qualifiedemployees. In such case, the Certificate of CompensationPayment/Tax Withheld (Bureau of InternalRevenue [BIR] Form 2316) filed by theemployer and duly stamped 'received' by theBIR shall be tantamount to substituted filing ofthe Annual Income Tax Return of theemployees.Substituted filing shall apply only to employeeswho meet all of the following conditions:

the employee receives purelycompensation income (regardless ofamount) during the taxable year,the employee receives the income onlyfrom one employer in the Philippinesduring the taxable year,the amount of tax due from the employeeat the end of the year equals the amount oftax withheld by the employer, andthe employee’s spouse also complies withall three mentioned conditions.

Substituted filing, however, will not apply tonon-resident aliens engaged in trade orbusiness in the Philippines.All individual taxpayers who do not qualify forsubstituted filing are required to file theirreturns on a calendar-year basis. The returnmust be filed on or before 15 April of thesucceeding year.

P A G E 1 8G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

Payments and Invoicing

P A G E 2 0

Ease of Doing Business

The ease of doing business index is anindex created by Simeon Djankov, aneconomist at the Central and EasternEurope sector of the World Bank Group.Higher rankings (a low numerical value)indicate better, usually simpler,regulations for businesses and strongerprotections of property rights.According to the World Bank Philippinesranked 95th in the World in 2019 in termsof ease of doing business.

G L O B A L E M P L O Y E R G U I D E : P H I L I P P I N E S

GLOBALEMPLOYERGUIDEPHILIPPINES

Related Documents