Pharma Pharma and Biotech Industry Outlook and Biotech Industry Outlook A look at trends and opportunities in this increasingly challenging A look at trends and opportunities in this increasingly challenging environment with a focus on the generics landscape environment with a focus on the generics landscape October 2012 October 2012 [email protected] [email protected]

Pharma and Biotech Industry Outlook - A look at trends and opportunities in this increasingly challenging environment with a focus on the generics landscape

Aug 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PharmaPharma and Biotech Industry Outlookand Biotech Industry Outlook

A look at trends and opportunities in this increasingly challenging A look at trends and opportunities in this increasingly challenging environment with a focus on the generics landscapeenvironment with a focus on the generics landscape

October 2012October 2012

[email protected]@frost.com

Market Overview

2

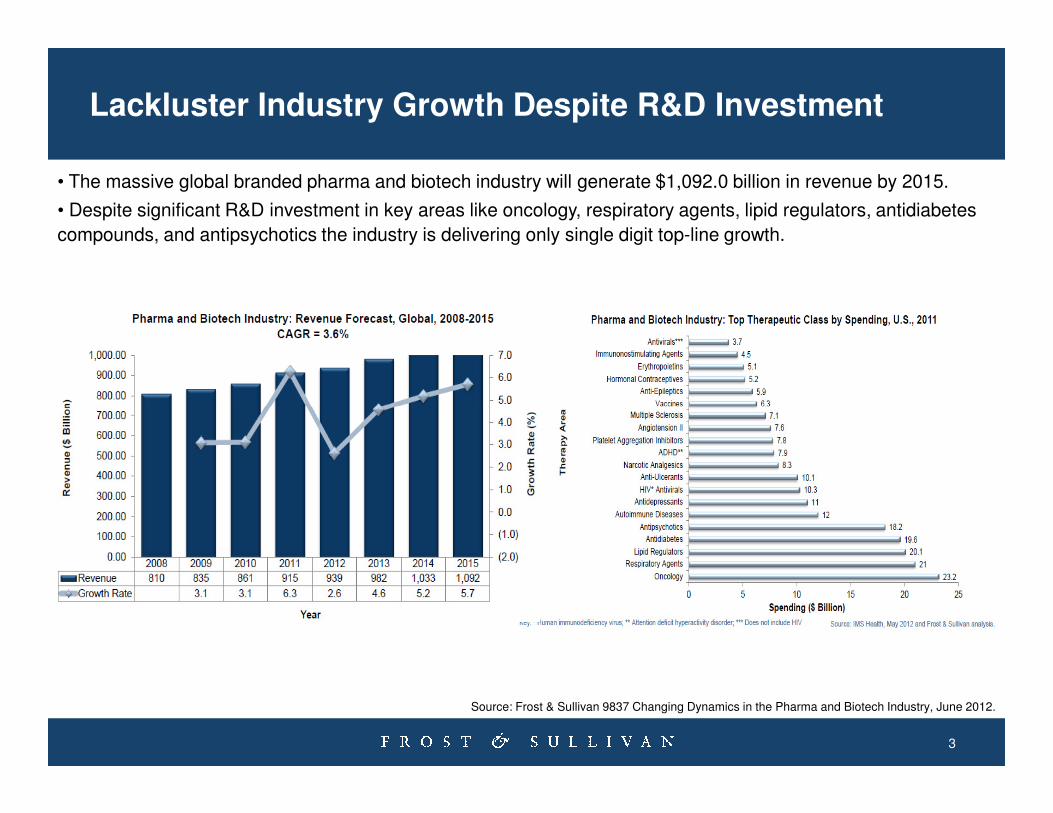

Lackluster Industry Growth Despite R&D Investment

• The massive global branded pharma and biotech industry will generate $1,092.0 billion in revenue by 2015.

• Despite significant R&D investment in key areas like oncology, respiratory agents, lipid regulators, antidiabetes

compounds, and antipsychotics the industry is delivering only single digit top-line growth.

3

Source: Frost & Sullivan 9837 Changing Dynamics in the Pharma and Biotech Industry, June 2012.

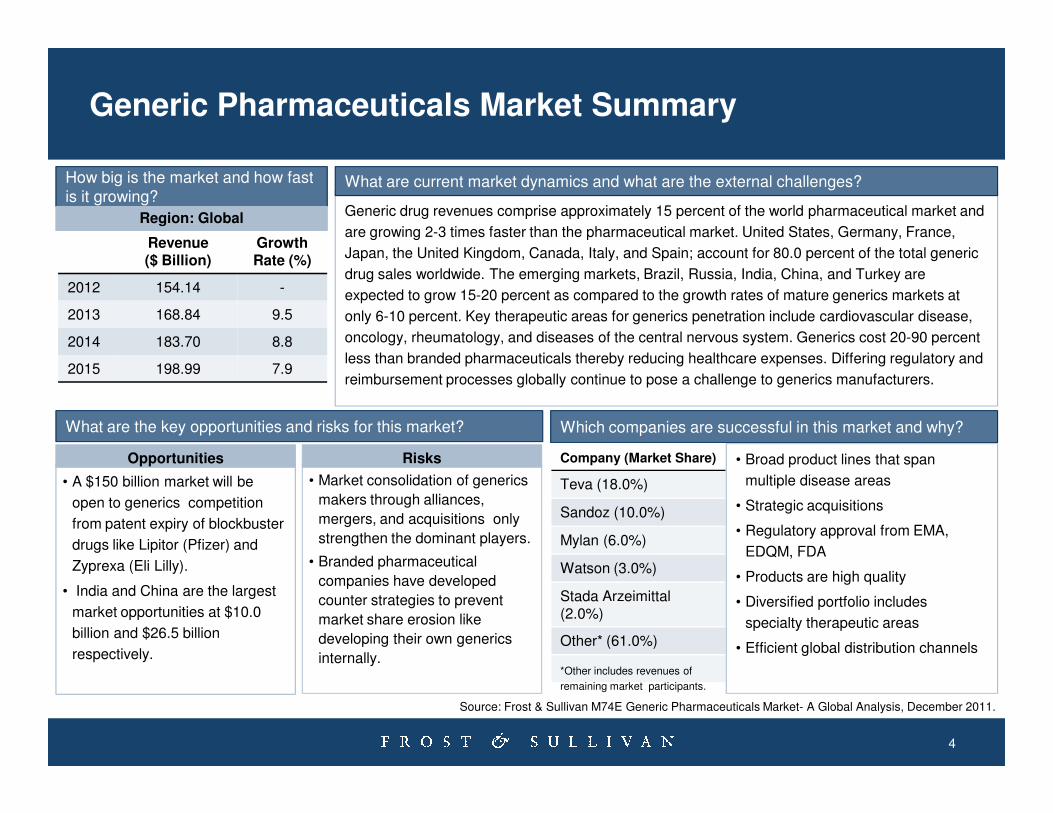

Generic Pharmaceuticals Market Summary

Generic drug revenues comprise approximately 15 percent of the world pharmaceutical market and

are growing 2-3 times faster than the pharmaceutical market. United States, Germany, France,

Japan, the United Kingdom, Canada, Italy, and Spain; account for 80.0 percent of the total generic

drug sales worldwide. The emerging markets, Brazil, Russia, India, China, and Turkey are

expected to grow 15-20 percent as compared to the growth rates of mature generics markets at

only 6-10 percent. Key therapeutic areas for generics penetration include cardiovascular disease,

oncology, rheumatology, and diseases of the central nervous system. Generics cost 20-90 percent

less than branded pharmaceuticals thereby reducing healthcare expenses. Differing regulatory and

reimbursement processes globally continue to pose a challenge to generics manufacturers.

How big is the market and how fast is it growing?

What are current market dynamics and what are the external challenges?

Revenue($ Billion)

GrowthRate (%)

2012 154.14 -

2013 168.84 9.5

2014 183.70 8.8

2015 198.99 7.9

Region: Global

4

• A $150 billion market will be

open to generics competition

from patent expiry of blockbuster

drugs like Lipitor (Pfizer) and

Zyprexa (Eli Lilly).

• India and China are the largest

market opportunities at $10.0

billion and $26.5 billion

respectively.

Company (Market Share)

Teva (18.0%)

Sandoz (10.0%)

Mylan (6.0%)

Watson (3.0%)

Stada Arzeimittal(2.0%)

Other* (61.0%)

Opportunities • Broad product lines that span

multiple disease areas

• Strategic acquisitions

• Regulatory approval from EMA,

EDQM, FDA

• Products are high quality

• Diversified portfolio includes

specialty therapeutic areas

• Efficient global distribution channels

What are the key opportunities and risks for this market? Which companies are successful in this market and why?

• Market consolidation of generics

makers through alliances,

mergers, and acquisitions only

strengthen the dominant players.

• Branded pharmaceutical

companies have developed

counter strategies to prevent

market share erosion like

developing their own generics

internally.

Risks

Source: Frost & Sullivan M74E Generic Pharmaceuticals Market- A Global Analysis, December 2011.

*Other includes revenues of

remaining market participants.

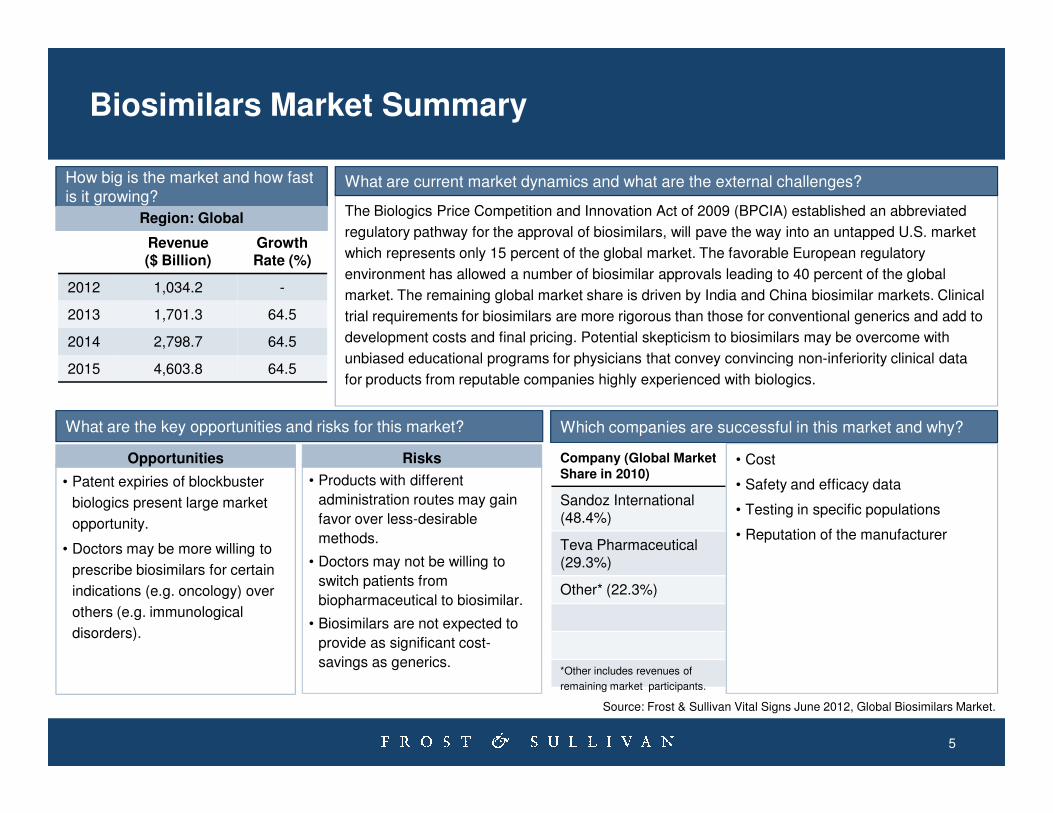

Biosimilars Market Summary

The Biologics Price Competition and Innovation Act of 2009 (BPCIA) established an abbreviated

regulatory pathway for the approval of biosimilars, will pave the way into an untapped U.S. market

which represents only 15 percent of the global market. The favorable European regulatory

environment has allowed a number of biosimilar approvals leading to 40 percent of the global

market. The remaining global market share is driven by India and China biosimilar markets. Clinical

trial requirements for biosimilars are more rigorous than those for conventional generics and add to

development costs and final pricing. Potential skepticism to biosimilars may be overcome with

unbiased educational programs for physicians that convey convincing non-inferiority clinical data

for products from reputable companies highly experienced with biologics.

How big is the market and how fast is it growing?

What are current market dynamics and what are the external challenges?

Revenue($ Billion)

GrowthRate (%)

2012 1,034.2 -

2013 1,701.3 64.5

2014 2,798.7 64.5

2015 4,603.8 64.5

Region: Global

5

• Patent expiries of blockbuster

biologics present large market

opportunity.

• Doctors may be more willing to

prescribe biosimilars for certain

indications (e.g. oncology) over

others (e.g. immunological

disorders).

Company (Global Market Share in 2010)

Sandoz International (48.4%)

Teva Pharmaceutical(29.3%)

Other* (22.3%)

Opportunities • Cost

• Safety and efficacy data

• Testing in specific populations

• Reputation of the manufacturer

What are the key opportunities and risks for this market? Which companies are successful in this market and why?

• Products with different

administration routes may gain

favor over less-desirable

methods.

• Doctors may not be willing to

switch patients from

biopharmaceutical to biosimilar.

• Biosimilars are not expected to

provide as significant cost-

savings as generics.

Risks

Source: Frost & Sullivan Vital Signs June 2012, Global Biosimilars Market.

*Other includes revenues of

remaining market participants.

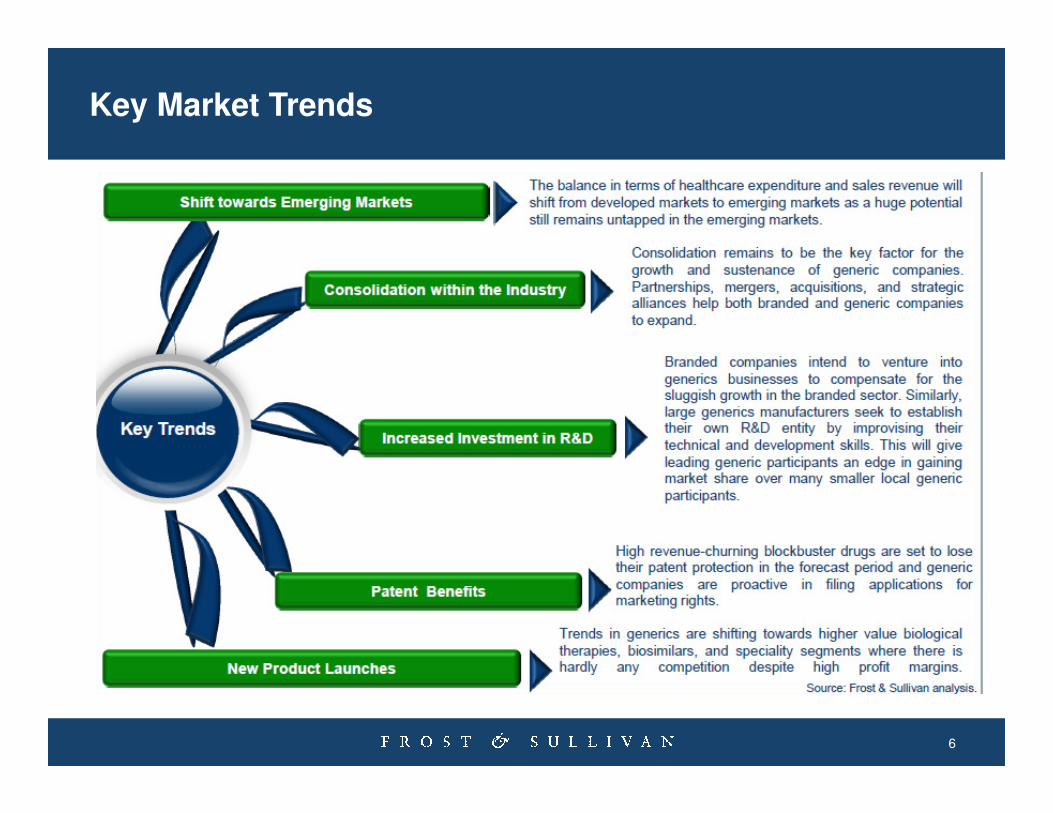

Key Market Trends

6

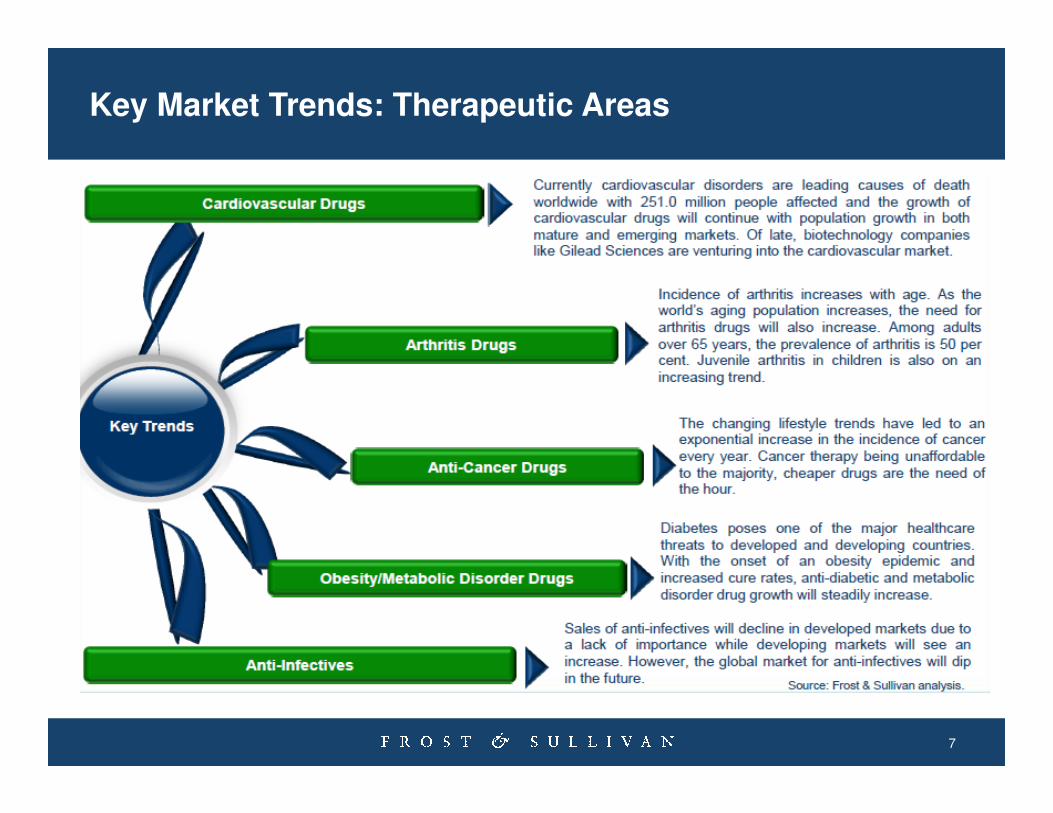

Key Market Trends: Therapeutic Areas

7

Asia outlook

8

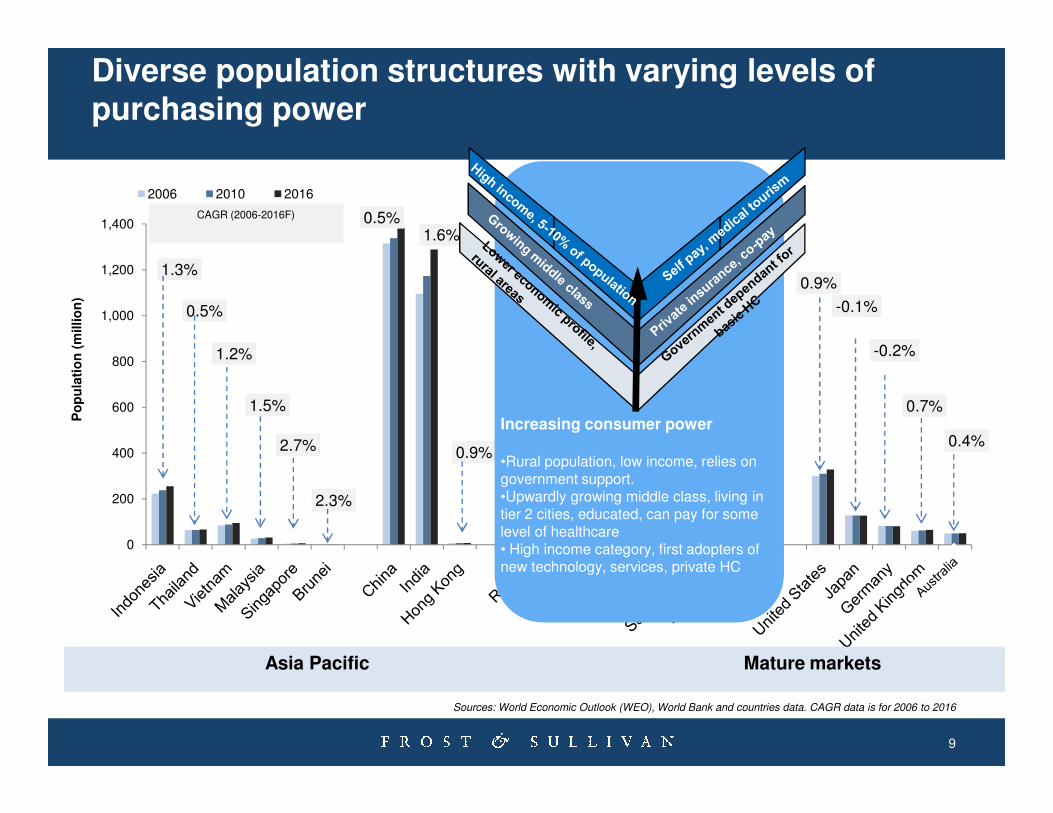

Diverse population structures with varying levels of purchasing power

1.3%

0.5%

1.2%

1.5%

0.5%1.6%

-0.5%

1.0%

2.1%-0.2%

0.9%

-0.1%

-0.2%

0.7%600

800

1,000

1,200

1,400

Po

pu

lati

on

(m

illio

n)

2006 2010 2016

CAGR (2006-2016F)

9

1.5%

2.7%

2.3%

0.9%

2.6%

0.2%

3.9%

0.7%

0.4%

0

200

400

600

Po

pu

lati

on

(m

illio

n)

Asia Pacific Mature markets

Sources: World Economic Outlook (WEO), World Bank and countries data. CAGR data is for 2006 to 2016

Increasing consumer power

•Rural population, low income, relies on government support. •Upwardly growing middle class, living in tier 2 cities, educated, can pay for some level of healthcare• High income category, first adopters of new technology, services, private HC

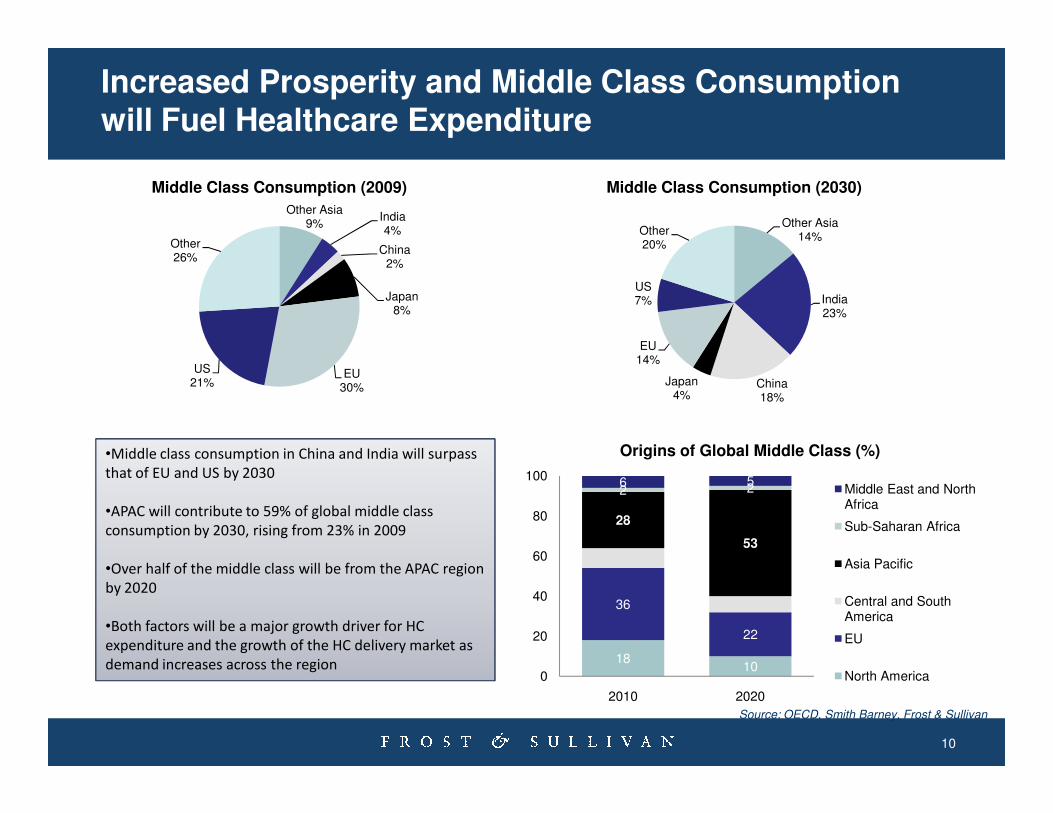

Increased Prosperity and Middle Class Consumption will Fuel Healthcare Expenditure

Other Asia9%

India4%

China2%

Japan8%

EU30%

US21%

Other26%

Middle Class Consumption (2009)

Other Asia14%

India23%

China18%

Japan4%

EU14%

US7%

Other20%

Middle Class Consumption (2030)

10

•Middle class consumption in China and India will surpass

that of EU and US by 2030

•APAC will contribute to 59% of global middle class

consumption by 2030, rising from 23% in 2009

•Over half of the middle class will be from the APAC region

by 2020

•Both factors will be a major growth driver for HC

expenditure and the growth of the HC delivery market as

demand increases across the region 1810

36

22

28

53

2 26 5

0

20

40

60

80

100

2010 2020

Origins of Global Middle Class (%)

Middle East and North Africa

Sub-Saharan Africa

Asia Pacific

Central and South America

EU

North America

Source: OECD, Smith Barney, Frost & Sullivan

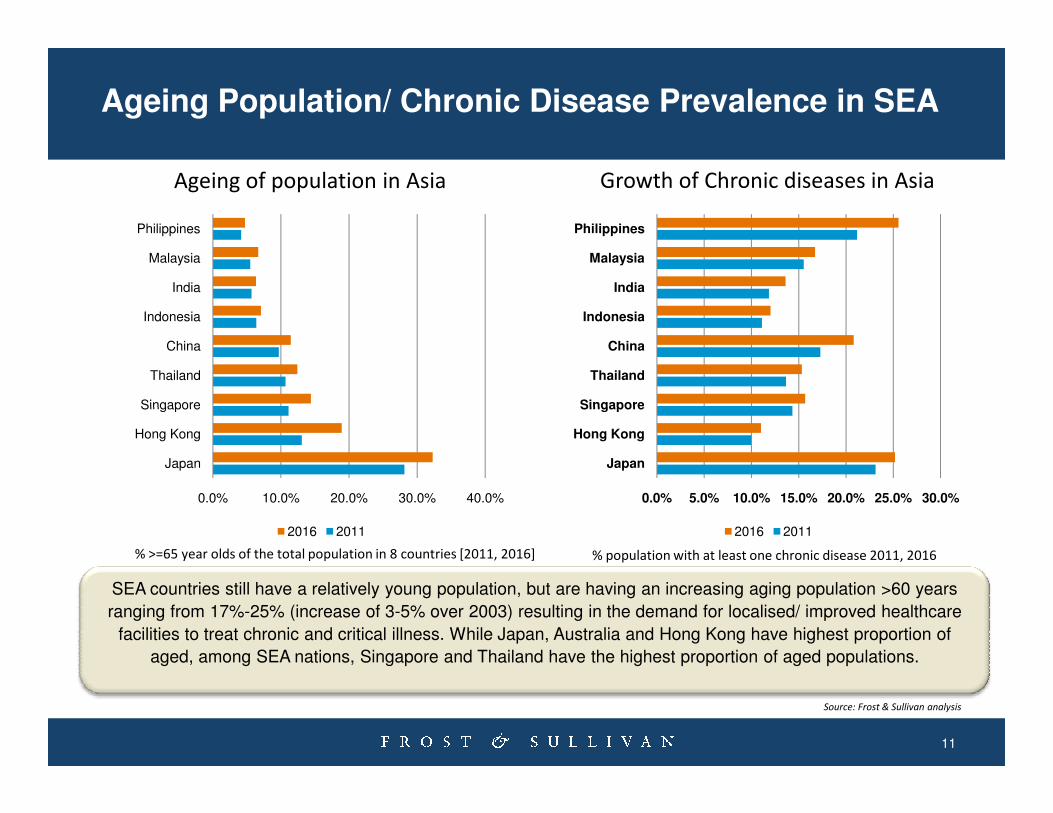

Ageing Population/ Chronic Disease Prevalence in SEA

Ageing of population in Asia Growth of Chronic diseases in Asia

Singapore

Thailand

China

Indonesia

India

Malaysia

Philippines

Singapore

Thailand

China

Indonesia

India

Malaysia

Philippines

11

SEA countries still have a relatively young population, but are having an increasing aging population >60 years

ranging from 17%-25% (increase of 3-5% over 2003) resulting in the demand for localised/ improved healthcare

facilities to treat chronic and critical illness. While Japan, Australia and Hong Kong have highest proportion of

aged, among SEA nations, Singapore and Thailand have the highest proportion of aged populations.

% population with at least one chronic disease 2011, 2016% >=65 year olds of the total population in 8 countries [2011, 2016]

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

Japan

Hong Kong

Singapore

2016 2011

0.0% 10.0% 20.0% 30.0% 40.0%

Japan

Hong Kong

Singapore

2016 2011

Source: Frost & Sullivan analysis

The Last Word

12

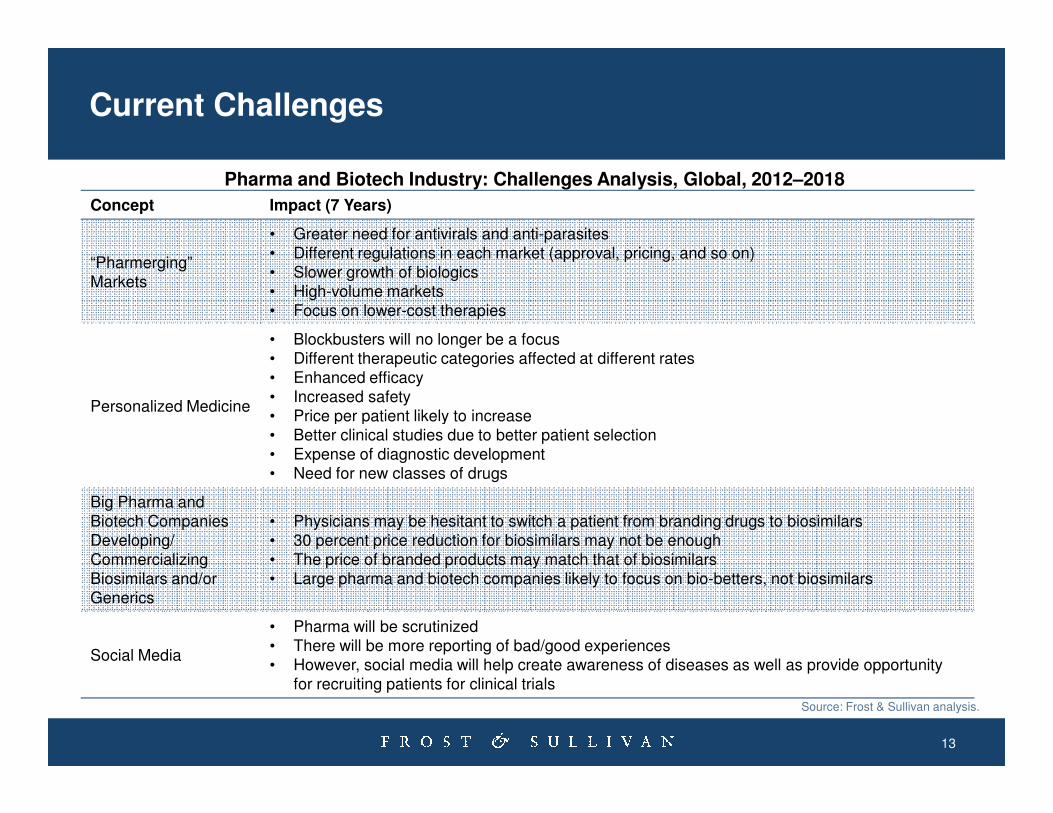

Current Challenges

Concept Impact (7 Years)

“Pharmerging” Markets

• Greater need for antivirals and anti-parasites• Different regulations in each market (approval, pricing, and so on)• Slower growth of biologics• High-volume markets• Focus on lower-cost therapies

Personalized Medicine

• Blockbusters will no longer be a focus• Different therapeutic categories affected at different rates• Enhanced efficacy• Increased safety• Price per patient likely to increase

Pharma and Biotech Industry: Challenges Analysis, Global, 2012–2018

13

Personalized Medicine• Price per patient likely to increase• Better clinical studies due to better patient selection• Expense of diagnostic development• Need for new classes of drugs

Big Pharma and Biotech Companies Developing/CommercializingBiosimilars and/orGenerics

• Physicians may be hesitant to switch a patient from branding drugs to biosimilars• 30 percent price reduction for biosimilars may not be enough • The price of branded products may match that of biosimilars• Large pharma and biotech companies likely to focus on bio-betters, not biosimilars

Social Media

• Pharma will be scrutinized• There will be more reporting of bad/good experiences• However, social media will help create awareness of diseases as well as provide opportunity

for recruiting patients for clinical trials

Source: Frost & Sullivan analysis.

The Last Word

14

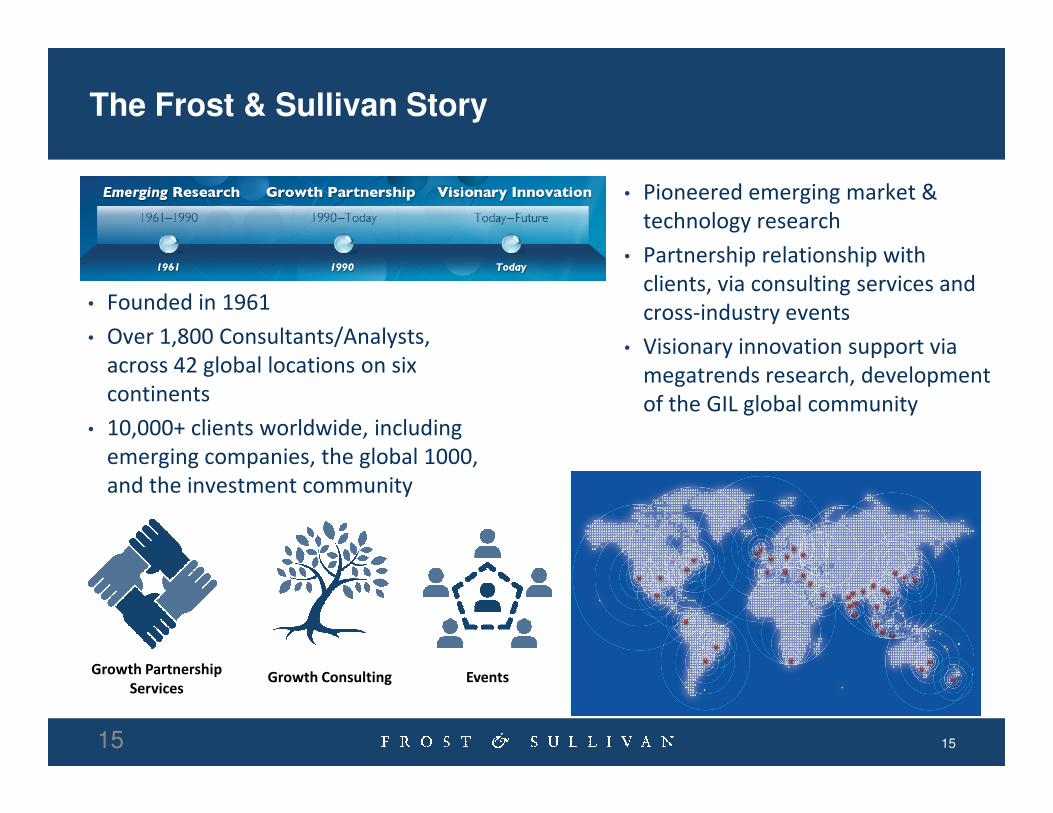

The Frost & Sullivan Story

• Founded in 1961

• Over 1,800 Consultants/Analysts,

across 42 global locations on six

continents

• Pioneered emerging market &

technology research

• Partnership relationship with

clients, via consulting services and

cross-industry events

• Visionary innovation support via

megatrends research, development

of the GIL global community

15

continents

• 10,000+ clients worldwide, including

emerging companies, the global 1000,

and the investment community

Growth Partnership

ServicesGrowth Consulting Events

15

of the GIL global community

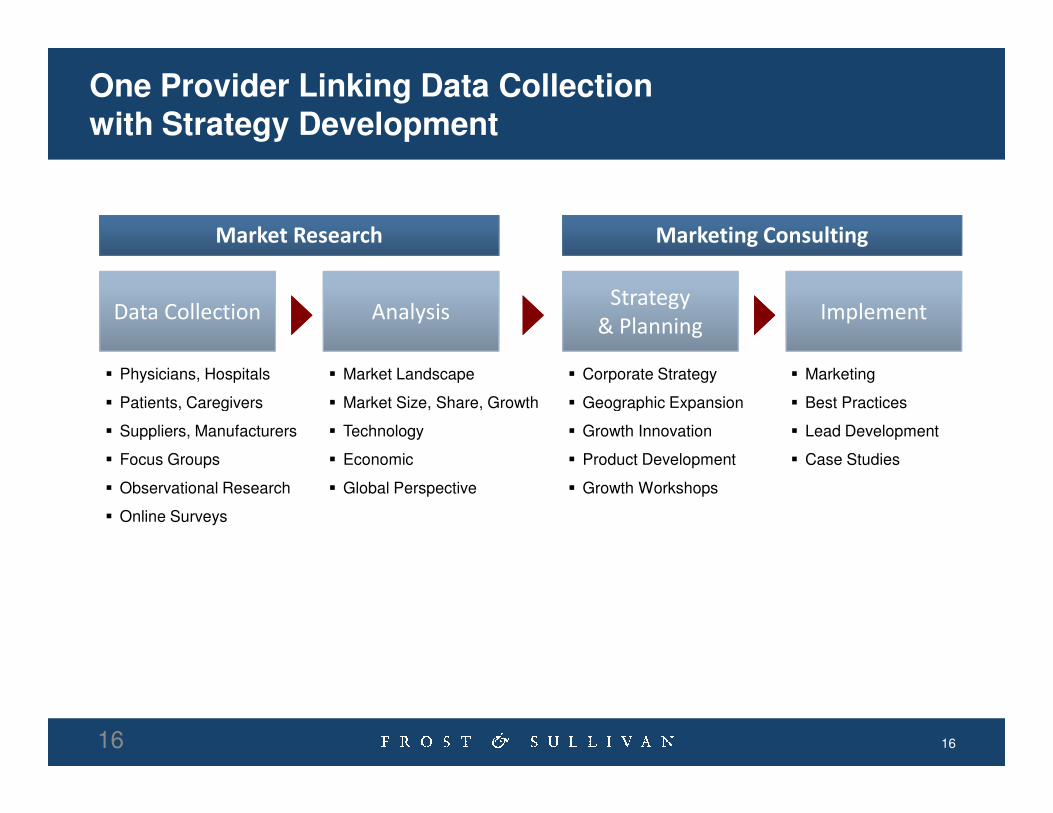

One Provider Linking Data Collection with Strategy Development

Market Research Marketing Consulting

Data Collection AnalysisStrategy

& PlanningImplement

� Physicians, Hospitals

� Patients, Caregivers

� Market Landscape

� Market Size, Share, Growth

� Corporate Strategy

� Geographic Expansion

� Marketing

� Best Practices

1616

� Patients, Caregivers

� Suppliers, Manufacturers

� Focus Groups

� Observational Research

� Online Surveys

� Market Size, Share, Growth

� Technology

� Economic

� Global Perspective

� Geographic Expansion

� Growth Innovation

� Product Development

� Growth Workshops

� Best Practices

� Lead Development

� Case Studies

Healthcare ProgramsCore Growth Markets

� Convergence of Therapeutics/Diagnostics

� Pharma Pipelines

� Next Generation Biologics

� Generics/Biosimilars

� Vaccines

� Life Science Research Tools

Life Sciences Advanced MedTech Connected Health

� Medical Imaging Modalities& Services

� Contrast & Radiopharma

� Surgical & Orthopaedic Solutions

� Infection Control Solutions

� Wound Management

� Patient Monitoring Solutions

� Provider Information Technology

� Analytics

� Health Information Exchange

� Revenue Cycle Management

� Telehealth

� Remote Monitoring

� Video Telemedicine

17

Enabling efficient and outcomes

oriented healthcare delivery

Defining how information

technology improves patient care,

operational efficiencies, and cost

control

Ensuring clients have the tools to

succeed in the new era of

personalized medicine

17

� Next Generation Sequencing

� Contract Outsourcing

� Ventilation and Anaesthesia

� Sleep Diagnostics & Therapy

� Video Telemedicine

� mHealth

Core Geographies: Top 7 EU, U.S., Japan and selected emerging markets (BRIC, APAC and Africa), depending on pillar

Core Know-How: Market landscaping, end-user insights, technology tracking, benchmarking, visionary innovation

Core Delivery Platforms: Online access, analyst interactivity, private analyst briefings, quick response database search

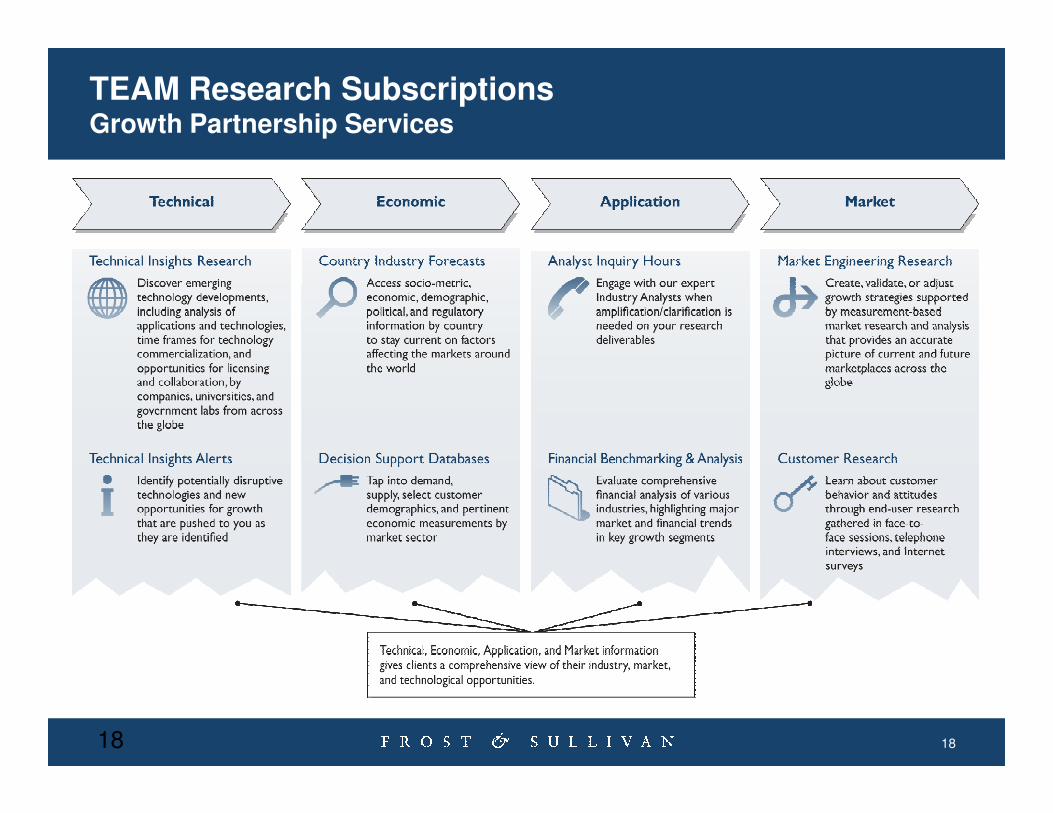

TEAM Research SubscriptionsGrowth Partnership Services

1818

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

19

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

Additional Information

Donna Jeremiah

Director Corporate Communications, Asia [email protected]: +61 (02) 8247 8927

20

Jessie Loh

ManagerCorporate Communications, Asia [email protected]. (65) 6890 0942

Carrie Low

ExecutiveCorporate Communications, Asia [email protected]. (603) 6204 5910

Contact Your Life Sciences Team

Jennifer BriceGlobal Program Manager – Life Sciences

+1 (650) 475 4560

Reenita DasGlobal Leader, Growth Partnership ServicesHealthcare

(+1) 408 8579 386

21

Geeta DhanoaAssociate Director, Growth Partnership Services – APAC, Healthcare

(+60) 03 62045828

Rhenu BhullerVice President, Healthcare GVP, Pharmaceuticals

(+65) 6890 0986

Related Documents