THE PARTHENON GROUP Jeff Woods Partner, Head of the U.S. Healthcare Practice Capital Roundtable Keynote Address February 13, 2014 An Evolving Market: Perspectives on the forces shaping the U.S. Healthcare system This document was created before Parthenon joined Ernst & Young LLP on August 29, 2014, and has not been updated to reflect the combination.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE PARTHENON GROUP

Jeff WoodsPartner, Head of the U.S. Healthcare Practice

Capital Roundtable Keynote Address

February 13, 2014

An Evolving Market: Perspectives on the forces shaping the

U.S. Healthcare system

This document was created before Parthenon joined Ernst & Young LLP on August 29, 2014, and has not been updated to reflect the combination.

THE PARTHENON GROUP

2

Consumer Growth

Private Equity Education

Healthcare

Information & Media

Industrials

San Francisco(2000)

Boston(1991)

London(1997)

Mumbai(2008)

Shanghai(2012)

• Founded in 1991 as a strategic advisory firm

• 275 members in 2014

• Offices in Boston, London, Mumbai, San Francisco, Shanghai, and Singapore

• Client mix includes Global 1000 and mid-market corporations, private equity firms, and educational institutions

The Parthenon Group Overview

Singapore(2014)

THE PARTHENON GROUP

3

Suppliers Providers PayersLife Sciences Gov’t/ Other

• Informatics

• Medical equipment

• Revenue cycle mgmt.

• Temporary staffing

• Managed care

• Medicare/Medicaid/PDP

• Brokers

• Workers compensation

• Cosmeceuticals

• Diabetes supplies

• Medical Devices

• CRO’s

• Healthcare funding

• Medical education

• Dental

• Diagnostic imaging

• Physical therapy

• Urgent care

Healthcare Practice Experience

THE PARTHENON GROUP

4

$2.8T

Provider Life Sciences Payer Gov’t/Public Health

U.S. Healthcare Spend by Segment, 2012

Industry PerspectivesFragmentation and complexity create inefficiency across the U.S. healthcare system

THE PARTHENON GROUP

5

Number of U.S. PE Investments, 1995-2013EPE Investments in

Healthcare (U.S.), 2000-2013

0

20

40

60

80

100%

('00-'04)

n=997

('05-'09)

n=1,264

('10-'12)

n=785

2013

Payers

Info/Internet

Pharma/Biotech

Diagnostics

HealthProducts

MedicalDevices

Soft-ware

Pro

vide

rs

n=239

%of

Tota

lHea

lthca

reD

eals

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1995

874

1996

1997

1998

1999

2000

3,609

2001

2002

2003

2004

2005

2006

2007

2,844

2008

2009

2010

2011

2012

2,115

2013

1,823

Num

bero

fPE

Inve

stm

ents

HealthcareOther

`Note: Includes buyout deals of US targets only; Healthcare excludes biotech`

Industry PerspectivesReported 2013 healthcare deal volume was down 20%, but roughly proportional to overall deal flow

THE PARTHENON GROUP

6

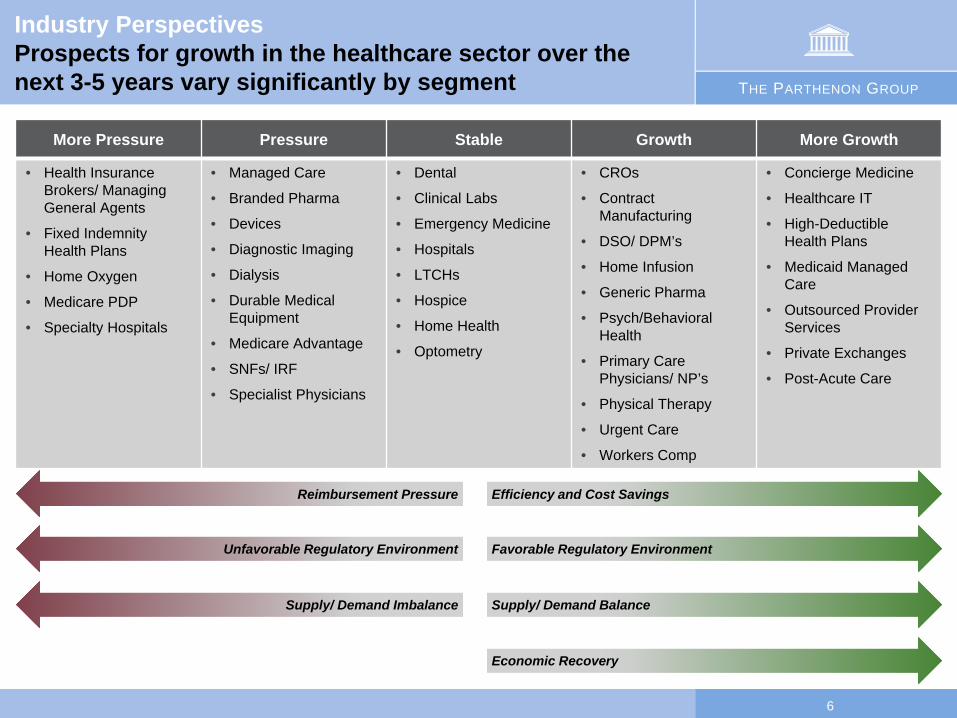

Industry PerspectivesProspects for growth in the healthcare sector over the next 3-5 years vary significantly by segment

Economic Recovery

Favorable Regulatory Environment

Efficiency and Cost SavingsReimbursement Pressure

Unfavorable Regulatory Environment

Supply/ Demand BalanceSupply/ Demand Imbalance

More Pressure Pressure Stable Growth More Growth

• Health Insurance Brokers/ ManagingGeneral Agents

• Fixed Indemnity Health Plans

• Home Oxygen

• Medicare PDP

• Specialty Hospitals

• Managed Care

• Branded Pharma

• Devices

• Diagnostic Imaging

• Dialysis

• Durable Medical Equipment

• Medicare Advantage

• SNFs/ IRF

• Specialist Physicians

• Dental

• Clinical Labs

• Emergency Medicine

• Hospitals

• LTCHs

• Hospice

• Home Health

• Optometry

• CROs

• Contract Manufacturing

• DSO/ DPM’s

• Home Infusion

• Generic Pharma

• Psych/Behavioral Health

• Primary Care Physicians/ NP’s

• Physical Therapy

• Urgent Care

• Workers Comp

• Concierge Medicine

• Healthcare IT

• High-DeductibleHealth Plans

• Medicaid Managed Care

• Outsourced Provider Services

• Private Exchanges

• Post-Acute Care

THE PARTHENON GROUP

7

Four observations on the healthcare landscape…

1

2

3

Investment ThemesParthenon believes investments focused on these themeswill benefit from strong, favorable market dynamics

Challenges and opportunities will arise from expanded gov’t role in healthcare

Access to care issues are looming

Variation within the supply of healthcare delivery materially impact performance of multi-site providers

Healthcare is still a very local business– knowing your customers and referral base is a formidable competitive advantage

4

THE PARTHENON GROUP

8

0

100

200

300M

2012

Non-Group/Other

Employer

Uninsured

Medicaid & CHIP

268M

2018F

Exchanges

Non-Group/Other

Employer

UninsuredMedicaid Expansion

Medicaid & CHIP

280M

-10

0

10

20

30

40M

2012

2M

2013

2M

2014

15M

-1M

2015

22M

-2M

2016

31M

-5M

2017

33M

-5M

2018

Med

icai

dEx

chan

ges

Empl-oyer

34M

-5M

Expanded Gov’t RoleReform will add up to 30M newly insured lives through 1) Medicaid Expansion and 2) Insurance Exchanges…

Health Insurance Status, U.S. Non-Elderly, 2012-2020FIncludes Full Impact of Healthcare Reform

Incremental Covered Lives Added UnderReform, Cumulative, 2012-2020F

-- Confidential: Not to be reproduced without written permission of The Parthenon Group --

1

THE PARTHENON GROUP

9

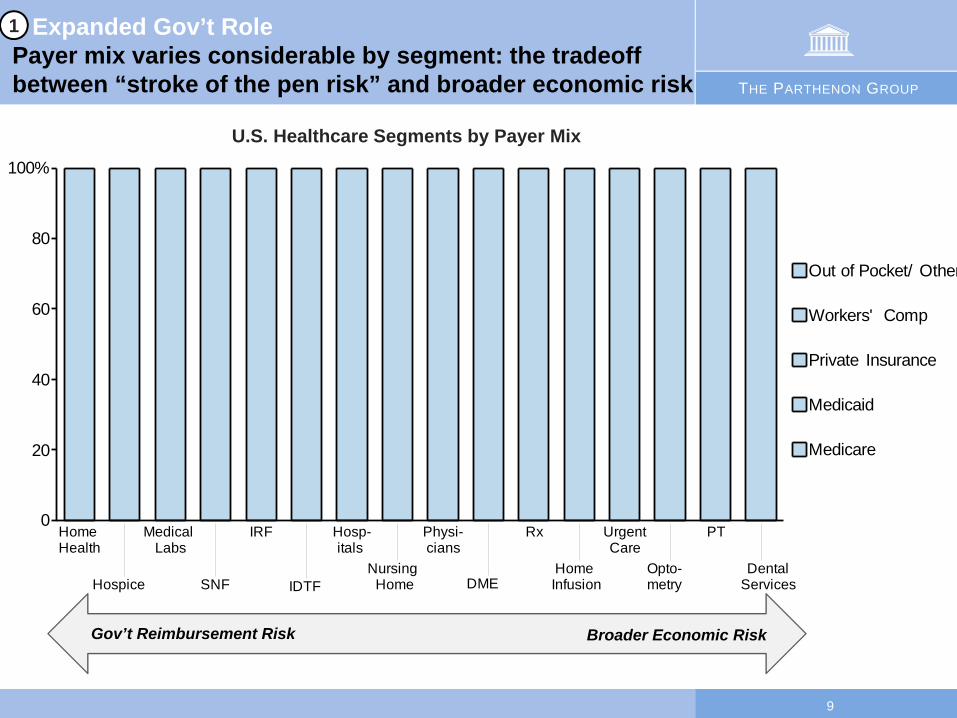

0

20

40

60

80

100%

HomeHealth

MedicalLabs

IRF Hosp-itals

Physi-cians

Rx UrgentCare

PT

Hospice SNF IDTFNursing

Home DMEHomeInfusion

Opto-metry

DentalServices

Medicare

Medicaid

Private Insurance

Workers' Comp

Out of Pocket/ Other

Broader Economic RiskGov’t Reimbursement Risk

U.S. Healthcare Segments by Payer Mix

Expanded Gov’t RolePayer mix varies considerable by segment: the tradeoff between “stroke of the pen risk” and broader economic risk

1

THE PARTHENON GROUP

10

Comparison of MA Physician Workforce vs. U.S. Total, 2010

MA Reform Passed in 2006

Primary Care

Other Special-

ists

Surg-eons

% o

f MA

Phy

sici

ans

Acc

eptin

g N

ew

Pat

ient

s

MA Physician Accepting New Patients, ’05–‘12

Access to care IssuesAccess issues are looming as 30MM newly insured will enter the healthcare system

2

0

20

40

60

80

100%

FamilyMedicine

/ GP20

12Internal

MedicineOB/GYN Cardiology Gastro-

enterologyOrtho

Surgery20

06

45 44 38 29 44 16Avg. Timeto Appt (Days)

-- Confidential: Not to be reproduced without written permission of The Parthenon Group --

THE PARTHENON GROUP

11

3

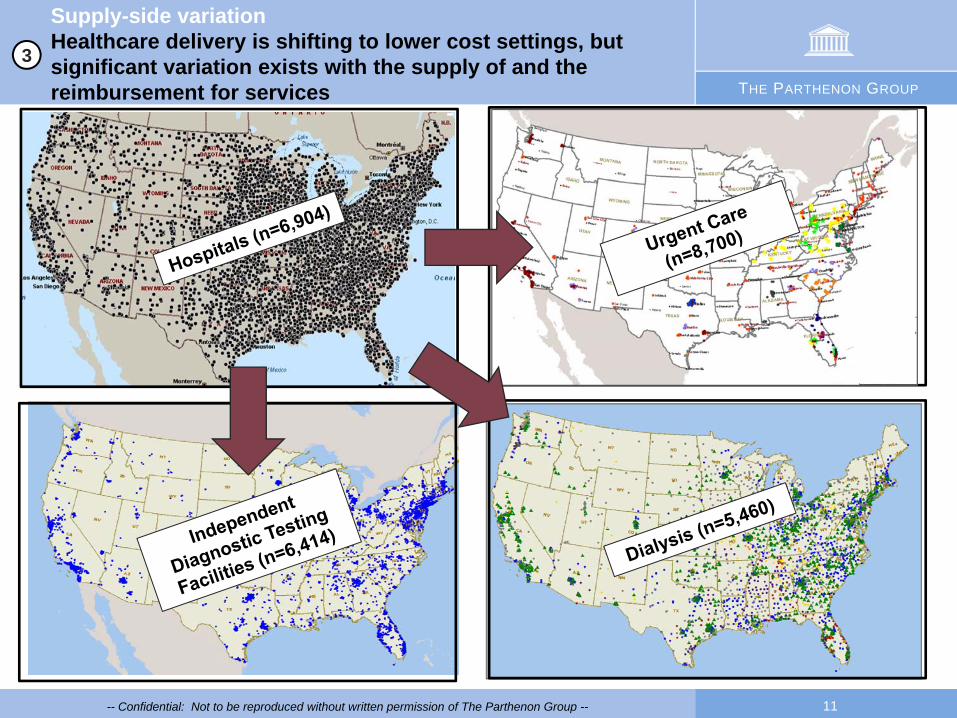

Supply-side variationHealthcare delivery is shifting to lower cost settings, but significant variation exists with the supply of and the reimbursement for services

-- Confidential: Not to be reproduced without written permission of The Parthenon Group --

THE PARTHENON GROUP

12

15 Miles

FacilityCustomer

Customer Referrals by Zip Code (15-Mile Radius)

90% of outpatients travelled less than 15-miles for care at this facility

4 Marketing/ Referral StrategiesThe vast majority of healthcare services are delivered within a referral base of 15-miles or less”

0

20

40

60

80

100%

All Sites

60-80%

80-100%

20-40%

40-60%

n=41

Shar

eof

Res

pons

es

Q: What percent of your total referrals come from your top 10 referring physicians?

THE PARTHENON GROUP

13

Agenda

• Parthenon’s Healthcare Practice

• Perspectives on the U.S. Healthcare Industry

• Investment Themes

• Appendix

THE PARTHENON GROUP

14

Areas of Expertise

Consumer Growth

Private Equity Education

Healthcare

Information & Media

Industrials

THE PARTHENON GROUP

15

Jeff Woods Partner, Head of the U.S. Healthcare Practice

AppendixHealthcare Team

Roger Brinner, Ph.DPartner, Chief Economist

Dr. Brinner is the Chief Economist of The Parthenon Group. He is well known as an expert economist and articulate analyst of the U.S. and international economies, and he has many long-term relationships with corporate clients on issues relating to enterprise strategies and planning. Dr. Brinner’s experience includes senior positions at respected business, academic, and government institutions. Dr. Brinner has been a professor at Harvard University and the Massachusetts Institute of Technology, and for more than 20 years, led the preeminent economic research group Standard & Poor’s/ Data Resources.

Dr. Brinner received a B.A. in Economics from Kalamazoo College and a Ph.D. in Economics from Harvard University.

David NierenbergPrincipal

Mr. Nierenberg is a Principal in the Boston office of the Parthenon Group. Previously, Mr. Nierenberg worked for five years as a consultant with Clarion Healthcare.

Mr. Nierenberg has partnered with many clients across the pharmaceutical, biotech, and medical device industries. His healthcare experience includes managed care strategy; portfolio optimization; life-cycle management; product marketing; sales force effectiveness; and due diligence.

Mr. Nierenberg received his BA magna cum laude, Phi Beta Kappa in History & Science from Harvard University. He completed his MBA at Kellogg, where he graduated Honors and Beta Gamma Sigma.

Mark LaudyPartner, San Francisco Office HeadMr. Laudy oversees the firm’s San Francisco office. His work focuses on business unit strategy, mergers and acquisitions, and growth. Mr. Laudy works extensively with private equity clients on issues of strategic due diligence, and also advises corporations in the consumer products, technology, and financial services industries. Prior to joining Parthenon, Mr. Laudy was with the consulting firm McKinsey & Company, and also with the data communications company Riverstone Networks.

Mr. Laudy graduated summa cum laude and Phi Beta Kappa with a B.A. from Yale College and received a J.D., with distinction, from Stanford Law School.

Jay Bartlett Partner and Co-Head of the Private Equity Practice

Mr. Bartlett is a Partner and Co-head of Parthenon’s Global Private Equity Practice. His work includes conducting due diligence of and developing strategy for companies in a broad variety of sectors, including consumer products, retail, publishing, education, industrial and business services. Prior to joining Parthenon, Mr. Bartlett was Director of Business Development for the Salt Lake Olympic Committee and Olympics.com, and was a consultant with Bain & Company.

Mr. Bartlett received his B.A. in economics, magna cum laude, from the University of Vermont, and completed his M.B.A. at the Tuck School of Business at Dartmouth, where he was elected Edward Tuck Scholar.

Mr. Woods is a Partner in the Boston office of The Parthenon Group and the Head of the firm’s U.S . Healthcare Practice. Mr. Woods has more than a decade of consulting experience in healthcare, including the hospital, medical device and health insurance industries. He has considerable experience in due diligence and portfolio work for private equity clients. Further, his corporate client work includes strategy development, operational improvement, M&A, and sales force optimization. Previously, Mr. Woods worked in the business development group at Guidant and in the decision-support software division at Health Management Systems.

Mr. Woods holds a B.A. in Biology from Dartmouth College, an M.S. in Evaluative Clinical Sciences from Dartmouth Medical School, and an M.B.A. with distinction from the Tuck School of Business

Tim Dutterer Partner, Technology Practice

Mr. Dutterer is a Partner in Parthenon’s Private Equity Practice in San Francisco where he focuses on the technology sector and emerging consumer brands. His work includes due diligence services, growth strategy development, and exit planning. Previously, Mr. Dutterer was a technology consultant at IBM and PricewaterhouseCoopers where he advised corporate, government, and non-profit clients on technology and strategy development.

Mr. Dutterer received his B.A. cum laude in Public Policy from The College of William and Mary and his M.B.A. with distinction from the Harvard Business School..

THE PARTHENON GROUP

16

AppendixHealthcare/ Private Equity Practice Services

Due DiligenceServices

Portfolio Company Performance

Improvement Program

Private Equity Strategy

Development

180 Day Plan Development

Annual portfolio assessment and adjustment strategy

Business strategies for private equity firms

Identification of proprietary deal sourcing options through industry screens and assessments

Marketing and positioning strategy

Customer and market growth assessments

Industry attractiveness assessments

Business growth forecasts

Target strategic position assessments

Synergy audits

Acquisition opportunity assessments

Collaborative development of action-oriented road map to be executed upon closing and for first 6 months of investment

Builds upon key issues and opportunities highlighted in diligence

Development of key performance indicators

Mergers & Acquisitions

New Market / Channel Strategy

Customer Segmentation

Pricing Strategy

Marketing Effectiveness

Sales Force Optimization

Product Mix / Segmentation

Working Capital Improvement

Logistics & Supply Chain Optimization

SG&A Cost Reduction

Industry attractiveness assessments

Business growth forecasts

Tracking of customer loyalty, company growth and evolution of market position

Networking support

Offers third party assessment of company positioning, track record and future prospects

Vendor Due Diligence

Typical Project Duration:

1 to 3 Months 3 to 4 Weeks 3 to 8 Weeks 1 to 6 Months 1 to 3 Months

Exit Strategy Planning & Support

THE PARTHENON GROUP

17

ExperienceCompleted Transactions

Equity Provider:Audax Group

Aug 2008

Commercial due diligence

FL-based dental practice management company

Equity Provider:Audax Group

May 2008

Commercial due diligence

Provider of dental practice management

and administrative support services

Equity Provider:Actis Capital

Nov 2010

Commercial due diligence

Outsourced IT and BPO services provider to

hospitals

Equity Provider:General Atlantic

Sep 2010

Commercial due diligence

Multi-site urgent care provider

Commercial due diligence

Equity Provider:Parthenon Capital

May 2007

Provider of revenue cycle management

software

Equity Provider:Audax Group

Jan 2008

Commercial due diligence

Third Party Administrator (TPA) of disability and absence management

Equity Provider:Morgan Stanley PE

Dec 2010

Commercial due diligence

Provider of mobile dentistry services to

Medicaid youth

Commercial due diligence

Manufacturer of blood glucose testing devices

for diabetics

Equity Owner:Gores Group

Apr 2008

180 day plandevelopment

Operator of freestanding diagnostic imaging

centers

Equity Owner:Monitor Clipper

Jul 2009

Third party cost-containment service

provider to workers’ comp payers

Portfolio Improvement

Equity Provider:Catterton Partners

Sep 2011

Commercial due diligence

Multi-site dental implant centers

Equity Provider:Charlesbank

Feb 2012

Portfolio Improvement

Provider of mobile lasik and cataract surgical

equipment

Equity Provider:Catterton Partners

Jul 2009

Cosmeceutical skin care brand

Commercial due diligence

Commercial due diligence

Equity Provider:Hellman & Friedman

Apr 2012

Third party administrator of workers’ comp

services

Equity Provider:Tower Three Partners

Jan 2011

XactiMed

Sedgwick PHNS.

ReedGroup Consolident,Inc

DiagnosticHealth

Great Expressions

Dental Centers“Look For The Smile

Above Our Name”

MSCCare Management StriVectin

MedExpress Great.Care.Fast

Urgent Care

ReachOut HealthCareAmerica

FacetTechnologies

SightpathMedical

ClearChoiceDental Implant

Centers

THE PARTHENON GROUP

18

Equity Provider:Piramal/ IndUS

Growth PartnersMay 2012

Commercial due diligence

Provider of data, analytics and consulting

services to the healthcare industry

Equity Provider:Ontario Teachers

Pension PlanNov 2012

Commercial due diligence

The largest dental services organization

(DSO) in the U.S.

ExperienceCompleted Transactions, cont.

Equity Provider:Ameritox

Aug 2013

Commercial due diligence

Provider of pain management services to Workers Comp payers

Equity Provider:TransUnion

Sept 2013

Commercial due diligence

Equity Provider:TA Associates

Sept 2013

Commercial due diligence

Provider of Revenue Cycle Management service to hospitals

Leading provider of long-term care

pharmacy operating software

PE Sponsor:Odyssey / One Call

MedicalSept 2013

Post-Merger Integration

Provider of third party cost containment

services provider to workers’ comp payers

Sponsor:Bigalow & Co.

Nov 2013

Sell-side due diligence

Electronic patient scheduling, check-in and

billing solutions

Equity Provider:Catterton Partners

Feb 2012

Commercial due diligence

Outsourced provider of core measures

abstraction services to hospitals

PE Sponsor:Odyssey Partners

Oct 2013

Sell-side due diligence

Leading 3rd party cost containment services provider to workers’

comp payers

Equity Provider:Pexco LLC,/ Odyssey Investment Partners

Sept 2013

Commercial due diligence

Precision injection molder to the medical

device industry

PE Sponsor:Odyssey / One Call

MedicalSept 2013

Post-Merger Integration

Provider of transportation and translation services

PE Sponsor:Apax / One Call Medical

Dec 2013

Post-Merger Integration

Provider of third party cost containment

services provider to workers’ comp payers

Patient Point Decision Resources group

Heartland Dental Care

EScan Data Systems INC

WI SoftWriters

PRIUM Medical Cost

Management Services

Align Networks

Q-Centrix Quality Measures

Outsourcing

OneCallCare Management

3i Corp.com

Spectrum Plastics Group

TechHealth Simplifying the Process of Care

Related Documents