File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am 1 DIPARTIMENTO DI DISCIPLINE ECONOMICO-AZIENDALI UNIVERSITÀ DEGLI STUDI DI BOLOGNA PERSPECTIVES ON STRATEGY: MANAGEMENT AND ACCOUNTING DISCOURSE IN HISTORICAL PERSPECTIVE Luca Zan Department of Management, Univeristy of Bologna; email: [email protected] Paper submitted to the 22 nd volume of Advances in Strategic Management, Expanding Perspectives on the Strategy Process INSEAD Conference, Fontainblue, 24th – 26th August, 2003 Preliminary Draft, August 2003 ABSTRACT The aim of the paper is tracing and identifying, within the international literature on management, a number of new departures that are of interest to, and importance for, historical inquiry. If historians have to understand the role of actors and managers – it is argued – they are likely to benefit from an in-depth understanding of management knowledge. Thus three different perspectives are investigated, under which the relationship between the specialist knowledge within the management field and historical work can be looked at (the relevance of management literature; history of accounting though; and history of management practices). Far from being the one way application of a clear cut knowledge transfer (from management to history), however, within a less simplistic view the adoption of a historical perspective is seen as questioning to a significant extent the taken-for-granted identity of management studies as a whole, as a practically oriented discipline, and the very articulation in sub disciplines (such as "strategic" management), calling for a more catholic, comprehensive view of management studies as a whole, with greater degrees of awareness about its own evolution. Key words: Management theory and practice; Management processes; Management and accounting history; Strategic change; Accounting Historiography; Venice Arsenal

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

1

DIPARTIMENTO DI DISCIPLINE ECONOMICO-AZIENDALI UNIVERSITÀ DEGLI STUDI DI BOLOGNA

PERSPECTIVES ON STRATEGY: MANAGEMENT AND ACCOUNTING DISCOURSE IN

HISTORICAL PERSPECTIVE Luca Zan

Department of Management, Univeristy of Bologna; email: [email protected]

Paper submitted to the 22nd volume of Advances in Strategic Management, Expanding Perspectives on the Strategy Process

INSEAD Conference, Fontainblue, 24th – 26th August, 2003

Preliminary Draft, August 2003

ABSTRACT The aim of the paper is tracing and identifying, within the international literature on management, a number of new departures that are of interest to, and importance for, historical inquiry. If historians have to understand the role of actors and managers – it is argued – they are likely to benefit from an in-depth understanding of management knowledge. Thus three different perspectives are investigated, under which the relationship between the specialist knowledge within the management field and historical work can be looked at (the relevance of management literature; history of accounting though; and history of management practices). Far from being the one way application of a clear cut knowledge transfer (from management to history), however, within a less simplistic view the adoption of a historical perspective is seen as questioning to a significant extent the taken-for-granted identity of management studies as a whole, as a practically oriented discipline, and the very articulation in sub disciplines (such as "strategic" management), calling for a more catholic, comprehensive view of management studies as a whole, with greater degrees of awareness about its own evolution.

Key words: Management theory and practice; Management processes; Management and accounting history; Strategic change; Accounting Historiography; Venice Arsenal

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

2

1. INTRODUCTION The value of interdisciplinary dialogue takes on a specific set of meanings within context of historical research. As soon as one acknowledges the role of actors in the development of organizations – especially that of managers –, the need fully to grasp the logic and behaviors occurring within a network of specialized concepts and meanings emerges, e.g. management as a body of knowledge. Accordingly, the aim of the paper is tracing and identifying, within the international literature on management, a number of new departures that are of interest to, and importance for, historical inquiry.

Given its apparent "technicality", accounting immediately underlines the complex structures of knowledge upon which the interpretation of a given fact or piece of information necessarily relies. Even when less highly structured notions relating to managerial action are entailed, however, what arises is the tricky task of interpreting such notions from within specialized debates: the best example is perhaps the ambiguity surrounding the notion of strategy over thirty years of debates within strategic management studies 1. In any case, such inner controversies and disputes simply risk to be ignored by business (or management, or accounting) historians, given the effects of disciplinary boundaries; in turn, and for the same reason, management and accounting scholars risk to largely misunderstand the historical meaning of their contributions.

This paper seeks to contribute a series of reflections on theory development within management studies using a historical perspective, though not merely focusing on last years’ events. The perspective adopted is that of a "specialist" investigation, based on the knowledge and research experiences that revolve around that knot of disciplines that includes business studies, managerial science, accounting and business economics – with all the inevitable difficulties of defining their content, within a context of supranational interaction, that are familiar to anyone who has an even cursory acquaintance with the international conference circuit in "our fields". Rather than attempt any systematic reconstruction of the state of the art, this paper has the more modest goal of tracing and identifying, within the international literature on management, a number of new departures that are of interest to, and importance for, historical inquiry. Besides, more than the "domestic" issues of historical research, what interests us here is their relevance and application from and to accounting and management discourse. Indeed in trying to explain possible uses of specialists' tools for (accounting-business) historians, we shall revisit several meaning of management and accounting research that are commonly taken for granted.

The paper is structured in three sections that reflect three different perspectives under which the relationship between specialists knowledge in the management field and historical work can be looked at according to the aim of the paper. The first section investigates the implications for historical research that may flow from the tradition of management studies as these have developed in the English-speaking world, in three quite separated theoretical contexts: (a) the longitudinal approach within strategic management literature; (b) some issues related to a sociology of knowledge approach in management field, in particular referring to the 1 A case in point is provided by the concept of strategy, where the following wording reveals a tortuous cognitive and theoretical path to the more general debate, well described by Chandler: "In a recent article ... Nelson, taking as his starting point his own early work with Winter as well as more recent work by David Teece, Giovanni Dosi, William Lazonick and myself, presents 'an ongoing theory of the dynamic capacities of the firm'. The article brings into focus 'three different yet closely linked aspects of the firm that need to be clear if one wishes to describe the firm adequately: its strategy, structure and core capacities'. In Nelson's view, it is their strategy and structure that constitute the capacities of firms, rather than the transactions that they undertake. Strategy, Nelson writes, '[is] what management experts talk about, not that of games theory ...'" (Chandler, 1991: p. 84, my emphasis. It is a pity that he then makes a point that would strike strategic management scholars as no longer tenable, in view of the way that debate has proceeded over the last few decades: "that is, a set of broad commitments that the firm pursues and that define and rationalise its goals and the way in which it intends to reach them".)

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

3

controversial relationship between management theories and practices; and (c) some of the key assumptions of critical accounting, and their direct translation into the so-called “new accounting history” approach.

Taking a history-of-ideas approach, the second section outlines serious problems in reconstructing any history of management, given the lack of sense of history that seems to be shared in the field (with few exceptions, e.g. the naive position by Ansoff, 1984, for strategic management), and the self-perception of innovation and discontinuity that seems to characterize management scholars. It is merely worth stressing here that even in the last few decades such research has been undertaken within management field prevalently by accounting historians, focusing to some extent (in any case greater that that of strategic management scholars) to "strategy" issues in historical investigation. Thus the paper the inquiry will move into comparativist territory, engaging with accounting historiographies of varying provenance. In particular, the separation between accounting historiographies is underlined, and some of the odds of this situation are investigated drawing on the Italian tradition – largely unknown by the ethnocentrism of the dominating Anglo-American literature; and largely selfreferential in its own identity.

The third section describes two interesting historical research projects on managerial and accounting practices in pre-industrial revolution contexts: the Spanish Royal Tobacco Factory on 1773 (Carmona, Ezzamel, Gutierrez, 1997) and the Venice Arsenal (Zan & Hoskin, 1999; Zan, 2003). In addition to their own elements of interest at a substantive level, I shall discuss here briefly on the findings of these two researches as "applications" of specific management (and particularly strategic management and strategic change) and accounting skills to historical investigation. Some implications of such a multifaceted, multilevel understanding of the relationship between (strategic?) management and accounting specialisms and historical research are then developed in the concluding remarks, with particular reference to the research agenda of the strategic management field.

2. IS STRATEGY AND MANAGEMENT LITERATURE RELEVANT FOR HISTORICAL INQUIRY? Given the unceasing quest for novelty and for fresh "lessons" to learn and impart, as well as the tides of sheer fashion that characterize strategy and management studies, it may in some ways appear paradoxical to look to this area for theoretical or methodological relevance to historical inquiry. What is disconcerting is the utter lack of historical memory about business and managerial practices (the “real world”), or indeed in relation to the development of theories and research traditions on these issues (the world of ideas).

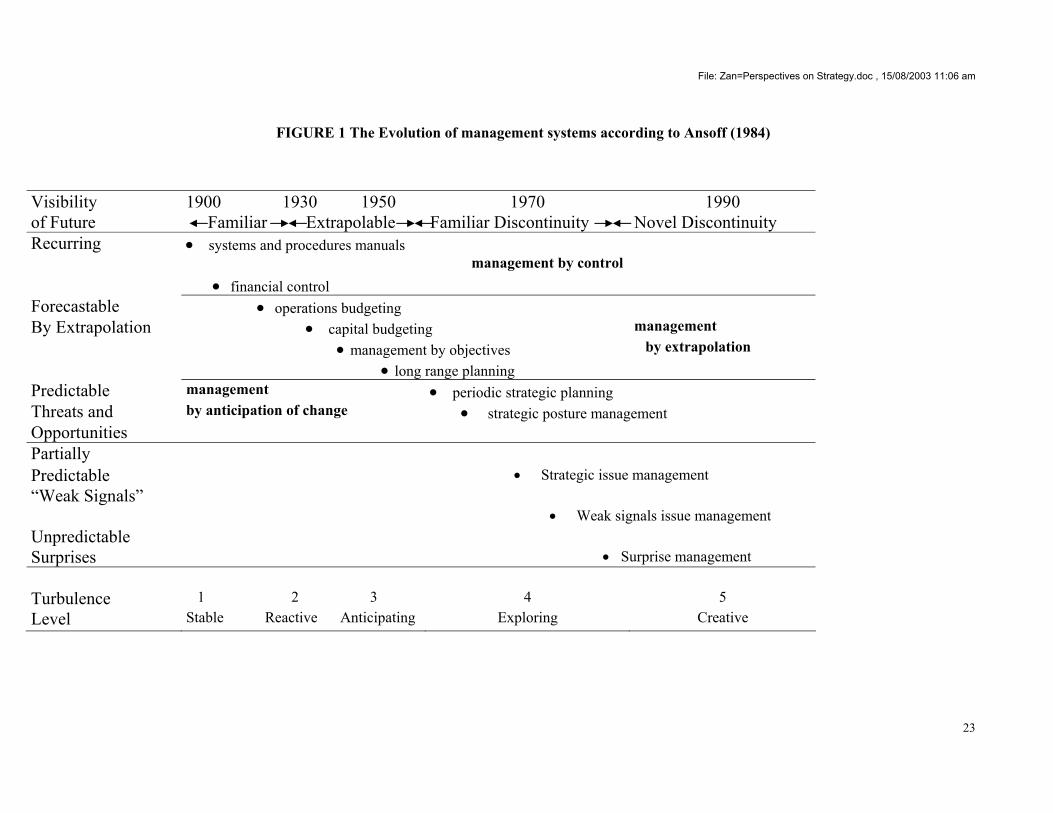

Faced with a reconstruction of the development of "management systems" such as that provided by Ansoff (1984, Chapter 2), one is struck by two opposing sensations (see Figure 1). On the one hand, one can see the potential for an historicized view of time and managerial issues. In such a context, "time" no longer stands exclusively for future time, confined within a logic (even in formal terms) of forecasting, anticipating and discounting values, the time of so-called problem-solving approach, a further consequence of the prescriptive bias and the resulting disciplinary identity of management studies. "Time" then covers past time also, that of conditions and practices that "come from afar", however confusedly and vaguely.

[Insert Figure 1 about here]

On the other hand, this figure looks a trifle ridiculous today, given that the past is

exclusively recent, indeed quite incapable of reaching back beyond the Second World War, almost as if the world of management had been born at that time and had subsequently evolved

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

4

in the midst of new and more or less innovative watchwords (management by extrapolation in the 40s to 50s; management by anticipation in the 60s and 70s; and management by flexible rapid response from the 70s on). In Ansoff's view, new and specific technicalities were associated with these three periods respectively: a) operations budgeting, capital budgeting, management by objectives, long-range planning; b) periodic strategic planning, strategic posture management; c) strategic issue management; weak signals issue management; surprise management. Within this framework, the present assumes the character of a definitive discontinuity, a clean break with all that went before, which, owing to the "turbulence" and "objective" increase in innovative and competitive processes, is irreparable 2. Here indeed the terms "before" and "after" are yet again evacuated into poorly understood ideal types (see for example the prevailing narrative covering the development of planning systems: from Long Range Planning to Strategic Planning to Strategic Management), that is to say, into un-problematized and paralyzing dichotomies (including the current knee-jerk reference to the Fordist/Post-Fordist firm).

Beyond a mere appearance of practical uses, however, it is worth recalling that within the experience and tradition of strategy and management studies (accounting included) there are a number of features that might prove to be important tools even for the analysis of the evolutionary paths of practices from a historical angle: (1) the longitudinal approach within strategic management literature; (2) some issues related to a sociology of knowledge approach in management field, in particular referring to the controversial relationship between management theories and practices; and (3) some of the key assumptions of critical accounting, and their direct translation into the so-called “new accounting history” approach. I am totally aware that the very coupling of these different and divided streams of research is absolutely unusual in any of these fields. But the deconstruction of taken for granted boundaries of research is part of the game of the paper, aiming at “expanding perspectives on the Strategy Process”.

1. The first such feature is the longitudinal approach adopted by at least a section of this literature, linked to a less simplistic assumption regarding the nature of the decision-making processes undertaken by the actors involved, with important consequences for the analyst's own "reconstructive" and sense-making effort. Indeed the very problemitization of the concept of strategy, between content and process, the very notion of emergent strategies, as Mintzberg will put it, fundamentally the "destabilizing" impact itself of the concept of strategy (Biggiero, 1990), throw up important investigative leads for the reconstruction of plausible unanticipated consequences that the intrinsic complexity of social and economic operation entails with regard to intention: both elements (complexity and intention) being more or less consciously reconstructed by the actor and capable of reconstruction by the analyst. On the one hand, the centrality of learning processes strongly relegitimize the importance of "practices" in organizational action. On the other hand, all the literature on "strategic change" (see Normann, 1977; Mintzberg 1978, 1994; Kimberly, & Miles, 1980; Quinn, 1980; Johnson, & Scholes, 1984; Pennings, 1985; Pettigrew, 1985, 1987, 1989, 1990; Johnson, 1987; Zan, 1987, 1995; Mintzberg & Waters, 1990; Grant, 1991; Knights, & Morgan, 1991; Pettigrew, & Whipp, 1991; Zan, Zambon, Pettigrew, 1993; Clegg, Hardy, Nord, 1996; Whipp, 1996, 2002; Baden-Fuller, van den Bosch, Volberda, 2001;Grant, Wailes, Michelson, Brewer, Hall, 2002. Cfr. also Crozier & Fridberg, 1977; Van de Ven &, Astley , 1981; Astley & Van De Ven, 1983; Burgelman, 1983; Bourgeois, 1984) provides an important point of reference in terms also of the "operationalization" of research, which may constitute the meeting-point par excellence for business historians and business scholars with historical interests, where "change" is an analytic

2 For a critique of this position, which one might term "presumption of hindsight" or arrogance of posterity, according to which present-day processes of change and "complexification" raise issues of knowledge intrinsically greater than those thrown up by any other historical context, cf. Zan, 1995.

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

5

category in its own right. However, there is no ambition to reconstruct an "objective" ranking of discontinuities, as if some might be more unique than others.

Moreover, it is worth remarking that the inevitable drop in prescriptive capacity that accompanies the assertion of a processual view presents a curious outcome, for strategy scholars, a sort of collective drive "back to origins", if one recalls the importance of business history studies in the construction of a disciplinary identity for strategy studies, especially around the work of Chandler (1962). Once the naive image of a strategy expert (guru) has faded and gone, the strategy specialist still retains a role of some importance, if not in the ex ante pinpointing of (more or less mega-) trends, at least in the ex-post reconstruction of historically located processes. For, despite everything, the tools used in management studies may demonstrate great interpretive power, at least in comparison with others (see below).

2. In the quest for implications applicable to the field of historical research, a second line

of investigation may be followed in the kind of broader-based work on the nature of management studies to be found in the international literature. This current of research applies reflexively to the community of knowledge-producers in management studies an analysis of the reasons and consequences concerning the functioning of this ultra-complex "reputational organization" (Whitley, 1984a). While there is no need for everyone to turn themselves into sociologists of knowledge, it is at least essential to attain some awareness of such aspects (i.e. local varieties and idiosyncratic characterizations affecting mechanisms of validating research standards, and the resulting disciplinary fragmentation and variations in the construction of the disciplinary domain in different spatial and temporal contexts). But, as far as these processes are concerned, it is above all the increasing relative autonomy of academic practices from managerial practices that has to be grasped, not as some kind of degenerative process, but as a cleavage between practice and theory that is inevitable – even in the field of business and management studies (Asthley, 1984). The differences in relational contexts between the world of company practice and the academic world (Whitley's "knowledge producers") mean that discursive practices at the two levels operate in relatively discrete ways. In a previous paper, I was referring to the example of the temporal gulf that divides the phenomenological reality analyzed by Chandler in relation to multi-division firms and, on the other hand, the spread of this analysis across academia in the last thirty years. 3

The critical and problematic nature of the relation between practice and theory is one of management studies' distinguishing features, conferring upon the field a somewhat fuzzy, partly contradictory, but basically very open and dynamic, epistemological status. Yet to eschew such a problematization of the practice/theory relationship would be once again to risk adopting a position of naivety and the frequent oddities of the field – including the construction of a sense of caste, the managerial ideology and the professional identity of management scholars – would remain unaccounted for.

3. A third promising avenue of research with possible implications in the field of

historical analysis is to be sought in perspectives that pay special attention to embeddedness, and here the entire "critical" accounting current springs to mind. Developing over the last 20 years (for a discussion cf. the special issues on accounting history Accounting, Organizations and Society, 1991; Accounting, Auditing & Accountability Journal, 1996; Critical Perspectives on Accounting, 1998), critical accounting aims to recover the meaning of accounting and control practices within the social and organizational context in which they are elaborated, while addressing with particular sensitivity issues such as the mobilization of attention and collective

3 Reference was also made to the history of double-entry bookkeeping, which appears to corroborate this discreteness between theory and practice, having in effect been a practice devoid of literature for two centuries or so, subsequently becoming a literature devoid of theory for a further three (see Zan 1994, 1995).

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

6

action, conflict and above all power. Suspicious of neutral notions of progress, antithetical to a linear view that would see accounting practices developing “towards greater accuracy and truthfulness", this approach "is concerned with significant shifts of accounting and social relations and the struggles associated with these " (Miller, Hopper, Laughlin, 1991, p. 399).

This perspective has not found much favor in continental Europe and in other areas of management research. The reasons for this may well lie in its perceived untechnicality and its sociological derivation, a feature which is not always appreciated in the fields of management and business economics (associated with a perceived undermining of academic identity and disciplinary specialization). However, in the very process of operationalization, this current has translated into the adoption of a particular stance towards historical research (albeit confined to the field of accounting and control), which has now coalesced in the form of a solid group of academics clustered round "new accounting history"4. Sympathetic with such an approach in its basic assumptions, the writer however wishes to embrace a broader stance in terms of the “object of analysis” (i.e. not focusing merely on accounting), in terms of theoretical perspectives (opening up to different disciplinary backgrounds as for instance strategic management literature), if possible avoiding the ethnocentrism characterizing – so far – this approach too.

From the foregoing it is possible to sketch a number of "partial conclusions", as well as

some major implications for addressing discourse on management from a historical vantage point, drawing on our understanding as management scholars, possibly under a "modest" approach (Jönsson 1996). Certain crucial points have to be borne in mind:

- the separateness of thought and action, where strategies, to a significant extent "emergent", do not constitute a given and clear cut element, and demand a process of re-construction of the actor and the analyst, largely leaving room for “unanticipated consequences of human action”;

- an attention to local and subjective processes of knowledge/partial ignorance (Loasby, 1976), regarding the complexity of economic and organizational action as it may plausibly be perceived by the actors themselves, free from any "presumption of hindsight";

- the need to avoid flattening out practices and theories, making allowances for contradictions or even just significant reciprocal mismatches between them, acknowledging them, in other words, as discursive practices that operate in separate contexts (the real world vs. the Academia);

- a close attention to relational and power profiles which basically represent one of the features common to much of organizational thought over the last few years (see Cyert & March, 1993, pp. 214-46).

3. HISTORY OF THOUGHT: REFLECTIONS ON THE "CASE" OF ACCOUNTING Ansoff's cited reconstruction of the evolution of planning and strategy systems speaks volumes about the scant attention paid by American management academics to the history of thought. The 4 For a description of this approach, see the issue of AOS devoted to "New Accounting History" and the previously cited introductory essay by Miller, Hopper and Laughlin 1991; see also the special issue of AAAJ on "Accounting History into the Twenty-First Century", in particular the essays by Carnegie and Napier 1996; Funnel, 1996; Jones 1996). Also see the incisive abstract of the paper by Miller, Hopper and Laughlin (1991, p. 395): "Over the last decade accounting history has changed significantly. This change entails both a pluralization of the methodologies and a change in the position of history within the discipline of accounting. The extent of this change is held to entitle us to speak of the 'new accounting history' as a loose assemblage of diverse research questions and issues. It involves attention to a variety of agents and agencies, the conditions of possibility of transformation in accounting knowledge and practice, the institutional forces that shape actions and outcomes and the rationales that set out the objectives of accounting. The new accounting history is located in relation to changes in the discipline of history itself, and is held to have implications for the current burgeoning of interest in 'field studies' of accounting".

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

7

crucial importance of such a perspective becomes strikingly apparent every time disenchantment sets in with the latest in the succession of constantly ebbing and flowing fashions (down to the fall of the "American myth" of Bob Locke, 1996; Engwall, 1998; Carmona). The relevance of a history of thought perspective is further underscored when interactions occur between academics from different backgrounds (in terms of country as well as of discipline, given that the latter is frequently defined by the former). Yet in this writer's experience, the crucial importance of studying the history of thought must not be misunderstood. Perhaps more than to appreciate variations and differences in managerial practices, its utility lies in grasping the peculiarities and idiosyncrasies of different academic communities, of particular social routes to disciplinary construction. Such processes occur in a "scientific marketplace" that is beset with frictions and barriers that undermine the permeability and clear functioning that would be taken for granted by models of "perfect competition".

In this sense the history of accounting constitutes what is perhaps an exemplary case (and the distance itself between accounting and other management studies “subfields” tends to be a socially constructed issue). It is worth briefly recalling some of the points that emerged from a previous piece of research (Zan, 1994; see also the extensive bibliography, which contains references I shall not duplicate here). For whereas the last few years have seen the gathering of a relatively widespread awareness regarding the specifically national characteristics of contemporary accounting thought, what is bewildering is the gulf and incomparability between accounting historiographies, different in periodization, in the writers that are known and deemed interesting, and in the issues they address. It is as if one were looking at the histories of quite unconnected disciplines. On the positive side, however, one might say that this situation – which is rarely encountered in any other field – is itself an engine for theoretical pluralism. Indeed, the history of how different communities of academics recount the history of thought itself provides a description that is much more complex and nuanced than that which each individual historiography is capable of supplying. Further than due to methodological or epistemological differences, this is above all the plain consequence of reciprocal ignorance.

Considered in this way, the Anglocentric view betrays a sort of “cultural imperialism”, where the inevitable reference to Paciolo and occasionally to some other sixteenth or seventeenth century Italian author goes hand in glove with unalloyed ignorance as to the development of Italian accounting and its related historiography. Indeed, it is not just Italy, but the whole European continent, that remains, “cut off by coastal fog”. In contrast with historical studies in general, almost all accounting historians are, in the strictest sense, English speakers, and bibliographies in this field are also crammed almost exclusively with papers and books in English. An art or music historian could never get away with such a display of "arrogance".

If, under these circumstances, the markedly autarchic character of Italian accounting historiography is not all that surprising, it is by means of a comparison of the different narratives that one can identify areas that reveal points of weakness, above all as regards methodology. Some comments on this tradition are here introduced – though perhaps the very existence of such a literature may be ignored by not a few of English speaking accounting historians (Zan, 1994), not to say by other management scholars (cf. also Zambon, 1995).

A critical assessment of the Italian historiography from an international standpoint Drawing on the above revisiting of management and accounting literature, the first weakness of the Italian historiography that emerges is the reductionism in assuming an unproblematic relation between practices and theories, which is particularly curious, given the history of the spread of double-entry bookkeeping and the lengthy genesis of accounting theories. Yet in fact (with the exception of Besta, 1922, and some of his pupils) the history of Italian accounting is largely a history of thought and of the relevant literature as it evolved from Paciolo onward. Without

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

8

wishing to detract in any way from that literature, what is striking is the absence of any systematic investigation of accounting practices even by those (like Melis, for example) who brought formidable scholarship to bear upon the accounting practices of periods "prior" to the existence of an accountancy literature. Indeed it is almost beyond comprehension that, while asserting the superiority of practices over period literature (Melis, 1950), from 1497 onward it is the literature alone that is recounted. It is hard to track down precisely what practices were in use, to trace for example the emergence of depreciation or costing (as a practice, whether or not it preceded its theorization). Above all it is hard to uncover any far-reaching investigation into the period that holds the greatest interest for international debate, i.e. 1800 to the present day.

The second point that comparison with other historiographies serves to highlight is the strong teleological connotation of the "precursors" metaphor that tends often to be invoked in Italy when reconstructing the evolution from the discipline of accounting (Villa, 1840-1; Cerboni, 1886 ; Rossi, 1882 ; Besta, 1922) to economia aziendale (Zappa, 1937). While, on the one hand, this connotation runs the risk of anachronism and of "penalizing" the meaning of individual contributors assessed with hindsight, it could, on the other hand, lead to end-of-history type positions, owing to the gravitational pull of "what happened afterward", i.e. the rise of Zappa-inspired business economics. If in principle it is fair to suppose that every author, however brilliant, tends eventually to be overtaken and that the end-of-history position is not therefore sustainable, in the case of accounting history this fails to grasp the specificity of Italian developments – by examining how they differ from other historiographical traditions. Indeed, it is very likely that a scholar from the English-speaking world would find the thinking of Besta (if they actually made the effort to familiarize themselves with it) much more accessible and congenial than Zappa’s. Bearing this in mind, it is arguable that spatial variation (different academic contexts in different countries) underscores the relativism of the question (i.e. the relativism in assessing and eventually opting for one of the two competing position, Besta's or Zappa's). Whether or not in agreement with the currently dominating position in Italian thinking (i. e. the superiority of Zappa’s thought) such a pluralist attitude would allow for a more fully conscious appreciation of the differences between alternative approaches. While avoiding simplistic dichotomies or polarization – a sort of “which side are you on” between Zappa or Besta, ignoring the existence of a richer range of schools and contributors, as described by Giannessi (1954) – a less dogmatic attitude would help to identify theoretical conflicts and discontinuities when these emerge.

Still in comparativist vein, the ethnocentric closure (i.e., how it occurs, beyond the fact that it does occur) that the history of Italian thought registers between the wars is strikingly relevant here 5. When, in an extremely interesting book (1947, p. 169), Onida writes about 5 The same ethnocentrism applies to the very term economia aziendale, which indeed brings out not only the risk of incomprehension ("concern economic " was defined as "awkward English usage" by Hopwood and Schreuder, 1984) but a further difficulty relating to the processes of "double translation", whereby the losses in terms of awareness are extremely perilous. If, taking a closer look, the concept of a "concern" is nowadays largely incomprehensible to academics in the field of management and accounting other than in the specific and more technical sense of the "going concern" assumption, the concept is perfectly easy to trace, having had a meaning very similar to that of "firm" in past current language. (The translator of this paper – whom I wish to acknowledge here – underlines this point, arguing in his notes that Websters International glosses "concern" as "firm". In addition, he suggests, “if one looked at the young Daniel Defoe's economic journalism (early 18th century), one would find this word on many pages, used in this precise sense. The etymology is no accident and speaks of early puritanical capitalism: one's moral ‘concern’ was also supposedly the business of one's livelihood’”.) Old American institutionalism also used such a notion, and Zappa's thinking is indebted to this institutionalism in a consistent and quite explicit way (Panozzo, 1997). However, there is some danger of losing trace of this aspect which, indeed, other exponents of this school in later reconstructions failed to emphasize – that is to say, in the historical process of disciplinary "institutionalization". Looked at in this light, it is curious to note how the concept of "concern", when transferred and "trans-lated" into other linguistic and disciplinary contexts assumes meanings (firm) which, under the fertilizing effect of local debates, render any "back-translation" difficult if not impossible to understand (the "awkward usage" to which Hopwood & Schreuder refer). Bearing in mind a similar process of "forgetting by

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

9

Taylor – which he does without any particular sympathy – he "locates" him in relation to the economia aziendale literature: "A further notable branch of economia aziendale studies [literally: studi economico-aziendali], widely cultivated in Anglo-American thinking, regards the organization of labor and the search for more efficient methods and instruments for the management, performance and control of work within the company". This assertion, while on the one hand clearly demonstrating the power that the school had already acquired over the definition of disciplinary boundaries and connotations, rather naively discloses its distance from, indeed apparent incomprehension of, one of the greatest organizational and managerial breakthroughs to occur in modern times in the thinking but especially in the practices of management, that is the explosion of the scientific management phenomenon. This, however, is not a problem that affects this author alone, but rather the relevant Italian literature as a whole, if (as has been calculated) the name Taylor and the terms derived from or associated with it (“taylorism”, “organizzazione scientifica”, etc.), in the period between 1922 and 1944, receive a total of 8 mentions in the Rivista Italiana di Ragioneria, 3 of which occur in Masi's work (1921, 1922a, 1922b) and the other 5 in 5 different writers (Semeraro, 1929; Candeli, 1929; Lorusso, 1932; Arena, 1933; author unknown, 1933).

This awkwardness in taking on board innovations in practices is equally apparent in connection with another crucial "movement", the technique that, perhaps more than any other, marked the emergence of a broad-based managerial culture and ideology: financial ratio analysis. After all, from the 1920s onward, with the introduction of the DuPont system (but in fact even earlier, see Horrigan, 1968), financial ratios swept rapidly across the entire world (not just large corporations but also financial institutions, small businesses, soon reaching all students, not just those who attended American business schools: as for the Italian anomaly, see Toninelli, 1997). Again, rather curiously, amid other rare exceptions 6, there surfaced the "anomalous" figure of Masi who, as early as 1933, published a book on this subject (though in fact it was preceded by other publications by engineers). This was then followed by 30 years silence within the economia aziendale community of scholars.

The value of comparative historiography In terms of method, a comparison between historiographies can give rise to a number of interesting points. The process of making oneself understandable within quite different theoretical and cognitive frameworks necessarily entails a diversification and broadening of awareness and knowledge. Considered in this way, the "history of accounting histories" proves to be an interesting field of investigation with possible repercussions both in terms of historical narratives and interpretations and in terms of a heightened understanding of the difficulties that can be thrown up by more far-reaching processes of harmonization including in the field of accounting, as a result of the legacy and relative inertia of the structures of thought in different countries (on this point, see also Carnegie & Napier, 1996).

Whether in terms of analysis, content or the stance demanded of the scholar, this comparative effort is anything but straightforward. In a sense, there is a parallel here with the theory of markets, where extreme positions are easy to argue (perfect competition and

doing", it would be interesting to investigate what was left of the American institutionalists' original concept once it had emigrated into the field of American accounting (for a preliminary, albeit unsatisfactory, reconstruction, see Covaleski, Dirsmith and Samuel, 1995); and, working in the opposite direction, what an economist (however old-institutionalist and American) would make of the new meanings that have enriched, and simultaneously impoverished, the old term (interesting enough Leathers & Raines, 1991, have argued that Commons' thought was strongly influenced by Italian thinkers, but rather unexpectedly the reference was to Giuseppe Mazzini). 6 Searching through the titles of papers published in the 1921-44 period by the Rivista Italiana di Ragioneria for Italian or English wording connected to ratio analysis, only two titles came up: Giannessi, 1937; Colombo, 1928.

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

10

monopoly) whereas, if one strays from such extremes, the less clear-cut and deterministic but more interesting paths of oligopoly analysis begin to open up. In the case that interests us here, confronted with the consistent articulation of thinking, historically and historiographically, in national traditions which, in spatial terms, are by definition self-referential, and faced too with the ongoing breakneck expansion of one of these traditions at the expense of the others, rather than retreat to the extremes to defend the purity of one's local tradition or, alternatively, accept passively and a-critically the currently dominant traditions of the English-speaking countries (by no means free of cultural imperialist attitudes), one can instead go down the comparativist road, embracing theoretical variety.

4. MANAGEMENT AND ACCOUNTING PRACTICES: TWO ARCHIVAL RESEARCH PROJECTS It is not within the scope of this paper to develop a systematic literature review of the work done from a historical perspective on company practices by accounting and management academics. It is merely worth stressing here that even in the last few decades such research has been undertaken prevalently by accounting scholars, in particular following the interesting innovations of new accounting history (Miller et al, 1991 and Carnegie & Napier, 1996; AOS, 1991; AAAJ, 1996; CPA, 1998). More generally in fact, despite the broad-ranging and keen interest in processual approaches and longitudinal investigations in management studies as a whole, these tend to produce reconstructions or company histories over relatively limited time spans – the literature on strategic change is typical in this regard. Historical views by organizational scholars tend on the other hand to focus on the evolution of ideas (e.g. Bonazzi, 1982) 7.

Instead I shall focus here briefly on the findings of two pieces of research – into the Spanish Royal Tobacco Factory and the Venice Arsenal. These seem of particular interest as "applications" of specific management and accounting skills to historical investigation. Moreover, both are the work of a network of European academics straddling the fields of management and accounting in historical perspective 8. The Royal Tobacco Factory The article by Carmona, Ezzamel and Guttierrez (1997) is the first fruit to spring from the research project into the Royal Tobacco Factory. It focuses on the analysis of the accounting and control system that was introduced into the organization in 1773. One of the most important

7 As I pointed out elsewhere (Zan,2001), the dynamics of journal Management History is rather telling about the problematic status of history within the field: “‘The Journal of Management History is the first to offer a specifically academic assessment of current management trends in the light of the contributions made by major thinkers in the field. …[It] critically evaluates the backgrounds, ideas and influences of the major contributors to management thinking …By placing contemporary thinking in a historical context, management theorists and academics gain greater understanding of the roots of new management concepts and how they are developed in response to social, economic and political factors” (cf. http://gort.ucsd.edu/newjour/j/msg02375.html , emphasis added.) Curiously enough, more recently this journal has merged into Management Decision (cf. http://www.emeraldinsight.com/jmh.htm), though a sense of history is difficult to be found in the characterization provided to that journal: ‘The rapid changes in the business environment brought about by technological innovation; socio-cultural development, economic fluctuations and other factors have demanded new answers, innovative approaches and fresh thinking. Management Decision has consistently provided a ready and informative source of all these elements’" . 8 Cf. the series of EIASM workshop on the topic: Bologna 1996; Seville, 1999; Lisbon, 2002. Cf. Jones, 1997.

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

11

primary sources has been a fully-fledged "control manual" started that same year and entitled the Instrucción Sobre Costes.

Manufacturing presented a series of processes articulated in appropriately codified stages and differentiated by product, i.e. snuff and cigars. The control systems took the form of a series of instruments for the physical monitoring of the materials (in order to prevent the theft of precious raw product, the trading of which was, besides, strictly regulated), as well as for costing. In particular the cost accounting system had a bewildering structure based on cost centers (casillas), which gave rise to calculations of the cost of transforming the products, as is fully described in the instruction manual of 1773 and reported by Carmona and colleagues. Working from other primary sources, their article also describes an interesting example of the way in which information on cost was exploited to optimize manufacturing processes and to increase production and productivity, on the basis of a month-long experiment that was successfully conducted in 1778. This indicates a very concrete use of the cost figures that the cost control system generated, with a strong efficiency-oriented, almost "scientific" drive. Some of the experiments conducted in order to reach what one would now refer to as "make or buy" decisions are also highly interesting.

This extremely modern system of costs and control as well as the related and also highly advanced managerial practices have numerous points of considerable interest. A more detailed description is provided in the article by Carmona et al; here I shall just reproduce some of the points raised during discussions on an earlier draft of the paper (see Zan, 1999).

First, what is surprising in this multi-product company is the capability and sensitivity with which "internal differentiation" (to use Lawrence and Lorsh's term) is treated and managed. For example, differentiation between manufacturing processes led to a structuration in distinct stages and separate information pooling "centers" for snuff and for cigars, with costs calculated and attributed to the two manufacturing processes, according to the differing organization of labor involved. What is more, the close attention paid to internal differentiation is also apparent in the way that labor is managed with reference to subtle organizational aspects. Worker recruitment and hiring, for instance, were decided in accordance with varying criteria. For the production of snuff, where a simpler manufacturing process requiring less skill was involved, day labor was used. For the more complex process of manufacturing cigars, which demanded greater manual dexterity, workers were hired by the week. In today's jargon, the human assets specificity of the two manufacturing processes provided the underpinning for this shrewd differentiation in recruitment policies. This was also reflected in differentiation affecting payment systems themselves. Curiously enough, on the cigar manufacturing side, a team piece-rate was implemented which, moreover, was subject to the achievement of specified standards of quality, revealing a degree of sophistication worthy of today's control systems.

Second, what stands out is the pervasiveness and, at the same time, the selectivity of the control processes within the Compagnia. The confinement of managers' responsibility to matters of manufacturing efficiency (ruling out any assumption of economic accountability for the purchase of raw material) generated a costs system that was extremely responsive to information management requirements, and focused on transformation costs. Thus, in both general terms and at each separate level, the degree of consistency between tasks and control (of quality, quantities and costs) is indeed impressive and confers a strong "modern" connotation on the enterprise.

Third, the sophistication of the Compagnia's calculating practices serves similarly to characterize the entire gamut of the organization's managerial practices. It is curious, however, to observe the direct and concrete recourse made to "experiments" in assessments of the comparative costs of different alternatives, suggesting a limited capacity for abstract reasoning.

That said, the most interesting aspect here is not this set of sophisticated features but rather the spatial and temporal situation in which it took shape, i.e. in a publicly-owned company, indeed a state monopoly that was not open to competition, in eighteenth century Spain, a country as yet untouched by any industrial take off. Looked at in this context, the

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

12

examination of the control systems of a firm that pre-dates the Industrial Revolution, as is the case of the Royal Tobacco Factory, would appear to support the feeling that undue historiographical emphasis has tended to be laid upon the processes associated with the Industrial Revolution in the evolution of capitalist systems, and thus upon points of rupture rather than points of continuity, perhaps the consequence of a widespread "macro" vision. If, on the contrary, a "micro" vision is pursued – such as the insights allowed by a management studies perspective – the wealth of managerial practices and instruments strikes the investigator as slightly older and at least in part appears to constitute a precondition for, and a source of capitalist development itself. While “scarcely” pre-dating the industrial revolution in the case of the Royal Tobacco Factory or very much older in cases of industrial and costs accounting from the fifteenth and sixteenth century, this might have rather more devastating theoretical and methodological implications. The Venice Arsenal Partly based on points that emerged from research into the Spanish Royal Tobacco Factory – and which were discussed at a conference in 1991 – interest in the issues raised led to an ongoing research project into the Venice Arsenal, conducted with some colleagues (Hoskin, Zambon, Zan, 1994; Zan, Zambon, 1998). While not wishing on this occasion to address our findings analytically (for a preliminary reconstruction, see Zan & Hoskin, 1999; Zan 2003), this does seem a good opportunity to outline the grounds for interest in such research, the kind of phenomena upon which it can shed light as well as certain of its main theoretical and methodological implications.

In my view, the reasons for engaging with this rather unusual topic did not lie solely in an a priori historical interest in the relevance of managerial accounting practices for economic development. Indeed, to return to the point made above, if one takes on board the importance of a relative separation between practices and theories, the need "to get one's hands dirty" in the study of accounting and managerial practices (as opposed to theories) becomes quite unavoidable. Moreover, facing major theoretical issues of academic debate (for example, the concept of strategy and everything that turns upon it), an attempt may be made to falsify concepts and theories by applying them to a variety of either spatial situations (for example, to anomalous organizations, where economic and managerial discourse encounters particular difficulties in making itself understood or just gaining acceptance, as for example with museums or other non-profit organizations) or temporal situations, possibly even by "playing" on the concept of strategy or other current constructs in order to gauge to what extent they represent categories that are indissolubly linked to present-day characteristics and phenomena (see Ansoff's "turbulence"). Such attempts at falsification should in any case contribute towards a clearer grasp and awareness of theoretical and methodological issues of current debates.

If this holds true in general terms, the choice of the Arsenal as a research project has a crucial and substantial motivation (Hoskin, Zambon, Zan, 1994). Given the body of law overseeing the functioning of the Venetian Republic, regulations that applied to the industrial construction of galleys at the Arsenal as well as many related decisions were the subject of deliberations and other formal documents that were then kept as records. This has had a twin-effect that has made the said records a unique research opportunity. First, of course, is the fact that the relevant documents have been conserved. But above all they constitute an early example of the emergence of a management "discourse". It was necessary not just to manage but also to "talk" about the management process, to articulate verbally what was being done as a normal matter of course, to construct concepts, ideas and abstractions on the operations undertaken. Moreover, it was necessary to write about them. This constitutes an early example of separation between practice and conceptualization or, in other words, the emergence of a discorso sul

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

13

maneggio as Drachio termed it in 1586 9. And, indeed, what is being uncovered is of vast interest, though it is important to stress that while our research has brought to light some new sources, the bulk of our findings are simply the product of reading the already existing literature on the Arsenal from an accounting and management studies perspective.

Within a broader process of internalization of the construction of military galleys at the Arsenal, – which had begun in the first decades of the sixteenth century, transforming the Arsenal into one of the largest manufacturing centers in the world at that time, employing thousands of workers, the victory at Lepanto had a number of very far-reaching consequences. For, ironically, the victory highlighted the critical importance and unreliability of the Venetian war machine. Having destroyed and confiscated what remained of the Turkish army, within a short space of time Venice was facing a Turkish army even stronger than before. This prompted the decision to create a reserve force of 100 light galleys and 12 extra-large ones, to be kept in a state of war-readiness (see Lane, 1978).

Indeed the Arsenal faced serious problems in managing the production process and it is plausible that these were aggravated by the hugely increased need for coordination that the production "for stock" of such a large reserve of ships entailed. Moreover, the literature (Lane, 1934; Davis, 1992) contains clear signs of the emergence of specific initiatives aimed at restructuring the way that the Arsenal was managed, on the basis of indications from two "professionals", Tadini and Drachio. There are varying opinions on the outcome of these interventions. Lane expressed an optimistic (and simplistic) view, seeming to regard the problems as having been solved merely because they had been identified (once again collapsing managerial thought and action). This, however, is countered by the negative view advanced by Concina, who goes so far as to assert that "administrative skills seem to be lacking" (Concina, 1984, p. 175), thus underestimating the historical problem posed by the construction of the administration itself in a modern industrial complex.

Given this framework – and keeping in mind the problematic nature of the relationship between "saying and doing" in the field of business, our research has analyzed in considerable depth the contents and meanings of the strategic manufacturing reorganization schemes, relating them to preceding conditions and attempting to assess their impact. To this end, we have reconstructed the evolution of a sort of "reporting system" that consisted in the periodical reports presented by advisers (savi) and supervisors (provveditori) (for detailed information on the primary sources, see Zan & Hoskin, 1999, the findings of which are reviewed below). We have analyzed developments in the contents of these reports in terms of appraisal, detailed examination and the identification of issues concerning the organizational of the manufacturing processes undertaken at the Arsenal, while also studying the emergence of lines of argument and considerations of an economic-accounting nature.

To be more precise, discursive regularities and shifts traceable in these documents have been sought, carefully distinguishing between the early documents (1580-6), pre-dating the contributions made by the two "professionals", and the later ones (down to 1646). What one finds is a sophisticated awareness of manufacturing processes and the issues relating to their organization. What stands out is a widespread and ongoing discussion of management problems relating, for example, to the sourcing of materials, the availability and discipline of the labor force (regarding both appropriations of materials and levels of attendance and industriousness or, in present-day terms, absenteeism and productivity), the conditions under which manufacturing processes were undertaken in terms of both production levels and organization (in particular, discussion on decisions on contracting-out and work discipline and control).

9 Baldissera Drachio, Ricordi intorno la casa dell'Arsenal, 1586, P.P.A., b. 533. Apart from the coincidental Foucaultian flavour of the expression "management discourse" (discorso sul maneggio), since reference has already been made to the problems of "double translation", it is worth recalling that it is from the Italian term "maneggio" that the English term "management" derives.

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

14

Revisiting the Drachio and Tadini documents – already familiar to economic historians – one cannot but be strongly impressed by the marked air of understatement with which such documents are handled in literature on the Arsenal.

The earliest case (Drachio, 1586) represents a clearly worked out and systematic reorganization proposal implicating different levels in a coordinated plan, the whole scheme permeated by a performative principle that viewed an implicit notion of efficiency not as a tool for maximizing economic "returns" but as a moral imperative for the safety and prosperity of the Venetian Republic. Examination of the organization of production and logistics touched on a variety of different matters, including the best techniques and methods for cutting, shipping and storing timber. The crucial issue of component standardization was then discussed, with a call for the creation of a "common timber" to overcome the individual character of the component design and construction process (hitherto entrusted to each single craftsman), in order to move away from a "workshop" model of organization in boat production. Attention also focused on redesigning the manufacturing plant's lay-out in order to make a more rational use of space, in line with the demands of production. The issue of labor organization, to use present-day terminology, was addressed, on the one hand, with a definition of task-specific work teams and, on the other, with detailed debate on procedures for monitoring work attendance and performance. Lastly, the overall organizational structure was discussed and a proposal for a single top-level structure, endowed with significant powers, was put forward.

In some respects, the proposals made by Tadini (1593, 1594), with their attempt to impose discipline on the workforce and render it "governable", were even more far-fetched. Tadini argued that an effort should be made to eliminate unevenness in the day-to-day availability of workers, which undermined any attempt to manage production economically. In an effort to involve gang bosses, what was suggested was a sort of half-yearly productivity target with related incentives (corresponding to approximately 10% of "normal" wages). This was to be accompanied by a set of scheduling mechanisms covering the coming week, to be updated weekly after checking the extent to which the previous week's schedule had been fulfilled. While "middle-level workers" were offered the carrot, rather more repressive control regulations were suggested for disciplining the unskilled workforce, and a series of incentives for unbroken attendance, checks on attendance and devices for registering "movements" were proposed. These would even make it possible to check that an individual work hand was present and hard at work. Lastly, Tadini put forward a special ad hoc work team structure, to which was earmarked an annual budget setting out the savings to be achieved by the proposed structure.

The later period, until approximately 1650, saw a further sophistication of discourse on "maneggio", with organizational refinements, increasingly effective managing procedures and methods for governing the labor force. An example of this is the introduction of a method for measuring "work in progress" in man months. Also, forecasts and expenses relating to consumption materials became current as did calculations bearing on the workforce. The type of general complaints made during the preceding period gave way to calculative practices of labor needs that were based on "technical" parameters. Criteria were elaborated for reaching decisions on the restructuring of ships and on contracting out. To all of this was added a further new development: the systematic use of concepts and data regarding annual consumption and costs of materials, culminating with the astonishing document by Molin in 1633 (skillfully described by Forsellini, 1930) which presented the cost of manufacturing extra-large and light galleys.

To sum up, while a more detailed illustration of the results of our ongoing research will be available on another occasion, what has been demonstrated is the existence of a well developed managerial discourse, with a wealth of innovations of a modern kind relating both to accounting calculations (industrial costs as well as the more general process of book and account keeping) and also to management practices, designed on the one hand to discipline the work of subordinates and on the other hand to structure more effectively the organization of managerial work.

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

15

This provides further confirmation of the way that a "micro" view tends to put the clock back, in the search for antecedents and continuity in the development of modern management practices. In parallel, this shows the possibility of applying modern management knowledge and notion to previous periods as well. And, indeed, an explicit reference to current days’ literature on strategic change was needed in the discussion about management and accounting innovation and change processes at the Arsenal 10.

5. IMPLICATIONS AND CONCLUSIONS

While in terms of history of thought one is simply left with the idea of the need to fulfill the lack of contribution in the literature, in terms of practices the case of the Venice Arsenal (and to some extent that of the Spanish Royal Tobacco Factory too) makes it possible to develop a number of far-reaching implications for historical understanding of business evolution, from a management studies perspective. Recalling what was said in the introduction, these implications apply at three different levels at least: in relation to a number of the dominant approaches in the literature of business history; in relation to a number of issues specific to accounting history; ; and, thirdly, in relation to particular ideas regarding the nature of management studies seen – themselves – in historical perspective. 1. Though admittedly from the standpoint of "outsiders" (i.e. not as business historians) it nonetheless seems reasonable, on the basis of Zan & Hoskin (1999), to point to a number of basic limitations in the kind of approach that was adopted by Chandler, which potential diffusion in the management field (see for instance Johnson & Kaplan, 1987).

The first limitation of this approach is its Anglo-centric vision which means that it tends to perceive the emergence of administrative coordination in nineteenth century America because it simply knows nothing about previous (European) history. This bias is even graver if one recalls that, as early as the 1930s, Lane's work on the Venice Arsenal was available in English, supplying a further example of "forgetting by doing" processes in the academic community (nor does Forsellini's work appear to be well known beyond a small circle of Venice scholars ). Actually, the Venice Arsenal is an example of "administrative coordination", a modern form of organization permanently devoted to manufacturing, in Europe, approximately 300 years earlier. If nothing else, the Royal Tobacco Factory confirms that the Arsenal was not an exceptional case. Even if it provides no basis for any claim to statistical significance, it does serve to point research in a specific direction and, as they say, "if you don't look, you won't find".

A second limitation – assuming it is not in fact an ideological foible – is the firm-centrism (Zan, 2003) that dominates the literature of business history, wholly absorbed with the analysis of this kind of economic unit, as if to imply that it was the development of the firm that generated economic innovation and development. Regrettably for such a hypothesis, if one takes the trouble of consulting the records, one soon discovers the extraordinary role played by "non-profit" organizations (or organizations that are other than firms, as for instance the sections and offshoots of pre-nineteenth century European bureaucracies) in development and innovation, even in managerial innovations. This point holds not only for the Venice Arsenal but also for

10 “Though the strategic content of any proposals (as well as the organisational context) at the Arsenal is unlikely to have much in common in substantive terms with what is generally discussed in current strategy literature, a judicious use of such work can help making sense of the new wider dynamics of what get said and thought within and around this organisational space. This also allows one to import the interactionist perspective focussed on the interplay between the ‘actor and the system’ or the calls for a dialectical tension between deterministic and voluntaristic assumptions in organisation theories, thus enriching what is usually approached by new (and old) accounting history” (Zan, 2003)

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

16

other state-umbrella bodies, as is confirmed by the incredible management control system implemented by the Royal Tobacco Factory as early as 1773 and by the introduction of the notion of standards into the Springfield Armory (Chandler, 1981, pp. 154-9; Hoskin and Macve, 1994).

A third limitation, finally, lies in the economistic nature of the explanation that ascribed organizational innovations and, crucially, the very creation of administrative coordination to the need to economize on costs and achieve economies of scale in new production plants. The research findings on the Venice Arsenal might be put to amusing use in refuting a good few of Chandler's statements; for example: "The modern multi-unit firm took the place of the traditional model when managerial coordination made it possible to achieve greater productivity, lower costs and high profits than through market coordination" (Chandler 1981, p. 49); "The modern firm made its first historical appearance when the volume of trade reached a level at which managerial coordination became more efficient and profitable than coordination through the workings of the market" (ibid., p. 51). The following, succinct expression of Chandler's outlook is revealed as particularly threadbare, bearing in mind the Arsenal research: "Given the small size of firms prior to mid-nineteenth century, specialization would remain confined within the company circle. The business would be run by the proprietors, while the need for the thorough and meticulous internal organization, detailed statistics and cost calculation methods, which were to become such a marked feature of the modern firm, was not yet felt" (Chandler, 1980, p. 20). For in actual fact the Venice Arsenal presents no economies of scale. Rather than any need to economize, what propelled the development of an accounting and managerial discourse was managerial complexity itself, in relation both to sheer size and to the need for coordination. This had grown exponentially with the decision to maintain a reserve of 100 galleys, with all the logical and timing intricacies that this entailed. After all, even today, with the benefit of concepts such as the bill of materials and reticular techniques such as CPM and Pert, the job of managing such a business would be tough indeed. The Spanish Royal Tobacco Factory case also explodes many of the conventional explanations. For however counter-intuitive it may appear, what one is actually talking about is a company that is run as a monopoly, impervious therefore to competition, not profit-led, and located in pre-industrial revolution Spain.

It is curios, on the one hand, to discover that an epistemologically careful use of management studies and strategic management – despite their relative minor “status” (Whitley 1984b) – are useful in falsifying some basic understanding of business history. On the other hand, one could argue how dangerously management studies can re-import the same mistakes and misunderstanding of business history 11. 2. Regarding the various implications that the empirical cases reviewed above might suggest for accounting history, I would make just few points. First, it is reasonable to question whether, even referring to the Italian tradition of accounting (or economia aziendale), there is really anything so mould-shattering in the fact that the Venice Arsenal and the Royal Tobacco Factory were both non-profit-led bodies. The answer is that there is not. For, after all, the concept of the azienda, 11 It is curious to note how the Chandler’s picture is taken “as such”, without any critical assessment, in the following quotations from the well-known works by Johnson and Kaplan (1987): "Before the early nineteenth century, virtually all exchange transactions occurred between an owner-entrepreneur and individuals who were not a part of the organisation: ....transactions occurred in the market and measures of success were easily obtained. ....As a consequence of the Industrial Revolution and the ability to achieve gain through economies of scale, it became efficient for...owners to commit significant sums of capital to their production processes.... . The long-term viability and success of these 'managed' organisations revealed the gains that could be earned by managing a hierarchical organisation. ....The emergence more than 150 years ago of such organisations created a new demand for accounting information. ...(A) demand arose for measures to determine the 'price' of output from internal operations,....owners devised measures to summarise the efficiency by which labour and materials were converted to finished products, measures that also served to motivate and evaluate the managers..." (Johnson & Kaplan, 1987, pp. 6-7). For a critique see also Ezzamel, Hoskin & Macve, 2000; Loft, 1995; Ezzamel, 1994.

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

17

however problematical, well describes the economic unit in question and indeed sketches in some of its characteristics ("durable, dynamic, all of a piece"). In other words, it may be worth emphasizing that the charge of firm-centrism would not apply to the Italian tradition, given its focus on a wider set of economic organizations, the azienda (nor possibly to the German with the associated notion of Betrieb).

However, what is most immediately striking about the Venice Arsenal relates to "control". It is not so much the (albeit surprising) development of a sophisticated costing system to handle manufacturing processes of far greater complexity than those involved in the textile industry that seizes one's attention. What stands out is rather the emergence of an extremely modern management discourse, with broad relevance in terms of the allocation of some sort of economic responsibility and accountability for managerial tasks between the "principal" and their "agent" (right down to gang bosses level). Contrary to what is usually asserted, modern form of management accounting is in fact only a century or so younger than the spread of double-entry bookkeeping: in one way or another it has been around for 400 years. One cannot help being taken aback by the abyss that separates the case of the Venice Arsenal from what accounting history normally indicates to be the relevant period, the nineteenth century. Yet again the Royal Tobacco Factory emphasizes that the Arsenal does not present an isolated case, though perhaps it would also be wrong to portray it as widespread.

And if, following the Second World War, management accounting in Italy – along with business practices in general – apparently received a strong impetus from the influence of English-speaking countries, why were the historical antecedents completely mislaid, in terms of both theory and practices, until, say, a couple of decades ago? The relative backwardness of Italy's economic system and the family basis of Italian capitalism are the justifications that are normally brought in, arguing that, owing to this background, the conditions and demands that led elsewhere to the emergence of a modern discourse on management were missing. If what has been stated in relation to the Venice Arsenal is correct, it is not a matter of the failure of something to emerge but rather of the interruption of a process of development (or of development that followed other paths, perhaps spreading with the "Italian method" through seventeenth and eighteenth century Europe: a possible topic for future research). But, again, one cannot help wondering to what extent this umpteenth example of "forgetting by doing" relates to the academic world and/or business practices in Italy. 12

More in general, and considering the process of extension of management discourse to public sector all over the world, isn’t it curios to “re-import” from private sector notions and approaches that have been largely developed inside state bureaucracies centuries ago (as in the Venice case), but then followed by a similar process of “forgetting by doing”?

3. If much of this article has been devoted to interrogating the contribution made by management literature (broadly defined) to historical investigation, it is perhaps now worth explicitly turning the question briefly on its head. What implications might a historical perspective hold for the approach and conceptual framework of management studies, either as a whole or specifically in terms of "strategic" outlook?

What the Venice Arsenal and Royal Tobacco Factory cases do is roundly to refute Ansoff's hypothesis on the genesis of "strategic" management, as well as all the related explanations (as to how the concept of strategy or, more generally, how management studies developed). Such efforts proceed by casting "complexity" as a distinguishing feature of bodies in 12 One could argue to what extent did the development of schools (e.g. Zappa versus Besta) influence different approaches to historiography, possibly with an impact on processes of memory retention and disciplinary identity building, with regards to aspects of economic control. More crudely, if the battle of ideas had culminated in triumph for the positions championed by Besta (who defined administration as "the science of economic control") is it not possible that "mere" managerial practices might as a consequence have been the focus of greater academic attention and theoretical interest?

File: Zan=Perspectives on Strategy.doc , 15/08/2003 11:06 am

18

modern competitive economies (a position that has been labeled as "the presumption of hindsight").

Here too lies a radical rift with the whole literature dealing with so-called postfordism (see also Fontana, 1997). If complexity is a feature common to economic activity, the issue is how to contextualize it within the infinite gamut of shapes that it can assume, rather than to bisect the history of the world into two dichotomous epochs, “B.F. & A.F.”: before and after Ford. This is not to say that nothing can change or has changed in the life and history of organizations, just that change is always contingent on specific reality and indeed, as it were, constitutes it. And this is what gives usefulness to the notion of strategy itself as a sense making category, its function in highlightening the specificness of the individual firm or organization (Zan, 1990, 1995), making one questioning its own differences while educating to a notion of variety; dialoguing with analytical and relational complexity 13. While a renewed sense of history – in methodological terms – suggests the need to go back to the issue of change, on a more general level it could also be uses as a theory testing tool to weakening the dominance of the analytical approach (Toninelli, 1999; Zan, 2001).

If one then asks the question "what really have we invented?" in the management field, especially if one considers the furious development of research and managerial education over the last few decades, one is certainly tempted to declare that a sizable chunk of what is "new" is the wrapping itself and the mechanism by which "management discourse" has been packaged within the educational and academic institution. Another chunk is the rediscovery of what had been forgotten. And the rest is, indeed, innovation.

REFERENCES Accounting, Auditing & Accountability Journal, Special Issue on Accounting history into the twenty-first

century, edit by Carnegie G.D., & Napier C.J., 1996, Vol. 9, No. 3 Accounting, Organizations and Society, Special Issue on The New Accounting History, edited by Miller

P., Hopper T., Laughlin R, 1991, vol. 16, n 5/6 Ansoff H.I., 1984, Implanting Strategic Management, Prentice Hall, Englewood Cliffs (trad it

Organizzazione innovativa, IPSOA, 1987) Arena A., 1933, "Luci ed ombre del fordismo", Rivista Italiana di Ragioneria Arena G., 1973, “Sul contenuto della Storia della Ragioneria”, Rivista Italiana di Ragioneria e di

Economia Aziendale, Aprile, n. 4, pag 185-188 Astley W.G., 1984, "Subjectivity, sophistry and symbolism in management science", Journal of

Management Studies, vol. 21, no. 3: 259-272 Astley W.G., Van De Ven A.H., 1983, "Central Perspectives and Debates in Organization Theory",