PERSONAL FINANCE 101 brought to you by

Personal Finance 101 with WealthBar

Aug 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PERSONAL FINANCE 101brought to you by

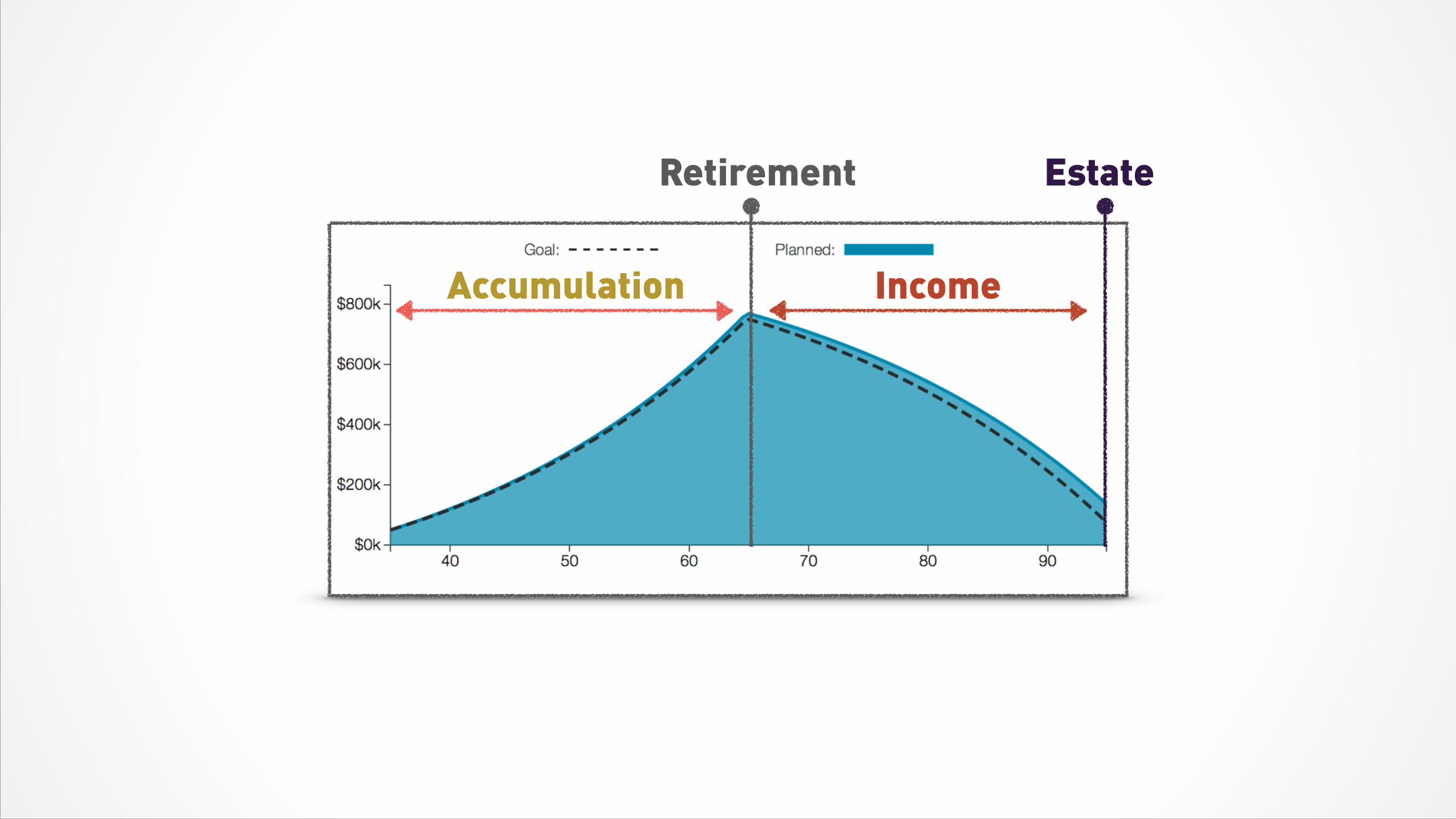

Accumulation Income

Retirement Estate

RENTING VS OWNINGWho will win?

http://www.qwantz.com/index.php?comic=1636

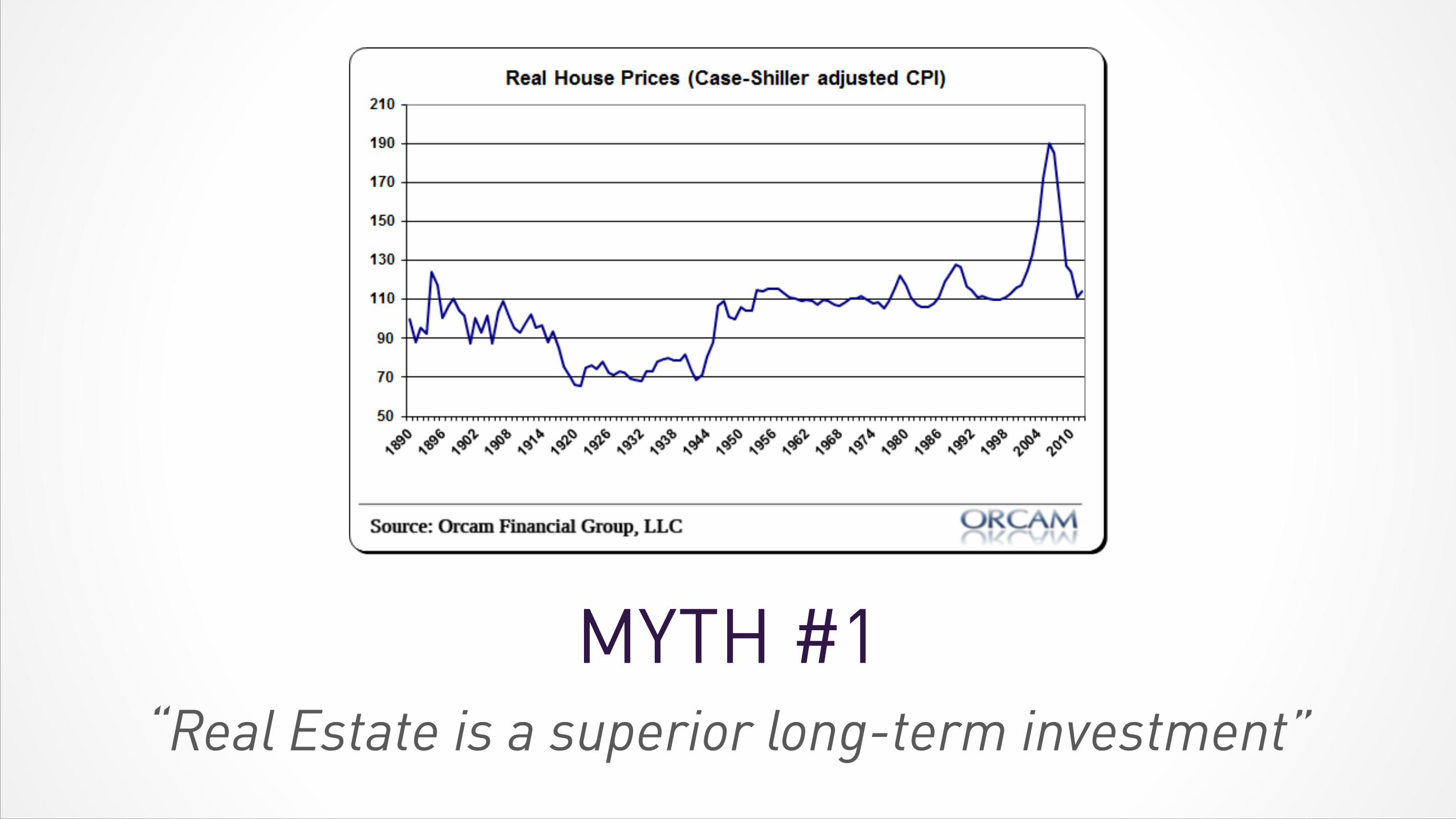

MYTH #1“Real Estate is a superior long-term investment”

MYTH #2“Paying rent is paying someone else’s mortgage”

MAINTENANCE

UTILITIES

MORTGAGE INTEREST

STRATA FEESTAXES

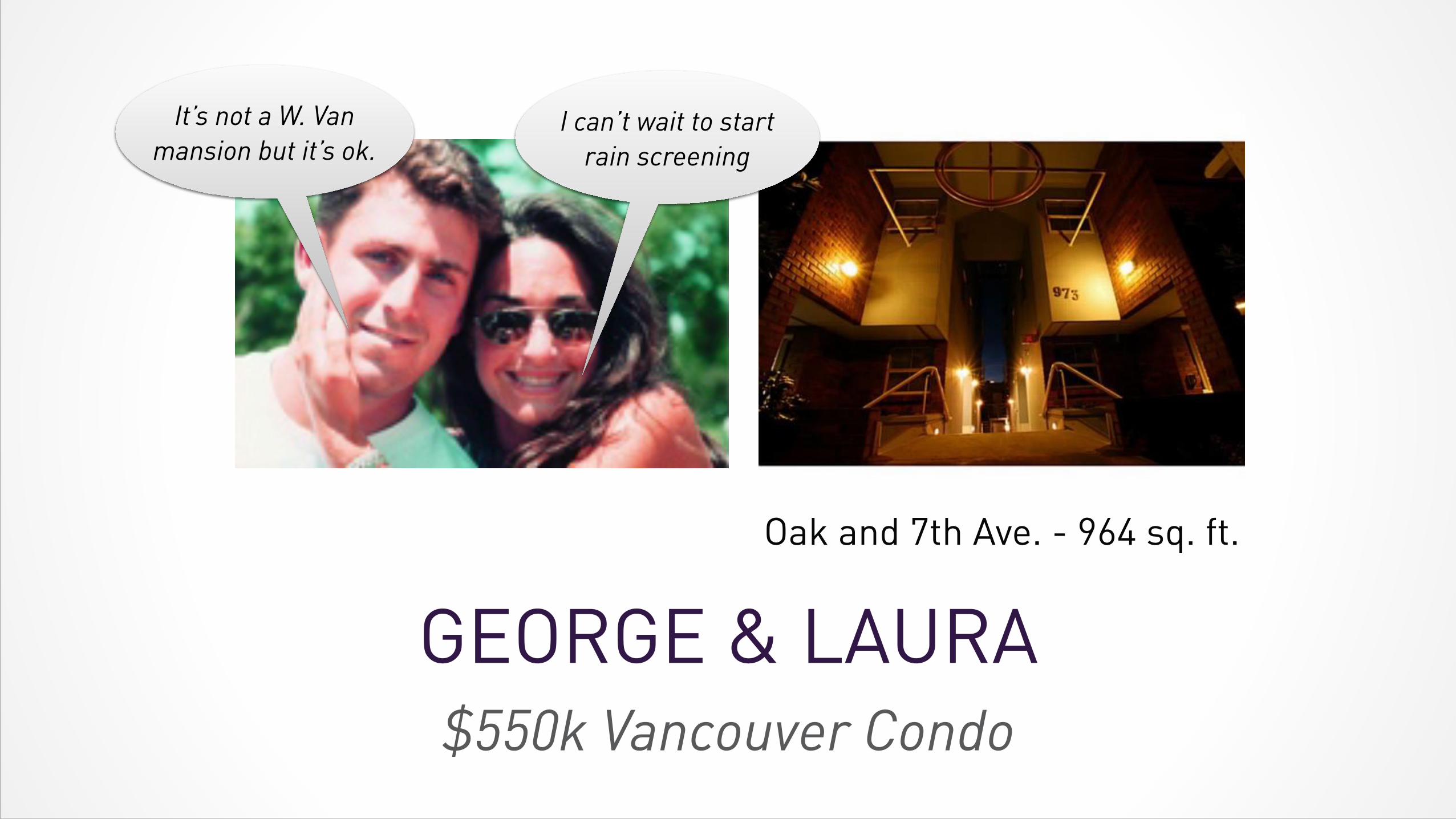

GEORGE & LAURA$550k Vancouver Condo

It’s not a W. Van mansion but it’s ok.

Oak and 7th Ave. - 964 sq. ft.

I can’t wait to start rain screening

GEORGE & LAURACosts of Housing

Downpayment $110,000

Monthly Costs $2,950

Closing Costs $14,000

Appreciation ~3%/yr

Comparable Rental $1,800/mo

Investment Return ~5%/yr

GEORGE & LAURA10 Years Later

Owning Renting

Home $740k

Mortgage ($302k)

Closing Costs ($29k)

Investments $383k

Total $409k $383k

Difference $26k

INSURANCEWhat is it good for!?

http://www.qwantz.com/index.php?comic=1349

WHEN YOU NEED INSURANCE

Marriage

Children

New Home

WHY YOU NEED INSURANCE

Covering Debts Replacing Income

HOW MUCH IS ENOUGH?

George Laura

Income $35,000 $90,000

Mortgage $440,000

Children None

Coverage $500k (T-10) @ $31/mo

$1,150k (T-10) @ $59/mo

ADVANCED NEEDS

• Tax owing at death

• Charitable giving

• Estate equalization

• Legacy

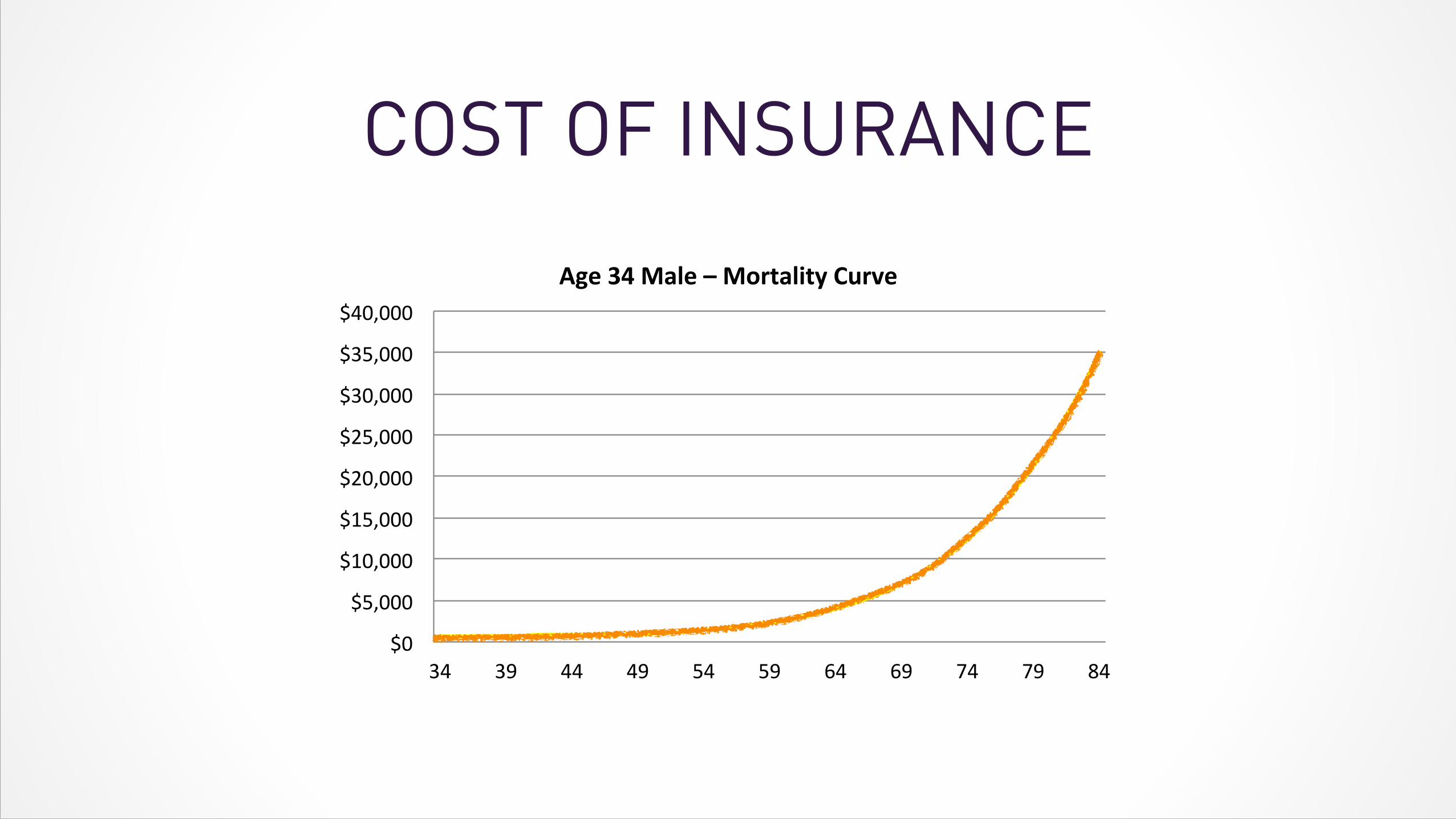

COST OF INSURANCE

Smoker Status

Gender

$$$ Size of Benefit

Health

COST OF INSURANCE

$0#

$5,000#

$10,000#

$15,000#

$20,000#

$25,000#

$30,000#

$35,000#

$40,000#

34# 39# 44# 49# 54# 59# 64# 69# 74# 79# 84#

Age$34$Male$–$Mortality$Curve$

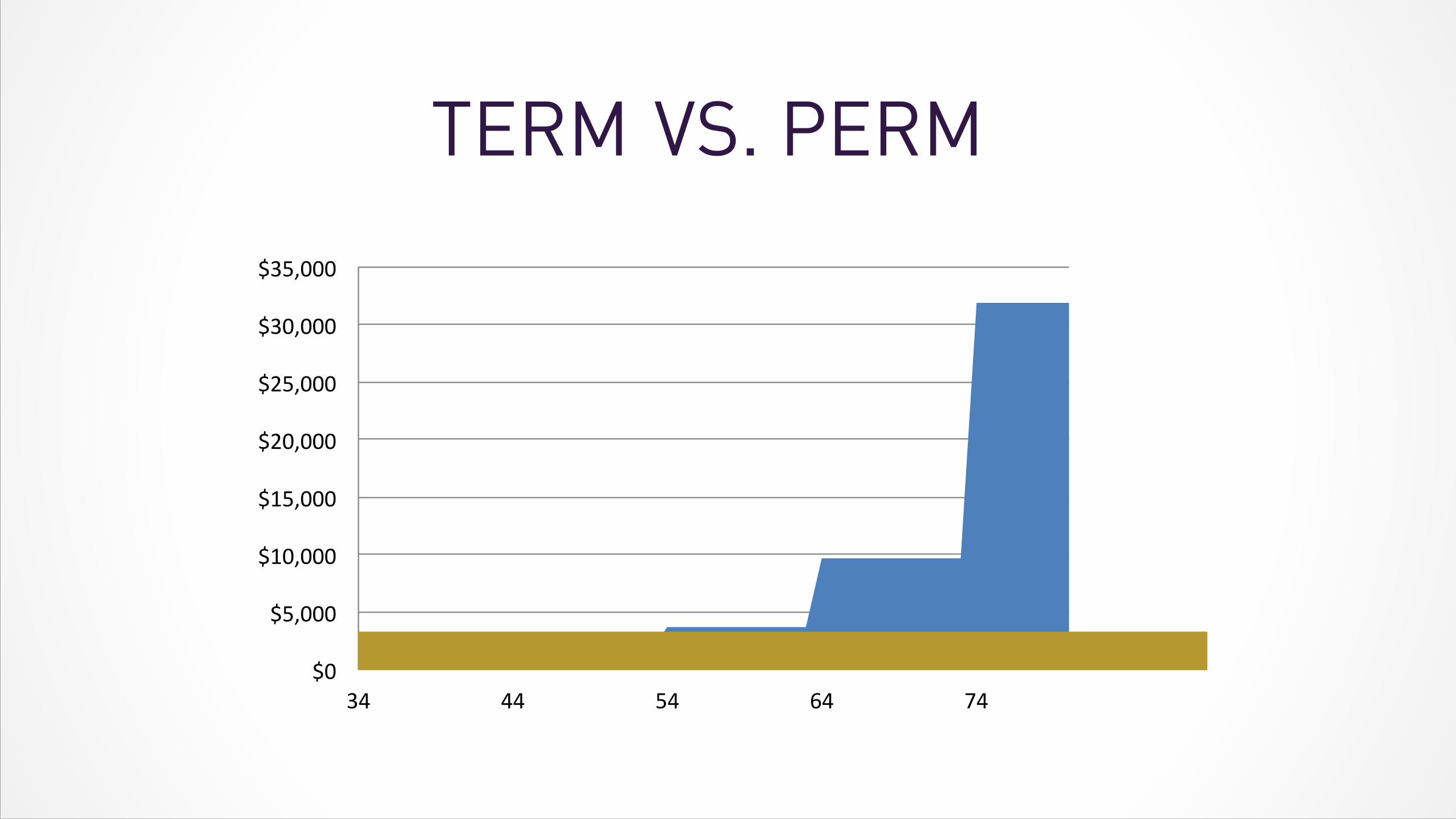

TERM

$0#

$5,000#

$10,000#

$15,000#

$20,000#

$25,000#

$30,000#

$35,000#

34# 44# 54# 64# 74#

VS. PERM

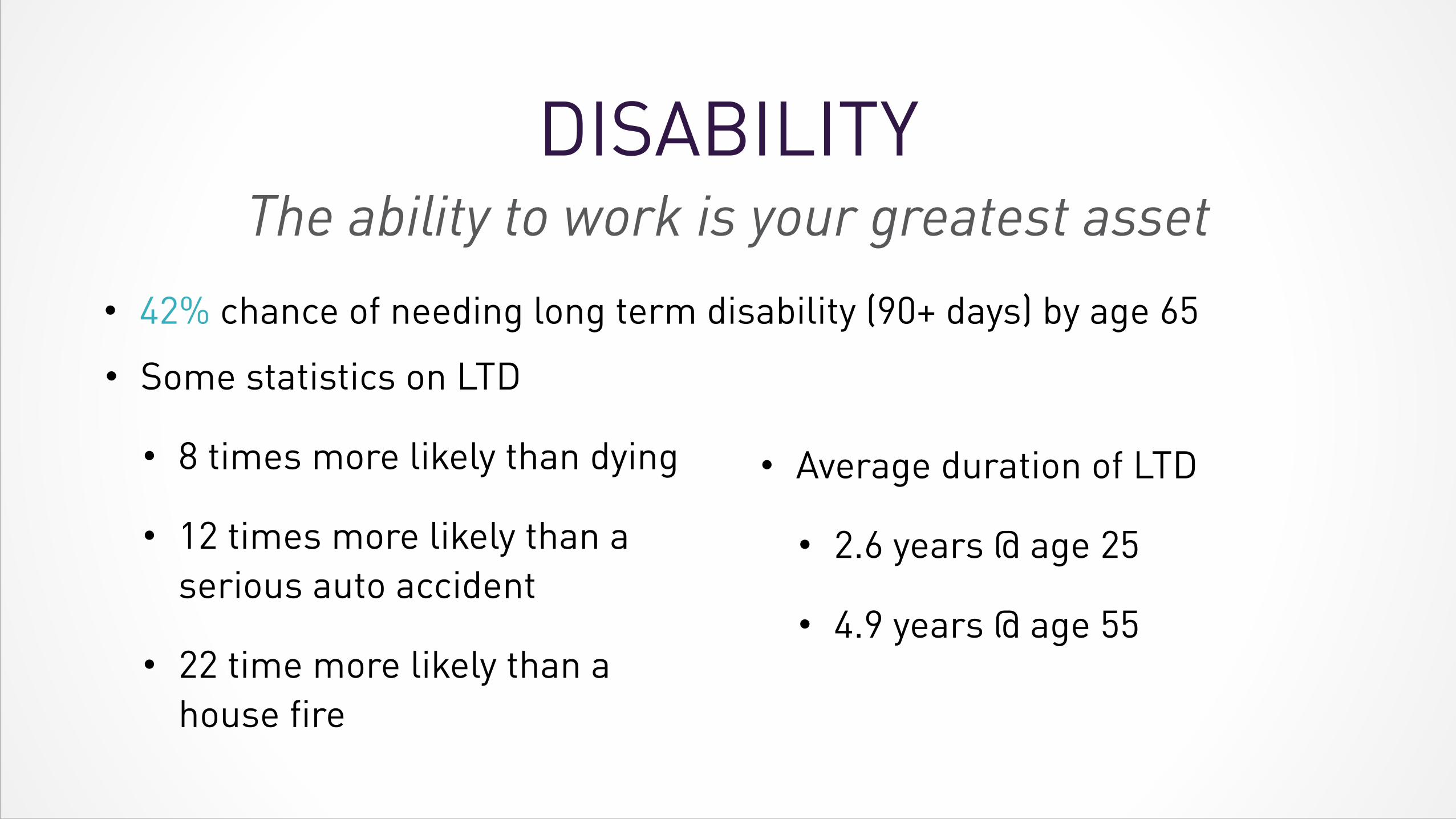

DISABILITY

• Some statistics on LTD

• 8 times more likely than dying

• 12 times more likely than a serious auto accident

• 22 time more likely than a house fire

• Average duration of LTD

• 2.6 years @ age 25

• 4.9 years @ age 55

The ability to work is your greatest asset• 42% chance of needing long term disability (90+ days) by age 65

GROUP DISABILITYNot always enough

• May be cancellable

• Premiums may not be guaranteed

• Regular or any occupation?

• Coverage is not usually transferrable to another job/company

THE PRICE OF ADVICEWho is your advisor and what do they do?

http://www.qwantz.com/index.php?comic=1076

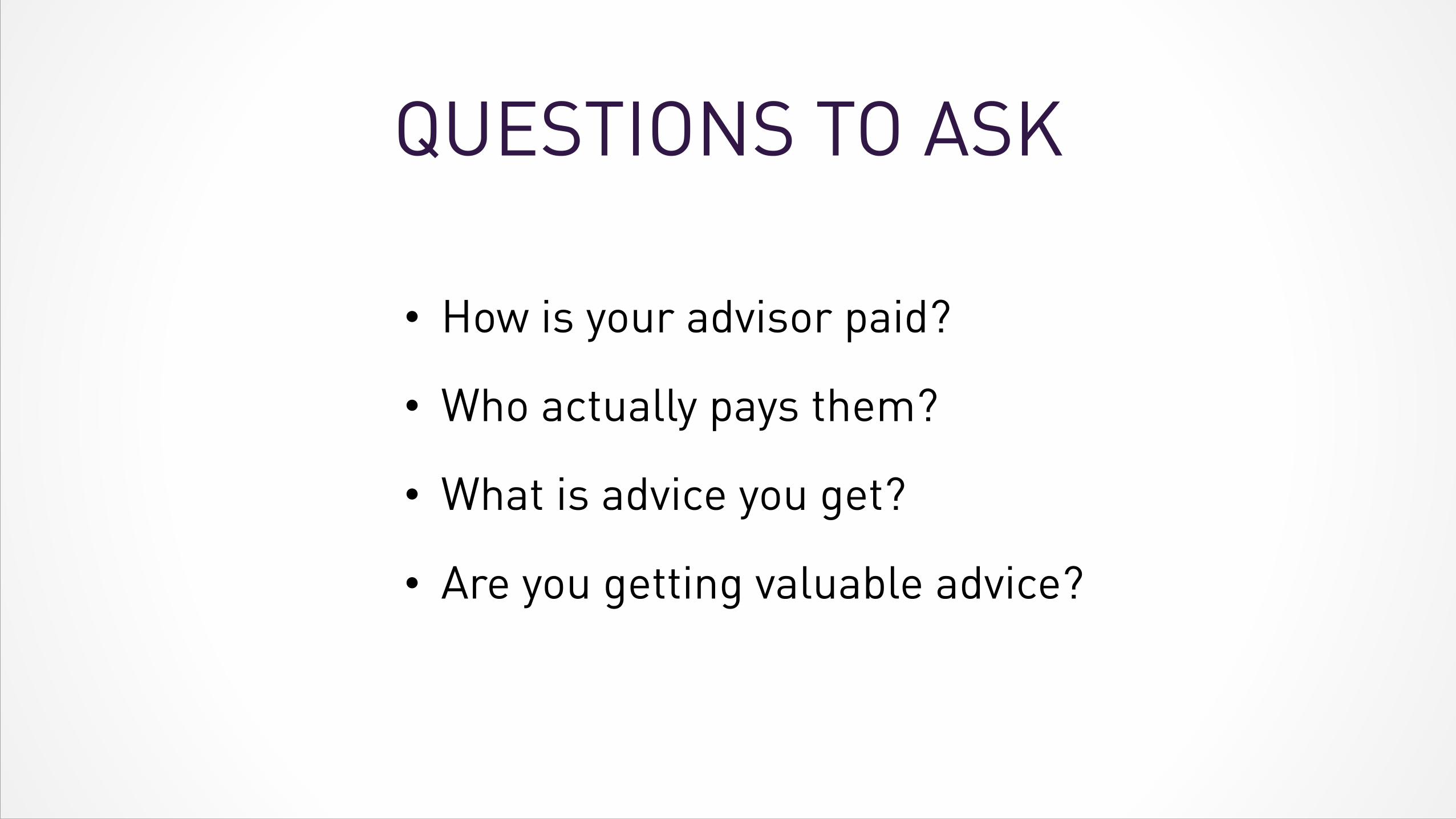

QUESTIONS TO ASK

• How is your advisor paid?

• Who actually pays them?

• What is advice you get?

• Are you getting valuable advice?

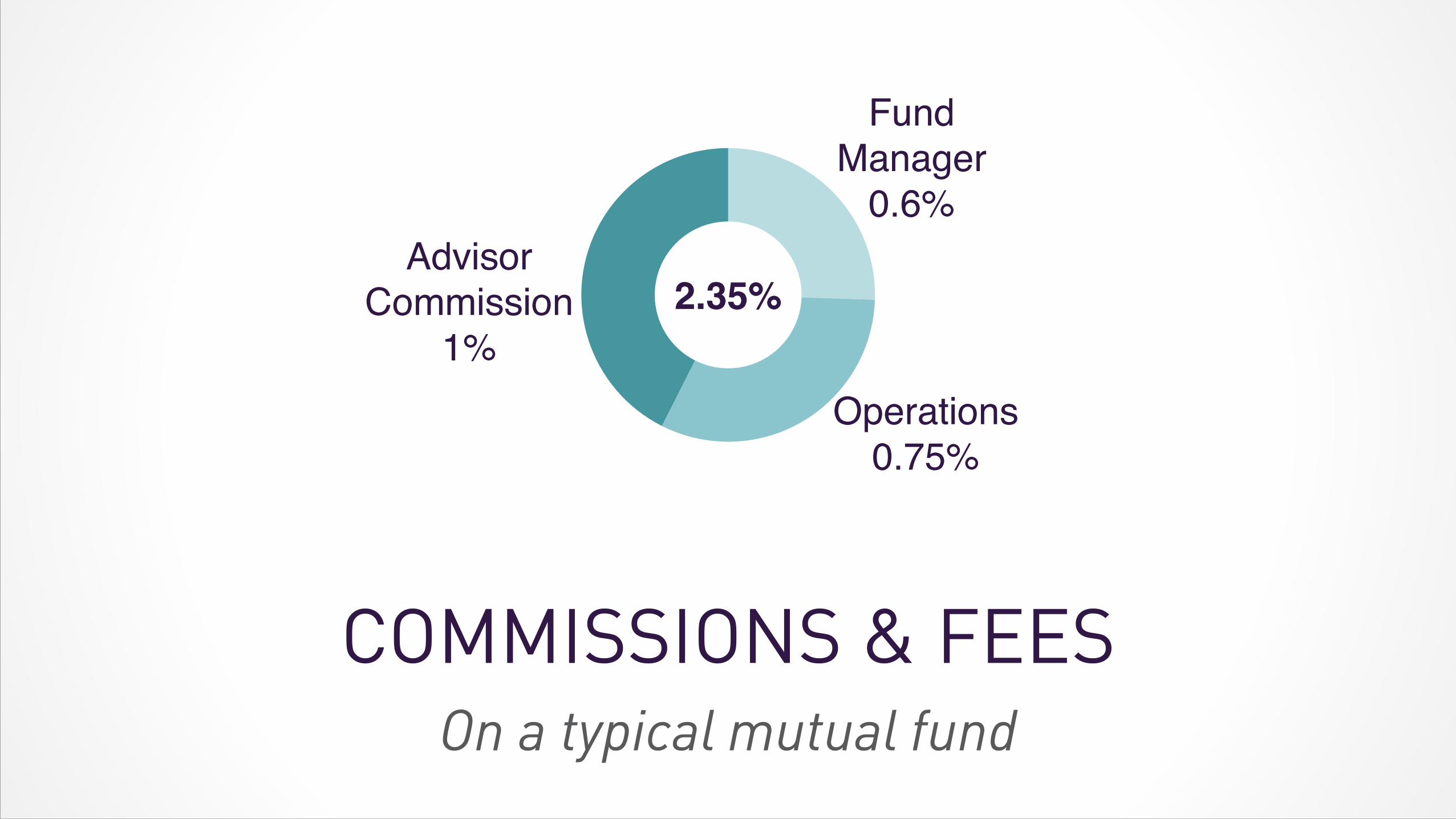

COMMISSIONS & FEESOn a typical mutual fund

Stocks 60%

Bonds 35%

Cash 5% 5% Cash

60%!Stocks

35%!Bonds

COMMISSIONS & FEESOn a typical mutual fund

Advisor!Commission!

1%

Fund!Manager!

0.6%

Operations!0.75%

2.35%

WHO WORKS FOR WHOM?Seeks advice

Recommends investment

Provides investment

and pays advisor

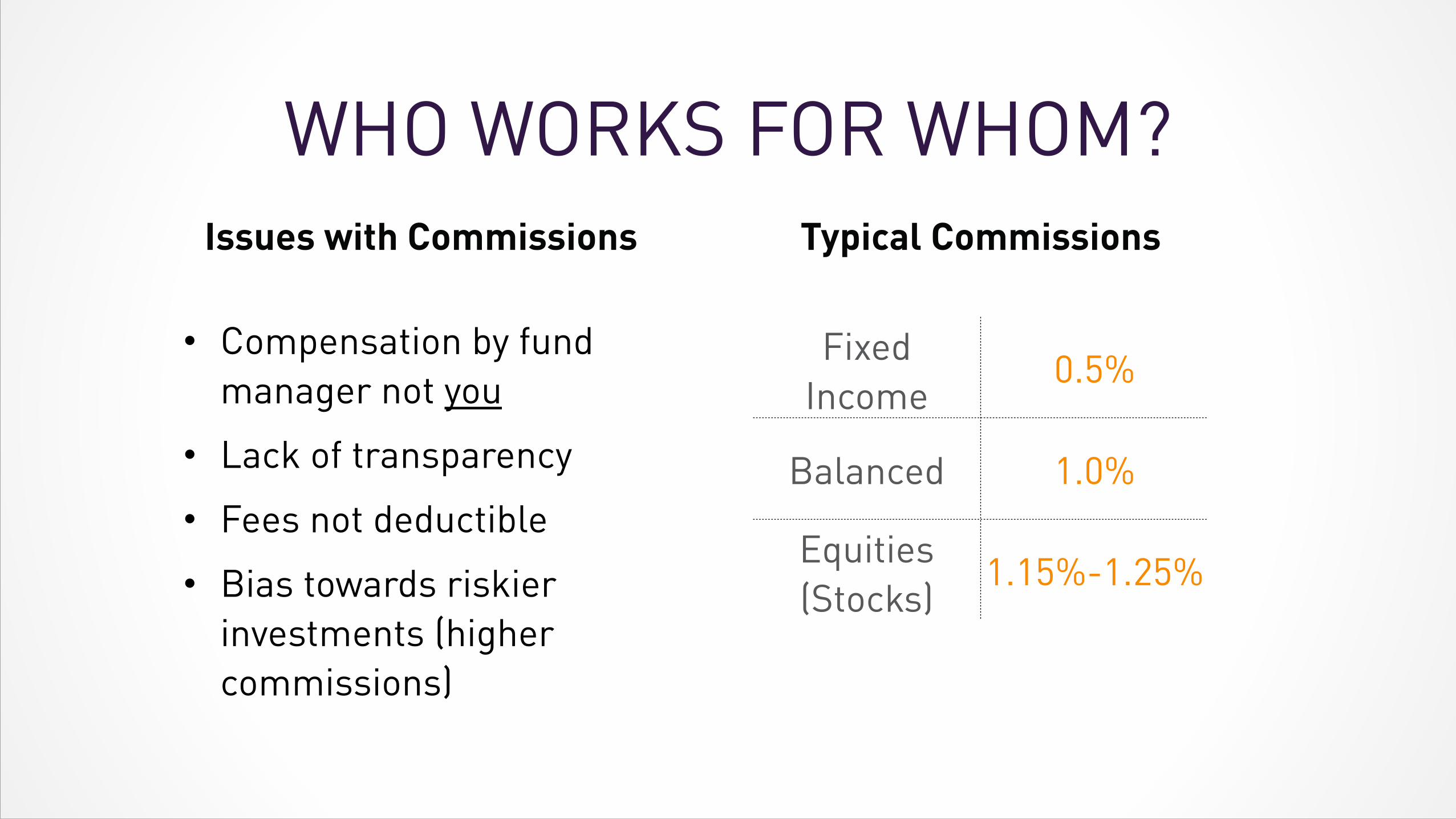

WHO WORKS FOR WHOM?

Fixed Income (Bonds)

0.5%

Balanced 1.0%

Equities (Stocks)

1.15%-1.25%

• Compensation by fund manager not you

• Lack of transparency • Fees not deductible • Bias towards riskier

investments (higher commissions)

Issues with Commissions Typical Commissions

WHO WORKS FOR WHOM?Seeks advice

Recommends investment

Provides investment

at a reduced cost

Pays advisor fee

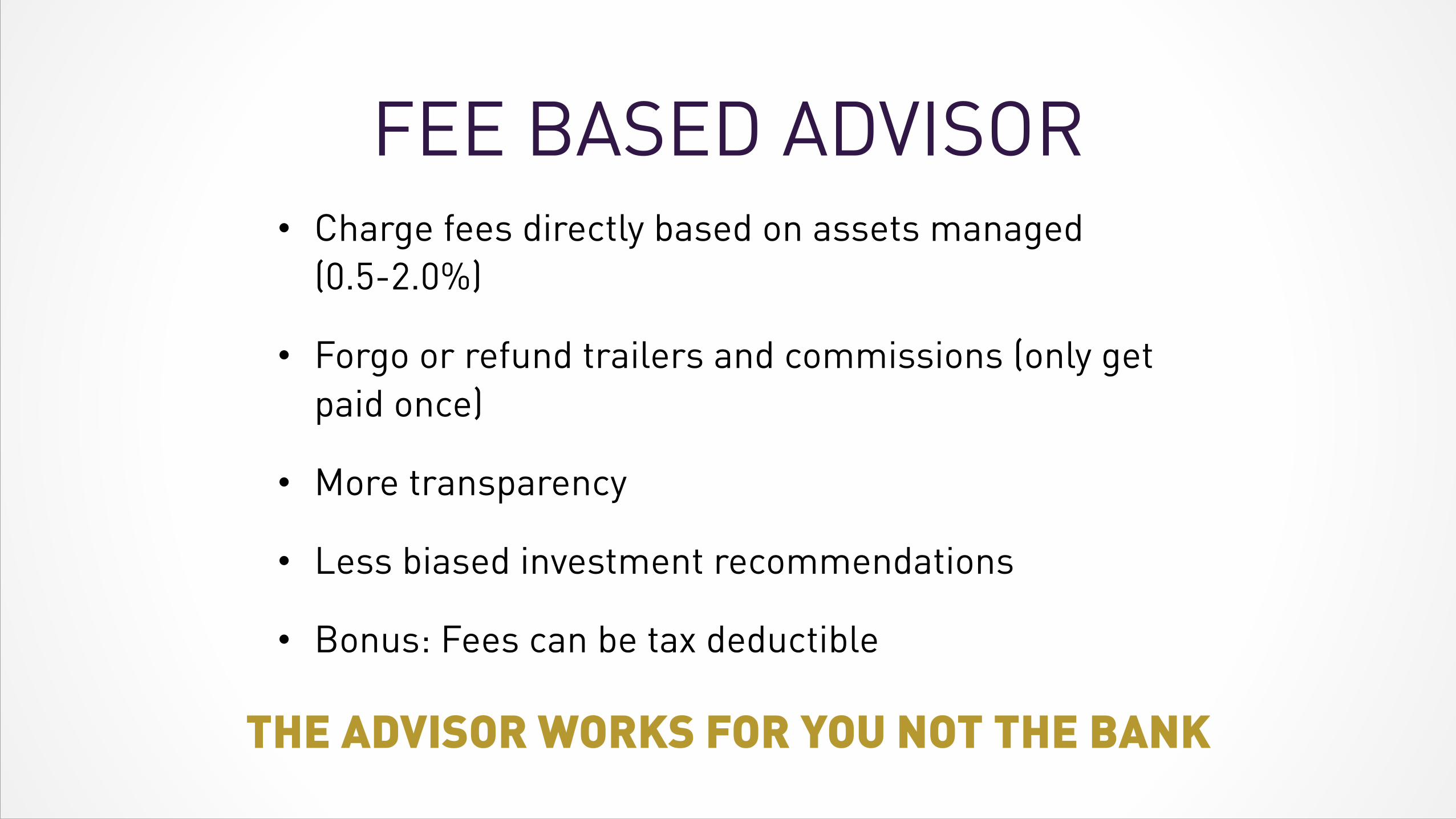

FEE BASED ADVISOR• Charge fees directly based on assets managed

(0.5-2.0%)

• Forgo or refund trailers and commissions (only get paid once)

• More transparency

• Less biased investment recommendations

• Bonus: Fees can be tax deductible

THE ADVISOR WORKS FOR YOU NOT THE BANK

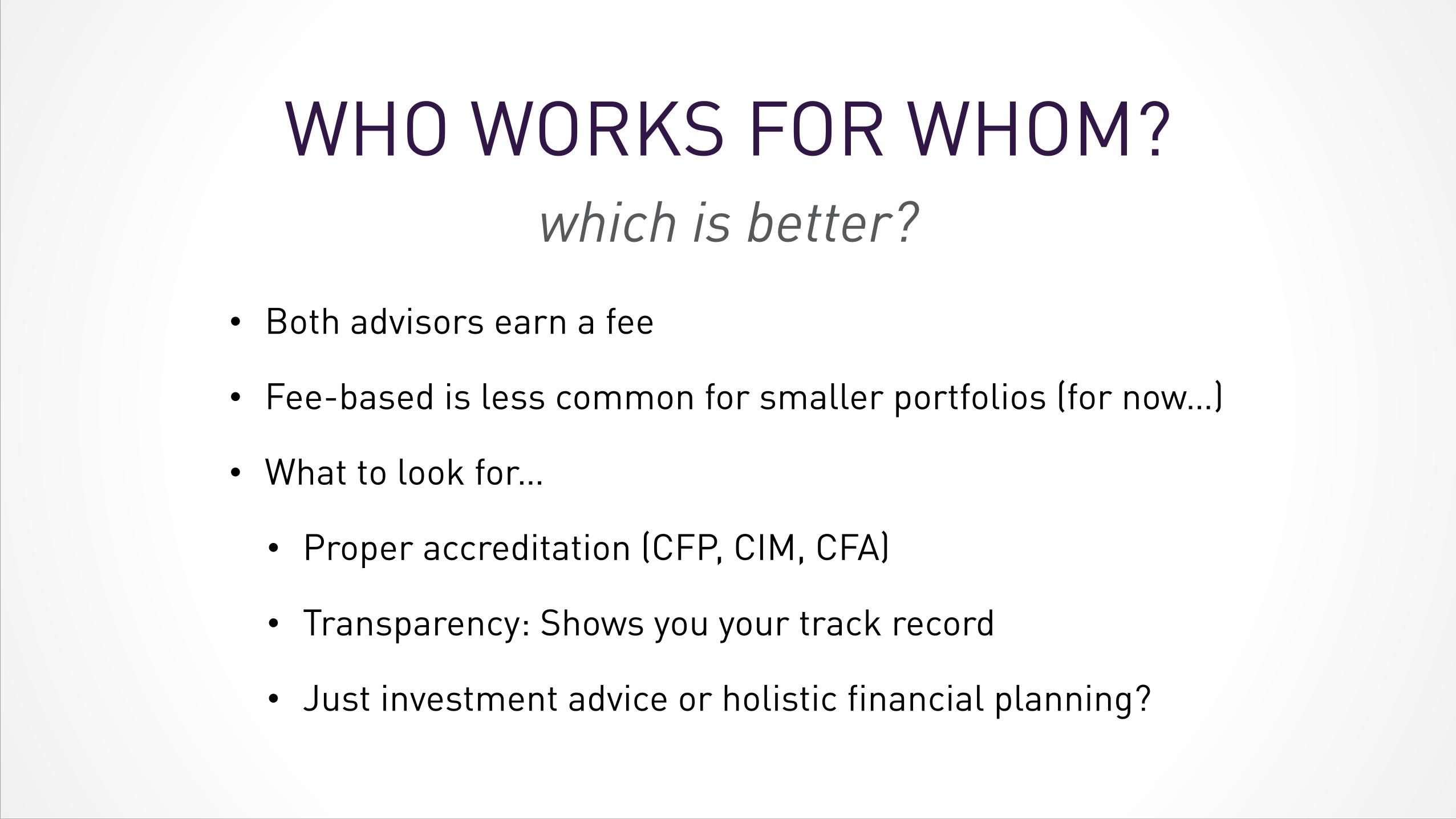

WHO WORKS FOR WHOM?which is better?

• Both advisors earn a fee

• Fee-based is less common for smaller portfolios (for now…)

• What to look for…

• Proper accreditation (CFP, CIM, CFA)

• Transparency: Shows you your track record

• Just investment advice or holistic financial planning?

DOING YOUR RESEARCHOnline Research Tools

DOING YOUR RESEARCHVolatility and Risk

DOING YOUR RESEARCHFees and Costs

DOING YOUR RESEARCHStrategy

THANKS FOR COMINGQuestions?

Related Documents