Everything you need to know to get started Trading Guide Perpetual Futures v0.2

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Everything you need to know to get started

Trading GuidePerpetual Futures

v0.2

IntroductionThis handy guide will explain everything you need to know about EQUOS Perpetual futures, from the very basics for the newbies right up to the intricacies for the most advanced traders.

Table of ContentsWhat are Perpetual Futures?

Why Trade Perpetuals?

Tell me the basics

The Technicals

Product Specifications

Exchange Index

Marking

Basis & Basis Payment Calculation

P&L

Leverage and Margin

Liquidation Process

Further Reading

3

3

4

8

8

9

9

12

14

15

21

28

What are Perpetual Futures?

Perpetual futures are futures contracts with no maturity, as opposed to dated futures, which expire at a pre-set date and time such as every month or every quarter. Any position in a perpetual future stays open until the trader decides to close the trade by executing an offsetting trade, or until the trade gets liquidated by EQUOS. We will come back to this later.

As perpetual futures have no set expiry they are, in a way, similar to spot exposure. To ensure that perpetual prices are kept in line with the spot market, the contracts have an exchange of payment between buyers and sellers depending on where the future price is trading relative to the underlying spot price. At EQUOS, we refer to the spread between spot and perpetual futures prices as Basis. Other platforms may refer to this value as funding, which is the equivalent practice.

Why Trade Perpetual Futures?

Margin: the advantage of trading a perpetual future over a spot contract is that perpetuals offer the trader the ability to trade on margin - rather than having to fund the full notional of the trade(the USDC value of the position) , the trader has the option to put down only part of the notional in margin. Therefore, trading perpetuals is more capital efficient. We will explain more about margin in the next section.

No need to own the underlying: a perpetual future is a derivative, which means that the payoff of the contract is based on the underlying asset, such as Bitcoin BTC, but there is no need to own the underlying itself. Any profits and losses will be settled directly in USDC in your account.

Ability to trade both directions: traders can buy (go long) or sell (go short) perpetual futures, therefore they can benefit from prices going up as well as prices going down. This cannot be easily done when trading the underlying directly.

Risk management: traders can use perpetual futures to hedge positions.

3Perpetual Futures Trading Guide

Tell me the basics

When trading or reading about perpetuals, you will see a lot of terminology that is being used. We explain the most common terms here.

P&L stands for Profit & Loss, which can be both realized and unrealized. Unrealized P&L can be viewed as profits or losses on paper. Realized P&L are the profits or losses reflected in your account. In traditional markets, P&L is unrealized when the price of an underlying asset changes after a trader has opened a position, but before the trader has closed their position.

On EQUOS, P&L for open perpetual futures positions is always unrealized - P&L is only realized when the position is closed.

P&L

Notional Value

The notional value, often shortened to notional, is the total value of a position. For example, a position of 2 BTC Perpetual futures where one BTC Perpetual future is priced at 10,000 USDC will have a notional of 20,000 USDC.

On EQUOS traders have the option to partly fund the notional of their per-petual trades. In other words, a trader can have a notional exposure that is a multiple higher than the cash used to place the trade. This is referred to as leverage. Margin, also called collateral, is the amount that a trader has funded their account to trade with.

Leverage and Margin

4Perpetual Futures Trading Guide

Leverage

On EQUOS traders have the option to trade perpetual futures with leverage. For cryptocurrency futures, leverage trading is actually more similar to margin trading. On EQUOS the derivatives products, such as our BTC Perpetual future, are not leveraged. However, traders have the option to fund each dollar of notional exposure with a smaller amount of capital, called margin or collateral. For example, if you are using 5x leverage, your notional exposure is 5x the amount you have put down as funding. In other words, you are funding 1/5th of your trade with margin.

On EQUOS, the amount of leverage available to trade depends on your position size - the larger the position you have, the less amount of leverage you are allowed. Conversely, the smaller your position is, the larger the amount of leverage you are allowed.

Initial Margin

The amount of capital required to open any new position is also referred to as the Initial Margin. To open a larger sized position requires a relatively larger amount of Initial Margin than to open a smaller sized position.

A trader may choose at any time to increase the balance in their margin account to exceed the Initial Margin requirement. Increasing the margin balance would reduce the trader’s leverage.

Initial Margin:the minimum amount of USDC required to open any new position.

Total Account Margin: total USDC equivalent notional of all assets available for margin, including any unrealized P&L, less any capital required for open non-margin (spot) orders.

Leverage:the ratio between your margin balance and the notional exposure of your portfolio.

Margin: the amount of capital used to fund a trade.

Total Account Margin

Not all assets that are in your portfolio, may necessarily be eligible to be used as margin. The USDC equivalent notional of all assets that are eligible to be used for margin, including any unrealized P&L and less any capital required for non-margin (spot) trades, is your Total Account Margin.

As long as the Total Account Margin is higher than the Initial Margin requirement, a trader is able to continue to send orders. As soon as the Total Account Margin falls below the Initial Margin requirement, the trader can no longer send orders unless they reduce their notional position.

5Perpetual Futures Trading Guide

Liquidation is when a position has to be unwound because insufficient margin remains in the account.

EQUOS has unique features and functionality explicitly dedicated to managing liquidation orders. When the position has been unwound, the trader is charged a liquidation fee. If there is any margin left in the account after liquidation and the payment of the liquidation fee, this will be returned to the trader.

Liquidation

To avoid liquidation, your account needs to have a minimum amount of margin, this value is called the Margin Liquidation Trigger. When your Total Account Margin reaches the level of the Margin Liquidation Trigger, your account will start to get liquidated.

Specifically, an account is flagged for liquidation when the Total Account Margin falls below the Margin Liquidation Trigger. At this point the liquidation engine takes over the position, and will try to unwind the position at the best available price.

Margin Liquidation Trigger

Liquidation: when a position is forced to be closed out because insufficient margin remains in the trader’s account to keep the position open.

Margin Liquidation Trigger: the minimum amount of USDC equivalent notional required to avoid forced liquidation. If the Total Account Margin falls below the Margin Liquidation Trigger, the account’s positions will get liquidated.

6Perpetual Futures Trading Guide

On EQUOS we differentiate between the Market Price and the Mark Price of the perpetual. The Market Price is the last traded price of the product on EQUOS. There may be instances where the last traded price of the product is out of proportion compared to the market, for example in case of a particular large order or an illiquid order book, both of which may move the last traded price significantly up or down. The Mark Price therefore is used to indicate a fairer value for the contract, taking an average over a certain time period to smooth out any temporary spikes in prices, preventing unnecessary liquidations.

The Exchange Index is a basket of spot contracts across a multiple of exchanges, which is used as a reference price to ensure our Mark Price does not diverge too far from the rest of the market due to, for example, market manipulation or an illiquid order book.

How the Market Price and Exchange Index are used to calculate the Mark Price is explained in detail in The Technicals section.

Market Price, Mark Price and the Exchange Index

As we mentioned previously, perpetuals have a mechanism to ensure pricing aligns with the underlying spot product - see Market Price, Mark Price and the Exchange Index. We refer to the spread between the Spot and the Perpetual contract as Basis. The resulting exchange of payment between long and short holders of the contract is called the Basis Payment.

Basis and Basis Payment

7Perpetual Futures Trading Guide

The Technicals

In this section, we describe the technical aspects of the EQUOS BTC Perpetual futures in more detail. These product specifications are valid at the time of writing (September 2020) but may be changed at any time by EQUOS. To make sure you are up to date at any point, please refer to the EQUOS website.

Product Specification

EQUOS BTC Perpetual future Product Specification

Instrument Type Perpetual future

Ticker BTC/USDC[F]

Name BTC/USDC [Perpetual Future]

Underlying 1 BTC

Settlement Cash settled in USDC

Minimum Trade Size 0.001 BTC

Tick Size 0.01 USDC

ExpiryThe perpetual futures are non-expiring, which means that positions in the contract are never “expired” or “matured”, however, there is a process every 8 hours that applies.

Market Price Last traded price if the future is not paused

Mark Price

3-second TWAP of the Market Price or, if not available, Exchange Index + Basis at last Basis calculation

The TWAP is based on the average of the open, high, low and close of each 1 second bar. The Mark Price will be capped at (Exchange Index +0.2%) and floored at (Exchange Index -0.2%)

Max Leverage 125x

Initial Margin Depending on position size, starting from 0.8%

Basis8 hour TWAP of (Spot Market Price - Future Market Price)

The Basis is capped/floored at +/- 0.375% x Mark Price

Basis Payment Position Size x Basis

Basis Calculation Window Based on an 8-hour TWAP period

Basis Settlement Basis settlements take place every day at 04:00, 12:00 and 20:00 UTC

Fees Fees are charged based on customer fee tier

Liquidation Fee 0.375%

Position Limit There is no maximum position limit for this product.

8Perpetual Futures Trading Guide

Exchange Index

On EQUOS the Exchange Index serves as a bound for the Perpetual Mark Price, such that where EQUOS Perpetual prices diverge too far from the Exchange Index, the Perpetual Mark Price is set to the Exchange Index +/- a spread.

The Exchange Index is the average of the last traded BTC Spot price over several exchanges. For the EQUOS BTC Perpetual contract the Exchange Index consists of the following exchanges, equally weighted and converted into USDC:

Marking

On EQUOS, we differentiate between the Market Price and the Mark Price of the perpetual. The Market Price is the last traded price of the product on EQUOS.

The Market Price may deviate (significantly) from the rest of the market for example in case of large orders or an illiquid order book. The Mark Price gives a fairer value for the contract by taking a 3-second TWAP of the Market Price. A TWAP is the average of the open, high, low and close price for a specific period. In the case of the Mark Price these periods are three 1-second intervals. As the Mark Price is used for P&L calculation and to determine whether the position needs to be liquidated, using a TWAP to smooth out temporary spikes in prices should prevent unnecessary liquidations.

Exchange Product (Spot)

Binance BTC/USDT or BTC/USDC, whichever was traded last

Coinbase BTC/USD

Bitstamp BTC/USDC

Kraken XBT/USD

Gemini BTC/USD

Prices are retrieved every 100ms. Any prices older than 100ms are removed. If no exchange provides a price in the last 100ms, the Exchange Index will keep the previous price.

Market Price: the last traded price.

9Perpetual Futures Trading Guide

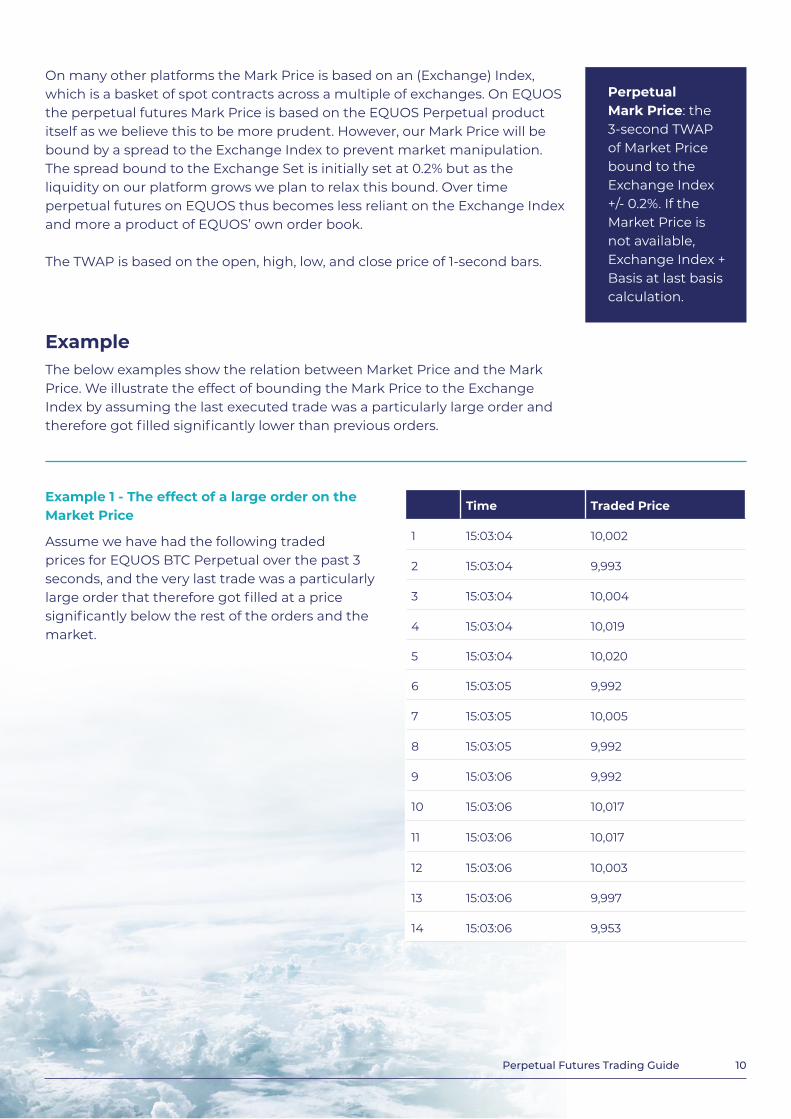

Perpetual Mark Price: the 3-second TWAP of Market Price bound to the Exchange Index +/- 0.2%. If the Market Price is not available, Exchange Index + Basis at last basis calculation.

ExampleThe below examples show the relation between Market Price and the Mark Price. We illustrate the effect of bounding the Mark Price to the Exchange Index by assuming the last executed trade was a particularly large order and therefore got filled significantly lower than previous orders.

Time Traded Price

1 15:03:04 10,002

2 15:03:04 9,993

3 15:03:04 10,004

4 15:03:04 10,019

5 15:03:04 10,020

6 15:03:05 9,992

7 15:03:05 10,005

8 15:03:05 9,992

9 15:03:06 9,992

10 15:03:06 10,017

11 15:03:06 10,017

12 15:03:06 10,003

13 15:03:06 9,997

14 15:03:06 9,953

Example 1 - The effect of a large order on the Market Price

Assume we have had the following traded prices for EQUOS BTC Perpetual over the past 3 seconds, and the very last trade was a particularly large order that therefore got filled at a price significantly below the rest of the orders and the market.

On many other platforms the Mark Price is based on an (Exchange) Index, which is a basket of spot contracts across a multiple of exchanges. On EQUOS the perpetual futures Mark Price is based on the EQUOS Perpetual product itself as we believe this to be more prudent. However, our Mark Price will be bound by a spread to the Exchange Index to prevent market manipulation. The spread bound to the Exchange Set is initially set at 0.2% but as the liquidity on our platform grows we plan to relax this bound. Over time perpetual futures on EQUOS thus becomes less reliant on the Exchange Index and more a product of EQUOS’ own order book.

The TWAP is based on the open, high, low, and close price of 1-second bars.

10Perpetual Futures Trading Guide

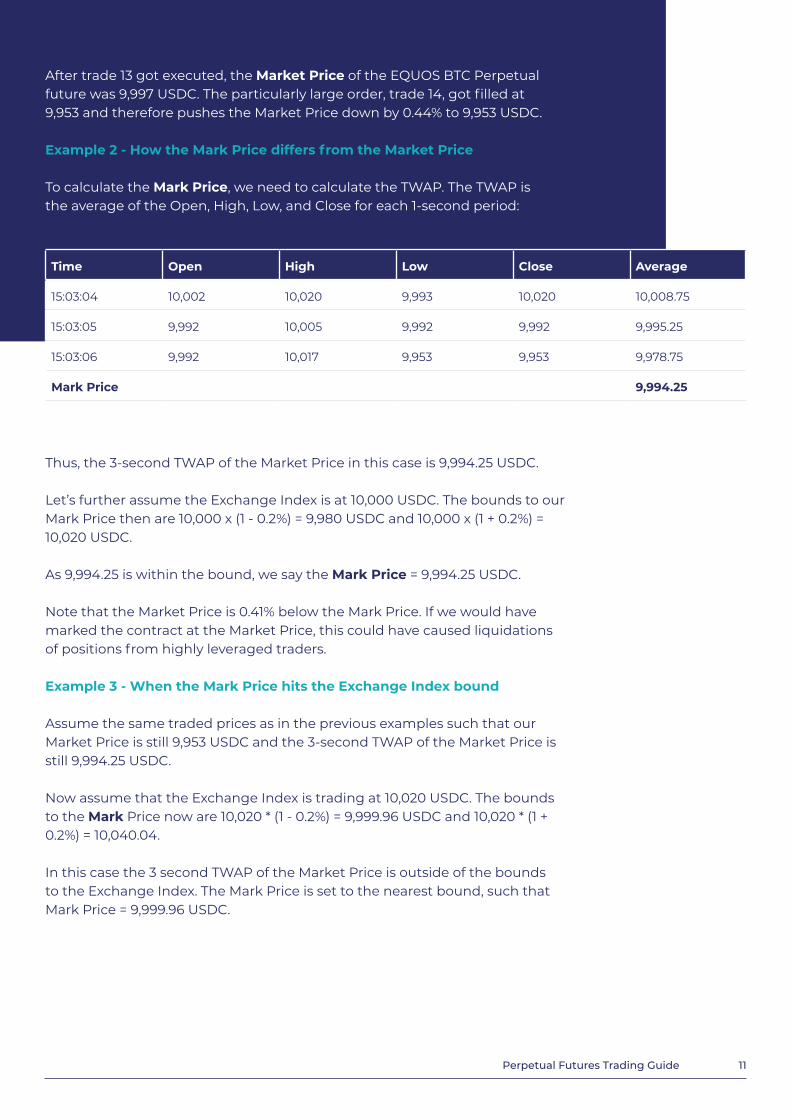

After trade 13 got executed, the Market Price of the EQUOS BTC Perpetual future was 9,997 USDC. The particularly large order, trade 14, got filled at 9,953 and therefore pushes the Market Price down by 0.44% to 9,953 USDC.

Example 2 - How the Mark Price differs from the Market Price

To calculate the Mark Price, we need to calculate the TWAP. The TWAP is the average of the Open, High, Low, and Close for each 1-second period:

Time Open High Low Close Average

15:03:04 10,002 10,020 9,993 10,020 10,008.75

15:03:05 9,992 10,005 9,992 9,992 9,995.25

15:03:06 9,992 10,017 9,953 9,953 9,978.75

Mark Price 9,994.25

Thus, the 3-second TWAP of the Market Price in this case is 9,994.25 USDC.

Let’s further assume the Exchange Index is at 10,000 USDC. The bounds to our Mark Price then are 10,000 x (1 - 0.2%) = 9,980 USDC and 10,000 x (1 + 0.2%) = 10,020 USDC.

As 9,994.25 is within the bound, we say the Mark Price = 9,994.25 USDC.

Note that the Market Price is 0.41% below the Mark Price. If we would have marked the contract at the Market Price, this could have caused liquidations of positions from highly leveraged traders.

Example 3 - When the Mark Price hits the Exchange Index bound

Assume the same traded prices as in the previous examples such that our Market Price is still 9,953 USDC and the 3-second TWAP of the Market Price is still 9,994.25 USDC.

Now assume that the Exchange Index is trading at 10,020 USDC. The bounds to the Mark Price now are 10,020 * (1 - 0.2%) = 9,999.96 USDC and 10,020 * (1 + 0.2%) = 10,040.04.

In this case the 3 second TWAP of the Market Price is outside of the bounds to the Exchange Index. The Mark Price is set to the nearest bound, such that Mark Price = 9,999.96 USDC.

11Perpetual Futures Trading Guide

Basis & Basis Payment Calculation

At EQUOS, the Basis is calculated and settled in USDC every 8 hours at 04:00, 12:00, and 20:00 UTC.

In order to calculate the Basis of the perpetual future, we compare the difference between the Market Price of the EQUOS Spot contract and the Market Price of the EQUOS Perpetual contract over the past 8 hours:

Basis = 8 hour TWAP of (Spot Market Price - Perpetual Market Price)

The TWAP is based on the average of the open, high, low and close of each 1 minute bar.

The Basis is capped/floored at +/- 0.375% * Perpetual Mark Price at the Basis calculation time to avoid instantaneous liquidation for positions with high leverage.

Note that the Market Price may be different from the Mark Price used to value futures contracts during trading hours, which is bound by the Exchange Index to protect market participants against manipulative trading.

Basis

Basis Payment

The Basis Payment is an exchange of payment between long and short holders of the perpetual contract, based on the calculated Basis:

Basis Payment = Position Size * Basis

The Basis and Basis Payment are defined from a long holders perspective such that when Spot Market Price < Perpetual Market Price, every long holder of the contract pays the short holders of the contract a value equal to their Position Size x Basis.

The Basis Payment is only paid or received if a position in the contract is held at the time of Basis calculation.

12Perpetual Futures Trading Guide

Examples

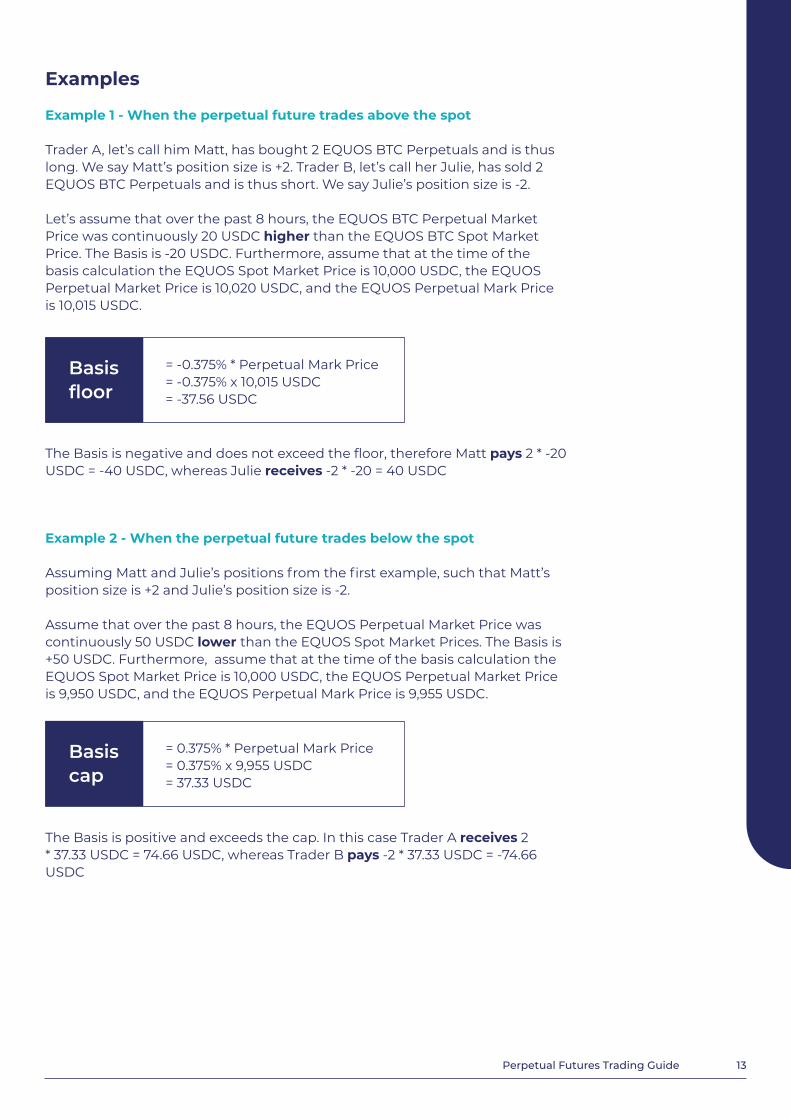

Example 1 - When the perpetual future trades above the spot

Trader A, let’s call him Matt, has bought 2 EQUOS BTC Perpetuals and is thus long. We say Matt’s position size is +2. Trader B, let’s call her Julie, has sold 2 EQUOS BTC Perpetuals and is thus short. We say Julie’s position size is -2.

Let’s assume that over the past 8 hours, the EQUOS BTC Perpetual Market Price was continuously 20 USDC higher than the EQUOS BTC Spot Market Price. The Basis is -20 USDC. Furthermore, assume that at the time of the basis calculation the EQUOS Spot Market Price is 10,000 USDC, the EQUOS Perpetual Market Price is 10,020 USDC, and the EQUOS Perpetual Mark Price is 10,015 USDC.

Example 2 - When the perpetual future trades below the spot

Assuming Matt and Julie’s positions from the first example, such that Matt’s position size is +2 and Julie’s position size is -2.

Assume that over the past 8 hours, the EQUOS Perpetual Market Price was continuously 50 USDC lower than the EQUOS Spot Market Prices. The Basis is +50 USDC. Furthermore, assume that at the time of the basis calculation the EQUOS Spot Market Price is 10,000 USDC, the EQUOS Perpetual Market Price is 9,950 USDC, and the EQUOS Perpetual Mark Price is 9,955 USDC.

The Basis is negative and does not exceed the floor, therefore Matt pays 2 * -20 USDC = -40 USDC, whereas Julie receives -2 * -20 = 40 USDC

Basis floor

= -0.375% * Perpetual Mark Price = -0.375% x 10,015 USDC= -37.56 USDC

= 0.375% * Perpetual Mark Price = 0.375% x 9,955 USDC= 37.33 USDC

The Basis is positive and exceeds the cap. In this case Trader A receives 2 * 37.33 USDC = 74.66 USDC, whereas Trader B pays -2 * 37.33 USDC = -74.66 USDC

Basis cap

13Perpetual Futures Trading Guide

P&LEQUOS Perpetual futures are USDC denominated, therefore any P&L is settled in USDC. P&L on open EQUOS Perpetual future positions is always unrealized. Unrealized P&L is updated continuously based on the latest Mark Price:

Unrealized P&L cannot be withdrawn from the platform. To realize and withdraw P&L, a trader can close and re-enter the trade. Realized P&L on the position is based on the difference between the entry and the exit price.

Examples

In a real life example, let’s call our trader Andy. Andy enters into a long position of 1.5 EQUOS BTC Perpetual at $10,000. Assume the Mark Price is at 10,005 USDC

Position Unrealized P&L Realized P&L

1.5 BTC 7.50 USDC 0 USDC

Andy’s Unrealized P&L

= Position Size x (Mark Price - Entry Price)= 1.5 * (10,005 USDC - 10,000 USDC)= 7.50 USDC

Andy’s P&L balances are

Andy’s P&L balances now areAt the next Basis cycle, assume the Basis is +10 USDC, and the Mark Price has reduced to 9,975 USDC. Position Unrealized P&L Realized P&L

1.5 BTC -37.50 USDC +15 USDC

At some point before the next Basis calculation, Andy decides to unwind his full position by selling 1.5 EQUOS BTC Perpetual and is able to do so at 9,950 USDC.

Andy’s Unrealized P&L on the trade

= Position Size x (Exit Price - Entry Price)= 1.5 x (9,950 USDC - 10,000 USDC) = -75 USDC

Position Unrealized P&L Realized P&L

0 BTC 0 USDC -60 USDC

Andy’s Total P&L balances, including trade P&L and funding, are

At the next Basis calculation, the Basis is -15 USDC. The Mark Price of the EQUOS BTC Perpetual has dropped further to 9,800 USDC. As Andy does not hold any positions anymore, his P&L balances remain unchanged:

Position Unrealized P&L Realized P&L

0 BTC 0 USDC -60 USDC

Realized P&L = Position Size x (Exit Price - Entry Price)

Unrealized P&L = Position Size x (Mark Price - Entry Price)

14Perpetual Futures Trading Guide

Leverage and Margin

Maximum leverage, margin requirements, and assets eligible for margin as discussed in this section may be updated from time to time. To ensure you are up to date, please find a link to the latest information in section 5.

Currently, EQUOS accounts can only be funded with USD and USDC in order to be used as margin for trading perpetual futures. The Total Account Margin expresses the total of assets available for margin in USDC equivalent, including any unrealized P&L and minus any capital for open spot orders. On EQUOS, any USD is converted into USDC on a 1-for-1 basis.

Eligible Collateral

Leverage limits and Initial Margin

EQUOS offers a maximum of 125x leverage but the overall leverage allowed for a position depends on the size of that position. This is set out in the table below. The limits on position sizes for given leverage levels are designed such that they align the expected risk on the platform with regard to trading volume to the size of the Liquidation Reserve. This is to limit the probability of auto-deleveraging (ADL). These limits will be reviewed regularly and amended as necessary.

Leverage Max notional exposure (USDC) Initial Margin Margin Liquidation Trigger

125.0 10,000 0.80% 0.40%

100.0 25,000 1.00% 0.50%

75.0 50.000 1.33% 0.67%

50.0 150,000 2.00% 1.00%

40.0 250,000 2.50% 1.25%

20.0 400,000 5.00% 2.50%

10.0 700,000 10.00% 5.00%

5.0 1,000,000 20.00% 10.00%

4.0 1,500,000 25.00% 12.50%

3.3 2,500,000 30.00% 15.00%

2.0 12,500,000 50.00% 25.00%

1.5 25,000,000 66.67% 33.33%

Any notional over USDC 25,000,000 requires 100% Initial Margin.

15Perpetual Futures Trading Guide

The Initial Margin required for a certain size position is directly related to the maximum leverage available for that position size. On EQUOS, the Initial Margin requirement follows a tax style bracket approach, starting from the highest leverage bucket. This means that a trader who wants to open a BTC Perpetual position with a 25,000 USDC notional has to pay 0.80% Initial Margin on the first 10,000 USDC and 1% on the remaining 15,000 USDC.

The leverage on any account is the ratio between the margin balance and the notional exposure of that account. Explicitly:

Account Leverage = Position Notional / Total Account Margin

This may be different from the maximum leverage that is allowed at the inception of the trade as inferred from the above table, which is a function of the notional exposure and the Initial Margin required:

Maximum Leverage = Position Notional / Initial Margin

A trader’s Total Account Margin thus needs to be at least equal to the Initial Margin for them to be able to execute the trade. However, a trader can at any point reduce their leverage by ensuring their Total Account Margin exceeds the Initial Margin.

On EQUOS, margin is also required for open orders (orders that have been sent to the order book, but that have not yet been filled). The margin on open orders is included in the account’s Initial Margin, but also shown separately as Reserved Margin.

16Perpetual Futures Trading Guide

The Margin Liquidation Trigger is always 50% of the Initial Margin required for open position(s) only. The Margin Liquidation Trigger thus does not take into account any open order(s), and it is independent of the Total Account Margin in the account at the time when the trade was executed.

Margin Liquidation Trigger

Examples

For simplicity let’s assume the EQUOS BTC Spot and EQUOS BTC Perpetual futures are both trading and being marked at 10,000 USDC throughout all below examples.

Example 1a - What is Total Account Margin?

Trader A, let’s call her Maria, has the following asset in her EQUOS wallet:

• 5 Bitcoin, currently marked at 10,000 USDC

• 1,500 USDC

• 1,000 USD

At EQUOS, USD is always converted into USDC at a 1-for-1 ratio. The value of Maria’s assets equals 5 x 10,000 USDC + 1,500 USDC + 1 USDC x 1,000 = 52,500 USDC

As BTC cannot currently be used as margin the assets available for margin, the Total Account Margin, is 2,500 USDC only.

Maria’s account does not currently have any leverage.

17Perpetual Futures Trading Guide

Example 1b - How to calculate Margin and Leverage

Assume Maria wants to buy 100,000 USDC worth of EQUOS BTC Perpetual futures. To do so, the Initial Margin requirement would be:

10,000 x 0.8% = 8015,000 x 1.0% = 15025,000 x 1.33% = 332.5050,000 x 2.0% = 1,000Initial Margin = 1,562.50 USDC

The maximum leverage allowed on this trade is thus:

Maximum Leverage = Position Notional / Initial Margin = 100,000 / 1,562.50 = 64x

As Maria’s Total Account Margin is 2,500 USDC, which is higher than the Initial Margin, she is able to send the order. She will send an order to buy 10 BTC Perpetuals at 10,000 USDC, which gets filled straight away. Now that Maria has a position, we can calculate the overall leverage of the account as follows:

Account Leverage = Position Notional / Total Account Margin = 100,000 / 2,500 = 40x

The Leverage, Position and Margin balances for the Perpetual are:

• Leverage: 40x

• Position Size: 10 BTC

• Position Notional: 100,000 USDC

• Total Account Margin: 2,500 USDC

• Initial Margin: 1,562.50 USDC

• Reserved Margin: 0 USDC

• Margin Liquidation Trigger: 781.25 USDC

18Perpetual Futures Trading Guide

Example 1c - The effect of sending an order on Initial Margin

In addition to her existing position, Maria sends a limit order to buy another 5 BTC Perpetuals with a limit price of 9,000 USDC. This means that the order will only get executed at a price of 9,000 USDC or better which, in the case of a buy order, is lower.

Buying 5 BTC Perpetual futures at 9,000 USDC yields a notional position of 5 x 9,000 USDC = 45,000 USDC. This exposure will be added to the existing 100,000 USDC position to calculate the Initial Margin requirement on the total position.

The additional notional exposure sits in the 2% margin bucket (which has a total notional of 150,000 USDC), and the additional Initial Margin requirement as a result of the new order is 45,000 USDC x 2% = 900 USDC. The overall Initial Margin requirement, including the new order, is 2,462.50 USDC.

As Maria has 2,500 USDC Total Account Margin, she can send the order. The limit order will not be filled straight away, since the current price of 10,000 USDC is above the limit price of 9,000 USDC. Therefore, the order stays open and the margin requirement on the order is shown under Reserved Margin. The Margin Liquidation Trigger remains unchanged, as do the leverage, posi-tion size, position notional, and total account margin:

• Leverage: 40x

• Position Size: 10 BTC

• Position Notional: 100,000 USDC

• Total Account Margin: 2,500 USDC

• Initial Margin: 2,462.50 USDC

• Reserved Margin: 900 USDC

• Margin Liquidation Trigger: 781.25 USDC

19Perpetual Futures Trading Guide

Example 2 - Total Account Margin with an open Spot order to buy BTC

Another trader, let’s call him Dan has the following balances and positions:

• 20,000 USDC

• 10,000 USD

• 5 Bitcoin

• 1 BTC Perpetual marked at 10,000 USDC

• Unrealized P&L of -500 USDC

• 1 open spot order to buy 2 BTC at a price of 9,000 USDC

The USDC equivalent notional of all assets available for margin = 20,000 USDC + 1 USDC x 10,000 = 30,000 USDC.

The capital required for open spot orders = 2 x 9,000 USDC = 18,000 USDC.

Dan’s Total Account Margin, which is the USDC equivalent of all assets avail-able for margin plus any unrealized P&L and minus any capital required for open spot orders, thus is:

Total Account Margin = 30,000 - 500 - 18,000 = 11,500 USDC

Example 3 - Total Account Margin with an open Spot order to sell BTC

In another example, let’s call our trader Jack, he has the following balances and positions:

• 20,000 USDC

• 10,000 USD

• 5 Bitcoin

• 1 BTC Perpetual marked at 10,000 USDC

• Unrealized P&L of -500 USDC

• 1 open spot order to sell 2 BTC at a price of 9,000 USDC

The USDC equivalent notional of all assets available for margin = 20,000 USDC + 1 USDC x 10,000 = 30,000 USDC.

The capital required for open spot orders in this case is zero as there is no ben-efit for selling USDC proceeds from selling BTC, until the trade has executed. Hence:

Jack’s Total Account Margin = 30,000 - 500 - 0 = 29,500 USDC

Check out our latest articles Leverage, Margin, and Liquidation, which is linked in the next section.

20Perpetual Futures Trading Guide

Liquidation Process

As we explained in the previous sections in this guide, an account is only able to send new orders as long as its Total Account Margin is higher than the Initial Margin required for all open positions and open orders. As soon as the Total Account Margin drops below the Initial Margin, the account can no longer send any new orders unless such order would reduce the existing position (e.g. a sell order, when the current position is long). To continue adding positions (e.g. add buy orders, when the current position is long), the trader will have to transfer additional funds that can be used for margin to their wallet, close open orders, or close open positions.

The Total Account Margin includes any (un)realized P&L and thus, if the market moves against the position such that the P&L on the position is negative, the Total Account Margin will reduce. When the Total Account Margin falls below the Margin Liquidation Trigger, the account will start to get liquidated. This means that EQUOS will take over your positions and try to unwind them by either attempting to sell, if the position to be liquidated is long, or attempting to buy, if the position to be liquidated is short.

When is an account liquidated?

21Perpetual Futures Trading Guide

Examples

Trader A, let’s call her Clare, has 10 BTC Perpetuals marked at 10,000 USDC, such that her Notional Position is 100,000 USDC. We know, from the previous example, that the Initial Margin requirement for a 100,000 USDC position is 1,562.50 USDC.

Assume Clare has 1,750 USDC deposited in her wallet. She has not made any P&L as she has only just executed the trade, and there are no open orders. Her Total Account Margin is 1,750 USDC which is higher than the Initial Margin required of 1,562.50 USDC. Therefore, Clare can continue to send more orders if she wants to.

Example 1 - When a loss reduces the Total Account Margin below the Initial Margin

Before Clare sends another order, however, the mark price of the EQUOS BTC Perpetual future reduces to 9,950 USDC. Clare’s Notional Position is now 10 x 9,950 USDC = 99,500 USDC. Clare has thus lost 500 USDC on their position. Therefore, her Total Account Margin = 1,750 - 500 = 1,250 USDC.

Because the Notional Position has changed, the Initial Margin now is 1,552.50 USDC and the Margin Liquidation Trigger is 776.25 USDC. As the Total Account Margin is now below the Initial Margin, Clare can no longer send any new orders. The account is not yet liquidated, as the Total Account Margin is still higher than the Margin Liquidation Trigger.

If Clare wants to send more orders, she will have to deposit additional funds that are eligible for margin.

Example 2 - When a loss reduces the Total Account Margin below the Margin Liquidation Trigger

The mark price of the EQUOS BTC Perpetual reduces further to 9,900 USDC. Clare’s Notional Position is now 10 x 9,900 USDC = 99,000 USDC, and she has lost 1,000 USDC in total on her position. Her Total Account Margin is 1,750 - 1,000 = 750 USDC

The Initial Margin required for a 99,000 USDC Notional Position is 1,542.50 USDC, and the Margin Liquidation Trigger is at 771.25 USDC. Because the Total Account Margin has fallen below the Margin Liquidation Trigger, EQUOS will start to liquidate Clare’s position.

22Perpetual Futures Trading Guide

The Zero Price is the point where the Total Account Margin would be fully depleted. An account that gets liquidated is charged a liquidation fee which will be taken from the account’s margin balance. The Zero Price is adjusted to reflect the liquidation fee to ensure sufficient funds remain in the account to pay this fee upon liquidation.

Zero Price

Fees

Any order that is executed as a result of a liquidation is charged a liquidation fee of 0.375% on the order size executed, at the price at which the liquidation order was (partially) filled. No trading fees will be charged to the account for this transaction.

The liquidation fee will be paid to EQUOS’ Liquidation Reserve. A trader on EQUOS can never lose more than their Total Account Margin. However, there may be occasions where a liquidation order cannot be filled above the Zero Price. In other words, the liquidation is loss making. As long as it is able to do so, the Liquidation Reserve will cover these losses.

We’ve written a more detailed blog post on how liquidations work, which can be found on our medium page that is linked in the next chapter.

23Perpetual Futures Trading Guide

EQUOS has unique features and functionality explicitly dedicated to managing liquidation orders. By using three lines of defense we aim to minimize the likelihood of Auto-DeLeveraging (ADL). Although EQUOS aims to minimize the chances of such an event, it should be noted that the risk of ADL can never be completely removed. EQUOS aims to prevent the possibility of ADL using the following 3 functions:

1. Liquidation Platform - a dedicated liquidity pool exclusively used for liquidation. We invite market makers to join the Liquidation Platform in order to add greater depth and provide price competition to ensure that liquidation orders are executed at the market price for the account holder.

2. EQUOS order book - if there is no liquidity available at the Zero Price or better on the Liquidation Platform then orders will be sent to the main EQUOS order book.

3. Liquidation Reserve - if there is not enough liquidity on the EQUOS order book then the Liquidation Reserve will take the position at the Zero Price.

It should be noted that the Liquidation Platform is only accessible to participants invited to join that process.

Liquidations at EQUOS

When a position needs to get liquidated, the risk engine first sends an order to our Liquidation Platform with a limit price based on the Zero Price. Quotes in the Liquidation Platform are hidden.

The Liquidation Platform prices can only be filled by liquidation orders, never by regular market orders. If the order can be filled in full the account is liquidated at this price and the liquidation is now complete. If the order is completed above the Zero Price then any excess funds, after fees are charged, are retained by the account holder. If the order was not fully filled, the liquidation moves to step 2.

Liquidation platform1

24Perpetual Futures Trading Guide

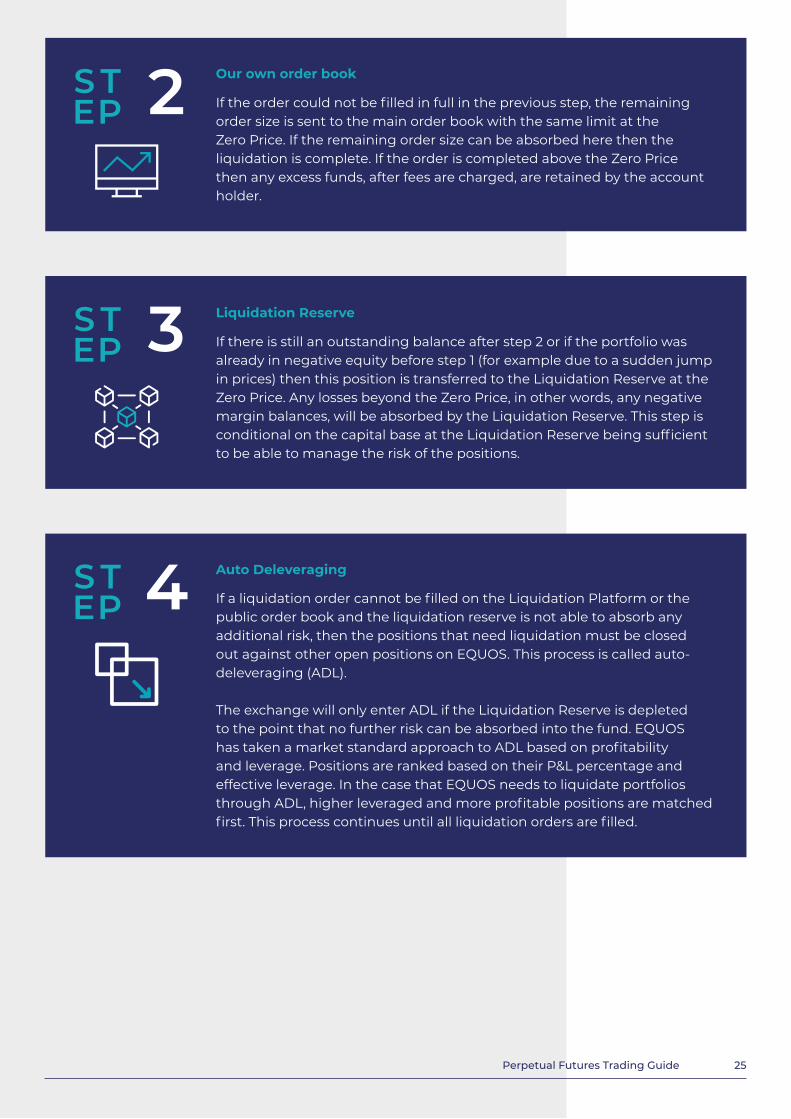

If the order could not be filled in full in the previous step, the remaining order size is sent to the main order book with the same limit at the Zero Price. If the remaining order size can be absorbed here then the liquidation is complete. If the order is completed above the Zero Price then any excess funds, after fees are charged, are retained by the account holder.

Our own order book2

If there is still an outstanding balance after step 2 or if the portfolio was already in negative equity before step 1 (for example due to a sudden jump in prices) then this position is transferred to the Liquidation Reserve at the Zero Price. Any losses beyond the Zero Price, in other words, any negative margin balances, will be absorbed by the Liquidation Reserve. This step is conditional on the capital base at the Liquidation Reserve being sufficient to be able to manage the risk of the positions.

Liquidation Reserve3

If a liquidation order cannot be filled on the Liquidation Platform or the public order book and the liquidation reserve is not able to absorb any additional risk, then the positions that need liquidation must be closed out against other open positions on EQUOS. This process is called auto-deleveraging (ADL).

The exchange will only enter ADL if the Liquidation Reserve is depleted to the point that no further risk can be absorbed into the fund. EQUOS has taken a market standard approach to ADL based on profitability and leverage. Positions are ranked based on their P&L percentage and effective leverage. In the case that EQUOS needs to liquidate portfolios through ADL, higher leveraged and more profitable positions are matched first. This process continues until all liquidation orders are filled.

Auto Deleveraging4

25Perpetual Futures Trading Guide

Examples

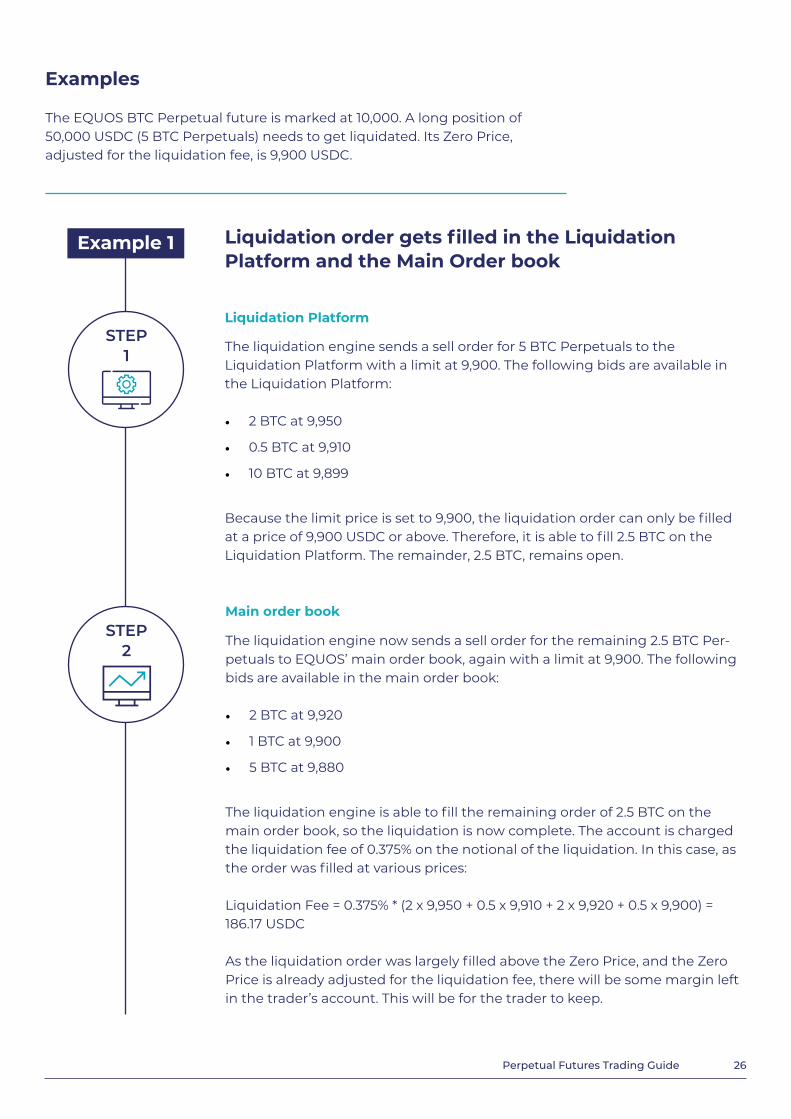

The EQUOS BTC Perpetual future is marked at 10,000. A long position of 50,000 USDC (5 BTC Perpetuals) needs to get liquidated. Its Zero Price, adjusted for the liquidation fee, is 9,900 USDC.

The liquidation engine sends a sell order for 5 BTC Perpetuals to the Liquidation Platform with a limit at 9,900. The following bids are available in the Liquidation Platform:

• 2 BTC at 9,950

• 0.5 BTC at 9,910

• 10 BTC at 9,899

Because the limit price is set to 9,900, the liquidation order can only be filled at a price of 9,900 USDC or above. Therefore, it is able to fill 2.5 BTC on the Liquidation Platform. The remainder, 2.5 BTC, remains open.

The liquidation engine now sends a sell order for the remaining 2.5 BTC Per-petuals to EQUOS’ main order book, again with a limit at 9,900. The following bids are available in the main order book:

• 2 BTC at 9,920

• 1 BTC at 9,900

• 5 BTC at 9,880

The liquidation engine is able to fill the remaining order of 2.5 BTC on the main order book, so the liquidation is now complete. The account is charged the liquidation fee of 0.375% on the notional of the liquidation. In this case, as the order was filled at various prices:

Liquidation Fee = 0.375% * (2 x 9,950 + 0.5 x 9,910 + 2 x 9,920 + 0.5 x 9,900) = 186.17 USDC

As the liquidation order was largely filled above the Zero Price, and the Zero Price is already adjusted for the liquidation fee, there will be some margin left in the trader’s account. This will be for the trader to keep.

Liquidation order gets filled in the Liquidation Platform and the Main Order book

STEP1

STEP2

Example 1

Liquidation Platform

Main order book

26Perpetual Futures Trading Guide

The liquidation engine sends a sell order for 5 BTC Perpetuals to the Liqui-dation Platform with a limit at 9,900. The following bids are available in the Liquidation Platform:

• 2 BTC at 9,900

• 10 BTC at 9,899

Because the limit price is set to 9,900, the liquidation order can only be filled at a price of 9,900 USDC or above. The liquidation engine is thus able to fill 2 BTC on the liquidation platform.

Liquidation order cannot be filled on the Liquidation Platform or the Main Order Book

STEP1

STEP2

STEP3

Example 2

Liquidation Platform

The liquidation engine now sends a sell order for the remaining 3 BTC Perpet-uals to EQUOS’ main order book, again with a limit at 9,900. The following bids are available in the main order book:

• 2 BTC at 9,899

• 5 BTC at 9,880

As there are no bids available at or above the limit price, the order cannot be filled on the main order book.

Main order book

The remaining liquidation order of 3 BTC is sent to the Liquidation Reserve, who will take the position at a price of 9,900 USDC as long as its capital base is sufficient to manage the risk of the positions.

The account that was liquidated is charged the liquidation fee, which will be paid to the Liquidation Reserve. The trader does not have any margin left in his account.

Liquidation Reserve

27Perpetual Futures Trading Guide

All information in this guide including calculations, maximum leverage, margin requirements, and assets eligible for margin amongst others may be updated from time to time. To ensure you are up to date, please see our help pages here.

Further Reading

Read our Medium page

Follow us on Twitter

Join our Telegram group

28Perpetual Futures Trading Guide

Related Documents