1 Performance Review 3Q / 9M 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Performance Review3Q 9M 2013

2

Introduction Strategic Review3Q 9M 2013Alex Thursby Group Chief Executive Officer

3

Continued strength in 3Q 2013 results

3

Net earnings of AED 1035bn for 3Q 2013 down 8 y-o-y as growth in fee and net

interest income was offset by higher expenses and lower investment and other income

Strong underlying year-over-year top line results as net fee and commission grew

185 to AED 450bn in 3Q 2013

As expected 1-time gains related to hedging strategies did not repeat in 3Q 2013

impacting sequential and year-over-year comparisons

Balance sheet increased to AED 345bn up 15 ytd as deposits continued to grow

NPL ratio at 332 in 3Q 2013 remains below the expected peak of 375

Robust capital amp liquidity position maintained with the CAR at 178 and Tier-I ratio

at 161

4

Q3 2013 ndash Awards amp Accomplishments

4

Sheikh Khalifa Excellence Award (SKEA) ndash Diamond Category

Upgraded by SampP to AA-A-1+ from A+A-1

Ranked in World‟s 50 Safest Banks for 5th consecutive year (Global Finance)

ldquoThe Strongest Bank Balance Sheet in the UAE for 2013rdquo ndash Asian Banker

Magazine

ldquoBest Cast Management Services in the Middle Eastrdquo at EMEA Finance

Treasury Services Award Ceremony

5

What we want to change ndash

our mission to be core to our chosen customers

5

Our strategy to deliver this will be built around 3 geographical pillars and

will be achieved primarily through organic growth

Build the largest

safest and best

performing bank

first in UAE and

over time in GCC

Deepen our Wholesale

network across the new

West-East corridor amp

further integrate our

existing European amp

North American

platforms into this

network

Build 5 international bank

franchises in the largest and

fastest growing economies in

the West-East corridor

1

2 3Wholesale Network

Markets

New Franchise

Markets

Home Market

Time to complete build - 5 years

6

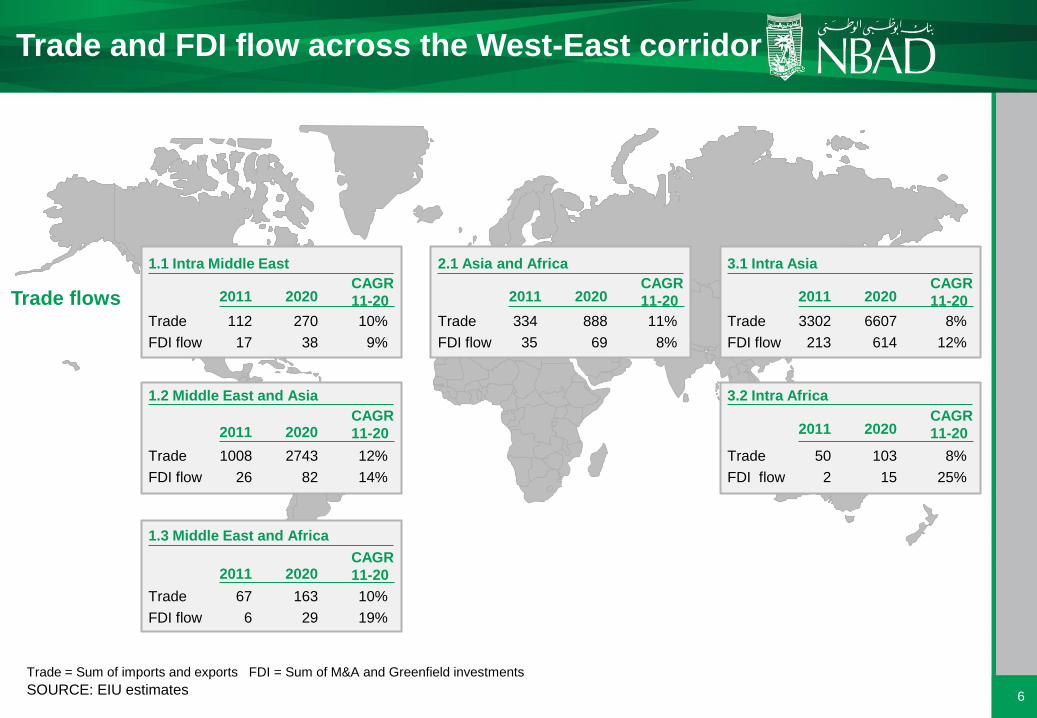

Trade and FDI flow across the West-East corridor

6SOURCE EIU estimates

Trade = Sum of imports and exports FDI = Sum of MampA and Greenfield investments

Trade flows

11 Intra Middle East

Trade

2011

112

12 Middle East and Asia

2011

13 Middle East and Africa

2011

21 Asia and Africa 31 Intra Asia

Trade 3302 6607 8

32 Intra Africa

50Trade 103 8

FDI flow 17

2020

270

2020

2020

38

CAGR

11-20

10

CAGR

11-20

CAGR

11-20

9 FDI flow 213 614 12

FDI flow 2 15 25

2011 2020CAGR

11-20 2011 2020CAGR

11-20

2011 2020CAGR

11-20

Trade

FDI flow

334

35

888

69

11

8

Trade

FDI flow

Trade

FDI flow

1008

26

2743

82

12

14

10

19

163

29

67

6

7

Key industry sectors aligned to our

network markets strategy

7

Key sectors

Financial

Institutions

Aviation rail

and transport

services

Real Estate

and family

conglomerates

Traders and

retailers

Energy and

Resources

Why is it an opportunity Illustrations

Significant and fastest growing segment globally

40 contributor to the global Wholesale bank and the

biggest volume segment in flow products

Controls 70 of the volumes in certain products

Strategic sector in the UAE amp aligned with Abu Dhabi 2030

Attractive sector for corporate credit with low counterparty

risk

Substantial growth amp potential of supply chain business

Strategic sector the UAE amp aligned with Abu Dhabi vision

2030

National champions with significant growth aspirations

Big 6 airlines within the new West-East corridor

Strategic sector the UAE (20 of UAE GDP) amp aligned

with Abu Dhabi vision 2030

Highly attractive sector for Arab investors

Attractive for GCCAsian and other investors

Strategic and high growth sectors in the region

UAE is the 18th biggest trading country in world ahead

of countries like India Brazil and Australia

Retailing is USD ~$48Bn market in GCC expected to

grow at ~8 annually from 201317

8

We will increasingly utilise an bdquooriginate to

distribute‟ model

8

Originate from Customers Distribute to Customers

Government of Abu Dhabi

Financial institutions

Energy and resources

Aviation rail and transport services

Real estate and family conglomerates

Traders and retailers

Financial institutions

Hedge funds

Pension funds and Insurance

Sovereigns

Private banks

HNW and affluent

On and off balance

sheet

Primary distribution

Secondary

distribution

Reverse inquiries

Cross-sell Cross-sell

Cash and Trade

FX and derivatives

Bonds syndications

Commodities

Specialised lending

Corporate finance

Flo

w

pro

du

cts

Clearingsettlements

Cash and trade

FX and derivatives

Bonds

Loans

Flo

w

pro

du

cts

Single distribution hub

9

Wholesale banking model aligning to

West-East corridor

91 Relationship sales and product service

Abu DhabiThe GulfMiddle East

MumbaiIndian sub-continent

LagosSouth and West Africa

Singapore

South-East Asia

Australia Papua New

Guinea

Hong KongGreater China Korea

and Japan

London

Scandinavia

Switzerland and

European Union

WashingtonNorth and South

America

Global financial markets and booking

centers

Abu Dhabi

Singapore or Hong Kong

London

Key industry sectors

Financial institutions (Singapore)

Energy and resources (Abu Dhabi)

Aviation rail and transport

(Abu Dhabi)

Real estate and family conglomerates

(Abu Dhabi)

Traders and retailers (Abu Dhabi)

Cash and trade

Abu Dhabi

DCM

Abu Dhabi

Hong Kong

Advisory and specialized lending

Abu Dhabi

Banking hubs1Customer geographies Centers of excellence Operating centers

Abu Dhabi

(BCM in Al Ain)

One more location at a

future point (eg India

or Philippines)

ParisFrance and North Africa

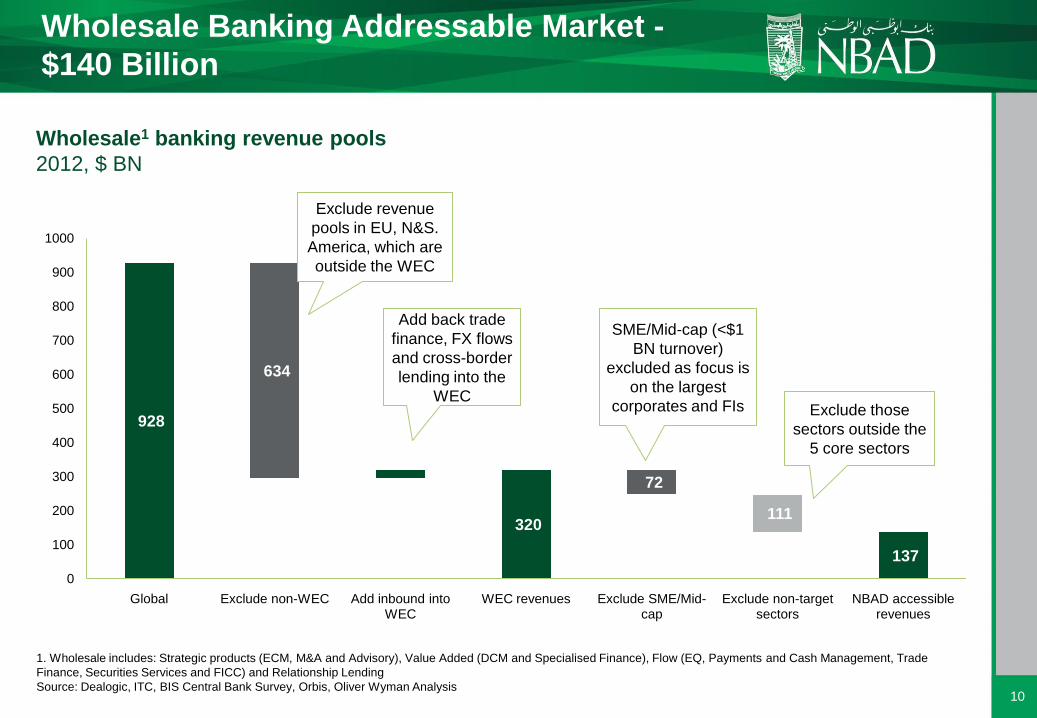

10

634

26

320

72

111

137

928

0

100

200

300

400

500

600

700

800

900

1000

Global Exclude non-WEC Add inbound into WEC

WEC revenues Exclude SMEMid-cap

Exclude non-target sectors

NBAD accessible revenues

1 Wholesale includes Strategic products (ECM MampA and Advisory) Value Added (DCM and Specialised Finance) Flow (EQ Payments and Cash Management Trade

Finance Securities Services and FICC) and Relationship Lending

Source Dealogic ITC BIS Central Bank Survey Orbis Oliver Wyman Analysis

Add back trade

finance FX flows

and cross-border

lending into the

WEC

SMEMid-cap (lt$1

BN turnover)

excluded as focus is

on the largest

corporates and FIs Exclude those

sectors outside the

5 core sectors

Exclude revenue

pools in EU NampS

America which are

outside the WEC

Wholesale Banking Addressable Market -

$140 Billion

10

Wholesale1 banking revenue pools

2012 $ BN

11

Strategic Update ndash Progress Report

11

Strategic 5-year Strategy developed and approved by Board

Streamlined the Group to 3 Core Businesses (Introduced new reporting

structure)

bull Global Wholesale

bull Global Wealth

bull Gulf Retail amp Commercial

New revenue campaigns across the business excellent pipelines

Streamlining operations and organisation structure

Building the Spine to a World Class Level

12

Results DiscussionMichael A Miller Head of Investor Relations

13

OPERATING INCOME REVENUES

Up 11 in 9M‟13 driven by higher NII and non-interest

income down 2 3Q‟13

3Q9M 2013 ndash Income statement highlights

13

OPERATING EXPENSES

Increased 10 y-o-y and 12 9M bdquo13 reflecting continued

investment in our business

IMPAIRMENT CHARGES net

Down 19 y-o-y and 5 9M‟13 vs 9M‟12

NET PROFITS

Down 8 year-over-year and up 14 9M‟13 vs 9M‟12

2250 2363 2194

6350 7067

3Q12 2Q13 3Q13 9M12 9M13

AED Mn+11

-2

728 795 801

2078 2323

3Q12 2Q13 3Q13 9M12 9M13

AED Mn+12

+10

367 301 299

971 921

3Q12 2Q13 3Q13 9M12 9M13

AED Mn

-5-19

1125 1212 1035

3212 3656

3Q12 2Q13 3Q13 9M12 9M13

AED Mn+14

-8

14

ASSETS

Up 56 sequentially as loans and deposits both grew

3Q9M 2013 ndash Balance sheet highlights

14

EQUITY

Up 34 sequentially due mostly to growth in profits

Includes AED 4bn Government of Abu Dhabi (GoAD) Tier-I capital notes

LOANS amp ADVANCES net

Up 52 sequentially as growth came from both the UAE

and internationally

CUSTOMER DEPOSITS

Up 46 with growth continuing to come from net inflows

of gov‟t deposits

305 301 322 327 345

Sep12 Dec12 Mar13 Jun13 Sep13

AED Mn+56

297 311 312 322 333

Sep12 Dec12 Mar13 Jun13 Sep13

AED Mn+34

163 165 162 173 183

Sep12 Dec12 Mar13 Jun13 Sep13

AED Mn+52

194 190 206 219 229

Sep12 Dec12 Mar13 Jun13 Sep13

AED Mn+46

15

Revenues by Segment

15

GB 2108

GFM 770

IBD 1002

DBD 1445

Islamic 195 GW 249

HO 581

9M12

GB 2102

GFM 884

IBD 1178

DBD 1564

Islamic 218 GW 320

HO 801

9M13 (Old)

GWB 3593

RampC 2197

GW 516

HO 762

9M13 (New)

51

7

31

11

AED mn

REVENUES 6350 7067Up 11

Note In the new structure the segment previously referred to as IBD has been allocated across the 3 major business segments

Contribution

16

GB 1926

GFM 669

IBD 684

DBD 806

Islamic 122 GW 101

HO (36)

9M12

GB 1893

GFM 763

IBD 806

DBD 869

Islamic 142 GW 161 HO 110

9M13 (Old)

GWB 3111

RampC 1203

GW 355

HO 75

9M13 (New)

Operating Profits by Segment

16

AED mn

OPERATING PROFITS 4272 4744Up 11

66

7

25

2

Note In the new structure the segment previously referred to as IBD has been allocated across the 3 major business segments

17

Key Ratios

17

Ratio 9M 2012 9M 2013

Efficiency

Diluted Earnings Per Share (EPS in AED) (restated for 2012) 069 079

Return on Equity (regulatory capital)(annualised including Govt of Abu Dhabi Tier-I capital notes)

153 151

Net Interest Margin (NIM)(Based on average total assets and annualised NII for the period)

216 200

Cost ndash Income ratio 327 329

JAWS (Revenues growth less Expenses growth)

-73 -05

Liquidity

Percentage lent(Loans Assets)

54 53

Loans to Customer Deposits ratio 84 80

Solvency

Capital adequacy 201 178

Tier-I ratio 158 161

Leverage ratio(Assets Equity)

102x 104x

Asset

Quality

Non-performing loans ratio[NPLs (Gross loans ndash Interest in Suspense)]

331 332

Specific Provision coverage(Specific Provisions NPLs)

525 534

Collective Provision coverage(Collective Provisions net Credit-risk weighted assets)

152 156

18

Summary of Expectations ndash FY2013

18

Top line revenue growth 7 - 8

Expense growth 10 - 11

Balance sheet growth driven by lending growth 10 - 15 and deposit

growth of 12 - 16

Provisioning expected to reduce gradually as we reach peak delinquency

levels NPLs to peak below 375 of performing loans

Simplificationflattening of organisation

19

Corporate access links

Corporate Headquarters

One NBAD Tower Sheikh Khalifa St

PO Box 4 Abu Dhabi UAE

Tel +971-2-6111111

Fax +971-2-6273170

Website httpwwwnbadcom

investorrelationsnbadcom

Michael Miller

Head ndash Investor Relations

Abhishek Kumat

Investor Relations

Khuloud Al Mehairbi

Investor Relations

Ehab Khairi

Corporate Communications (Media amp PR)

20

Appendix

21

What we want to change ndash

our mission to be core to our chosen customers

VisionTo be recognised as the

Worldrsquos Best Arab Bank

Mission Be core to our chosen customers helping them grow by providing

exceptional products and services across our West-East Corridor and

provide an environment to attract and develop exceptional and

diverse talent

Our

Values Value our people

and foster great

team work

Put our customers

at the forefront and

ldquodo the right things

the right wayrdquo

Respect our heritage

and be loyal to our

stakeholders

Customer

Value

Proposition

SafetyRelationshipConnected ServiceInsight

21

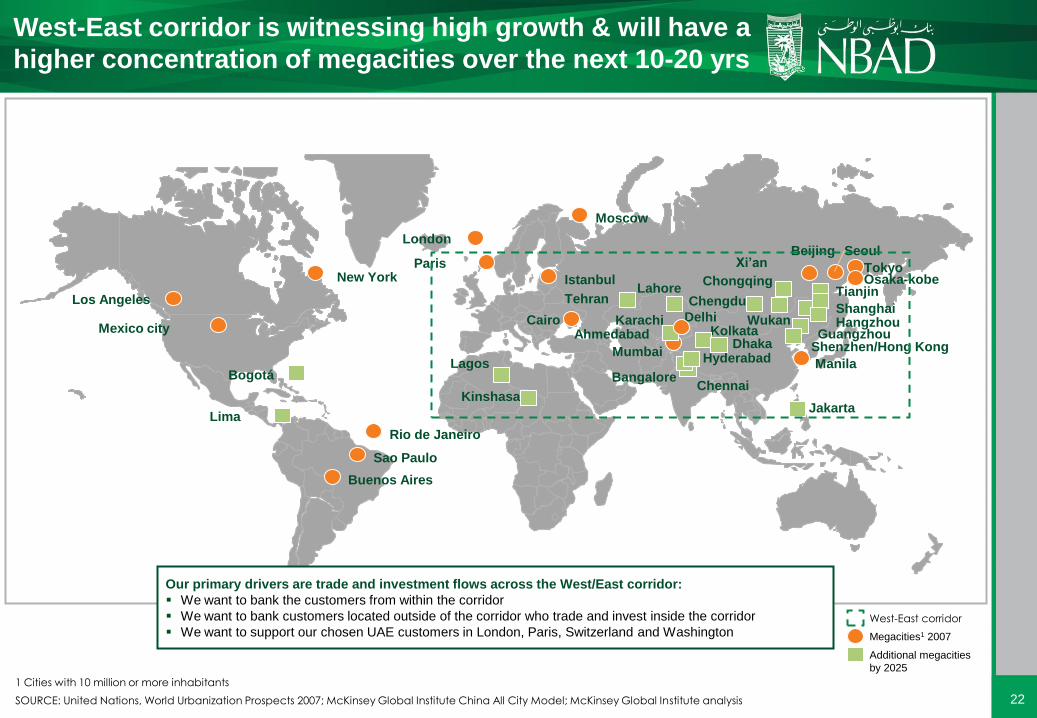

22

West-East corridor is witnessing high growth amp will have a

higher concentration of megacities over the next 10-20 yrs

SOURCE United Nations World Urbanization Prospects 2007 McKinsey Global Institute China All City Model McKinsey Global Institute analysis

1 Cities with 10 million or more inhabitants

Megacities1 2007

Additional megacities

by 2025

West-East corridor

Los Angeles

Mexico city

Bogotaacute

Lima

Rio de Janeiro

Sao Paulo

Buenos Aires

London

Paris

Moscow

Cairo

Lagos

Kinshasa

Istanbul

TehranLahore

KarachiAhmedabad

Mumbai

BangaloreChennai

Hyderabad

Delhi

Chengdu

KolkataDhaka

Chongqing

Xi‟anBeijing Seoul

Tianjin

ShanghaiHangzhou

Guangzhou ShenzhenHong Kong

Manila

Jakarta

TokyoOsaka-kobeNew York

Wukan

Our primary drivers are trade and investment flows across the WestEast corridor

We want to bank the customers from within the corridor

We want to bank customers located outside of the corridor who trade and invest inside the corridor

We want to support our chosen UAE customers in London Paris Switzerland and Washington

22

23

Operating Income amp Expenses

Interest vs Non-Interest Income (AED mn)

2250 23182510

23632194

69 6761

7175

31 33 39 29 25

3Q12 4Q12 1Q13 2Q13 3Q13

Non-Interest Income Net Interest amp Islamic Financing Income

Composition of Non-Interest Income (AED mn)

Net fee and commission income 81

Net gain on investments

2

Net foreign exchange

gain15Other

operating income

2

AED 555mn (Q3rsquo13)

Operating Expenses (AED mn)

494 512 505 543 545

173 229

159 192 193

49 47 48 52 52 11 2 15 8 11

728 790 727 795 801

3Q12 4Q12 1Q13 2Q13 3Q13

Staff costs Other general amp admin expenses

Depreciation Donations and charity

Key points

bull Q3‟13 Net Interest income of AED 16bn up y-o-y by 56 on

higher volumes amp lower interest expenses

bull Q3‟13 Non-interest income of AED 555mn down 20 y-o-y

due mainly to lower investment income and gains on hedging

strategies in Q3‟12

bull Net fee and commission income up 185 y-o-y in Q3

bull Expenses of AED 801mn higher by 10 y-o-y

23

24

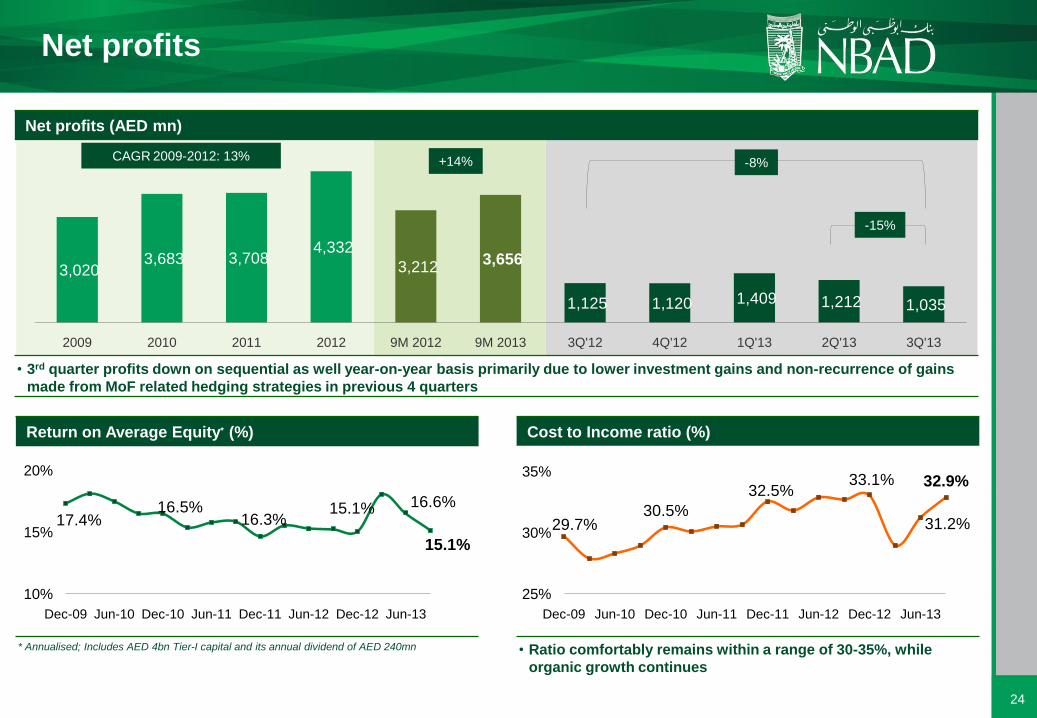

Net profits (AED mn)

bull 3rd quarter profits down on sequential as well year-on-year basis primarily due to lower investment gains and non-recurrence of gains

made from MoF related hedging strategies in previous 4 quarters

3020 3683 3708

4332

3212 3656

1125 1120 1409 1212 1035

2009 2010 2011 2012 9M 2012 9M 2013 3Q12 4Q12 1Q13 2Q13 3Q13

Cost to Income ratio ()

bull Ratio comfortably remains within a range of 30-35 while

organic growth continues

Return on Average Equity ()

Annualised Includes AED 4bn Tier-I capital and its annual dividend of AED 240mn

Net profits

CAGR 2009-2012 13

174165

163151 166

151

10

15

20

Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13

297305

325331

312

329

25

30

35

Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13

+14

-15

-8

24

25

Composition of Assets ndash AED 345bn

bull A very liquid balance sheet structure

Key points

bull Margins compressed by 11bps to 195 in Q3 from Q2 as

shorter duration low-yielding assets increased whilst still

impacted by higher deposits placed across various classes of

liquid assets like cash and inter-bank markets

bull Optical loans to deposits ratio at 80 at end-Seprsquo13

emphasis on increasing stableterm borrowings

bull Regulatory loans to stable resources ratio well within

stipulated UAE Central Bank cap

bull Framework ready to be compliant with regulations on

(Basel-III) liquidity

Loans amp Customer Deposits (AED bn)

Net Interest Margin ()

NIM (Qtr) - based on Net Interest amp Islamic financing Income (annualised) amp total average

assets for the quarter NIM (Ytd) ndash based on total average assets for the period

Assets amp liquidity

216

206

197

206

195

216

219

197205

200

3Q12 4Q12 1Q13 2Q13 3Q13

NIM (Qtr) NIM (Ytd) Cash amp balances

with central banks15 Due from

banks amp Reverse

repos15

Investments13

Loans53

Fixed assets amp Other assets

4

163 165 162173

183194 190

206219

229213 209

225241 249

3Q12 4Q12 1Q13 2Q13 3Q13

Loans Deposits Deposits + Term Borrowings

25

26

112132 137

160 165 183

2008 2009 2010 2011 2012 9M13

Loans (net) - growth trend (AED bn)

CAGR 2008-9Mrsquo13 11

bull Lending momentum continued in 3Q with loans increasing by 5 in

the quarter taking the year-to-date growth to 11

Loans (gross) by customer type

bull Stronghold in Corp amp Private sector amp Government related businesses

bull Lucrative opportunities for short-term lending ndash trade-finance related

activities albeit at lower margins

Loans (gross) by industry

bull Diversified portfolio across economic sectors

bull Retail loan growth to remain challenging

Loans by geography

Based on location of booking of the loan

Loans and advances

UAE73

Europe17

GCC2

MENA (ex-GCC)2

Asia5

USA1

Real Estate17

Govt12Construction

2

Energy12

Personal loans for

consumption 9

Loans to Individuals

for Business7

Banks amp FI17

Trading3

Transport4

Services12 Mfg

4

Others (incl Agriculture)

01

Govt 1212

Public Sector 2425

CorpPvt 3435

Individuals 1516

Banks 1512

+109

2012

(AED 1708bn)

9M 2013

(AED 1894bn)

3736

+109

26

27

Provisions amp NPLs (AED mn)

bull NPLs ratio at 332 at end-9M‟13 (34 at end-2012) Provisions on loans amp advances - excludes all other provisions

Provisions amp NPLs

Key points

bull Strong asset quality ndash one of the lowest NPL ratios amongst

major UAE banks

bull NPL ratio of 332 at end-9Mrsquo13 (34 at end-FYrsquo12) NPLs

increased by AED 143mn in 3Qrsquo13 ndash incremental NPLs have

declined for the past 11 quarters

bull Specific provisions at 534 of NPLs at end-9Mrsquo13 (end

FYrsquo12 ndash 534) in addition to collaterals

bull Collective provisions at AED 2771mn continue to be fully

compliant with the Central Bank of UAErsquos minimum

requirement of 15 for collective provisions well ahead of

the effective date (year end 2014)

5380 5518 5650 58226114

2451 2428 2428 25572771

5578 5781 5961 6121 6264

2009 2010 2011 2012 9M 13

Total Provisions Collective Provisions NPLs

27

28

NPLs (NBAD vs UAE Banks)

Average NPL ratio of ENBD NBAD ADCB FGB (Source NBAD Published financials)

NPLs above as stated by the banks as impaired loans and advances

Provisions amp NPLs (hellipcont‟d)

Provision coverage (NBAD vs UAE Banks) ndash 9M‟13

bull High provision coverage (in addition to substantial collaterals) NPLs and Coverage ratios above as disclosed by the banks

6264

35898

5900 5109 98

55

105 75

NBAD ENBD ADCB FGB

NPLs Provisions Coverage (total) AED mn

125

231294

3403329Mrsquo13

27

74 71 67

769Mrsquo13

Dec-09 Dec-10 Dec-11 Dec-12

NBAD Average

Impairment charges amp Addition to NPLs (AED mn)

bull NPLs increased by AED 143mn in 3Q‟13 ndash additions to NPLs declining

since last 11 quarters

Impairment charges (AED mn)

9M 2013 9M 2012

Charge for the period

Specific provisions 1025 1266

Collective provisions 343 130

1368 1396

Recoveries amp write-backs (481) (549)

Write-offs 19 50

Provisions for other impaired assets 15 74

Impairment charges net 921 971

367 365 322 301 299

54 162

-

129

214 234 203 180 160

143

3Q12 4Q12 1Q13 2Q13 3Q13

Total Impairment charges net

Collective prov charges

Addition to NPLs

33 141 46 39

NPL ratio

28

29

Investments ndash AED 457bn

bull HFT ndash AED 28bn HTM ndash AED 35bn AFS ndash AED 394bn

HFT - Debt4

HFT - Equity amp Funds

2

Held to Maturity (Debt)

8

AFS - Equity amp Funds

03

AFS - Debt86

Investments by issuer

Investments by ratings

bull 78 of Investment book is rated A amp above

Investments by region

Based on location of the issuer of the security or parent in case of SPVrsquos

Investments

Sovereign30

Govt Related Entities

22

Banks amp FIs -Sovereign

Guaranteed3

Banks amp FIs -Covered Bonds12

Banks amp FIs29

Corporate Pvt Sector

3

Supranational1

Europe 262

GCC 190

MENA (ex-GCCampUAE)

59

USA 25

Australia amp Others 71

UAE 392

AAA 115

AA 457

A 211

BBB 53

BB amp below 71

Unrated -Debt 71

Equity amp Funds 23

29

30

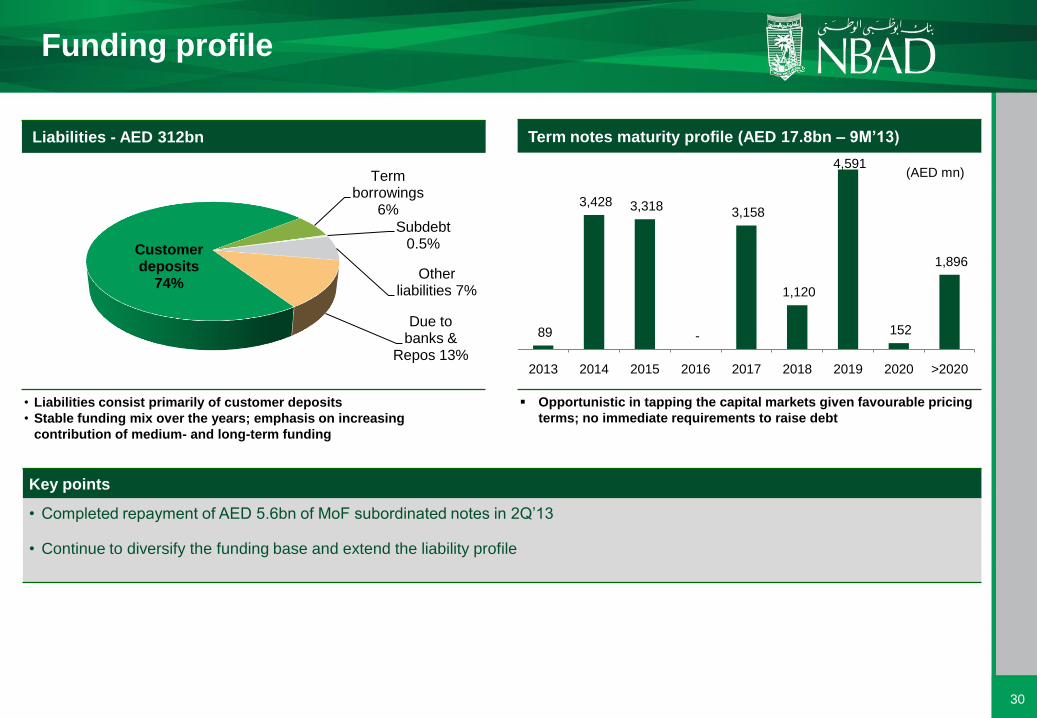

Term notes maturity profile (AED 178bn ndash 9M‟13)

Opportunistic in tapping the capital markets given favourable pricing

terms no immediate requirements to raise debt

Key points

bull Completed repayment of AED 56bn of MoF subordinated notes in 2Qrsquo13

bull Continue to diversify the funding base and extend the liability profile

Funding profile

Liabilities - AED 312bn

bull Liabilities consist primarily of customer deposits

bull Stable funding mix over the years emphasis on increasing

contribution of medium- and long-term funding

89

3428 3318

-

3158

1120

4591

152

1896

2013 2014 2015 2016 2017 2018 2019 2020 gt2020

(AED mn)

Due to banks amp

Repos 13

Customer deposits

74

Term borrowings

6

Subdebt 05

Other liabilities 7

30

31

Key points

bull YTD 206 growth in deposits across all customer types ndash

government GREs corporate and retail customers

bull Substantial funding from government amp public sector entities

reflecting our long standing relationship with them

Deposits by customer type

bull Substantial funding from government amp public sector entities

reflecting our long standing relationship with them

Govt 3336

Public Sector 2019

CorpPvt 24

25

Individual 23

20

Customer deposits

+206

Deposits growth trend (AED bn)

bull Steady and substantial growth in customer deposits

2012

(AED 1903bn)

9M 2013

(AED 2295bn)

55

5398 116 123

152190

229

2008 2009 2010 2011 2012 9M13

Deposits by geography

Based on location of booking of deposit

UAE78

Europe12

GCC1

MENA (ex-GCC)4

Asia3

USA2

CAGR 2008-9Mrsquo13 20

31

32

Regulatory Capital resources (AED bn)

293 304 305

318 327

372 373

347 350 361

Sep-12 Dec-12 Mar-13 Jun-13 Sep-13

Tier-I Capital Resources

Capital adequacy ()

201210

197185

178

158172 173 168 161

8

12

Sep-12 Dec-12 Mar-13 Jun-13 Sep-13

Total CAR Tier I

Capital Resources (Basel-II)

UAE CB CAR requirement

Minimum Tier-I requirement

Key points

bull Capital Resources (Basel-II) of AED 361bn down 3 y-o-y

after repayment of AED 56bn MoF notes

bull Tier-I capital of AED 327bn up 116 y-o-y on higher

earnings

bull Capital Adequacy ratio (Basel-II) at 30 Sep 2013 at 178

and 161 on Tier-I well above the Basel-II and UAE Central

Bankrsquos minimum requirements of 12 and 8 respectively

9M 2013 Tier-I Tier-II Total

as at Dec 2012 30411 6855 37266

Net profits (year-to-date) 3656 - 3656

Dividends paid (1599) - (1599)

Change in eligible Collective Prov 256 256

Change in eligible AFS reserve - (73) (73)

Change in Subdebt (incl MoF

Repayment amp Buyback of subdebt)- (3678) (3678)

Others (incl shares under ESOP) 280 5 285

as at Jun 2013 32748 3365 36113

32

33

Results at a Glance

2Q13 3Q13

growth3Q12

growth9M13

growth

Income statement (AED mn)

Net Interest Income (incl income from Islamic f inancing)

1672 1640 -19 1553 56 4848 68

Other Income 691 555 -198 697 -204 2219 225

Revenue 2363 2194 -71 2250 -25 7067 113

Expenses (795) (801) 08 (728) 101 (2323) 118

Operating Profits 1568 1393 -112 1522 -85 4744 110

Impairment Charges net (301) (299) -07 (367) -186 (921) -52

Prov for Taxes (56) (59) 67 (31) 945 (166) 866

NET PROFIT 1212 1035 -146 1125 -80 3656 138

Balance Sheet (AED bn)

Assets 327 345 56 305 133 345 133

Loans amp Advances 173 183 52 163 120 183 120

Deposits amp Others 219 229 46 194 185 229 185

Ratios

RoE (regulatory capital) 153 126 -26 155 -29 151 -01

NIM 206 195 -11bps 216 -21bps 200 -16bps

Cost Income 336 365 29 323 42 329 02

JAWS -79 54 -126 -05 -05

AED mn

33

34

Balance sheet

AED bn

Balance Sheet Jun13 Sep13 growth Sep12 growth Dec12 growth

Assets

Cash amp Balances with

Central Banks544 519 -45 411 263 549 -56

DFB amp Reverse Repos 442 508 151 539 -56 331 535

Investments 397 457 151 330 384 356 285

Loans amp Advances 1735 1825 52 1629 120 1646 109

Short term (lt1 yr) 684 772 129 544 419 608 271

Long term 1050 1053 02 1085 -30 1038 14

Other Assets 151 142 -58 136 41 124 147

Total Assets 3267 3451 56 3045 133 3006 148

Liabilities amp Equity

DTBReposECPs 357 457 282 409 116 403 134

Deposits amp Others 2194 2295 46 1936 185 1903 206

CASA 499 514 30 426 206 447 148

Others 1695 1781 51 1511 179 1456 224

Term BorrowingsSubdebt 229 209 -90 266 -214 247 -156

Short term (lt1 yr) 25 38 550 28 357 28 349

Long term 205 170 -167 237 -283 219 -222

Other Liabilities 166 158 -49 136 155 141 118

Capital amp Reserves 322 333 34 297 120 311 70

Total Liabilities amp Equity 3267 3451 56 3045 133 3006 148

34

35

Disclaimer

The information contained herein has been prepared by National Bank of Abu Dhabi PJSC (ldquoNBADrdquo) NBAD relies on information

obtained from sources believed to be reliable but does not guarantee its accuracy or completeness

This presentation has been prepared for information purposes only and is not and does not form part of any offer for sale or

solicitation of any offer to subscribe for or purchase or sell any securities nor shall it or any part of it form the basis of or be relied

on in connection with any contract or commitment whatsoever

Some of the information in this presentation may contain projections or other forward-looking statements regarding future events or

the future financial performance of NBAD These forward-looking statements include all matters that are not historical facts The

inclusion of such forward-looking information shall not be regarded as a representation by NBAD or any other person that the

objectives or plans of NBAD will be achieved NBAD undertakes no obligation to publicly update or publicly revise any forward-

looking statement whether as a result of new information future events or otherwise

35

36

SKEA Diamond Winner 2013

THANK YOU

Winning this prestigious

award would not have

been possible without

our customers

shareholders and every

member of NBAD staff

NBADrsquos ongoing journey

of excellence will

continue

Transcription for NATIONAL BANK of ABU DHABI

October 30th 2013

Corporate Participants Michael Miller National Bank of Abu Dhabi ndash Head of Investor Relations Alex Thursby National Bank of Abu Dhabi ndash Group Chief Executive Officer Abhijit Choudhury National Bank of Abu Dhabi ndash Group Chief Risk Officer Jamil ElHalabi National Bank of Abu Dhabi ndash Group Chief Financial Officer Stephen Jordan National Bank of Abu Dhabi ndash Group Treasurer Abdulla AbdulRaheem National Bank of Abu Dhabi ndash Deputy Group Chief Executive Officer

Conference Call Participants Nisreen Assi Arqaam Capital Shabbir Malik EFG-Hermes Vikram Viswanathan HSBC Aarthi Chandrasekaran NBK Capital

Presentation Operator Good afternoon ladies and gentlemen and welcome to NBAD Third Quarter 2013 Financial Results Conference Call I will now hand over the call to Michael Miller Head of Investor Relations at NBAD Sir you may begin

Michael Miller Good afternoon and welcome to National Bank of Abu Dhabirsquos Third Quarter 2013 Results call Today Alex Thursby our Group Chief Executive Officer

will provide some highlights from the third quarter and then we will provide some more details on the strategic vision for the Bank followed by a strategic update highlighting some of the progress we have made to date After his remarks I will provide an overview of the results for the third quarter and first nine months of 2013 During the call we will be referring to our Performance Review which is available on the Investor Relations portion of our website Following the prepared remarks we will open up the lines for QampA and for that portion of the call we have in the room Abdullah AbdulRaheem Deputy Chief Executive Officer Abhijit Choudhury Group Chief Risk Officer and Stephen Jordan our Group Treasurer Now I will turn it over to Alex

Alex Thursby Thank you Michael and good afternoon everyone I just want to first of all just to give you some overview of how I see the third quarter and you will see me talk about quarter-on-quarter a lot and you can expect me to do that in the future as we look forward to give you more transparency as to the actual performance of the Bank how wersquore going against the drivers that we set out This quarter was a normalisation We tried to highlight as best we could to you in the end of the second quarter so you see now the rural business or the true operating performance of the business in this quarterrsquos results This is the Third quarter for the last five that you now see that clear clarity on the performance of the Bank I am very pleased in a number of areas and there is some headway being made as we look to transform the Bank going forward and I will talk a little bit about that later on The headline for me is very much deposits and asset growth was more than acceptable and very pleasing particularly on the asset growth and to give you a little bit more insight a lot of the asset growth is in the short term tenure of the book and this is critical as we start to approach a more complex regulatory environment where liquidity judgment under Basel III and is being applied by the Central Bank here will start to have more effect on the industry than possibly has been acknowledged at this stage The second thing is that margin has been compressed and there are some reasons for that and I will go through those with you The first is that relative to our peers we are under-scale in the retail bank and therefore

the first wave of re-pricing of the asset side of the book tends to hit the corporate side and that has done so with us The second is that we are a custodian of liquidity and we have had a lot of liquidity over the last six months coming in from the Government and that we have found it difficult to place that liquidity in high-earning assets at acceptable risk so we have a lot of money currently with the Fed However going forward part of the transformation of the Bank is to use that natural competitive position of a strength of liquidity into short-term asset growth The third thing is that wersquore starting to see the average tenure of our book decrease again this is positive from a liquidity point of view but has a small effect on our earnings and we are also starting to see the effect of our lsquooriginate to distributersquo strategy which was started actually before my tenure but is continuing to be driven at a high pace If I may just go to the compression issue directly relative to pricing of risk in the market it is very clear to us that wersquore starting to see in the corporate side major compression on the Dubai marketplace and small compression issues in Abu Dhabi It is my view that that will continue in the industry and may intensify in certain parts of the industry but we have seen some greatly which started approximately six months ago I now want to talk about the non-interest income That area is very specific We had a lot of one-offs in that area but when you strip those one-offs we are quarter-on-quarter flat but that is ndash in the businesses that wersquore trying to grow has started to show some good increases in the businesses that wersquore trying to stop or some of the things that weve been doing in the past wersquore stopping wersquore seeing contraction Again I believe this is a good sign from my point of view is that wersquore starting to see the areas that we want to grow wersquore getting growth and the areas that we want to pull back from wersquore seeing that contraction That correction could take as long as six months to nine months from here but I think most of it will be finished by maybe the first quarter of next year and the last quarter of this year With regards to the provisioning we have decided that we want to go straight to a level of provisioning required by the Central Bank of 15 and we have provided to 156 we see that as a good balance but it is also interesting to note that with the good asset growth of around 5556 quarter-on-quarter we have taken an increased collective provision there but weve also increased the collective provisions in line with what is required from the Central Bank Those requirements will come into 2014 but weve gone early and we believe that wersquore well balanced in our approach with regards to provisioning

I think thatrsquos enough really just to give you a high level of where I see the results and if I can just quickly move through to slide four and emphasise or explain to you that we are clearly starting to move forward in some of the engagements with our clients but clearly the outstanding two things is the Sheikh Khalifa Excellence Award and just as importantly the upgrade now of our bank to AA- by SampP That now makes us as one of 25 ndash we think 25 ndash banks in the world that have that rating agency support of AA- and above This is very critical if we start moving into the next formation of our strategy For many of you yoursquove seen slide five so I wont both going through that again but I just want to highlight under slide six our views of why this West-East Corridor is so significant You can see through this the high growth rates that we expect to see in investment and trade flows over the next seven or eight years or so and that this represents a real opportunity for our bank particularly for our wholesale bank as we go through the strategy I want to give you a little bit of highlight as to the high level strategy that wersquore taking for our wholesale bank and you can expect to see over subsequent calls we will go through each of the businesses but I do want to highlight that pillar one of our strategy together with pillar two are our priorities and pillar one which is about strengthening our commercial business and retail business we will highlight to you possibly at the next quarterly call at the full year-end if not fairly soon after but I can assure you we have started to take action in this area already and you have already seen the launch of a new mortgage product which is very close to our positioning with the Central Bank with the new mortgage laws that are coming into play Our West-East Corridor strategy for the wholesale bank will be focused upon five key industry groups and wersquore already starting to reorganise ourselves in these five key industry groups (financial institutions energy and resources aviation real estate and family conglomerates and traders and retailers) Itrsquos about banking 800 clients across that Corridor over a period of the next five years and to start to get deep and meaningful with those clients rather than spreading ourselves over lots of clients with one-product capacity or two-product capacities With the closing margins not only in this market but as a global phenomenon cross-sell is critical to give you the ROE that wersquore looking for and that is absolutely significant in our strategy You also will see that part of the strategy on page eight formulates how we think We look at originating transactions and lending transactions and debt capital market transactions from the respective segments we use our balance sheet more as a warehouse It does not mean throwing out all of our fixed term loans ndash absolutely not ndash but what it does mean is that we circulate our balance sheet so that we can become core for the customers we choose This is critical but we also then start to develop a new form of customer for this

bank which is the financial institutions as we distribute that paper into the market and we have already commenced this in a meaningful What both avenues mean though is that in the financial institutions space we can further cross-sell into our markets positioning where I think weve done a good job over the last nine months under Mahmoodrsquos leadership together with Rola but just as importantly in the trade finance area where we have a lot more work to do going forward Cross-sell on the origination side that is with our corporate customers in the segments that I mentioned is very obvious and we will be focusing on our cross-sell build-out and you should expect to see over the foreseeable future a continuation of the growing on non-fee income as we develop that cross-sell particularly in FX and particularly in trade and on a broader platform wealth The issue then is how do we cost effectively build a model across the West-East Corridor servicing 800 clients across five industry segments Clearly we will use the Gulf in the Middle East as our key area where we service clients from our Abu Dhabi and Dubai offices It is our intent in the long run but not immediately to build out Mumbai and Lagos to service customers from their respective areas We also will be upgrading our Hong Kong office immediately and our London office immediately as we continue to build out our markets capacity and our trade capacity in our London office and we will be doing so the same in Singapore which will be the priority country for the next six months in order to get a new license Our focus is on building out London for our customers who deal in the Corridor (that has commenced) and building out Singapore as a new operational area for those customers from Southeast Asia and for those who operate within that Paris and Washington will be like London as [flow] country and weve already started the upgrading of those offices but there is still a way to go This is very important This is not about putting flags on maps in every place This is about choosing the customers that you want to be core to and putting a operational platform and locational platform in order to service them We do not need to have multiple branches in every place in Asia the Middle East or Africa to be successful with our high value wholesale customers If I can now then just move to the next slide which is part of our strategic deck that we are putting together as they all are this will give you some idea of what we see as the assessable wallet for ourselves We have taken the wholesale banking revenue pool we have excluded those who are no longer within the West-East Corridor and we have added what we call lsquoin-boundrsquo that is business that comes outside the Corridor into the Corridor That gives us an idea that we have approximately $320 billion of corporate and commercial revenue wallet inside the West-East Corridor Weve then

excluded the SME middle-cap and weve also excluded our non-target segment We believe the assessable wallet for the industries that we operate in is approximately $140 billion of wallet What wersquore also coming to the conclusion is that 53-58 and sorry I cannot be more precise than that is wallet that comes from flow products (cash trade FX) This is critical This is a fundamental change in the way that we have dealt business before where our corporate lending book has been the pre-determinant or the driver of profitability and profit growth Going forward we will use our balance sheet and lending as an anchor through which then to develop the biggest form of the wallet This has huge consequences not only in terms of the business model but in the risk profile and it is in my humble view that the risk profile of the Bank will further improve through this wholesale strategy not deteriorate But above it all it is built around the customers rather than around what products do I want to do and then decide the rest later and this is a fundamental difference for many banks globally who have preceded I just quickly want to turn to page 11 for you and quickly go through what weve done in the last quarter We have already commenced ndash this is fairly obvious ndash our strategy on the wholesale bank and wersquore expecting to present that to our Board either December or January in its fullest extent We have also started our strategy for the commercial business here in the UAE and I will again hopefully be able to give you more information of that We are clearly changing our business model where we see ourselves as a fantastic opportunity to develop a substantive commercial segment We believe that we currently stand at the momenthellipwersquore about a 2 market share player and we are massively under-scale and we see this as a real opportunity for growth in the longer run but it is a momentum business and it will take a little while to build that momentum so please donrsquot have 30 growth in your quarter four earnings We have started off various new campaigns and pipelines including in trade and I am very pleased to suggest that our short-term assets within that asset growth or loan growth has moved to 125 growth in the last quarter That is a very good start to what we hope is a continuing trend over the next year or so We have also started our streamlining of the organisation We have reorganised in many parts of the Bank at the very top level and the direct reports to myself and their direct reports and wersquore now moving through the organisation and we are redeploying resources into other areas where we want to grow We think there are some continuations of costs that can be taken out of the business but we see that as an opportunity to invest into the business rather than taking a quarterly positive cost effect That streamlining has commenced and will continue in terms of many of its facets probably into February of next year

We are also starting to look and I think this is important from your area at building the spine and the strength of the Bank in terms of its MIS in terms of the way that we look at product profitability in terms of building out better capabilities in our systems etc and I wont bore you through going through all the actions there but you will see next year from the first quarter of next year full transfer pricing full cost allocation and full cost allocation of selective provisioning into the businesses This is a critical ingredient to see the real profitability of businesses and product groups as we move forward In summary I am very excited about what the opportunities for this bank show You now have the real position of the Bank We are in a more difficult operating environment here in the UAE but we are growing so we are correcting things that we think need to be corrected and then moving forward in things that we think are the future growth areas We have started that process but there is much more to do over the next 18 months or so On that note I will pass you back to Michael to give you a more detailed explanation of the result and then for me to give you some guidance

Michael Miller Thank you As Alex mentioned there our performance reflects a continued strength in the third quarter overall we are starting to see signs of momentum as our balance sheet continues to grow through lending and deposits In the quarter top and bottom line growth was muted somewhat as hedging gains related to the repayment of the Ministry of Finance notes we had seen over the past four quarters did not recur and these will not repeat again This was in line with our expectations and in line with our previous communications Now turning to page 13 operating revenue growth was 11 for the first nine months of 2013 compared to the first nine months of 2012 driven by a higher net interest income and non-interest income Operating expenses were up 12 for the nine-month period for nine months 2013 versus the first nine months of 2012 and 10 year-over-year for Q3 reflecting continued investment in our business Impairment charges were 299 million in the third quarter and 921 million for the first nine months of the year reflecting decreases of 19 and 5 respectively Net profits were up 14 for the first nine months of the year to AED 3656 billion reflecting solid growth trends Third quarter 2013 profits were down 8 and the decline was driven again by the non-repeating hedging gains that we saw over the past four quarters

Now turning to the balance sheet on page 14 assets increased to 345 billion up 148 year-to-date and 56 sequentially driven by growth and lending in deposits Equity grew 34 sequentially to 333 billion in the September quarter due to growth in profits Sequentially customer loans were up 52 and customer deposits were up 46 as we saw growth in deposits across customer types Turning to page 15 on the next two slides we have shown the breakdown for revenues and operating profit by segment under our previous reporting structure for the first nine months of 2012 and 2013 and then we have also shown the new reporting segments for the first nine months of 2013 (global wholesale banking retail and commercial global wealth and head office) Going forward we will report based on this new structure and so for revenues of 7067 billion during the first nine months of 2013 the global wholesale banking division contributed 51 retail and commercial 31 global wealth 7 and head office 11 On slide 16 you can see that the breakdown for operating profits of AED 4744 billion for the first nine months of 2013 with 66 global wholesale bank 25 retail and commercial 7 global wealth and 2 head office Turning to the key ratio slide on 17 we look at these from an efficiency liquidity solvency and asset quality perspective for the first nine months of 2013 efficiency ratios were diluted EPS of AED 079 representing growth of 147 year-over-year return on equity was 151 net interest margin was 2 for the first nine months of 2013 down from 216 during the same period in 2012 The cost to income ratio was 329 essentially flat with 327 for the first nine months of 2012 Now for the liquidity ratio percentage lent was 53 so 53 of our balance sheet is lent to customers in the form of loans and deposits Our loans to deposits ratio was 80 Next the solvency ratios capital adequacy of 178 Tier 1 ratio of 161 and leverage of 104 times Finally asset quality ratios the NPL ratio was 332 which is within the peak of 375 we have measured in the past and as we have told you before rather than looking at total provisioning coverage which is provisions over NPLs and was 976 in the third quarter of 2013 we prefer to look at the specific and collective coverage separately and both are shown here Specific provision coverage was 534 in addition to collateral and collective provision coverage was 156 which is in compliance with the Central Bank requirement of 15 and goes into effect in 2014

Now to the final slide to go over guidance I will turn it back over to Alex

Alex Thursby Thank you very much Now I just want to re-emphasise to you the critical thing around now that we have normalisation of our quarterly earnings so we do expect top line revenue growth still to remain somewhere in the 7 to 8 We believe that there would be potentially some more margin compression but that will be offset with good loan growth somewhere in the vicinity of 193 to 195 billion ndash not growth but final outstandings Expense growth could be somewhere in the vicinity of 10 to 11 as we continue to invest in the business but we also take some one-off charges that are required as we move forward with the restructuring of the business end-to-end We see good deposit growth continuing wersquore ahead of that at the moment but I think itrsquos very difficult to predict the flows of what is our natural habitat with the Government so Im being a little bit conservative together with the team here in NBAD in terms of this but clearly we have had very strong deposit growth and that bodes well for the future as our expectation Provisioning I think has reached its peak and our NPLs as you can see have slightly gone down in the quarter We would expect that to continue at similar rates but we certainly donrsquot see a bad upside beyond 375 you will continue to hear of the simplification of flattening our organisation as we execute that and that will be critical going forward in terms of putting our costs into better areas of growth On that note I think if I can now pass on to QampA and the team here will endeavour to answer all of your questions I have got Abhijit Stephen and Abdulla in addition to Jamil so wersquore happy to take any questions and answer them as best we can for you within normal confidentiality Over to you guys

Question and Answer Session Operator Ladies and gentlemen if you wish to ask a question please press 01 on your telephone keypad Thank you for holding until we have the first question We have a question from Nisreen Assi Arqaam Capital Please go ahead

Nisreen Assi Good afternoon everyone thank you so much for the conference call Okay so the lending growth expected for the full year is down to 15 could you please explain what factors will be driving this growth and will you be targeting higher yielding sectors For the fees and commission income growth what are your expectations going forward Thank you

Alex Thursby Let me take onhellipI have given you a highlight to where we see our growth in the loan book The predominant nature of where that will come from our loan book in the retail side is growing well but it is a small proportion of the total balance sheet and we specifically see that in credit cards personal loans but increasingly mortgages will become a significant business for us not only for the next quarter but for future quarters other than that and you see that with the launch of the product that we have just made which is a very interesting product because it discounts rate relative to risk and this segmentation of risk and return in the marketplace is quite innovative we think in the mortgage side We will also be very targeted of where wersquore trying to put that product into the market and we do see good growth in mortgages on the whole but we do see that there are low risk parts of the business that we really want to be very critical on and I go back to my very first date of the bank where I said to you guys that segmentation is key The largest part of our growth will come out of the short-term lending book on the wholesale side and that will be predominantly around trade in the immediacy over the next quarter and we see that area as being not only a phenomena here in the UAE but also in a broader platform across the West-East Corridor I do want to emphasise though we are doing term assets but we are focusing more on the key segments that we wish to so you can start to see us continuing to grow in our lease finance area for the airline industry is one example where we see good credit risk and also good cash flow ensuring that we maintain a sustainably good book in the wholesale area In summary retail will continue to grow but it is starting from a much smaller base and trade finance with a little bit of growth in the term loan book In regards to fee income wersquore starting to see in the last month of the last quarter wersquore starting to see some momentum around foreign exchange particularly and some of our loan fees as well and establishment fees We would expect that to continue We also expect trade finance to be growing in the new business that we want to do but we will have some offsets as we

withdraw from certain markets in our trade finance business so you wonrsquot start to really see growth in that area in the fee income area to possibly to the thirdsecond quarter of next year As I said our real ndash when you take all the one-offs we were flat quarter-on-quarter and it is difficult to say next quarter whether we will be flat or slightly up but it will depend on the run-offs that we have on the businesses that we do not wish to continue but in the longer run this will be a big driver of the bankrsquos profitability as we move forward and we are gearing up our investment particularly in markets and wealth management to facilitate that We are actually seeing good growth in some of our wealth management fees but again it is a small business relative to the whole bank as a whole so it will take a little time for that to come

Nisreen Assi Okay thank you and if you may allow me one more follow-up question Do you have any plans in the short-term for bond issuances

Alex Thursby We are very liquid at the moment in our position and I will leave it at that very liquid

Nisreen Assi Okay thank you

Alex Thursby We have lots of plans for bond issuance for our clients

Nisreen Assi Thank you so much

Operator We have a question from Shabbir Malik EFG-Hermes Please go ahead

Shabbir Malik Thank you very much for the presentation this is Shabbir Malik from EFG-Hermes I had a question about your profitability Your ROE in the nine months was about 15 and ROA I guess was about 15 and this number

includes some one-offs In your view what would be a sustainable ROA or an ROE level for the bank and what kind of time horizon are we looking at in order for you to achieve that and what would be the drivers of that improvement if you see an improvement in this Secondly earlier on in the presentation you talked about growth in certain areas of growth in fee income and areas of contraction If you could just highlight once more what those were ndash the areas of growth and areas of contraction that would be good

Alex Thursby I will let Michael repeat what I said for the second part and I will take the first part of the question because I think it is a very good question In the medium-term I believe that an adequate ROE for a bank of our type is somewhere in the vicinity of 15 and that we may oscillate down and up over the next year to 18 months above that and below that but that is our target ROE in the medium-term for this business The simple reason is that I believe it is a continuing trend that some of the ROEs not only here in the UAE but globally have been inflated with very rich margins after the prices and I think what wersquore beginning to see that as you start to normalise return and I just want to give you an idea our spread in 2010 was 257 today as you all know it is around 195 If you go further back it was 195 so we have had the hump on the camelrsquos back so to speak so wersquore returning and normalising How do you retain that while also taking a lower risk is very simple you create velocity within the Wholesale Bank which tends to be your ROE drag products and you develop more ROE through your flow business in the Wholesale Bank The ROE in the Retail Bank that is fully matured tends to be quite positive so continuing to invest in our retail business and trying to work out how we can grow aggressively is what wersquore working on will also be a key driver In addition continuing to develop our wealth product proposition our Private Bank proposition is also other areas but I would put the first two as the major drivers for right now so continuing to develop non-fee non-interest income from foreign exchange trade various other payments collections continuing to develop our Retail Bank aggressively is the way that we will get to our ROE targets on a sustainable way but I do want to highlight for you that ROEs I think will oscillate both up and down a little while as we invest in the business and we do some correction of the business as the previous was so please donrsquot take one quarter as being 17 and being a model for the future Conversely if you get 12 donrsquot take that

as being a model for the future either We want to oscillate on or around that 15 over time What I would point out to you is that if you put a taxed effect upon all of our banks there is room for improvement in ROE versus good international competitors

Shabbir Malik Good thanks and on the fee income the areas of growth in the third quarter and areas of contraction

Alex Thursby Michael if you wish to highlight that I think we have probably gone through it but again if youhellip

Michael Miller Sure on a year-over-year basis on a fee income perspective it came from a combination of stronger markets higher volumes increased lending in credit cards and the growth came mainly from two drivers which were lending fees and credit cards Some of the contractions I believe was in the areas of letters of credit with trade finance however what we expect going forward as we continue to capture more of those trade flows is that we would see that increase over time

Alex Thursby Just to reiterate there are certain forms of trade that we are pulling out of which will take us about nine months to get out of from here in a meaningful way

Shabbir Malik Thank you very much

Alex Thursby Just if I can add for you one more important thing is the long-term drivers of fees is wealth management trade markets DCM and for ROE improvement in addition to that retail and SME where again they also contribute to the non-funded income line

Operator We have a question from Mr Vikram Viswanathan HSBC Sir please go ahead

Vikram Viswanathan Good afternoon gentlemen thank you very much for hosting this call My question is on the capital side versus the current dividend pay-out ratio You obviously are a very well capitalised bank at this point in time Does it give you room to expand your pay-out ratio probably going forward Yes I think that is about it yes

Alex Thursby Look it is a very good question and I donrsquot think we have come to a final conclusion Wersquore comfortable at the current pay-out ratio so I think you can be reasonably sure that where they stand is a good base but we havenrsquot yet thought about that and I want to see some more capital planning over the five year plan as wersquore building for various businesses before we come to a conclusion What I will assure you is we will be transparent on that when we have come to that final conclusion but to give you a little bit of help I do see pay-out levels of last year being at least able to maintain but we are about growth and we are about changing the business model as we do that growth engine Wersquore not about optimisation We see an ability to this bank to grow specifically in the UAE in the retail and commercial space and specifically in the wholesale area on the West-East Corridor and I will consider that when recommendations to the Board

Vikram Viswanathan Sure just a follow up question on your strategy you were talking about expanding your centres mostly from what I understand you would like to have regional centres in important cities like London Hong Kong Singapore etc right so it seems to be a very organic route to take whilst some of your competitors in Abu Dhabi have been doing bolt-on and small acquisitions Does this mean that the strategy is to start from scratch in other parts of the world and there will be no real acquisitions

Alex Thursby It is a very good question Look the fundamental that wersquore applying here is that our planning is based upon organic and I think there are fundamental disciplines that say that If you want to base your growth on purely inorganic activity you start doing silly things but we wonrsquot discount it but I donrsquot think you should think too much about it to be perfectly frank and I

think right now our planning ids based upon organic We believe that can be very successful particularly in the parts of the world that we want to play in We have seen a lot of new players in Asia develop very good organic businesses and very quickly ANZ to say just one that I am obviously quite close to in their results again I think a couple of days showed the value of that organic plan they have in Asia What I will say is that clearly Africa is a place where I see you can grow organically Right now around the Wholesale Bank for wholesale reasons I see very little chance of us acquiring I think you can build from scratch Relative to our retail and commercial proposition that is an area that we could look at at some point but we also need to learn how to grow quickly and aggressively and that will be our priority organically by the way growing quickly and aggressively

Vikram Viswanathan Fair enough thank you that was very clear thank you

Operator We have a question from Aarthi Chandrasekaran NBK Capital Marsquoam please go ahead

Aarthi Chandrasekaran Hi thank you for the call and good afternoon I have two questions the first one on provisioning Can you elaborate more on the strong recovery that enjoyed this quarter it is up 45 year-on-year and your expectation of provisioning trends declining is this based on continuing strong growth in recoveries That is my first question My second question is what would be your medium-term normalised cost of risk and also if you can just give us some initial thought on 2014 lending growth and margin trends Thank you

Alex Thursby I will take the last one last

Abhijit Choudhury

I think there were a number of questions there I think just to rearticulate the question first was the question regarding recoveries which we have had so far the second was in terms of the cost of risk I believe Hello can you hear me

Aarthi Chandrasekaran Yes youre right

Abhijit Choudhury I think if you look at the trend of provisioning that we have had it has shown a gradual downward trend I will address the issue of cost of risk first The cost of risk overall approximately has been in the region of about I think 65 or 70 basis points as compared to about 130 basis points relative to competition and what I mean by the cost of risk is if you were to take into account the provisions for the year relative to your total loan book If you were to look at the contribution or the amount of provisionings which we have had to do out of our porting income that has been in the region of I think I believe between 15 and 19 relative to competition over 30 and one of the reasons why we have maintained this gradual trend has been for the simple reason that we have had our provision impact which has been about a couple of quarters ahead of competition which we started way back in 2008 If you look at the NPLs and you will find that the NPLs in terms ofhellipwe gave a market guidance of about 35 and 375 starting from around end of 2012 in fact the end of 2011 and it is pretty much now plateaued around that level and you will see a gradual progressive declining trend in terms of our NPLs as well over a period of time We feel that we have also peaked in terms of NPLs and we donrsquot see it going beyond this level so therefore it brings us to the question in terms of our recoveries recoveries have been healthy so far some of it a good part of it had been write-backs where we have successfully worked out in terms of ndash with clients who have been in trouble but we have tried to successfully restructure by getting hold of additional security etc Moving forward we see a similar sort of trend Our annual provisioning has been in the level of about 12-13 billion We expect for the next couple of quarters perhaps provisioning on a quarter-by-quarter to be at that level of about between 250 and 300 You will notice that most of the provisioning has been collected provisioning specific provisioning has shown a decline that is once again an indication in terms of the portfolio quality improving and us in turn emerging out of like everybody else in terms of the crisis which we have all been in The collected provisioning increase has largely been as a result of the growth in terms of our loan book As also as some of you are aware that the Central

Bank has recently changed the guidelines on classification of commercial and non-commercial entities All in all the two or three questions you asked we expect the trend to in turn continue We have been very stringent in terms of our follow-up on our problem loans as a result of which we have had successful restructuring We expect if anything the cost of risk to in turn reduce from that [60-70] basis points and I think the last question was in terms of loan growth wasnrsquot it

Aarthi Chandrasekaran Yes it was on the loan and the margin trend for next year

Aarthi Chandrasekaran As far as loan growth is concerned I think Alex has already provided an indication I think he mentioned a number of 193-195 We are at about 183 In good part we have had a growth of about 129 I believe in terms of our short-term assets in the last quarter so I think loan growth will continue mainly in the area of short-term trades As far as margins are concerned quite frankly I think that is also an indication which has been given we see margin compression I think in terms of exact levels of where we are to use ndash want of any other term I think anatomically NBADrsquos structure is such that our margins have ranged between the 26 level and 19 and I think moving forward youre going to see average tenure declining and there will be a higher churn rate as far ashellipor using the word lsquovelocityrsquo on our loan book along with flow income to keep up our bottom line but margin compression could behellip

Alex Thursby I think when I just talk about margins the influences on margin are enormous It is about how much we can redeploy of our excess liquidity into working assets that can positively affect it actually It is about how much excess liquidity we have but if I can just get down to the raw market and we have started doing some of these things by the way in terms of managing our excess liquidity better but it is difficult in this environment when you have got so much liquidity as we currently have and I think that is good for the bank because it gives you sustainability of earnings and it is time to turn it up I think in the market my sense is that in the corporate market there will still continue to be some margin compression from Dubai I think that is starting to come through quite aggressively and I think it will continue for a while

longer I donrsquot expect a second phase of it though so it is just the finishing off of the current phase that I think will come through I think the key is what will happen in the commercial segment and that I canrsquot tell you at this moment and that is not a big business for us You should probably ask the people who have big businesses in commercial who are closer to that In the retail space I think it will be interesting to see how these new mortgage laws play out I think they are very good for sustainability and safety excellent in fact and I think it is just what we need but I do see people having to chase the really good business will price down so therefore it is your cost of funding that allows you to compete in that business and that is why we want to go for that I think We see that as a margin accretion to our total book albeit that it is going to take a while to build up to a meaningful level so we willhellipthe key for us will be how aggressive we can grow in two or three of these areas There are lots of levers that fit in the pie of margin that are there and I donrsquot think it rules everything I think what you will see from us is that our non-funded revenue over a period of time will start to increase quite well and I think this is part of the transformation of this bank and it may well happen in other banks as they develop their strategies from the current way We are in an environment globally where there is margin compression or should I say normalisation of margins to pre-2008 levels We should not forget where we are now versus where we were pre-2008 so businesses have to change

Michael Miller I think we have time for one more question if there is

Operator We have no further questions for the moment

Alex Thursby Thank you very much for giving us your time As I said in summary wersquore very pleased with the momentum we have started to build we are now clear as to what our real position is with the market and that will give everyone a better communication about guidance etc going forward but what I will say is please enjoy the Formula 1 in Abu Dhabi people tell me it is the best week in UAE of course we would say that from Abu Dhabi and I

am sure Dubai will have something to say about that In saying that it is a great week for the UAE as well as Abu Dhabi and wersquore very delighted to be a major sponsor of the event that is I know for a fact is very well liked by the participants and highly regarded It is quite unique in the sense of its transition from the evening into the night and that is quite a unique Grand Prix Have a good time keep your ears plugged and hopefully see you at the next quarter results if not before Thank you very much

Operator Ladies and gentlemen this concludes todayrsquos conference Thank you all for your participation You may now disconnect

3

Continued strength in 3Q 2013 results

3

Net earnings of AED 1035bn for 3Q 2013 down 8 y-o-y as growth in fee and net

interest income was offset by higher expenses and lower investment and other income

Strong underlying year-over-year top line results as net fee and commission grew

185 to AED 450bn in 3Q 2013

As expected 1-time gains related to hedging strategies did not repeat in 3Q 2013

impacting sequential and year-over-year comparisons

Balance sheet increased to AED 345bn up 15 ytd as deposits continued to grow

NPL ratio at 332 in 3Q 2013 remains below the expected peak of 375

Robust capital amp liquidity position maintained with the CAR at 178 and Tier-I ratio

at 161

4

Q3 2013 ndash Awards amp Accomplishments

4

Sheikh Khalifa Excellence Award (SKEA) ndash Diamond Category

Upgraded by SampP to AA-A-1+ from A+A-1

Ranked in World‟s 50 Safest Banks for 5th consecutive year (Global Finance)

ldquoThe Strongest Bank Balance Sheet in the UAE for 2013rdquo ndash Asian Banker

Magazine

ldquoBest Cast Management Services in the Middle Eastrdquo at EMEA Finance

Treasury Services Award Ceremony

5

What we want to change ndash

our mission to be core to our chosen customers

5

Our strategy to deliver this will be built around 3 geographical pillars and

will be achieved primarily through organic growth

Build the largest

safest and best

performing bank

first in UAE and

over time in GCC

Deepen our Wholesale

network across the new

West-East corridor amp

further integrate our

existing European amp

North American

platforms into this

network

Build 5 international bank

franchises in the largest and

fastest growing economies in

the West-East corridor

1

2 3Wholesale Network

Markets

New Franchise

Markets

Home Market

Time to complete build - 5 years

6

Trade and FDI flow across the West-East corridor

6SOURCE EIU estimates

Trade = Sum of imports and exports FDI = Sum of MampA and Greenfield investments

Trade flows

11 Intra Middle East

Trade

2011

112

12 Middle East and Asia

2011

13 Middle East and Africa

2011

21 Asia and Africa 31 Intra Asia

Trade 3302 6607 8

32 Intra Africa

50Trade 103 8

FDI flow 17

2020

270

2020

2020

38

CAGR

11-20

10

CAGR

11-20

CAGR

11-20

9 FDI flow 213 614 12

FDI flow 2 15 25

2011 2020CAGR

11-20 2011 2020CAGR

11-20

2011 2020CAGR

11-20

Trade

FDI flow

334

35

888

69

11

8

Trade

FDI flow

Trade

FDI flow

1008

26

2743

82

12

14

10

19

163

29

67

6

7

Key industry sectors aligned to our

network markets strategy

7

Key sectors

Financial

Institutions

Aviation rail

and transport

services

Real Estate

and family

conglomerates

Traders and

retailers

Energy and

Resources

Why is it an opportunity Illustrations

Significant and fastest growing segment globally

40 contributor to the global Wholesale bank and the

biggest volume segment in flow products

Controls 70 of the volumes in certain products

Strategic sector in the UAE amp aligned with Abu Dhabi 2030

Attractive sector for corporate credit with low counterparty

risk

Substantial growth amp potential of supply chain business

Strategic sector the UAE amp aligned with Abu Dhabi vision

2030

National champions with significant growth aspirations

Big 6 airlines within the new West-East corridor

Strategic sector the UAE (20 of UAE GDP) amp aligned

with Abu Dhabi vision 2030

Highly attractive sector for Arab investors

Attractive for GCCAsian and other investors

Strategic and high growth sectors in the region

UAE is the 18th biggest trading country in world ahead

of countries like India Brazil and Australia

Retailing is USD ~$48Bn market in GCC expected to

grow at ~8 annually from 201317

8

We will increasingly utilise an bdquooriginate to

distribute‟ model

8

Originate from Customers Distribute to Customers

Government of Abu Dhabi

Financial institutions

Energy and resources

Aviation rail and transport services

Real estate and family conglomerates

Traders and retailers

Financial institutions

Hedge funds

Pension funds and Insurance

Sovereigns

Private banks

HNW and affluent

On and off balance

sheet

Primary distribution

Secondary

distribution

Reverse inquiries

Cross-sell Cross-sell

Cash and Trade

FX and derivatives

Bonds syndications

Commodities

Specialised lending

Corporate finance

Flo

w

pro

du

cts

Clearingsettlements

Cash and trade

FX and derivatives

Bonds

Loans

Flo

w

pro

du

cts

Single distribution hub

9

Wholesale banking model aligning to

West-East corridor

91 Relationship sales and product service

Abu DhabiThe GulfMiddle East

MumbaiIndian sub-continent

LagosSouth and West Africa

Singapore

South-East Asia

Australia Papua New

Guinea

Hong KongGreater China Korea

and Japan

London

Scandinavia

Switzerland and

European Union

WashingtonNorth and South

America

Global financial markets and booking

centers

Abu Dhabi

Singapore or Hong Kong

London

Key industry sectors

Financial institutions (Singapore)

Energy and resources (Abu Dhabi)

Aviation rail and transport

(Abu Dhabi)