Perception of Consumers (Income-Earners) on Islamic Insurance (Takaful) Services’ Consumption in Kano Metropolis, Nigeria Garba Bala Bello, PhD Department of Business Administration and Entrepreneurship, Bayero University, Kano (BUK), Nigeria. GSM: 08054557452 E-Mail:[email protected] And Habibu Ayuba Government Secondary Commercial School, Airport Road, Kano, Nigeria. GSM: 08030527135 E-Mail: [email protected]/[email protected] A PAPER PRESENTED AT THE 1 ST INTERNATIONAL CONFERENCE OF THE INTERNATIONAL INSTITUTE OF ISLAMIC BANKING AND FINANCE, BAYERO UNIVERSITY KANO NIGERIA, APRIL 17 - 19, 2014. Abstracts Consumers’ significant perception of service offerings has been the yearning of businesses. It is a prerequisite of ascertaining service (Takaful) consumption. This paper aims at examining some factors that explain favorable consumers’ perception of Islamic insurance (Takaful) services consumptions in Kano Metropolis, Nigeria. It involves 266 respondents whose responses were employed in testing two (2) models representing different constructs explaining consumers’ perception. Two dimensions: awareness and income earners’ trust and confidence; were tested in Model A, using multiple regression. It was discovered that consumers’ awareness of Takaful services showed least effect in influencing favorable perception of Takaful consumption. The trust and confidence reposed on the Takaful operators by consumers made average impact on determining favorable perception of Takaful services consumptions. Model B’ dimensions: age, marital status, gender, qualification, occupation, and income of consumer; were found to be insignificantly capable of impacting any influence on consumers’ favorable perception of Islamic services consumption in Kano Metropolis, Nigeria. These findings are unique as many studies have discovered factors such as income of consumers as capable of determining demand of Takaful services. Therefore, the paper recommends that the consumers’ 1 | Page

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Perception of Consumers (Income-Earners)on Islamic Insurance (Takaful) Services’Consumption in Kano Metropolis, Nigeria

Garba Bala Bello, PhDDepartment of Business Administration and Entrepreneurship,

Bayero University, Kano (BUK), Nigeria.GSM: 08054557452

E-Mail:[email protected]

AndHabibu Ayuba

Government Secondary Commercial School, Airport Road, Kano,Nigeria.

GSM: 08030527135 E-Mail: [email protected]/[email protected]

A PAPER PRESENTED AT THE 1ST INTERNATIONAL CONFERENCE OF THEINTERNATIONAL INSTITUTE OF ISLAMIC BANKING AND FINANCE,BAYERO UNIVERSITY KANO NIGERIA, APRIL 17 - 19, 2014.

Abstracts Consumers’ significant perception of service offerings has been theyearning of businesses. It is a prerequisite of ascertaining service(Takaful) consumption. This paper aims at examining some factors thatexplain favorable consumers’ perception of Islamic insurance (Takaful)services consumptions in Kano Metropolis, Nigeria. It involves 266respondents whose responses were employed in testing two (2) modelsrepresenting different constructs explaining consumers’ perception. Twodimensions: awareness and income earners’ trust and confidence; weretested in Model A, using multiple regression. It was discovered thatconsumers’ awareness of Takaful services showed least effect ininfluencing favorable perception of Takaful consumption. The trust andconfidence reposed on the Takaful operators by consumers made averageimpact on determining favorable perception of Takaful servicesconsumptions. Model B’ dimensions: age, marital status, gender,qualification, occupation, and income of consumer; were found to beinsignificantly capable of impacting any influence on consumers’favorable perception of Islamic services consumption in Kano Metropolis,Nigeria. These findings are unique as many studies have discoveredfactors such as income of consumers as capable of determining demand ofTakaful services. Therefore, the paper recommends that the consumers’

1 | P a g e

awareness of Takaful should be intensified; but, this along is notadequate to ensure consumers consumption of the services. Takafuloperators, therefore, should work very hard to build and win consumers’trust and confidence by showing that their offering is effective to meetthe need of the society.

Keywords: Perception, Takaful/Islamic Insurance,Consumption, Income earners/consumers, TakafulOperators/Insurance companies, Kano Metropolis,Nigeria, Risk Management Tools/Takaful products

1.0 IntroductionLiteratures have assertedthat human perceptionserves as a primary toolinfluencing consumers’purchasing decision of anygiven offerings: productsor services (Kotler, 2000;Kotler and Keller, 2005).This indicates that thesuccess of an offering,especially at itsintroductory stage in theexisting market largelydependent on its ability towin favorable consumers’perception. This alsoenables customers to see aservice as worthy ofpatronage capable ofmeeting and satisfying

individual needs. It allowsa consumer to select,organize and interpretinformation inputs (about aproducts/services) tocreate a meaningfulpictures of the world (viewof products/services andTakaful operators) todetermine if the services(risk transfer) are capableof solving their problem.People perceive not onlyphysical stimuli (productor service) but alsostimuli relating to thesurrounding field(insurance industry andcompanies proving theservices). The otherinterplay shaping the

2 | P a g e

perception includes thoseconditions that are moreinert to the consumer.Among many is theindividual level of income,education and his age toname but a few. Individualalways emerges withdifferent perception of thesame object(product/service/Takaful).This is due to the factthat individual perceptualprocess can be selectiveattention, selectivedistortion, or selectiveretention. The influence ofthese factors enables oneto make choice of a productor service. Therefore,every provider of servicesuch as Takaful operatorsin insurance Industry needsto explore avenue that canguarantee having winningfavorable public perceptionof their offerings,especially Islamic(Takaful) insurance whichis very new in Kano Marketand Nigerian insuranceindustry.

Islamic insurance service(Takaful) enters Kanomarket in the year 2003.Introduced to the market byAfrican Allied InsurancePLC, later by other

insurance companiesCornerstone insurance PLCand Niger insurance PLC)follow the suite. With morethan ten (10) years in themarket, there is no muchinformation with regard toits penetration andconsumers’ patronage inKano market as observed.This necessitates the needfor the study. But, manystudies conducted on thesubject matter, are carriedout in some countries likeMalaysia and GulfCooperation Countries (GCC)which have very differentsocio- economiccharacteristics with thearea understudy.

Takaful is an insuranceservice that is acting as asubstitute to theconventional insuranceservices of the West. It isan Islamic insurancebusiness whose aim andoperations do not involveany element that does notcomply with shariah. It isa joint guarantee whoseobjective is a cooperationand mutual help among themembers of definedgroup/participants againstlosses or damages of aproperty and life

3 | P a g e

inflicting upon oneanother. The members of thegroup agree to guaranteejointly that should any oneof them to suffer acatastrophe or disaster, hewould receive certain sumof money to meet up thelosses/damages. All membersfool their resources andefforts together in supportof the needy.

It is observed that some ofthe drivers which move theconsumption/demand ofTakaful services, amongothers include religiousbelief of the people,successful development ofIslamic bankinginstitution, role ofIslamic financialinstitutions indistributing Takafulproducts (Atiquzzafar,2011), public awareness ofTakaful services and marketeducation (Bashir, Mail andAbd’Ali, 2011) and publictrust and confidence in theinstitution (Takafuloperators). Oluwokudejo(2009) examined thatNigerian InsuranceCompanies have for longenjoying discredited imageand poor reputation thatequally reflected on the

public perception. That iswhy this study wants toexplore the perception ofconsumers; income earnersonly, include both actualand potential customers ofTakaful in Kano Metropolis;on the Islamic Insuranceservices (Takaful)consumption in the studyarea.

2.0 Literature ReviewAyuba (2013) discoveredthat the non- economicfactors determining Takafulservices consumption inKano Metropolis; among manyare: public perception ofthe Islamic insuranceservices’ consumption,public awareness and publictrust and confidencereposed on the TakafulOperators available in themarket and so on. Factshave indicated that all theTakaful services providersare insurance companiesoffering conventionalinsurance businessconcomitantly (Ado, 2013).This has created a gapbetween what is known aboutpublic perception ofconventional insurancewhich many Muslim, due totheir religious belief,have had negative

4 | P a g e

perception of and thecurrent position of Takafulservices sold and providedby these conventionalinsurance companies. Thisbrings us to the needs toexplore the variables thatcan be related to and causethe consumers’ perceptionof Takaful.

Yazid, Arifin, Husin andDaud (2012) in theiranalytical study, havereported model that canexplain the determinants ofFamily Takaful demand. Themodel states that there arenine (9) economic factors:income, inflation, interestrate, financialdevelopment, savings,unemployment rate,pensions, stock and priceof Takaful; and seven (7)socio-economic factorswhich include: lifeexpectancy, dependencyratio, education, age,urbanization, householdsize and employment status.It is against thisbackground that the studyhas seen the relevance oftesting the socio economicdemography (gender, age,marital status, academicqualifications,occupational status, and

income level) of therespondents if they causeincome earners favorableperception of the Takafulconsumption.

Besides, previous studies(Billah, undated; Taylor,2005; Rahman,etal 2008;Rahman, 2009 and Ayuba,2013) have equally examinedthat awareness of publicover the Takaful servicesand activities of Takafuloperator is a significantfactor enabling people todiffentiate Islamicinsurance from theconventional insurance. Itclears people misconceptionabout the concept ofinsurance which serves as ahindrance in the overallgeneral insuranceconsumption especially in aconcentrated settlement ofdominant Muslim Umma.Alamasi (2010) and Isa andDandogo (2010) attributedlow level of publicawareness of Takafulservices as a greatchallenge for the Islamicinsurance’ penetrationworldwide. This study,however, attempt todetermine if public levelof awareness predictsincome earners’ perception

5 | P a g e

of Takaful servicesconsumption.Similarly, Oluwokudejo(2009) discovered thatNigerian indifference toconventional insurance wasnot due to religion butinstead he attributed thelow patronage to lack oftrust in the industry. Omarand Owasu-Frimpong (2007)earlier on had seen lowinsurance culture inNigeria as a result of lackof confidence in theindustry. The situationalso brought aboutcumulative negativeexperience to customer.This was justified byObalola (2010) who saidthat the Nigerian insurancecompanies’ reputation hadfor long enjoyed longdiscredited image whichreflected on the publicperception and it had leadto the widespread apathytoward insurance servicesin Nigeria. Observing thesefacts, one can easily seethe need to know theposition of Takaful. Thisis because; all theexisting Takaful operatorsin Nigerian Insuranceindustry are sub-divisionor window operation of thecompanies running business

of conventional insurance.It is this that has calledfor this study to see ifthe consumers’ trust andconfidence cause favorableperception of the Takafulservice consumption.

It is widely observed thatthe consumers’ pre-consumption expectation ofservice providers and post-consumption perceptions ofa service offered is drivenby the gap between theexpectations andperformance’s perception.As noted by Nath and Devlin(undated); the consumers’gap between expectation andperception of serviceexists invariably in four(4) variables which are:lack of knowledge ofconsumers’ needs anddesires; inadequate servicestandards; inability todeliver the servicestandard and delivery isnot matching promises madeby the service providers.This research hasconsidered that inabilityof the Takaful operators(all of them equally offerservices of conventionalinsurance) to consider therelevance of these four (4)factors aforementioned;

6 | P a g e

affect the level ofconsumers’ trust andconfidence reposed on thefirms. In addition; thisdisregard to these factorsaffected the firms’ effortto create sizeable level ofawareness of the servicesto the consumers in themarket.

Therefore, on the bases ofthe foregoing; the paperhypothesizes in null form,as follows:HO1: Consumers level ofawareness of Takafulservices has no significanteffect on their perceptionof Takaful servicesconsumption in KanoMetropolis.HO2: Consumers level ofTrust and Confidencereposed on TakafulOperators has nosignificant effect on theirperception of Takafulservices consumption inKano Metropolis.HO3: Consumers’ socioeconomic factors have nosignificant effect on theirperception of Takafulservices consumption inKano Metropolis.

3.0 Methodology of thestudy

This study is a basic/pureresearch which is designedfor fact findings. Itemployed exploratory surveydesign as an avenue toachieve the researchobjectives and to ascertainthe veracity of the study’shypotheses formulated toenable exploring thephenomena under study. Thedata collected is cross-sectional which is used inanswering the researchquestions relatingconsumers’ socio- economicdemographic factors;income- earners’ level ofawareness of Takafulservices and their trustand confidence reposed onthe Takaful Operators(independent variables) tothe income- earners(consumers) perception ofTakaful services in KanoMetropolis, Nigeria. Thechoice of the city was dueto its cosmopolitan naturemaintaining leadershipposition in trade andcommerce throughoutNorthern Nigeria. It alsoaccommodated almost allethnics group of Nigeria.

Judgmental samplingtechnique was used. Thetotal sum of 384 items of

7 | P a g e

questionnaire wasdistributed to the subjectsof the study. Thequestionnaire is designedto contain many parts: 6demographic variables, 6questions determiningAwareness, 3 questionsdetermining perception and3 questions determiningIncome-earners Trust andConfidence reposed onTakaful Operator in KanoMetropolis. It was based on5-points likert scaleanchored on at 1 stronglydisagreed, 2 disagree, 3neutral and 5 stronglyagreed. The researcher wasable to retrieve 266 itemsof questionnairerepresenting 69.27%. Thequestionnaire designed wassubjected to validity andreliability test usingCronbach’s Alpha statistic.The data collected wassubjected to stability andnormality test usingskewness and kurtosisstatistic in determiningthe assumption ofparametric test. Thestatistical tools used inanalyzing the data includeddescriptive statistics andinferential parametric toolof linear multipleregression. This data

analysis was done usingSPSS 17.

3.1 Validity andReliability of the ResearchInstrument

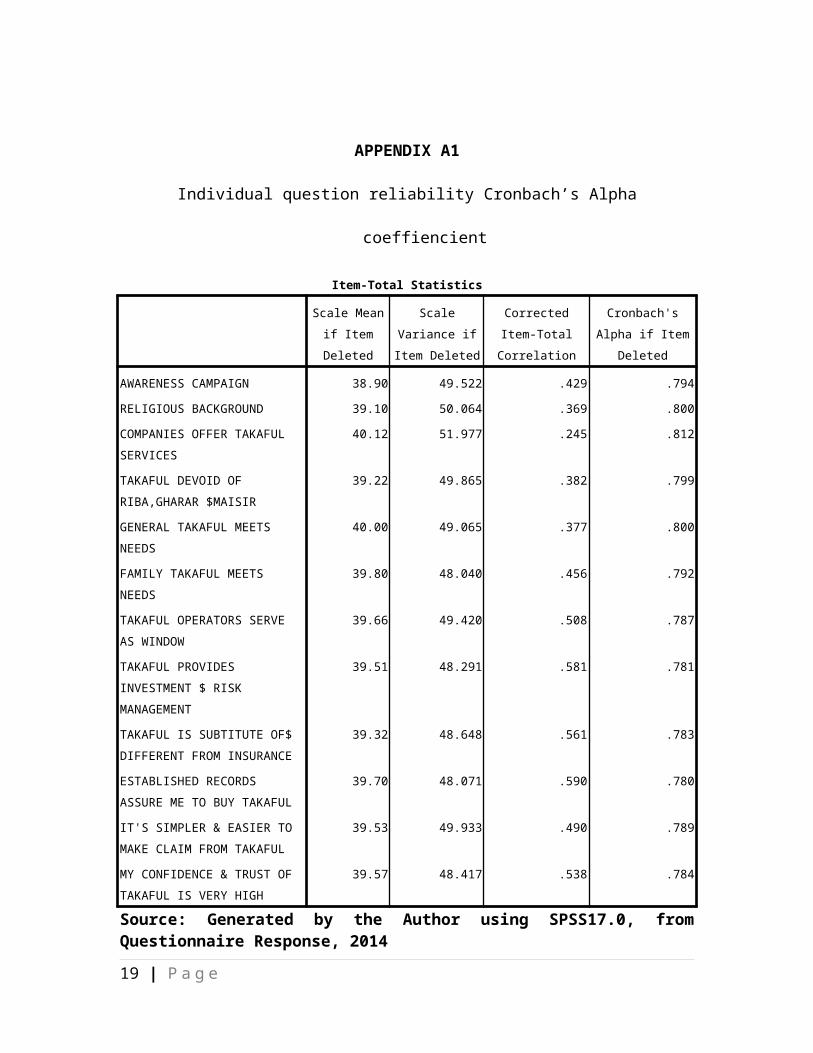

The original draft of thequestionnaire is given tothe experienced academicianand managers of Takafulbusiness to assess anddetermine the face andcontent validity of theinstrument. The items ofquestions in the testinstrument are validated onthese criteria: readabilityof the questions, languagelevel, and the adequacy ofthe question and thecontent coverage of thesubject matter. Afterrestructuring andcorrection, the final copyof the questionnaire isproduced. It consists oftwelve (12) questions(Appendix D); perception (3questions); awareness (6questions) and trust andconfidence (3 questions).

Besides; the instrument wassubjected to reliabilitytest. Since likert scalewas used in thequestionnaire, theCronbanch’s Alpha

8 | P a g e

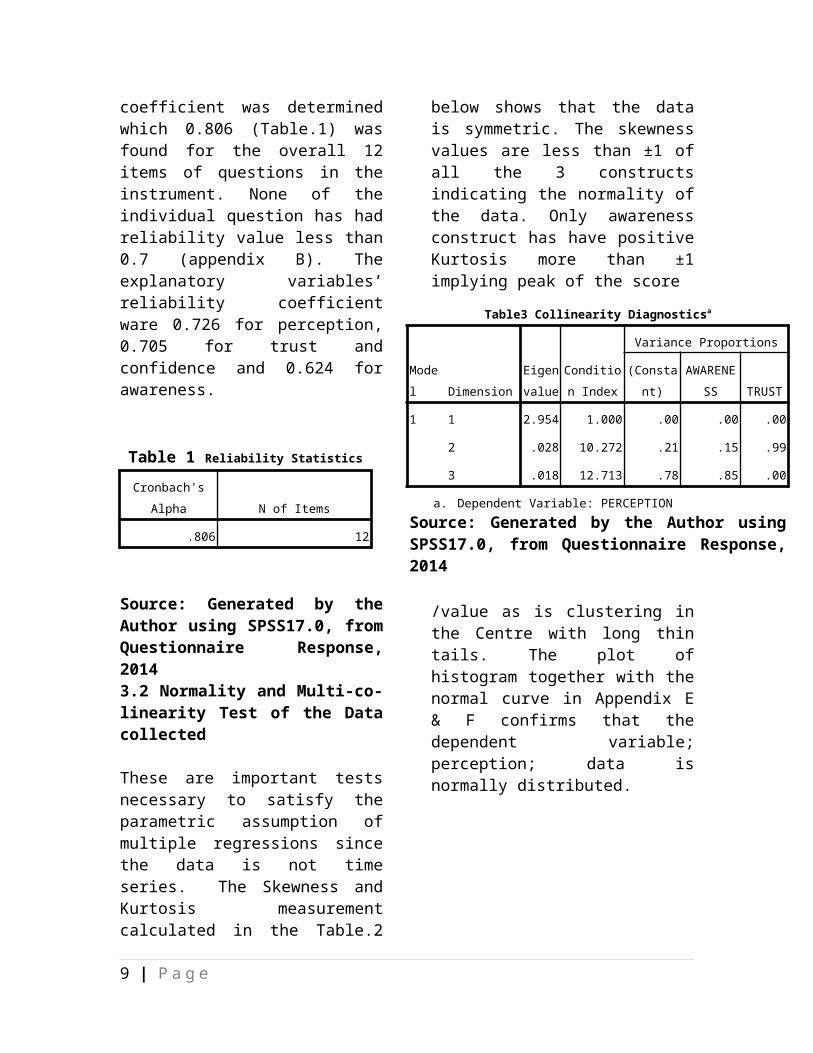

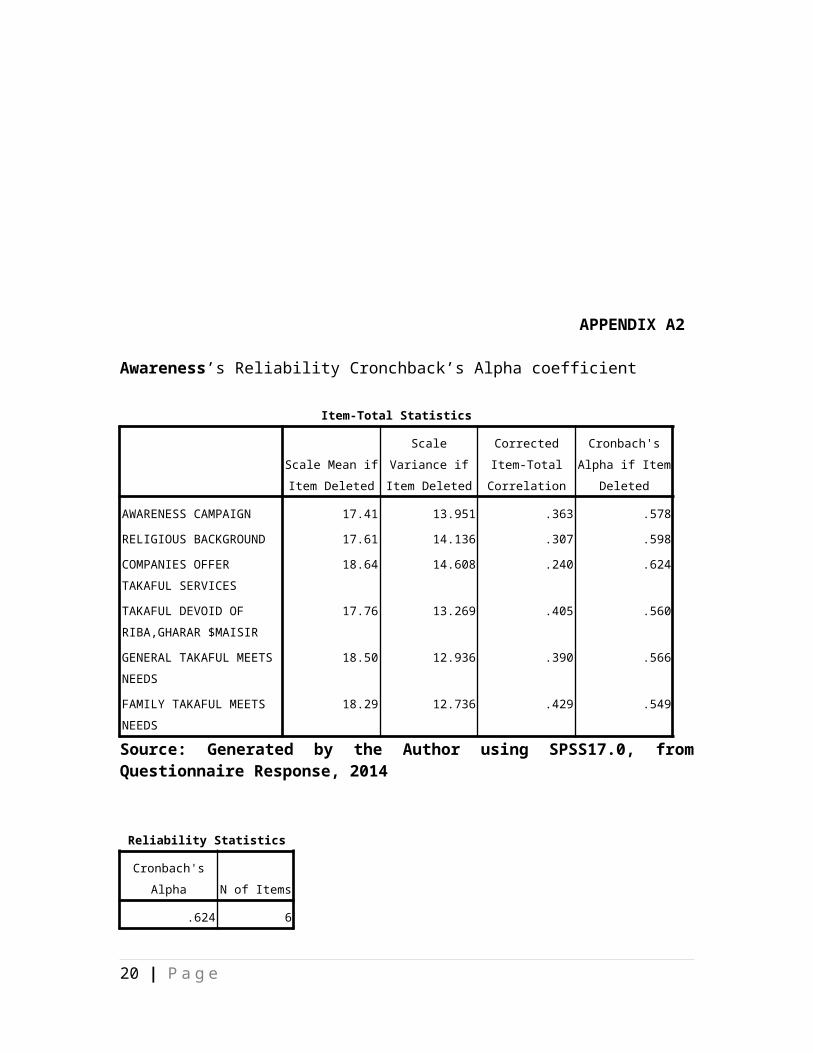

coefficient was determinedwhich 0.806 (Table.1) wasfound for the overall 12items of questions in theinstrument. None of theindividual question has hadreliability value less than0.7 (appendix B). Theexplanatory variables’reliability coefficientware 0.726 for perception,0.705 for trust andconfidence and 0.624 forawareness.

Table 1 Reliability StatisticsCronbach's

Alpha N of Items

.806 12

Source: Generated by theAuthor using SPSS17.0, fromQuestionnaire Response,20143.2 Normality and Multi-co-linearity Test of the Datacollected

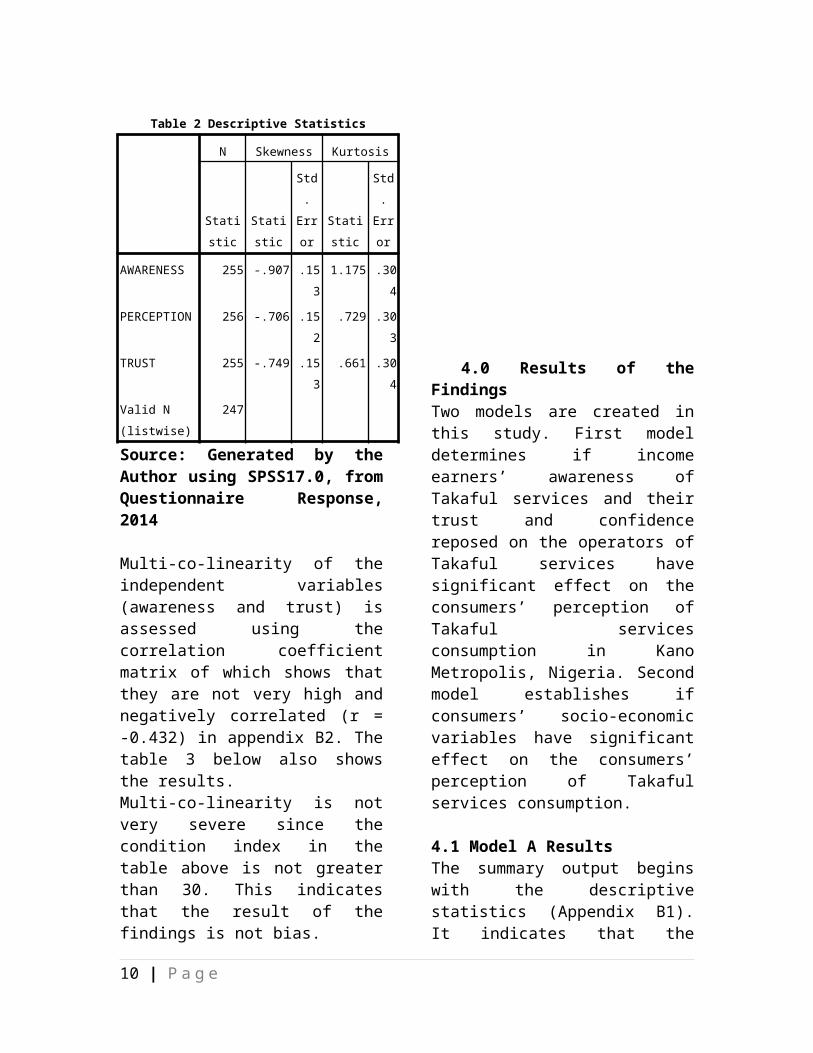

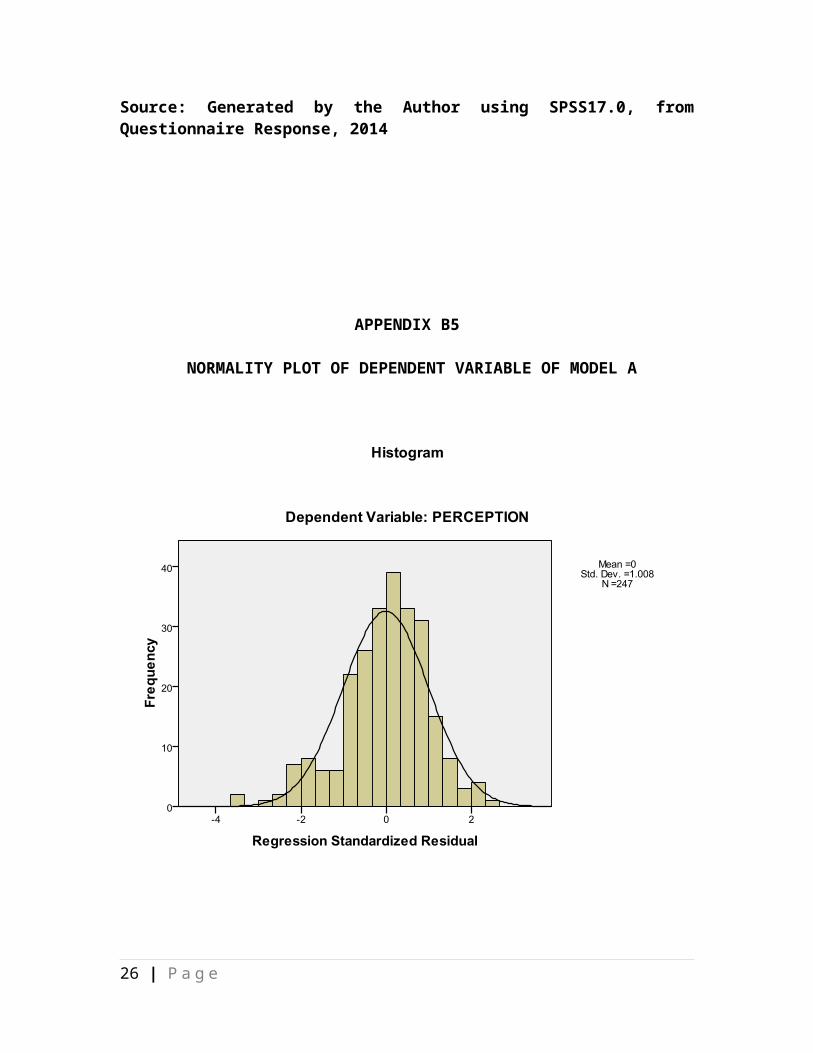

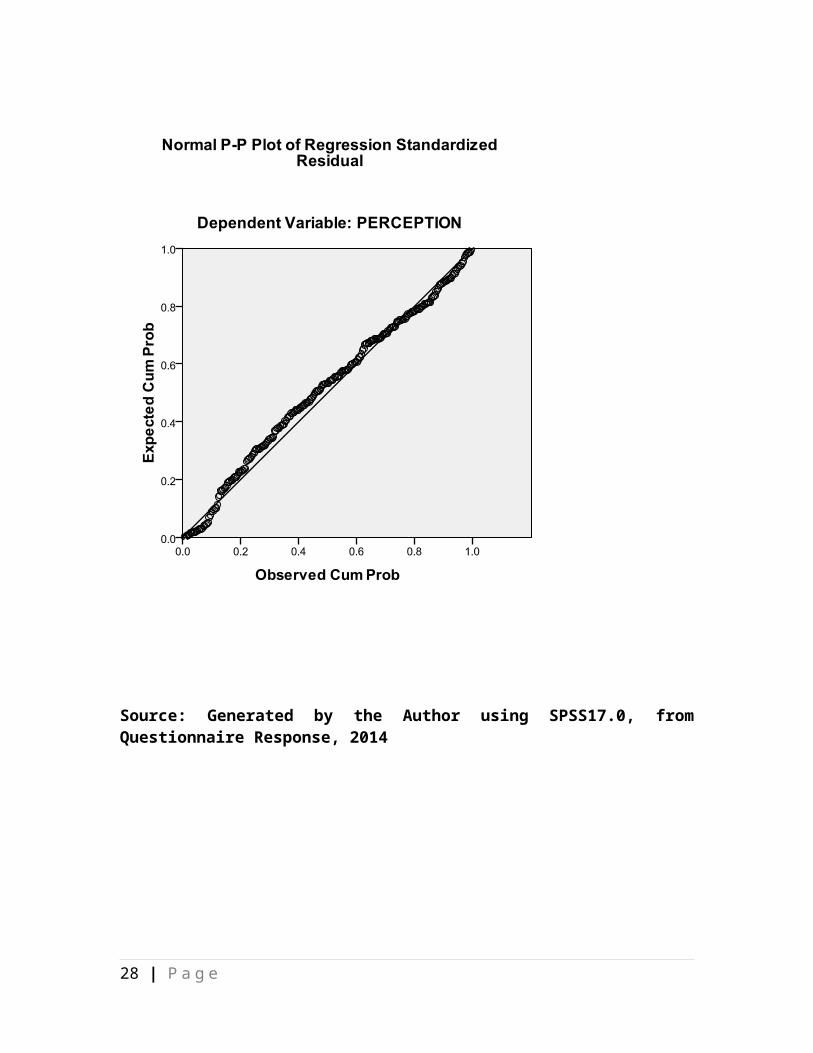

These are important testsnecessary to satisfy theparametric assumption ofmultiple regressions sincethe data is not timeseries. The Skewness andKurtosis measurementcalculated in the Table.2

below shows that the datais symmetric. The skewnessvalues are less than ±1 ofall the 3 constructsindicating the normality ofthe data. Only awarenessconstruct has have positiveKurtosis more than ±1implying peak of the score

/value as is clustering inthe Centre with long thintails. The plot ofhistogram together with thenormal curve in Appendix E& F confirms that thedependent variable;perception; data isnormally distributed.

9 | P a g e

Table3 Collinearity Diagnosticsa

Model Dimension

Eigenvalue

Condition Index

Variance Proportions

(Constant)

AWARENESS TRUST

1 1 2.954 1.000 .00 .00 .00

2 .028 10.272 .21 .15 .99

3 .018 12.713 .78 .85 .00

a. Dependent Variable: PERCEPTIONSource: Generated by the Author usingSPSS17.0, from Questionnaire Response,2014

Source: Generated by theAuthor using SPSS17.0, fromQuestionnaire Response,2014

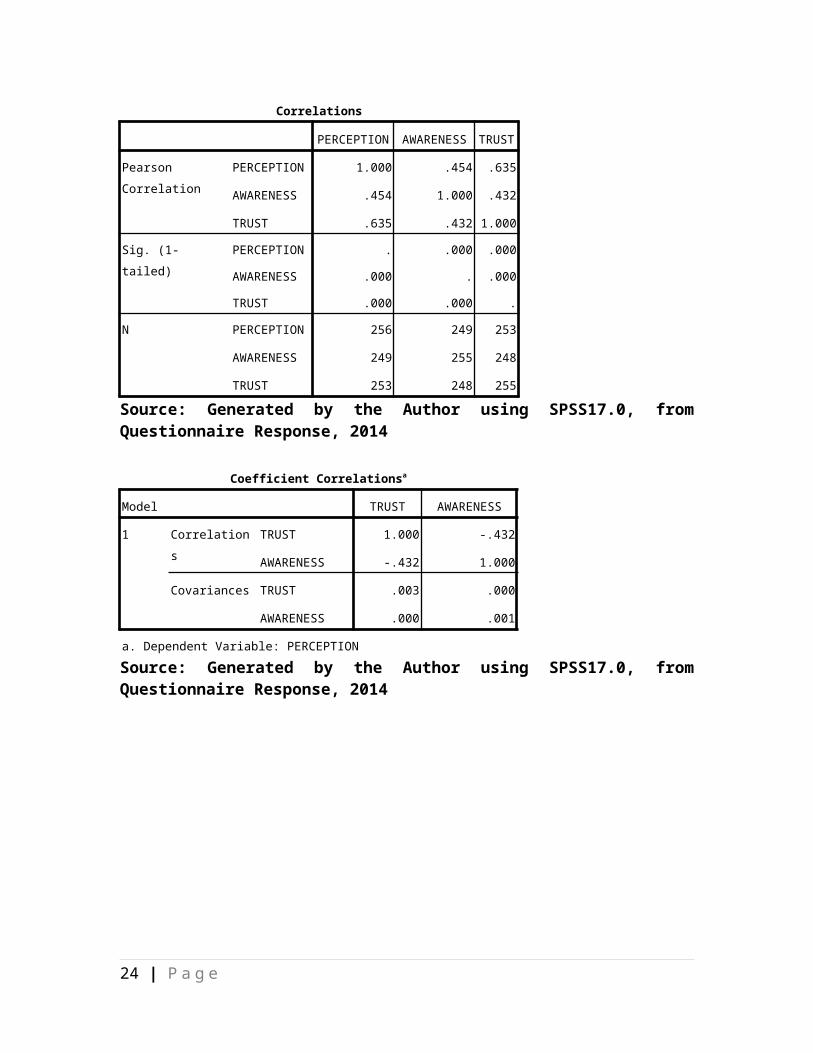

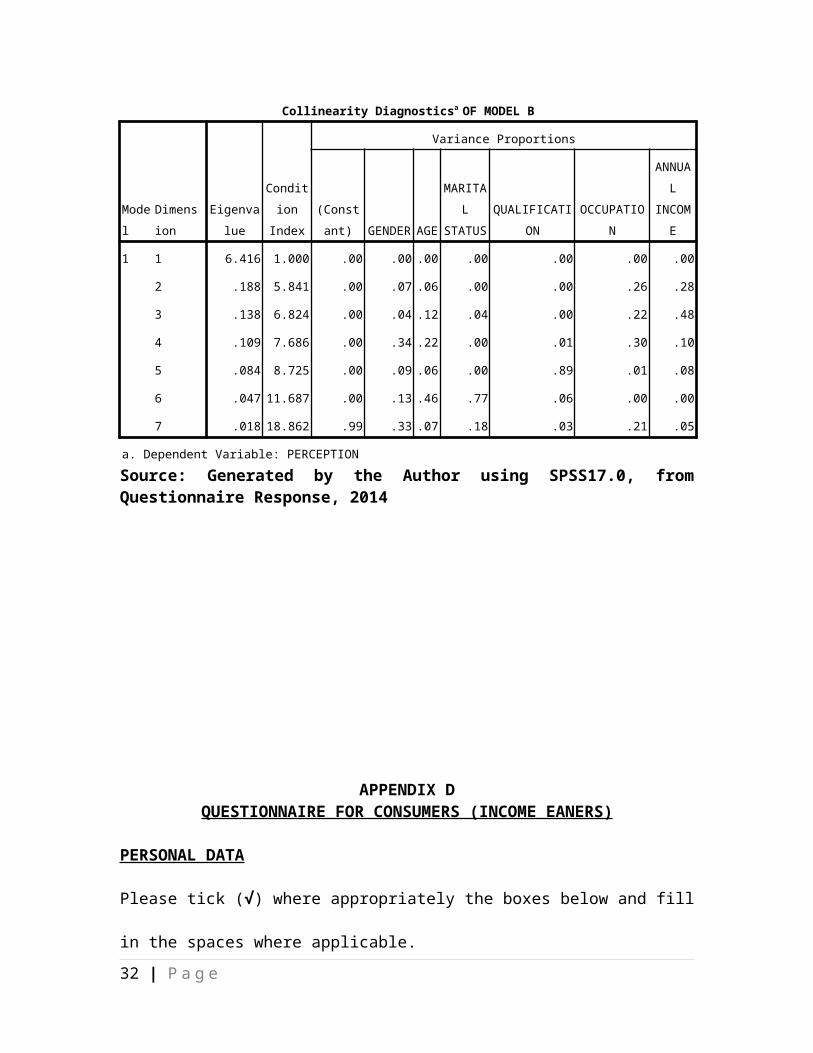

Multi-co-linearity of theindependent variables(awareness and trust) isassessed using thecorrelation coefficientmatrix of which shows thatthey are not very high andnegatively correlated (r =-0.432) in appendix B2. Thetable 3 below also showsthe results.Multi-co-linearity is notvery severe since thecondition index in thetable above is not greaterthan 30. This indicatesthat the result of thefindings is not bias.

4.0 Results of theFindingsTwo models are created inthis study. First modeldetermines if incomeearners’ awareness ofTakaful services and theirtrust and confidencereposed on the operators ofTakaful services havesignificant effect on theconsumers’ perception ofTakaful servicesconsumption in KanoMetropolis, Nigeria. Secondmodel establishes ifconsumers’ socio-economicvariables have significanteffect on the consumers’perception of Takafulservices consumption.

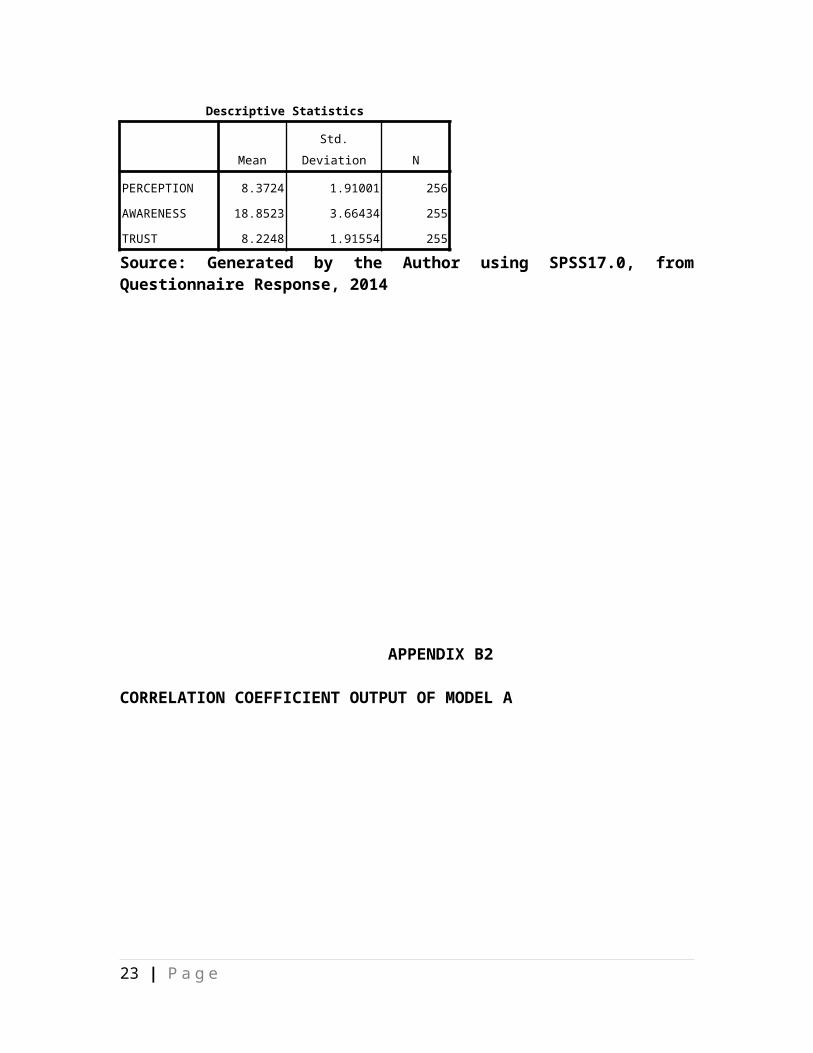

4.1 Model A ResultsThe summary output beginswith the descriptivestatistics (Appendix B1).It indicates that the

10 | P a g e

Table 2 Descriptive Statistics

N Skewness Kurtosis

Statistic

Statistic

Std.

Error

Statistic

Std.Error

AWARENESS 255 -.907 .153

1.175 .304

PERCEPTION 256 -.706 .152

.729 .303

TRUST 255 -.749 .153

.661 .304

Valid N (listwise)

247

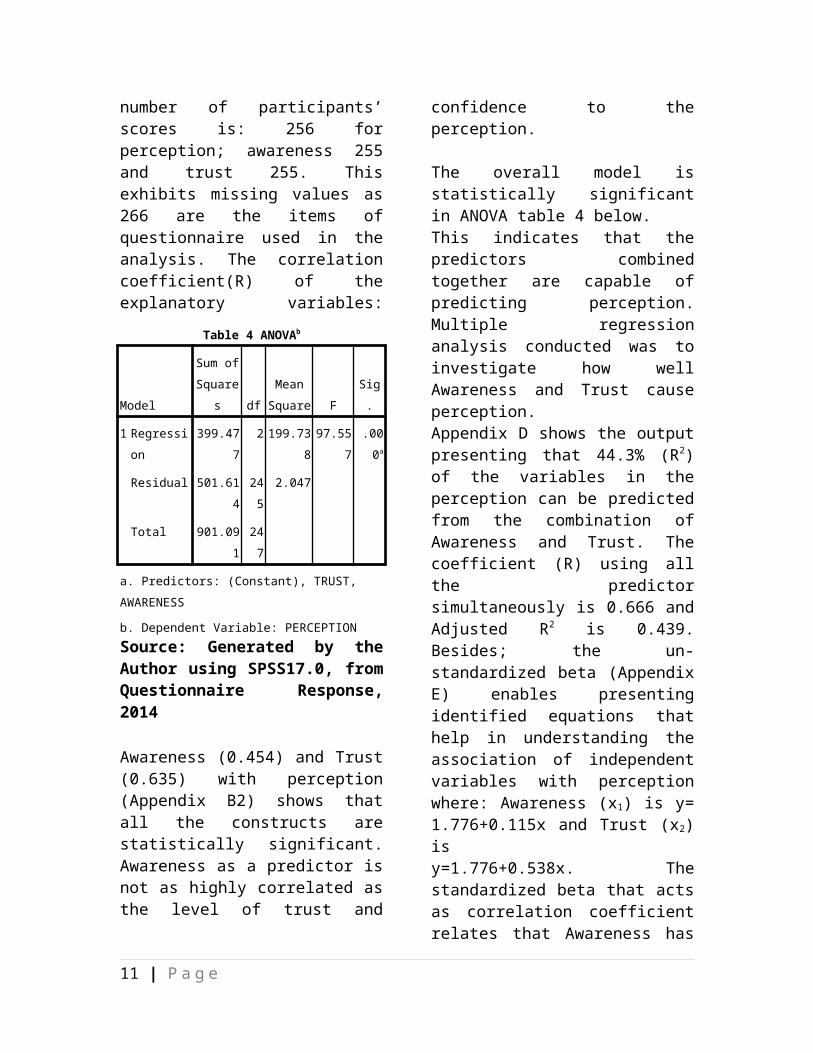

number of participants’scores is: 256 forperception; awareness 255and trust 255. Thisexhibits missing values as266 are the items ofquestionnaire used in theanalysis. The correlationcoefficient(R) of theexplanatory variables:

Awareness (0.454) and Trust(0.635) with perception(Appendix B2) shows thatall the constructs arestatistically significant.Awareness as a predictor isnot as highly correlated asthe level of trust and

confidence to theperception.

The overall model isstatistically significantin ANOVA table 4 below.This indicates that thepredictors combinedtogether are capable ofpredicting perception.Multiple regressionanalysis conducted was toinvestigate how wellAwareness and Trust causeperception. Appendix D shows the outputpresenting that 44.3% (R2)of the variables in theperception can be predictedfrom the combination ofAwareness and Trust. Thecoefficient (R) using allthe predictorsimultaneously is 0.666 andAdjusted R2 is 0.439.Besides; the un-standardized beta (AppendixE) enables presentingidentified equations thathelp in understanding theassociation of independentvariables with perceptionwhere: Awareness (x1) is y=1.776+0.115x and Trust (x2)isy=1.776+0.538x. Thestandardized beta that actsas correlation coefficientrelates that Awareness has

11 | P a g e

Table 4 ANOVAb

Model

Sum ofSquare

s dfMean

Square FSig.

1 Regression

399.477

2 199.73897.55

7.000a

Residual 501.614

245

2.047

Total 901.091

247

a. Predictors: (Constant), TRUST, AWARENESS

b. Dependent Variable: PERCEPTIONSource: Generated by theAuthor using SPSS17.0, fromQuestionnaire Response,2014

22.1% capability to causeperception and Trust has54% ability to predictperception. These valueshave small andmedium/average effectrespectively according toCohen (1988) cited inMorgan, Leech, Gloecknerand Barrett (2004).

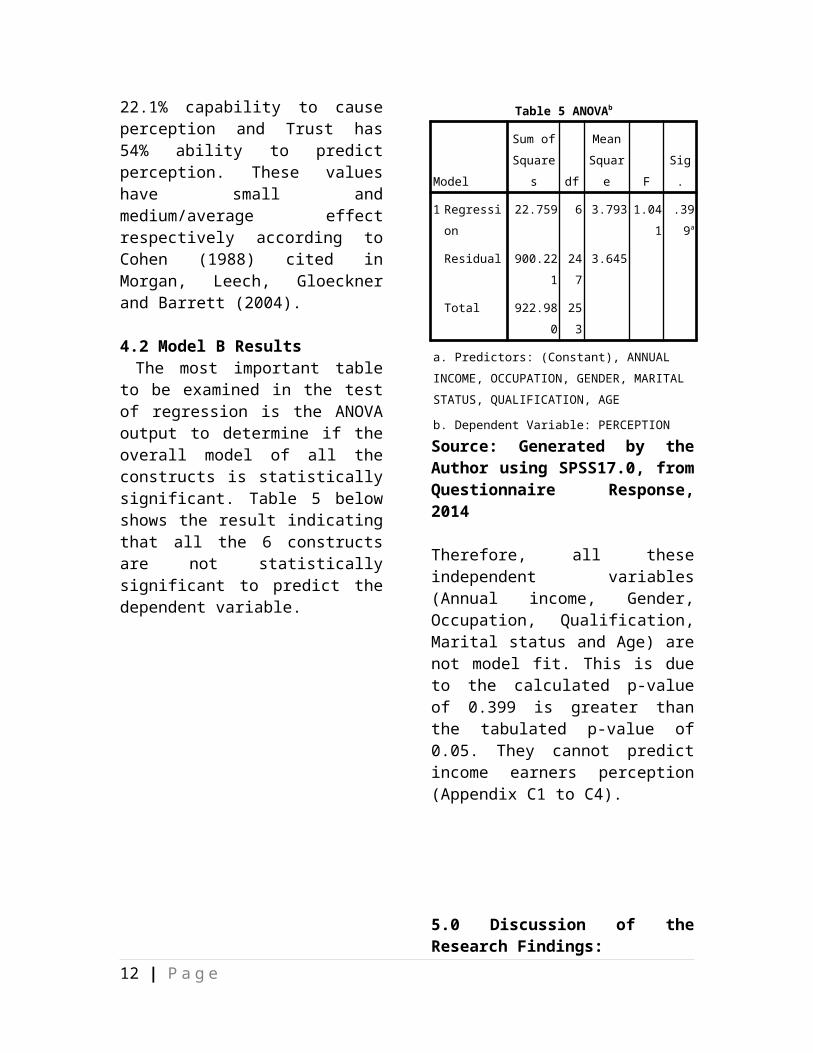

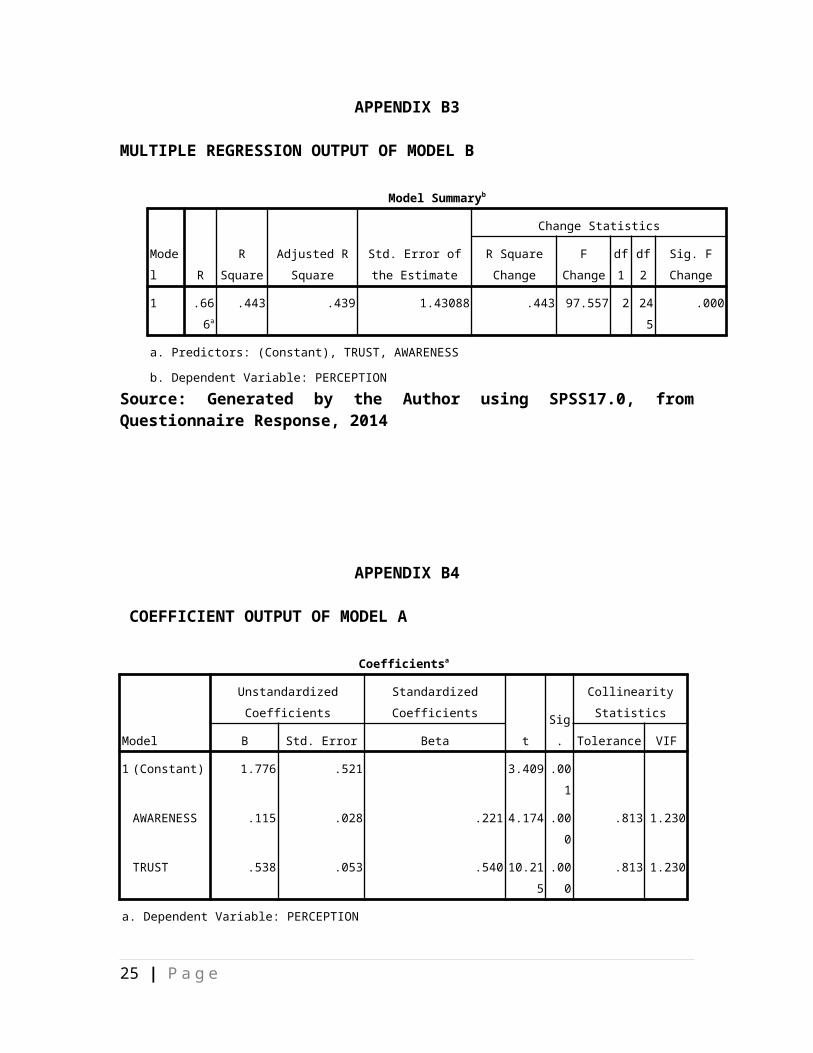

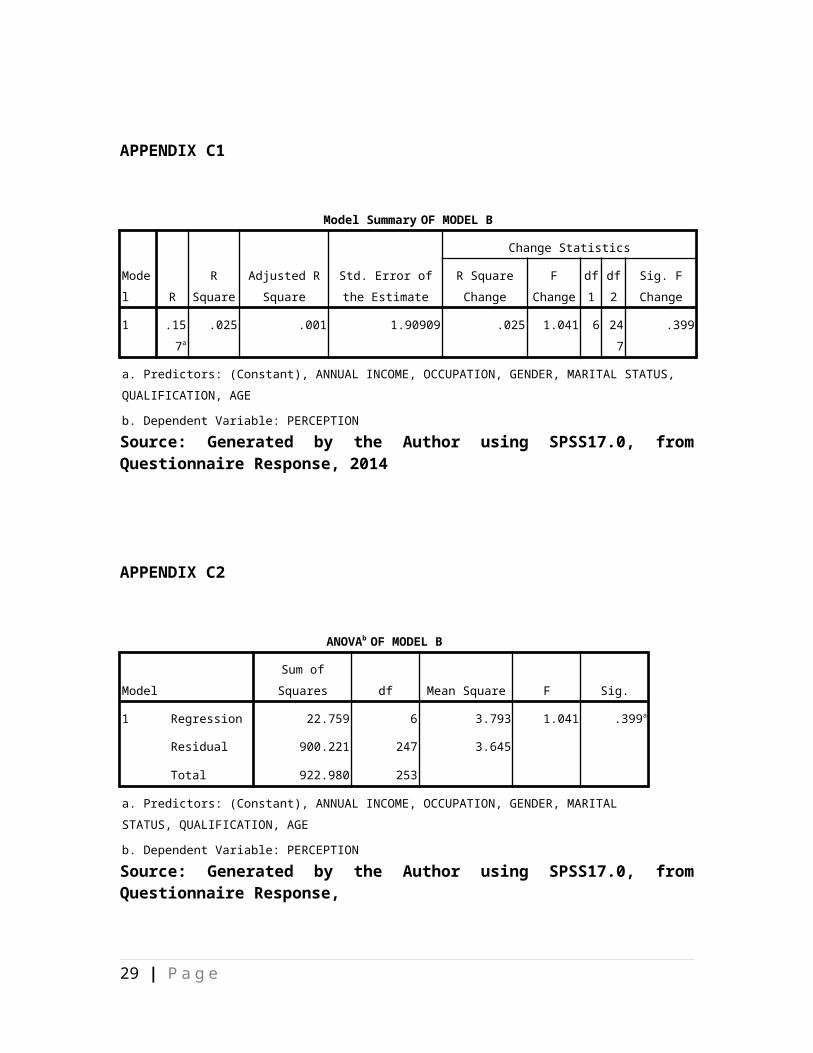

4.2 Model B Results The most important tableto be examined in the testof regression is the ANOVAoutput to determine if theoverall model of all theconstructs is statisticallysignificant. Table 5 belowshows the result indicatingthat all the 6 constructsare not statisticallysignificant to predict thedependent variable.

Table 5 ANOVAb

Model

Sum ofSquare

s df

MeanSquare F

Sig.

1 Regression

22.759 6 3.793 1.041

.399a

Residual 900.221

247

3.645

Total 922.980

253

a. Predictors: (Constant), ANNUAL INCOME, OCCUPATION, GENDER, MARITAL STATUS, QUALIFICATION, AGE

b. Dependent Variable: PERCEPTIONSource: Generated by theAuthor using SPSS17.0, fromQuestionnaire Response,2014

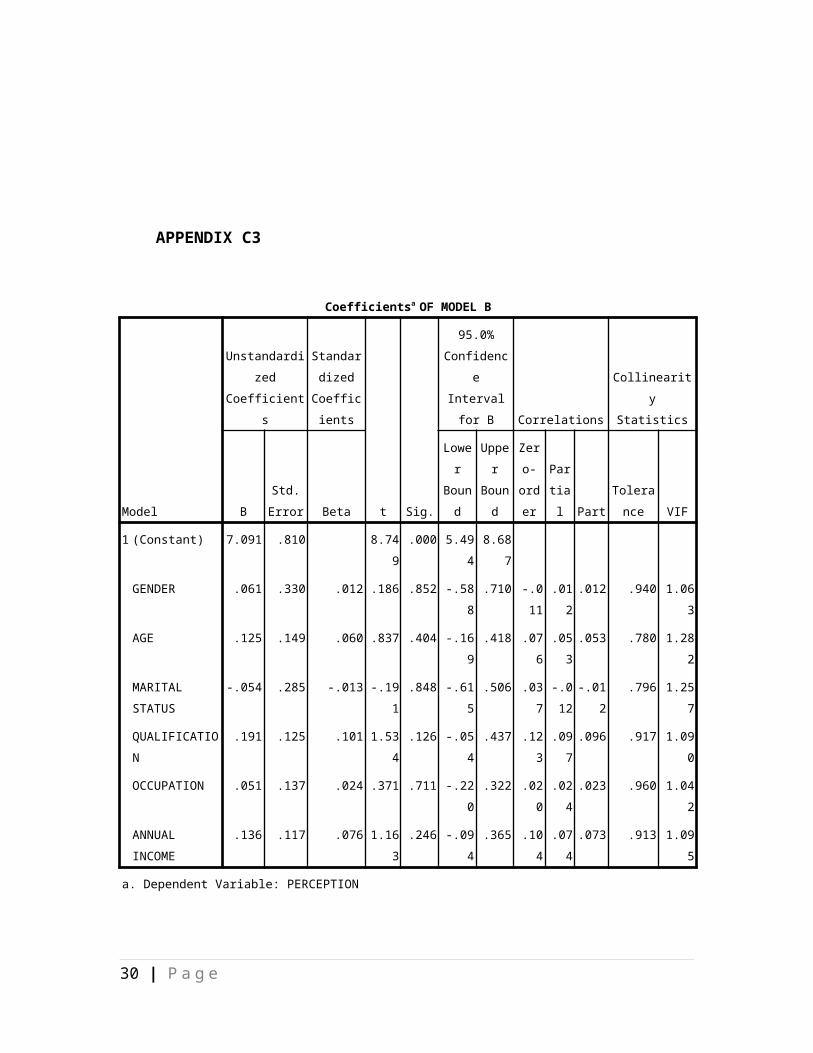

Therefore, all theseindependent variables(Annual income, Gender,Occupation, Qualification,Marital status and Age) arenot model fit. This is dueto the calculated p-valueof 0.399 is greater thanthe tabulated p-value of0.05. They cannot predictincome earners perception(Appendix C1 to C4).

5.0 Discussion of theResearch Findings:

12 | P a g e

It is observed that theservice providers lack ofan in-depth insight intothe customers ‘preferencealways create disconnectbetween what customers wantand what service provideroffers. Takaful is amongthe services of insuranceprovided that has hadintangible element whichrequires in-depth analysisto understand whatcustomers want. This hasmade the research to makean attempt to develop theinstrument to measureconsumers’ perception ofTakaful consumption in theNigerian insuranceindustry. The three (3)constructs: awareness;trust and confidence andsocio-economic factors aretested to determine if theycan predict consumers’perception on theconsumption of Takaful inKano market.

The study’s findings haveindicated that among thetwo models tested, model Bis not significant, notmodel fit and incapable inpredicting dependentvariable: perception. Thisshows that only awareness

level and level of trustand confident reposed onTakaful operator (of modelA) are good predictors andsignificant to causeperception of consumers’perception of Takafulservices consumption

Consumers’ level ofawareness of Takafulservices is found totypically having stronginfluence to influenceconsumers favorableperception of Takafulservices consumption. Thisexplains that creatingconsumers’ awareness ofTakaful services isrequisite, but that aloneis not enough to ensureconsumption of theservices. Operators shouldnote that there is need towork on creating awarenessof their offerings whichwould pave way to makeconsumers see Takaful asrelevant in meeting theirneeds.

Similarly, it is discoveredthat the consumers’ trustand confidence reposed onthe Takaful operators isgreater than typical andaveragely effective incausing favorable

13 | P a g e

perception of Takafulservices consumption. Thisis justified if due regardis paid to the reportedhistorical experience ofNigerians over the servicesdelivery of Nigerianinsurance industry.Besides, all the Takafuloperators are also offeringthe services ofconventional insurance astheir main business.Because, all the Takafulservices provided in KanoMetropolis acts as eitherwindow operation orsubsidiary of theseNigerian insurancecompanies. Therefore,establishing consumers’trust and confidence isprimary to all Takafuloperators for them to beable to win favorableconsumers perception.

5.1 Conclusion andRecommendations: Theresearch explores thecauses of consumers’perception of Takafulservices consumption inKano Metropolis, Nigeria.The implications of thefindings indicate that theconsumers’ socio- economicfactors can not causefavorable perception of

Takaful servicesconsumption. It isconcluded that at the levelof Takaful servicesdevelopment and consumptionin the Kano Metropolis,gender, age, maritalstatus, educationalqualifications, type ofoccupation and income levelof the consumers are notcapable of predicting howTakaful is seen as worthyof consuming or not in themarket.

It is imperative that theconsumers’ awareness ofTakaful services should beintensified. Takafuloperators and the Nigerianinsurance commission haveto embark on awarenesscampaign on the existenceof Takaful services in theKano market and Nigeria ingeneral. This entailsemploying all avenues;marketing strategists areneeded in ensuring that thetarget consumers have seenthe relevant of Takaful andits capability to meettheir needs which is leftopened by the conventionalinsurance. The operatorsshould know that creationof awareness of Takafulservices is not enough.

14 | P a g e

There is need to back itwith actions and efforts.

Building and winning trustand confidence of consumersis a stepping stone to markthe beginning of thesuccess in Takaful servicesconsumption in Kano market.It is established that theTakaful operator need tochange and reshape theirreputation to be distinctand quite different fromthe past negative image ofNigerian conventionalinsurance companies.

5.2 Suggestion for furtherResearch: This study has discoveredunique findings which are:that the socio-economicfactors are not significantin explaining consumers’perception. This calls fornew study that caninvestigate this position.Besides, as an exploratoryresearch, new research isneeded to re-affirm theposition of the consumers’level of awareness andtheir trust and confidencereposed in Takafuloperator.

15 | P a g e

References

Ado. A (2013): Takaful:Insurance PracticeAccording to IslamicPrinciples; aPresentation Made for AConversion Programme atthe Islamic Institutefor Accounting andFinance in Nigeria.

Alamasi. A. (2010):“Surveying Developmentin Takaful Industry:Prospects andChallenge”; Review ofIslamic EconomicJournal, Vol. 13, No 2,pp 195 – 210.

Atiquzzafau (2011):Takaful: Concepts andModels: Presentationfor the DistanceLearning Course on

Islamic Finance at IITEand IIUI

Ayuba. H (2013):Determinants of theIslamic Insurance(Takaful) ServicesConsumption in KanoMetropolis, Nigeria;Unpublished M.ScDissertation Submittedto the DepartmentBusiness Administrationand EntrepreneurshipStudies, BayeroUniversity Kano (BUK),Nigeria.

Basher. M. S HJ Mail. N. Hand Abd’Ali. M. J. A(2011): ConsumerPerception on TakafulBusiness in BrunerDurussalam, Presentedin InternationalConference onManagement (ICM)Proceeding.

Billah M. M (c) (undated):Development andApplication of Islamicinsurance (Takaful):Retrieved fromwww.Mamma.com dated25/4/2011.

Isa. B. k and Dandago. K.S(2010): PromotingCooperative Takaful toCommercial TakafulStatus for SocietalRegeneration: A case

16 | P a g e

study of A.A. ZubairuInitiative. Presentedat 2nd InternationalConference on IslamicEconomic and TradeIntegration, held inTehran, Iran.

Obalola. M .A (2010) Ethicsand SocialResponsibility in theNigerian InsuranceIndustry: A Multi-Methods Approach. A PhDThesis Submitted to De-Montfort University,Leicester.

Olawokudejo. F (2009):“Does Religion Affectthe Procurement ofInsurance Policies?Evidence fromNigerian”; “TheNigerian Journal ofRisk and Insurance”:Vol.6 (1) pp.30

Omar .O.E and Owasu-frimpong .N (2007):Life Insurance inNigerian: AnApplication of theTheory of ReasonedAction to Consumers’Attitude and PurchaseIntention; The serviceIndustries Journal:vol.27 (7) pp.963

Kotler P. (2000): MarketingManagement: 10th

Edition, Prentice Hall

of India Limited, NewDelhi.

Kotler .P. and Keller .K.(2005): MarketingManagement: 12th Edition:Prentice Hall of IndiaPrivate Ltd., NewDelhi.

Morgan.G.A, Leech; N. L,Gloeckner. G.W. andBarrett. K.C. (2004)SPSS For introductoryStatistics: Use andInterpretation; 2editions: LawrenceErlbaum AssociatesPublishers Mahwan, NewJersey, and London

Rahman. Z. A, Yusuf. R. M,and Bakar. F. A (2008):“Family Takaful: ItsRole in social EconomicDevelopment and as aSavings and InvestmentInstrument inMalaysia”. An extensionShariah journal, vol.16, No. 1 pp 89 – 105.

Rahman. Z. A (2009):“Takaful: PotentialDemand and Growth”;Journal of Kau, IslamicEconomics, Vol. 22, No.1 pp 171 – 1.

Taylor. D. Y (2005): TenYear Master Plan forthe Islamic FinancialIndustry (Takaful).Retrieved from

17 | P a g e

www.Google.com dated22/5/2011.

Yazid. A. S, Arifin. J,Hussain. M .R, Daud. W.N. W (2012):”Determinants of FamilyTakaful (Islamic LifeInsurance); AConceptual FrameworkFor a Malaysian Study”.

International Journalof Business andManagement; Vol.7,No.6, March, 16th.

18 | P a g e

APPENDIX A1

Individual question reliability Cronbach’s Alpha

coeffiencient

Item-Total Statistics

Scale Meanif ItemDeleted

ScaleVariance ifItem Deleted

CorrectedItem-TotalCorrelation

Cronbach'sAlpha if Item

Deleted

AWARENESS CAMPAIGN 38.90 49.522 .429 .794

RELIGIOUS BACKGROUND 39.10 50.064 .369 .800

COMPANIES OFFER TAKAFUL SERVICES

40.12 51.977 .245 .812

TAKAFUL DEVOID OF RIBA,GHARAR $MAISIR

39.22 49.865 .382 .799

GENERAL TAKAFUL MEETS NEEDS

40.00 49.065 .377 .800

FAMILY TAKAFUL MEETS NEEDS

39.80 48.040 .456 .792

TAKAFUL OPERATORS SERVE AS WINDOW

39.66 49.420 .508 .787

TAKAFUL PROVIDES INVESTMENT $ RISK MANAGEMENT

39.51 48.291 .581 .781

TAKAFUL IS SUBTITUTE OF$ DIFFERENT FROM INSURANCE

39.32 48.648 .561 .783

ESTABLISHED RECORDS ASSURE ME TO BUY TAKAFUL

39.70 48.071 .590 .780

IT'S SIMPLER & EASIER TO MAKE CLAIM FROM TAKAFUL

39.53 49.933 .490 .789

MY CONFIDENCE & TRUST OF TAKAFUL IS VERY HIGH

39.57 48.417 .538 .784

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

19 | P a g e

APPENDIX A2

Awareness’s Reliability Cronchback’s Alpha coefficient

Item-Total Statistics

Scale Mean ifItem Deleted

ScaleVariance ifItem Deleted

CorrectedItem-TotalCorrelation

Cronbach'sAlpha if Item

Deleted

AWARENESS CAMPAIGN 17.41 13.951 .363 .578

RELIGIOUS BACKGROUND 17.61 14.136 .307 .598

COMPANIES OFFER TAKAFUL SERVICES

18.64 14.608 .240 .624

TAKAFUL DEVOID OF RIBA,GHARAR $MAISIR

17.76 13.269 .405 .560

GENERAL TAKAFUL MEETS NEEDS

18.50 12.936 .390 .566

FAMILY TAKAFUL MEETS NEEDS

18.29 12.736 .429 .549

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

Reliability Statistics

Cronbach'sAlpha N of Items

.624 6

20 | P a g e

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

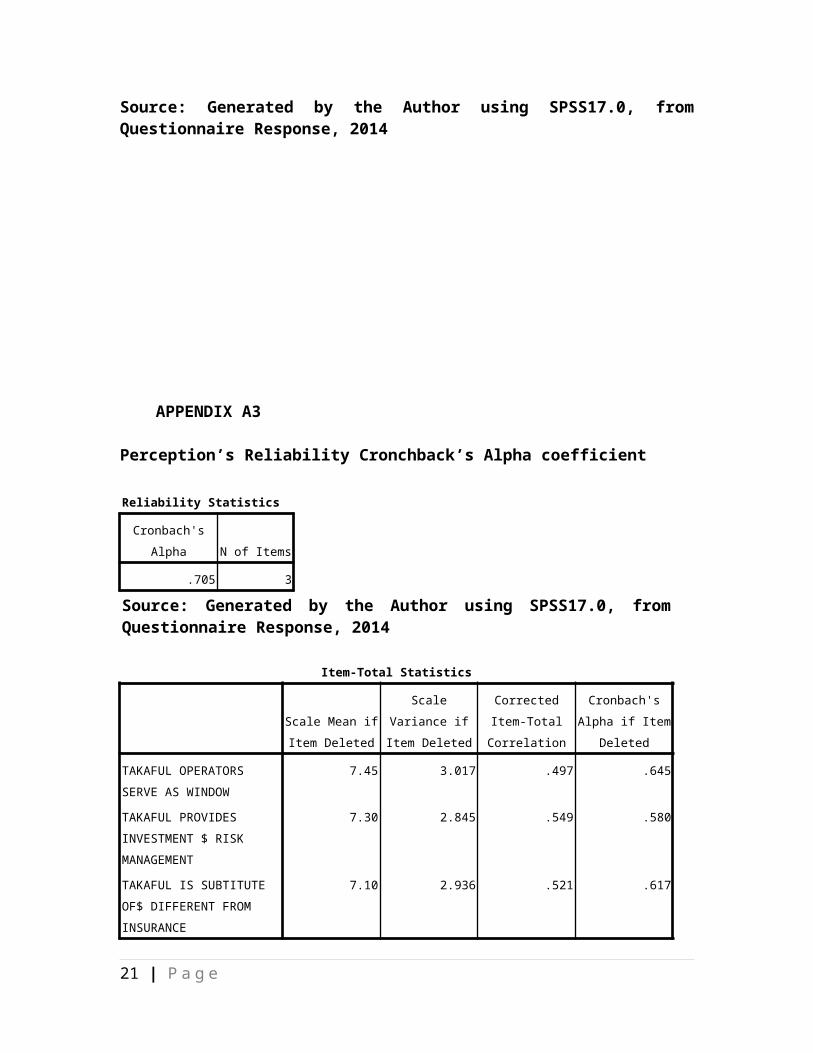

APPENDIX A3

Perception’s Reliability Cronchback’s Alpha coefficient

Reliability Statistics

Cronbach'sAlpha N of Items

.705 3

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

Item-Total Statistics

Scale Mean ifItem Deleted

ScaleVariance ifItem Deleted

CorrectedItem-TotalCorrelation

Cronbach'sAlpha if Item

Deleted

TAKAFUL OPERATORS SERVE AS WINDOW

7.45 3.017 .497 .645

TAKAFUL PROVIDES INVESTMENT $ RISK MANAGEMENT

7.30 2.845 .549 .580

TAKAFUL IS SUBTITUTE OF$ DIFFERENT FROM INSURANCE

7.10 2.936 .521 .617

21 | P a g e

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

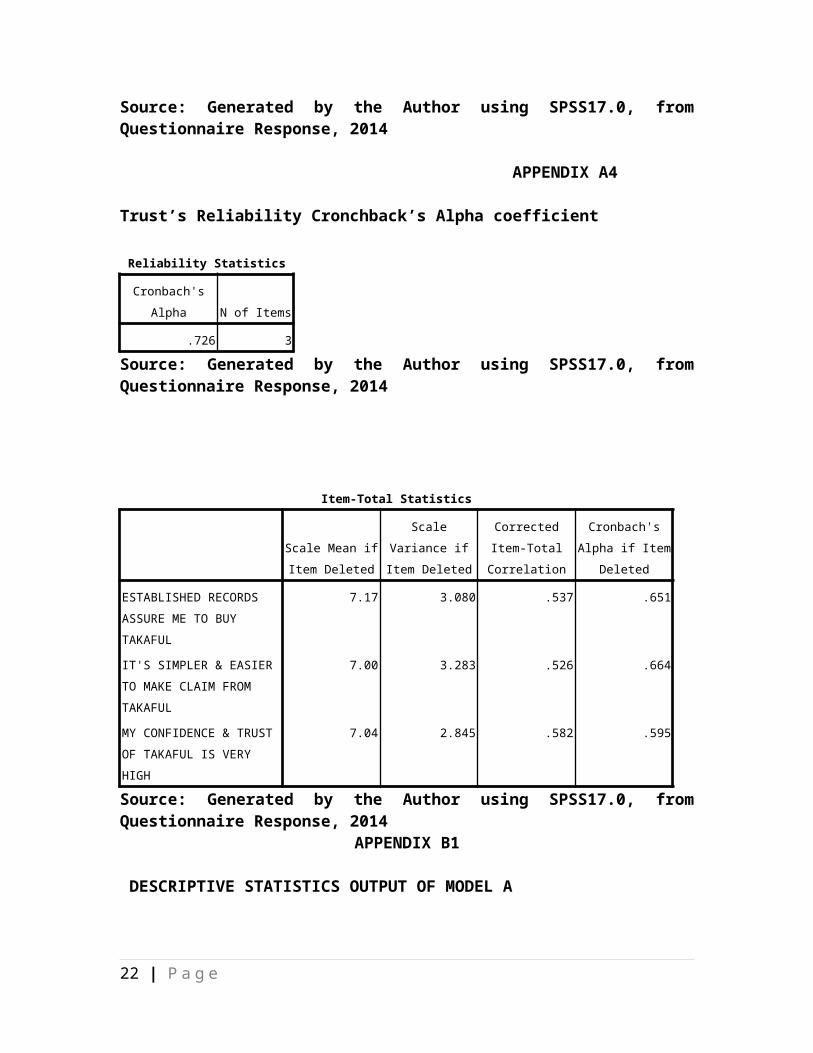

APPENDIX A4

Trust’s Reliability Cronchback’s Alpha coefficient

Reliability Statistics

Cronbach'sAlpha N of Items

.726 3

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

Item-Total Statistics

Scale Mean ifItem Deleted

ScaleVariance ifItem Deleted

CorrectedItem-TotalCorrelation

Cronbach'sAlpha if Item

Deleted

ESTABLISHED RECORDS ASSURE ME TO BUY TAKAFUL

7.17 3.080 .537 .651

IT'S SIMPLER & EASIER TO MAKE CLAIM FROM TAKAFUL

7.00 3.283 .526 .664

MY CONFIDENCE & TRUST OF TAKAFUL IS VERY HIGH

7.04 2.845 .582 .595

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

APPENDIX B1

DESCRIPTIVE STATISTICS OUTPUT OF MODEL A

22 | P a g e

Descriptive Statistics

MeanStd.

Deviation N

PERCEPTION 8.3724 1.91001 256

AWARENESS 18.8523 3.66434 255

TRUST 8.2248 1.91554 255

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

APPENDIX B2

CORRELATION COEFFICIENT OUTPUT OF MODEL A

23 | P a g e

Correlations

PERCEPTION AWARENESS TRUST

Pearson Correlation

PERCEPTION 1.000 .454 .635

AWARENESS .454 1.000 .432

TRUST .635 .432 1.000

Sig. (1-tailed)

PERCEPTION . .000 .000

AWARENESS .000 . .000

TRUST .000 .000 .

N PERCEPTION 256 249 253

AWARENESS 249 255 248

TRUST 253 248 255

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

Coefficient Correlationsa

Model TRUST AWARENESS

1 Correlations

TRUST 1.000 -.432

AWARENESS -.432 1.000

Covariances TRUST .003 .000

AWARENESS .000 .001

a. Dependent Variable: PERCEPTIONSource: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

24 | P a g e

APPENDIX B3

MULTIPLE REGRESSION OUTPUT OF MODEL B

Model Summaryb

Model R

RSquare

Adjusted RSquare

Std. Error ofthe Estimate

Change Statistics

R SquareChange

FChange

df1

df2

Sig. FChange

1 .666a

.443 .439 1.43088 .443 97.557 2 245

.000

a. Predictors: (Constant), TRUST, AWARENESS

b. Dependent Variable: PERCEPTIONSource: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

APPENDIX B4

COEFFICIENT OUTPUT OF MODEL A

Coefficientsa

Model

UnstandardizedCoefficients

StandardizedCoefficients

tSig.

CollinearityStatistics

B Std. Error Beta Tolerance VIF

1 (Constant) 1.776 .521 3.409 .001

AWARENESS .115 .028 .221 4.174 .000

.813 1.230

TRUST .538 .053 .540 10.215.00

0.813 1.230

a. Dependent Variable: PERCEPTION

25 | P a g e

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

APPENDIX B5

NORMALITY PLOT OF DEPENDENT VARIABLE OF MODEL A

26 | P a g e

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

APPENDIX B6

27 | P a g e

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

28 | P a g e

APPENDIX C1

Model Summary OF MODEL B

Model R

RSquare

Adjusted RSquare

Std. Error ofthe Estimate

Change Statistics

R SquareChange

FChange

df1

df2

Sig. FChange

1 .157a

.025 .001 1.90909 .025 1.041 6 247

.399

a. Predictors: (Constant), ANNUAL INCOME, OCCUPATION, GENDER, MARITAL STATUS, QUALIFICATION, AGE

b. Dependent Variable: PERCEPTIONSource: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

APPENDIX C2

ANOVAb OF MODEL B

ModelSum ofSquares df Mean Square F Sig.

1 Regression 22.759 6 3.793 1.041 .399a

Residual 900.221 247 3.645

Total 922.980 253

a. Predictors: (Constant), ANNUAL INCOME, OCCUPATION, GENDER, MARITAL STATUS, QUALIFICATION, AGE

b. Dependent Variable: PERCEPTIONSource: Generated by the Author using SPSS17.0, fromQuestionnaire Response,

29 | P a g e

APPENDIX C3

Coefficientsa OF MODEL B

Model

Unstandardized

Coefficients

StandardizedCoefficients

t Sig.

95.0%Confidenc

eIntervalfor B Correlations

Collinearity

Statistics

BStd.Error Beta

Lower

Bound

Upper

Bound

Zero-order

Partial Part

Tolerance VIF

1 (Constant) 7.091 .810 8.749

.000 5.494

8.687

GENDER .061 .330 .012 .186 .852 -.588

.710 -.011

.012.012 .940 1.06

3

AGE .125 .149 .060 .837 .404 -.169

.418 .076

.053.053 .780 1.28

2

MARITAL STATUS

-.054 .285 -.013 -.191

.848 -.615

.506 .037

-.012

-.012

.796 1.257

QUALIFICATION

.191 .125 .101 1.534

.126 -.054

.437 .123

.097.096 .917 1.09

0

OCCUPATION .051 .137 .024 .371 .711 -.220

.322 .020

.024.023 .960 1.04

2

ANNUAL INCOME

.136 .117 .076 1.163

.246 -.094

.365 .104

.074.073 .913 1.09

5

a. Dependent Variable: PERCEPTION

30 | P a g e

Source: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

APPENDIX C4

31 | P a g e

Collinearity Diagnosticsa OF MODEL B

Model

Dimension

Eigenvalue

Condition

Index

Variance Proportions

(Constant) GENDER AGE

MARITAL

STATUSQUALIFICATI

ONOCCUPATIO

N

ANNUAL

INCOME

1 1 6.416 1.000 .00 .00 .00 .00 .00 .00 .00

2 .188 5.841 .00 .07 .06 .00 .00 .26 .28

3 .138 6.824 .00 .04 .12 .04 .00 .22 .48

4 .109 7.686 .00 .34 .22 .00 .01 .30 .10

5 .084 8.725 .00 .09 .06 .00 .89 .01 .08

6 .047 11.687 .00 .13 .46 .77 .06 .00 .00

7 .018 18.862 .99 .33 .07 .18 .03 .21 .05

a. Dependent Variable: PERCEPTIONSource: Generated by the Author using SPSS17.0, fromQuestionnaire Response, 2014

APPENDIX DQUESTIONNAIRE FOR CONSUMERS (INCOME EANERS)

PERSONAL DATA

Please tick (√) where appropriately the boxes below and fill

in the spaces where applicable.32 | P a g e

1. Sex: a. Male b. Female

2. Kindly do indicate the age group.

a. 18 – 25Years b. 26 – 35Years c. 36

– 45Years

d. 46 – 55Years e. 55Years and above.

3. Your marital status is:-

a. Single b. Married c. Separate

d. Widowed

e. Divorced

4. Qualification of the Respondents

a. WAEC/Equivalent b.

OND/NCE/Equivalent

c. HND/B.Sc/B.A/B.Ed d. MBA/MBF/ACA or

Equivalent

e. M.Sc. /Ph.D. f.

Others (Please Specify)……………..

5. Occupational status of the Respondents

a. Business Man/Woman b. Civil

Servant

33 | P a g e

c. Private Organization Employee c.

Military/Paramilitary

d. Others (Please specify)…………………………….…………………

6. Annual Income Level of the Respondents

a. Below N500,000 P/A b. N500,001 –

N1,000,000 P/A

c. N1, 000,001 – N5, 000,000 P/A d. N5,

000,001 – 10,000,000 P/A

e. N10, 000,001 – And Above

Instruction: Below are statements that describe how you see,

feel or think about Islamic Insurance services consumption

in Kano Metropolis, Nigeria. Please, answer the questions

by using scales to rank them 1 to 5 to indicate your level

of agreement or disagreement with each statement as

presented below.

KEY: 1 = Strongly Disagree (SD) 2 = Disagree (D)

3 = Undecided (UD) 4 = Agree (A)

5 = Strongly Agree (SA)

S/N SECTION 1 (AWARENESS CONSTRUCT) RANK

QUESTIONS

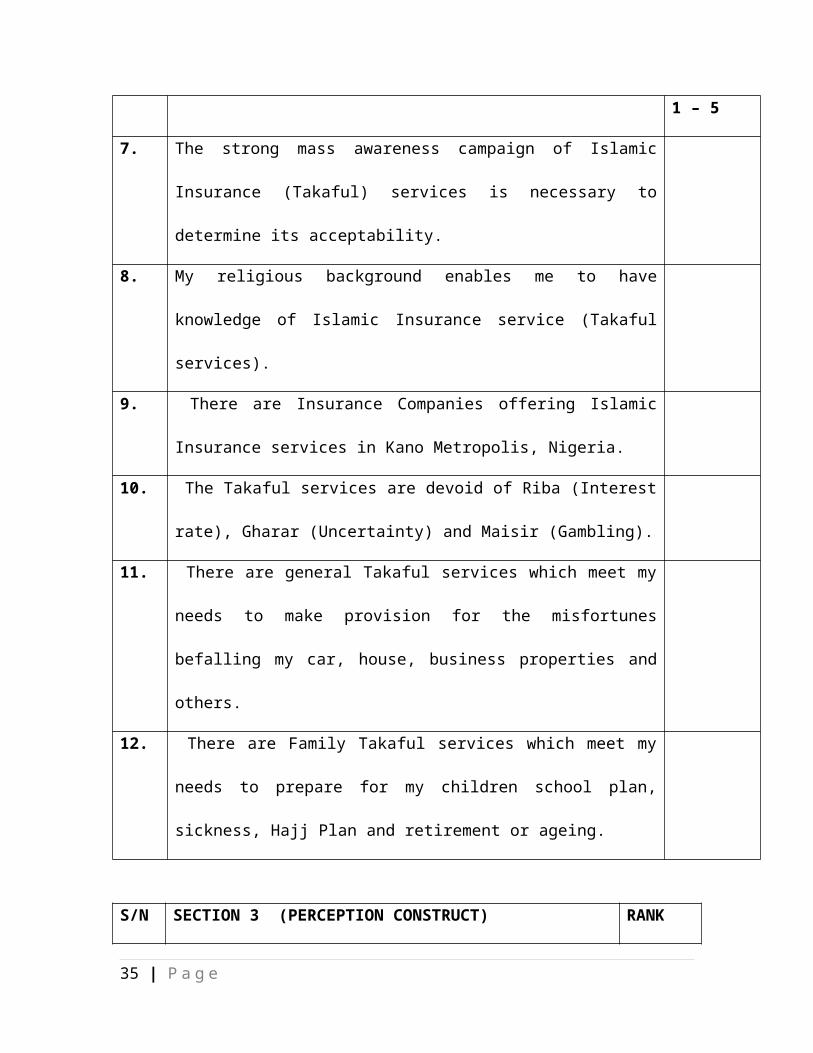

34 | P a g e

1 – 5

7. The strong mass awareness campaign of Islamic

Insurance (Takaful) services is necessary to

determine its acceptability.

8. My religious background enables me to have

knowledge of Islamic Insurance service (Takaful

services).

9. There are Insurance Companies offering Islamic

Insurance services in Kano Metropolis, Nigeria.

10. The Takaful services are devoid of Riba (Interest

rate), Gharar (Uncertainty) and Maisir (Gambling).

11. There are general Takaful services which meet my

needs to make provision for the misfortunes

befalling my car, house, business properties and

others.

12. There are Family Takaful services which meet my

needs to prepare for my children school plan,

sickness, Hajj Plan and retirement or ageing.

S/N SECTION 3 (PERCEPTION CONSTRUCT) RANK

35 | P a g e

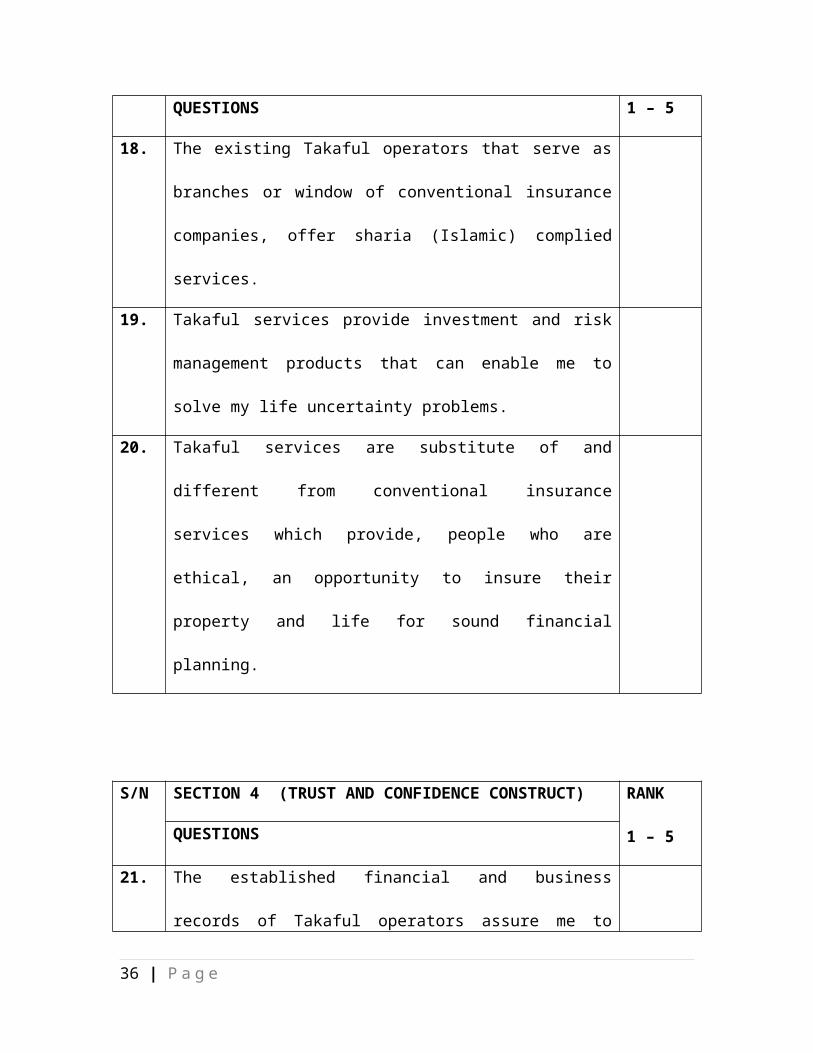

1 – 5QUESTIONS

18. The existing Takaful operators that serve as

branches or window of conventional insurance

companies, offer sharia (Islamic) complied

services.

19. Takaful services provide investment and risk

management products that can enable me to

solve my life uncertainty problems.

20. Takaful services are substitute of and

different from conventional insurance

services which provide, people who are

ethical, an opportunity to insure their

property and life for sound financial

planning.

S/N SECTION 4 (TRUST AND CONFIDENCE CONSTRUCT) RANK

1 – 5QUESTIONS

21. The established financial and business

records of Takaful operators assure me to

36 | P a g e

invest my money by buying Takaful services.

22. It seems simpler and easier to make claim

(receipt of compensation as at the time when

the disaster befalls one) from the Takaful

operators than from the conventional

insurance companies.

23. My confidence and trust are very high on the

Takaful companies operating in Kano

Metropolis, Nigeria.

Thank you so much for the valuable time you spent in answeringthis questionnaire. Please, feel free to contact me forimprovement regarding to the questionnaire through my address.

37 | P a g e

Related Documents