FUND OF HEDGE FUNDS - EASY TO SUCCEED Pensions&Investments February 19, 2010 http://www.pionline.com/white-papers/2373942 Rob Brown, PhD, CFA I. INTRODUCTION Over the last dozen years, the fund of hedge funds (hereafter referred to as FoF) industry experienced amazing exponential growth, followed by collapse, and today, has once again embarked on a period of rapid growth. In 2000, the size of the FoF industry was estimated to be $83.5 billion 1 . Over the subsequent seven years, it grew by 974%, reaching total assets under management of $897 billion. By 2009, the FoF industry had fallen to $430 billion, a 52% decline. Current projections call for the FoF industry to grow by 196% over the next four years, reaching $2,600 billion by the end of 2013. FoF grew fast, shrank catastrophically, and are once again following a path of exponential growth. This paper attempts to identify why FoF have failed in the past, why certain isolated FoF will fail in the future, and what is required for a FoF to succeed in both the short- and long-run. The framework presented here is directly applicable to: (i) research and due diligence efforts designed to select FoF, (ii) those institutional investors who, instead of hiring one or more FoF, decide to directly manage a portfolio of individual hedge funds themselves, and (iii) Trustee Boards who must oversee, evaluate, and measure an internal hedge fund program directed by staff. II. WINNING THE LOSER’S GAME Charlie Ellis has been one of the investment industry’s more prolific contributors. He founded Greenwich Associates, served as chair and governor of the CFA Institute, acted as associate editor for both The Journal of Portfolio Management and The Financial Analysts Journal, and served on the faculty of the Harvard Business School, the Yale School of Management, and the Investment Workshop at Princeton. In 1975, Charlie Ellis, famously observed that investing was “a loser's game.” Like amateur tennis, he wrote in the classic Winning the Loser's Game 2 (required reading for past CFA candidates), investing is an activity in which the victor often prevails because he makes fewer mistakes than his rival does. Ellis speaks to how short- and long-run success is most often a function of avoiding the missteps made by your competitors as opposed to winning larger bets than the next guy. But FoF are not your typical investment. Their short- and long-run success is driven and defined to a far greater extent (a full order of magnitude greater) by the simple avoidance of a series of classic mistakes. Therefore, FoF are unusually well defined by the Winning the Loser’s Game paradigm. FoF stand out within the broadly defined investments industry as both one of its greater successes (growing by 974% in just seven years) and one of its greatest failures (shrinking by 52% in just two years). These two opposing extremes

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FUND OF HEDGE FUNDS - EASY TO SUCCEED

Pensions&Investments

February 19, 2010

http://www.pionline.com/white-papers/2373942

Rob Brown, PhD, CFA

I. INTRODUCTION

Over the last dozen years, the fund of hedge funds (hereafter referred to as FoF) industry experienced amazing

exponential growth, followed by collapse, and today, has once again embarked on a period of rapid growth. In 2000,

the size of the FoF industry was estimated to be $83.5 billion1. Over the subsequent seven years, it grew by 974%,

reaching total assets under management of $897 billion. By 2009, the FoF industry had fallen to $430 billion, a 52%

decline. Current projections call for the FoF industry to grow by 196% over the next four years, reaching $2,600 billion

by the end of 2013.

FoF grew fast, shrank catastrophically, and are once again following a path of exponential growth. This paper

attempts to identify why FoF have failed in the past, why certain isolated FoF will fail in the future, and what is

required for a FoF to succeed in both the short- and long-run. The framework presented here is directly applicable

to: (i) research and due diligence efforts designed to select FoF, (ii) those institutional investors who, instead of

hiring one or more FoF, decide to directly manage a portfolio of individual hedge funds themselves, and (iii) Trustee

Boards who must oversee, evaluate, and measure an internal hedge fund program directed by staff.

II. WINNING THE LOSER’S GAME

Charlie Ellis has been one of the investment industry’s more prolific contributors. He founded Greenwich Associates,

served as chair and governor of the CFA Institute, acted as associate editor for both The Journal of Portfolio

Management and The Financial Analysts Journal, and served on the faculty of the Harvard Business School, the Yale

School of Management, and the Investment Workshop at Princeton. In 1975, Charlie Ellis, famously observed that

investing was “a loser's game.” Like amateur tennis, he wrote in the classic Winning the Loser's Game2

(required

reading for past CFA candidates), investing is an activity in which the victor often prevails because he makes fewer

mistakes than his rival does. Ellis speaks to how short- and long-run success is most often a function of avoiding the

missteps made by your competitors as opposed to winning larger bets than the next guy.

But FoF are not your typical investment. Their short- and long-run success is driven and defined to a far greater extent

(a full order of magnitude greater) by the simple avoidance of a series of classic mistakes. Therefore, FoF are

unusually well defined by the Winning the Loser’s Game paradigm.

FoF stand out within the broadly defined investments industry as both one of its greater successes (growing by 974%

in just seven years) and one of its greatest failures (shrinking by 52% in just two years). These two opposing extremes

speak to the outsized investment opportunities available to FoF and the similarly outsized perils that they must

successfully mitigate in order to succeed. Profound opportunity and peril are the defining elements of the

environment within which FoF operate, and it is for this reason that the Winning the Loser’s Game paradigm holds

most strongly for this segment of the investments industry.

FoF operate within a far harsher environment that is located closer to the eye of the storm than more traditional

investment management structures. Hedge funds are generally defined by greater focus, concentration, and leverage.

They often make use of shorting and derivatives. Their trades or positions may make use of more embryonic and less

widely understood opportunities/risks. Hedge funds often push on regulatory boundaries. These attributes of the

hedge fund environment mean that their investment, business, and operational opportunities and risks are generally

better defined, better understood, far more potent, and arise with sharper edges. Frequently, these opportunities

and challenges have been poorly managed or inadequately dealt with by individual FoF. This paper applies the Ellis

framework to the management of a successful FoF, in the sense of identifying the primary missteps to which FoF are

most susceptible. Following the Ellis framework, and given the bountiful opportunities available to FoF, if a FoF can

avoid these specific missteps, then they are likely to experience significant investment success.

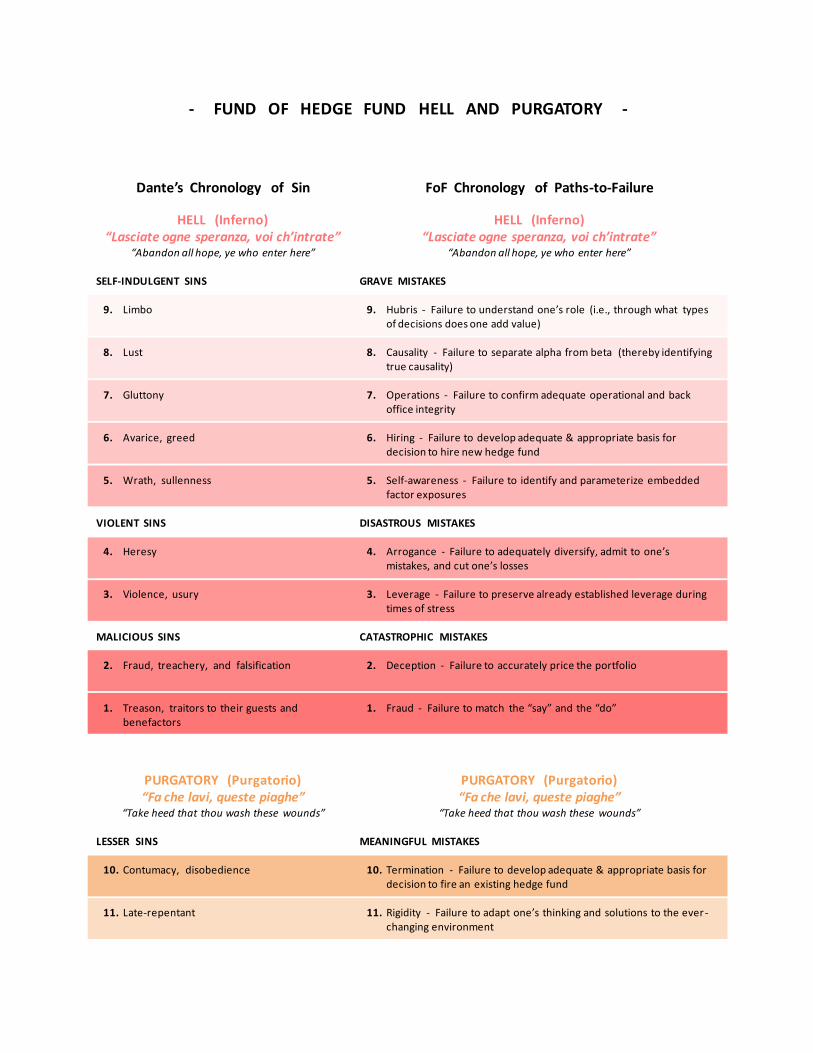

III. FRAMEWORK FOR CATEGORIZING VARIOUS FoF MISTAKES

The remainder of this paper identifies the primary missteps to which FoF are most susceptible. These mistakes vary in

terms of severity, probability of occurrence, and ability to recover from such missteps. As a result of these

differences, the identification and discussion of the alternate paths-to-failure benefits from a framework for

categorizing them and a specific chronology for their review. For this purpose, I adopt the framework provided by

Dante Alighieri in his The Divine Comedy3 from the fourteenth century. This may at first seem like an odd structure for

arranging a discussion of the ways that FoF can fail, but Dante’s framework offers three attractive attributes.

First, he breaks the various paths-to-failure (or sin in his parlance) into four distinct categories (self-indulgent

sins, violent sins, malicious sins, and the sins of the unrepentant). These categories help us understand the

relative criticality of the different FoF missteps – and speak to their origins.

Second, he provides a specific chronology for examining each sin (path-to-failure). Starting with the 9th most

egregious sin and progressing through ever more offensive violations, eventually reaching the single most

dire (all of which are located in Hell or Inferno). Dante than steps back and progresses through two final, but

significantly lesser sins, that although traumatic, do not doom one to Hell (they are located in Purgatory or

Purgatorio).

Third, Dante provides a description of each sin (or region of Hell and Purgatory) that proves disturbingly

relevant or eerily resonant for the different ways in which specific FoF have failed over the last several years

(think Madoff, Petters, Austin, Topiary).

The following schematic provides a representation of Dante’s categorization scheme and the chronology with which

he reviews those paths-to-failure, along with the parallel labels for how FoF can or have misstepped.

Dante’s Chronology of Sin

HELL (Inferno)“Lasciate ogne speranza, voi ch’intrate”

“Abandon all hope, ye who enter here”

SELF-INDULGENT SINS

9. Limbo

8. Lust

7. Gluttony

6. Avarice, greed

5. Wrath, sullenness

VIOLENT SINS

4. Heresy

3. Violence, usury

MALICIOUS SINS

2. Fraud, treachery, and falsification

1. Treason, traitors to their guests and benefactors

PURGATORY (Purgatorio)“Fa che lavi, queste piaghe”

“Take heed that thou wash these wounds”

LESSER SINS

10. Contumacy, disobedience

11. Late-repentant

- FUND OF HEDGE FUND HELL AND PURGATORY -

FoF Chronology of Paths-to-Failure

HELL (Inferno)“Lasciate ogne speranza, voi ch’intrate”

“Abandon all hope, ye who enter here”

GRAVE MISTAKES

9. Hubris - Failure to understand one’s role (i.e., through what typesof decisions does one add value)

8. Causality - Failure to separate alpha from beta (thereby identifyingtrue causality)

7. Operations - Failure to confirm adequate operational and backoffice integrity

6. Hiring - Failure to develop adequate & appropriate basis fordecision to hire new hedge fund

5. Self-awareness - Failure to identify and parameterize embedded factor exposures

DISASTROUS MISTAKES

4. Arrogance - Failure to adequately diversify, admit to one’s mistakes, and cut one’s losses

3. Leverage - Failure to preserve already established leverage duringtimes of stress

CATASTROPHIC MISTAKES

2. Deception - Failure to accurately price the portfolio

1. Fraud - Failure to match the “say” and the “do”

PURGATORY (Purgatorio)“Fa che lavi, queste piaghe”

“Take heed that thou wash these wounds”

MEANINGFUL MISTAKES

10. Termination - Failure to develop adequate & appropriate basis fordecision to fire an existing hedge fund

11. Rigidity - Failure to adapt one’s thinking and solutions to the ever -changing environment

The preceding diagram delineates the eleven most critical mistakes to which FoF are most susceptible. These eleven

are numbered according to their severity, probability of occurrence, and ability of a FoF to recover from – with the

lowest (highest) number being the most (least) critical. Following Dante’s lead, I have arranged these eleven into four

distinct categories, labeled: “Grave Mistakes,” “Disastrous Mistakes,” “Catastrophic Mistakes,” and “Meaningful

Mistakes.” Grave, disastrous, and catastrophic paths-to-failure are all located in Hell – signifying the lack of hope for

redemption or recovery. The last category of meaningful mistakes resides in Purgatory, signifying the egregious

nature of the sin or mistake, but leaving hope for the FoF to redeem itself and potentially recover. Obviously, the

coloration dovetails with the egregiousness of the FoF failure.

The remainder of this paper examines these eleven alternate modes by which FoF can fail. I examine them in the

order followed by Dante during his travels through the various regions of Inferno and Purgatorio.

IV. ELEVEN WAYS THAT FoF FAIL

GRAVE MISTAKES, SELF-INDULGENT SINS - MISTAKES 9. - 5.

We begin by examining five mistakes that will inevitably doom a FoF to eventual failure – although the day of

reckoning may be far into the future. These five failings, Hubris, Causality, Operations, Hiring, and Self-awareness, are

the direct result of a “self-indulgent” process on the part of the FoF.

9. Hubris - Failure to understand one’s role (i.e., through what types of decisions does one add value). The

mistake that some FoF make is to believe that they have the ability to predict the timing of when a beta (factor

exposure) or the timing of when a hedge fund style (alpha opportunity) will pay off. This false belief that they have

“Oracle of Delphi”-type powers that enable them to predict the timing of future events leads such FoF to time markets

or to time their allocations to hedge fund sectors.

FoF make this mistake when they forget the rule of relative comparative advantage. FoF do have a relative

comparative advantage to: (i) identify and parameterize the attributes of individual hedge funds, (ii) select superior

hedge funds, (iii) construct more efficient and well-behaved portfolios of hedge funds, and (iv) draw important

distinctions about the relative alpha opportunities across various hedge fund sectors. However, FoF have no particular

expertise (and probably operate with a meaningful relative disadvantage) in the prediction of when a beta or market-

imperfection (alpha source) will be rewarded.

An important distinction needs to be drawn between:

Claiming the ability to know in the advance the timing of future events –which leads one to time their

allocations to various hedge fund styles.

VERSUS

Developing a deep understanding of how pockets of imperfection and mispricing within markets vary in

terms of size, consistency, durability, and competition across the multitude of different market sectors.

The first of these is the mistake of “Hubris.” The second of these plays directly to FoF relative comparative advantage

in understanding how hedge fund strategies differ in terms of competition and opportunity resulting from the

breakdown of perfect market efficiency.

8. Causality - Failure to separate alpha from beta (thereby identifying true causality). The mistake that some FoF

make is to restrict their analysis to “total return” as opposed to breaking “total return” down into its component parts,

i.e., the portions that were caused by or are attributable to the various betas (or market exposures) inherent within its

strategy and the portion attributable to alpha (the harvesting of market imperfections). The mistake of “Causality”

applies to the evaluation of all active investment opportunities and applies just as much to long-only investment

managers as it does to hedge funds or private equity LBO funds.

If a large-cap value long-only manager returns +25% and I conclude that they have done a superior job, then I have

committed the mistake of “Causality” if the S&P 500 Value Index returned +26%. If a long/short biotechnology hedge

fund manager returns +20% and I conclude that they have done a superior job, then I have committed the mistake of

“Causality” if they were net-long 40% biotech stocks and the biotechnology index rose 55%.

All hedge funds carry with them one or more embedded betas. Although some hedge funds have labeled themselves

“market-neutral,” all this means is that this fund might potentially have a zero value with respect to one or more

betas. It does not mean that they have neutralized all betas – which would be virtually impossible and probably non-

economic. Some of the betas or factor exposures that hedge funds carry around include:

Interest rates (i.e., term structure of US Treasury bonds)

Credit spreads (i.e., term structure of credit spreads over Treasuries)

Equity risk premia

Currencies

Commodities

Volatility (i.e., term structure of implied volatilities across various capital markets)

Liquidity risk premia

To properly attribute performance to causal-skill versus simple market exposure, the FoF must first identify the factors

to which a hedge fund is exposed, and then second, parameterize the size of the factor loadings.

7. Operations - Failure to confirm adequate operational and back office integrity. The mistake that some FoF make

is to restrict their analysis and evaluation of hedge funds to purely investment-type issues. This is a mistake because

the investment success of a hedge fund portfolio also depends on business, operations, and back office

considerations. The following exhibit identifies the primary components of an appropriate evaluation of these non-

investment focused factors.

6. Hiring - Failure to develop adequate & appropriate basis for decision to hire new hedge fund. The mistake that

some FoF make is to hire a new hedge fund manager because the past returns were attractive, the fund has a good

reputation, the fund tells a good story and is staffed by highly pedigreed professionals, or the FoF likes the sector of

the market within which the hedge fund operates. These are all examples of making a decision to hire without

adequate basis. The objective of hiring a new hedge fund manager is to capture the benefits of larger, more

consistent, and more durable alpha. Given this objective, hiring decisions are then logically based on the very specific

causes of alpha. The following exhibit identifies the four specific causes of alpha.

Business, Operations, and Back Office

Risk Assessment and Mitigation

Structure

Side pockets

Liquidity provisions

Lines of credit, leverage

Cashmanagement

ISDAs

Operations

Trade execution, authorization, reconciliation

Trade quality & cost

Information technology and

systems

Disaster recovery

Compliance officer,

procedures

Pricing

Valuation policy, methodology, pricing sources

Administrator’s expertise and independence

Fraud

Portfolio and security –level confirmation

Individual trade confirmation

Investment process

confirmation

Alpha opportunity viability

assessment

Monthly return consistency / plausibility

Business

Key person

Ownership structure

Regulatory actions

Auditor response

Service Providers

Fund Administrator

Prime Brokers / Custodian

Bank

Legal Council

Auditor

InsuranceProvider

Counterparties

For example, some FoF who hired Long-Term Capital did so on the basis of reputation, pedigreed professionals, and

attractive past returns. Such decisions to hire Long-Term Capital were made without adequate understanding of the

nature of the competition, the characteristics and properties of market’s mispricing, and the manager’s process for

harvesting the market imperfection. Similarly, those FoF who hired Madoff did so on the basis of past returns, a good

story, and manager persona. The decisions to hire Madoff were made without adequate understanding of the

manager’s process for identifying and harvesting the market mispricings or even the nature of the market inefficiency.

“Hiring” without adequate basis is a corruption of intellectual integrity.

5. Self-awareness - Failure to identify and parameterize embedded factor exposures. The mistake that some FoF

make is to ignore the embedded betas (factor exposures) carried forward into their portfolio by each of their

underlying hedge fund managers. Two seminal research papers, “Determinants of Portfolio Performance” 4, and

“Determinants of Portfolio Performance II: An Update” 5

initiated a stream of follow-on research and eventual

industry-wide understanding that the single largest determinant of return, both in the short- and in the long-run for

any reasonably diversified portfolio will be that portfolio’s asset allocation (i.e., the portfolio’s allocation to various

betas or factor exposures).

Because all hedge funds carry forward into a FoF portfolio embedded betas (factor exposures) this is a critical

determinant of FoF performance. However, the problem is made far worse by the speed and degree to which

underlying hedge funds change their embedded factor exposures (betas). Therefore, if a FoF fails to maintain “Self-

Alpha

(out-performance)

at the individual hedge fund level

How inefficient is the

marketplace (to what

extent is market-failure

present)

Where are the mispricings

and market-failures

located (what parts of the

marketplace)

How good is the

manager’s process and

tools for, first, identifying

and, second, harvesting

the mispricings

How many other hedge

funds are competing for

the same opportunity

Where does out-performance come from? – What causes alpha?

awareness” of its embedded betas, it delivers to its clients a potentially large and rapidly evolving determinant of

future returns that remains unidentified and therefore fully unknown.

By mid-2008, portable alpha had become a popular structure employed by institutional investors, including pensions,

foundations, and endowments. In many cases, the implementers made use of hedge funds as their alpha engines, but

they frequently failed to take into account the embedded betas carried forward by their underlying hedge fund

managers. As a result of their failure to maintain “Self-awareness” they unknowingly doubled-up on the beta within

the portable alpha structures that they built. Their failure to maintain “Self-awareness,” led them to assume that a

diversified portfolio of hedge funds was market-neutral. The market declines of 2008 and early-2009 brought to their

attention the mistake that they had made as they experienced excessive losses due to their excess beta.

DISASTROUS MISTAKES, VIOLENT SINS - MISTAKES 4. & 3.

We next examine two far more egregious mistakes, Arrogance and Leverage. Numerous examples of FoF failures over

the last several years can be directly traced back to these two sins which are truly “violent” in their impact.

4. Arrogance - Failure to adequately diversify, admit to one’s mistakes, and cut one’s losses. The mistake that

some FoF make is to believe too strongly in their own infallibility (i.e., they suffer from “Arrogance”) with respect to

the decisions they make and the portfolio structures they build. Most frequently, this path-to-failure takes one of the

following three forms: (i) over-concentration in individual hedge funds or hedge fund styles, (ii) unwillingness to admit

to one’s own mistakes with respect to decisions, analysis, and logic, and (iii) unwillingness to cut one’s loses.

This is a particularly insidious mistake, since it most frequently leads to the construction of unusually fragile portfolio

structures or analyses that are sub-optimal, or worse yet, inapplicable. The last two-hundred years of investment

industry history are rife with examples of Mr. Market eventually punishing those who suffered from excessive

“Arrogance.” Recently, a widely-publicized hedge fund manager made billions for himself and his clients as a result of

an isolated, concentrated bet that structured credit spreads would widen (mortgage backed securities and related

instruments). But today, this fund manager has established a new and similarly concentrated bet that gold will be the

next big winner. Such distilled and unrepentant “Arrogance” results in remarkably unstable, sharp-edged “solutions.”

More frequently, at the FoF level, “Arrogance” takes the form of an unwillingness to admit that the logic underlying

the decisions that were made is either fundamentally flawed or patently sub-optimal. An example could include the

FoF who builds a portfolio of levered relative value trades while refusing to admit that such a structure inordinately

exposes their clients to an expansion of implied volatilities and liquidity risk premia.

There will always exist unknowns and never imagined relationships. “Arrogance” undermines proper appreciation for

the presence and potential potency of these unknowns – resulting in over-concentrated portfolio structures and over-

confident investment analyses.

3. Leverage - Failure to preserve already established leverage during times of stress. The mistake that some FoF

make is to hire underlying hedge funds that employ leverage, or to make use of leverage at the FoF level itself, that is

particularly susceptible to withdrawal at the worst possible point in time. This is not a new problem, and easily

parallels the stock-based margin account or the levered commercial real estate structure. Both are remarkably

susceptible to call (forced liquidation) at the worst possible time, i.e., forced liquidation when the relative valuation

opportunity is at its all time greatest and most attractive. This results in the investor being forced out of his position

when the forward-looking payoff is at its absolute greatest, and the pain of immediate liquidation is at its most

disastrous.

To avoid this mistake, FoF must hire only underlying hedge funds that have the ability to preserve their leverage when

market stress reaches its most extreme. Similarly, this also applies at the FoF level, if the FoF employs additional

leverage.

CATASTROPHIC MISTAKES, MALICIOUS SINS - MISTAKES 2. & 1.

There exist two final mistakes, Deception and Fraud, which are of such an extreme and offensive nature, that when

discovered, they result in almost instantaneous unraveling. Unfortunately, the last several years have offered several

examples of these two truly “malicious” sins.

2. Deception - Failure to accurately price the portfolio. The mistake that some FoF make is to succumb to the

“Deception” of smoothing their valuations in an attempt to deceptively (but legally, from an accounting standpoint)

make their month-to-month returns (and therefore, underlying portfolios) look less risky than they really are.

Numerous investment instruments exist that facilitate, avoid, or otherwise side-step the need to mark-to-market. The

last several years have provided a painfully long list of such instruments. Asset backed lending (ABL) has provided the

most widely recognized example. The playing field of ABL often allows participants to carry their exposures at “cost”

or “par value” instead of marking them to current and available market value. Any investment instrument, for which a

weak and relatively efficient current market exists, is susceptible to abusive manipulation of this type (e.g., trade

claims).

This is a truly “malicious” violation in that it is an intentional act, initiated and pursued with full knowledge, whereby

some party must mandatorily be harmed. If a FoF portfolio is over-valued, then new contributions are being

disadvantaged and already existing investors would be better served by liquidating their positions and reinvesting the

proceeds at current market values. If a FoF portfolio is under-valued, then already existing investors are being

disadvantaged whenever a new contribution arrives, and would be better served by closing the fund to new investors.

In either case, existing and prospective investors are being fundamentally misled as to the inherent riskiness of the

underlying portfolio.

Unfortunately, several FoF exist today that are following the path of the “living dead.” Prior to the 2008 debacle, they

loaded up on ABL and related “smoothing” instruments. They failed to mark-to-market and as a consequence gated

their investors in order to avoid paying out redemptions at their artificially inflated stated valuations. Today, they

preserve their gates (directly or more likely, indirectly via side-pockets or “liquidating trusts”), delaying the recognition

that their stated asset values significantly exceed their real-world current mark-to-market values.

1. Fraud - Failure to match the “say” and the “do”. The mistake that some underlying hedge funds have made is to

intentionally and maliciously deceive their limited partner, investor clients. Thankfully, to my knowledge, no FoF has

yet to engage in explicate “Fraud.”

“Fraud” occurs when the “say” and the “do” fail to match. Yes, we can equivocate as to the severity of the deception,

but nevertheless, intentionally saying one thing and then doing another is just plain and simple, “Fraud.” This is truly

the inner sanctum of Hell, and those who intentionally place themselves within this category, deserve what inevitably

results. 2008 offered several examples, perhaps the most widely publicized include Madoff and Petters.

The fact that no FoF has yet to engage in fraud does not, in any way excuse them from having invested their clients’

assets in hedge fund frauds such as Madoff, Petters, or Westridge. Frequently (but not always), fraud is detectable, in

advance (as it was with Madoff, Petters, and Westridge), by determining what the hedge fund does, why the market

imperfection they claim to exploit exists, what they do to both identify and harvest the market mispricing, and by

confirming the existence and vitality of each relationship and position that the hedge fund claims to be present.

MEANINGFUL MISTAKES, LESSER SINS - MISTAKES 10. & 11.

After traveling through the nine rings of Hell (mistakes 9. through 1.), Dante progressed to Purgatory on his continuing

journey of understanding and enlightenment. He next traversed the two final and lesser sins located on the outer

periphery of Purgatory. Purgatorio, unlike Inferno, allows for the redemption from one’s mistakes. For this reason, I

have segmented out two final missteps to which FoF are most susceptible to, i.e., Termination and Rigidity.

10. Termination - Failure to develop adequate & appropriate basis for decision to fire an existing hedge fund. The

mistake that some FoF make is to terminate their underlying hedge fund managers without an adequate basis for their

“Termination” decisions. This mistake closely parallels the 6th

path-to-failure (see above), i.e., that of hiring a hedge

fund without adequate basis. However, the damage done by firing a manager without an adequate basis for the

decision is generally, significantly less onerous than the damage that is frequently wrought by the hiring of a hedge

fund without adequate basis.

By way of an example, perhaps a FoF has been investing with a long/short equity sector hedge fund dedicated to the

micro-, small-, and mid-cap equities of US-based banks. Hypothetically, this hedge fund delivered double-digit

negative returns in 2007 and 2008 and as a result the FoF terminated their relationship with this hedge fund manager.

Then, the return to normalcy of 2009 unfolded, and this long/short bank-sector specialist delivered a +39% return and

is expected to continue to deliver double-digit returns for the next couple of years as the US bank sector heals and

fundamental relative valuations (both negative and positive) are logically rewarded.

This example of the termination of a hedge fund without having first developed an adequate and appropriate basis for

the decision, results in the sacrifice of future alpha. However, to the extent that new hedge funds are hired on the

basis of sound, forward-looking analysis, the extent of the damage may be significantly reduced. Nevertheless, it’s

much preferred to retain an existing value-added hedge fund than it is to identify and hire a new replacement

manager.

11. Rigidity - Failure to adapt one’s thinking and solutions to the ever-changing environment. The mistake that

some FoF make is to rigidly maintain the same perspectives that they first established a dozen years earlier. This

mistake will inevitably erode the foundational vitality of a FoF, but at the same time, it is the most forgiving and

recoverable of the paths-to-failure.

Market inefficiencies and associated market failures evolve at a remarkably rapid pace and to an unusual degree. This

is as a result of the evolutionary pace of individual: (i) macro economies, (ii) capital markets, (iii) investment vehicles,

instruments, and securities, (iv) information sources, and (v) regulatory constraints. The rapid pace and diversity of

evolution serves as a primary reason for the fundamental existence of hedge funds. Hedge funds are present, in part,

because they provide a structure that adapts more quickly and to a greater extent to the evolving capital market

environment than any other investment management structure.

Andrew Lo of Massachusetts Institute of Technology comments6: “Hedge funds are the Galapagos Islands of finance.

The rate of innovation, evolution, competition, adaptation, births and deaths, the whole range of evolutionary

phenomena, occurs at an extraordinary rapid clip.” In 2006, for example, 1,518 new hedge funds were launched, but

717 folded; academic studies suggest that almost half of hedge funds fail to last five years7.

FoF parallel underlying hedge funds in their need to evolve at a rapid pace or else become victim to extinction. Events

of the last several years provide a ready example. By the end of 2006, fixed income markets had become unusually

efficient, offering little in the way of alpha opportunities. As a result, many FoF concentrated their portfolios on

long/short equity hedge funds (sometimes exclusively). But, by January 2009, the broadly defined fixed income arena

had experienced a degree of market failure and disassembly not witnessed since the 1930s. The tide turned, and fixed

income now offered many times the alpha opportunities then available in long/short equity. Those FoF who failed to

evolve during this time were placed at a meaningful competitive disadvantage to their more flexible and adaptive

brethren.

V. SUCCESS IS EASY - AVOID FAILURE AND YOU WILL WIN

This paper set forth the proposition that the design, construction, and ongoing management of a successful FoF, in

both the short- and the long-run, is a relatively easy task. The ready ease of this task is a direct function of the vast

opportunity set available for the harvesting of alpha – in size, with consistency, and with durability. Nevertheless, FoF

have frequently failed in their mission. I argue that these failings are in the Ellis, Winning the Loser’s Game, sense --

not the result of any lack of opportunity, but instead are the result of making one or more of eleven specific mistakes

along the way.

As Ellis observes, investing is an activity in which the victor often prevails because he makes fewer mistakes than his

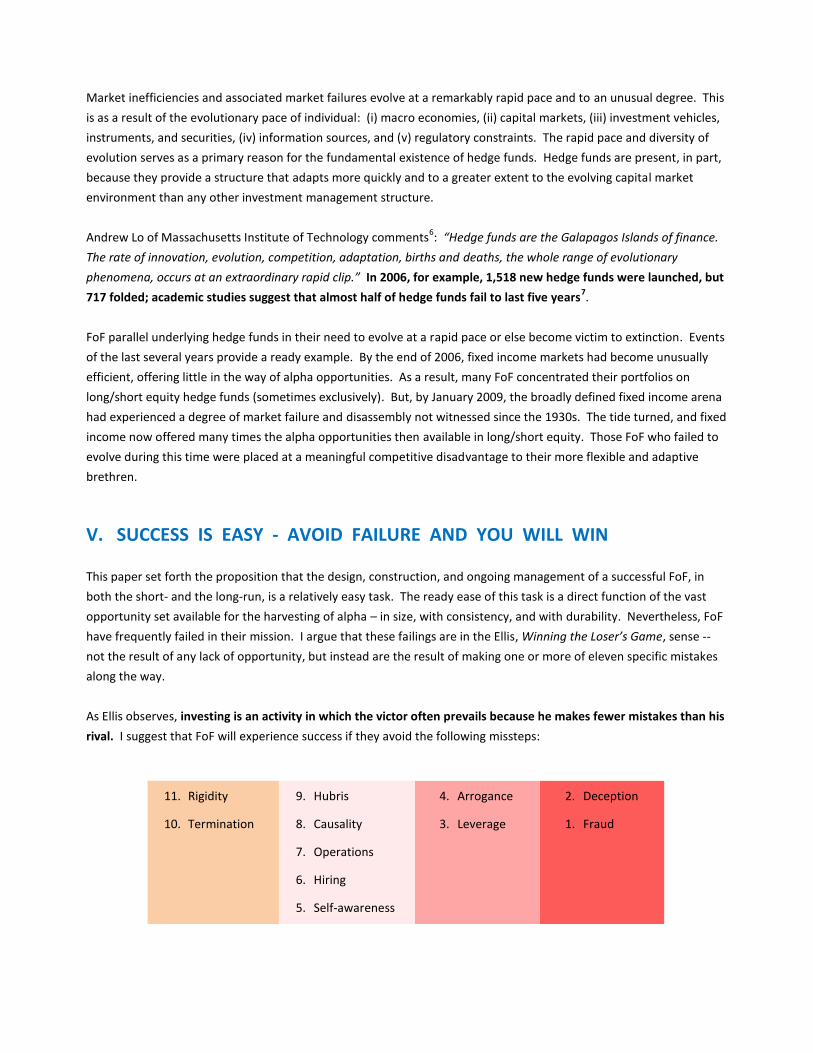

rival. I suggest that FoF will experience success if they avoid the following missteps:

11. Rigidity 9. Hubris 4. Arrogance 2. Deception

10. Termination 8. Causality 3. Leverage 1. Fraud

7. Operations

6. Hiring

5. Self-awareness

The last several years have provided numerous examples of FoF failures. In each case, the reasons for their collapse

can be directly traced back to one or more of these eleven paths-to-failure.

Some investors have reacted to recent FoF and hedge fund collapses with poorly developed thinking that fails to tie

their proposed solution with the root cause of the original mistake. Consider two examples:

1. Some have suggested that the solution for fraud and illiquidity is to abandon limited partnerships and instead

use only separate accounts. This of course is a flawed line of reasoning – as we all recall, Bernie Madoff’s

clients all had separate accounts. And if one’s separate account holds the same securities as every other

client of the specific hedge fund manager in question, then all investors are still left with the same liquidity

problem – only worse, for now no General Partner is present who could step in and control the behavior of

the crowd so as to better protect each individual interest, i.e., prevent the elephants from all attempting to

race through the door at the same moment.

2. Some have suggested that the solution for the problem of knowing your factor exposures is to install new

quantitative systems or models that will inform us as to our forward-looking risks. Those who suggest such

“solutions” are obviously unaware of how the vast teams of analysts and risk managers making use of

complex Value-at-Risk models failed to identify factor exposures at financial institutions around the world

during the 2008-2009 global economic collapse. The problem of identifying and parameterizing embedded

factor exposures is generally not one of insufficient data or analytics. Instead, it is more often a challenge of

properly evaluating and interpreting what is already present in abundance.

Finally, the framework presented by this paper was designed to provide a template for use by Trustee Boards at

pensions, foundations, and endowments that are responsible for the oversight of internal hedge fund programs. It is

also meant as a road map for the management of an internal hedge fund program as well for use by those who are

performing due diligence on and making selections of external FoF.

Victory is already yours – you have only to avoid eleven classic missteps.

Rob Brown, PhD, CFA

Chief Investment Officer, Senior Vice President

United Capital Financial Advisers, LLC

Email [email protected]

FOOTNOTES

1. “The Hedge Fund of Tomorrow: Building an Enduring Firm,” Thought Leadership Series, April 2009, CaseyQuirk, The Bank of New York Mellon, Pages 7 – 22.

2. “Winning the Loser’s Game: Timeless Strategies for Successful Investing,” Charles D. Ellis, McGraw-Hill, 4th edition (March 14, 2002).

3. “The Divine Comedy” (Italian: La Divina Commedia) is an epic poem written by Dante Alighieri between 1308 and his death in 1321 (sometimes referred to in colloquial American culture as “Dante’s Inferno”). It is widely considered to be the central poem of Italian literature, and is seen as one of the greatest works of world literature. It is divided into three parts, the Inferno, Purgatorio, and Paradiso. The poem is written in the first person, and tells of Dante’s journey through the three relative realms of the dead. The Roman poet Virgil guides Dante through nine rings of Hell and the nine circles of Purgatory. Hell is divided into three main regions: Upper Hell (the first five circles) for the self-indulgent sins; Circles six and seven for the violent sins; and Circles eight and nine for the malicious sins. Dante called his poem “Comedy” (the adjective “Divine” was added later in the 14th century due to the nature of the material addressed by this epic poem) because poems in the ancient world were classified as either High (“Tragedy”) or as Low (“Comedy”). Low poems had happy endings (as does Dante’s The Divine Comedy).

4. “Determinants of Portfolio Performance,” Gary P. Brinson, L. Randolph Hood, and Gilbert L. Beebower, The Financial Analysts Journal, July/August 1986.

5. “Determinants of Portfolio Performance II: An Update,” Gary P. Brinson, Brian D. Singer, and Gilbert L. Beebower, The Financial Analysts Journal, 47, 3 (1991).

6. “Capital Ideas Evolving,” Peter Bernstein, John Wiley & Sons, May 2007.

7. “Guide to Hedge Funds: What they are, what they do, their risks, their advantages,” Philip Coggan, The Economist, Bloomberg Press, 2008.

Related Documents