LCP ACCOUNTING FOR PENSIONS 2015 2015 sees yet more changes in the UK pensions landscape. With new reporting and governance requirements on the horizon, our 22nd annual survey looks at how FTSE 100 companies manage their pension risks.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LCP ACCOUNTING FOR PENSIONS 2015

2015 sees yet more changes in the UK pensions landscape. With new reporting and governance requirements on the horizon, our 22nd annual survey looks at how FTSE 100 companies manage their pension risks.

2

For further information please contact Bob Scott, Nick Bunch or the partner

who normally advises you.

This report may be reproduced in whole or in part, without permission,

provided prominent acknowledgement of the source is given. The report

is not intended to be an exhaustive analysis of IAS19. Although every

effort is made to ensure that the information in this report is accurate,

Lane Clark & Peacock LLP accepts no responsibility whatsoever for any

errors, or the actions of third parties. Information and conclusions are

based on what an informed reader may draw from each company’s

annual report and accounts. None of the companies have been contacted

to provide additional explanation or further details.

View a full list of our services at www.lcp.uk.com

© Lane Clark & Peacock LLP August 2015

We would like to thank those from LCP who have made this report possible:

Catriona Armstrong

Nick Bunch

Richard Chini

Emma Colpus

Jeremy Dell

Peter Fitchett

Linda Gilhooly

Tricia Gulliver

Sam Jenkins

Claire Jones

Geraint Jones

Andrew Keenan

Stuart Levy

Sarah Lossin

Dorothy Mendoza

Martin Mercer

Paul Meredith

Chris Mitcheson

Holly Moffat

David Poynton

Charlotte Quarmby

Robin Rangeley

Max Root

Bob Scott

Joanne Stewart

Laura Strachan

Sam Tomes

Alex Waite

Shaun Wood

Chris Wragg

22

LCP Accounting for Pensions 2015

p5 1. Executive Summary

p8 2. Analysis of FTSE 100 accounting disclosuresp10 2.1 Introduction

p10 2.2 The FTSE 100 accounting deficit

p14 2.3 How have companies been managing their

pension commitments?

p18 2.4 Analysis of pension disclosures

p36 Appendix 1 - FTSE 100 accounting disclosure listing

p40 Appendix 2 - FTSE 100 accounting risk measures

3

Although FTSE100 companies have reduced their overall pension contributions again, many still have big schemes with big deficits.

Bob ScottPARTNER, LCP

Welcome to our 22nd annual survey of FTSE 100 companies’ pension disclosures.

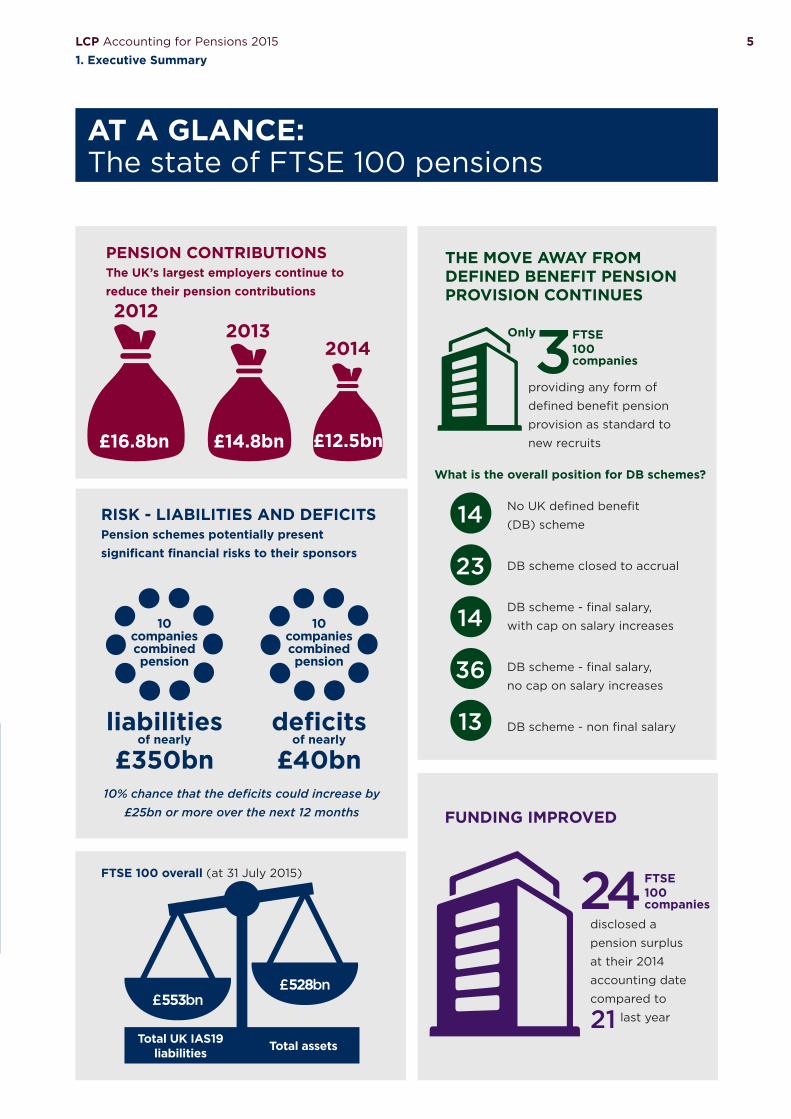

AT A GLANCE: The state of FTSE 100 pensions

THE MOVE AWAY FROM DEFINED BENEFIT PENSION PROVISION CONTINUES

PENSION CONTRIBUTIONS The UK’s largest employers continue to reduce their pension contributions

£12.5bn

20142013

£14.8bn

2012

£16.8bn

RISK - LIABILITIES AND DEFICITSPension schemes potentially present significant financial risks to their sponsors

10% chance that the deficits could increase by £25bn or more over the next 12 months

£553bn£528bn

liabilities of nearly

£350bn

10 companiescombined pension

deficits of nearly

£40bn

10 companiescombined pension

disclosed a

pension surplus

at their 2014

accounting date

compared to

21 last year

FUNDING IMPROVED

24 FTSE 100 companies

FTSE 100 companies

providing any form of

defined benefit pension

provision as standard to

new recruits

3 Only

What is the overall position for DB schemes?

No UK defined benefit

(DB) scheme

DB scheme closed to accrual

DB scheme - final salary,

with cap on salary increases

DB scheme - final salary,

no cap on salary increases

DB scheme - non final salary

14

23

14

36

13

Total UK IAS19 liabilities Total assets

FTSE 100 overall (at 31 July 2015)

5LCP Accounting for Pensions 2015

1. Executive Summary

6 LCP Accounting for Pensions 2015

1. Executive Summary

Contributions down again � The UK’s largest employers continue to reduce their pension

contributions. Total contributions to defined benefit schemes were

£12.5 billion in 2014, compared to £14.8 billion in 2013 and £16.8 billion in

2012.

Pensions: a potential risk for some � Yet those pension schemes potentially present significant financial risks

to their sponsors. Our research shows that:

– 10 companies had combined pension liabilities of nearly £350 billion;

– 10 companies had combined pension deficits of nearly £40 billion; and

– there is a 10% chance that those deficits could increase by at least a

further £25 billion over the next 12 months.

� From October, new reporting rules will require companies not only to

disclose their principal risks but to indicate which of those risks could

potentially stop them trading and then to identify the steps they have

taken to mitigate those risks.

Net deficit slightly lower � We estimate that the FTSE 100 as a whole had an overall (net) IAS19

deficit in respect of UK pensions of £25 billion at 31 July 2015, with total

IAS19 liabilities of £553 billion against assets of £528 billion.

A number of companies that paid large contributions in previous years have reverted to more "normal" levels.

7LCP Accounting for Pensions 2015

1. Executive Summary

Liabilities rise to record levels � Recent falls in corporate bond yields have caused reported liability

values to rise to record levels - for example, in its December 2014

accounts Royal Dutch Shell reported pension liabilities of more than

$100 billion and the accounting liabilities of BT Group’s main pension

scheme were over £50 billion at the end of March 2015.

Defined benefits - the end of the road � With almost all new FTSE 100 employees now being auto-enrolled into

defined contribution pension schemes, the move away from defined

benefit pension provision has continued. This will accelerate when

contracting out ceases in April 2016.

� Tesco currently provides new joiners with access to a career average

revalued earnings (CARE) scheme but has recently announced plans to

close this to new joiners and to future accrual, which would leave only

3 companies providing new employees with defined benefit pensions as

standard.

� A number of other FTSE 100 companies, including Anglo American

and Standard Life announced that they would be closing their defined

benefit schemes to existing members, leaving a dwindling number

of companies with an ever reducing number of employees accruing

additional pension on a defined benefit basis.

Exe

cuti

ve S

umm

ary

What steps are companies taking to address pension risk?Pension risk may well be one of the main risks for FTSE 100 companies with legacy

defined benefit pension schemes.

See pages 14 - 17

8

Contentp8 2. Analysis of FTSE 100 accounting disclosuresp10 2.1 Introductionp10 2.2 The FTSE 100 accounting deficitp14 2.3 How have companies been managing their pension commitments?p18 2.4 Analysis of pension disclosures

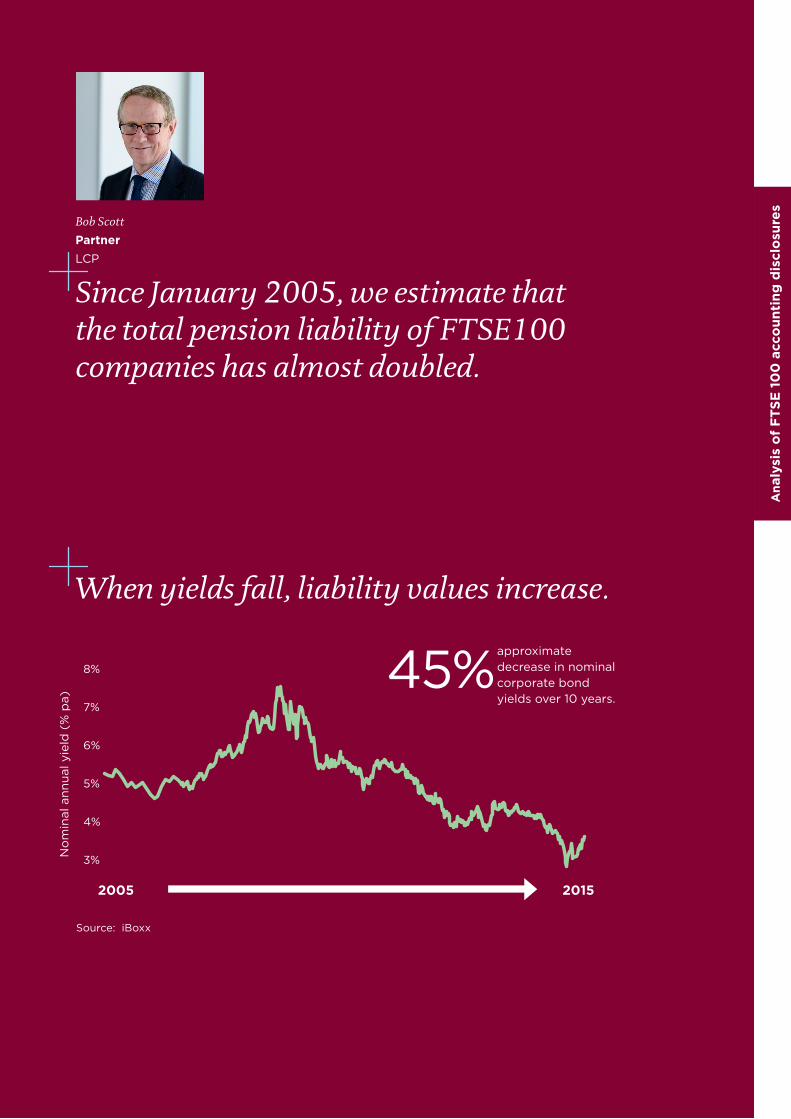

Since January 2005, we estimate that the total pension liability of FTSE100 companies has almost doubled.

Bob Scott

Partner LCP

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

When yields fall, liability values increase.

2%

3%

4%

5%

6%

7%

8%

December2004

December2005

December2006

December2007

December2008

December2009

December2010

December2011

December2012

December2013

December2014

No

min

al a

nnua

l yie

ld (

% p

a)

UK AA rated corporate bond yields

Source: iBoxx

2005 2015

Source: iBoxx

45%approximate decrease in nominal corporate bond yields over 10 years.

No

min

al a

nnua

l yie

ld (

% p

a)

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures10

2. Analysis of pension disclosures

2.1. IntroductionWe have analysed the defined benefit pension disclosures for 87

FTSE 100 companies reporting in 2014. 12 of the FTSE 100 have been

excluded as they do not sponsor a material defined benefit pension

scheme and Dixons Carphone has also been excluded as no post-merger

accounts are available for 2014. A full list and summary details of the

87 companies’ key pension disclosures are set out in appendix 1.

The information and conclusions of this report are based solely on detailed

analysis of the information that companies have disclosed in their annual

report and accounts and other publicly available information. We do

not approach companies or their advisers for additional information or

explanation.

We have concentrated on the financial position of the defined benefit

pension schemes in which the companies’ employees and former

employees participate. Some companies offer post-retirement healthcare,

which we have excluded from our analysis, where possible. Overseas

pension arrangements have been included, except where otherwise

indicated.

All of the companies analysed have reported under international

accounting standards (IAS19 for pension costs) as required under

EU regulations.

2.2. The FTSE 100 accounting deficitWe estimate that the combined FTSE 100 pension deficit in respect of

UK liabilities was £25 billion at the end of July 2015, reflecting total IAS19

liabilities of £553 billion against assets of £528 billion.

Since January 2005, we estimate that the total pension liability of

FTSE 100 companies has almost doubled. We have included a list of the

ten companies with the largest disclosed pension liabilities in appendix 2.

£25 billionThe estimated UK pension

deficit for FTSE 100

companies under IAS19.

11LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

Over the last 5 years the total deficit has fluctuated between £10bn and nearly £60bn.

A combination of strong investment returns, payment of deficit

contributions and low levels of inflation has offset the impact of significant

falls in bond yields, which have led to a material increase in reported

liability values.

Overall, the total deficit has reduced by £12 billion from the position at

30 June 2014. However, the change in deficit or surplus for a particular

company’s pension scheme depends heavily on its investment strategy

and, in particular, on the extent to which it has been hedged against

changes in long-term interest rates.

-70

-60

-50

-40

-30

-20

-10

0

10 Jun

2010

Dec

20

10

Jun

2011

Dec

20

11

Jun

2012

Dec

20

12

Jun

2013

Dec

20

13

Jun

2014

Dec

20

14

Jun

2015

£ b

illio

n

Estimated IAS19 position for UK schemes of FTSE 100 companies

The chart below shows how the accounting deficit has developed over

the past five years. Our figures include unfunded pension promises but

exclude, where possible, the overseas pension schemes sponsored by

FTSE 100 companies and any employee benefits other than pensions.

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures12

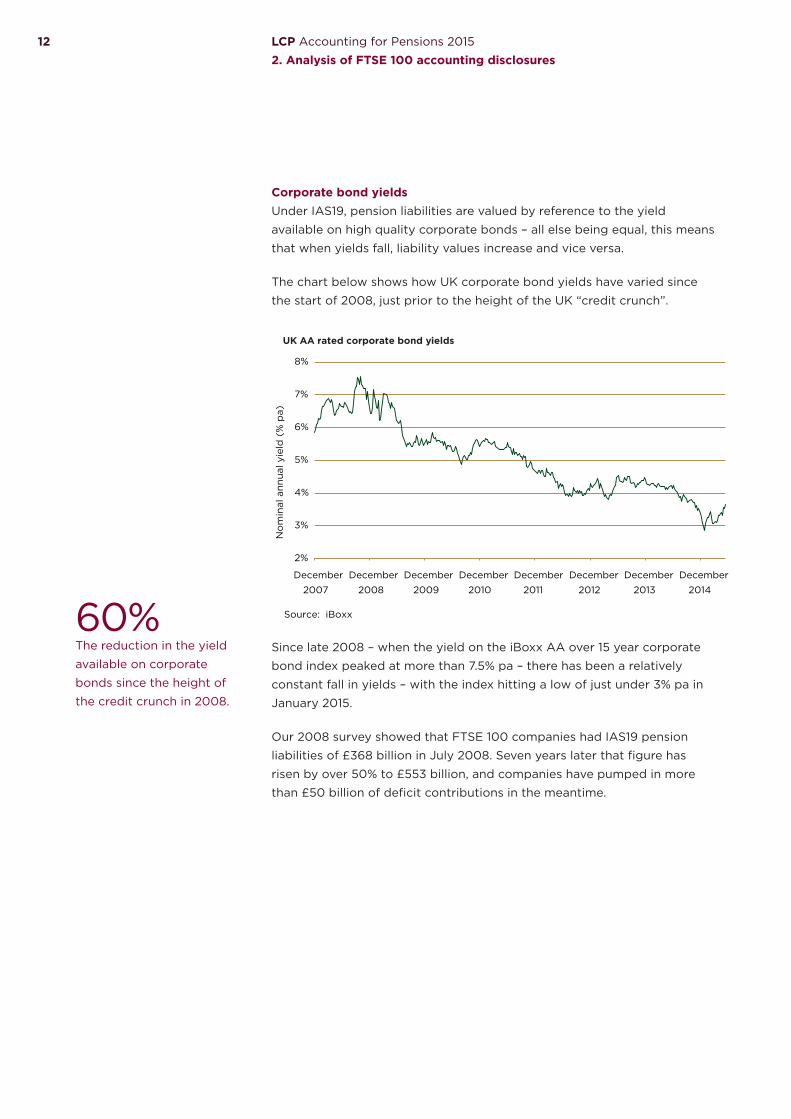

Corporate bond yieldsUnder IAS19, pension liabilities are valued by reference to the yield

available on high quality corporate bonds – all else being equal, this means

that when yields fall, liability values increase and vice versa.

The chart below shows how UK corporate bond yields have varied since

the start of 2008, just prior to the height of the UK “credit crunch”.

2%

3%

4%

5%

6%

7%

8%

December

2007

December

2008

December

2009

December

2010

December

2011

December

2012

December

2013

December

2014

No

min

al a

nnua

l yie

ld (

% p

a)

UK AA rated corporate bond yields

Source: iBoxx

Since late 2008 – when the yield on the iBoxx AA over 15 year corporate

bond index peaked at more than 7.5% pa – there has been a relatively

constant fall in yields – with the index hitting a low of just under 3% pa in

January 2015.

Our 2008 survey showed that FTSE 100 companies had IAS19 pension

liabilities of £368 billion in July 2008. Seven years later that figure has

risen by over 50% to £553 billion, and companies have pumped in more

than £50 billion of deficit contributions in the meantime.

60%The reduction in the yield

available on corporate

bonds since the height of

the credit crunch in 2008.

13LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

Pension risk – the viability statementThe increase in the size of reported liabilities illustrates the potentially

material level of pension risk being run by a number of FTSE 100

companies. Our research shows that:

� 10 companies reported combined pension liabilities of nearly

£350 billion;

� 10 companies reported combined pension deficits of nearly £40 billion;

and

� there is a 10% chance that those deficits could increase by at least a

further £25 billion over the next 12 months due to financial factors alone.

Under current accounting standards, companies are already required to

disclose details of the risks associated with their pension schemes in their

accounts. However, from October 2015, additional reporting requirements

will come into force under an updated version of the UK corporate

governance code.

This will require the directors of most listed companies to confirm that

they have carried out a robust assessment of the main risks facing their

business, including those that would threaten its solvency. Furthermore,

there is a new requirement to include a “viability statement” in the annual

accounts, confirming whether the directors expect the company will be

able to continue in operation, taking into account its current position and

principal risks.

Pension risk may well be one of the main risks for FTSE 100 companies

with legacy defined benefit pension schemes. The new requirement may

therefore increase the level of disclosure required in relation to this.

Based on the information in existing accounting disclosures,

BAE Systems, BT Group, International Airlines Group, Sainsbury’s and

RSA Insurance Group are companies that may be running significant levels

of pension risk relative to the size of their business.

Pension risk may well be one of the main risks for FTSE 100 companies with legacy defined benefit pension schemes.

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures14

2.3. How have companies been managing their pension commitments?

Reductions in defined benefit pension provisionNone of the FTSE 100 companies we have analysed provide traditional

final salary pensions to new employees and there are only 4 FTSE 100

companies providing any form of defined benefit pension provision

as standard to new recruits. These are Diageo, Johnson Matthey and

Morrisons, which provide cash balance schemes, and Tesco, which

provides a career average revalued earnings (“CARE”) scheme. In its 2015

accounts Tesco reported that it was in consultation to close this CARE

scheme to both new entrants and future accrual.

A number of other companies stated that they had either closed their

defined benefit pension scheme to future accrual during the last year, or

had plans to do so in the near future:

� Anglo American announced that its only remaining UK plan with

continuing accrual will close on 30 September 2015.

� Hammerson closed its pension scheme to accrual in July 2014 and as a

result disclosed a £3 million gain in its 2014 accounts.

� Morrisons reported that it was consulting on the closure of its 2 historic

CARE schemes to future accrual.

� Standard Life announced that it will close its pension plan to accrual

from April 2016, replacing it with an enhanced defined contribution

pension plan.

In addition, HSBC, Severn Trent and Weir Group have all previously

reported that they have reached agreement to close their pension

schemes to future accrual during 2015.

The move away from defined benefit pension provision continues apace.

15LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

With the move towards defined contribution pension provision firmly

established, other changes have been made in recent years that reduce

the employer cost of the remaining defined benefit pensions still being

built up. For example, in its March 2015 accounts, Babcock disclosed that it

had capped pensionable salaries and increased employee contributions to

one of its three main pension schemes, with similar changes expected to

come into effect in its other two main schemes from June 2015.

The chart below shows the numbers of companies providing continuing

defined benefit pension provision, after allowing for the changes listed

above. These changes will leave only 36 FTSE 100 companies providing

traditional final salary pensions to any of their employees.

No UK defined benefit (DB) scheme14

23

14

36

13

DB scheme closed to accrual

DB scheme - final salary, with cap on salary increases

DB scheme - final salary, no cap on salary increases

DB scheme - non final salary

With the ability to contract out of the state pension system coming to

an end in April 2016, we are likely to see an acceleration in the number

of companies closing their pension schemes to future accrual, in order

to mitigate the increase in national insurance cost that arises when the

current rebate most receive disappears.

36FTSE 100 companies

providing traditional final

salary pension accrual to

any employees.

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures16

Liability management exercisesMany companies are naturally now placing increased focus on managing

their legacy pension arrangements and removing risk from their balance

sheet. One popular way of achieving this is to carry out a pension increase

exchange (“PIE”) exercise, where members of the pension scheme are

given the option to exchange some or all of the future increases on

their pension in return for a higher current level of pension. This reduces

inflation risk and can result in a cost saving, if members accept a deal

which is less than fair value.

Several FTSE 100 companies carried out liability management exercises

during 2014:

� BAE Systems reported that it carried out a PIE exercise in its main

scheme in May 2014, with 38% of pensioners opting to exchange future

increases on part of their pensions for higher non-increasing pensions.

� Centrica offered pensioners the option to receive a higher pension in

return for giving up certain future increases linked to RPI, which gave

rise to a past service credit of £10 million.

� GKN reported that it had commenced a PIE exercise to mitigate inflation

risk, which would conclude in early 2015.

� Taylor Wimpey has completed a flexible retirement offer for deferred

members, which allowed participants to realise part of their pension at

an earlier date than previously anticipated. This has resulted in

£25 million of pension liability being transferred out of its pension

schemes.

� On the back of a PIE exercise for pensioners which resulted in a 28%

take up rate, TUI Travel has introduced pension increase exchange as a

standard retirement option for active and deferred members, with a

£28 million past service credit arising on the basis of expected future

take up rates.

Liability management exercises can be a “win-win” for companies and members.

17LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

Pension freedoms and flexibilitiesIt is too early for companies to have reported in their accounts on the

impact of the 2014 budget changes. However, since April 2015, defined

contribution schemes have become more attractive as individuals can

access their pension savings with much greater flexibility than previously.

This gives rise to opportunities for companies to manage their defined

benefit liabilities by giving members the opportunity to access those

flexibilities. This could be via partial transfer values at retirement; full

commutation of smaller pensions; or simply by offering to pay for members

to take financial advice on their options.

De-risking of investment strategiesAs pension schemes mature and the time horizon for payment of benefits

decreases, companies and pension scheme trustees have typically looked

to reduce the investment risks posed by the pension scheme.

This is of increasing importance as schemes close to future accrual and

ongoing contributions reduce because pensions and other benefits then

need to be paid out of investment income or by realising assets.

With increasingly complex investment strategies – some of which are not

fully explained in accounting disclosures – it has become more difficult to

split FTSE 100 pension scheme assets into bonds and equities. However,

the general trend away from equities does appear to have continued with a

modest movement of assets out of equities and into bonds and other asset

classes during 2014. This is illustrated in the chart below.

Equities

Bonds

Other

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

0%

20%

40%

60%

80%

100%

30%The average allocation of

FTSE 100 pension scheme

assets to equities.

Overall asset allocation for FTSE 100 companies with December year-ends

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures18

2.4. Analysis of pension disclosuresThe average pensions note runs to just over five pages, with most

companies also having several paragraphs of pension commentary in the

main body of their reports. The longest disclosure was produced by BP,

which covered 10 pages of its 2014 report.

Funding levelsIAS19 takes a snapshot of the accounting surplus or deficit at the

company’s year-end and in most cases this is the number that appears on

the balance sheet.

However, in some cases, complex rules under IAS19 can result in a

restriction on the asset recognised on the balance sheet where a pension

scheme is in surplus, or a higher liability being recognised as a result of

the funding agreements in place with the pension scheme trustees. 18

companies were affected by this issue in 2014 and in some cases the

amounts involved were material – for example, Scottish & Southern Energy and Standard Life added £201 million and £414 million to their

balance sheets respectively.

Recently proposed changes to the IAS19 accounting standard may mean

that these adjustments are more common in future. However, the impact

will depend on the precise wording of each company’s pension scheme

rules.

Of the 87 FTSE 100 companies we analysed, 24 disclosed pension assets

equal to or in excess of accounting liabilities, which compares to 21 of

these companies last year. This general improvement was despite the large

fall in corporate bond yields, and arose due to strong investment returns

over 2014 for schemes that had significant levels of hedging against falls

in interest rates, either through investment in government and corporate

bonds, or as a result of holding interest rate swaps.

Royal Mail disclosed the highest 2014 funding level – 183% as at

31 March 2014. 38 companies reported being less than 90% funded on an

accounting basis at their 2014 year-end. This is the same number as in

2013.

24FTSE 100 companies

disclosed a pension surplus at

their 2014 accounting date.

19LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

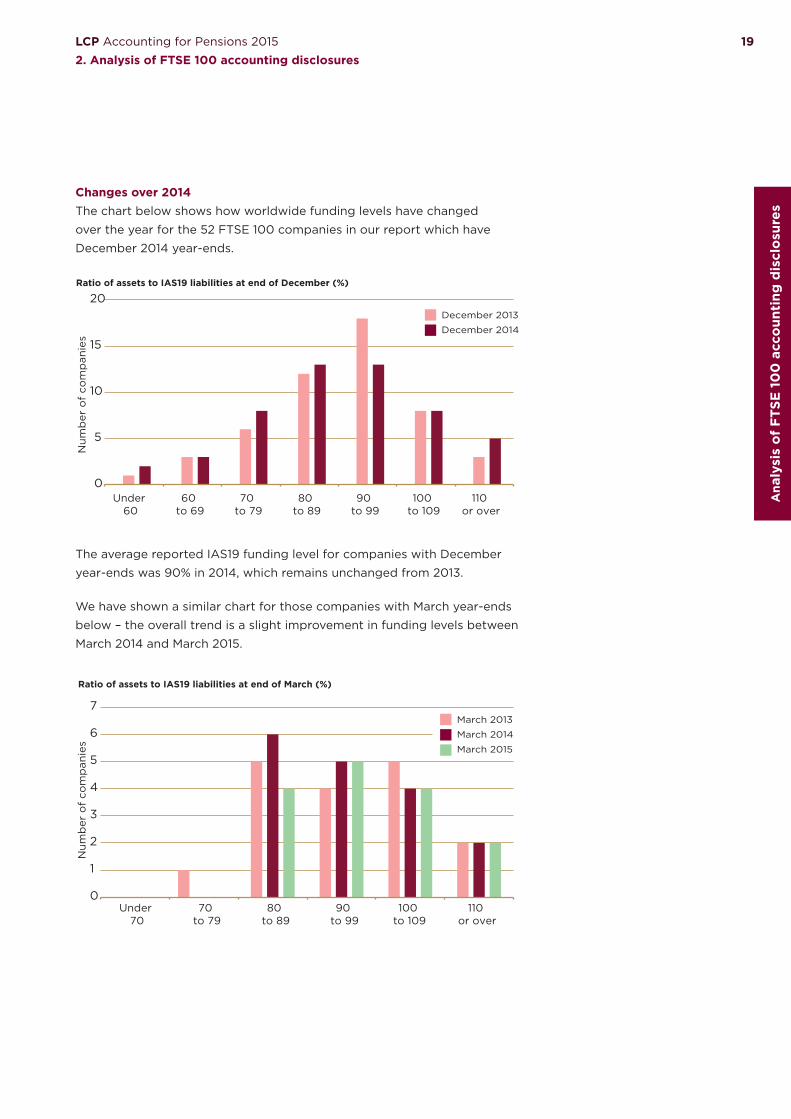

Changes over 2014The chart below shows how worldwide funding levels have changed

over the year for the 52 FTSE 100 companies in our report which have

December 2014 year-ends.

Ratio of assets to IAS19 liabilities at end of December (%)

December 2013

December 2014

0

5

10

15

20

Under 60

60 to 69

70 to 79

80 to 89

90 to 99

100 to 109

110 or over

Num

ber

of

com

pan

ies

The average reported IAS19 funding level for companies with December

year-ends was 90% in 2014, which remains unchanged from 2013.

We have shown a similar chart for those companies with March year-ends

below – the overall trend is a slight improvement in funding levels between

March 2014 and March 2015.

March 2013

March 2014

March 2015

Ratio of assets to IAS19 liabilities at end of March (%)

0

1

2

3

4

5

6

7

Under 70

70 to 79

80 to 89

90 to 99

100 to 109

110 or over

Num

ber

of

com

pan

ies

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures20

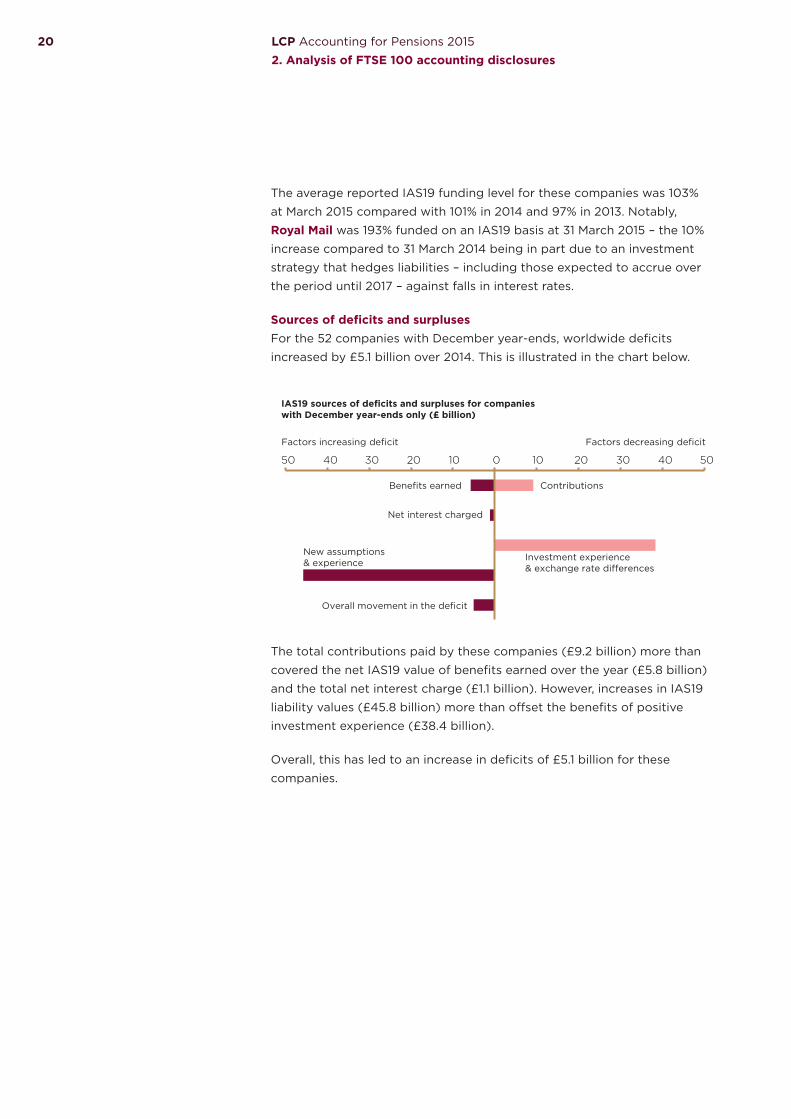

The average reported IAS19 funding level for these companies was 103%

at March 2015 compared with 101% in 2014 and 97% in 2013. Notably,

Royal Mail was 193% funded on an IAS19 basis at 31 March 2015 – the 10%

increase compared to 31 March 2014 being in part due to an investment

strategy that hedges liabilities – including those expected to accrue over

the period until 2017 – against falls in interest rates.

Sources of deficits and surplusesFor the 52 companies with December year-ends, worldwide deficits

increased by £5.1 billion over 2014. This is illustrated in the chart below.

IAS19 sources of deficits and surpluses for companies with December year-ends only (£ billion)

Benefits earned

Net interest charged

Investment experience & exchange rate dierences

New assumptions & experience

Overall movement in the deficit

50 40 30 20 10 0 10 20 30 40 50

Factors increasing deficit Factors decreasing deficit

Contributions

The total contributions paid by these companies (£9.2 billion) more than

covered the net IAS19 value of benefits earned over the year (£5.8 billion)

and the total net interest charge (£1.1 billion). However, increases in IAS19

liability values (£45.8 billion) more than offset the benefits of positive

investment experience (£38.4 billion).

Overall, this has led to an increase in deficits of £5.1 billion for these

companies.

21LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

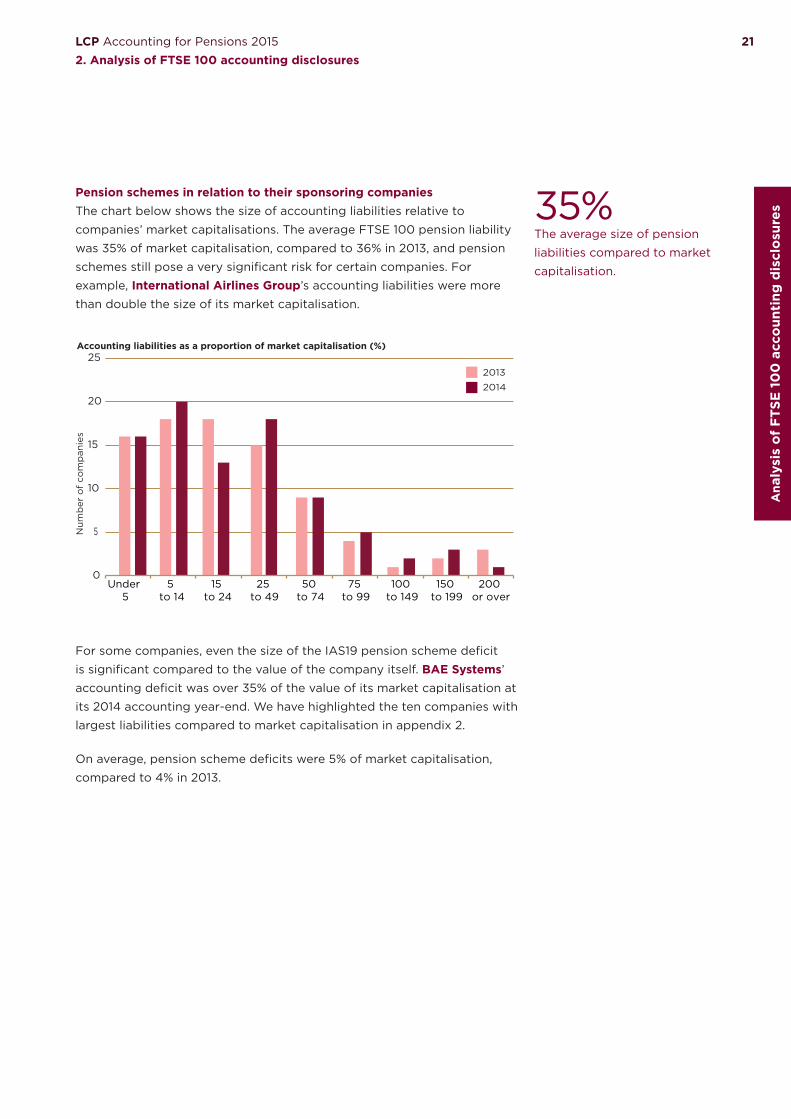

Pension schemes in relation to their sponsoring companiesThe chart below shows the size of accounting liabilities relative to

companies’ market capitalisations. The average FTSE 100 pension liability

was 35% of market capitalisation, compared to 36% in 2013, and pension

schemes still pose a very significant risk for certain companies. For

example, International Airlines Group’s accounting liabilities were more

than double the size of its market capitalisation.

Accounting liabilities as a proportion of market capitalisation (%)

0

5

10

15

20

25

Under 5

5 to 14

15 to 24

25 to 49

50 to 74

75 to 99

100 to 149

150 to 199

200 or over

Num

ber

of

com

pan

ies

2013

2014

For some companies, even the size of the IAS19 pension scheme deficit

is significant compared to the value of the company itself. BAE Systems’

accounting deficit was over 35% of the value of its market capitalisation at

its 2014 accounting year-end. We have highlighted the ten companies with

largest liabilities compared to market capitalisation in appendix 2.

On average, pension scheme deficits were 5% of market capitalisation,

compared to 4% in 2013.

35%The average size of pension

liabilities compared to market

capitalisation.

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures22

Pension scheme contributionsFTSE 100 companies paid contributions totalling £12.5 billion into their

defined benefit pension schemes in 2014 of which we estimate just over

half – £7.1 billion – went towards the cost of additional benefit accrual for

current employees.

Whilst this is a significant amount to have been paid, it is a noticeable

reduction from the £14.8 billion of contributions paid in 2013, £16.8 billion

paid in 2012 and £16.9 billion paid in 2011. The fall mainly reflects large

one-off contributions made by a small number of companies to their

pension schemes in previous years. For example, Diageo made a one-off

contribution to its UK pension plan of £400 million in 2013 which was

not repeated in 2014 and the 2012 figures include a £2 billion special

contribution made by BT Group.

The chart below shows how company payments, including those to

defined contribution pension schemes, have changed since 2007.

Employer contributions to pension schemes

Deficit contributions (DB schemes)

Employer service cost (DB schemes)

Employer DC costs

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014

£ b

illio

n

£2.3 bnThe reduction in employer

contributions to defined

benefit pension schemes

this year.

23LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

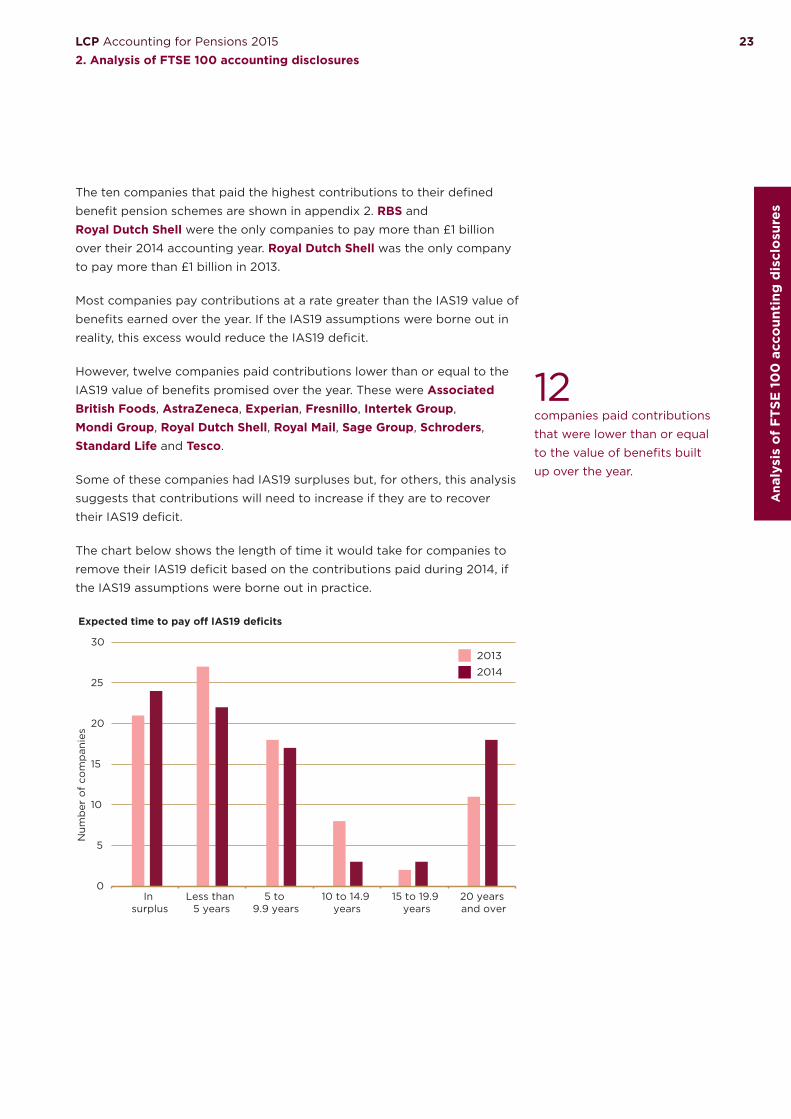

The ten companies that paid the highest contributions to their defined

benefit pension schemes are shown in appendix 2. RBS and

Royal Dutch Shell were the only companies to pay more than £1 billion

over their 2014 accounting year. Royal Dutch Shell was the only company

to pay more than £1 billion in 2013.

Most companies pay contributions at a rate greater than the IAS19 value of

benefits earned over the year. If the IAS19 assumptions were borne out in

reality, this excess would reduce the IAS19 deficit.

However, twelve companies paid contributions lower than or equal to the

IAS19 value of benefits promised over the year. These were Associated British Foods, AstraZeneca, Experian, Fresnillo, Intertek Group, Mondi Group, Royal Dutch Shell, Royal Mail, Sage Group, Schroders, Standard Life and Tesco.

Some of these companies had IAS19 surpluses but, for others, this analysis

suggests that contributions will need to increase if they are to recover

their IAS19 deficit.

The chart below shows the length of time it would take for companies to

remove their IAS19 deficit based on the contributions paid during 2014, if

the IAS19 assumptions were borne out in practice.

Expected time to pay o� IAS19 deficits

2013

2014

0

5

10

15

20

25

30

In surplus

Less than 5 years

5 to 9.9 years

10 to 14.9 years

15 to 19.9 years

20 years and over

Num

ber

of

com

pan

ies

12companies paid contributions

that were lower than or equal

to the value of benefits built

up over the year.

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures24

Pension schemes versus shareholdersThe chart below shows how dividends paid compare to pension deficits.

Of the 63 FTSE 100 companies that disclosed a pension deficit in 2014,

23 disclosed a deficit that was greater than or equal to the dividends paid

to their shareholders in 2014. However, in 25 cases, the 2014 dividend was

more than double the deficit at the 2014 financial year-end, suggesting

that these companies could pay off their pension scheme deficit relatively

easily if they wanted to.

Percentage of deficit that could be paid o� with one year's declared dividends (%)

0

5

10

15

20

Under 50

50 to 99

100 to 149

150 to 199

200 to 249

250 to 299

300 to 349

350 to 399

400 or over

Num

ber

of

com

pan

ies

2014

2013

The chart below shows the company contributions paid over companies’

2014 and 2013 accounting years as a percentage of dividends distributed

over these periods and therefore illustrates the amount of cash paid to

pension schemes in preference to shareholders. In 2014, seven companies,

including Lloyds Banking Group and RBS, paid at least as much in pension

contributions as they distributed in dividends during their accounting year.

Contributions paid as a proportion of dividends paid (%)

0

5

10

15

20

25

30

35

40

Under 10

10 to 19

20 to 29

30 to 39

40 to 49

50 to 59

60 to 69

70 to 79

80 to 89

90 to 99

100 or over

Num

ber

of

com

pan

ies

2014

2013

7companies paid at least as

much in pension contributions

as they distributed in dividends.

25LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

Key assumptionsWe consider below the various assumptions used to place an IAS19 value

on pension benefits. Where a company operates pension schemes in more

than one country, we have considered the assumptions used for the UK if

separately given. Where a company has disclosed a range of assumptions,

we have taken the mid-point.

Life expectancyUnder the IAS19 standard, companies are required to disclose any

“significant actuarial assumptions”, and we would generally expect

this to include mortality. 78 of 87 companies have provided sufficient

information in their 2014 accounts for us to derive basic mortality statistics

– specifically a male life expectancy at age 65 in the UK. This compares

to 74 out of 89 in 2013. Of the remaining 9, eight provided either non-UK

life expectancies, a range of life expectancies, or a narrative description of

their mortality assumptions. Coca Cola HBC was the only company that

did not disclose any information about the mortality assumption used.

The following charts show the range of life expectancies assumed under

IAS19 by FTSE 100 companies for males aged 65 on the balance sheet

date.

Life expectancy assumptions reported in 2014UK males aged 65 on the accounting date

2013

2014

0

5

10

15

20

25

30

35

85.9 or less 86 to 86.9 87 to 87.9 88 to 88.9 89 to 89.9 90 or above

Num

ber

of

com

pan

ies

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures26

The average assumed life expectancy was 88.0 years – up from 87.9 years

in the same companies’ 2013 accounts.

The average life expectancy disclosed by companies in their 2008

accounts was just 86.5 years so the average has increased by 1.5 years in

the past 6 years – or by 3 months every year.

However, last year we noted that the rate of increase in assumed life

expectancy appeared to be slowing and this trend has continued in 2014.

Although 46 companies disclosed higher life expectancy assumptions

in 2014, adding 0.4 years on average, 12 companies disclosed lower life

expectancy assumptions for some or all of their membership. For example,

Standard Life reduced its average disclosed life expectancy for a 60

year old male by 2 years, from 91 to 89 in 2014, whilst Capita reduced its

average assumed life expectancy for a 65 year old male in its main pension

scheme by 1.3 years, from 89.1 to 87.8 in 2014.

Land Securities assumed the longest life expectancy, stating in its 2014

accounts that male pensioners currently aged 60 will live on average to

age 91.1.

Research has shown that two of the main factors influencing life

expectancies are socio-economic group and income. In this respect it is

interesting to analyse the FTSE 100 companies’ assumed life expectancies

by the sector in which the company operates.

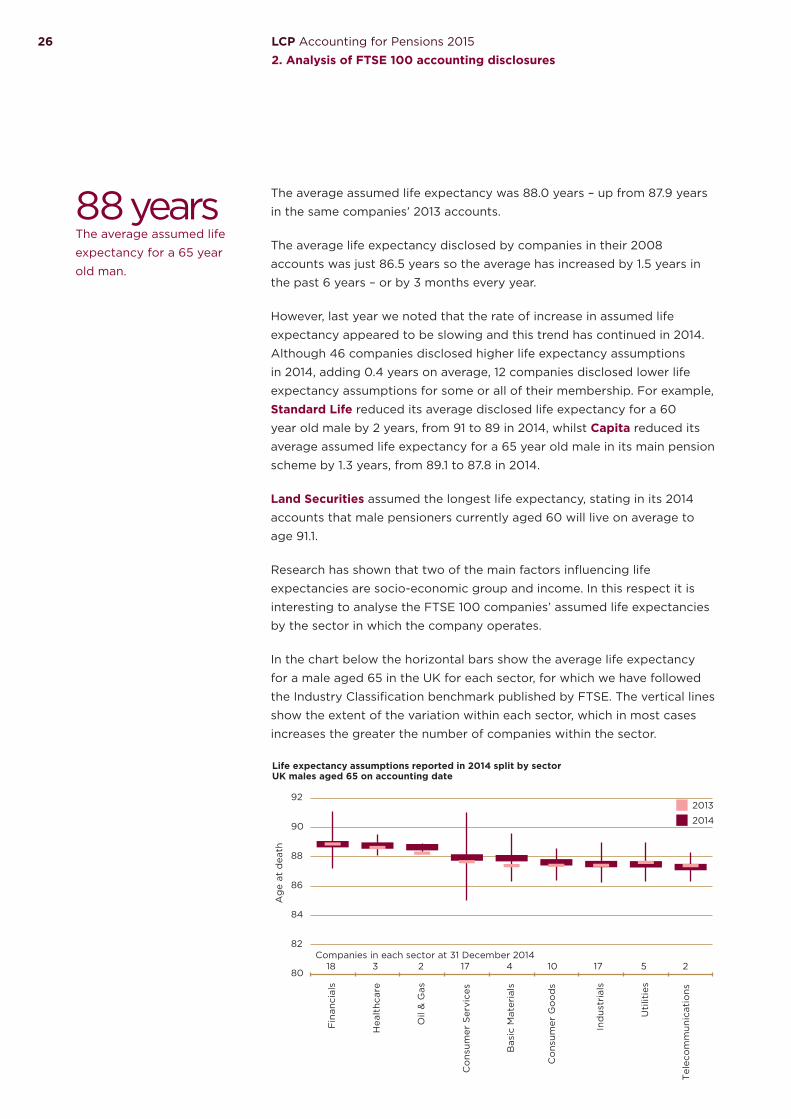

In the chart below the horizontal bars show the average life expectancy

for a male aged 65 in the UK for each sector, for which we have followed

the Industry Classification benchmark published by FTSE. The vertical lines

show the extent of the variation within each sector, which in most cases

increases the greater the number of companies within the sector.

Life expectancy assumptions reported in 2014 split by sectorUK males aged 65 on accounting date

2014

2013

80

82

84

86

88

90

92

Fin

anci

als

Hea

lthc

are

Oil

& G

as

Co

nsum

er S

ervi

ces

Bas

ic M

ater

ials

Co

nsum

er G

oo

ds

Ind

ustr

ials

Uti

litie

s

Tel

eco

mm

unic

atio

ns

Ag

e at

dea

th

18 23 17 2104 17Companies in each sector at 31 December 2014

5

88 yearsThe average assumed life

expectancy for a 65 year

old man.

27LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

This chart shows that the highest average assumed life expectancies are

found in the financials and healthcare sectors, as last year. The lowest

average assumed life expectancy is found in the telecommunications

sector.

The biggest change was in the basic materials sector, where the average

assumed life expectancy increased from 87.4 to 87.9.

Future improvements in mortalityAs well as setting assumptions to estimate how long current pensioners

will live on average, companies must also decide how life expectancies for

future pensioners will change as a result of improvements in mortality. The

allowance for future improvements can have a significant impact on the

IAS19 value of pension scheme liabilities, and hence deficits.

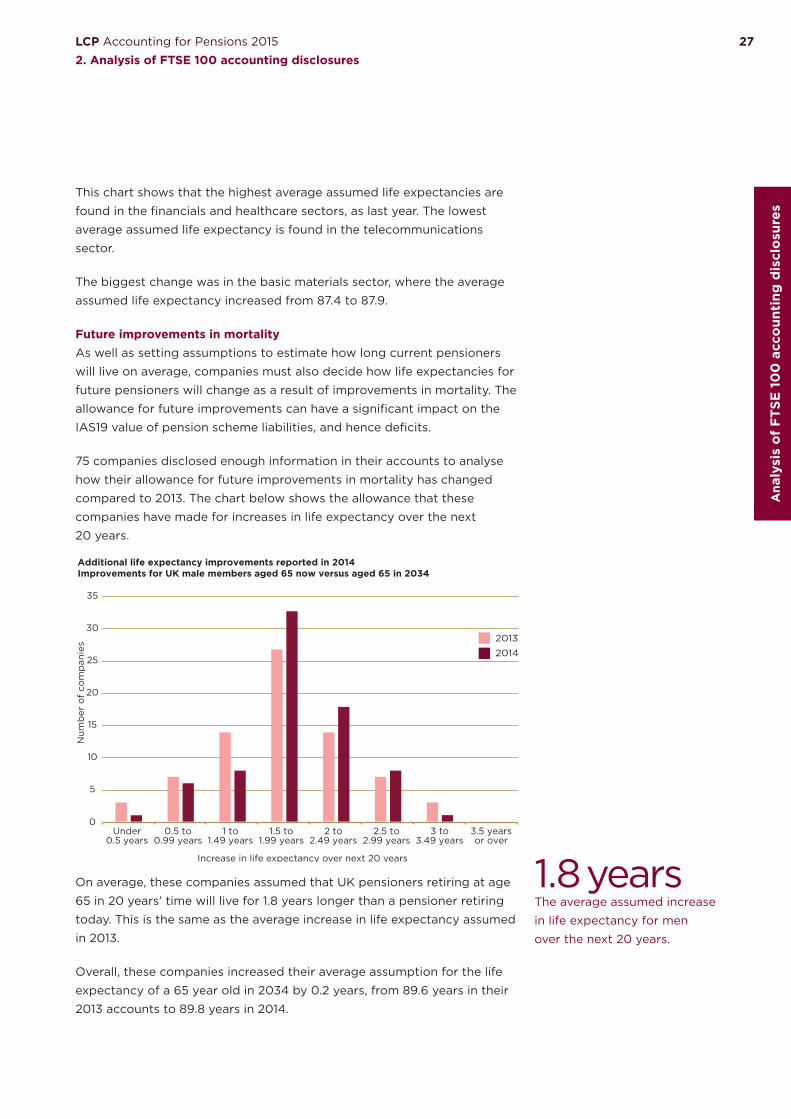

75 companies disclosed enough information in their accounts to analyse

how their allowance for future improvements in mortality has changed

compared to 2013. The chart below shows the allowance that these

companies have made for increases in life expectancy over the next

20 years.

0

5

10

15

20

25

30

35

Num

ber

of

com

pan

ies

Additional life expectancy improvements reported in 2014Improvements for UK male members aged 65 now versus aged 65 in 2034

Increase in life expectancy over next 20 years

Under0.5 years

0.5 to0.99 years

1 to1.49 years

1.5 to1.99 years

2 to2.49 years

2.5 to2.99 years

3 to3.49 years

3.5 yearsor over

2013

2014

On average, these companies assumed that UK pensioners retiring at age

65 in 20 years’ time will live for 1.8 years longer than a pensioner retiring

today. This is the same as the average increase in life expectancy assumed

in 2013.

Overall, these companies increased their average assumption for the life

expectancy of a 65 year old in 2034 by 0.2 years, from 89.6 years in their

2013 accounts to 89.8 years in 2014.

1.8 yearsThe average assumed increase

in life expectancy for men

over the next 20 years.

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures28

Discount rates and inflationThe discount rate is used to calculate a present value of the projected

pension benefits. A lower discount rate means a higher IAS19 value of

pension liabilities and vice versa.

The typical FTSE 100 company has pension liabilities that are linked to

price inflation. A decrease in the price inflation assumption will lead to a

lower level of projected benefit payments, and hence a lower IAS19 value

being placed on those benefits, all other things being equal.

We have analysed the discount rates used by 45 companies and the RPI

inflation assumption of 40 companies with a December year-end, together

with the assumption for CPI inflation disclosed by 18 of these companies.

Similarly, we have analysed the discount rates used by 13 companies and

the RPI inflation assumption of 12 companies with a March 2015 year-end,

together with the assumption for CPI inflation disclosed by 7 of these

companies. The results are summarised in the charts below.

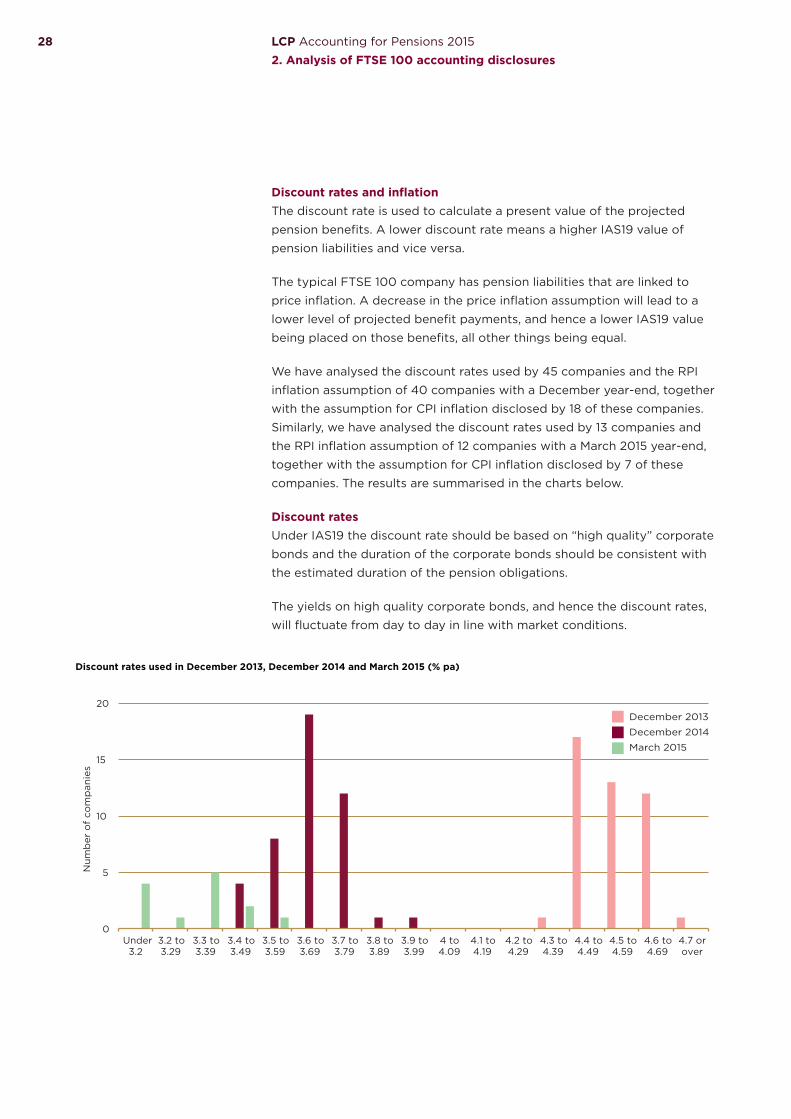

Discount ratesUnder IAS19 the discount rate should be based on “high quality” corporate

bonds and the duration of the corporate bonds should be consistent with

the estimated duration of the pension obligations.

The yields on high quality corporate bonds, and hence the discount rates,

will fluctuate from day to day in line with market conditions.

December 2013

December 2014

March 2015

Discount rates used in December 2013, December 2014 and March 2015 (% pa)

0

5

10

15

20

Under3.2

3.2 to3.29

3.3 to3.39

3.4 to3.49

3.5 to3.59

3.6 to3.69

3.7 to3.79

3.8 to3.89

3.9 to3.99

4 to4.09

4.1 to4.19

4.2 to4.29

4.3 to4.39

4.4 to4.49

4.5 to4.59

4.6 to4.69

4.7 orover

Num

ber

of

com

pan

ies

29LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

The average discount rate decreased significantly over the year to

December 2014, from 4.5% pa in December 2013 to 3.6% pa in

December 2014. The average discount rate used by FTSE 100 companies

with a March 2015 year-end was even lower at 3.3% pa. The spread of

discount rates used by FTSE 100 companies with a December 2014

year-end has increased compared to December 2013, with a 0.5% spread

of rates compared to a 0.35% spread last year. Centrica disclosed the

highest discount rate for a FTSE 100 company with a December year-end

in their 2014 accounts (3.9% pa in 2014 compared to 4.6% pa in 2013).

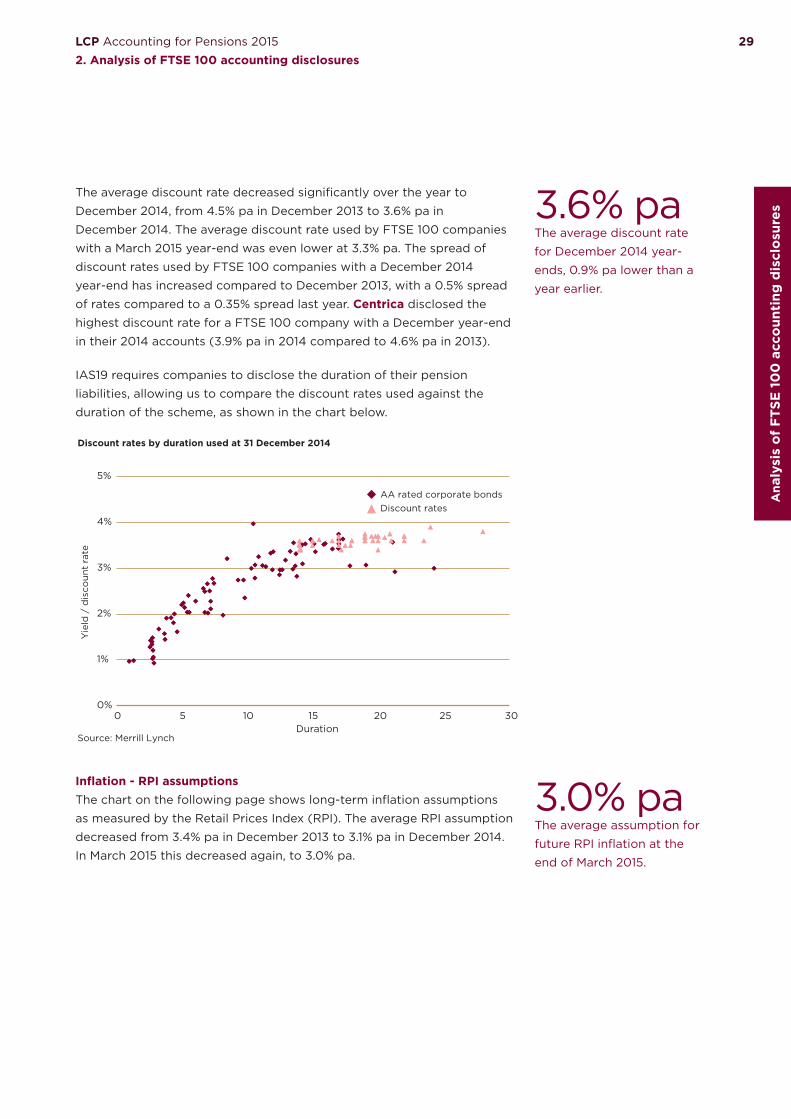

IAS19 requires companies to disclose the duration of their pension

liabilities, allowing us to compare the discount rates used against the

duration of the scheme, as shown in the chart below.

AA rated corporate bondsDiscount rates

Discount rates by duration used at 31 December 2014

Source: Merrill Lynch

0%

1%

2%

3%

4%

5%

0 5 10 15 20 25 30

Yie

ld /

dis

coun

t ra

te

Duration

Inflation - RPI assumptionsThe chart on the following page shows long-term inflation assumptions

as measured by the Retail Prices Index (RPI). The average RPI assumption

decreased from 3.4% pa in December 2013 to 3.1% pa in December 2014.

In March 2015 this decreased again, to 3.0% pa.

3.6% paThe average discount rate

for December 2014 year-

ends, 0.9% pa lower than a

year earlier.

3.0% paThe average assumption for

future RPI inflation at the

end of March 2015.

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures30

0

5

10

15

20

25

30

Under 2.9 2.9 to 3.09 3.1 to 3.29 3.3 to 3.49 3.5 to 3.69 3.7 or over

Num

ber

of

com

pan

ies

RPI inflation used in December 2013, December 2014 and March 2015 (% pa)

December 2013

December 2014

March 2015

For December 2014 year-ends, the highest RPI inflation assumption was

3.35% pa, adopted by Standard Life. At the other extreme RELX Group

and Unilever, who both reported at the same date, adopted an assumption

of 2.9% pa. In general, the December 2014 RPI inflation assumptions had a

similar spread to those used in 2013, but were lower.

The Bank of England publishes statistics for future price inflation implied

by gilt spot rates. These showed that long-term RPI inflation implied by

20 year gilt spot rates was around 3.3% pa at the end of December 2014.

This suggests that, in order to justify an assumption much lower than

this for future RPI inflation, companies may be allowing for a significant

“inflation risk premium”. This represents the theoretical return that

investors are willing to forgo when investing in index-linked gilts, in return

for the inflation protection that these assets provide.

In practice, it is the discount rate net of assumed future price inflation

which is the key assumption.

The chart below shows the difference between the discount rate and

the assumption for RPI inflation (the net discount rate) for companies

reporting as at 31 December 2013, 31 December 2014 and 31 March 2015.

It shows that the net discount rate has reduced since December 2013,

from an average of 1.1% pa to 0.5% pa at 31 December 2014. Notably, two

companies were using negative net discount rates at 31 March 2015. These

were British Land and Land Securities, adopting net discount rates of

-0.2% pa and -0.1% pa respectively.

31LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

0

5

10

15

20

Under 0

0 to 0.19

0.2 to 0.39

0.4 to 0.59

0.6 to 0.79

0.8 to 0.99

1 to 1.19

1.2 or over

Num

ber

of

com

pan

ies

Discount rates in excess of RPI inflation used in December 2013, December 2014 and March 2015 (% pa)

December 2013December 2014March 2015

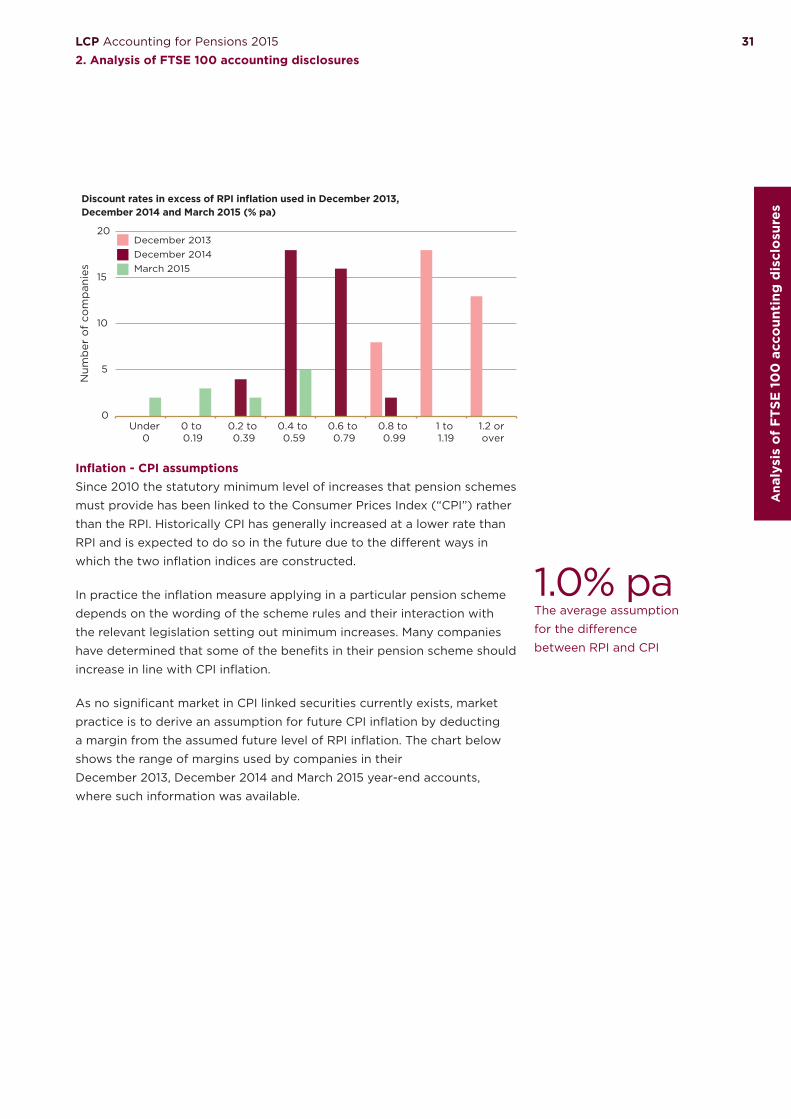

Inflation - CPI assumptionsSince 2010 the statutory minimum level of increases that pension schemes

must provide has been linked to the Consumer Prices Index (“CPI”) rather

than the RPI. Historically CPI has generally increased at a lower rate than

RPI and is expected to do so in the future due to the different ways in

which the two inflation indices are constructed.

In practice the inflation measure applying in a particular pension scheme

depends on the wording of the scheme rules and their interaction with

the relevant legislation setting out minimum increases. Many companies

have determined that some of the benefits in their pension scheme should

increase in line with CPI inflation.

As no significant market in CPI linked securities currently exists, market

practice is to derive an assumption for future CPI inflation by deducting

a margin from the assumed future level of RPI inflation. The chart below

shows the range of margins used by companies in their

December 2013, December 2014 and March 2015 year-end accounts,

where such information was available.

1.0% paThe average assumption

for the difference

between RPI and CPI

LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures32

0

5

10

15

Under 0.8 0.8 to 0.89 0.9 to 0.99 1 to 1.09 1.1 or over

Num

ber

of

com

pan

ies

Di�erence in RPI and CPI inflation assumptions used in December 2013, December 2014and March 2015 (% pa)

December 2013

December 2014

March 2015

At 31 December 2014 the average margin was 1.0% pa compared to

0.9% pa at 31 December 2013. At 31 December 2014, Aviva, Persimmon,

Schroders and Rolls-Royce Holdings used a long-term CPI inflation

assumption of 1.1% pa below their RPI inflation assumption, the largest

margin at that date.

Increases in pensionable payFor schemes that still relate benefits to pay close to retirement, the

assumed rate of growth in pensionable pay affects the disclosed IAS19

liability and the cost of benefits being earned. A lower assumption

produces a lower projected pension and hence lower pension liabilities as

well as a lower charge to operating income.

The average assumption for increases in pensionable pay (in excess of

the RPI inflation assumption) was 0.1% in 2014. In recent years a number

of companies have introduced caps on or even frozen increases in

pensionable salary and as a result disclosed a salary increase assumption

lower than RPI inflation. The average assumption has dropped from

0.5% pa in 2013 and from 1.5% pa 10 years ago.

0.1% paThe average assumption for

real increases in pensionable

pay, down from 1.5% pa 10

years ago.

33LCP Accounting for Pensions 2015

2. Analysis of FTSE 100 accounting disclosures

Ana

lysi

s o

f FT

SE 1

00

acc

oun

ting

dis

clo

sure

s

Pensionable pay growth rates used in excess of RPI inflation (% pa)

2013

2014

0

5

10

15

20

25

30

Under -1.5

-1.5 to -0.76

-0.75 to -0.01

0 to 0.74

0.75 to 1.49

1.5 to 2.24

2.25 or over

Num

ber

of

com

pan

ies

As the number of active members in final salary pension schemes has

reduced, the assumption for salary growth has become less significant.

34

Contentp36 Appendix 1 - FTSE 100 accounting disclosure listing

p40 Appendix 2 - FTSE 100 accounting risk measures

24 FTSE 100 companies disclosed a pension surplus in 2014, compared to 21 companies in 2013

Nick Bunch

Partner LCP

Ap

pen

dic

es

Thi

s ta

ble

sho

ws

the

key

dis

clo

sure

s m

ade

by

the

com

pan

ies

in t

he F

TS

E 1

00

as

at 3

1 D

ecem

ber

20

14 t

hat

rep

ort

ed IA

S19

fig

ures

in t

heir

20

14 a

cco

unts

. The

so

urce

of

the

dat

a is

eac

h co

mp

any’

s an

nual

rep

ort

and

acc

oun

ts f

or

the

acco

unti

ng p

erio

d e

ndin

g in

20

14. T

he m

arke

t va

lue

of

asse

ts a

nd s

urp

lus/

(defi

cit)

fig

ures

exc

lud

e p

ost

ret

irem

ent

med

ical

ben

efits

whe

re p

oss

ible

and

rel

ate

to t

he w

orl

dw

ide

po

siti

on

of

each

co

mp

any,

no

t ju

st t

he U

K s

chem

es. F

igur

es s

how

n ar

e b

efo

re d

efer

red

tax

and

bef

ore

any

bal

ance

shee

t as

set

limit

s ha

ve b

een

app

lied

. All

fig

ures

are

ro

und

ed t

o t

he n

eare

st m

illio

n p

oun

ds.

The

dis

coun

t ra

te a

nd p

rice

infl

atio

n as

sum

pti

ons

ref

er t

o t

hose

dis

clo

sed

fo

r th

e

com

pan

ies’

mai

n U

K s

chem

es w

here

ava

ilab

le. “

ND

” m

eans

no

UK

sp

ecifi

c fi

gur

es w

ere

dis

clo

sed

.

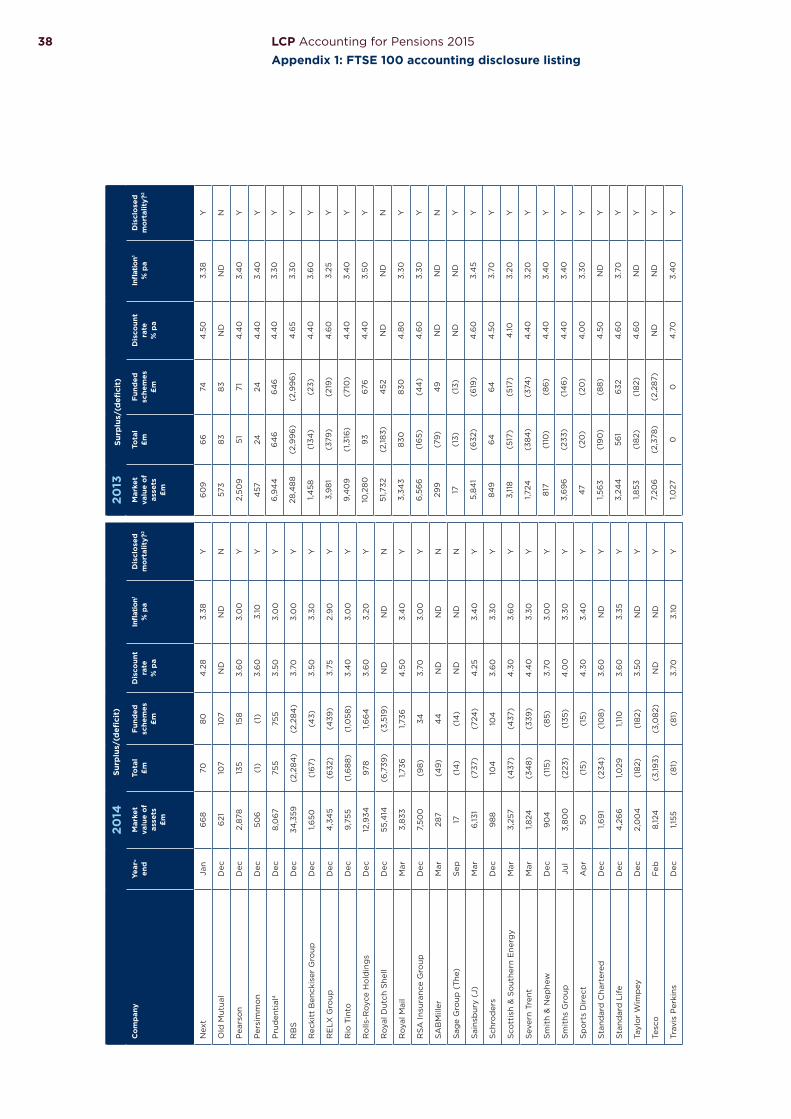

2014

Surp

lus/

(defi

cit)

Co

mp

any

Year

-en

dM

arke

t va

lue

of

asse

ts

£m

Tota

l£m

Fund

ed

sche

mes

£m

Dis

coun

t ra

te%

pa

Infla

tion1

% p

aD

iscl

ose

d

mo

rtal

ity?

2

3i G

roup

Mar

89

919

719

74

.50

3.4

0Y

Ab

erd

een

Ass

et M

anag

emen

tS

ep19

2(4

)(4

)4

.00

3.20

Y

Ag

gre

koD

ec9

1(7

)(7

)3.

80

3.30

Y

Ang

lo A

mer

ican

Dec

3,6

01

(159

)(1

9)

3.6

03.

10Y

Ash

tead

Gro

upA

pr

84

66

4.3

03.

50Y

Ass

oci

ated

Bri

tish

Fo

od

sS

ep3,

48

5(3

1)4

64

.103.

40

Y

Ast

raZ

enec

aD

ec6

,778

(1,8

70)

(1,4

93)

3.50

3.10

Y

Avi

vaD

ec15

,474

2,30

42,

424

3.70

3.10

Y

Bab

cock

Inte

rnat

iona

l Gro

upM

ar3,

220

(26

8)

(26

8)

4.5

03.

30Y

BA

E S

yste

ms3

Dec

23,6

75(5

,38

7)(5

,20

8)

3.6

03.

20Y

Bar

clay

sD

ec28

,874

(1,3

29)

(1,0

43)

3.6

73.

05

Y

Bar

ratt

Dev

elo

pm

ents

Jun

330

33

4.3

03.

30Y

BG

Gro

upD

ec1,2

85

(16

5)(1

17)

3.70

3.10

Y

BH

P B

illit

on

Jun

778

(48

)13

4.10

3.10

Y

BP

Dec

28,14

1(5

,50

7)(8

83)

3.6

03.

00

Y

Bri

tish

Am

eric

an T

ob

acco

Dec

6,2

53(6

28)

(34

1)3.

40

3.0

0Y

Bri

tish

Lan

d C

oM

ar13

16

64

.40

3.70

Y

BT

Gro

upM

ar4

0,11

3(7

,022

)(6

,953

)4

.25

3.25

Y

Bun

zlD

ec36

6(7

0)

(52)

ND

ND

Y

Cap

ita

Dec

94

0(1

93)

(19

3)3.

753.

00

Y

Car

niva

lN

ov37

47

73.

85

3.20

Y

Cen

tric

aD

ec6

,44

46

211

13.

90

3.0

0Y

Co

ca-C

ola

HB

CD

ec26

7(1

12)

(28

)N

DN

DN

Co

mp

ass

Gro

upS

ep2,

307

(176

)21

4.0

03.

20Y

CR

HD

ec1,5

94

(54

1)(4

95)

3.50

3.0

0Y

Dia

geo

Jun

7,4

80

(473

)(2

35)

4.2

03.

30Y

2013

Surp

lus/

(defi

cit)

Mar

ket

valu

e o

f as

sets

£m

Tota

l£m

Fund

ed

sche

mes

£m

Dis

coun

t ra

te%

pa

Infla

tion1

% p

aD

iscl

ose

d

mo

rtal

ity?

2

90

717

017

04

.40

3.30

Y

176

(4)

(4)

4.5

03.

40

Y

78(6

)(6

)4

.50

3.70

Y

3,18

9(2

15)

(85)

4.4

03.

40

Y

780

14

.20

3.4

0Y

3,23

3(3

)6

44

.70

3.50

Y

6,2

23(1

,34

7)(1

,031

)4

.50

3.50

Y

12,3

98

239

357

4.4

03.

40

Y

3,20

5(2

61)

(26

1)4

.40

2.8

0Y

21,3

74(3

,54

0)

(3,3

57)

4.5

03.

40

Y

25,7

43

(1,6

64

)(1

,36

6)

4.4

63.

42

Y

295

(13)

(13)

4.7

03.

40

Y

1,16

3(1

01)

(57)

4.5

03.

40

Y

1,24

8(4

0)

344

.50

3.6

0Y

26,0

83

(3,4

86

)58

14

.60

3.30

Y

5,76

7(3

77)

(138

)4

.40

3.4

0Y

120

11

4.10

3.20

Y

41,5

66

(5,8

56)

(5,7

84

)4

.20

3.30

Y

336

(45)

(30

)N

DN

DY

84

8(1

18)

(118

)4

.50

3.30

Y

329

(4)

(4)

4.4

03.

40

Y

5,6

83

40

82

4.6

03.

30Y

253

(91)

(10

)N

DN

DN

2,14

9(2

09

)(2

4)

4.4

03.

40

Y

1,929

(330

)(2

91)

4.6

03.

30Y

7,0

82

(536

)(2

97)

4.6

03.

30Y

LCP Accounting for Pensions 2015

Appendix 1: FTSE 100 accounting disclosure listing36

37LCP Accounting for Pensions 2015

Appendix 1: FTSE 100 accounting disclosure listing

2014

Surp

lus/

(defi

cit)

Co

mp

any

Year

-en

dM

arke

t va

lue

of

asse

ts

£m

Tota

l£m

Fund

ed

sche

mes

£m

Dis

coun

t ra

te%

pa

Infla

tion1

% p

aD

iscl

ose

d

mo

rtal

ity?

2

Dir

ect

Line

Insu

ranc

e G

roup

Dec

83

44

3.4

03.

10Y

Exp

eria

nM

ar6

65

144

54

.30

3.30

Y

Fre

snill

oD

ec13

(9)

(3)

ND

ND

N

Fri

end

s Li

feD

ec1,6

3859

593.

67

ND

Y

G4

SD

ec2,

04

0(3

19)

(26

4)

3.70

3.0

0Y

GK

ND

ec2,

627

(1,7

11)

(1,0

95)

3.53

3.0

8Y

Gla

xoS

mit

hKlin

eD

ec16

,112

(1,6

89

)(1

,238

)3.

60

3.0

0Y

Gle

nco

re X

stra

taD

ec2,

342

(68

6)

(68

6)

ND

ND

N

Ham

mer

son

Dec

62

(40

)(2

8)

3.6

03.

10N

HS

BC

Ho

ldin

gs

Dec

28,7

771,7

731,7

86

3.70

3.20

Y

Imp

eria

l To

bac

co G

roup

Sep

3,0

94

(474

)28

4.0

03.

20Y

Inte

rCo

ntin

enta

l Ho

tels

Gro

upD

ec11

2(7

1)(1

5)3.

703.

30Y

Inte

rnat

iona

l Air

lines

Gro

upD

ec21

,195

3811

53.

63

2.9

0Y

Inte

rtek

Gro

upD

ec12

0(2

5)(2

5)3.

60

ND

Y

ITV

Dec

3,34

1(3

46

)(2

98

)3.

60

3.0

3Y

John

son

Mat

they

Mar

1,456

(117

)(1

17)

4.6

03.

40

Y

Kin

gfi

sher

Feb

2,12

7(1

00

)(1

00

)4

.40

3.30

Y

Land

Sec

urit

ies

Gro

upM

ar19

62

24

.25

3.6

0Y

Leg

al &

Gen

eral

Gro

up4

Dec

1,910

(49

4)

(49

4)

3.6

03.

10Y

Lloy

ds

Ban

king

Gro

upD

ec38

,133

89

08

90

3.6

72.

95

Y

Lond

on

Sto

ck E

xcha

nge

Gro

up5

Mar

44

4(2

3)(2

3)4

.50

3.4

0Y

Lond

on

Sto

ck E

xcha

nge

Gro

up5

Dec

507

(24

)(2

4)

3.70

3.10

Y

Mar

ks &

Sp

ence

r G

roup

Mar

6,7

2920

020

14

.45

3.4

0Y

Meg

git

tD

ec76

1(2

71)

(254

)3.

60

3.10

Y

Mo

ndi G

roup

Dec

110

(14

8)

(36

)N

DN

DN

Mo

rris

on

(Wm

) S

uper

mar

kets

Feb

3,0

94

(11)

(11)

4.5

03.

50Y

Nat

iona

l Gri

dM

ar21

,638

(1,2

76)

(1,0

28)

4.3

03.

30Y

2013

Surp

lus/

(defi

cit)

Mar

ket

valu

e o

f as

sets

£m

Tota

l£m

Fund

ed

sche

mes

£m

Dis

coun

t ra

te%

pa

Infla

tion1

% p

aD

iscl

ose

d

mo

rtal

ity?

2

66

(2)

(2)

4.4

03.

50Y

654

2353

4.5

03.

40

Y

14(7

)(2

)N

DN

DN

1,410

(4)

(4)

4.4

1N

DY

1,66

0(5

04

)(4

72)

4.4

03.

40

Y

2,53

2(1

,271

)(7

63)

4.3

53.

28Y

15,2

25(6

13)

(20

7)4

.50

3.4

0Y

2,20

7(5

90

)(5

90

)N

DN

DN

58(3

3)(2

1)4

.60

3.4

0N

24,5

769

410

64

.45

3.6

0Y

2,9

24(6

21)

(16

2)4

.30

3.30

Y

44

5(9

1)(1

1)4

.60

3.6

0Y

19,10

9(3

)6

54

.55

3.28

Y

113

(13)

(13)

4.5

0N

DY

2,8

70(4

45)

(40

1)4

.53

3.38

Y

1,413

(19

5)(1

95)

4.5

03.

40

Y

2,0

87

00

4.6

03.

30Y

193

66

4.3

03.

50Y

1,64

6(4

64

)(4

64

)4

.40

3.50

Y

32,5

68

(78

7)(7

87)

4.6

03.

30Y

274

(26

)(2

6)

4.5

03.

40

Y

NA

NA

NA

NA

NA

NA

6,9

3024

824

94

.30

3.4

0Y

68

8(1

90

)(1

77)

4.6

03.

40

Y

100

(127

)(3

2)N

DN

DN

2,8

39(2

0)

(20

)4

.85

3.70

Y

21,7

70(1

,90

6)

(1,6

40

)4

.30

3.4

0Y

38 LCP Accounting for Pensions 2015

Appendix 1: FTSE 100 accounting disclosure listing

2014

Surp

lus/

(defi

cit)

Co

mp

any

Year

-en

dM

arke

t va

lue

of

asse

ts

£m

Tota

l£m

Fund

ed

sche

mes

£m

Dis

coun

t ra

te%

pa

Infla

tion1

% p

aD

iscl

ose

d

mo

rtal

ity?

2

Nex

tJa

n6

68

708

04

.28

3.38

Y

Old

Mut

ual

Dec

621

107

107

ND

ND

N

Pea

rso

nD

ec2,

878

135

158

3.6

03.

00

Y

Per

sim

mo

nD

ec50

6(1

)(1

)3.

60

3.10

Y

Pru

den

tial

4D

ec8

,06

775

575

53.

503.

00

Y

RB

SD

ec34

,359

(2,2

84

)(2

,28

4)

3.70

3.0

0Y

Rec

kitt

Ben

ckis

er G

roup

Dec

1,650

(16

7)(4

3)3.

503.

30Y

RE

LX G

roup

Dec

4,3

45

(632

)(4

39)

3.75

2.9

0Y

Rio

Tin

toD

ec9

,755

(1,6

88

)(1

,058

)3.

40

3.0

0Y

Ro

lls-R

oyce

Ho

ldin

gs

Dec

12,9

349

781,6

64

3.6

03.

20Y

Roy

al D

utch

She

llD

ec55

,414

(6,7

39)

(3,5

19)

ND

ND

N

Roy

al M

ail

Mar

3,8

331,7

361,7

364

.50

3.4

0Y

RS

A In

sura

nce

Gro

upD

ec7,

500

(98

)34

3.70

3.0

0Y

SA

BM

iller

Mar

287

(49

)4

4N

DN

DN

Sag

e G

roup

(T

he)

Sep

17(1

4)

(14

)N

DN

DN

Sai

nsb

ury

(J)

Mar

6,13

1(7

37)

(724

)4

.25

3.4

0Y

Sch

rod

ers

Dec

98

810

410

43.

60

3.30

Y

Sco

ttis

h &

So

uthe

rn E

nerg

yM

ar3,

257

(437

)(4

37)

4.3

03.

60

Y

Sev

ern

Tren

tM

ar1,8

24(3

48

)(3

39)

4.4

03.

30Y

Sm

ith

& N

ephe

wD

ec9

04

(115

)(8

5)3.

703.

00

Y

Sm

iths

Gro

upJu

l3,

80

0(2

23)

(135

)4

.00

3.30

Y

Sp

ort

s D

irec

tA

pr

50(1

5)(1

5)4

.30

3.4

0Y

Sta

ndar

d C

hart

ered

Dec

1,69

1(2

34)

(10

8)

3.6

0N

DY

Sta

ndar

d L

ife

Dec

4,2

66

1,029

1,110

3.6

03.

35Y

Tayl

or

Wim

pey

Dec

2,0

04

(18

2)(1

82)

3.50

ND

Y

Tesc

oF

eb8

,124

(3,19

3)(3

,08

2)N

DN

DY

Trav

is P

erki

nsD

ec1,1

55(8

1)(8

1)3.

703.

10Y

2013

Surp

lus/

(defi

cit)

Mar

ket

valu

e o

f as

sets

£m

Tota

l£m

Fund

ed

sche

mes

£m

Dis

coun

t ra

te%

pa

Infla

tion1

% p

aD

iscl

ose

d

mo

rtal

ity?

2

60

96

674

4.5

03.

38Y

573

83

83

ND

ND

N

2,50

951

714

.40

3.4

0Y

457

2424

4.4

03.

40

Y

6,9

44

64

66

46

4.4

03.

30Y

28,4

88

(2,9

96

)(2

,99

6)

4.6

53.

30Y

1,458

(134

)(2

3)4

.40

3.6

0Y

3,9

81

(379

)(2

19)

4.6

03.

25Y

9,4

09

(1,3

16)

(710

)4

.40

3.4

0Y

10,2

80

93

676

4.4

03.

50Y

51,7

32(2

,183)

452

ND

ND

N

3,34

38

308

304

.80

3.30

Y

6,5

66

(16

5)(4

4)

4.6

03.

30Y

299

(79

)4

9N

DN

DN

17(1

3)(1

3)N

DN

DY

5,8

41

(632

)(6

19)

4.6

03.

45

Y

84

96

46

44

.50

3.70

Y

3,11

8(5

17)

(517

)4

.103.

20Y

1,724

(38

4)

(374

)4

.40

3.20

Y

817

(110

)(8

6)

4.4

03.

40

Y

3,6

96

(233

)(1

46

)4

.40

3.4

0Y

47

(20

)(2

0)

4.0

03.

30Y

1,56

3(1

90

)(8

8)

4.5

0N

DY

3,24

456

16

324

.60

3.70

Y

1,853

(18

2)(1

82)

4.6

0N

DY

7,20

6(2

,378

)(2

,28

7)N

DN

DY

1,027

00

4.7

03.

40

Y

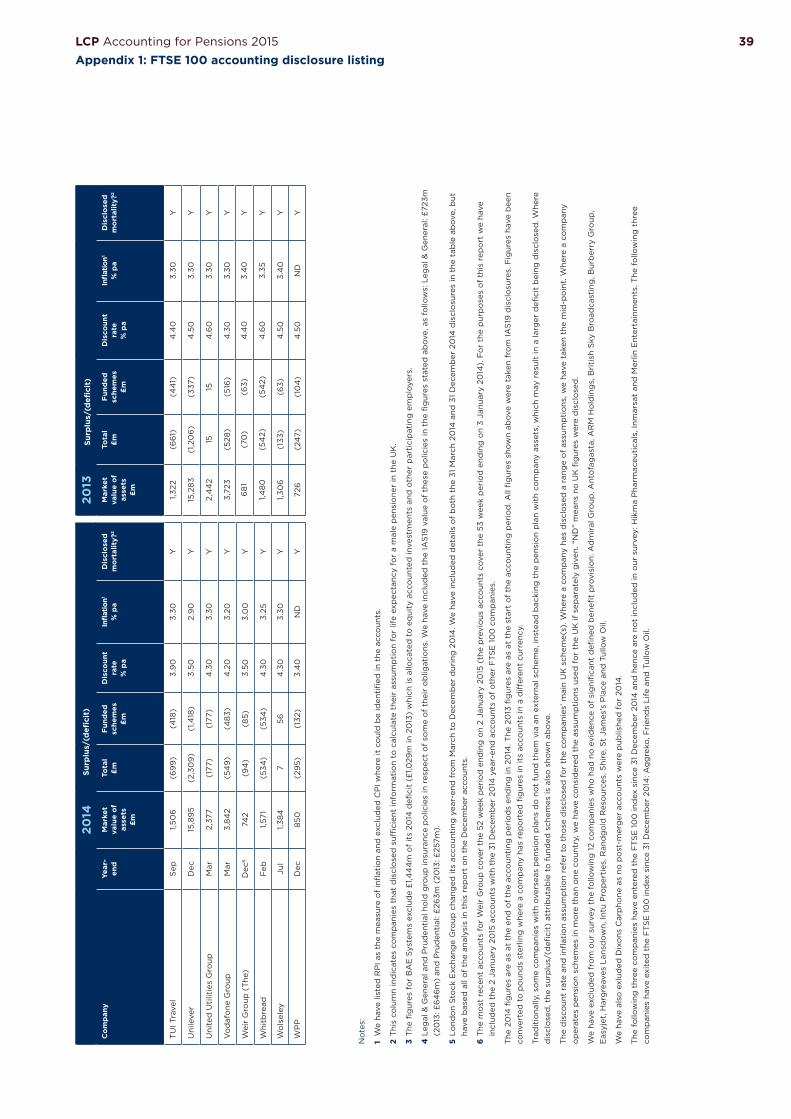

39

No

tes:

1 W

e ha

ve li

sted

RP

I as

the

mea

sure

of

infl

atio

n an

d e

xclu

ded

CP

I whe

re it

co

uld

be

iden

tifi

ed in

the

acc

oun

ts.

2 T

his

colu

mn

ind

icat

es c

om

pan

ies

that

dis

clo

sed

suffi

cien

t in

form

atio

n to

cal

cula

te t

heir

ass

ump

tio

n fo

r lif

e ex

pec

tanc

y fo

r a

mal

e p

ensi

one

r in

the

UK

.

3 T

he fi

gur

es f

or

BA

E S

yste

ms

excl

ude

£1,4

44

m o

f it

s 20

14 d

efici

t (£

1,029

m in

20

13)

whi

ch is

allo

cate

d t

o e

qui

ty a

cco

unte

d in

vest

men

ts a

nd o

ther

par

tici

pat

ing

em

plo

yers

.

4 L

egal

& G

ener

al a

nd P

rud

enti

al h

old

gro

up in

sura

nce

po

licie

s in

res

pec

t o

f so

me

of

thei

r o

blig

atio

ns. W

e ha

ve in

clud

ed t

he IA

S19

val

ue o

f th

ese

po

licie

s in

the

fig

ures

sta

ted

ab

ove,

as

follo

ws:

Leg

al &

Gen

eral

: £72

3m

(20

13: £

64

6m

) an

d P

rud

enti

al: £

263m

(20

13: £

257m

).

5 Lo

ndo

n S

tock

Exc

hang

e G

roup

cha

nged

its

acco

unti

ng y

ear-

end

fro

m M

arch

to

Dec

emb

er d

urin

g 2

014

. We

have

incl

uded

det

ails

of

bo

th t

he 3

1 M

arch

20

14 a

nd 3

1 D

ecem

ber

20

14 d

iscl

osu

res

in t

he t

able

ab

ove,

but

ha

ve b

ased

all

of

the

anal