Pension reform in the United Kingdom: An economic perspective Richard Disney Institute for Fiscal Studies: [email protected] University of Sussex: [email protected] University College, London: [email protected] NIESR Conference: The Evolution of Pensions: Reforms and their Consequences December 11, 2015

Pension reform in the United Kingdom: An economic perspective Richard Disney Institute for Fiscal Studies: [email protected][email protected] University.

Jan 19, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Pension reform in the United Kingdom: An economic perspective

Richard Disney

Institute for Fiscal Studies: [email protected] University of Sussex: [email protected] University College, London: [email protected]

NIESR Conference: The Evolution of Pensions:

Reforms and their ConsequencesDecember 11, 2015

This talk + some backgroundTopics in my talk:

What rationale for pension provision, especially for public intervention in provision?

The four phases of public pension provision in UK since 1946

Private pension provision in UK – employer-provided plans + voluntary (i.e. individual) purchase of annuities

General comments Semantics: ‘Social insurance’, ‘pensions’, ‘social security’,

‘welfare’ – multiple policies impinge on pension regime.

Multiple pension targets multiple pension instruments? (analogy – Tinbergen, 1952). (e.g. World Bank, 1994, ‘multi-pillar’ approach). Instruments not independent e.g public pensions affect private retirement saving.

A framework for analysing pension reform

‘Pensions’ primarily insurance against uncertain length of life. Development of pension arrangements in UK required calculation of ‘life tables’ (Gilbert, 1966; Creedy & Disney, 1985).For various reasons, voluntary risk-pooling arrangements could not provide comprehensive coverage.

So why public intervention in pensions?

Standard framework e.g. Diamond (1977) lists five rationales: Market failure Paternalism Redistribution Revenue-raising Administrative cost

Market failureLong life is a ‘good risk’, which is understood. Hard to see a moral hazard rationale for intervention.(though generous pensions may increase longevity)

Hence the rationale for intervention might be: adverse selection in annuity markets.Some (conflicting) evidence on adverse selection in UK annuity market: e.g. Cannon and Tonks, 2004; Einav, Finkelstein and Schrimpf, 2010; and Finkelstein and Poterba, 2002, 2004.

But this surely a rationale for compulsion, not for public provision of pensions as such.

PaternalismTwo rationales:

People don’t understand longevity risk (e.g. myopia), or People do understand risk but social planner has different

preferences over e.g. level of saving that is optimal.

This issue mostly hinges around: is level of retirement saving by individuals ‘optimal’?

How is ‘optimality’ defined? An arbitrary replacement rate (e.g. Pensions Commission, 2004) or by a life-cycle model (Banks et al, 2005; Crawford and O’Dea, 2014)?

Need a counterfactual – with no public pension what would saving have been?

‘Crowding out’ most likely where public pension replicates private saving (Disney, 2006)

‘Rational’ response by UK savers to retirement incentives? See e.g. Chung et al, 2008; Disney, Emmerson and Wakefield, 2010 )

RedistributionIssue is often confused by vague definitions of ‘redistribution’ (e.g. ‘from young to old’).

‘Intergenerational’ (between DOB cohorts) and ‘intragenerational’ (within DOB cohorts)Intergenerational:

Gainers have been early cohorts in NI programme + ‘large’ cohorts (baby boomers). Future IRRS look negative in UK (Disney, 2004; Disney and Emmerson, 2005)

Intragenerational Formula progressivity v differential mortality (Creedy,

Disney & Whitehouse, 1993) Treatment of spouses, crediting in non-participation etc

(Crawford, Keynes and Tetlow, 2014).

Revenue-raising

General idea is that people are more likely to contribute to a pension if they believe the contribution ‘pays’ for their own pension.

This not true in practice even in private DB plan where pension rights are ‘backloaded’ (Ippolito, 1997).

But especially not true in unfunded (PAYG) public programmes where current contributions ‘pay’ current pensions.

But the ‘contributory principle’ is still defended as ‘core’ of UK programme despite redistribution?

Scrap separate NI system? (Dilnot, Kay and Morris, 1984) Unlikely to happen due to ‘revenue-raising’ feature.

Integrate NI & personal taxes better (Mirrless, 2011)

Administrative costsA mundane reason for public intervention?

But much of Beveridge’s famous report (1942) hinged on lower costs of publicly-provided ‘social insurance’ v. (then) private pension contracts.

And issue of admin costs resurfaced in late-1980s with development of ‘Personal Pensions’ (e.g. , Murthi, Orszag and Orszag, 1999).

The trade-off? low cost ‘one size fits all’ pensions (e.g. ‘Workplace

Pensions’) v. individually-tailored pension contracts (+ adverse selection?)

Public pensions in the United Kingdom: The four stages of evolution

Comprehensive public provision introduced in UK in 1946 National Insurance Act. Many changes since!

I distinguish four phases: Social insurance Earnings replacement Tax credits A Citizen’s Pension?

Social insuranceThe introduction of ‘National Insurance’ in 1946

Contribution-based eligibility; flat benefits and flat contributions

A residual means-tested sector

Object: to alleviate old-age poverty; ‘earnings replacement’ to be left to private sector.

Problem 1: paying benefits immediately to newly retired (without contribution histories) exhausted National Insurance Fund.

Need to raise additional finance – partial shift to earnings-related contributions. Problem 2: Basic state pension so low that many pensioners still on means-tested benefits.

Earnings replacementCritics of ‘social insurance’ pointed to low level of income of those without additional private pensions.Left-wing solution: comprehensive publicly-provided earnings replacement?Right-wing solution: compulsory private insurance above BSP?

The solution (?) the 1975 Act: A second tier earnings-related pension (SERPS) Earnings-related contributions (to a ceiling) Additional provisions of credits for e.g. child care and

generous spouses’ pensions ‘Approved’ employer-provided pensions (DB plans) could opt-

out of second tier (and paying lower NI contribution)

The problem: It all cost too much! (Hemming & Kay, 1981, 1982)

Tax creditsThe problem: cost, especially with rising numbers of pensionsSolution 1: cut back generosity of SERPS and introduce new private pensions (see later)Solution 2: move towards a tax credit programme (Gordon Brown’s preferred option for redistribution)The Labour reforms 1999 onwards:

Uprate basic state pension more slowly (prices not earnings) Focus on means-tested sector, but supplement ‘Minimum Income

Guarantee’ (then called Pension Credit Guarantee) by a tapered benefit (at 40% withdrawal) ‘Pension Credit Saving Credit’. Hence a two-tier NIT-type structure.

Issues: Effective MTR lower but more people means-tested ‘Taper’ subsequently steepened worsened incentives Co-existence of medium-term 2-tier NIT with long run 2-tier

‘social insurance’?

A citizen’s pension?Pensions Act 2014:

Scraps earnings-related public provision, opting-out of tier 2 by employer-provided plans

Combines two tiers into one flat pension. Raise pensionable age to 67 in stages.

Appraisal ‘Back to Beveridge’?? (the Minister responsible a Liberal

(Democrat) MP, as was Beveridge!). But eligibility for higher flat pension not just contribution-

based, closer to a duration-of-residency eligibility requirement, as in New Zealand than the ‘contributory principle’.

The ‘triple lock’ of uprating as best of prices or earnings growth or +2.5% - no longer ‘lifting pensions out of poverty’ – they are doing better than workers since 2008!

Evaluation

UK has tried every conceivable kind of public pension provision since 1946!Advantages:

Multiple instruments can achieve multiple targets Has (broadly) achieved aim of eliminating pensioner

poverty Has (broadly) responded to demographic ageing without

rapidly rising pension contributions.

Disadvantages: Constant tinkering with pensions by politicians hinders

rational retirement saving plans by individuals. Different ‘models’ of provision cause over-complexity esp.

in late 1980s/early 1990s, and in 2000s.

Private pension provision in the United Kingdom

I briefly investigate two models of private pension delivery in UK:Employer-provided pension plans

Defined contribution (DC) where pension depends on value of contributions by employee and employer, return on fund, annuity rate and age of taking pension

Defined benefit (DB) where pension depends on years of service, some measure of earnings (e.g. final or career average), and age of taking pension

In DB plan, employer undertakes investment risk but employee takes on tenure and earnings risk (Bodie, Marcus and Merton, 1988; Disney and Whitehouse, 1996)

Individually-purchased annuities (DC personal accounts)

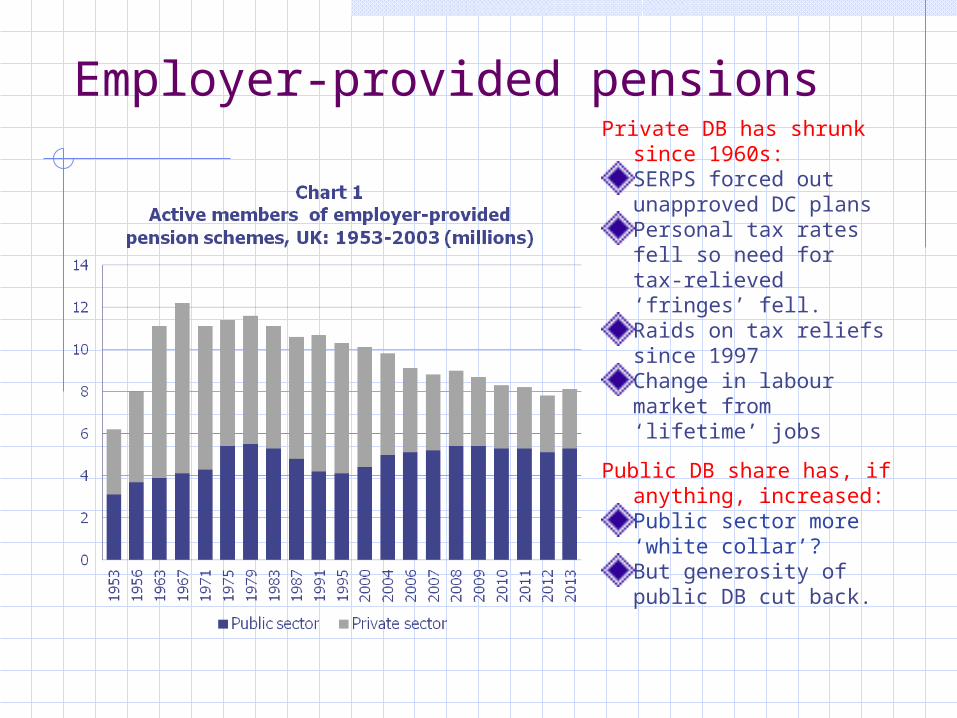

Employer-provided pensionsPrivate DB has shrunk

since 1960s:SERPS forced out unapproved DC plansPersonal tax rates fell so need for tax-relieved ‘fringes’ fell.Raids on tax reliefs since 1997Change in labour market from ‘lifetime’ jobs

Public DB share has, if anything, increased:Public sector more ‘white collar’?But generosity of public DB cut back.

The annuity market and individually-provided pensions

The ‘voluntary’ annuity market was relatively small:Finkelstein & Poterba (2002) cite 1/6th of annuitants and 6% of new annuitants were voluntary market v. compulsory market.New data are useful on take-up characteristics e.g. Banks, Crawford and Tetlow (2015).

The major expansion of individual accounts arose from replacement of s226 plans by Personal Pensions after 1988Employees could opt-out of SERPS (or employer plan) and have NI contributions + 2% bonus put in a PP account.Returns initially v. attractive but subsequent rebate changes (+ lower returns & annuity rates + high charges) eroded generosity (Disney & Whitehouse, 1992a, 1992b) little net new saving?Introduction of Stakeholder Pensions (low cost simplified version of PPs) had little effect on take-up but tax relief changes did have an effect (Disney, Emmerson and Wakefield, 2010)

New ‘Workplace Pensions’ will supersede these accounts?

ConclusionI suggested a standard set of criteria for evaluating and motivating UK pension policy.

The UK programme has been reformed constantly and has been highly complex at times.

This has provided a ‘test-bed’ for various forms of provision, and scope for (limited) evaluation!

At the present time, the UK programme has a degree of clarity, irrespective of ‘optimality’ (or otherwise)

Better data (ELSA additional waves, ASHE, WAS etc) are assisting current research.

Related Documents

![Index [ifs.org.uk]](https://static.cupdf.com/doc/110x72/621c50a39561082b99290f64/index-ifsorguk.jpg)