PENGUMUMAN Equity Research PT Multi Indocitra Tbk (MICE) (Tercatat Di Papan : Pengembangan) No.Peng-ER-00010/BEI.PPJ/08-2011 (dapat dilihat di internet : http://www.idx.co.id ) PT Bursa Efek Indonesia telah menerima surat melalui email dari PT Pemeringkat Efek Indonesia dengan No. 1062/PEF-DIR/VIII/2011 tanggal 11 Agustus 2011 mengenai Publikasi Laporan Penilaian Target Harga Referensi Saham PT Multi Indocitra Tbk sebagaimana terlampir (lampiran 19 lembar). Demikian agar maklum. Jakarta, 12 Agustus 2011 Umi Kulsum Andre P.J. Toelle Kepala Divisi Penilaian Perusahaan Sektor Jasa Kepala Divisi Perdagangan Saham Tembusan Yth. : 1. Ketua Badan Pengawas Pasar Modal dan LK; 2. Kepala Biro Transaksi dan Lembaga Efek Bapepam dan LK; 3. Kepala Biro PKP Sektor Jasa Bapepam dan LK; 4. Pusat Referensi Pasar Modal; 5. Direksi PT Multi Indocitra Tbk. lau_MICE_er_20110812_10

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PENGUMUMAN

Equity Research PT Multi Indocitra Tbk (MICE)

(Tercatat Di Papan : Pengembangan) No.Peng-ER-00010/BEI.PPJ/08-2011

(dapat dilihat di internet : http://www.idx.co.id) PT Bursa Efek Indonesia telah menerima surat melalui email dari PT Pemeringkat Efek Indonesia dengan No. 1062/PEF-DIR/VIII/2011 tanggal 11 Agustus 2011 mengenai Publikasi Laporan Penilaian Target Harga Referensi Saham PT Multi Indocitra Tbk sebagaimana terlampir (lampiran 19 lembar). Demikian agar maklum.

Jakarta, 12 Agustus 2011

Umi Kulsum Andre P.J. Toelle Kepala Divisi Penilaian Perusahaan Sektor Jasa Kepala Divisi Perdagangan Saham Tembusan Yth. : 1. Ketua Badan Pengawas Pasar Modal dan LK; 2. Kepala Biro Transaksi dan Lembaga Efek Bapepam dan LK; 3. Kepala Biro PKP Sektor Jasa Bapepam dan LK; 4. Pusat Referensi Pasar Modal; 5. Direksi PT Multi Indocitra Tbk.

lau_MICE_er_20110812_10

PEFINDO CREDIT RATING INDONESIA

1062/PEF-DIR/VlII/2011

Jakarta, 11 Agustus 2011

Kepada Yth.1. PT Multi Indocitra, Tbk

JI. Cideng Timur No. 73Jakarta Pusat,10160

u.p. Bapak Sukwan Widayat, Direktur

2. PT Bursa Efek IndonesiaGedung Bursa Efek IndonesiaJI. Jend. Sudirman Kav 52-53Jakarta Selatan, 12190

u.p. Bapak Ito Warsito, Direktur UtamaBapak Eddy Sugito, Direktur Penilaian Perusahaan

Perihal: Publikasi Laporan Penilaian Target Harga Referensi Saham PT Multi IndocitraTbk.

Dengan hormat,

Sehubungan dengan penugasan yang kami peroleh untuk melakukan Penilaian Target HargaReferensi Saham, dengan ini kami sampaikan hasil penilaian kami atas saham PT Multi IndocitraTbk (MICE) dalam versi Bahasa Indonesia dan Bahasa Inggris.

Apabila masih ada hal-hal yang memerlukan penjelasan lebih lanjut, mohon agar menghubungi kami.Atas perhatian dan kerjasamanya, kami ucapkan terima kasih.

Hormat kami,

Ronald T. Andi Kasim, CFADirektur Utama

e Rizalirektur

Tembusan : Bapak I Gede Nyoman Yetna, Kepala Divisi Pencatatan Sektor Riil, PT Bursa EfekIndonesia

/ma

PT. Pemeringkat Efek IndonesiaPanin Tower Senayan City 1ih FloorJI Asia Afrika Lot. 19, Jakarta 10270, INDONESIAPhone: (62-21) 7278 2380' Fax: (62-21) 7278 2370

Halaman 1 dari 9 halaman

Kontak: Equity & Index Valuation Division Phone: (6221) 7278 2380 [email protected]

“Pernyataan disclaimer pada halaman akhir

merupakan bagian yang tidak terpisahkan dari dokumen ini”

www.pefindo.com

Multi Indocitra, Tbk Laporan Kedua

Equity Valuation

10 Agustus 2011

Target Harga

Terendah Tertinggi 475 530

Produk Perawatan Bayi

Kinerja Saham

2000

2500

3000

3500

4000

4500

200

300

400

500

600

700

800

7/15/2010 8/27/2010 10/15/201011/29/2010 1/13/2011 2/28/2011 4/11/2011 5/25/2011 7/8/2011

MICE IHSG

Sumber: Bloomberg

Informasi Saham Rp

Kode saham MICE

Harga Saham per 10 Agustus 2011 430

Harga Saham Tertinggi 52 Minggu Terakhir 710

Harga Saham Terendah 52 Minggu Terakhir 330

Kapitalisasi Pasar Tertinggi 52 Minggu (Miliar) 426

Kapitalisasi Pasar Terendah 52 Minggu (miliar) 196

Penilaian Saham Sebelumnya Saat ini

Tertinggi 900 530

Terendah 810 475

Market Value Added & Market Risk

-250

-200

-150

-100

-50

0

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Maret-10 Maret-11

M

V

A

M

a

r

k

e

t

R

i

s

k

MVA Market Risk

Pemegang Saham (%)

PT Buana Graha Utama 60,44

Publik (kepemilikan < 5%) 27,05

Haiyanto 6,50

Surono Subekti 6,01

Perubahan Berkelanjutan

PT. Multi Indocitra, Tbk (“MICE”) didirikan pada tanggal 11 Januari 1990 dengan maksud dan tujuan untuk semula mendistribusikan produk perawatan dan perlengkapan untuk kebutuhan bayi, ibu hamil dan menyusui serta produk perawatan kulit. Produk tersebut dibuat di pabrik modern yang berlokasi di Cikande, Banten. Sampai tanggal 31 Desember 2010, MICE mempunyai sekitar 1.046 karyawan. Produk perlengkapan untuk bayi, anak-anak, serta ibu hamil dan menyusui diproduksi oleh anak perusahaan MICE, yaitu PT Pigeon Indonesia yang memproduksi antara lain botol susu dan dot bayi silicon dengan merek “Pigeon”. Sedangkan

produk perawatan kulit diproduksi oleh anak perusahaannya, PT Multielok Cosmetic yang memproduksi antara lain bedak, sampo, sabun cair untuk bayi, anak-anak dan remaja. Sejalan dengan peluang bisnis yang ada, MICE telah mengembangkan lini usaha baru yaitu lampu hemat energi dengan merek HORI yang telah mulai dipasarkan di sebagian besar wilayah Indonesia sejak 2010.

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Multi Indocitra, Tbk

10 Agustus 2011 Halaman 2 dari 9 halaman

Penyesuaian Target Harga Saham Kami melakukan beberapa penyesuaian terhadap proyeksi kami sebelumnya dan menyesuaikan target harga saham MICE menjadi pada kisaran Rp 475-

Rp 530 per saham, berdasarkan pertimbangan-pertimbangan berikut:

Kinerja bagus di 2010, MICE berhasil membukukan pertumbuhan penjualan signifikan sebesar 24,34% YoY dibandingkan dengan tahun lalu yang hanya 10,59%. Ini dikarenakan peningkatan volume penjualan di beberapa produk MICE. Ditambah dengan lini bisnis baru yaitu Lampu Hemat Energi (LHE) dengan merek HORI, yang mulai memberi kontribusi sekitar 7,76% dari total penjualan MICE di tahun pertama distribusinya.

Meningkatnya pendapatan per kapita di Indonesia akan mendorong belanja konsumen ke produk bermerek. Perubahan ini karena peningkatan Produk Domestik Bruto (PDB) sebesar 28% YoY, menjadi US$ 3.005 per kapita di 2010, dari US$ 2.350 per kapita di 2009.

Meningkatnya jumlah penduduk Indonesia yang tumbuh sebesar 16% dalam 10 tahun terakhir, atau mencapai 238 juta orang di 2010, dari hanya 205 juta orang di 2000. Pertumbuhan ini menjadi pemicu bagi penjualan MICE yang terus meningkat. Seperti tercatat dari 2008 – 2010, pertumbuhan penjualan MICE sebesar 17% CAGR.

Asumsi risk free rate, equity premium, dan beta masing-masing adalah sebesar 6,94%, 7,50%, dan 0,94x.

Didorong oleh Pertumbuhan Ekonomi Realisasi pertumbuhan Produk Domestik Bruto (PDB) sampai 1Q2011 mencapai 6,5%, lebih baik dari tahun sebelumnya pada periode yang sama yang hanya 5,7%, dan diperkirakan meningkat selama 2011. Hasilnya,

permintaan di beberapa produk seperti produk perawatan bayi akan meningkat. Terbukti dari kinerja MICE dimana total penjualan di 1Q2011 tumbuh sebesar 14% atau mencapai Rp 105 miliar, lebih baik dari tahun sebelumnya pada periode yang sama sebesar Rp 92 miliar. Lini Bisnis Baru untuk Percepatan Pertumbuhan Di 2010, MICE telah mengembangkan lini bisnis baru yaitu Lampu Hemat Energi (LHE) dengan merek “HORI”. Saat ini MICE memiliki lebih dari 38 distributor “HORI” yang tersebar di area Jawa, Sumatera dan Kalimantan. Di tahun pertama distribusinya, MICE membukukan penjualan “HORI” sebesar Rp 33 miliar atau berkontribusi sekitar 7,76% dari total penjualan MICE. Seiring dengan meningkatnya permintaan lampu di 2011, kami percaya

“HORI” dapat memberi kontribusi lebih besar terhadap penjualan MICE. Selain itu, MICE juga mendistribusikan botol bayi bebas Bisphenol A (BPA) tahun ini. Dari Mei – Juli 2011, penjualan botol bebas BPA mencapai Rp 3,5 miliar. Dan diperkirakan akan tumbuh pada tahun-tahun mendatang karena botol adalah salah satu produk MICE yang menjadi pemimpin pasar. Prospek Bisnis Pertumbuhan penduduk dan meningkatnya daya beli konsumen karena kondisi ekonomi yang lebih baik memberikan kontribusi signifikan terhadap penjualan produk perawatan bayi. Sementara dari lini bisnis baru MICE yaitu “HORI”, diperkirakan mencatat pertumbuhan penjualan sebesar 58% YoY di 2011, seiring dengan meningkatnya permintaan LHE domestik. Ditambah

dengan peluncuran botol bayi bebas Bisphenol A (BPA) tahun ini, dimana botol merupakan pemimpin pasar untuk produk bayi, kami percaya pendapatan MICE dapat tumbuh sebesar 24,18% di 2011, atau mencapai Rp 526 miliar, dan tumbuh 25% CAGR selama periode 2011 – 2015.

Tabel 1: Ringkasan Kinerja

2008 2009 2010 2011P 2012P

Penjualan [Rp miliar] 308 340 423 526 640

Laba sebelum pajak [Rp miliar]

46 49 47 56 67

Laba bersih [Rp miliar] 24 30 28 37 45

EPS [Rp] 40 51 47 62 75

Pertumbuhan EPS [%] (20) 27 (7,2) 29 21

P/E [x] 4,0 5,1 8,6 6,9* 5,7*

PBV [x] 0,5 0,7 0,9 0,9* 0,8*

Sumber: PT Multi Indocitra Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing Berdasarkan harga saham MICE per 10 Agustus 2011 – Rp 430 / saham

PARAMETER INVESTASI

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Multi Indocitra, Tbk

10 Agustus 2011 Halaman 3 dari 9 halaman

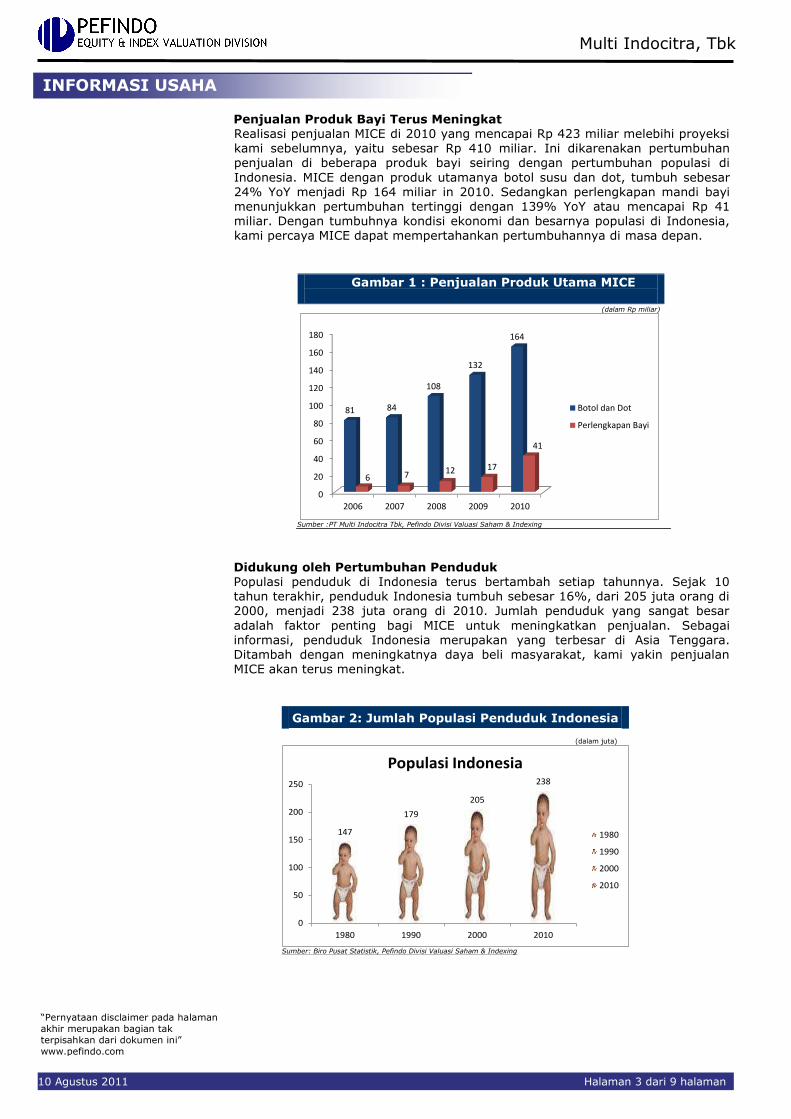

Penjualan Produk Bayi Terus Meningkat Realisasi penjualan MICE di 2010 yang mencapai Rp 423 miliar melebihi proyeksi kami sebelumnya, yaitu sebesar Rp 410 miliar. Ini dikarenakan pertumbuhan penjualan di beberapa produk bayi seiring dengan pertumbuhan populasi di

Indonesia. MICE dengan produk utamanya botol susu dan dot, tumbuh sebesar 24% YoY menjadi Rp 164 miliar in 2010. Sedangkan perlengkapan mandi bayi menunjukkan pertumbuhan tertinggi dengan 139% YoY atau mencapai Rp 41 miliar. Dengan tumbuhnya kondisi ekonomi dan besarnya populasi di Indonesia, kami percaya MICE dapat mempertahankan pertumbuhannya di masa depan.

Gambar 1 : Penjualan Produk Utama MICE

(dalam Rp miliar)

0

20

40

60

80

100

120

140

160

180

2006 2007 2008 2009 2010

81 84

108

132

164

6 7 12 17

41

Botol dan Dot

Perlengkapan Bayi

Sumber :PT Multi Indocitra Tbk, Pefindo Divisi Valuasi Saham & Indexing

Didukung oleh Pertumbuhan Penduduk Populasi penduduk di Indonesia terus bertambah setiap tahunnya. Sejak 10 tahun terakhir, penduduk Indonesia tumbuh sebesar 16%, dari 205 juta orang di

2000, menjadi 238 juta orang di 2010. Jumlah penduduk yang sangat besar

adalah faktor penting bagi MICE untuk meningkatkan penjualan. Sebagai informasi, penduduk Indonesia merupakan yang terbesar di Asia Tenggara. Ditambah dengan meningkatnya daya beli masyarakat, kami yakin penjualan MICE akan terus meningkat.

Gambar 2: Jumlah Populasi Penduduk Indonesia (dalam juta)

147

179

205

238

0

50

100

150

200

250

1980 1990 2000 2010

Populasi Indonesia

1980

1990

2000

2010

Sumber: Biro Pusat Statistik, Pefindo Divisi Valuasi Saham & Indexing

INFORMASI USAHA

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Multi Indocitra, Tbk

10 Agustus 2011 Halaman 4 dari 9 halaman

Pemimpin Pasar untuk Produk Bayi Di tahun 2005-2010, botol susu dan dot “Pigeon” MICE menyumbang sekitar 52% dari pangsa pasar nasional. Dalam hal kontribusi penjualan, botol dan dot berkontribusi sebesar 38,68% dari total penjualan MICE di 2010. Kontribusi ini diperkirakan tumbuh sejalan dengan membaiknya kondisi ekonomi di Indonesia. Dengan dukungan produk berkualitas baik, fasilitas produksi modern, cakupan luas dan jaringan distribusi

terintegrasi, kami yakin MICE dapat mempertahankan posisinya sebagai pemimpin pasar dalam produk bayi.

Gambaran Industri Perawatan Bayi 2011: Tetap Prospektif Kami memprediksi di 2011, penjualan produk perawatan bayi akan meningkat seiring tingginya belanja konsumen dan populasi penduduk yang terus tumbuh. Faktanya, selama 3 tahun terakhir MICE dapat mencatat pertumbuhan penjualan sebesar 17% CAGR. Banyaknya produk perlengkapan bayi dan balita impor dari China, Amerika dan Eropa tidak menghambat penjualan produk lokal dikarenakan

produk impor tersebut membidik konsumen kelas atas. Sementara persaingan di pasar menengah ke atas belum ketat. Hanya dengan inovasi dan promosi yang berkualitas yang akan menguasai pangsa pasar di industri ini. Selalu Menjaga Kualitas Produk

Salah satu faktor yang membuat MICE dapat mempertahankan pangsa pasar di

industrinya adalah karena kualitas produk-produknya. Pembuatan produk “Pigeon” yang dilakukan oleh anak Perusahaan dan Perusahaan afiliasi telah diperiksa kualitasnya untuk memastikan bahwa standar mutu yang ditetapkan oleh Pigeon Corporation Jepang telah diikuti. PT. Multielok Cosmetics dan PT. Pigeon Indonesia telah melewati beberapa sertifikasi, yaitu:

PT. Multielok Cosmetics: Sertifikat AS/NZS ISO 9001:2000 dari SAI Global Limited Australia, Sertifikat Cara Pembuatan Kosmetik yang Baik (CPKB) dari Kepala Badan Pengawas Obat dan Makanan Republik Indonesia.

PT. Pigeon Indonesia: Sertifikat AS/NZS ISO 9001:2001 dari SAI Global Limited

Australia.

Beberapa Penghargaan Mencerminkan Prestasi MICE Selama di industri perawatan bayi, MICE selalu mendistribusikan produk berkualitas tinggi kepada pelanggan. Melalui komitmen tersebut, MICE berhasil medapat penghargaan dalam beberapa kategori di 2010, seperti; Penghargaan

Top Brand dari Majalah Marketing untuk Kategori Botol Susu dan Perlengkapan

Makan Bayi dan Penghargaan Reader’s Choice dari Majalah Ibu dan Bayi untuk Kategori Botol dan Dot, Penghangat Botol, Alat Steril Botol, Pelindung Payudara, Pompa Payudara, Alat Makan Bayi dan Empeng.

Diversifikasi Botol Bayi Bebas Bisphenol A (BPA) MICE mulai mendistribusikan produk diversifikasi baru yaitu botol bebas BPA tahun ini. Ini dilakukan untuk memenuhi meningkatnya permintaan produk bayi

terutama permintaan akan botol bebas BPA. Sebagai pemimpin pasar botol bayi, MICE diperkirakan tidak butuh waktu lama untuk memperkenalkan produknya ke masyarakat. Dari Mei – Juli 2011, penjualan botol bebas BPA telah mencapai Rp 3,5 miliar. Dengan terus melakukan promosi yang berkualitas, kami percaya penjualan botol bebas BPA akan berkontribusi lebih tinggi untuk penjualan MICE di masa depan.

Ancaman dari Cina Tidak Menghambat Penjualan HORI Impor dari China ke Indonesia terus meningkat. Salah satunya adalah lampu. Di

1Q2011 impor lampu mencapai 45,78 juta unit, naik 14,74% dibandingkan periode yang sama tahun lalu. Ini karena meningkatnya kebutuhan lampu nasional sejalan dengan program penggratisan daya dari Perusahaan Listrik Negara (PLN). Selain itu, konsumsi lampu di 2011 diprediksi mencapai 260 juta unit, naik 30% dari 2010 yang hanya 200 juta unit. Di 2010, impor LHE dari

China sekitar 60% dari total konsumsi lampu nasional atau mencapai 161,25 juta unit.

Tetapi, ancaman produk China tidak signifikan mempengaruhi penjualan HORI. Karena HORI yang mulai dipasarkan sejak pertengahan 2010, berhasil berkontribusi 7,76% dari total penjualan MICE di 2010, atau Rp 33 miliar. Sementara itu, saat ini LHE HORI telah memiliki lebih dari 38 distributor yang

tersebar di Jawa, Sumatera dan Kalimantan. Juga sertifikasi produk HORI yang telah dimiliki oleh MICE adalah Standar Nasional Indonesia. Apalagi merek lampu

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Multi Indocitra, Tbk

10 Agustus 2011 Halaman 5 dari 9 halaman

HORI menduduki peringkat teratas dalam hal kualitas versi majalah SWA. Dengan strategi pemasaran yang tepat dan intensif, kami percaya penjualan HORI pada tahun 2011 mencapai Rp 52 miliar.

Strategi Pemasaran yang Tepat untuk Mendapatkan Daerah Potensial

Dalam mempertahankan loyalitas pelanggan, MICE melakukan promosi dengan berbagai rumah sakit untuk mensosialisasikan produk “Pigeon” kepada masyarakat. MICE juga mensponsori berbagai kegiatan sosial dan kegiatan usaha. Para distributor juga aktif terlibat dalam kegiatan pemasaran di daerah mereka. Ini terbukti efektif dalam meningkatkan penjualan MICE. Sejak 2008 sampai 2010, pertumbuhan penjualan adalah 17% CAGR. Dan masih memungkinkan untuk tumbuh karena ada beberapa daerah potensial di

Indonesia, seperti Sumatera yang memiliki tingkat pertumbuhan tertinggi dengan 5% per tahun, diikuti oleh Jawa 2,79% dan Bali 2,5%.

Gambar 7: Pertumbuhan Laju Penduduk di Indonesia

5%

2.79%

2.15%

Sumatera

Jawa

Bali

Sumber: Biro Pusat Statistik, Pefindo Divisi Valuasi Saham & Indexing

Gambar 3 : Konsumsi LHE di Indonesia

90

120

180200

260

0

50

100

150

200

250

300

2007 2008 2009 2010 2011P

Dal

am ju

ta u

nit

Konsumsi LHE

Konsumsi LHE

Sumber : Aperlindo. Pefindo Divisi Valuasi Saham & Indexing

Gambar 4 : Produkis LHE Indonesia

0

5

10

15

20

25

30

35

40

45

2008 2009 2010

24

4539

Dal

am ju

ta u

nit

Produksi LHE

Produksi LHE

Sumber : Aperlindo. Pefindo Divisi Valuasi Saham & Indexing

Gambar 5: Penjualan HORI

33

52

60

0

10

20

30

40

50

60

70

2010 2011P 2012P

Rp

mili

ar 2010

2011P

2012P

Sumber : Pt. Multi Indocitra Tbk, Estimasi Pefindo Divisi Valuasi Saham &

Indexing

Gambar 6: Impor Lampu dari China

34

36

38

40

42

44

46

1Q2010 1Q2011

39.03

45.78

Dal

am J

uta

Un

itImpor Lampu dari China

Impor Lampu dari China

Sumber : Aperlindo. Pefindo Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Multi Indocitra, Tbk

10 Agustus 2011 Halaman 6 dari 9 halaman

Prospek Usaha MICE Pertumbuhan penduduk dan meningkatnya daya beli konsumen karena kondisi ekonomi yang lebih baik memberikan kontribusi signifikan terhadap penjualan produk perawatan bayi. Sementara dari lini bisnis baru MICE yaitu “HORI”, diperkirakan mencatat pertumbuhan penjualan sebesar 58% YoY di 2011, seiring dengan meningkatnya permintaan LHE domestik. Ditambah dengan peluncuran botol bayi

bebas Bisphenol A (BPA) tahun ini, dimana botol merupakan pemimpin pasar untuk produk bayi, kami percaya pendapatan MICE dapat tumbuh sebesar 24,18% di 2011, atau mencapai Rp 526 miliar, dan tumbuh 25% CAGR selama periode 2011 – 2015.

Gambar 8 : Pertumbuhan Pendapatan MICE

423

506573

654

753

875

0

100

200

300

400

500

600

700

800

900

1000

2010 2011 2012 2013 2014 2015

Dal

am R

p m

iliar

2010

2011

2012

2013

2014

2015

Sumber:PT Multi Indocitra Tbk, Pefindo Divisi Valuasi Saham & Indexing

Strength Weakness

Pemimpin pasar dalam beberapa produk

bayi, seperti botol dan dot. Produk berkualitas tinggi dengan

Sertifikasi Standar Internasional. Diawasi langsung oleh Pigeon

Corporation of Japan. Mulai memproduksi botol bebas BPA

untuk memenuhi kebutuhan konsumen menengah dan atas.

Bergantung kepada principal-nya,

yaitu Pigeon Corporation of Japan.

Bergantung pada bahan baku impor untuk lampu.

Opportunity Threat

PDB per kapita Indonesia yang terus

tumbuh. Permintaan Lampu Hemat Energi (LHE)

yang terus meningkat. Populasi Indonesia yang terus

meningkat. Meningkatnya outlet spa untuk

perawatan bayi mempengaruhi penjualan produk bayi.

ACFTA dapat menyebabkan

persaingan yang semakin ketat dengan harga yang lebih murah.

Pemalsuan merek dagang oleh pihak lain.

Low entry barrier.

ANALISIS SWOT

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Multi Indocitra, Tbk

10 Agustus 2011 Halaman 7 dari 9 halaman

VALUASI

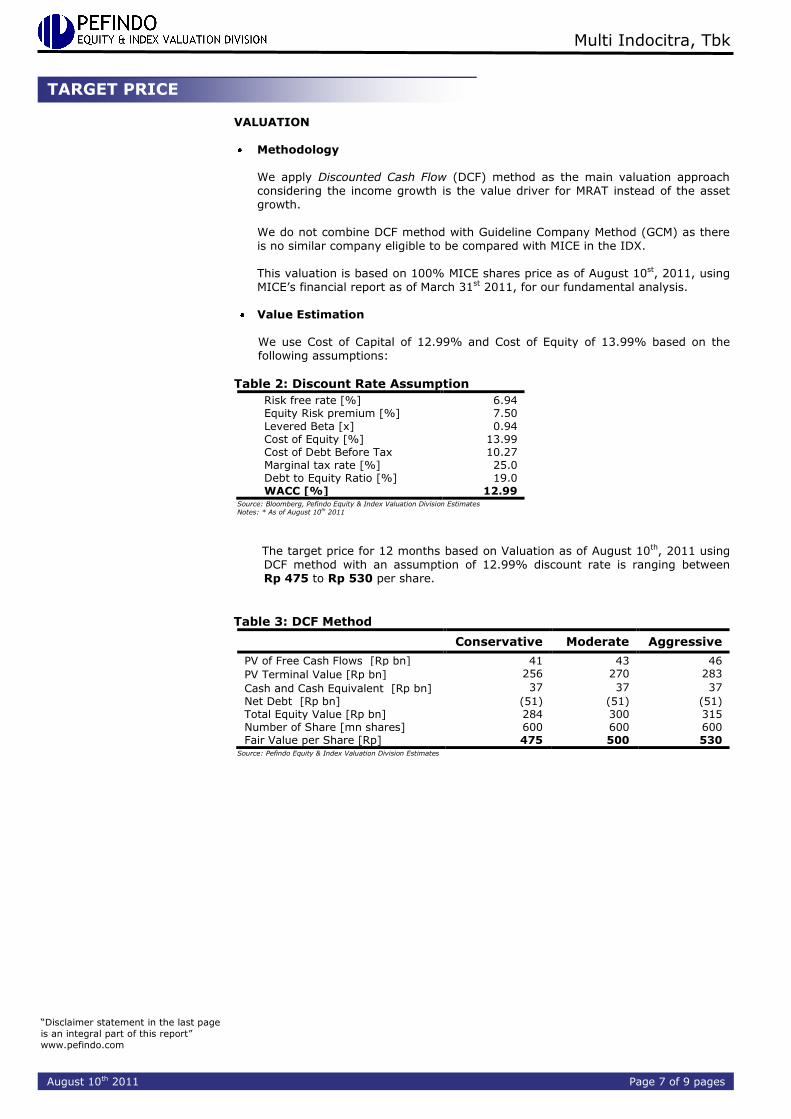

Metodologi

Kami mengaplikasikan metode discounted cash flow (DCF) sebagai metode penilaian utama dengan pertimbangan bahwa pertumbuhan pendapatan adalah merupakan faktor yang sangat mempengaruhi nilai (value driver) jika dibandingkan dengan pertumbuhan aset

Kami tidak mengkombinasikan perhitungan DCF ini dengan metode Guideline

Company Method (GCM) di dalam valuasi ini, disebabkan tidak terdapat peers yang benar-benar dapat diperbandingkan dengan MICE di Bursa Efek Indonesia.

Penilaian ini berdasarkan pada harga 100% saham MICE per 10 Agustus 2011, menggunakan laporan keuangan tanggal 31 Maret 2011 sebagai dasar dilakukannya analisa fundamental.

Estimasi Nilai

Kami menggunakan Cost of Capital sebesar 12,99% dan Cost of Equity sebesar 13,99 % berdasarkan asumsi-asumsi sebagai berikut:

Tabel 2: Asumsi Discount Rate

Risk free rate [%]* 6,94

Equity Risk premium [%]* 7,50

Levered Beta [x]* 0,94

Cost of Equity [%] 13,99

Cost of Debt Before tax 10,27

Marginal tax rate [%] 25,0

Debt to Equity Ratio 19,0

WACC [%] 12,99 Sumber: Bloomberg, Estimasi Pefindo Divisi Valuasi Saham & Indexing Catatan: * Per tanggal 10 Agustus 2011

Estimasi Target harga saham untuk 12 bulan berdasarkan posisi penilaian pada tanggal 10 Agustus 2011 dengan menggunakan metode DCF dan asumsi tingkat diskonto 12,99% adalah sebesar Rp 475 - Rp 530 per lembar saham.

Tabel 3: Metode DCF

Konservatif Moderat Agresif

PV of Free Cash Flows [Rp Miliar] 41 43 46

PV Terminal Value [Rp Miliar] 256 270 283

Cash and Cash Equivalent [Rp

Miliar]

37 37 37

Net Debt [Rp Miliar] (51) (51) (51)

Total Equity Value [Rp Miliar] 284 300 315

Number of Share [juta saham] 600 600 600

Fair Value per Share [ Rp] 475 500 530 Sumber: Estimasi Pefindo Divisi Valuasi Saham & Indexing

TARGET HARGA

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Multi Indocitra, Tbk

10 Agustus 2011 Halaman 8 dari 9 halaman

Tabel 4 : Laba Rugi

Laporan Laba Rugi

[dalam Rp Miliar] 2008 2009 2010 2011P 2012P

Penjualan 308 340 423 526 640

Harga Pokok Penjualan (157) (162) (194) (238) (295)

Laba Kotor 151 178 230 288 345

Beban Operasi (108) (134) (182) (229) (276)

Laba Operasi 43 44 48 58 69

Pendapatan [Beban]

lain-lain 3 5 (0)

(2) (3)

Laba Sebelum Pajak 46 49 48 56 67

Pajak 16 15 14 13 16

Hak Minoritas (6) (4) (6) (6) (6)

Laba Bersih 24 30 28 37 45

Sumber: PT Multi Indocitra Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

Tabel 5 : Neraca

Neraca

[dalam Rp Miliar] 2008 2009 2010 2011P 2012P

Aset

Aset Lancar

Kas dan Setara Kas 42 59 44 47 42

Piutang Usaha 58 57 97 119 145

Persediaan 63 59 71 85 105

Aset lain-lain 36 57 15 17 20

Total Aset Lancar 199 235 229 268 312

Aset Tetap 38 41 112 120 129

Aset lainnya 31 14 31 36 43

Total Aset Tetap 69 55 143 156 172

Total Aset 268 290 372 424 484

Kewajiban

Hutang Usaha 14 14 9 20 25

Pinjaman Jk. Pendek 3 4 30 32 32

Hutang yg jth tempo 1 1 8 8 11

Kewajiban lain-lain 12 14 21 25 30

Total Kewajiban jk. Pendek

30 33 68 85 98

Pinjaman Jk. Panjang 0 1 11 7 7

Pinjaman Jk. Panjang

lainnya 6 6 19 17 19

Total Kewajiban 36 39 86 76 78

Hak Minoritas 24 25 28 29 29

Total Ekuitas 208 226 257 294 340

Sumber: PT Multi Indocitra Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

2009 2010

P/E

PBV

1.12

1.13

1.14

1.15

1.16

1.17

1.18

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

2009 2010

ROA (%)

ROE (%)

TAT (%)

Tabel 6 : Rasio

Rasio 2008 2009 2010 2011P 2012P

Pertumbuhan [%]

Penjualan 26.27 10.59 24.34 24.18 21.72

Laba Operasi (6.24) 4.34 7.40 22.76 18.79

EBITDA (0.41) (2.03) 7.83 11.4 17.03

Laba Bersih (20.23) 26.75 (7.22) 32.03 21.67

Profitabilitas [%]

Marjin Laba Kotor 49.02 52.34 54.23 54.64 53.93

Marjin Laba Operasi 13.81 13.03 11.25 11.12 10.86

Marjin EBITDA 17.56 15.56 13.49 12.11 11.64

Marjin Laba Bersih 7.78 8.91 6.65 7.07 7.07

Solvabilitas [X]

Rasio Kewajiban Terhadap Ekuitas 0.17 0.17 0.33 0.35 0.35

Bunga Utang Terhadap Ekuitas 0.02 0.02 0.19 0.16 0.15

Rasio KewajibanTerhadap Aset 0.13 0.13 0.23 0.24 0.24

Likuiditas[X]

Rasio Lancar 6.70 7.17 3.40 3.16 3.19

Rasio Cepat 3.36 3.53 2.09 1.95 1.90

Sumber: PT Multi Indocitra Tbk, Estimasi Pefindo Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada halaman

akhir merupakan bagian tak

terpisahkan dari dokumen ini”

www.pefindo.com

Multi Indocitra, Tbk

10 Agustus 2011 Halaman 9 dari 9 halaman

DISCLAIMER

Laporan ini dibuat berdasarkan sumber-sumber yang kami anggap terpercaya dan dapat

diandalkan. Namun kami tidak menjamin kelengkapan, keakuratan atau kecukupannya. Dengan

demikian kami tidak bertanggung jawab atas segala keputusan investasi yang diambil berdasarkan laporan ini. Adapun asumsi, opini, dan perkiraan merupakan hasil dari pertimbangan internal kami per tanggal penilaian (cut-off date), dan kami dapat mengubah pertimbangan diatas sewaktu-waktu tanpa pemberitahuan terlebih dahulu. Kami tidak bertanggung jawab atas kekeliruan atau kelalaian yang terjadi akibat penggunaan laporan ini. Kinerja dimasa lalu tidak selalu dapat dijadikan acuan hasil masa depan. Laporan

ini bukan merupakan rekomendasi penawaran, pembelian atau menahan suatu saham tertentu. Laporan ini mungkin tidak sesuai untuk beberapa investor. Seluruh opini dalam laporan ini telah disampaikan dengan itikad baik, namun sewaktu-waktu dapat berubah tanpa pemberitahuan terlebih dahulu, dan disajikan dengan benar per tanggal diterbitkan laporan ini. Harga, nilai, atau pendapatan dari setiap saham Perseroan yang disajikan dalam laporan ini kemungkinan dapat lebih rendah dari harapan pemodal, dan pemodal juga mungkin mendapatkan

pengembalian yang lebih rendah dari nilai investasi yang ditanamkan. Investasi didefinisikan sebagai pendapatan yang kemungkinan besar diterima dimasa depan, namun nilai dari

pendapatan yang akan diterima tersebut kemungkinan besar juga akan berfluktuasi. Untuk saham Perseroan yang penyajian laporan keuangannya didenominasi dalam mata uang selain Rupiah, perubahan nilai tukar mata uang tersebut kemungkinan dapat menurunkan nilai, harga, atau pendapatan investasi pemodal. Informasi dalam laporan ini bukan merupakan pertimbangan pajak dalam mengambil suatu keputusan investasi.

Target harga saham dalam Laporan ini merupakan nilai fundamental, bukan merupakan Nilai Pasar Wajar, dan bukan merupakan harga acuan transaksi yang diwajibkan oleh peraturan perundang-undangan yang berlaku. Laporan target harga saham yang diterbitkan oleh Pefindo Divisi Valuasi Saham dan Indexing bukan merupakan rekomendasi untuk membeli, menjual, atau menahan suatu saham tertentu,

dan tidak dapat dianggap sebagai nasehat investasi oleh Pefindo Divisi Valuasi Saham dan Indexing yang behubungan dengan cakupan Jasa Pefindo kepada, atau kaitannya kepada, beberapa pihak, termasuk emiten, penasehat keuangan, pialang saham, investment banks, institusi keuangan dan perantara keuangan, dalam kaitannya menerima imbalan atau keuntungan lainnya dari pihak tersebut,

Laporan ini tidak ditujukan untuk pemodal tertentu dan tidak dapat dijadikan bagian dari tujuan investasi terhadap suatu saham dan juga bukan merupakan rekomendasi investasi terhadap suatu saham tertentu atau suatu strategi investasi. Sebelum melakukan tindakan dari hasil laporan ini, pemodal disarankan untuk mempertimbangkan terlebih dahulu kesesuaian situasi dan kondisi dan, jika dibutuhkan, mintalah bantuan penasehat keuangan. PEFINDO memisahkan kegiatan Valuasi Saham dengan kegiatan Pemeringkatan untuk menjaga

independensi dan objektivitas dari proses dan produk kegiatan analitis. PEFINDO telah menetapkan kebijakan dan prosedur untuk menjaga kerahasiaan informasi non-publik tertentu yang diterima sehubungan dengan proses analitis. Keseluruhan proses, metodologi dan database yang digunakan dalam penyusunan Laporan Target Harga Referensi Saham ini secara keseluruhan adalah berbeda dengan proses, metodologi dan database yang digunakan PEFINDO dalam melakukan pemeringkatan.

Laporan ini dibuat dan disiapkan Pefindo Divisi Valuasi Saham & Indexing dengan tujuan untuk meningkatkan transparansi harga saham yang tercatat di Bursa Efek Indonesia. Laporan ini

juga bebas dari pengaruh tekanan atau paksaan dari Bursa maupun Perseroan yang dinilai. Pefindo Divisi Valuasi Saham & Indexing akan menerima imbalan sebesar Rp.20.000.000, - dari Bursa Efek Indonesia untuk 2 (dua) kali pelaporan per tahun. Untuk keterangan lebih lanjut, dapat mengunjungi website kami di http://www.pefindo.com

Laporan ini dibuat dan disiapkan oleh Pefindo Divisi Valuasi Saham dan Indexing. Di Indonesia Laporan ini dipublikasikan pada website kami dan juga pada website Bursa Efek Indonesi a.

Page 1 of 9 pages

Contact: Equity & Index Valuation Division Phone: (6221) 7278 2380 [email protected] “Disclaimer statement in the last page is an

integral part of this report”

www.pefindo.com

Multi Indocitra, Tbk Secondary Report

Equity Valuation

August 10th, 2011

Target Price

Low High

475 530

Baby Care Product

Historical Chart

2000

2500

3000

3500

4000

4500

200

300

400

500

600

700

800

7/15/2010 8/27/2010 10/15/201011/29/2010 1/13/2011 2/28/2011 4/11/2011 5/25/2011 7/8/2011

MICE IHSG

Source : Bloomberg

Stock Information Rp

Ticker code MICE

Market price as of August 10th , 2011 430

Market price – 52 week high 710

Market price – 52 week low 330

Market cap – 52 week high (bn) 426

Market cap – 52 week low (bn) 196

Market Value Added & Market Risk

-250

-200

-150

-100

-50

0

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

March-10 March-11

M

V

A

M

a

r

k

e

t

R

i

s

k

MVA Market Risk

Stock Valuation Last Current

High 900 530

Low 810 475

Shareholders (%)

PT Buana Graha Utama 60.44

Public (ownership < 5%) 27.05

Haiyanto 6.50

Surono Subekti 6.01

Sustaining Transformation

PT. Multi Indocitra, Tbk ("MICE") was established on January 11th 1990 with objectives of distributing health care products and accessories for baby

needs, pregnant women, and breast feeding mothers and skin care products. The products are manufactured in a modern factory located in Cikande, Banten. As of December 31 2010, MICE has around 1,046 employees. Accessories for baby are produced by its subsidiary, PT. Pigeon Indonesia, which produces feeding bottle, silicon nipple under the brand name of “Pigeon”. While, its skin care products are produced by its subsidiary, PT. Multielok Cosmetic, which produces powder, shampoo, liquid soap for babies, kids and teenagers. In line with its business opportunity, MICE has developed new business line namely Compact Fluorescent Lamp (CFL) namely “HORI”, which has been commercially distributed in most areas of Indonesia since middle 2010.

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multi Indocitra, Tbk

August 10th 2011 Page 2 of 9 pages

Target Price Adjustment We have made some adjustments to our previous forecast and adjust our Target Price to the range of Rp 475 – Rp 530 per share, based on the following considerations: Superb performance in 2010, MICE successfully booked significant sales

growth of 24,34% compared to the previous year which grew by 10.59% YoY. This growth is due to the increased of sales volume on some of MICE’s products. Coupled with a new business line of compact fluorescent lamp (CFL) namely “HORI”, which starts to contribute around 7.76% of MICE’s total sales in the first of year of its distribution.

The increasing of income per capita in Indonesia will drive consumers spending into more various branded product. These changes occur as the increase in Gross Domestic Product (GDP) in Indonesia reach 28% YoY to US$ 3,005 per capita in 2010, from US$ 2,350 per capita in 2009.

The increasing population of Indonesia, which grow by 16% in the last 10 years, or reach 238 mn people in 2010, from only 205 mn people in 2000. This growth becomes a trigger of MICE sales which continue to rise. As recorded from 2008 – 2010, MICE booked sales growth of CAGR 17%.

Assumption risk free rate, equity premium, and beta which reach 6.94%, 7.50%, and 0.94x.

Driven by Economic Growth The realization of GDP (Gross Domestic Product) growth up to 1Q2011 reached 6.5%, better than previous year in the same period which was 5.7%, and it is predicted to rise along 2011. As a result, the demand for some products such as baby care products will increase. Proven by MICE performance, the total sales in 1Q2011 grew by 14% or reach Rp 105 bn, better than the same period last year which was Rp 92 bn.

New Business Line for Growth Acceleration In 2010, MICE has developed new business line namely Compact

Fluorescent Lamp (CFL) under the brand name of “HORI”. Currently MICE has more than 38 “HORI” distributors, which scatter in Java, Sumatera and Kalimantan areas. In the first year of its distribution, MICE booked Rp 33 bn sales of “HORI” or contribute around 7.76% of total MICE’s sales. In line with the increasing demand of lamp in 2011, we are confidence that “HORI” can give more contribution to MICE sales. Besides that, MICE also distribute baby bottle contains of free Bisphenol A (BPA) this year. From May – July 2011, sales of BPA-free bottle has reached Rp 3.5 bn. It is estimated to grow on the coming years since bottle is one of products of MICE that become market leader.

Business Prospect

Population growth and rising purchasing power of consumers due to better economic condition contribute significantly to the sales of baby care products. While the new MICE business line, “HORI”, is expected to book sales growth of 58%YoY in 2011 in line with the increasing demand for domestic CFL. Augmented with the launching of baby bottle containing free Bisphenol A (BPA) this year, in which bottle is a market leader for baby product, we believe that MICE’s revenue can grow by 24.18% in 2011, or reach Rp 526 bn, and grow by CAGR 25% during 2011 – 2015 periods. Table 1: Performance Summary

2008 2009 2010 2011P 2012P

Revenue [Rp bn] 308 340 423 526 640

Pre-tax Profit [Rp bn] 46 49 47 56 67

Net Profit [Rp bn] 24 30 28 37 45

EPS [Rp] 40 51 47 62 75

EPS Growth [%] (20) 27 (7) 29 21

P/E [x] 4.0 5.1 8.6 6,9* 5,7*

PBV [x] 0.5 0.7 0.9 0,9* 0,8*

Source:PT Multi Indocitra Tbk., Pefindo Equity & Index Valuation Estimates * Based on the MICE’s share price as of August 10

st 2011 – Rp 430 / share

INVESTMENT PARAMETER

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multi Indocitra, Tbk

August 10th 2011 Page 3 of 9 pages

Baby Products Sales Keep Increasing The actual sales of MICE in 2010 that reach Rp 423 bn was exceeding our previous projection, which was Rp 410 bn. It is due to sales growth in some baby products in

line with growing population in Indonesia. MICE with its main products feeding bottle and silicon nipple grow by 24% YoY to become Rp 164 bn in 2010. Meanwhile, baby toiletries depict the highest growth with 139% YoY to reach Rp 41 bn. With growing economic condition and huge population in Indonesia, we believe MICE can maintain its growth in the future.

Supported by Population Growth Indonesia population continues to grow each year. From the last 10 years, the population of Indonesia grew by 16%, from 205 mn people in 2000, becomes 238 mn people in 2010. The huge number of population is important factor for MICE to gain more sales. As information, Indonesia has the largest population in Southeast Asia. Augmented with the increasing people purchasing power in Indonesia, we believe that MICE’s sales will keep rising.

Figure 2: The Number of Indonesian Population

(in mn)

147

179

205

238

0

50

100

150

200

250

1980 1990 2000 2010

Indonesia Population

1980

1990

2000

2010

Source :Central Bureau of Statistics, Pefindo Equity & Index Valuation Division

Market Leader for Baby Products In 2005-2010, MICE’s feeding baby bottle and silicon nipple, namely “Pigeon”, accounted for about 52% of national market share. In terms of sales contribution, feeding bottle and silicon nipple contributes as much as 38.68% from MICE’s total sales in 2010. This contribution is estimated to grow in line with improvement of economic condition in Indonesia. With the support of good quality products, modern production facilities, wide coverage and integrated distribution networks, we are confident that MICE can maintain its position as a market leader in baby products.

Figure 1 : MICE Major Products Sales

(in Rp bn)

0

20

40

60

80

100

120

140

160

180

2006 2007 2008 2009 2010

81 84

108

132

164

6 7 12 17

41

Bottle and Silicon Nipple

Baby Toiletries

Source : PT Multi Indocitra tbk. Pefindo Equity and Index Valuation Division

BUSINESS INFORMATION

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multi Indocitra, Tbk

August 10th 2011 Page 4 of 9 pages

Baby Care Industry Outlook in 2011: Remains Prospective

We predict in 2011, sales of baby care products will increase as higher consumer spending and the population that continues to grow. In fact, during the past 3

years MICE is able to record sales growth as 17% CAGR. Many of imported baby and toddler products from China, America and Europe does not inhibit sales of local product due to that imported product targeting high-class consumer. While the competition in the middle-up market has not been rigorous. Only through

qualified innovation and promotion that will dominate market share in this industry. Always Maintain the Quality of Its Products One important factor that makes MICE retain the biggest market share in its industry is due to the quality of its products. The manufacturing of Pigeon products, which is carried out by the subsidiary and affiliated company have been carefully checked for its quality to make sure that the quality standard which is stipulated by Pigeon Corporation of Japan are followed. PT. Multielok Cosmetics and PT. Pigeon Indonesia have obtained some certifications, namely:

PT. Multielok Cosmetics: Certification AS/NZS ISO 9001:2000 from SAI

Global Limited Australia, Certification for Good Manufacturing Process (GMP) from the Indonesian Medicines and Food Supervisory Body

PT. Pigeon Indonesia: Certification AS/NZS ISO 9001:2000 from SAI Global Limited Australia.

Several Awards Reflect MICE Achievement During its existence in baby care industry, MICE always distribute high-quality products to the customer. Through that commitment, MICE successfully achieved some awards in many categories in 2010 Those awards are: Awards from Marketing

Magazine for Baby Milk Bottle and Baby Dining Set Category in Recognition of Outstanding Achievement in Building the Top Brand and Reader’s Choice Award from Mother and Baby Magazine for Baby Milk and Silicon Nipple, Bottle Warmer, Bottle Sterilization, Breast Pad, Breast Pump, Feeding Set and Pacifier categories. Diversification of Baby Feeding Bottles that Contains of Free Bisphenol A (BPA) MICE starts to distribute its new diversification product namely BPA-free bottle this year. It is produced to fulfill the increasing demand of baby products due to the rising demand of BPA-free bottle. As the market leader in baby bottle, MICE estimates to take no longer time to introduce it to society. From May – July 2011, sales of BPA-free

bottle has reached Rp 3.5 bn. By continuously doing qualified promotion, we believe the sales of BPA-free bottle can provide higher contribution to MICE sales in the future.

Threat from China Does Not Inhibit HORI sales The number of import products from China to Indonesia has continued to rise. One of them is lamp. In 1Q2011, the imported CFL products from China reach 45.78 mn units, rise by 14.74% compare to the same period last year. It is caused by the increasing of national need in line with free-power program from State Electrical Company. Moreover, lamp consumption in 2011 is estimated reach 260 mn units, rise by 30% from 2010 which was only 200 mn units. In 2010, the import number for CFL product from China was around 60% from total consumption of national lamp or

reaches 161.25 mn units. Nevertheless, Chinese product threat does not significantly affect “HORI” sales. It is proven since “HORI” brand that has been started to market in middle of 2010, successfully contributed as 7.76% of the total MICE sales in 2010, or as much as Rp 33 bn. Meanwhile, currently HORI has more than 38 distributors, which scatter across Java, Sumatera and Kalimantan areas. In addition, “HORI” also has certification from Indonesian National Standard, which certifies the quality of “HORI”. Moreover “HORI” brand is on the top rank in term of quality according to SWA magazine version. With appropriate and intensive marketing strategy, we are confidence the sales of “HORI” in 2011 will reach Rp 52 bn.

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multi Indocitra, Tbk

August 10th 2011 Page 5 of 9 pages

Appropriate Marketing Strategy to Gain Potential Areas In order to maintain customer’s loyalty to its products, MICE has promoted to various hospitals to socialize the “Pigeon” products to the society. MICE is also

active in sponsoring various social activities and business activities. The distributors are actively involved in these marketing activities in their area. This proved to be effective in increasing MICE sales. As recorded, MICE sales always rise every year. From 2008 to 2010, MICE booked sales growth of CAGR 17%. This growth is possible to increase since there are some potential places in Indonesia, such as Sumatera which has the highest population growth rate of 5% per year, followed by Java 2.79% and Bali 2.5%.

Figure 3: Indonesia CFL Consumption

90

120

180200

260

0

50

100

150

200

250

300

2007 2008 2009 2010 2011P

In m

n u

nit

s

CFL Consumption

CFL Consumption

Source : Aperlindo,. Pefindo Equity & Index Valuation Division

Figure 4 : Indonesia CFL Production

0

5

10

15

20

25

30

35

40

45

2008 2009 2010

24

4539

(In

mn

Un

its)

CFL Production

CFL Production

Source : Aperlindo,. Pefindo Equity & Index Valuation Division

Figure 5: HORI Sales

33

52

60

0

10

20

30

40

50

60

70

2010 2011P 2012P

Rp

bn

HORI Sales

2010

2011P

2012P

Source : PT Multi Indocitra Tbk, Pefindo Equity & Index Valuation Division

Estimates

Figure 6: Imported Lamp from China

34

36

38

40

42

44

46

1Q2010 1Q2011

39.03

45.78

In m

n u

nit

s

Imported Lamp from China

Imported Lamp fromChina

Source : Aperlindo,. Pefindo Equity & Index Valuation Division

Figure 7 : Population Growth Rate in Indonesia

(in %)

5%

2.79%

2.15%

Sumatera

Java

Bali

Source : Central Bureau of Statistics. Pefindo Equity & Index Valuation Division

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multi Indocitra, Tbk

August 10th 2011 Page 6 of 9 pages

MICE Business Prospect Population growth and rising purchasing power of consumers due to better economic condition contribute significantly to the sales of baby care products. While the new MICE business line, “HORI”, is expected to book sales growth of 58%YoY in 2011 in line with the increasing demand for domestic CFL. Augmented with the launching of baby bottle containing free Bisphenol A (BPA) this year, in which bottle is a market leader for baby product, we believe that MICE’s revenue can grow by 24.18% in 2011, or reach Rp 526 bn, and grow by CAGR 25% during 2011 – 2015 periods.

Figure 8 : MICE Sales Growth

423

506573

654

753

875

0

100

200

300

400

500

600

700

800

900

1000

2010 2011 2012 2013 2014 2015

In R

p b

n

2010

2011

2012

2013

2014

2015

Source: PT Multi Indocitra Tbk, Pefindo Equity & Index Valuation Division Estimates

Strength Weakness

Market leader in some baby products,

such as bottle and silicon nipple. High quality product with International

Certification Standard. Directly supervised by Pigeon

Corporation in Japan. Start to produce BPA-free bottle to fulfill

medium-high customer need.

Dependence on its main principal

that is Pigeon Corporation in Japan.

Rely on imported raw material for lamp.

Opportunity Threat

Indonesian GDP per capita that keep

growing. The demand for Compact Fluorescent

Lamp (CFL) continue to rise. The increasing population in Indonesia.

ACFTA might cause tighter

competition with lower price on imported product.

Fraudulent act by other parties. Low entry barrier.

SWOT ANALYSIS

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multi Indocitra, Tbk

August 10th 2011 Page 7 of 9 pages

VALUATION

Methodology We apply Discounted Cash Flow (DCF) method as the main valuation approach considering the income growth is the value driver for MRAT instead of the asset growth.

We do not combine DCF method with Guideline Company Method (GCM) as there is no similar company eligible to be compared with MICE in the IDX. This valuation is based on 100% MICE shares price as of August 10st, 2011, using MICE’s financial report as of March 31st 2011, for our fundamental analysis.

Value Estimation

We use Cost of Capital of 12.99% and Cost of Equity of 13.99% based on the following assumptions:

Table 2: Discount Rate Assumption

Risk free rate [%] 6.94 Equity Risk premium [%] 7.50

Levered Beta [x] 0.94 Cost of Equity [%] 13.99 Cost of Debt Before Tax 10.27 Marginal tax rate [%] 25.0 Debt to Equity Ratio [%] 19.0 WACC [%] 12.99

Source: Bloomberg, Pefindo Equity & Index Valuation Division Estimates Notes: * As of August 10

th 2011

The target price for 12 months based on Valuation as of August 10th, 2011 using DCF method with an assumption of 12.99% discount rate is ranging between Rp 475 to Rp 530 per share.

Table 3: DCF Method

Conservative Moderate Aggressive

PV of Free Cash Flows [Rp bn] 41 43 46

PV Terminal Value [Rp bn] 256 270 283

Cash and Cash Equivalent [Rp bn] 37 37 37

Net Debt [Rp bn] (51) (51) (51) Total Equity Value [Rp bn] 284 300 315 Number of Share [mn shares] 600 600 600 Fair Value per Share [Rp] 475 500 530

Source: Pefindo Equity & Index Valuation Division Estimates

TARGET PRICE

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multi Indocitra, Tbk

August 10th 2011 Page 8 of 9 pages

Table 4 : Income Statement

Income Statement [Rp bn] 2008 2009 2010 2011P 2012P

Sales 308 340 423 526 640

COGS (157) (162) (194) (238) (295)

Gross Profit 151 178 230 288 345

Operating Expense (108) (134) (182) (229) (276)

Operating Profit 43 44 48 58 69

Other Income (Charges) 3 5 (0) (2) (3)

Pre-tax Profit 46 49 48 56 67

Tax 16 15 14 13 16

Minority Interest (6) (4) (6) (6) (6)

Net Profit 24 30 28 37 45

Source: PT Multi Indocitra Tbk., Pefindo Equity & Index Valuation Division Estimates

Table 5 : Balance Sheet

Balance Sheet [Rp bn] 2008 2009 2010 2011P 2012P

Assets

Current Assets

Cash and cash equivalents 42 59 44 47 42

Receivables 58 57 97 119 145

Inventory 63 59 71 85 105

Other Assets 36 57 15 17 20

Total Current Assets 199 235 229 268 312

Fixed Assets 38 41 112 120 129

Other Assets 31 14 31 36 43

Total Fixed Assets 69 55 143 156 172

Total Assets 268 290 372 424 484

Liabilities

Trade payables 14 14 9 20 25

Short-term liabilities 3 4 30 32 32

Debt Maturity 1 1 8 8 11

Other liabilities 12 14 21 25 30

Total short-term

liabilities 30 33 68 85 98

Long-term liabilities 0 1 11 7 7

Other Long-term liabilities 6 6 19 17 19

Total Liabilities 36 39 86 76 78

Minority Interest 24 25 28 29 29

Total Equity 208 226 257 294 340

Source: PT Multi Indocitra Tbk., Pefindo Equity & Index Valuation Division Estimates

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

2009 2010

P/E

PBV

1.12

1.13

1.14

1.15

1.16

1.17

1.18

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

2009 2010

ROA (%)

ROE (%)

TAT (%)

Table 6 : Key Ratio

Ratio 2008 2009 2010 2011P 2012P

Growth [%]

Sales 26.27 10.59 24.34 24.18 21.72

Operating Profit (6.24) 4.34 7.40 22.76 18.79

EBITDA (0.41) (2.03) 7.83 11.4 17.03

Net Profit (20.23) 26.75 (7.22) 32.03 21.67

Profitability [%]

Gross Margin 49.02 52.34 54.23 54.64 53.93

Operating Margin 13.81 13.03 11.25 11.12 10.86

EBITDA Margin 17.56 15.56 13.49 12.11 11.64

Net Margin 7.78 8.91 6.65 7.07 7.07

Solvability [X]

Debt to Equity 0.17 0.17 0.33 0.35 0.35

Interest bearing debt to equity 0.02 0.02 0.19 0.16 0.15

Debt to Asset 0.13 0.13 0.23 0.24 0.24

Liquidity [X]

Current Ratio 6.70 7.17 3.40 3.16 3.19

Quick Ratio 3.36 3.53 2.09 1.95 1.90

Source: PT Multi Indocitra Tbk., Pefindo Equity & Index Valuation Division Estimates

“Disclaimer statement in the last page

is an integral part of this report”

www.pefindo.com

Multi Indocitra, Tbk

August 10th 2011 Page 9 of 9 pages

DISCLAIMER

This report was prepared based on the trusted and reliable sources. Nevertheless, we do not guarantee its completeness, accuracy and adequacy. Therefore we do not responsible of any investment decision making based on this report. As for any assumptions, opinions and predictions were solely our internal judgments as per reporting date, and those judgments are subject to change without further notice. We do not responsible for mistake and negligence occurred by using this report. Last performance could not always be used as reference for future outcome. This report is not an offering recommendation, purchase or holds particular shares. This report might not be suitable for some investors. All opinion in this report has been presented fairly as per issuing date with good intentions; however it could be change at any time without further notice. The price, value or income from each share of the Company stated in this report might lower than the investor expectation and investor might obtain lower return than the invested amount. Investment is defined as the probable income that will be received in the future; nonetheless such return may possibly fluctuate. As for the Company which its share is denominated other than Rupiah, the foreign exchange fluctuation may reduce the value, price or investor investment return. This report does not contain any information for tax consideration in investment decision making. The share price target in this report is a fundamental value, not a fair market value nor a transaction price reference required by the regulations. The share price target issued by Pefindo Equity & Index Valuation Division is not a recommendation to buy, sell or hold particular shares and it could not be considered as an investment advice from Pefindo Equity & Index Valuation Division as its scope of service to, or in relation to some parties, including listed companies, financial advisor, broker, investment bank, financial institution and intermediary, in correlation with receiving rewards or any other benefits from that parties. This report is not intended for particular investor and cannot be used as part of investment objective on particular shares and neither an investment recommendation on particular shares or an investment strategy. We strongly recommended investor to consider the suitable situation and condition at first before making decision in relation with the figure in this report. If it is necessary, kindly contact your financial advisor.

PEFINDO keeps the activities of Equity Valuation separate from Ratings to preserve independence and objectivity of its analytical processes and products. PEFINDO has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process. The entire process, methodology and the database used in the preparation of the Reference Share Price Target Report as a whole is different from the processes, methodologies and databases used PEFINDO in doing the rating. This report was prepared and composed by Pefindo Equity & Index Valuation Division with the objective to enhance shares price transparency of listed companies in Indonesia Stock Exchange (IDX). This report is also free of other party’s influence, pressure or force either from IDX or the listed company which reviewed by Pefindo Equity & Index Valuation Division. Pefindo Equity & Index Valuation Division will earn reward amounting to Rp 20 mn from IDX for issuing report twice per year. For further information, please visit our website at http://www.pefindo.com This report is prepared and composed by Pefindo Equity & Index Valuation Division. In Indonesia, this report is published in our website and in IDX website.

Related Documents