© Copyright 2016 by K&L Gates LLP. All rights reserved. Jacob Ghanty, Partner, K&L Gates LLP Payment Services and Money Transfer in the FinTech Space - What is next?

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© Copyright 2016 by K&L Gates LLP. All rights reserved.

Jacob Ghanty, Partner, K&L Gates LLP

Payment Services and Money Transfer in the FinTech Space - What is next?

OVERVIEW Regulatory Issues in Payments and FinTech –

Jacob Ghanty Block Chain and Key Trends Within the

Payments Systems Space – Anthony Watson Shape of Things to Come: Digital/Mobile

Payments, Banking & Commerce – Jean-Stephane Gourevitch

Panel discussion

klgates.com 2

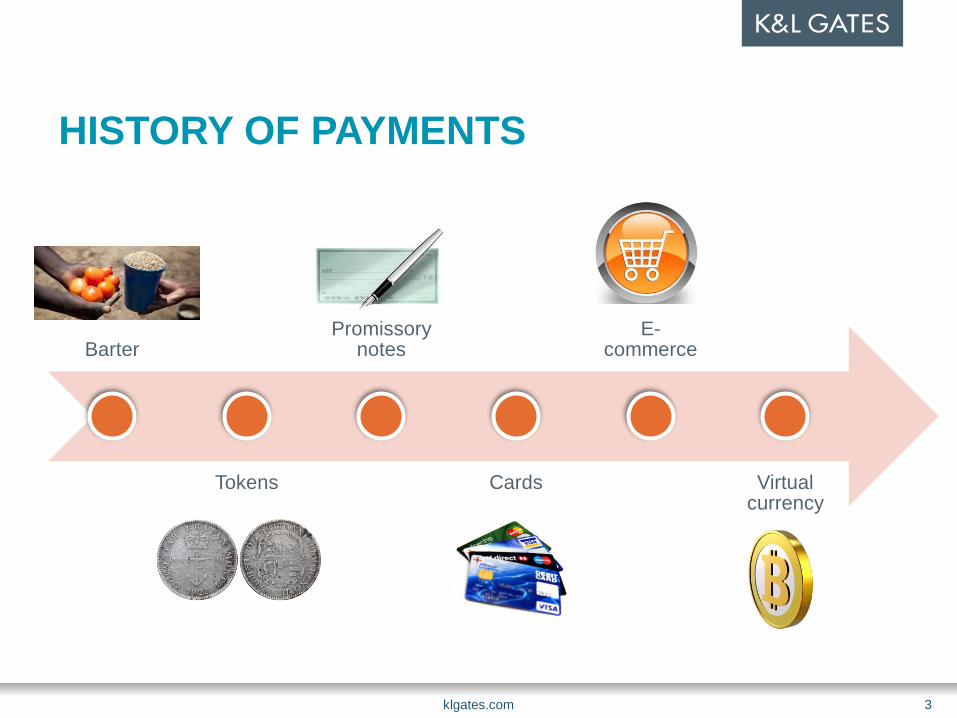

HISTORY OF PAYMENTS

Barter

Tokens

Promissory notes

Cards

E-commerce

Virtual currency

klgates.com 3

INDUSTRY OVERVIEW £75 trillion payments sector in UK Diverse range of players including-

Clearing banks Challenger banks Infrastructure (e.g. Bacs, CHAPS) Card companies Bill payment firms Money transmitters Prepaid card providers

Technology and regulation as drivers of change

klgates.com 4

NEW PAYMENT SERVICES DIRECTIVE - PSD 2

What? • New European legislation governing payment services

When?

• Published in Official Journal on 23 December 2015 • Implementation by 13 January 2018

What’s new?

• New types of payment service: • Payment initiation services • Account information services

Interesting points

• Extra territorial scope • Exemptions narrowed

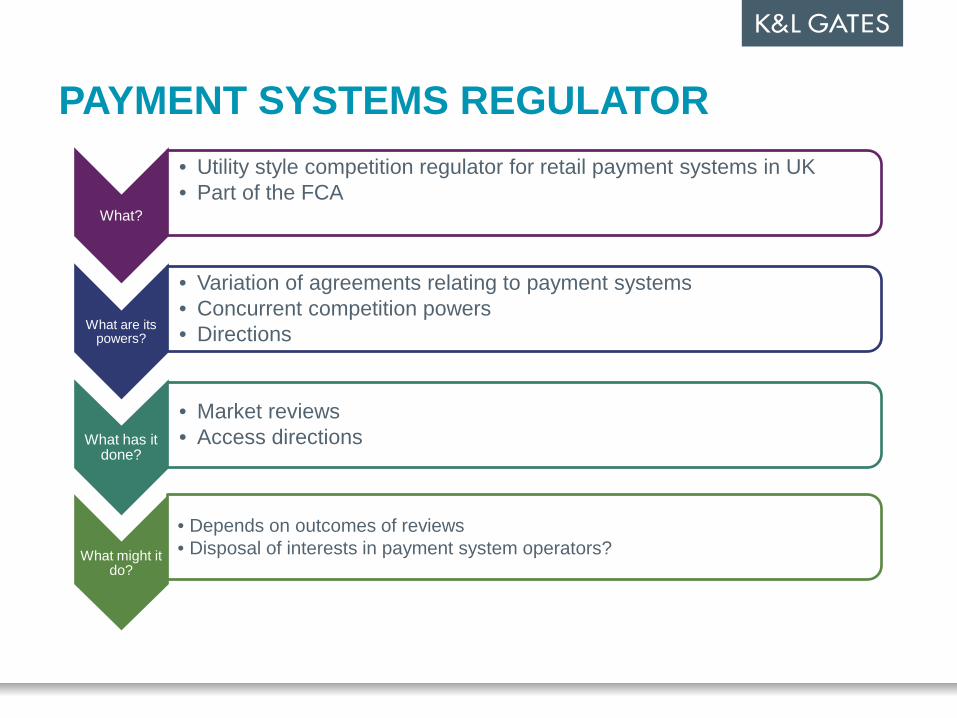

PAYMENT SYSTEMS REGULATOR

What?

• Utility style competition regulator for retail payment systems in UK • Part of the FCA

What are its powers?

• Variation of agreements relating to payment systems • Concurrent competition powers • Directions

What has it done?

• Market reviews • Access directions

What might it do?

• Depends on outcomes of reviews • Disposal of interests in payment system operators?

OUTLOOK: EMERGING THEMES FOR 2016

Emerging Themes

2016

Cyber risk

Competition-based

remedies

Open Banking Standard

4th Money Laundering Directive

Consolidation in FinTech

New entrants to banking

market

Build up to PSD2

© Copyright 2016 by K&L Gates LLP. All rights reserved.

Anthony Watson, President & Chief Executive Officer, Uphold Inc.

Block Chain and Key Trends Within the Payments Systems Space

Shape of things to come:

Digital/Mobile Payments, Banking & Commerce Seminar on Payment Services and Money Transfer

Jean-Stéphane Gourévitch CEO and Founder, Mobile Convergence Ecosystems Ltd. &

Business Development, Europe, Matchi.biz

GOOD EVENING !

Summary

• Mobile/digital payments a fundamental building block for digital/mobile banking and commerce but also financial inclusion

• Overall ecosystem is becoming much more complex integrating mobile money/payments, mobile banking and mobile commerce

• But also much more competitive through new entrants on payments markets and regulatory pressures

• It develops both on horizontal and vertical ways (general payment systems/products and industry verticals specific systems/products) and adapt to customer/user requirements

1. Some figures and data

EXPONENTIAL GROWTH OF USERS AND TRANSACTIONS

Sources: Pymnts.com; Gartner, Juniper Research, GSMA; Pew Research

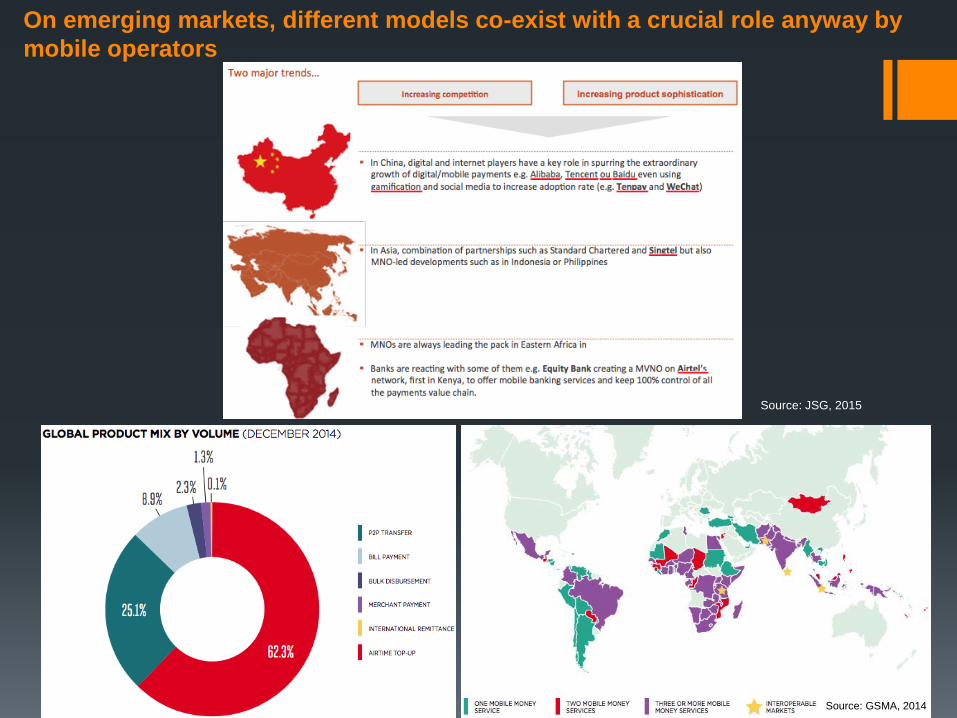

On emerging markets, different models co-exist with a crucial role anyway by mobile operators

Source: GSMA, 2014

Source: JSG, 2015

ANOTHER VISION…. World population per continent…

SOURCE: The Guardian and Visa, November 2015

The world per bank accounts held in banks/financial institutions

The world per mobile money penetration

The world per use of online shopping/payments

2. Digital and mobile payments developments in emerging and developed countries

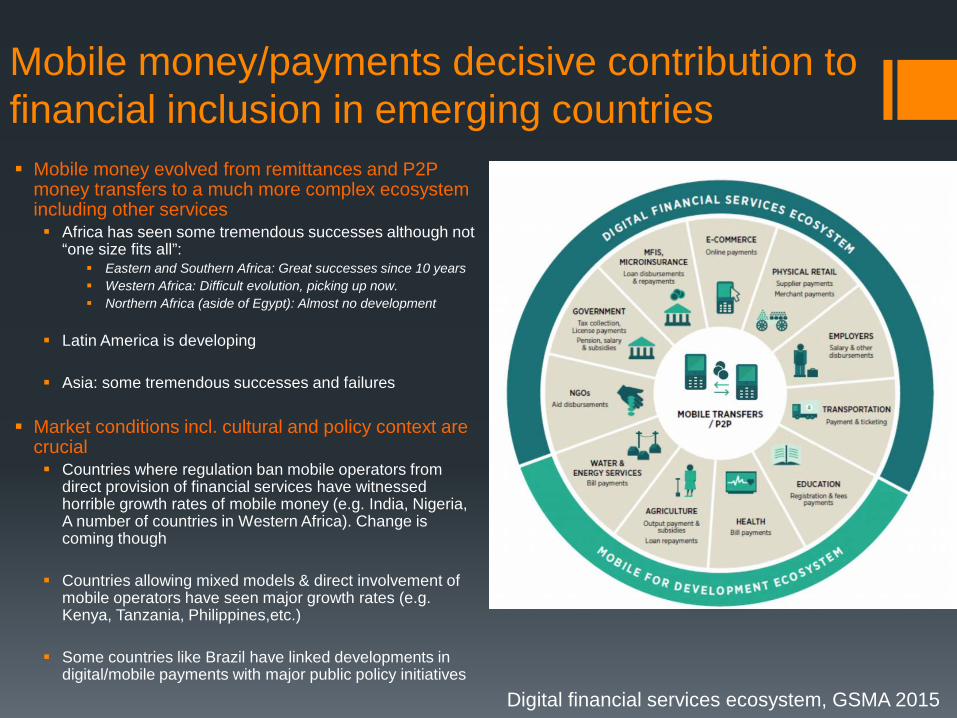

Mobile money/payments decisive contribution to financial inclusion in emerging countries Mobile money evolved from remittances and P2P

money transfers to a much more complex ecosystem including other services Africa has seen some tremendous successes although not

“one size fits all”: Eastern and Southern Africa: Great successes since 10 years Western Africa: Difficult evolution, picking up now. Northern Africa (aside of Egypt): Almost no development

Latin America is developing Asia: some tremendous successes and failures

Market conditions incl. cultural and policy context are crucial Countries where regulation ban mobile operators from

direct provision of financial services have witnessed horrible growth rates of mobile money (e.g. India, Nigeria, A number of countries in Western Africa). Change is coming though

Countries allowing mixed models & direct involvement of

mobile operators have seen major growth rates (e.g. Kenya, Tanzania, Philippines,etc.)

Some countries like Brazil have linked developments in

digital/mobile payments with major public policy initiatives

Digital financial services ecosystem, GSMA 2015

Mobile Payments growing in developed country, with an increasingly competitive ecosystem and some of this growth driven by contactless/M-payments in mass transit, mobile commerce, etc.

Source: JSG, 2015

• Increasingly part of broader products • e.g. mobile banking, mobile wallets

• Specialisation for industry verticals: • Transportation • Hospitality, Restaurants, Bars; • Healthcare & wellness; • Education; • Energy

• Mobile Payments are growing and the use of cash decreasing

• Retail & mobile commerce Increasingly engine for growth &

integration of mobile payments & other facilities

• Major retailers use digital/mobile technologies to not only improve shop floor and checkout management.

• Increasingly essential to cover the whole customer shopping journey before, during and after visiting a shop/store.

• Digital/Mobile wallets combining payments, loyalty, coupons redeeming functions.

A good example of competition in the remittances/payments market

The use and inclination to use m-Payments & m-Payments apps in particular for shopping is growing in developed countries

Source: ING, 2015

Financial inclusion is a real problem in developed countries too…

• Solutions like Compte Nickel in France has shown that addressing the unbanked and Excluded markets with proper solutions is viable commercially (from 0 to 225,000 customers in 1 year) even in developed countries • Real concerns of impacts (and legitimacy) of bank de-risking e.g. money transfers/ remittances. Is it really because of regulation and risks or …to smother a market banks are losing

Source: Financial Inclusion Commission, UK, March 2015

3. The Regulatory context

Policy & Regulation have key roles as enabler or obstacle to market developments

Governments, Regulatory Authorities, Competition Authorities, Standardisation bodies increasingly active

Market and dominance issues around agents networks exclusivity in Eastern Africa leading competition/regulatory authorities to act (e.g. Kenya, Zimbabwe, Tanzania, Uganda)

Competition Actions and investigations in the EU (ECJ decision on MasterCard, 11 September 2014, new investigations on Merchant fees) and MasterCard and Visa continuous legal actions in the US

Interoperability and proprietary standards concerns in both emerging and developed countries EU Regulation to cap Multilateral Interchange Fees and change card schemes rules entering into force Push to increase speed in faster payments developments (US, etc.)

New specific payments/financial services legislations opening the markets: Review of the Payment Service Directive 2007 (PSD2 adopted) and soon the E-Money Directive 2009 Regulation on Payments Banks in India, 2014 and 2015 New strategic review of the payments sector in France New developments in the UK New Payment and E-Money Regulations in Turkey, 2014 and 2015 Regulation from People’s Bank of China on mobile payments, 2015

Partnerships are also on the rise either intra or inter sectors, and Competition authorities are increasingly acting

Oscar/Weve case in the UK, Telefonica/BBVA/Caixa in Spain in the past few years, etc. Creation of the Polish Payment Standard (PSP) by the competition authority and the Financial regulator in 2014 Acquisition of PSPs by banks (Leetchi/MangoPay by Arkea), or stakes in challenger or neo banks by incumbent

banks (Atom Bank/BBVA, BBVA/Simple)

Convergence of relevant legislations/regulatory authorities Creation of the Payment Systems Regulator (PSR) in the UK Increased cooperation between digital/telecom regulators, financial services regulators and competition

authorities (e.g. EU, Kenya, Tanzania, Ghana, India, Bangladesh, Philippines)

The EU Regulation on Interchange Fees

19 May 2015, Regulation on Interchange Fees for Card-Based Payment Transactions published in the EU Official Journal. It applies caps on interchange fees charged by cardholders’ banks to merchants’ banks every time a consumer makes a card based purchase.

8 June 2015: Entry into force

Ban on “steering rules” comes into force

9 December 2015 New interchange fee caps come into force

- Debit card transactions – Domestic: 0.2% of the value of the transaction or a per transaction fee of no more than €0.05 with a 0.2% cap and International 0.2% of the value of the transaction

-Credit card transactions – Domestic: 0.3% of the value of the transaction but Member States may define a lower cap and International: 0.3% of the value of the transaction

- “Universal”* card transactions – 0.2% of the value of the transaction or a per transaction fee of no more than €0.05 with a 0.2% cap and 0.3% of the value of the transaction for those transactions treated as credit card transactions

Territorial restrictions within the EU prohibited Payee’s payment service provider (PSP) must provide the payee with breakdown of charges for card transaction

incl. interchange fee and Merchant Services charge (MSC)

9 June 2016 Payment card schemes and processors must be independent, and cannot present bundled prices for both services Any rules hindering co-badging of two or more payment brands or applications prohibited Acquiring PSPs must offer and charge MSCs to the payees on an “unblended” basis “Honour all cards” rule is abolished

9 December 2016 Member States may no longer define a share of no more than 30% of the domestic payment transactions for

“universal” cards to be treated as credit card transactions

9 December 2018 Three party payment card schemes are no longer exempted from the Regulation

9 December 2020 Member States are no longer allowed to permit PSPs to apply a weighted average interchange fee

THE PSD2 adopted end of 2015: KEY ELEMENTS

1- Extension of scope: • non-EU currencies • OLO (one-leg out) transactions • clarification of "main activity", "regular occupation or business activity"; group collection/payment factories; & acquiring • narrowing of exemptions like: commercial agent; limited network; digital devices; ATM operators 2- Business rules: • Application of charges/SHA, value dating and availability of funds • obligations on payee's PSPs regarding misdirected • Payments (incorrect unique identifiers) 3- Security measures, including: • Operational risk framework • Incident reporting • The use of "strong customer authentication" when a payer accesses his payment account online, initiates a "electronic remote

payment transaction" or carries on any other action through a remote channel which may imply a risk of payment fraud or other abuses, authentication to include elements dynamically linking the transaction to a specific amount and payee

4. Two new types of payment service introduced:

• Payment initiation services (PIS) • Account information services (AIS)

• PSD2’s approach is to set out framework for: • rights of PSU and obligations of AS PSP and PIS/AIS TPP • modus operandi between AS PSP and PIS/AIS TPP

• PS’s rights include right to: • use a TPP where payment account is accessible online; • seek compensation from his AS PSP for unauthorised payment transactions (but AS PSP may have a remedy against the

PIS TPP) • PIS TPP’s obligations include to:

• act only within PSU’s explicit consent; • authenticate itself towards AS PSP every session; • not modify the transaction, nor hold the payer’s funds

4. A new paradigm

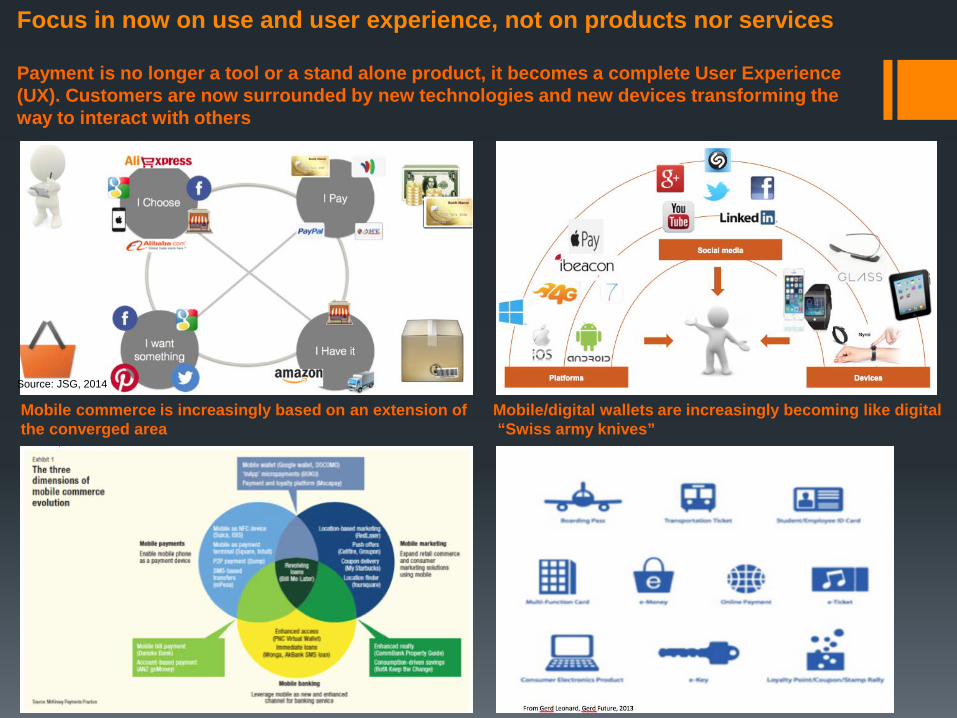

Focus in now on use and user experience, not on products nor services

Payment is no longer a tool or a stand alone product, it becomes a complete User Experience (UX). Customers are now surrounded by new technologies and new devices transforming the way to interact with others

Source: JSG, 2014

Mobile commerce is increasingly based on an extension of the converged area

Mobile/digital wallets are increasingly becoming like digital “Swiss army knives”

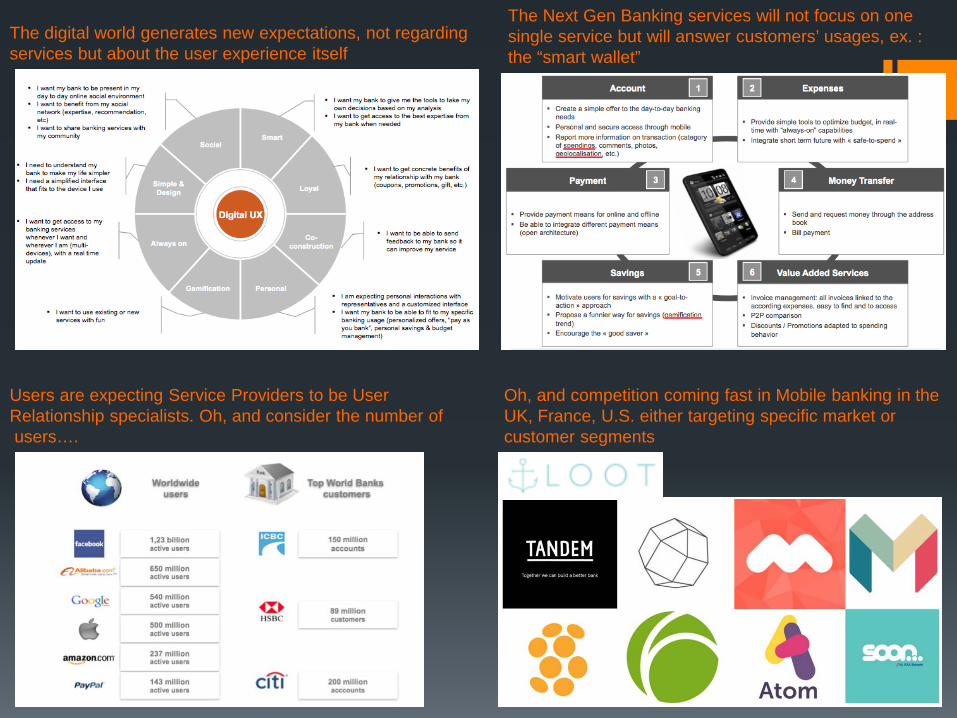

The digital world generates new expectations, not regarding services but about the user experience itself

Users are expecting Service Providers to be User Relationship specialists. Oh, and consider the number of users….

The Next Gen Banking services will not focus on one single service but will answer customers’ usages, ex. : the “smart wallet”

Oh, and competition coming fast in Mobile banking in the UK, France, U.S. either targeting specific market or customer segments

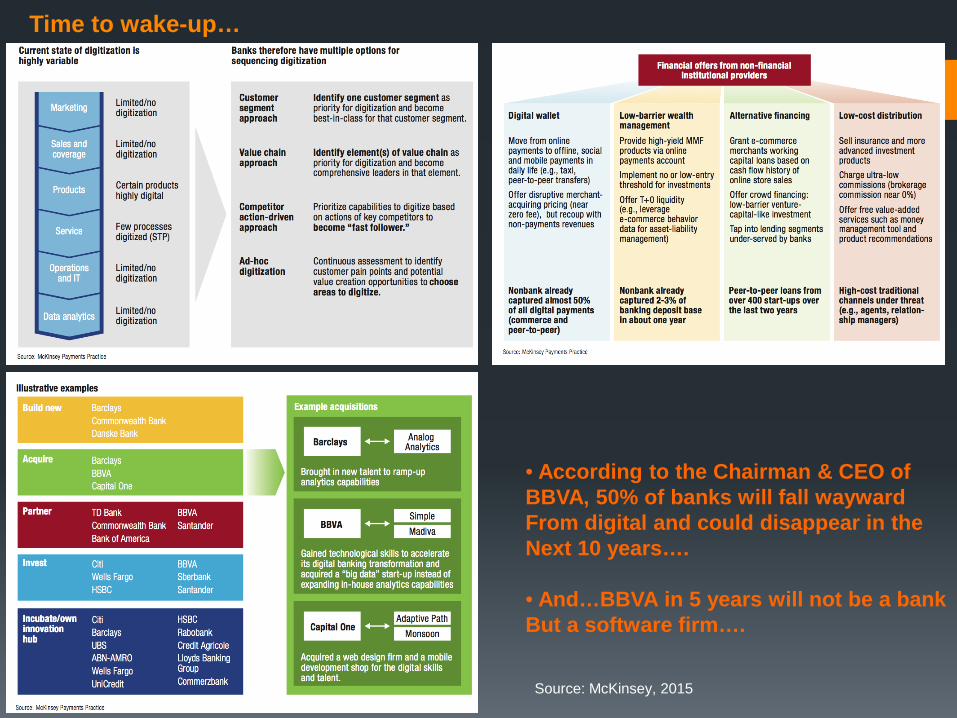

Time to wake-up…

• According to the Chairman & CEO of BBVA, 50% of banks will fall wayward From digital and could disappear in the Next 10 years…. • And…BBVA in 5 years will not be a bank But a software firm….

Source: McKinsey, 2015

Conclusions

• Digital payments increasingly part of a broader, integrated, converged offering (payments+ banking + commerce) • Competition starting to hit at incumbent players both on specific vertical industry or customer segments but also through general payments systems • Regulation is playing a key role in Intensifying the competitive heat

•The future: Convergence with other fintech products also emerging (Virtual currencies, P2P lending, Crowdfunding, Insurance, etc.

Any questions?

Jean-Stéphane Gourévitch [email protected]

+44(0)788 775 4615 @jsgourevitch

uk.linkedin.com/in/jeanstephanegourevitch

Thank you very much for your attention!

Panel Discussion

klgates.com 32

Related Documents