Proudly supported by Kantar, the Leader in Mobile Marketing Research January 30-31, 2013 Kuala Lumpur, Malaysia Asia-Pacific Edition 2013 WWW.MRMW.NET Organized by TM

Passive mobile measurement: The next big thing in market research? - TNS

Jul 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Proudly supported by Kantar, the Leader in Mobile Marketing Research

January 30-31, 2013

Kuala Lumpur, Malaysia

Asia-Pacific Edition 2013 WWW.MRMW.NET

Organized by

TM

Thank you to our sponsors!

Title Sponsor Platinum Sponsor Gold Sponsors

Silver Sponsor Exhibitor Networking Evening Sponsor Networking Break Sponsor

Association Partners

Media Partners

©TNS 2012

Passive mobile measurement: The next big thing in market research?

©TNS 2012

As the internet becomes more affordable and readily available in APAC, it is stealing share of attention away from traditional media

68

55

31 29

13

Internet for leisure

TV Radio Newspapers Magazines

% using at least once a day – Global

83

81

62

48

64

54

64

40

93

88

34

45

14

17

25

47

24

30

16

28

Singapore

Australia

China

Indonesia

Thailand

Internet for leisure TV Radio Newspapers

% daily users

Mobile: The Key to Marketing in Asia

©TNS 2012

And as mobile data becomes cheaper and wifi more ubiquitous, mobile is becoming a key portal to the internet, especially in emerging markets

93 95 89

37

69

34 27

49

12

23

7 8 16

52

27

53

37

49

71

30

16 10 9

0 1

Singapore Australia China Indonesia Thailand

% accessing using the internet in the past 4 weeks via:

PC at work

PC at Internet café

PC at home Mobile phone

Tablet

Mobile: The Key to Marketing in Asia

©TNS 2012 4

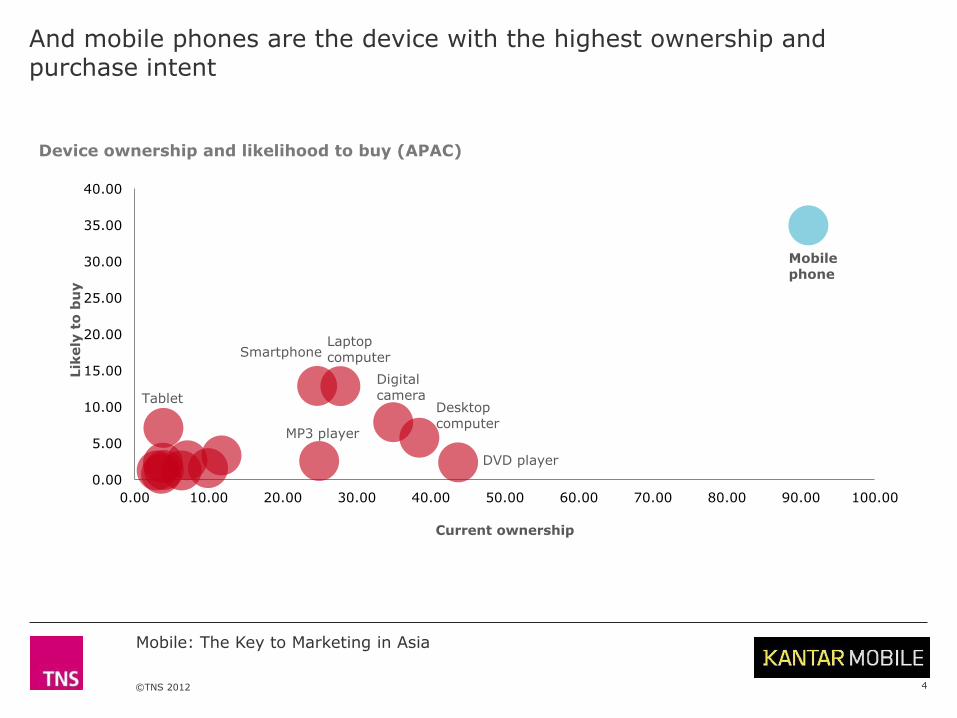

And mobile phones are the device with the highest ownership and purchase intent

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

0.00 10.00 20.00 30.00 40.00 50.00 60.00 70.00 80.00 90.00 100.00

Smartphone

Device ownership and likelihood to buy (APAC)

Current ownership

Lik

ely

to

bu

y

Tablet Desktop computer

Laptop computer

Digital camera

DVD player

MP3 player

Mobile: The Key to Marketing in Asia

Mobile phone

©TNS 2012

Consumer trends…

5

Quantified Self ‘Check-ins’ Visual Content Voice-based UI

Real-time Status Mobile Wallet New Devices Enterprise Consumer

©TNS 2012 6

Many of these uniting

location, voice, mCommerce

©TNS 2012 7

Mobile

©TNS 2012 8

©TNS 2012

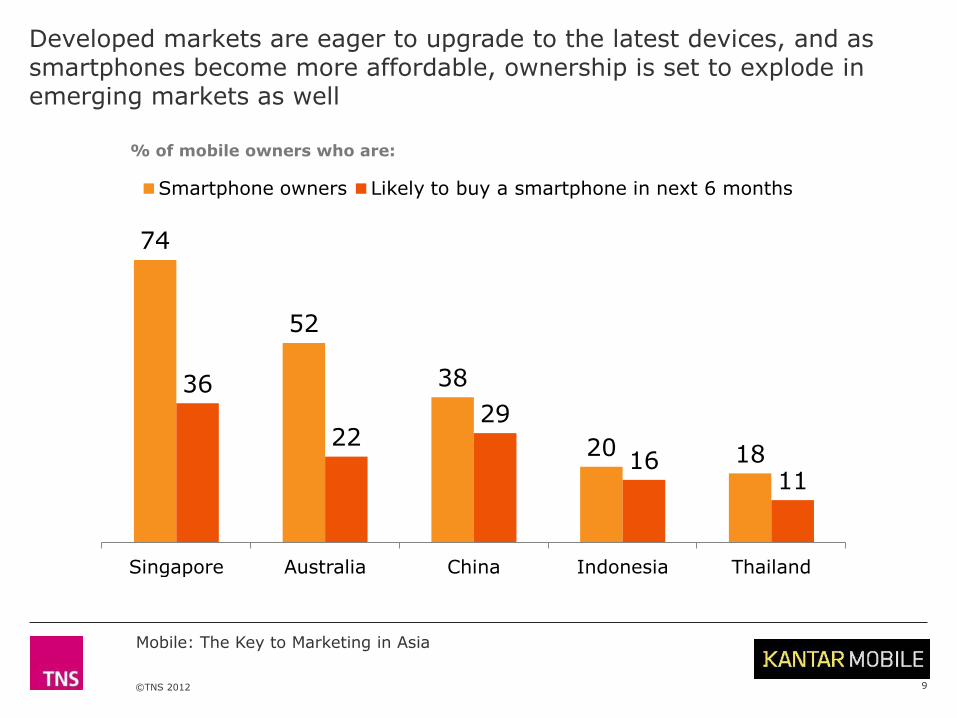

Developed markets are eager to upgrade to the latest devices, and as smartphones become more affordable, ownership is set to explode in emerging markets as well

9

74

52

38

20 18

36

22 29

16 11

Singapore Australia China Indonesia Thailand

Smartphone owners Likely to buy a smartphone in next 6 months

% of mobile owners who are:

Mobile: The Key to Marketing in Asia

©TNS 2012 10

©TNS 2012

Finger on the CMO’s pulse

11

Early days, but act fast

Beyond mobile marcoms

A step-change opportunity

©TNS 2012

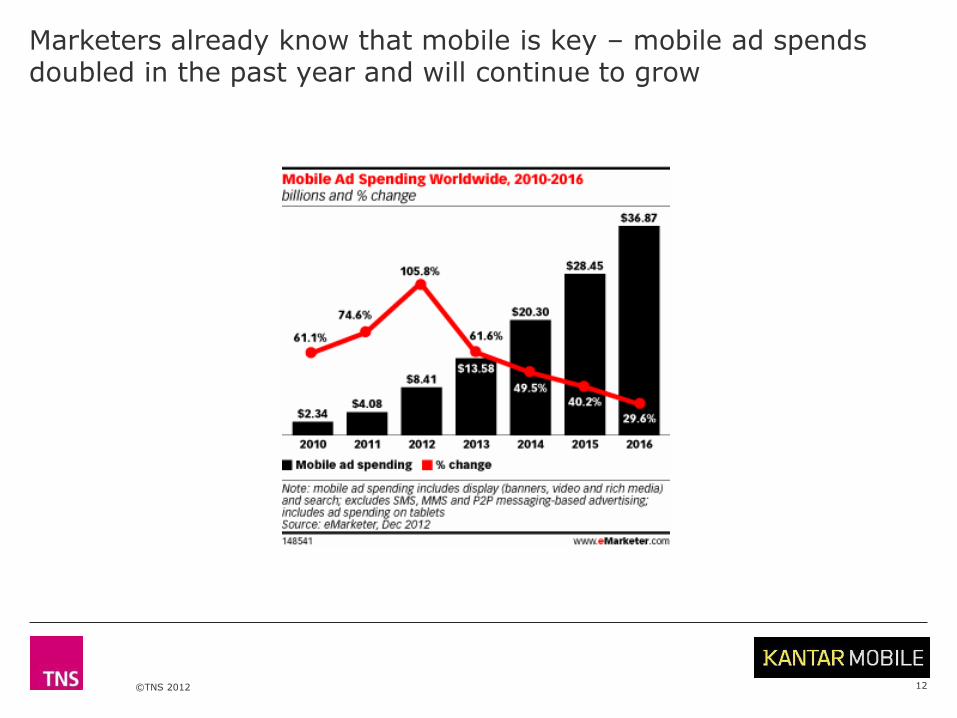

Marketers already know that mobile is key – mobile ad spends doubled in the past year and will continue to grow

12

©TNS 2012

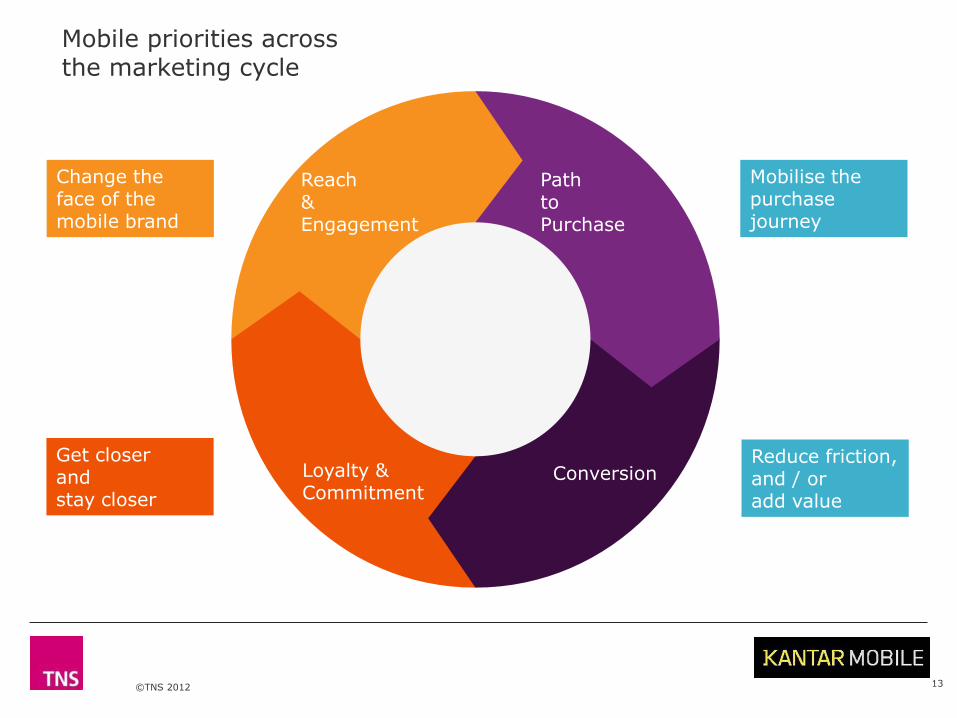

Mobile priorities across the marketing cycle

13

Change the face of the mobile brand

Mobilise the purchase journey

Reduce friction, and / or add value

Get closer and stay closer

Reach & Engagement

Path to Purchase

Loyalty & Commitment

Conversion

©TNS 2012

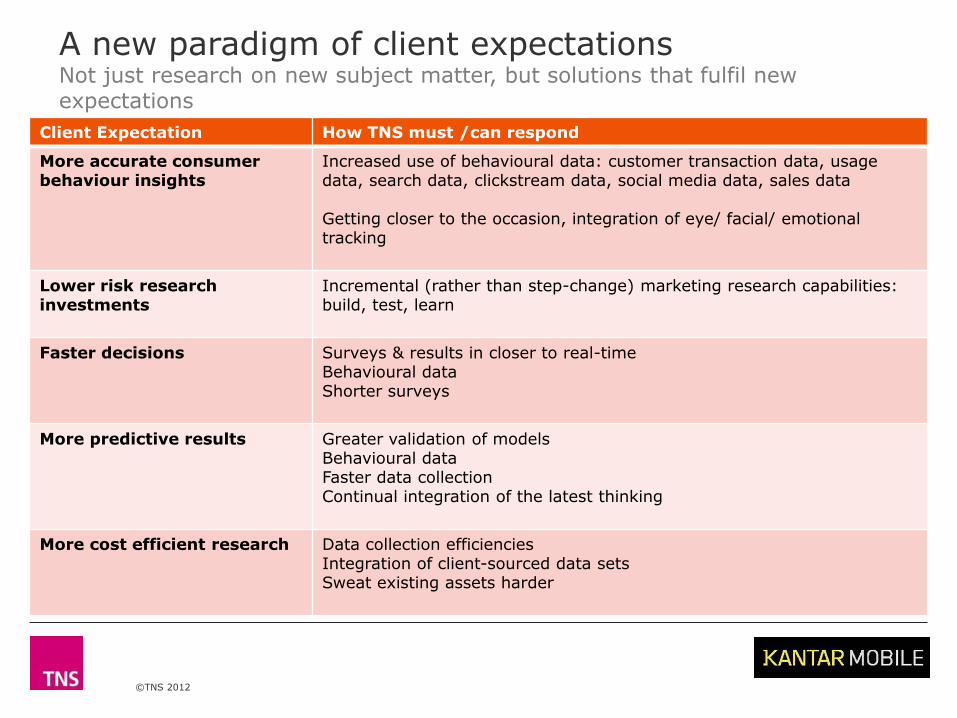

A new paradigm of client expectations Not just research on new subject matter, but solutions that fulfil new expectations

Client Expectation How TNS must /can respond

More accurate consumer behaviour insights

Increased use of behavioural data: customer transaction data, usage data, search data, clickstream data, social media data, sales data Getting closer to the occasion, integration of eye/ facial/ emotional tracking

Lower risk research investments

Incremental (rather than step-change) marketing research capabilities: build, test, learn

Faster decisions

Surveys & results in closer to real-time Behavioural data Shorter surveys

More predictive results

Greater validation of models Behavioural data Faster data collection Continual integration of the latest thinking

More cost efficient research

Data collection efficiencies Integration of client-sourced data sets Sweat existing assets harder

14

©TNS 2012 15

24:7

Mobile Behavioural Always-on

©TNS 2012

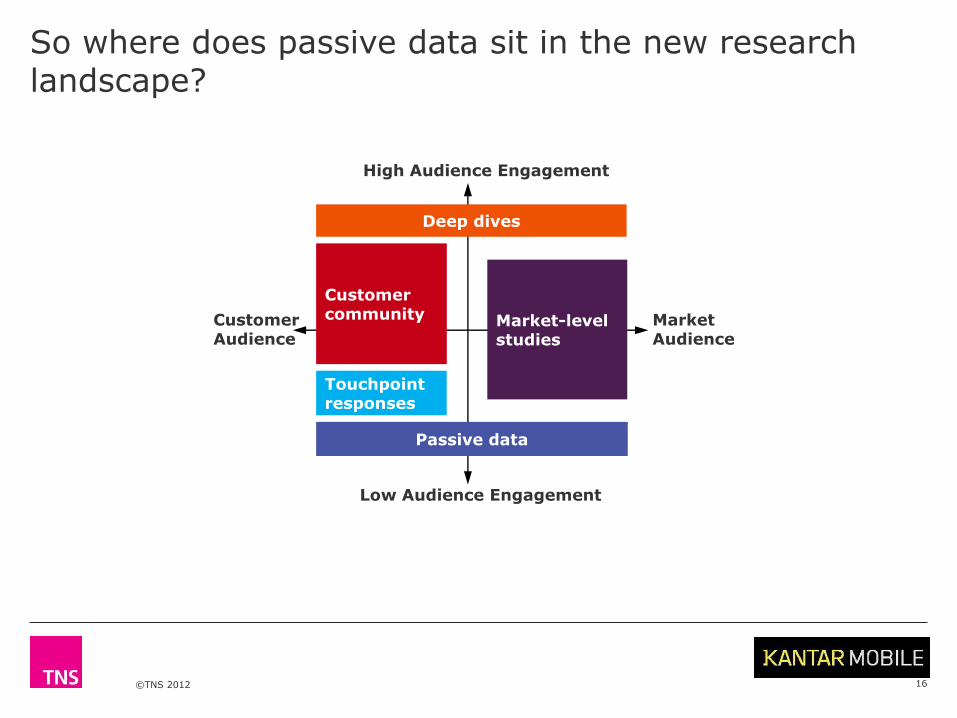

Touchpoint responses

Customer community Market-level

studies

Deep dives

Passive data

Customer Audience

Market Audience

High Audience Engagement

Low Audience Engagement

16

So where does passive data sit in the new research landscape?

©TNS 2012 17

©TNS 2012

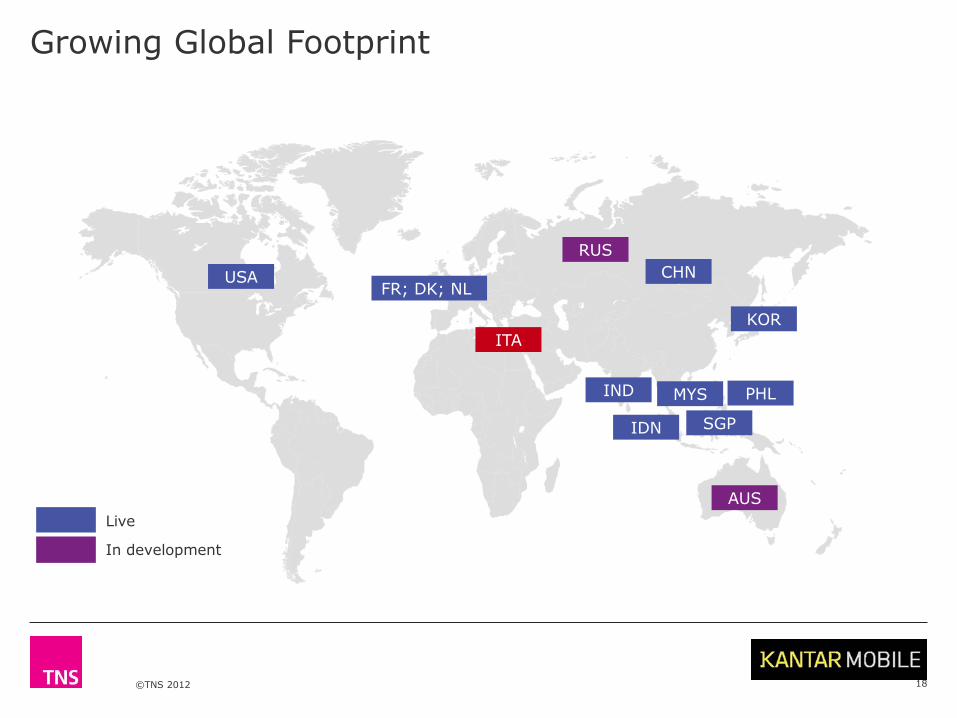

Growing Global Footprint

18

USA CHN FR; DK; NL

SGP

KOR

IND

IDN

AUS

MYS PHL

RUS

Live

In development

ITA

©TNS 2012

Keys to success

Need to build up a panel of respondents willing to trust you with their data and incentivize/engage them so that they remain on the panel

Maintaining a balance of panel members which is representative of the mobile population instead of skewed to fixed line internet users

Special software, analytic capabilities and storage facilities to handle this kind of Big Data; need to have defined aims in order to leverage data effectively

Metering capabilities that can cope with the rapidly changing mobile OS landscape (covering the range of OSes and new versions as they are released)

Ability to overlay passive data with attitudinal and stated behaviour – passive in isolation has limited value

Panel management

Representivity

Data management

Agility

Data integration

©TNS 2012

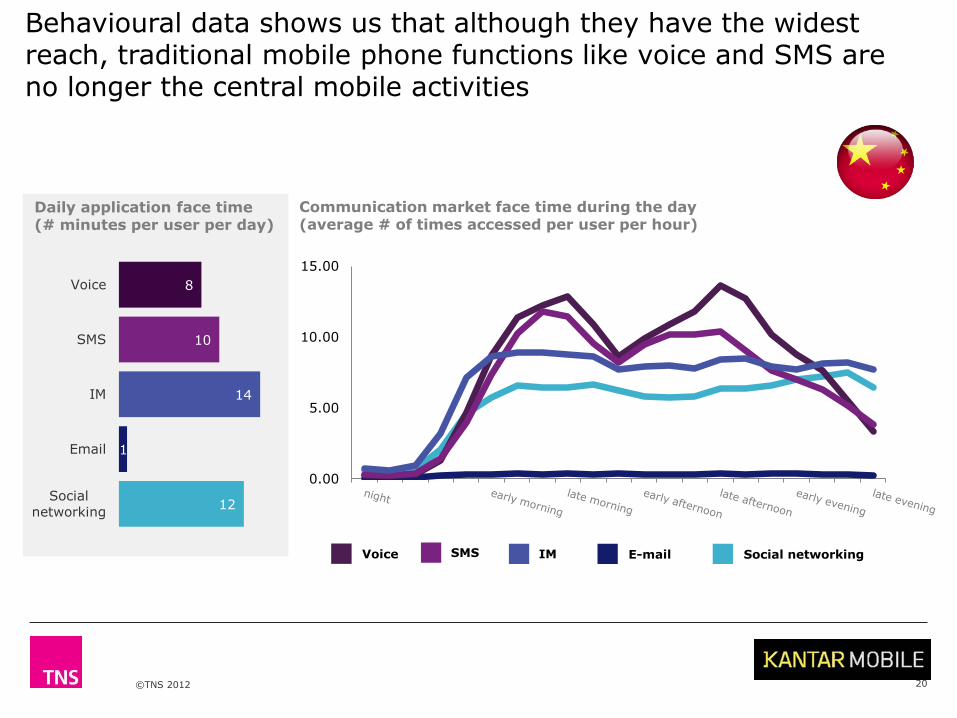

8

10

14

1

12

Voice

SMS

IM

Social

networking

0.00

5.00

10.00

15.00

20

Communication market face time during the day (average # of times accessed per user per hour)

Voice SMS IM E-mail Social networking

Daily application face time (# minutes per user per day)

Behavioural data shows us that although they have the widest reach, traditional mobile phone functions like voice and SMS are no longer the central mobile activities

©TNS 2012

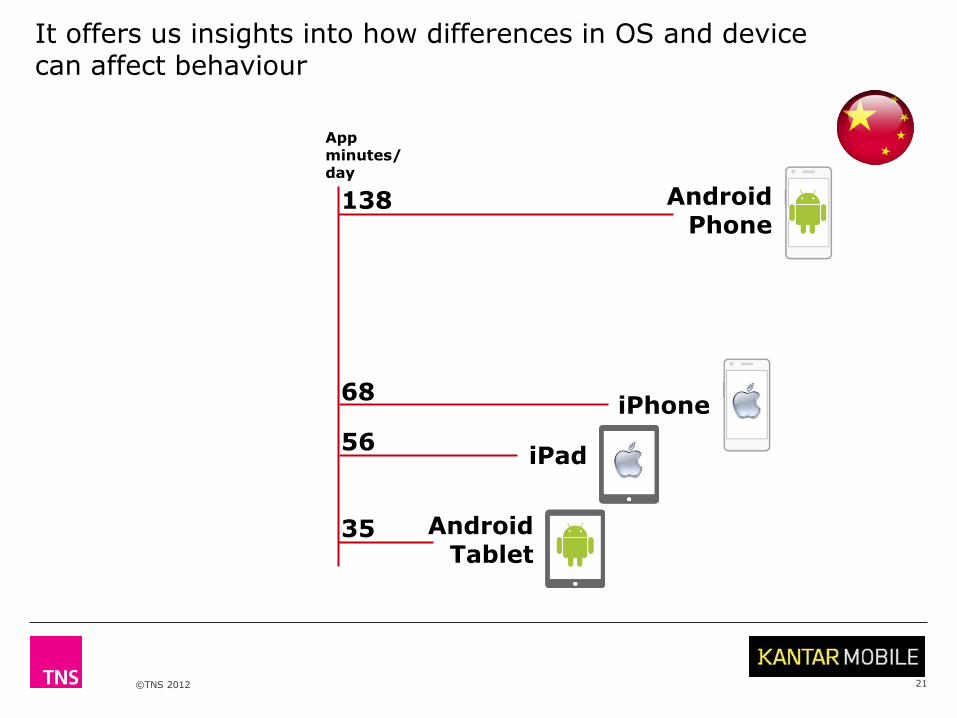

35

68

21

iPhone

Android Phone

138

App minutes/ day

56 iPad

Android Tablet

It offers us insights into how differences in OS and device can affect behaviour

©TNS 2012

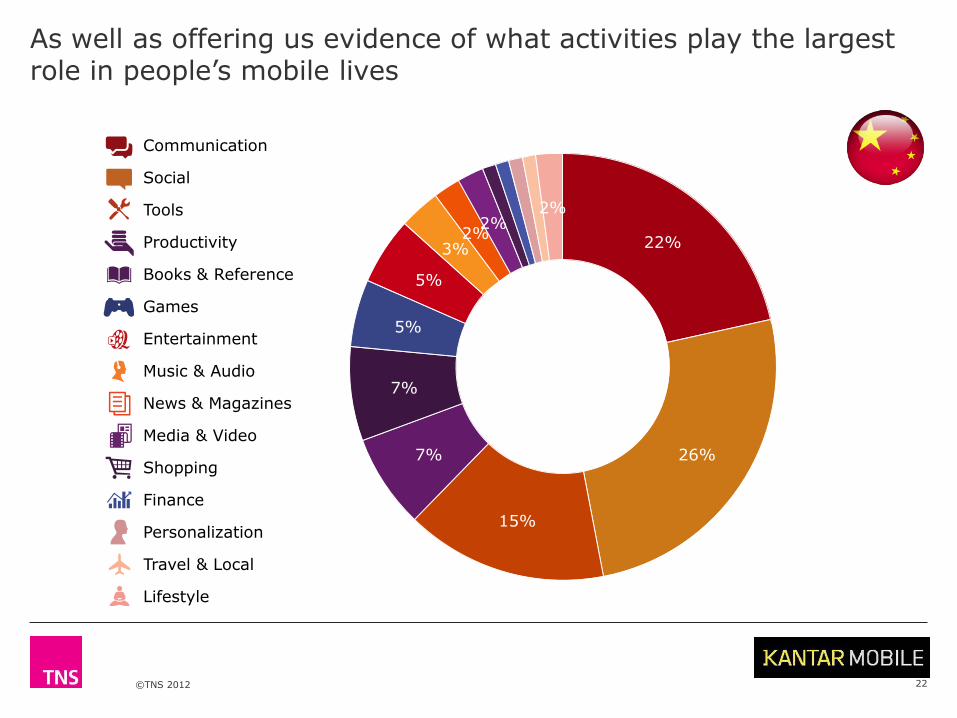

As well as offering us evidence of what activities play the largest role in people’s mobile lives

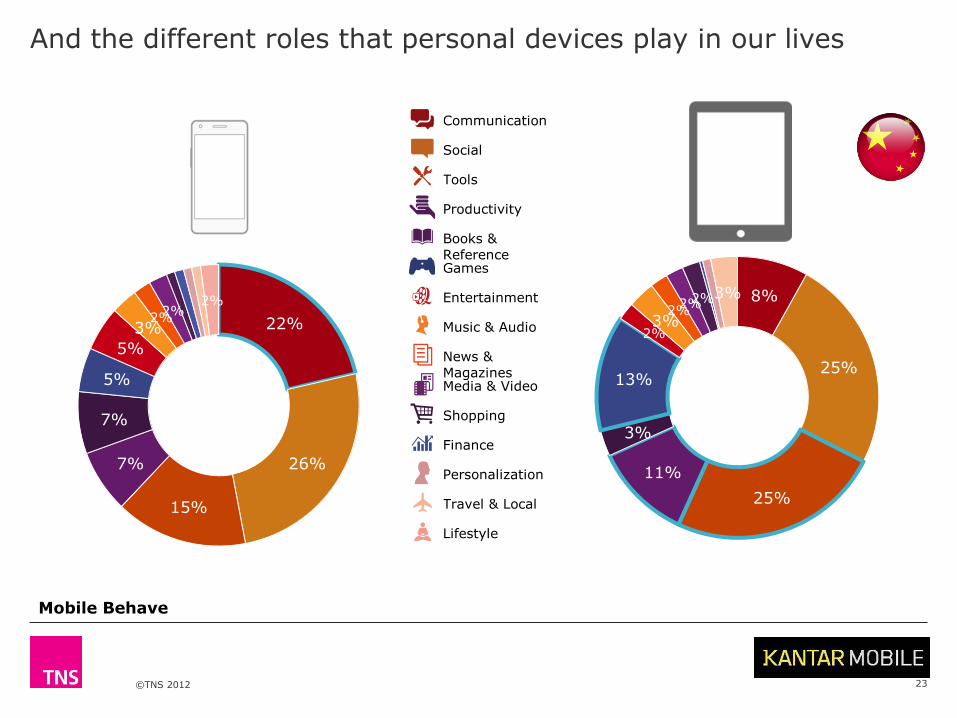

22

22%

26%

15%

7%

7%

5%

5%

3% 2%

2% 2%

Communication

Social

Tools

Productivity

Books & Reference

Games

Entertainment

Music & Audio

News & Magazines

Media & Video

Shopping

Finance

Personalization

Travel & Local

Lifestyle

©TNS 2012

8%

25%

25%

11%

3%

13%

2% 3%

2% 2% 2% 3%

And the different roles that personal devices play in our lives

22%

26%

15%

7%

7%

5%

5%

3% 2%

2% 2%

Communication

Social

Tools

Productivity

Books &

Reference Games

Entertainment

Music & Audio

News &

Magazines Media & Video

Shopping

Finance

Personalization

Travel & Local

Lifestyle

23

Mobile Behave

©TNS 2012

©TNS 2012 25

*

3G

WiFi

18 minutes

a day

26 minutes

a day

Total daily market time

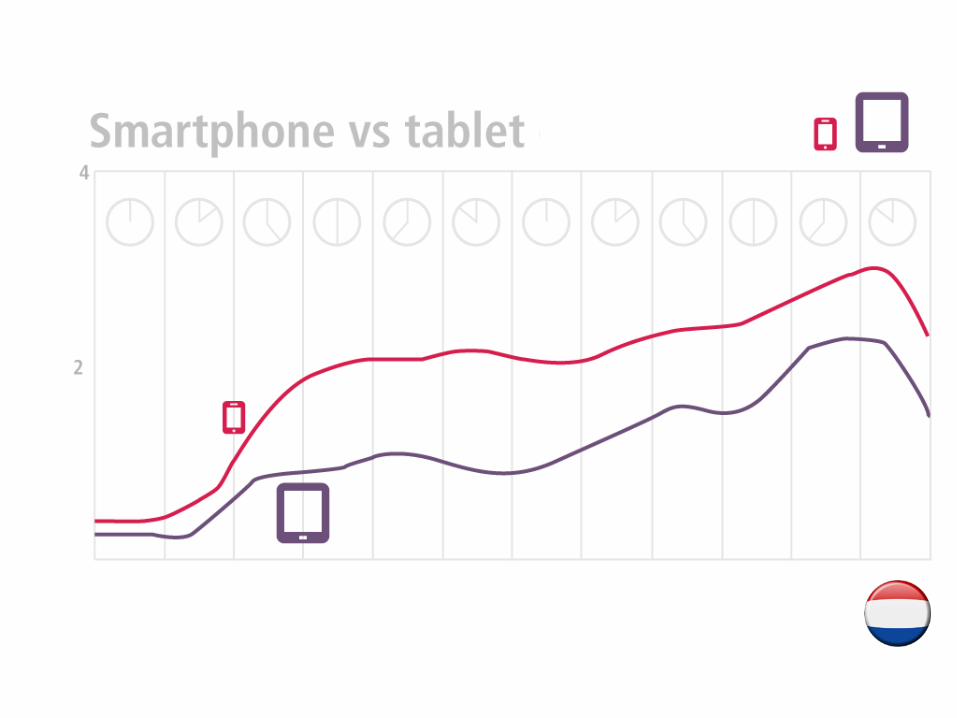

And can demonstrate that mobile phone usage is not always mobile

©TNS 2012 26

©TNS 2012 27

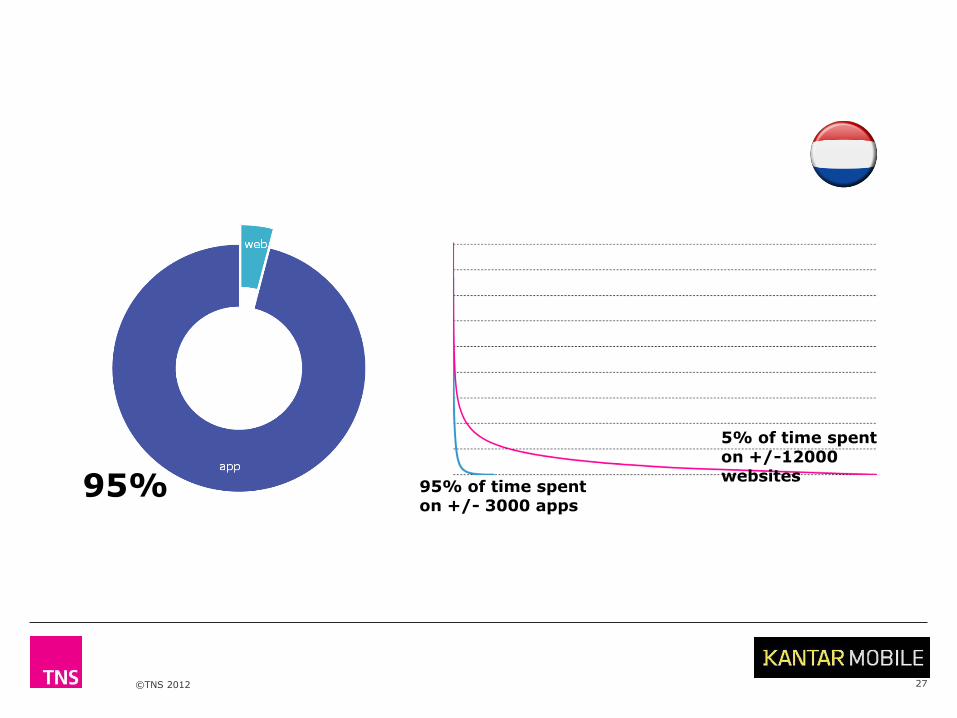

95% 95% of time spent on +/- 3000 apps

5% of time spent on +/-12000 websites

©TNS 2012 28

©TNS 2012 29

Relevance

Independence

Convenience

Experience

Transparency

©TNS 2012

1. Retain participants

2. Communities as opposed to panels

3. Represent all OS

4. Active and passive

5. Multiple data sources

6. Big data ability

7. Nimble, flexible, iterate

7 mobile research strategy ingredients

©TNS 2012

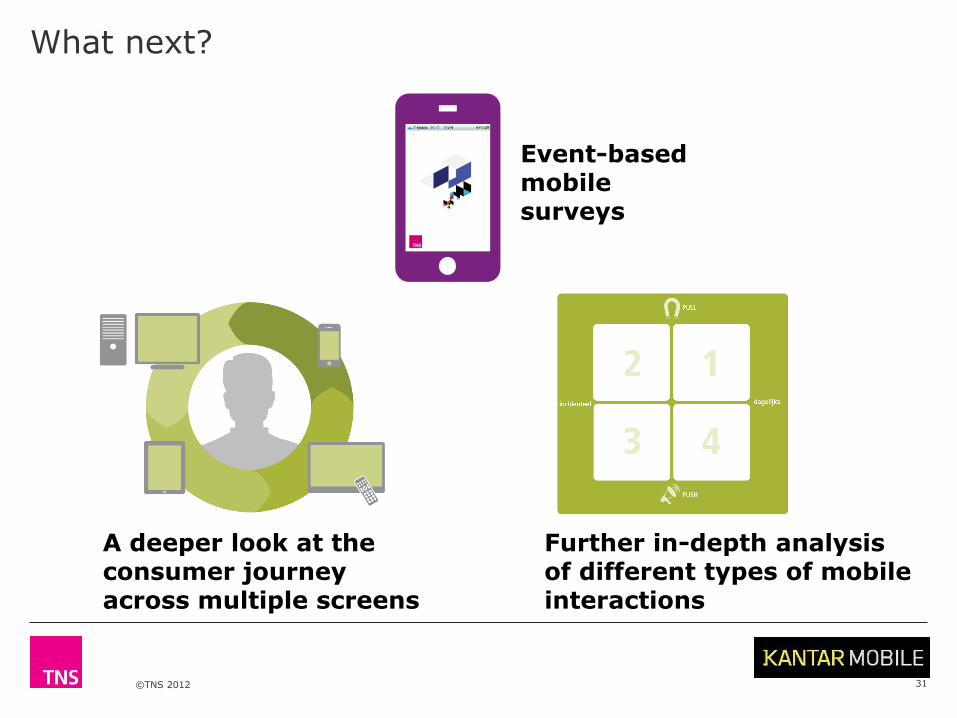

What next?

31

Event-based mobile surveys

A deeper look at the consumer journey across multiple screens

Further in-depth analysis of different types of mobile interactions

©TNS 2012

Thank you

James Fergusson Global Head, Digital and Technology Remy Bleijendaal Digital Consultant and Mobile Behave development lead

Thank you to our sponsors!

Title Sponsor Platinum Sponsor Gold Sponsors

Silver Sponsor Exhibitor Networking Evening Sponsor Networking Break Sponsor

Association Partners

Media Partners

Proudly supported by Kantar, the Leader in Mobile Marketing Research

January 30-31, 2013

Kuala Lumpur, Malaysia

Asia-Pacific Edition 2013 WWW.MRMW.NET

Organized by

TM

Related Documents