Part 5 Chapter 20 The valuation of a project under different financing strategies. Marc B.J. Schauten

Part 5 Chapter 20 The valuation of a project under different financing strategies. Marc B.J. Schauten.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Part 5

Chapter 20

The valuation of a project under different financing strategies.

Marc B.J. Schauten

Example

Consider a project to produce product SMART. I = 4000.Cash flow is $ 1600 pre-tax per year for 5 years. RU = 10%. Tax rate = 35%.

NPV base case = -I + [EBIT x (1-C)] /(1+RU)t

Example Ru = 10%Tax rate = 35%

Year EBIT EBIT(1-tc) disc.factor PV of 31 2 3 4 51 1600 1040 0,9090909 945,52 1600 1040 0,8264463 859,53 1600 1040 0,7513148 781,44 1600 1040 0,6830135 710,35 1600 1040 0,6209213 645,8

3942

NPV base case = -I + [EBIT x (1-C)] /(1+RU)t = -4000 + 3942 = -58

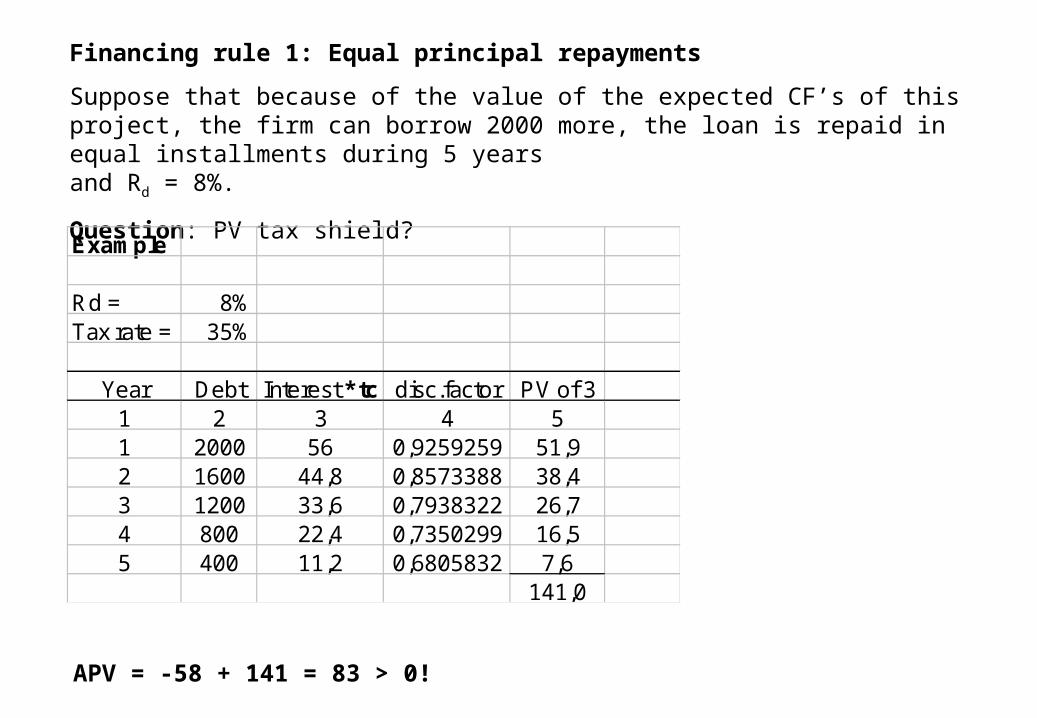

Financing rule 1: Equal principal repayments

Suppose that because of the value of the expected CF’s of this project, the firm can borrow 2000 more, the loan is repaid in equal installments during 5 yearsand Rd = 8%.

Question: PV tax shield?

Example

Rd = 8%Tax rate = 35%

Year Debt Interest * tc disc.factor PV of 31 2 3 4 51 2000 56 0,9259259 51,92 1600 44,8 0,8573388 38,43 1200 33,6 0,7938322 26,74 800 22,4 0,7350299 16,55 400 11,2 0,6805832 7,6

141,0

APV = -58 + 141 = 83 > 0!

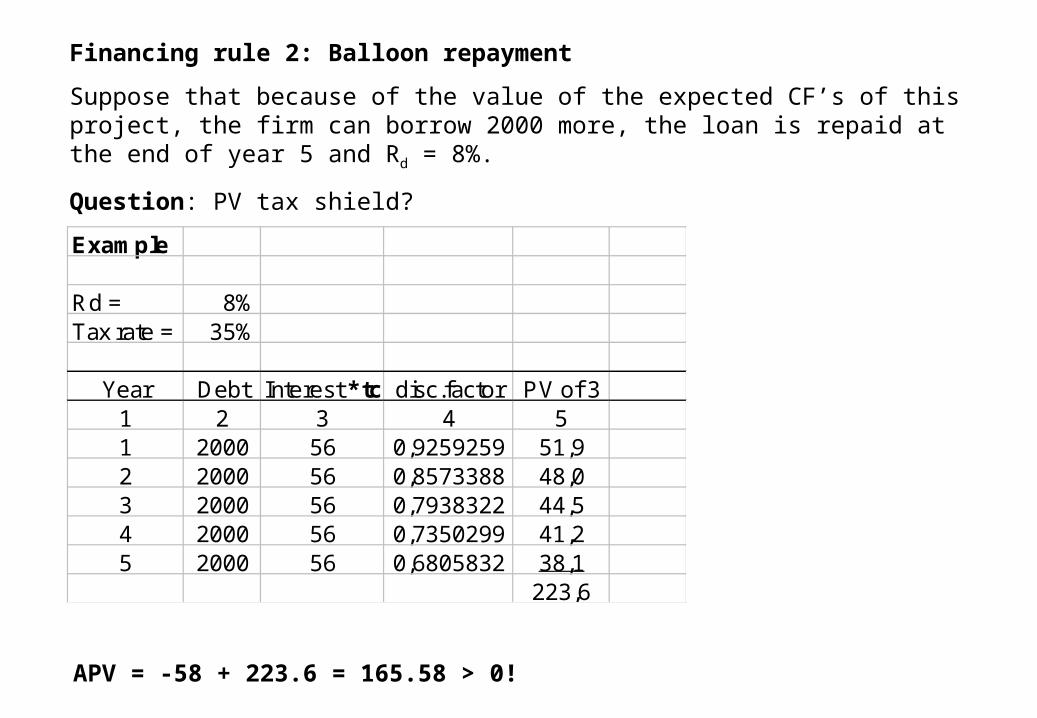

Financing rule 2: Balloon repayment

Suppose that because of the value of the expected CF’s of this project, the firm can borrow 2000 more, the loan is repaid at the end of year 5 and Rd = 8%.

Question: PV tax shield?

Example

Rd = 8%Tax rate = 35%

Year Debt Interest * tc disc.factor PV of 31 2 3 4 51 2000 56 0,9259259 51,92 2000 56 0,8573388 48,03 2000 56 0,7938322 44,54 2000 56 0,7350299 41,25 2000 56 0,6805832 38,1

223,6

APV = -58 + 223.6 = 165.58 > 0!

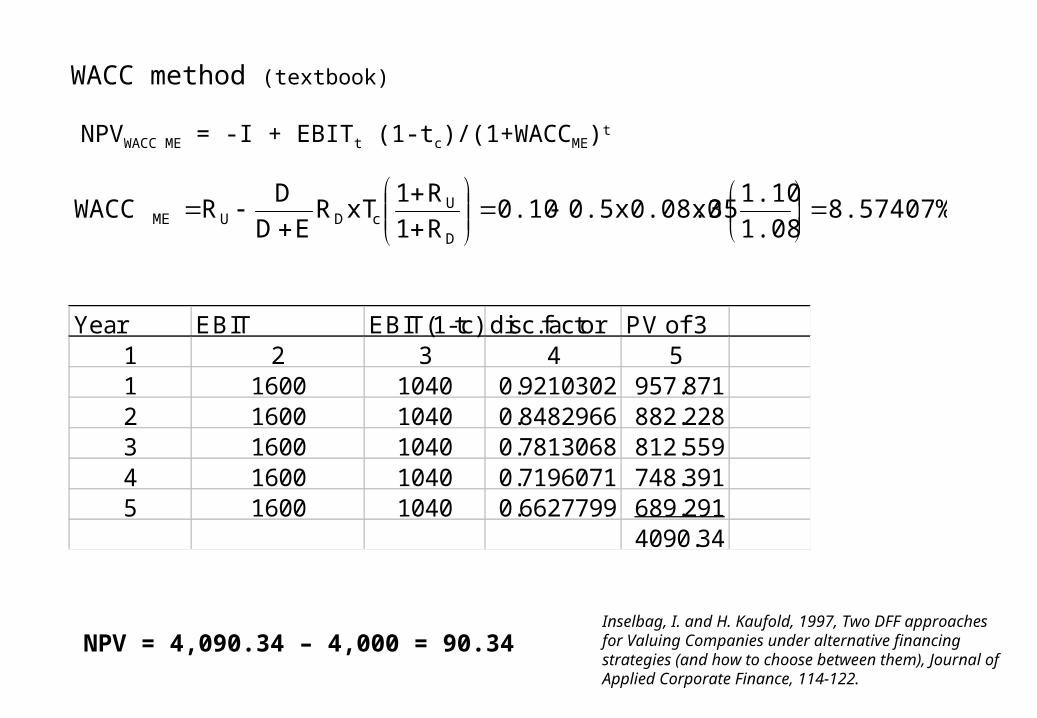

Financing rule 3: Target capital structure

Assume that the project will be financed for 50% with debt, Rd = 8%.

Use the WACC MM?

Assumptions (a.o.) of WACC MM:

- PVTS = tc D

Alternatives are: 3a) Miles Ezzell WACC and 3b) Harris Pringle / Ruback WACC

Ad 3a) Assumptions WACC Miles Ezzell:

- debt as a proportion of the total market value is remains constant during the life of the project;

- the project generates stable/unstable CFs that could be finite and/or variable.

- ME do not discount the tax shield with RD only. As long as future taxshields are tied to uncertain future cash flows, discount with Ru.

D

UcDUME R1

R1xTR

ED

DRWACC

NPVWACC ME = -I + EBITt (1-tc)/(1+WACCME)t

Year EBIT EBIT(1-tc) disc.factor PV of 31 2 3 4 51 1600 1040 0.9210302 957.8712 1600 1040 0.8482966 882.2283 1600 1040 0.7813068 812.5594 1600 1040 0.7196071 748.3915 1600 1040 0.6627799 689.291

4090.34

NPV = 4,090.34 – 4,000 = 90.34

8.57407%1.08

1.10.350.5x0.08x00.10

R1

R1xTR

ED

DRWACC

D

UcDUME

WACC method (textbook)

Inselbag, I. and H. Kaufold, 1997, Two DFF approaches for Valuing Companies under alternative financing strategies (and how to choose between them), Journal of Applied Corporate Finance, 114-122.

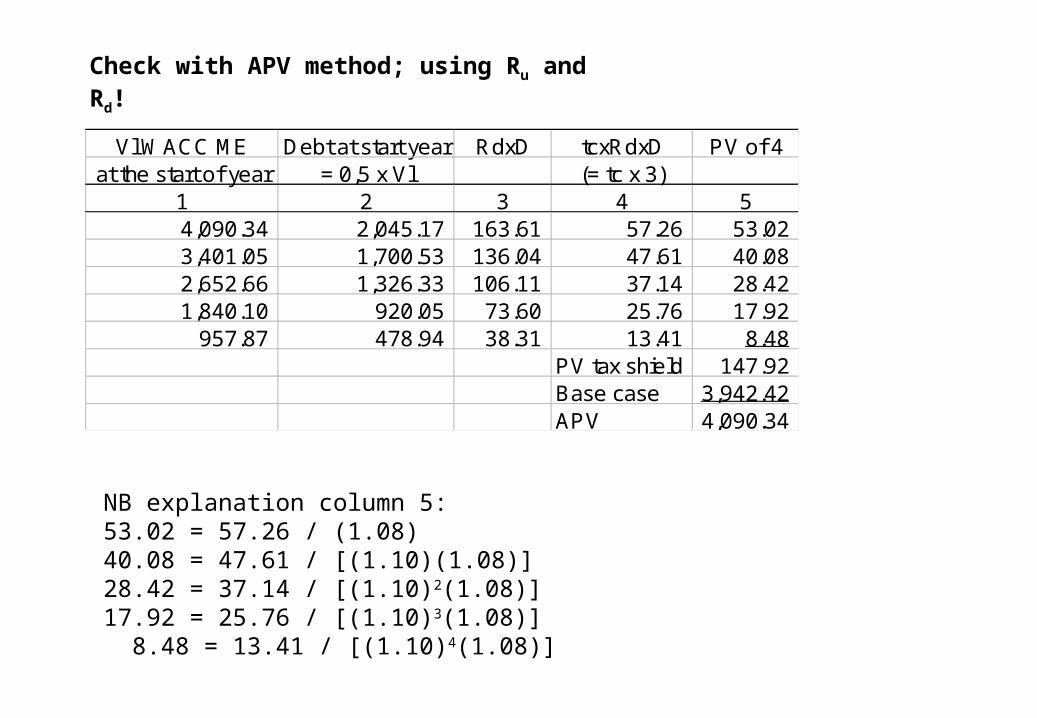

Vl WACC ME Debt at start year RdxD tcxRdxD PV of 4at the start of year = 0,5 x Vl (= tc x 3)

1 2 3 4 54,090.34 2,045.17 163.61 57.26 53.023,401.05 1,700.53 136.04 47.61 40.082,652.66 1,326.33 106.11 37.14 28.421,840.10 920.05 73.60 25.76 17.92

957.87 478.94 38.31 13.41 8.48PV tax shield 147.92Base case 3,942.42APV 4,090.34

NB explanation column 5:53.02 = 57.26 / (1.08)40.08 = 47.61 / [(1.10)(1.08)]28.42 = 37.14 / [(1.10)2(1.08)]17.92 = 25.76 / [(1.10)3(1.08)] 8.48 = 13.41 / [(1.10)4(1.08)]

Check with APV method; using Ru and Rd!

0.119481480.5

0.5

1.08

0.350.0810.08)(0.10.1

E

D

r1

Tr1)r(rrr

d

dduue

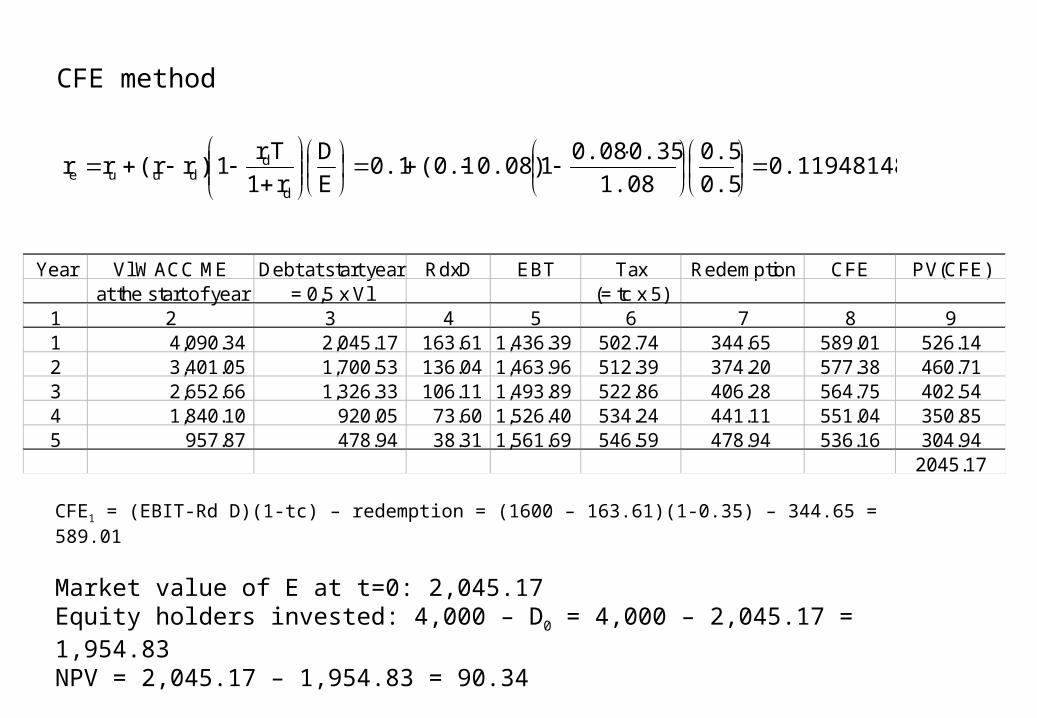

CFE method

CFE1 = (EBIT-Rd D)(1-tc) – redemption = (1600 – 163.61)(1-0.35) – 344.65 = 589.01

Market value of E at t=0: 2,045.17Equity holders invested: 4,000 – D0 = 4,000 – 2,045.17 = 1,954.83NPV = 2,045.17 – 1,954.83 = 90.34

Year Vl WACC ME Debt at start year RdxD EBT Tax Redemption CFE PV(CFE)at the start of year = 0,5 x Vl (= tc x 5)

1 2 3 4 5 6 7 8 91 4,090.34 2,045.17 163.61 1,436.39 502.74 344.65 589.01 526.142 3,401.05 1,700.53 136.04 1,463.96 512.39 374.20 577.38 460.713 2,652.66 1,326.33 106.11 1,493.89 522.86 406.28 564.75 402.544 1,840.10 920.05 73.60 1,526.40 534.24 441.11 551.04 350.855 957.87 478.94 38.31 1,561.69 546.59 478.94 536.16 304.94

2045.17

Financing rule 3: Target capital structure

Assume that the project will be financed for 50% with debt, Rd = 8%.

Ad 3b) Harris and Pringle (1985) and Ruback (2002) assume tax shields are discounted at RU (see Part 5 note B)

cDURuback TRED

DRWACC

0.086000.350.080.50.10TRED

DRWACC cDURuback

NPVWACC Ruback = -I + EBITt (1-tc)/(1+WACCRuback)t

Year EBIT EBIT(1-tc) disc.factor PV of 31 2 3 4 51 1600 1040 0.9208103 957.642 1600 1040 0.8478916 881.813 1600 1040 0.7807474 811.984 1600 1040 0.7189202 747.685 1600 1040 0.6619892 688.47

4087.57

NPV = 4,087.57 - 4,000 = 87.57

WACC method (textbook)

NPV = 4,087.57 - 4,000 = 87.57

Year Vl WACC Ruback D=0,5*Vl RdxD tcxRdxD PV of (5)at the start of year (=tcx(4))

1 2 3 4 5 61 $4,087.57 $2,043.79 $163.50 $57.23 $52.022 $3,399.10 $1,699.55 $135.96 $47.59 $39.333 $2,651.43 $1,325.71 $106.06 $37.12 $27.894 $1,839.45 $919.73 $73.58 $25.75 $17.595 $957.64 $478.82 $38.31 $13.41 $8.32

PV tax shields $145.15Base case $3,942.42

$4,087.57

Check with APV method; using Ru only!

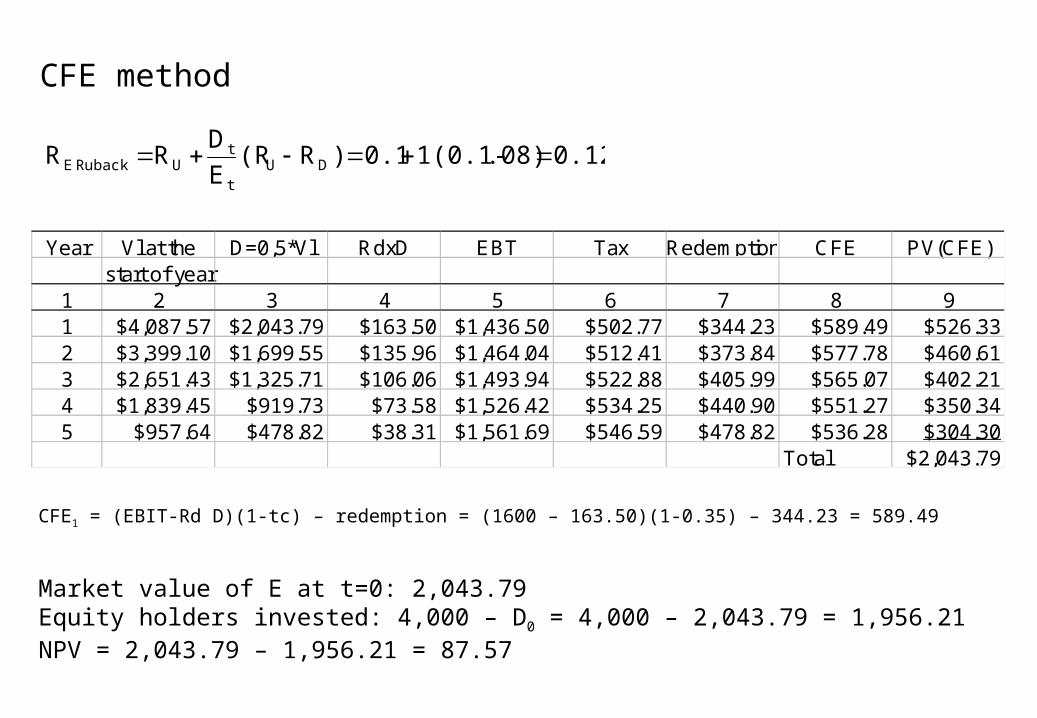

Year Vl at the D=0,5*Vl RdxD EBT Tax Redemption CFE PV(CFE)start of year

1 2 3 4 5 6 7 8 91 $4,087.57 $2,043.79 $163.50 $1,436.50 $502.77 $344.23 $589.49 $526.332 $3,399.10 $1,699.55 $135.96 $1,464.04 $512.41 $373.84 $577.78 $460.613 $2,651.43 $1,325.71 $106.06 $1,493.94 $522.88 $405.99 $565.07 $402.214 $1,839.45 $919.73 $73.58 $1,526.42 $534.25 $440.90 $551.27 $350.345 $957.64 $478.82 $38.31 $1,561.69 $546.59 $478.82 $536.28 $304.30

Total $2,043.79

CFE method

0.12.08)1(0.1-0.1)R(RE

DRR DU

t

tURuback E

CFE1 = (EBIT-Rd D)(1-tc) – redemption = (1600 – 163.50)(1-0.35) – 344.23 = 589.49

Market value of E at t=0: 2,043.79Equity holders invested: 4,000 – D0 = 4,000 – 2,043.79 = 1,956.21NPV = 2,043.79 – 1,956.21 = 87.57

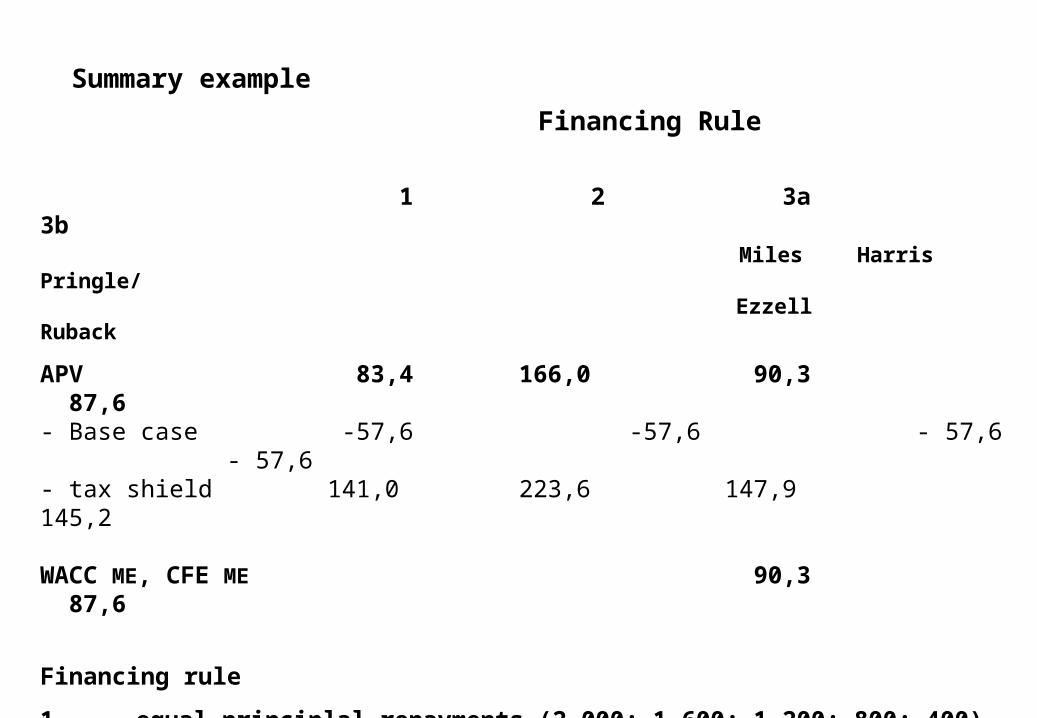

Financing Rule

1 2 3a 3b Miles Harris Pringle/ Ezzell Ruback

APV 83,4 166,0 90,3 87,6 - Base case -57,6 -57,6 - 57,6 - 57,6 - tax shield 141,0 223,6 147,9 145,2 WACC ME, CFE ME 90,3 87,6

Financing rule

1 equal principlal repayments (2,000; 1,600; 1,200; 800; 400)

2 balloon repayment (2,000; 2,000; 2000; 2000; 2000)

3 target capital structure / debt rebalanced (50% of project value)a) ME: (2,045; 1,701; 1,326; 920; 479)

b) HP/R:(2,044; 1,700; 1,326; 920; 479)

Summary example

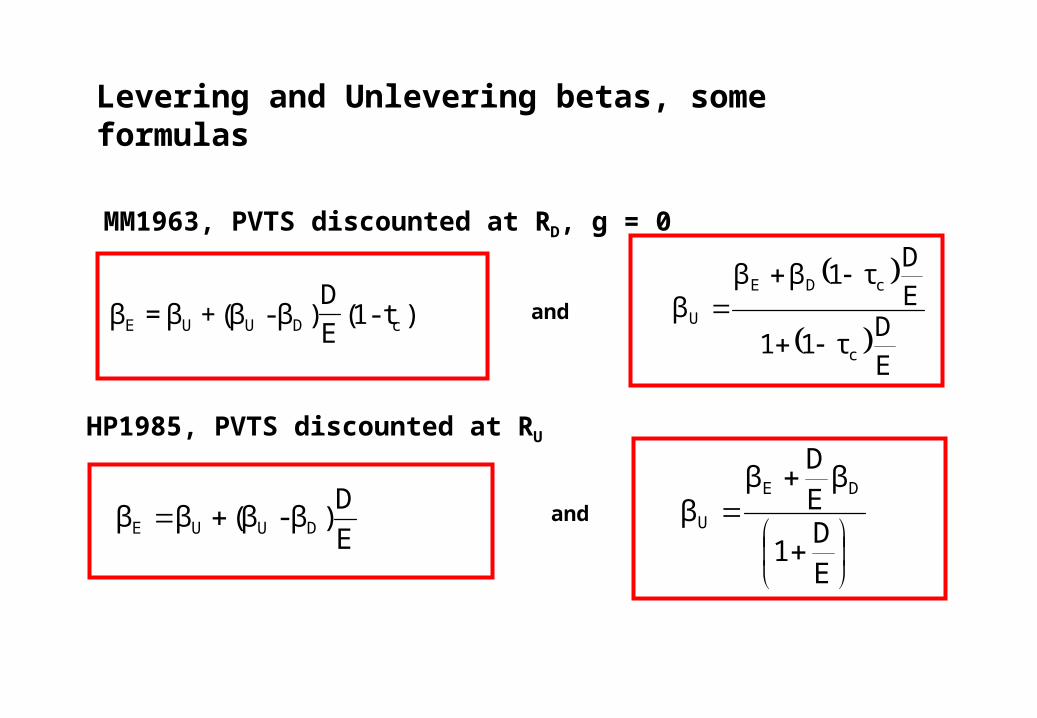

MM1963, PVTS discounted at RD, g = 0

Levering and Unlevering betas, some formulas

HP1985, PVTS discounted at RU

)t-1(E

D)β-β(+β=β cDUUE

E

Dτ11

E

Dτ1ββ

β

c

cDE

U

and

E

D)β-β(ββ DUUE

E

D1

βE

Dβ

βDE

Uand

MM1963: Discount rate tax shield is rd, g = 0

The expected economic income for the providers of capital is: )D(R+)E(R=)D(Rτ+)(RV DEDcUU

Rewriting gives:E

DRDRRVR DDcUU

E

DcU

UE R

E

D)(1R

E

VR →

MM63 tells us that: DVV cUL and EDVL , this results in: )D(1EV cU

(1)

(2)

If we insert (2) in (1) we find: )R)(R(1E

DRR DUcUE

Relation WACC and rd

(3) Remark: (3) = Proposition II MM63!

EDc RED

E)R(1

ED

DWACC

(4)

If we insert (3) in (4) we find:

( ) ( )Rτ-1E+D

D+R

E+D

E=)R(Rτ-1

E

D

E+D

E+R

E+D

E+)Rτ-(1

E+D

D=WACC UcUDUcUDc -

1=E+D

D+

E+D

ESince

(5)

We can rewrite (5) into:

cU ED

D1RWACC (6)

Relation E en D

)R)(R(1E

DRR DUcUE

)R(RβRR FMEFE

)R(RβRR FMUFU

)R(RβRR FMDFD

E

Dτ11

E

Dτ1ββ

β

c

cDE

U

Following the CAPM:

(3)

(7)

(8)

(9)

Inserting (7)-(9) in (3) gives:

)t-1(E

D)β-β(+β=β cDUUE and

HP1985: Discount rate tax shield is ru

The expected economic income for the providers of capital is: )D(R+)E(R=)R(PVTS+)(RV DEUUU

→Substitute VU = E+D - PVTS

)E(R+)D(R=)PVTS(R+PVTS)-D+(ER EDUU

)E(R+)D(R=)D(R+)E(R EDUU

)D(R-)D(R+)E(R=)E(R DUUE

)R-(RE

D+R=R DuUE

→→→

Note that (1) is the same as proposition II of Miller and Modigliani (1958)

(1)

When substituting (1) in the equation in order to calculate the WACC,by taking the weighted average of RD after taxes and RE, we find

DRctLV

D-uR=WACC (2)

Relation E en D

)R(RE

D+R=R DUUE -

)R(RβRR FMEFE

)R(RβRR FMUFU

)R(RβRR FMDFD

Following the CAPM:

(3)

(4)

(5)

(6)

Inserting (4)-(6) in (3) gives:

)R(RβR)R(RβRE

D)R(RβR)R(RβR FMDFFMUFFMUFFMEF →

E

D1

βE

Dβ

βDE

U

DL

EL

U βV

D+β

V

E=β

andE

D)β-β(ββ DUUE

Related Documents