Part 21: Generalized Method of Moments 1-1/67 Econometrics I Professor William Greene Stern School of Business Department of Economics

Part 21: Generalized Method of Moments 21-1/67 Econometrics I Professor William Greene Stern School of Business Department of Economics.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Part 21: Generalized Method of Moments21-1/67

Econometrics IProfessor William Greene

Stern School of Business

Department of Economics

Part 21: Generalized Method of Moments21-2/67

Econometrics I

Part 21 – GeneralizedMethod of Moments

Part 21: Generalized Method of Moments21-3/67

I also have a questions about nonlinear GMM - which is more or less nonlinear IV technique I suppose.

I am running a panel non-linear regression (non-linear in the parameters) and I have L parameters and K exogenous variables with L>K.

In particular my model looks kind of like this: Y = b1*X^b2 + e, and so I am trying to estimate the extra b2 that don't usually appear in a regression.From what I am reading, to run nonlinear GMM I can use the K exogenous variables to construct the orthogonality conditions but what should I use for the extra, b2 coefficients?Just some more possible IVs (like lags) of the exogenous variables?I agree that by adding more IVs you will get a more efficient estimation, but isn't it only the case when you believe the IVs are truly uncorrelated with the error term?So by adding more "instruments" you are more or less imposing more and more restrictive assumptions about the model (which might not actually be true).

I am asking because I have not found sources comparing nonlinear GMM/IV to nonlinear least squares. If there is no homoscadesticity/serial correlation what is more efficient/give tighter estimates?

Part 21: Generalized Method of Moments21-4/67

I’m trying to minimize a nonlinear program with the least square under nonlinear constraints. It’s first introduced by Ané & Geman (2000). It consisted on the minimization of the sum of squared difference between the moment generating function and the theoretical moment generating function

Part 21: Generalized Method of Moments21-5/67

2 212

2 2121

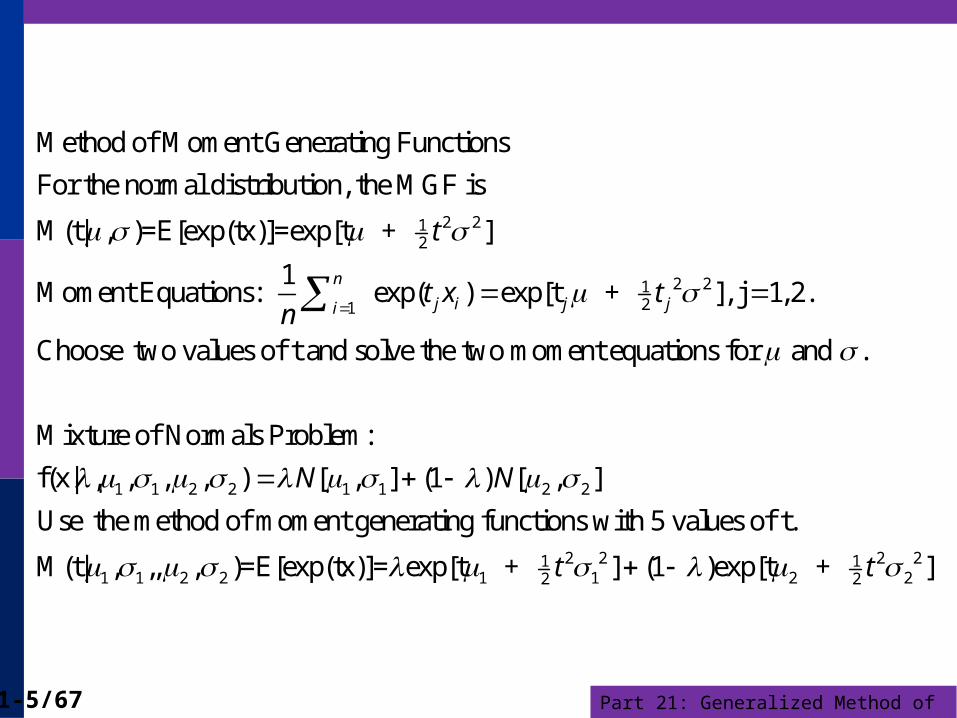

Method of Moment Generating Functions

For the normal distribution, the MGF is

M(t| , )=E[exp(tx)]=exp[t + ]

1Moment Equations: exp( ) exp[t + ], j 1, 2.

Choose two values of t

n

j i j ji

t

t x tn

1 1 2 2 1 1 2 2

1 1 2 2

and solve the two moment equations for and .

Mixture of Normals Problem:

f(x| , , , , ) [ , ] (1 ) [ , ]

Use the method of moment generating functions with 5 values of t.

M(t| , ,, , )=E

N N

2 2 2 21 11 1 2 22 2[exp(tx)]= exp[t + ] (1 )exp[t + ]t t

Part 21: Generalized Method of Moments21-6/67

1 1 21

1 1 2 2

5 2 2 2 21 11 1 2 22 21

Finding the solutions to the moment equations: Least squares

1M̂(t ) exp( ), and likewise for t ,...

Minimize( , , , , )

M̂(t ) exp[t + ] (1 )exp[t + ]

Altern

n

ii

jj

t xn

t t

1 1 2 2 1 1 2 21

ative estimator: Maximum Likelihood

L( , , , , ) log [x | , ] (1 ) [x | , ]N

i iiN N

Part 21: Generalized Method of Moments21-7/67

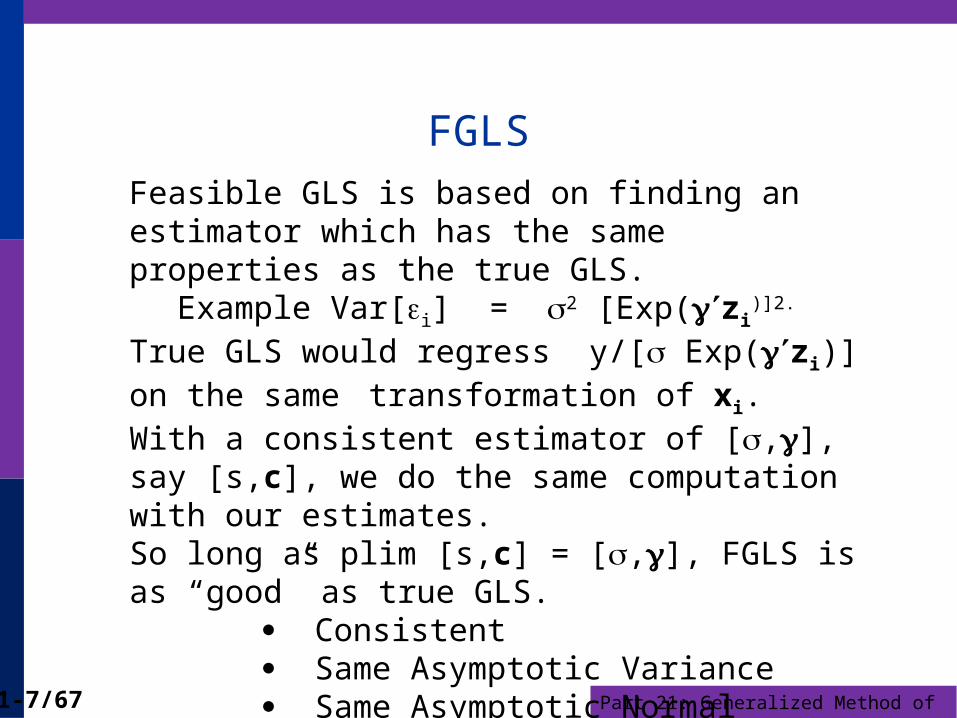

FGLSFeasible GLS is based on finding an estimator which has the same properties as the true GLS.

Example Var[i] = 2 [Exp(zi)]2.

True GLS would regress y/[ Exp(zi)] on the same transformation of xi.With a consistent estimator of [,], say [s,c], we do the same computation with our estimates.So long as plim [s,c] = [,], FGLS is as “good” as true GLS. Consistent Same Asymptotic Variance Same Asymptotic Normal Distribution

Part 21: Generalized Method of Moments21-8/67

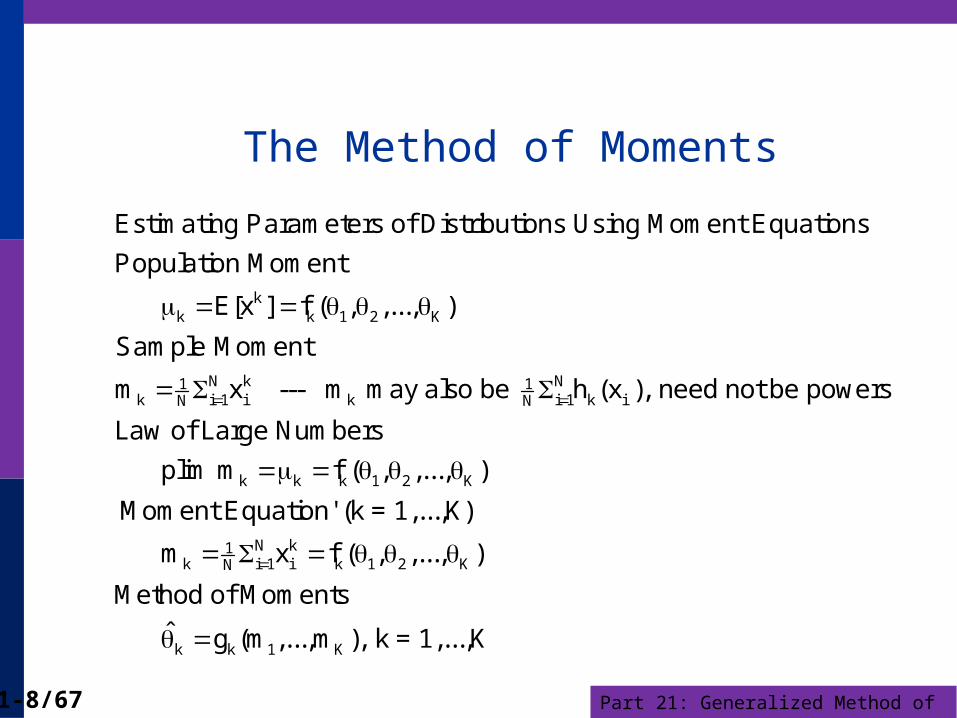

The Method of Moments

kk k 1 2 K

N k N1 1k i 1 i k i 1 k iN N

Estimating Parameters of Distributions Using Moment Equations

Population Moment

E[x ] f ( , ,..., )

Sample Moment

m x --- m may also be h (x ), need not be powers

Law of L

k k k 1 2 K

N k1k i 1 i k 1 2 KN

k k 1 K

arge Numbers

plim m f ( , ,..., )

'Moment Equation' (k = 1,...,K)

m x f ( , ,..., )

Method of Moments

ˆ g (m ,...,m ), k = 1,...,K

Part 21: Generalized Method of Moments21-9/67

Estimating a Parameter

Mean of Poisson p(y)=exp(-λ) λy / y! E[y]= λ.

plim (1/N)Σiyi = λ. This is the estimator

Mean of Exponential p(y) = λ exp(- λy) E[y] = 1/ λ.

plim (1/N)Σiyi = 1/λ

Part 21: Generalized Method of Moments21-10/67

Mean and Variance of a Normal Distribution

2

2

2 2 2

N N 2 2 21 1i 1 i i 1 iN N

2 N 2 2 N 21 1i 1 i i 1 iN n

1 (y )p(y) exp

22

Population Moments

E[y] , E[y ]

Moment Equations

y , y

Method of Moments Estimators

ˆ=y, ˆ y (y ) (y y)

Part 21: Generalized Method of Moments21-11/67

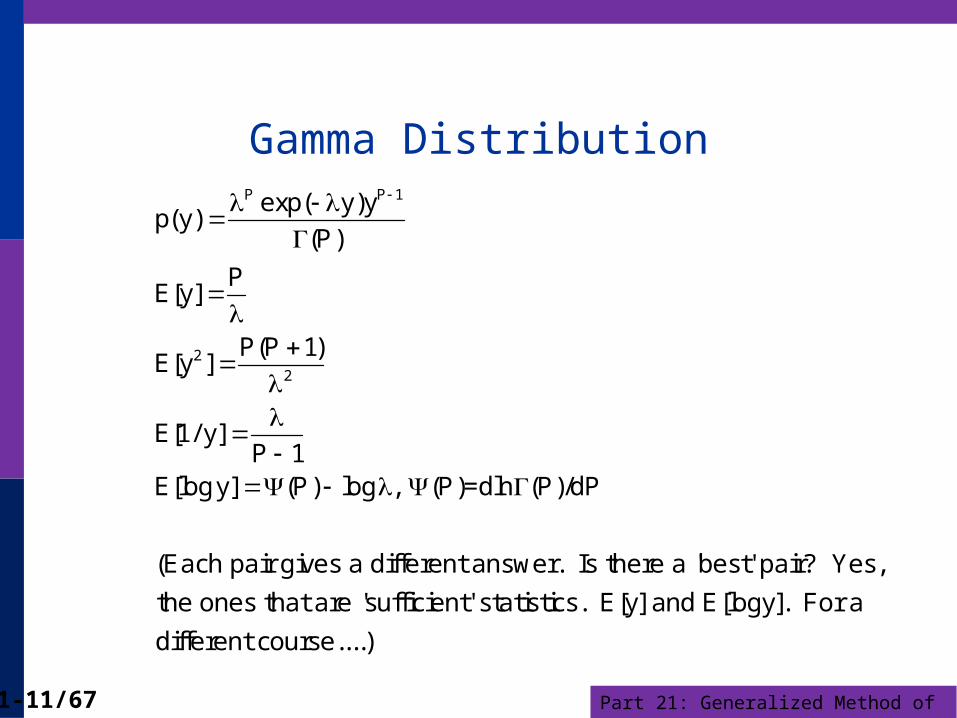

Gamma DistributionP P 1

22

exp( y)yp(y)

(P)

PE[y]

P(P 1)E[y ]

E[1/ y]P 1

E[logy] (P) log , (P)=dln (P)/dP

(Each pair gives a different answer. Is there a 'best' pair? Yes,

the ones that are 'sufficient' statistics.

E[y] and E[logy]. For a

different course....)

Part 21: Generalized Method of Moments21-12/67

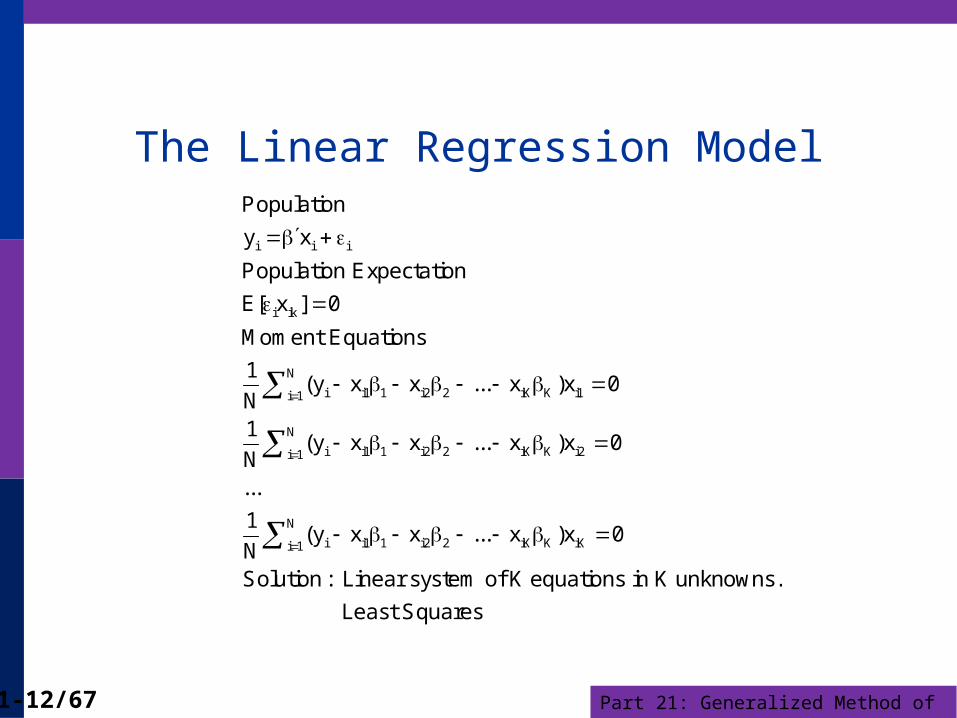

The Linear Regression Model

i i i

i ik

N

i i1 1 i2 2 iK K i1i 1

N

i i1 1 i2 2 iK K i2i 1

N

i i1 1 i2 2 iK K iKi 1

Population

y x

Population Expectation

E[ x ] 0

Moment Equations

1(y x x ... x )x 0

N1

(y x x ... x )x 0N...

1(y x x ... x )x 0

NSolution : Linea

r system of K equations in K unknowns.

Least Squares

Part 21: Generalized Method of Moments21-13/67

Instrumental Variables

i i i

i ik 1 K

N

i i1 1 i2 2 iK K i1i 1

N

i i1 1 i2 2 iK K i2i 1

i i1 1i 1

Population

y x

Population Expectation

E[ z ] 0 for instrumental variables z ... z .

Moment Equations

1(y x x ... x )z 0

N1

(y x x ... x )z 0N...

1(y x

N

N

i2 2 iK K iK

-1IV

x ... x )z 0

Solution : Also a linear system of K equations in K unknowns.

b = ( )

Z'X Z'y/n ( /n)

Part 21: Generalized Method of Moments21-14/67

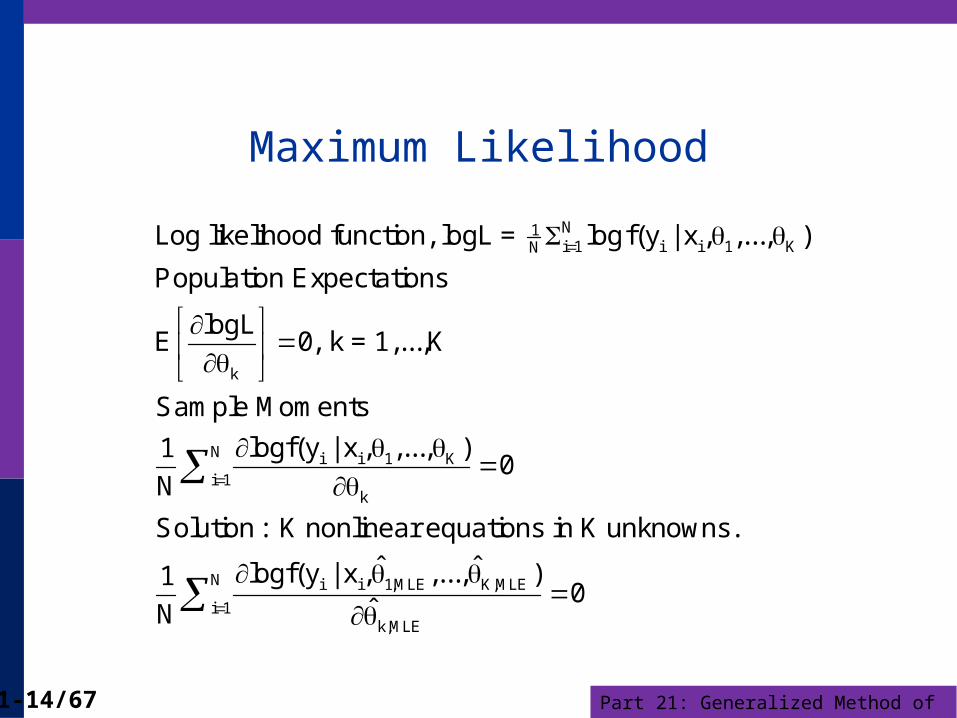

Maximum Likelihood

N1i 1 i i 1 KN

k

N i i 1 Ki 1

k

Log likelihood function, logL = logf(y | x , ,..., )

Population Expectations

logLE 0, k = 1,...,K

Sample Moments

logf(y | x , ,..., )10

N

Solution : K nonlinear equations in K un

N i i 1,MLE K,MLE

i 1k,MLE

knowns.

ˆ ˆlogf(y | x , ,..., )10

ˆN

Part 21: Generalized Method of Moments21-15/67

Behavioral Application

t 1t t

t

t

t

t+1 t 1 t

t t 1 t

Life Cycle Consumption (text, page 455)

c1E (1 r) 1 0

1 c

discount rate

c consumption

information at time t

Let =1/(1+ ), R c / c , =-

E [ (1 r)R 1| ] 0

What is in the information set? Each piece of 'information'

provides a moment equation for estimation of the two parameters.

Part 21: Generalized Method of Moments21-16/67

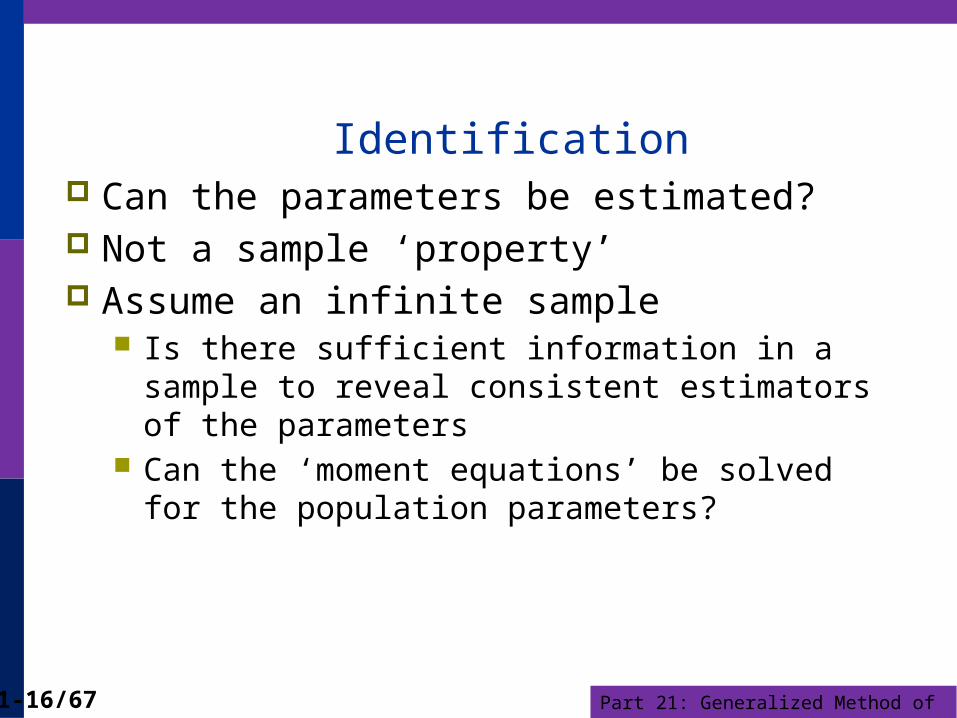

Identification Can the parameters be estimated? Not a sample ‘property’ Assume an infinite sample

Is there sufficient information in a sample to reveal consistent estimators of the parameters

Can the ‘moment equations’ be solved for the population parameters?

Part 21: Generalized Method of Moments21-17/67

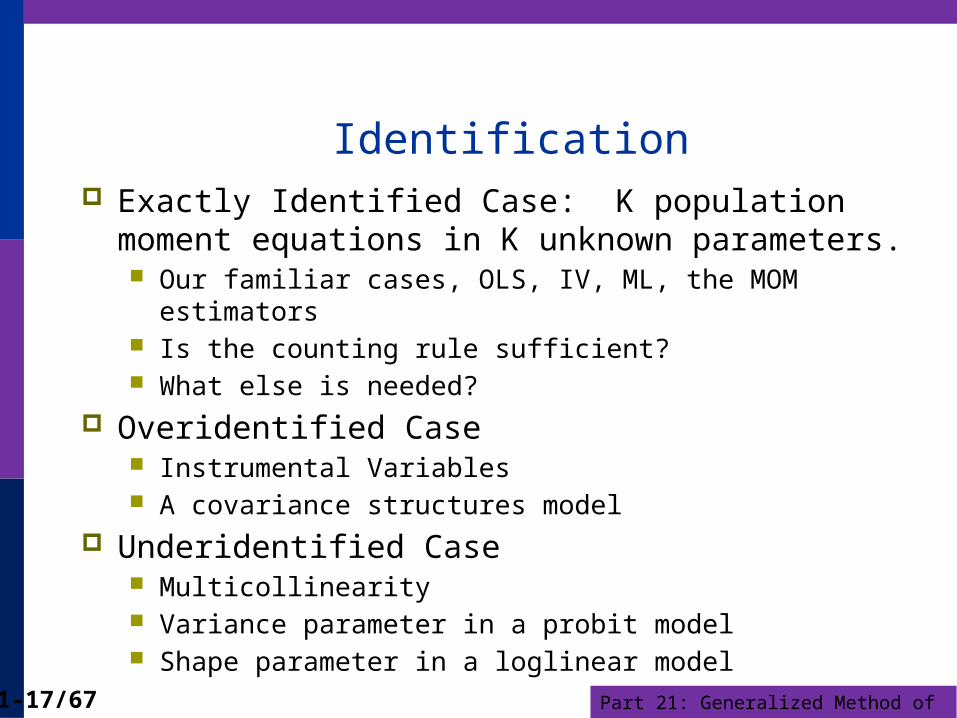

Identification Exactly Identified Case: K population moment equations

in K unknown parameters. Our familiar cases, OLS, IV, ML, the MOM estimators Is the counting rule sufficient? What else is needed?

Overidentified Case Instrumental Variables A covariance structures model

Underidentified Case Multicollinearity Variance parameter in a probit model Shape parameter in a loglinear model

Part 21: Generalized Method of Moments21-18/67

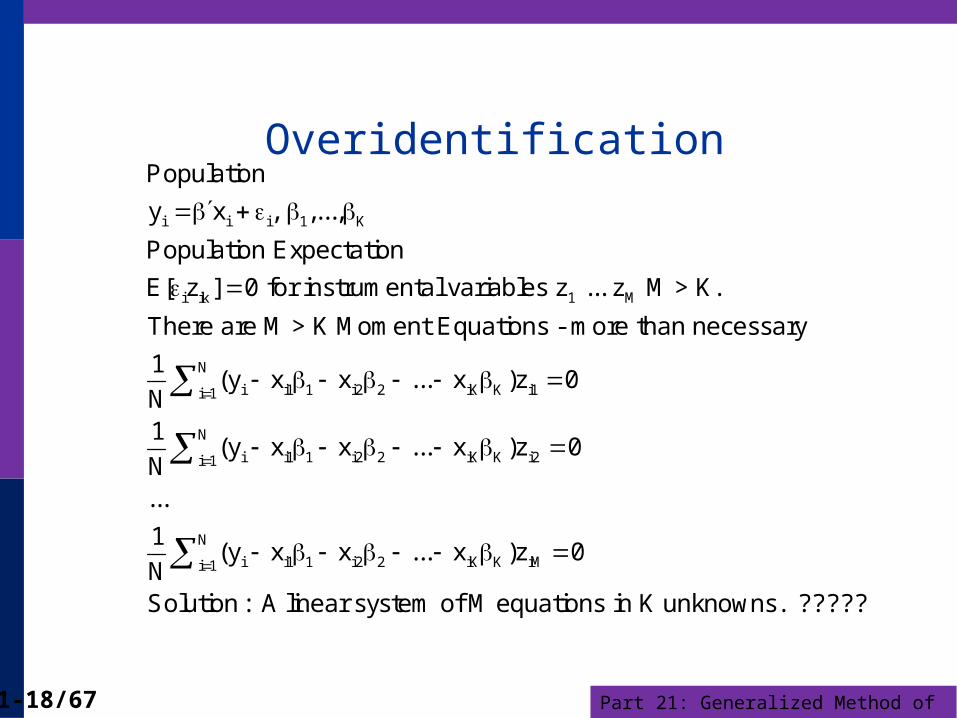

Overidentification

i i i 1 K

i ik 1 M

N

i i1 1 i2 2 iK K i1i 1

Population

y x , ,...,

Population Expectation

E[ z ] 0 for instrumental variables z ... z M > K.

There are M > K Moment Equations - more than necessary

1(y x x ... x )z 0

N1

N

i i1 1 i2 2 iK K i2i 1

N

i i1 1 i2 2 iK K iMi 1

(y x x ... x )z 0N...

1(y x x ... x )z 0

NSolution : A linear system of M equations in K unknowns. ?????

Part 21: Generalized Method of Moments21-19/67

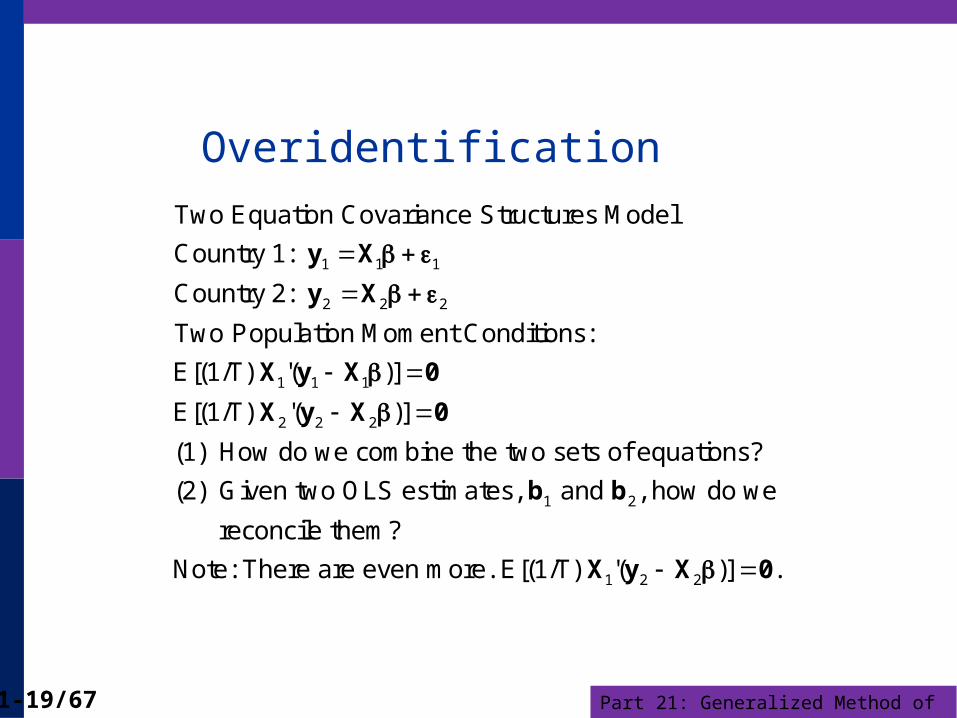

Overidentification

1 1 1

2 2 2

1 1 1

2 2 2

Two Equation Covariance Structures Model

Country 1:

Country 2:

Two Population Moment Conditions:

E[(1/T) '( )]

E[(1/T) '( )]

(1) How do we combine the two sets of eq

y X

y X

X y X 0

X y X 0

1 2

1 2 2

uations?

(2) Given two OLS estimates, and , how do we

reconcile them?

Note: There are even more. E[(1/T) '( )] .

b b

X y X 0

Part 21: Generalized Method of Moments21-20/67

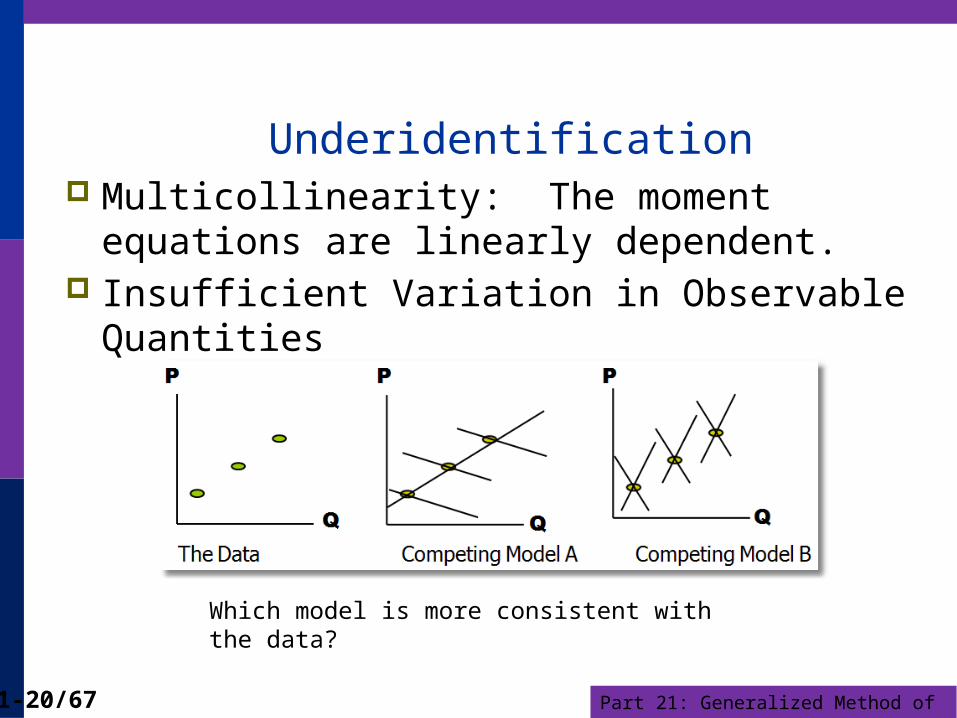

Underidentification Multicollinearity: The moment equations are

linearly dependent. Insufficient Variation in Observable Quantities

Which model is more consistent with the data?

Part 21: Generalized Method of Moments21-21/67

Underidentification – Model/Data

z

x

i i i

i i 0 i0

i

Consider the Mover - Stayer Model

Binary choice for whether an individual 'moves' or 'stays'

d 1( u 0)

Outcome equation for the individual, conditional on the state:

y | (d 0) =

y | (d 1)

xi 1 i1

2 2i0 i1 0 1 0 1

=

( , ) ~N[(0,0),( , , )]

An individual either moves or stays, but not both (or neither).

The parameter cannot be estimated with the observed data

regardless of the sample size.

It is unidentified.

Part 21: Generalized Method of Moments21-22/67

Underidentification - Math

0

0 1

1

0 1

When a parameter is unidentified, the log likelihood is invariant

to changes in it. Consider the logit binary choice model

exp( x)Prob[y=0]=

exp( x) exp( x)

exp( x)Prob[y=1]=

exp( x) exp( x)

Probabil

0 0

0 1 0 1

1 1

0 1 0

ities sum to 1, are monotonic, etc. But, consider, for any 0,

exp[( )x] exp( x)Prob[y=0]=

exp[( )x] exp[( )x] exp( x) exp( x)

exp[( )x] exp( x)Prob[y=1]=

exp[( )x] exp[( )x] exp( x

1

0

) exp( x)

The parameters are unidentified. A normalization such as 0 is needed.

Part 21: Generalized Method of Moments21-23/67

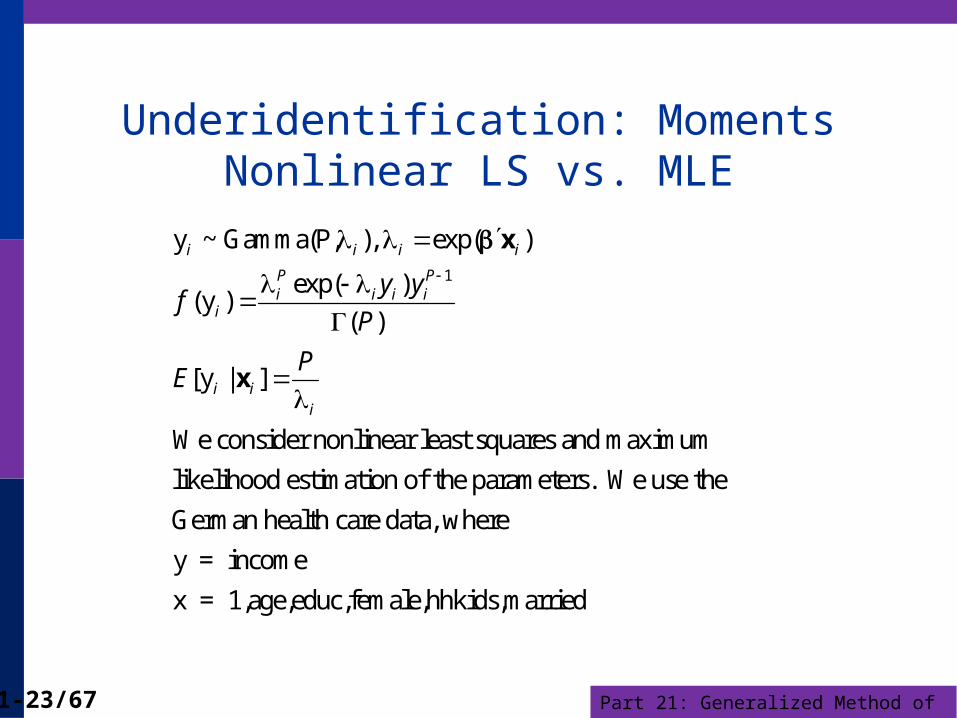

Underidentification: MomentsNonlinear LS vs. MLE

1

y ~ Gamma(P, ), exp( )

exp( )(y )

( )

[y | ]

We consider nonlinear least squares and maximum

likelihood estimation of the parameters. We use the

German health care data, where

y

i i i i

P Pi i i i

i

i ii

y yf

P

PE

x

x

= income

x = 1,age,educ,female,hhkids,married

Part 21: Generalized Method of Moments21-24/67

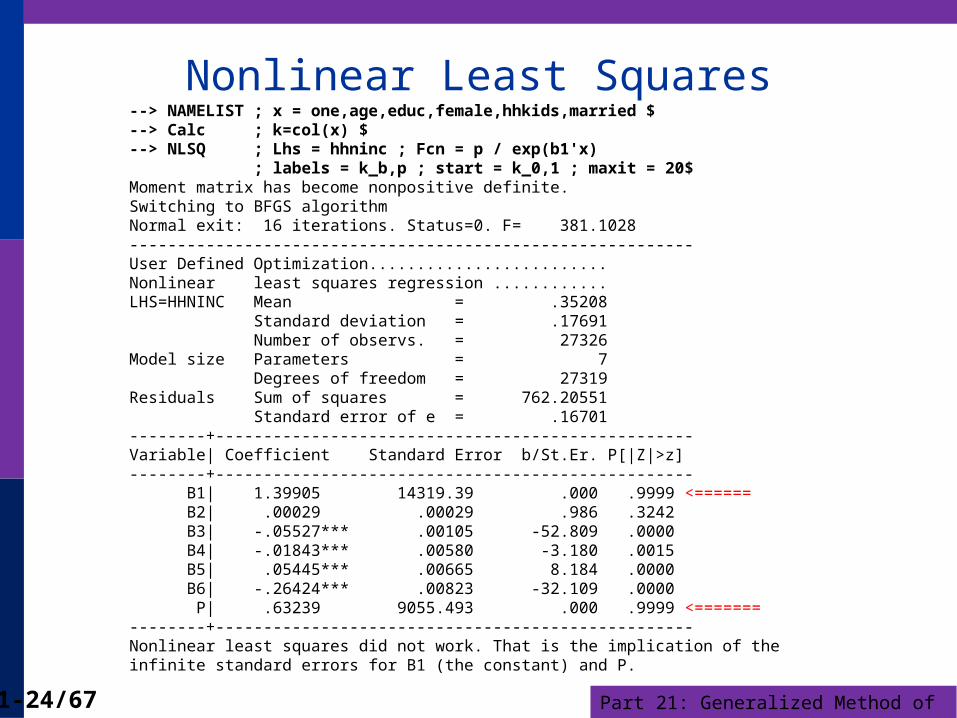

Nonlinear Least Squares--> NAMELIST ; x = one,age,educ,female,hhkids,married $--> Calc ; k=col(x) $--> NLSQ ; Lhs = hhninc ; Fcn = p / exp(b1'x) ; labels = k_b,p ; start = k_0,1 ; maxit = 20$Moment matrix has become nonpositive definite.Switching to BFGS algorithmNormal exit: 16 iterations. Status=0. F= 381.1028-----------------------------------------------------------User Defined Optimization.........................Nonlinear least squares regression ............LHS=HHNINC Mean = .35208 Standard deviation = .17691 Number of observs. = 27326Model size Parameters = 7 Degrees of freedom = 27319Residuals Sum of squares = 762.20551 Standard error of e = .16701--------+--------------------------------------------------Variable| Coefficient Standard Error b/St.Er. P[|Z|>z]--------+-------------------------------------------------- B1| 1.39905 14319.39 .000 .9999 <====== B2| .00029 .00029 .986 .3242 B3| -.05527*** .00105 -52.809 .0000 B4| -.01843*** .00580 -3.180 .0015 B5| .05445*** .00665 8.184 .0000 B6| -.26424*** .00823 -32.109 .0000 P| .63239 9055.493 .000 .9999 <=======--------+--------------------------------------------------Nonlinear least squares did not work. That is the implication of theinfinite standard errors for B1 (the constant) and P.

Part 21: Generalized Method of Moments21-25/67

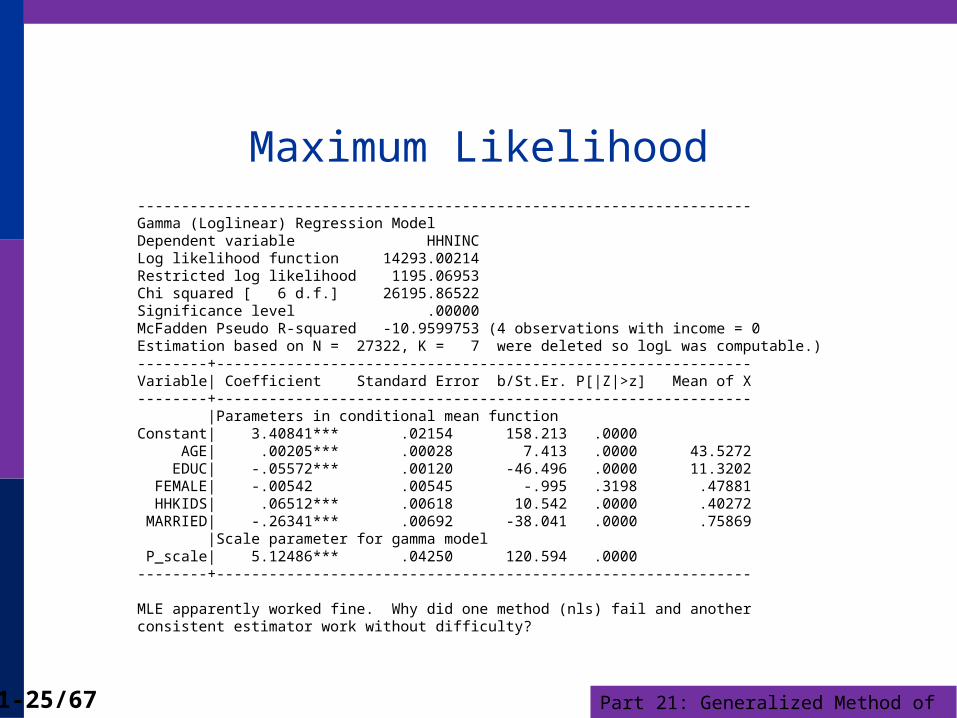

Maximum Likelihood----------------------------------------------------------------------Gamma (Loglinear) Regression ModelDependent variable HHNINCLog likelihood function 14293.00214Restricted log likelihood 1195.06953Chi squared [ 6 d.f.] 26195.86522Significance level .00000McFadden Pseudo R-squared -10.9599753 (4 observations with income = 0Estimation based on N = 27322, K = 7 were deleted so logL was computable.)--------+-------------------------------------------------------------Variable| Coefficient Standard Error b/St.Er. P[|Z|>z] Mean of X--------+------------------------------------------------------------- |Parameters in conditional mean functionConstant| 3.40841*** .02154 158.213 .0000 AGE| .00205*** .00028 7.413 .0000 43.5272 EDUC| -.05572*** .00120 -46.496 .0000 11.3202 FEMALE| -.00542 .00545 -.995 .3198 .47881 HHKIDS| .06512*** .00618 10.542 .0000 .40272 MARRIED| -.26341*** .00692 -38.041 .0000 .75869 |Scale parameter for gamma model P_scale| 5.12486*** .04250 120.594 .0000--------+-------------------------------------------------------------

MLE apparently worked fine. Why did one method (nls) fail and another consistent estimator work without difficulty?

Part 21: Generalized Method of Moments21-26/67

Moment Equations: NLS

2

1 1

1

1

1

[ | ] / exp( )

' / exp( )

2'0

exp( )

2'

exp( )

Consider the term for the constant in the model, . Notice that

the first order condition for

i

N N

i i ii i

N ii

i

N iii

i

E y P

y P e

e

P

e P

x x

e e x

e e

x

e ex 0

x

1

1

the constant term is

20. This doesn't depend on P, since we can divide

exp( )

both sides of the equation by P. This means that we cannot find

solutions for both and P. It is easy to see

N ii

i

e P

x

1 1

1

why NLS cannot distinguish

P from . E[y|x] = exp((logP- ) ...). There are an infinite number

of pairs of (P, ) that produce the same constant term in the model.

Part 21: Generalized Method of Moments21-27/67

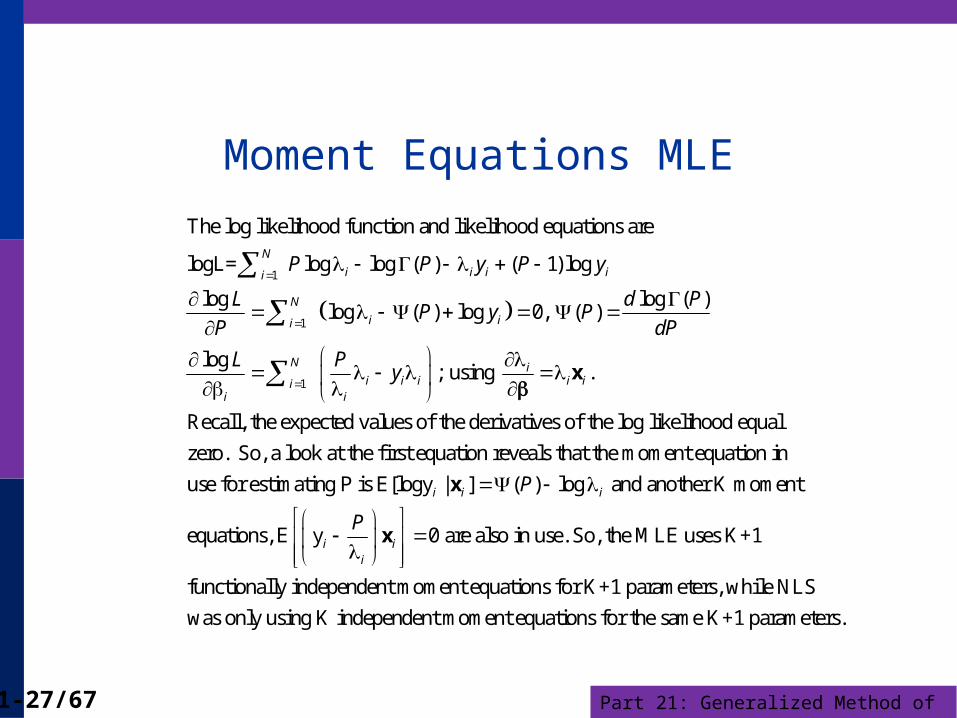

Moment Equations MLE

1

1

1

The log likelihood function and likelihood equations are

logL= log log ( ) ( 1) log

log log ( )log ( ) log 0, ( )

log; using .

Recall

N

i i i ii

N

i ii

N ii i i i ii

i i

P P y P y

L d PP y P

P dP

L Py

x

, the expected values of the derivatives of the log likelihood equal

zero. So, a look at the first equation reveals that the moment equation in

use for estimating P is E[logy | ] ( ) log and anothei i iP x r K moment

equations, E y 0 are also in use. So, the MLE uses K+1

functionally independent moment equations for K+1 parameters, while NLS

was only using K independent moment equation

i ii

P

x

s for the same K+1 parameters.

Part 21: Generalized Method of Moments21-28/67

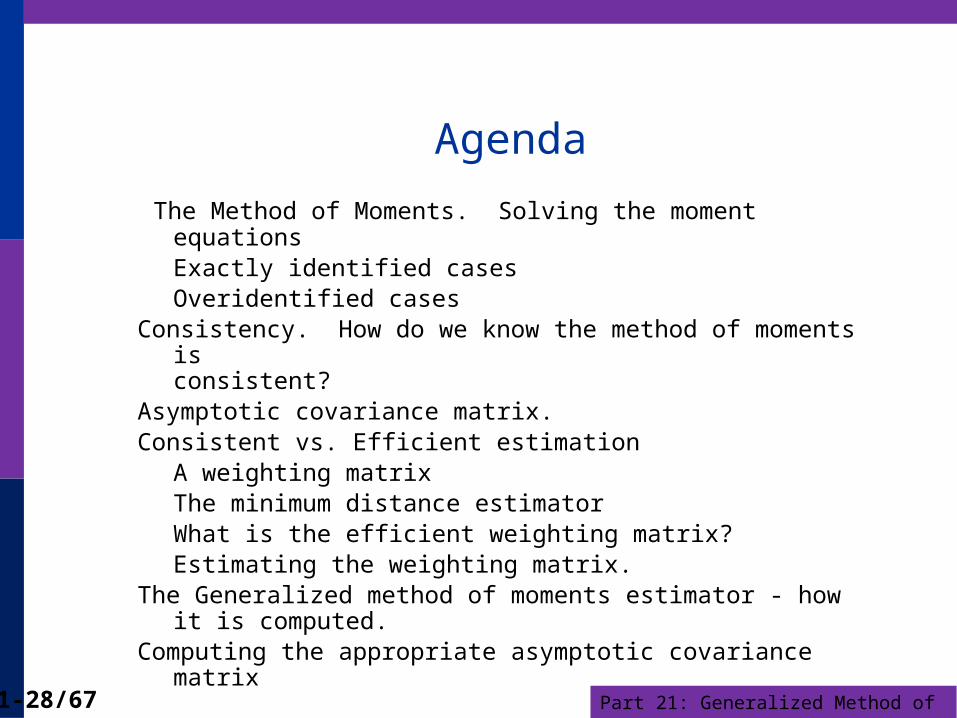

Agenda

The Method of Moments. Solving the moment equationsExactly identified casesOveridentified cases

Consistency. How do we know the method of moments is consistent?

Asymptotic covariance matrix.Consistent vs. Efficient estimation

A weighting matrixThe minimum distance estimatorWhat is the efficient weighting matrix?Estimating the weighting matrix.

The Generalized method of moments estimator - how it is computed.Computing the appropriate asymptotic covariance matrix

Part 21: Generalized Method of Moments21-29/67

The Method of MomentsMoment Equation: Defines a sample statistic that

mimics a population expectation:

The population expectation – orthogonality condition:

E[ mi () ] = 0. Subscript i indicates it depends on data vector indexed by 'i' (or 't' for a time series setting)

Part 21: Generalized Method of Moments21-30/67

The Method of Moments - Example

P P 1i i

i

i i

N1 i=1 i

N2 i=1 i

Gamma Distribution Parameters

exp( y )yp(y )

(P)

Population Moment Conditions

PE[y ] , E[logy ] (P) log

Moment Equations:

E[m ( ,P)] = E[{(1/n) y } P / ] 0

E[m ( ,P)] = E[{(1/n) logy } (

(P) log )] 0

Part 21: Generalized Method of Moments21-31/67

Application

2 21 1 2 2

2 21 2

1

2

Solving the moment equations

Use least squares:

Minimize {m E[m ]} {m E[m ]}

(m (P / )) (m ( (P) log ))

m 31.278

m 3.221387

Plot of Psi(P) Function

P

-10

-8

-6

-4

-2

0

2

-12

1 2 3 4 5 60

PSI

Part 21: Generalized Method of Moments21-32/67

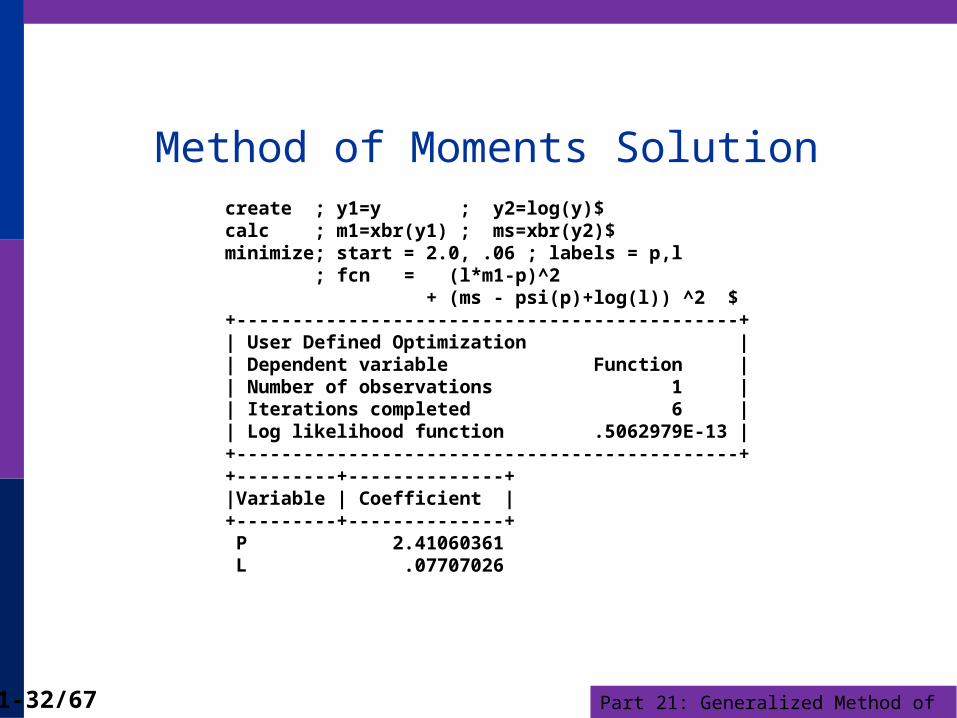

Method of Moments Solutioncreate ; y1=y ; y2=log(y)$calc ; m1=xbr(y1) ; ms=xbr(y2)$minimize; start = 2.0, .06 ; labels = p,l ; fcn = (l*m1-p)^2 + (ms - psi(p)+log(l)) ^2 $+---------------------------------------------+| User Defined Optimization || Dependent variable Function || Number of observations 1 || Iterations completed 6 || Log likelihood function .5062979E-13 |+---------------------------------------------++---------+--------------+ |Variable | Coefficient | +---------+--------------+ P 2.41060361 L .07707026

Part 21: Generalized Method of Moments21-33/67

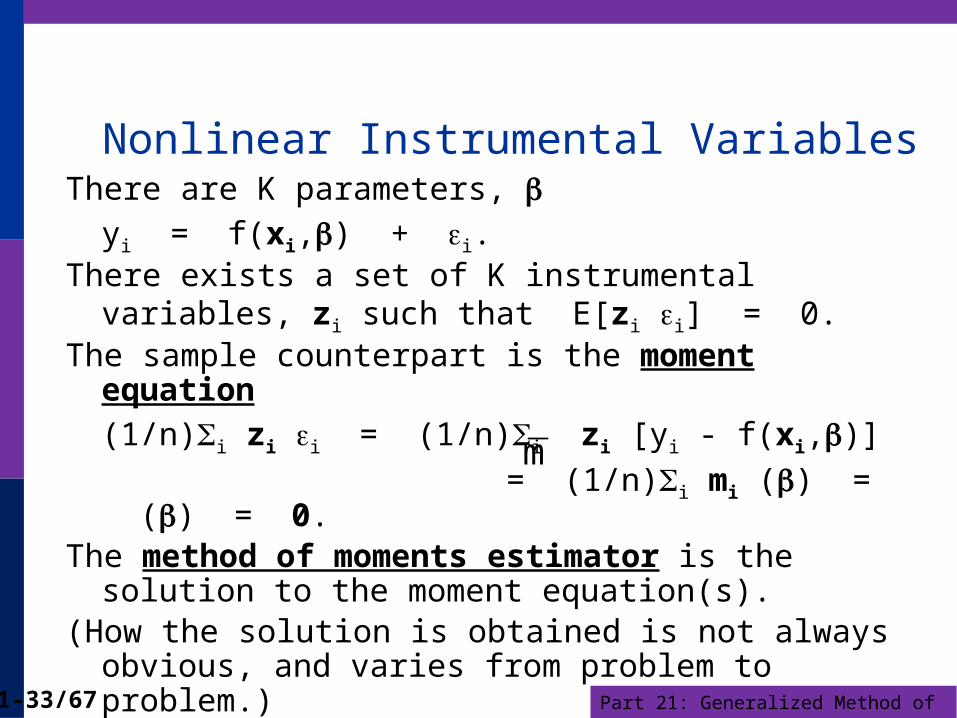

Nonlinear Instrumental VariablesThere are K parameters,

yi = f(xi,) + i.

There exists a set of K instrumental variables, zi such that E[zi i] = 0.

The sample counterpart is the moment equation

(1/n)i zi i = (1/n)i zi [yi - f(xi,)] = (1/n)i mi () = () = 0.The method of moments estimator is the solution to the

moment equation(s). (How the solution is obtained is not always obvious, and

varies from problem to problem.)

m

Part 21: Generalized Method of Moments21-34/67

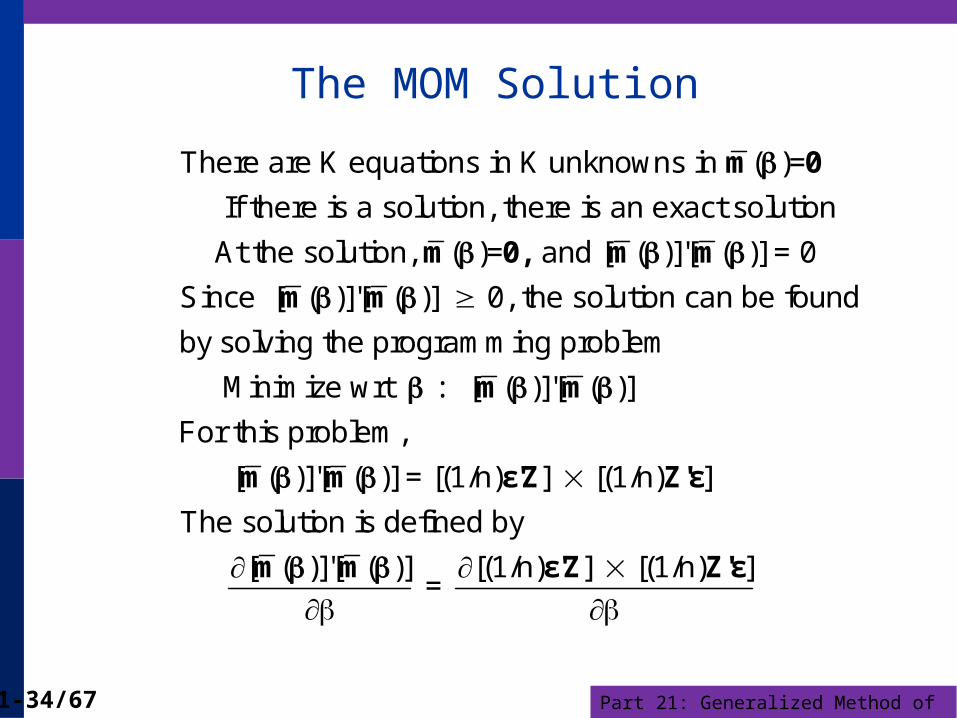

The MOM Solution

There are K equations in K unknowns in ( )=

If there is a solution, there is an exact solution

At the solution, ( )= and [ ( )]'[ ( )] = 0

Since [ ( )]'[ ( )] 0, the solution can be fou

m 0

m 0, m m

m m

nd

by solving the programming problem

Minimize wrt : [ ( )]'[ ( )]

For this problem,

[ ( )]'[ ( )] = [(1/n) ] [(1/n) ]

The solution is defined by

[ ( )]'[ ( )] [(1/n) ] =

m m

m m

m m

ε'Z Z'ε

ε'Z [(1/n) ]

Z'ε

Part 21: Generalized Method of Moments21-35/67

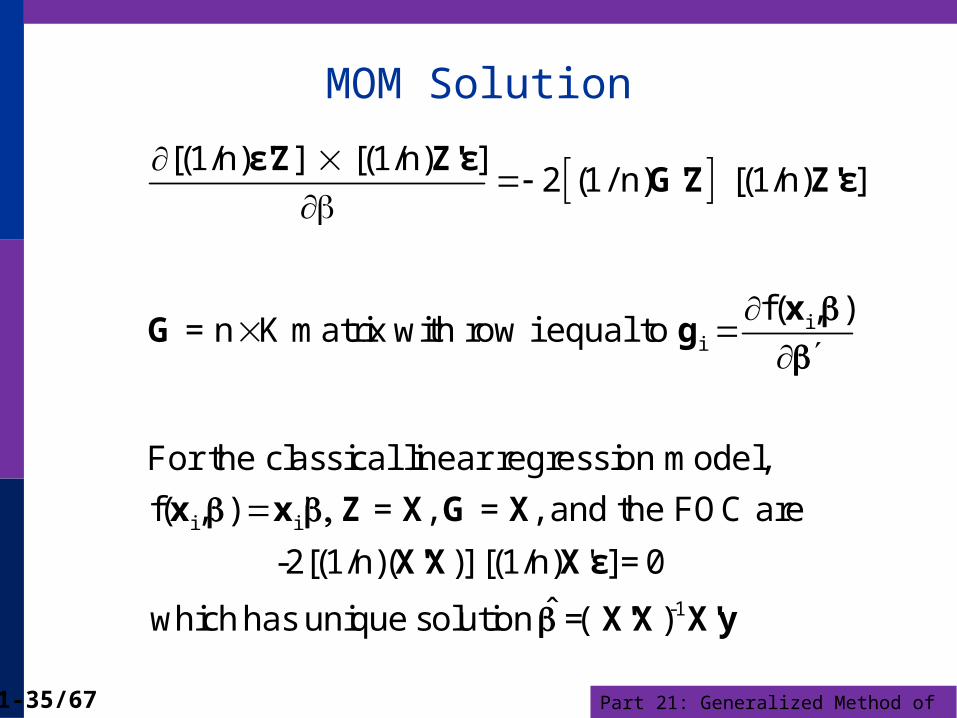

MOM Solution

ii

i i

[(1/n) ] [(1/n) ]2 (1/ n) [(1/n) ]

f( , ) = n K matrix with row i equal to

For the classical linear regression model,

f( , ) ' = , = , and the FOC are

-2[(1

xG g

x x Z X G X

ε'Z Z'εG'Z Z'ε

/n)( )] [(1/n) '

ˆ

X'X X

X'X X'y

ε-1

] = 0

which has unique solution =( )

Part 21: Generalized Method of Moments21-36/67

Variance of the Method of Moments Estimator

n

ii 1

i i

-1 -1

The MOM estimator solves m( )=

1 1( )= ( ) so the variance is for some

n NGenerally, = E[ ( ) ( ) ]

The asymptotic covariance matrix of the estimator is

1Asy.Var[ ]=( ) ( ) w

N

0

MOM

β

m β m β Ω Ω

Ω m β m β '

β G Ω G'( )

here m β

G=β'

Part 21: Generalized Method of Moments21-37/67

Example 1: Gamma Distribution

2

n1 P1 i 1 in

n12 i 1 in

i i i

i i i

1 PN

i 1 1

m (y )

m (logy (P) log )

Var(y ) Cov(y ,logy )1 1Cov(y ,logy ) Var(logy )n n

1

n '(P)G

Part 21: Generalized Method of Moments21-38/67

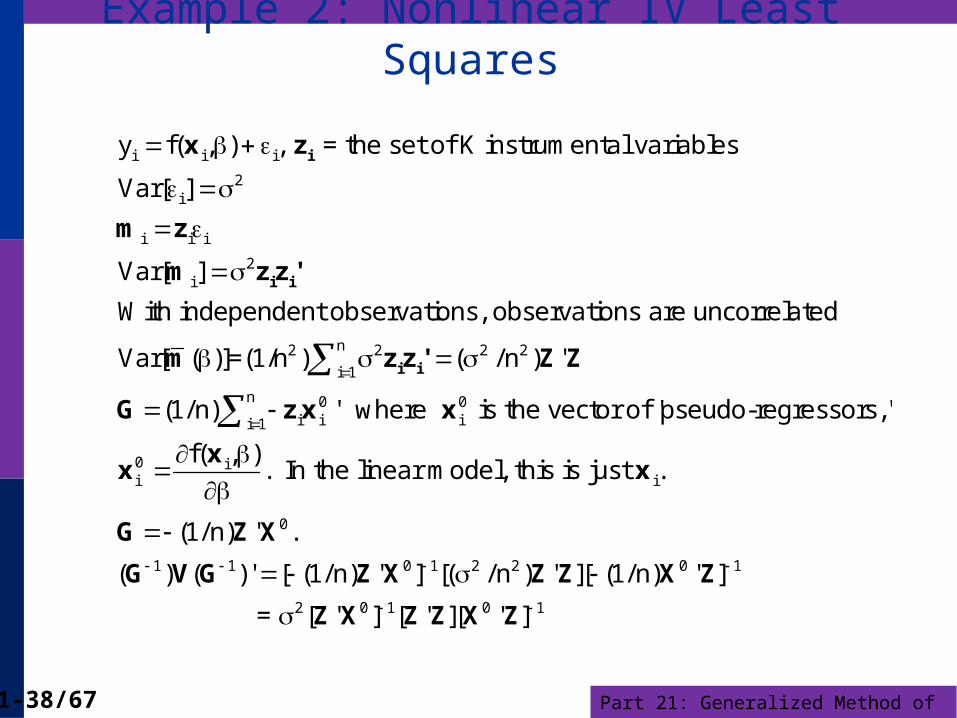

Example 2: Nonlinear IV Least Squares

i i i

2i

i i i

2i

n2 2 2 2

i 1

0i i

y f( , ) , = the set of K instrumental variables

Var[ ]

Var[ ]

With independent observations, observations are uncorrelated

Var[ ( )]=(1/n ) ( /n ) '

(1/n) '

i

i i

i i

x z

m z

m zz'

m zz' Z Z

G zx

n 0ii 1

0 ii i

0

1 1 0 1 2 2 0 1

2

where is the vector of 'pseudo-regressors,'

f( , ). In the linear model, this is just .

(1/n) ' .

( ) ( )' [ (1/n) ' ] [( / n ) ' ][ (1/n) ' ]

= [

x

xx x

G Z X

G V G Z X Z Z X Z

Z 0 1 0 1' ] [ ' ][ ' ]X Z Z X Z

Part 21: Generalized Method of Moments21-39/67

Variance of the Moments

i

n

i i i ii=1

n

i ii=1

How to estimate = (1/n) = Var[ ( )]

Var[ ( )]=(1/n)Var[ ( )] = (1/n)

Estimate Var[ ( )] with Est.Var[ ( )] = (1/n) ( ) ( )'

Then,

ˆ ˆ ˆ(1/ n) (1/ n) ( ) ( )'

For the linear regression

V m

m m

m m m m

V m m

i i i

n n 2i i i i i i ii=1 i=1

n-1 2 -1MOM i i ii=1

n-1 2 -1i i ii=1

model,

,

ˆ (1/ n) (1/ n) e e (1/ n) (1/ n) e

(1/ n)

Est.Var[b ] [(1/ n) ] [(1/ n) (1/ n) e ][(1/ n) ]

= [ ] [ e ][ ]

m x

V x x' x x'

G X'X

X'X x x' X'X

X'X x x' X'X (familiar?)

Part 21: Generalized Method of Moments21-40/67

Properties of the MOM Estimator Consistent?

The LLN implies that the moments are consistent estimators of their population counterparts (zero)

Use the Slutsky theorem to assert consistency of the functions of the moments

Asymptotically normal? The moments are sample means. Invoke a central limit theorem.

Efficient? Not necessarily Sometimes yes. (Gamma example) Perhaps not. Depends on the model and the available

information (and how much of it is used).

Part 21: Generalized Method of Moments21-41/67

Generalizing the Method of Moments Estimator

More moments than parameters – the overidentified case

Example: Instrumental variable case, M > K instruments

Part 21: Generalized Method of Moments21-42/67

Two Stage Least SquaresHow to use an “excess” of instrumental variables

(1) X is K variables. Some (at least one) of the K

variables in X are correlated with ε.

(2) Z is M > K variables. Some of the variables in

Z are also in X, some are not. None of the

variables in Z are correlated with ε.

(3) Which K variables to use to compute Z’X and

Z’y?

Part 21: Generalized Method of Moments21-43/67

Choosing the Instruments Choose K randomly? Choose the included Xs and the remainder randomly? Use all of them? How? A theorem: (Brundy and Jorgenson, ca. 1972) There is a

most efficient way to construct the IV estimator from this subset: (1) For each column (variable) in X, compute the predictions of

that variable using all the columns of Z. (2) Linearly regress y on these K predictions.

This is two stage least squares

Part 21: Generalized Method of Moments21-44/67

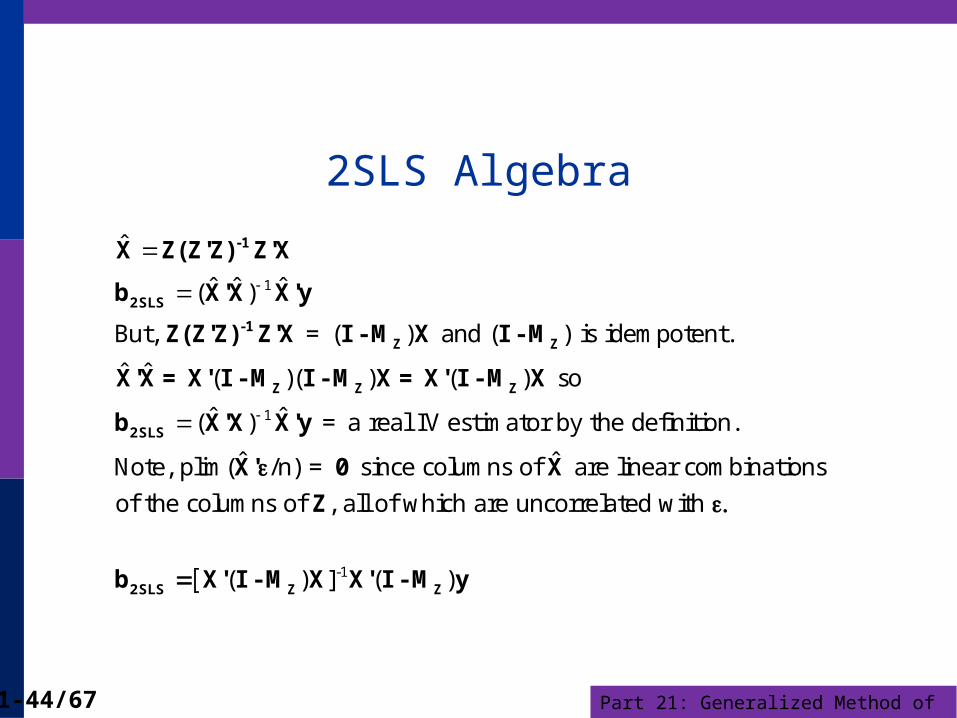

2SLS Algebra

1

1

ˆ

ˆ ˆ ˆ( )

But, = ( ) and ( ) is idempotent.

ˆ ˆ ( )( ) ( ) so

ˆ ˆ( ) = a real IV estimator by the definition.

ˆNote, plim( /n) =

-1

2SLS

-1Z Z

Z Z Z

2SLS

X Z(Z'Z) Z'X

b X'X X'y

Z(Z'Z) Z'X I -M X I -M

X'X= X' I -M I -M X= X' I -M X

b X'X X'y

X' 0

-1

ˆ since columns of are linear combinations

of the columns of , all of which are uncorrelated with

( ) ] ( )

2SLS Z Z

X

Z

b X' I -M X X' I -M y

Part 21: Generalized Method of Moments21-45/67

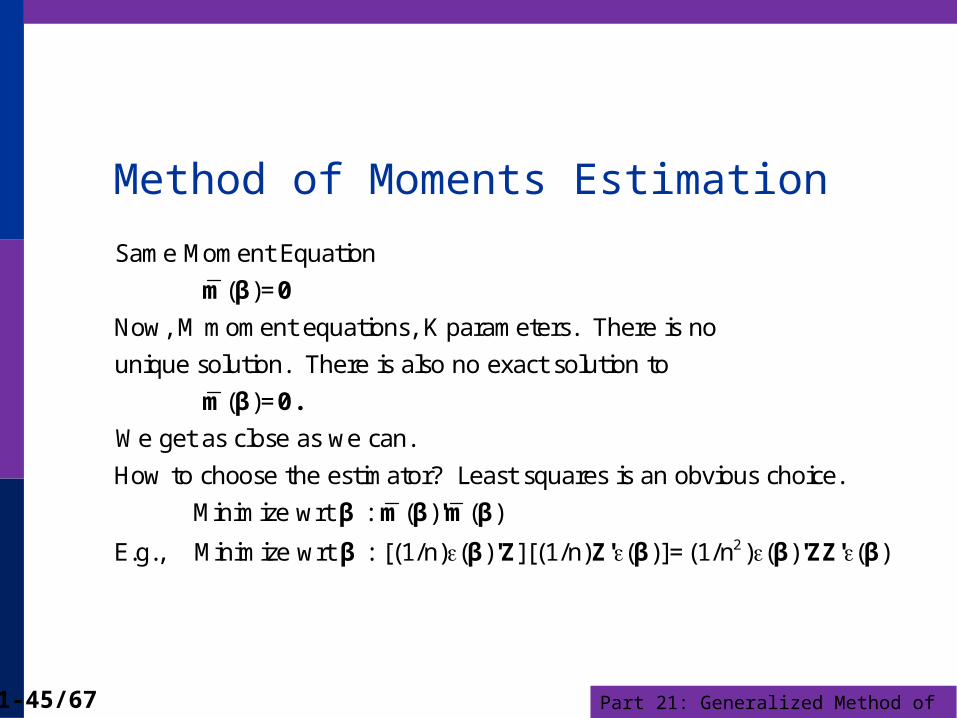

Method of Moments Estimation

m β 0

m β 0.

Same Moment Equation

( )=

Now, M moment equations, K parameters. There is no

unique solution. There is also no exact solution to

( )=

We get as close as we can.

How to cho

β m β 'm β

β β 'Z Z' β β 'ZZ' β2

ose the estimator? Least squares is an obvious choice.

Minimize wrt : ( ) ( )

E.g., Minimize wrt : [(1/n) ( ) ][(1/n) ( )]=(1/n ) ( ) ( )

Part 21: Generalized Method of Moments21-46/67

FOC for MOM

m β 'm β β= G β 'm β

β 'ZZ' β β = - X Z Z' y - Xβ

0

2 2

First order conditions

(1) General

( ) ( )/ 2 ( ) ( ) = 0

(2) The Instrumental Variables Problem

(1/n ) ( ) ( )/ (2/n )( ' )[ ( )]

=

Or,

X Z Z' y - Xβ 0

0

X Z Z' y - Xβ 0

Z' y - Xβ 0

( ' )[ ( )] =

(K M) (M N)(N 1) =

At the solution, ( ' )[ ( )] =

But, [ ( )] as it was before.

Part 21: Generalized Method of Moments21-47/67

Computing the Estimator

Programming Program No all purpose solution Nonlinear optimization problem –

solution varies from setting to setting.

Part 21: Generalized Method of Moments21-48/67

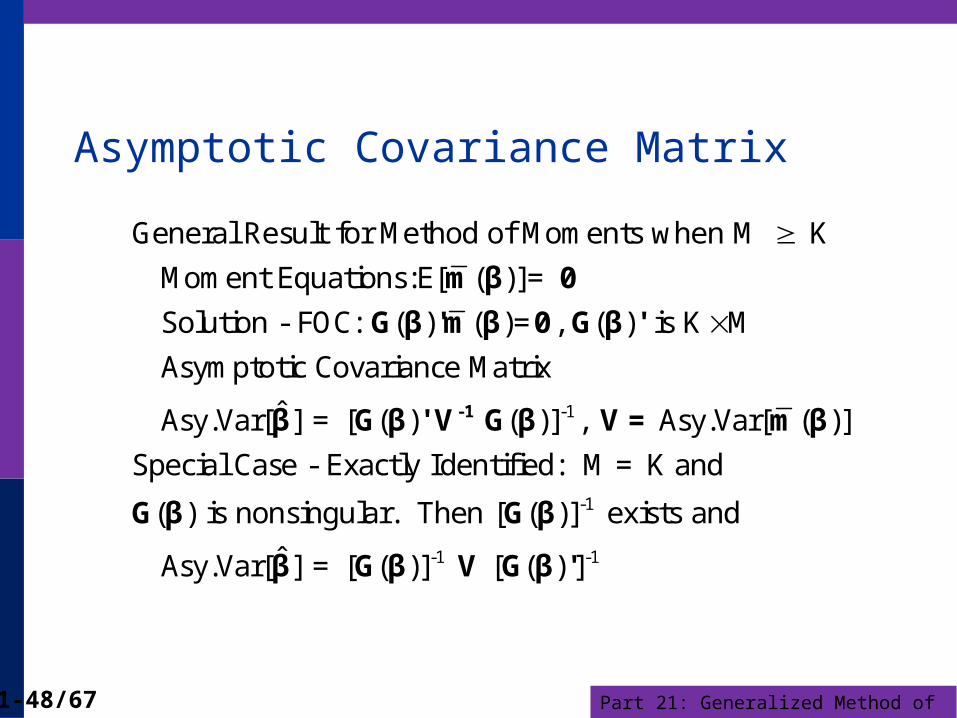

Asymptotic Covariance Matrix

-1

m β 0

G β 'm β 0 G β '

β G β ' V G β V= m-1

General Result for Method of Moments when M K

Moment Equations:E[ ( )]=

Solution - FOC: ( ) ( )= , ( ) is K M

Asymptotic Covariance Matrix

ˆ Asy.Var[ ] = [ ( ) ( )] , Asy.Var[ β

G β G β

β G β V G β '

-1

-1 -1

( )]

Special Case - Exactly Identified: M = K and

( ) is nonsingular. Then [ ( )] exists and

ˆ Asy.Var[ ] = [ ( )] [ ( ) ]

Part 21: Generalized Method of Moments21-49/67

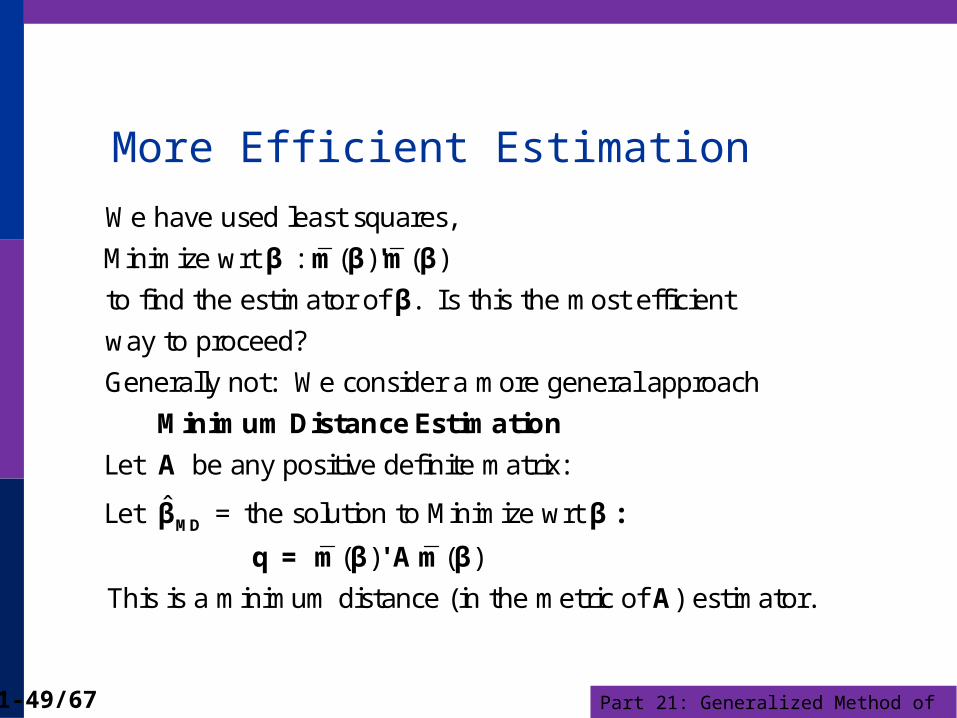

More Efficient Estimation

β m β 'm β

β

Minimum Distance Est

We have used least squares,

Minimize wrt : ( ) ( )

to find the estimator of . Is this the most efficient

way to proceed?

Generally not: We consider a more general approach

MD

imation

A

β β:

q = m β ' A m β

A

Let be any positive definite matrix:

ˆLet = the solution to Minimize wrt

( ) ( )

This is a minimum distance (in the metric of ) estimator.

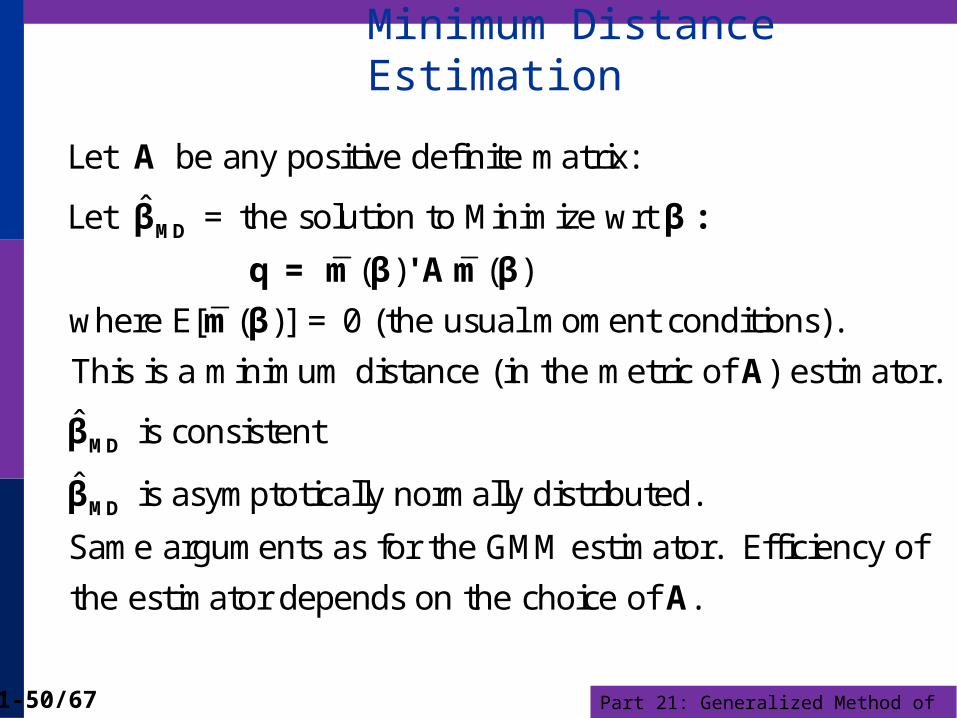

Part 21: Generalized Method of Moments21-50/67

Minimum Distance Estimation

MD

A

β β:

q = m β ' A m β

m β

Let be any positive definite matrix:

ˆLet = the solution to Minimize wrt

( ) ( )

where E[ ( )] = 0 (the usual moment conditions).

This is a minimum distance (in th

MD

MD

A

β

β

A

e metric of ) estimator.

ˆ is consistent

ˆ is asymptotically normally distributed.

Same arguments as for the GMM estimator. Efficiency of

the estimator depends on the choice of .

Part 21: Generalized Method of Moments21-51/67

MDE Estimation: Application

i iy Xβ ε ε X

b β

i i i

i

N units, T observations per unit, T > K

, E[ | ] 0

Consider the following estimation strategy:

(1) OLS country by country, produces N estimators of

(2) How to combine the estimators?

We hav

2

N

b β

b β0

...

b β

β?

1

e 'moment' equation: E

How can I combine the N estimators of

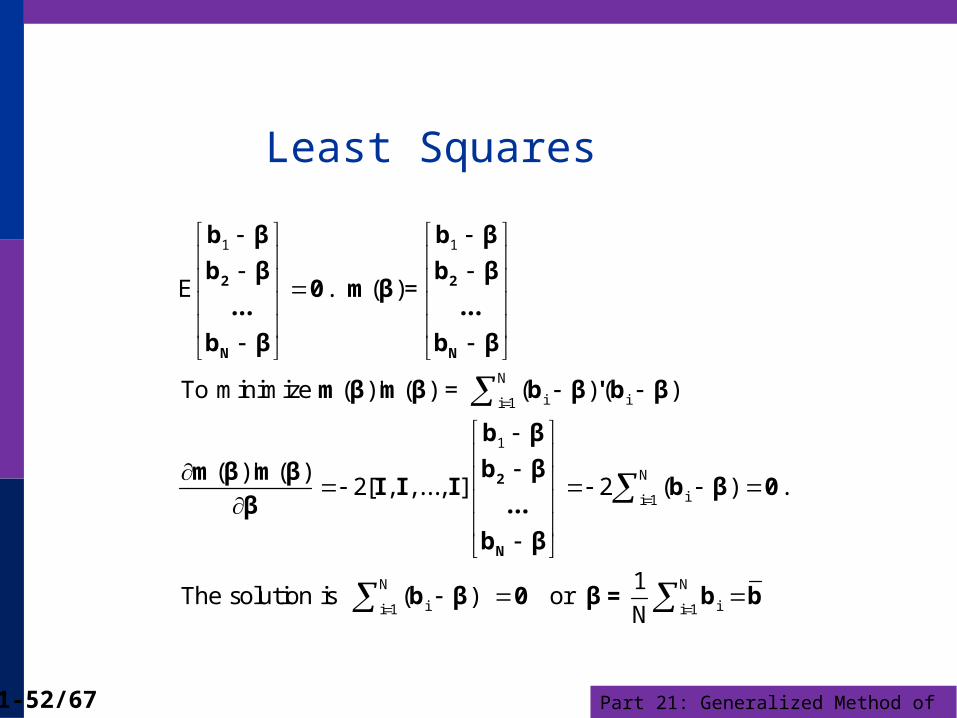

Part 21: Generalized Method of Moments21-52/67

Least Squares

2 2

N N

2

N

b β b β

b β b β0 m β

... ...

b β b β

m β m β b β ' b β

b β

b βm β m βI I I b β 0

...β

b β

b β

1 1

N

i ii 1

1

N

ii 1

i

E . ( )=

To minimize ( )' ( ) = ( ) ( )

( )' ( )2[ , ,..., ] 2 ( ) .

The solution is ( )

0 β= b bN N

ii 1 i 1

1 or

N

Part 21: Generalized Method of Moments21-53/67

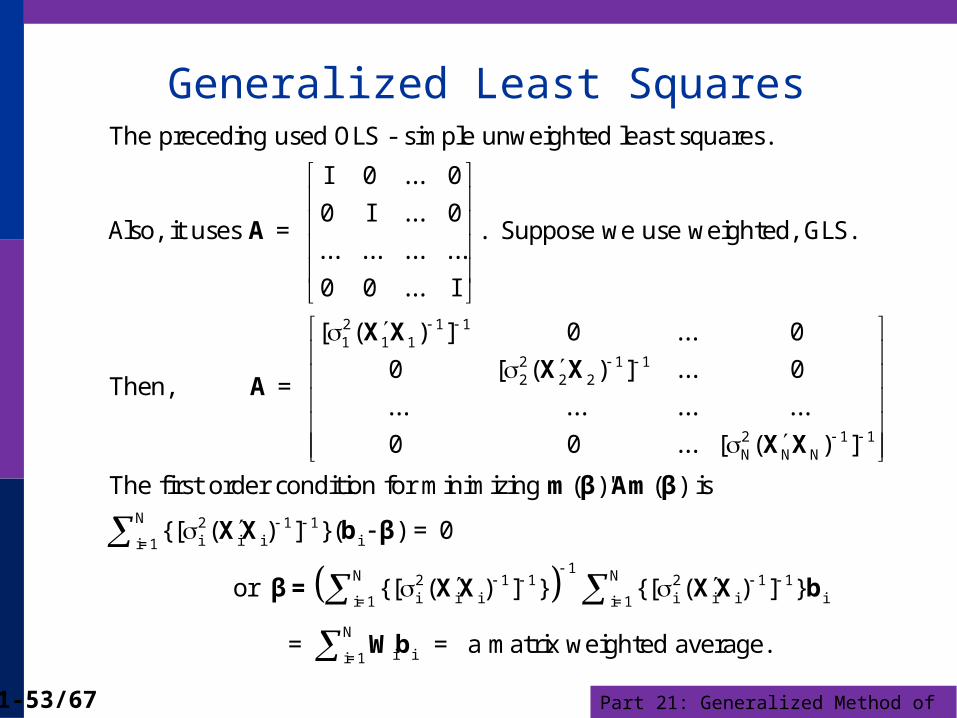

Generalized Least Squares

A

X X

X XA

2 1 11 1 1

22 2 2

The preceding used OLS - simple unweighted least squares.

I 0 ... 0

0 I ... 0Also, it uses = . Suppose we use weighted, GLS.

... ... ... ...

0 0 ... I

[ ( ) ] 0 ... 0

0 [ (Then, =

X X

m β Am β

XX b β

β = XX

1 1

2 1 1N N N

N 2 1 1i i i ii=1

1N 2 1 1 2i i i ii=1

) ] ... 0

... ... ... ...

0 0 ... [ ( ) ]

The first order condition for minimizing ( )' ( ) is

{[ ( ) ] }( ) = 0

or {[ ( ) ] } {[ (

XX b

Wb

N 1 1i i ii=1

N

i ii=1

) ] }

= = a matrix weighted average.

Part 21: Generalized Method of Moments21-54/67

Minimum Distance Estimation

The minimum distance estimator minimizes

( ) ( )

The estimator is

(1) Consistent

(2) Asymptotically normally distributed

(3) Has asymptotic covariance matrix

ˆAsy.Var[ ] [ ( )MD

q = m β ' A m β

β G β 1 1( )] [ ( ) ( )][ ( ) ( )] 'AG β G β 'AVAG β G β 'AG β

Part 21: Generalized Method of Moments21-55/67

Optimal Weighting Matrix

A

A

A

A

is the Weighting Matrix of the minimum distance estimator.

Are some 's better than others? (Yes)

Is there a best choice for ? Yes

The variance of the MDE is minimized when

= {Asy.

generalized method of moments estimator

m β

A V

-1

-1

Var[ ( )]}

This defines the .

=

Part 21: Generalized Method of Moments21-56/67

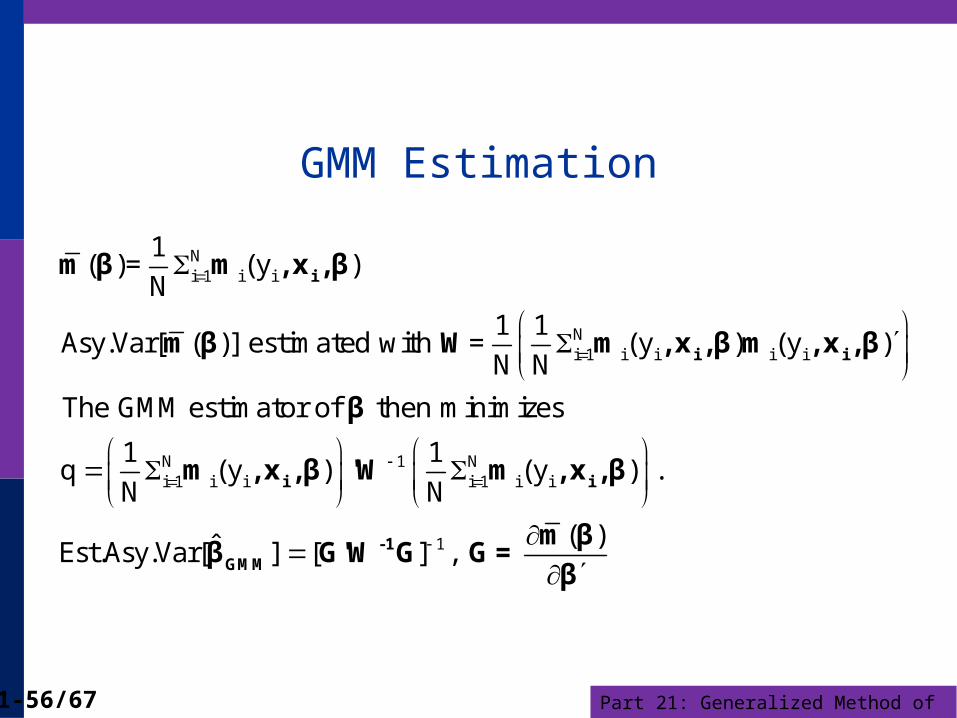

GMM Estimation

i

i i

i i

GM

m β m ,x ,β

m β W m ,x ,β m ,x ,β

β

m ,x ,β 'W m ,x ,β

β

Ni 1 i i

Ni 1 i i i i

N 1 Ni 1 i i i 1 i i

1( )= (y )

N1 1

Asy.Var[ ( )] estimated with = (y ) (y )N N

The GMM estimator of then minimizes

1 1q (y ) (y ) .

N N

ˆEst.Asy.Var[

-1

M

m βG'W G G=

β1 ( )

] [ ] ,

Part 21: Generalized Method of Moments21-57/67

GMM Estimation

i

i

m β m ,x ,β 0

m ,x ,β 'W m ,x

Ni 1 i i

N 1 Ni 1 i i i 1 i i

Exactly identified GMM problems

1When ( ) = (y ) is K equations in

NK unknown parameters (the exactly identified case),

the weighting matrix in

1 1q (y ) (y

N N

i

-1 -1 -1

,β

m β 0

G'W G G WG'1

)

is irrelevant to the solution, since we can set exactly

( ) so q = 0. And, the asymptotic covariance matrix

(estimator) is the product of 3 square matrices and becomes

[ ]

Part 21: Generalized Method of Moments21-58/67

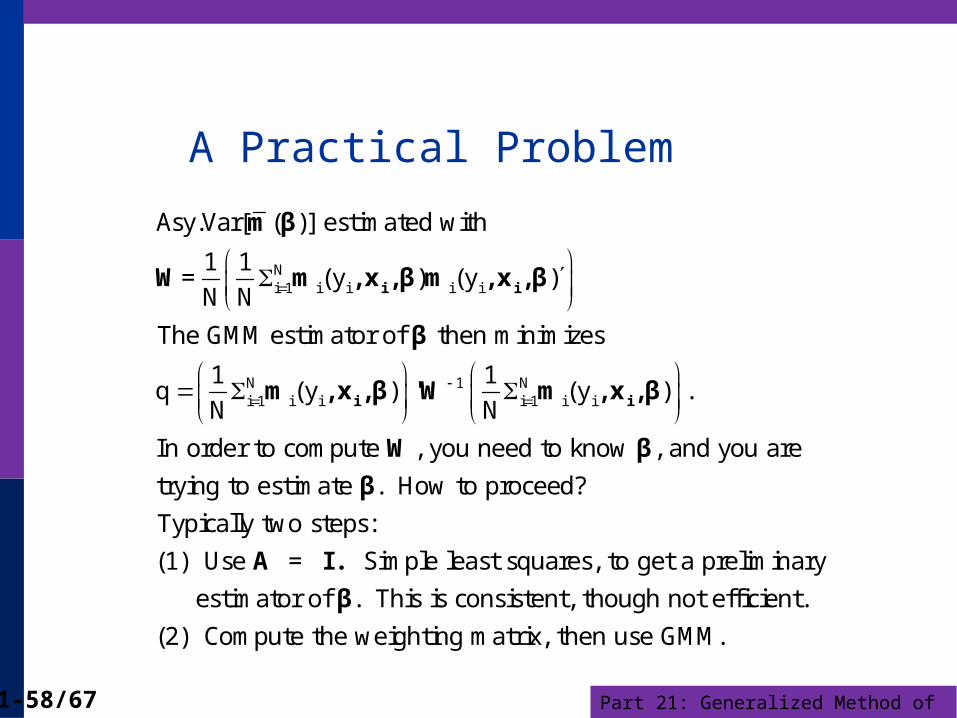

A Practical Problem

Ni 1 i i i i

N 1 Ni 1 i i i 1 i i

Asy.Var[ ( )] estimated with

1 1= (y ) (y )

N N

The GMM estimator of then minimizes

1 1q (y ) (y ) .

N N

In order to compute , you need to know

i i

i i

m β

W m ,x ,β m ,x ,β

β

m ,x ,β 'W m ,x ,β

W , and you are

trying to estimate . How to proceed?

Typically two steps:

(1) Use = Simple least squares, to get a preliminary

estimator of . This is consistent, though not efficient.

(2

β

β

A I.

β

) Compute the weighting matrix, then use GMM.

Part 21: Generalized Method of Moments21-59/67

Inference

Testing hypotheses about the parameters:

Wald test

A counterpart to the likelihood ratio test

Testing the overidentifying restrictions

Part 21: Generalized Method of Moments21-60/67

Testing Hypotheses

m β 'W m β

β

restricted unrestrict

(1) Wald Tests in the usual fashion.

(2) A counterpart to likelihood ratio tests

GMM criterion is q = ( ) ( )

when restrictions are imposed on

q increases.

q q ded chi squared[J]

(The weighting matrix must be the same for both.)

Part 21: Generalized Method of Moments21-61/67

Application: Dynamic Panel Data Model

βxi,t i,t i,t 1 i,t i

(Arellano/Bond/Bover, Journal of Econometrics, 1995)

y y u

Dynamic random effects model for panel data.

Can't use least squares to estimate consistently. Can't use FGLS without

esti

x

xi,1 i i,1

i,1 i i,2

mates of parameters.

Many moment conditions: What is orthogonal to the period 1 disturbance?

E[( u) ] 0 = K orthogonality conditions, K+1 parameters

E[( u) ] 0 = K more orthogonality

xi,1 i i,1

conditions, same K+1 parameters

...

E[( u) ] 0 = K orthogonality conditions, same K+1 parameters

The same variables are orthogonal to the period 2 disturbance.

There are hundreds, sometimes thousands of moment conditions, even for

fairly small models.

Part 21: Generalized Method of Moments21-62/67

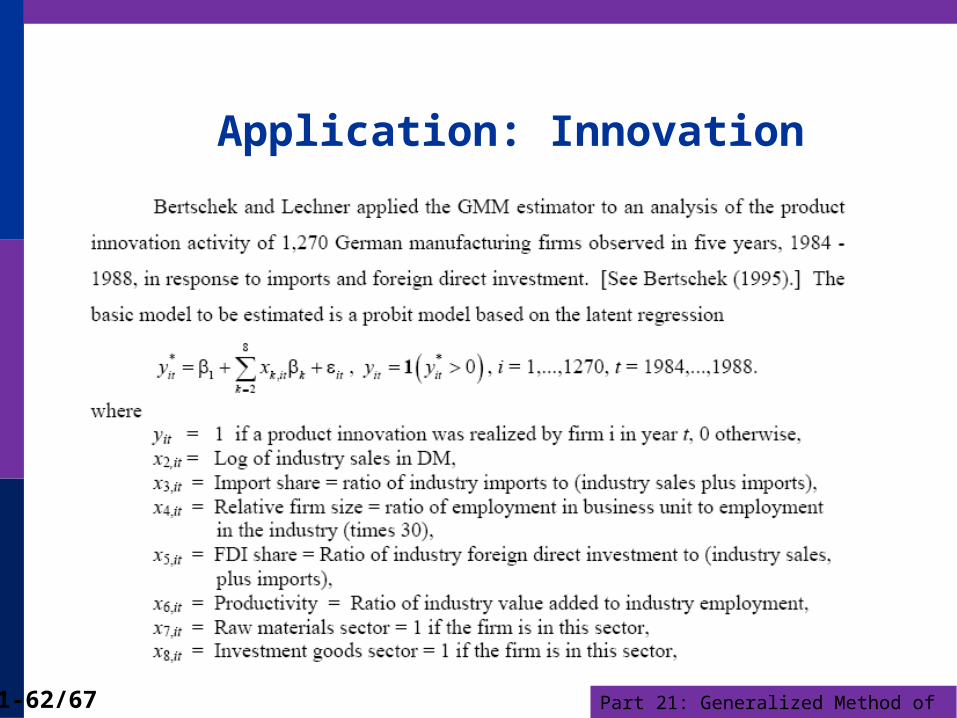

Application: Innovation

Part 21: Generalized Method of Moments21-63/67

Application: Innovation

Part 21: Generalized Method of Moments21-64/67

Application: Multivariate Probit Model

5 4 3 2 1

5 1 2 3 4 5

5 - variate Probit Model

y * , y 1[y * 0]

log [{(2 1) , 1,...,5}, ]

Requires 5 dimensional integration of the joint no

i i i i i

it it it it it

i it it i i i i iL y s t ds ds ds ds ds

x x x x x

x

1 1 1

2 2 2

3 3 31

4 4

rmal density. Very hard!

But, E[y | ] ( ).

Orthogonality Conditions: E[{y - ( )}

{y - ( )}

{y - ( )}1

Moment Equations: {y - ( )}

{y - ( )}

it it it

it it it

i i i

i i in

i i ii

i i

n

x x

x x 0

x x

x x

x x

x

4

5 5 5

45 equations in 9 parameters.

{y - ( )}i

i i i

0

x

x x

Part 21: Generalized Method of Moments21-65/67

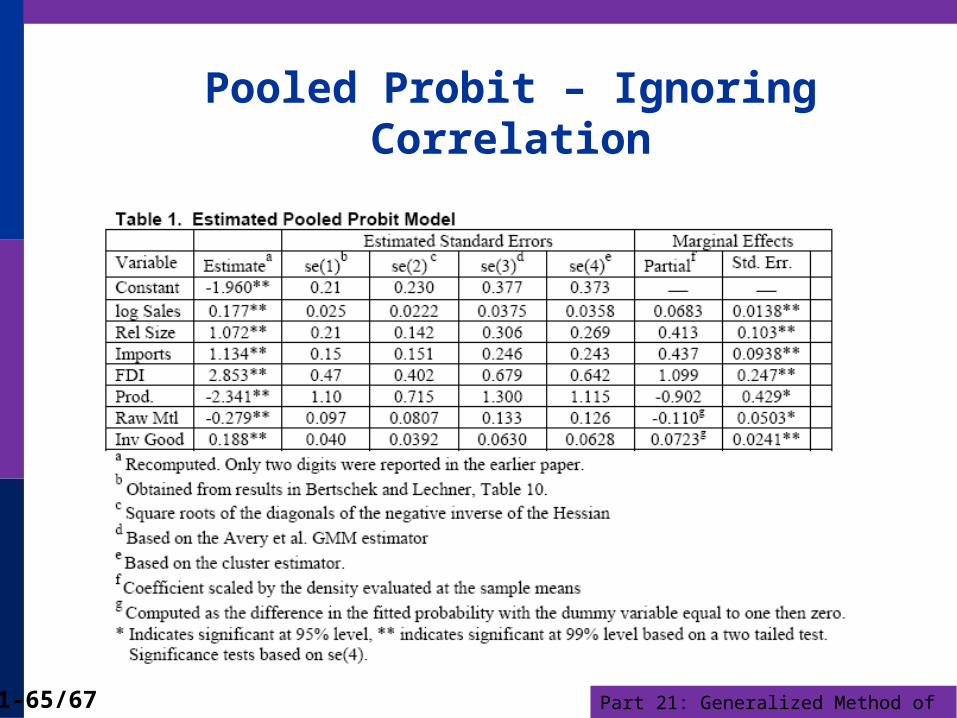

Pooled Probit – Ignoring Correlation

Part 21: Generalized Method of Moments21-66/67

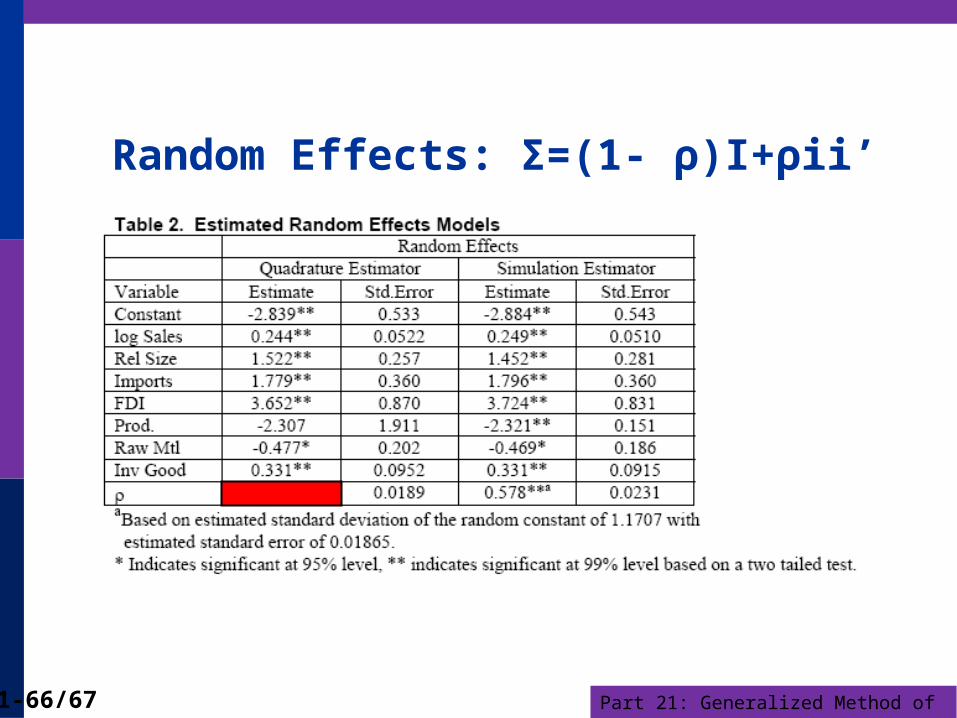

Random Effects: Σ=(1- ρ)I+ρii’

Part 21: Generalized Method of Moments21-67/67

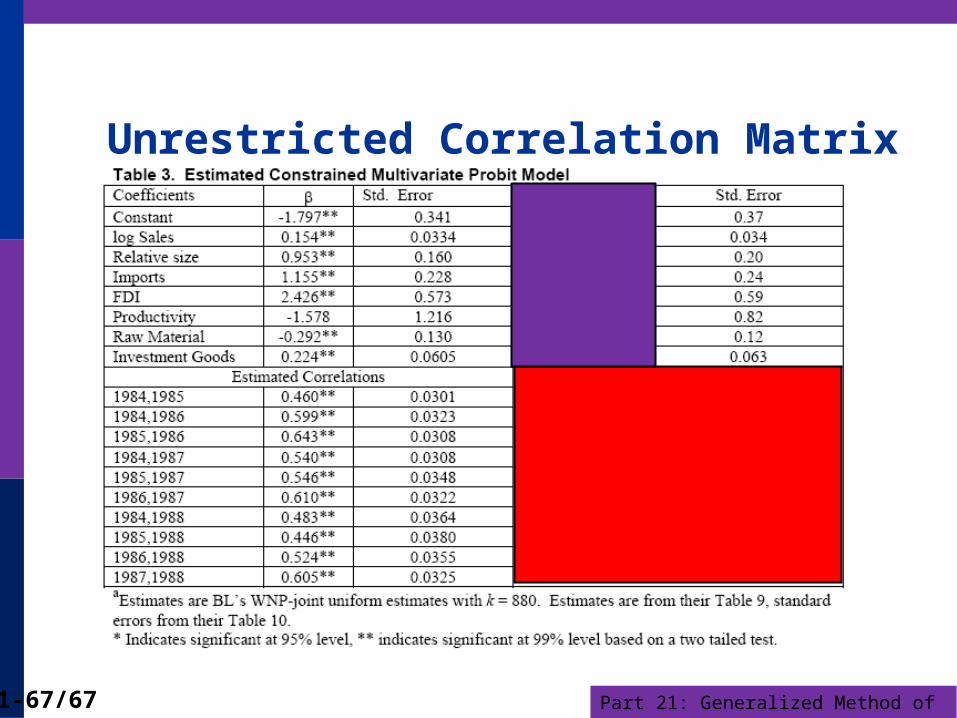

Unrestricted Correlation Matrix

Related Documents

![Part 2: Basic Econometrics [ 1/51] Econometric Analysis of Panel Data William Greene Department of Economics Stern School of Business.](https://static.cupdf.com/doc/110x72/56649d305503460f94a09019/part-2-basic-econometrics-151-econometric-analysis-of-panel-data-william.jpg)

![Part 2A: Basic Econometrics [ 1/75] Econometric Analysis of Panel Data William Greene Department of Economics Stern School of Business.](https://static.cupdf.com/doc/110x72/5697bf731a28abf838c7f4cc/part-2a-basic-econometrics-175-econometric-analysis-of-panel-data-william.jpg)