COMPANY PROFILE Piaggio Vehicle Private Limited is a 100% subsidiary of Piaggio & C. S.p.a,Italy.Piaggio Vehicles Private Limited was incorporat ed on Feb rua ry 17, 1998, as a joi nt ventu re betwe en Piagg io & C. S.p. a Ita ly, Simest Spa, Ital y to manufacture and market world-class diesel 3-wheelers in India. The company acquired the auto unit from Greaves Limited on March 31, 1998, located in Baramati, India. On August 30, 2001; Piaggio& C. SpA Italy acquired the entire shareholding of Greaves Limited consequent to which the Board of Directors passed a resolution to change its name to Piaggio Vehicles Private Limited. The company was incorporated to manufacture and market world-class diesel 3-wheelers & 4-wheelers in India. The company launched its Ape range of multi –utility, diesel 3-wheelers in India on 31 st July 1999. The parent company Piaggio and C.SpA, Italy transports its light weight, diverse product range with sales turn over exceeding $1.00 billion; vespa is one of them which are popular in India for last 20 years. Piaggio & C. Spa Italy is a $1.3 bn. Global Transportation Company in the field of light transport vehicles covering a very diverse product range comprising of 2-wheelers, 3-wheelers and 4-wheelers for cargo as well as passenger mobility. The Ape vehicles, which are, preferred mode of transportation in many countries. The Ape range comprises pick-ups, delivery vans, Drive Away Chassis for various customized applications, and various ‘Special Purpose Vehicles’ optimally designed for specific needs and applications. Piaggio Vehicle Private Limited manufactures the Ape vehicles, as per Piaggio’s international standards of design and manufacturing in Baramati near Pune in Maharashtra state. It had got capacity of 36000 vehicles per annum, which will be 72000 after the expansion.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 1/58

COMPANY PROFILE

Piaggio Vehicle Private Limited is a 100% subsidiary of Piaggio & C. S.p.a,Italy.Piaggio Vehicles Private Limited

was incorporated on February 17, 1998, as a joint venture between Piaggio & C. S.p.a Italy, Simest Spa, Italy to

manufacture and market world-class diesel 3-wheelers in India. The company acquired the auto unit from Greaves Limited

on March 31, 1998, located in Baramati, India. On August 30, 2001; Piaggio& C. SpA Italy acquired the entire shareholding

of Greaves Limited consequent to which the Board of Directors passed a resolution to change its name to Piaggio Vehicles

Private Limited.

The company was incorporated to manufacture and market world-class diesel 3-wheelers & 4-wheelers in India. Thecompany launched its Ape range of multi –utility, diesel 3-wheelers in India on 31st July 1999. The parent company Piaggio

and C.SpA, Italy transports its light weight, diverse product range with sales turn over exceeding $1.00 billion; vespa is one

of them which are popular in India for last 20 years.

Piaggio & C. Spa Italy is a $1.3 bn. Global Transportation Company in the field of light transport vehicles covering a

very diverse product range comprising of 2-wheelers, 3-wheelers and 4-wheelers for cargo as well as passenger mobility.

The Ape vehicles, which are, preferred mode of transportation in many countries. The Ape range comprises pick-ups,

delivery vans, Drive Away Chassis for various customized applications, and various ‘Special Purpose Vehicles’ optimally

designed for specific needs and applications. Piaggio Vehicle Private Limited manufactures the Ape vehicles, as per

Piaggio’s international standards of design and manufacturing in Baramati near Pune in Maharashtra state. It had got

capacity of 36000 vehicles per annum, which will be 72000 after the expansion.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 2/58

For the purpose of selling and providing after sales services to the customers company has got 6 regional offices at

Delhi, Bangalore, Chennai, Pune, Chandigarh and Kolkata & around 800 dealerships across the country.

The company has come a long way from its modest beginning in 1999 and can currently boast of a population of

more than 1,50,000 Ape vehicles on Indian and overseas roads. The company has ambitious plans for the future and is

currently executing an expansion project to double the plant capacity. PVPL has also embarked upon a project for

developing vehicles with alternate fuels like Petrol, LPG & CNG for higher capacity 3-wheelers and 4-wheelers in India.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 3/58

EVOLUTION OF PVPL

Piaggio Vehicles Pvt. Ltd. was formed in April 1998, which was formerly known as PGVL which was a joint venture

between Piaggio & Greaves, it is a 100% subsidiary of Piaggio & C. spa, Italy, which was formed in April 1998 in order to

manufacture and market world-class diesel 3-wheelers in India. Piaggio Vehicles Pvt. Ltd. launched its APE range of multi-

utility, diesel 3- wheeler in India on 31st July 1999.

Establishment of the PVPL, Baramati plant

Piaggio set up the Piaggio Vehicles Pvt. Ltd. a 100% subsidiary based at Baramati near 100 km from Pune in the

southwest of India for the production of three-wheeler vehicles. Piaggio Vehicles is bound to become a focal point for

Piaggio's commercial vehicle expansion outside Europe and in particular in Asiatic markets. PVPL has invested around Rs

65 crore of which equity component was 34 crore for its three-wheeler manufacturing facility. The Ape comes from the

stables of the $1.3 billion Piaggio & C. spa of Italy. It is being manufactured by Piaggio Vehicles Pvt. Limited (PVPL), a

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 4/58

100% subsidiary with its manufacturing base at Baramati, near Pune. The plant has an initial capacity to manufacture

36,000 vehicles per annum.

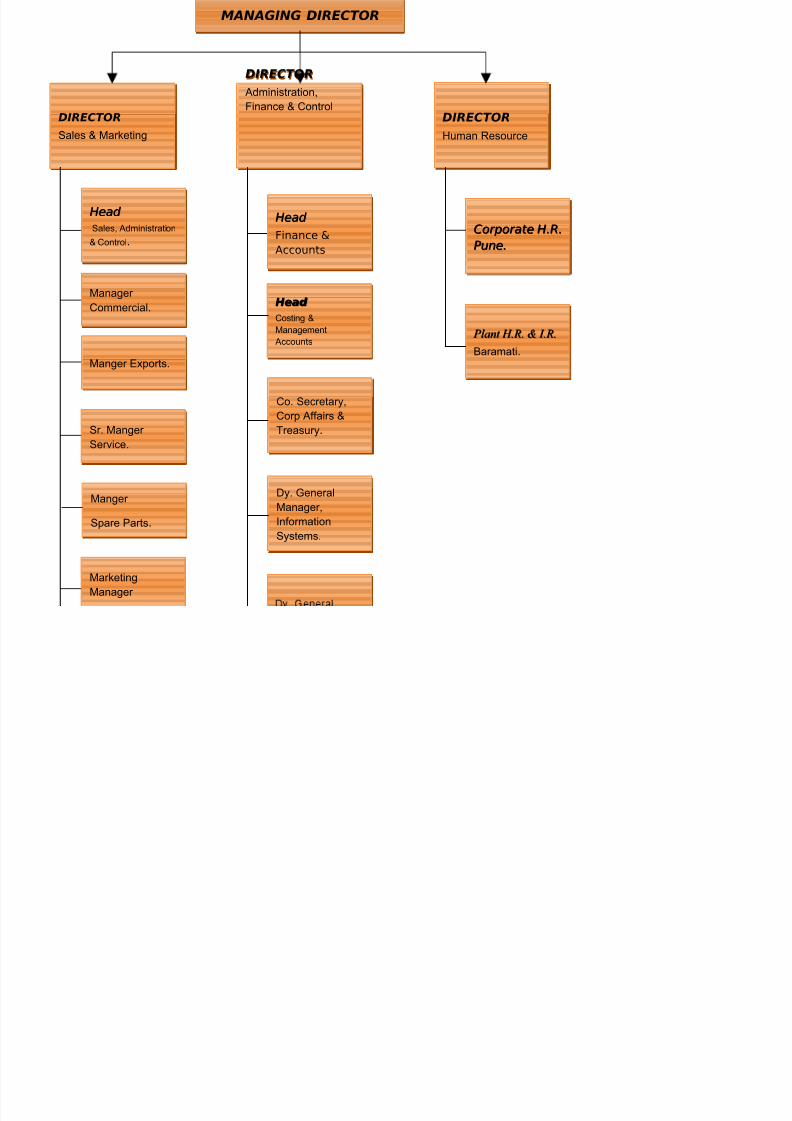

ORGANIZATIONAL STRUCTURE

MANAGING DIRECTOR

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 5/58

MANAGING DIRECTOR

MANAGING DIRECTOR

DIRECTOR

Sales & Marketing

DIRECTOR

Sales & Marketing

DIRECTOR

Administration,

Finance & Control

DIRECTOR

Administration,

Finance & Control

Head Head

Sales, Administration

& Control.

Head Head

Sales, Administration

& Control.

DIRECTOR

Human Resource

DIRECTOR

Human Resource

Manager

Commercial.

Manager

Commercial.

Manger Exports.

Manger Exports.

Marketing

Manager

Marketing

Manager

Sr. Manger

Service.

Sr. Manger

Service.

Manger

Spare Parts.

Manger

Spare Parts.

Head Head

Finance &

Accounts

Head Head

Finance &

Accounts

Head Head

Costing &

Management

Accounts

Head Head

Costing &

Management

Accounts

Co. Secretary,

Corp Affairs &

Treasury.

Co. Secretary,

Corp Affairs &Treasury.

Dy. General

Manager,

Information

Systems.

Dy. General

Manager,

Information

Systems.

Plant H.R. & I.R. Plant H.R. & I.R.

Baramati.

Plant H.R. & I.R. Plant H.R. & I.R.

Baramati.

Corporate H.R.Corporate H.R.

Pune.Pune.

Corporate H.R.Corporate H.R.

Pune.Pune.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 6/58

Managers/Ass.

.Managers

Regional Offices

Managers/Ass.

.Managers

Regional Offices

, .,

.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 7/58

VISION

♦ To be the no.1 and the most profitable global player with world-class quality and technology leadership in the 3-

wheeler Vehicle category offering transport solutions for specific customer needs.

♦ To be perceived as a unique, high impact, fast response, innovative and growth oriented company, which is known

around the world for its unmatched level of excellence.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 8/58

MISSION

To become a market leader in the 3- wheeler vehicle segment and achieve the status of a world-class company, which

manufactures and markets a wide range of high quality products to the satisfactions of customers in the domestic and

overseas market by ensuring:

♦ Low cost of manufacture.

♦ Highly profitable growth.

♦ Sustainable domestic and global competitiveness.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 9/58

♦ Maximized shareholder’s satisfaction & pride.

♦ Business ethics.

Through a continuous improvement of process focused on:

♦ Total quality

♦ Resources productivity

♦ Technology

♦ Cost effectiveness

And by offering an interactive professional environment of trust, openness, self- Confidence and commitment, which

encourages team efforts, employee empowerment and career progression.

NEW DEVELOPMENT PLAN

♦ Engines for the 3/4-wheeler sector:

PVPL is now going to develop new engines in 3/4 -wheeler sector. PVPL will manufacture two twin-

cylinder diesel engines in India, a 1000cc and a 1200cc. Then a turbo diesel which PVPL is going to developed

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 10/58

together with a major UK engineering company, one of the top firms in the diesel sector. PVPL has intended to build

this engine in India. It will be used on future Piaggio commercial vehicles starting from around 2010.

The production site has already been built, training courses are already underway, the production lines have

already been designed and assigned to various suppliers and PVPL is currently completing a significant scouting

operation for Indian suppliers of components for this engine. The development of a 4 wheel light commercial vehicle

equipped with 1000cc and 1200cc diesel engines as well as a 450cc engine and other mid-size engines uses in-house

production expertise as well as the strategic relationship has developed and contracts has been signed with Daihatsu,

Greaves, a major Indian engine manufacturer and Lombardini/Kholer.

So a light commercial vehicle will be built around this engine in India as well as Europe. It is Intended for

markets that are already open in Europe and will certainly open up in India from 2010 onwards

ECONOMICS-BUSINESS & MARKETS:

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 11/58

In 2009 the Piaggio Group reported worldwide sales of 6, 48,600 vehicles i.e. 4, 75,500 two-wheelers & 1,

78, 100 commercial vehicles. Group consolidated net sales in 2009 amounted to € 1570 million, down 7.2% from

€16792 million in 2007. Specifically, the two-wheeler sector reported a revenue decrease of 10% to €1180 million in

2009, offset in part by the 2.4% improvement in commercial vehicles, where 2009 revenue totalled € 389 million.

In the commercial vehicles business, the growth reported by the group in Europe and India- with revenues

from vehicles sales increasing in by 3.8% & 2.5% respectively-was achieved in a context of declining demand in

both regions. The industrial gross margin was €468 million compared with €498 million in 2007,

with a significant improvement in the return on net sales (29.9%, up from 29.5% in 2007) as a result of incisiveaction to contain product costs.

PVPL has 18% market share of the total 3-wheeler market in the category. In the cargo market segment it

accounts for over 42% of the market share and 9% market share for 4-wheelers.

Starting from zero base, in two years, PVPL has emerged as the second largest manufacturer of 3-wheeler in the

country with market leadership in the cargo segment.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 12/58

OBJECTIVES OF STUDY

♦ To study management of Fixed Assets of an organization.

♦ To study the process of Capitalization of any asset in an organization.

♦ To carry out Physical Verification of Fixed Assets present in the company.

♦ To analyze and interpret the Fixed Asset Register (FAR) data of the company.

♦ To make suggestions, if any.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 13/58

INTRODUCTION

Fixed Assets are ‘long-lived assets’ in the sense that they provide enduring benefits to the entity.

An enterprise holds a fixed asset (property, plant and equipment, or intangible assets) for use in production

and supply of goods or services, for rental or for administrative purposes on a continuing basis. It expects to use a

fixed asset for more than one accounting period and does not intend to sell the same in the normal course of business.

Examples of fixed assets are land, building, plant and equipment, furniture and fixtures, vehicles, goodwill, and

patent.

Disposal of a fixed asset on retirement is a peripheral activity.

Fixed assets may be tangible or intangible. Tangible fixed assets are those that have physical substance, while

intangible fixed assets do not have this. Examples of intangible assets are software, patent and licence granting

broadcasting rights.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 14/58

Assets acquired for safety and environmental reasons qualify as fixed assets. Although they may not directly

increase future economic benefits, they help the entity to obtain future economic benefits from other fixed assets. For

example, pollution control equipment installed in the chemical plant to reduce emission of harmful waste is a fixed

asset. In absence of the equipment, the enterprise would not be allowed to operate and it would not be able to

generate cash flows from the use of other assets.

Sometimes, it may be appropriate to aggregate individually insignificant items, such as moulds, tools dies, and

to apply the criteria to the aggregate value. Similarly, an entity may expense an item, which would otherwise be

categorized as fixed asset, if the expenditure is not material.

The main issues in the accounting for tangible fixed assets are the determination of:

♦ The timing of recognition of fixed assets

♦ The cost of acquisition

♦ The carrying amount

♦ Depreciation charges to be recognized in the profit and loss account

An enterprise recognizes a fixed asset in its balance sheet only when it is available for use. Fixed assets are initially

recognized at costs. The accumulation of costs commences when the management commits to the acquisition of the fixed

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 15/58

asset and ceases when the asset is substantially ready for use. Subsequent expenditure on an existing fixed asset is added to

its carrying cost only if the expenditure adds to the service potential of the asset.

A fixed asset is carried at cost less accumulated depreciation and accumulated impairment loss. The depreciable

amount, that is, the cost less estimated residual value of the asset, is allocated over the estimated useful life of the asset.

Depreciation for a particular year represents the value of the depreciable amount allocated to that particular year

NATURES OF FIXED ASSETS

Identification of Fixed Assets

The standard gives a definition of fixed asset, but does not prescribe specific criteria for the classification of

assets as fixed. Therefore, an enterprise applies judgement in deciding which assets should be classified as fixed assets, after

taking in to consideration its nature of business and specific circumstances.

The standard permits aggregation of individually insignificant items. Similarly, it permits an enterprise to

expense an item which would otherwise be classified as fixed assets, because the amount of the expenditure is not material.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 16/58

Components of Cost

1. The cost of an item of fixed asset comprises its purchase price, including import duties and other non-refundable taxes or

levies and any directly attributable cost of bringing the asset to its working condition for its intended use; any trade

discounts and rebates are deducted in arriving at the purchase price. Examples of directly attributable costs are:

(i) Site preparation;

(ii) Initial delivery and handling costs;

(iii) Installation cost, such as special foundations for plant; and

(iv) Professional fees, for example fees of architects and engineers.The cost of a fixed asset may undergo changes subsequent to its acquisition or construction on account of exchange

fluctuations, price adjustments, changes in duties or similar factors.

2. Administration and other general overhead expenses are usually excluded from the cost of fixed assets because they do

not relate to a specific fixed asset. However, in some circumstances, such expenses as are specifically attributable to

construction of a project or to the acquisition of a fixed asset or bringing it to its working condition, may be included as part

of the cost of the construction project or as a part of the cost of the fixed asset.

3. The expenditure incurred on start-up and commissioning of the project, including the expenditure incurred on test runs

and experimental production, is usually capitalized as an indirect element of the construction cost. However, the expenditure

incurred after the plant has begun commercial production, i.e., production intended for sale or captive consumption, is not

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 17/58

capitalized and is treated as revenue expenditure even though the contract may stipulate that the plant will not be finally

taken over until after the satisfactory completion

4. If the interval between the date a project is ready to commence commercial production and the date at which commercial

production actually begins is prolonged, all expenses incurred during this period are charged to the profit and loss statement.

However, the expenditure incurred during this period is also sometimes treated as deferred revenue expenditure to be

amortized over a period not exceeding 3 to 5 years after the commencement

Self-constructed Fixed Assets

In arriving at the gross book value of self-constructed fixed assets, the same principles apply as those described in

paragraphs 1 to 4. Included in the gross book value are costs of construction that relate directly to the specific asset and cost

that are attributable to the construction activity in general and can be allocated to the specific asset. Any internal profits are

eliminated in arriving at such costs.

Non-monetary Consideration

1. When a fixed asset is acquired in exchange for another asset, its cost is usually determined by reference to the fair market

value of the consideration given. It may be appropriate to consider also the fair market value of the asset acquired if this is

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 18/58

more clearly evident. It may be noted that this paragraph relates to “all expenses” incurred during the period. This

expenditure would also include borrowing costs incurred during the said period. Since Accounting Standard (AS) 16,

Borrowing Costs, specifically deals with the treatment of borrowing costs, the treatment provided by AS 16 would prevail

over the provisions in this respect contained in this paragraph as these provisions are general in nature and apply to “all

expenses”, that is sometimes used for an exchange of assets, particularly when the assets exchanged are similar, is to record

the asset acquired at the net book value of the asset given up; in each case an adjustment is made for any balancing receipt

or payment of cash or other consideration.

2. When a fixed asset is acquired in exchange for shares or other securities in the enterprise, it is usually recorded at its fair

market value, or the fair market value of the securities issued, whichever is more clearly evident.

Improvements and Repairs

1. Frequently, it is difficult to determine whether subsequent expenditure related to fixed asset represents improvements that

ought to be added to the gross book value or repairs that ought to be charged to the profit and loss statement. Only

expenditure that increases the future benefits from the existing asset beyond its previously assessed standard of performance

is included in the gross book value, e.g., an increase in capacity.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 19/58

2. The cost of an addition or extension to an existing asset which is of a capital nature and which becomes an integral part of

the existing asset is usually added to its gross book value. Any addition or extension, which has a separate identity and is

capable of being used after the existing asset is disposed of, is accounted for separately.

Amount Substituted for Historical Cost

1. Sometimes financial statements that are otherwise prepared on a historical cost basis include part or all of fixed assets at a

valuation in substitution for historical costs and depreciation is calculated accordingly. Such financial statements are to be

distinguished from financial statements prepared on a basis intended to reflect comprehensively the effects of

2. A commonly accepted and preferred method of restating fixed assets is by appraisal, normally undertaken by competent

valuers. Other methods sometimes used are indexation and reference to current prices which when applied is cross checked

periodically by appraisal method.

3. The revalued amounts of fixed assets are presented in financial statements either by restating both the gross book value

and accumulated depreciation so as to give a net book value equal to the net revalued amount or by restating the net book

value by adding therein the net increase on account of revaluation. An upward revaluation does not provide a basis for

crediting to the profit and loss statement the accumulated depreciation existing at the date of revaluation.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 20/58

4. Different bases of valuation are sometimes used in the same financial statements to determine the book value of the

separate items within each of the categories of fixed assets or for the different categories of fixed assets. In such cases, it is

necessary to disclose the gross book value included on each basis.

5. Selective revaluation of assets can lead to unrepresentative amounts being reported in financial statements. Accordingly,

when revaluations do not cover all the assets of a given class, it is appropriate that the selection of assets to be revalued be

made on a systematic basis. For example, an enterprise may revalue a whole class of assets within a unit.

6. It is not appropriate for the revaluation of a class of assets to result in the net book value of that class being greater than

the recoverable amount of the assets of that class.

7. An increase in net book value arising on revaluation of fixed assets is normally credited directly to owner’s interests

under the heading of revaluation reserves and is regarded as not available for distribution. A decrease in net book value

arising on revaluation of fixed assets is charged to profit and loss statement except that, to the extent that such a decrease is

considered to be related to a previous increase on revaluation that is included in revaluation reserve, it is sometimes charged

against that earlier increase. It sometimes happens that an increase to be recorded is a reversal of a previous decrease arising

on revaluation which has been charged to profit and loss statement in which case the increase is credited to profit and loss

statement to the extent that it offsets the previously recorded decrease.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 21/58

Retirements and Disposals

1. An item of fixed asset is eliminated from the financial statements on disposal.

2. Items of fixed assets that have been retired from active use and are held for disposal are stated at the lower of their net

book value and net realizable value and are shown separately in the financial statements. Any expected loss is recognized

immediately in the profit and loss statement.

3. In historical cost financial statements, gains or losses arising on disposal are generally recognized in the profit and loss

statement.

4. On disposal of a previously revalued item of fixed asset, the difference between net disposal proceeds and the net book

value is normally charged or credited to the profit and loss statement except that, to the extent such a loss is related to an

increase which was previously recorded as a credit to revaluation reserve and which has not been subsequently reversed or

utilized, it is charged directly to that account. The amount standing in revaluation reserve following the retirement or

disposal of an asset which relates to that asset may be transferred to general reserve.

Valuation of Fixed Assets in Special Cases

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 22/58

1. In the case of fixed assets acquired on hire purchase terms, although legal ownership does not vest in the enterprise, such

assets are recorded at their cash value, which, if not readily available, is calculated by assuming an appropriate rate of

interest. They are shown in the balance sheet with an appropriate narration to indicate that the enterprise does not have full

ownership thereof.

2. Where an enterprise owns fixed assets jointly with others (otherwise than as a partner in a firm), the extent of its share in

such assets, and the proportion in the original cost, accumulated depreciation and written down value are stated in the

balance sheet. Alternatively, the pro rata cost of such jointly owned assets is grouped together with similar fully owned

assets. Details of such jointly owned assets are indicated separately in the fixed assets register.

3. Where several assets are purchased for a consolidated price, the consideration is apportioned to the various assets on a

fair basis as determined by competent valuers.

Fixed Assets of Special Types

1. Goodwill, in general, is recorded in the books only when some consideration in money or money’s worth has been paid

for it. Whenever a business is acquired for a price (payable either in cash or in shares or otherwise) which is in excess of the

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 23/58

value of the net assets of the business taken over, the excess is termed as ‘goodwill’. Goodwill arises from business

connections, trade name or reputation of an enterprise or from other intangible benefits enjoyed by an enterprise.

2. As a matter of financial prudence, goodwill is written off over a period. However, many enterprises do not write off

goodwill and retain it as an asset.

Disclosure

1. Certain specific disclosures on accounting for fixed assets are already required by Accounting Standard 1 on ‘Disclosure

of Accounting Policies’ and Accounting Standard 6 on ‘Depreciation Accounting’.

2. Further disclosures that are sometimes made in financial statements include:

(i) Gross and net book values of fixed assets at the beginning and end of an accounting period showing additions, disposals,

acquisitions and other movements;

(ii) Expenditure incurred on account of fixed assets in the course of construction or acquisition; and

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 24/58

(iii) Revalued amounts substituted for historical costs of fixed assets, the method adopted to compute the revalued amounts,

the nature of any indices used, the year of any appraisal made, and whether an external valuer was involved, in case where

fixed assets are stated at revalued amounts.

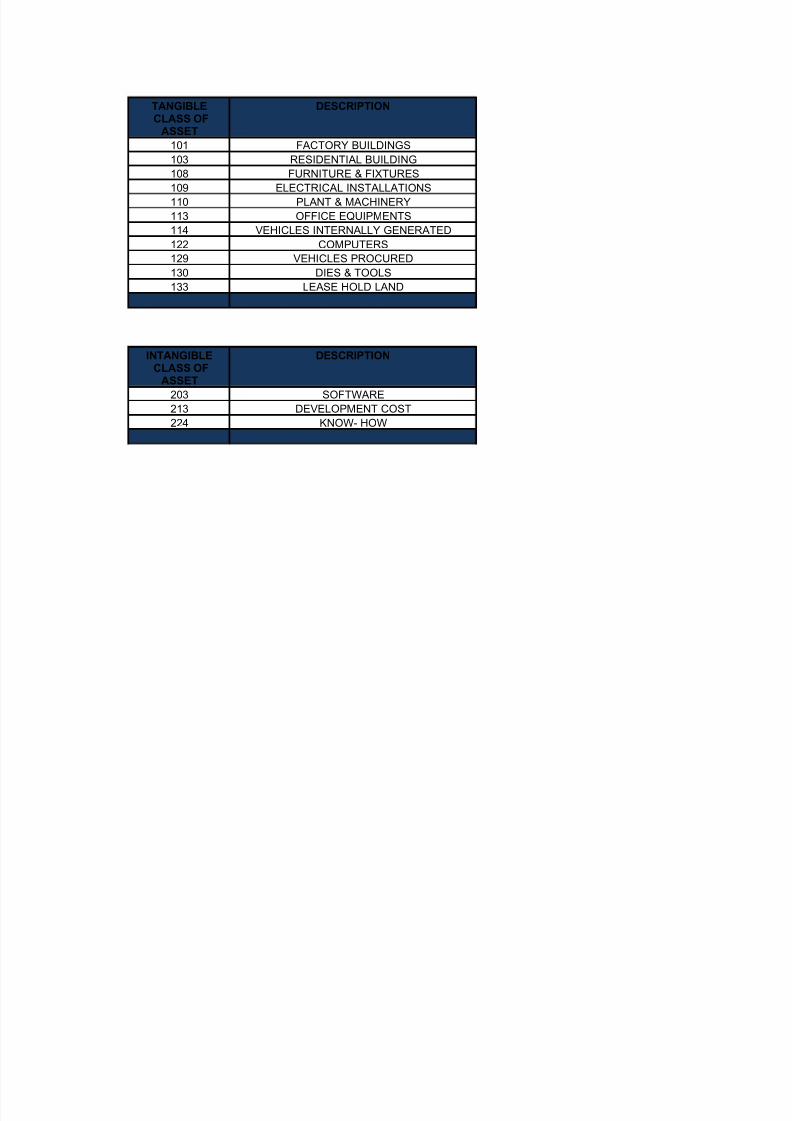

CLASS OF ASSETS

In an organization assets are classified in to two classes i.e. Tangible and Intangible assets. The table below shows

the class of assets and its description:

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 25/58

TANGIBLE DESCRIPTION

CLASS OF

ASSET

101 FACTORY BUILDINGS

103 RESIDENTIAL BUILDING

108 FURNITURE & FIXTURES

109 ELECTRICAL INSTALLATIONS

110 PLANT & MACHINERY

113 OFFICE EQUIPMENTS

114 VEHICLES INTERNALLY GENERATED

122 COMPUTERS

129 VEHICLES PROCURED

130 DIES & TOOLS

133 LEASE HOLD LAND

INTANGIBLE DESCRIPTION

CLASS OF

ASSET

203 SOFTWARE

213 DEVELOPMENT COST

224 KNOW- HOW

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 26/58

Companies (Auditor's Report) Order, 2003PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY PART II, SECTION 3 - SUB - SECTION(i)

MINISTRY OF FINANCE

(DEPARTMENT OF COMPANY AFFAIRS)

1. Definitions. In this Order, unless the context otherwise requires,-

(a) Act means the Companies Act, 1956 (1 of 1956);

(b) chit fund company, nidhi company or mutual benefit company means a company engaged in the business

of managing, conducting or supervising as a foreman or agent of any transaction or arrangement by which it

enters into an agreement with a number of subscribers that every one of them shall subscribe to a certain sumof installments for a definite period and that each subscriber, in his turn, as determined by lot or by auction or

by tender or in such other manner as may be provided for in the agreement, shall be entitled to a prize amount,

and includes companies whose principal business is accepting fixed deposits from, and lending money to,

members;

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 27/58

(c) finance company means a company engaged in the business of financing, whether by making loans or

advances or otherwise, of any industry, commerce or agriculture and includes any company engaged in the

business of hire-purchase, lease financing and financing of housing;

(d) investment company means a company engaged in the business of acquisition and holding of, or dealing in,

shares, stocks, bonds, debentures, debenture stocks, including securities issued by the Central or any State

Government or by any local authority, or in other marketable securities of a like nature;

(e) manufacturing company means a company engaged in any manufacturing process as defined in the

Factories Act, 1948 (63 of 1948);

(f) Mining company means a company owning a mine, and includes a company which carries on the business

of a mine either as a lessee or occupier thereof;

(g) processing company means a company engaged in the business of processing materials with a view to their

use, a sale, delivery or disposal;

(h) service company means a company engaged in the business of supplying, providing, maintaining and

operating any services, facilities, conveniences, bureaux and the like for the benefit of others;

(i) Trading company means a company engaged in the business of buying and selling goods.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 28/58

3. Matters to be included in the auditor’s report. The auditor’s report on the account of a company to

which this Order applies shall include a statement on the following matters, namely:-

(i) (a) whether the company is maintaining proper records showing full particulars, including quantitative

details and situation of fixed assets;

(b) Whether these fixed assets have been physically verified by the management at reasonable intervals;

whether any material discrepancies were noticed on such verification and if so, whether the same have been

properly dealt with in the books of account;

(c) If a substantial part of fixed assets have been disposed off during the year, whether it has affected the

going concern;

(ii) (a) whether physical verification of inventory has been conducted at reasonable intervals by the

management;

(b) Are the procedures of physical verification of inventory followed by the management reasonable and

adequate in relation to the size of the company and the nature of its business. If not, the inadequacies in such

procedures should be reported;

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 29/58

(c) Whether the company is maintaining proper records of inventory and whether any material discrepancies

were noticed on physical verification and if so, whether the same have been properly dealt with in the books

of account;

(iii) (a) has the company either granted or taken any loans, secured or unsecured to/from companies, firms or

other parties covered in the register maintained under section 301 of the Act. If so, give the number of parties

and amount involved in the transactions.

(b) whether the rate of interest and other terms and conditions of loans given or taken by the company,

secured or unsecured, are prima facie prejudicial to the interest of the company;

(c) Whether payment of the principal amount and interest are also regular;

(d) If overdue amount is more than one lakh, whether reasonable steps have been taken by the company for

recovery/payment of the principal and interest;

(iv) Is there an adequate internal control procedure commensurate with the size of the company and the nature

of its business, for the purchase of inventory and fixed assets and for the sale of goods. Whether there is a

continuing failure to correct major weaknesses in internal control;

(v) (a) whether transactions that need to be entered into a register in pursuance of section 301 of the Act have

been so entered;

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 30/58

(b) Whether each of these transactions have been made at prices which are reasonable having regard to the

prevailing market prices at the relevant time;

(This information is required only in case of transactions exceeding the value of five lakh rupees in respect of

any party and in any one financial year).

(vi) in case the company has accepted deposits from the public, whether the directives issued by the Reserve

Bank of India and the provisions of sections 58A and 58AA of the Act and the rules framed there under,

where applicable, have been complied with. If not, the nature of contraventions should be stated; If an order

has been passed by Company Law Board whether the same has been complied with or not?

(vii) in the case of listed companies and/or other companies having a paid-up capital and reserves exceeding

Rs.50 lakhs as at the commencement of the financial year concerned, or having an average annual turnover

exceeding five crore rupees for a period of three consecutive financial years immediately preceding the

financial year concerned, whether the company has an internal audit system commensurate with its size and

nature of its business;

(viii) where maintenance of cost records has been prescribed by the Central Government under clause (d) of

sub-section (1) of section 209 of the Act, whether such accounts and records have been made and maintained;

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 31/58

(ix) (a) is the company regular in depositing undisputed statutory dues including Provident Fund, Investor

Education and Protection Fund, Employees State Insurance, Income-tax, Sales-tax, Wealth Tax, Custom Duty,

Excise Duty, cess and any other statutory dues with the appropriate authorities and if not, the extent of the

arrears of outstanding statutory dues as at the last day of the financial year concerned for a period of more

than six months from the date they became payable, shall be indicated by the auditor.

(b) In case dues of sales tax/income tax/custom tax/wealth tax/excise duty/cess have not been deposited on

account of any dispute, then the amounts involved and the forum where dispute is pending may please be

mentioned.

(A mere representation to the Department shall not constitute the dispute).

(x) whether in case of a company which has been registered for a period not less than five years, its

accumulated losses at the end of the financial year are not less than fifty per cent of its net worth and whether

it has incurred cash losses in such financial year and in the financial year immediately preceding such

financial year also;

(xi) Whether the company has defaulted in repayment of dues to a financial institution or bank or debenture

holders? If yes, the period and amount of default to be reported;

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 32/58

(xii) whether adequate documents and records are maintained in cases where the company has granted loans

and advances on the basis of security by way of pledge of shares, debentures and other securities; If not, the

deficiencies to be pointed out.

(xiii) Whether the provisions of any special statute applicable to chit fund have been duly complied with? In

respect of nidhi/ mutual benefit fund/societies;

(a) Whether the net-owned funds to deposit liability ratio is more than 1:20 as on the date of balance sheet;

(b) Whether the company has complied with the prudential norms on income recognition and provisioning

against sub-standard/default/loss assets;

(c) Whether the company has adequate procedures for appraisal of credit proposals/requests, assessment of

credit needs and repayment capacity of the borrowers;

(d) Whether the repayment schedule of various loans granted by the nidhi is based on the repayment capacity

of the borrower and would be conducive to recovery of the loan amount;

(xiv) if the company is dealing or trading in shares, securities, debentures and other investments, whether

proper records have been maintained of the transactions and contracts and whether timely entries have been

made therein; also whether the shares, securities, debentures and other securities have been held by the

company, in its own name except to the extent of the exemption, if any, granted under section 49 of the Act;

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 33/58

(xv) Whether the company has given any guarantee for loans taken by others from bank or financial

institutions, the terms and conditions whereof are prejudicial to the interest of the company;

(xvi) Whether term loans were applied for the purpose for which the loans were obtained;

(xvii) Whether the funds raised on short-term basis have been used for long term investment and vice versa; If

yes, the nature and amount is to be indicated;

(xviii) Whether the company has made any preferential allotment of shares to parties and companies covered

in the Register maintained under section 301 of the Act and if so whether the prices at which shares have been

issued is prejudicial to the interest of the company;

(xix) Whether the management has disclosed on the end use of money raised by public issues and the same

has been verified;

(xx) whether any fraud on or by the company has been noticed or reported during the year; If yes, the nature

and the amount involved is to be indicated.

PROCEDURE FOR CAPITALIZATION

FINANCIAL SANCTION

START

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 34/58

UOTATIONS FROM PROSPECTIVE SUPPLIERS

EVALUATIONS OF PURCHASE ORDERS

RAISING PURCHASE ORDER AFTER EVALUATION

PROCUREMENT PLANNING ANDRELEASE OF SCHEDULE

FEEDING INTO SYSTEM

MAKING OF DELIVERY SCHEDULESBY THE SYSTEM

PRINTING OF DELIVERY SCHEDULES

POSTING OF DELIVERY

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 35/58

FOLLOW UP OF SCHEDULE

RECEIVING OF MATERIALS FROMTHE VENDORS

GATE ENTRY

UALITY & UANTITY COUNTING

VERIFICATION & GRN PRINTING

MATERIAL INSPECTION BY QCDEPARTMENT

GRN COMES FROM STORES

A

A

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 36/58

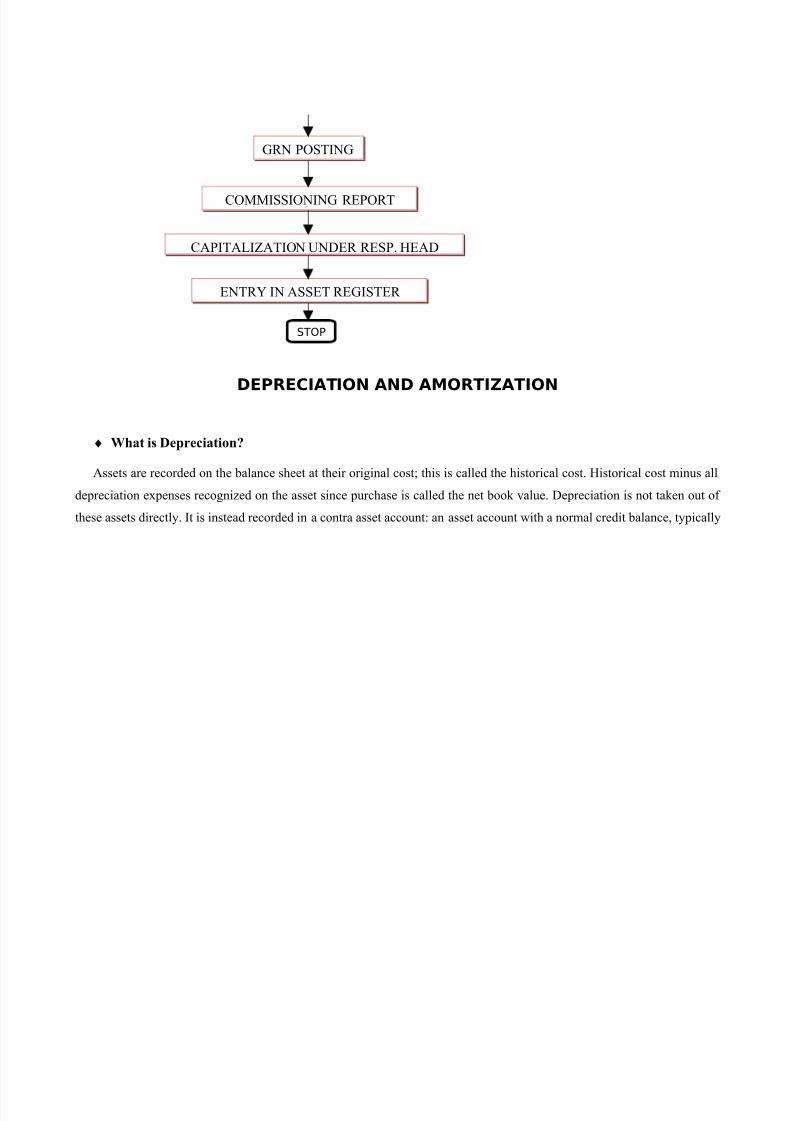

DEPRECIATION AND AMORTIZATION

♦ What is Depreciation?

Assets are recorded on the balance sheet at their original cost; this is called the historical cost. Historical cost minus all

depreciation expenses recognized on the asset since purchase is called the net book value. Depreciation is not taken out of

these assets directly. It is instead recorded in a contra asset account: an asset account with a normal credit balance, typically

GRN POSTING

COMMISSIONING REPORT

CAPITALIZATION UNDER RESP. HEAD

ENTRY IN ASSET REGISTER

STOP

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 37/58

called "accumulated depreciation". Balancing an asset account with its corresponding accumulated depreciation account will

result in the net book value.

The net book value will never fall below the salvage value, meaning that once an asset is fully depreciated, no further

expenses will be taken during its life. Salvage value is the estimated value of the asset at the end of its useful life. In this

way, total depreciation for an asset will never exceed the estimated total cash outlay (depreciable basis) for the asset.

In simple words we can say that depreciation is the reduction in the value of an asset due to usage, passage of time,

wear & tear, technological outdating or obsolescence, depletion, inadequacy, rot, rust, decay or other such factors.

Salvage value is the estimated value of an asset at the end of its useful life. In accounting, the salvage value of an

asset is its remaining value after depreciation. This is also known as residual value or scrap value. It is the net cash inflow

that occurs when the asset is liquefied at the end of its life. Salvage value can be negative if the residual asset requires

special treatment to terminate—for example, used nuclear materials or CRT's containing lead.

Depreciation and its related concept, Amortization (generally, the depreciation of intangible assets), are non-cash

expenses. Neither depreciation nor amortization will directly affect the cash flow of a company, as both are accounting

representations of expenses attributable to a given period. In accounting statements, depreciation may neither figure in the

cash flow statement, nor be "added back" to net income (along with other items) to derive the operating cash flow.

Depreciation recognized for tax purposes will, however, affect the cash flow of the company, as tax depreciation will reduce

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 38/58

taxable profits; there is generally no requirement that treatment of depreciation for tax and accounting purposes be identical.

Where depreciation is shown on accounting statements, the figure usually does not match the depreciation for tax purposes

♦ Treatment: -

Depreciation is considered an expense and is listed in an income statement under expenses. In addition to vehicles that

may be used in our work, we also have to depreciate office furniture, office equipment, any buildings we own, and

machinery and scientific equipments we use for research. Land is not considered an expense, nor can it be depreciated. Land

does not wear out like vehicles or equipment.

To find the annual depreciation cost for our assets, we need to know the initial cost of the assets. We also need to

determine how many years we think the assets will retain some value for us. On the basis of this the rate of depreciation is

decided.

♦ Accounting

A company needs to report depreciation accurately in its financial statements in order to achieve two main objectives:

1. Matching its expenses with the income generated by means of those expenses, and

2. Ensuring that the asset values in the balance sheet are not overstated. (An asset acquired in Year 1 is unlikely to be

worth the same amount in Year 5.)

Depreciation is an estimated or expected view of the decline in value of an asset. For example, an entity may depreciate

its equipment by 15% per year. This rate should be reasonable in aggregate (such as when a manufacturing company is

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 39/58

looking at all of its machinery), and consistently employed. However, there is no expectation that each individual item

declines in value by the same amount, primarily because the recognition of depreciation is based upon the allocation of

historical costs and not current market prices.

Accounting standards bodies have detailed rules on which methods of depreciation are acceptable, and auditors should

express a view if they believe the assumptions underlying the estimates do not give a true and fair view.

♦ Recording depreciation

For historical cost purposes, assets are recorded on the balance sheet at their original cost; this is called the historical

cost. Historical cost minus all depreciation expenses recognized on the asset since purchase is called the book value.Depreciation is not taken out of these assets directly. It is instead recorded in a contra asset account: an asset account with a

normal credit balance, typically called "accumulated depreciation". Balancing an asset account with its corresponding

accumulated depreciation account will result in the net book value. The net book value will never fall below the salvage

value, meaning that once an asset is fully depreciated, no further expenses will be taken during its life. Salvage value is the

estimated value of the asset at the end of its useful life. In this way, total depreciation for an asset will never exceed the

estimated total cash outlay (depreciable basis) for the asset. The exception to this is in many price-regulated industries

(public utilities) where salvage is estimated net of the cost of physically removing the asset from service. (Decommissioning

a nuclear power plant is a nontrivial expense.) If the expected cost of removal exceeds the expected raw (or gross) salvage,

then the net of the two (called net salvage) may be negative. In this case, the depreciation recorded on the regulated books

may exceed the depreciable basis. Companies have no obligation to dispose of depreciated assets, of course, and many fully

depreciated assets continue to generate income.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 40/58

Recording a depreciation expense will involve a credit to an accumulated depreciation account. The corresponding debit

will involve either an expense account or an asset account that represents a future expense, such as work in progress.

Depreciation is recorded as an adjusting journal entry.

A write-down is a form of depreciation that involves a partial write off. Part of the value of the asset is removed from the

balance sheet. The reason may be that the book value (accounted value) of the fixed asset has diverged from the market

value and causes the company a loss. An example of this would be a revaluation of goodwill on an acquisition that went

bad.

Methods of depreciation

There are several methods for calculating depreciation, generally based on either the passage of time or the level of

activity (or use) of the asset.

♦ Straight-line Method

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 41/58

Straight-line depreciation is the simplest and most-often-used technique, in which the company estimates the

salvage value of the asset at the end of the period during which it will be used to generate revenues (useful life) and will

expense a portion of original cost in equal increments over that period. The salvage value is an estimate of the value of the

asset at the time it will be sold or disposed of; it may be zero or even negative. Salvage value is also known as scrap value

or residual value.

♦ Declining-Balance Method

Depreciation methods that provide for a higher depreciation charge in the first year of an asset's life and

gradually decreasing charges in subsequent years are called accelerated depreciation methods. This may be a more

realistic reflection of an asset's actual expected benefit from the use of the asset: many assets are most useful when they are

new. One popular accelerated method is the declining-balance method. Under this method the Book Value is multiplied by

a fixed rate.

♦ Activity depreciation

Activity depreciation methods are not based on time, but on a level of activity. This could be miles driven for

a vehicle, or a cycle count for a machine. When the asset is acquired, its life is estimated in terms of this level of activity.

Each year, the depreciation expense is then calculated by multiplying the rate by the actual activity level.

♦ Sum-of-Years' Digits Method

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 42/58

Sum-of-Years' Digits is a depreciation method that results in a more accelerated write-off than straight line,

but less than declining-balance method. Under this method annual depreciation is determined by multiplying the

Depreciable Cost by a schedule of fractions.

♦ Units-of-Production Depreciation Method

Under the Units-of-Production method, useful life of the asset is expressed in terms of the total number of

units expected to be produced. Annual depreciation is computed in three steps.

First, a Depreciable Cost is computed.

Second, Depreciation per Unit is computed. Depreciation charge per unit is computed by dividing Depreciable Cost byTotal Units, expected to be produced during the useful life of the asset.

Depreciable Cost = Original Cost - Salvage Value

Book Value = Original Cost - Accumulated Depreciation

Depreciation per Unit = Depreciable Cost / Total Units of production

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 43/58

Third, annual depreciation, or Depreciation Expense, by another name, is computed. Depreciation Expense equals

Depreciation per Unit multiplied by the number of units produced during the year.

Book Value, as always, is calculated by subtracting Accumulated Depreciation from the Original Cost.

♦ Group Depreciation Method

Group Depreciation method is used for depreciating multiple-asset accounts using straight-line-depreciation

method. Assets must be similar in nature and have approximately the same useful lives.

♦ Composite Depreciation Method

The composite method is applied to a collection of assets that are not similar, and have different service

lives. For example, computers and printers are not similar, but both are part of the office equipment. Depreciation on all

assets is determined by using the straight-line-depreciation method.

Depreciation Expense = Depreciation per Unit * Units produced during the Year

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 44/58

Taxes

When a company spends money for a service or anything else that is short-lived, this expenditure is usually

immediately tax deductible in some countries, and the company enjoys an immediate tax benefit.

To be eligible for depreciation, an asset must have two features:

1. it has a useful life beyond the taxable year (essentially why it was capitalized in the first place), and

2. it wears out, decays, declines in value due to natural causes, or is subject to exhaustion or obsolescence.

Therefore, when a company buys an asset that will last longer than one year, like a computer, car, or building, the

company cannot immediately deduct the cost and enjoy an immediate large tax benefit. Instead, the company must

depreciate the cost over the useful life of the asset, taking a tax deduction for a part of the cost each year. Eventually the

company does get to deduct the full cost of the asset, but this happens over several years. In the jurisdictions accounting

depreciation and tax depreciation are almost always significantly different numbers, as in many instances a form of "accelerated depreciation" can be used for tax purposes to lower (taxable) net income in a given period (or, in some

instances, a fixed asset may be allowed to be expensed for tax purposes; Section 179 of the Internal Revenue Code allows

for this treatment in some circumstances). Technically, these are not considered "tax reductions" but tax deferrals lowering

taxable income now by increasing expenses should increase future taxable income (and taxes) at a later date.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 45/58

Importantly, no depreciation deduction is allowed for inventories or other property held for sale to customers in the ordinary

course of business. Land is also not depreciable. However, improvements to land, including landscaping, are usually

depreciable.

There are generally five variables that a taxpayer must take into account when computing the correct depreciation

deduction:

1. The depreciation base (the asset’s cost basis),

2. The asset’s class life (estimated life expectancy of the asset),

3. The applicable recovery period (the number of years the taxpayer can claim depreciation deductions),

4. The applicable depreciation method (see double declining balance method or straight-line method), and

5. The applicable convention (§ 168(d)(4) of the code—generally the half-year convention).

National accounts

In national accounts, depreciation represents the decline in the aggregate capital stock arising from the use of capitalin production, also referred to as consumption of fixed capital. Hence, depreciation is equal to the difference between

aggregate (gross) investment and net investment or between Gross National Product and Net National Product. Unlike

depreciation in business accounting, depreciation in national accounts is, in principle, not a method of allocating the costs of

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 46/58

past expenditures on fixed assets over subsequent accounting periods. Rather, fixed assets at a given moment in time are

valued according to the remaining benefits to be derived from their use.

RATES OF DEPRECIATION

Rate of Depreciation on Fixed Assets as per Company Act, 1956 are:

The fixed assets are valued at cost of acquisition or construction or at manufacturing cost (in case of own

manufactured / fabricated assets) in the year of capitalization less accumulated depreciation (except freehold land and

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 47/58

livestock). Depreciation on fixed assets for the year is provided on straight-line method as per Companies act, at the

following rates:

Note: These rates are only for shift I.

Besides this, the

following points may also be

taken care off regarding

depreciation.

1. All Fixed Assets other than

Land and Buildings, the depreciated value of which at the beginning of the year is Rs. 10000 or less; and all Fixed Assets,

other than Land & Buildings purchased in the year for a sum of less than Rs. 10000 each, are depreciated at the rate of

100% retaining a residual value for accounting control.

2. Full depreciation is provided on additions during the year.

3. No depreciation is provided on Land and Livestock.

Rate of Depreciation on Fixed Assets as per Income Tax Act, 1961 are:

Depreciation on fixed assets for the year is provided on written-down method as per Income tax act, at the following

rates:

Nature of assets Rate of depreciation

Factory buildings 3.34%

Residential buildings 1.63%

Electrical installations and equipment 4.75%

Plant & machinery 4.75%

Vehicles - Car 20%

Vehicles other than cars 33.33%Office equipment 4.75%

Computers 16.21%Furniture & fixtures 6.33%

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 48/58

Nature of assets Rate of depreciation

I.BUILDING1. Building which are used mainly for residential purposes

except hotels and boarding houses.2. Building other than those used mainly for residential purposes

and not covered by sub-items (1) above & (3) below.3.Building acquired on or after the 1st day of sep, 2002 for

installing P&M forming part of water supply project or water treatment system and which is put to use for the purpose of businessof providing infrastructure facilities under (i) of sub-section (4 ) of sec 80-IA.

4. Purely temporary erections such as wooden structures

5

10

100

100

II.FURNITURE AND FIXTURE10

III.PLANT & MACHINERY

1. P&M other than those covered by sub-items (2 ),(3 ) & (8 ) below:

2. Motors cars, other than those used in a business running themon hire, acquired or put to use on or after the 1 st day of Apr,1990.

3. (i) Aeroplanes – Aeroengines(ii) Motor buses, motor lorries and motor taxis used in a

business of running them on hire(iii) commercial vehicle which is acquired by the assessee on

or after the 1st

day of Oct, 1998, but before the 1st

day of Apr,1999 & is put to use for any period before the 1st day of Apr,1999 for the purposes of business in accordance with the 3rd

provision to clause (ii ) of sub-sec (1) of sec 32.(iv) New commercial vehicle which is acquired on or after the1st day of Oct, 1998, but before the 1st day of Apr, 1999 inreplacement of condemned vehicle of over 15 years of age &is put to use for any period before the 1st day of Apr, 1999 for the purposes of business in accordance with the 3rd proviso to

15

15

40

30

40

60

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 49/58

clause (ii) of sub-sec (1) of sec 32.(v) New commercial vehicle which is acquired on or after the1st day of Apr, 1999, but before the 1st day of Apr, 2000 in

replacement of condemned vehicle of over 15 years of age &is put to use for any period before the 1st day of Apr, 2000 for the purposes of business in accordance with the 3rd proviso toclause (ii) of sub-sec (1) of sec 32.(vi) New commercial vehicle which is acquired on or after the1st day of Apr, 2001 but before the 1st day of Apr, 2002 & is

put to use for any period before the 1st day of Apr, 2002 for the purposes of business.(vii) Moulds used in rubber & plastic goods factories(viii) Air pollution control equipment(ix) Water pollution control equipment

(x) Solidwaste control equipment.(xi) P&M, used in semi-conductor industry covering allintegrated circuits (ICS) ranging from SSI to LSI.(xia) Life saving medical equipment

4. Containers made of glass or plastic used as re-fills5. Computer including computer software6. P&M, used in weaving, processing & garment sector of textile

industry, which is purchased under TUFS on or after the 1st

day of Apr, 2001 but before the 1 st day of Apr, 2004 & is putto use before the 1st day of Apr, 2004.

7. P&M, acquired & installed on or after the 1st day of Sep,

2002 in a water supply project or a water treatment system &which is put to use for the purpose of business of providinginfrastructure facility under clause (i) of sub-sec (4) of sec 80-IA.

8. (i) Wooden parts used in artificial silk manufacturingmachinery(ii) Cinematograph films – bulbs of studio lights(iii) Match factories – wooden match frames(iv) Mines & quarries

60

50

30

100

100

100

30

40

50

60

50

100

100

100

100

100

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 50/58

(v) Salt works – salt pans, reservoirs & condensers, etc., madeof earthy, sandy or clayey or any other similar material(vi) Flour mills – rollers

(vii) Iron & steel industry – rolling mill rolls(viii) Sugar works – rollers(ix) Energy saving devices, being

A. Specialized boilers & furnacesB. Instrumentation & monitoring system for monitoring

energy flowsC. Waste heat recovery equipmentD. Co-generation systemsE. Electrical equipmentF. BurnersG. Other equipment

(x) Gas cylinder including valves & regulators(xi) Glass manufacturing concerns(xii) Mineral oil concerns(xiii) Renewal energy devices

9. (i) Books owned by assessees carrying on a profession – (a) Books, being annual publications(b) Books, other than those covered by entry (a) above

(ii) Books owned by assessees carrying on business in runninglending libraries.

10080

80

80

80

80

80

80

80

80

80

60

6060

80

100

60

100

IV. SHIPS(1)Ocean-going ships including dredgers, tugs, barges, survey

launches & other similar ships used mainly for dredging purposes & fishing vessels with wooden hull

(2) Vessels ordinarily operating on inland waters, not covered by sub-item (3) below

(3)Vessels ordinarily operating on inland waters being speed boats

20

20

20

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 51/58

Notes -

1. "buildings" include roads, bridges, culverts, wells & tube-wells.

2. "factory buildings" does not include offices, godowns, officers & employees' quarters, roads, bridges, culverts, wells &

tube-wells.

3. "speed boat" means a motor boat driven by a high speed internal combustion engine capable of propelling the boat at a

speed exceeding 24 Kilometers per hour in still water & so designed that when running at a speed it will plane, i.e., its bow

will rise from the water.

4. Where, during any financial year, any addition has been made to any asset, or where any asset has been sold, discarded,

demolished or destroyed, the depreciation on such assets shall be calculated on a pro rata basis from the date of suchaddition or, as the case may be, up to the date on which such asset has been sold, discarded, demolished or destroyed.

5. The following information should also be disclosed in the accounts:

(i) depreciation methods used; &

(ii) depreciation rates or the useful lives of the assets, if they are different from the principal rates specified in the Schedule.

6. The calculations of the extra depreciation for double shift working & for triple shift working shall be made separately in

the proportion which the number of days for which the concern worked double shift or triple shift, as the case may be, bears

to the normal number of working days during the year. For this purpose, the normal number of working days during the

year shall be deemed to be -

(a) in the case of a seasonal factory or concern, the number of days on which the factory or concern actually worked during

the year or 180 days, whichever is greater;

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 52/58

(b) in any other case, the number of days on which the factory or concern actually worked during the year or 240 days,

whichever is greater.

The extra shift depreciation shall not be charged in respect of any item of machinery or plant which has been specifically,

excepted by inscription of the letters "N.E.S.D." (meaning "No Extra Shift Depreciation") against it in sub-items above &

also in respect of the following items of machinery & plant to which the general rate of depreciation of 13.91 per cent

applies-

(1) Accounting machines.

(2) Air-conditioning machinery including room air-conditioners.

(3) Building contractor's machinery.

(4) Calculating machines.

(5) Electrical machinery

(6) Hydraulic works, pipelines & sluices

(7) Mineral oil concerns - field operations.

7. "Continuous process plant" means a plant which is required & designed to operate 24 hours a day.

8. Notwithstanding anything mentioned in this Schedule depreciation on assets, whose actual cost does not exceed fivethousand & rupees, shall be provided depreciation at the rate of hundred per cent:

Provided that where the aggregate actual cost of individual items of plant & machinery costing Rs. 5,000 or less constitutes

more than 10 per cent of the total actual cost of plant & machinery, rates of depreciation applicable to such items shall be

the rates as specified in Item II of the Schedule.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 53/58

AMORTIZATION

What Does Amortization Mean?

1. The paying off of debt in regular installments over a period of time.

2. The deduction of capital expenses over a specific period of time (usually over the asset's life). More specifically, this

method measures the consumption of the value of intangible assets, such as a patent or a copyright.

While amortization and depreciation are often used interchangeably, technically this is an incorrect practice because

amortization refers to intangible assets and depreciation refers to tangible assets.

Amortization is the process of increasing or accounting for, an amount over a period of time. Particular instances of

the term include:

Amortization is also used in the context of zoning regulations and describes the time in which a property owner has

to relocate when the property's use constitutes a preexisting nonconforming use under zoning regulations.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 54/58

RECONCILIATION OF ASSET REGISTERS

A fixed asset register is a statutory register maintained under section 209(1) (c) of the Companies Act. 1956. This

register requires a company to maintain various details relating to all its assets that form a part of its total fixed asset block.

Any failure to maintain this register as required by the statute may entail penalty, which may extend to imprisonment in

some cases.

Apart from statutory requirements, a well maintained asset register could also help in the following:

INSURANCE

When the correct value or description of assets is not known, there stands a risk of over or under insuring assets.

While over insuring would entail excess cost in the form of premium charges, under insuring would imply that the

enterprise will not be able to recover adequate amount of claims from the insurance company if any unfortunate event

strikes.

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 55/58

IMPAIRMENT OF ASSETS

As per Accounting Standard 28 issued by ICAI, all enterprises will be required to account for any loss on impairment

of assets. A well maintained asset register would be the basic requirement for complying with this requirement.

COSTING RECORDS

Proper maintenance of assets assists the enterprise in deriving information regarding output and efficiency of

machines and other assets. This in turn aids the allocation of overheads and cost control.

ASSIST STATUTORY INVESTIGATIONS

Often statutory investigations and audits like the excise audit or cost audit call for asset registers. A systematic

maintenance of asset registers can make the audit proceedings less cumbersome.

MONITORING ASSETS

Monitoring and maintenance of assets becomes more meaningful and simpler when all data relating to assets is

tabulated and maintained in the form of a register.

However, though the exercise appears to be uncomplicated and undemanding on paper, the reality is far from that. In

most cases, it is very difficult to get any details of assets that were acquired a long time back. Even if any acquisitions were

documented at the time of purchase, most records are either lost or destroyed due to natural calamities or have simply been

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 56/58

misplaced or discarded. Also, often when assets are discarded or transferred between plants no matching entry is made in

the asset register. Entries if made also seldom carry accurate technical descriptions. In such a situation, it becomes

excessively difficult to maintain an asset register.

As a result the assets on ground seldom match the assets as appearing in the asset register. Also the net block value of

assets as shown in the fixed asset register does not represent the value of net block as shown in the Balance Sheet. For the

purpose of a meaningful maintenance of the asset register, it thus becomes pertinent to reconcile the assets as they appear in

the books with the actually existing assets.

The process of reconciliation entails in following three stages:

PHYSICAL VERIFICATION

This refers to a physical verification of assets on ground. Thereafter these assets are classified and segregated on the

basis of block of assets as defined by the Companies Act. This exercise requires an intense technical knowledge for the

accurate identification of assets. The assets verified, classified and segregated are then tabulated against other details like

acquisition date and cost, accumulated depreciation etc.

VALUATION OF ASSETS

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 57/58

After the technical exercise, the assets need to be assigned a carrying cost. In some cases where there is no data

relating to the actual cost of acquisition, it also involves ascertaining a current value as carrying cost of the asset. As there

are many variants of current value, this process also requires expertise in finance. Depending on the situation, the carrying

cost is to be fixed at one of the following values for each asset - market value, realizable value or the distress sale value.

MATHEMATICAL RECONCILIATION

After the technical assessment and assignment of values, the figures relating to each asset block are reconciled with

their values as appearing in the Balance Sheet.

METHODOLOGY OF STUDY

8/8/2019 paresh report1

http://slidepdf.com/reader/full/paresh-report1 58/58

Data collection is an essential part of a research proposal the task of data collection starts after the objective of the

study and the Research Design has been decided. The Research data is generally of two types.

(I) Primary Data: -

Oral interview of Company Finance Manager was taken to get relevant information or data from the

Company.

(II) Secondary Data: -

The study is mainly based on secondary data for the purpose of this study, secondary data has been collected

from annual reports and relevant records of the M/s. Piaggio Vehicles Pvt. Ltd., Baramati.

Related Documents