Hyman et al.: Paradigms, Policies and People 89 PARADIGMS, POLICIES, AND PEOPLE: EXPLORING THE LINKAGES BETWEEN NORMATIVE BELIEFS, PUBLIC POLICIES AND UTILITY CONSUMER PAYMENT PROBLEMS Drew Hyman, Jeffrey Bridger, John Shingler, and Mollie Van Loon Department of Agricultural Economics and Rural Sociology The Pennsylvania State University ABSTRACT This article takes a step toward unifying normative and empirical policy analysis by examining the convergence of societal metatheories, public policy models, and empirical data on consumers. It begins with fhe premise that policies resf on a foundafion of normative beliefs or metafheories that, in turn, put boundaries around the possible and give social meaning to the policies and programs that flow from them. The interaction of social mefatheories about poverty and existing policies to deal with people with utility payment problems is examined. The article continues wifh the idea that good policy arguments are supported with empirical data and factual evidence. An empirical cluster analysis of a represenfative sample of consumers provides a basis for idenfifying the extent to which the empirical clusters conform to any or all of the metafheory-policy linkages. The ultimafe message is that theory and practice ought to demarcate where they are deductively metaphysical, based on beliefs about a subjecf, where they are inductively empirical, based on objective measurements relevant to the situation to which applied, and where a mixed approach is used. Linkage of fhe three types of information allows policy research to identify options in light of the values and metatheories on which they are based and the objective characteristics and effects on fheir objects of acfion. The implications are that when policies are based on beliefs thaf reflect only a part of empirical reality, implemenfafion may fail or be inefficient and ineffective.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Hyman et al.: Paradigms, Policies and People 89

PARADIGMS, POLICIES, AND PEOPLE: EXPLORING THE LINKAGES BETWEEN

NORMATIVE BELIEFS, PUBLIC POLICIES AND UTILITY CONSUMER PAYMENT PROBLEMS

Drew Hyman, Jeffrey Bridger, John Shingler, and Mollie Van Loon

Department of Agricultural Economics and Rural Sociology

The Pennsylvania State University

ABSTRACT

This article takes a step toward unifying normative and empirical policy analysis by examining the convergence of societal metatheories, public policy models, and empirical data on consumers. It begins with fhe premise that policies resf on a foundafion of normative beliefs or metafheories that, in turn, put boundaries around the possible and give social meaning to the policies and programs that flow from them. The interaction of social mefatheories about poverty and existing policies to deal with people with utility payment problems is examined. The article continues wifh the idea that good policy arguments are supported with empirical data and factual evidence. An empirical cluster analysis of a represenfative sample of consumers provides a basis for idenfifying the extent to which the empirical clusters conform to any or all of the metafheory-policy linkages. The ultimafe message is that theory and practice ought to demarcate where they are deductively metaphysical, based on beliefs about a subjecf, where they are inductively empirical, based on objective measurements relevant to the situation to which applied, and where a mixed approach is used. Linkage of fhe three types of information allows policy research to identify options in light of the values and metatheories on which they are based and the objective characteristics and effects on fheir objects of acfion. The implications are that when policies are based on beliefs thaf reflect only a part of empirical reality, implemenfafion may fail or be inefficient and ineffective.

90 Policy Studies Review 18:2 (Summer 2001 )

INTRODUCTION

This article examines the interaction of societal metatheories, public policy models, and empirical data on consumers. It begins with the idea that “all policy arguments are normative in purpose and that a good policy argument supports its normative claim with factual and value-based ‘good reasons’ (Ball: 1995). ” That is, societal policies rest on a foundation of normative beliefs and metatheories put boundaries around the possible and give social meaning to the sectoral and jurisdictional policies and programs that flow from them. Specifically, the interaction of social metatheories about poverty and existing policies to deal with people with utility payment problems is examined. The normative metatheory-policy linkage is followed by an empirical cluster analysis of people with utility payment problems toward identifying the extent to which there is a logical policy fit between the empirical clusters and any or all of the metatheory-policy linkages. We are thus examining the extent to which public policies, which reflect different patterns of normative beliefs, in this case public policies related to the inability of some consumers to pay their utility bills, reflect the empirical realities of the polity.

We focus on a pervasive and persistent policy issue in contemporary American society--the failure of some consumers to pay their bills, and to pay them on time. The development of practices and policies to deal with nonpayers is an age-old problem. A market economy tends to see this as a private relationship between buyers and sellers. A democratic society, however, becomes concerned when the operation of the economy leads to health and safety problems that are seen as contrary to the public interest and a topic for public policy. In this case, we begin by conceptually linking existing public policies for dealing with people with utility payment problems to a typology of metatheories about poverty in the U.S. These linkages are then examined in relation to a series of empirically defined profiles of consumers based on how different groups handle monthly payments when they are short of cash and whether they had utility payment problems in the last year. It suggests that policies for cutting off services or products may be appropriate for some consumers but may create health and safety problems for others. At the same time, public

Hyman et al.: Paradigms, Policies and People 91

perceptions and public policies rest on a foundation of beliefs and societal metatheories that constrain consideration of some actions and channel programs in certain directions.

The Public Policy Context

Since the late 197Os, rates of residential nonpayment of utility bills have increased at a rate exceeding the growth in consumer income (Pobjecky:l976, Pennsylvania Public Utility Commission, 1992:29, Colton, 1992). During this period government funding for energy assistance decreased and utility arrears increased. In Pennsylvania, for example, energy assistance for the Low Income Home Energy Assistance Program (LIHEAP) declined by 32 percent from 1985 to 1991. The results of these trends are evident in their impact on utility collections measures. From 1987 to 1990 total residential utility customer debt in Pennsylvania rose by 31 percent (from $217 million to $287 million). In the same period, the number of residential customers owing at least $1000 increased by 134 percent (from 9, 810 to 22,977). (Pennsylvania Public Utility Commission: 1992). A study by the National Consumer Law Center in 1995 found similar trends occurring in the majority of states: cuts in energy assistance, increased energy bills, and the rising cost of water service all combine to increase the energy burden on residential households, resulting in increased utility collections expenses, shutoffs or write-offs (Saunders and Spade: 1995).

Traditionally, nonpayment has been considered a market economic issue: "no pay no service." This view undergirds the dominant market approach to nonpayment of bills. Under this policy, which we call the collections model, utility companies typically rely on overdue notices, threats of termination, and eventual shutoffs to deal with consumers who cannot or do not pay their utility bills. In recent decades, this approach has created public health and safety concerns as customers with terminated service face threats to health, safety, and loss of life due to lack of heat in the winter and lack of cooling in the summer. These problems led to public policy intervention at the federal level and in many states. Several additional policy models have emerged (Hyman, Wadsworth, and Alexander: 1987). A second approach,

92 Policy Studies Review 18:2 (Summer 2001 )

the amortization model, provides due process procedures for notice and termination cases. It assumes that utility payment problems exist because of some sort of temporary emergency such as job loss or a health crisis and the consequent cash flow reduction. However, this model does not prohibit termination nor does it provide payment assistance.' A third approach to payment problems is the transfer payment/financial aid model. The policies associated with this model reflect the widely shared belief that public utilities are necessities of life that should not be allocated strictly on market criteria. In addition, it is assumed that increases in nonpayment rates are associated with poverty, unemployment, or similar circumstances (Ritti and Hyman: 1981, Hyman, Wadsworth, and Alexander: 1987). Given these considerations, it is not surprising that the transfer payment/financial aid model relies on a mix of government, nonprofit, and private efforts that provide supplemental income and promote conservation and usage reduction. Observation of events in the field lead us to a fourth approach, the physical environment model, which sees a combination of climate, weather, and housing as causal forces. Policies and programs for weather conditions and poorly insulated housing stock drive up heating and cooling costs beyond the affordability of many customers. Weatherization, conservation, and usage reduction are seen as complimentary and appropriate measures to reduce utility costs and, in turn, make bills more affordable. Underlying each of these models are different

'Federal guidelines embodied in the Public Utility Regulatory Policies Act of 1978 (PURPA), Sections 11 5 (9) and 304 (2) do not prohibit the termination of residential utility service (P.L. 95-61 7, 92 Stat. 3117 et. seq. (16 U.S.C. 2601 et. seq.)). Rather, the guidelines specify procedures for prior notice before termination begins, for reasonable opportunity to dispute, for protection during health emergencies, special provisions for vulnerable populations, and opportunities for time payment arrangements to retire the outstanding amount (PURPA, 1978). Comparable Pennsylvania statutes (Title 52, PA Code, Chapter 56) establish statewide regulations requiring due process procedures to be followed by both consumers and companies when termination of service is threatened.

Hyman et al.: Paradigms, Policies and People 93

sets of values and metatheories about the etiology of the problems they seek to ameliorate and the people they intend to help.

Social Metatheories about Wealth and Poverty

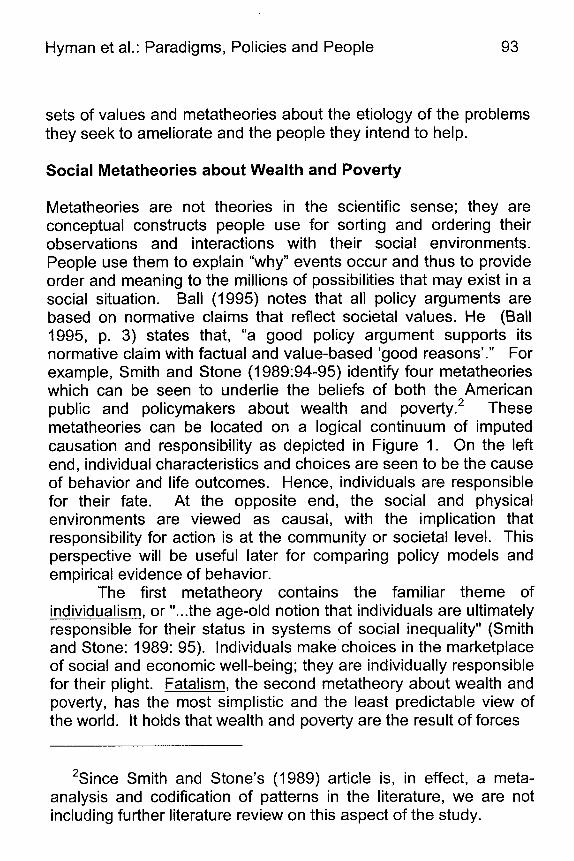

Metatheories are not theories in the scientific sense; they are conceptual constructs people use for sorting and ordering their observations and interactions with their social environments. People use them to explain “why” events occur and thus to provide order and meaning to the millions of possibilities that may exist in a social situation. Ball (1995) notes that all policy arguments are based on normative claims that reflect societal values. He (Ball 1995, p. 3) states that, “a good policy argument supports its normative claim with factual and value-based ‘good reasons’.” For example, Smith and Stone (1 989:94-95) identify four metatheories which can be seen to underlie the beliefs of both the American public and policymakers about wealth and poverty.2 These metatheories can be located on a logical continuum of imputed causation and responsibility as depicted in Figure 1. On the left end, individual characteristics and choices are seen to be the cause of behavior and life outcomes. Hence, individuals are responsible for their fate. At the opposite end, the social and physical environments are viewed as causal, with the implication that responsibility for action is at the community or societal level. This perspective will be useful later for comparing policy models and empirical evidence of behavior.

The first metatheory contains the familiar theme of individualism, or ”...the age-old notion that individuals are ultimately responsible for their status in systems of social inequality” (Smith and Stone: 1989: 95). Individuals make choices in the marketplace of social and economic well-being; they are individually responsible for their plight. Fatalism, the second metatheory about wealth and poverty, has the most simplistic and the least predictable view of the world. It holds that wealth and poverty are the result of forces

2Since Smith and Stone’s (1989) article is, in effect, a meta- analysis and codification of patterns in the literature, we are not including further literature review on this aspect of the study.

n

7

Figure 1

Metatheories and the C

ontinuum of C

ausation and Responsibility

0

0

N

?! 03

Figure 2 M

etatheories and Policy M

odels

S H 0 R T-TE RM

LONG-TERM

PhSICAl FI N A NC IA L

(CULTURAL) (STRUCTURAL)

MOD El M

ODEL

ENVIRONMENT FI NANClAL

COLLECT1 ONS A MO RTI ZATl 0 N MOD El

ASSISTANCE ASSISTANCE

MODEL

MODEL

Hyman et al.: Paradigms, Policies and People 95

so complex and unpredictable as to be virtually unmanageable. What is important is being in the right (or wrong) place at the right (or wrong) time. As Smith and Stone (1989:95) put it, the causes of wealth and poverty are attributed to "...quirks of birth, human nature, chance, and related forces over which people and social structures have no control.'' The third, cultural or subcultural, metatheory (culturalism) modifies the individualist rnetatheory's emphasis on individual responsibility with a quasi-fatalistic injection of social structural and situational considerations. This is a more comprehensive perspective insofar as both personality and social structures are seen to interact as mutually reinforcing products so as to create "...self-perpetuating, adaptive ways of life ...'I (Smith and Stone: 1989:94). In other words, social structure and life experiences combine to produce distinct subcultures which characterize both the wealthy and the poor. The culture or personality of some groups or individuals will lead them to dominate social and economic institutions while others are less successful in weathering the vicissitudes of the marketplace. The fourth metatheory is what Smith and Stone (1989:95) call structuralism/situationalism. This is a rather deterministic perspective in which broad social structural forces are seen as the main causes of wealth and poverty. These forces are responsible for the distribution of wealth rather than either the marketplace or the intersection of individual traits of the wealthy and the poor. From this perspective social and economic structures fail to provide equal opportunity to all. The wealthy control society's major social and economic and institutions and, through this control, maintain and legitimize the unequal distribution of life chances. It is the social and economic environment rather than individual behavior that determines one's plight.

Social Metatheories and Public Policy Options

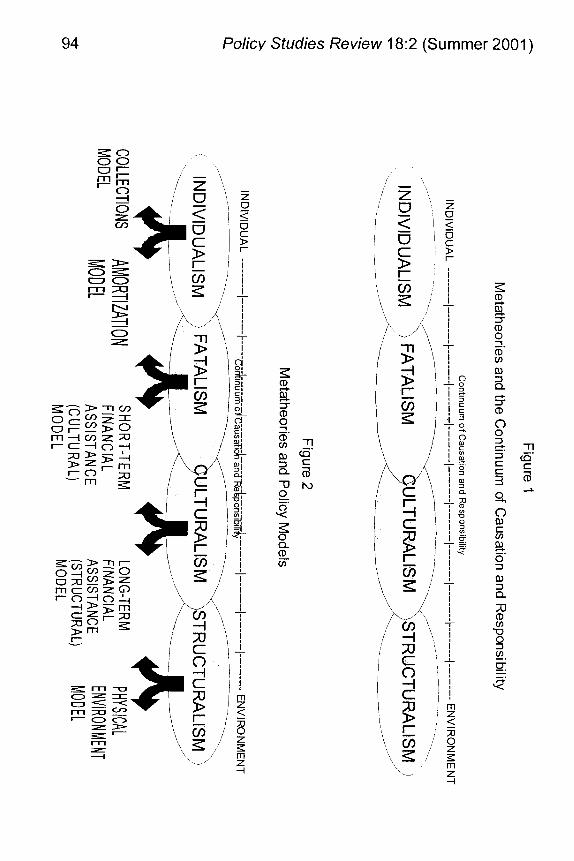

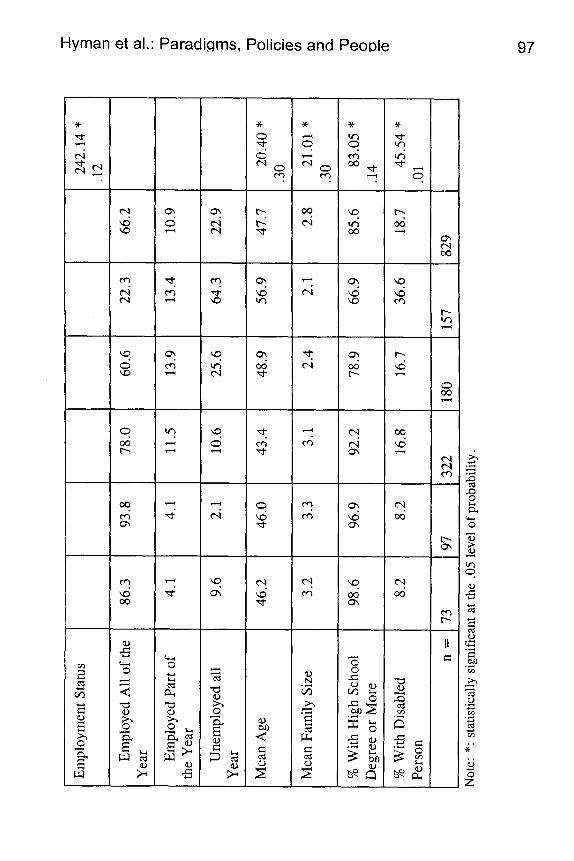

These metatheories are not simply academic abstractions. They provide the parameters (worldview) within which their adherents view social and economic issues and, in turn, they may become the basis for argument, advocacy, and eventually public and private policies and programs (Bak1995). Figure 2 shows how the various policies that address consumers with utility payment problems can

r TA

BLE

1 : D

ESC

RIP

TIV

E ST

ATI

STIC

S O

F T

HE

CLU

STER

CH

AR

AC

TER

ISTI

CS

BY T

HE

FIV

E C

LUST

ER S

OLU

TIO

N

% W

ith P

aym

ent

Prob

lem

s in

Pre

viou

s Y

ear

Esta

blis

hed

Syst

ems

Mar

gina

l C

LUST

ER V

AR

IAB

LE

1 Intere

sts

1 Manag

ers

1 Househ

olds

8.2

12.4

22

.4

% o

f Res

pond

ents

Who

W

ould

Put

Off

Payi

ng

50%

or m

ore

of B

ills

in

Mon

th

Mea

n #

of A

pplia

nces

O

wne

d

32.9

34

.0

37.0

31

.1

Mea

n In

com

e 1 $75,

000

1 $62,50

0 1 $37,

182

22.3

Hom

e O

wne

rshi

p st

atus

Ow

n W

ith N

o M

ortg

age

Ow

n W

ith M

ortg

age

64.4

53

.6

45.7

30.1

35

.1

35.4

I R

ente

rs

1 5.

5 1

11.3

1

18.9

Con

sum

ers

$20,

333

$9,2

52

7-

7.6

27.2

I

32.8

I

38.9

Ove

rall

22.2

4.4

32.2

$34,

527

37 .O

39.3

23.6

Chi S

q. I

F Si

g.

Eta 20

.02

* .0

7 89.9

0 *

.55 10

.65

* .0

4

4472

.84

* .9

8 122.

14 *

.18

h

v) c 3 3 $

h) 0

0

2

Empl

oym

ent S

tatu

s

86.3

4.1

9.6

46.2

3.2

98.6

8.2

13

~~

Empl

oyed

All

of t

he

Yea

r

242.

14 *

.12

93.8

78

.0

60.6

22

.3

66.2

4.1

11.5

13

.9

13.4

10

.9

2.1

10.6

25

.6

64.3

22

.9

46.0

43

.4

48.9

56

.9

47.7

20

.40

* .3

0

3.3

3.1

2.4

2.1

2.8

21.0

1 *

.30

96.9

92

.2

78.9

66

.9

85.6

83

.05

* .1

4

8.2

16.8

16

.7

36.6

18

.7

45.5

4 *

.01

97

322

180

i57

829

Empl

oyed

Par

t of

the

Yea

r

Une

mpl

oyed

all

Yea

r

Mea

n A

ge

Mea

n Fa

mily

Siz

e

% W

ith H

igh

Scho

ol

Deg

ree

or M

ore

% W

ith D

isab

led

Pers

on

n=

N

ote:

*:

statis

tical

ly si

gnifi

cant

at th

e .0

5 le

vel o

f pro

babi

lity

98 Policy Studies Review 18:2 (Summer 2001)

be seen as jurisdictional policies that logically reflect the value- based societal policies articulated in these popular metatheories about the causes of wealth and poverty (Palumbo:1987, Nakamura: 1987, Yanow: 1987, Hyman, Wadsworth and Alexander: 1991 ).

For instance, the traditional market-based collections model for dealing with nonpayment of utility bills can be conceptualized as a logical manifestation of beliefs in individualism. It assumes that the individual is ultimately responsible for him or herself and family in the marketplace. The amortization model is reflective more of fatalism insofar as it is intended to provide temporary respite in times of hard luck (i.e. seasonal unemployment, health crisis, unexpected expenses). The short term payment arrangement policies of the model are best thought of as a helping hand to individuals during unfortunate emergencies. The assistance based approaches have several variants which can be seen to flow from the remaining metatheories. Short term assistance such as credit counseling and one-time crisis grants rely in part on a culturalist interpretation of payment behavior by assuming that certain payment troubled consumers need outside or expert assistance in managing their finances. Complaints about those who take advantage of the system tend to be based on the culturalist argument that some people are highly motivated to pursue only their self interest. Longer term assistance based approaches such as annual heating grants and lifeline programs tend to rely on Structuralist ideas about poverty. There is an implicit assumption that larger social forces beyond individual control, such as structural unemployment and underemployment, lead to a chronic inability to pay. Additionally, if the structuralist ideas are extended to the non-social environment, additional policies are encapsulated in what we will call the physical environment model. Conservation education, usage reduction measures (e.9. water heater and refrigerator replacement) and weatherization address the physical character of housing and factors related to climate and weather conditions. The question naturally arises as to what extent these metatheories and their associated policy approaches conform empirically to consumer characteristics and behavior. Or, another way of putting the matter is: do public policy models, and the metatheories which support them, reflect empirical behavioral

Hyman et al.: Paradigms, Policies and People 99

patterns of consumers? In what follows, we attempt to provide a preliminary answer to this question.

Data And Procedures For The Empirical Analysis

Data for a multivariate cluster analysis were drawn from a statewide representative sample of residential telephone customers in Pennsylvania. The sample was purchased from a national survey sampling firm. It was stratified by region of the state to ensure proportional representation of rural and urban areas and of low income residents. Interviewers asked to speak to the person in the household who makes decisions about utility services. If this person was not available at the time of the first call, arrangements were made for call backs. These procedures resulted in a completed statewide sample of 1006 telephone customers.

In order to identify different types of customers and payment behaviors, hierarchical cluster analysis was performed. Cluster analysis is a statistical technique which identifies sub-groups of people or objects according to how they differ on a set of variables. It is particularly useful for identifying groups clients, patients or consumers for determining treatment strategies, marketing methods and public programs. For this study, it places a representative statewide sample of consumers into relatively homogenous groups based on inter-object similarities (Kachigan: 1982: 261). Once these subgroups are identified they can be compared with respect to input variables used to construct the clusters as well as related variables for which data are available.

Statistical issues that must be considered when using cluster analysis are similar to those involved in exploratory factor analysis. A first issue involves determining the optimal cluster solution. This issue involves determining the relative homogeneity of the clusters; that is, “the discriminatory power of each group for the input variables and data, and the replicability of the solution” (Thomas, et al, 1996:354). Since each case represents a relatively unique individual, there are potentially as many clusters as there are cases. Thus the optimal solution is some number of clusters more than one and less than “n,” where “n” is the number of cases in the database. The choice is in large part determined by the amount of detail desired by the analyst (or their client), or the logical fit with

100 Policy Studies Review 18:2 (Summer 2001)

the task or problem at hand. This relates to the second issue to be considered--the validity of the cluster solution “regarding statistical significance tests on input variables and external criteria” (Thomas, et al, 1996: 354). Our preliminary analysis examined twelve and then seven possible cluster solutions. Each of these solutions was systematically compared on the input variables. After considering the possible combinations, we retained the five cluster solution for this study as the solution allowing for the optimum level of parsimony and detail. In other words, the more numerous cluster solutions resulted in distinctions between groups which were so fine as to be analytically unwieldy for present purposes. However, it will be seen that the two, three, five and seven cluster solutions might well serve for developing policy alternatives of more or less specificity. That is, the different cluster solutions differentiate potential targets for public policies much as markets are segmented to increase the probability of sales. Thus, the analysis that follows is based on the five cluster solution derived from the following input variables:

Bill Payment Behavior: 1) Presence or absence of one or more overdue electric, gas, water, telephone bills during the previous year. Respondents were also asked if they had received a termination notice during the previous year; 2) Percent of applicable bills that the respondent would put off paying if they were short of cash at the end of the month. (These include mortgage or rent payment, car or truck payment, telephone bill, electric bill, credit card, money for food, water or sewer bill, loan payment, home heating or fuel bill, and cable television bill).

Economic Variables: I ) Total household income; 2) Employment Status of the main earner.

Demoqraphic Variables: 1) Education of the main earner in the household (dichotomized as less than high school and high school education or more); 2) Age of main earner; 3) Family size; 4) Presence or absence of disabled persons in the household.

Social Status Variables: 1) Home ownership status (defined as own with no mortgage, own with a mortgage, or renting/leasing). 2)

Hyman et al.: Paradigms, Policies and People 101

Appliance ownership (appliances include washer and dryer, dishwasher, black and white television, color television., microwave, home computer, and VCR.)

In addition to these input variables for cluster formation, several other variables are used to compare the consumer groups. These include source of income of main wage earner, gender and marital status of respondent, stated reason for payment problem, and degree of payment problem.

Research Results

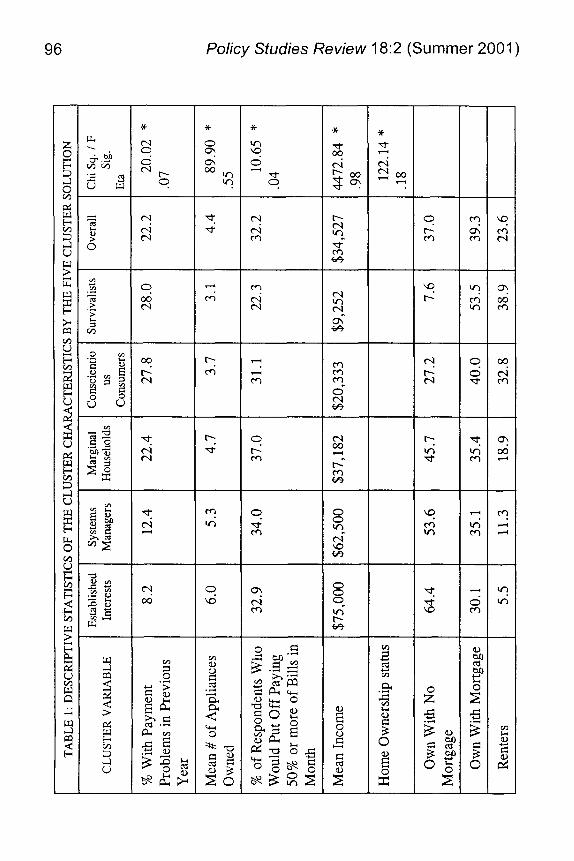

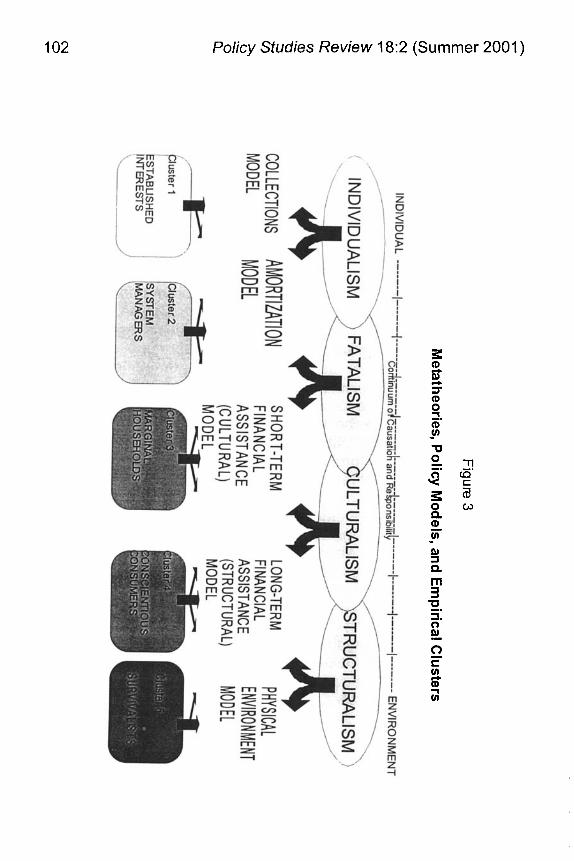

The clusters are labeled to reflect what we believe to be salient characteristics of their members as follows: established interests, systems managers, marginal households, conscientious consu mers , and st rug g I i ng su rvival ists .

Furthermore, there is a distinct progression in the incidence of utility payment problems across clusters: established interests tend to experience the lowest rate of payment problems while the survivalist experience the highest rate. With few deviations, this pattern applies for the other study variables as well. Tables 2-5 present additional information on the clusters. The following summaries highlight the characteristics of the consumer cluster profiles.

The Established Interests constitute about one in ten consumers (8.8 percent). For the most part, these individuals are well established professionals with a low rate of payment problems. Moreover, the economic and social characteristics of those with payment problems and those without payment problems are not noticeably different. In fact, 80 percent of those reporting a payment problem during the previous year do not provide a reason for not being able to pay their utility bill. A majority are between the ages of 35 and 49 (mean age=46.2). Over 90 percent have completed high school or more. Most have fairly high incomes derived mainly from salary and wages (mean income=$75,000), own their homes with no mortgage (64.4 percent report that they do not have a mortgage), and are likely to own most of the major appliances mentioned by the interviewers (mean number of appliances=6.0). Most are married (81.3 percent of the men and

102 Policy Studies Review 18:2 (Summer 2001)

Hyman et al.: Paradigms, Policies and People 103

92.7 percent of the women are married), and they are likely to have children (mean family size=3.2).

This cluster has the lowest rate of characteristics frequently associated with social problems. Relatively few report being unemployed during the previous year (9.6 percent). Few have disabled persons living in the household (8.2 percent). Only about one third would put off paying 50 percent or more of their monthly bills if they were short of cash at the end of the month. Of the 8.2 percent who received an overdue utility bill for an electric, gas, telephone or water utilities bill, only 16.7 percent eventually received a termination notice.

As a group, these "established interests" clearly have the ability to pay their bills and most do so on time. Of the small percentage who do not pay immediately, all but a few pay prior to receiving a ten day termination notice. This group of consumers logically reflects both the individualistic and cultural theories about wealth. Individually they have achieved economic independence and well-being. Socially, they exhibit the characteristics for higher status in American society. Thus, they would not be expected to have utility payment problems except as they seek to manipulate the system for their personal benefit. They are not targets for any of the assistance policies for dealing with non payment of utility bills except the "no pay no service" Collections Model, which seems to be the best fit among the options. For those consumers who do have overdue bills, it might be appropriate to ascertain whether individualistic manipulation for personal gain or some temporary crisis beyond their control is the precipitating factor before action is taken to cut off service.

The System ManaQers constitute another one in ten consumers (I 1.7 percent). These individuals have fairly high incomes, yet 12.4 percent report experiencing one or more overdue bills during the last year. Based on their economic and social status, there are no compelling explanations for such a rate of payment problems. They may use nonpayment as a way to manage cash flow, although a significant percentage cite fatalistic events as being associated with instance of nonpayment. Over 90 percent have completed high school or more. They have high incomes derived primarily from salaries and wages (mean income=$62,500), most own their homes but a sizable portion are

104 Policy Studies Review 18:2 (Summer 2001)

paying a mortgage (53.6 percent own with no mortgage; 35.1 percent own with a mortgage), but they own most major appliances (mean number of appliances=5.3). A majority are married (77.3 percent of the men and 86.8 percent of the women are married), and they are likely to have children living at home (mean family size=3.3). The system managers, also, have a fairly low rate of characteristics frequently associated with social problems. Few experienced any unemployment during the previous year (2.1 percent were unemployed during the previous year), and compared to the more "stressed" groups, relatively few of these consumers have disabled persons living in their households (8.2 percent). However, approximately one third would put off paying 50 percent or more of their bills if they were short of money at the end of the month. But, of those who report an overdue bill, half (50 percent) offer no reason for their payment problems and the other half cite some mitigating factor (including no money, illness, unemployment, high bills, or other financial problems). Of those who reported overdue utility bills (12.3 percent), one in four eventually receive termination notices.

Compared to the established interests, these consumers, have somewhat lower incomes and a higher rate of payment problems. They may consist of a mix of consumers who manipulate the system to benefit their cash flow, and those with long term costs associated with mortgages, careers and children living in the household. Particularly noticeable is the high percent (50 percent) who cite temporary factors (unemployment, high bills, etc.) that prevent timely payment. For the former, the Collections Model logically has the best fit, seeking to assure that the costs of system manipulation are borne more directly by the manipulators, rather than other rate payers. For this group, the Amortization Model features provisions for extended payment plans may be appropriate when temporary inabilities to pay exist.

The Marginal Households constitute almost two in five consumers (38.8 percent). A majority are over the age of 35 (mean age=43.4), and most have at least a high school education (92.2 percent have a high school degree). These consumers generally have average incomes (mean income=$37,182), and over 80 percent derive the majority of their income from salary and wages. Although most either own their homes with a mortgage or own them

Hyman et al.: Paradigms, Policies and People 105

outright, approximately 20 percent are renters (1 8.9 percent), and have fewer major appliances (an average of 4.7) than the first two groups. A majority are married although 16 percent of the women and 31.4 percent of the men are either single, divorced, or widowed. The average marginal household has fewer children living at home (mean family size=3.1) than the first two clusters, but more than the last two clusters.

Although most of these individuals can be considered average in terms of income, they cite a number of factors that most likely affect their ability to make timely utility bill payments. For instance, slightly more (10.6 percent) report that the main earner was unemployed during all of the previous year and 16.8 percent have a disabled person living in the household. With such factors combined with the other background characteristics, it is not surprising that approximately 37 percent say they would put off paying more than half of their bills if they were short of money at the end of the month. Nearly 25 percent of the respondents in this cluster experienced an overdue bill during the last year, and, when asked why they did not pay a utility bill on time, nearly 70 percent cite a combination of unemployment, illness, lack of money, extra high utility bills, or other financial problems. Of those who experienced an overdue bill, 45.8 percent received at least one termination notice.

On the surface, these consumers appear to be middle class and would seem to be candidates for the individualistic approach inherent in the collections model. However, the fact that many express behavioral patterns of putting off bill payment and cite management, household or personal factors for their payment problems, suggests that policies which reflect a combination of fatalistic and cultural metatheories may be more appropriate for this group. (This classification seems even more appropriate after consideration of the first two clusters.) For many of these people, the Collections Model would leave them without utility services during extreme weather conditions and/or may lead to the types health and safety risks discussed in Hyman, Meyer and Wadsworth (1 985). The amortization model seems logically most appropriate here, perhaps combined with credit counseling for some, and short- term financial aid where extreme hardship or disability exists.

106 Policy Studies Review 18:2 (Summer 2001)

The Conscientious Consumers constitute 21.7 percent of the consumers in this sample. Approximately half of these individuals are over the age of 40 (mean age=48.9) with a mean income of $20,333. Moreover, if one considers such factors as their high unemployment rate (25.6 percent report that the head of household was unemployed all of the previous year), the high percentage of respondents who have disabled persons living in the household (1 6.7 percent), and many with low educational attainment (78.9 percent completed high school or more), it is not surprising that the level of payment problems is higher than the previous three clusters.

Approximately 30 percent of this cluster relies on social security and/or pensions for their annual income, and although a majority either own their homes outright or own with a mortgage, approximately one third are renters (27.2 percent own with no mortgage; 40.0 percent own with a mortgage), and they own comparatively few major appliances (the mean number of appliances is 3.7). For male and female respondents, approximately 1/2 are either single, divorced, or widowed (50 percent of the men and 51.6 percent of the women fall in these categories). The mean family size is 2.4, suggesting that few have children living at home; however, this cluster (and the next) has a significantly higher percentage of female single heads of household with children (13.6 percent).

Despite the fact that they have higher rates of the characteristics frequently associated with social problems than the first two groups, these households are similar to established interests and less than the other previous groups in terms of similar percentages of persons saying they would put off paying more than half of their bills if they were short of money at the end of the month--hence the label “conscientious” consumers! Of those who report an overdue bill, over 90 percent cite one or more of the following reasons: unemployment, illness, lack of money, extra high utility bills or other financial difficulties. Of those who report an overdue bill, 56.0 percent received at least one termination notice which is the highest among all of the clusters.

These consumers logically reflect the downside of the structural/situational metatheory. For the most part, serious problems beyond their control prevent timely bill payment.

Hyman et al.: Paradigms, Policies and People 107

However, their attitude toward putting off paying bills suggests that the motivation to pay is there, and manipulation of the system does not seem to be a serious issue. Financial Aid Model policies that provide payment assistance, lifeline rates, and/or Conservation Model usage reduction measures and weatherization are logically the most appropriate fit for many households in this cluster for which the Amortization Model may compound their plight.

The final group, the Survivalists constitutes about one in five consumers (1 8.9 percent). By virtually any standard, these people are living in severe poverty (mean income=$9,;!52). Not surprisingly, they also report the highest rate of payment problems (28.0 percent). The factors contributing to this situation are neatly summarized by the following statistics: 64.3 percent of main earners were unemployed during all of the previous year; approximately 36.6 percent of households have disabled members; 62.4 percent derive most of their income from social security and/or pensions while 7 percent rely on unemployment compensation and public assistance.

While the current public policy debate might lead one to think that these are mainly young single-parent households, approximately 50 percent are over the age of 60 (mean age=56.9), and they have relatively small families (mean family size=2.1) compared to the other groups. However, approximately 80 percent of these consumers are women, and of these, 41.3 percent are widows. Like the previous cluster, this cluster also has a significantly higher percentage of single female headed households with children. These consumers also own the fewest major appliances (mean number of appliances=3.1). It is not surprising that of those who report an overdue bill, almost 90 percent cite some combination of the following reasons for their inability to pay: unemployment, illness, lack of money, unusually high utility bills or other financial problems; and of those who received an overdue bill, 54.5 percent also received at least one termination not ice.

The popular metatheory which attributes poverty to structural trends logically describes this group of consumers. After all, they report high rates of long term unemployment, contain the highest percentage of single female-headed households (both with young children and older women) and households with disabled.

108 Policy Studies Review 18:2 (Summer 2001 )

Nevertheless, hey don't seem to be characterized by some sort of "culture of poverty" which encourages irresponsible use of financial resources (they own few major appliances and they do not put off paying bills like the other groups). In short, these are people for whom collections policies and extended payment arrangements are not likely to meet with success. They need policies which either improve their economic situation or substantial ongoing financial assistance to survive.

Discussion: Metatheories, Policy Models and Empirical Clusters

Fischer (1980) and Fischer and Forester (1993) call for the unification of normative and empirical policy analysis. In this analysis, the empirical clusters of a statewide sample of consumers can be seen to coincide with different normative metatheories about the etiology of utility payment problems, and in turn, different models of public policy which have been established in the polity. Figure 3 depicts what we see as the logical relationship among these three levels of phenomena. Note first that the empirical clusters tend to conform generally to different points along the logical causationhesponsibility continuum as do the policy modes and metatheories. This finding suggests that different metatheories, and the policy options which flow from them, can each be seen to apply to some aspects of what we find to be empirical reality. Each policy model appears to be reflective of some, and none for all, of the empirical profiles.

Note also that the clusters do not have a one-to-one fit with the policy models. Rather, we believe that when the models are arranged as in Figure 3, aspects of adjacent policy approaches may be most appropriate for those on the margins of adjacent clusters. This is not surprising if we recognize that these conceptual types are each encapsulating a great deal of empirical variation. It follows that some overlap and flexibility in response options would be appropriate. We also recognize that our selection of the five-cluster solution is a professional judgment. This solution is the one that shows the most clear distinctions between the groupings. Accordingly, finer breakdowns might allow a closer fit to the policy models, but would not change the overall picture. The

Hyman et al.: Paradigms, Policies and People

THREE Cluster Solution

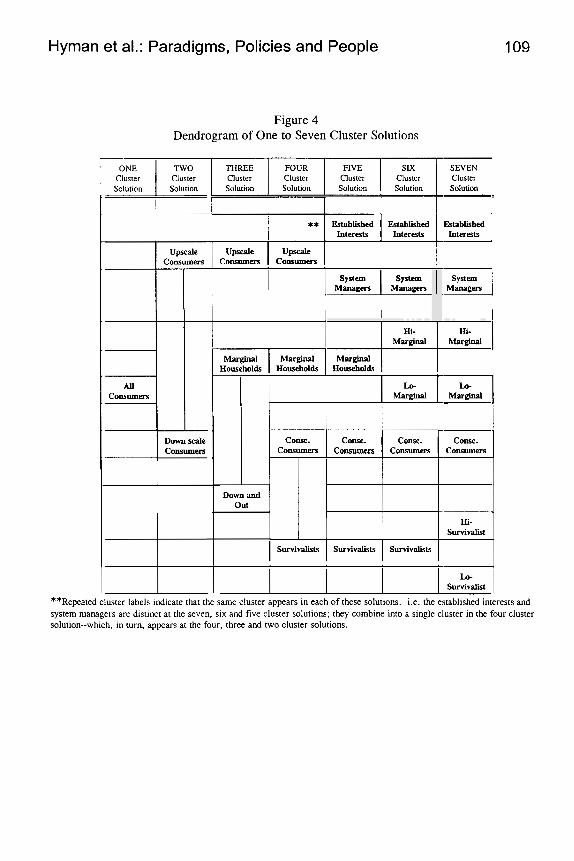

Figure 4 Dendrogram of One to Seven Cluster Solutions

FOUR FIVE SlX SEVEN Cluster Cluster Cluster Cluster Solution Solution Solution Solution -

** Established Established Established Interests Interests Interests

Cluster Cluster

I

Lo- Marginal

Down scale consumers

Lo- Marginal

c o w . consumers

Down and o u t

I upscale I Upscale Consumers Consumers

c o w . conse. c o w . consumers consumers consumers

Hi- 1 survivalist

Marginal I Marginal Households Households

system I system I system Managers Managers Managers

Households

I survivalists I survivalists I survivalists I

I09

**Repeated cluster labels indicate that the same cluster appears in each of these solutions. i.e. the established interests and system managers are distinct at the seven, six and five cluster solutions: they combine into a single cluster in the four cluster solution--which, in turn, appears at the four, three and two cluster solutions.

1 I 0 Policy Studies Review 18:2 (Summer 2001)

logical relationship between perceptions (metatheories), policy models, and people is apparent, and has implications for public policy and further research.

The identification of distinct clusters of customers with different payment patterns thus provides an opportunity for examining how social perceptions qua metatheories can be logically linked to public policy models, and in turn to empirical groupings. We are quick to point out that this is not a causal analysis. We are not showing that metatheories cause the different types of payment problems. Nor are we showing that empirical observation (i.e. by decision makers) of different groups with payment problems leads directly to policies. What does seem reasonable to conclude, however, is that there is a logical connection between the metatheories and the policy models in use, and that they can be seen to bear a relationship to the empirical clusters of consumers. This linkage between perceptions, policies and people is important for policy makers, professionals in the field and researchers. These findings challenge policy makers to recognize the perceptual constraints their beliefs put on consideration of policy options. It challenges professionals in the field to explicitly recognize and demonstrate their plans and programs are appropriate for the target groups to which they are applied: program efficiency and effectiveness are definitively tied to the metatheory-policy model-target group linkage. It challenges researchers to step outside of their analytical preconceptions and incorporate both normative and empirical elements in both their thoughts and research.

Adherents of each of the policy models claim it to be “the” answer to utility payment problems; each is rooted in a different set of values and normative beliefs. The framework presented above juxtaposes normative metatheories, existing policies, and the five empirical clusters providing a framework for examining the logical implications of different courses of action. The examination of how these linkages illuminate the dominant policy approaches currently in use in the public utility arena provides an example of the implications for public policy and implementation. First, the traditional collections model for payment views utility bills as a current expense payable on demand. If the bill remains unpaid for the period immediately following delivery (usually 30-60 days)

Hyman et al.: Paradigms, Policies and People 111

service is terminated. This approach incurs collection costs as soon as bills become overdue and makes no distinctions among consumers on either their ability or willingness to pay. The fundamental assumption of this model is that people have resources--as one utility executive put it, "they can pay but won't." It follows, on the one hand, that prompt action to collect is appropriate, and if unsuccessful, denial of further service is appropriate. On the other hand, where there is either a temporary or chronic inability to pay, this model is both unrealistic and illogical to apply--as with the marginal households, conscientious consumers, and the survivalists. In the latter case, the direct costs of unsuccessful collections, termination and amortization agreements and the indirect costs in terms of health, safety, and well-being can be considerable and may far exceed the amount at risk for nonpayment. Hyman, Meyer and Wadsworth (198534) suggest that "a uniform response to nonpayment may be both inappropriate from both company, consumer, economic, and broader societal perspectives." They go on to say that, "a monolithic response may be suboptimal from the point of view of utility company profit maximization." It follows that when empirical consumer characteristics are not congruent with the metatheoretical assumptions of the collections model, then another line of reasoning and action ought to be applied.

Second, the amortization (payment agreement) model recognizes that utilities have become necessities of life in modern society (Hyman, Meyer and Wadsworth: 1985), and shutoffs which pose threats to the health and safety of consumers are contrary to the public good. Federal and state regulatory intervention in the 1970s led to policies that required companies to offer amortization agreements when consumers have a temporary inability to pay. This model addresses financial and personal emergencies. It is logically appropriate for situations as reported by some of the established interests and the systems managers. However, in situations where survival expenses are greater than incomes, diseconomies arise on the one hand from applications of the collections model (they are logically inappropriate), and on the other hand from failure to provide supplementary financial assistance (which is necessary). In the former case, people with a temporary financial crisis will pay as they get control of their

112 Policy Studies Review 18:2 (Summer 2001)

situation: a time-payment option up front seems both appropriate and economical for both companies and consumers. In the latter case, application of the amortization model to those with long-term inability to pay leads to promises that cannot be kept. The logical result is a series of defaults on payment agreements, renegotiations or terminations--all of which are costly to both companies and consumers, and which incur direct and indirect costs without providing benefits of continued sales for companies and continued service for customers. These are people whose survival expenses are greater than their income. Third, the transfer paymentdfinancial aid model seeks to provide targeted supplemental aid, or customer assistance programs that provide affordable payments combined with assistance or writeoffs for low income consumers who successfully meet their payment obligations for a specified period. There is a range of sub-options to this model depending on whether inability to pay is acute or chronic. Short-term crisis assistance seems appropriate when people have a temporary inability to pay (acute, short-term), and their resources will not be adequate for them to catch up (otherwise the amortization model is appropriate). Many consumers in the clusters we call conscientious consumers and survivalist are expected to fit this category depending on the severity of their problem. For those who have a chronic (long-term) inability to pay, income plans, lifeline rates, etc., are new and emerging policies that recognize such situations. It is important to recognize that prompt identification and screening (triage) of payment troubled consumers in such situations can lead to prompt, appropriate intervention. On the one hand, triage can avoid the costs of failed collections, amortization agreements, terminations, dispute settlements, threats to health and safety, and eventual writeoffs of uncollectible bills. On the other hand, these approaches should not be applied across the board. To the extent that those from the first two or three clusters receive responses that are inappropriate for their objective situations, public support will be undermined. It also follows that the costs of endless rounds of collection processes and amortization agreements for the few among the established interests and system managers who use due process as a means to avoid payment for services that they can afford could be avoided through swift and effective action--again if early triage occurs.

Hyman et al.: Paradigms, Policies and People 113

These findings when combined with the metatheories about wealth and poverty challenge policy makers and researchers to be more inclusive and targeted in their endeavors. Approaching a policy situation from a single perspective or policy model as so frequently occurs may exclude key options required for effectively dealing with the issue at hand. In the public utility field, the analysis herein might lead companies and regulators to consider adopting a system that avoids unnecessary collections actions for the first three clusters, provides automatic amortization to a preset level of credit risk, and affords opportunities to identify and provide appropriate financial assistance and usage reduction for those in the last three clusters with a true inability to pay. Hyman, Meyer and Wadsworth (1985) show that such a flexible response approach imposes minimum intervention and minimum paperwork for those with an ability to pay combined with remuneration (e.g. interest) to companies when utility bills are not immediately paid; is an appropriate intervention to assure health, safety and reasonable service for those who would pay but cannot (a net inability to pay); and prompt punitive action for those who could pay but don’t. They also suggest that the costs of the program might be offset by the avoided costs of collections, amortization, and complaint handling under the existing system. [Note: A section on the details of the flexible response option has been deleted. in response to reviewer‘s comments].

Nor is the five cluster solution the ultimate answer. As noted earlier, we also examined a variety of cluster solutions, choosing the five clusters for more detailed examination. The choice is a matter of judgment related to the purpose at hand and different cluster solutions might be considered in the policy process. For example the established interests and system managers are distinct at the seven, six, and five cluster levels and join into a single cluster at the four-cluster solution. For policy and program purposes it might be reasonable to consider this an “upscale” cluster and look for a single policy suitable for them. Similarly, what we have called the marginal households at the five cluster level is the combination of two different clusters at the six and seven cluster solutions. The conscientious consumers are constant from the seven to four cluster solutions and combine with the survivalist at the three cluster solution into a cluster that might be considered

114 Policy Studies Review 18:2 (Summer 2001)

are also situations where the structural/situational factors of illness, unemployment, disability, etc. are so dominant that financial assistance is needed. A flexible response system would be most appropriate .

Conscientious Consumers: These people place high priority on paying their utility bills, perhaps even to the point of threatening their health and safety in their drive to keep from asking for help. Many of them may have serious problems that could be ameliorated by existing programs. An issue may be identifying those at risk and initiating contact to determine whether usage reduction, consumer education, lifeline rates or payment assistance are appropriate. Again, a flexible response system may be appropriate .

Survivalists: These people need help. Education, training and employment assistance, which could assist some of these people to enter the mainstream, are both appropriate and beyond the purview of utility payment policies; and, utility payment problems may be able to serve as an indicator for referrals to other systems. Additionally, assistance to lower utility bills (e.9. conservation measures) and financial assistance to pay bills are fundamental and ubiquitous needs.

The "bottom line" is that segmentation of target populations is not only possible for public policy but also necessary for efficient and effective public policy responses. In the specific case examined here, nonpayment is associated with a variety of conditions, and effective action may require a variety of responses. Pluralism among causes of wealth and poverty, diversity of consumer types with payment problems, and variety of programs can be combined to target policies to where they are needed and tailor interventions to those who need them.

In conclusion, this examination of the congruence between social metatheories, public policy options, and empirical consumer clusters provides insights into why some policies can be implemented successfully and why some cannot. On the one hand, when metatheoretical world views constrict the vision of policymakers to the extent that they create policies that do not

Hyman et al.: Paradigms, Policies and People 115

recognize the realities of the populations to whom they are to be applied, then implementation can be expected to fail. Policy failure would also be expected when a mismatch occurs between the policy model in use and the target group: policies are applied to those for whom the metatheory is not appropriate. Identification of policies that are appropriate for specific people or situations should lead to more efficient, effective and humane implementation. In the case of utility payment problems, economic, social, and personal costs increase for companies and society when non-congruent models are applied in the field of action--that is when the metatheory and policy in use do not apply to the empirical situations of the consumers involved. Conversely, we would expect both cost efficiency and program effectiveness to increase where there is congruence between the situations of the consumers and the policies and metatheories being applied. Attention to the issues raised in this paper should improve both the effectiveness of policy research and evaluation as well as the effectiveness of policies and programs in meeting their objectives.

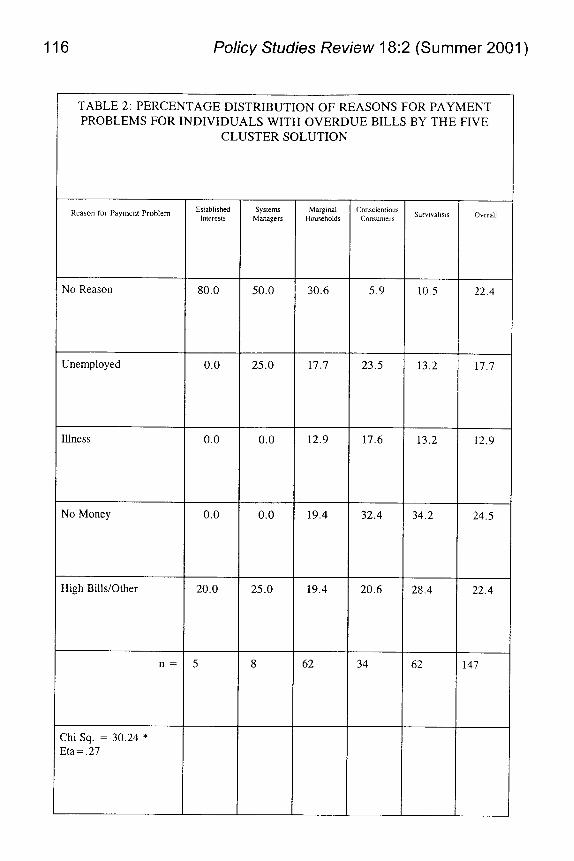

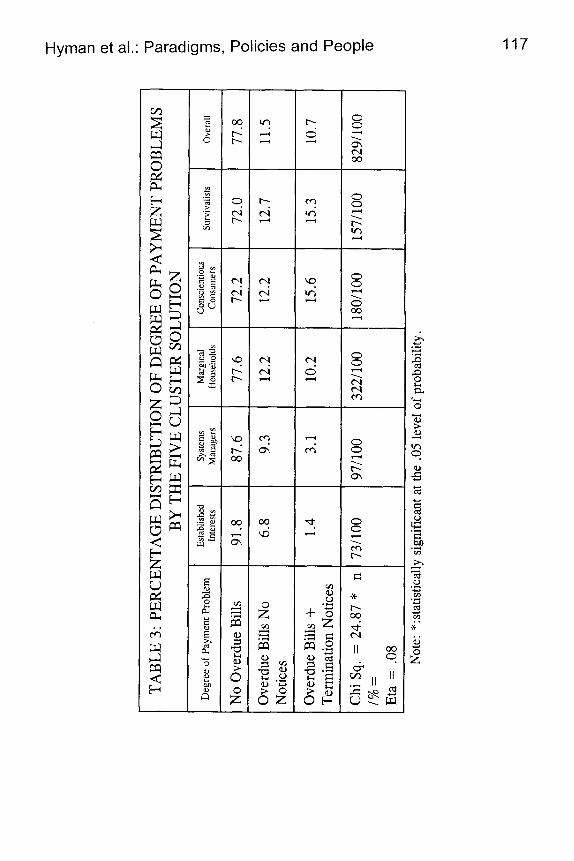

116

TABLE 2 : PERCENTAGE DISTRIBUTION O F REASONS FOR PAYMENT PROBLEMS FOR INDIVIDUALS WITH OVERDUE BILLS BY THE FIVE

CLUSTER SOLUTION

Policy Studies Review 18:2 (Summer 2001)

'

Esrablished Interests

Systems Managers

Marginal Households

Conscientious Consumers Survivalists Reason for Payment Problem Overall

80.0 50.0 30.6 5.9 10.5 22.4

17.7

12.9

0.0 25.0 17.7 23.5 13.2

0.0 12.9 17.6 13.2 0.0

0.0 19.4 32.4 34.2 24.5 0.0

20.0 25.0 19.4 20.6 28.4 22.4

I47 5 8 62 34 62

Chi Sq. = 30.24 * Eta=.27

TAB

LE 3

: PER

CEN

TAG

E D

ISTR

IBU

TIO

N O

F D

EGR

EE O

F PA

YM

ENT

PRO

BLE

MS

BY T

HE

FIV

E C

LUST

ER S

OLU

TIO

N

1 M

argi

nal

Hou

seho

lds

Esta

blish

ed

Deg

ree

of P

aym

ent P

robl

em

inte

rest

s I

I I

Ove

rall

I No

Ove

rdue

Bill

s I

91.8

'

77.8

~~

Ove

rdue

Bill

s N

o 1 6

.8

Not

ices

Chi

Sq.

= 2

4.87

* n

1% =

Et

a =

.08

Ove

rdue

Bill

s +

Term

inat

ion

Not

ices

73/1

00

Syst

ems

Man

ager

s

87.6

9.3

3. I

97/1

00

77.6

12.2

10.2

322/

100

1 Con

scie

ntio

us

Con

sum

ers

72.2

12.2

15.6

180/

100

Surv

ival

ists

72.0

12.7

15.3

157/

100

11.5

10.7

829/

100

Not

e: *

:sta

tistic

ally

sig

nific

ant a

t the

.05

leve

l of p

roba

bilit

y.

118 Policy Studies Review 182 (Summer 2001)

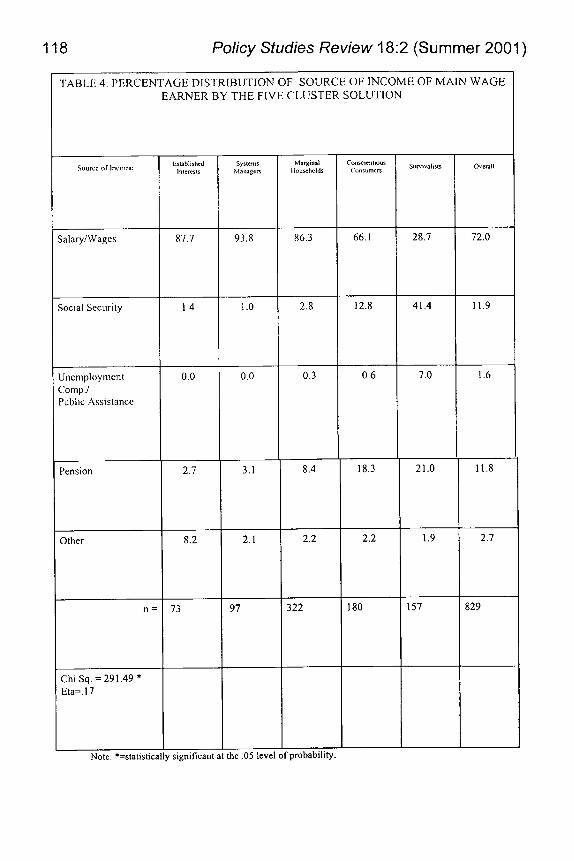

66.1 '

TABI,I: 4: PERCENTAGE DISTRIBUTION OF SOURCE OF INCOME OF MAIN WAGE EARNER BY THE FIVE CLUSTER SOLUTION r

Overall

93.8 86.3 72.0 28.7

41.4 I .o 2.8 12.8 11.9

0.0 0.6 7.0 1.6 0.3

8.4 18.3 11.8 3.1 21.0

1.9

157

2.1 2.2 2.2 2.7

97 322 180 829

probability. he .05 leve

Hyman et al.: Paradigms, Policies and People 119

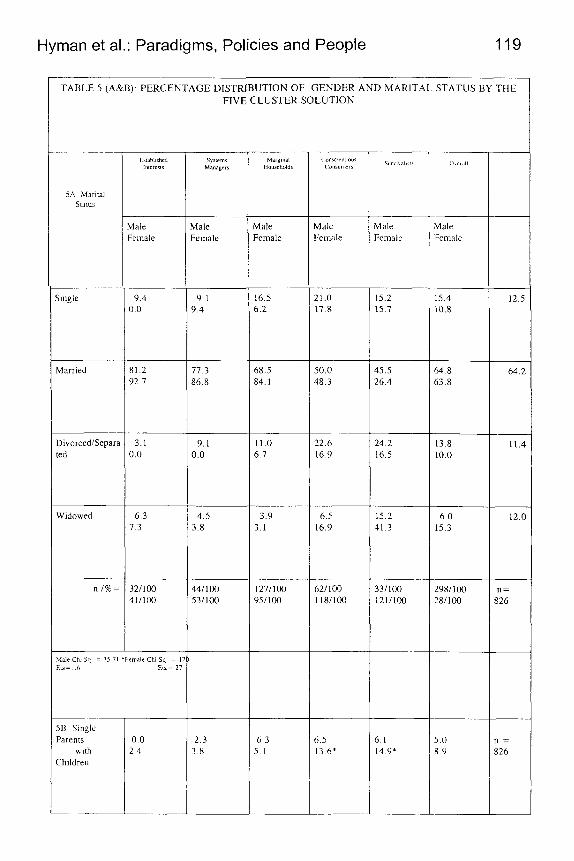

TABLE 5 (A&B): PERCENTAGE DISTRIBUTION OF GENDER AND MARITAI. STATUS BY THE FIVE CLUSTER SOLUTION

Margl". llouwho

Male Female

16.5 6.2

( 1 i C l l l I

!Male Female

5A Marilal Starus

Male Female

Male +male

Male Female

Male Female

Single 9 4 o n

9.1 9.4

21.0 17.8

15.4 10.8

12.5 15.2 15.7

Married 81.2 92.7

50.0 48.3

15.5 26.4

4 4 8 53 8

64.2 68.5 84. I

11.0 6.7

77.3 86.8

9.1 0.0

DivorcedlSepar; ted

3.1 0.0

22.6 16.9

24.2 16.5

13.8 10.0

11.4

Widowed 6 3 7 3

4.5 3.8

6 5 16.9

15.2 11.3

6.0 15 3

12.0 3.9 3.1

1271100 95/100

n l % = 321100 411100

44/100 531100

2981100 281100

n = 326

62/100 1181100

331100 1211100

Male Chi Sq = 25 1 1 *Fernale Chi Sq = I Era= 16 m a = 21

5B. Single Parents

Wlll l

Children

0 0 2 4

2 3 3 8

6 3 5.1

6 5 13 6'

5 1 14.9'

5 0 8 9

1 =

326

120 Policy Studies Review 18:2 (Summer 2001 )

REFERENCES

Ball, William J. "A Pragmatic Framework for the Evaluation of Policy Arguments," Policy Studies Review, (Spring/Summer 1995), 14:1/2, pp. 3-24.

Colton, Roger. "Understanding Why Customers Don't Pay: The Need for Flexible Collection Practices," New Directions in Low lncome Fuel Assistance, Weatherization and Rate Programs, Boston: Nation Consumer Law Center, 1992.

Colton, Roger. Energy Policy and the Poor: Determining the Cost Effectiveness of Utility Credit and Collection Techniques, Boston: National Consumer Law Center, 1990.

Fischer, F. Politics, Values and Public Policy: The Problem of Methodology, Westview Press, (1 980).

Fischer, F. and J. Forester, eds. The Argumentative Turn in Policy Analysis and Planning, Duke University Press, (1 993).

Hyman, Drew, P. Meyer and M. Wadsworth. "Optimizing the Public and Private Effects of Utility Service Terminations," Public Utilities Fortnightly, December 26, 1985, pp. 29-36.

Hyman, Drew, Mike Wadsworth, and David Alexander. "Values, Policy-Making and Implementation: The Roots of Bias in Utility Regulation and Energy Mediation Policy," Administration and Society, Vol. 23, No. 3, November, 1991 , pp. 31 0-332.

Hyman, Drew, Mike Wadsworth and David Alexander. "The Political Economy of Consumer Energy Subsidies," in Energy Resources Development, New York: Quorum, 1987.

Kachigan, Sam. Multivariate Statistical Analysis: A Conceptual Introduction, New York: Radius Press, 1982.

Hyman et al.: Paradigms, Policies and People 121

Nakamura, Robert T. (1987). "The Textbook Policy Process and Implementation Research," Policy Studies Review, Vol. 7, No. 1 , pp. 142-154.

Palumbo, Dennis J. (1 987). "Implementation: What We Have Learned and Still Need to Know--Introduction." Policy Studies Review, Vol. 7 No. 1 , pp. 91 -1 02.

Pennsylvania Public Utility Commission Bureau of Consumer Services, Final Report on the Investigation of Uncollectible Balances, Docket No. 1-900002, (February 1992).

Pobjecky, D.J. (1976). "Rates Follow Service: The Power of Public Utility Commissions to Regulate Quality of Service." Baylor Law Review, vol. 28, pp. 1138-1 156.

Ritti, R.R. and Drew Hyman (1981). "The Administration of Poverty." Social Problems, 25, pp. 157-1 75.

Saunders, Margot Freeman and Maggie Spade. Energy and fhe Poor: The Crisis Continues. National Consumer Law Center, January, 1995.

Smith, Kevin B. and Lorene H. Stone. "Rags, Riches and Bootstraps: Beliefs About the Causes of Wealth and Poverty," The Sociological Quarterly, Vol. 30, No. 1 , 1989, pp. 93-1 07.

Yanow, Dvora. (1987). "Toward a Policy Culture Approach to Implementation," Policy Studies Review, Vol. 7, No. 1 I pp. 103-1 15.

Related Documents